Central Banks Haven’t Bought This Much Gold Since Nixon Was President

Date Posted: February 1, 2019

Read time: 53 min

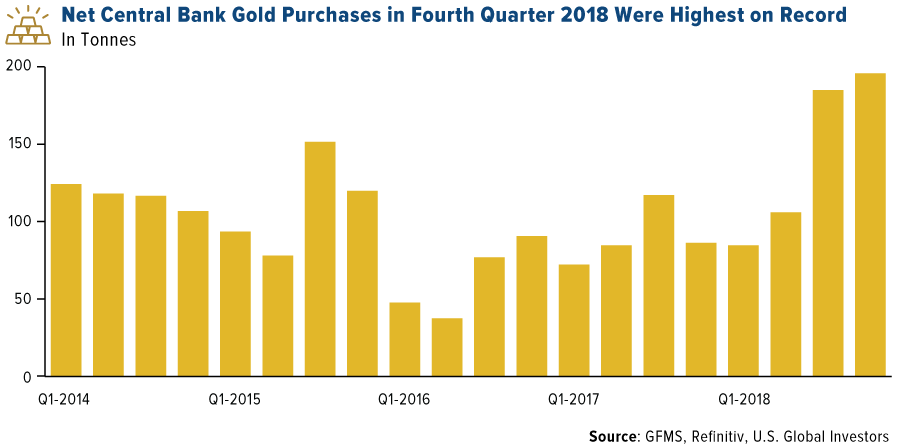

Last year was a watershed in the size of official gold purchases, as central banks added 651.5 tonnes to their holdings. Not only is this a remarkable 74 percent change from 2017, but it's also the most on record going back to 1971.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Something big is happening in the gold market right now, and nowhere is that more apparent than in central banks of emerging economies. Last year was a watershed in the size of official gold purchases, as banks added an incredible 651.5 tonnes (worth some $27.7 billion) to their holdings, according to the World Gold Council (WGC). Not only is this a remarkable 74 percent change from 2017, but it’s also the most on record going back to 1971, when President Richard Nixon brought a formal end to the gold standard. In the final quarter of 2018 alone, central banks purchased as much as 195 tonnes, the most for any quarter on record, according to leading precious metal research firm GFMS.

As I’ve shared with you before, central banks have been net buyers of the yellow metal since 2010 in an effort to diversify their reserves away from the U.S. dollar. This very week, I had the opportunity to discuss the issue with SmallCapPower’s Vasudha Sharma. You can watch the conversation by clicking here.

Most Western nations already have a comfortable weighting in gold relative to their total reserves, so the demand is almost strictly from emerging markets. Among the biggest purchasers last year were Russia, Turkey and Kazakhstan, and we also saw China add to its holdings for the first time since 2016. Meanwhile, Hungary, Poland, India and a number of other countries took deliveries for the first time this century.

Central Banks Recognize Gold as an Effective Diversifier and Store of Value

With gold representing a whopping 74 percent of U.S. reserves, the Federal Reserve has historically had the largest position among global central banks. (Venezuela’s weighting, at 76 percent, has lately roared past the U.S., but that’s thanks solely to hyperinflation and its rapidly deteriorating economy. I’ll have more to say on Venezuela later.)

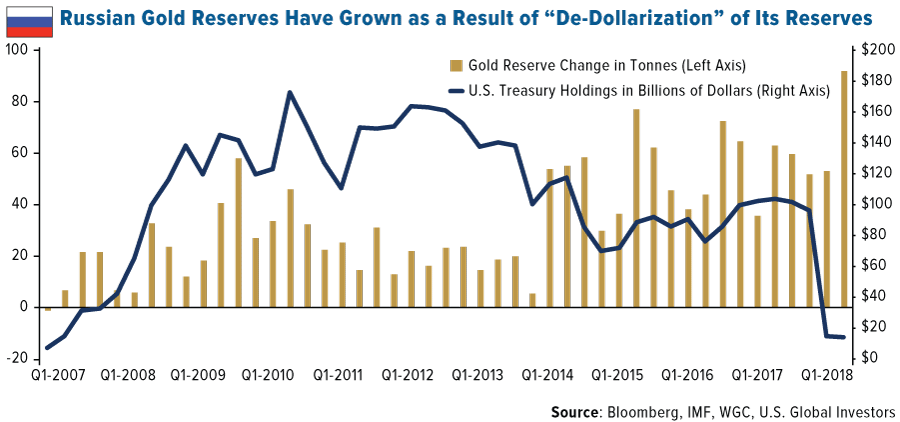

Other countries have a lot of catching up to do—i.e., gold buying—to get to the same level of diversification. Russia, for instance, has the fifth most gold in the world at 2,066.2 tonnes, but this amount represents only 17.6 percent of its total reserves. In sixth place is China, whose holdings (a reported 1,842.6 tonnes) represent a very small 2.3 percent of reserves.

Below you can see Russia’s ongoing strategy of “de-dollarization.” To date, the Eastern European country has liquidated nearly its entire position in U.S. Treasuries to fund its rotation into gold. According to the WGC, Russia bought 274.3 tonnes in 2018, its greatest amount on record, and the fourth consecutive year of purchases above 200 tonnes.

Gold Is the Only Thing Left of Value in Venezuela

Gold made even more headlines this week as it relates to Venezuela. The beleaguered South American country, as you probably know, is in the midst of a potential transfer of power, from current president and dictator Nicolas Maduro to the more centrist Juan Guaido, whom the U.S., European Union and other world governments have recognized as the de facto head of state.

Since the U.S. and other countries have imposed heavy sanctions on Venezuela and its oil industry, the cash-strapped country has had to rely on its gold holdings to make international bond payments, mostly to Russia and China. But the days of Maduro’s plundering of Venezuela’s hard currency might be numbered, and not just because he could be removed from power soon.

Venezuela’s Nicolas Maduro (left) shakes hands with Russian president Vladimir Putin. Both strongmen’s countries have a strong fondness and appetite for gold.

