Wheels Up! Economic Recovery Could Be Faster Than Expected

Date Posted: May 29, 2020

Read time: 52 min

NULL

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Sometimes it can be challenging to remain optimistic, to look past the never-ending raft of negative headlines and see the upside.

This past week was no exception.

The number of COVID-19 deaths in the U.S. exceeded 100,000, a significant toll, with cases continuing to climb in new hot spots.

Meanwhile, political and racial tensions are running high. Violent protests erupted in Minneapolis in response to alleged police brutality. The incident also led to an escalation of the ongoing feud between Twitter and President Donald Trump, when Twitter blocked one of the president’s tweets for violating its rule about “glorifying violence.”

And across the Pacific, protests resumed in Hong Kong following China’s passage of a national security law that, among other things, enables Chinese law enforcement officials to operate within the special administrative region. The U.S. State Department announced that it no longer considers Hong Kong to have reasonable autonomy under Chinese rule.

You get the idea.

As troubling as these developments are, it’s important not to lose sight of the good that appears to be taking place right now. Investors that focus only on the negative tend to miss out on the opportunities.

Record Inflows into Airline Stocks

Consider airlines. Shares of commercial carriers flew up 10 percent on Tuesday on renewed hopes that a vaccine against the novel coronavirus can be developed as soon as year-end.

Dr. Anthony Fauci, the leading U.S. expert on infectious diseases, shared his outlook on Wednesday, telling CNN that “we have a good chance… that we might have a vaccine that would be deployable by the end of the year, by December and November.”

Airline stocks, as measured by the NYSE Arca Airline Index, are still down some 57 percent from their trading range soon before travel restrictions grounded flights. This, I believe, represents the greatest buying opportunity in airline stocks since at least 9/11.

Indeed, we’ve been seeing record daily inflows into airline equities in the two months since bookings began to make their recovery. As of May 29, positive inflows had found their way into airlines for a remarkable 62 straight days, according to Eric Balchunas, senior ETF analyst at Bloomberg.

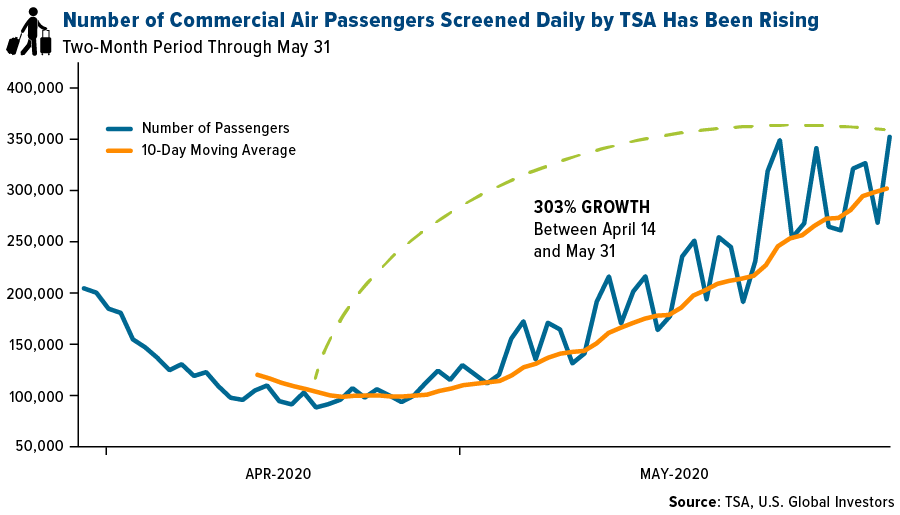

The number of passengers screened daily in the U.S. by the Transportation Security Administration (TSA) has steadily been gaining momentum since carriers were first grounded in an effort to limit the spread of the pandemic. On May 22, as many as 348,673 people boarded commercial flights in the U.S., up nearly 300 percent from a low of 87,534 people on April 14, and well above the 10-day moving average.

Some carriers have begun to announce plans to expand routes. In a press release dated May 28, Southwest Airlines said it would resume some flights to Mexico and the Caribbean on July 1, and by the fall would add “more frequencies and more nonstop flight options” for business travelers from Phoenix, Denver, Las Vegas and Nashville. Effective December 17, Southwest will introduce several new nonstop links, including Phoenix and Memphis, Denver and Birmingham, and Atlanta and Louisville.

Deutsche Bank recently gave Southwest a Buy rating as bookings for the Dallas-based carrier are once again outpacing cancellations—and much sooner than previously anticipated. What’s more, revenues look better-than-expected, with load factors running at between 25 percent and 30 percent, quite a bit higher than the forecast 5 percent to 10 percent, according to Deutsche.

Some airlines are so (cautiously) optimistic about a quick rebound in air travel that they’re leaving the Trump administration’s $29 billion in pandemic relief aid untapped—for now. Bloomberg reports that of the four big carriers, only American Airlines has so far said it would be borrowing from the pool of funds, which comes with strings attached. The other three are taking a wait-and-see approach, hoping the summer travel season will encourage travelers to return to the skies. Wheels up!

Trucking Rally Could Be Telegraphing a Faster-Than-Expected Recovery

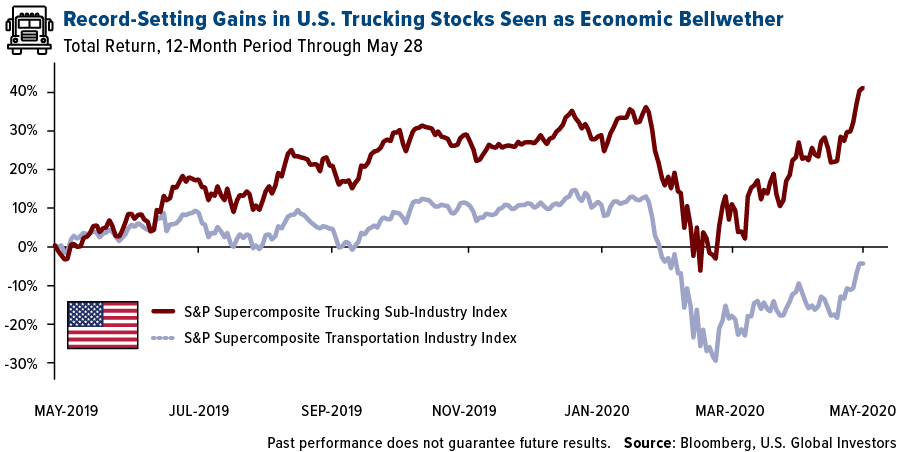

It isn’t just airlines that are telegraphing a faster-than-expected recovery. Shares of domestic trucking companies have been on a tear, notching all-time highs in two of the past three trading days. Leaders have been Avis Budget (up 31.3 percent from a month ago), Saia Inc. (up 27.5 percent) and Old Dominion Freight Line (up 16.5 percent).

