Still Plenty of Gas in the Base Metal Rally Tank

Date Posted: December 11, 2020

Read time: 47 min

At the very heart of this rally is rapidly strengthening factory activity around the globe. The big standout is China, the only major economy to see a robust recovery following the pullback that was triggered by the coronavirus pandemic.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

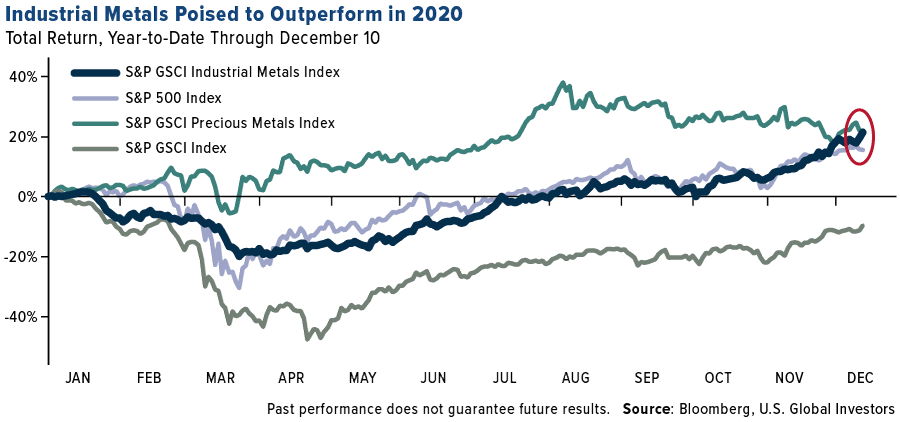

Industrial metals are well on their way to being among the top performers of 2020, supported by red hot demand from China and global supply concerns.

As of today, the MSCI Industrial Metals Index—which tracks the price of copper, nickel, aluminum and more—was up 21.4% year-to-date, just below the index of precious metals, up 21.9%. The broader S&P GSCI, which measures metals as well as agricultural and energy-related commodities, was underwater by nearly 10%.

As I discussed last week, copper prices have been on a tear this year thanks not only to the economic strength of China, the metal’s biggest consumer, but also because of its essential role in nascent technologies such as electric vehicles (EVs) and renewable green energy.

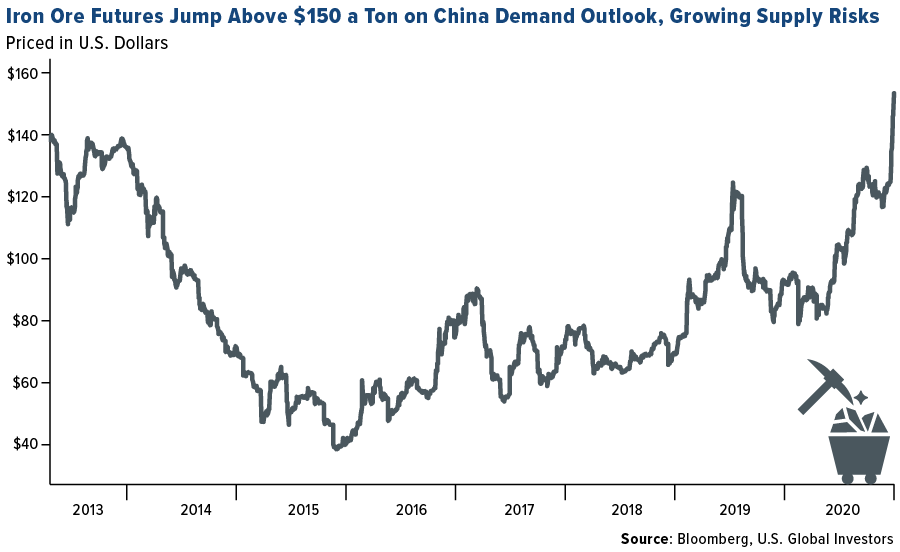

The very hottest major commodity, however, has been iron ore. Used to make steel, the metal has increased nearly 70% in 2020, with iron futures trading on the Singapore Exchange topping $155 per metric ton today for the first time since the contract came online in 2013.

At the very heart of this rally is rapidly strengthening factory activity around the globe. In November, a number of countries’ manufacturing sectors were in expansion mode, according to the monthly purchasing manager’s index (PMI), which is a leading indicator for demand.

But the big standout is China, the only major economy to see a robust recovery following the pullback that was triggered by the coronavirus pandemic.

The U.S., by comparison, is rebounding nicely, but it still has a long way to go before it reaches pre-pandemic levels. As of November, the number of jobs in the country was still below the February peak by nearly 10 million.

Plenty of Gas in the Tank

I believe the rally is only getting started, and we could see ever higher asset prices in 2021, for a couple of significant reasons.

Number one, President-elect Joe Biden plans to make infrastructure one of his top priorities soon after taking office next month. Proposals have the U.S. spending as much as $2 trillion not only to improve roads, bridges and seaports but also beef up the EV sector, add charging stations, convert school buses to zero emissions and more.

Biden’s plans could attract private investment in infrastructure, including from pension and insurance investment funds, according to Reuters. This, in turn, could prop up the base metals market.

The second big reason has to do with inflation driven by additional stimulus packages and money-printing. This week, legendary Bridgewater Associates money manager Ray Dalio held an “Ask Me Anything” event on Reddit, during which he said that the “flood of money and credit” was unlikely to recede next year. As such, “assets will not decline when measured in the depreciating value of money,” the billionaire investor suggested.

All that money will need to go somewhere, in other words, and that includes base metals and other commodities.

Congress is currently considering a $908 billion stimulus bill that’s supported by the White House. According to Barron’s, the International Monetary Fund (IMF) chief economist Gita Gopinath is urging Congress to pass the relief package even at the risk of heating up inflation, which would be supportive of commodities.

Remember, the Federal Reserve seems no longer interested in containing inflation. In August, Fed Chair Jerome Powell unveiled a new policy approach that would allow inflation to average 2% over time, meaning price spikes month-to-month would be tolerated.

Emerging Markets: “The Most Important Chart” as We Head Into 2021

Besides base metals, I’m also bullish on emerging markets. Below is a chart that CLSA calls “the most important chart for global investors to pay attention to as we go into 2021.”