Venezuela’s Nicolas Maduro (left) shakes hands with Russian president Vladimir Putin. Both strongmen’s countries have a strong fondness and appetite for gold.Photo: Kremlin | Creative Commons Attribution 4.0 International

This week Guaido sent a letter to U.K. Prime Minister Theresa May and the Bank of England (BoE), urging them not to send $1.2 billion from any sale of Venezuela’s gold reserves—held in the BoE’s vaults—to Maduro’s “illegitimate and kleptocratic regime,” according to the Financial Times. “Maduro has stolen a huge quantity of state assets,” including Venezuelan gold, a part of the letter reads. “There is no doubt that he will, if allowed, also steal the assets held by the Bank of England, which rightly ought to be saved to support the recovery of Venezuela.” The bank has honored Guaido’s request and is blocking Maduro’s efforts to sell the metal.

Later in the week, a Russian Boeing 777 allegedly landed in the capital city of Caracas and was loaded up with as much as 20 tonnes of Venezuelan gold, according to Bloomberg. It was later reported that the jet, for reasons unknown, left Caracas without the gold payment. There are new reports, however, also by Bloomberg, that another aircraft, this one from the United Arab Emirates (UAE), has landed in the country and is awaiting delivery of the gold instead.

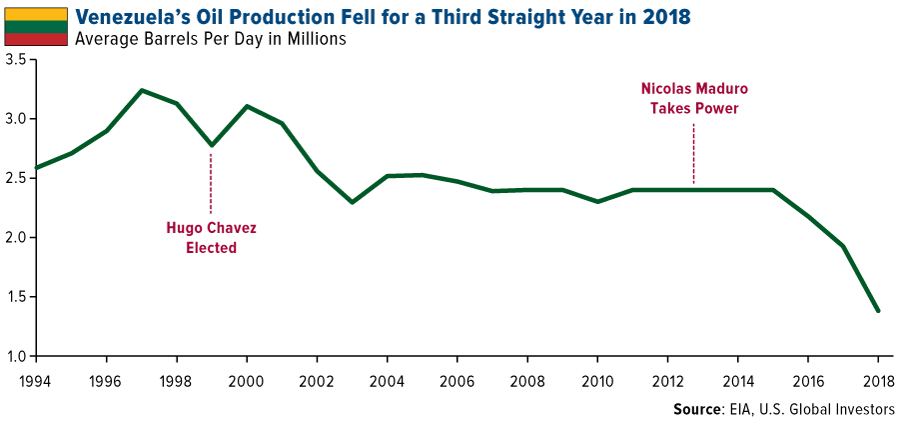

These incidents are certainly dramatic, and I’m eager to see how they play out, but I think the key takeaway is that gold is an exceptional store of value. It’s the only asset of any value to which a socialist autocrat like Maduro still has access. The bolivar is worthless, and the country’s once powerful and influential oil industry is fading fast. Without gold, Maduro is powerless.

Four Straight Months of Gains. What’s Gold’s Next Move?

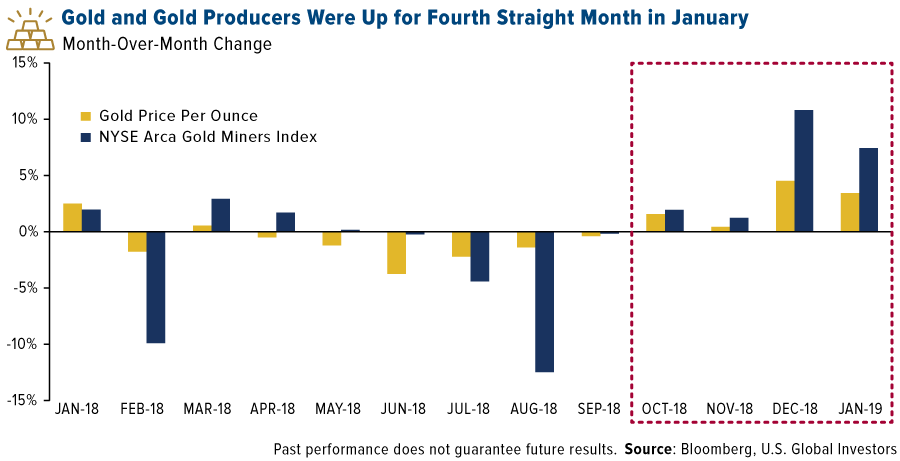

The gold rally that began late last year, when equities turned rocky, continued into the new year as the historic U.S. government shutdown gripped investors, and signs that Fed Chair Jerome Powell was set to pause monetary tightening intensified. For the fourth straight month in January, both the price of gold and gold mining stocks posted strong gains. Before then, the price of gold was down for six straight months, a losing streak we hadn’t seen in 40 years, when the yellow metal fell each month from December 1988 to May 1989.

The yellow metal ended last month at a nine-month high, and with the U.S. dollar expected to lose momentum on higher deficit spending, we could see prices surge to as high as $1,400 or even $1,500 an ounce this year.

I’m not alone in my bullishness. Billionaire Sam Zell, creator of the real estate investment trust (REIT), bought gold for the first time in his life, citing the fact that supply is shrinking.

And Mad Money’s Jim Cramer also came out strongly in favor of the yellow metal this week.

“We are big gold believers here,” Cramer commented. “Now gold is at $1,300, we think gold is going to $1,400, $1,500. We suggest that everybody have a little bit of gold in their portfolio.”

I second Cramer’s suggestion. My recommendation has always been a 10 percent weighting in gold, with 5 percent in bullion and jewelry, the other 5 percent in high-quality gold mining stocks and well managed gold mutual funds and ETFs.

Have a great Super Bowl weekend!

