Investor Alert

Afghanistan Is Sitting on a Gold Mine. Literally.

Date Posted: August 27, 2021

Read time: 44 min

On behalf of everyone at U.S. Global Investors, I want to extend my deepest sympathies and condolences to the U.S. service members and their families, U.S. allies and all others who were impacted by the suicide bombings that took place in Kabul on Thursday. I pray that the victims’ loved ones find peace and that the remaining Americans return home without incident.

Afghanistan is sitting on a gold mine. I don’t mean that figuratively.

The country sits atop what could be one of the world’s largest reserves of various metals and minerals, including not just gold but also platinum, silver, copper, iron, aluminum and uranium. It’s believed to have so much lithium, an increasingly important metal that’s widely used in battery technology, that Afghanistan could one day be known as the “Saudi Arabia of lithium,” according to a 2010 memo by the U.S. Department of Defense.

The combined value of its minerals is estimated at between $1 trillion and $3 trillion. By comparison, opium poppy production in the country was valued at only $350 million in 2020, despite an increase in cultivation from the previous year.

Afghanistan Rich in All-Important REEs. Will They Fall into the Right Hands?

Among Afghanistan’s rich resources are rare earth elements (REEs). REEs are those metals with unpronounceable names that are used in the manufacture of advanced technologies, including electric vehicles, wind turbines and missile guidance systems. Your iPhone contains a number of them. Each F-35 fighter jet carries about half a ton of these strategic elements.

As I’ve shared with you before, China has virtually cornered the global REE market. The U.S. has only one developed deposit—the Mountain Pass Mine near Las Vegas, owned by MP Materials—which supplies about 15.8% of the world’s REEs. In October 2020, former President Donald Trump signed an executive order addressing America’s overreliance on these “critical minerals” from “foreign adversaries,” including China.

And speaking of China, it’s not letting a good opportunity go to waste. Mere hours after the Taliban completed its swift takeover of Afghanistan, a Chinese foreign ministry spokesperson said that Beijing was ready to participate in “Afghanistan’s reconstruction and development.”

I genuinely hope the development of Afghanistan’s resources, with or without China’s help, improves its citizens’ quality of life and brings the country into the 21st century. With time, and with the right execution, Afghanistan could become one of the wealthiest countries in the region.

That said, the odds are not in the country’s favor, sadly. The so-called “resource curse” is a real thing.

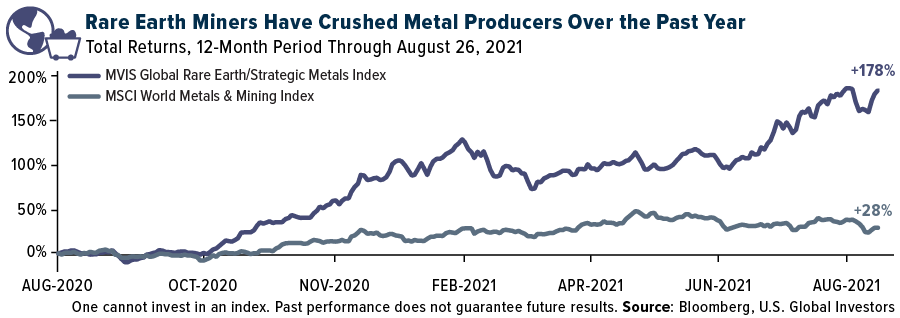

REE Miners on a Tear

Due to their scarcity and increasing strategic importance in advanced technologies, from lasers to X-rays to fiber optics, prices for many rare earths are elevated and are expected to continue rising.

This has been good for producers. As measured by the MVIS Global Rare Earth/Strategic Metals Index, shares of the group are up nearly 180% for the 12-month period, compared to producers of more conventional metals, which have risen 28%.

In July, in fact, the rare earth index was up a whopping 26%, making it MV Index Solutions’ top performing hard asset index for the month. The biggest mover for the month was China Northern Rare Earth High-Tech Company, up 130%, mostly on expectations of even higher demand from the electric vehicle (EV) sector, which could have a compound annual growth rate (CAGR) of 46% over the next five years. China’s carbon neutrality ambitions are another driver, with REEs being needed for wind turbines, solar arrays and more.

We like number two company Standard Lithium, up 47% in July. A speculative play, the Vancouver-based company, which has projects in Arkansas and San Bernardino Country, California, began trading in New York in July under the ticker SLI.

Lithium is a key component in the production of batteries, the demand for which is expected to jump many times over as the world transitions to the electrification of everything. Case in point: This week, California announced it would increase its solar and wind power capacity this year to help meet its target of 50% renewable energy generation by 2025. Toward that end, the state plans to add another 1.6 gigawatts (GW) of solar capacity and 0.4 GW of onshore wind capacity in 2021, along with 2.5 GW of battery storage capacity.

