SPACs Power Past 2020 Record, Raising More Than $83 Billion in Three Months

Date Posted: March 19, 2021

Read time: 50 min

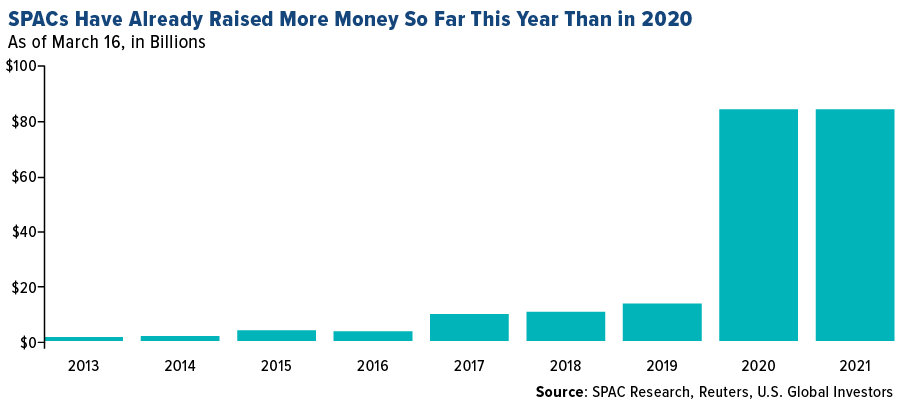

We're not quite three months into 2021, and yet U.S. SPACs have already raised more money than the record $83.4 billion that was raised in all of 2020. So what exactly are SPACs, and why have they become so popular all of sudden?

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Wall Street thought 2020 was the Year of the SPAC, or special purpose acquisition company (SPAC).

Turns out, this title was premature.

We’re not quite three months into 2021, and yet U.S. SPACs have already raised more money than the record $83.4 billion that was raised in all of 2020.

So what exactly are SPACs, and why have they become so popular all of sudden?

Also known as blank check companies, SPACs are companies that have no explicit business plan other than to acquire or merge with an unspecified private company at some point. They’ve been around since the 1990s but haven’t drawn a whole lot of investor attention until recently, for reasons I’ll get into later.

The Basics of SPACs

The way SPACs work is, they list on an exchange like the New York Stock Exchange (NYSE) and then typically have up to 24 months to acquire a target company. If a deal isn’t made by the two-year mark, they must dissolve and return the gross proceeds to shareholders.

One of the most well-known examples is Virgin Galactic, which began trading under the ticker SPCE in October 2019 after merging with Social Capital Hedosophia, a SPAC founded by venture capitalist Chamath Palihapitiya.

Since SPACs don’t make anything or own any assets, it’s the founders that are the main draw. Think Palihapitiya, an early Facebook executive, outspoken advocate of bitcoin and potential California governor candidate. Other SPAC sponsors have included big names such as Bill Ackman, Shaquille O’Neal and former House Speaker Paul Ryan. Investors may bank on founders having the right connections to close a deal with a hot tech startup and bring it to market.

In other words, it’s a case of betting on the jockey (the founders) rather than the horse (the company).

Again, SPACs were once quirky backwaters in the $50 trillion U.S. stock market. The NYSE didn’t bother listing any until May 2017. Just five years ago, Goldman Sachs had a strict policy against them.

Flash forward to today, and junior Goldman bankers are issuing complaints of grueling working conditions due to the boom in SPAC issuances. A survey of first-year Goldman analysts showed that many have been working 100-hour weeks on average since January. “My body physically hurts all the time and mentally I’m in a really dark place,” one respondent wrote.

An Alternative to Traditional IPOs

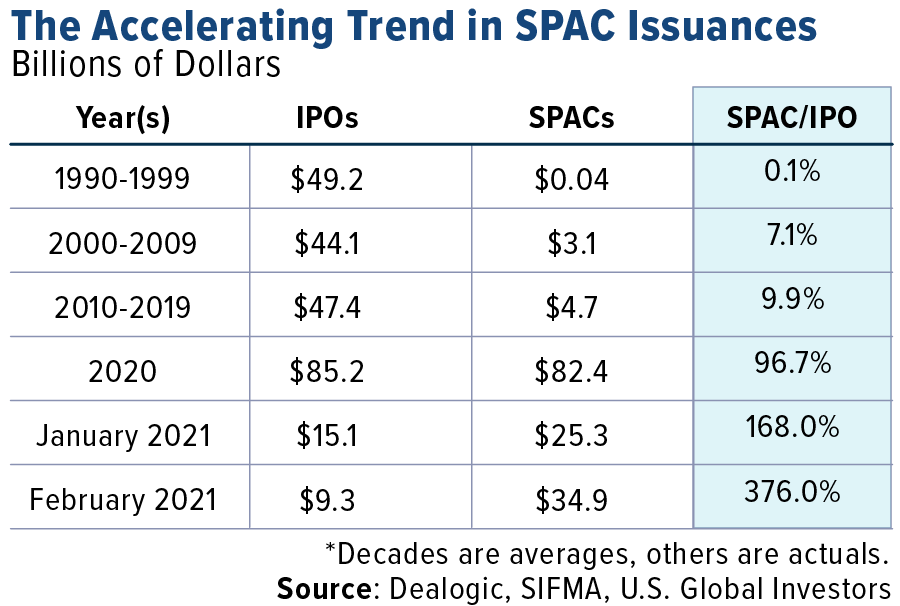

When it comes to tapping public markets, the trend is definitely in SPACs’ favor. Last year, 248 SPACs listed, a record, compared to 209 traditional initial public offerings (IPOs). To my knowledge, this is the first time SPAC issuances outpaced IPO issuances. The amount of cash raised was also a nearly one-to-one ratio.

The trend has only accelerated so far this year. Last month, for every $1 raised in an IPO, the SPAC market raised $3.76.

So let me return to an earlier question: Why are these companies so popular all of a sudden?

The short answer is that, in a lot of ways, it’s easier for a company to go public through an acquisition or reverse merger than to jump through the regulatory hoops and get listed on an exchange. Traditional IPOs clearly have benefits, including greater visibility and prestige, but they can be costly and time intensive. An IPO can take up to two to three years to close, whereas a SPAC can be completed in as little as two to three months.

