7 Market-Moving Charts Investors Need to See

Date Posted: March 22, 2019

Read time: 55 min

Stocks erased their weekly gains and bond yields fell today as investors reacted to a number of economic developments. Chief among them were a Treasury yield curve inversion, the first since before the financial crisis, and continued slowdown in the pace of U.S. manufacturing expansion.

Press Release: U.S. Global Investors Continues GROW Dividends

Stocks erased their weekly gains and bond yields fell today as investors reacted to a number of economic developments. Chief among them were a Treasury yield curve inversion, the first since before the financial crisis, and continued slowdown in the pace of U.S. manufacturing expansion.

I had my eye on several other market-moving news items, some of which I share with you below.

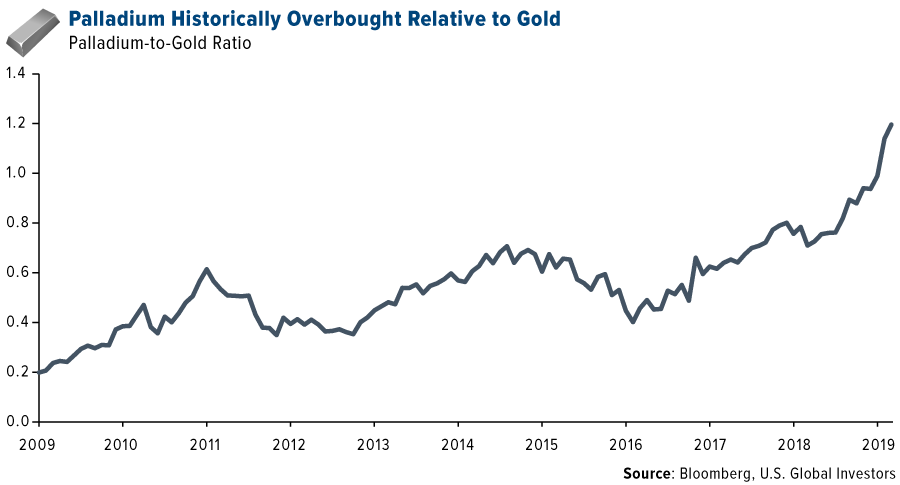

1. Palladium in Overbought Territory

The price of palladium briefly topped $1,600 an ounce for the first time ever this week on a widening supply-demand imbalance. Markets sent the metal higher on news out of Russia that the world’s number one producer of palladium was set to ban the export of scrap metal, which would have the effect of squeezing global supply even further. This comes a week after car manufacturers signaled an increase in demand for palladium, which is used in the production of pollution-scrubbing catalytic converters.

As such, the palladium-to-gold ratio—or the measure of how many ounces of gold can be purchased with one ounce of palladium—is now at an historical high.

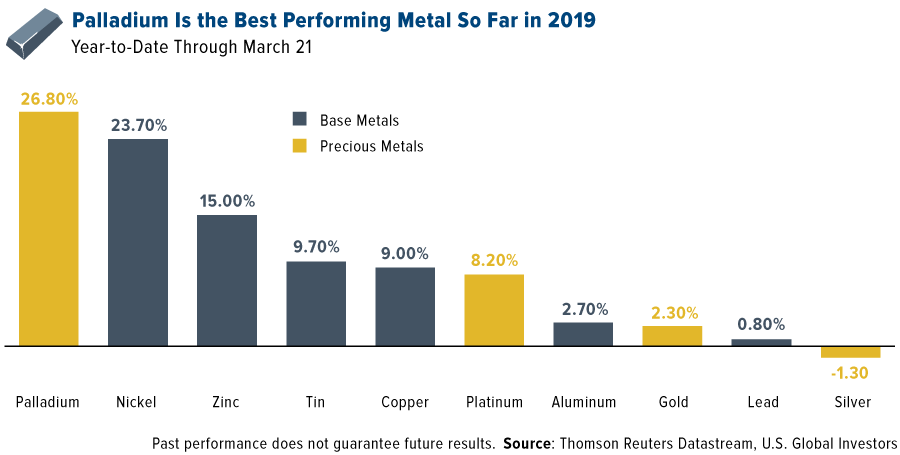

2. Nickel Also Performing Well on Supply Deficit Concerns

Palladium is the best performing metal so far in 2019, up nearly 27 percent. In second place is nickel, which is facing supply issues of its own. Global demand for nickel in 2019 is estimated at around 2.4 million metric tons, two thirds of which will be processed in stainless steel mills, mostly in China, according to Reuters.

