Investor Alert

Remembering 9/11 on the 20th Anniversary

Date Posted: September 10, 2021

Read time: 46 min

Twenty years ago tomorrow, I was in Manhattan with colleagues, attending a financial industry conference.

At the time, we didn’t know how fortunate we were that our 9:00 a.m. meeting had been changed to 11:00 a.m.

I was on route when the unimaginable happened. The cell phones in the city stopped working, but mine had a San Antonio area code, so I was able to get through to the U.S. Global Investors office to let everyone know we were safe.

With me were two company executives and the extraordinary Nancy Holmes (no relation, although she would often joke that I was her adopted son). She was advising my company as a PR strategist at the age of 82.

I’ve written about Nancy before. She led one of the most interesting and full lives I have ever known. She was a code clerk for the U.S. Army, a model in Paris for Balmain, a photojournalist for Columbia Pictures and a bestselling author and editor, including editor-at-large for Worth magazine. Like me, she was a world traveler, but in that dark hour we all just wanted to go home to Texas.

The night of 9/11, New York City completely shut down. The cabs disappeared and the subways stopped running. The airports would remain closed for many days.

The next morning, I found a driver to take us to New Jersey, where I had reserved one of the last available rental cars in the area. The four of us loaded into a Ford Expedition and began the long ride home. An adrenaline rush enabled me to drive us straight through for 30 hours.

We turned off the car radio because the nonstop coverage of the tragedy was too much to bear. Instead, Nancy entertained us with stories of her incredible trailblazing life, including her close friendships with the rich and famous, from Joan Collins and Elizabeth Taylor to Sean Connery and former hedge fund manager Julian Robertson. A bright light, Nancy passed away in 2007.

On the 20th anniversary of 9/11, I remember all the people who didn’t get to return home to their families, and I give thanks that I was among those lucky enough to do so.

Managing One Crisis to the Next

So much of life is managing risk. That’s true on a micro, personal-level scale as well as a macro, country-level scale. Crises often can’t be prevented, but how you deal with them makes all the difference.

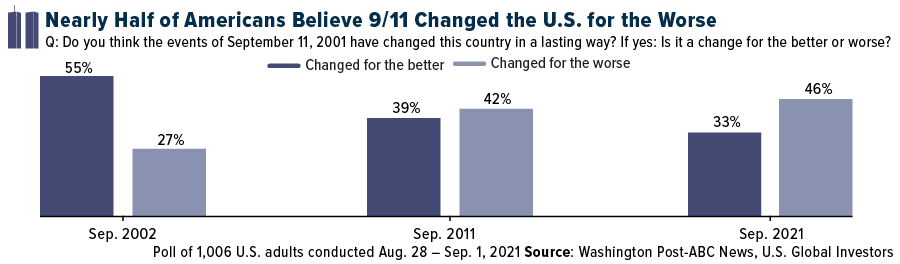

Here we are 20 years following 9/11, and one poll shows that a growing percentage of Americans believe the event changed the country for the worse. According to the poll, which was conducted between August 28 and September 1, more than eight in 10 Americans say the events of that day changed the U.S. in a lasting way. Of those, 46% say the change has been for the worse. That’s up from the 42% who said the same in 2011, and way up from the 27% one year after 9/11.

I can’t definitively say why people feel this way. I will point out that the terrorist attacks handed us the Transportation Security Administration (TSA), the Department of Homeland Security and the PATRIOT Act, all of which some see as unfavorable government overreaches.

This makes me wonder how people will reflect on our handling of the current health crisis one year, 10 years and 20 years into the future. Will the decisions made by today’s leaders be revered, or will they be reviled? I’m thinking specifically of President Joe Biden’s announcement this week that people working in businesses with more than 100 employees must either get vaccinated or else submit to weekly health screenings.

Then there are the lockdowns. I’ve heard some suggest that the states and countries that have enacted the most restrictive lockdown measures have among the most fragile health care systems. Perhaps a consequence of the pandemic should be that we strengthen health care, including responsiveness, equity and efficiency.

Toward that end, we should focus on preventing the underlying medical conditions that worsened many COVID patients’ diagnosis and recovery. A July report by the Centers for Disease Control and Prevention (CDC) found that a vast majority of Americans hospitalized with COVID between March 2020 and March 2021 suffered from at least one other underlying health issue, the most frequently observed being critical hypertension (50% of cases), disorders of lipid metabolism (49%) and obesity (33%).

Where’s the Yield?

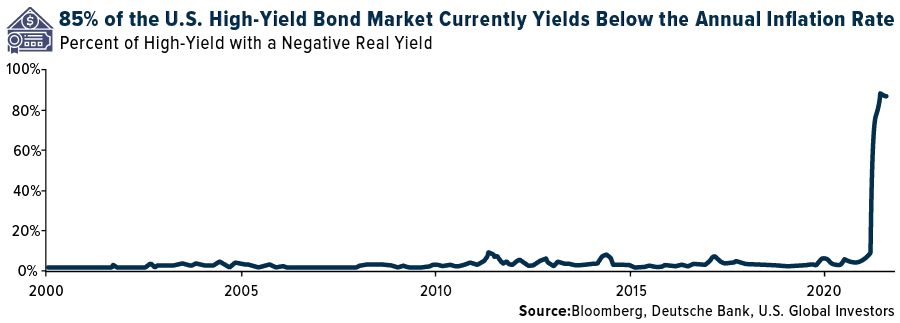

Speaking of managing risk, with real rates below zero, many yield-starved investors are being forced into riskier and riskier assets, including high-yield junk bonds. But even these are no longer offering a positive real return, what with inflation at multiyear highs.

