Need-to-Know Numbers You Might Have Missed This Week

Date Posted: November 29, 2019

Read time: 51 min

Another year, another Thanksgiving. I hope all of my American friends and readers had the chance to spend some quality time with family as we begin the busy holiday shopping season.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Another year, another Thanksgiving. I hope all of my American friends and readers had the chance to spend some quality time with family as we begin the busy holiday shopping season. The leading retail trade group expects sales this month and in December to increase as much as 4.2 percent over last year, for a total potential value of $730.7 billion.

Part of this growth is due to the market selloff that happened at the end of 2018. But there’s more to the story than that.

As I told you last week, the U.S. purchasing manager’s index (PMI), a leading indicator of economic activity, turned up for the third straight month in November. This is a good reflection of healthy demand, and a possible signal of further upside. There’s still a month left to 2019, and yet stocks are already up an incredible 28 percent.

Below are some more need-to-know numbers you might have missed from this past week.

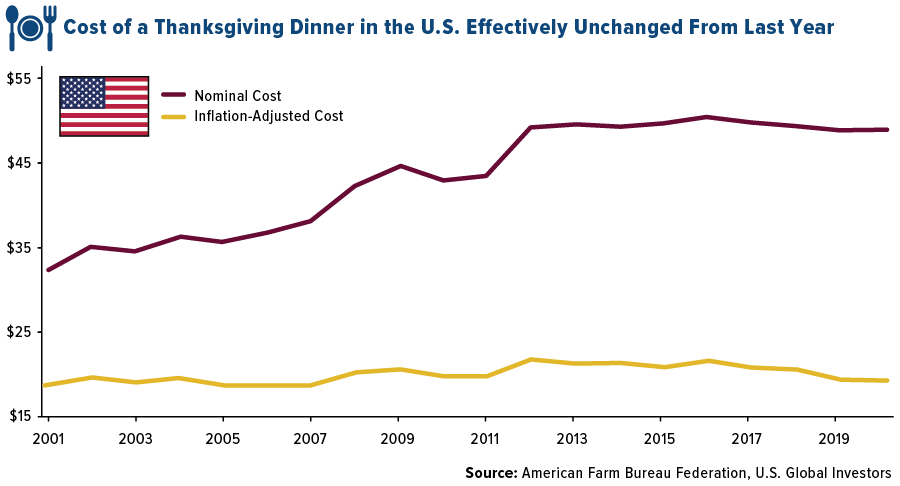

$0.01 Increase for a Thanksgiving Dinner

One of the more interesting ways to measure U.S. inflation is by tracking the annual price of a typical Thanksgiving dinner for 10. That’s what the American Farm Bureau Federation (AFBF) has been doing for the past 34 years, and in its most recent survey, the group found that the total cost was effectively flat, rising only $0.01—from $48.90 in 2018 to $48.91 today. That’s as little as $5 per person. As Evercore ISI pointed out in a research note this week, the cost of a Thanksgiving dinner is lower now than it was eight years ago—the first time we’ve seen that since 1947.

“Americans continue to enjoy the most affordable food supply in the world,” commented AFBF Chief Economist John Newton.

55 Million Travelers

If you traveled at all this week, I hope you planned ahead. An estimated 55 million people in the U.S. were expected to hit the road or take to the skies this Thanksgiving season, up 1.6 million people, or nearly 3 percent, from last year, according to the American Automobile Association (AAA). That’s the most people since 2005. Looking at air travel alone, some 4.45 million Americans are expected to fly on domestic airlines, an annual increase of 4.6 percent.

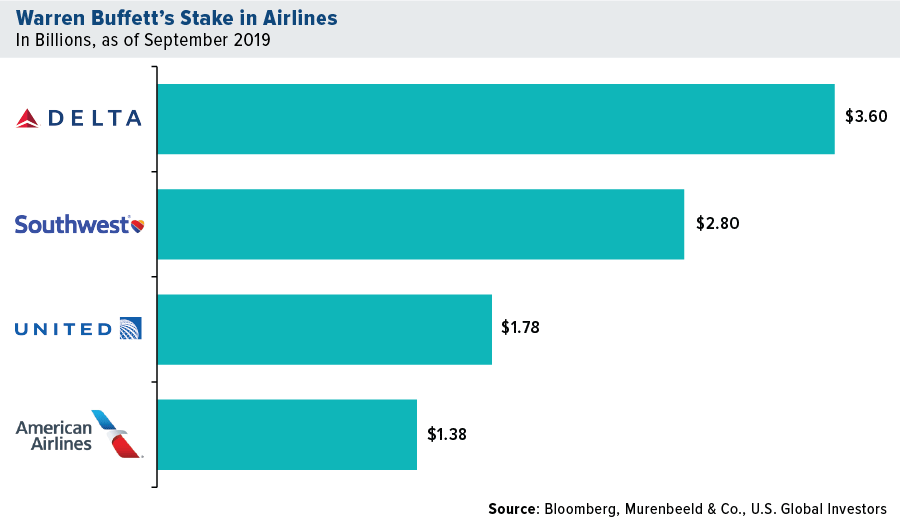

$10 Billion Stake in U.S. Airlines

Speaking of airlines… In this week’s equity and bond report, Murenbeeld & Co. analysts Brian Bosse and Chantelle Schieven bring to our attention a lesson inspired by Warren Buffett—namely, investors must change when the facts change.

As recently as 12 years ago, Buffett was famously warning investors to steer clear of the airline industry, which had been destroying capital at least since deregulation in 1978. After the industry consolidated and restructured a couple of years later, however, airlines have committed themselves to capacity growth discipline and returning value to shareholders.

“When an industry changes from reliably destroying shareholder capital into providing reliable positive returns which create economic value, then astute investors should take notice,” Boose and Schieven write.

Buffett certainly took notice, and today his stake in the “Big Four” carriers stands at just under $10 billion.

Another industry that Murenbeeld & Co. call out for transforming from “money wasters to money spinners”? The mining industry.

$3.7 Billion Deal

Like airlines before it, the gold mining industry is seeking to improve shareholder value through consolidation, among other means. This week, we learned that Kirkland Lake Gold will be buying rival Detour Gold in an all-stock deal valued at C$4.9 billion ($3.7 billion). This is just the latest deal in the current wave of consolidation that began last year with the Barrick-Randgold deal and Newmont-Goldcorp deal.