Gold Market

This week spot gold closed at $1,317.65, up $14.50 per ounce, or 1.11 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.62 percent. The S&P/TSX Venture Index was up 3.03 percent. The U.S. Trade-Weighted Dollar fell 0.19 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-28 | Hong Kong Exports YoY | -1.7% | -5.8% | -0.8% |

| Jan-29 | Conf. Board Consumer Confidence | 124.0 | 120.2 | 126.6 |

| Jan-30 | Germany CPI YoY | 1.6% | 1.4% | 1.7% |

| Jan-30 | ADP Employment Change | 181k | 213k | 263k |

| Jan-30 | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | 2.50% |

| Jan-31 | Initial Jobless Claims | 215k | 253k | 200k |

| Jan-31 | New Home Sales | 570k | 657k | 562k |

| Jan-31 | Caixin China PMI Mfg | 49.6 | 48.3 | 49.7 |

| Feb-1 | Eurozone CPI Core YoY | 1.0% | 1.1% | 1.0% |

| Feb-1 | Change in Nonfarm Payrolls | 165k | 304k | 222k |

| Feb-1 | ISM Manufacturing | 54.0 | 56.6 | 54.3 |

| Feb-2 | Durable Goods Orders | 1.7% | — | 0.8% |

| Feb-4-Feb-8 | GDP Annualized QoQ | 2.6% | — | 3.4% |

| Feb-5-Feb-15 | Housing Starts | 1253k | — | 1256k |

| Feb-5-Feb-15 | New Home Sales | 575k | — | 657k |

| Feb-5-Feb-15 | Durable Goods Orders Preliminary | 1.7% | — | — |

| Feb-5-Feb-15 | Durable Goods Orders Final | — | — | — |

| Feb-7 | Initial Jobless Claims | 220k | — | 253k |

Strengths

- The best performing metal this week was gold, up 1.11 percent. Gold traders were bullish on the outlook for a 12th straight week and the most bullish in five weeks, according to the weekly Bloomberg survey. The yellow metal is up more than 2 percent for the year and is set for a fourth monthly gain. This comes as the dollar is down for a third month. Gold saw a boost in particular on Wednesday when the Federal Reserve signaled that it’s moving away from its bias toward higher U.S. borrowing costs, which boosts the appeal of gold.

- Demand for gold in China, the world’s number one consumer, rose 5.7 percent in 2018 to 1,151 tonnes, says the China Gold Association. Jewelry consumption was also up 5.7 percent, while bar demand was up 3.2 percent. China, also the world’s top gold miner, saw output fall 5.9 percent to 401 tonnes last year. According to the World Gold Council (WGC), demand will remain steady in 2019, even as there are signs of slowing economic growth and political uncertainties.

- U.S. Mint data showed this week that gold coin sales rose to 65,000 ounces in January, the most in two years. This comes after several months of “horribly lacking” sales, says Peter Thomas at metals broker Zaner Group. Net purchases of gold holdings in ETFs are now at 2.01 million ounces for the year, according to data compiled by Bloomberg. For the first time in what seems like forever, ETFs also added silver to their holdings. On Thursday alone there were 1.18 million troy ounces added – the largest one-day increase since November 13.

Weaknesses

- The worst performing metal this week was palladium, down 0.66 percent as hedge funds cut their net long position to the lowest in six weeks. U.S. pending home sales fell in December for the third straight month. This is another sign that the housing market is weakening amid elevated property prices and higher borrowing costs, writes Bloomberg. GFMS wrote in a report this week that it sees gold at $1,292 an ounce in 2019, compared to current prices sitting around $1,309. They write that demand for defensive assets such as gold is likely to pick up on deepening economic concerns, but that physical markets are likely to be subdued because of high price levels.

- Venezuela is preparing to send 15 metric tonnes of its central bank reserves to the UAE, as the country’s economy struggles and President Nicolas Maduro faces opposition from within and abroad to step down as leader. U.S. National Security Advisor John Bolton wrote in a tweet on Wednesday: “My advice to bankers, brokers, traders, facilitators, and other businesses: don’t deal in gold, oil, or other Venezuelan commodities being stolen from the Venezuelan people by the Maduro mafia.”

- After several weeks of increasing gold reserves week-on-week, data from the Turkish central bank showed that reserves fell $555 million from the prior week. As of January 25, Turkey’s holdings were worth $19.9 billion, down 22 percent year-over-year.

Opportunities

- The Federal Open Market Committee (FOMC) released several decisions this week that could be positive for gold. As summarized by David Doyle at Macquarie Group, those changes are: being patient in market future adjustments and removing forward guidance on further rate hikes. The balance sheet normalization path is also flexible, and the Fed is willing to use the balance sheet if economic conditions warrant it. Brown Brother Harriman wrote that the Fed sent a clear signal to buy equities and sell the dollar, which is positive for gold.

- Central banks globally are buying gold at the fastest rate since 1971 when the gold standard was ended in the United States. Governments purchased 651.5 tonnes of gold in 2018, which is a 74 percent increase from the previous year. Metals Focus forecasts that these central banks might purchase another 600 tonnes in 2019. Russia and Turkey were among the largest buyers last year. Russia bought 274.3 tonnes of the yellow metal in an effort to de-dollarize its reserves. Gold consumption in India could be on the mend in 2019, as it is an election year, which could boost spending in the world’s second largest gold consuming country, according to the WGC.

- Silver could see a boost from increased solar power demand in sub-Saharan Africa. Bloomberg’s Takehiro Kawahara writes that “favorable economics and demand from commercial and industrial clients, largely mining companies and manufacturers, means more solar sales are being made directly to businesses.” Two gold miners rethought their strategies and shuttered projects that could have been non-economical. Iamgold shelved its Cote project construction while Eldorado suspended the advancement of a mill project in Turkey. These decisions to shutter potentially marginal expansion projects were immediately rewarded with significant share price gains for the two companies making good capital allocation decisions.

Threats

- The U.S. Treasury Department announced on Wednesday that it plans to issue another record-breaking amount of debt, creating growing criticism and questioning of whether President Donald Trump’s tax cuts will pay for themselves. The Treasury is raising its long-term debt issuance at its quarterly refunding auctions to $84 billion, which is $1 billion more than three months ago, writes Bloomberg. Debt sales have already risen past those last seen after the worst economic crisis since the Great Depression.

- In more Venezuela gold news, a Russian plane arrived in Caracas on Wednesday to take away 20 tonnes of gold, but then the plane left the country without the gold. The Maduro regime then halted its plans to ship the gold out of the country after the U.S. issued a warning for other countries not to deal with Venezuela’s gold.

- Juan Guaido, recognized by many nations as Venezuela’s true leader, wrote in a letter to the U.K. asking the Bank of England to not allow Maduro access to $1.2 billion in Venezuelan gold reserves held in the country. There is a risk, however, that if Guaido gains power, he could turn around and sell the gold, too.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.32 percent. The S&P 500 Stock Index rose 1.55 percent, while the Nasdaq Composite climbed 1.38 percent. The Russell 2000 small capitalization index gained 1.29 percent this week.

- The Hang Seng Composite gained 1.82 percent this week; while Taiwan was down slightly 0.37 percent and the KOSPI rose 1.18 percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.687 percent.