There are other upsides to SPACs, including requiring fewer disclosures. Deal points are limited to the SPAC founder(s) and chief executive of the target company; therefore, investor roadshows are effectively eliminated.

This was an especially attractive feature in 2020 during the pandemic, which may have contributed to the SPAC boom.

I’ve written before about how the number of IPOs has been shrinking for years—both in the U.S. and abroad—as the increase in regulations makes it tougher and more expensive to get (and stay) listed. Companies are choosing to remain private for longer periods of time, often going public years after they’ve already become multibillion-dollar businesses with household name brands. (Think Uber, Lyft, Airbnb and DoorDash, all of which began trading in the past two years.)

This hurts retail investors, who never get to participate in a company’s meteoric rise from nothing.

For many investors and executives, SPACs can be seen as a “loophole” of sorts, allowing companies to get a public listing without going through the more typical channels. I don’t know if I would agree with that term, but I wouldn’t be surprised if regulators start to crack down on these types of companies.

Inflation Concerns at a Record High?

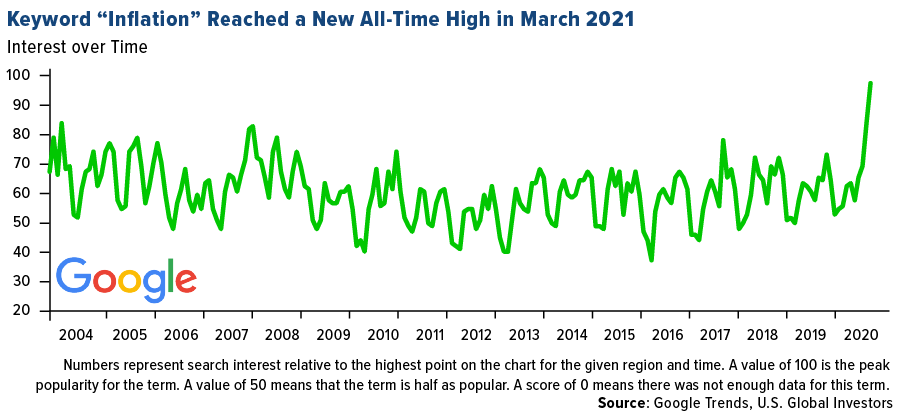

Switching gears, I learned this week that Google searches for the keyword “inflation” hit their highest level this month since at least 2004, when the online search giant began collecting information. This tells me that people are starting to get concerned with the direction consumer prices are headed in, and how this will affect their pocketbooks and investments.

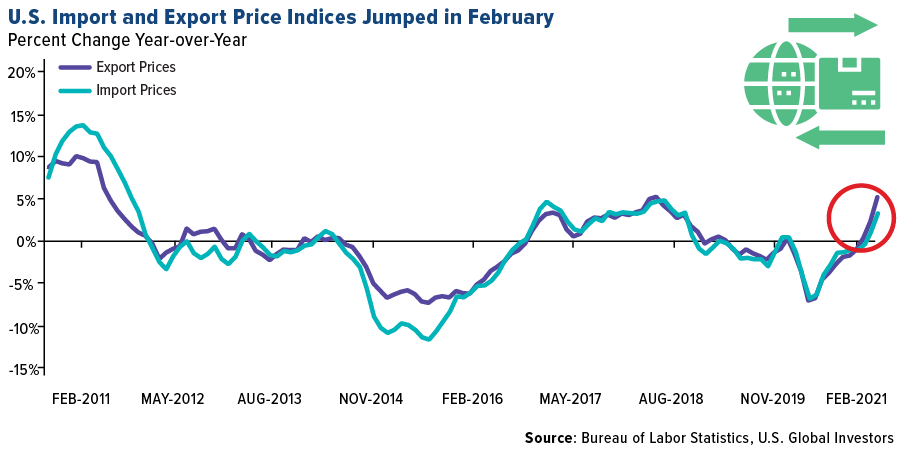

The consumer price index (CPI) rose 1.7% year-over-year last month, but as I’ve said before, is the CPI “fake news”? This measure doesn’t include food and energy, and yet those are the goods and services seeing some of highest inflation right now. Grocery prices increased the most in nearly a decade last year, and this rate could surge even more this year as shipping rates go up. In February, the cost to export from the U.S. jumped 5.2% over last year, the most since June 2018, while import costs rose 3.0%.

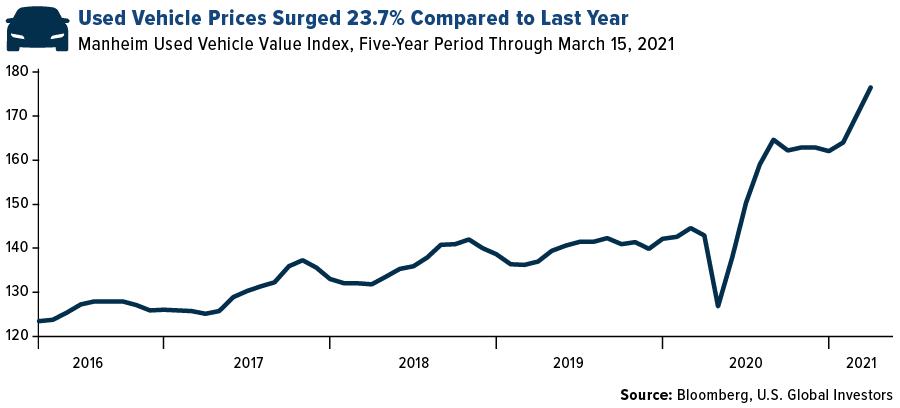

This, coupled with rising commodity prices, is having a huge effect on big-ticket items like cars and trucks. According to the Manheim Used Vehicle Value Index, wholesale prices for preowned automobiles increased a jaw-dropping 23.7% from March 2020 to today. Like I said recently, if you’re in the market for a new car, you might want to lock in today’s prices before they go up anymore.

This week, Federal Reserve Chair Jerome Powell said he expects the U.S. economy to grow 6.5%, which would be the most in almost 40 years. Even if this results in higher-than-normal inflation, Powell committed to continue high-growth monetary policies, including near-zero rates and asset purchases.