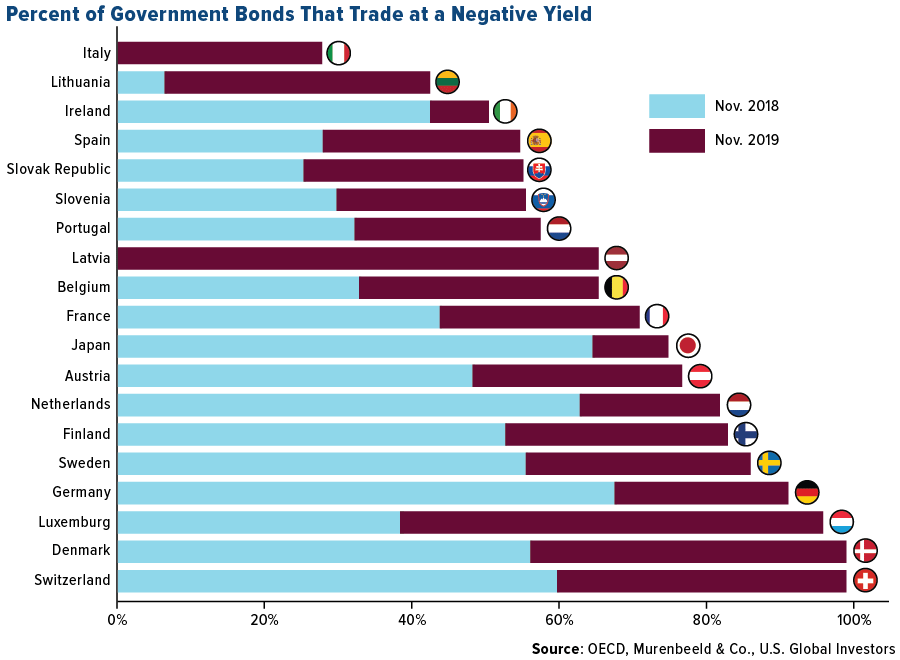

$12 Trillion in Negative-Yielding Debt

One of the key drivers of the price of gold this year has been the surging mountain of negative-yielding government bonds. According to Murenbeeld, this amount, as of November, is a mind-boggling $12 trillion. That’s down from $17 trillion in August, but if you look below, you’ll see that more than half—and, in some cases, close to 100 percent—of some economies’ outstanding debt is trading at negative yields.

16,700 Percent Return in 50 Years

This week marks 50 years since the debut of the Hang Seng Index, the widely quoted gauge of the 50 largest companies trading in Hong Kong. From its launch in November 1969, the Hang Seng is up some 16,700 percent, making it the world’s best-performing stock index by a wide margin.

Originally intended as a measure of local firms, the Hang Seng has increasingly become a proxy of China’s economy.

Today, about half of the Hang Seng is represented by mainland Chinese heavyweights such as Tencent, China Mobile and Geely Automotive. Shares of Chinese e-commerce giant Alibaba began trading in Hong Kong for the first time this week. With a market cap of 4 trillion Hong Kong dollars ($513 billion), Alibaba is already the city’s biggest stock, meaning we’ll likely see it join the Hang Seng, possibly as soon as its next rebalance.

As I wrap up today’s note, I want to wish everyone a blessed holiday weekend! I often say that having gratitude improves your way of looking at the world. It’s important that we take stock not only in our finances but also the people who matter most, from family and friends to coworkers and business associates.

Gold Market

This week spot gold closed at $1,463.91,up $2.31 per ounce, or 0.16 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.18 percent. The S&P/TSX Venture Index came in up just 0.69 percent. The U.S. Trade-Weighted Dollar ended the week unchanged.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-26 | Hong Kong Exports YoY | -8.4% | -9.2% | -7.3% |

| Nov-26 | New Homes Sales | 705k | 733k | 738k |

| Nov-26 | Conf. Board Consumer Confidence | 127.0 | 125.5 | 126.1 |

| Nov-27 | GDP Annualized QoQ | 1.9% | 2.1% | 1.9% |

| Nov-27 | Durable Goods Orders | -0.9% | 0.6% | -1.4% |

| Nov-27 | Initial Jobless Claims | 221k | 213k | 228k |

| Nov-28 | Germany CPI YoY | 1.2% | 1.1% | 1.1% |

| Nov-29 | Eurozone CPI Core YoY | 1.2% | 13% | 1.1% |

| Dec-1 | China Caxin PMI Mfg | 51.5 | — | 51.7 |

| Dec-2 | ISM Manufacturing | 49.5 | — | 48.3 |

| Dec-4 | ADP Employment Change | 145k | — | 125k |

| Dec-5 | Initial Jobless Claims | 216k | — | 213k |

| Dec-5 | Durable Goods Orders | — | — | 0.6% |

| Dec-6 | Change in Nonfarm Payrolls | 190k | — | 128k |

Strengths

- The best performing metal for the week was palladium, up 3.66 percent. Palladium reached a fresh record this week, reports Bloomberg, hitting $1,842.76 an ounce and extending this year’s rally to 46 percent. Gold also witnessed safe haven buying following Trump’s signing of a bill supporting Hong Kong protestors. Despite renewed hopes for a U.S.-China trade pact, holdings in gold-backed ETFs also rose the most since mid-October, helping support prices.

- According to central bank governor Adam Glapinski, Poland repatriated around 100 tons of gold from the Bank of England in a bid to demonstrate the strength of the nation’s $586 billion economy, writes Bloomberg. Poland could generate “multi-billion” profits if it sold its holdings, but has no plans to do so, he said. In Turkey, official gold reserves, including deposits and swaps, increased 2.7 percent to $26.6 billion, compared to September, according to central bank in Ankara.

- A news release from JP Morgan highlights that Impala Platinum Holdings’ $758 million acquisition of North American Palladium has received key regulatory approvals, with the deal expected to close on December 13. As the research note goes on to explain, the bank expects Impala to return to net cash in 2020, with under $1 billion estimated in 2021 if spot PGM prices hold. This would indicate strong capacity in 2020 to pay its first dividend since 2013. Impala may yet snatch up one of Canada’s long-life precious metals assets at a highly discounted valuation.