In a report dated December 10, analysts at the Hong Kong-based financial firm write that they see emerging markets (EMs) offering the “greatest opportunity” next year. If you take a look at the chart, you can see that the EM universe, as measured by the MSCI Emerging Markets Index (MXEF), is currently testing resistance that goes back to late 2007.

If a breakout occurs, CLSA says, it would be “similar to the recognition phase in 2004 following the 1994 – 2004 secular bear market pattern.” To give you some idea of the returns EM investors may have seen at the time, the MXEF increased over 200% in the four-year period ended December 31, 2007.

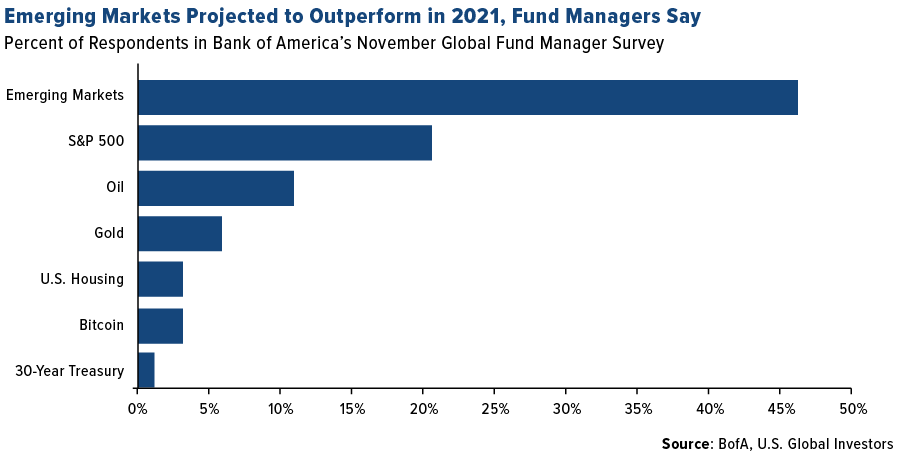

Looking ahead to 2021, I agree with CLSA and others in believing EMs look well-positioned to outperform, particularly now that a few different COVID-19 vaccine candidates are becoming available. In November, close to half of fund managers participating in a Bank of America survey said they believe emerging markets are poised to outperform next year, ahead of the S&P 500, oil and gold.

Meanwhile, JPMorgan points out that EMs are currently under-owned on a relative basis, and that after being largely ignored by investors this year, they could rally as much as 20% in 2021.

Attractive Dividend Yields

The EM investment case is strengthening even more as the U.S. has joined Europe and Japan in offering near-zero or even negative real yields. More than 75% of all debt issued by governments in developed markets (DMs) now trades at a negative real yield, according to JPMorgan.

This phenomenon isn’t reserved just for government debt, though. For the first time ever, investment-grade corporate debt in the U.S. trades with an effective real yield of 0%, the Wall Street Journal reports.

This is forcing yield-starved investors to seek alternatives.

EMs could be such an alternative. Some of the most attractive dividend yields are offered by stocks listed in emerging economies, particularly those in Central and Eastern Europe (CEE). For the year so far, dividend yields for Russian stocks, as measured by the MOEX Russia Index, have averaged 6.5%. That’s nearly 3.5 times greater than the average yield offered by U.S. stocks over the same period. At only 1.9%, the yield for the S&P 500 was only a few basis points above inflation.

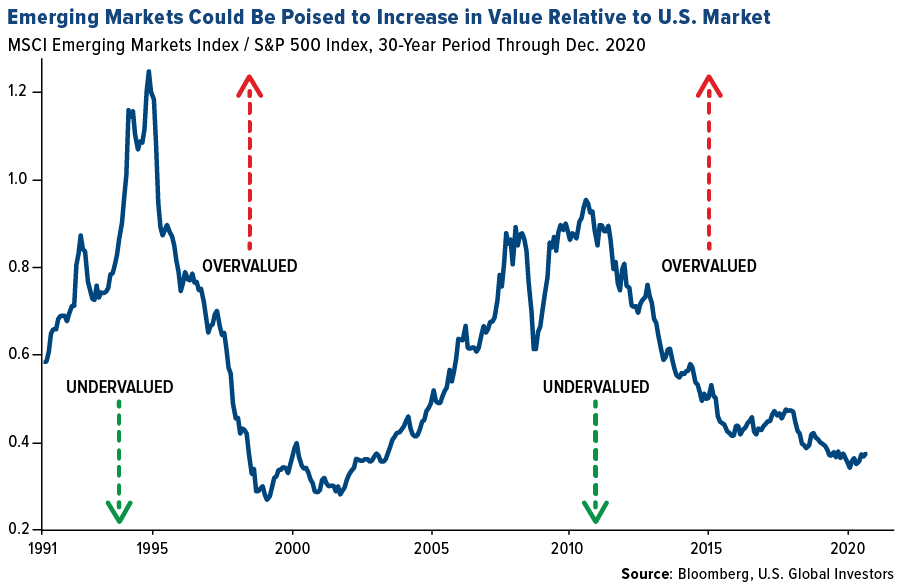

Undervalued Compared to U.S. Market

Compared to the U.S. market, EMs also appear to be undervalued, making now an exciting entry point. The chart below shows you the ratio between the MSCI Emerging Markets Index and S&P 500. As you can see, EM stocks are more undervalued on a relative basis now than at any other time since the early 2000s.

HIVE a Crypto Proxy

Many of you listened in to the recent HIVE Blockchain Technologies webcast, where we reported record revenue and cash flow for the second quarter of fiscal 2021. I mentioned that investors are trading HIVE as a proxy for the cryptocurrencies it mines, primarily Ethereum and Bitcoin.

This week, the popular Motley Fool investment advice website recommended HIVE for that very reason.

“You can directly purchase and hold Bitcoin in your portfolio. But for most investors, this may be too technical or too risky,” the site writes. Instead, it says, you could bet on HIVE, the first publicly traded crypto-mining firm.

HIVE “is a convenient proxy for cryptocurrency exposure,” Motley Fool adds.