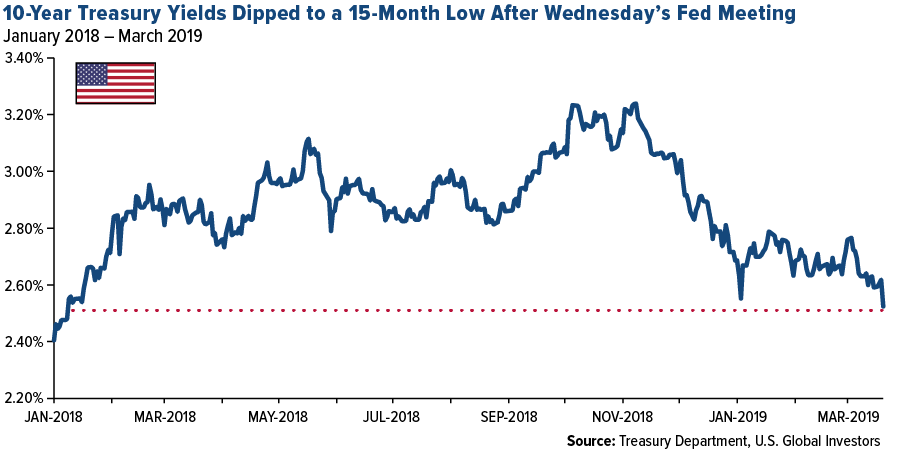

3. Markets Grapple With First Yield Inversion Since Before the Financial Crisis

The yield on the 10-year Treasury fell to a more-than-one-year low this week on a dovish Federal Reserve. Fed Chair Jerome Powell indicated that interest rates were likely to stay unchanged throughout 2019 as officials assess the impact of a potential global economic slowdown. “Just as strong global growth was a tailwind,” Powell said, “weaker global growth can be a headwind to our economy.”

On Friday, the yield curve between the three-month and 10-year yield inverted, or turned negative, for the first time since before the financial crisis. Although past performance does not guarantee future results, it’s worth noting that such an inversion has preceded every U.S. recession over the last 60 years.

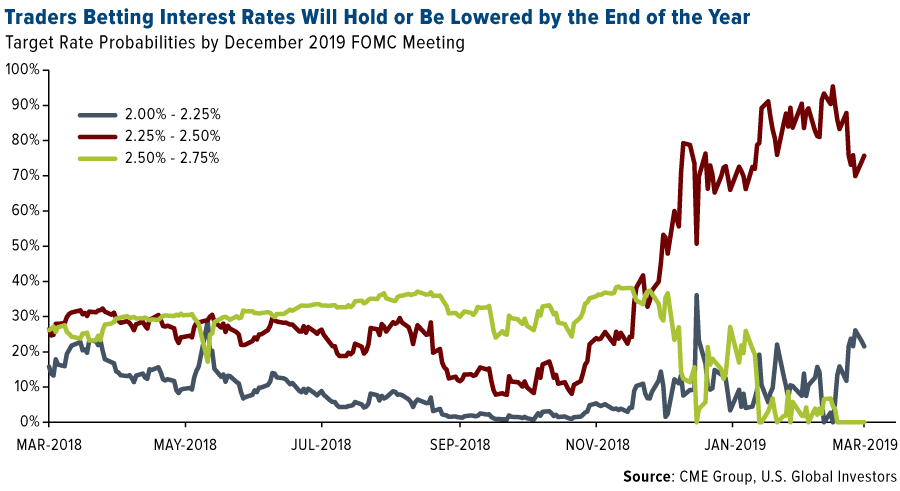

4. Traders Don’t See Rates Changing

Even before Wednesday’s Fed announcement, a surging number of futures traders were betting that rates would stay unchanged, or even be lowered, between now and the end of 2019. Three quarters of traders this month were positive that rates would stay pat in the 2.25 percent to 2.50 percent range, up sharply from 26 percent of traders 12 months earlier, according to the CME Group’s FedWatch Tool. The probability that rates will be hiked by the end of the year are now at 0 percent.

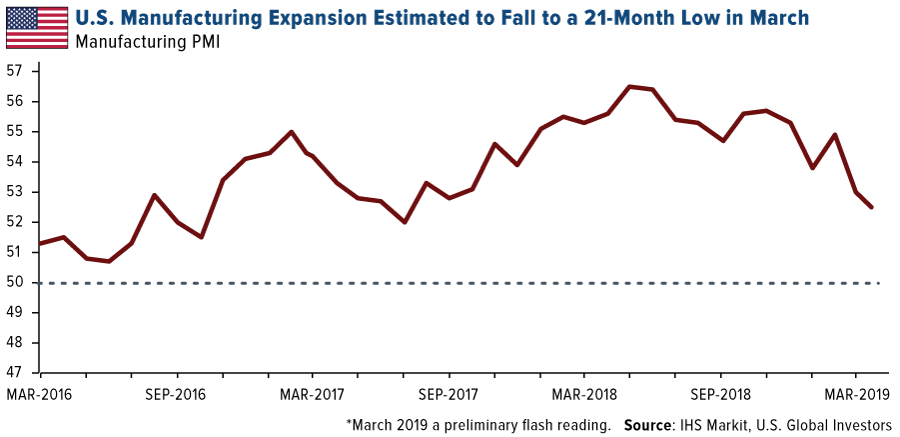

5. Pace of Manufacturing Growth Continues to Slow

The preliminary U.S. purchasing manager’s index (PMI), released today, shows manufacturing growth slowing to a 21-month low, from 53 in February to 52.5 in March. “Softer business activity growth reflected more subdued demand conditions in March, with new work rising at the weakest pace since April 2017,” the IHS Markit report reads.

