The Retirement Crisis Is Much Worse Than You Think

Date Posted: March 20, 2019

Read time: 7 min

According to a recent survey, one in five American adults have nothing saved for retirement or emergencies.

Are you sitting down for this? According to a recent survey, one in five American adults have nothing saved for retirement or emergencies. A further 20 percent have squirreled away only 5 percent or less of their annual income to meet certain financial goals. Less than a third of all Americans have saved at least 11 percent or more.

The survey, conducted by Bankrate in late February and early March, is just the latest indication that the U.S. faces a major retirement crisis. Every day, some 10,000 baby boomers turn 65, and they’re reaching retirement in worse financial shape than the previous generation for the first time since Harry Truman was president, according to a report by the Wall Street Journal.

The survey also raises the question of why some working-age adults haven’t been able to take full advantage of a booming U.S. economy and historic bull market to build wealth. Unemployment is near a 50-year low, and wage gains were at their highest level in a decade last month.

According to Bankrate, the number one reason (40 percent) why Americans aren’t saving is that they have too many other expenses. Sixteen percent said they “haven’t gotten around to it,” while the same percentage blamed the low quality of their job.

Indeed, not every employer provides access to a retirement plan such as a 401(k). A recent study by the National Institute on Retirement Security (NIRS) found that a little over half of working American adults have access to an employer-sponsored 401(k)-type plan. Only 40 percent actually participate.

As such, the median retirement account balance among all working-age Americans is—again, are you sitting down?—$0.00. That’s the median balance, remember, so half of all Americans have more than that. The other half, meanwhile, have even less than $0.00 to their name.

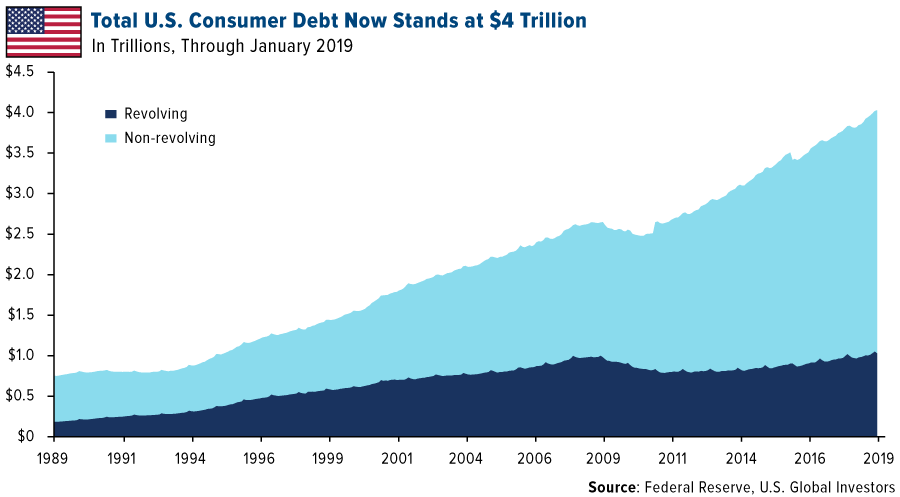

A Record $4 Trillion in Consumer Debt

That brings me to my next point. Interestingly, only 13 percent of those surveyed by Bankrate cited debt as the reason why they’re not saving as much as they should. I say “interesting” because total U.S. consumer debt, including revolving and non-revolving debt, now stands at more than $4 trillion, the most ever.

Debt affects us all, but it can seriously hinder workers’ ability to retire on time. The more you’re on the hook to pay lenders, the less you have to pay yourself.

Revolving debt, such as credit card debt, is now valued at more than $1 trillion, which exceeds the all-time high right before the financial crisis. And according to the Federal Reserve Bank of New York, people age 60 and older owe about a third of this total.

Non-revolving debt—auto loans, student loans, mortgages—is even worse. Student loan debt alone stands at an astronomical $1.5 trillion. It doesn’t help that, since the 1980s, the cost of college tuition has increased almost eight times faster than wages.

But if you think this burden belongs only to young people, you’re sorely mistaken. As many as 2.8 million Americans over the age of 60 are saddled with student debt, according to CNBC. Those over 50 owed more than $260 billion last year, up dramatically from $46 billion in 2006.