According to one estimate, by Deutsche Bank’s Jim Reid, a whopping 85% of the U.S. high-yield bond market currently yields below the annual inflation rate. It’s important to note that this figure has never been above 10% in the past. Even if the consumer price index (CPI) were to fall to 3% (from 5.4% currently), that would still be above 35% of the high-yield market.

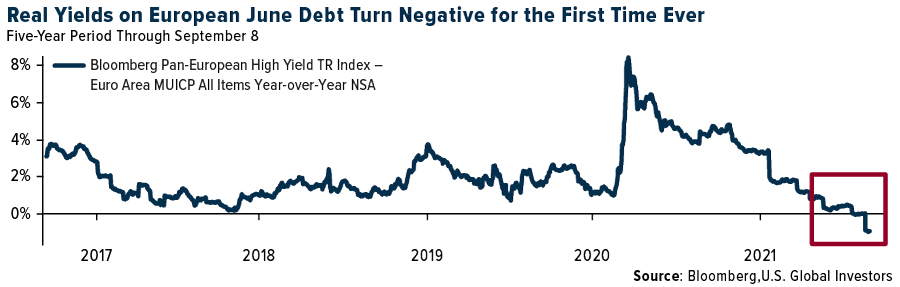

And it’s not just the U.S. For the first time ever, inflation-adjusted yields on junk-rated debt have turned negative after consumer prices increased the most in over a decade in Europe.

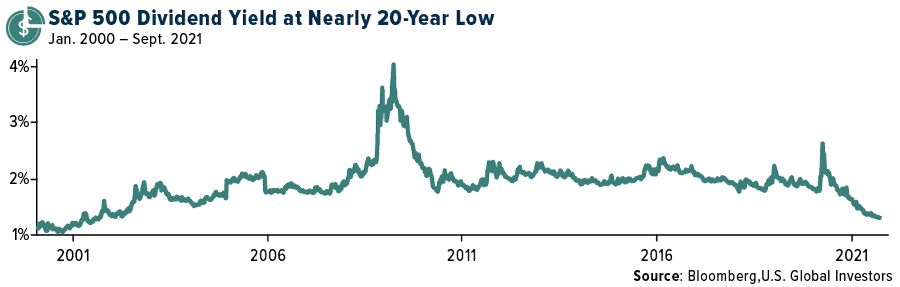

Stock prices have gained significantly so far this year, which is good, but this has the effect of making the dividend yield look less appealing. As of today, the S&P 500 dividend yield was 1.32%, the lowest point since March 2002, and well below the annual inflation rate.

So, where’s the yield? Some investors had hoped to try their hand at crypto lending, but the future legality of this activity is now in the air.

Coinbase’s Crypto Lending Program Halted by Regulators

Before I proceed, it’s important to note that crypto lending isn’t entirely new. Similar to securities lending, it allows investors to earn interest on select crypto assets. Some online platforms have already been letting customers lend out their assets in exchange for income.

But not Coinbase, the largest U.S. cryptocurrency exchange, which has been hoping to launch its own crypto lending platform for months.

That’s because the Securities and Exchange Commission (SEC) has warned the company that if it takes the next step in launching the service, nicknamed Lend, the SEC will sue. Making matters worse, the SEC refuses to explain what law Coinbase is in danger of violating; nor will it give guidance on how Coinbase can launch Lend and still comply with federal securities law. That’s according to Coinbase’s chief legal officer Paul Grewal, who detailed the company’s legal struggles this week in a blog post.

All Coinbase knows at this point, Grewal writes, is that it can “either keep Lend off the market indefinitely without knowing why or we can be sued.” He adds that regulatory uncertainty and ambiguity “only serve to unnecessarily stifle new products that customers want and that Coinbase and others can safely deliver.”

Indeed, investors are starving for yield right now, and it appears some will remain so.

As I’ve said before, commonsense regulations are important to help maintain a safe, level playing field for all parties. Imagine a basketball game with no referees. Cheating would have no repercussions. Now imagine the same game, but with many referees, and with the rules changing arbitrarily. Unfortunately, that’s the scenario Coinbase finds itself in right now.

For more news and updates on this unique and up-and-coming industry and other major markets, subscribe to Frank Talk at usfunds.com/subscribe.

Index Summary

- The major market indices finished down. The Dow Jones Industrial Average lost 2.15%. The S&P 500 Stock Index fell 1.69%, while the Nasdaq Composite lost 1.61%. The Russell 2000 small capitalization index lost 2.81% this week.

- The Hang Seng Composite gained 0.84% this week, while the KOSPI fell 2.35%.

- The 10-year Treasury bond yield gained 2 basis points to finish at 1.28%.

