Warren Buffett Bets Big on Airlines

Date Posted: March 6, 2020

Read time: 59 min

Ever on the hunt for a great bargain, billionaire investor Warren Buffett boosted his company's stake in Delta Air Lines once again. Berkshire Hathaway acquired some 976,000 Delta shares last week for roughly $45.3 million, according to a filing on Monday, raising its total holdings to 17.9 million shares.

U.S. Global Investors Announces Completion of Sale of Ownership Interest in Galileo

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Ever on the hunt for a great bargain, billionaire investor Warren Buffett boosted his company’s stake in Delta Air Lines once again. Berkshire Hathaway acquired some 976,000 Delta shares last week for roughly $45.3 million, according to a filing on Monday, raising its total holdings to 17.9 million shares. This was enough to bring Buffett’s ownership of the U.S. long-haul carrier up to more than 11 percent.

Once a critic of airline stocks, Buffett has become one of their greatest champions, noting the industry’s strong fundamentals and the fact that it’s protected by an economic moat.

Accumulating shares now appears to be a strategic move to capitalize on lower fuel costs—Brent crude oil is down 30 percent so far this year—as well as coronavirus-impacted travel, which has depressed airline stock prices.

Buffett isn’t alone in thinking airlines look like a steal right now. In a note to clients this week, Citigroup analyst Stephen Trent maintained his Buy ratings on Delta, United Airlines and Spirit Airlines, writing that “if coronavirus concerns fade in the coming weeks and the U.S. is able to avoid recession, this scenario could see a recovery in ex-Asia demand, which could lead airline stock prices and earnings streams to stabilize.”

What’s more, the domestic airline industry could soon receive fiscal stimulus in the wake of the COVID-19 epidemic. Speaking to various business news networks on Friday, National Economic Council director Larry Kudlow hinted that the U.S. government is considering “timely and targeted micro-measures” for certain industries, including airlines, hospitality and agricultural. It’s unclear at the moment what those measures might look like.

Kudlow ruled out a large-scale economic stimulus package similar to the one passed in response to the global financial crisis, calling the idea a “budget buster.”

Airline Stocks on Sale, Most Discounted Since 9/11

As one the most exposed industries to global travel disruptions, airlines have seen a deeper selloff than the market and now look like an attractive bargain.

So far, COVID-19 has had a far greater impact on global airline stocks than the 2002-2003 SARS epidemic did. The chart below shows the daily percent change of the NYSE Arca Global Airlines Index starting on the day of the first reported incident of either infection—November 15, 2002 in the case of SARS, December 31, 2019 in the case of COVID-19. Airline stocks found their bottom on the 77th trading day into the SARS epidemic, down approximately 25 percent. They exceeded that level in close to half the time during the COVID-19 outbreak, falling 25.72 percent on the 42nd trading day. Airlines were off about 30 percent as of Thursday’s close.

Below is the 14-day relative strength index (RSI) for the airlines index, going all the way back to 2001. It shows that airline stocks right now are the most oversold since September 2001. The RSI hit 13.9 on March 3, the lowest it’s been since September 21, 2001, just days after 9/11, when the index was at 7.7.

Obviously there are multiple factors investors should consider, including time period and asset class, but as a general rule, when the RSI falls below 30, it’s been a good buy signal, and anything below 20 has been a screaming buy. Buffett presumably knew this before the rest of us.

Is More QE on the Way?

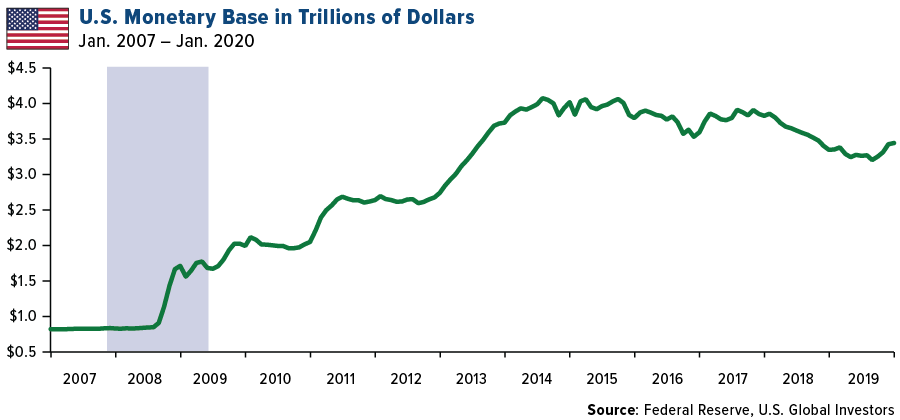

We may not get a huge spending package, but don’t rule out quantitative easing (QE). You can see the amount of money printing the Federal Reserve had to do in the days following the 2008 crisis. The U.S. monetary base, or the overall total circulation of money, exploded from just under $1 trillion pre-crisis to as much as $4 trillion at its peak in mid-2014.

The Fed is unlikely to print money to combat the economic impact of the coronavirus, according to Cornerstone Macro’s Melissa Turner, but it may have to do more QE.

“In that case,” Turner writes, “something on the order of $500 billion to $1 trillion is probably what the Fed will do.”

Earlier in the week, the Fed lowered the interest rate 50 basis points in its first emergency meeting since the crisis more than 10 years ago. The Fed has cut rates between regularly scheduled policy meetings only six times since 1998, and in each instance, it cut rates again at its next meeting—March 17, in this case.

Additional cuts could send short-term yields to 0 percent, says DoubleLine Capital CEO Jeffrey Gundlach.

“We will see short rates headed toward zero,” the billionaire said on CNBC’s “Halftime Report. “I’m in the camp that the Fed is going to cut rates again.”

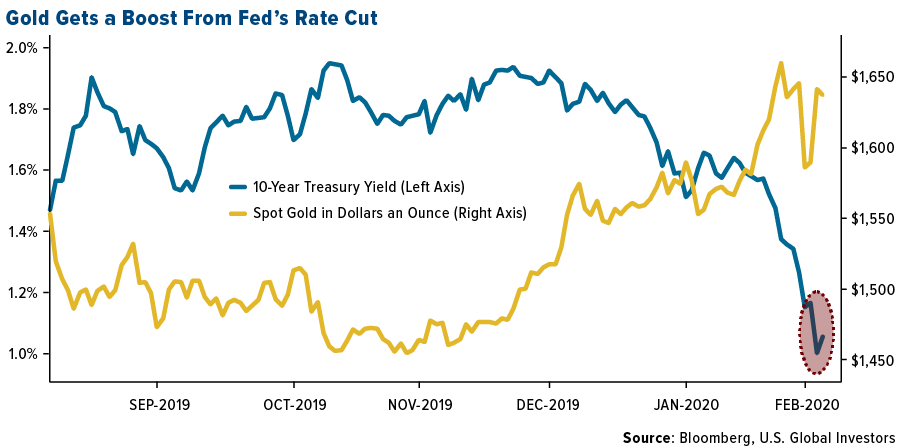

He’s not wrong. Today the nominal yield on the 10-year Treasury plunged below 0.7 percent for the first time ever as investors sought shelter from the equity selloff. This had the effect of lifting gold prices up nearly 8 percent for the week, its best weekly advance since 2008. The yellow metal’s next test is $1,700 an ounce.

