Calling All Commodity Bulls

Date Posted: October 23, 2020

Read time: 49 min

Another week, another cyber-attack. With only 11 days remaining before the election, Iran and Russia were singled out by U.S. officials for stealing voter registration data and sending emails designed to intimidate voters.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Another week, another cyber-attack. With only 11 days remaining before the election, Iran and Russia were singled out by U.S. officials for stealing voter registration data and sending emails designed to intimidate voters.

This attack is more of the same from foreign adversaries who wish to divide Americans, and to sow discord and mistrust in the democratic process.

Earlier this month, I shared with you a report by Microsoft showing that Russia is by far the number one source of cyber threats, followed by Iran, China and North Korea.

I’m telling this to you now as a reminder not only to stay vigilant and read the news with a critical eye, especially when it pertains to the upcoming election. I also want to remind you of the value you get by being an Investor Alert subscriber.

I believe what our team produces every single week, without fail, can be stacked up against financial newsletters produced by companies and institutions many times our size. We regularly work late on Friday to bring you timely research and insight that can’t be found in a lot of places. The Microsoft report is a good example of that. We were also one of the first firms to talk about the monthly purchasing manager’s index (PMI), and now I see it being reported everywhere.

The Investor Alert—or “IA,” as we call it—is absolutely free to you, but for us, it’s resource-intensive. If I had to guess, I would say we spend at least $1 million a year just on the IA.

We’ve been doing this for a long time, and we’ll continue to do it for as long as there are still readers.

With that said, I’d like to take this opportunity to say thank you for being a subscriber. If you like what you read and find value in it, please consider forwarding the IA to someone you think might also enjoy it. It would be much appreciated!

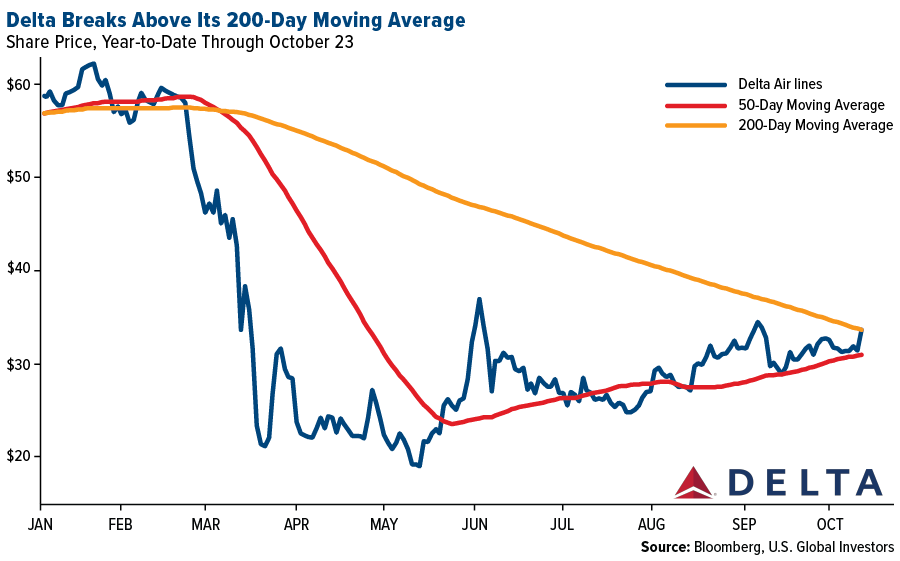

Liftoff! Delta Jumps Above Its 200-Day Moving Average

A week after reporting earnings, Delta Air Lines jumped more than 7 percent on Thursday after the carrier announced it would continue to block the middle seat until at least January of next year. This jump helped its share price climb above the 200-day moving average for the first time since February, which many traders see as a bullish signal.

Delta and Alaska Airlines will be the only remaining major U.S. carriers that still block the middle seat after Southwest Airlines begins filling the seat on December 1. The low-cost carrier said in a tweet that it would unblock the middle seat after November 30, citing a body of research that supports the notion that masks and ventilation sufficiently protect passengers from the virus.

Among the studies was the one I shared with you last week. The Department of Defense (DoD) found that mask-wearing passengers are at very low risk of being infecting with the coronavirus, even on a packed flight.

“It is a very safe environment with all of the air-filtering technology and wearing masks,” Southwest CEO Gary Kelly told CNBC this week. “The science supports that.”

We continue to see the domestic airline industry recover off the April lows. Last Sunday, the number of people cleared to fly commercial in the U.S. exceeded 1 million for the first time since the pandemic struck.

Goldman: Get Ready for a Commodities Bull Market

Jet regrade—the relative strength of jet fuel prices versus diesel—looks primed for a bull market in 2021 as flight demand continues to increase, according to Goldman Sachs. By next summer, jet fuel demand is expected to be higher by 3.9 million barrels per day than where it stands right now.

Among other commodities that could also surge next year, the investment bank says, are silver, copper, gold, natural gas and Brent crude oil.

In a note to clients this week, Goldman analysts cited a weaker dollar, inflation and additional monetary and fiscal stimulus as reasons for a potential rally in commodity prices. A 12-month return of 30 percent is forecast for the S&P GSCI, which tracks 24 commodities from all commodity sectors. Industrial metals, including copper, could increase 5.5 percent; precious metals, 18 percent; and energy, more than 42 percent.

Goldman sees the price of gold averaging $2,300 an ounce in 2021, while silver is projected to average $30 an ounce.

Here at U.S. Global Investors, we’re very bullish on commodities, particularly industrial and precious metals. The manufacturing PMI in a number of countries shows that factories are expanding capacity on a greater number of new orders. In August, the U.S. manufacturing PMI registered 56.0, the highest reading since November 2018. The PMI in China—the world’s biggest importer of metals and other raw materials—was 51.5 last month, well above the five-year average of 50.6.