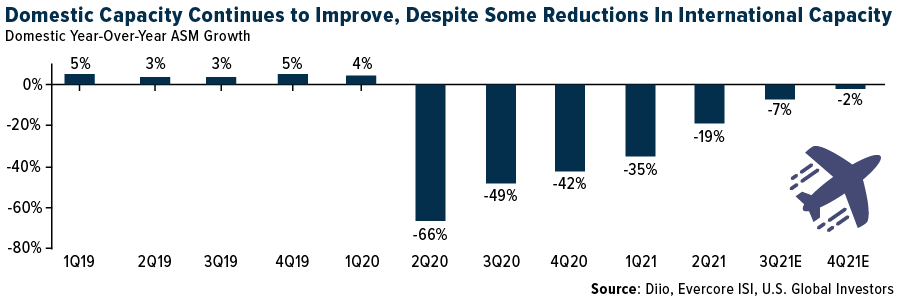

Airline Sector

Strengths

- The best performing airline stock for the week was Hainan Air, up 14.3%. In Europe, bookings increased 27% this week, the highest weekly growth since January 2021. International net sales declined by 5 points to -75% (versus -70% in the prior week) but grew 14% this week due to the base being much lower in 2019.

- British Air is reducing costs. The airline’s pilots are set to be paid less than their budget airline counterparts at easyJet underwent sweeping reforms to the U.K. flag carrier’s short-haul operation at Gatwick Airport. Industry insiders say junior BA captains will be paid less than £100,000 British pound sterling (GBP) a year under the new deal, less than the GBP 108,000 starting salary paid to their peers at easyJet.

- American Airlines is taking another step to encourage workers to get vaccinated against COVID-19. The company told workers in a memo late last week that it will stop offering a special pandemic leave to unvaccinated workers starting next month. “Going forward, given there is an FDA-approved vaccine, pandemic leave will only be offered to team members who are fully vaccinated and who provide their vaccination card to us,” the company executives wrote in the memo.

Weaknesses

- The worst performing airline stock for the week was easyJet, down 13.50%. Global system net sales were down 63.6% versus 2019 levels. Likewise, domestic and international stocks were down 32.1% and 46.5%, respectively, versus 2019. Pricing softened another 3% to 6% in all channels this week, which reflects the seasonal decline in leisure travel, increase in delta variant cases, and the lack of corporate demand.

- The labor union representing American Airlines pilots said it will begin informational picketing in the coming weeks at the carrier’s major hubs to protest their work schedule, fatigue, and lack of adequate accommodation over the summer months.

- American Airlines is witnessing a business slowdown. Revenues at American are 6 points lower than expected in the current quarter, falling from a 20% drop in the third quarter to a 26% drop. The airline’s expected net loss will widen in the third quarter due to the revenue shortfall.

Opportunities

- At a Bank of America conference, Japan Air said the industry is lobbying for vaccinated travelers to be exempted from 14-day quarantines and hopes there could be some changes made as early as autumn with the new Japanese Prime Minister. They are confident that leisure travel will be stronger with post-COVID demand boosted by pent-up pressure and changes in lifestyles. Japan Air hopes to capture leisure demand through its growing low-cost carrier portfolio where it is confident it can achieve strong operating margins, and the airline also looks to gain market share in transpacific travel with foreign competitors slowly to restore capacity.

- Daily website visits for EU airlines were up by 3 points to -18% versus 2019 levels (and compared to the -21% in the prior week). Turkish Airlines showed the biggest improvement of +10 points, followed by Lufthansa at +7 points.

- EasyJet yesterday announced a GBP £1.2 billion capital raise, a new $400 million revolving credit facility, and disclosed an unsolicited takeover offer, which was rejected by its board. However, its new guidance for FY1Q22 capacity at 60% of 2019 levels and mid-term EBITDAR margin of mid-teens is far below its competitors.

Threats

- U.S. airlines website visits are -4% for the week compared to flat last week. The only airlines to remain above 2019 levels this week are Southwest (+8%) and JetBlue (+1%). All other carriers had negative comparisons.

- Alaska Airline’s third quarter revenue is expected to be down 20% with non-fuel costs slightly higher. The carrier did not see the operational challenges that some carriers experienced, perhaps related to a more conservative growth plan. As expected, case growth has had some impact on bookings: July was strong and August slipped a bit, while September will take the biggest hit.

- Third quarter planned growth for U.S. carriers based on current scheduling data is 0.30% lower versus the last update at down 18% versus 2019 levels (-7% domestic, -44% international). Fourth quarter schedules indicate a 6% capacity decline (-2% domestic, -18% international), 4.2% lower due to broad based cuts over the last three weeks.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 1.1%. The best performing country in Asia this week was China, gaining 3.7%.

- The Russian ruble was the best relative performing currency in emerging Europe this week, losing only 0.20%. The Indonesian rupiah was the best performing currency in Asia this week, gaining 0.30%.

- China reported stronger trade data. Exports grew by 15.7% year-over-year versus expected growth of 8.4%. Imports grew by 23.1% versus expected 18.5%. Trade balance in August was reported at $58.34 billion compared to $56.58 billion in July and expected $53.20 billion.