JPMorgan: Buy the Dip

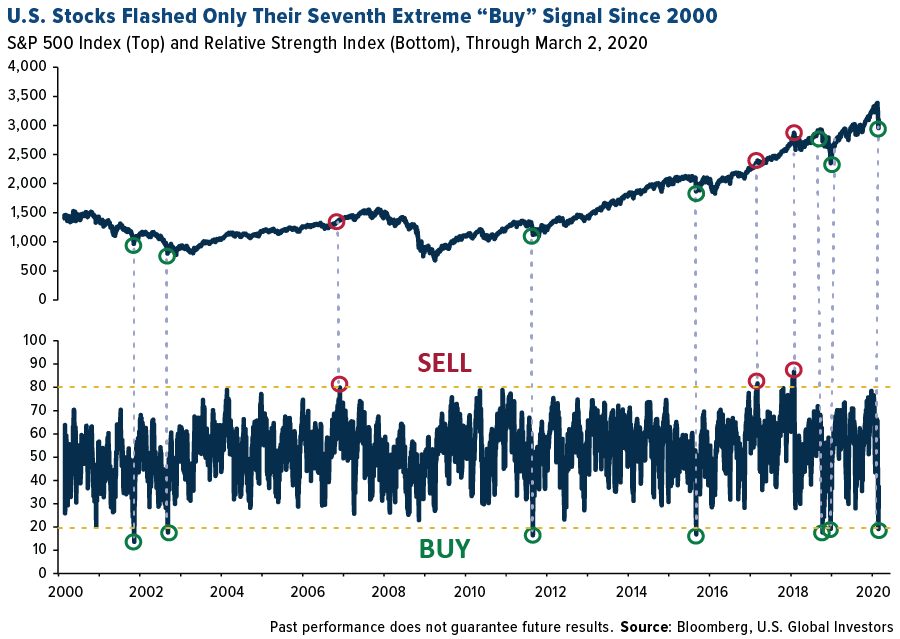

There could be other deals than airline stocks for bargain hunters. On Monday, the S&P 500 Index touched 20 on the RSI, only its seventh time to do so since the turn of this century. According to CLSA, stocks have historically been up 86 percent of the time 10 trading days following these conditions. That would put us at March 16 if we’re using March 2 as day one. We’ll see then if the probability holds.

JPMorgan strategists seconded the bullish call, advising clients this week to buy the dip.

“We expect the impact of COVID-19 to be temporary and mitigated by broad policy stimulus, even as the virus spread is proving more severe than anticipated,” wrote bank analysts in a note. They explained that they had previously been trimming risk from their portfolios over the past couple of months, but now they see “the risk-reward as increasingly skewed to the upside for risky assets and use the current pullback to add back to cyclical exposures at the margin.”

The risk may be too high for some investors, in which case I recommend gold as a diversifier. I like to advocate the 10 Percent Golden Rule, with 5 percent of your portfolio in gold bullion (coins, bars, jewelry), the other 5 percent in high-quality gold stocks, mutual funds and ETFs.

Good investing!

Think gold could hit $10,000 an ounce? Find out why it could by clicking here!

Gold Market

This week spot gold closed at $1,673.17, up $88.14 per ounce, or 5.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 11.01 percent. The S&P/TSX Venture Index came in up just 1.79 percent. The U.S. Trade-Weighted Dollar tumbled 2.16 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-1 | Caixin China PMI Mfg | 46.0 | 40.3 | 51.1 |

| Mar-2 | ISM Manufacturing | 50.5 | 50.1 | 50.9 |

| Mar-3 | Eurozone CPI Core YoY | 1.2% | 1.2% | 1.1% |

| Mar-4 | ADP Employment Change | 170k | 183k | 209k |

| Mar-5 | Initial Jobless Claims | 215k | 216k | 219k |

| Mar-5 | Durable Goods Orders | -0.2% | -0.2% | -0.2% |

| Mar-6 | Change in Nonfarm Payrolls | 175k | 273k | 273k |

| Mar-11 | CPI YoY | 2.2% | — | 2.5% |

| Mar-12 | PPI Final Demand YoY | 1.8% | — | 2.1% |

| Mar-12 | Initial Jobless Claims | 6 | — | 216k |

| Mar-12 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Mar-13 | Germany CPI YoY | 1.7% | — | 1.7% |

Strengths

- The best performing metal this week was gold, up 5.56 percent. After getting hit last Friday with a virus-driven sell-off, gold rebounded on Monday to retake its safe haven status. Gavin Wendt, senior resource analyst at MineLife Pty., told Bloomberg that “gold’s fundamentals remain overwhelmingly strong and any near-term price corrections aren’t significant in terms of the bigger picture.” The yellow metal finished the week strong, hitting a new seven-year high on Friday of as much as $1,690 an ounce intraday.

- Investors seem to be returning to gold. BullionVault’s gold index measuring the balance of buyers against sellers rose to 55.1 in February, up from 53.5 a month earlier, reports Bloomberg. Investments in commodity ETFs grew by 10 percent last week for the 11th straight week of inflows, led by precious metals ETFs.

- Gold had its biggest one-day advance in almost four years after the Federal Reserve cut interest rates by 50 basis points to help mitigate the negative economic effects of the coronavirus. The rate cut led to Treasury yields plunging, which is historically good for the price of gold. The 10-year yield fell below 0.7 percent and the yellow metal could soon test $1,700 an ounce.

Weaknesses

- The worst performing metal this week was palladium, down 1.24 percent on news of declining car sales in China. After gold’s decline last Friday, RBC Capital Markets said in a note that the event “does not spell the end of gold-positive conditions, as investors seem to have cashed out to cover losses elsewhere.” Gold was headed for a great end to this week, but fell slightly as investors are likely cashing in gains to cover losses in the stock market.