That said, I think gold is a prudent investment to help stem the impact of inflation on your portfolio. I often advocate the 10% Golden Rule, with 5% in gold bullion (bars, coins, jewelry) and 5% in gold mining stocks, mutual funds and ETFs.

Gold Market

This week spot gold closed the week at $1,745.23, up $18.12 per ounce, or 1.05%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.46%. The S&P/TSX Venture Index came in up 1.38% The U.S. Trade-Weighted Dollar rose 0.31%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-16 | ZEW Survey Expectations | 74.0 | 76.6 | 71.2 |

| Mar-16 | ZEW Survey Current Situation | -62.0 | -61.0 | -67.2 |

| Mar-17 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.1% |

| Mar-17 | Housing Starts | 1560k | 1421k | 1584k |

| Mar-17 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Mar-18 | Initial Jobless Claims | 700k | 770k | 725k |

| Mar-23 | New Home Sales | 881k | — | 923k |

| Mar-24 | Durable Goods Orders | 0.9% | — | 3.4% |

| Mar-24 | Hong Kong Exports YoY | 40.0% | — | 44.0% |

| Mar-25 | Initial Jobless Claims | 728k | — | 770k |

| Mar-25 | GDP Annualized QoQ | 4.1% | — | 4.1% |

Strengths

- The best performing precious metal for the week was palladium, up 11.14%. South African platinum stocks jumped as much as 4.4% on Tuesday after Norilsk Nickel, a top producer, reduced its forecast production from its Arctic mines due to flooding, reports Bloomberg. Palladium rose 4.3% on the news of tighter supply. RBC forecasts estimates that the Norilsk reductions would be the equivalent of 7.6% of global supply of palladium.

- Gold had a second weekly gain despite higher Treasury yields thanks to a weaker U.S. dollar. The yellow metal rose on Wednesday directly following the Fed meeting where bankers kept a zero-rate outlook.

- Poland’s central bank governor said it wants to buy at least 100 tons of gold in the coming years and store it locally. Since becoming governor in 2016, Adam Glapinski said Poland has transferred gold to Polish vaults, where there is already 229 tons.

Weaknesses

- The worst performing precious metal for the week was platinum, down by just 0.66%. Platinum was up the prior week by 6.45%, so most of the gains held. The 10-year Treasury yield hit a 14-month high of 1.75% on Thursday. Fed Chair Jerome Powell remained dovish at the end of the Wednesday Fed meeting, despite upgrading the economic outlook. Bloomberg notes the dovish message only briefly stemmed the rise of bond rates.

- Investors withdrew from commodity-focused ETFs for the sixth straight week. According to Bloomberg data, precious metals ETFs saw $585.8 million in outflows. However, the outflow was $1.12 billion less than the week prior.

- As reported by Reuters, Mexico could revoke a concession held by Americas Gold and Silver Corporation, a Canadian miner, in northern Mexico if it does not accept its new trade union representation there, President Andres Manuel Lopez Obrador said on Wednesday. The President noted that the miner had rejected the outcome of a vote by workers at the mine to put labor representation under the control of trade union.

Opportunities

- GV Gold PJSC, a Russian gold miner backed by BlackRock, is planning a $500 million IPO in Moscow. Bloomberg reports a group of shareholders plan to sell shares and are seeking a valuation of $1.8 billion. GV Gold is a top 10 Russian miner and operates several Siberian deposits.

- Gran Colombia and Gold X are combining to form a new, mid-tier, Latin American-focused gold producer. All issued and outstanding Gold X shares will be acquired by Gran Colombia in exchange for Gran Colombia common shares on the basis of 0.6948 of a Gran Colombia share for each Gold X share. The combined company will have around $100 million in cash and financing support from Wheaton Precious Metals.

- Sudan’s Mining Ministry said in a statement that it is deploying a team to restart production at a network of gold mines in Darfur that were previously linked to the family of the country’s most powerful militia leader. The mines were handed over to Sudan’s government recently after being held by members of militia chief Mohamed Hamdan’s family, reports Bloomberg. The transfer of mines is a step toward formalizing the gold mining sector, which is an alternative to oil. Sudan lost three quarters of its oil reserves in 2011 when South Sudan seceded.

Threats

- Argentine President Alberto Fernandez faced environmental protesters this week who are against the government’s efforts to begin mining in Chubut. Argentina has large untapped deposits of lithium, copper, gold and silver. Bloomberg notes one of the major barriers to development is anti-mining sentiment sparked by three cyanide incidents in two years at a Barrick Gold mine in the San Juan province.

- NatWest, a major U.K. bank, is facing landmark money laundering charges for failing to properly monitor a company’s account that received cash deposits totaling $365 million, reports Bloomberg. According to a court summary, the charges relate to the bank’s relationship with Fowler Oldfield, an England-based gold dealer.

- Inflation fears are growing across the markets. Commodities tumbled on Thursday, with oil falling 7%, on concerns that the Fed will allow inflation to accelerate. The Bloomberg Commodity Spot Index fell 2.4%, the biggest drop since mid-September. “Treasury yields and the dollar are responding to the Fed, and that is currently having a negative impact on the commodities,” Arlan Suderman, chief commodities economist at StoneX, said in an email.

Index Summary

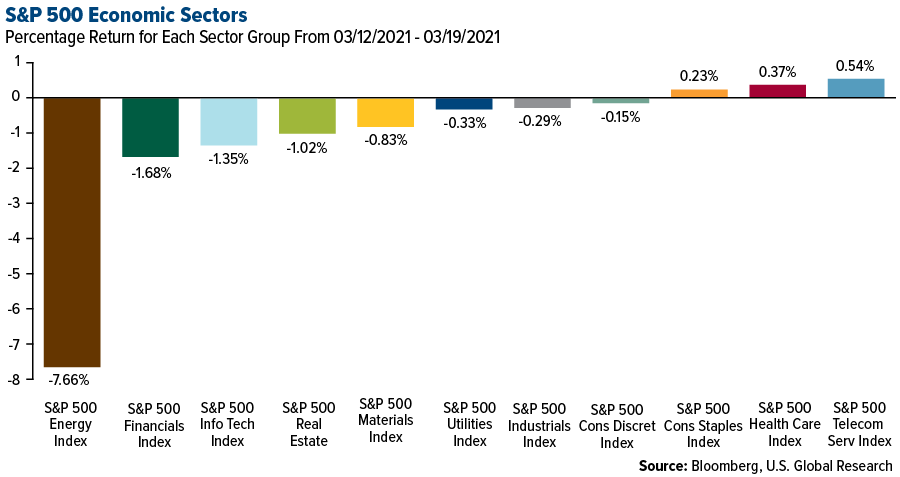

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.46%. The S&P 500 Stock Index fell 0.45%, while the Nasdaq Composite fell 0.79%. The Russell 2000 small capitalization index lost 2.58% this week.