Shares of the company are up close to 1,270% for the year.

Looking for tips on buying airline stocks? Watch my most recent educational video by clicking here! Be sure to like and subscribe.

Gold Market

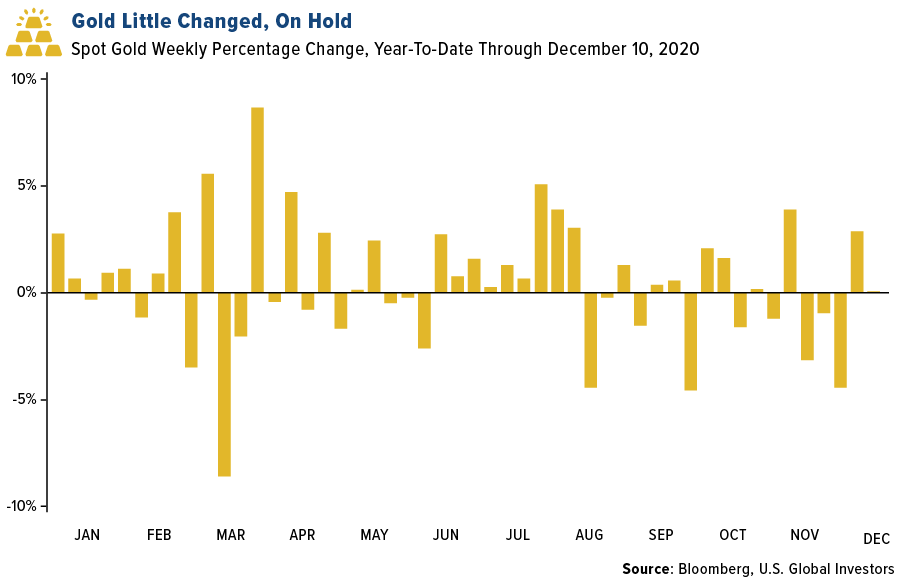

This week spot gold closed at $1,862.73, up $23.87 per ounce, or 1.30 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher/lower by 2.89 percent. The S&P/TSX Venture Index came in up 2.03 percent. The U.S. Trade-Weighted Dollar rose 0.10 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-8 | Germany ZEW Survey Expectations | 46.0 | 55.0 | 39.0 |

| Dec-8 | Germany ZEW Survey Current Situation | -66.0 | -66.5 | -64.0 |

| Dec-10 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Dec-10 | Initial Jobless Claims | 725k | 853k | 716k |

| Dec-10 | CPI YoY | 1.1% | 1.2% | 1.2% |

| Dec-11 | Germany CPI YoY | — | -0.3% | -0.3% |

| Dec-11 | PPI Final Demand YoY | 0.7% | 0.8% | 0.5% |

| Dec-14 | China Retail Sales YoY | 5.0% | — | 4.3% |

| Dec-16 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Dec-17 | Eurozone CPI Core YoY | 0.2% | — | 0.2% |

| Dec-17 | Housing Starts | 1530k | — | 1530k |

| Dec-17 | Initial Jobless Claims | 780k | — | 853k |

Strengths

- The best performing precious metal for the week was spot gold, up 1.30%. The State Street SPDR Gold MiniShares fund added a net $163 million on December 7, bringing total assets up by 4.7% to 3.62 billion. Bloomberg notes the fund has attracted net inflows of $2.11 billion in the past 12 months.

- Zambia’s central bank signed gold purchase deals with a local unit of First Quantum Minerals, which produces gold as a byproduct at its copper mine in the country. The bank also signed a deal with a state-owned mining investment company that buys gold from small-scale producers, reports Bloomberg. The southern African nation plans to hold gold for the first time since 1995 to bolster foreign exchange reserves after defaulting earlier this year.

- Wheaton Precious Metals announced it will pay Capstone Mining $150 million for 50% of its silver production up to 10 million ounces. The royalty and streaming company will use its $2 billion revolving credit facility to fund the transaction, reports Kitco News. Wheaton is also in talks regarding a potential gold stream from Capstone. In its five-year outlook starting in 2021, the company said attributable silver produce is forecast to average 820,000 ounces per year.

Weaknesses

- The worst performing precious metal for the week was platinum, down 3.38% after a stellar 9.59% jump the previous week. Anglo American Platinum also announced its production level would return back to normal levels in 2021 following repairs at their refinery. Gold dropped from a two-week high on Wednesday as investors assessed renewed concerns over the progress of stimulus negotiations among U.S. lawmakers, reports Bloomberg. Spot gold fell to $1,840, while silver fell 2% and platinum and palladium also fell.

- ETFs backed by gold cut 45,912 troy ounces from holdings on December 7, marking the 11th straight day of declines, and bringing 2020 net purchases to 23.8 million ounces. According to Bloomberg data, total gold held by ETFs has still risen 29% so far this year to 106.7 million ounces.

- Morgan Stanley said in a note this week that it expects gold and other precious metals to come under pressure in 2021 as markets normalize and the yield curve steepens. The eventual tapering of U.S. monetary stimulus could weigh on gold and analysts see it trading in the $1,800s range for much of the year before moving lower in 2022.

Opportunities

- HSBC Securities says there’s still support from accommodative monetary and fiscal policies, as well as geopolitical risks, for gold’s rally next year. “The financial, economic, and health uncertainties generated by the Covid-19 pandemic and its aftermath are still likely to continue to support gold in 2021 and even 2022, albeit at a reduced level,” James Steel, chief precious metals analyst, said in a note this week.

- Although commodities could enter a “period of pause” this winter, Citigroup says the outlook across the complex looks robust in 2021 due to tightening market conditions across industrial metals. The bank predicts a gold rebound next year and says silver, palladium and platinum may end the year higher than current prices. Citigroup’s three-month gold price target is $1,850 an ounce and expects strong buying support on dips below $1,800.

- Morgan Stanley is bearish on gold in 2021, but it is bullish on silver. The bank expects silver to continue to outperform gold in the coming year due to strong growth in electronics and solar power.

