What Tariffs and the NBA Finals Mean for Gold’s Rally

Date Posted: June 7, 2019

Read time: 51 min

As we close out another week, I'm currently in Toronto, the mining finance capital of the world. But at the moment, all eyes are on the Toronto Raptors, now the most valuable sports franchise in Canada as they make their way through the NBA Finals.

Press Release: U.S. Global Investors Continues GROW Dividends

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

As we close out another week, I’m currently in Toronto, the mining finance capital of the world. But at the moment, all eyes are on the Toronto Raptors, now the most valuable sports franchise in Canada as they make their way through the NBA Finals.

The whole country of Canada has rallied around this international team, which has players from all over and whose main superstar, Kawhi Leonard, previously played for San Antonio, home of U.S. Global Investors. The enthusiasm and energy surrounding the Raptors is infectious, and I truly believe that this type of positivity can lead to success in all areas of life—even when it comes to investing and economics.

Letting negative energy get in the way is disruptive, as we saw this week when Warriors part-owner Mark Stevens shoved Raptors player Kyle Lowry from courtside. Even LeBron James called out Stevens’ unsportsmanlike behavior, writing in an Instagram post, “There’s absolutely no place in our BEAUTIFUL game for that AT ALL.”

Economic wealth is made and lost by the attitudes we choose to present to the world. Because of his negativity, Stevens, a billionaire venture capitalist, will be fined $500,000 and be banned from the NBA for a year. There may also be further, unforeseen ramifications.

This brings me to the topic of the U.S.-China trade war, which some may argue is about as negative as you can get. Did you know the biggest losers in the stand-off will be the two superpowers themselves, responsible for 40 percent of trade around the world? The U.S. is projected to lose as much as $94 billion in exports, China $205 billion, according to the United Nations Conference on Trade and Development (UNCTD).

Another loser is the average American, whose tax reform savings has already been wiped out by the trade war, according to Bloomberg.

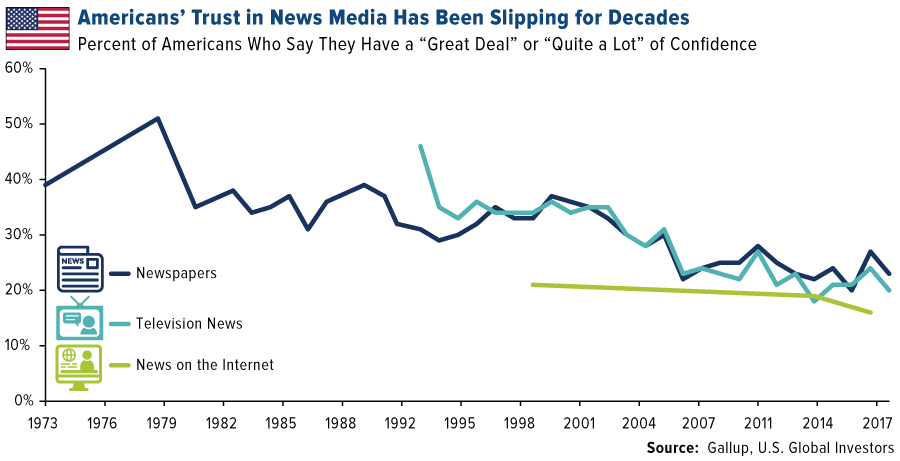

Trust in Institutions Has Been Slipping

Americans’ trust in institutions, from the federal government to banks to the news media, has been deteriorating for decades. Sixty years ago, three quarters of Americans expressed faith in the government to do the right thing “most of the time” or “just about always.” Today, only one in five people, a near-record low, believes our leaders make decisions in the country’s best interest.

The news media fares just as poorly. A new survey finds that Americans believe “fake news” is a bigger problem right now than violent crime, illegal immigration and terrorism.

Just take a look at the chart below, based on Gallup polling data going back to 1973. Whether it’s newspapers, television news or, more recently, online news, Americans’ faith is steadily eroding. Last year, the percent of Americans who said they have a “great deal” or “quite a lot” of confidence in newspapers stood at a near-record low of 23 percent. Trust in television and online news was even lower.

So where can you still put your trust in today’s often cynical world? Friends and family. Our churches and other religious organizations. Our jobs.

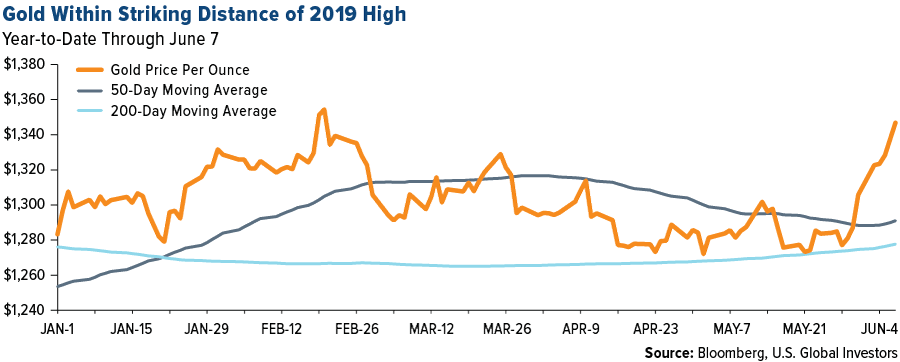

As an investor, I continue to have great faith in gold as a store of value during times of economic and geopolitical uncertainty. It’s behaved precisely as I expect it to. In response to heightened global trade concerns and weakening economic indicators, investors have piled into the yellow metal, pushing its price up for a remarkable eight straight days as of today. We haven’t seen such a winning streak since June 2014, when gold traded up for 10 straight days.