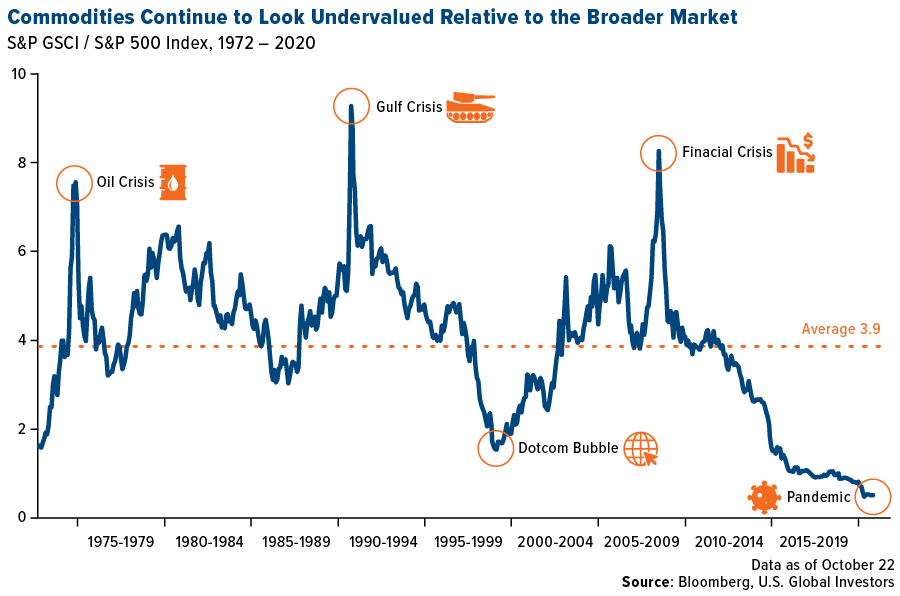

As I’ve noted before, commodities continue to look remarkably cheap relative to stocks. Below is a chart showing the ratio between the S&P GSCI and S&P 500. At no other time going back to 1972 have commodities been as undervalued as they are today. If Goldman’s projections turn out to be accurate, now could be a phenomenal buying opportunity.

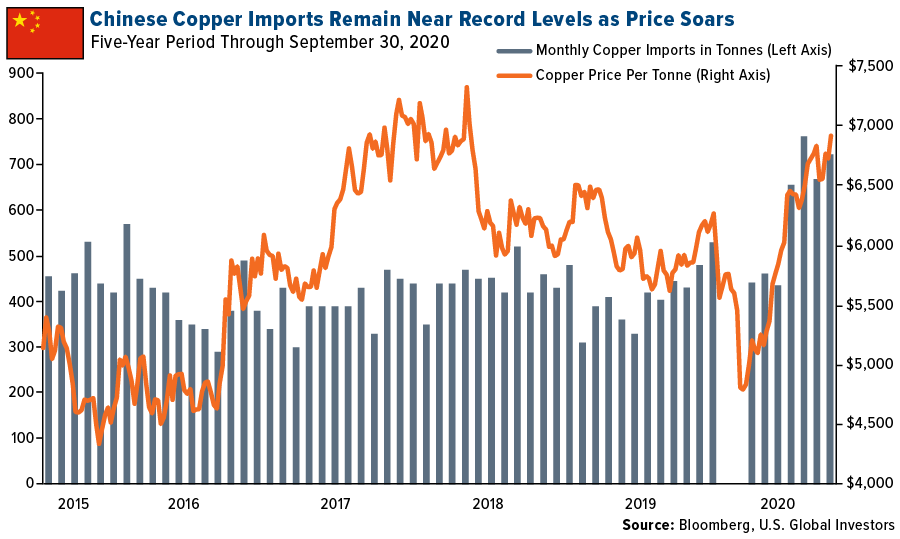

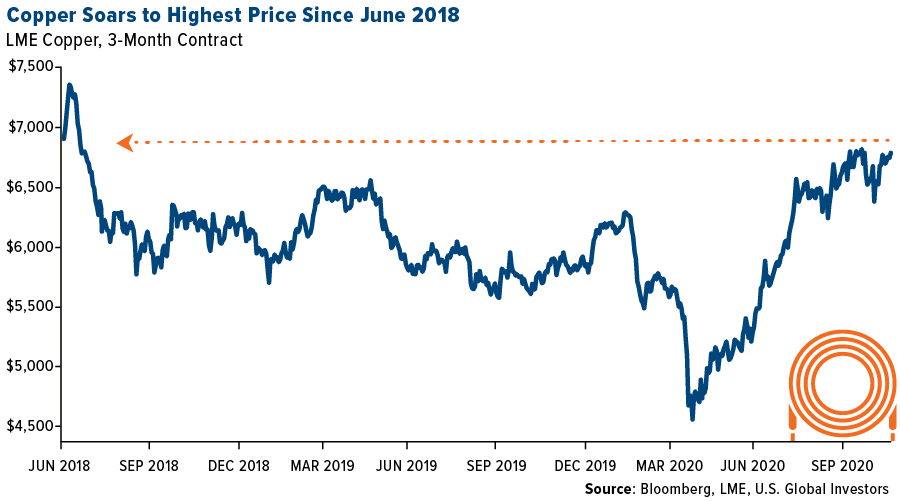

Doctor Copper Briefly Crosses Above $7,000 a Tonne, Thanks in Large Part to China

“Doctor copper” is so named because its price is seen as a good indicator of economic health. If that’s the case, then the economy isn’t nearly as bad as we thought it was.

In intraday trading on Wednesday, copper briefly crossed above $7,000 a tonne, its highest level since June 2018. From its low in late March, the red metal has risen close to 50 percent on hopes of further government stimulus and increased demand, particularly from the renewable energy industry and China.

In July, China’s copper imports hit an all-time high of 762,210 tonnes as the government unleashed stimulus aimed at building bridges, roads, railroads, broadband and more.

That includes renewable energy projects such as wind and solar. According to a report this month by the Global Wind Energy Council (GWEC), China led the world in adding new offshore wind capacity in 2019, with 2.4 gigawatts (GW) installed, representing nearly 40 percent of total new wind power across the globe.