Weaknesses

- The worst performing country in emerging Europe for the week was Turkey, losing 1.8%. The worst performing country in Asia this week was South Korea,losing 3.4%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 1.2%. The South Korean won was the worst performing currency in Asia this week, losing 1.0%.

- The Eurozone Investors’ Confidence Index declined to 19.6 in September from 22.2 and ZEW survey that measures the expectation of the economic growth in the euro area fell to 31.1 from 42.7.

Opportunities

- The European Central Bank will continue its emergency monthly bond buying program at a slightly slower pace but is not planning to end the Pandemic Emergency Purchase Program (PEPP), which has kept borrowing costs low and helped the economy to recover from the negative effects of the pandemic. The bank left the rates unchanged and said inflation may moderately exceed its goal for a transitory period.

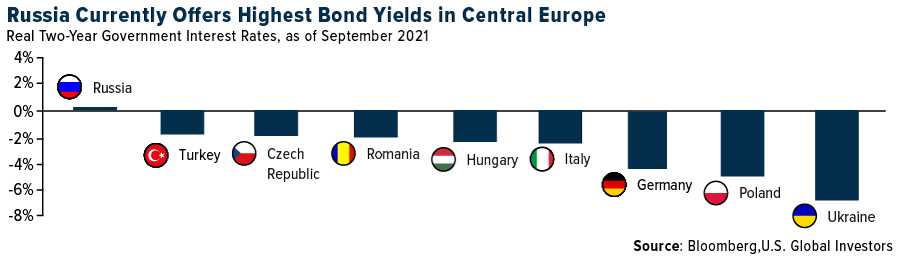

- Money has been flowing into Russia as it offers positive real rates attracting investors looking for higher yielding instruments. The Russian economy has been supported by stronger oil and gas prices. The country’s extra revenue from the sale of oil and gas will be spent on social benefits that will further boost the economy and improve living conditions.

- Chinese gaming firms including Tencent and NetEase were asked by the Chinese government to ensure they implement new rules for the sector. They were told last month to limit kids access to their video games and end focus on profits in gaming. CLSA, the leading and longest running brokerage and investment group in Asia, thinks that this creates opportunity for companies that focus their business model on listening, music, streaming, and podcasting.

Threats

- Fitch Ratings cut the ratings of China Evergrande Group and two of its subsidiaries on Wednesday targeting the property firm over its struggles to restructure huge debts. There is a growing concern among investors that the company may default; it has more than $300 billion in liabilities.

- China retail sales, which will come out next week, most likely will show a slowdown in sales. Bloomberg economists predict the data to show retail sales growing at 7% on year-over-year basis in August, down from 8.5% in July. Another outbreak of COVID-19 cases in the later summer months and imposed restrictions have most likely negatively affected the retail sales.

- Poland once again may be fined by the European Commission over the rule-of-law disagreement. Poland was given a deadline of August 16 to halt a controversial regime to discipline judges and has since failed to meet the EU request, sparking talks about imposing monetary disciplinary action in central emerging Europe’s largest country. Back in 2017, the EU’s top court gave Poland two weeks to stop increased logging in the Bialowieza forest or face fines of at least 100,000 euros per day.

Energy and Natural Resources Market

Strengths

- Aluminum prices are the highest in a decade as the coup in Guinea has clouded the supply outlook, reports Bloomberg, with the risk of mining disruption threatening to expedite the global market’s descent into deepening deficits. One leading supplier, United Co. RUSAL International PJSC, warned it may need to evacuate staff if the situation deteriorates.

- Western lumber pricing continued to make gains this week with mills reporting their strongest sales in months. Prices ended the week up 8% at $425 per thousand board feet, down 62% relative to the second quarter of the year, down 55% year-over-year, and up 76% year-to-date.

- U.S. natural gas prices have broken out of the $3.85-$4.15 per metric million British thermal unit (mmBtu) trading range since late-July, rallying approximately 20% in the past week to $4.71/mmBtu. The move was initially triggered by a large surprise in storage injections, which has added to existing winter storage concerns, further increasing the winter risk premium priced in the market.

Weaknesses

- The Chilean Copper Commission reported copper production at 465 kt in July, which is flat versus the previous year. Production saw a decline of 3% month-to-month. Year-to-date copper production in Chile currently totals 3,262,000 tons, 1% below 2020 levels (3,297,000 tons). Peru’s Ministry of Mines and Energy reported that copper mining production in July decreased 4% year-to-year.

- Hurricane Ida appears to have most impacted the Chlor-Alkali and Vinyls chains. While overall damage assessments remain underway, early indications suggest that the bulk of chemical production in the Baton Rouge area has returned to full operation while facilities in the southern Louisiana region (i.e., Taft, Plaquemine, Geismar, etc.) remain shut down. Chemical producers have largely been reporting limited physical damage to facilities. However, several factors including restoration of power, utilities, hydrogen / nitrogen supply, feedstocks availability and logistics continue to limit the restart of facilities across this southern Louisiana region.