It’s now within striking distance of its 2019 high of about $1,356 an ounce, which should spur even more investors to get off the sidelines and participate.

White House Still Moving Forward With Tariff on All Mexican Goods

Indeed, there are a number of warning signs that suggest investors should proceed with caution as the U.S. economic expansion turns 10 years old. Global manufacturing growth reversed for the first time since 2012, with the purchasing manager’s index (PMI) falling for a record 13 months in May.

This weakness turned up in the monthly jobs reports from the federal government and payroll services provider Automatic Data Processing (ADP). The Labor Department reported today that U.S. employment edged up only 75,000 in May, far below expectations of 175,000.

According to ADP, the U.S. added 27,000 jobs, making May the weakest month for job gains in more than nine years. I don’t know about you, but I can’t help reading this as a direct negative consequence of the White House’s escalating trade war with China and threat to impose a tariff on all imports from Mexico. The U.S. goods producing sector was hit hardest, with construction losing 36,000 positions, natural resources and mining losing 4,000 and manufacturing losing 3,000.

The 5 percent Mexican tariff is still reportedly on track to be imposed on Monday, despite negotiations that took place this week between U.S. and Mexican officials.

As I’ve explained elsewhere, tariffs are essentially taxes and, as such, they’re inflationary. This has historically supported the price of gold.

Besides Walmart and Costco, a number of other retailers have been telling customers and investors that prices will be going up thanks to either the Chinese and/or Mexican tariff. Discount retailer Five Below said it will likely need to raise prices on certain items above $5 for the first time. Dollar General and Dollar Tree both alerted shoppers that they will be “facing higher prices as 2019 progresses.”

|

Discussing the trade war, JPMorgan’s Michael Cembalest, who hosts the “Eye on the Market” podcast, reminded listeners this week of an article written back in August 2015 by Trump’s National Economic Council director, Larry Kudlow, and former Trump pick for the Federal Reserve Board of Governors Stephen Moore. In the article, titled “Why Trump’s protectionist ways will hurt the economy,” Kudlow and Moore compared then-candidate Trump unfavorably to Herbert Hoover, the last Republican “trade protectionist.”

“Does Trump aspire to be a 21st century Hoover with a modernized platform of the 1930 Smoot-Hawley tariff that helped send the U.S. and world economy into a decade-long depression and a collapse of the banking system?” the two asked.

For better or worse, we may end up getting an answer to this question in the coming weeks and months.

What the Gold/Silver Ratio Is Telling Us

Another sign of slowing economic growth is the surging gold/silver ratio. This ratio tells you how many ounces of silver it takes to buy one ounce of gold. This week it crossed above 90 for the first time in 26 years, meaning silver has not been this undervalued relative to gold since the first year of Bill Clinton’s first term.

The reason this is important is that half of silver demand comes from industrial applications. When the demand cools, the price of silver falls. One of the metal’s primary uses is in semiconductors, sales of which have been falling. According to the Semiconductor Industry Association (SIA), global sales were $32.1 billion in April, a 14.6 percent decrease from the same month last year. This is the deepest plunge since the financial crisis.

Buying silver, then, could be a contrarian play, but I recommend also that you maintain a 10 percent weighting in gold. Although the yellow metal’s price has surged this week, it’s still not quite in overbought territory when you look at the 14-day relative strength index (RSI). There could be further upside potential, especially if Trump moves forward with the Mexican tariff.

Will inflationary tariffs finally boost gold? Watch my latest interview with Kitco’s Daniela Cambone by clicking here!

Gold Market

This week spot gold closed at $1,340, up $35.35 per ounce, or 2.71 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.10 percent. The S&P/TSX Venture Index came in off just 0.83 percent. The U.S. Trade-Weighted Dollar was pummeled 1.20 percent lower.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

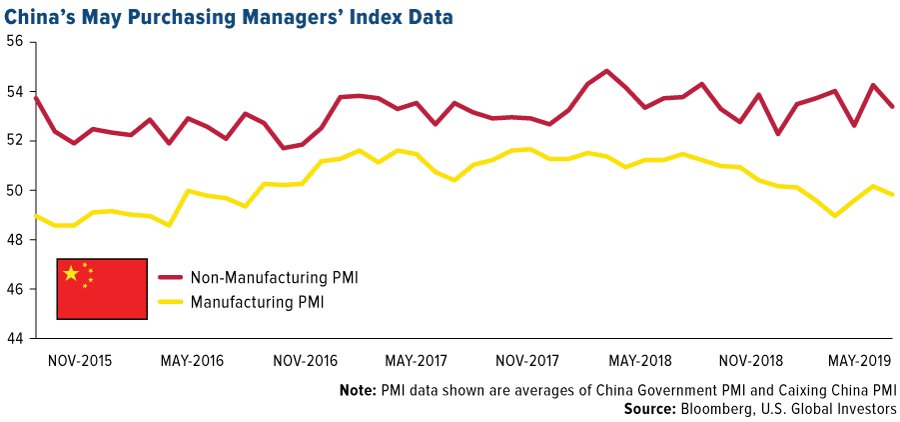

| Jun-2 | Caxin China PMI Mfg | 50.0 | 50.2 | 50.2 |

| Jun-3 | ISM Manufacturing | 53.0 | 52.1 | 52.8 |

| Jun-4 | Eurozone CPI Core YoY | 0.9% | 0.8% | 1.3% |

| Jun-4 | Durable Goods Orders | — | -2.1% | -2.1% |

| Jun-5 | ADP Employment Change | 185k | 27k | 271k |

| Jun-6 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jun-6 | Initial Jobless Claims | 215k | 218k | 218k |