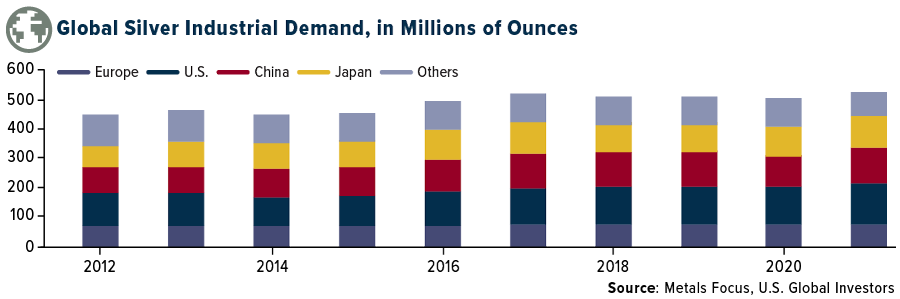

New Touchscreen Tech Constructive for Silver

We’re also bullish on silver for the same reasons. As Metals Focus reports this week, a growing number of countries are installing greater than 1 GW of photovoltaic (PV) capacity for solar power. In 2020, this number stood at 18, compared to 11 in 2018. The group also notes that replacement PV cells are constructive for the white metal, as “very little silver is recovered from old PV cells.”

Also adding to my bullishness is news that a new technique to make the conductive glass found in touchscreens, one using silver, may soon replace current methods that use a metal called indium.

Although indium is not technically a rare earth element, its economics are very much the same. About 70% of known deposits are in China. Output is unstable, with much of the supply existing only as a byproduct of zinc mining. And yet it’s used to make the ubiquitous touchscreens found in smartphones, laptops, ATMs, car stereos, cash registers and more.

An Australian scientist may have developed a solution that would help the world wean itself off of indium. Writing in the Conversation, Behnam Akhavan says that he and his team at the University of Sydney have discovered a way to make touchscreens with silver and tungsten oxide instead of indium.

“The entire process takes only a few minutes, produces minimal waste, is cheaper than using indium, and can be used for any glass surface such as a phone screen or window,” Akhavan writes, adding that he’s conducting further research to adapt the technology for wearing electronic devices.

This is positive news for silver demand, which is already strong from the renewable energy industry.

This week, Russian producer Polymetal International says it sees greater industrial demand pushing the white metal up to $30 an ounce, compared to $24 today.

Investors Losing 4% on the 10-Year Treasury

The (virtual) Jackson Hole Economic Symposium is underway, and Federal Reserve Chair Jerome Powell suggested what’s been on everyone’s mind for weeks now. The central bank may begin tapering its monthly bond-buying program by the end of the year, though rates are unlikely to be hiked just yet.

That’s despite inflation running above 5% year-over-year.

This just means bond yields will be negative for longer, benefiting gold and precious metals. The 10-year yield fell nearly 5 basis points today to 1.30%. When adjusted for inflation, investors are paying the government 4% for the pleasure of holding its debt.

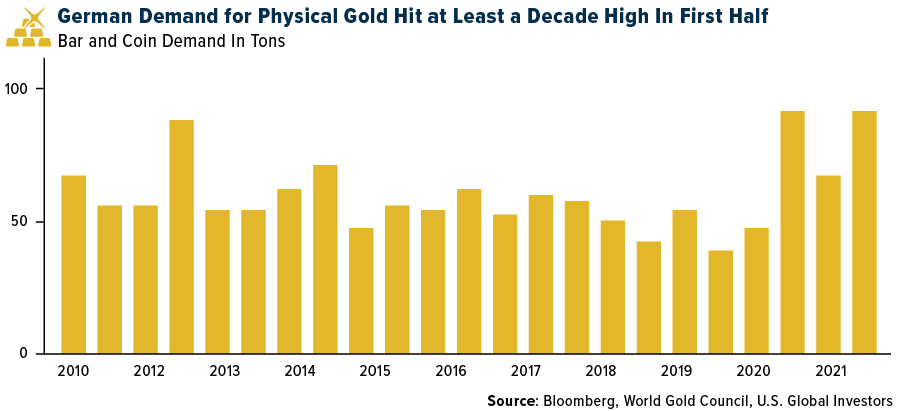

Take a look at what German investors are doing in the face of potentially higher inflation. Purchases of gold bars and coins in the first half of 2021 rose to their highest levels since at least 2009.

As always, I recommend a 10% weighting in gold, with 5% in physical bullion and 5% in gold mining stocks and ETFs. It’s important to rebalance on a regular basis.

For more on gold and other specialized assets and markets, be sure to subscribe to our YouTube channel by clicking here!