Threats

- JPMorgan says the rise of cryptocurrencies into mainstream finance is coming at the expense of gold. Eddie Spence of Bloomberg writes that money has poured into Bitcoin funds and out of gold funds since October and believes the trend will only continue in the long run as more institutional investors take positions in cryptocurrencies. The Grayscale Bitcoin Trust has seen inflows of almost $2 billion since October, compared with outflows of $7 billion for exchange-traded funds backed by gold, according to JPMorgan.

- South Africa’s mining production in October fell 6.3% from a year ago and comes after a 3.4% drop in September. The median estimate in a Bloomberg survey was for a 4.7% contraction. Gold production dropped 3.9% and 1.1% in September. Production in what was once the world’s top producer has declined steadily for years. Platinum-group metals production did rise 2.4% in October after a 0.4% decline in September.

- Bloomberg reports that foreigners are using a gold ETF to pull cash out of Nigeria amid a dollar shortage. Portfolio managers buy the Newgold Issuer Ltd. ETF listed in Lagos, then transfer holdings to the fund’s primary listing in South Africa to sell for rands. According to Jolomi Odongharo, head of research at Cordros Capital, fear of devaluation and the opportunity cost of keeping money in Nigeria means investors are willing to take the loss when selling out.

Index Summary

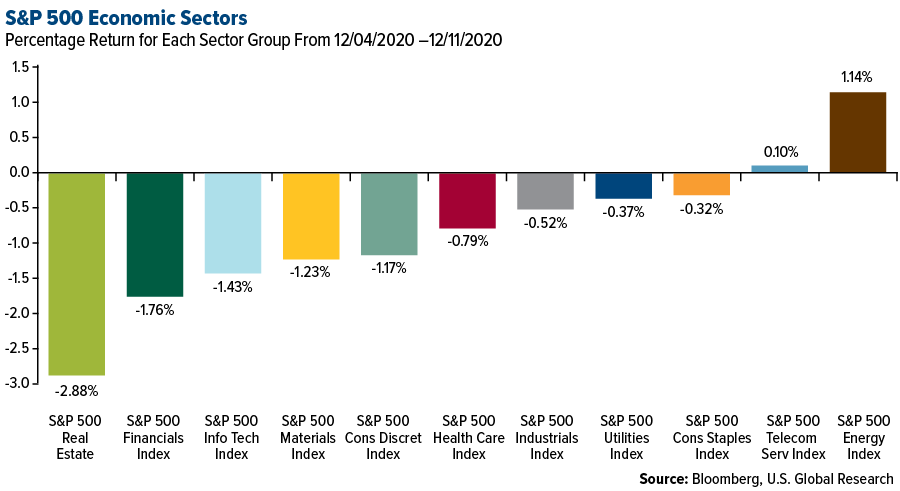

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.57%. The S&P 500 Stock Index fell 1.01%, while the Nasdaq Composite fell 0.69%. The Russell 2000 small capitalization index gained 1.01% this week.

- The Hang Seng Composite lost 1.23% this week; while Taiwan was up 0.91% and the KOSPI rose 1.41%.

- The 10-year Treasury bond yield fell 7 basis points to 0.891%.

Domestic Economy and Equities

Strengths

- The University of Michigan’s preliminary sentiment index rose 4.5 points to 81.4, from a final November reading of 76.9, according to figures Friday that topped all estimates in Bloomberg’s survey of economists. The median projection was 76.

- The Senate passed a one-week government spending bill, giving President Donald Trump just enough time to sign it and avert a government shutdown.

- Walt Disney was the best performing S&P 500 stock for the week, increasing 14.00%. Shares hit an all-time high after it issued a bold forecast for its new streaming services, projecting a Netflix-like trajectory that could bring the company as many as 350 million subscribers worldwide by 2024 thanks to an onslaught of programming from Marvel, Star Wards and Pixar.

Weaknesses

- Initial jobless claims soared to 853,000 last week, as the surge in coronavirus cases pushed more businesses to implement stricter measures on social distancing, forcing more people out of their job. Economists had predicted the latest weekly jobless claims total would be around 730,000, higher than the prior week’s newly revised tally of 716,000.

- Small-business owner confidence in the U.S. economy decreased in November compared with the previous month. The NFIB Small Business Optimism Index stood at 101.4 in November, 2.6 percentage points less than October’s level. The reading roughly matches expectations from economists polled by The Wall Street Journal, who expected the index to come in at 102.0.

- Carnival was the worst performing S&P 500 stock for the week, falling 9.08%, after announcing it is postponing cruises, again. Dates vary, but cruises are being pushed back to at least late May and early June. This is in addition to the cruises that are already postponed into September.

Opportunities

- Positive feedback loop set to drive stocks higher in 2021. JPMorgan’s Kolanovic said the VIX index will likely average around the 17 level in 2021, which is well below its average of 28 in 2020.

- JPMorgan sees $1 trillion in stock market inflows in 2021. Investors are looking at a pretty positive environment especially for the first half of next year, top strategist Dubravko Lakos-Bujas said.

- State Street Corp. is exploring options for its asset management business, including a merger with a competitor, as it seeks to gain scale, people familiar with the matter said. The Boston-based firm has been informally working with an adviser to review strategic alternatives for the unit, known as State Street Global Advisors, according to the people. It has evaluated potential combinations with the asset management operations of rivals including Invesco Ltd. and UBS Group AG.

Threats

- Facebook faces a breakup after being hit with double lawsuits. Both lawsuits, from the FTC and 46 states, revolve around the company’s acquisitions of Instagram in 2012 and WhatsApp in 2014.

- GameStop Corp. plunged as much as 22%, the most since September 2019, after the video-game retailer missed third-quarter sales estimates and announced plans to sell up to $100 million in stock.

- Conn’s slid nearly 20% after the rent-to-own retailer posted disappointing results in its third-quarter earnings report as customer traffic continued to decline during the pandemic.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was once again lumber, up 16.42%, led by robust housing demand and low mortgage rates. Iron ore is among the top performers for the year due to surging demand in China. The metal rose above $150 a ton this week and futures in Singapore have surged 70% in 2020.