Weaknesses

- The worst performing metal for the week was silver, up just 0.21 percent on little news during the holiday week. For the first time in three weeks, gold bears outnumbered bulls in a weekly poll of traders and analysts carried out by Bloomberg. Adding to that sentiment, gold headed for its biggest monthly drop in three years, as Bloomberg reports, as lingering optimism over a U.S.-China trade deal eased demand.

- As the national bureau of statistics reported Monday, China’s gold imports fell in the month of October nearly two-thirds from a year prior. As mentioned above, another big contributing factor for gold falling this week was signs of progress in the trade talks sapping haven demand. As China and India gold imports slump as well, Capital Economics says the “gold price rally is now behind us, and that ongoing weakness in consumer demand will be one of the factors weighing on the price of gold over the coming year.”

- Chinese consumers are grappling with the slowest economic growth since the early 1990s, writes Bloomberg, which could put a dent in gold consumption and the overall gold price in the coming year. Another Bloomberg headline could mean weaker gold prices as well – apparently a growing chorus of strategists and investors is calling for a weaker dollar. However, option traders are reluctant to bet against the greenback, the article continues.

Opportunities

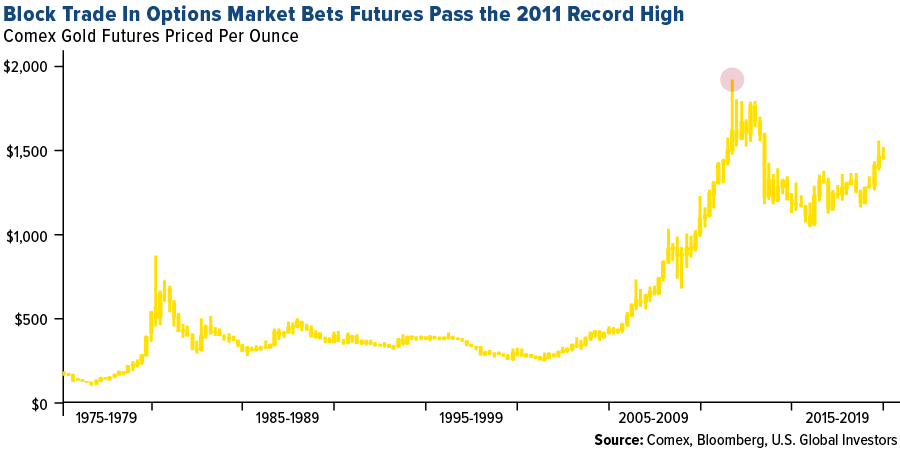

- The gold options market saw $1.75 million in block trades betting the precious metal could almost triple in more than a year (and surpass the record), reports Bloomberg. Mid-week in New York, 5,000 lots for a gold option giving the holder the right to buy the precious metal at $4,000 an ounce in June 2021 changed hands, the article reads. On a semi-related note, Goldman Sachs is looking positive at gold too. The group believes that late-cycle concerns, heightened political uncertainty, coupled with only modest growth acceleration, should support demand for the yellow metal moving into 2020, Bloomberg reports. Silver could also get a rally in the New Year, according to HSBC Global Research analysts, based on firm gold prices and rising investor demand.

- An M&A spree is sweeping the gold mining industry, reports Bloomberg. Canada’s Kirkland Lake Gold has agreed to buy Detour Gold Corp. for C$4.9 billion ($3.7 billion). Kirkland CEO Tony Makuch is facing an uphill battle to convince both investors and analysts that he made the right decision. “We have to do work to create that value but we see opportunity to create value not recognized yet,” Makuch said in a Bloomberg Television interview. In a similar piece of news, Evolution Mining has agreed to buy Newmont Goldcorp’s Red Lake complex (Newmont’s highest-cost project). According to a statement by the company on Monday, Newmont will get $375 million in cash for the sale of the complex in Ontario, Canada, and as much as $100 million in additional payments tied to new resource discoveries.

- Toronto-based Triple Flag Precious Metals Corp. announced plans to raise $360 million through an initial public offering (IPO) next year, reports the Financial Post. With gold prices rising and equity financings still slow for mining companies, Triple Flag said it plans to open up a 17 percent stake to public investment, by issuing 20 million shares, priced between $15 and $18. In other company news, AngloGold Ashanti has narrowed its list of bidders for its remaining South African assets, reports Bloomberg. The company is now evaluating offers from Sibanye Gold and Harmony Gold Mining.

Threats

- Gold is the new obsession for East Europe’s nationalist leaders, reads one Bloomberg headline this week. Slovakia joined a host of countries seeking to repatriate gold while Serbia, Poland and Hungary all boosted their bullion reserves, the article explains. According to Slovakia’s former premier Robert Fico, parliament should force the central bank to bring back the nation’s gold stored in the U.K. But why? According to Fico, the gold isn’t safe in the U.K. because of Brexit and a possible global economic crisis.

- Global central banks, including policy makers from the European Central Bank and the Federal Reserve, are approaching the end of 2019 with a collective shudder at the risky behavior their low interest-rate policies are encouraging, writes Bloomberg. “Stock indexes from the U.S. to India are at records, and low sovereign bond yields have pushed funds into property seeking better returns,” the article reads.

- In a roundup of “Risks in 2020,” Bloomberg asked several experts what they have their eye on. Anne Richards, CEO of Fidelity International, had the following to say: “Negative bond yields are now of systemic concern. With central bank rates at their lowest levels and U.S. Treasuries at their richest valuations in 100 years, we appear to be close to bubble territory, but we don’t know how or when this bubble will burst.” Richards goes on to explain that another area of concern is with liquidity. She says that as capital becomes less free-flowing, it will weaken the ability of the financial system to respond dynamically to unforeseen liquidity events, such as an unexpected counterparty failure.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.63 percent. The S&P 500 Stock Index rose 0.99 percent, while the Nasdaq Composite climbed 1.71 percent. The Russell 2000 small capitalization index gained 2.24 percent this week.

- The Hang Seng Composite lost 0.80 percent this week; while Taiwan was down 0.67 and the KOSPI fell 0.67 percent.