| Jun-7 | Change in Nonfarm Payrolls | 175k | 75k | 224k |

| Jun-11 | PPI Final Demand YoY | 2.0% | — | 2.2% |

| Jun-12 | CPI YoY | 1.9% | — | 2.0% |

| Jun-13 | Germany CPI YoY | 1.4% | — | 1.4% |

| Jun-13 | Initial Jobless Claims | 215k | — | 218k |

| Jun-13 | China Retail Sales YoY | 8.0% | — | 7.2% |

Strengths

- The best performing metal this week was silver, up 3.06 percent, partly on the stronger gold price and on the news that the world’s third largest refinery was forced to halt production due to a failed blast furnace. The yellow metal was on fire this week and is heading for its best week in a year. The weekly Bloomberg survey showed that most gold traders and analysts are bullish going into next week as gold rose near the highest level in three months. Investors took note of the rally as assets in the largest bullion-backed ETF rose 2.2 percent on Monday – the equivalent of 16.44 metric tons. Much of the gold price action is driven by the growing geopolitical tensions surrounding the trade war.

- Another big driver for gold this week was poor ADP data and job growth. Companies in May added the fewest U.S. workers in any month since 2010, according to ADP data. Only 75,000 jobs were added in May versus an expected 175,000.

- Gold imports to the world’s second largest consumer of the metal, India, grew 36 percent in May from a year earlier, as customers rushed to buy after prices fell to their lowest level this year last month due to a stronger rupee, and then have subsequently risen this month so far.

Weaknesses

- The worst performing metal this week was platinum, up just 1.49 percent as hedge funds pushed their bearish view to a 15-week high. Bloomberg reports that Venezuela defaulted on a gold swap agreement valued at $750 million with Deutsche Bank. In 2016 Venezuela signed an agreement for a cash loan and put 20 tons of gold as collateral. A big headwind for gold in the past few months has been the troubled South American nation’s gold reserve selling, which amounted to $570 million in just May alone. Any wonder why gold was having difficulty going up when you have a significant distressed seller in the market?

- Dacian Gold saw its shares plunge a whopping 76 percent in this week after it received multiple downgrades because of lowered guidance. RBC Capital Markets analyst Paul Hissey said “Dacian is likely to now be uninvestable for some at any price.” RBC lowered its price target for the gold miner from $3 to just $0.50. Gold explorer NuLegacy announced on Monday that it had suspended all field exploration on its Red Hill property in Nevada to preserve cash. The stock fell 55 percent this week on the news.

- Tiffany & Co. said sales to Chinese tourists fell by more than 25 percent last quarter due to the trade war tension with the U.S. The Swiss Competition Commission said that it is suspending its investigation into whether banks colluded in precious metals trading due to a lack of evidence. Perhaps now they can investigate Glencore since almost every other security regulation agency outside of Switzerland has an investigation open against them.

Opportunities

- Ecuador just made a big show of support for the nation’s mining industry. The Vice President and Minister of Energy and Non-renewable Natural Resources visited Lundin Gold’s flagship project, where 50 percent of the construction is completed. The officials also presented a new Public Mining Policy that focuses on supporting large-scale operations and investments, and eradicating illegal mining.

- The focus on “weak dollar policy” continues from lawmakers. Senator Elizabeth Warren called for “actively managing” the U.S. dollar’s valuation as a part of a plan to create more American jobs. A weaker dollar has historically been positive for the price of gold. President Trump has also been critical of a strong dollar.

- The junior gold space is starting to get interesting as major miners are striking deals to fund some of the best projects they see going forward. PolarX secured an initial investment of $4.3 million from Lundin Mining to acquire an earn-in option on its Alaskan copper-gold projects with a staged spending program of up to $24 million on the property. PolarX has already drilled and identified a skarn deposit, which it will retain the ownership to, but Lundin is interested in any major copper-gold porphyry deposits on the land package which is all on state land, thus unencumbered by federal permitting or native titles. TriStar Gold announced that it will sell Royal Gold a stake in the company and a 2 percent net smelter royalty on its Castelo de Sonhos property in Brazil. The funding for TriStar will cover its budget for the next two years. Lastly, Chakana Copper Corp announced that it completed a previously announced private placement with Gold Fields to fund its project.

Threats

- Bloomberg reports that the trade war has already wiped out most of the average American’s household savings from the 2017 tax cuts. Only $100 remains of the average $930 tax break due to tariffs on Chinese imports. The additional tariffs and now added to Mexican imports on Monday, could cost middle-earning households a massive $4,000.

- South Africa’s Minister of Mineral Resources and Energy said this week that gold output from the once top producer will continue to decline due to a lack of exploration for new deposits.

- Liquidity in the credit market could be a big problem soon. Bank of America’s CEO Brian Moynihan said that leveraged finance threatens to become an issue in the broader market. According to a survey of investors at JPMorgan Chase’s U.S. Macro Quantitative and Derivatives Conference in New York last month, the greatest risk to quant strategies wouldn’t be an equity bear market or a rate increase. Rather, it would be a collapse in liquidity. Pimco’s fund managers are also concerned about liquidity after noticing that the bid-offer spread shows trading costs are approaching the December levels.

Index Summary

- The major market indices finished mostly up this week. The Dow Jones Industrial Average gained 4.71 percent. The S&P 500 Stock Index rose 4.41 percent, while the Nasdaq Composite climbed 3.88 percent. The Russell 2000 small capitalization index gained 3.34 percent this week.