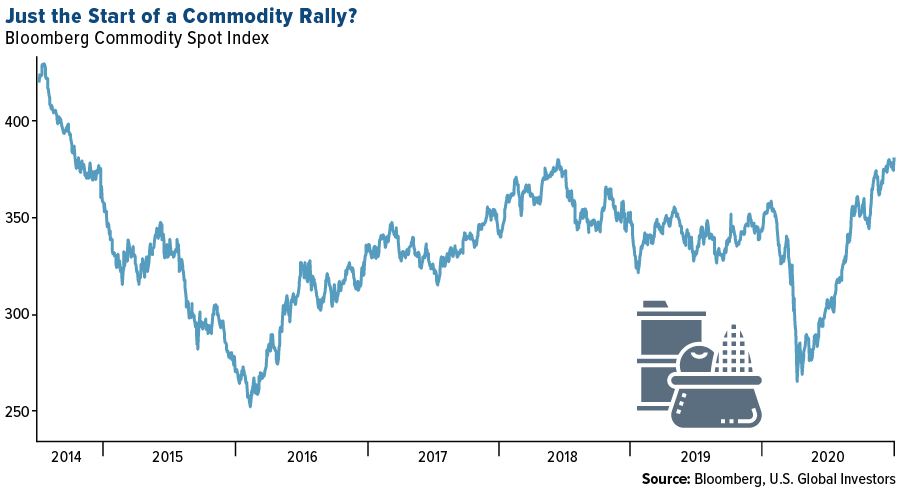

- Commodities are staging a comeback as the global economy recovers from its steep downturn. The Bloomberg Commodity Spot Index rose 1.3% on Thursday to the highest level since 2014. Bloomberg notes that copper is surging, oil is recovering and strong Chinese demand is boosting crop prices.

- Trading group Trafigura had a record year for trading profits, seeing a $1 billion boost to its total equity. CEO Jeremy Weir says the company took more than $1.5 billion in write downs and impairments for under-performing industrial assets earlier this year, but overall “it was a stunning year.” Bloomberg notes the surge in gross profit is a sign that raw materials traders took advantage of wild price swings and demand imbalances caused by the virus.

Weaknesses

- The worst performing commodity for the week was crude palm oil, down 0.79 percent on little news. The “widowmaker” natural gas trade collapsed on forecasts for a mild winter. Bloomberg reports the spread between March and April futures – a bet on how tight supplies of natural gas will be at the end of North American winter – fell below zero on Tuesday. This is the first time the trade collapsed so early in the heating season since 2015. Gas futures are down nearly 30% since the end of October.

- Morgan Stanley said in a note this week that it expects gold and other precious metals to come under pressure in 2021 as markets normalize and the yield curve steepens. The eventual tapering of U.S. monetary stimulus could weigh on gold and analysts see it trading in the $1,800s range for much of the year before moving lower in 2022.

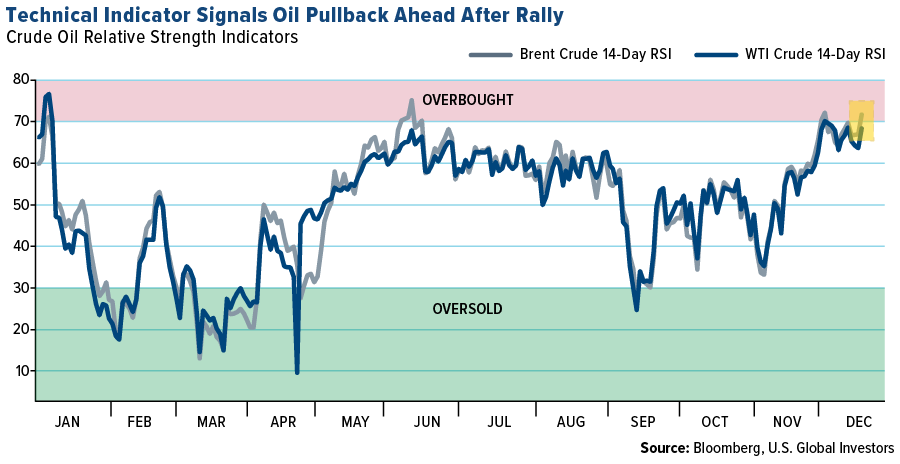

- Oil retreated at the end of the week after topping $50 a barrel on Thursday. Although the fuel looks overbought, it is a huge positive to rise above the key $50 level amid vaccine approval that could boost demand. A growing number of virus cases remains a long-term threat for demand.

Opportunities

- Copper miners are booming thanks to seven-year high copper prices, falling currencies in producing nations and low oil costs. This combination of factors is helping miners keep costs down. Glencore’s copper department could be set to make more than $5,000 on each of 1.1 million tons it hopes to produce in 2021, reports Bloomberg. CEO Ivan Glasenberg said “it’s looking very good for copper going forward.”

- The rally in food prices is also boosting demand for fertilizer. Just a few companies produce potash, the potassium-rich fertilizer mined underground, and estimates are for record demand in 2021, according to Bloomberg Green Markets. Nutrien, the world’s top producer, said it expects 2020 to be its best year ever for sales. 2020 U.S. farm income is on track to increase $43 above 2019. Seth Goldstein, senior equity analyst at Morningstar, forecasts potash prices pushing the mid-$200s a ton and may continue higher to $280 by 2023.

- The BNP Paribas Energy Transition fund has climbed 131% so far this year, beating most peers in its ESG category, and is expanding investments in Asian renewable stocks. The fund’s Asia allocation has grown to 18% from 11% and is exploring additional investments in China, Hong Kong, India and South Korea as the region focuses on green initiatives. The fund has $1.8 billion in investments.

Threats

- Crude oil moved into overbought territory after Brent rose above $50 a barrel on Thursday. The relative strength index (RSI) jumped above 70 – a level considered overbought. Although prices are at their highest since March, the fuel could be headed for a correction after moving too far, too fast.

- Wind energy has exploded in Norway in recent years but faces growing backlash from voters. A November survey found that only 36% of the country is favorable about onshore wind as an energy source, down from 84% in 2011. Oil has increased in popularity – up to 29% from 16% five years ago. Bloomberg notes that industry consultant StormGeo Nena Analysis said it is unlikely any more wind farms will be built on land in the decade to 2034.