Confidence Lacking in Retirement Preparedness

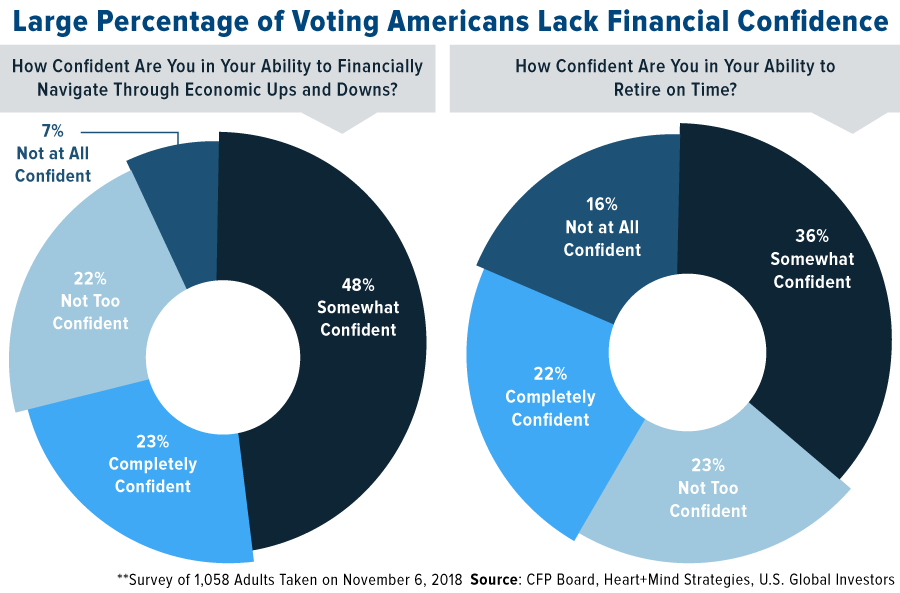

All combined, it’s little wonder that a significant number of Americans feel some anxiety when it comes to their financial stability and retirement preparedness, despite a strong U.S. economy. A CFP Board survey conducted on Election Day 2018 found that less than a quarter of voting-age Americans were “completely confident” about their ability to navigate through economic ups and downs. Even less, 22 percent, felt the same about their ability to retire on time.

So what’s the solution?

Fund Your Financial Goals Affordably

I’ve heard from a number of people over the age of 50 who say they worry they haven’t adequately prepared for retirement, and yet are at a loss as to where to start. They want to build wealth fast but might have second thoughts about investing in the market.

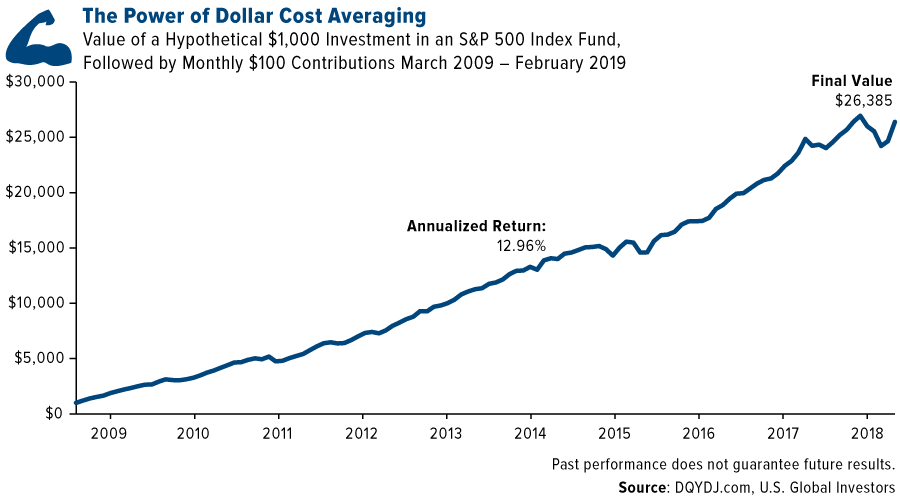

I want to reassure those people that they need not put a significant amount in the market all at once, which for most people is impractical and risky. The truth is that they have options. One of the best, I think, is dollar cost averaging, which allows investors to fund their financial goals affordably.

In short, dollar cost averaging is an investing technique that lets investors add to an initial investment incrementally over time, usually once a month. That way, investors don’t break the bank, and as an added bonus, they don’t need to worry about market timing.

It’s a technique that has worked well for investors in the past. Take a look at the chart below. It shows a hypothetical initial investment of $1,000 in an S&P 500 Index in March 2009. Ten years later, after regular monthly contributions of only $100, the value of that initial investment grew at an annualized 12.96 percent to more than $26,385.

This is just an illustration. The past 10 years have been an exceptionally profitable time to invest, and there’s no guarantee that the good times will last.

Also, $26,000 won’t sustain anyone through retirement, but remember, we were using only a hypothetical $1,000. All else being equal, an initial investment of $10,000 in March 2009 would today be worth more than $64,766, for an impressive annualized return of 14.81 percent.

Sound enticing? The good news is that U.S. Global Investors provides investors the opportunity to invest with dollar cost averaging! We call it the ABC Investment Plan, and I’m very proud to give investors this option. Investment minimums are just $1,000 initially and then $100 a month. With the ABC Investment Plan, you get to choose the day of the month your investment is transferred from your checking or savings account to your investment account.

That way, some of the worry is eliminated from your retirement preparations or other financial goals.

Interested in the ABC Investment Plan? Get started today! Download the application by clicking here!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

You cannot invest directly in an index.

A program of regular investing doesn’t assure a profit or protect against loss in a declining market. You should evaluate your ability to continue in such a program in view of the possibility that you may have to redeem fund shares in periods of declining share prices as well as in periods of rising prices.

The S&P 500 Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.