In the past, trucking stocks—and transport stocks in general—have been seen as an economic bellwether since they reflect changes in overall business activity.

According to Matt Maley, chief market strategist at Miller Tabank & Co., the rally in trucking stocks tells us that “the economy is going to bounce back in a much stronger way” than many are anticipating. For the 12-month period, the S&P Supercomposite Trucking Sub-Industry Index was up nearly 40 percent, far outperforming the broader Transportation Industry Index, down 6 percent through May 28.

China to Operate More Flights Than the U.S. for the First Time Ever

Improvements in economic conditions are also happening elsewhere. Countries are finally beginning to reopen, including China, where the novel coronavirus originated.

In fact, China’s economy appears to have reopened the most of any other major Asian country. A report by Brown Brothers Harriman (BBH) indicates that China is closest to returning to normal, considering a number of important factors. In the five-point graph below, you can see that China is ranked number one in school openings, removing penalties/fees and allowing non-essential businesses to open. The country also ranks highly in borders and social distancing.

“A structure has been put into place for the tracing of the virus, and China seems well in control over the pandemic,” BBH analysts write.

Most surprising is that China’s domestic carriers are on track to operate more flights than American carriers for the first time ever this month, according to Bloomberg. Airlines in China are reportedly flying 65 percent of normal capacity, compared to around 26 percent in the U.S.

Wheels up!

Interested in learning more about investing in airlines in the age of COVID-19? Register for our FREE webinar, taking place June 17 at 1:00 Central time, by clicking on the banner below!

Gold Market

This week spot gold closed at $1,731.71, down $2.97 per ounce, or 0.17 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.31 percent. The S&P/TSX Venture Index came in up 3.05 percent. The U.S. Trade-Weighted Dollar fell 1.55 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-25 | Hong Kong Exports YoY | -4.50% | -3.70% | -5.80% |

| May-26 | New Homes | 480k | 623k | 619k |

| May-26 | Conference Board Consumer Confidence | 87 | 86.6 | 85.7 |

| May-28 | Germany CPI YoY | 0.60% | 0.60% | 0.90% |

| May-28 | Durable Goods Orders | -19.00% | -17.20% | -16.60% |

| May-28 | GDP Annualized QoQ | -4.80% | -5.00% | -4.80% |

| May-28 | Initial Jobless Claims | 2100k | 2123k | 2446k |

| May-29 | Eurozone CPI Core YoY | 0.80% | 0.90% | 0.90% |

| May-31 | Caixin China PMI Mfg | 49.6 | — | 49.4 |

| Jun-1 | ISM Manufacturing | 43.5 | — | 41.5 |

| Jun-3 | ADP Employment Change | -9500k | — | -20236k |

| Jun-3 | Durable Goods Orders | — | — | -17.20% |

| Jun-4 | ECB Main Refinancing Rate | 0.00% | — | 0.00% |

| Jun-4 | Initial Jobless Claims | — | — | 2123k |

| Jun-5 | Change in Nonfarm Payrolls | -8000k | — | -20537k |

Strengths

- The best performing precious metal for the week was silver, up 3.78 percent on stronger industrial demand. After a slow start to the week, gold and silver were moderately higher in midday U.S. trading Thursday as haven demand returned due to China’s security law imposition on Hong Kong. The move by China ratcheted up tensions with the U.S. Gold rose Friday morning as investors awaited President Trump’s news conference to announce his China response. Broader equity markets have been somewhat euphoric on the immediate fear-of-missing-out hope for a COVID-19 vaccine. However, with little mention in the news, American investors cannot get enough gold. Swiss gold exports to the U.S. surged to 111.7 tons in April – the most on record.

- The annual “In Gold We Trust” report was published by Incrementum AG this week and it was filled with bullish expectations for gold. Fund managers and authors of the report Ronald-Peter Stoeferle and Mark Valek wrote that gold could approach $5,000 an ounce and possibly even push toward $9,000 an ounce by 2030. “The proprietary valuation model shows a gold price of $4,800 at the end of this decade, even with conservative calibration.” Kitco News notes that in the 2019 report, they accurately predicted that gold was in the early stages of a new bull market.

- New data out of Russia shows that gold production rose by 9.26 percent in 2019 for a total of 343.54 metrics tons, compared to 314.42 in 2018. Russia is the third-largest gold producer in the world. In April, Russian banks asked the Russian central bank to restart its official gold purchases, citing concerns over gold exports. Silver production was down 11.1 percent on an annual basis in 2019, totaling 996.17 tons, reports Kitco News.

Weaknesses

- The worst performing precious metal for the week was palladium, down 1.16 percent. Gold fell for a third straight day as of Wednesday as signs of improvement in some economies rolled back haven demand and offset concerns about growing U.S.-China tensions over Hong Kong. Gold fell toward $1,700 an ounce on strong economic data from China, but then finished the week around $1,731.

- Sibanye-Stillwater, the world’s largest platinum producer, said that it tested 120 employees for COVID-19 and 51 tested positive for the virus. The company used contact-tracing to identify who needed to be tested after two employees at Rustenburg operations in South Africa contracted the virus. Coronavirus outbreaks at mining operations could halt production and result in reduced output.