- According to Goldman Sachs, after a strong share price performance between January and May 2021 for refining (up 40%), the performance of the group has broken down from June to September (refining as measured by the S&P 1500 now only up 17% year-to-date). The bank attributes the recent weakness in the equities to (1) demand and COVID concerns, consistent with negative recent global GDP revisions, (2) tight inland crude differentials and (3) negative earnings-per-share (EPS) revisions around the second-quarter earnings season.

Opportunities

- China’s steel industry consolidation has been showing signs of acceleration in recent months, with seven major merger and acquisition (M&A) related transactions announced over the July to August timeframe, bumping up the share of China’s top five steelmakers’ output in the process. The Asian nation wants its top five steelmakers to account for 40% of the country’s total steel output by 2025, as it aims to meet its ambitious decarbonization goals. China’s steel industry accounts for around 15%-20% of national carbon emissions, annually. The recent M&A transactions have raised the share of China’s top steelmakers from 26% to 30% of total steel production.

- The European Union (EU) is suggesting that the U.S. impose tariff-rate quotas on steel and aluminum imports in a bid to reach an agreement with the U.S. on exempting the EU from its Section 232 measures, sources told FastMarkets. The U.S. and EU are widely expected to reach an agreement by November 1, 2021, on an exemption for European steel and aluminum.

- Coal was up 12% this week to $289 per ton. Imported met coal into China was up 9.3% this week to $470 per ton. Met coal was up again as supply disruptions in China drove further market tightness, outweighing weaker steel demand due to production cuts.

Threats

- Bank of America is sticking to its view that U.S. exploration and production (E&P) capital expenditure (capex) could be up about 30% in 2022. This includes year-over-year Private / Public E&P capex growth of 50% / 20%. Adjusted for M&A, the Private E&P rig count is now up 85% year to date, with activity clearly driven more by robust wellhead economics than capital discipline. This drilling could have a negative impact on oil prices.

- Oil weakened as the dollar rose this week, offsetting bullish Chinese trade data that added to positive economic signs emerging from key energy users. A stronger dollar is making commodities priced in the currency less attractive. Prices earlier got a lift from a surge in Chinese trade data, suggesting sturdy demand for goods in the U.S. and Europe.

- Coal shipments fell on the month, hampered by the delta variant outbreak in key supplier regions like Indonesia and Mongolia. Coal cargoes have slipped 10%, helping to boost domestic futures markets to record highs.

Domestic Economy and Equities

Strengths

- Weekly initial jobless claims came in at 310,000, a new pandemic low, and the seventh consecutive week below 400,000 claims. The number came in below the consensus of 335,000 and prior’s week upward revised 345,000.

- New York city edges close to normal pre-pandemic life. The city’s entire municipal labor force, the largest in the nation, will return to work on Monday. Furthermore, on Monday, New York City students will return to public schools.

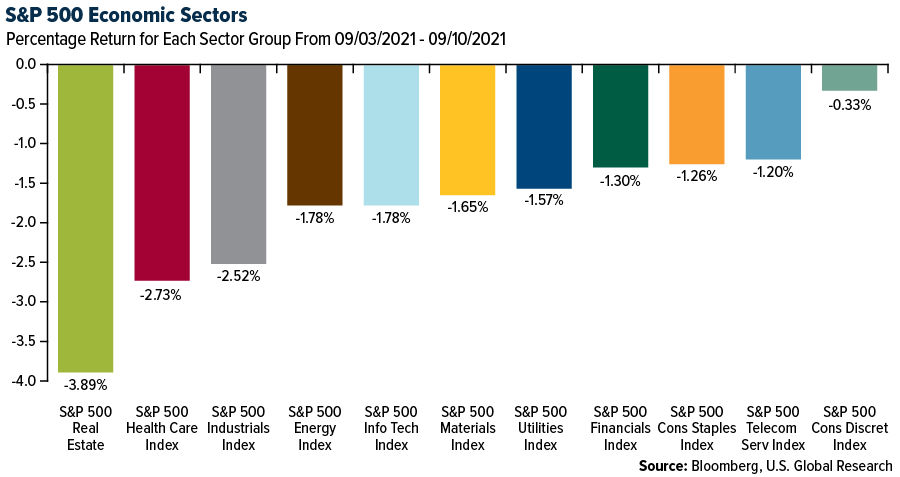

- Moderna was the best performing S&P 500 stock for the week, increasing 7.99%. The company has announced the development of a single-dose vaccine shot that is a combination of a Covid-19 booster as well as a seasonal flu jab.

Weaknesses

- Job openings outnumbered the unemployed by more than 2 million in July as companies struggled to fill a record number of vacancies, the Labor Department reported on Wednesday. The department’s Job Openings and Labor Turnover Survey showed 10.9 million positions are available. This is much higher than the FactSet estimate of 9.9 million openings and the June total of 10.18 million openings.

- The Market Composite Index, a measure of mortgage loan application volume, decreased by 1.9% on a seasonally adjusted basis from one week earlier. The Refinance Index decreased 3% from the previous week and was 4% lower than the same week one year ago.

- PulteGroup was the worst performing S&P 500 stock for the week, losing 11.23%. Their shares declined after PulteGroup released an update to guidance that is below prior guidance provided in the late July.