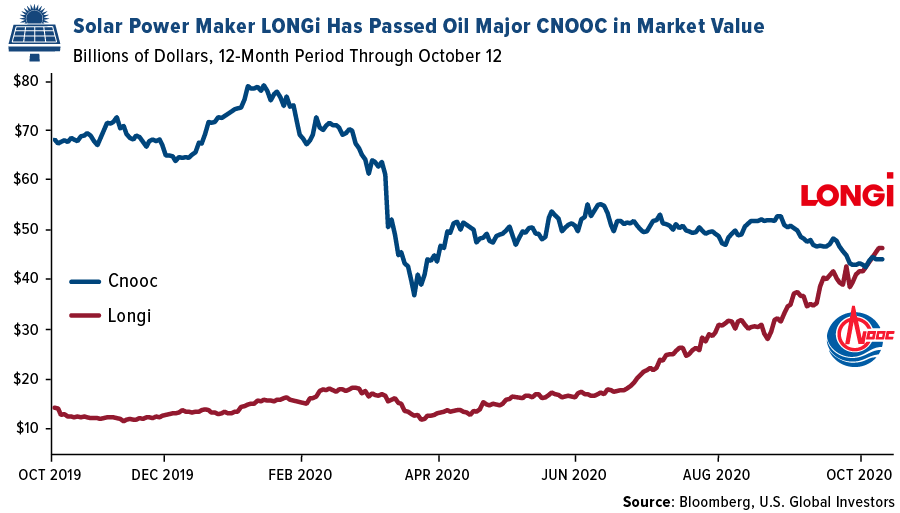

The market cap of China’s LONGi Green Energy Technology, the world’s largest solar power company, recently climbed higher than that of oil major China National Offshore Oil Corporation (CNOOC), the country’s largest oil and gas producer. This not only represents a significant shift in energy trends, but it’s also highly supportive of copper prices.

I expect China’s appetite for metals and other raw materials to keep pace as it continues to stimulate its economy—which managed to grow, I should add, an historically low and yet impressive 4.9 percent in the third quarter compared to the same period last year.

We’ll receive third-quarter economic data for the U.S. on Thursday of next week. I hope to see a huge improvement over the second quarter, when real GDP fell at an annual rate of 31.4 percent, according to Bureau of Economic Analysis (BEA).

Virtual Junior Mining Expo

I’m very excited to share with you that I’ll be participating in the first-ever Virtual Junior Mining Expo, featuring 10 top junior mining companies. This virtual event is co-hosted by my friends at Streetwise Reports, and it will take place Thursday, November 12, at 1:00 pm Eastern. What’s more, it’s absolutely free.

To register for the event, please click here. I hope you’ll join us!

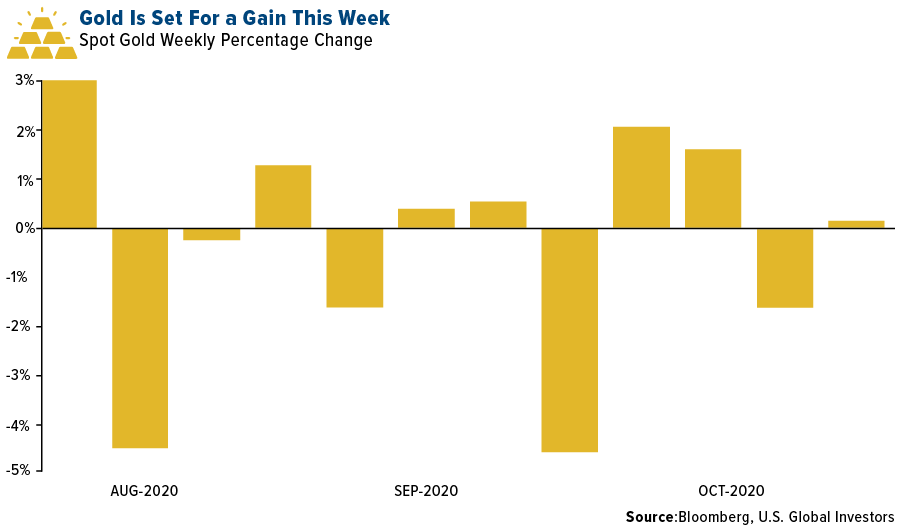

Gold Market

This week spot gold closed at $1,902.05, up $2.76 per ounce, or 0.15 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.94 percent. The S&P/TSX Venture Index came in off 0.99 percent. The U.S. Trade-Weighted Dollar fell 1.02 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-18 | China Retail Sales YoY | 1.6% | 3.3% | 0.5% |

| Cct-20 | Housing Starts | 1465k | 1415k | 1388k |

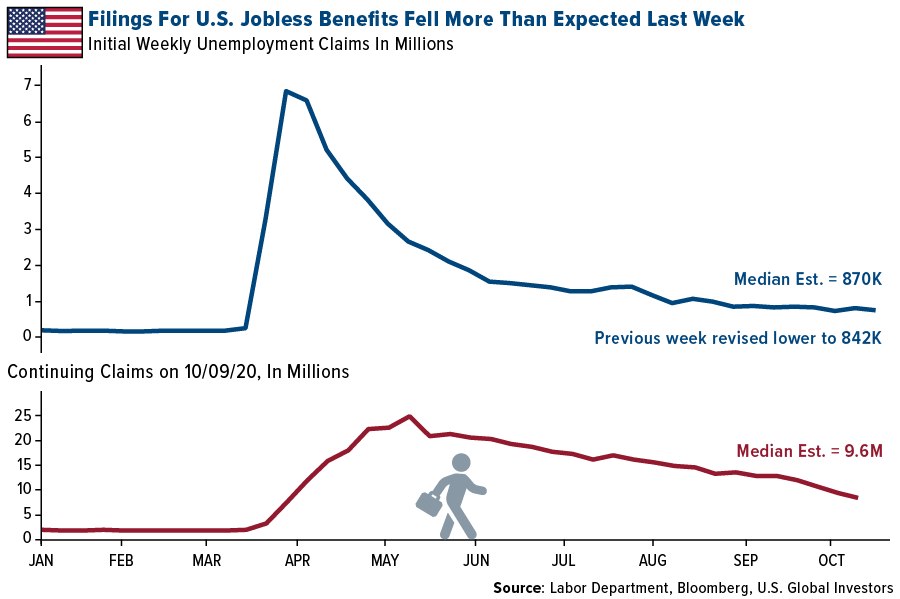

| Oct-22 | Initial Jobless Claims | 870k | 787k | 842k |

| Oct-26 | New Home Sales | 1025k | — | 1011k |

| Oct-27 | Hong Kong Exports YoY | -0.4% | — | -2.3% |

| Oct-27 | Durable Goods Orders | 0.6% | — | 0.5% |

| Oct-27 | Conf. Board Consumer Confidence | 101.8 | — | 101.8 |

| Oct-29 | Initial Jobless Claims | 788k | — | 787k |

| Oct-29 | GDP Annualized QoQ | 31.9% | — | -31.4% |

| Oct-29 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Oct-29 | Germany CPI YoY | -0.3% | — | -0.2% |

| Oct-30 | Eurozone CPI Core YoY | 0.2% | — | 0.2% |

Strengths

- The best performing precious metal for the week was platinum, up 4.64 percent on perhaps sentiment that demand should pick up with more hydrogen research and production. Gold edged up on Friday as the U.S. dollar weakened on German data showing factories recovering solidly. The yellow metal finished the week positive after a steep drop last week.