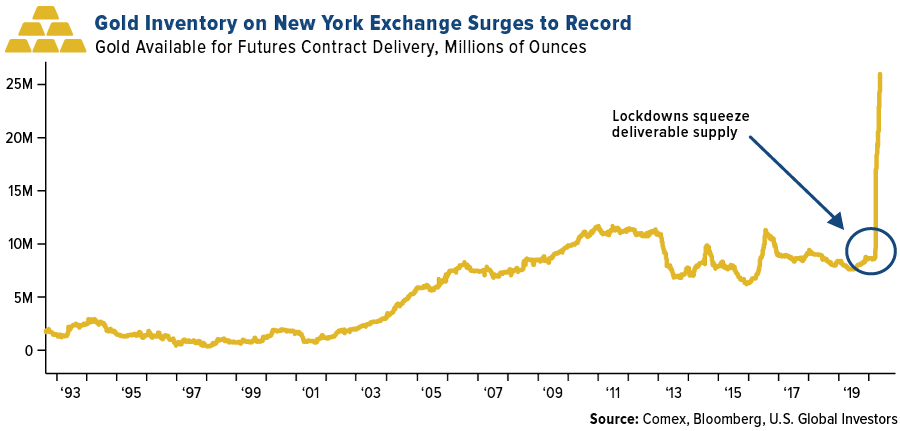

- The New York gold market is continuing to create headaches for traders. After the coronavirus pandemic grounded flights and created concern about physical delivery, gold futures rose to the highest premium to the spot price in four decades and attracted a flood of the metal to the U.S. Now contract holders are trying to avoid taking delivery from the massive inventory reports Bloomberg. This is like what happened with oil earlier this year, where demand plunged after stockpiles rose. The June gold contract is now below spot prices, just after seeing a $12 premium in mid-May and a $60 premium in March. New York exchange inventories stood at a record 26.3 million ounces as of Wednesday. Since the end of March, more than 17 million ounces have flowed into Comex.

Opportunities

- Gold miners in Australia are resuming a pandemic-disrupted exploration boom as metal prices surge amid a lack of new major discoveries. According to government estimates, spending on gold exploration in the country rose to a new record in the fourth quarter of 2019, while the annual total of more than $656 million was 20 percent higher than 2018. S&P Global Market Intelligence said in a report this month that there have been no major gold discoveries in the past three years. Rob Bills, CEO of Emmerson Resources Ltd., said “the cost of drilling hasn’t gone up, and there’s plenty of drill rigs out there, the market is quite responsive to discoveries, we’re quite positive.”

- Shandong Gold Mining plans to set up Streamers Gold Mining Corp. in Toronto to complete the purchase of TMAC Resources, according to a statement on the Shanghai Stock Exchange. The gold miner could invest C$210 million to set up a unit in Canada. Bloomberg News reports that on May 8, TMAC Resources said Shandong agreed to acquire all outstanding shares.

- Gold is known as a store of value and it has been providing a vital lifeline worldwide to those devastated by the economic impact of COVID-19. In Thailand, gold exports rose 830 percent from the same month a year earlier to 48 tonnes. This was also a 90 percent increase from March, as people sell their gold to get a hold of cash, reports Kitco News. Last month Thailand’s Prime Minister even asked people to sell gold gradually as shops could not handle the large volumes of sellers.

Threats

- Gold has seen its rally losing steam over the past month potentially due to rising real yields. Bloomberg’s Sungwoo Park notes that real yields are increasing in large economies such as the U.S., China and Japan, as inflation fell while sovereign yields rose. “That reduces the opportunity cost of holding no-yielding gold.” Other headwinds include improving risk appetite as more and more economies globally re-open as coronavirus restrictions are lifted.

- South Africa’s mines have been operating with half their workforce since a five-week shutdown ended at the beginning of May and starting on Monday all workers can return. However, there are questions surrounding how workers will be able to safely social distance in cramped mining conditions. The country has seen virus flare-ups temporarily closing individual operations, which could curb output and hurt profitability, reports Bloomberg. RMB Morgan Stanley analysts said in a note that “we could see a reset in South African mine production capacity lower, even once government mandated employment restrictions have been lifted.” Impala Platinum Holdings said that it takes between four and five hours to get tens of thousands of workers underground as screenings and health protocols slow the start of their morning shift.

- Cleveland Federal Reserve Bank President Loretta Mester cautioned that the economic recovery from the COVID-19 pandemic could be slow on a Bloomberg TV interview this week. “When we have so many people out of work it’s hard to imagine that we see a quick V-shaped recovery.”

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.75 percent. The S&P 500 Stock Index rose 3.01 percent, while the Nasdaq Composite climbed 1.77 percent. The Russell 2000 small capitalization index gained 2.84 percent this week.

- The Hang Seng Composite gained 1.21 percent this week; while Taiwan was up 1.21 percent and the KOSPI rose 3.02 percent.

- The 10-year Treasury bond yield fell 1 basis point to 0.652 percent.

Domestic Equity Market

Strengths

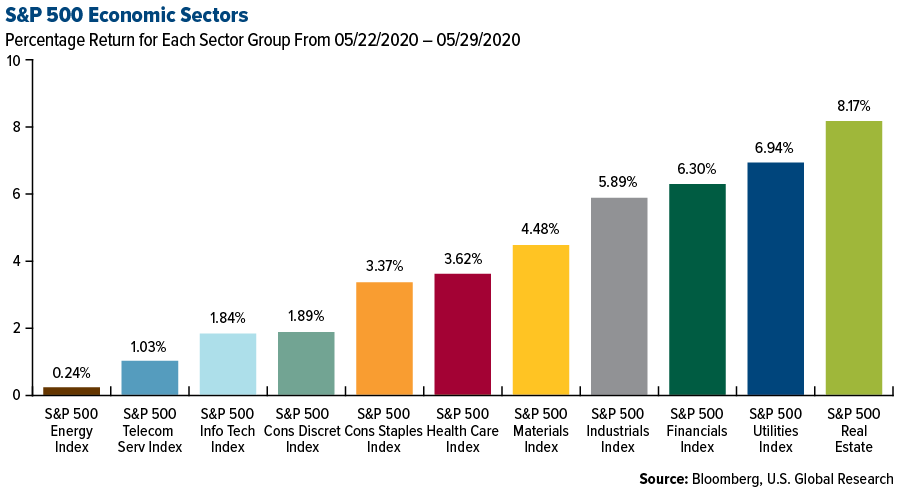

- Real estate was the best performing sector of the week, increasing 8.17 percent compared to an overall increase of 3.30 percent for the S&P 500.

- Dollar Tree was the best performing S&P 500 stock for the week, increasing 20.50 percent.

- American Tower and Crown Castle rose Friday after Oppenheimer’s Timothy Horan upgraded the stocks to outperform from perform, citing “strong/accelerating demand from carriers.” Mobile broadband is “more important now than ever,” he wrote in a note. He expects a meaningful rebound in tower activity from combined T-Mobile/Sprint this year, Dish buildouts, strong Verizon spend and rural fixed wireless, aided by government subsidies. He added that multiple 5G-build channel checks this week confirm his bullish view.

Weaknesses

- Energy was the worst performing sector for the week, increasing 0.24 percent.