- The Hang Seng Composite gained 0.81% this week; while Taiwan was down 1.14% and the KOSPI fell 0.49%.

- The 10-year Treasury bond yield rose 10 basis points to 1.727%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was KARMA, rising 1,846.19%.

- Crypto.com, the cryptocurrency exchange platform and card issuer, is partnering with Visa and plans to debut its fiat lending program. In the press release, Crypto.com revealed that the company’s partnership with Visa is in line with their efforts to expand the reach of its Visa card, which is already used in more than 30 countries including U.S., Canada, as well as nations in Europe and across the Asia-Pacific. In addition to its physical Visa card, Crypto.com is planning on issuing virtual cards within Europe. Its fiat lending program, named “Spending Power”, will allow Crypto.com Visa cardholders to use the cryptocurrency balance in their wallet as loan collateral and spend fiat in merchant platforms that support Visa payments.

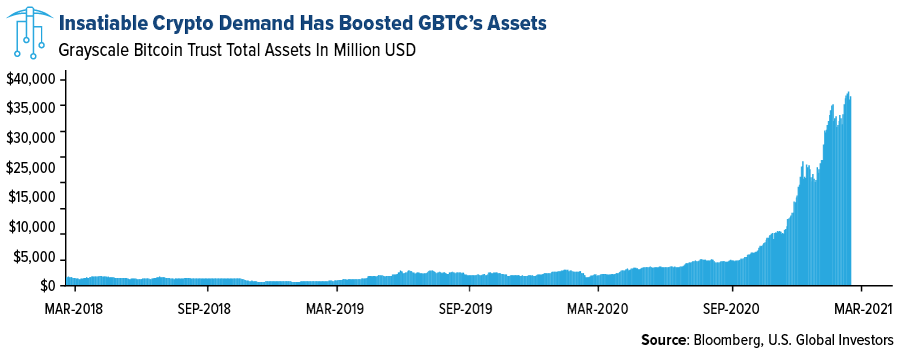

- Jerome Powell, the U.S. Federal Reserve Chair, said that central bank digital currencies (CBCDs) will have to coexist with cash. He cited a report on CBCDs from the Bank of International Settlements and a group of seven central banks, including the Fed, and acknowledged that a CBCD needs to coexist with cash and other types of money in a flexible and innovative payment system and that improvements in the global payments system will have to come from both the public and the private sector. Additionally, he reported that the Fed Board of Governors is conducting experiments on CBCDs along with the Federal Reserve Bank of Boston. The chart below showcases the ‘fear of missing out’ phenomena occurring in the cryptocurrency markets as Grayscale’s Bitcoin Trust Fund’s assets have reached new highs even as it trades at a discount compared to its net asset value.

click to enlarge

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Rewardiqa, down 66.64%.

- A Canadian communications provider, Sky Global, has been accused of facilitating criminal organizations to launder millions in cryptocurrencies with encrypted phones. The company is alleged to have helped these organizations transfer illegally obtained funds into Bitcoin and other cryptocurrencies. The indictment also states that Sky Global obstructed investigations of drug trafficking and money laundering by remotely deleting evidence on said encrypted phones when seized by law enforcement.

- The People’s Bank of China and the Supreme People’s Court released a statement saying that money laundering using Bitcoin and other virtual currencies poses serious threat to social and financial stability. The Chinese government prosecuted 707 people for all money laundering in 2020, 368% higher than 2019, but it did not mention the share of prosecutions involving cryptocurrencies.

Opportunities

- The U.S. Securities and Exchange Commission (SEC) has formally kicked off its 45-day window to make an initial decision on VanEck’s Bitcoin exchange-traded fund (ETF). If the filing is approved, the ETF would be the first open Bitcoin exchange-traded product in the U.S. VanEck filed for the ETF with the Cboe BZX Exchange earlier this year.

- Bank of America, the second-biggest lender in the U.S., published a report on cryptocurrencies and blockchain titled “Bitcoin’s Dirty Little Secrets.” In it, the bank says that it is intrigued by possible applications of decentralized finance (DeFi) and calls it potentially more disruptive than Bitcoin. The bank sees DeFi as a radical change to mainstream capital markets but acknowledges that it has a long way to go if it wants to challenge established financial institutions.

- Deutsche Bank’s report on Bitcoin calls it “too important to ignore” given its $1 trillion market capitalization. In December 2020, the bank revealed its plans to develop a fully integrated custody platform for its institutional clients and their digital assets. The report also states that Bitcoin’s price appreciation could continue if it attracts entry from asset managers and companies. The bank also believes that Bitcoin still must transform its potential into results, as it estimates that less than 30% of transactional activity in Bitcoin is related to payments.

Threats

- iCE3, a South African cryptocurrency exchange, is urging its users to withdraw cryptocurrency holdings, except Bitcoin and Litecoin, from its platform after it found discrepancies in its balances. The exchange said that it held consultation talks with its partner Merkeleon.com, an Austrian-based software firm, and was unable to reach a satisfactory conclusion. In addition to halting withdrawals of Bitcoin and Litecoin, iCE3 also suspended deposits and trading in the two cryptocurrencies pending the outcome of a full investigation and reconciliation.

- The report titled “Bitcoin’s Dirty Little Secrets”, by Bank of America, claims that the main argument for investing in Bitcoin is not diversification, stable returns, or inflation protection, but sheer price appreciation which depends on Bitcoin’s demand outpacing its supply. It also added that the CO2 emissions from mining Bitcoin are equal to that of Greece. The report also noted that 95% of total mined coins are controlled by only 2.4% of addresses, which makes Bitcoin impractical as a payment mechanism or even as an investment vehicle.