- The Hang Seng Composite lost 0.20 percent this week; while Taiwan was down 0.85 percent and the KOSPI rose 1.50 percent.

- The 10-year Treasury bond yield fell 4 basis points to 2.082 percent.

Domestic Equity Market

Strengths

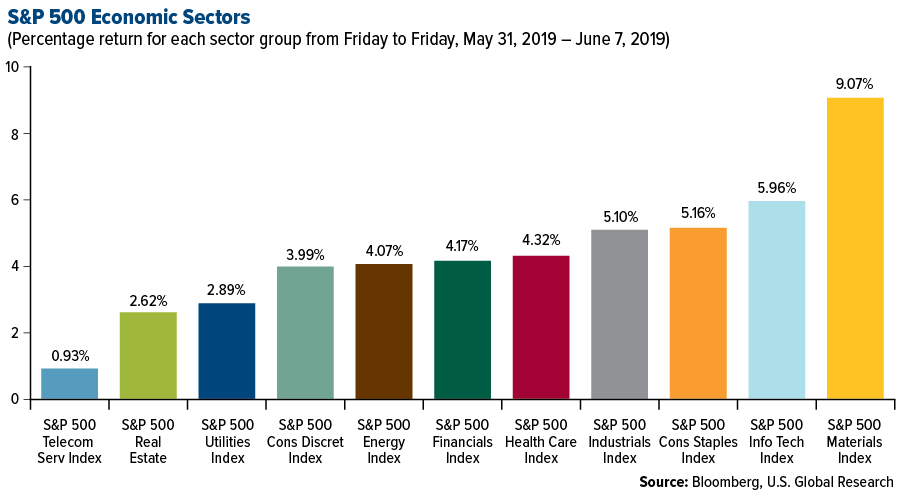

- Materials was the best performing sector of the week, increasing by 9.07 percent versus an overall increase of 4.44 percent for the S&P 500.

- Campbell Soup was the best performing stock for the week, increasing 18.65 percent.

- A flurry of deals made the first Monday of June the second biggest day for mergers and acquisitions this year, according to data compiled by Bloomberg. More than $40 billion of transactions were announced on Monday alone.

Weaknesses

- Communication services was the worst performing sector for the week, increasing by 0.93 percent versus an overall increase of 4.44 percent for the S&P 500.

- Centene was the worst performing stock for the week, falling 6.13 percent.

- Cloudera shares plunged 42 percent on Thursday, its largest intraday drop on record, after the software company reported dismal first quarter earnings. The company also announced that CEO Tom Reilly will be leaving, just five months after its merger with Hortonworks.

Opportunities

- Amazon unveiled a new Prime Air drone it says "within months" will start delivering packages. The new device can fly up to 15 miles, deliver packages up to 5 pounds and get deliveries to customers within 30 minutes.

- Shares of Advanced Micro Devices climbed 8 percent in the wake of an upgrade from a major Wall Street firm. Morgan Stanley reversed its previous views on the graphics processing chipmaker, boosting its rating on AMD from underweight to equal weight and pushing its price target up by $11 to $28 per share.

- American Airlines stock has begun to take flight as investors seem to be paying more attention to planned growth opportunities like the company’s expansion at its key Dallas-Fort Worth hub, and similar expansions in Charlotte and Washington.

Threats

- Big tech is taking big hits this week. Facebook, Google and Amazon all lost 4.5 percent to 7.5 percent on Monday after multiple reports suggested some of the biggest names in tech were being looked at over antitrust concerns.

- An overlooked signal of the stock market’s future suggests a tough road ahead, Morgan Stanley says. Narrow leadership and overt divergence between market sectors worsens the overall equity outlook for 2019, according to the firm’s chief U.S. equity strategist.

- Facebook investors voted to oust Mark Zuckerberg as chairman, but it doesn’t matter. Results from Facebook’s shareholder meeting showed 68 percent of outside investors wanted Zuckerberg replaced as chairman. However, the proposal didn’t pass because the CEO has voting control of the company.

The Economy and Bond Market

Strengths

- The unemployment rate for the month of May remained at 3.6 percent, the same as the month prior, reports MarketWatch.

- Average hourly earnings rose by 0.2 percent in May, the same as April’s rate. Over the last 12 months, earnings rose by a solid 3.1 percent.

- A gauge of U.S. consumer sentiment climbed to the second-highest level since 2000. The Bloomberg Consumer Comfort Index rose to 61.7 in the week ended June 2, according to a report on Thursday.

Weaknesses

- According to the Labor Department, job creation fell sharply in May, with nonfarm payrolls up by just 75,000, even as the unemployment rate remained at a 50-year low. The decline was the second in four months that payrolls increased by less than 100,000, CNBC reports.

- The ISM manufacturing index unexpectedly fell in May to the lowest level since October 2016, coming in at 52.1. As Bloomberg reports, this is a sign that President Trump’s trade war with China is weighing on the economy as he considers further tariffs.

- The U.S. trade deficit narrowed in April, reports Bloomberg, as both exports and imports tumbled. The deficit in goods and services shrank to $50.8 billion.

Opportunities

- Investors are racing into ETFs tracking short-term U.S. government debt as the inversion between shorter- and longer-dated Treasury bills deepens. The SPDR Bloomberg Barclays 1-3 Month T-Bill ETF has attracted $1.31 billion during the past five days, the record streak of inflows, according to data compiled by Bloomberg. The fund, which uses the ticker symbol BIL, added $476 million on Wednesday, the most in a single day since November. Yields on one-month Treasuries remain higher than those on one-year bills, an atypical relationship that has expanded as traders price-in an increasing likelihood that the Federal Reserve will cut interest rates to offset the impact of escalating trade tensions on growth.