- Noble Energy was the worst performing S&P 500 stock for the week, falling 13.05 percent.

- Billionaire investor Carl Icahn sold his 39 percent stake in Hertz at an almost $2 billion loss on Tuesday after the car-rental giant filed for bankruptcy last week.

Opportunities

- U.S. lawmakers are pushing through legislation to speed up broadband funding after the coronavirus exposed a lack of access in rural areas. Senior lawmakers have proposed a $16 billion bill to speed up broadband infrastructure funding by the Federal Communication Commission (FCC), the Wall Street Journal reported.

- Apple has bought machine learning startup Inductiv to improve data used in Siri. Inductiv, from Ontario, Canada, will work on machine learning and data science for Apple and is the latest in a string of AI acquisitions from the iPhone maker in recent years, Bloomberg reported.

- Amazon is reportedly in talks to buy secretive self-driving car company Zoox for less than $3.2 billion. Amazon is in late-stage discussions to acquire secretive self-driving car company Zoox, according to the Wall Street Journal.

Threats

- Nearly two-thirds of publicly traded restaurants are at risk of bankruptcy as the Covid-19 pandemic batters the industry, according to a new study. The concern is higher for small companies and restaurants that specialize in dine-in, consulting firm Aaron Allen & Associates said in an analysis. It identified Bloomin’ Brands Inc., Potbelly Corp. and Chili’s owner Brinker International Inc. among those at greater risk.

- Trump signed an executive order threatening social media companies after Twitter fact-checked his tweets. The move comes two days after Twitter fact-checked two of Trump’s tweets pushing false claims about voting by mail.

- Renault to take 3.6 billion euro hit from Nissan losses. French carmaker Renault said on Thursday that losses at its Japanese partner Nissan, in which it has a 43 percent stake, would drag on its on net earnings by 3.6 billion euros ($3.96 billion) in the first quarter.

The Economy and Bond Market

Strengths

- Sales of newly-built single-family houses occurred at a seasonally-adjusted annual rate of 623,000, the government reported Tuesday. That was 0.6 percent above the revised pace of 619,000 in March, writes MarketWatch.

- Consumer sentiment rose to a final reading of 72.3 in May from a final April level of 71.8, according to reports on the University of Michigan gauge released Friday.

- Despite the widespread business and health challenges brought on by the COVID-19 pandemic, two-thirds of American business leaders are optimistic the U.S. economy will make a full recovery within the next year, according to a new survey from professional services firm TMF Group. “It’s an encouraging sign that business leaders in the U.S. are expressing this type of optimism, particularly based on the unprecedented challenges experienced throughout the economy over the last few months,” said Larry Harding, TMF Group’s head of North America.

Weaknesses

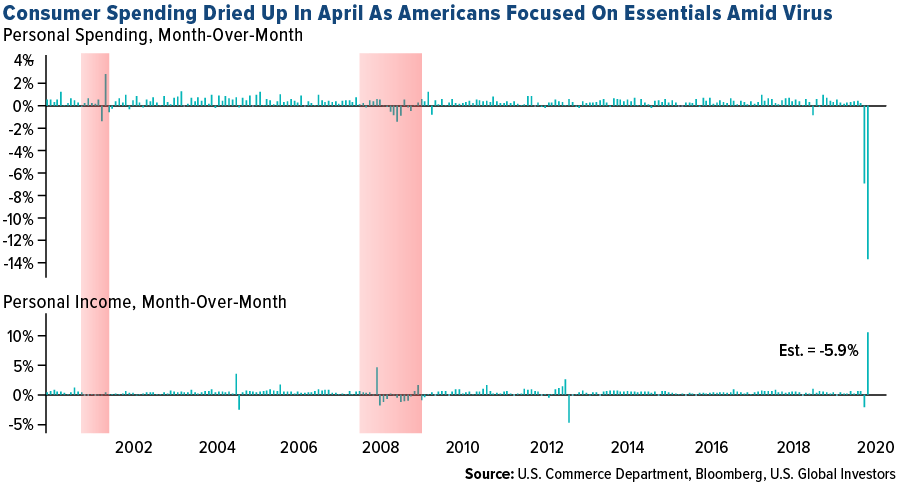

- Consumer spending plunged 13.6 percent in April — the most on record — after the coronavirus pandemic halted purchases of all but the most essential goods and services, according to a Commerce Department report Friday. Incomes, on the other hand, posted a record 10.5 percent increase thanks to relief payments distributed under the CARES Act. With the drop in spending, the personal savings rate jumped to a record 33 percent from 12.7 percent.

- The U.S. economy shrank at an even faster pace than initially estimated in the first three months of this year, writes CNBC, with economists continuing to expect a far worse outcome in the current April-June quarter. The Commerce Department reported Thursday that the gross domestic product fell at an annual rate of 5 percent in the first quarter, a bigger decline than the 4.8 percent drop first estimated a month ago.

- More than 2.1 million Americans filed for unemployment benefits for the first time last week, the 10th straight week that jobless claims have been in the millions as the coronavirus continues to cripple the economy. The total number of people who have sought unemployment assistance now stands at more than 40 million since the crisis began in mid-March, reports NBCnews.com.

Opportunities

- The Federal Reserve’s weekly balance sheet update showed its holdings of exchange-traded funds continued to grow over the past week, and added a line item for another emergency lending program for state and local government borrowers, known as the Municipal Liquidity Facility, which has yet to launch. “On May 26, 2020, the Federal Reserve Bank of New York received Treasury’s equity contribution for the MLF program,” the explanatory note said.

- Governor Andrew Cuomo said his administration will now focus on reopening New York City, the only state region still on lockdown, reports Bloomberg. The economy will need government help to bounce back, Cuomo said, so the state plans to fast-track its plan to rebuild Penn Station while “ridership is low and while we need the jobs.”

- Junk and lower-rated municipal bonds offer value while high-grade state and local debt has gotten expensive, according to Barclays strategists led by Mikhail Foux. “Although high quality spreads have become rich, we see the real value is in trading down in credit quality as both BBBs spreads and HY bonds have lagged the rally,” they wrote.

Threats

- The coronavirus pandemic is messing with how economic data is produced, and making it hard to work out how badly it’s hitting the global economy, the International Monetary Fund said this week.

- Governments and central banks have made significant headway with their responses to battle the coronavirus pandemic, but an "all in" approach could backfire, according to Mohamed El-Erian, chief economic adviser at Allianz.