- India’s gold imports continue to fall amid record high local prices. Bloomberg reports that the country’s imports fell 44 percent from a year earlier to just 39.4 tons in February. The Perth Mint reported its gold coin and bar sales fell to 22,921 ounces last month, down from 48,299 ounces in January.

- China’s massive decline in car sales in February sent palladium down early in the week. The precious metal is used to curb emissions from cars and has rallied significantly as countries are requiring stricter emission standards. Anglo American Platinum saw its biggest plunge in a decade after the company reported an explosion at a key processing plant and cut production estimates, reports Bloomberg. The company declared force majeure and said it would be unable to process material while the repairs on the plant occur. Both platinum and palladium jumped on Friday after the news broke.

Opportunities

- Goldman Sachs remains bullish on gold. Head of global commodities research Jeffrey Currie said in a note that “gold has immunity to the virus.” Juan Carlos Artigas, director of investment research at the World Gold Council (WGC), said that “uncertainty surrounding the potential impact of COVID-19 on the global economy combined with the unscheduled 50-basis point rate cut by the U.S. Federal Reserve will likely support gold investment demand.”

- With the U.S. cutting rates, other central banks globally could soon follow. Bloomberg’s Aoyon Ashraf reminded investors that in 2008 gold fell along with equities, but once the global rate cuts began the yellow metal had a crazy bull run to $1,900 an ounce – its all-time high.

- Legendary investor Jeffrey Gundlach said Thursday in a CNBC interview that he thinks the Fed will cut rates by another 50 basis points at the next meeting in two weeks. The economic impact of the coronavirus continues to worsen, with the S&P 500 down 9 percent in the last 10 days and a growing number of companies have issued sales warnings. Gundlach noted that “Gold is the best thing to own now and is headed to new highs.”

Threats

- Treasury yields plummeted to record lows as demand for haven assets grew due to the global health emergency economic fears. Long-bond rates had their biggest intraday drop since 2009, according to Bloomberg. Tony Farren of Mischler Financial Group said “we expected the virus to have a big impact. But it has gone way beyond our wildest expectations.” A credit crisis is brewing as companies fear hurt income and the ability to repay debt. John McClain, a portfolio manager at Diamond Hill Capital Management, said “this is what the start of a recession after a long bull market feels like.”

- The coronavirus is a hotbed for lawsuits against hospitals, restaurants, day care centers and more. Many businesses could face claims that they failed to adequately protect people, according to Bloomberg. Some have already been filed, including the pilots’ union at American Airlines against the carrier to keep it from serving China.

- As new information comes out daily about the coronavirus, it can be hard to know which of it is true or not. Two of President Trump’s aids said on Friday that the outbreak had been contained, even as the number of cases rose above 200 in the U.S. and test kits remain in short supply, writes Bloomberg’s Justin Sink. Larry Kudlow said “the vast majority of Americans are not at risk for this virus.” This contrasts with the view of Marc Lipsitch, professor of epidemiology at Harvard and director of the Center for Communicable Disease Dynamics, who said that it is likely that 20 percent to 60 percent of people worldwide will eventually contract the virus. President Trump signed an $8.3 billion emergency coronavirus aid package on Friday. Who will be paying for this? Bloomberg’s Ben Steverman writes that plunging interest rates and lower stock prices make it easier for the super-wealthy to pass on billions of dollars to their descendants tax-free. One wealth advisor noted in a Bloomberg story that their clients have more money than they ever could spend and that the super wealthy could deploy sophisticated strategies to transfer the wealth to their dependents while protecting those fortunes from the IRS.

Index Summary

- The major market indices finished mostly up this week. The Dow Jones Industrial Average gained 1.79 percent. The S&P 500 Stock Index rose 0.61 percent, while the Nasdaq Composite climbed 0.10 percent. The Russell 2000 small capitalization index lost 1.84 percent this week.

- The Hang Seng Composite gained 1.00 percent this week; while Taiwan was up 0.26 percent and the KOSPI rose 2.68 percent.

- The 10-year Treasury bond yield fell 37 basis points to 0.778 percent.

Domestic Equity Market

Strengths

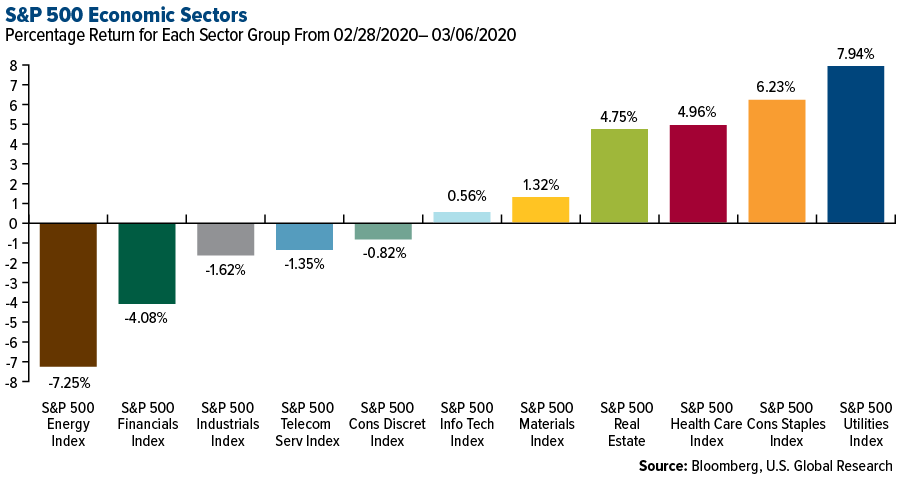

- Utilities was the best performing sector of the week, increasing by 7.94 percent versus an overall increase of 0.57 percent for the S&P 500.

- Cabot Oil & Gas Corp was the best performing S&P 500 stock for the week, increasing 17.52 percent.

- Gilead Sciences surged on Friday after an analyst suggested the company could unveil the test results of a coronavirus treatment later this month. Officials in China are testing Gilead’s drug, remdesivir, in two groups of patients with Covid-19. Evercore ISI analyst Umer Raffat suggested Friday the results of that study could be available in March. "Either a data monitoring committee gives us preliminary results from an ‘interim analysis,’ or perhaps the first (study) is near completion," Raffat said in a report.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 7.25 percent versus an overall increase of 0.57 percent for the S&P 500.

- Norwegian Cruise Line Holdings was the worst performing S&P 500 stock for the week, falling 27.27 percent.