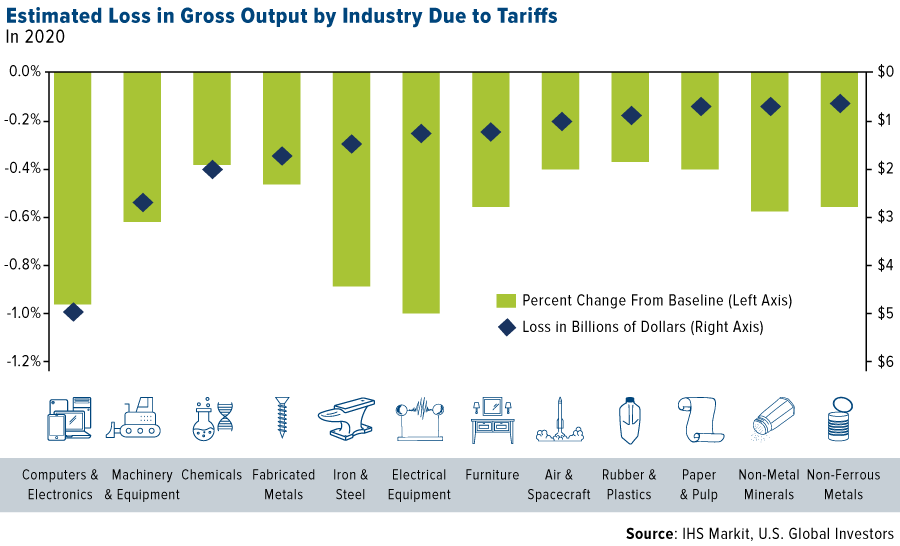

6. A “Substantial” Amount of Tariffs

Markets also appear to be coming to terms with the realization that tariffs could be the norm for a lot longer than anticipated. This week President Donald Trump said that the U.S. would keep trade barriers on China-made imports in place for a “substantial period of time”—even after a deal is eventually reached.

The U.S. currently has tariffs on approximately $265 billion worth of Chinese goods. This resulted in an eye-opening $2.7 billion tax increase on American businesses in November 2018 alone, according to Census Bureau data. Companies, as you might expect, have largely passed these extra costs on to consumers.

And then there’s lost export revenue and jobs to consider. According to a report this month by IHS Markit, tariffs are estimated to have a negative impact on the U.S. economy over the next 10 years. Ramifications include suppression of hundreds of thousands of American jobs, a dramatic reduction in consumers’ real spending power and a loss in gross output in a number of industries.

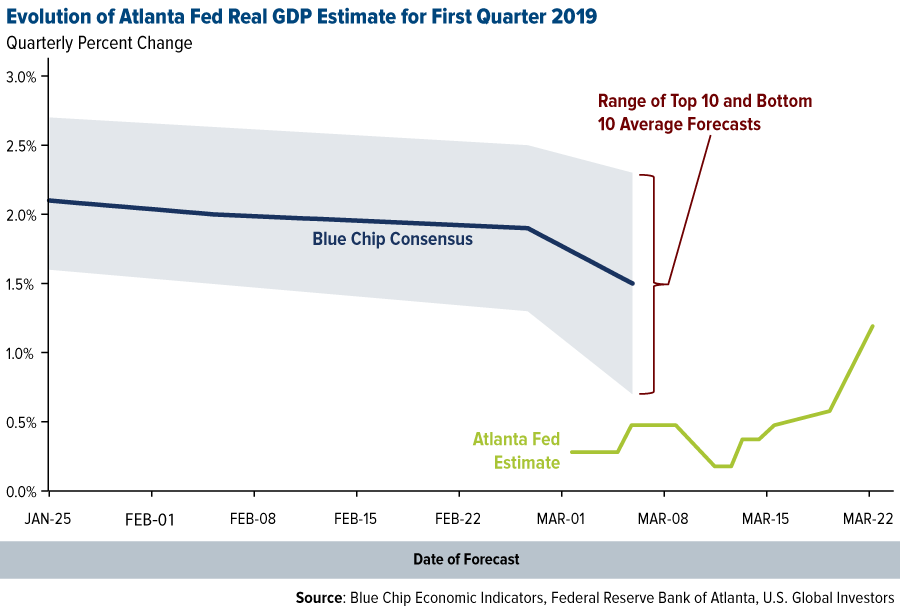

7. Fed Decides the Government Shutdown Wasn’t as Bad as All That

The good news is that today the Atlanta Fed revised up its estimate for real U.S. gross domestic product (GDP) growth in the first quarter. It now stands at 1.2 percent quarter-over-quarter, up from an anemic 0.4 percent on March 13.

The new estimate still trails the Blue Chip consensus of top U.S. business economists. But it appears that Fed policymakers have determined that the government shutdown between December 22 and January 25 didn’t impact the U.S. economy as negatively as previously thought.

For even more timely market commentary, subscribe to my award-winning CEO blog, Frank Talk!