- New Jersey may have to cut half the state’s 400,000 public employees if the federal government doesn’t help make up a $10.1 billion revenue shortage through June 2021, Governor Phil Murphy said.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, up 5.77 percent after Indonesia announced it will keep its export tax at zero for third month in June. Hydrogen companies have had a strong 2020 so far as the clean energy gains popularity. England’s ITM Power Plc has gained 290 percent this year, Norway’s Nel ASA is up 70 percent and France’s McPhy Energy SA is up around 50 percent, according to Bloomberg. “There’s greater recognition that hydrogen is fairly core to achieve our decarbonization agendas going forward,” said Marc Elliott an analyst at Investec Securities Ltd, ITM’s corporate broker. “It could be bigger than the natural gas industry.”

- Home builders have help up surprisingly well during the pandemic. An S&P index of homebuilders has nearly doubled since cratering on March 23 and is now down less than 2 percent for the year. New home sales posted a surprise gain in April and homebuilder stocks have surged in recent weeks, reports Bloomberg. “Housing has followed V shaped recovery, no questions asked — as quickly as it fell, it’s coming back,” said Ali Wolf, chief economist at Meyers Research. “We’re all doing pretty well right now and we’re all, quite frankly, very surprised,” said Lee Whitaker, vice presidents of Pacesetter Homes, a small Texas builder.

- Oil futures in New York rose 2.7 percent on Thursday despite U.S government data showing that American crude stockpiles rose last week. The demand outlook for fuel is improving as the four-week average of gasoline supplied to the market has steadily risen as lockdown measures are eased. OPEC members Nigeria and Algeria both lifted official selling prices for their supply – a sign that they believe customers are willing to pay more for their barrels. Output cuts have started to chip away at the massive oversupply and U.S. oil output will reach a low point of 10.7 million barrels a day in June. Bloomberg notes that the fuel has surged around 80 percent in May as of Wednesday. The commodity finished the week up 5.65 percent.

Weaknesses

- The worst performing major commodity for the week was coffee, down 7.05 percent due to lower demand from coffee shops during coronavirus-induced lockdowns. Bloomberg reports that the SEC and CFTC have both opened investigations into the $4.64 billion United States Oil Fund (USO) that lost 75 percent of its value in the two months ended April 30. The regulators are probing whether the fund’s risks were properly disclosed to investors. USO is a popular ETF that uses complex derivatives to track oil.

- The International Wrought Copper Council said that global copper demand is forecast to fall 5.4 percent to 22.625 million tons in 2020. However, they do expect demand to bounce back 4.4 percent in 2021 along with a strong rebound in production.

- Natural gas flows from Russia, Europe’s biggest supplier, through Belarus and Poland to Germany fell to zero on Tuesday after a sharp price decline on Sunday. Bloomberg notes that shipments via the Yamal-Europe pipeline into Austria fell by 25 percent from its 10-day average. “Such a significant reduction in gas transit is primarily driven by weak demand in Europe amid warm winter, high levels of gas in underground storage and demand distortion due to Covid-19,” VTB Capital said in a note.

Opportunities

- Sibanye-Stillwater CEO Neal Froneman said the company will enter the battery space in “due course” and that combustion engines, which use platinum-group metals, will still be used for many years to come. Froneman said in a Kitco interview this week that “part of our strategy is to enter the battery electric metals space in due course, but from a PGM perspective, the gasoline internal combustion engine has a good 10 years in front of it.”

- Trafigura is planning a major increase in renewable-energy investments over the next half-decade. The group wants to add 2 GW of renewable energy assets to its portfolio by 2027, up from about 350 MW now. Tokyo Gas Co. Ltd, a Japanese natural gas producer, made a $22 million investment in developer of floating platforms for wind turbines Principle Power Inc. This is another sign that fossil fuel companies are continuing to shift their investments toward renewable energy, reports Bloomberg Green.

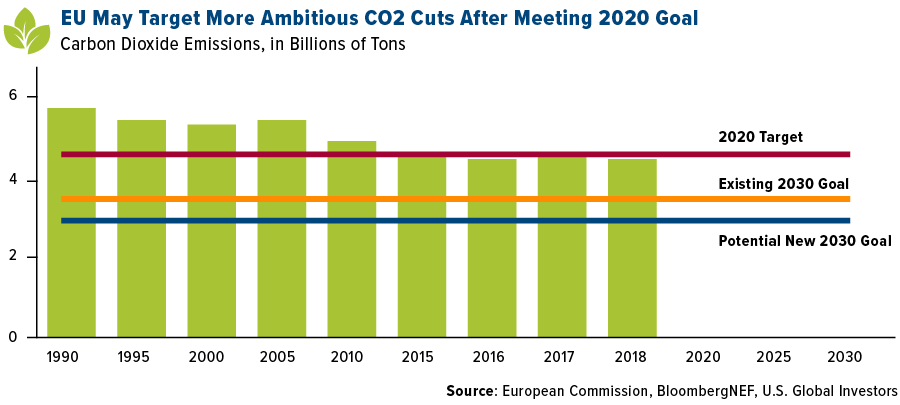

- A $824 billion economic recovery plan was unveiled by the European Commission this week, and one of its key pillars is meeting climate-neutrality goals, reports Bloomberg. The stimulus program aims to accelerate the transition to clean transportation, increase energy savings and boost renewable energy production. The EU has already hit its 2020 target for reduced CO2 emissions, leading some to speculate that they could set even more ambitious cuts. “Member states will design national recovery plans, with the twin green and digital transition at their heart and they will be assessed accordingly,” said EU Commission Executive Vice-President Frans Timmermans.

Threats

- The coronavirus pandemic has weakened demand for electric vehicles and could spell long-term trouble for lithium and other battery metal producers. Seth Goldstein, a lithium industry analyst at Morningstar, said “the pandemic further kicks the EV can down the road.” Morningstar began the year with expectations that global demand for lithium would rise 15 percent, but now expects a 5 percent drop in demand for 2020. Abermarle Corp slowed expansion projects in Chile and Australia, Tianqi Lithium Corp is hurt by debt and is selling its controlling stake in the world’s largest lithium mine and SQM said it could shelve expansion plans for next year, according to Kitco News.

- Farmers are reporting more and more COVID-19 infections among workers just ahead of the peak summer produce season. Bloomberg notes that all the nearly 200 employees at a farm in Tennessee tested positive, 50 workers had the virus at a farm in New Jersey and almost 170 workers were infected at a tomato and strawberry greenhouse in New York. There could be labor shortages, which spells trouble for produce shelves as certain summer crops like berries have a very short life span.