- Gold exports to the U.K. from Switzerland hit a one-year high in September, according to data from the Swiss customs authority. Bloomberg reports bullion bars are being sent to London vaults to meet requirements for physically backed ETFs.

- Russia’s largest gold producer, Polyus PJSC, announced its Skuhoi Log deposit in Siberia holds the world’s biggest gold reserves, according to a new audit. Data shows the deposit has 40 million ounces of proven reserves with an average gold content of 2.3 grams per ton.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 0.15 percent. Gold fell more than 1 percent on Thursday after hopes disappeared for a pre-election stimulus package. Gold ETF investors have been selling, with funds poised for the first back-to-back weekly outflow this year. Ole Hansen of Saxo Bank says investors might be selling because they view a Biden election win as largely priced in, limiting gold’s upside potential.

- The Perth Mint is being investigated for links to global organized crime syndicates and for failing to conduct identity checks required to prevent money laundering, reports The Financial Review. The refinery’s failure to conduct background checks on Euro-Pacific customers raises the possibility that it sold and is storing precious metal holdings of tax cheats and foreign criminals.

- Lundin Gold’s large-scale Fruta del Norte gold mine in Ecuador could soon face production shutdown due to protests. Local protesters blocked access to the mine to push for the reconstruction of a bridge over the Zamora River that collapsed on Saturday, along with other demands, reports Bloomberg. Lundin had pledged $2.6 million to finance the bridge.

Opportunities

- Citigroup estimates silver could surge to $40 an ounce in the next 12 months due to a recovery in industrial demand and strong investor appetite for precious metals. Analysts including Max Layton wrote in a note that silver will outperform gold because it is “more levered than gold to inflation overshoots, rebounding manufacturing activity.”

- Billionaire hedge fund manager John Paulson said that gold “is going to gain relevance in the near future” and that it is not a “get-rich-quick investment,” but a long-term store of value to protect against inflation. Bloomberg notes Paulson made the comments at Grant’s 2020 Fall Conference on Tuesday. The investor expects a strong economic recovery after the pandemic, with expanding credit and inflation.

- Petra Diamonds made a deal with its creditors to save the business with almost $700 million of debt maturing in two years. Bloomberg reports the deal will see bondholders swap debt for equity and own 91 percent of shares and will have a partial reinstatement of existing bonds. Petra was once worth $1.5 billion but had suffered from debt and falling diamond prices before the pandemic hit. CEO Richard Duffy said the deal “provides the business with a stable, deleveraged capital structure that will ensure the short and long-term viability of the company.”

Threats

- Echelon Capital Markets sales desk wrote in a note to clients this week that reports of Kinross considering selling its Americas assets and moving its primary listing to London is likely to do the miner more harm than good. The firm added that Kinross’ potential move could leave investors concerned the stock’s share price performance has run its course, up more than 90 percent this year.

- Centamin Plc, an Egyptian-focused miner, fell as much as 19 percent in London trading on Wednesday after announcing it will produce less gold than expected in 2021. Centamin operates the Sukari gold mine in Egypt, seen as one of the best gold deposits in the world not owned by a major producer, but the company has long faced operational and political challenges. The company said 2021 output will be between 400,000 and 430,000 ounces, which is below analyst consensus of around 500,000 ounces, reports Bloomberg.

- Sibanye Stillwater is no longer actively pursuing buying assets from companies they were previously in talks with due to higher metal prices that are pushing valuations higher. Bloomberg notes Sibanye is famous for its deal-making and wants to buy gold mines in North America, but assets are now considered too expensive and might not add value to investors.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.95 percent. The S&P 500 Stock Index fell 0.53 percent, while the Nasdaq Composite fell 1.06 percent. The Russell 2000 small capitalization index gained 0.41 percent this week.

- The Hang Seng Composite rose 1.14 percent this week; while Taiwan was up 1.16 and the KOSPI rose 0.82 percent.

- The 10-year Treasury bond yield rose 9 basis points to 0.839 percent.

Domestic Equity Market

Strengths

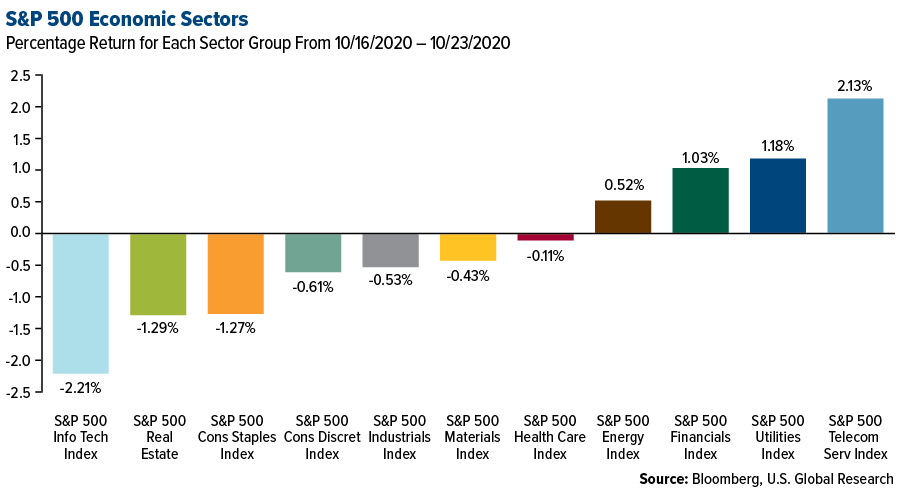

- Communication services was the best performing sector of the week, increasing by 2.13 percent versus an overall decrease of 0.51 percent for the S&P 500.

- Align Technology was the best performing S&P 500 stock for the week, increasing 39.53 percent.

- Snap stock soared in after-hours trading on Tuesday, reports Barron’s, after it reported second-quarter user growth and financial results hat beat Wall Street estimates.