Domestic Equity Market

Strengths

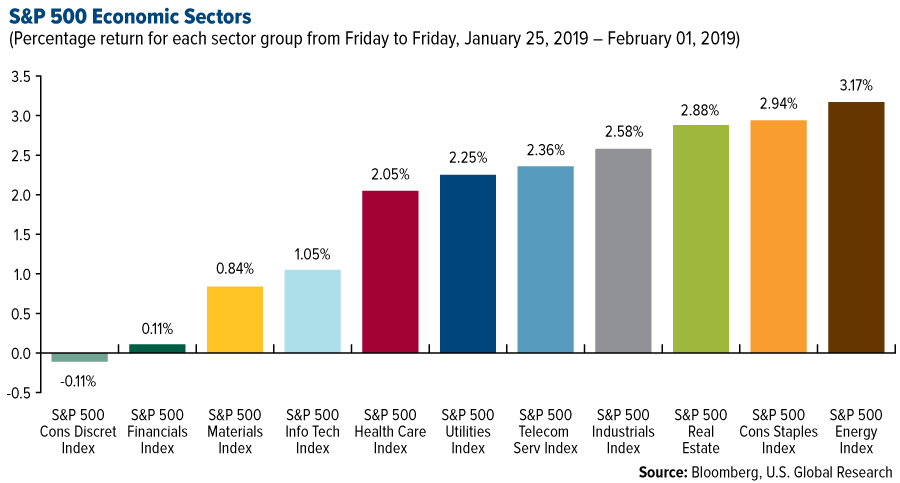

- Energy was the best performing sector of the week, increasing by 3.17 percent versus an overall increase of 1.43 percent for the S&P 500.

- Charter Communications was the best performing stock for the week, increasing 17 percent.

- Amazon beat Wall Street’s expectations with its fourth quarter results. The company’s cloud business brought in $26 billion in 2018, and shows no sign of slowing down.

Weaknesses

- Consumer discretionary was the worst performing sector for the week, decreasing by 0.11 percent versus an overall increase of 1.43 percent for the S&P 500.

- Allergan was the worst performing stock for the week, falling 10.33 percent.

- Deutsche Bank’s stock slipped further after a weaker-than-expected earnings report. The struggling bank has been implementing cost-cutting programs to improve efficiency, but it fell short on that front as well.

Opportunities

- The world’s biggest tech stocks are at a crucial turning point. Since the broader market tends to take its cues from tech, the next few months could determine the fate of risk assets.

- Although General Electric posted mixed fourth quarter results, shares were up more than 13 percent as the company made progress on deleveraging its power business. It also announced it had reached a settlement in principal with the Department of Justice regarding its former subprime-mortgage business.

- CEO Elon Musk declared Tesla will be profitable for “all quarters going forward.” Musk made the comments on the electric car maker’s fourth quarter earnings call, after the company posted its third quarterly profit.

Threats

- A record number of companies with poor credit are trading publicly in the U.S. and Europe. This is a troubling sign for the overall market.

- Facebook listed Amazon as a competitor for the first time in its annual report. The filing marks the first time Amazon has appeared in one of Facebook’s regulatory filings, and it underscores the growing importance of Amazon in an online ad market that has long been dominated by Google and Facebook.

- iPhone sales slowed during Apple’s worst holiday quarter in a decade. The smart phone sales fell 15 percent in the holiday quarter, and Apple says the weakness will most likely have an impact on the current quarter as well.

The Economy and Bond Market

Strengths

- Job growth in January defied expectations. Despite a partial government shutdown, the longest in history, nonfarm payrolls surged by an incredible 304,000, the Labor Department reported Friday. Economists surveyed by Dow Jones had expected payrolls to rise by 170,000.

- American manufacturers say business picked up in the first month of 2019 after moderating sharply in December. The Institute for Supply Management (ISM) said its manufacturing index rebounded in January to 56.6 percent from 54.3 percent in the prior month.

- November sales of new homes soared 16.9 percent from a month earlier to 657,000, the Commerce Department said Thursday. Economists had expected sales to reach an annual rate of only 571,000. The November report on home sales had been postponed because of the partial shutdown of the federal government.

Weaknesses

- Italy has officially entered a recession. Europe’s fourth-largest economy contracted 0.2 percent in the fourth quarter, after shrinking 0.1 percent in the third quarter, according to data released Thursday by the statistics agency Istat.

- Initial jobless claims jumped by 53,000 to 253,000 in the week ended January 26, the U.S. government said Thursday. The spike stemmed mostly from seasonal abnormalities that occur around the holidays and are likely to fade soon, according to economists.

- The University of Michigan’s consumer sentiment index plunged to 91.2 in January from 98.3 in December, the worst reading since Donald Trump was elected president. The government shutdown rattled consumers and, unlike previous bouts, the numbers didn’t materially improve even after some 800,000 workers went back to work. That’s because there’s the possibility of another shutdown on February 15, as Congressional negotiators remain at an impasse over funding the border wall desired by Trump.

Opportunities

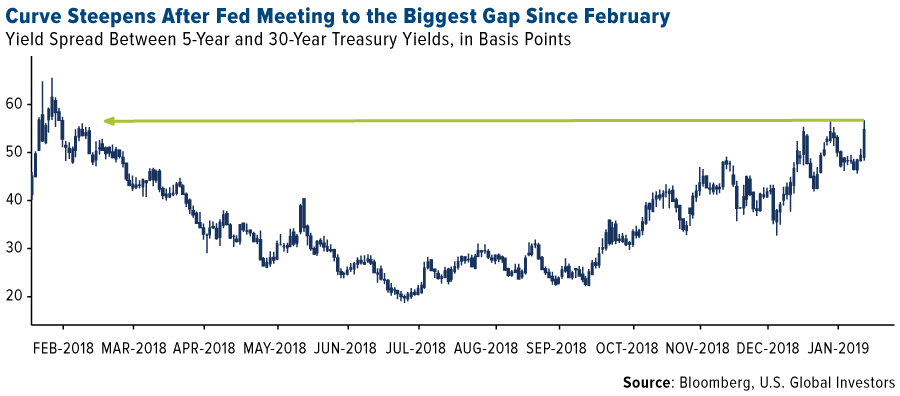

- The U.S. yield curve between five and 30 years steepened to a level unseen since February after Wednesday’s Fed decision and comments from Chairman Jerome Powell spurred a pullback in expectations for policy tightening. The spread widened as much as 7.3 basis points to 56.6 basis points as Treasuries across much of the curve rallied. The market shifted as the Fed said it will be “patient” on any future interest-rate moves and signaled flexibility on the path for reducing its balance sheet.