- The yield curve’s recent inversion is poised to reverse, according Vanguard Group’s Gemma Wright-Casparius. The market hasn’t priced the inflationary impact of tariffs, according to Wright-Casparius, and the Fed will likely ease policy “very aggressively” should growth meaningfully slow. “It’s almost a win-win on the steepener at some level,” she commented at the Bloomberg Invest New York conference this week.

- A highlight in U.S. economic data next week will be Friday’s retail sales figures. Retail sales are expected to increase by 0.6 percent month-over-month in May, which would suggest U.S. consumer spending is holding up in what would be a healthy sign for second quarter growth.

Threats

- Comments from Fed Chairman Jerome Powel, along with some technical assistance from Italian mathematician Fibonacci, the recent slump in U.S. Treasury yields came to a halt Tuesday, reports Bloomberg. The 10-year benchmark yield rose 6 basis points after Powell signaled an openness to possible interest-rate cuts while stopping short of signaling any kind of imminent move, the article explains. Yields had slumped more than 50 basis points from mid-April and hit the closely watched Fibonacci technical support around the 2.06 percent level at the start of the week.

- Will a U.S. recession happen before next spring? "Recent conversations with investors have reinforced the sense that markets are underestimating the impact of trade tensions," Morgan Stanley’s chief economist, Chetan Ahya, wrote. "Investors are generally of the view that the trade dispute could drag on for longer, but they appear to be overlooking its potential impact on the global macro outlook."

- Ray Dalio, billionaire founder of Bridgewater Associates, said that he views the U.S.-China trade conflict as more than a “trade war” and that increasing export controls would be a major escalation. “History shows that countries in conflict have seen that such conflicts can easily slip beyond their control and become terrible wars that all parties, including the leaders who got their countries into them, deeply regretted, so the parties in the negotiations should be careful that that doesn’t happen,” Dalio wrote in a post. “Right now we are seeing brinksmanship negotiations, so it is a risky time.”

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was lead, which gained 6.52 percent as Nystar’s Port Pirie smelter in Australia halted production and declared force majeure on shipments to customers due failure of a blast furnace. Lead inventories are at their lowest since 2009. JPMorgan’s Infrastructure Investments Group has agreed to buy El Paso Electric Co. for $2.78 billion in cash, which is a 17 percent premium to the closing price on May 31. Shares of El Paso rose as much as 15 percent on Monday before trading began, reports Bloomberg. Although iron ore has taken a tumble the last few weeks, inventories at China’s ports has contracted to the lowest since January 2017, with the volume of ore from Brazil now lower than the level when the Vale SA dam disaster occurred in January. This could be positive for the iron price.

- Bloomberg’s Olga Tanas reports that Russia has resolved one of the biggest obstacles to restoring the flow of uncontaminated crude oil to Eastern Europe after settling how to handle compensation claims. This should ease concerns of a tightening global oil market. In April it was discovered that millions of tons of tainted oil from Russia was piped into Germany, Poland, Belarus and Ukraine.

- According to BloombergNEF research, the cost of battery production at gigafactories is falling. It estimates new build capital expenditure costs have fallen 34 percent and are set to fall another 43 percent by 2020, making electric vehicles more affordable in the future.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 4.56 percent. According to Bloomberg, natural gas futures are hovering at the lowest level for this time of year since 2012. Production is surging and Texas drillers are even shooting excess gas back into older wells to deal with overproduction. The International Energy Agency (IEA) released its Gas 2019 report that estimates natural gas demand will rise 1.6 percent annually until 2024. However, that estimate is in stark contrast to growth of 4.6 percent in 2018. Hedge funds cut their net-long bets on natural gas for the week ended May 28, which was a three-year low amid falling prices.

- Copper is set for an eighth straight weekly decline as the continuing global trade war casts a shadow over demand outlooks for the red metal. Half of copper traders were neutral on the metal in the weekly Bloomberg survey. The chief commercial officer of Codelco, the world’s largest copper miner, said this week that “at the current prices, many miners are in the red, all over the world.” Another metal affected by the trade war is zinc. The metal hit a four-month low on Monday.

- In another poor week globally for oil, Brent crude fell 12 percent in the three days through Monday and sunk to under $60 per barrel. WTI crude also continued to fall this week amid growing U.S. crude inventories. WTI was trading near $53 per barrel on Wednesday.

Opportunities

- BloombergNEF reports that Europe is increasingly challenging China for supply of cobalt out of the Democratic Republic of Congo to be used in batteries. Europe-based Glencore Plc and Umicore SA entered into a long-term cobalt supply agreement where cobalt produced at Glencore operations will go to Umicore’s refineries. BNEF also forecasts that electric vehicle sales will continue to rise and hit 10 million by 2025 and 28 million by 2030, after hitting a record of 2 million sold in 2018.

- Although a poor week for oil overall, some are still bullish on the fuel further out. UBS sees a tighter market supporting crude within the next three months and predicts a rise toward $75 per barrel. Citigroup says forget the trade war and is sticking to its target of $78 per barrel in the next three months due to supply risks.

- The push for companies to become more green-friendly has expanded into the airline industry. Several airlines have made small steps such as replacing plastic stir sticks and straws with those made from sustainable materials. Delta announced that it will eliminate plastic wrap used in its in-flight amenity kits. United announced it plans to open a processing facility in Indiana to convert 700,000 tons of trash from Chicago into 33 million gallons of biofuel, which can be blended with traditional jet fuel. Airlines account for around 2 percent of annual global carbon emissions.