Weaknesses

- Information technology was the worst performing sector for the week, decreasing by 2.21 percent versus an overall decrease of 0.51 percent for the S&P 500.

- Citrix Systems was the worst performing S&P 500 stock for the week, falling 11.24 percent

- The slow pace of workers returning to the office along with high levels of new supply are “just too much” for the office REIT sector to deal with, Evercore ISI’s Steve Sakwa wrote in a note. The analyst downgraded Boston Properties, Kilroy, Paramount and Vornado in the note.

Opportunities

- Tesla stock surged on Thursday, gaining 17.7 percent after the company reported third-quarter revenue of $6.3 billion, reports CNBC. The electric-vehicle maker’s profit was a surprise.

- Apple launched a 24/7 music channel, writes Business Insider. Apple Music TV is an MTV-style channel featuring new videos, interviews, premieres, and live shows.

- UBS posted a 99 percent jump in third-quarter net profit. The Swiss lender saw net income rise to $2.1 billion, smashing analyst expectations of $1.5 billion for the quarter as revenue from trading and wealth management surged.

Threats

- Google is facing the biggest antitrust lawsuit in two decades, reports CNBC. The U.S. Department of Justice accused the tech giant of using a network of illegal, exclusionary business deals that disadvantage smaller competitors, building an unfair advantage in search and online advertising.

- Netflix said Tuesday that it added 2.2 million paid subscribers during the third quarter, compared with a Wall Street forecast of 3.3 million.

- Warren Buffett may have cut his Wells Fargo stake because the bank ignored his advice. Berkshire Hathaway slashed its position in the bank by over 60 percent this year perhaps because directors hired a Wall Street executive as their new CEO.

The Economy and Bond Market

Strengths

- Existing-home sales rose 9.4 percent in September from August to a seasonally adjusted annual rate of 6.54 million, the highest rate since May 2006, according to the National Association of Realtors. Economists surveyed by The Wall Street Journal expected a 6.2 percent monthly increase in sales of previously owned homes, which make up most of the housing market.

- California collected $54.1 billion in revenue for the first three months of the fiscal year that began July 1, $8.7 billion more than projected, according to the state department of finance. The biggest driver was personal income tax receipts, 48 percent higher than forecast at $9.3 billion.

- New filings for jobless claims in the U.S. totaled 787,000 last week, the lowest total since the early days of the coronavirus pandemic. Economists surveyed by Dow Jones had been expecting 875,000 for the week ended October 17. The total reflected a decline of 55,000 from the downwardly revised 842,000 in the previous week.

Weaknesses

- The Bloomberg Consumer Comfort Index fell 1.6 points to 46.6 last week. Americans’ optimism about their personal finances declined 1.3 points to 60.3, the lowest point since August, while a measure of comfort in the buying climate decreased 2.1 points. Such a decline means that American’s may be growing cautious about their spending.

- The economy’s travails are evident in the Back-to-Normal index (BNI) developed by Moody’s Analytics and CNN Business. The BNI measures how the economy is performing compared to its pre-pandemic normal. Currently, the index is sitting at just over 80 percent. In other words, the economy is operating 20 percent below where it was when the pandemic hit back in March.

- The unemployment rate for young people age 20 to 24 was 12.5 percent in September, the highest among adults. Joblessness for them peaked at nearly 26 percent at the height of the pandemic in April — quadruple the level two months earlier — a bigger jump than in any previous recession back to the 1940.

Opportunities

- Next week, the first reading of third-quarter GDP is anticipated to be strong. Annualized GDP growth for the third quarter is expected to be 32 percent, following a dive of negative 31.4 percent in the second quarter.

- UBS Global Wealth Management expects the pandemic to accelerate an exodus out of urban hubs and into the lower-tax Sunbelt states that have seen their populations swell for years. UBS said that Americans are likely to keep moving to low-tax states and has suggested investors tilt more of their portfolios toward those areas. New York, California and Illinois saw the most outmigration on an adjusted gross income basis in 2018, according to the most recent Internal Revenue Service data compiled by the bank, while low-tax destinations like Florida, Arizona and Texas reaped the highest gains. Idaho and South Carolina are also benefiting as strong retirement destinations.

- “In the U.S., I see extraordinarily good growth in 2021,” Gabelli, chairman of Gamco Investors, said at the annual CNBC Financial Advisor Summit. “That’s because of a long runway for automobiles, a long runway for housing and I see some return of spending in commercial aviation.”

Threats

- A broad measure of the economy grew again in September, but the slower pace of expansion likely signals that the U.S. lost some momentum. The Conference Board leading economic index rose 0.7 percent last month, following increases of 1.4 percent in August and 2 percent in July. “The decelerating pace of improvement suggests the U.S. economy could be losing momentum heading into the final quarter of 2020,” said Ataman Ozyildirim, director of business cycles research.

- The Treasury Department opposes extending the Federal Reserve’s $500 billion municipal lending program beyond the end of 2020 or easing the costly terms that have left it virtually unused. The Trump administration’s views were laid out in response to questions from the Congressional Oversight Commission, which was created to monitor the central bank lending efforts ushered in by the March economic stimulus bill. Extending the Fed’s ability to intervene in the municipal market improved the confidence of investors and caused prices to rebound from the selloff that erupted in March and threatened to curtail governments’ ability to raise cash.

- “The vaccine outlook will ultimately dwarf the election in terms of market impact,” Goldman Sachs’s strategists said. An earlier-than-expected vaccine would send equity values higher while a delay could send the market lower no matter what the election’s outcome, the bank’s analysis shows.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was natural gas, up 6.82 percent and marking its third weekly gain. Copper hit a two-year high in London on Wednesday, helped by a rally in the yuan and concerns over risks of widening supply disruptions, writes Bloomberg. The metal reached its high of $7,034 then eased back to $6,915 later in the week. Lundin Mining suspended operations at one of its Chilean mines and shipments from MMG’s Las Bambas operation were disrupted due to a protester blockage – both spurring concerns of tighter supply.

- Natural gas futures rose above $3 in the U.S. for the first time in nearly two years, supported by forecasts for cold weather. Gas rose as much as 3.1 percent on Wednesday and futures are up 69 percent since June.

- The Asian Renewable Energy Hub in western Australia, set to become the world’s largest renewable energy export facility, got the green light to fast-track through the approval process toward its target of exports by 2028. The facility will produce hydrogen using electricity from wind and solar.