- Helmerich & Payne fell 8.5 percent on Friday, the most in one day. The shares declined to $29.09, lower than any close since 2009

Opportunities

- One way to gauge whether the U.S. equity sell-off is getting long in the tooth is to compare the S&P 500 Index’s implied volatility to historical volatility. When the implied falls bellows the historical data, it suggests you may be closer to the end of the selling than the beginning. While a crossover has the potential of occurring in the near-term, it will take time for markets to heal, which suggests the ultimate low in stocks may still be many days away.

- The relative attraction of U.S. stocks over bonds has hit its highest ever for income investors after the latest collapse in Treasury yields. The spread between the 12-month forward dividend yield on the S&P 500 Index and the 10-year U.S. Treasury yield jumped to the widest on record this week, according to data compiled by Bloomberg.

- Utility stocks have more to offer income-seeking investors now that the yield on 10-year Treasury notes has set a record low. The S&P 500 Utility Index’s dividend yield surpassed the Treasury yield by more than 200 basis points Tuesday, when the latter fell below 1 percent for the first time, according to data compiled by Bloomberg. That gap was the widest since 2013.

Threats

- The Dow Jones Transportation Average, which is trading at its lowest level versus the broader U.S. market since the financial crisis, closed in bear market territory on Thursday. The 20 percent drop from its most recent peak came amid renewed concerns over the economic impact of the coronavirus. Airlines were among the gauge’s largest percentage decliners after the International Air Transport Association sad the outbreak could cost the industry $63 billion to $113 billion in lost revenue from passengers this year, up from an estimate of $30 billion just two weeks ago.

- Shares of Royal Caribbean Cruises, Norwegian Cruise Line Holdings and Carnival Corp. all plummeted Thursday after a ship operated by Carnival’s Princess Cruises was linked to California’s first coronavirus death. The three operators led declines on a percentage basis in the S&P 500 Consumer Discretionary Index.

- Through Thursday, the 10-day realized volatility in the S&P 500 Low Volatility Index exceeded that of the benchmark itself.

The Economy and Bond Market

Strengths

- Employers added a stronger than expected 273,000 jobs in February, matching the prior month’s revised gain, according to a Labor Department report Friday.

- The unemployment rate fell back to a half-century low of 3.5 percent, while average hourly earnings advanced 3 percent from a year earlier.

- America’s service industries enjoyed the fastest growth in a year last month as orders surged, showing momentum in the biggest part of the economy just as coronavirus concerns started to become more widespread. The Institute for Supply Management’s non-manufacturing index unexpectedly rose 1.8 points to 57.3 in February.

Weaknesses

- Treasury yields hurtled toward zero Friday as concern about the global economic and financial impact of the coronavirus spurred demand for havens and traders amped up bets on further central bank easing this month. Yields on the 30-year, 10-year and five-year securities fell to record lows.

- Global manufacturing contracted in February by the most since 2009 as the coronavirus severely disrupted demand, trade and supply chains. The JPMorgan Global Manufacturing PMI fell 3.2 points to 47.2. Production plunged the most in almost two decades while the measure of new export orders also fell to the lowest since 2009.

- The Federal Reserve could cut rates again at the next meeting in just two weeks. The Fed’s 50 basis point cut this week failed to calm global financial markets, with safe-haven Treasury yields hitting all-time lows. The S&P 500 index dropped over 10 percent from its February 19 closing high, after logging its biggest weekly percentage decline since October 2008.

Opportunities

- The White House is considering measures to respond to the economic impact of coronavirus, an administration official said, including deferring taxes for the industries hardest hit by the virus, primarily hospitality and travel.

- While the Fed took the emergency measure of cutting rates by 50 basis points on Tuesday, traders think there’s more to come, based on index swaps and futures pricing. In both instances, the market sees at least one more cut of 25 basis points this month, with a Federal Open Market Committee decision slated for March 18.

- Federal Reserve Bank of Boston President Eric Rosengren said policy makers should be allowed to buy a broader range of assets if they lack sufficient ammunition to fight off a recession with interest rate cuts and bond purchases.

Threats

- The OECD offered an interim global economic outlook report Monday and cut the forecast for 2020 global growth to 2.4 percent from the “already weak” 2.9 percent estimate released in November.

- China’s economy has been ravaged by the virus in recent weeks, with many factories staying closed and consumers turning defensive. The PMIs for February showed a collapse in economic activity.

- Investors will be watching for the February CPI numbers next week, but with the Fed so focused on the virus, economic data might not matter much. The Fed is not reacting to any real weakness in the US economy. Rather, it’s trying to shield the economy from the future virus impact.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was iron ore pricing out of China, which gained 6.65 percent. Nitrogen dioxide levels rising across China’s heartland indicates that economic activity is picking up again, according to data compiled by Wind.com. Levels of the gas, which is produced during the burning of fossil fuels, fell in February after the government locked down communities to contain the coronavirus. According to a Bloomberg Economics report, the Chinese economy was running at 60 percent to 70 percent last week, up from around 50 percent in February.

- Bloomberg reports that Brown University’s endowment sold 90 percent of its holdings in companies that extract fossil fuels. Brown President Christina H. Paxson wrote “we do not plan to make new investments in fossil fuel companies unless and until they make significant progress in converting themselves into providers of sustainable energy.”

- Peru says that its copper output will increase 2.4 percent this year to 2.5 million tons. The nation’s Mining and Energy Minister announced that production will continue to rise in the next three years to reach 3 million tons by 2022 as new mines begin operations.

Weaknesses

- The worst performing major commodity for the week was sugar, which fell 7.92 percent as slumping energy markets lowered the prospects for cane-based ethanol production. Even after the U.S. Federal Reserve’s emergency interest rate cut of 50 basis points, commodities still dropped as investors don’t think it will be enough to counter the economic impact of the coronavirus. Rate cuts are generally positive for housing, but the lumber market still fell. Open interest in lumber had lost 25 percent in six sessions by Wednesday.

- Oil continues to get beaten down by demand concerns over the coronavirus. The Organization of Petroleum Exporting Countries (OPEC) is trying to support prices by reducing production further by 1.5 million barrels a day – the lowest level of production since mid-2009. Russia is not joining in the production cuts, which puts the alliance on the brink of failure. Bloomberg reports that oil fell to a more-than two year low on the news. Equinor CEO Eldar Saetre said in an interview that “there’s a high level of uncertainty and a broad range of outcomes” that will impact global oil demand in 2020. Crude has fallen around 24 percent so far this year and OPEC cut its demand forecast from 990,000 barrels a day to just 480,000.