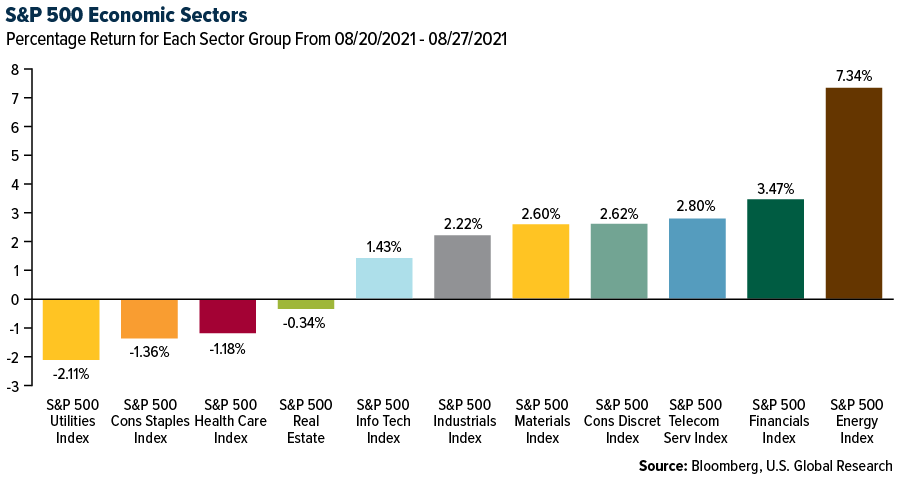

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.96%. The S&P 500 Stock Index rose 1.53%, while the Nasdaq Composite climbed 2.82%. The Russell 2000 small capitalization index gained 5.05% this week.

- The Hang Seng Composite gained 3.41% this week; while Taiwan was up 5.31% and the KOSPI rose 2.40%.

- The 10-year Treasury bond yield rose 4 basis points to 1.305%.

Airline Sector

Strengths

- The best performing airline stock for the week was Qantas Airways, up 22.2%, as the company lays out a plan for an overseas restart. U.S. airlines continue to ramp up capacity. Based on current schedule data, domestic capacity is expected to be -7.3% in the third quarter and +1.0% in the fourth quarter, comparing 2021 to 2019 levels.

- Management at Southwest Airlines made comments recently stating that the Company has a competitive advantage in the current labor environment as it did not furlough employees during the pandemic. This should allow Southwest to bring employees back more easily. The airline has already recalled employees that were on voluntary leave programs and will continue to recall all employees by the end of the third quarter.

- Last week, Southwest Airlines and the International Association of Machinists and Aerospace Workers (IAM) reached a tentative agreement to reward more than 5,000 of Southwest’s customer service employees, reports Yahoo! Finance. The provisional agreement with the IAM is related to an increase in wages and other benefits for employees, to ensure “members at Southwest Airlines receive the wages and benefits they bargained for at the negotiating table,” according to IAM Chief of Staff, Richard Johnsen.

Weaknesses

- The worst performing airline stock for the week was Avianca, down 8.3%. System net sales decelerated for the fourth straight week with a significant step back to -58.9% versus 2019 for the week ending September 15, versus -53.8% last week (a level not seen since mid-May). Domestic tickets sold online fell below 2019 levels to -4.3% (versus +2.4% last week). Domestic tickets sold decelerated at a faster pace this week to -29.3% (versus -23.9% last week) while international tickets sold declined modestly -46.0% (versus -44.5% last week). Domestic tickets sold through large corporate channels fell -58.4% (versus -55.7% last week).

- Air Canada earnings are under pressure. The timing of the earnings recovery and necessary deleveraging is highly dependent on the resumption of business and long-haul international travel, which accounted for 50% and 48% of pre-pandemic passenger revenue.

- American Airlines joined other U.S. carriers in warning that the delta variant of COVID-19 is slowing sales and leading travelers to cancel flight reservations, pushing August revenue below the company’s expectations. The carrier is also preparing for a more “muted” uptick in business travel into the fourth quarter but isn’t yet ready to change its financial guidance.

Opportunities

- Southwest Airlines is stepping up its recruiting efforts. According to Bloomberg, Southwest began offering an incentive program to encourage its employees to refer friends and family to apply for jobs with the airline. The Southwest Airlines Gratitude (SWAG) Program consists of an internal rewards program which allows employees to collect points and redeem them for air miles, flight guest passes, concert tickets, and more. If the referral accepts the job and works for Southwest for at least 6 months, the referrer can receive 20,000 SWAG points – a value estimated to be $300.