- In the U.S., Monday will kick the week off with factory orders. They are forecast to have risen 0.4 percent month-on-month in November after slumping a little more than 2.1 percent the prior month. Given the strength in manufacturing data this week, results are likely to meet or exceed expectations.

- Monday will also see the release of November final durable goods orders, which are expected to continue their upward rebound to 1.5 percent from the prior 0.8 percent.

Threats

- The ISM non-manufacturing PMI comes out in the U.S. on Tuesday, with the closely-monitored activity gauge projected to ease to 57.0 in January from an upwardly revised 58.0 in December.

- On Tuesday, President Trump will deliver the State of the Union address before Congress, a week late after House Speaker Nancy Pelosi pulled the original invitation during the government shutdown. Trump looks sure to keep up the pressure for the border wall and may renew calls for infrastructure spending. Even with Wall Street focused on upcoming company results, the annual address has the potential to move markets. Historically, markets have been more likely to trade down following State of the Union addresses.

- The extended winter freeze that so far has pounded entire regions of the U.S. figures to chill the economy, too. AccuWeather estimates a total cost to the economy of up to $14 billion, and while much of that will be recouped, up to $5 billion could be lost permanently. The hit will occur across a wide range of the economy, including business, school and museum closings, auto sales, significant insurance claims, flight and rail cancellations, increased consumer costs for heating oil and natural gas, a decreased demand for gasoline, and lost wages for non-salaried employees, among other impacts.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 9.96 percent after Canfor curtailed its production at three mills. Oil is set for its biggest January gain on record, or in at least 36 years. West Texas Intermediate (WTI) crude futures could rise almost 20 percent for the month on the heels of OPEC output cuts kicking in and a dovish Federal Reserve tone boosting markets. This marks a big rebound for oil, which plunged almost 40 percent in the fourth quarter of 2018. OPEC crude output fell the most in two years in January. Another commodity on the rise in 2019 is zinc. The metal lost 26 percent last year, but is now approaching its 200-day moving average with forecasts predicting a climb to $2,800 a ton within three months.

- Toyota Motor and Panasonic announced a joint venture this week to manufacture lithium-ion batteries for electric vehicles that would help reduce battery costs, reports Bloomberg. The partnership will be mutually beneficial – by helping Toyota increase its electric vehicle presence and helping Panasonic reduce its reliance on partner Tesla.

- According to a report this week from Bloomberg New Energy Finance, companies and government agencies are hungry for renewable energy. In 2018, contracts were signed for a total of 13.4 gigawatts of clean power, nearly double the 2017 figure of 6.1 gigawatts. Although the contracts still only represent a fraction of total electricity used, there are a growing number of industries signing such contracts and making commitments to renewable energy.

Weaknesses

- Natural gas was the worst performing commodity this week falling 13.72 percent. The polar vortex moving through the U.S. Midwest and East this week has come too late to keep the natural gas rally going, reports Bloomberg. The record cold weather is set to fade by next week, proving to be only a short-lived spike in demand. On Monday, natural gas futures fell to their lowest since early January and reversed the gains from the prior week. However, the price steadied later in the week and finished January down 4.3 percent.

- A dam collapse at Vale SA’s Feijao mine in rural Brazil has left nearly 100 dead and at least 250 people missing. This is the second fatal disaster for the world’s biggest producer of iron ore. The Brazilian police have so far arrested five people—three Vale employees and two subcontractors—who attested to the instability of the dam. The company suspended dividends and its shares tanked as much as 20 percent on Monday.

- Aluminum fell as much as 1.9 percent on Monday after the U.S. Treasury Department removed sanctions on Russia’s Rusal and two other firms linked to billionaire Oleg Deripaska. The lifting of sanctions removes the prospect of massive supply disruptions that shocked the market, and sent aluminum prices soaring last April when sanctions were first imposed.

Opportunities

- As discussed above, the Vale dam collapse is a terrible tragedy. However, it did result in iron prices surging, at first, on the news of reduced supply as a result of the mine disaster. Vale, the world’s largest iron producer, announced that it would cut 40 million tons of output. All grades of spot iron rose on Wednesday, with top-grade material popping 6.9 percent to $100.30 a ton, the highest level since 2017, reports Bloomberg. Singapore Exchange futures climbed as much as 9.5 percent, the most since March 2017. Nickel prices also rose on Wednesday over fear that the iron disruption could carry over to that metal as well. Bloomberg writes that prices soared to a three-month high on the London Metals Exchange, similar to the rally in iron and nickel contracts on Chinese exchanges. However, many are predicting that the iron rally will be short-lived.

- According to domestic media, China has ended a three-year freeze on approvals for nuclear reactors, which will clear the construction of four Hualong One reactors. China remains committed to prioritizing clean energy sources and this week ordered grid companies to purchase output from renewable producers. The world’s largest consumer of energy has taken steps to lower curtailment and cut overcapacity in the green energy sector, writes Bloomberg. Additionally, China’s crackdown on pollution had led to an increase in LNG consumption as a replacement for coal, which has triggered new gas projects globally to meet the growing demand.

- Chile, home to the world’s largest reserves of lithium and currently the number two producer, said this week that it is closer to becoming a manufacturing hub for rechargeable batteries used in electric vehicles, writes Bloomberg. Currently it exports the raw lithium to China, where batteries are made, but hopes for battery makers to begin installing lithium processing plants locally.

Threats

- The U.S. imposed sanctions on Venezuela’s state-owned oil company PDVSA that effectively blocks the nation from exporting crude oil to the U.S. This was a bold measure to up the pressure on President Nicolas Maduro to resign and cede power to National Assembly leader Juan Guaido, who many countries are now backing as the country’s true head of state. However, these sanctions come at a less-than-ideal time for American refiners in the Gulf of Mexico, where exports are picking up, as the sanctions could reduce the supply of oil for these refiners to process.