- As China’s economy suffers from the virus outbreak, shoppers are staying home and pushing the diamond industry into further trouble. De Beers, the world’s largest diamond miner, said its sales fell by more than a third last week from its first sale of the year in January, reports Bloomberg.

Opportunities

- Chevron CEO Mike Wirth pledged as much as $80 billion in dividends and share buybacks over the next five years in its annual investor meeting on Tuesday. The boost will come from crude production in the Permian Basin and New Mexico, which will double over the time period and eventually account for a third of Chevron’s global output.

- European Commission President Ursula von der Leyen unveiled a draft law on Wednesday that would make it illegal by 2050 to emit more greenhouse gases than can be removed from the atmosphere, reports Bloomberg. “It offers predictability and transparency for European industry and investors. And it gives direction to our green growth strategy and guarantees that the transition will be gradual and fair,” von der Leyen said about the new regulations that could make Europe the first climate-neutral continent.

- Banks are finally starting to back big battery storage projects as costs drop and demand grows. BloombergNEF found that prices for lithium-ion batteries fell by half from 2016 and 2019 and the U.S. has just 1,400 megawatts of battery storage today. The U.S. Energy Storage Association hopes to have 35,000 megawatts online in the next five years.

Threats

- The Air Force said it has spent $500 million on cleaning up “forever chemicals” that have polluted bases across the country, reports Bloomberg. These difficult to clean up chemicals, such as perfluorinated carboxylic acid (PFAS), are used in firefighting foam and efforts to create an effective foam that does not use the chemical have failed. Defense Secretary Mark Esper created a task force to manage potential pollution at 401 facilities with an estimated cost of $2 billion.

- The world might lose half of its sandy beaches by the end of this century if global temperatures continue rising. A study in Nature Climate Change says that a 4 degree Celsius increase in temperatures from pre-industrial levels would lead to erosion and more coastal flooding. The study predicts that sandy beaches would be eroded by 40 to 250 meters under the worst-case scenario.

- The Polish Centre for Climate and Energy Analysis found that prices in the European Union (EU) carbon market could triple by 2030 if it moves forward with the strictest emission-reduction target under the Green Deal climate strategy, reports Bloomberg. Emission permits could reach $85 a ton if the bloc plans to cut greenhouse gases 55 percent by the end of the decade.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 3.6 percent. The Bucharest stock exchange was the best place to hide as most markets in Europe sold off on the fear of the coronavirus spreading rapidly. Met Life and OMV Petrom were the best performing stocks, gaining 11.7 percent and 6.8 percent respectively.

- The Hungarian forint was the best performing currency this week, gaining 3.5 percent. All currencies in central emerging Europe appreciated in the past five days, with the exception of the ruble, after the U.S. dollar weakened due to the Federal Reserves’ unexpected decision to cut rates by 50 basis points.

- Health care was the best performing sector among eastern European markets.

Weaknesses

- Greece was the worst performing country this week, losing 6 percent. Banks trading on the Athens stock exchange sold off sharply, losing 10 percent of its market share in the past five days. Greece closed schools and universities and cancelled large public gatherings in an effort to minimize the spread of coronavirus.

- The Russian ruble was the worst performing currency in the region this week, losing 2.5 percent. Russia refused to agree to OPEC production cuts of 1.5 million barrels per day. The price of Brent crude oil dropped 10 percent in the past five days.

- Energy was the worst performing sector among eastern European markets.

Opportunities

- Russia and Turkey announced a ceasefire in the crisis in Syria’s Idlib province. The agreement reached on Thursday calls for the creation of a security corridor along the strategic M-4 highway policed by joint Russian-Turkish patrols, as well as steps to allow the return of refugees and access for humanitarian aid.

- According to Virologist Thomas Pietschmann, the coronavirus is not very heat-resistant, which means that the virus quickly breaks down when temperatures rise. With winter behind us the end to the coronavirus could be just few month away. The recent selloff in equites could present a good time to add to quality names that were too expensive to buy few weeks ago. Russian stocks offer the highest dividends among major global emerging markets.

- The airline industry could lose $63 billion to $113 billion in passenger revenue this year, the International Air Transportation Association said, revising its estimate of a $30 billion hit made just two weeks ago, as tourists prefer to stay home until the coronavirus is contained. Economies that depend on travel and tourism will be negatively impacted. However, as this chart below illustrates, central emerging European counties (including Poland, the Czech Republic and Hungary) do not rely on tourism as a source of income. Hungary) do not rely on tourism as a source of income.

Threats

- The final February manufacturing PMI for the eurozone was released at 49.2, slightly above the flash PMI of 49.1. The final service PMI was 52.6 versus 52.8, leaving the Composite PMI unchanged at 51.6. The latest PMI readings do not include the impact of the coronavirus spread in Europe and the expectation is that following months readings will be much weaker, with the possibility of the service PMI falling below the 50 level. A reading above 50 represents expansion while below 50 is contraction.

- The Moscow government and a Russian watchdog (Rospotrebnadzor) have released an updated list of 11 countries with “unfavourable” situations regarding the coronavirus. This is the list of countries coming from which people are obliged to “self-isolate” themselves for 14 days after arrival includes China, South Korea, Iran, Italy, France, Germany, Spain, Switzerland, Great Britain, Norway and the USA. Other countries may follow with similar restrictions on travel.

- The ECB will meet next week on March 12. While Bloomberg economists are expecting no rate cuts, some analysts predict at least a 10 basis point cut to the deposit rate, which is already at negative 50 basis points. If the deposit rate is cut by an additional 10 basis points next week, institutions will have to pay 60 basis points for depositing funds overnight. European banks’ profits will be under further pressure.

China Region

Strengths

- China’s Shanghai Composite rose 5.35 percent for the week, and both Korea’s KOSPI and Thailand’s SET jumped more than 2 percent on the week, as well.

- Information Technology constituted the best relative sector performance in Hong Kong’s Hang Seng Composite for the week, gaining 2.29 percent.

- Most emerging market currencies gained slightly on the week as the U.S. Federal Reserve slashed interest rates here and the U.S. dollar weakened. The Malaysian ringgit was the best EM currency in the region.

Weaknesses

- India’s SENSEX dropped 1.82 percent on the week, while Singapore’s FTSE Straits Times Total Return Index declined by 1.66 percent. The Philippines was slightly down—just 13 basis points on the week—but other regional indices bounced back a bit for the week.

- Materials declined 1.34 percent in the HSCI sector show this week.