Threats

- Tariffs against Mexican imports, which are set to take effect on Monday if no immigration agreement is reached, could jeopardize America’s largest natural gas market. Bloomberg reports that conduits crossing into Mexico carry more than 6 percent of the natural gas produced in the U.S. and Mexico is also the second-largest importer of American gas shipped in tankers. If the tariffs go into effect, Mexico could retaliate with its own tariffs against U.S. imports.

- The threat of the rare earth metal supply being cut off to the U.S. from China also continues. China’s National Development and Reform Commission monthly meeting discussed strengthening supervision over export controls and establishing a mechanism to track and approve rare earth exports. Just hours later, the U.S. Commerce Department promised “unprecedented action” to ensure that the U.S. won’t be cut off from supplies of rare earths, which are essential components in many everyday electronics.

- According to Bloomberg Law, Canada is considering a near-total ban on agricultural uses of the chlorpyrifos pesticide. Canadian regulators are considering the ban after studies showed that the pesticide poses too high a risk for plant and animal life. Several other agencies globally are investigating the use of the pesticide. This could be negative for food prices if costs increase due to reduced use of pesticides.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 3.5 percent. The Istanbul exchange was closed most of the week in observation of Ramadan, gaining more than 4 percent in a single day of trading on Friday. Akbank gained 6.6 percent and Garanti Bank rose 6.1 percent.

- The Hungarian forint was the best performing currency this week, gaining 3 percent against the U.S. dollar. A dovish shift at the Federal Reserve pushed emerging market currencies higher, with the forint rebounding from an eight-month low.

- Communication services was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.7 percent. Greek banks corrected over the past five days after gaining 90 percent year to date. Eurobank and Alpha Bank both released weaker first-quarter results.

- Turkish lira was the worst relative performing currency this week, gaining 20 basis points against the dollar. Ongoing domestic and international geopolitical tensions continue to put pressure on the country’s currency.

- Industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- The European Central Bank (ECB) kept interest rates at a record low and reached an agreement on how to provide additional cheap cash to local banks. Rate hikes are delayed and are expected to remain on hold at least through the first half of 2020. Mario Draghi boosted inflation and growth predictions for this year, but trimmed growth forecasts and consumer price inflation (CPI) for 2020 and 2021. The ECB indicated that is ready to support the economy as growth weakens, but also noted that economic data in the region is not too bad.

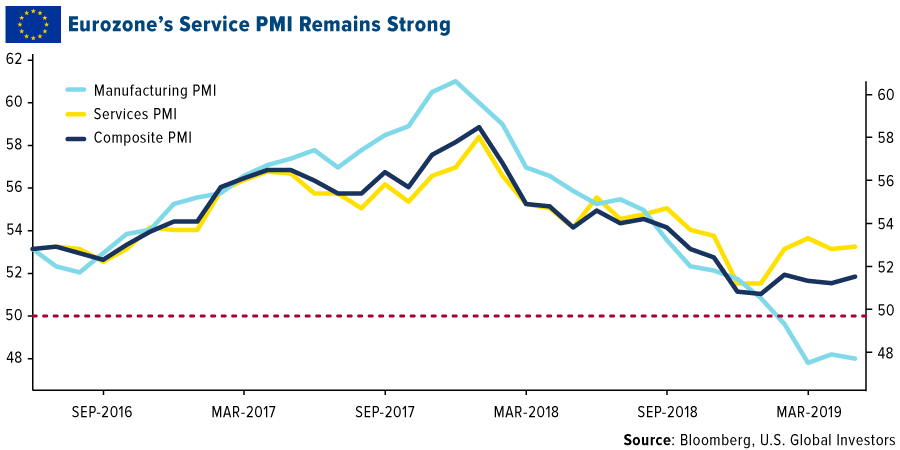

- Final Manufacturing PMI data for the eurozone came in at 47.7, below the 50 level that separates growth from expansion. Trade tensions, Brexit worries and Italy’s high debt level are putting pressure on the European manufacturing sector, but the EU’s domestic service sector remains strong. Service PMI for the eurozone was reported at 52.9, keeping the Composite PMI comfortably above the 50 level.

- A big economic event is taking place in Russia this week, with strong Chinese delegation, led by president Xi Jinping. Russia has worked with Asia to replace plunging interest from the West, and more deals between both countries are expected to be signed at the Economic Forum in St. Petersburg.

Threats

- The EU said Italy could face sanctions over high debt levels in the country. Italy’s public debt is at 2.3 trillion euros ($2.6 trillion), or 132.2 percent of Italy’s GDP- way above the 60 percent EU ceiling. Italy’s collation government is deeply divided on how to handle the country’s high level of debt. To make things worse, Italy revised its growth downward for the first quarter of this year.

- Russia’s central bank governor, Nabiullina, is ready to lower interest rates in the near future, but she also worries that it may not be enough to stimulate the economy. Foreign investment is needed in Russia to stimulate stagnating growth. However, with sanctions imposed on Russia by Western countries, foreign investments have been hampered.

- Theresa May is stepping down as a leader of the Tory party but she will remain Prime Minister of Great Britain until her replacement is found. There are 11 candidates, and Boris Johnson is among them. Johnson resigned from the cabinet in July in protest at May’s handling of Brexit. Some analysts estimate that the British pound will sell off if he gets the new prime minister post.