Gold Market

This week spot gold closed at $1,313.70, up $11.22 per ounce, or 0.86 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.79 percent. The S&P/TSX Venture Index came in up 1.60 percent. The U.S. Trade-Weighted Dollar rose just 0.01 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-19 | ZEW Survey Current Situation | 13.0 | 11.1 | 15.0 |

| Mar-19 | ZEW Survey Expectations | -11.0 | -3.6 | -13.4 |

| Mar-19 | Durable Goods Orders | 0.4% | 0.3% | 0.4% |

| Mar-20 | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | 2.50% |

| Mar-21 | Initial Jobless Claims | 225k | 221k | 223k |

| Mar-26 | Hong Kong Exports YoY | -7.3% | — | -0.4% |

| Mar-26 | Housing Starts | 1220k | — | 1230k |

| Mar-26 | Conf. Board Consumer Confidence | 132.0 | — | 131.4 |

| Mar-28 | GDP Initial Jobless Claims | 2.50% | — | 2.50% |

| Mar-28 | Initial Jobless Claims | 223k | — | 221k |

| Mar-28 | Germany CPI YoY | 1.5% | — | 1.5% |

| Mar-29 | New Home Sales | 620k | — | 607k |

Strengths

- The best performing metal this week was platinum, up 1.85 percent on Citi recommendation and hedge funds boosting the net long position in the past week. Gold traders and analysts are bullish again this week, according to the weekly Bloomberg survey, as the Federal Reserve adopted a more dovish tone and indicated it won’t raise interest rates this year. Several countries went shopping for the yellow metal this week. Turkey’s gold reserves rose $224 million from the previous week and are now worth $20.7 billion as of March 15, according to official weekly figures from the central bank. Colombia increased holdings to 0.61 million ounces in February and are now at the highest level since 1992. Qatar’s holdings climbed to 1.31 million ounces, Ukraine’s reserves are up to 0.79 million ounces and the Kyrgz Republic’s rose to 0.38 million ounces in February. Palladium continues to shine as it topped the $1,600 per ounce level for the first time on Tuesday.

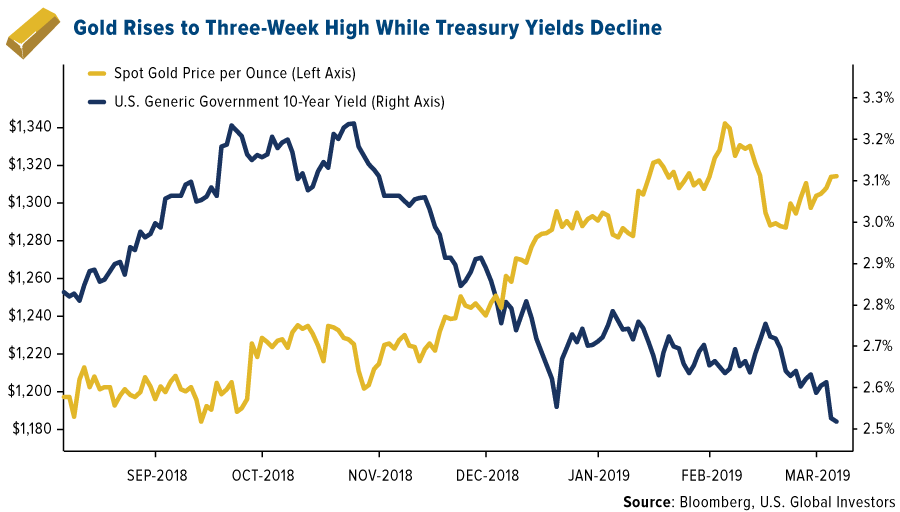

- Gold traded up to its highest level in three weeks after Fed Chairman Jerome Powell announced on Wednesday that interest rates could be on hold for “some time.” Bloomberg reports that the yield on 10-year Treasuries fell to a 14-month low of 2.52 percent and a gauge of the dollar fell the most since January. Nicky Shiels, commodity strategist at Scotiabank, says that gold will be an outperformer in the longer run during this cycle of monetary policy in which the Fed applies a prolonged pause on interest rate hikes. Investors and traders are weighing the latest U.S.-China trade developments as some familiar with the matter are concerned that China is pushing back against American demands. China may prefer to keep rebuffing President Trump, knowing he desperately needs a deal going into elections.

- Copper mining continues to gain traction in Ecuador. BHP Group has agreed to invest about $75 million for copper exploration on a deposit owned by Luminex Resources. Bloomberg reports that Luminex has already attracted interest from other miners with both Anglo American and First Quantum Minerals agreeing to back other projects it owns. Ecuador’s Deputy Mining Minister Fernando Benalcazar said this week that Lundin Gold’s Fruta del Norte gold project and Tongling Nonferrous Metal Group’s Mirador copper project will both start producing by the end of this year. These projects mark the country’s first two large-scale mining operations.

Weaknesses

- The worst performing metal this week was palladium, up just 0.04 percent as money managers cut their bullish outlook to the least bullish in the past 19 weeks. The yield spread between 3-month bills and 10-year Treasuries fell to zero this week as a surge of buying pushed long-end rates sharply lower, writes Bloomberg. This is the first time this section of the Treasury yield curve has turned negative since 2007 and is a closely watched recession gauge. Kathy Jones, chief fixed-income strategist at Charles Schwab, said that “it’s clearly a sign that the market is worried about growth and moving into Treasuries from riskier asset classes.”

- St. Barbara shares plunged more than 30 percent on Friday after it downgraded production guidance for its flagship Gwalia mine in Western Australia, reports the Australian Financial Review. CEO Bob Vassie says that the company is working on a list of merger and acquisition opportunities and isn’t put off by the big plunge in company shares. Vassie also said that the production disruption is simply short-term pain for long-term gain. St. Barbara had been considering a hydraulic lifting system to get ore to the surface faster than current trucking system. It was a smart decision to not risks the capital on this new ore moving system as there are more attractive uses of capital identified.