- The 10-year Treasury bond yield remained essentially unchanged at 1.772 percent.

Domestic Equity Market

Strengths

- Consumer discretionary was the best performing sector of the week, increasing by 1.76 percent versus an overall increase of 1.01 percent for the S&P 500.

- Best Buy was the best performing S&P 500 stock for the week, increasing 10.99 percent.

- Best Buy rallied after reporting better-than-expected earnings and sales and raising its guidance ahead of Black Friday. The company reported a profit of $1.13 a share, beating forecasts for $1.03, according to FactSet. Sales of $9.76 billion topped estimates for $9.70 billion.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 1.55 percent versus an overall increase of 1.01 percent for the S&P 500.

- Dollar Tree Inc. was the worst performing S&P 500 stock for the week, falling 16.18 percent.

- Dollar Tree shares fell early in the week after reporting mixed fiscal third-quarter results and issuing disappointing guidance, reports the Wall St. Journal. Although sales of $5.75 billion topped analyst expectations, earnings of $1.08 a share came up short.

Opportunities

- Under Armour shares were upgraded to strong buy from outperform by Raymond James’ Matthew McClintock, who cited the company’s valuation, “strong like a rock” infrastructure, and fewer execution and headline risks.

- The United States Food and Drug Administration has approved Biocon Ltd. and Mylan NV’s supplemental biologics license application for a drug substance to be manufactured at the Indian drugmaker’s new facility in Bengaluru, writes Bloomberg. This additional approval of its new manufacturing facility for pegfilgrastim in Bengaluru will enable Biocon Biologics and Mylan to scale up capacity multifold and address the growing market opportunities in the U.S. and other global markets, the company said.

- Autodesk analysts raised their price targets on the stock this week after it reported third-quarter results and gave an outlook for its free cash flow that was seen as strong.

Threats

- Uber lost its license to operate in London thanks to fraudulent drivers. The ride share giant said it would appeal the decision, and CEO Dara Khosrowshahi said the decision was wrong.

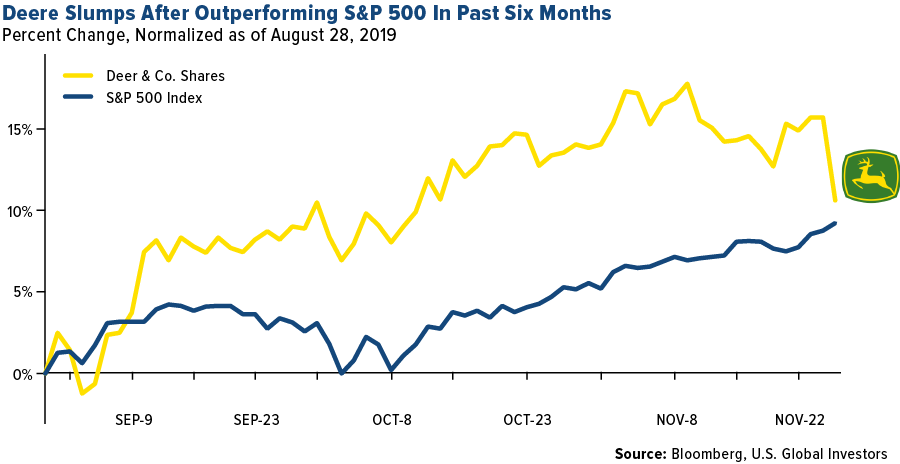

- Deere posted modestly stronger -than –expected, fourth-quarter earnings but cautioned that construction and agricultural equipment sales in the coming financial year are likely to decline sharply as trade uncertainty hammers demand.

- Dell announced that a shortage of chips from its main supplier, Intel, would hit sales for the final months of the year.

The Economy and Bond Market

Strengths

- U.S. economic growth picked up slightly in the third quarter, reports Reuters, with growth domestic product coming in at a 2.1 percent annualized pace and topping the previous estimate, according to a Commerce Department report. The upward revision largely reflects an inventory accumulation in the period, as consumer spending growth was unrevised.

- The number of people who applied for unemployment benefits fell sharply in the week before the U.S. Thanksgiving holiday, writes MarketWatch, putting jobless claims back near historic lows and reflecting the persistent strength in the U.S. labor market. Initial jobless claims fell 15,000 to 213,000 in the seven days ended November 23, the government reported Wednesday.

- Following a steep drop in U.S. durable goods orders in the prior month, the Commerce Department reported a 0.6 percent climb in orders in October, writes Nasdaq.com. The unexpected increase in orders came as jumps in orders for aircraft and parts more than offset a steep drop in orders for motor vehicles in parts, resulting in a 0.7 percent increase in orders for transportation equipment.

Weaknesses

- According to data released by the Conference Board on Tuesday, consumer confidence fell for a fourth consecutive month in November, reports CNBC, as economic conditions weaken toward the end of the year. This “suggests that economic growth in the final quarter of 2019 will remain weak,” said Lynn Franco, senior director of economic indicators at The Conference Board, in a statement.

- On Wednesday, the Commerce Department reported that U.S. personal income came in nearly flat for October, reports Nasdaq, while personal spending rose in line with estimates. When it comes to real disposable income, or income adjusted to remove price changes, a drop of 0.3 percent was seen due to the “unwinding of farm subsidies paid out by the Trump administration and a decrease in interest income as the Federal Reserve cut rates,” the article explains.

- The Chicago Purchasing Management Index came in at 46.3 in November, reports MarketWatch, a measure of economic activity in the Midwest. Economists expected a November reading of 46.5, according to the StreetAccount consensus on FactSet.

Opportunities

- Next Friday will see the release of November’s U.S. nonfarm payrolls. Forecasts call for a strong 190,000, up from October’s 128,000.

- Next week’s release of the unemployment rate is forecast to show a slight improvement from 3.6 percent to 3.5 percent.

- Next week’s final November Markit U.S. Manufacturing PMI is expected to hold steady from its preliminary reading of 52.2.

Threats

- While Monday’s November ISM Manufacturing release is forecast to improve to 49.5 from October’s 48.3, the reading is expected to remain below the 50 mark that signals expansion or contraction.