- Russia appears to be preparing for the possibility of lower budget revenues in the case that global oil demand declines sooner than expected, reports Bloomberg. Russia’s Deputy Finance Minister said in an interview “the peak of consumption may have already passed” and “the risk is rising in the longer term.” The world’s top energy exporter generates a significant percentage of its revenues from oil. Russia has also been slow to transition to renewables, with less than 1% of power coming from renewables.

Airline Sector

Strengths

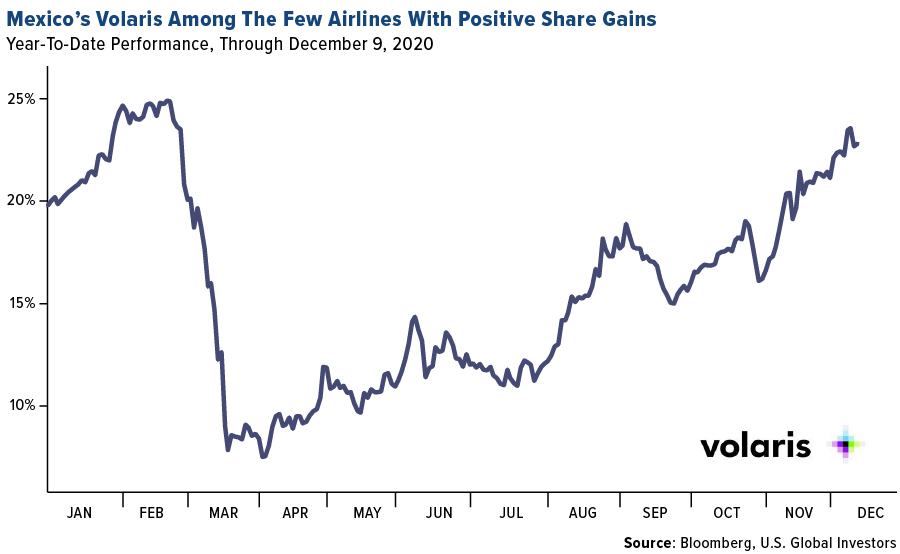

- The best performing airline for the week was Hainan Meilan International Airport, up 6.32%. Mexico’s biggest airline, Volaris, is restoring seat capacity to 100% of last year’s level and is targeting profitability in the second quarter of next year. Bloomberg reports the carrier plans to use proceeds from a $173 million stock sale to grab market share from competitors in at least a dozen Mexican destinations. Volaris cut fares by 30% earlier this year to entice travelers and is one of the few carriers to have positive stock performance in 2020.

- Brazil’s Gol Linhas Aereas Inteligentes said it will be the first carrier to resume regular flights with the Boeing 737 Max by beginning domestic routes from Sao Paulo this week. The airline said it has trained 140 of its pilots in the U.S. on the new Max material. The Max will return to service in the U.S. when American Airlines uses it between Miami and New York later this month.

- American Airlines announced it will expand its pre-flight COVID-19 testing program to boost demand. Passengers can take at-home test kits and with a negative result they can avoid or shorten quarantines. The carrier is expanding domestic offerings after offering similar testing programs for some international routes.

Weaknesses

- The worst performing airline for the week was EasyJet, down 11.91%.

- Southwest CEO Gary Kelly said in an interview that “January and February are bound to be really rough months – wintertime, high caseloads – and they are seasonally soft anyway.” The executive expects depressed travel amid surging U.S. virus cases, on top of the seasonally weak start to the year, reports Bloomberg. Kelly added “we can get started on the vaccine progress and get started on recovery, but we’ve got a long way to go.”

- According to the Transition Pathway Initiative, only 18% of airline, car and shipping companies have set carbon-reduction plans in line with pledges in the Paris Climate Target to keel global warming to 2 degrees Celsius or below by 2050. IAG, Delta and Southwest were deemed not to be aligned with the accord, which was agreed to five years ago. Bloomberg Green notes the report called out airlines as clear laggards largely because of their reliance on offsets to meet emissions targets rather than gross reductions.

Opportunities

- Once India’s largest airline by market value, now bankrupt Jet Airways India plans to restart operations by summer of 2021. A consortium of investors has created a plan to revive the airline, including a dedicated freighter service and hubs in small Indian cities. Jet Airways will continue to operate all its historic domestic slots and restart international operations after approval from regulators and a bankruptcy tribunal, reports Bloomberg.

- As international travel remains subdued, U.S. airlines are waiving change fees in hopes of luring more passengers. United dropped change fees on all tickets bought in the U.S. for international travel and Delta eliminated them on flights from North America, reports Bloomberg. According to the U.S. Transportation Department, 10 American carriers collected more than $2.84 billion in ticket cancellation and change fees in 2019.

- AirAsia Group CEO Tony Fernandes said in a Bloomberg TV interview this week the carrier is expanding its base in Southeast Asia and is in talks about starting three new airlines in the region. Fernandes is “quietly optimistic for 2021” and expects air travel to return to pre-virus levels in the next six to 12 months.

Threats

- A coalition of 17 airline industry employee groups wrote a letter to the Centers for Disease Control and Prevention (CDC) asking that airline employees move near the front of the line for receiving vaccines to ensure smooth shipments by air cargo. Joseph DePete, president of the Air Line Pilots Association, said cargo-airline pilots have experienced “an alarming increase in Covid-19 exposure and infections.” Airlines will be key in distributing a vaccine globally and must ensure pilots are safe from exposure and any potential side effects from taking the vaccine.

- Europe’s airlines face a growing threat from trains after governments agreed to expand night-train servings linking major cities. Bloomberg Green reports that ministers from France, Germany, Austria and Switzerland announced a plan to increase rail traffic between cities including Paris, Berlin, Vienna and Milan to curb rising carbon emissions. The Trans-Europe Express 2.0 program launches in late 2021 and will allow travel between multiple national borders without changing trains.

- South Africa Airways (SAA) is facing a new battle with unions over salaries – the latest challenge in getting the bankrupt carrier back in the skies. The carrier is offering employees three months of back pay, but it is unclear is the union will reject it. Bloomberg notes around 1.2 billion rand is needed to pay back salaries and the government has struggled to come up with the cash. SAA has been grounded since March due to the virus and entered bankruptcy protection a year ago.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 4.8%. The best performing country in Asia this week was Vietnam, gaining 2.4%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 1.5%. The Thailand baht was the best performing currency in Asia this week, gaining 35 basis points.