China Region

Strengths

- The best performing index in the region for the week was Thailand’s SET Index, which climbed 2.06 percent, while Singapore’s Straits Times Total Return Index rose 1.56 percent for the week, and Korea’s KOSPI was up 1.50 percent.

- The best performing sector in Hong Kong’s Hang Seng Composite Index since last Friday was telecommunications, which climbed 3.28 percent in the holiday-shortened week.

- The Nikkei Vietnam Manufacturing purchasing managers’ index (PMI) clocked in at 52.0.

Weaknesses

- The worst performing index in the region for the week was the Shanghai Composite, which fell by 2.26 percent in a short week of trading.

- The poorest performing sector in Hong Kong’s Hang Seng Composite Index this week was energy, which fell by 3.11 percent.

- The Caixin China Services PMI missed expectations this week, coming in at only a 52.7, well shy of analysts’ expectations for a 54.0 print and down from the prior reading of 54.5. Malaysia, Singapore and Taiwan had Nikkei PMI prints that both came in within contractionary sub-50.0 territory.

Opportunities

- The Malaysian ringgit enjoyed a bounce back this week with higher energy prices and following holiday closures on Wednesday and Thursday.

- Amid shifting supply chains and as part of the ongoing unknown factors of the U.S.-China trade spat, Vietnam’s companies are borrowing the most in six years, a recent Bloomberg News story highlighted this week. Vietnam “is likely to continue to benefit from [the] shift away from Chinese goods,” the article, entitled “Trade War Is Making Vietnam Offshore Loans Market a Winner,” stressed. The still-small loan market in Vietnam has seen dollar-syndicated loan volumes rise some 119 percent to more than $2 billion so far year to date.

- The U.S. dollar continued to weaken from its recent highs over the course of the past week, which brought some reprieve to emerging markets and which, if sustained, could help bolster emerging markets and currencies.

Threats

- The threat of U.S.-China trade war escalation continues, with obvious potential regional and global implications. Increasingly, consensus is shifting away from any near-term fix on the U.S.-China front, with tariffs accordingly then seen as more likely to stick around (with some lack of clarity perhaps also likely to stick around until we get more resolution one way or the other). U.S. President Donald Trump said he would decide on the next round of China tariffs following the upcoming G20 summit.

- On that note, the weakening of the Chinese yuan may pose another threat as Chinese officials seem to be indicating there is not necessarily any firm line in the sand on yuan levels, bringing the possibility of the yuan weakening beyond seven closer to potential reality. The offshore spot renminbi weakened enough to put in new year-to-date highs (lows), while the CNY remains at elevated levels. Of course, now if the Fed talks or allows talk of rate cuts here in the United States, we have an interesting and perhaps less one-sided situation developing then on the U.S.-China currency front. Stay tuned, but bear in mind that any severe weakening in the yuan could also cause outflow concerns, as has happened in the past.

- As part of the fallout from the ongoing trade spat, China’s threats to consider restrictions of rare earths exports—a market in which China controls more than 70 percent of critical global supply—continue to garner attention, as does the U.S. Commerce Dept.’s threat to consider “unprecedented action” should China indeed follow through.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 7 was Bitcoin 2, up 1,144.32 percent.

- Some crypto critics are changing their opinions on the digital currency, reports Ethereum World News, including Agustin Carstens, the General Manager at the Bank for International Settlement (BIS). At a conference on technology-enabled disruption, Carstens said “digital assets might have room as part of financial assets, but not as a cash substitute.” As the article explains, this is the first instance that the BIS general manager is casting bitcoin and other digital currencies in a positive light.

- Walmart is continuing to expand in the blockchain industry by coining a new consortium, reports Forbes. The retail giant has joined MediLedger, a consortium building and blockchain solution for tracking the provenance of pharmaceuticals.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 7 was Plus-Coin, down 89.83 percent.

- In one of the most high-profile cryptocurrency crackdowns yet, a $100 million lawsuit has been filed by the Securities and Exchange Commission (SEC) against social-media startup Kik Interactive, reports CNBC. Allegedly Kik, which launched a digital currency to be traded within its messaging app, conducted an illegal securities offering.

- “Bitcoin is again feeling the pull of gravity amid a rally in gold – a classic safe-haven asset,” writes CoinDesk. The popular digital currency corrected from a high near $9,100 on May 30 to a two-and-a-half week low of $7,432 on June 4. The correct is noteworthy, as it is accompanied by a sharp rally in the price of gold, as seen in the chart below. The two assets share an inverse relationship since the final quarter of 2018.

Opportunities

- One blockchain entrepreneur wants to change legendary investor Warren Buffet’s mind regarding cryptocurrency, reports CNBC. On Tuesday, Justin Sun, founder of cryptocurrency Tron and CEO of file-sharing company BitTorrent, told the news outlet that he paid $4.57 million for a three-hour lunch in which he invited Buffett. “I want him to learn what the younger generations are doing,” explained Sun, who added that he is a fan of Buffett’s long-term value investing strategy and wants to pay him “back for his inspiration.”

- In one of the biggest developments yet in an effort to make use of blockchain technology, a group of financial firms led by UBS plans to start using a bitcoin-like token to settle cross-border trades, writes the Wall St. Journal. The 14 firms have collectively invested $63.2 million in the new company that will control development of the token, called the utility settlement coin, or USC.

- In testimony to the U.S. House Ways and Means Committee on June 4, Congressman Ted Budd highlighted two bills he hopes will receive bipartisan support, writes CoinDesk. The bills are the Cryptocurrency Tax Fairness Act and the Virtual Value Tax Fit of 2018. Budd referred to the development and protection of the domestic blockchain industry an issue of national security during his speech.