- The mounting U.S.-China tensions after China imposed national security legislation on Hong Kong this week could threaten U.S energy. China is already behind on its promise to buy $52 billion worth of American oil, gas and other energy products. According to trade data from March and April, “China could be well short of its purchasing obligations for politically important agriculture products and energy goods,” writes ClearView Energy Partners. The U.S. added 33 Chinese entities to a trade blacklist and declared that Hong Kong no longer warrants special treatment under American law.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 4.8 percent. The country’s central bank unexpectedly cut its main rate for the third time in a row to 10 basis points from 50 basis points. Jastrzebska Spolka Weglowa (JSW), a coking coal producer, was the best performing equity trading on the Warsaw Stock Exchange despite the ongoing outbreak of the coronavirus among its employees, gaining 28 percent over the past five days.

- The Polish zloty was the best performing currency this week, gaining 3.3 percent. The zloty advanced despite the central bank unexpectedly cutting rates on Thursday. Poland reported better-than-expected first-quarter growth of 2 percent versus 1.9 percent. Inflation declined in May to 2.9 percent year-over-year, slightly below expectations of 3 percent.

- Consumer discretionary was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst relative performing country this week, gaining 94 basis points. As of Friday morning, Russia reported 387,623 COVID-19 cases, the third largest number in the world after the U.S. and Brazil. Nearly half of the reported cases in Russia come from Moscow, the nation’s capital, with a population of 13 million. Polymetal International, a gold producer, was the worst performing equity among stocks trading in the Vaneck Russia ETF, losing 4 percent over the past five days.

- The Turkish lira was the worst performing currency in the region this week, losing 10 basis points. Turkey reported growth of 4.5 percent in the first quarter on a year-over-year basis, below the expected 4.9 percent and prior quarter’s GDP of 6 percent. Trade balance deficit reached $4.6 billion in April versus the expected $4 billion. Turkey raised the tax on individual foreign currency purchases to 1 percent from 0.2 percent.

- Energy was the worst performing sector among eastern European markets this week.

Opportunities

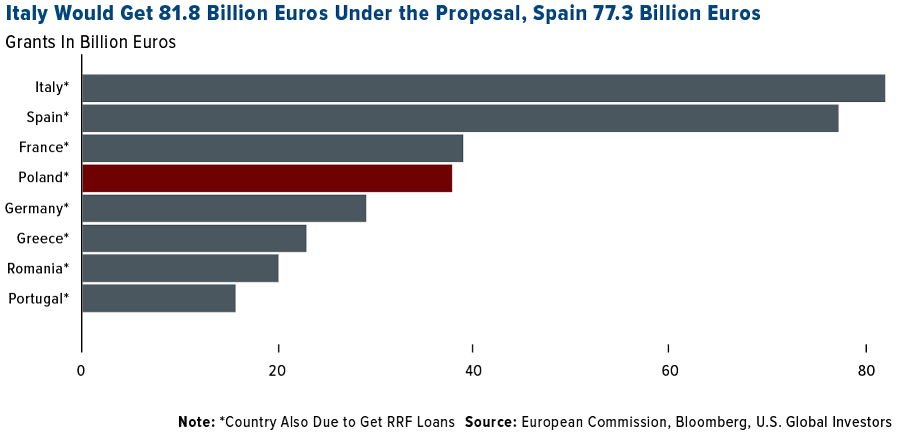

- The European Union proposed 2.4 trillion ($2.6 trillion) in total stimulus to fight effects of the pandemic. This week the EU officially proposed a 750 billion euros joint debt issuance. 500 billion is planned to be distributed by grants and the remaining 250 billion will be distributed in the forms of loans. Poland will be the fourth largest recipient of the recovery fund, followed by Italy, Spain and France.

- More restrictions are being lifted across Europe as the number of reported COVID-19 cases continues to decline. Restaurants, bars, cafes, hair salons and shops have been allowed to reopen in Italy, providing social distancing is enforced. In Poland, beauty salons, hairdressers, restaurants and cafes reopened as well. In Spain, cinemas, museums and theatres are opening at reduced capacity. The famous Acropolis reopened in Greece. Germany plans to ease social distancing steps from June 29, a week earlier than previously planned, and aims to lift a travel warning for 31 European countries from mid-June.

- Magnitogorsk Iron and Steel Works (MMK) took third place in the 2020 Value Creators ranking, published by the international consulting company Boston Consulting Group (BCG). The ranking evaluates the world’s leading companies by total shareholder return (TSR) generated over the past five years (from 2015-2019). MMK is the leader among Russian steel companies with a 40 percent TSR.

Threats

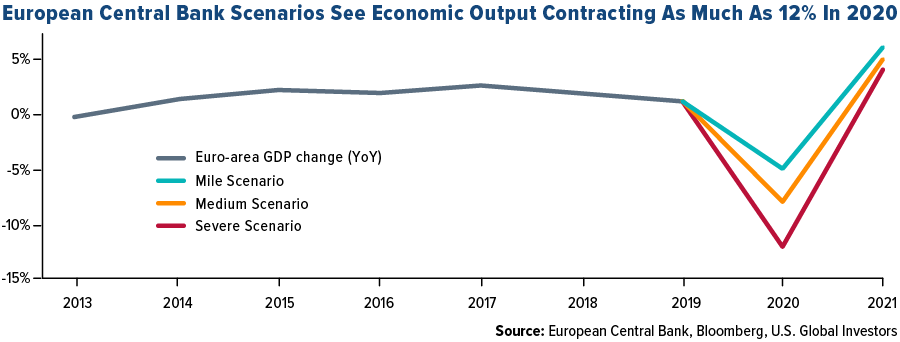

- ECB President Christine Lagarde and Vice President Luis De Guindos both said Wednesday that eurozone output is set to shrink between 8 percent and 12 percent this year. Under a mild scenario, GDP will contract by 5 percent and under a severe scenario 12 percent, as businesses were forced to close due to the coronavirus pandemic. On a positive note, the ECB expects growth to rebound in 2021.

- Euro-area economic sentiment rose to 67.5 in May from a record low of 64.9 the previous month. Still, it missed the consensus for 70.6. Industrial confidence improved slightly while service confidence weakened. Consumer confidence stayed unchanged. Latest confidence data shows that a recovery may take longer.