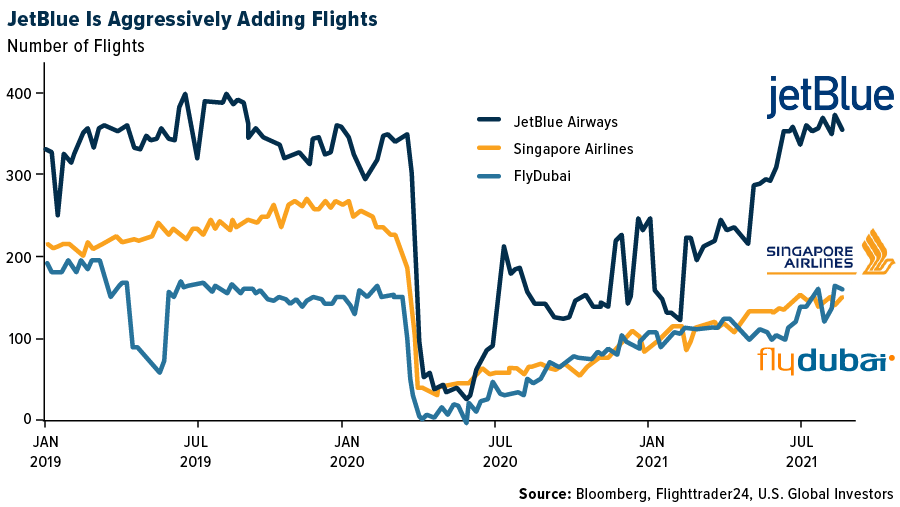

- JetBlue has been aggressively adding flights. As seen in the chart below, the carrier is outpacing two other international airlines. These three names represent the fastest growing airlines on a year-over-year basis.

- The Transportation Security Administration (TSA) extended its travel mask mandate through January 18 to minimize the spread of COVID-19 on public transportation. Last week, the TSA announced it will be extending the face mask requirement for individuals across all transportation networks throughout the U.S., including airports, onboard commercial aircraft, and commuter bus and rail systems.

Threats

- According to Bank of America, U.S. airlines’ website visits fell below 2019 levels to -1% for the week ending August 18 versus 2019, compared to +2% last week. More airlines are reporting near-term demand headwinds due to the delta variant and the end of the peak summer travel season.

- According to Bank of America, sporadic COVID-19 outbreaks and China’s zero tolerance to COVID means domestic revenues have yet to sustainably recover to pre-pandemic levels. The latest outbreak means that first-half August traffic is back to 37% of 2019 levels.

- A plan by Delta Air Lines Inc. to penalize unvaccinated workers underscores the dilemma faced by employers that want inoculated workers without triggering the practical problems associated with absolute vaccinate-or-terminate mandates, writes Bloomberg, such as firing employees who are both noncompliant and difficult to replace. The Atlanta-based airline announced Wednesday that it plans to assess a $200 monthly surcharge to unvaccinated workers who are part of the company’s health-care plan. Imposing that type of penalty can have implications under laws governing wellness programs and anti-bias protections, legal observers said.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Poland, gaining 2.7%. The best performing country in Asia this week was Thailand, gaining 6.7%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 1.7%. The Thailand baht was the best performing currency in Asia this week, gaining 2.5%.

- Chinese ADRs outperformed this week after a large sell off last week due to investors’ worry about new regulations on technology companies coming out in China. This week Pinduoduo and JD.com (both giant e-commerce platforms) outperformed after releasing very strong second-quarter results. Pinduoduo announced its first-ever quarterly net profit and JD.com reported a revenue beat. Cathie Wood’s Ark Investment Management, which has been dumping Chinese tech stocks this year, bought shares of JD.com after the company reported on Monday.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 1.2%. The worst relative performing country in Asia this week was Indonesia, gaining 0.50%.

- The Russian ruble was the worst relative performing currency in emerging Europe this week, gaining 0.44%. The Pakistani rupee was the worst performing currency in Asia, losing 1%.

- China’s industrial profits rose 16.4% year-over-year in July, slowing further from 20.0% in the previous month. FactSet reported profit growth remaining steady, but also noted a recovery remains uneven with lingering uncertainties.

Oppurtunities

- Europe’s final Manufacturing PMI for August will likely remain at a very strong level (above 61) next week when the data is released. Service PMI and Composite PMI should be unchanged too, well above the 50 level that separates growth from contraction.

- Minutes from the European Central Bank’s (ECB’s) meeting showed that bank members had an extensive debate over new guidance on interest rates. The Governing Council agreed on a longer period of unchanged or lower interest rates and the ECB will be more accepting of above target inflation. The dovish tone out of Europe and the United States pushed equites higher on Friday.

- China fully reopened its Meishan container terminal in Ningbo following a two-week shutdown. Normal operations were set to restart on Wednesday following the August 11 closure after one worker tested positive for COVID-19. Ningbo is the world’s third busiest container port, and its reopening should elevate the global shipping disruption.

Threats

- Bloomberg economists predict China PMIs will weaken. The non-manufacturing PMI could drop to 52.0 in August from 53.3 in July. The Caixin PMI is projected to come in lower as well, at 50.1 and just slightly above the 50 level that separates growth from contraction. Service PMI will likely drop too. PMI data will be released next week.

- China plans to propose new rules that would effectively ban companies with large amounts of sensitive consumer data from going public in the United States. Companies with less sensitive data, such as those in the pharmaceutical industry, are still likely to receive Chinese regulatory approval for foreign listings, FactSet said.

- The central bank in Hungary raised interest rates in August by 30 basis points to 1.5%, the highest level in the European Union, matching the pace of hikes in July and June. Hungary and the Czech Republic have been hiking rates due to inflation overshooting the central bank’s tolerance bend. For now, Poland and Romania are putting off rate increases despite intensifying price pressures.