- Franco-Nevada stock fall as much as 5 percent after reporting revenue and earning miss this week. Short-interest ratio in shares of the company rose 333 percent, according to Toronto stock exchange data leading up to the miss. Bloomberg reports that the number of days needed to close all short positions in Franco-Nevada increased to 9.1 on March 15 from 2.1 on February 28.

Opportunities

- One of last year’s best-performing hedge funds, the Global Macro Fund by Crescat Capital, says the “trade of the century” is to buy gold and sell stocks as risk assets are due for another meltdown, writes Bloomberg’s Sarah Ponczek. According to the firm, it’s only a matter of time before bearish bets pay off as indicators are warning that a recession is imminent in the coming quarters. Crescat says that corporate insiders are currently selling stocks hand over first, which indicates a potential stock bubble burst. Two gold miners are buying back their shares – a sign of responsible management. Roxgold announced that it recently purchased for cancellation a total of 4,949,000 common shares at an average price of C$0.84 per share. Golden Star Resources said on Monday that it will buy back up to 5.4 million common shares, or 5 percent of issued and outstanding shares.

- Citigroup is bullish on platinum because its sister metal, palladium, continues to surge. Although platinum’s volatility surged to a six-month high, the bank believes the investment case for the metal is strong. It thinks substitution will eventually occur, which would raise demand and tighten supply further. Analysts including Max Layton wrote in a March 19 report that “platinum currently appears to embed an in-the-money call option on palladium.”

- Wheaton Precious Metals rose 4.3 percent on Thursday after it reported higher profits and higher sales than estimated, reports Bloomberg. National Bank of Canada writes that Wheaton is primed for future growth due to stronger than anticipated production at several of its mines. Bloomberg Intelligence highlighted this week that silver complacency is as low as it gets with lowest-for-longest implied volatility since 1993. Mike McGlone writes that “when commodities reach such extremes, up is typically the path of least resistance.” Silver could also see a boost from steady solar demand out of the European Union, which may need about 100 gigawatts of new photovoltaic power capacity by 2030, according to National Energy and Climate Plans from the bloc’s members.

Threats

- South Africa continues to experience rolling blackouts that pose big risks for the mining industry. In an effort to avoid a total grid collapse, state-run Eskom has implemented rotating blackouts and is working to assess the breakdowns across the grid. Bloomberg reports that many of Eskom’s coal-fired plants are old and unplanned breakdowns have increased. The company is also spending massive unplanned amounts on diesel to run turbines. Miners in the nation risk sending workers underground when the electricity supply is unstable.

- Bloomberg reports that Citigroup has settled a Venezuela gold swap transaction. The bank plans to sell the gold it received as collateral while also depositing about $260 million into a U.S. account that was previously controlled by President Maduro’s central bank. This is negative for the yellow metal, as distressed central bank selling usually hurts the gold price.

- Although palladium continues to be one of the hottest metals, some believe the rally will end soon. Georgette Boele, co-coordinator of FX and precious metals strategy at ABN Amro Bank, says that palladium “is the most overrated precious metal” and that the shortage is more than reflected in its price. Palladium prices rose as auto catalyst manufactures scrambled to get their hands on the metal to meet tightening emission controls. However, passenger car sales fell 17 percent last month and could signal weakening demand for the metal, writes Bloomberg’s Rupert Rowling.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.34 percent. The S&P 500 Stock Index fell 0.77 percent, while the Nasdaq Composite fell 0.60 percent. The Russell 2000 small capitalization index fell 3.06 percent this week.

- The Hang Seng Composite gained 0.38 percent this week; while Taiwan was up 1.91 percent and the KOSPI rose 0.50 percent.

- The 10-year Treasury bond yield fell 15 basis points to 2.44 percent.

Domestic Equity Market

Strengths

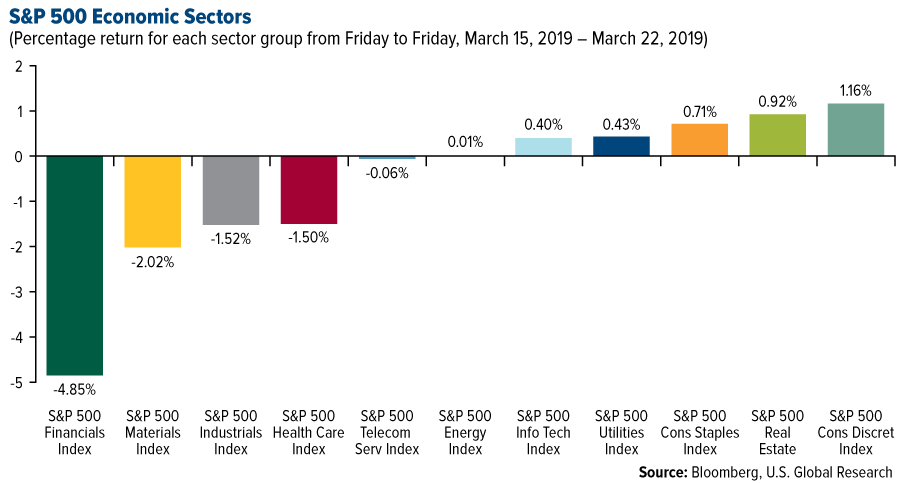

- Consumer discretionary was the best performing sector of the week, increasing by 1.16 percent versus an overall decrease of 59 basis points for the S&P 500.

- Conagra Brands was the best performing stock for the week, increasing 15.14 percent.

- Disney closed on its $71 billion deal for 21st Century Fox. The deal gives Disney content like ”The Simpsons" and "Spider-Man" for when it launches its own video streaming service.

Weaknesses

- Financials was the worst performing sector for the week, decreasing by 4.85 percent versus an overall decrease of 59 basis points for the S&P 500.

- Biogen was the worst performing stock for the week, falling 33.84 percent.

- Bayer shares fell sharply after a jury determined its Roundup weed killer causes cancer. Shares dropped more than 12 percent in Frankfurt, Germany, after a San Francisco jury found the product caused a customer to develop cancer.

Opportunities

- Lyft has kicked off its initial public offering (IPO) road show. The ride-hailing company is seeking a $23 billion valuation as it pitched investors this week, Reuters reported. The IPO, which is set to price next week, is already oversubscribed, according to people familiar with the matter.

- Google announced a huge gaming initiative: a Netflix-like video-game streaming platform named Stadia. The service is intended to run high-resolution blockbuster games on any device that runs Google’s Chrome — from smartphones and tablets to computers and TVs. It also announced a game studio that will create Stadia-exclusive games and content. The company didn’t reveal much, but the studio will be led by Jade Raymond, a former executive at both EA and Ubisoft.

- Gains among the most stable U.S. stocks point toward market strength rather than weakness, according to Ari Wald, Oppenheimer’s head of technical analysis. Wald drew the conclusion in a report from the S&P 500 Low Volatility Index’s performance. The indicator set a record last Friday after climbing 17 percent in the post-Christmas rally, according to data compiled by Bloomberg.

Threats

- Spotify described Apple as a "monopolist" as it complained over the pair’s App Store spat. After Apple contested Spotify’s antitrust filing to the EU, Spotify told Variety: "Every monopolist will suggest they have done nothing wrong and will argue that they have the best interests of competitors and consumers at heart."

- The next earnings recession could send stocks tumbling. The stock market rallied during the earnings recession of 2015-2016, but Morgan Stanley’s chief U.S. equity strategist, Mike Wilson, said equities won’t be so lucky this time.

- FedEx fell more than 5 percent after the bell on Tuesday after disappointing third fiscal quarter results and slashing its full-year earnings guidance for the second time since December, according to CNBC. The company reported earnings per share of $3.03 versus expectations of $3.11 and revenue of $17.01 billion versus $17.67 billion estimates. FedEx Executive Vice President and CFO said “slowing international macroeconomic conditions and weaker global trade growth trends continue.”

The Economy and Bond Market

Strengths

- The Conference Board’s forecast in its U.S. Leading Economic Index shows that the economy should continue to expand in the near term, rising in February for the first time in five months. February’s reading rose 0.2 percent to 111.5.

- State and local-government bonds are headed for their strongest start to a year since 2014, reports Bloomberg. The movement is due to an influx of cash into municipal-debt mutual funds as investors seek out tax havens and the Federal Reserve holds off on interest-rate increases, the article continues. In 2019 so far, the sector has returned an overall 1.8 percent, putting it on track for the best first quarter in five years.

- As reported by the Labor Department on Thursday, initial claims for state unemployment benefits fell 9,000, to a seasonally adjusted 221,000 for the week ended March 16. Despite the slowing pace of job growth, this points to still strong labor market conditions.

Weaknesses

- The Federal Reserve left interest rates unchanged on Wednesday, in a range between 2.25 percent and 2.5 percent. Officials noted that they expect not to hike rates this year and expect to end its runoff process in late September, reports Business Insider.

- U.S. factory orders rose minimally in January while shipments continued to fall for a fourth straight month, reports Reuters. The 0.1 percent rise in new orders for U.S.-made goods, as reported by the Commerce Department on Tuesday, offers more evidence of a slowdown in manufacturing activity.

- For the fourth time in five months, U.S. consumer expectations for the economy dimmed, reports Bloomberg. Bloomberg Consumer Comfort’s monthly gauge of economic expectations fell to 47.5 from 54.5.

Opportunities

- Is growth bottoming out? Not all indicators are pointing in the same direction. A 25 percent year-on-year expansion in China’s new lending in January and February, a rebound in European industrial output in January, and a rise in the JPMorgan global composite PMI are all positive. Plunging export orders for China, Japan and Germany, and just 20,000 jobs created in the U.S. in February are not. According to Bloomberg Economics, the global economy has slowed more than expected in the first quarter, but the balance of recent evidence is now pointing toward stabilization. The bottom for global growth this year is somewhere between now and soon.

- Numerous states will see an increase in online sales-tax revenue following the U.S. Supreme Court decision last year letting them collect taxes from online retailers without a physical presence in their jurisdiction, according to a report by Moody’s Investors Service. "Given the prominence of sales taxes in the state revenue mix and the growing size of the e-commerce sector, online sales tax revenue will be increasingly important to states over the coming years," analyst Joshua Grundleger said.