- Germany’s Federal Financial Supervisory Authority (BaFin) issued a consumer protection alert on its website warning investors about the risks involved in cryptocurrency investments. The statement echoed the stance taken by the European Securities and Markets Authority and the European Banking Authority. BaFin stated that retail investors need to be aware of the risks of incurring 100% losses from their crypto investments as there is no protection against losses for retail consumers in the cryptocurrency space. In 2021 alone, regulators from South Africa, U.K., and even Thailand have issued similar warnings as the bull market run for digital assets continues.

Domestic Economy and Equities

Strengths

- The Federal Reserve kept rates anchored near zero and maintained the current pace of asset purchases, following the conclusion of this week’s meeting. Officials also upgraded expectations for GDP growth and inflation and cut estimates for the unemployment rate. More members foresee rate hikes in coming years, but not enough to change the forecast for none through at least 2023.

- The Philadelphia Federal Reserve’s business activity index jumped to 51.8 in March from 23.1 in the prior month. Economists surveyed by the Wall Street Journal expected the index to slip to 22. The result was stronger than the similar index released by the New York Fed that hit an eight-month high of 17.4 in March. Economists use the New York and Philadelphia regional indexes to gauge the strength of the national ISM manufacturing index, which expanded last month at the fastest pace since the pandemic struck one year ago.

- Hartford Financial Services Group was the best performing S&P 500 stock for the week, increasing 22.06%. Chubb Ltd. proposed an acquisition of Hartford Financial Services Group Inc. for about $23.2 billion in cash and stock in what could be one of the industry’s biggest deals in years.

Weaknesses

- Sales at U.S. retailers fell 3% in February due to a lapse in government aid and unusually bad weather. Sales fell in every major retail group except for groceries and gasoline, two major household staples. Some slowdown in sales was expected in February after the government aid was spent, but the Democratic-led Congress just approved additional payments to bring the total to $2,000 for those who meet the income thresholds. The money is being sent out currently and much of it is likely to be spent in March and April. Economists polled by Dow Jones and The Wall Street Journal had forecast a small 0.1% decline in retail sales.

- Industrial output fell sharply in February as severe winter storms battered much of the country, disrupting a wide range of manufacturing activities from autos to chemical plants. The expectation is that the drop will be temporary although there are concerns about growing global supply chain problems. The Federal Reserve reported Tuesday that industrial production fell 2.2% in February, reflecting a big decline in output at factories and oil and gas refineries. Industrial production fell last month interrupting a string of four positive monthly gains as U.S. factories recovered from the pandemic-induced recession of last spring.

- NOV Inc was the worst performing S&P 500 stock for the week, decreasing 12.34%. Shares began falling Tuesday after the company said it expects to report first-quarter results that are lower than previously guided on winter-weather disruptions in Texas and Oklahoma, softer-than-anticipated customer orders, reduced oil-field customer spending and the effects of the pandemic.

Opportunities

- L’Oreal was double upgraded to Add from Sell at AlphaValue, which cites optimism for the French beauty products maker’s faster-than-expected expansion in e-commerce and outlook in China. Four out of the 10 influential cosmetic brands in China are from L’Oreal and its leading position in the Asian country is stable, AlphaValue analyst Jie Zhang says. The company has “unrivaled” leadership in the dermo-cosmetic & beauty-tech market; all these elements will continue driving top-line and profit growth going forward, allowing L’Oreal to remain an “industry front-runner.”

- Ford Motor was upgraded to Overweight from Equal Weight by Barclays analyst Brian Johnson, saying the automaker will likely shift toward electric vehicles much more aggressively in the 2025-2030 period, sooner than what consensus believes. Johnson noted Ford will likely highlight a strategy centered around two dedicated battery electric vehicle platforms during its Spring investor day.

- BofA analyst Elizabeth Suzuki upgraded Petco to Buy from Neutral with an unchanged price target of $28 after a strong Q4 report and an initial outlook for 2021 that was ahead of expectations. Amid continued elevated pet adoption trends, she views Petco as well positioned to continue to benefit from industry-demand tailwinds, the analyst said. The company "appears to be off to a solid start," said Suzuki.

Threats

- Deutsche Bank analyst Steve Powers added Molson Coors to the firm’s "short-term Sell catalyst list." The analyst believes the company’s Q1 results are likely to come under "material pressure" from adverse February weather in Texas and a more recent cybersecurity breach in March. Both likely caused downtime in Molson’s operations and shipments for several days and may have incurred elevated cash costs, Powers told investors in a research note. He believes this is likely to result in downward consensus revisions near-term.

- JPMorgan analyst Andrea Teixeira downgraded Kimberly-Clark to Underweight from Neutral with a price target of $123, down from $144. Management’s "heightened focus" on reinvestment and innovation will likely translate to faster sales growth over the long term, but the company’s near-term earnings growth is likely to face greater pressure, particularly as the benefits from operating leverage "fade meaningfully" as volumes continue to slow, Teixeira told investors in a research note. The analyst believes the combination of rising input costs and a normalizing promotional environment will likely strain Kimberly-Clark’s margins.

- D.A. Davidson analyst Linda Bolton Weiser downgraded Clorox to neutral from buy and lowered her price target on the stock to $189 from $234. Weiser noted that consensus estimates have been pricing in only a 1.7% decline in sales for March, which may be too optimistic, and comparisons only will get more difficult from then on. Weiser anticipates a sales slowdown as demand may have peaked during the height of the pandemic.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was palladium, up 11.05%. Palladium is expected to gather strong momentum due to greater industrial demand as COVID-19 vaccines roll out. Investors continue to bet that the market for palladium could see an even larger deficit this year than previously thought as the loss of production at Nornickel’s Arctic mines will offset the higher mine supply from South Africa. There is a higher demand from automakers after years’ slump, as palladium is crucial for automobile pollution-control devices.