Energy and Natural Resources Market

Strengths

- Natural gas was the strongest commodity for the week, gaining 13.48% on gas fields being idled with Hurricane Ida approaching the Gulf of Mexico. European natural gas futures also surged this week, and the heating season has not even started, as storage levels are unusually low.

- Global demand for lithium is accelerating at a faster clip than previously thought, according to the world’s second-largest producer of the rechargeable battery ingredient. With electric-vehicle demand surging more than 150% in the first half from a year ago, SQM forecasts that global demand could increase more than 40% this year.

- Iron ore surged on expectations of a recovery in economic growth, including additional support from the Chinese government. Futures in Singapore rebounded as much as 10% as a potential boost to the U.S. vaccination drive lifted sentiment across assets from stocks to base metals. Separately, China’s central bank chief vowed to stabilize the supply of credit and boost the amount of money supporting smaller businesses (and the real economy) after both credit and economic growth slowed in July.

Weaknesses

- The weakest commodity for the week was Powder River Basin (PRB) coal, off just 0.42% with bulk commodity demand up. Production growth is up 26.6% year-over-year for PRB coal. Western SPF pricing experienced a thirteenth consecutive drop as buyers continued to work down higher-priced inventories while some producers increased shipments to offshore markets. Western SPF ended the week down 8% to $385, down 60% relative to the second half of 2021, down 55% year-over-year, yet up 82% year-to-date. Overall lumber markets remain weak, as can be seen in the chart below.

- World steel output fell 6.9% month-to-month (up 3.3% year-to-year) in July led by China (down 10.5% month-to-month, down 8.4% year-to-year). The world ex-China production fell 2.3% month-to-month (up 21% year-to-year) with most regions decelerating. Global utilization fell 5.7 points month-to-month to 76.6% in July.

- Norway leads the world in the adoption of electric vehicles (EVs). From a standing start a decade ago, EVs have grown to 64% of new car sales in July 2021. To stay on track with ‘Net Zero by 2050’, the IEA recently estimated that EVs will need to account for 60% of car sales globally by 2030. In the IEA’s Net Zero scenario, global oil demand will have fallen by 25% by the time EVs hit 60% of new car sales.

Opportunities

- Russia’s ambassador to Kabul, Dmitry Zhirnov, said on Wednesday that the Taliban is open for Russian participation in the development of Afghanistan’s natural resources. “The Taliban is open to our participation in (Afghanistan’s) economy, including the development of natural resources,” said Zhirnov to a YouTube channel “Soloviev Live”, according to TASS.

- According to Morgan Stanley, despite macro noise, underlying fundamentals remain attractive for the exploration and production (E&P) sector. Since the end of June, E&Ps and oil have fallen by 20% and 15%, respectively, as the market has become increasingly concerned about refined product demand amid resurging COVID cases globally. They believe there will be a growing mismatch between the sector’s performance and underlying energy market fundamentals, which remain constructive in the second half of 2021.

- Nickel hasn’t yet cracked $20,000 per ton this quarter, but the metal continues to flash the kind of signals that suggest, sooner or later, it will do so. Given it’s used in both stainless steel and electric batteries, it combines old and new economy appeal in a single commodity. With top miner BHP Group expecting a small deficit this year, stockpiles have been contracting in LME sheds, as well as in China.

Threats

- OceanaGold announced the temporary suspension of mining and most milling operations at its Macraes and Waihi mines in New Zealand, as of August 17. This comes on the back of the country-wide COVID-19 lockdown. The company expects the operations to be suspended until at least August 28.

- Plant workers at Codelco’s Andina copper mine are expected to reject management’s latest wage offer, signaling a stoppage at the central Chilean operation will continue, according to the union’s president. Under the country’s collective-bargaining rules, leaders of the Suplant union are required to present the new offer to members but “there’s no chance” it will be approved in a vote.

- Goldman attended the SMU Steel Summit in Atlanta. The group came away from the event with continued confidence around the steel price environment for the remainder of the year on strong U.S. demand trends and tight supply. However, the debate around pinpointing the inflection point was top of mind as the ramp up of new supply and higher imports could catalyze the decline in steel prices from current highs.

Domestic Economy and Equities

Strengths

- New-home sales rose for the first time since March. Sales came in at a seasonally adjusted annualized rate of 708,000 in July, the Census Bureau said, up from an adjusted 701,000 rate in June. This sales rate was higher than the 680,000 expected.

- The U.S. economy grew at a 6.6% annual rate last quarter, slightly faster than previously estimated. The report from the Commerce Department estimated that the nation’s gross domestic product accelerated slightly in the April-June quarter from the 6.5% it had initially reported last month.

- Penn National Gaming was the best performing S&P 500 stock for the week, increasing 23.5%. Penn is the largest gaming company with 43 gaming properties across 20 states. Recently, the company announced another casino opening in Pennsylvania.