- Japanese carmaker Nissan has decided to shut its factory in Barcelona where 3,000 people are employed after four decades of operations, the Spanish government said on Thursday. The decision came despite the government’s efforts to keep the plant open, Foreign Minister Arancha Gonzalez Laya told the national radio station. Spain’s car industry is the European Union’s second biggest after that of Germany, accounting for 10 percent of the country’s GDP.

China Region

Strengths

- India was the best performing country this week, gaining 5.7 percent. India’s economy grew at 3.1 percent in the three months through March compared with a year ago. That was higher than the median 1.6 percent estimate in a Bloomberg survey of economists and down from a revised 4.1 percent in the previous quarter. Eicher Motors, a car manufacturer/distributor, was the best performing equity among stocks trading on the NSE Nifty 50 Index, gaining 19 percent over the past five days.

- The Indonesia rupiah was the best performing currency this week, gaining 1.8 percent. The rupiah recorded a third weekly gain after the bank of Indonesia Governor Perry Warjio said Thursday that he saw the currency as undervalued. Low inflation, narrow current account deficit and stronger inflows will further strengthen the exchange rate against the U.S. dollar, he said.

- Consumer staples was the best performing sector among equites trading on the Hong Kong Stock Exchange.

Weaknesses

- Hong Kong was the worst relative performing market this week, gaining 14 basis points. Despite China moving forward with the new security law that will give the communist party more control over Hong Kong, stocks finished slightly higher supported by strong global equity performance. Vitasoy, a food manufacturer and distributor, was the worst performing equity among stocks trading in the iShares MSCI Hong Kong ETF, losing 20 percent over the past five days, erasing all gains from the prior week.

- The Pakistani rupee was the worst performing currency this week, losing 1.4 percent. The currency is under pressure due to external debt outflows, falling remittances and weakening exports.

- Conglomerates was the worst performing sector among equites trading on the Hong Kong Stock Exchange.

Opportunites

- On Monday, Japan lifted the state of emergency and released a phased plan for fully re-opening its economy by August. Kyodo News reports that restrictions on domestic travel and large-scale events will be gradually eased every three weeks after assessing COVID-19 cases at the time.

- Lombard Odier says that Asian currencies are set to outperform their emerging-market peers for the rest of 2020, but their performance could be capped by the U.S.-China trade tensions. Bloomberg notes that the New Taiwan dollar (TWD) is the company’s favorite currency pick in Asia due to Taiwan’s success in containing the spread of COVID-19. LombaRulerd is also modestly constructive on the Korean won for similar reasons.

- German Chancellor Angela Merkel said the European Union has a “great strategic interest” in maintaining cooperation with China, reports Bloomberg. According to Eurostat data, China was the third largest trading partner for EU exports of goods and the largest partner for EU imports of goods, at 9 percent and 19 percent, respectively.

Threats

- China’s National People’s Congress voted on Wednesday in favor of a decision to impose national security legislation on Hong Kong. This is a big escalation in China’s attempts to exert more influence on the territory after widespread pro-democracy protests that lasted much of 2019. The new law is aimed at tackling secession, subversion, terrorism and foreign interference in Hong Kong, but the plan has already triggered the first big protests in the city in months. Aljazeera reports that the new law will alter Hong Kong’s Basic Law to require its government to enforce measures to be decided later by Chinese leaders. This move has amped up tensions globally between China and its trading partners, especially the U.S. Secretary of State Mike Pompeo announced that the State Department no longer considered Hong Kong to have significant autonomy under Chinese rule, which could trigger the end to some or all of special trade and economic relations with Hong Kong.

- The China Banking Insurance Regulatory Commission said that bad loans at banks now stand at a high level due to the impact of the coronavirus pandemic. The non-performing loan (NPL) ratio of China’s 134 city commercial banks stood at 2.49 percent by the end of March, while that of rural banking institutions was at 4.9 percent. FactSet and Reuters note those rates were higher than the industry wide average NPL ratio of 2.04 percent by the end of the first quarter.

- Japan released April economic data that was worse than predicted. Japan’s industrial production in April posted the biggest drop since the 2011 tsunami. Auto sales dropped by more than a fifth and department store sales fell 71.5 percent. Retail sales for the month were also worse than expected but could rise in May after the nationwide state of emergency was lifted.

Blockchain and Digital Currencies

Strengths

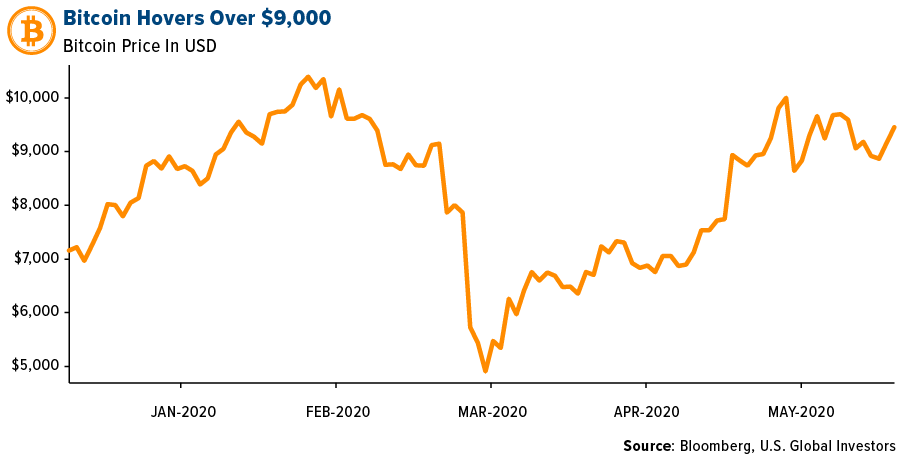

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 29 was Baz Token, up over 9,000 percent. Bitcoin had a solid week, holding steady slightly above the $9,000 mark.

- As reported by CoinDesk, Gemini has become the first U.S. crypto exchange and custodian to partner with Samsung, the companies announced on Thursday. Users of Samsung Blockchain in both the U.S. and Canada can now connect to Gemini’s mobile app to buy, sell and trade crypto after the companies built an integration between the two applications.

- Cryptocurrency exchange Coinbase is acquiring Tagomi, a prime brokerage platform specializing in digital asset trading, reports CoinDesk. “We are going to be integrating the Tagomi platform into our product suite and it will form the foundation for the future of our institutional business,” head of corporate development Shan Aggarwal said.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended May 29 was Switch, down 88.66 percent.