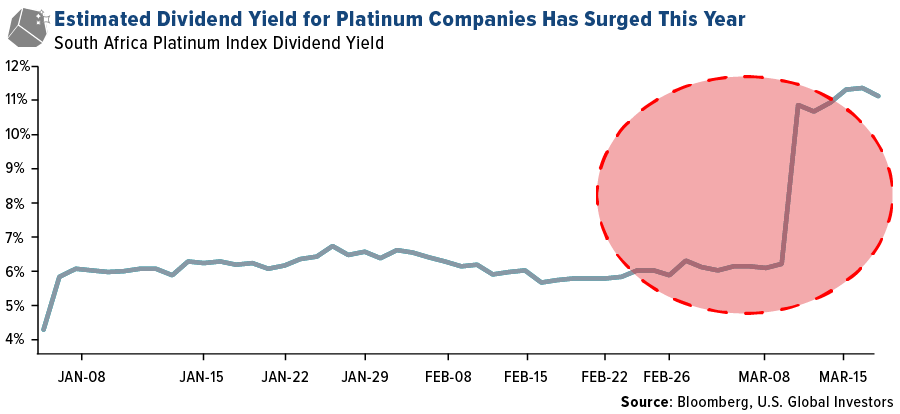

- South African platinum stocks reached their highest levels in more than 12 years due to an upswing in demand and constricted supply. Johannesburg’s index of platinum stocks has soared 30% this year and over the past 12 months, the FTSE/JSE Africa Platinum Mining Index is up more than 300% as of this week thanks to surging prices for palladium and rhodium, which are dug up with platinum and used in vehicle pollution-control devices. The chart below shows that the estimated dividend yields on the platinum index has surged to 11.5% from 4.3% at the end of 2020 on the back of higher expected earnings.

- Aluminum rallied back towards its two-year highs as additional metal was ordered out of London Metal Exchange warehouses in Asia, signaling a robust regional demand. Aluminum orders hit the highest level in more than a year as Russian aluminum giant United Co RUSAL said it expects demand for the metal to grow 5% to 6% this year, building on a strong recovery in orders toward the second half of 2020. Citigroup Inc. raised its three-month price target for aluminum to $2,300 a ton, up from $2,200 previously, on reports that authorities in Inner Mongolia are clamping down on output.

Weaknesses

- The worst performing commodity for the week was palm oil, down 6.62%. Palm oil recorded its largest weekly drop in two months as declines in rival vegetable oils and petroleum continued to weigh on the market and high prices curbed buying. Futures sank as much as 3.5% to reach their lowest since start of March and the rolling most-active contract is down nearly 10% this week.

- Oil declined for a fifth consecutive day as inflation concerns rattled broader sentiment, and physical markets in Asia cooled down. Prices headed for the biggest weekly slump since October, followed by a surge in Treasury yields that pushed the dollar higher and signs of a softer near-term crude demand in Asia. Oil prices are up 20% year-to-date on the expectation of a strong recovery from the pandemic and OPEC+ deciding to extend supply curbs. Analysts and traders do believe that this decline is just a blip in a longer bull cycle.

- Vine Energy Inc. went public this week, marking the first U.S. shale driller in four years to go public. It fell short of its capital raising goal of $361 million, raising a total of $301 million and selling 21.5 million shares. The weak IPO accentuates investor appetite for the cash-intensive shale industry that has waned after years of poor returns and a pandemic-driven crash in 2020.

Opportunities

- Petroleos Mexicanos (Pemex), the state-owned oil company, reported that it has discovered what is expected to be a billion-barrel oil field in Tabasco, Mexico, as it aims to reverse a decade-and-a-half of sinking production. In addition to sinking production, Pemex has accumulated a total debt of $113 billion which is the highest of any major oil company in the world, and its bonds have been downgraded to junk by Fitch Ratings and Moody’s Investors Services Inc. To help the company shift course, President Andres Manuel Lopez Obrador has canceled competitive oil and gas auctions that allowed private companies to exploit Mexico’s oil territories and has ordered Pemex to focus on easier-to-reach and less expensive blocks in onshore fields and shallow-waters.

- Volkswagen AG (VW) revealed its strategy to become the world’s biggest electric vehicle maker with a plan to build six battery factories in Europe and global investments in charging stations. VW has already reached agreements for two sites and is exploring options for the other four plants for a total capacity of 240 gigawatt-hours by the end of the decade. It also said that the company will add 50 purely battery-powered vehicles to its lineup by 2030. VW is planning on investing $477 million by 2025 to build out much-needed charging infrastructure in Europe, after the region overtook China in EV sales in 2020.

- South Chungcheong province, home to almost half of South Korea’s coal-fired power plants, is reportedly planning on spending around $27.6 billion through 2025 to build an off-shore wind power farm and a blue hydrogen production plant. This investment is part of President Moon Jae-in’s campaign to put the country on a path of carbon neutrality by 2050. President Moon has pledged to phase out coal and nuclear energy, which accounts for almost half of the country’s power generation and accelerate the shift towards renewable power. The planned investment is expected to curtail 177 million metric tons of carbon dioxide emissions and create more than 236,000 jobs by 2025.

Threats

- A surge of Iranian oil into China is hurting OPEC efforts of tightening supply and pushing prices upward. China, the world’s largest crude oil importer, is currently buying close to 1 million barrels a day of sanctioned crude, condensate and fuel oil from Iran and displacing favored grades from countries like Norway, Angola, and Brazil. Although Iran is a member of OPEC, it is exempted from the supply restrictions. Around 10 million barrels of Angolan oil due for April export were still without buyers as of this week, compared to a typical month when such cargoes would have been sold out by now. Additionally, three supertankers carrying oil from Norway have been floating off China for at least two weeks without discharging and only 16 million barrels of North Sea crude left Europe for Asia in February, the lowest in four months. Analysts believe that increased flows from Iran have put the spot market in a weak position.

- The International Energy Agency (IEA) said that global oil demand will not return to pre-pandemic levels until 2023 and that growth will be subdued thereafter amidst new working habits and a shift away from fossil fuels. In IEA’s report, they believe that fuel consumption will average just over 101 million barrels a day in 2023 and oil demand in the middle of the decade will be about 2.5 million barrels lower than they projected last year. The agency also expects electric vehicles to become more prevalent this decade and with an increase in efficiency of internal combustion engines, demand for gasoline is expected to stagnate. The report adds that if governments act more swiftly on environmental reforms than expected, and consumers eschew business travel and embrace recycling, about 5.6 million barrels of daily oil demand could be eliminated by 2026.