- China continues to release strong economic data. Exports hit their highest monthly total ever, increasing by 21.1% in November from a year ago. At the same time, imports declined, putting China’s overall trade surplus at $75 billion last month, up from October’s $58 billion.

Weaknesses

- The worst performing country in emerging Europe for the week was the Czech Republic, losing 40 basis points. The worst performing country in Asia this week was China, losing 2.8%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 80 basis points. The South Korean won was the worst performing currency in Asia this week, losing 70 basis points.

- Europe struggles to bring the number of coronavirus cases down and is trying not to impose more restrictive measures before Christmas, limiting business activities and social gatherings. Virus cases among the elderly are again on the rise across Europe, with rising death tolls in nursing homes.

Opportunities

- Germany, Poland, and Hungary agreed on a compromise to unblock the EU’s budget and stimulus plan. Poland and Hungary have threatened to veto the budget and recovery plan over the EU’s proposal to distribute funds accordingly to the country’s rule-of-law. The revised agreement says that the rule of law mechanism would only apply to new outlays from the EU.

- CLSA is anticipating a conclusive breakout from the 2007-2020 secular emerging market bear market pattern and is recommending investors overweight emerging market assets versus developed markets in 2021 and beyond. Further suggestions include increasing exposure to large-cap stocks to benefit from the initial breakout and momentum stage as more money will flow into that space.

- Expectations of economic growth improved in Europe, followed by optimism over a COVID-19 vaccine becoming available sooner rather than later. China and Russia have been distributing COVID-19 vaccines already and this week on Tuesday the United Kingdom became the first Western country vaccinating people against the coronavirus.

Threats

- The U.S. Administration imposed travel restrictions on 14 Chinese individuals for curtailing a pro-democracy move in Hong Kong. In retaliation, China imposed restrictions on U.S. officials. Names were not announced yet, but China said it will apply to government representatives and their immediate families as well as non-government organizations.

- The lira may continue its long-term downtrend despite the current government’s attempts to strengthen its currency. The U.S. Administration may announce sanctions on Turkey for buying military equipment from a non-NATO member, Russia. Also, Europe is discussing sanctions on the country for its maritime activities in the eastern Mediterranean Sea.

- Once again, Brexit talks have been extended. The United Kingdom and the eurozone cannot come to a deal and time is running out. The UK will exit the eurozone on December 31 with or without a deal. Businesses have been moving assets out of the UK for years now, and this process will intensify if it leaves the EU without a deal.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended December 11 was ALL BEST ICO, up over 72,000%

- On December 7, MicroStrategy – the world’s largest publicly traded business intelligence firm – revealed plans to invest proceeds from a $400 million securities offering into bitcoin, writes CoinTelegraph. At the current price, the $400 million would increase the company’s holdings by 20,833 – bringing its total crypto stash to almost 62,000 BTC.

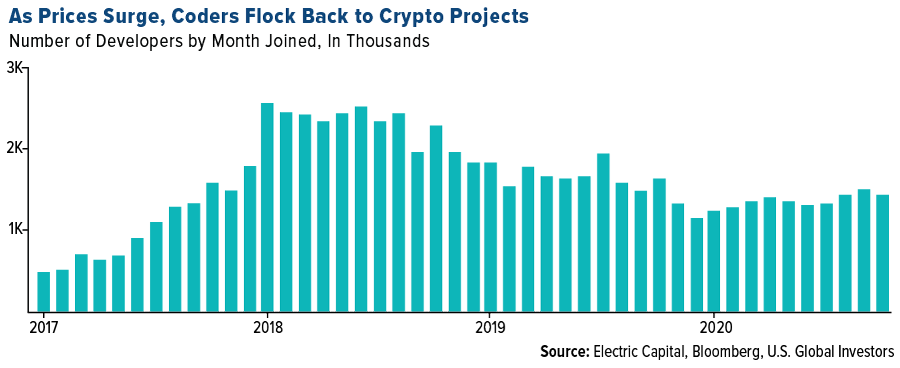

- With bitcoin on a tear and so many DeFi projects taking off, the number of new monthly crypto developers rose 15%, writes Bloomberg, and that was in the first 10 months of the year. As explained in the article, while crypto price moves are often fueled by pure speculation, developer activity is one of the best barometers of a project’s promise and health.

click to enlarge

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended December 11 was Basin Cash, down 96%.

- As mentioned in the “strengths” section, MicroStrategy announced it was buying more bitcoin. Unfortunately, Citibank didn’t like the news, reports CoinTelegraph. The bank downgraded the business intelligence firm to “sell” from “neutral” on Tuesday due to its “disproportionate” bitcoin focus.

- Mid-week, bitcoin fell below $18,000, reports CoinTelegraph, in the latest continuation of its bearish comedown from all-time highs. CoinTelegraph Markets analyst Michael van de Poppe shared the following assessment on his Twitter page: “Testing levels multiple times doesn’t make the level stronger. Downtrend likely to continue? I think so, unless $18,500 – 18,700 is reclaimed, I think we’ll continue correcting.”

Opportunities

- According to people familiar with the matter, BBVA – the second-largest bank in Spain – is poised to enter the cryptocurrency trading and custody space, writes CoinDesk. One source with knowledge of the plan told CoinDesk that the bank is “launching its Europe-wide crypto initiative from Switzerland.”

- On Wednesday, Bitwise Asset Management announced that its 10 Crypto Index Fund is now available to U.S. investors as a public-traded cryptocurrency index fund, reports CoinDesk. In a news release, the company explained that after a Form 211 for quotation of the fund’s shares was reviewed by FINRA, the fund was enabled to be listed on the over-the-counter markets and trades under the ticker symbol “BITW.”

- Rafael Schultze-Kraft, chief technical officer of Glassnode, says a slew of bitcoin market indicators are “insanely bullish,” and believes that prices could increase by more than 10 times, writes CoinTelegraph. Each of his predictions and estimates show the digital currency breaking into six figures, with all but one suggesting bitcoin will exceed $200,000.