Weaknesses

- The worst performing commodity for the week was once again lumber, down 3.73 percent on expected seasonal slowdown in construction. However, prices are likely to remain firm with the strong housing market. The giant United States Oil Fund (USO) had its largest one-day of outflows since 2016 of $195 million and hasn’t seen a day of positive inflows since early September. While USO surged as much as 82 percent from its April lows, it has lost momentum since the end of August, with oil prices stagnating near $40 a barrel, writes Bloomberg.

- Tianqi Lithium Corp fell as much as 5.7 percent in Shenzhen after posting a fifth straight quarterly loss as prices and sales volumes of lithium chemical products fell, reports Bloomberg. Tianqi is one of the world’s major producers of the material used in electric cars and has been struggling to repay a loan.

- BHP Group’s Olympic Dam copper operation in Australia keeps shrinking. The project was once slated for a $33 billion expansion to create one of the world’s largest mines. BHP announced this week that its latest $2.5 billion project at the site has been cancelled after understanding how high-grade metals are distributed underground, reports Bloomberg.

Opportunities

- Allonnia LLC launched on Thursday with $40 million in funding to work on engineering microbes to get rid of pollutants in wastewater and soil. The new venture is backed by Bill Gates and hopes to make sure “forever chemicals” don’t end up lasting forever, reports Bloomberg.

- Goldman released a bullish forecast for commodities this week. The bank forecasts a 12-month return of 28 percent as a structural bull market for commodities emerges in 2021 due to shrinking inventories. Metals and crops are expected to perform strongly, with Brent crude oil seen at $65 a barrel.

- Oriented Strand Board (OSB) is a low-cost alternative to plywood and its price is soaring thanks to high demand and tight supplies. Bloomberg notes that homebuilders are now spending on average $4,600 more to build a home. Although lumber tumbled from its August high, it is still up 26 percent so far in 2020. The surge in OSB demand is expected to benefit the few companies that make the material, with Norbord, Louisiana-Pacific Corp., Koch Industry Inc.’s Georgia-Pacific, and Weyerhaeuser accounting for nearly 75% of North American production.

Threats

- Satellite data released by GHGSat Inc shows global methane emissions were 1,800 parts per billion on average for the last six months. The company’s satellites detect methane emitted by oil and gas wells, coal mines, farms and more. “We’ve got a situation where for more than the last decade there’s been a significant and unexplained upward tick in global methane atmospheric concentrations,” said Jonathan Elkind, a senior research scholar at Columbia University’s Center on Global Energy Policy.

- Centamin Plc, an Egyptian-focused miner, fell as much as 19 percent in London trading on Wednesday after announcing it will produce less gold than expected in 2021. Centamin operates the Sukari gold mine in Egypt, seen as one of the best gold deposits in the world not owned by a major producer, but the company has long faced operational and political challenges. The company said 2021 output will be between 400,000 and 430,000 ounces, which is below analyst consensus of around 500,000 ounces, reports Bloomberg.

- Columbia Shipmanagement, one of the world’s biggest managers of seafarers on commercial vessels, said it is preparing to halt crew changes again if coronavirus cases continue to increase worldwide and force port closures, reports Bloomberg. The company froze crews for over two months previously when countries restricted crew changes, sparking a humanitarian crisis for seafarers stranded on ships months after contracts ended.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 1.3 percent. The central bank left its main rate unchanged at 60 basis points. Logistic company Waberer’s International was the best performing equity trading on the Budapest Stock Exchange (BUX Index) gaining 9 percent over the past five days. Majority shareholder Mid Europa Partners agreed to sell a 24 percent stake to a unit of Hungarian real estate developer Indotek. The transaction is subject to regulatory approval and is planned to close by the end of the first quarter 2021.

- The Russian ruble was the best relative performing currency this week, losing 2 percent. The Bank of Russia kept the rate on hold as well, for the second policy meeting in a row, but may renew easing once the U.S. presidential vote has passed. The country’s benchmark was left at 4.25 percent. A Biden victory in the U.S. may push the Russian currency lower on renewed talks about sanctions.

- Materials was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 90 basis points. As of Friday, Romanian officials confirmed 5,028 new COVID-19 cases in the past 24 hours – the highest daily count registered in Romania since the start of the pandemic. Banca Transilvania was the worst performing equity trading on the Bucharest Stock Exchange, losing 3.1 percent over the past five days.

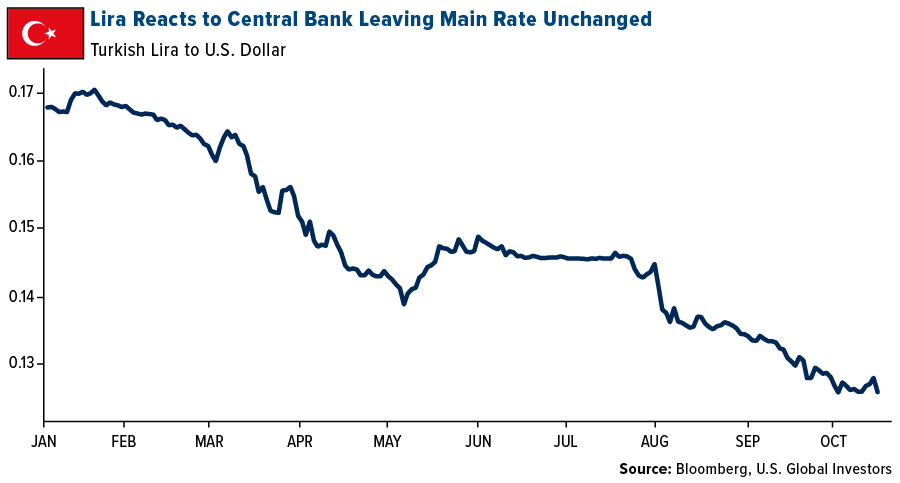

- The Turkish lira was the worst performing currency in the region this week, losing 60 basis points. The central bank unexpectedly left its one-week repo rate unchanged at 10.25 percent but hiked the late- liquidity window rate to 14.75 percent from 13.25 percent.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- Russia indicated that it may delay scheduled production hikes to stabilize oil prices as restrictions due to the coronavirus pandemic dampened the demand. Under the current plan, the OPEC and non-OPEC members are set to relax production curbs, adding nearly 2 million barrels a day in fresh oil production in January 2021. A decision will be made at the next meeting at the end of November and a higher oil price should bode well for the Russian economy.