- Last week we suggested the China purchasing manager’s index (PMI) data would almost surely show significantweakness. Well, here’s what that looks like. All misses, as expected. Manufacturing PMI fell to 35.7, non-manufacturing to 29.6, while the Caixin China Manufacturing PMI dropped to 40.3 and the Services down to 26.5. Again, on the bright side, China is reportedly getting back to work—though still far from at full capacity and with more new COVID-19 cases popping up—and so one hopes the rebound is quick. But here we document the sharpness of the decline, hopefully behind us to stay.

Opportunites

- One headline worth sharing this week is one that ran in the Bloomberg earlier in the week: “Hong Kong’s Stocks Become Rare Shelter From Global Volatility.” From violent protests and trade war concerns to coronavirus concerns at present—among, perhaps, other concerns for the economy in contraction in the HK SAR—it is nonetheless noteworthy that once prices have been thoroughly pummeled and sentiment beaten down, it seems some trades and international investors may be prepping for expected fiscal stimulus from China to counter coronavirus effects further and stimulate demand. The article notes that fund flows from the mainland already indicate some mainlanders have starting stepping in, with the most flows in February since January 2018.

- The stimulus in response to the coronavirus outbreak continues to flow, with more than $50 billion already committed now from governments around the world to offset anticipated (or realized and realizing!) economic setbacks.

- Another positive article this week scrolling across Bloomberg News worth sharing as is: “Travel Demand is Rebounding in China as Virus Worry Recedes.” The article noted that hotel bookings to March 1 jumped 40 percent week over week, per one online travel company, while peak daily bookings for domestic flights in China were up 230 percent from the lows of February. That’s hardly the whole travel industry, mind you, and it hardly solves increasingly complicated border situations internationally even as the rest of the world continues raising travel bans and restrictions, but it is something, and—given some of the satellite imagery making the media rounds this week of China’s industrial areas, things are beginning to pick back up in observable ways there.

Threats

- …but in the rest of the world, coronavirus confirmed-case concerns continue. The question increasingly becomes—at least from an economic opportunity standpoint, or an economic threat one—how long does the virus drag on growth? To what extent will supply chains be hit further than they are already? Increasingly, and as the Federal Reserve noted this week, the problem may be both supply and demand issues at this point. And of course, if a broader selloff or souring of sentiment ensues globally, which babies get chucked out with the proverbial bathwater? To be sure, COVID-19 concerns topped the charts this week, kicking off what could be a month of the wrong kind of “March Madness.” One is always hopeful for the best outcome. But markets sense uncertainty. And there remains all that we don’t yet know about the extent of the virus at this point. Could China end up with re-infections or new outbreaks? There remains much about the virus we don’t yet know.

- Hong Kong’s property market suffered at least another minor setback this week as values on existing homes declined by 1.78 percent week over week.

- Singapore downgraded its forecast for overall economic growth this calendar year to -0.5 to 1.5 percent. The city-state’s baseline view is still, at this point at least, one expecting a 0.5 percent expansion for the year, but there remains “a significant degree of uncertainty over the length and severity of the outbreak,” media reported Ministry of Trade and Industry official Gabriel Lim said.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 6 was HyperExchange, up 536.38 percent.

- Chinese manufacturers are gradually resuming business after the coronavirus outbreak delayed shipments and activity. As a result, the computer processing power of the bitcoin network is growing again, reports CoinDesk. According to data from PoolIn, one of the largest bitcoin mining pools, the average hashing power on bitcoin over the past seven days ending March 4 is up 5.4 percent from where it stagnated for a month beginning January 28.

- Atlas Holding LLC runs the Greenidge Generation power plant in New York that also doubles as a bitcoin mining operation. The plant installed 7,000 crypto mining machines that use the electricity the plant already produces to generate around $50,000 worth of bitcoin each day, or around 5.5 coins per day. Bloomberg reports that the machines work off “behind-the-meter” power, which is extremely low cost. This is part of a growing trend of installing crypto mining facilities at existing power generation locations.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 6 was ShineChain, down 39.19 percent.

- Facebook and its partners are considering redesigning the Libra cryptocurrency project in order to woo reluctant global regulators. Facebook hoped to create a single global digital currency, but after opposition to only accepting a single coin, the project is now thinking of vamping into more of a payments network. If the project becomes a payments network, average consumers might not understand the difference between it and existing apps such as PayPal. Bloomberg reports that the group will soon re-introduce the Libra.

- The U.K. Financial Conduct Authority issued a warning to cryptocurrency derivatives exchange BitMEX from targeting British residents without its consent or approval. The authority said in a note this week that “almost all firms and individuals offering, promoting or selling financial services or products in the U.K. have to be authorized by us.”

Opportunities

- India’s Supreme Court gave a win to cryptocurrency exchanges after striking down the Reserve Bank of India’s April 2018 decision that effectively banned banks from offering services to support cryptocurrencies. Bloomberg’s Upmanyu Trivdei writes that “the ruling is an opportunity for virtual currency investors and businesses in India to push against stricter rules being planned by a skeptical government, and potentially raises hopes for projects.”

- Bitcion had a strong start to the week after having its worst week since November. The coin rallied more than 4 percent on Monday as investors rethink its status as a safe haven during the coronavirus market turmoil. Don Guo, CEO of Broctagon Fintech Group, said “crypto isn’t bound by international borders or trade relations and, if this continues, we could not only see the price of Bitcoin skyrocket.”

- EY, ConsenSys and Microsoft have thought of a new way of using the public ethereum mainnet to connect firms’ internal systems for resource planning. CoinDesk reports they are calling it the Baseline Protocol, which would use ethereum as a message-orientated middleware rather than a source-of-truth data repository. John Wolpert, head of Web3Studio at ConsenSys, said that the concept should be attractive to chief security officers of large enterprises since their critical data all remains within their firewalls.

Threats

- KPMG wrote in a report this week that the cryptocurrency market needs to improve how it secures digital assets before it continues to grow. The firm said that at least $9.8 billion in digital assets have been stolen by hackers since 2017 due to poorly written code and security. Sal Ternullo, co-author of the report, said “institutional investors especially will not risk owning crypto assets if their value cannot be safeguarded in the same way their cash, stocks and bonds are.”

- Deputy Governor at the Bank of Japan Masayoshi Amamiya said at the Future of Payments Form this week that the Japanese central bank digital currency (CBDC) currently has little merit and that advanced economies do not need their own cryptocurrencies. “At this point, there is no need to implement new steps to ensure people’s access to central bank money.”