- Next Friday’s University of Michigan Sentiment preliminary December reading is at risk of disappointing expectations. Particularly given this week’s lackluster print of the Conference Board Consumer Confidence Index.

- Next week’s factory orders report is forecast to register flat growth. Even this is at risk given this week’s weak Chicago PMI.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was wheat, which gained 4.14 percent. Inventories in Europe are low, drops in Russian and Australian output have tightened the market, and recent weather issues in Argentina and France have all pushed prices up by 20 percent over the past year. Oil was heading for a fourth weekly gain, but on Friday prices tanked as much as 4.9 percent as Russia and Saudi Arabia grow intolerant to cheating and revenue losses, overshadowing next week’s OPEC meeting.

- Fortescue CEO Elizabeth Gaines said at a media conference in Perth this week that the company is focused on a range of copper opportunities that are in the exploration phase. “We’ve identified copper as the commodity we’re interested in because we believe there will be growth in electric vehicles and demand for better materials.” Another big miner moving more toward copper is BHP Group, which increased its stake in Ecuadorian copper miner SolGold Plc to 14.7 percent. Deutsche Bank commodity strategist Nick Snowdon wrote in a note this week that the bank expects China’s copper consumption growth to reaccelerate in 2020 after a sluggish year of demand.

- Rio Tinto, the world’s second largest miner, announced this week that it will lift its spending on new iron ore projects in Australia to more than $4 billion. Rio will invest $749 million to bring its Western Turner Syncline Phase 2 project into production from 2021, reports Bloomberg. This is a sign of confidence of demand led by China for iron ore picking up. Rivals BHP Group and Fortescue Metals Group are also spending big on iron projects in Australia.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 14.43 percent as record production offsets demand growth and December weather forecasts outline milder conditions. Nickel prices have dropped 17 percent this month, putting it on course for the biggest monthly loss among major commodities, reports Bloomberg. Deere & Co. issued a more cautious outlook than expected for 2020 as the continued trade war and difficult growing conditions keep North American farmers from replacing large equipment, reports Bloomberg. Global sales of agriculture and turf equipment are forecast to fall 5 percent to 10 percent for fiscal 2020 and construction and forestry equipment are also anticipated to fall 10 percent to 15 percent.

- The Canadian National (CN) strike ended on Tuesday after eight days – marking Canada’s longest railroad strike in at least a decade. The company reached a tentative agreement with workers, but shippers warned that it could take weeks before service resumes as normal, reports Reuters. Half of the nation’s exports are transported via rail and the strike will likely cost the economy around $750 billion and cut fourth quarter GDP by 0.1 percentage point, according to Brian DePratto, a senior economist at TD.

- United Nations-backed Libyan government troops retook the El-Feel oil field from eastern commander Khalifa Haftar and halted output. National Oil Corp (NOC) chairman said that airstrikes were at the gates of the oilfield and that staff were in a safe area. El-Feel produces around 70,000 barrels a day and is operated by a joint venture between Eni SpA and state-producer NOC. Libya has Africa’s largest crude reserves and relies on exports for most of its revenue, which could be hurt due to the oilfield’s temporary shuttering.

Opportunities

- Animal fat is gaining prominence as the “renewable diesel”. Bloomberg reports that Marathon Petroleum Corp., Phillips 66 and HollyFrontier are joining Valero Energy Corp. in developing new projects designed to produce a second-generation fuel made from animal fat that is nearly chemically identical to the petroleum form. This new version of biodiesel is processed at much higher temperatures in specialized equipment, solving the issue of prior biofuels not packing the same punch as petroleum-based fuel. A report by Piper Jaffray & Co. shows that Valero’s existing joint venture in the renewable diesel field could generate $1.4 billion in earnings by 2024.

- According to Goldman Sachs Group, efforts to combat climate change are restricting capital into drilling in mining, which should limit commodities supply and support higher prices in 2020. Bloomberg reports that the commodities analysts made their top trade recommendation a long position in the oil-heavy Enhanced S&P GSCI index. The November 25 report says “capex declines should keep prompt supplies tight where inventories have already been depleted.”

- Coal-reliant Poland is finally taking steps to meet European climate targets. Poland will auction support for 3.4 gigawatts of onshore wind and solar power in December, worth as much as $8.3 billion. The country generates 80 percent of its power from coal and had almost completely halted the expansion of wind energy for several years. Bloomberg reports that the auction would boost wind capacity by around 40 percent.

Threats

- Despite growing efforts to curb the use of coal, the amount of electricity generated from the polluting fossil fuel rose 7 percent in 2018, according to a BloombergNEF report. Coal consumption is falling in the U.S. and Europe, but it continues to grow in many emerging markets as it is cheaper than wind or solar power. The study also found that investments in clean energy across emerging markets fell 21 percent to $133 billion due to pullbacks from China, India and Brazil.

- Codelco, the world’s largest copper producer, is owned by the Chilean state and could face troubles as protests threaten funding. Protesters are demanding big changes from the government, which could hurt funding for the copper producer that had planned to spend $20 billion over the next 10 years to modernize its aging mines. BMO managing director of commodities research Colin Hamilton says “targeting flat production is optimistic” and “Codelco might not be the world’s largest copper miner in three to four years.”

- American LNG suppliers may be forced to halt production as the global glut of natural gas has exploded. Citigroup said in a note to clients this week that prices for LNG may collapse in Europe and Asia next year which would force U.S. suppliers to curb output. Morgan Stanley sees as much as 2.7 billion cubic feet a day of American exports curtailed around the second or third quarter, assuming normal weather, reports Bloomberg. Chinese demand for U.S. LNG has plunged amid the trade war while Europe’s gas storage is nearly full.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 1.7 percent. Banks were the best performing equites trading on the Bucharest exchange with BRD-Groupe Societe Generale SA gaining 4.4 percent and Banca Transilvania up 3.2 percent. Wood & Company published a positive research report on both names, mainly due to banks’ large capital buffers and ability to pay high dividends. Moreover, the Romanian Premier said that he is looking for ways to cancel the bank tax.

- The Hungarian forint was the best performing currency this week, gaining 5 basis points. Strong economic data supported the currency. GDP came in at 5 percent in the third quarter on a year-over-year basis, making Hungary the fastest growing economy in central emerging Europe. Unemployment remains at a record low level of 3.5 percent.