- U.S., China and India, the world’s three biggest consumers of coal, are getting ready to boost usage so much that it will almost be as if the pandemic-induced drop in emissions never happened. U.S. power plants are going to consume 16% more coal this year than in 2020, and then another 3% in 2022. China and India account for two-thirds of coal demand and have no plans of shifting away from the dirtiest fossil fuel in the short term. The increase in coal usage for U.S. stems from higher natural gas prices and for China and India, it reflects rising electricity demand that is keeping coal as the dominant source of power generation.

Airline Sector

Strengths

- The best performing airline stock for the week was Wizz Air, up 14.6%. China, the first country to emerge from the pandemic, is showing what air travel may look like for everyone else soon. February traffic in China was up 178% versus year-ago levels.

- Air travel is showing some signs of improvement in the U.S. Delta has seen bookings increase over the past five to six weeks. Southwest and JetBlue are indicating the same. Domestic bookings are at 64% of levels seen in March 2020. Recent TSA screening volumes have been 1.3-1.4 million people per day, the highest since March 2020. This has been helping the airlines, as United and Delta indicated they would be cash flow positive this month.

- Shares on Sun Country Airlines jumped by 40% on the day of its IPO. This illustrates the rapidly improving sentiment among airline investors. The stock trades on the Nasdaq with the symbol SNCY. Frontier Airlines is planning to go public shortly.

Weaknesses

- The worst performing airline stock for the week was Volaris, down 7.5% Delta indicated that first quarter revenues would be down 60-65% from year-ago levels and would be at the low end of prior guidance. Operating expenses would be down 35-40%, but at the high end of prior guidance. Liquidity is $16.5 billion, below prior guidance of $18-19 billion.

- Capacity is still being cut by U.S. and European airlines. However, traffic is rising at U.S. airlines, indicating higher load factors. Traffic has been weak in Europe, due to a slow vaccine rollout and shutdowns. Many countries in Europe will allow international travel to resume in May, but France and Germany remain restricted.

- After a one-year investigation, Iran released its final report on the crash of a Ukrainian aircraft that killed 176 people. It was blamed on human error when military downed the jetliner with two surface-to-air missiles.

Opportunities

- Portuguese Airline TAP and Emirates have signed a code share agreement to expand their partnership. This will allow passengers of both airlines to expand their connections to new routes.

- Airlines are starting to offer “quarantine free” flights. Delta, for example, has been offering these flights between New York and Italy. Rapid COVID testing occurs before and after travel. These types of flights can be a bridge until more people worldwide can be fully vaccinated. Alitalia and KLM have been doing the same thing.

- Capital markets remain open for the airlines. Indigo Partners sold 7.7 million Wizz shares. Cost Verde sold 77 million new shares to finance LATAM. Nearly $10 billion of airline debt was issued into the high yield market, mostly from American Airlines. Apollo-backed Sun Country Airlines raised $218 million in an IPO.

Threats

- British Airways needs capital and plans to tap the junk bond market. IAG, the parent of British Airways, Iberia, and Aer Lingus, will be doing the offering of $1.2 billion. The belief is that the amount will be $600 million per maturity, with two different maturities. However, the debt is likely to be junk rated. This could make the debt expensive because of the risk incurred by investors.

- The U.K.’s travel restrictions have been hurting British Airways significantly. They are working with the Government to develop a plan to resume international flights by summer. The carrier is seeing demand to travel but is being held back by the U.K. government. The carrier is trying to rebuild its flight schedule, but international travel will start no earlier than May 17.

- Two new airlines are preparing to fly as the industry ramps-up post-COVID, presenting competition in the space. Avelo will be led by the former President of Allegiant Airlines. The new airline will start in April and will service smaller airports in large metro areas. Cheap financing on aircraft and unused labor in the industry will allow them to offer rock-bottom fares. Breeze Airways will be a new low-cost carrier focusing on markets that do not have nonstop service. It will be led by the former leader of JetBlue.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 1.1%.The best performing country in Asia this week was Pakistan, gaining 2.5%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 4.2%.The Pakistani rupee was the best performing currency in Asia this week, gaining 1.3%.

- India’s foreign reserves surpassed Russia’s, to become the world’s fourth largest, boosting foreign investors and credit ratings companies’ confidence that the government can meet its debt obligations. India’s reserves can cover roughly 18 months of imports.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 2.7%. The worst performing country in Asia this week was the Philippines, losing 4.4%.

- The Polish zloty was the worst performing currency in emerging Europe this week, losing 1.3%. The Taiwanese dollar was the worst performing currency in Asia, losing 1%.

- Experts warn that European countries are at the start of a third wave of COVID-19. Europe’s decision to pause the use of the AstraZeneca vaccine over health concerns is likely to lead to slower recovery.

Opportunities

- The Central Bank of Turkey once again delivered stronger-than-expected rate hikes supporting its currency. The one-week repo rate was raised to 19% from 17%. Most economists expected only a 1% increase. Without major geopolitical hiccups and an improving domestic pandemic situation, the Turkish currency may move higher thanks to tight monetary policy.

- Indonesia, a top supplier of nickel used in production of batteries for electric vehicles, aims to boost sales of electric cars with a new regulation that will cut tax breaks for hybrid cars. Battery-powered electric vehicles will retain their 0% luxury tax rate, while plug-in hybrid vehicles will see their tariff increase to 5% from 0%.

- Xioami, a Chinese smartphone maker, was removed from the U.S. blacklist allowing U.S. investors to hold the company’s shares again. FTSE Russell has proposed that Xiaomi should be eligible for re-inclusion in FTSE Russell indices effective from June 21, 2021. China seeks to reverse many policies that were put in place under the Trump presidency.