Weaknesses

- August’s Richmond Fed Manufacturing Index, which measures manufacturing activity across the central Atlantic region in the United States, fell to the lowest level since June 2020. The Index fell 18 points month-over-month to 9 from 27. Each component of the Index (shipments, new orders, and employment) decreased from the month of July.

- Preliminary August Markit Composite PMI, which is comprised of Manufacturing PMI and Service PMI, was reported at 55.4 in August, lower than the July reading of 59.9. Both Manufacturing and Service PMIs weakened, but both remain above the 50 level that separates growth from contraction.

- Dollar Tree was the worst performing S&P 500 stock for the week, losing 11.4%. Telsey cut downgraded Dollar Tree to market perform from outperform, due to higher supply chain and shipping costs.

Opportunities

- Nasdaq, the well-known technology heavy index, closed above 15,000 for the first time this week. The Pfizer vaccine’s full FDA approval by regulators has boosted broader market sentiment, raising hopes that more unvaccinated people will get the shot. Despite record high levels of Delta variant COVID cases, there could be more upside in U.S. equities as some reports state that the Street may be underestimating the impact of fiscal and monetary stimulus and the reopening processes.

- On Tuesday afternoon, Democrats adopted a $3.5 trillion budget resolution, paving the way for negotiations on a reconciliation bill focused on childcare, education, health care and climate change. Nancy Pelosi, Speaker of the United States House of Representatives, agreed to put the infrastructure bill on a path to approval by September 27.

- Federal Reserve Chairman Jerome Powell said the central bank could begin reducing its monthly bond buying this year, though it won’t be in a hurry to begin raising interest rates thereafter. Stocks rose on Friday on Powell’s dovish taper tone.

Threats

- The Conference Board Consumer Confidence, a leading monthly indicator, will be released next week. Bloomberg Economist expect a slightly weaker reading than in July. They also predict the Manufacturing PMIs reading to be weaker as well. Chicago PMI is expected to fall to 68.9 from 73.4 and the ISM Manufacturing PMI 59.0 versus 59.5. Nevertheless, both PMIs will remain above the 50 level that separates the expansion from contraction.

- On Thursday, tragic news emerged that thirteen U.S. military members were killed due to two explosions outside Kabul’s international airport. In the past two weeks, the United States rushed to evacuate U.S. citizens and Afghans who helped American troops during the war. This deadly attack took place just days before the August 31 deadline to withdraw all U.S. personnel from Afghanistan. ISIS has claimed responsibility for the bombings.

- COVID cases are still on the rise in the U.S., but the pace of infections is showing signs of slowing, especially in some of the states that have been hit hardest by the Delta variant. An average of more than 12,200 Americans were admitted to hospitals with Covid-19 each day during the week ended Aug. 23, Centers for Disease Control and Prevention data shows. That’s an increase of 6.6% from the week before, a smaller jump than has been seen in recent weeks.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was XLMDOWN, rising 12,213,988%. The host of CNBC’s “Mad Money”, Jim Cramer, has recommended putting up to 5% of a portfolio into cryptocurrency, reports Bitcoin.com. He stated that he owns Ethereum directly, affirming that he is a believer.

- Bloomberg ETF analysts think that the U.S. Securities and Exchange Commission (SEC) could approve a Bitcoin futures ETF by this October, reports CoinTelegraph. “A launch could come as soon as October, and we believe the SEC should permit several at once to avoid handing out a first-mover advantage,” one of the analysts commented.

- Tech giant Microsoft has won a blockchain-related patent for techniques for implementing a cross-chain token management system, reports CoinTelegraph. The patent, which was granted on Tuesday, but filed in February 2019, describes a “ledger-independent token service,” or a software service enabling individuals and organizations to create and manage tokens across multiple distributed ledger networks and platforms.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Lendefi (old), down 94.96%.

- As reported by Kelly Crow of the Dow Jones, scammers seem to be seeking a new frontier in the crypto arena. NFTs (non-fungible tokens) are supercharging the art market, but users warn they have a dark side. According to the article, scammers and hackers are increasingly exploiting security gaps in the rapidly expanding marketplace; all the while, artists and collectors who aren’t crypto literate are proving easy marks, cyber-defense experts say.

- A former central bank official, nominated to head South Korea’s financial watchdog, has expressed criticism about recognizing cryptocurrency as a financial asset, reports Bitcoin.com. On Wednesday, he was quoted by the Korea Herald as stating: “International organizations, including the Group of 20 and the International Monetary Fund, as well as a lot of market experts, find it difficult to consider virtual currencies as a financial asset, and think they could not function as a real currency.

Opportunities

- PayPal announced a new cryptocurrency service in the U.K., reports Bloomberg, allowing clients in the U.K. to buy, hold and sell digital assets. A statement by the company notes that the service will be rolled out this week and is the first international expansion of this crypto service beyond the United States.