- According to analysts at Wood Mackenzie, new projects in the Democratic Republic of Congo (DRC), the world’s largest source of cobalt, will create a “tsunami” of new cobalt supply. The firm expects cobalt prices to average $29 per pound this year with downside risks due to oversupply. Bloomberg reports that Glencore said much of its cobalt production in the DRC this year will only be sold in 2020. The price of cobalt has fallen significantly as of late, down to around $20 per pound, far from its high of close to $45 last March. Lower prices have put pressure on Glencore’s profits.

- The Middle East was once a big importer of liquefied natural gas (LNG). However, imports fell 37 percent last year. This is in stark contrast to its demand in 2015 that outpaced global growth. Bloomberg writes that the main reason for the reduced demand for LNG is domestic gas resources have been found in Egypt and the United Arab Emirates (U.A.E.). Globally, demand for LNG remains strong and supply is expected to rise almost 18 percent by 2030.

Emerging Europe

Strengths

- Czech Republic was the best performing country this week, gaining 2.5 percent. Banks were the best performers on expectations of strong fourth quarter results. Moneta Bank gained 5.6 percent and Komercin Bank gained 4 percent.

- The Turkish lira was the best performing currency this week, gaining 1.3 percent against the dollar. The Federal Reserve’s dovish tone lifted the lira.

- Industrial was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 33 basis points. Equites trading on the Bucharest exchange continue to trade weaker after the government proposed to tax banks, telecom and energy companies to boost its income. This week the government published its 2019 budget proposal. Growth is assumed at 5.5 percent, inflation at 2.8 percent and the budget deficit at 2.55 percent.

- The Czech koruna was the worst performing currency this week, losing 26 basis points against the dollar. The central bank has tightened its rates by over 150 basis points since June 2016, and analysts expect the tightening cycle to continue this year.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- The dovish turn by the Fed this week, dropping any bias towards hiking rates and softening the rhetoric on balance sheet policy, is significant for emerging market assets, according to JPMorgan research. This week’s rally in emerging market equites and currencies could continue if positive news comes out of China-U.S. trade talks.

- Greece has sold a five-year bond, worth 2.5 billion euros, yielding 3.6 percent this week. It was the country’s first bond issuance since the end of its third bailout program in August of last year. The bond sale drew over 10 billion euros in demand, suggesting growing confidence among investors in the Greece’s economic recovery.

- Polish GDP was reported at 5.1 percent in 2018, higher than expected. Strong household spending supported by fiscal stimulus was the main diver of the country’s economic growth. Growth is expected to slow down to 3.6 percent this year, however, the country is expected to grow faster than the rest of Europe or the U.S.

Threats

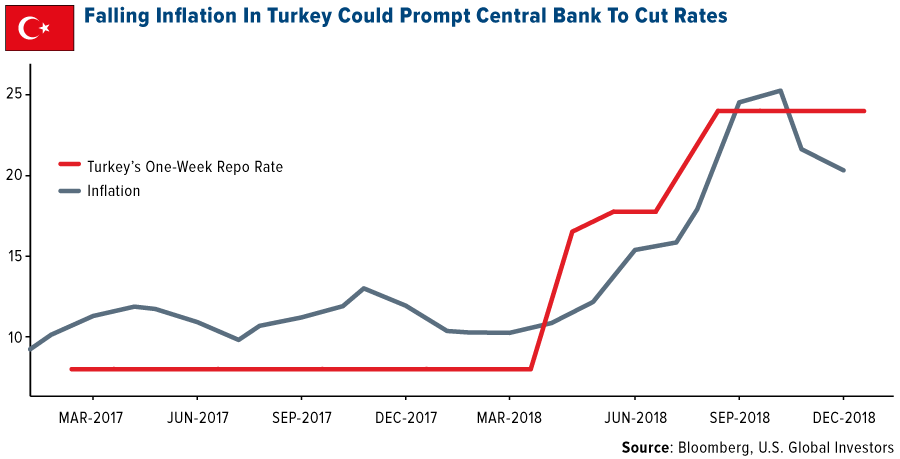

- Turkey’s central bank forecast inflation at the end the year at 14.6 percent, down from the previous call for 15.2 percent. Back in July of last year, the bank hiked its rate by 625 basis points to support the lira. Some analysts predict that falling inflation may open the door for a rate cut in the near future.

- Bloomberg reported that euro-area economic confidence extended its worst losing streak in a decade at the start of 2019, as member states faced trade uncertainties and domestic problem. The European Commission’s economic sentiment index dropped by more than forecasted in January, reaching the lowest in more than two years. According to Bloomberg, investors are positioning not for normalization in monetary policy, but for another long run of easy money.

- Italian GDP shrank 0.2 percent in the fourth quarter, followed by negative 0.1 percent in the third quarter. Analysts often define two straight quarters of declining GDP as a “technical recession.” However, Bloomberg Economists said the decline was probably due to budget woes and expect the slump had already ended.

China Region

Strengths

- Hong Kong’s Hang Seng Composite Index jumped 1.82 percent for the week, while Thailand’s SET Index climbed 1.72 percent for the week.

- China’s official Manufacturing PMI, while still in contractionary territory below 50, did beat expectations with a 49.5 print, coming in ahead of an anticipated 49.3. China’s Non-manufacturing PMI also beat, coming in at 54.7, ahead of analysts’ expectations for a 53.8 print.

- The U.S. and China reportedly made “tremendous progress” during this week’s high-stakes talks between President Donald Trump and China’s Vice Premier Liu He. Treasury Secretary Steven Mnuchin and U.S. Trade Representative Robert Lighthizer will meet with Chinese President Xi Jinping sometime later this month at least once. China is slated to pick up “substantially” its purchases of U.S. crops, energy and services, although these purchases may have been the easy money on the table, so to speak. Technology and intellectual property rights remain (presumably) sticking points as the talks migrate to Beijing next later this month. In the meantime, the U.S. and China continue to talk and work toward a resolution. President Trump affirmed that this is not the sort of deal one wants to renegotiate, that the deadline on tariffs as it stands remains intact, and that progress is being made, although “much work remains to be done.” Official Chinese outlets called the talks candid, specific, and fruitful. Trump is reportedly considering planning a meeting with President Xi, possibly near the time of the summit with North Korea’s Kim Jong Un.