- Consumer discretionary was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 80 basis points. MOL Hungarian Oil & Gas was the biggest contributor to the Budapest exchange underperformance, which shares declined by 1.5 percent. MOL sold Treasury shares in a deal signed on November 11.

- The Turkish lira was the worst performing currency in the region this week, losing 63 basis points. Turkey’s decision to test the S-400 anti-aircraft missile system purchased from Russia sparked fresh talks in the U.S. Senate to impose sanctions on the NATO ally mandated by the current law.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- French consumer confidence rose to a two-year high of 106.0 versus consensus 103.0 and prior 104.0. President Macron’s stimulus measures have been supportive. Households have become more optimistic about their financial situation and ability to make significant purchases. Fears of unemployment have also fallen further below the long-term average and consumer assessment of living standards improved.

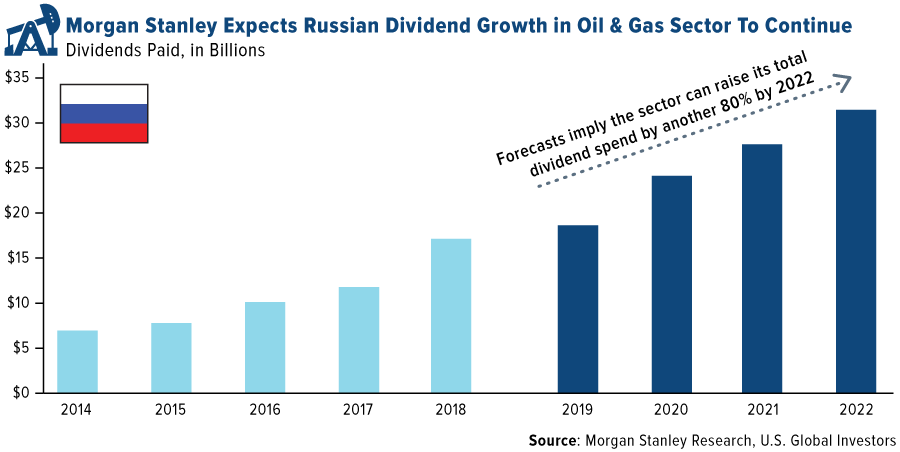

- Morgan Stanley predicts that Russian oil and gas total sector dividends could grow by 80 percent in three years, despite over the last four years Russian oil and gas companies increased dividends almost three-fold. Increasing dividend payments are higher priority as a strong balance sheet will provide cushion in case of weaker market conditions.

- Takeover by European buyers nearly tripled in the month of November standing at $53 billion, and a majority of half the deal volume came from purchases of U.S. companies. Louis Vuitton (LVMH) announced Monday it will acquire Tiffany & Co. for $16.2 billion, and Novartis announced buying Parsippany, a New Jersey-based medicine company for $9.7 billion. There were a slew of smaller deals, but another big deal could come before year end with Irish Kerry Group Plc working on due diligence on a potential takeover of DePont de Nemours Inc.’s $25 billion nutrition unit, Bloomberg news has reported.

Threats

- According to a new survey, most young Russians (53 percent), aged 18 to 24 years would like to emigrate from Russia. Higher age groups have less of a desire to leave the country but the numbers are still high, with 30 percent of those aged 25 to 39 wanting to leave and 19 percent of 40 to 54 years old wishing to emigrate. Those with a desire to leave Russia want a better future for their children, a stronger economy and a different political situation in the country.

- Turkey is at odds with its NATO allies over its recent military in northeastern Syria, and its purchase of the Russian S-400 missile system. On December 3, leaders of NATO countries will meet in celebration of the 70th anniversary of the North Atlantic Treaty Organization. The President of Turkey might ask leaders of France, Germany and the U.K. to help fund the buffer zone in Northern Syria, creating political tension between NATO members.

- Investment by Czech companies continued its decline in the third quarter, recording the first annual decline in two-and-a-half years, according to the Czech Statistics Office. Companies are feeling a gradual weakening of demand, which, along with rising wages, is creating pressure on profitability, said Lubos Ruzicka, an analyst at Raiffeisenbank AS in Prague. Overall, economic growth slowed to 2.5 percent, but still remains well ahead of the euro area’s expansion.

China Region

Strengths

- India was the best performing country in the region this week, gaining 1.08 percent.

- Some of the world’s largest brokerages are turning bullish on South Korea, whose tech-heavy stock market has been one of the biggest victims of U.S.-China trade tensions. Goldman Sachs and Morgan Stanley have both upgraded South Korean equities to overweight in the past week.

- Materials was the best performing sector this week up 1.5 percent.

Weaknesses

- Malaysia was the worst performing country in the region this week, losing 2.20 percent. Foreign direct investment inflows to Malaysia from China plummeted to 19 million ringgit ($4.6 million) in the first half of 2019, from more than 700 million ringgit in 2018, according to data from the country’s central bank.

- Profits at Chinese industrial enterprises fell for a third month, dropping by the most since at least 2011. Industrial profits declined 9.9 percent in October, after September’s 5.3 percent decrease.

- Telecommunications was the worst performing sector this week down 3.42 percent.

Opportunities

- China said it will raise penalties on violations of intellectual property rights in an attempt to address one of the sticking points in trade talks with the U.S. The country will also look into lowering the thresholds for criminal punishments for those who steal IP, according to guidelines issued by the government on Sunday. The U.S. wants China to commit to cracking down on IP theft and stop forcing U.S. companies to hand over their commercial secrets as a condition of doing business there. China said it’s aiming to reduce frequent IP violations by 2022.

- South Korea on Friday suspended its plans to pull out of its intelligence-sharing pact known as the General Security of Military Information Agreement and said it would temporarily withdraw a complaint it made against Japan at the World Trade Organization. The developments marked a rare reversal in tensions that have plunged to new depths in recent years and spilled over to hurt trade and tourism. These initial moves are positive in moving both economic and diplomatic relations between Japan and South Korea back toward normalcy. But as long as Japan retains the ability to suspend exports of the critical materials, the resulting uncertainty will continue to weigh on both economies and potentially the global technology supply chain.