- Valkyrie Investments thinks it might be at the top of the queue for approval from the SEC for the first U.S. Bitcoin ETF, writes Bloomberg. This is thanks to a quirk that allows smaller issuers to file confidentially for the new offerings. Two months ago, Valkyrie sought regulatory permission for a futures-based fund, the article continues, likely the first company to do so before an onslaught by others following positive comments on the structure by the SEC.

- Billionaire Simon Nixon wants to bolster his crypto investments, writes Bloomberg, as more of the world’s ultra-rich embrace digital currencies. According to a statement from his family office – Seek Capital – the firm is aiming to “increase its allocation to crypto as we feel it is an important area for the future.”

Threats

- Earlier this month the Senate approved measures intended to help provide regulation of the cryptocurrency industry, via the bipartisan infrastructure bill. Some industry and national-security officials warn, however, that the proposal could unintentionally push illicit crypto transactions into markets where the U.S. government has no reach, writes the Dow Jones. This adds to the threat to American companies, government agencies and individuals.

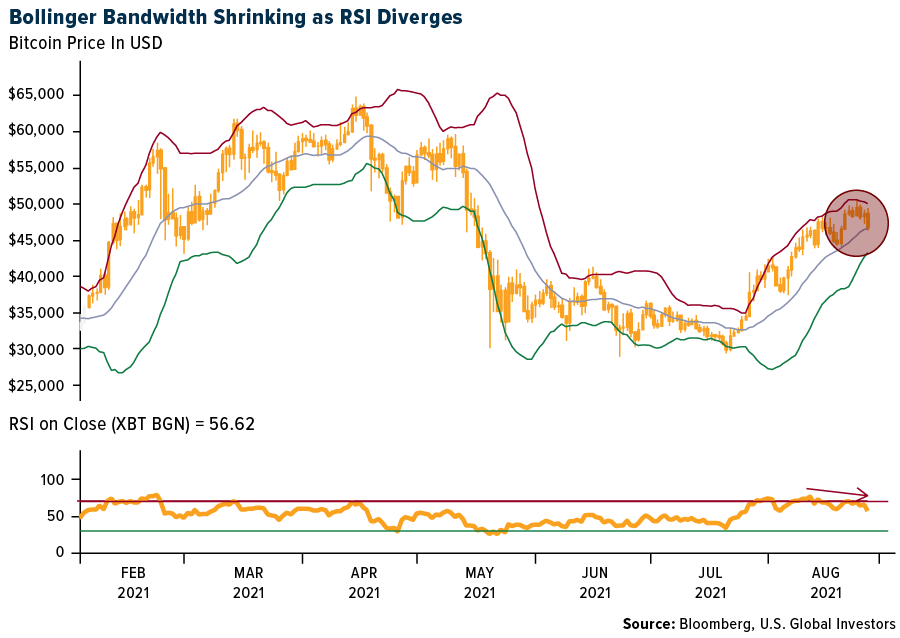

- Bitcoin fell as much as 4.9% on Thursday, reports Bloomberg, and chart patterns signal that its rally since July could be at risk of fading. John Bollinger, inventor of Bollinger bands, in a tweet suggested taking some profits or hedging.

- People’s Daily Online reported that Yin Youping, deputy director of the Financial Consumer Rights Protection Bureau of the People’s Bank of China, is stepping up public awareness that virtual currencies, like Bitcoin, are not legal tender and have no value support. They are pure investment speculation and consumers should eschew their use, warned Youping.

Gold Market

This week spot gold closed the week at $1,817.57, up $36.46 per ounce, or 2.05%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.18%. The S&P/TSX Venture Index came in up 3.12%. The U.S. Trade-Weighted Dollar fell 0.87%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-24 | New Home Sales | 697k | 708K | 701k |

| Aug-25 | Durable Goods Orders | -0.3% | -0.1% | 0.8% |

| Aug-26 | Hong Kong Exports YoY | 26.8% | 26.9% | 33.0% |

| Aug-26 | Initial Jobless Claims | 350k | 353K | 349k |

| Aug-26 | GDP Annualized QoQ | 6.7% | 6.6% | 6.5% |

| Aug-30 | Germany CPI YoY | 3.9% | — | 3.8% |

| Aug-31 | Eurozone CPI Core YoY | 1.5% | — | 0.7% |

| Aug-31 | Conf. Board Consumer Confidence | 123.0 | — | 129.1 |

| Aug-31 | Caixin China PMI Mfg | 50.1 | — | 50.3 |

| Sep-1 | ADP Employment Change | 650k | — | 330k |

| Sep-1 | ISM Manufacturing | 58.6 | — | 59.5 |

| Sep-2 | Initial Jobless Claims | 349k | — | 353k |

| Sep-2 | Durable Goods Orders | — | — | -0.1% |

| Sep-3 | Change in Nonfarm Payrolls | 750k | — | 943k |

Strengths

- The best performing precious metal for the week was palladium, up 6.44%, despite hedge funds cutting their net long positioning to a 14-month low. Gold rose the most in two weeks, up 1.40% on Friday, as Federal Reserve Chairman Jerome Powell’s testimony signaled central bank tapering may be appropriate this year and that it won’t be in a hurry to raise interest rates thereafter.