Weaknesses

- Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite Index fell by 1.03 percent since last Friday, although the market was closed today for Federal Territory Day and so did not participate in the final weekday’s trading. Taiwan’s Capitalization Weighted Stock Index dropped 37 basis points for the week, narrowly edging out Singapore’s Straits Times Total Return, which declined by only 35 basis points.

- Conglomerates and utilities were the only two sectors to finish the week in the red in Hong Kong’s Hang Seng Composite Index, falling 76 basis points and 60 basis points respectively.

- China’s Caixin Manufacturing PMI missed expectations this week, clocking in at a contractionary 48.3, well shy of consensus for a 49.6 print. Next week we’ll get the Caixin Services PMI.

Opportunities

- Next week mainland Chinese equity markets will be closed for the Lunar New Year, as will Taiwan. Most other markets in the region will be closed for at least a portion of the week. Happy Year of the Pig, everybody! Given returns so far this year for emerging markets, and this week’s Fed statement, one is tempted to quote without further explanation a WSJ article headline from earlier in the week that stated rather simply, “Year of the Pig Lures Bulls.”

- Bloomberg News reported this week that Philippine economic growth should pick up this year to at least 7 percent, buoyed by spending on midterm elections and moderating inflation, according to Economic Planning Secretary Ernesto Pernia.

- A more dovish-sounding Fed this week put rate hikes on hold. Emerging markets rallied, with a distinct possibility of rallying further on a weaker dollar and/or more dovish Fed interest rate policy.

Threats

- The March 1 deadline for the U.S. imposition of further tariffs on China “remains intact,” according to the Trump administration, and without the tariffs, the president argued, the two sides wouldn’t even be talking. Thus while Larry Kudlow talked up the “good vibes” from the talks this week and both the U.S. and China hailed the progress made, there are still clear sticking points, and, at least until further notice, strict deadlines, before which the two sides will need to come to some sort of agreement, even if that includes extending the truce for some period of time. Headline risk around the U.S.-China trade negotiations remains a threat for the near future until resolution is reached and markets achieve more certainty.

- India placed heavy restrictions on what Amazon can sell in the country, while Amazon rival Flipkart will also presumably be forced to remove thousands of products from its service, the New York Times reported this week. “Flipkart could lose as much as a quarter of its sales in the short term, according to Technopak, an Indian consulting firm,” the article continues.

- Several major earnings reports this week highlighted the slowing pace of the Chinese economy, as (for example) companies from Caterpillar to Starbucks, and Apple to Nvidia noted slowdowns in China. While earnings reports are, by definition, backward looking, and some commentary on earnings calls did note some elements of improvement or slightly more optimistic tones, the numbers underscore the global risks posed by any real or potential Chinese slowdown and/or a trade war between the world’s two largest economies.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 1 was Bitcoiin, not to be confused with Bitcoin, up 827.52 percent.

- On Tuesday, cryptocurrency exchange and custodian Gemini Trust Co., founded by the Winklevoss twins, secured a critical third-party financial evaluation of its firm, reports MarketWatch. The examination, known as SOC for Service Organizations, evaluates Gemini’s design and internal security controls and was conducted and validated by Deloitte. The Winklevoss twins have emerged as leaders in the push for stricter regulation for the digital currency industry that has been stigmatized with scandals around manipulation and exchange hacks, the article continues.

- According to Bloomberg, Fidelity Investments is planning a March launch for its bitcoin custody service. Large investors at the mutual fund giant will have a range of cryptocurrency products, with bitcoin storage being one of the first. Ether custody is expected to be the second crypto service available, Seeking Alpha notes.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 1 was Consentium, down 63.87 percent.

- It looks like bitcoin’s painful 2018 is following the digital currency into the New Year, with prices touching the lowest in more than a month at the start of the week, reports Bloomberg. Since the weekend, bitcoin fell as much as 5.2 percent, with Ether and Bitcoin Cash both falling more than 10 percent. The major coins were mostly unchanged mid-week, trading near their 2019 lows.

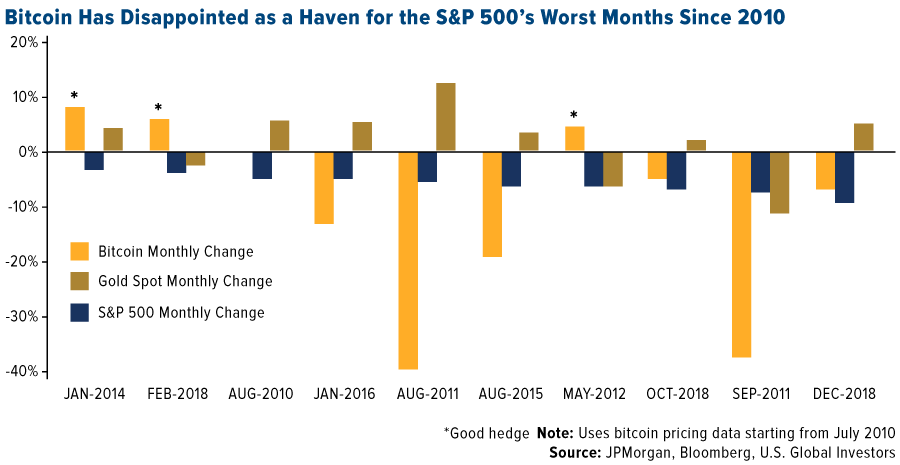

- One of the common arguments in bitcoin’s favor says that the digital currency is a good hedge against U.S. stock losses, writes Bloomberg. That argument isn’t holding up too well according to analysis from John Normand of JPMorgan Chase. As you can see in the chart below, during the 10 worst monthly performances for the S&P 500 (and since the earliest available bitcoin pricing on Bloomberg in July 2010), the digital currency showed a positive return in only three of those months, the article continues.

Opportunities

- One potential U.S. presidential candidate and former CEO of Starbucks Howard Schultz is one big name that still sees cryptocurrencies as a future part of a cashless, digital economy, reports Coindesk – even though Schultz has previously said he doesn’t see bitcoin, in particular, as a “legitimate” currency. Back in January 2018, Schultz told investors in a quarterly earnings call that he thinks blockchain technology has numerous potential uses, particularly when it comes to helping his company transition to new payment methods. And more recently, the article continues, Starbucks revealed last summer that it has been working with the Intercontinental Exchange on Bakkt, the upcoming futures exchange.