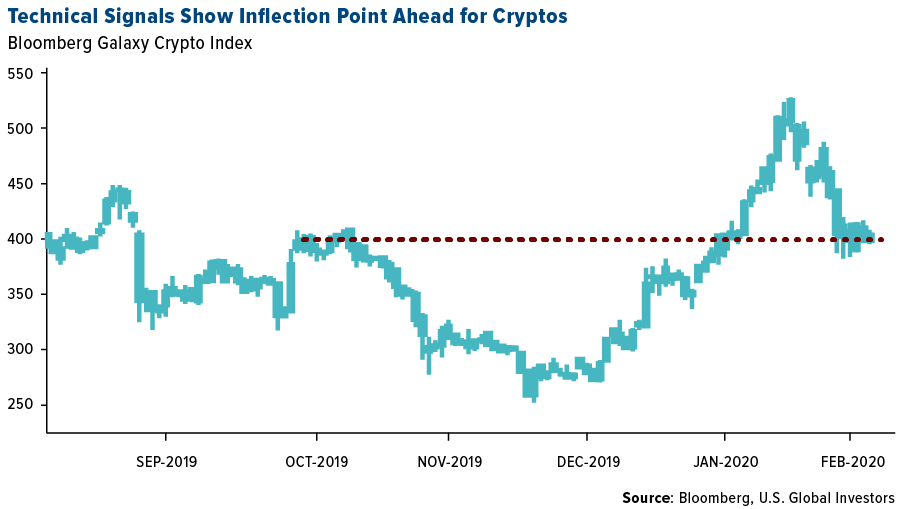

- As of March 4, the Bloomberg Galaxy Crypto Index had lost nearly 18 percent as global stock markets whipsaw and after Warren Buffett pronounced that digital assets have no value. Cryptocurrencies are losing their status as a safe haven that moves in the opposition direction of the stock market. Bloomberg reports that its crypto index is lingering near a key inflection point after trending lower.

Airline Sector

Strengths

- United Airlines is buying the Westwind School of Aeronautics, a flight training school in Phoenix, to help increase the supply of future pilots. The program is expected to train pilots for United Express regional carriers, which have struggled to fill jobs known for challenging schedules and entry-level pay, reports Bloomberg. The airline is also exploring ways to boost financing programs for aviators’ education. United anticipates 300 students will graduate in 2021.

- Airbus unveiled a curvaceous aircraft design at the Singapore Airshow that blends the wing and body, a design feature that could cut carbon emissions by 20 percent, reports Reuters. “Blended wing body” aircraft produce less aerodynamic drag and are more efficient to fly. Airbus has been performing test flights at a secret location since last year. Jean-Brice Dumont, executive vice president of engineering at Airbus, told reporters at the show: “We need these disruptive technologies to meet our environmental challenge. It is the next generation of aircraft; we are studying an option.”

- The Seamless Air Alliance, a nonprofit group of 30 companies including Airbus and Delta, says that its new technology infrastructure will make in-flight connectivity systems modular and hopes to introduce a global standard that will improve in-flight Wi-Fi. Currently, airlines only have the equipment of their chosen internet service provider. A new universal standard of being able to switch between providers would create a smooth experience for customers and save billions in the long run.

Weaknesses

- The International Air Transport Association (IATA) warned that the airline industry expects its first annual decline in global passenger demand in 11 years due to the impact of thousands of cancelled flights. Passenger demand is forecast to drop by 0.6 percent in 2020, compared with a December estimate of 4.1 percent growth for the year. Bloomberg reports that the global health crisis will shave around $30 billion from revenue. Several airlines have issued concerns of falling revenue, with Asian airlines expecting the biggest hit.

- On February 5, Pegasus Airlines flight 2193 crashed upon landing at Istanbul’s Sabiha Gokcen Airport. Three people were killed in the accident and the other 180 people on board were injured after the aircraft broke into three pieces. In the midst of bad weather, the plane failed to come to a stop, overshooting the runway and plunging 20 meters down an embankment. The aircraft was a Boeing 737-800, which has a strong safety record, and predates the grounded 737 MAX. Possible causes of the accident include pilot error, poor working conditions of the runway, bad weather and Pegasus’ security protocols.

- Boeing said that returning the 787 MAX jets to service will take several quarters. Randy Tinseth, Boeing’s vice president of marketing, said in an interview that the company will first ensure the 400 planes with customers and the 300 more stored in factories are flying again before ramping up production, reports Bloomberg.

Oppurtunites

- JetBlue founder David Neeleman has a new airline called Breeze Airways that aims to fly routes that aren’t currently served, having already identified 500 potential routes. Neeleman said “we’ll go to larger cities, but from cities that don’t have any service. I don’t think we’re going to fly a single route that anybody is flying on. There’s no reason to fly places that already have competition.” Breeze will have a similar model to other low-cost carriers and will only fly two models of planes.

- Boeing said that airlines in Southeast Asia will need 4,500 new aircraft over the next 20 years to meet growing demand from the region’s middle class, reports Bloomberg. The manufacturing giant said that expected new orders are worth $710 billion at the Singapore Airshow. Growth is driven by carriers in Vietnam, Thailand and Indonesia. Boeing announced some positive news in February: it received its first order of 2020. Japan’s ANA Holdings Inc. confirmed that it plans to take 20 more 787 Dreamliner wide-body jets.

- A new trend is emerging in carriers flying longer distances on smaller planes. Bloomberg reports that China Aircraft Leasing Group Holdings is considering ordering long-range jets from the Airbus A320neo aircraft line. Airbus’ A321XLR is a long-range version of the A320 narrow body that already has 450 orders and commitments, challenging Boeing’s 737 MAX model.

Threats

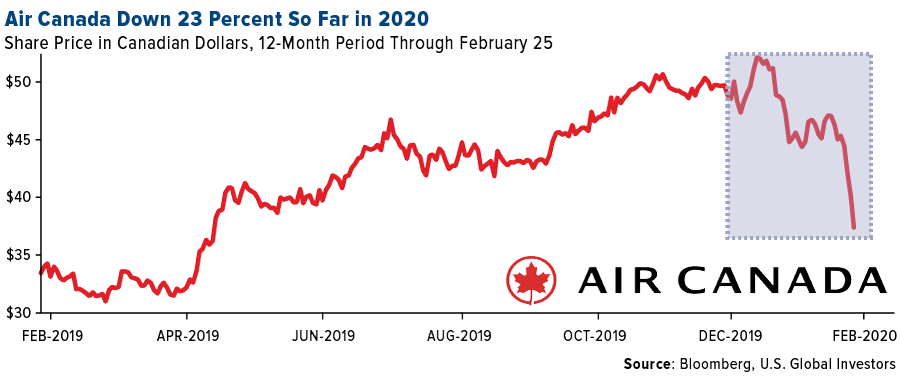

- The coronavirus continues to negatively impact the global airline industry. Carriers around the world have cancelled more routes as the virus spreads further and travelers fear flying. Notably, United withdrew its 2020 profit forecast, citing uncertainty from the virus. Lufthansa has frozen hiring. Air Cathway said that 25,000 of its employees have taken unpaid leave – around 75 percent of its workforce. One of the harder hit stocks is Air Canada, which has lost $3 billion in market value from January 13 to February 25. Air Canada was the top performing airline stock in 2019, rising 87 percent on plans to boost its global presence. According to the Bloomberg World Airlines Index, the stock is now the worst so far in 2020, down 28 percent as of February 25.