- Sibanye Stillwater, the world’s biggest platinum miner, announced a record first-half dividend after metals prices soared. Sibanye joins other South African platinum-group metals producers in reaping windfall profits after supply deficits pushed palladium and rhodium to record highs. The Johannesburg-based company will pay a first-half dividend of about 8.5 billion rand ($570 million), at the top end of its 25% to 35% payout ratio.

- Polymetal International, Russia’s second-biggest gold miner, will speed up a new silver project as it sees demand for the metal, including in solar panels, pushing up prices to $30 an ounce. The miner will fast-track development of the open-pit mine at the Prognoz deposit in Russia’s Yakutia region and process the ore at Polymetal’s existing Nezhda concentrator. The first payable concentrate production is expected in the third quarter of 2023.

Weaknesses

- The worst performing precious metal for the week platinum. OceanaGold has temporarily suspended gold mining operations in New Zealand as the nation’s Covid-19 lockdown restrictions start up.

- Exchange-traded funds continued to reduce gold holdings, bringing this year’s net sales to 7.2 million ounces, according to data compiled by Bloomberg. There were six straight days of declines, the longest losing streak since July 8. Total gold held by ETFs fell 6.7% this year to 99.9 million ounces, the lowest level since May 10.

- Steppe Gold released second-quarter results, producing 7,200 ounces of gold, lower than consensus of 9,700 ounces of gold. The company also ceased leaching in early July due to cyanide supply import issues.

Opportunities

- Citi sees palladium demand surging in 2022 through 2023 as its analysts expect the automobile industry to enter a strong restocking phase. The bank notes that car inventories are at their lowest level in over 50 years of data. Demand for platinum, palladium and particularly rhodium is minting South Africa largest trade surplus in history. The tripling of rhodium prices has made it South Africa’s most valuable export, as noted on Bloomberg.

- Silvercorp announced a normal course issuer bid to acquire up to 7,054,000 shares, representing approximately 4% of the shares issued and outstanding. The repurchase program will run until August 26, 2022.

- The specter of rising inflation caused the Ontario Teachers’ Pension Plan to increase its exposure to inflation-sensitive assets including gold and “a broad basket of commodities” in the first half of the year as investment teams continued to grapple with fallout from the global COVID-19 pandemic. Net investments in commodities accounted for 12% of the asset mix in the first half of the year, up from 8% at the end of 2020.

Threats

- Climate issues regarding drought and fires in the western U.S. and Canada are causing some operators to curtain field activities. Parts of Europe and eastern Siberia are also seeing massive fires. Drought has captured more than 95% of the land in 11 western states, including all of California, Oregon, Nevada, Idaho, Montana and Utah, according to the U.S. Drought Monitor. Jim Rouiller, who’s been a meteorologist for 40 years and heads the Energy Weather Group, says the summer has forced some rethinking among him and his colleagues. “This is very abnormal,” he said. “There is also a stronger signal for global warming in the picture. I do believe now more than I have that it is occurring. I just don’t know the magnitude but the change is happening and it is going to keep on increasing.”

- Kinross’s stock continues to decline and lose value. The company’s shares are 1.2% above the 52-week low of $5.64, giving the company a market cap of $7 billion. The stock is currently down 21.7% year-to-date, down 34.6% over the past 12 months, and up 17.5% over the past five years.

- Gold jewelers across India closed shop for a day on August 23 to protest against the new “arbitrarily implemented” quality standards in the country, the National Task Force on Hallmarking, representing 350 jewelry associations, said in a statement. About 160 million to 180 million pieces of jewelry are estimated to be certified under the new standards this year. At the current capacity of hallmarking centers of about 200,000 pieces daily, it will take almost four years to certify this year’s production, Task Force member Dinesh Jain said in the statement.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Southwest Airlines

Air Canada

American Airlines

JetBlue Airways Corp.

Delta Air Lines

Pinduoduo

JD.com

BHP Group

Oceana Gold

Standard Lithium Ltd.

Polymetal International PLC

Sibanye Stillwater Ltd.

OceanaGold Corp.

Silvercorp Metals Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Richmond Fed Manufacturing Index is based upon mail-in surveys from a representative sample of manufacturing plants and seeks to track industrial performance.

MVIS Global Rare Earth/Strategic Metals Index covers the largest and most liquid companies which are active in the rare earth/strategic metals sector. The index is reviewed on a quarterly basis, float market capitalization weighted, and the maximum component weight is 8%. The MSCI World Metals & Mining Index is a free float weighted equity index. Compound annual growth rate (CAGR) is the rate of return that would be required for an investment to grow from its beginning balance to its ending balance, assuming the profits were reinvested at the end of each year of the investment’s life span.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.