Threats

- Mexican authorities have reported an increase in the use of crypto assets to launder funds by criminal syndicates in Latin America, reports CoinTelegraph. The head of the major Mexican financial intelligence unit is now complaining that local law enforcement has only a quarter of the staff it needs to respond to crypto laundering from cartels, the article continues.

- The SEC enforcement director since 2017, Stephanie Avakian, who led investigations during the entirety of the SEC’s initial coin offering (ICO) crackdown, plans to leave the agency this year. This is a threat to the industry because she was in charge of making sure the industry was being conducted in a professional and legal manner – she was responsible for managing crypto-related securities violations, particularly the ICO projects that attempt to raise capital without filing.

- Over the weekend, attorneys for Ethereum developer Virgil Griffith filed documents arguing that they still don’t know what exactly he is being accused of, writes CoinDesk. Last year he was accused of violating U.S. sanctions law by going to North Korea and teaching locals how to transfer funds using cryptocurrency, however, he has yet to receive an actual list of crimes he is being indicted for.

December 10, 2020Even More Tech Firms Are Leaving Silicon Valley for Texas |

December 3, 2020Copper Bull Run May Only Be Getting Started |

November 30, 2020This Stock Is Up More Than 1,000% This Year |

|||

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.89 | -0.08 | -7.95% |

| Oil Futures | 46.60 | +0.34 | +0.73% |

| Hang Seng Composite Index | 4,145.82 | -51.56 | -1.23% |

| S&P Basic Materials | 444.19 | -5.51 | -1.23% |

| Korean KOSPI Index | 2,770.06 | +38.61 | +1.41% |

| S&P Energy | 306.38 | +3.44 | +1.14% |

| Nasdaq | 12,377.87 | -86.36 | -0.69% |

| DJIA | 30,046.37 | -171.89 | -0.57% |

| Russell 2000 | 1,911.48 | +19.03 | +1.01% |

| S&P 500 | 3,661.60 | -37.52 | -1.01% |

| Gold Futures | 1,843.00 | +3.00 | +0.16% |

| XAU | 138.61 | -0.73 | -0.52% |

| S&P/TSX VENTURE COMP IDX | 778.96 | +9.85 | +1.28% |

| S&P/TSX Global Gold Index | 310.69 | -1.90 | -0.61% |

| Natural Gas Futures | 2.59 | +0.02 | +0.70% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,770.06 | +284.19 | +11.43% |

| 10-Yr Treasury Bond | 0.89 | -0.09 | -8.90% |

| Gold Futures | 1,843.00 | -25.10 | -1.34% |

| S&P Basic Materials | 444.19 | +8.52 | +1.96% |

| S&P 500 | 3,661.60 | +88.94 | +2.49% |

| DJIA | 30,046.37 | +648.74 | +2.21% |

| Nasdaq | 12,377.87 | +591.44 | +5.02% |

| Oil Futures | 46.60 | +5.15 | +12.42% |

| Hang Seng Composite Index | 4,145.82 | +74.89 | +1.84% |

| S&P/TSX Global Gold Index | 310.69 | -28.10 | -8.29% |

| XAU | 138.61 | -1.99 | -1.42% |

| Russell 2000 | 1,911.48 | +174.54 | +10.05% |

| S&P Energy | 306.38 | +52.56 | +20.71% |

| S&P/TSX VENTURE COMP IDX | 778.96 | +50.71 | +6.96% |

| Natural Gas Futures | 2.59 | -0.44 | -14.45% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 138.61 | -13.73 | -9.01% |

| S&P/TSX Global Gold Index | 310.69 | -73.84 | -19.20% |

| Gold Futures | 1,843.00 | -128.90 | -6.54% |

| DJIA | 30,046.37 | +2,511.79 | +9.12% |

| S&P 500 | 3,661.60 | +322.41 | +9.66% |

| Nasdaq | 12,377.87 | +1,458.28 | +13.35% |

| Korean KOSPI Index | 2,770.06 | +373.58 | +15.59% |

| Natural Gas Futures | 2.59 | +0.27 | +11.62% |

| S&P Basic Materials | 444.19 | +41.31 | +10.25% |

| Russell 2000 | 1,911.48 | +403.73 | +26.78% |

| Oil Futures | 46.60 | +9.30 | +24.93% |

| Hang Seng Composite Index | 4,145.82 | +392.58 | +10.46% |

| S&P/TSX VENTURE COMP IDX | 778.96 | +36.91 | +4.97% |

| S&P Energy | 306.38 | +63.42 | +26.10% |

| 10-Yr Treasury Bond | 0.89 | +0.21 | +31.42% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2020):

Gol Linhas Aereas Inteligentes

American Airlines Group Inc

Southwest Airlines Co

Delta Air Lines Inc

United Airlines Holdings Inc

Nutrien Ltd

Wheaton Precious Metals Corp

easyJet PLC

Facebook Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Commodity Spot Index measures the price movements of commodities included in the Bloomberg CI and select subindexes. It does not account for the effects of rolling futures contracts or the costs associated with holding physical commodities and is quoted in USD. The relative strength index (RSI) is a momentum indicator used in technical analysis that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The S&P GSCI Industrial Metals Index provides investors with a reliable and publicly available benchmark for investment performance in the industrial metals market. The S&P GSCI Precious Metals Index provides investors with a reliable publicly available benchmark for investment performance in the precious metals market. The S&P GSCI serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. The MSCI Emerging Markets Index is a free-float weighted equity index that captures large and mid-cap representation across Emerging Markets (EM) countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country. MOEX Russia Index is a cap-weighted composite index calculated based on prices of the most liquid Russian stocks of the largest and dynamically developing Russian issuers presented on the Moscow Exchange. The dividend yield, expressed as a percentage, is a financial ratio (dividend/price) that shows how much a company pays out in dividends each year relative to its stock price. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. The University of Michigan of Consumer Sentiment Index is comprised of measures of attitudes toward personal finances, general business conditions, and market conditions or prices. The National Federation of Independent Business (NFIB) Small Business Optimism Index is a composite of ten seasonally adjusted components. It provides an indication of the health of small businesses in the U.S., which account of roughly 50% of the nation’s private workforce.