- On Monday, the total number of bitcoins held in cryptocurrency exchanges wallets dropped to an 18-month low, to just above 2.3 million, reports CoinDesk. This decline signifies an 11 percent year-to-date reduction in the number of bitcoins held by exchanges.

- Bitcoin tumbled mid-week on rumors that its anonymous creator, who goes by the pseudonym Satoshi Nakamoto, was moving coins mined in early 2009. The act was perceived by some as a “near-sacrilegious event,” writes Bloomberg.

Opportunities

- CoinShares has released a new index linking bitcoin and gold, reports Decrypt, in order to leverage the risk-off attributes of gold with bitcoin’s propensity for higher returns. The new index is called the CoinShares Gold and Cryptoassets Index (CGCI) and is designed to provide investors exposure to cryptocurrencies, in a “risk-managed” way.

- Grayscale has ramped up its bitcoin accumulation to a rate equivalent to 150 percent of the new BTC created since halving, estimates independent researcher Kevin Rooke. CoinTelegraph reports that data published by Rooke points out Grayscale adding 18,910 BTC to its trust since the halving, while only 12,337 bitcoins have been mined since May 11.

- A digital identity and payments platform known as Nuggets, has developed a way to accept deliveries without needing a physical signature, reports CoinDesk. The blockchain ID solution aims to combat a spoke in fraud during the coronavirus pandemic.

Threats

- Even though bitcoin is trading above $9,000 again, technical indicators suggest it could be stuck in a funk, writes Bloomberg. The largest cryptocurrency needs to break out of the downtrend it formed when its May high failed to take out the one reached in February. “Any further rally that withers before overcoming a previous high may signal bitcoin entered a potential downtrend, further indicating bearish sentiment,” the article continues.

- Ahead of an investor call mid-week, Goldman Sachs declared in a slide deck that “cryptocurrencies including bitcoin are not an asset class,” reports CNBC. The deck detailed several reasons why cryptocurrencies couldn’t be considered an asset class in their own right, the article continued, claiming they don’t generate cash flow like bonds or earnings through exposure to global economic growth.

- Ransomware attacks are a rising trend across Colombia, according to a study unveiled on May 28 by the National Police of Colombia. In fact, 30 percent of all ransomware attacks within Latin America have specifically targeted the country. Ransom payments generally range between 0.5 and 5 bitcoin, CoinTelegraph reports, depending on the current price of the cryptocurrency.

May 27, 2020Growth Is Crushing Value Right Now |

May 26, 2020You Can’t Just Print More Gold |

May 21, 2020Investing in Airlines Amid COVID-19 |

|||

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.65 | -0.01 | -1.21% |

| Oil Futures | 35.16 | +1.91 | +5.74% |

| Hang Seng Composite Index | 3,321.58 | +39.60 | +1.21% |

| S&P Basic Materials | 348.38 | +15.52 | +4.66% |

| Korean KOSPI Index | 2,029.60 | +59.47 | +3.02% |

| S&P Energy | 291.59 | +2.65 | +0.92% |

| Nasdaq | 9,489.87 | +165.29 | +1.77% |

| DJIA | 25,383.11 | +917.95 | +3.75% |

| Russell 2000 | 1,394.04 | +38.51 | +2.84% |

| S&P 500 | 3,044.31 | +88.86 | +3.01% |

| Gold Futures | 1,745.20 | -8.30 | -0.47% |

| XAU | 120.10 | -4.14 | -3.33% |

| S&P/TSX VENTURE COMP IDX | 553.32 | +16.38 | +3.05% |

| S&P/TSX Global Gold Index | 328.29 | -23.42 | -6.66% |

| Natural Gas Futures | 1.84 | +0.11 | +6.07% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,029.60 | +172.52 | +9.29% |

| 10-Yr Treasury Bond | 0.65 | +0.02 | +3.82% |

| Gold Futures | 1,745.20 | +26.00 | +1.51% |

| S&P Basic Materials | 348.38 | +11.88 | +3.53% |

| S&P 500 | 3,044.31 | +104.80 | +3.57% |

| DJIA | 25,383.11 | +749.25 | +3.04% |

| Nasdaq | 9,489.87 | +575.16 | +6.45% |

| Oil Futures | 35.16 | +20.10 | +133.47% |

| Hang Seng Composite Index | 3,321.58 | -127.01 | -3.68% |

| S&P/TSX Global Gold Index | 328.29 | -13.50 | -3.95% |

| XAU | 120.10 | +0.63 | +0.53% |

| Russell 2000 | 1,394.04 | +33.28 | +2.45% |

| S&P Energy | 291.59 | -4.69 | -1.58% |

| S&P/TSX VENTURE COMP IDX | 553.32 | +75.96 | +15.91% |

| Natural Gas Futures | 1.84 | -0.03 | -1.77% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 120.10 | +20.27 | +20.30% |

| S&P/TSX Global Gold Index | 328.29 | +63.10 | +23.79% |

| Gold Futures | 1,745.20 | +91.90 | +5.56% |

| DJIA | 25,383.11 | -383.53 | -1.49% |

| S&P 500 | 3,044.31 | +65.55 | +2.20% |

| Nasdaq | 9,489.87 | +923.39 | +10.78% |

| Korean KOSPI Index | 2,029.60 | -25.29 | -1.23% |

| Natural Gas Futures | 1.84 | +0.08 | +4.79% |

| S&P Basic Materials | 348.38 | +13.68 | +4.09% |

| Russell 2000 | 1,394.04 | -103.83 | -6.93% |

| Oil Futures | 35.16 | -11.93 | -25.33% |

| Hang Seng Composite Index | 3,321.58 | -378.64 | -10.23% |

| S&P/TSX VENTURE COMP IDX | 553.32 | +32.73 | +6.29% |

| S&P Energy | 291.59 | -47.71 | -14.06% |

| 10-Yr Treasury Bond | 0.65 | -0.61 | -48.34% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2020):

TMAC Resources Inc

Impala Platinum Holdings Ltd

Polymetal International

Magnitogorsk Iron and Steel Works

Southwest Airlines Co.

American Airlines Group Inc.

American Tower Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. Standard and Poor’s Supercomposite Trucking Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 30, 1994.The parent index is SPR. This is a GICS Level 4 Sub-Industry group. Standard and Poor’s Supercomposite Transportation Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 30, 1994. The parent index is SPRL2. This is a GICS Level 2 Industry group. Intraday values calculated by Bloomberg and not supported by S&P.