Threats

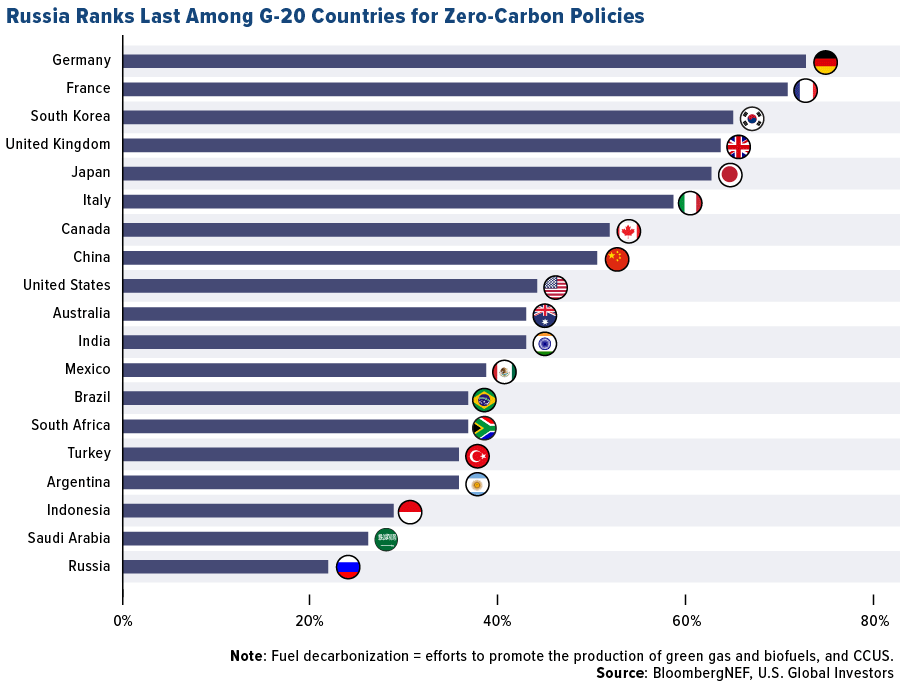

- Russia ranks last among G-20 countries for zero-carbon policies. Russia still very much depends on coal or oil for jobs. Any shift to more climate-friendly energy production will not happen soon as it will require a significant amount of capital.

- The United States once again threatened to impose more sanctions on Russia for the country’s interference in the U.S. Presidential elections and imprisonment of Alexei Novalny, the biggest opponent of President Putin. Rumors are that some punitive measures might be announced as early as next week.

- Rockets from Syria hit the Turkish border town of Kilis, the Turkish Defense Ministry said, adding that it informed Russia about the attack and hit targets in retaliation. Kilis, which hosts a large number of Syrian refugees, has been caught in cross-border shelling on several occasions during the conflict.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.73 | +0.10 | +6.21% |

| Oil Futures | 61.52 | -4.09 | -6.23% |

| Hang Seng Composite Index | 4,563.16 | +36.55 | +0.81% |

| S&P Basic Materials | 488.32 | -4.10 | -0.83% |

| Korean KOSPI Index | 3,039.53 | -14.86 | -0.49% |

| S&P Energy | 370.11 | -30.71 | -7.66% |

| Nasdaq | 13,215.24 | -104.63 | -0.79% |

| DJIA | 32,627.97 | -150.67 | -0.46% |

| Russell 2000 | 2,292.14 | -60.65 | -2.58% |

| S&P 500 | 3,925.61 | -17.73 | -0.45% |

| Gold Futures | 1,744.10 | +21.70 | +1.26% |

| XAU | 141.57 | +1.84 | +1.32% |

| S&P/TSX VENTURE COMP IDX | 995.15 | +12.92 | +1.32% |

| S&P/TSX Global Gold Index | 294.66 | +8.73 | +3.05% |

| Natural Gas Futures | 2.54 | -0.06 | -2.31% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,039.53 | -94.20 | -3.01% |

| 10-Yr Treasury Bond | 1.73 | +0.46 | +35.77% |

| Gold Futures | 1,744.10 | -31.70 | -1.79% |

| S&P Basic Materials | 488.32 | +22.75 | +4.89% |

| S&P 500 | 3,925.61 | -5.72 | -0.15% |

| DJIA | 32,627.97 | +1,014.95 | +3.21% |

| Nasdaq | 13,215.24 | -750.26 | -5.37% |

| Oil Futures | 61.52 | +0.38 | +0.62% |

| Hang Seng Composite Index | 4,563.16 | -477.66 | -9.48% |

| S&P/TSX Global Gold Index | 294.66 | +4.89 | +1.69% |

| XAU | 141.57 | +4.14 | +3.01% |

| Russell 2000 | 2,292.14 | +36.03 | +1.60% |

| S&P Energy | 370.11 | +22.56 | +6.49% |

| S&P/TSX VENTURE COMP IDX | 995.15 | -89.20 | -8.23% |

| Natural Gas Futures | 2.54 | -0.68 | -21.09% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 141.57 | -6.68 | -4.51% |

| S&P/TSX Global Gold Index | 294.66 | -32.98 | -10.07% |

| Gold Futures | 1,744.10 | -153.10 | -8.07% |

| DJIA | 32,627.97 | +2,324.60 | +7.67% |

| S&P 500 | 3,925.61 | +203.13 | +5.46% |

| Nasdaq | 13,215.24 | +450.49 | +3.53% |

| Korean KOSPI Index | 3,039.53 | +269.10 | +9.71% |

| Natural Gas Futures | 2.54 | -0.10 | -3.64% |

| S&P Basic Materials | 488.32 | +37.92 | +8.42% |

| Russell 2000 | 2,292.14 | +314.09 | +15.88% |

| Oil Futures | 61.52 | +13.16 | +27.21% |

| Hang Seng Composite Index | 4,563.16 | +369.27 | +8.80% |

| S&P/TSX VENTURE COMP IDX | 995.15 | +178.22 | +21.82% |

| S&P Energy | 370.11 | +71.78 | +24.06% |

| 10-Yr Treasury Bond | 1.73 | +0.79 | +84.90% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

China Southern Airlines

Delta Air Lines

Southwest Airlines

JetBlue Airways Corp.

Wizz Air Holdings

MMC Norilsk Nickel PJSC

Gran Colombia Gold Corp

Facebook Inc.

The Clorox Co.

Volkswagen AG

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Bloomberg Commodity Spot Index measures the price movements of commodities included in the Bloomberg CI and select subindexes. It does not account for the effects of rolling futures contracts or the costs associated with holding physical commodities and is quoted in USD. The Manheim Used Vehicle Value Index is a measurement of used vehicle prices that is independent of underlying shifts in the characteristics of vehicles being sold. Statistical analysis is applied to its database of more than 5 million used vehicle transactions annually. The Philadelphia Federal Index (or Philly Fed Index) is a regional federal-reserve-bank index measuring changes in business growth covering the Pennsylvania, New Jersey, and Delaware region.