- The Thai government on Tuesday introduced new stimulus measures intended to boost the lagging economy, amid sluggish exports and a slowdown in private consumption. Thailand said its latest round of stimulus will spur more than 100 billion baht ($3.3 billion) of spending, as it steps up efforts to fight an economic slowdown caused by baht strength and the U.S.-China trade war.

Threats

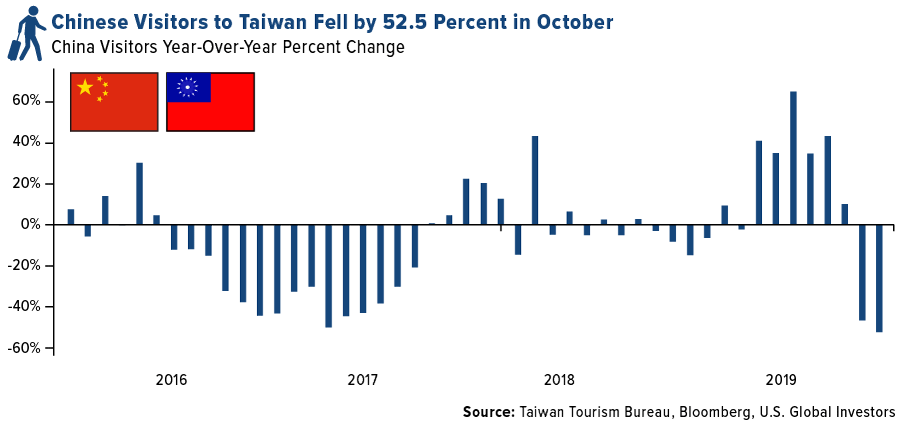

- The number of mainlanders traveling to Taiwan plunged by 52.5 percent year-over-year in October, according to data from its Tourism Bureau, following a big slump in September. As Bloomberg writes, China imposed a travel ban on individual travelers to Taiwan with effect from Aug. 1, although Chinese nationals are still allowed to visit in tour groups. The move came as Beijing attempted to isolate Taiwan and Tsai Ing-wen, its independence-leaning president.

- The Hong Kong District Council Election concluded with a significant shift in power from the pro-establishment camp to the pro-democracy party which has increased its representation on the District Council from 29percent of the seats to 86 percent, underpinned by a record voter turnout. While the outcome is likely to have a relatively minor impact on the legislative process, it does represent the first gauge of voter sentiment since the turmoil began in June 2020. Hong Kong leader Carrie Lam didn’t make any new concessions to protesters after pro-democracy forces won a landslide in local elections, a move that risks leading to further violence after months of unrest. While the specific Polytechnic situation appears to be winding down, the overall situation remains unresolved.

- Hong Kong’s exports and imports both contracted more than expected in October, dealing another blow to the ailing economy. While easing of tensions between the U.S. and China may offer some support to the re-export hub, another risk lies in the new U.S. law—just signed by President Trump on Wednesday—that now makes Hong Kong’s special trading status subject to annual State Department review for sufficient autonomy.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 29 was BitNautic Token, up over 203 percent.

- On Monday, an Ethereum “whale” (the term for someone who owns an incredible amount of a cryptocurrency) was reported to have transferred as many as 257,491 digital Ethereum coins, valued at around $35 million, to an undisclosed recipient. The total fee for the transaction? A low, low $0.07, according to BeInCrypto.com. One of crypto’s most attractive features is its ability to be traded peer-to-peer, thereby bypassing third parties and fees, and such stories serve to reinforce that feature.

- If prices can pass $7,400, bitcoin is looking at a short-term bull reversal, reads one CoinDesk headline this week. According to technical analysis, the popular digital currency has created a hammer candle on the three-day chart, a warning of an impending bull reversal. “A move above $7,380 would activate twin bullish cues on the four-hour chart and allow a rally to $8,000,” it continues.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 29 was Precium, down 99.93 percent.

- The price of bitcoin fell below $7,000 over the weekend as China reaffirmed its crackdown on domestic companies involved in crypto trading and fundraising, according to the Wall Street Journal. The world’s largest virtual currency by market cap briefly rose above $10,000 in October after China leader Xi Jinping signaled a turnaround in his attitude toward blockchain technology and cryptos. Since then, however, the Chinese government has kept up its pressure campaign on companies and exchanges that participate in cryptocurrency.

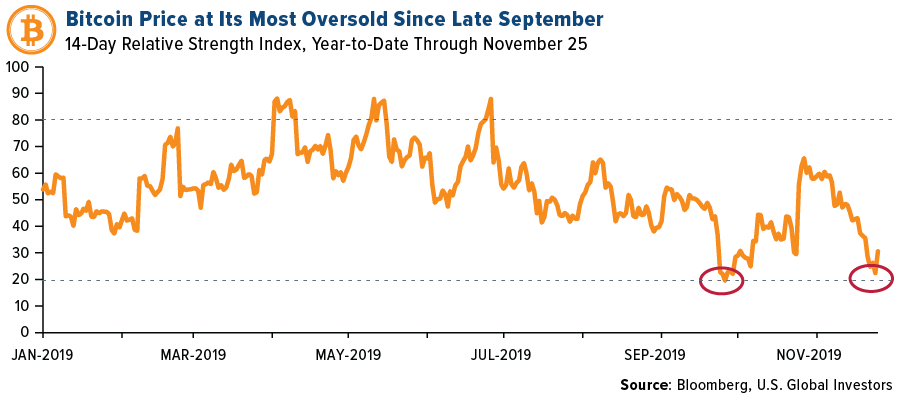

- As Bloomberg reports, bitcoin is on pace to post its worst month this year, dropping 23 percent since November 2018. And although the 14-day relative strength index shows the digital currency was oversold mid-week, other technical signals show the downturn could be coming to an end.

Opportunities

- Bitcoin appeared to be at its most oversold since late September in Sunday trading, closing in on the key “20” line based on the 14-day relative strength index (RSI). With its price now down nearly half since the 52-week high set on June 26, bitcoin could be set for a pause or rerating. Google searches for “bitcoin” spiked to its highest search rank since late October, according to Cointelegraph.