Threats

- Bitcoin’s price pullback appears to have stalled near historically strong support, reports Coindesk, and if a bounce takes place, it could be shallow. The popular coin is attempting recovery from the 30-day moving average, consistently reversing price pullbacks in the last four months. This time, however, bitcoin is more likely to end up creating a bearish lower high, the article explains, or may find acceptance below the average in the next day or two.

- Poloniex revealed Thursday that lenders in its bitcoin margin lending pool suffered a loss of roughly $13.5 million due to a flash crash in the Clams market on May 26, reports CoinDesk. The margin-tradable Clams market dropped by nearly 77 percent in value in 45 minutes on the crypto exchange, which caused a flurry of liquidations designed to cut losses in order to repay the lender, the article explains. “However, the speed and magnitude of the crash were too severe for Poloniex’s automatic liquidation system to function properly in the illiquid market,” Coindesk continues.

- On Wednesday, June 19, a bit of bitcoin fanfare will die, writes Bloomberg. This is the date that signifies the last bitcoin futures contract on the Cboe Global Markets Inc. will settle, with no more to follow. In an emailed statement, Cboe spokeswoman Suzanne Cosgrove said the group “is assessing its approach with respect to how it plans to continue to offer digital asset derivatives for trading, but we have nothing new to announce at this time.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 199.40 | +8.95 | +4.70% |

| Gold Futures | 1,345.20 | +34.10 | +2.60% |

| Natural Gas Futures | 2.34 | -0.12 | -4.69% |

| S&P/TSX VENTURE COMP IDX | 596.54 | -5.01 | -0.83% |

| 10-Yr Treasury Bond | 2.08 | -0.04 | -2.02% |

| Nasdaq | 7,742.10 | +288.95 | +3.88% |

| Oil Futures | 54.10 | +0.60 | +1.12% |

| Hang Seng Composite Index | 3,593.77 | -7.03 | -0.20% |

| S&P 500 | 2,873.34 | +121.28 | +4.41% |

| DJIA | 25,983.94 | +1,168.90 | +4.71% |

| Korean KOSPI Index | 2,072.33 | +30.59 | +1.50% |

| Russell 2000 | 1,514.39 | +48.90 | +3.34% |

| S&P Energy | 449.69 | +17.59 | +4.07% |

| S&P Basic Materials | 359.20 | +29.88 | +9.07% |

| XAU | 74.33 | +4.31 | +6.16% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.34 | -0.27 | -10.38% |

| S&P/TSX Global Gold Index | 199.40 | +19.54 | +10.86% |

| 10-Yr Treasury Bond | 2.08 | -0.40 | -16.18% |

| Oil Futures | 54.10 | -8.02 | -12.91% |

| Gold Futures | 1,345.20 | +57.80 | +4.49% |

| S&P 500 | 2,873.34 | -6.08 | -0.21% |

| S&P Energy | 449.69 | -21.26 | -4.51% |

| Hang Seng Composite Index | 3,593.77 | -268.89 | -6.96% |

| DJIA | 25,983.94 | +16.61 | +0.06% |

| Korean KOSPI Index | 2,072.33 | -95.68 | -4.41% |

| Nasdaq | 7,742.10 | -201.22 | -2.53% |

| S&P Basic Materials | 359.20 | +16.03 | +4.67% |

| Russell 2000 | 1,514.39 | -60.58 | -3.85% |

| S&P/TSX VENTURE COMP IDX | 596.54 | -1.71 | -0.29% |

| XAU | 74.33 | +5.99 | +8.76% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.34 | -0.53 | -18.39% |

| 10-Yr Treasury Bond | 2.08 | -0.56 | -21.14% |

| DJIA | 25,983.94 | +510.71 | +2.00% |

| Oil Futures | 54.10 | -2.56 | -4.52% |

| S&P 500 | 2,873.34 | +124.41 | +4.53% |

| Gold Futures | 1,345.20 | +46.20 | +3.56% |

| S&P Energy | 449.69 | -29.44 | -6.14% |

| Nasdaq | 7,742.10 | +320.64 | +4.32% |

| Korean KOSPI Index | 2,072.33 | -93.46 | -4.32% |

| S&P Basic Materials | 359.20 | +18.30 | +5.37% |

| Russell 2000 | 1,514.39 | -9.24 | -0.61% |

| Hang Seng Composite Index | 3,593.77 | -292.54 | -7.53% |

| S&P/TSX Global Gold Index | 199.40 | +9.32 | +4.90% |

| S&P/TSX VENTURE COMP IDX | 596.54 | -18.67 | -3.03% |

| XAU | 74.33 | +0.70 | +0.95% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Turkiye Garanti Bank

Alpha Bank

Delta Air Lines Inc

United Continental Holdings

American Airlines Group Inc

Lundin Gold Inc

PolarX Ltd

TriStar Gold Inc

Royal Gold Inc

Chakana Copper Corp

Gold Fields Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Consumer Comfort Index is a weekly, random-sample survey tracking Americans’ views on the condition of the U.S. economy, their personal finances and the buying climate. The ISM manufacturing composite index is a diffusion index calculated from five of the eight sub-components of a monthly survey of purchasing managers at roughly 300 manufacturing firms from 21 industries in all 50 states. The Bangkok SET Index is a capitalization-weighted index of all the stocks traded on the Stock Exchange of Thailand. The Straits Times Index comprises the top 30 SGX Mainboard listed companies on the Singapore Exchange selected by full market capitalization. The relative strength index (RSI) is a momentum indicator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset.