This Summer Could Be the Start of a New Roaring Twenties

Date Posted: March 12, 2021

Read time: 44 min

A little over a hundred years ago, the United States emerged from the double whammy of a world war and deadly pandemic. Eager to get back to "normal" life, Americans went on a decade-long spending splurge, buying cars and radios and stocks.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

A little over a hundred years ago, the United States emerged from the double whammy of a world war and deadly pandemic. Eager to get back to “normal” life, Americans went on a decade-long spending splurge, buying cars and radios and stocks.

Although we all know how it ended, the Roaring Twenties was largely a product of pent-up demand.

This summer, I believe we could see the start of a similar demand-driven economic boom as millions of Americans, newly vaccinated and $1,400 richer, make up for lost time by booking flights and vacations, going on cruises, visiting family out of state and more.

As I shared with you earlier this month, close to $18 trillion sit in Americans’ savings accounts right now—a record amount. Much of this cash is just waiting to be unleased into the U.S. economy.

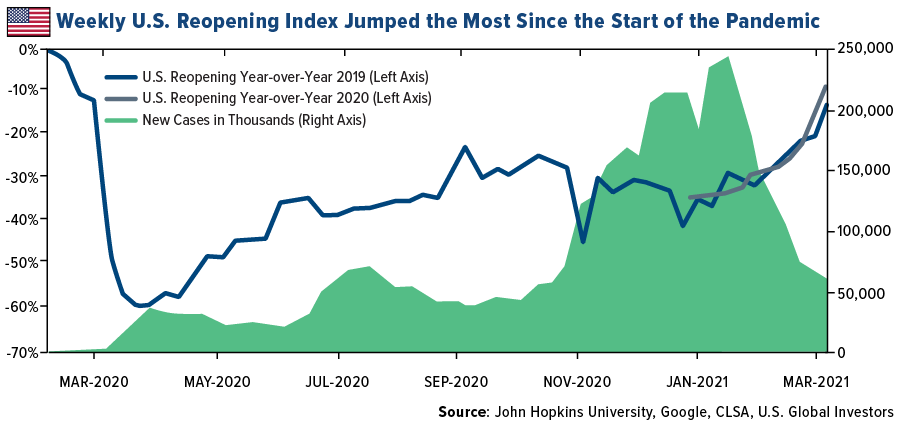

Things are already heading in the right direction. According to CLSA’s proprietary reopening index, the U.S. saw the biggest weekly gain since the start of the pandemic, up 8%, as the number of new daily infections dropped further. Here in Texas, all COVID-19 restrictions were lifted 100% on Wednesday, right on time for Spring Break.

Airlines Betting on a Strong Rebound in Summer Bookings

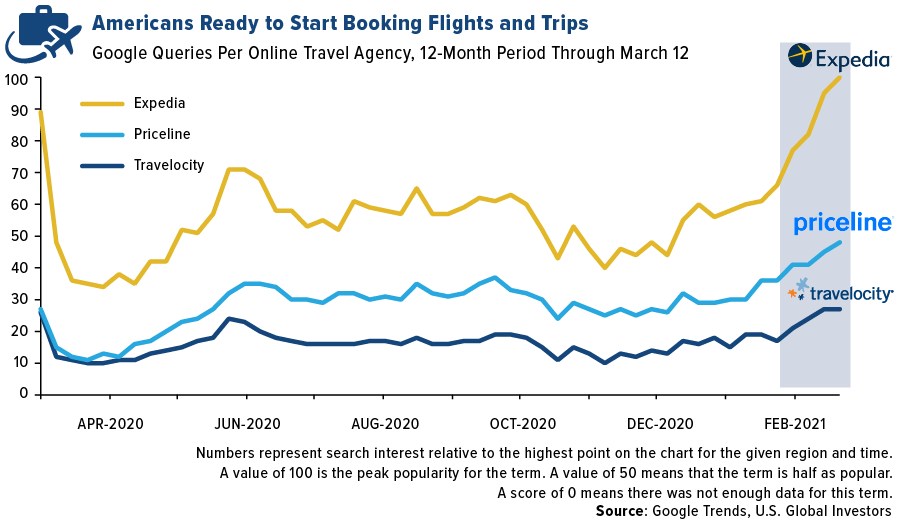

This week marks the one-year anniversary of the start of the pandemic, and if Google Trends data is any indication, Americans are ready to travel again. The number of Google queries for online travel agencies Expedia, Priceline and Travelocity hit pandemic highs this week as airlines announced new deals and routes.

Low-cost carriers Allegiant and Southwest recently expanded their networks to include 36 new non-stop routes in the former’s case, 17 in the latter’s. According to Bloomberg, this the second-largest network expansion in Allegiant’s history and the largest for Southwest since 2013.

Across the Atlantic, Lufthansa is also adding to its slate of summer destinations in anticipation of a strong rebound in bookings. Europe’s largest carrier will add around 20 new routes from Frankfurt and 13 from Munich to vacation spots such as the Caribbean, Canary Islands and Greece.

Meanwhile, credit card data from the end of February shows an uptick in airline booking among older Americans—those most likely to have been fully vaccinated. At a Raymond James conference last week, the CEOs of Delta and Spirit told investors that bookings took a positive turn in mid-February.

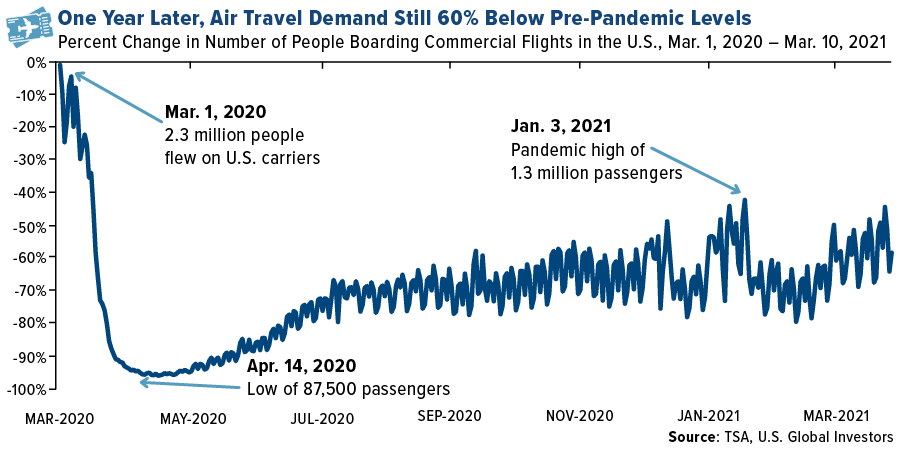

Passenger volume in the U.S. is still down about 60% compared to pre-pandemic levels, but I expect this to improve the closer we get to vacation season and as more people get their shots. Cowan aviation analyst Helane Becker, who helped us launch our airlines ETFs in 2015, told Yahoo Finance that she believed the number of daily passengers would cross above 1 million by March 20.

American Airlines is so optimistic on a recovery in summer leisure travel that it just increased the size of its debt financing, from $7.5 billion to $10 billion. The debt, according to MarketWatch, is underpinned by the carrier’s $20 billion AAdvantage loyalty program.

Another sign that airlines are sensing a shift in Americans’ appetite for air travel? Budget carrier Frontier filed to IPO this Monday, saying that it was “well positioned to take advantage of the anticipated demand recovery as vaccine distribution continues.” Rival carrier Sun Country also provided new details for its own upcoming IPO on Monday, telling investors it seeks to raise some $200 million to help pay off pandemic crisis loans from the federal government.

$15 Billion Stimulus for Airlines and Airline Contractors, $8 Billion for Airports

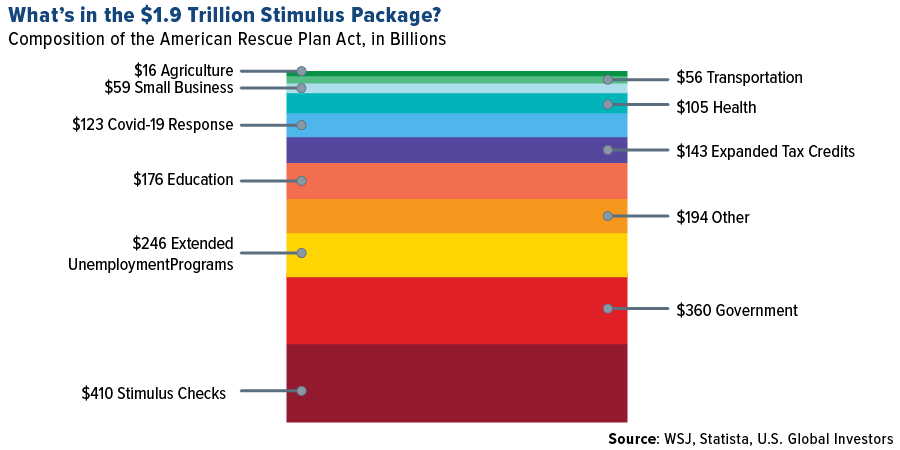

The U.S. aviation industry is set to receive another round of fresh stimulus now that President Joe Biden has signed the $1.9 trillion rescue package.

American and United immediately dropped plans to lay off or furlough a combined 27,000 workers.

Included in the bill is approximately $15 billion for airlines and airline contractors, $8 billion for airports and concessionaires.

As expected, U.S. airline and airport trade groups were quick to praise the rescue package. Airlines for America (A4A) wrote that it’s “vital to have our employees on the job and ready to assist as our nation prepares to move forward from this crisis,” while the American Association of Airport Executives (AAAE) said that the amount earmarked for airports “underscores the enormous financial impact that the pandemic is having on airports and the entire aviation ecosystem.”

How the Semiconductor Chip Shortage Will Contribute to Inflation

One of the anticipated consequences of economic reopening is higher inflation. Add trillions of dollars in new debt and money-printing, and inflation could end up being hotter than any of us expected.

This week, the Bureau of Labor Statistics (BLS) reported that the consumer price index (CPI) rose slightly to 1.7% year-over-year in February, up from 1.4% in January.

Of the items tracked by the BLS, used car and truck prices advanced the most at 9.3%. This was the sixth straight month that used vehicle prices jumped more than 9% compared to last year.

The reason for this is simple economics: Too few vehicles available for sale during the pandemic and too many buyers.

|

The price hike is likely to continue with the global shortage in semiconductor chips, which are used extensively in automotive manufacturing. The “smarter” our cars and trucks get, the more chips are needed.

In a research report this week, CLSA writes that the chip shortage “should ultimately hasten electrification of the global automotive industry.” With chip supply in question, automakers are shifting priority to the products highest in demand right now, i.e., electric vehicles (EVs). A number of companies, including Ford, General Motors and Toyota, have extended plant shutdowns due to limited chip availability.

As a result, prices for traditional internal combustion engine (ICE) vehicles will certainly face upward pressure as fewer of them roll off factory floors.

The moral to the story? If you’re in the market for a new car or truck, you might want to make a purchase sooner rather than later.

Ethereum Mining Revenue Broke Above $1 Billion for the First Time

The chip shortage has hit other industries, of course, including crypto mining. Demand from miners is so high right now that chipmaker Nvidia announced it will be releasing a new series of semiconductors designed specifically for mining Ethereum.

In other Ethereum-related news, Coin Metrics data shows that monthly revenue generated by Ethereum miners hit a record $1.37 billion in February, an incredible 1,300% increase from the same month in 2020, and a 65% increase from the previous month.

Miner revenue includes inflation rewards (block subsidy) and transaction fees. Miners are paid rewards in the blockchain’s native currency for producing valid blocks and processing transactions.

This is very good news for HIVE Blockchain Technologies, the only publicly traded crypto miner that mines both Bitcoin and Ethereum using 100% green energy.

Missed our webcast this week on crypto and gold? You’re in luck! The replay is available to listen to by clicking here.

Gold Market

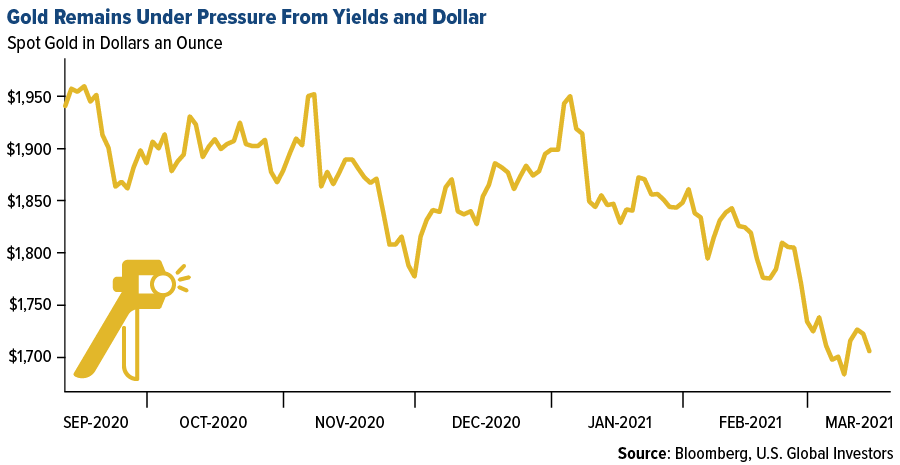

This week spot gold closed the week at $1,727.11, up $26.47 per ounce, or 1.56%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.93%. The S&P/TSX Venture Index came in up 6.96%. The U.S. Trade-Weighted Dollar fell 0.34%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-10 | CPI YoY | 1.7% | 1.7% | 1.4% |

| Mar-11 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Mar-11 | Initial Jobless Claims | 725k | 712k | 754k |

| Mar-12 | Germany CPI YoY | 1.3% | 1.3% | 1.3% |

| Mar-12 | PPI Final Demand YoY | 2.7% | 2.8% | 1.7% |

| Mar-16 | ZEW Survey Expectations | 74.0 | — | 71.2 |

| Mar-16 | ZEW Survey Current Situation | -61.5 | — | -67.2 |

| Mar-17 | Eurozone CPI Core YoY | 1.1% | — | 1.1% |

| Mar-17 | Housing Starts | 1570k | — | 1580k |

| Mar-17 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Mar-18 | Initial Jobless Claims | 700k | — | 712k |

Strengths

- The best performing precious metal for the week was platinum, up 6.45% as it continues to pick up momentum from electrification. Gold rose the most in two months on Tuesday, rebounding from a nine-month low on a weaker U.S. dollar before falling at the end of the week. Rory Townsend, head of gold research at Wood Mackenzie said that “we just don’t think bond yields will rise indefinitely. We expect to see a resurgence in gold in the second half of the year as inflation picks up.” President Joe Biden signed a $1.9 trillion COVID-19 stimulus bill this week.

- Franco-Nevada Corp reported record financial results for 2020, selling 521,564 gold equivalent ounces and increasing revenue by 21% to $1.02 billion. The company boosted its quarterly dividend by 15.4% to $0.30 a share.

- Wheaton Precious Metals reported over $1 billion in revenue for the year ended December 31, a 27% increase from the year prior due to a 28% increase in the average realized gold equivalent price. Kitco News reports the royalty and streaming company saw $208 million in operating cash flow in the fourth quarter and a net debt reduction of $275 million.

Weaknesses

- The worst performing precious metal for the week was palladium, but still up 1.47% as precious metals got an across-the-board boost. Gold dipped on Friday, nearly erasing gains made earlier in the week as both bond yields and the U.S. dollar rose. Higher Treasury bond yields weaken demand for non-interest-bearing bullion.

- ETFs backed by gold saw 144,432 troy ounces of outflows on Wednesday, bringing net sales for 2021 to 4.84 million ounces. Bloomberg data shows it to be the 19th straight day of declines.

- Silver is also facing headwinds from higher real rates. UBS Group AG’s global wealth management unit said high real rates are unlikely to fade soon and lowered its silver price forecasts to $25 an ounce across all time periods.

Opportunities

- Commodity strategists at RBC Capital Markets say the gold-versus-bitcoin comparison is overdone. Gold and bitcoin “may prove to be complementary assets that at times also compete on the margin.” Bitcoin is more volatile than gold and the two markets have different sizes and depths.

- Senior silver producer First Majestic Silver announced a deal to acquire Jerritt Canyon Canada Ltd. from Sprott Mining for $470 million in shares plus five million warrants. The move brings First Majestic into Nevada. The company said this acquisition, plus its two operating mines in Mexico, will help the North American producer hit its annualized production of 30 to 33 million silver equivalent ounces. This marks another consolidation transaction in the mid-tier space following the taking of Premier Gold by Equinox Gold. With the pull back in gold prices some attractive valuations can be found, where a deal might get done now.

- FireFox Gold shares rose nearly 30% after announcing it secured new gold concessions in the Central Lapland Greenstone Belt in Finland. The company is rapidly expanding its exploration reach in Finland, which is seeing somewhat of a gold rush.

Threats

- Bloomberg’s Eddie van der Walt writes that gold could decline further to $1,500 an ounce before finding a bottom as the “doomsday” reason to buy gold is over. Gold had a strong buy signal when the pandemic first broke out, but the vaccine rollout and economy recovery take away the safe-haven appeal. The investment case for gold is collapsing for many as yields remain high and outflows from gold-backed ETFs continue.

- Gold is “failing as an equity hedge” according to BlackRock portfolio manager Russ Koesterich. In a blog post last week, Koesterich says gold faces a double whammy of being a less effective hedge against stocks and inflation, plus the headwind of the economic recovery.

- Alamos Gold said it may take legal action against the government of Turkey for failing to renew its mining license, reports Bloomberg. Alamos has a 60-year mining permit for the Kirazli project that requires re-approval every 10 years, but operations have been halted since 2019 as the government has not renewed the permit. Alamos spent $6.6 million last year in Kirazli for holding costs and government, public and community-relations initiatives, according to its latest earnings release. In 2017, the company said 540,000 ounces of gold could be produced from the mine in five years.

Index Summary

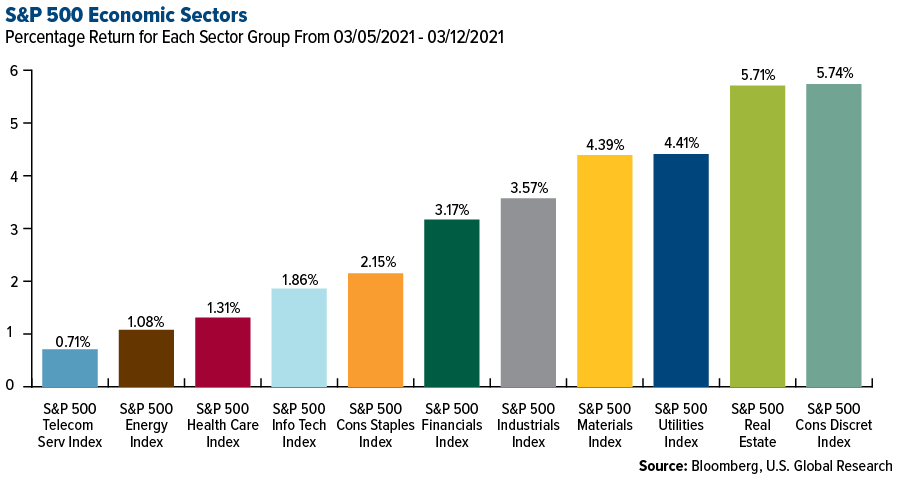

- The major market indices finished up this week. The Dow Jones Industrial Average gained 4.07%. The S&P 500 Stock Index rose 2.64%, while the Nasdaq Composite climbed 3.09%. The Russell 2000 small capitalization index gained 7.38% this week.

- The Hang Seng Composite lost 0.62% this week; while Taiwan was up 2.52% and the KOSPI rose 0.93%.

- The 10-year Treasury bond yield rose 6 basis points to 1.626%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Chiliz, rising 355.65%.

- The Central Bank of Russia is planning to launch its prototype of the ruble-backed digital currency. Alexey Zabotkin, the bank’s deputy chairman, explained that the prototype will be available for people to use and give feedback on, but will not support any real money transactions. The plan, according to Zabotkin, is to study the usage of the prototype and make necessary developments to start testing the digital currency in 2022.

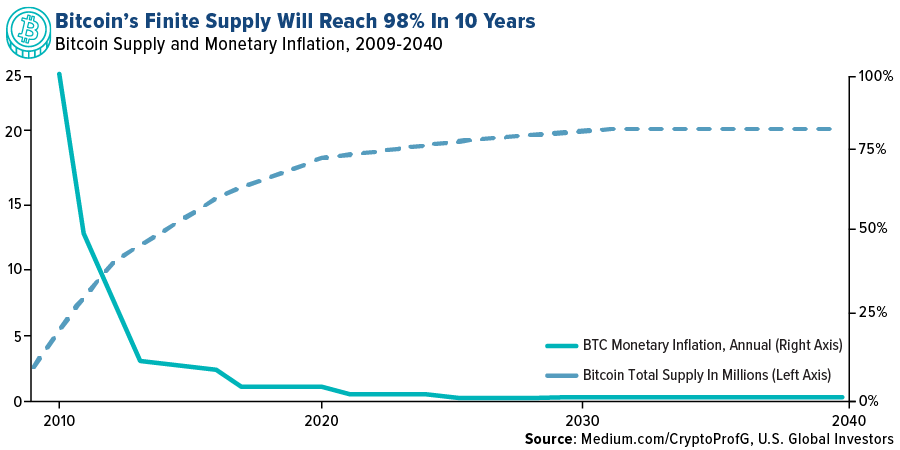

- Christie’s, the storied auction house, completed the sale of “EVERYDAYS: THE FIRST 5000 DAYS” by crypto artist Beeple. The digital artwork, created as a non-fungible token (NFT) on the Ethereum blockchain, was sold for a record $69.3 million. Ether was supported as a payment option for the first time by Christie’s, and it is unclear whether the buyer used fiat or cryptocurrency to buy the artwork. The chart below shows that Bitcoin’s finite supply will reach 98% within this decade and decrease its monetary inflation to near 0% within the same time frame.

click to enlarge

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was NEM, down 45.06%.

- Binance, the cryptocurrency exchange, is being investigated by the Commodity Futures Trading Commission (CFTC) to determine whether U.S. residents traded derivatives on it, which is a violation. For now, Binance has not been accused of any wrongdoing and the CFTC might not bring any enforcement action. This probe into Binance is another sign that regulators in the U.S. are trying to funnel investors into regulated channels.

- Analysis has shown that companies allocating their balance sheet to Bitcoin risk their company stock to be highly correlated with the volatile digital asset. The correlation coefficient between Bitcoin and an equal-weighted basket of five stocks that announced investments in the cryptocurrency – Tesla, MicroStrategy, Square, Meitu and Aker ASA – has shot up to an average of 0.72 this year from 0.26 in 2020.

Opportunities

- BlockFi, one of the world’s largest cryptocurrency lenders, raised $350 million in its Series D funding round, co-led by Bain Capital Ventures. This funding round gives BlockFi a valuation of $3 billion, and currently has $10 billion in outstanding loans and $15 billion in total assets. Zac Prince, BlockFi’s CEO, mentioned that the company has been operating profitably for several months and is looking to cement itself as the leading lender in the cryptocurrency industry, providing both trade execution services for institutions and opportunities for retail investors to get yield on their Bitcoin holdings.

- WisdomTree, the exchange-traded fund (ETF) giant, has become the latest investment company to apply for launching a Bitcoin ETF by filing an S-1 form with the U.S. Securities and Exchange Commission. The company intends to list the shares of its ETF on Cboe’s BZX Exchange. Grayscale is mulling either applying for a new Bitcoin ETF or converting the Grayscale Bitcoin Trust into an ETF.

- Binance is adding new features to its cryptocurrency payment platform that it released as a beta in February. Binance Pay is set to allow businesses to process payments in crypto, both online and in-person, via QR codes and a dedicated API. The beta version only allowed peer-to-peer payments and drew a reported 250,000 users and the platform supports more than 30 cryptocurrencies, including Bitcoin, Ether, dogecoin, as well as five fiat currencies: the Australian dollar, Brazilian real, euro, U.K. pound and Turkish lira.

Threats

- Uncertainty surrounding cryptocurrency regulations in South Africa is driving cryptocurrency startups away from the country in search for friendlier environments. Revix, a Cape Town-based crypto and fintech startup, is reportedly shifting its head office to the U.K. and planning a Germany-based location. This is just one of multiple crypto startups and exchanges leaving the country. The Financial Sector Conduct Authority (FSCA) is seeking to regulate digital currencies with more power to prosecute fraudsters and will focus on better protection for consumers rather than businesses, according to Head of Enforcement Brandon Topham.

- The Internet and Mobile Association of India (IAMAI) is appealing to the Indian government not to ban cryptocurrencies and is proposing that the government introduce mechanisms to regulate the crypto sector claiming that the country could see considerable benefits such as job creation. This is in response to the Indian government planning to introduce a bill into the parliament’s budget session that would ban “private cryptocurrencies.” Cryptocurrency trading volume in India reached $1.4 billion this January, before jumping to $2.3 billion in February.

- South Korea’s Financial Services Commission (FSC), the country’s leading financial regulator, has introduced penalties for cryptocurrency exchanges that do not implement stringent anti-money laundering laws. Crypto exchanges and other companies that facilitate crypto transactions will face fines between $26,000 to $52,000 if such laws are not implemented.

Domestic Economy and Equities

Strengths

- U.S. consumer sentiment improved in early March by more than forecast, reaching a one-year high as more vaccinations and fiscal relief boosted optimism in the economic outlook. The University of Michigan’s preliminary sentiment index jumped to 83 from 76.8 in February, data released Friday showed.

- The number of Americans filing new claims for jobless benefits dropped to a four-month low last week as an improving public health environment allows more segments of the economy to reopen, putting the labor market recovery back on track. Initial claims for state unemployment benefits decreased 42,000 to a seasonally adjusted 712,000 for the week ended March 6, the lowest level since early November.

- ViacomCBS Inc was the best performing S&P 500 stock for the week, increasing 27.88%. Shares extended a 12th straight weekly gain, as Citi said it is “dangerous to be bearish” on the media company despite the recent runup in shares.

Weaknesses

- A U.S.-U.K. trade deal may not happen until at least 2024 as Joe Biden prioritizes his domestic agenda and the overriding foreign policy challenge of China. The proposed Free Trade Agreement, which was approaching fruition at the end of Trump’s administration, is on ice amid questions over when, or even if, it will be revived.

- American companies now face the highest levels of debt on record — more than $10.5 trillion, according to the Federal Reserve and the Securities Industry and Financial Markets Association. Overborrowing can result in companies becoming “fallen angels” or “zombie” companies.

- Apa Corp was the worst performing S&P 500 stock for the week, decreasing 8.69%. APA Corp. and Total SE announced they had halted drilling at an oil discovery off the coast of Suriname after pressure built up to dangerous levels.

Opportunities

- Mizuho analyst Vijay Rakesh initiated coverage of the electric vehicle makers Tesla and NIO with buy ratings. Rakesh set a $775 share price target for Tesla and a $60 share price target for NIO.

- Costco was upgraded to overweight by Wells Fargo analyst Edward Kelly with a price target of $370. Kelly cited solid membership growth and potentially "sticky" market-share gains from the now-fading pandemic. He added that recent pullback in the shares could be a buying opportunity.

- Moody’s raised its outlook on the credit ratings of states and local governments to stable from negative after the passage of the $1.9 trillion relief bill, the first that helps states and municipalities make up for revenue lost during the pandemic. The company said it will help stabilize state finances and support various sectors such as mass-transit, hospitals and higher education.

Threats

- Acadia Pharmaceuticals saw analysts cut their price targets for the biopharm after the U.S. Food and Drug Administration paused a new drug application for pimavanserin, the company’s psychosis treatment.

- Several analysts lowered their one-year price targets for Poshmark after the online platform for selling high-end secondhand apparel forecast first-quarter revenue that missed estimates.

- Tanger Factory Outlet Centers was downgraded to sell from neutral by Goldman analyst Caitlin Burrows, who set a $12.50 price target on the mall operator’s stock. Burrows cited her view that Tanger’s fundamentals are weaker than before the Covid-19 pandemic erupted.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was tin, up 14.90%. EnergyAustralia is mulling accelerating the closure of a 100-year-old coal-fired plant and installing a giant storage battery to achieve a faster transition to clean power. The energy plant supplies about 20% of electricity demanded in the state of Victoria and is set to shut by mid-2028 rather than 2032. The company is planning on adding a four-hour, 350-megawatt utility-scale storage battery, which is larger than anything currently in operation globally, by 2026. Australia gas added a record amount of new renewable capacity in 2020, leading the transition away from fossil fuels.

- Copper rebounded from its lowest close in three weeks as the risk of a potential strike at a Chilean mine increased and China’s credit growth beat expectations. Antofagasta Plc’s workers at its biggest copper mine rejected the company’s final wage offer and moved a step closer to an organized strike. In 2020, the mine produced 372,100 tons of copper and the impasse is the latest in a slew of labor negotiations at Chilean mines, which account for around 25% of global copper supply. A stronger-than-expected new loans data in China boosted confidence in the country’s recovery, which is the largest importer of copper.

- Gasoline futures are at the highest levels since 2018 as expectations of global recovery and growth are high.

Weaknesses

- The worst performing commodity for the week was iron ore, down 5.96% as stockpiles of the ore hit a 22-month high in Chinese ports. In addition, Severstal PJSC announced plans to boost steel output with prices at a seven-year high.

- Iron ore’s rally since October is cooling off. On the demand side, China is stepping up the rhetoric about a fall in steel production this year while also signaling a slight tapering of support for its post-pandemic economy. On the supply side, ship-tracking data is pointing towards record volumes from Australia and official figures from Brazil show a year-over-year increase in cargoes. Chinese port stockpiles have hit the highest since November, with a record amount of ore from Brazil.

- India’s oil consumption fell almost 5% in February, which is the biggest annual drop since August 2020, amidst record high pump prices. Demand in the world’s third-largest crude importer was down from 18.1 million tons in February 2020, to 17.2 million tons in February 2021. Even though India’s oil consumption started showing signs of recovery in October 2020, demand has dropped in each of the next four months.

Opportunities

- Saudi Arabia is planning on ruling the hydrogen market in the coming decades, as the kingdom builds a $5 billion plant powered entirely by sun and wind that will be among the world’s biggest green hydrogen makers when it opens in the planned megacity of Neom in 2025. Countries throughout the world are setting up projects to utilize the gas for commercial and industrial purposes. Saudi Arabia currently has a renewable energy capacity of 700 megawatts, which is less than 2% of Spain’s installed capacity. Petrostates are expected to lose around $13 trillion by 2040 because of climate-change targets, and as the biggest exporter of crude, Saudi Arabia stands to lose the most.

- Grenergy Renovables SA, the Spanish renewable energy developer, is betting hydrogen and electrification will boost the country’s solar industry far beyond current expectations. The Spanish solar energy market has become a focal point for both local and international investors, with almost 3 gigawatts of new, subsidy free capacity commissioned in 2020. Spain is expected to double its solar capacity to 32.6 gigawatts and to increase wind capacity by 12% within the next three years. Grenergy is working on projects to produce hydrogen using renewables which are expected to be ready by 2025.

- Analysts at Cowen are expecting lithium and other rare earth minerals to soar as they are necessary components to the energy transition, which is gaining steam as governments look to decarbonize and both investors and policymakers mobilize to fund increased electrification through renewable means. They expect 13% global new electric vehicle penetration by 2025, up from 2.3% in 2019, and expand to 29% by 2030.

Threats

- Texas governor Greg Abbott is asking lawmakers to decide whether action needs to be taken to address the $16 billion in alleged overcharges for electricity during February’s blackout. Legislators are set to debate if the Electric Reliability Council of Texas (ERCOT), state’s grid operator, should retroactively adjust prices as the local power market is facing a potential financial crisis. The issue has been added as an emergency item in the current legislative session after regulators declined to act on an independent market monitor’s recommendation that charges should be reversed on the utility commission’s decision of pricing electricity at $9,000 a megawatt-hour over the course of two days during the cold snap.

- Oil’s rally to above $70 per barrel is creating genuine concerns for Asian refiners as they warn that the rapid surge in prices and spike in volatility will hurt demand and reduce already-tight processing margins. OPEC’s decision to keep oil production on a tight leash and Saudi Arabia deciding to keep its voluntary cuts in place through April sent the prices above $70 per barrel for the first time since early 2020. The issues facing refiners are illustrated in Singapore where margins dropped to 38 cents last week, lowest since January 26, 2021. The five-year seasonal average for margins is around $3.

- Trafigura Group, the world’s second largest metals trader, is expecting a global copper supply deficit if major new mine projects are not brought online as electrification drives higher prices and demand for the metal. Jeremy Weir, Trafigura’s CEO, said that this prolonged high price cycle is necessary to incentivize new production to come to stream and that the global market will need an additional 10 million tons of annual production to avoid supply deficit by 2030, with demand growth driven by electric vehicles, increased infrastructure spending and emerging markets growth.

Airline Sector

Strengths

- The best performing airline stock for the week was GOL, up 20.4%. Credit card spending shows that older Americans who have been vaccinated are starting to fly again. Spending from those aged 73-92 is four times higher than levels seen last year. The jump is not correlated to increases in lodging spending, meaning these are trips to visit family. Other age groups have not quite seen this much of a jump but should show increases as they are vaccinated.

- Frontier Airlines revived its plans to sell shares in a new IPO. The company wanted to go public last July but withdrew due to the pandemic. The company’s focus on the leisure market should position it well as vaccination continues and the pandemic recedes.

- Qantas Airways started its first passenger trial of a “vaccine passport” using the Common Pass digital health app. The Australian carrier has said that vaccination will be mandatory to fly on the airline.

Weaknesses

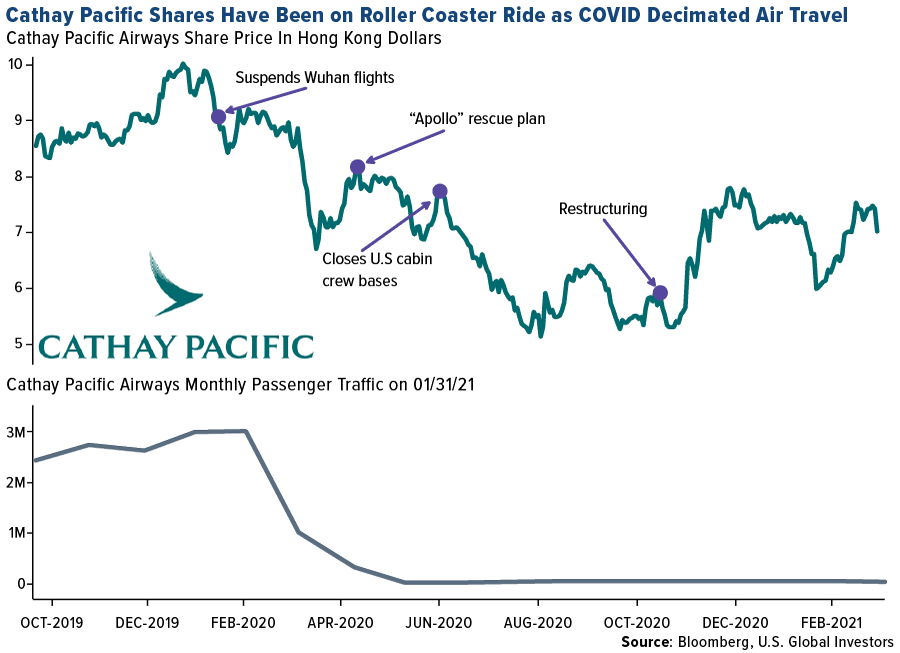

- The worst performing airline stock for the week was Air France, down 5.4%. Cathay Pacific reported a $2.8 billion loss in 2020, its worst on record. The company expects to operate below 50% of passenger capacity in 2021. At the low point of 2020, the carrier saw traffic fall 97-98 percent and flew as few as a few hundred passengers per day.

- Airline insiders have sold the most stock in three years, according to filings, with $50 million of stock sold in February. The largest sales were at Southwest, Delta, Allegiant and Mesa Air.

- Transat AT reported below consensus revenue and a loss of C$53.6 million. The company indicated that it would need C$500 million of financing if the deal it has with Air Canada is terminated.

Opportunities

- GE announced that it is merging its aviation leasing business with AerCap, including all planes, regional jets and helicopters. GE will own 45% of the new entity. This is the combination of the world’s first and second leading aircraft lessors, financing 2,000 aircraft, 900 engines and 300 helicopters. The new entity will have improved bargaining leverage versus Airbus and Boeing. Leasing is expected to remain favorable to owning aircraft due to airlines’ stretched balance sheets. Airlines have been selling aircraft they ordered to leasing companies and renting them back to obtain cash during the pandemic.

- American Airlines issued $6.5 billion of bonds and obtained a $2.5 billion term loan facility backed by the company’s loyalty program with proceeds to repay loans from the U.S. Treasury. Fitch affirmed its B- rating and removed the rating watch negative. Moody’s affirmed its B2 rating.

- U.S. airlines and travel groups are urging the Biden administration to develop a “virus passport” to document vaccinations and test results. A negative test is required for those entering the U.S. via airplane.

Threats

- The Boeing 737 MAX jet could have another mechanical issue. An aircraft headed to Newark Airport declared an emergency and shut down one engine for the landing due to an unknown mechanical issue related to low engine oil pressure.

- Higher fuel prices are generally a headwind for airlines, with some hedging costs and others not. Air Canada and Spirit tend to be less hedged while Southwest and Delta tend to be the most hedged.

- Some aggressive price cutting is starting among the airlines as they ramp up operations. Allegiant has been offering fares for as low as $39. Average domestic fares fell to $245, the lowest on record.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Russia gaining 3.5%. The best performing country in Asia was Taiwan, gaining 2.5%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 1.3%. The Indian rupee was the best performing currency in Asia, gaining 80 basis points.

- China’s credit growth picked up in February. Bank loan growth came in at 12.9% year-over -year in February versus 12.7% in January. Money supply growth also picked up to 10.1% year-over-year versus 9.4% in January.

Weaknesses

- The worst relative performing country in emerging Europe for the week was the Czech Republic, gaining 90 basis points. The worst performing country in Asia was Pakistan, losing 4.5%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 85 basis points. The Malaysian ringgit was the worst performing in Asia, losing 1.1%.

- The Unites States and United Kingdom are efficient in vaccine rollouts, but Europe has been criticized for slow progress. The euro-bloc is currently experiencing a lethargic immunization program and sees another wave of infections from Paris to Prague. There are rising cases in parts of the bloc, largely caused by the spread of more infectious virus variants.

Opportunities

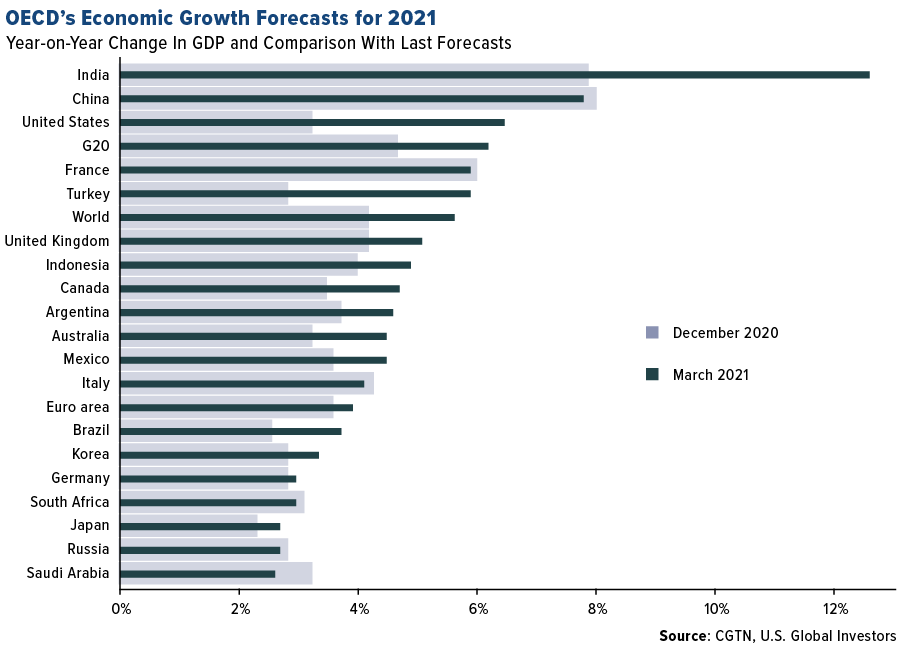

- The Paris-based Organization for Economic Cooperation (OECD) revised sharply its 2021 global growth forecast, projecting world economies to expend by 5.6%. Within emerging markets, the biggest positive revisions were assigned to India and Turkey.

- Thailand, which heavily depends on tourism revenue, will cuts its quarantine period from 14 to seven days, but travelers must be vaccinated and test three days prior arrival. To attract more visitors, the government launched a new initiative allowing foreign travelers to spend the seven days in quarantine on a yacht and will have to wear a wristband tracking their vitals and location.

- The European Central Bank pledged to ramp up government debt purchases in the coming months to contain rising bond yields. The bank kept the overall size of the pandemic program unchanged and held rates. The inflation forecast for this year was revised up to 1.5% from 1%. The GDP forecast was lifted to 4% for this year, up from 3.9%.

Threats

- The Washington Post reports that President Biden’s second big bill may be one sponsored by Senate Majority Leader Chuck Schumer that seeks to boost U.S. manufacturing and supply lines, diluting reliance on Chinese imports.

- Due to a spike in coronavirus infections, Poland will follow the Czech Republic and Hungary decisions to tighten anti-Covid restrictions. The government said that if the situation does not stabilize, then it may launch a countrywide lockdown again.

- There is a shortage of vaccines in Europe, and Eurozone members are looking to purchase the shots for higher price outside of the bloc. Hungary said it was paying the equivalent of about $37.5 per dose for Chinese company Sinopharm’s Covid-19 vaccine and $9.95 per dose for the Russian Sputnik-V vaccine, well above the price of Pizer/BioNTech or AstraZeneca vaccines approved by the European Medicines Agency.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.63 | +0.06 | +3.70% |

| Oil Futures | 65.61 | -0.48 | -0.73% |

| Hang Seng Composite Index | 4,526.61 | -28.35 | -0.62% |

| S&P Basic Materials | 492.42 | +20.69 | +4.39% |

| Korean KOSPI Index | 3,054.39 | +28.13 | +0.93% |

| S&P Energy | 400.82 | +4.28 | +1.08% |

| Nasdaq | 13,319.86 | +399.71 | +3.09% |

| DJIA | 32,778.64 | +1,282.34 | +4.07% |

| Russell 2000 | 2,354.02 | +161.81 | +7.38% |

| S&P 500 | 3,943.42 | +101.48 | +2.64% |

| Gold Futures | 1,722.90 | +24.40 | +1.44% |

| XAU | 139.73 | +6.15 | +4.60% |

| S&P/TSX VENTURE COMP IDX | 982.25 | +63.89 | +6.96% |

| S&P/TSX Global Gold Index | 285.73 | +5.35 | +1.91% |

| Natural Gas Futures | 2.59 | -0.11 | -4.04% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,054.39 | -46.19 | -1.49% |

| 10-Yr Treasury Bond | 1.63 | +0.50 | +44.79% |

| Gold Futures | 1,722.90 | -119.80 | -6.50% |

| S&P Basic Materials | 492.42 | +30.73 | +6.66% |

| S&P 500 | 3,943.42 | +33.54 | +0.86% |

| DJIA | 32,778.64 | +1,340.84 | +4.27% |

| Nasdaq | 13,319.86 | -652.67 | -4.67% |

| Oil Futures | 65.61 | +6.93 | +11.81% |

| Hang Seng Composite Index | 4,526.61 | -332.97 | -6.85% |

| S&P/TSX Global Gold Index | 285.73 | -24.80 | -7.99% |

| XAU | 139.73 | -3.92 | -2.73% |

| Russell 2000 | 2,354.02 | +71.58 | +3.14% |

| S&P Energy | 400.82 | +65.34 | +19.48% |

| S&P/TSX VENTURE COMP IDX | 982.25 | -82.60 | -7.76% |

| Natural Gas Futures | 2.59 | -0.32 | -10.96% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 139.73 | -0.37 | -0.26% |

| S&P/TSX Global Gold Index | 285.73 | -26.60 | -8.52% |

| Gold Futures | 1,722.90 | -118.60 | -6.44% |

| DJIA | 32,778.64 | +2,779.38 | +9.26% |

| S&P 500 | 3,943.42 | +275.32 | +7.51% |

| Nasdaq | 13,319.86 | +914.05 | +7.37% |

| Korean KOSPI Index | 3,054.39 | +307.93 | +11.21% |

| Natural Gas Futures | 2.59 | +0.04 | +1.53% |

| S&P Basic Materials | 492.42 | +45.90 | +10.28% |

| Russell 2000 | 2,354.02 | +431.32 | +22.43% |

| Oil Futures | 65.61 | +18.83 | +40.25% |

| Hang Seng Composite Index | 4,526.61 | +400.92 | +9.72% |

| S&P/TSX VENTURE COMP IDX | 982.25 | +206.91 | +26.69% |

| S&P Energy | 400.82 | +90.87 | +29.32% |

| 10-Yr Treasury Bond | 1.63 | +0.72 | +79.07% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

Franco-Nevada Corp

Wheaton Precious Metals Corp

FireFox Gold Corp

Alamos Gold Inc

GOL Linhas Aereas Inteligentes

Qantas Airways Ltd

Southwest Airlines Co

Delta Air Lines Inc

Allegiant Travel Co

Air Canada

American Airlines Group Inc

Spirit Airlines Inc

Moody’s Corp

Costco Wholesale Corp

Tesla Inc

Total SE

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The University of Michigan Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan. Each month at least 500 telephone interviews are conducted of a contiguous United States sample. Fifty core questions are asked. Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Mr. Holmes owns shares of HIVE while U.S. Global Investors owns convertible securities.