- Genesis Global Capital, an institutional cryptocurrency loans firm, reported processing nearly $1.1 billion in lends in borrows in 2018, writes Coindesk. In fact, the firm more than doubled its loan originations in the last three months of the year, compared to the previous six months. “Over the past year, through client feedback and the rise of derivative marketplaces, we saw a meaningful increase in the number of market participants wanting to borrow and/or lend digital currencies,” the firm stated in a report.

- As more and more companies need to prove they are meeting pledges to “go green,” the demand for tools to trace the original of renewable energy is rising in Europe, writes Bloomberg. In order to meet these needs, Acciona SA has developed a blockchain tool called Greenchain that could assist. Greenchain helps trace the origin of electricity in real time from any location, the article continues, echoing a similar product that Walmart patented in 2018.

Threats

- The armed wing of Hamas, an organization designated as a terrorist group in the U.S. and Europe, is cash-strapped and looking for funds, reports Bloomberg. In order to get around international restrictions on funding its organization, however, now the militant Palestinian group that rules the Gaza Strip is urging its supporters to donate in bitcoin to avoid constraints.

- New Zealand-based cryptocurrency exchange Cryptopia is still having trouble with stolen funds, reports Coindesk. In a post this week, blockchain data analytics firm Elementus said that Cryptopia’s hacker, after going quiet for some days, has stolen another $181,000 worth of Ether from 17,000 wallets. Just last week Elementus reported that $16 million worth of Ether and ERC-20 tokens had been stolen from Cryptopia wallets.

- According to data from CoinMkarketCap.com, over the past 12 months more than $400 billion in cryptocurrency market value has been wiped out, writes Bloomberg, with widespread adoption failing to materialize. Currently, total market capitalization stands around $113 billion.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 189.78 | +8.57 | +4.73% |

| Gold Futures | 1,322.40 | +18.20 | +1.40% |

| Natural Gas Futures | 2.74 | -0.44 | -13.81% |

| S&P/TSX VENTURE COMP IDX | 622.90 | +18.34 | +3.03% |

| 10-Yr Treasury Bond | 2.69 | -0.07 | -2.61% |

| Nasdaq | 7,263.87 | +99.00 | +1.38% |

| Oil Futures | 55.29 | +1.60 | +2.98% |

| Hang Seng Composite Index | 3,731.67 | +66.81 | +1.82% |

| S&P 500 | 2,706.17 | +41.41 | +1.55% |

| DJIA | 25,063.89 | +326.69 | +1.32% |

| Korean KOSPI Index | 2,203.46 | +25.73 | +1.18% |

| Russell 2000 | 1,501.91 | +19.06 | +1.29% |

| S&P Energy | 479.44 | +14.75 | +3.17% |

| S&P Basic Materials | 335.49 | +2.78 | +0.84% |

| XAU | 75.91 | +4.74 | +6.66% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.74 | -0.22 | -7.40% |

| S&P/TSX Global Gold Index | 189.78 | +4.51 | +2.43% |

| 10-Yr Treasury Bond | 2.69 | +0.07 | +2.52% |

| Oil Futures | 55.29 | +8.75 | +18.80% |

| Gold Futures | 1,322.40 | +31.90 | +2.47% |

| S&P 500 | 2,706.17 | +196.14 | +7.81% |

| S&P Energy | 479.44 | +46.59 | +10.76% |

| Hang Seng Composite Index | 3,731.67 | +375.98 | +11.20% |

| DJIA | 25,063.89 | +1,717.65 | +7.36% |

| Korean KOSPI Index | 2,203.46 | +193.46 | +9.62% |

| Nasdaq | 7,263.87 | +597.93 | +8.97% |

| S&P Basic Materials | 335.49 | +17.44 | +5.48% |

| Russell 2000 | 1,501.91 | +146.00 | +10.77% |

| S&P/TSX VENTURE COMP IDX | 622.90 | +51.90 | +9.09% |

| XAU | 75.91 | +4.97 | +7.01% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.74 | -0.50 | -15.38% |

| 10-Yr Treasury Bond | 2.69 | -0.44 | -14.18% |

| DJIA | 25,063.89 | -316.85 | -1.25% |

| Oil Futures | 55.29 | -8.40 | -13.19% |

| S&P 500 | 2,706.17 | -34.20 | -1.25% |

| Gold Futures | 1,322.40 | +71.70 | +5.73% |

| S&P Energy | 479.44 | -22.08 | -4.40% |

| Nasdaq | 7,263.87 | -170.19 | -2.29% |

| Korean KOSPI Index | 2,203.46 | +179.00 | +8.84% |

| S&P Basic Materials | 335.49 | -3.11 | -0.92% |

| Russell 2000 | 1,501.91 | -43.07 | -2.79% |

| Hang Seng Composite Index | 3,731.67 | +318.07 | +9.32% |

| S&P/TSX Global Gold Index | 189.78 | +23.48 | +14.12% |

| S&P/TSX VENTURE COMP IDX | 622.90 | -22.05 | -3.42% |

| XAU | 75.91 | +8.72 | +12.98% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Glencore PLC

IAMGOLD Corp

Eldorado Gold Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Economic Sentiment Indicator (ESI) is a composite indicator made up of five sectoral confidence indicators with different weights: industrial, construction, services, consumer and retail trade. It is published monthly by the European Commission. The FTSE Bursa Malaysia KLCI, also known as the FBM KLCI, is a capitalization-weighted stock market index, composed of the 30 largest companies on the Bursa Malaysia by market capitalization that meet the eligibility requirements of the FTSE Bursa Malaysia Index Ground Rules. The index is jointly operated by FTSE and Bursa Malaysia. The Taiwan Capitalization Weighted Stock Index is a stock market index for companies traded on the Taiwan Stock Exchange. The FTSE Straits Times Index (STI) is a capitalization-weighted stock market index that is regarded as the benchmark index for the Singapore stock market. It tracks the performance of the top 30 companies listed on the Singapore Exchange. The SET Index is a Thai composite stock market index which is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year. The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of U.S. consumer confidence levels conducted by the University of Michigan. It is based on telephone surveys that gather information on consumer expectations regarding the overall economy.