Opportunities

- Over seven million people stopped receiving unemployment benefits after the Labor Day weekend as the pandemic safety payments expired. The White House has said that there are no plans to expand federal unemployment benefits any further, The Associated Press reported. Due to the added pressure of no more unemployment benefits, companies may be able to fill up open positions before the busy shopping season ahead.

- President Joe Biden on Thursday ordered all federal workers and contractors to be vaccinated. Biden last month said he would impose staff vaccination requirements on all federally funded nursing homes, a directive expected to cover roughly 15,000 facilities employing 1.3 million people. Now, he is extending the order to a far wider group of providers, including major hospitals across the nation that receive Medicare or Medicaid funding. This move should boost vaccination rates and to help stop the spread of the coronavirus.

- President Biden held a meeting over a phone call with Chinese President Xi, the first phone call since February suggesting possible openness to further talks. American firms in China were counting on a meeting between Presidents Joe Biden and Xi Jinping this year, as they look for relief from trade barriers raised during the Trump administration.

Threats

- The market turned toward pessimism this week. FactSet reported that investors worry about an economic drag from Delta, a likely approach of a Fed taper, the looming debt-ceiling fight, and uncertainty about the $3.5 trillion stimulus bill.

- U.S. economic growth slowed over the summer as a surge in COVID-19 cases driven by the highly contagious delta variant forced consumers to pull back on spending, according to a new Federal Reserve report. In its region-by-region roundup of anecdotal information known as the Beige Book, the Fed reported that growth overall had “downshifted slightly to a moderate pace” during the July through August period that the report covers.

- Inflation will be released next week; it will most likely stay at an elevated level. Bloomberg economists predict the inflation to increase 5.3% on year-over-year basis. The inflation excluding food and energy is expected to raise 4.3% year-over-year.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Plethori, up 2,775%.

- Multinational payments giant Visa announced that it is planning to bring cryptocurrency services to traditional banking platforms in Brazil, reports Bitcoin.com. The credit card giant also said it is working with several crypto companies in the country to bring cryptocurrency payment cards to the market and hinted at a possible direct integration of Bitcoin in payments.

- The Harmony Foundation of the Harmony company, a proof-of-stake blockchain that claims to process transactions in two seconds at a low cost, is allocating more than $300 million in the network’s ONE token over a span of four years to attract projects. The initiative aims to support 10,000 startups with bounties, grants, and other scholarships. “We think that Harmony has the right vision for creating wealth together, for having the infrastructure and platform to do it,” Harmony founder Stephen Tse told CoinDesk on Thursday.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Didcoin, down 99.93%.

- Thailand’s SEC has temporarily suspended the services of the local branch of crypto exchange Huobi, reports CoinTelegraph, and recommended revoking its operating license with the Ministry of Finance. Huobi received the suspension order after failing to comply with local regulations related to its operations and management structure. With the suspension in place, the crypto exchange has been given three months to return all assets to its clients, the article states.

- According to CoinTelegraph, reports have emerged that a bug on OpenSea’s marketplace has deleted user owned non-fungible tokens (NFTs) valued at 28.44 Ether (ETH), equaling $100,000 USD in cost. Nick Johnson, lead developer of Ethereum Name Service (ENS), relayed the information after reportedly losing an NFT that was linked to the first ENS named rilxxlir.eth. (ENS is a naming system that allows users to store text-based content as an NFT on the Ethereum blockchain).

Opportunities

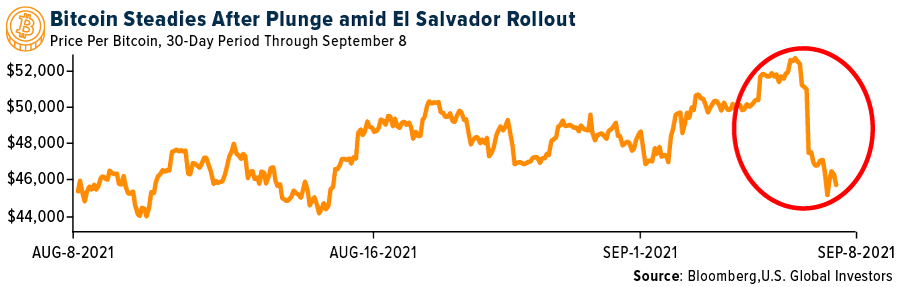

- Bitcoin is undergoing the biggest test in its 12-year history, writes Bloomberg, as El Salvador becomes the first country to adopt it as legal tender on Tuesday. Many will be monitoring the experiment to see if a significant number of people want to transact with Bitcoin when it circulates alongside the dollar, the article continues, and whether it brings any benefits to the violent, impoverished Central American nation.

- Following El Salvador making Bitcoin legal tender, privacy activist and whistleblower Edward Snowden says, “there is now pressure on competing nations to acquire Bitcoin — even if only as a reserve asset.” He warned, “Latecomers may regret hesitating.” Other countries are expecting to follow in El Salvador’s footsteps if adopting Bitcoin as legal tender proves to cause the cost of remittances to drop significantly. If so, according to Dante Mossi, executive president of the Central American Bank for Economic Integration (CABEI), “other countries will probably seek that advantage and adopt [Bitcoin]” as well.