- Next week’s January release of consumer personal spending could provide a boost to economists’ outlook for the economy. Current forecasts reflect growth of 0.3 percent versus the previous print of -0.5 percent.

Threats

- The Bloomberg Dollar Spot Index slumped after the Federal Open Market Committee (FOMC) surprised traders with a more-dovish-than-anticipated outlook at its meeting Wednesday. The gauge, which fell from its Tuesday close, fell below an upward trend line from its April low, and is now eyeing its year-to-date low from January 31, reports Bloomberg.

- As reflected in a Business Roundtable survey, U.S. CEO optimism has cooled for a fourth straight quarter, primarily due to lingering uncertainty surrounding global economic growth. The lobbying group’s CEO Economic Outlook Index fell 9.2 points to 95.2 in the first quarter, the lowest since the third quarter of 2017 though still above the gauge’s historical average, according to the survey released Wednesday.

- FedEx has warned that “weaker global trade growth trends continue,” pinning its disappointing quarter on a slowdown in macroeconomic conditions, reports Business Insider.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, which gained 7.18 percent as firmer oil prices and low inventories in Indonesia make palm oil more attractive for blending into biofuel. Bloomberg data shows that investments in ETFs focusing on commodities almost doubled in the past week, while outflows from energy ETFs narrowed. Commodity ETF inflows totaled $211 million in the week ended March 21, compared with $117 million in the prior period.

- BP Plc might become the next oil major to power operations with clean energy, as the company is in talks with a solar developer that it already partially owns, Lightsource BP, to buy power in the U.S. Lightsource BP Chief Commercial Officer Katherine Ryzhaya said that a contract could be signed within six months. Blomberg reports that in 2017 BP said it would invest $200 million in Lightsource BP over the next three years for a 43 percent stake.

- KGHM Polska Miedz SA, a copper producer in Poland, saw its shares rise the most in more than two months this week after the government proposed to lower the copper tax paid by the company by 15 percent. The goal of the lower tax is to help KGHM invest more in Poland after foreign acquisitions haven’t yet yielded expected benefits, reports Bloomberg. The company is significant in Poland, with 33,000 employees and 20 billion zloty of revenue.

Weaknesses

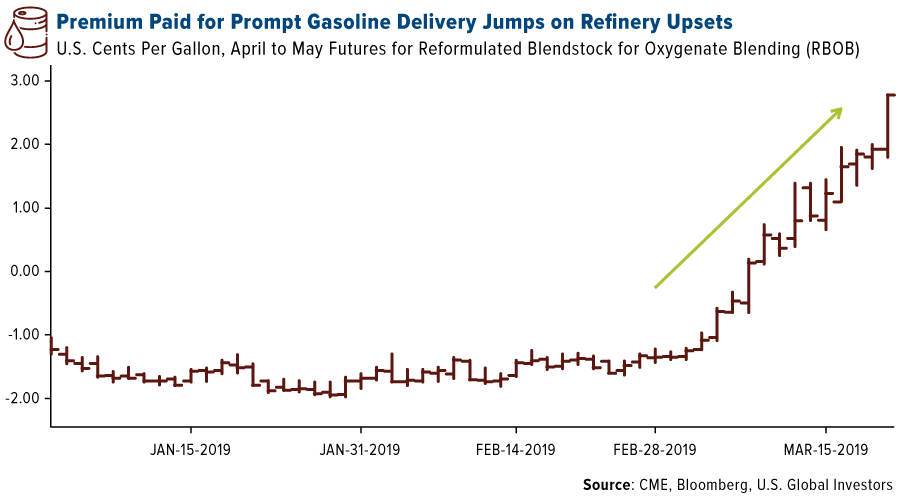

- The worst performing major commodity for the week was lumber, which fell 7.87 percent as Moody’s downgraded the outlook for global paper, packaging and forest products to negative. Gasoline futures in New York surged on Thursday as several refinery upsets tightened supply. April delivery futures rose to as much as 2.6 cents per gallon, the highest seasonal level in 12 years, according to Bloomberg. Consumers can expect to see higher prices at the pump. Oil fell below $60 a barrel, after climbing above $60 on Wednesday, as a stronger dollar capped a rally spurred by a bigger-than-expected drain from U.S. stockpiles, writes Bloomberg’s Ben Foldy. A fire broke out at the Intercontinental Terminals Co. tank farm in Texas, which holds as much as 13 million barrels of oil productions, and burned for four days until flames were extinguished. The fire sent a massive plume of black smoke in the air for several days and on Thursday the city of Deer Park urged its residents to stay indoors amid reports of carcinogen benzene in the air.

- Electric vehicles now account for over 50 percent of new vehicle sales in Norway, according to data from January and February, with nearly 250,000 purchased in the nation to date. China’s adoption of electric buses is eating away at oil demand. According to a report published by BloombergNEF, by the end of this year, a cumulative 270,000 barrels a day of diesel demand will have been displaced by electric busses, most of it in China. The report also highlighted that diesel displacement by electric vehicles will grow by 96,000 barrels a day this year. Although growing adoption of electric vehicles is positive for some, it is negative for oil prices.