- Airbus admitted to illegally trying to sway plane sales to discount carrier AirAsia Bhd and agreed to a $4 billion bribery settlement, reports Bloomberg News. Tony Fernandes, who built AirAsia, was one Airbus’ largest customers and made headlines by announcing big deals. This corruption probe had been going on for four years before settling in February. As a part of the deal, Fernandes will step away as CEO for two months while the Malaysian government investigates.

- Interjet, operated by ABC Aerolineas SA, is worrying investors after grounding four of its Airbus SE planes. The company says the planes are undergoing major maintenance and some speculate that those planes are actually being used for parts to keep other aircraft in operation, reports Bloomberg. The carrier is under financial stress and said in a court filing that its accumulated losses over the year could be considered a technical bankruptcy.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 278.88 | +29.84 | +11.98% |

| XAU | 103.01 | +8.86 | +9.41% |

| Gold Futures | 1,674.20 | +107.50 | +6.86% |

| Korean KOSPI Index | 2,040.22 | +53.21 | +2.68% |

| S&P/TSX VENTURE COMP IDX | 506.54 | +8.93 | +1.79% |

| DJIA | 25,864.78 | +455.42 | +1.79% |

| S&P Basic Materials | 335.02 | +4.35 | +1.32% |

| Hang Seng Composite Index | 3,637.26 | +36.05 | +1.00% |

| S&P 500 | 2,972.37 | +18.15 | +0.61% |

| Nasdaq | 8,575.62 | +8.25 | +0.10% |

| Russell 2000 | 1,449.22 | -27.21 | -1.84% |

| Oil Futures | 41.58 | -3.18 | -7.10% |

| S&P Energy | 318.64 | -24.89 | -7.25% |

| 10-Yr Treasury Bond | 0.78 | -0.37 | -32.35% |

| Natural Gas Futures | 1.72 | +0.04 | +2.14% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 278.88 | +19.38 | +7.47% |

| Gold Futures | 1,674.20 | +111.40 | +7.13% |

| XAU | 103.01 | +0.82 | +0.80% |

| Hang Seng Composite Index | 3,637.26 | -43.26 | -1.18% |

| Korean KOSPI Index | 2,040.22 | -125.41 | -5.79% |

| Nasdaq | 8,575.62 | -933.07 | -9.81% |

| S&P 500 | 2,972.37 | -362.32 | -10.87% |

| DJIA | 25,864.78 | -3,426.07 | -11.70% |

| S&P Basic Materials | 335.02 | -48.16 | -12.57% |

| Russell 2000 | 1,449.22 | -232.70 | -13.84% |

| Oil Futures | 41.58 | -9.17 | -18.07% |

| S&P Energy | 318.64 | -97.33 | -23.40% |

| 10-Yr Treasury Bond | 0.78 | -0.87 | -52.91% |

| S&P/TSX VENTURE COMP IDX | 506.54 | -69.82 | -12.11% |

| Natural Gas Futures | 1.72 | -0.14 | -7.58% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 278.88 | +30.93 | +12.47% |

| Gold Futures | 1,674.20 | +185.60 | +12.47% |

| XAU | 103.01 | +4.63 | +4.71% |

| Hang Seng Composite Index | 3,637.26 | +61.94 | +1.73% |

| Nasdaq | 8,575.62 | +4.92 | +0.06% |

| Korean KOSPI Index | 2,040.22 | -20.52 | -1.00% |

| S&P 500 | 2,972.37 | -145.06 | -4.65% |

| S&P/TSX VENTURE COMP IDX | 506.54 | -30.57 | -5.69% |

| DJIA | 25,864.78 | -1,813.01 | -6.55% |

| S&P Basic Materials | 335.02 | -36.48 | -9.82% |

| Russell 2000 | 1,449.22 | -165.61 | -10.26% |

| Oil Futures | 41.58 | -16.85 | -28.84% |

| Natural Gas Futures | 1.72 | -0.71 | -29.13% |

| S&P Energy | 318.64 | -110.70 | -25.78% |

| 10-Yr Treasury Bond | 0.78 | -1.03 | -57.04% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

OMV Petrom

Equinor ASA

Delta Air Lines Inc

United Airlines Holdings Inc

Spirit Airlines Inc

American Airlines Group Inc

Cabot Oil & Gas Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg World Airlines Index is a capitalization-weighted index comprised of global airlines. The Bloomberg Galaxy Crypto Index is a market capitalization-weighted index that tracks the performance of the largest cryptocurrencies traded in USD. The NYSE Arca Global Airline Index is a modified equal- dollar weighted index designed to measure the performance of highly capitalized and liquid international airline companies. The Index tracks the price performance of selected local market stocks or ADRs of major U.S. and overseas airlines. The relative strength index (RSI) is a momentum indicator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The RSI is displayed as an oscillator (a line graph that moves between two extremes) and can have a reading from 0 to 100. A monetary base is the total amount of a currency that is either in general circulation in the hands of the public or in the commercial bank deposits held in the central bank’s reserves. This measure of the money supply typically only includes the most liquid currencies; it is also known as the "money base." There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. The S&P 500 Low Volatility Index measures performance of the 100 least volatile stocks in the S&P 500. The index benchmarks low volatility or low variance strategies for the U.S. stock market. The Korean Composite Stock Price Index (KOSPI) is the main tracking index in South Korea. The SET Index is a Thai composite stock market index which is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year. Sensex, otherwise known as the S&P BSE Sensex index, is the benchmark index of the Bombay Stock Exchange (BSE) in India. Sensex comprises 30 of the largest and most actively-traded stocks on the BSE, providing an accurate gauge of India’s economy. The FTSE Straits Times Index (STI) is a capitalization-weighted stock market index that is regarded as the benchmark index for the Singapore stock market. It tracks the performance of the top 30 companies listed on the Singapore Exchange.