- Bank of New York Mellon will become the 28th bank to join the Marco Polo trade finance consortium, reports CoinDesk. The asset bank is evaluating the technology behind Marco Polo with the intention of onboarding clients, the article explains, if the network’s capabilities fit clients’ interests, according to global head of trade finance Joon Kim. “Our hope is that the business requirements of our clients will meet with what Marco Polo has to offer, and our intention is to move into live production A-S-A-P, Kim said.

- Claude Waelchli, a veteran of global bank UBS, is entering the increasingly crowded field of platforms for issuing digital securities on the blockchain, writes CoinDesk. Waelchli’s startup will be called Tokenyz and at launch will receive a finders fee from broker-dealers to which it refers clients and a technology fee for structuring transactions. “What we are currently looking into is creating a global alliance of the top experts in the space to provide an open forum for dialogue where you can have conversations and eventually work towards a common standard,” Waelchli said.

Threats

- In order to align with international anti-money-laundering standards, Estonia-based BitBay announced this week that it will delist the privacy-focused Monero cryptocurrency (XML), reports CoinDesk. XML will no longer be tradable from February 19, 2020, and the exchange will cease deposits of the currency as of this Friday, November 29. Monero’s privacy protections have led to other trading platforms halting support in recent months.

- In a blog post this week, South Korean cryptocurrency exchange Upbit’s CEO announced that the platform has lost crypto worth $49 million, writes CoinDesk. An abnormal transaction from its wallets resulted in the outflow of 342,000 ether (ETH) early on Wednesday. According to the article, withdrawals and deposits have already been suspended as a precaution and the exchange confirmed that the loss will be covered by its own assets.

- A resident of Washington petitioned to stop the Internal Revenue Service (IRS) from gathering data about his bitcoin holdings from the Bitstamp exchange, reports CoinDesk. On Monday, a federal judge denied that petition and instead ordered the IRS to narrow the scope of a summons it had issued to Bitstamp. As the article explains, the judge threw out several of the petitioner’s arguments on technical grounds, specifically noting that the IRS is conducting an audit of his holdings and transactions, which satisfies legal requirements for showing a legitimate purpose.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.77 | +0.00 | +0.11% |

| Oil Futures | 55.16 | -2.61 | -4.52% |

| Hang Seng Composite Index | 3,579.25 | -28.69 | -0.80% |

| S&P Basic Materials | 375.24 | +3.31 | +0.89% |

| Korean KOSPI Index | 2,087.96 | -14.00 | -0.67% |

| S&P Energy | 431.37 | -6.78 | -1.55% |

| Nasdaq | 8,665.47 | +145.59 | +1.71% |

| DJIA | 28,051.41 | +175.79 | +0.63% |

| Russell 2000 | 1,624.50 | +35.56 | +2.24% |

| S&P 500 | 3,140.98 | +30.69 | +0.99% |

| Gold Futures | 1,470.30 | -0.20 | -0.01% |

| XAU | 95.52 | +1.86 | +1.99% |

| S&P/TSX VENTURE COMP IDX | 533.33 | +3.31 | +0.62% |

| S&P/TSX Global Gold Index | 243.84 | +2.89 | +1.20% |

| Natural Gas Futures | 2.32 | -0.35 | -13.10% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,087.96 | +7.69 | +0.37% |

| 10-Yr Treasury Bond | 1.77 | +0.00 | +0.06% |

| Gold Futures | 1,470.30 | -33.50 | -2.23% |

| S&P Basic Materials | 375.24 | +6.46 | +1.75% |

| S&P 500 | 3,140.98 | +94.21 | +3.09% |

| DJIA | 28,051.41 | +864.72 | +3.18% |

| Nasdaq | 8,665.47 | +361.49 | +4.35% |

| Oil Futures | 55.16 | +0.10 | +0.18% |

| Hang Seng Composite Index | 3,579.25 | -26.68 | -0.74% |

| S&P/TSX Global Gold Index | 243.84 | +0.28 | +0.11% |

| XAU | 95.52 | +2.26 | +2.42% |

| Russell 2000 | 1,624.50 | +51.66 | +3.28% |

| S&P Energy | 431.37 | +2.69 | +0.63% |

| S&P/TSX VENTURE COMP IDX | 533.33 | -4.92 | -0.91% |

| Natural Gas Futures | 2.32 | -0.38 | -13.94% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 95.52 | -2.95 | -3.00% |

| S&P/TSX Global Gold Index | 243.84 | -18.14 | -6.92% |

| Gold Futures | 1,470.30 | -72.70 | -4.71% |

| DJIA | 28,051.41 | +1,689.16 | +6.41% |

| S&P 500 | 3,140.98 | +216.40 | +7.40% |

| Nasdaq | 8,665.47 | +692.08 | +8.68% |

| Korean KOSPI Index | 2,087.96 | +123.31 | +6.28% |

| Natural Gas Futures | 2.32 | +0.02 | +0.87% |

| S&P Basic Materials | 375.24 | +23.32 | +6.63% |

| Russell 2000 | 1,624.50 | +127.78 | +8.54% |

| Oil Futures | 55.16 | -1.55 | -2.73% |

| Hang Seng Composite Index | 3,579.25 | +125.35 | +3.63% |

| S&P/TSX VENTURE COMP IDX | 533.33 | -47.82 | -8.23% |

| S&P Energy | 431.37 | +9.63 | +2.28% |

| 10-Yr Treasury Bond | 1.77 | +0.28 | +18.52% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Geely Automotive Holdings Ltd.

BHP Group Ltd.

Eni SpA

Valero Energy

Phillips 66

Fortescue Metals Group Ltd.

Banca Transilvania SA

MOL Hungarian Oil & Gas PLC

Kirkland Lake Gold Ltd.

Detour Gold Corp.

Newmont Goldcorp Corp.

AngloGold Ashanti Ltd.

Harmony Gold Mining Co Ltd.

Impala Platinum Holdings

North American Palladium

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Taiwan Weighted Index contains all Taiwan Stock Exchange issues (560 common stocks). It is a market-capitalization weighted index. NIKKEI 225 Index is a price-weighted index of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The S&P GSCI Total Return Index in USD is widely recognized as the leading measure of general commodity price movements and inflation in the world economy. Index is calculated primarily on a world production weighted basis, comprised of the principal physical commodities futures contracts. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Free Cash Flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base.