- Russia’s largest independent gas producer, Novatek, is planning to start inviting international partners to produce blue hydrogen at the Yamal Peninsula. Russia is targeting hydrogen exports of around 200,000 tonnes per year in 2021, with volumes increasing to 2 million tonnes per year by 2035. Most exports will go to Europe.

- Ed Hyman from Evercore ISI said that the massive global stimulus is probably underappreciated, with 619 stimulus initiatives suggested around the world over the past year. The ECB will meet next week, and most likely the Central European Bank will remain accommodative and further support the economy under the pandemic. The probability for more to be done is increasing as the number of coronavirus infections are spiking again in Europe, with France recording more than 40,000 cases on Thursday.

Threats

- Bloomberg reported on a survey by McKinsey & Corporation carried out in August. The survey showed that over half of Europe’s small and medium-sized businesses say they’ll face bankruptcy in the next year if revenues don’t pick up. One in five businesses in Italy and France anticipate insolvency within six months. Bloomberg also highlighted that such businesses account for more than two-thirds of the workforce in the region and more than half of the economic valued-added.

- Turkey’s central bank left its main repo rate unchanged while Bloomberg’s economists expected a hike of 175 basis points to 12 percent from the current rate of 10.25 percent. The lira depreciated against the dollar on the day of the decision and may continue its weakness without the government’s firm action.

- Eurozone flash PMI for October showed the euro area economy back in contraction, with the composite reading at a four-month low of 49.4 versus consensus 49.2 and prior 50.4. Manufacturing activity is outpacing services sector activity, with Manufacturing PMI hit a 26-month high of 54.4 and Service PMI came in at a low of 46.2.

China Region

Strengths

- Philippines was the best performing country this week, gaining 10 percent. Equities outperformed its peers as COVID-19 cases are dropping and the economy is reopening. Foreign investors turned net buyers of Philippine stocks. Jollibee Foods Corporation was the best performing equity among the stocks trading in the iShares MSCI Philippines ETF (EPHE), gaining 22 percent over the past five days.

- The South Korean won was the best performing currency this week, gaining 100 basis points. The currency has been strengthening against the U.S. dollar since the beginning of June on improving fundamentals and exports. Finance Minister signaled discomfort over the currency’s rapid gains.

- Energy mineral stocks were the best performing among those trading on the Hong Kong Stock Exchange.

Weaknesses

- China was the worst performing market this week, losing 1.8 percent. Third-quarter GDP was reported at 2.7 percent versus an expected 3.3 percent. The economy grew by 4.9 percent versus an expected 5.5 percent on a year-over-year basis. This week China released slightly weaker GDP data but still is projected to record annual growth this year, one of few global economies to have revenue during the coronavirus pandemic. Walvax Biotechnology was the worst performing equity among stocks listed on the Shanghai and Snenzhen Stock Exchange (SHSZ300 index) losing 16 percent over the past five days.

- The Indian rupee was the worst performing currency this week, losing 57 basis points. India’s government is budgeting $7 billion to vaccinate the nation’s 1.3 billion people.

- Distribution services stocks were the worst performing among those trading on the Hong Kong Stock Exchange.

Opportunites

- Although missing estimates, China’s third-quarter GDP rose and shows signs of a broadening recovery. GDP expanded 4.9 percent in the quarter ended September 30 from a year earlier, lower than expectations for a 5.5 percent expansion. The strong number highlights how China is still on track to be the world’s only major growth engine due to its aggressive approach to managing the coronavirus pandemic.

- Ant Group, backed by Jack Ma, won approval from the Hong Kong stock exchange for its IPO. This is seen as a win as the company hopes to go public prior to the U.S. election. Bloomberg reports that the company plans a roadshow of at least 3.5 days to pitch the shares to investors.

- CLSA analysts wrote this week that a Joe Biden win in the U.S. presidential election could favor China in the near-term, since the new administration may adopt a comprehensive approach rather than the unpredictable actions that have characterized the Trump administration. Analysts also note that Chinese equities have reacted positively following previous elections that resulted in a Democratic president.

Threats

- The U.S. designated six more Chinese publications as “foreign missions,” adding to the growing list of media outlets it describes as controlled by Beijing. The outlets include the Economic Daily, Jiefang Daily, Yicai Global, Xinmin Evening News, Social Sciences in China Press and the Beijing Review.

- Goldman Sachs Group Inc.’s Asian unit was fined $350 million by the Hong Kong financial regulator for its role in Malaysia’s 1MDB investment scandal, reports Bloomberg. Goldman reached a deal with the U.S. Department of Justice to pay more than $2 billion to resolve a criminal investigation into its role in the scandal.

- U.S Secretary of State Mike Pompeo is visiting India next week to strengthen strategic ties. This is seen as another effort to bolster allies against Beijing. India is locked in a military standoff with China.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 23 was Culture Ticket, up 833 percent.

- Shares of Canada’s first publicly listed bitcoin fund are up 30 percent since its launch in April, reports CoinTelegraph.

- On Wednesday, PayPal officially confirmed it is entering the cryptocurrency market, reports CoinDesk. PayPal pledged to make crypto a “funding source for purchases at its 26 million merchants worldwide.” Bitcoin and other digital assets rallied following the announcement.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended October 23 was Penta, down 98 percent.

- Bitcoin appears to be a bit overheated, writes Bloomberg. After surging past $13,000 on Wednesday, price charts followed by technical analysts suggest the largest cryptocurrency may be due for a pause “in the wake of the exuberance triggered by the announcement that PayPal will let customers use cryptocurrencies,” the article continues.

- As the price of Ether picks up alongside that of bitcoin, CoinTelegraph writes that confidence in decentralized finance is beginning to shake as the industry’s growth and hype are slowing down. As the article explains, DeFi has been the major kick-starter for cryptocurrency popularity in 2020, but now, other digital assets seem to be ready to start thriving instead.

Opportunities

- Russian investors like cryptocurrency almost as much as they like gold, reports CoinTelegraph. A new report from the World Gold Council shows that cryptocurrency is the fifth-most popular investment tool in Russia after savings accounts, foreign currencies, real estate and life insurance.