- Golden State Warriors guard Stephen Curry has been signed as an “FTX global ambassador,” reports CoinDesk. Earlier this year, National Football League player Tom Brady and his wife also made a similar deal with FTX. This cryptocurrency derivatives exchange company is looking to seize the opportunity following recent stumbles by competing with Binance and surging interest in crypto trading in the U.S. The partnership with Curry extends FTX’s National Basketball Association foray beyond stadium naming rights. “I’m excited to partner with a company that demystifies the crypto space and eliminates the intimidation factor for first-time users,” Curry said in a press release.

Threats

- Before El Salvador’s launch of Bitcoin as legal tender on Tuesday, the country bought 400 Bitcoins (valued at $20 million USD), helping to drive the cryptocurrency’s price above $52,000 for the first time since May. Unfortunately, hours later, Bitcoin weakened and last traded down 0.51% at $46,561.74 USD, reports Reuters. Some El Salvadorians have taken to the streets in protest of the volatile digital currency, worried for their financial futures with Bitcoin as legal tender given half the country doesn’t have access to the necessary technology needed to use it.

- As reported by Bitcoin.com, 14 suspects allegedly behind a cryptocurrency scam have been arrested in Taiwan. According to the country’s Criminal Investigation Bureau (CIB), the scam allegedly defrauded more than 100 people out of about $5.41 million over the past year. On Sunday, the Taipei Times reported that the suspects now face charges of fraud, money laundering, and breaches of the country’s Organized Crime Prevention Act.

- The SEC is threatening to sue Coinbase Global, Inc., a U.S.-based cryptocurrency exchange platform, over its yet-to-be-launched “Lend” program. This program would give users 4% interest on deposits of the stablecoin USDC, with other assets to be added later. Despite ongoing discussions with the SEC, Coinbase was still issued a “Wells Notice,” reports CoinDesk on September 7. In a tweet thread on Tuesday, Coinbase CEO Brian Armstrong said his company had complied with all the SEC’s requests including providing subpoenaed records and testimony from employees. Unfortunately, this situation has resulted in Coinbase shares sinking, causing the stock ($COIN) to slide 4.1% on Nasdaq to $256.

Gold Market

This week spot gold closed the week at $1,788.35, down $39.37 per ounce, or 2.2%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.1%. The S&P/TSX Venture Index came in off 1.8%. The U.S. Trade-Weighted Dollar rose 0.6%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-7 | Germany ZEW Survey Expectations | 30.5 | 3.9% | 3.8% |

| Sep-7 | Germany ZEW Survey Current Situations | 34 | 1.6% | 0.7% |

| Sep-9 | ECB Main Refinancing Rate | 0% | 113.8 | 125.1 |

| Sep-9 | Initial Jobless Claims | 335k | 113.8 | 125.1 |

| Sep-10 | Germany CPI YoY | 3.9% | 49.2 | 50.3 |

| Sep-10 | PPI Final Demand YoY | 8.2% | 374k | 326k |

| Sep-14 | U.S. CPI YoY | 5.3% | — | 5.4% |

| Sep-14 | U.S. CPI Ex Food and Energy YoY | 4.2% | — | 4.3% |

| Sep-14 | China Retail Sales YoY | 7% | — | 8.5% |

| Sep-14 | China Industrial Production YoY | 5.8% | — | 6.4% |

| Sep-14 | China Surveyed Jobless Rate | 5.1% | — | 5.1% |

| Sep-15 | U.S. Empire Manufacturing | 18 | — | 18.3 |

| Sep-15 | U.S. Industrial Production MoM | 0.4% | — | 0.9% |

| Sep-15 | EU Industrial Production WDA YoY | 6% | — | 9.7% |

| Sep-16 | U.S. Initial Jobless Claims | 320k | — | 310k |

| Sep-17 | U.S. University of Mich. Sentiment | 72.3 | — | 70.3 |

| Sep-17 | EU CPI YoY | 3% | — | 2.2% |

| Sep-17 | EU CPI Core YoY | 1.6% | — | 1.6% |

Strengths

- The best performing precious metal for the was gold, even though it was down 2.2%. K92 Mining reported the latest assay results from its ongoing drilling program at the Kora deposit at the Kainantu Mine. These 32 diamond drill holes once again showcased the high-grade and continuous nature of Kora, with eight intersections exceeding 20 grams per ton (g/t) of gold equivalent grade (AuEq), 24 intersections exceeding 10 g/t AuEq and 41 intersections exceeding 5 g/t AuEq.

- Pure Gold is now formally guiding to operating rates of 1,000 tons per day by year end, 25% above the original design of 800 tons per day, with increased production rates from both the Main and East ramps. The net impact is that 2022-2024 free cash flow estimates have increased.

- Montage Gold announced the granting of a new exploration license and results from the Petit Yao Central target, both within trucking distance of the Kone Gold Project in Cote d’Ivoire. With infill drilling at Kone complete, Montage’s geological team is now focused on district exploration. The discovery of high-grade satellite deposits within trucking distance of Kone could have a material impact on the economics.