- Billionaire hedge fund manager Paul Tudor Jones says he’s even more bullish on bitcoin, lauding the “intellectual capital” behind the leading cryptocurrency in an interview on CNBC this week. “I like bitcoin even more now than I did then,” Jones said, referring to his May appearance on the show when he announced a single-digit percentage portfolio allocation to bitcoin, CoinDesk reports. “I think we’re in the first inning of bitcoin.”

- Kyrgyzstan’s acting President and Prime Minister Sadyr Japarov has proposed introducing a blockchain-based system to ensure fair elections in the near future, reports CoinTelegraph, and restore public faith in the democratic process. “We have three revolutions because of unfair elections,” Japarov said. “I consulted with the Central Election Commission and offered them to introduce blockchain technology. This system can be implemented in 3-6 months.”

Threats

- According to an attorney for the Electronic Frontier Foundation (EFF), the U.S. Department of Justice’s recent crypto enforcement framework (released earlier this month), is a threat to digital privacy rights. Marta Belcher, special counsel to the digital rights advocacy group, pointed out language on peer-to-peer exchanges, mixers/tumblers and “anonymity enhanced cryptocurrencies.”

- The People’s Bank of China is drafting a law that recognizes the renminbi in both physical and digital form, writes CoinDesk. This will also essentially clear the way for the digital yuan to be the one and only official yuan-pegged token in mainland China. “To prevent risks associated with virtual currency, any other legal entity or individuals can not issue or sell tokens to replace the circulation of the renminbi,” states article 22, section 3. As the article explains, this revision would take a toll on one of the biggest crypto-related businesses in China since many Chinese investors conduct crypto-to-crypto trading with stablecoins.

- Harvest Finance, a decentralized finance project, has an admin key that gives its holders the ability to mint tokens at will and steal users’ funds, writes CoinTelegraph. “This power could allow the governance key holders to create an unlimited number of tokens and drain funds in the token’s Uniswap pool, which currently holds $12 million in USDC,” the article explains.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.84 | +0.09 | +12.47% |

| Oil Futures | 39.74 | -1.14 | -2.79% |

| Hang Seng Composite Index | 3,899.96 | +43.96 | +1.14% |

| S&P Basic Materials | 414.64 | -1.79 | -0.43% |

| Korean KOSPI Index | 2,360.81 | +19.28 | +0.82% |

| S&P Energy | 229.96 | +1.18 | +0.52% |

| Nasdaq | 11,548.28 | -123.28 | -1.06% |

| DJIA | 28,335.57 | -270.74 | -0.95% |

| Russell 2000 | 1,640.50 | +6.70 | +0.41% |

| S&P 500 | 3,465.42 | -18.39 | -0.53% |

| Gold Futures | 1,904.90 | -1.50 | -0.08% |

| XAU | 145.46 | -1.63 | -1.11% |

| S&P/TSX VENTURE COMP IDX | 717.78 | -7.53 | -1.04% |

| S&P/TSX Global Gold Index | 352.51 | -12.28 | -3.37% |

| Natural Gas Futures | 2.96 | +0.18 | +6.64% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,360.81 | +27.57 | +1.18% |

| 10-Yr Treasury Bond | 0.84 | +0.17 | +24.67% |

| Gold Futures | 1,904.90 | +36.50 | +1.95% |

| S&P Basic Materials | 414.64 | +27.57 | +7.12% |

| S&P 500 | 3,465.42 | +228.50 | +7.06% |

| DJIA | 28,335.57 | +1,572.44 | +5.88% |

| Nasdaq | 11,548.28 | +915.29 | +8.61% |

| Oil Futures | 39.74 | -0.19 | -0.48% |

| Hang Seng Composite Index | 3,899.96 | +154.80 | +4.13% |

| S&P/TSX Global Gold Index | 352.51 | +3.91 | +1.12% |

| XAU | 145.46 | +9.71 | +7.15% |

| Russell 2000 | 1,640.50 | +189.05 | +13.02% |

| S&P Energy | 229.96 | +0.91 | +0.40% |

| S&P/TSX VENTURE COMP IDX | 717.78 | +40.74 | +6.02% |

| Natural Gas Futures | 2.96 | +0.83 | +39.15% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 145.46 | -1.02 | -0.70% |

| S&P/TSX Global Gold Index | 352.51 | -22.99 | -6.12% |

| Gold Futures | 1,904.90 | -12.50 | -0.65% |

| DJIA | 28,335.57 | +1,683.24 | +6.32% |

| S&P 500 | 3,465.42 | +229.76 | +7.10% |

| Nasdaq | 11,548.28 | +1,086.86 | +10.39% |

| Korean KOSPI Index | 2,360.81 | +144.62 | +6.53% |

| Natural Gas Futures | 2.96 | +1.17 | +65.66% |

| S&P Basic Materials | 414.64 | +26.62 | +6.86% |

| Russell 2000 | 1,640.50 | +150.30 | +10.09% |

| Oil Futures | 39.74 | -1.33 | -3.24% |

| Hang Seng Composite Index | 3,899.96 | +90.71 | +2.38% |

| S&P/TSX VENTURE COMP IDX | 717.78 | +37.58 | +5.52% |

| S&P Energy | 229.96 | -55.83 | -19.54% |

| 10-Yr Treasury Bond | 0.84 | +0.26 | +44.91% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2020):

B2Gold Corp

Banca Transilvania SA

Novatek

Lundin Mining Corp

Lundin Gold Inc

BHP Group Ltd

Norbord Inc

Louisiana-Pacific Corp

Centamin PLC

Polyus PJSC

Kinross Gold Corp

Sibanye Stillwater Ltd

Delta Air Lines Inc.

Alaska Air Group Inc.

Southwest Airlines Co.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Consumer Comfort Index is produced by Langer Research Associates of New York. Each release includes results among 1,000 randomly selected adults, with breakdowns available by age, race, sex, education, political affiliation and other groups. The Index has significant long-term correlations, including on a time-lagged basis, with a variety of key economic indicators.

The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables.

Moody’s Analytics and CNN Business have partnered to create a proprietary Back-to-Normal Index, comprised of 37 national and seven state-level indicators. The index ranges from zero, representing no economic activity, to 100%, representing the economy returning to its pre-pandemic level in March.

The S&P GSCI is widely recognized as a leading measure of general price movements and inflation in the world economy. It provides investors with a reliable and publicly available benchmark for investment performance in the commodity markets.