Weaknesses

- The worst performing precious metal for the week was palladium, down 11.8%. Gold slipped as Treasury yields advanced following the Labor Day holiday, ahead of auctions that will test appetite for U.S. government debt. Rates on the bonds had already surged following last Friday’s weaker-than-expected jobs report, limiting the upside for non-interest-bearing gold. Some investment banks have cut forecasts for U.S. growth this year, citing a “harder path” ahead for American consumers than expected.

- Exchange-traded funds (ETFs) continue to sell gold, bringing this year’s net sales to 7.27 million ounces, according to data compiled by Bloomberg. Total gold held by ETFs fell 6.8% this year to 99.8 million ounces.

- Sibanye Stillwater’s gold output may decline from 2025 with the planned closure of its Beatrix mine, head of the company’s South African gold division, Richard Cox, said on a call with investors. Beatrix’s remaining reserves support a five-year mine life.

Opportunities

- Gold Royalty Corp. (GROY), Abitibi Royalties (RZZ) and Golden Valley (GZZ) are combining, reports Yahoo! Finance. Under the terms of agreement, each RZZ shareholder will receive 4.61 shares of GROY, while each GZZ shareholder will receive 2.14 GROY shares. This implies a price of $25.33 per share of RZZ and $11.76 per share of GZZ, representing a premium of 22% and 86%. Post the transaction, the combined company is expected to have six royalties owned on operating mines with an additional 14 Feasibility/PEA stage royalties. The combined company is also expected to have $47 million cash and no debt.

- i-80 Gold Corp. said that it will create a comprehensive Nevada mining complex by acquiring certain processing infrastructure and gold deposits in Nevada. The gold producer and developer said it agreed to an asset exchange with Nevada Gold Mines LLC, which will include an autoclave as well as the Lone Tree and Buffalo Mountain gold deposits. The company also entered a definitive membership interest purchase to acquire Ruby Hill Mine from affiliates of Waterton Global Resource Management. As part of the agreement with Nevada Gold Mines, i-80 will exchange its 40% ownership in the South Arturo Property in Nevada and assign its option to acquire the adjacent Rodeo Creek exploration property.

- Silver Mines Ltd.’s Bowdens project in New South Wales — set to start operations in 2023 — will have an initial output target of 6 million ounces a year, said Managing Director Anthony McClure. That will make it the country’s biggest new mine for the metal in more than two decades, and Australia’s No. 2 silver producer behind South32 Ltd.‘s Cannington mine in Queensland.

Threats

- Oceana Gold said that Mr. Michael Holmes has resigned as the President and Chief Executive Officer of the Company, as well as from the Board of Directors, effective September 8, 2021. The Board has engaged a leading executive search firm to commence a global search for the Company’s next President and CEO. In recognition of leadership continuity, the Board has appointed Mr. Scott Sullivan who has recently joined the Company as Chief Operating Officer, to act as the Acting President and CEO of the Company.

- At Americas Gold and Silver Corp. (USA), the ongoing illegal blockade at Cosalá prohibited any exploration activity over the past year. With the lack of commercial operations, USA continues to issue shares at a dilutive level to stay cash positive.

- Owners of the Ballarat Gold Mine have been accused of contravening Victoria’s top workplace safety law by failing to keep updated safety plans and by appointing people to senior underground mining roles without the required qualifications. Victorian regulators have given the Singaporean-controlled mine until October 15 to fix the breaches, adding to doubts over the financial health of the mine after tens of millions of dollars were lent to doubtful debtors offshore in the past decade.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

i-80 Gold Corp

K92 Mining

Montage Gold

Oceana Gold Corp.

Pure Gold

Sibanye Stillwater

American Airlines Group Inc.

Alaska Air Group Inc.

Deutsche Lufthansa AG

easyJet PLC

Japan Air Co Ltd.

JetBlue Airways Corp.

Southwest Airlines Co.

Tencent Holdings Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Free Cash Flow (FCF) represents the cash that a company can generate after laying out the money required to maintain or expand its asset base.

The S&P 1500 Composite is a broad-based capitalization-weighted index of 1500 U.S. companies and is comprised of the S&P 400, S&P 500, and the S&P 600. The index was developed with a base value of 100 as of December 30, 1994. The Consumer Confidence Index (CCI) is an indicator which measures consumer confidence in the Economy. ZEW Germany Expectation of Economic Growth is a survey on the question of economic growth in six months. The consumer price index (CPI) is an index of the variation in prices paid by typical consumers for retail goods and other items.

The Bloomberg Pan-European High Yield Index measures the market of non-investment grade, fixed-rate corporate bonds denominated in the following currencies: euro, pounds sterling, Danish krone, Norwegian krone, Swedish krona, and Swiss franc. Inclusion is based on the currency of issue, and not the domicile of the issuer.

The harmonized index of consumer prices (HICP), used primarily within the European Union, is a measure of prices paid by consumers for a market basket of goods and services. It is calculated using the same methodology across countries to allow for comparable measures of inflation. The yearly (or monthly) growth rates represent the inflation rate. The dividend yield, expressed as a percentage, is a financial ratio (dividend/price) that shows how much a company pays out in dividends each year relative to its stock price.