- Severe storms and the threat of natural disaster have disrupted mining and other operations across the globe. The bomb cyclone in Colorado last week temporarily shut down the EPA’s plant treating contaminated wastewater from the Gold King Mine. Massive floods in the Midwest, which has severely impacted agriculture, livestock and more, could be just the beginning in a bad year for flooding. Tropical storm Veronica is expected to hit Western Australia hard this weekend with several commodity miners pausing operations and evacuating personnel.

Opportunities

- Vanadium is gaining traction with investors as Macquarie, a bank and top research firm, has initiated coverage of the metal. Vanadium is mainly used to strengthen steel, but also has applications in the battery and energy storage market. The metal had a massive rally last year due to growing use. The world’s largest exporter of iron ore, Australia, raised its price forecast for the metal to the mid-$60’s a ton, up from $52.60 in its December forecast, due to the threatening global deficit in the wake of Vale SA’s fatal dam disaster.

- Since the beginning of 2018, investors have preferred “boring” miners. Bloomberg writes that companies that have focused on capital returns and conservative strategies, such as Rio Tinto Group and BHP Group, have outperformed both the broader equity market and many of the underlying commodities that they produce. Christopher LaFemina, an analyst at Jeffries, said that “people want to own what are effectively bond proxies rather than cyclical companies” due to sluggish commodity prices on lackluster demand from China, the biggest metals consumer.

- In the renewable energy space this week, more oil majors are seeking to diversify by investing in the distributed energy sector. Bloomberg reports that Shell has committed up to $2 billion of annual investment through its New Energies division and has acquired electric vehicle charging provider Greenlots, battery manufacturer Sonnen and U.K. aggregators Limejump – all in the past two months. Tesla now has direct competition in the solar rooftop space. Standard Industries Inc., one of the largest roofing companies in the world, has begun offering its own version of a solar roof. The company said it expects to ship 2,000 orders this year. China News reports that clean energy will account for 80 percent of total installed capacity in China’s Greater Bay Area by 2035.

Threats

- One of the world’s largest aluminum producers suffered production outages after a cyberattack across its operations in Europe and the U.S., reports Bloomberg. Norsk Hydro ASA reported that its potlines, which process molten aluminum and need to be kept running constantly, had been switched to manual mode as a part of the attack. Colin Hamilton, managing director for commodities research at BMO, said that the company will “probably have to halt pretty much everything in the short term as they work on a back-up plan” and that “operationally, this is distinctly challenging.” This is just the latest attack in the commodities sector and highlights how crucial digital systems have become in the sector.

- The coal industry continues to take hits. UBS Group AG says that it will no longer provide project-level financing for new coal plants, strengthening its environmentally friendly policies. “The bank believes the transition to a low-carbon economy is vital,” said the bank in a statement on Thursday. In the annual Fossil Fuel Finance Report Card released this week by the Rainforest Action Network and other environmental groups, data shows that overall funding for fossil fuels has grown, but that coal funding declined 3.1 percent last year to $13.4 billion. Cloud Peak Energy, which made a bet 11 years ago that coal would remain indispensable to the U.S. power sector, announced last Friday that it might file for chapter 11 bankruptcy. Lastly, Vietnam has plans for $7.8 billion in gas-fired power projects that would see the nation become an LNG importer and cut its use of coal, reports Bloomberg.

- The threat remains of the U.S.-China trade war as negotiations are ongoing, reportedly rocky at times and taking longer than some thought. President Donald Trump said this week that the U.S. tariffs on $250 billion of Chinese exports are unlikely to go away anytime soon – even if a trade deal is reached. In-person negotiations between the two nations will resume next week in China.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 2.2 percent. The country’s government is working on a revised banking tax. Previously, the proposed tax stood at 1.2 percent of banks’ assets, while the revised tax could be as low as 0.2 to 0.4 percent, depending on banks’ market share.

- The Russian ruble was the best performing currency this week, gaining 22 basis points against the U.S. dollar. The United States, Canada and Europe imposed new sanctions on Russian individuals for the country’s aggressions toward Ukraine. Lack of new sanctions on specific companies and a stronger Brent crude oil price supported the ruble this week.

- Financials was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 3.4 percent. Tension leading up to the municipal election has put pressure on equities trading on the Istanbul exchange. Erste Bank downgraded Akbank and Garanti Banks to a “sell” rating. Both banks’ share price declined sharply on the negative review.

- The Turkish lira was the worst performing currency this week, losing 6.6 percent against the U.S. dollar. On Friday, a report came out showing that local individuals and businesses have been buying hard currency ahead of elections, while foreign investors were shorting the lira as well. Later that day, the central bank of Turkey unexpectedly tightened its monetary policy and suspended one-week repo auctions. Currently, the central bank has two other instruments reserved for emergency lending; overnight lending with a rate of 25.5, and the late liquidity window with a rate of 27 percent. The rate of the suspended repo auction was 24 percent.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- One expectation for the eurozone’s economic growth is looking less pessimistic. The ZEW Indicator of Economic Sentiment for the euro area climbed further than analysts had expected, to a level of -2.5 in March, from -16.6 a month earlier. The possible further delay in the Brexit process, and progress made in trade negotiations between China and the U.S. created some optimism around the eurozone’s future.

- European stock performance is near historical lows versus global shares, as measured by the MSCI Europe Index versus the MSCI World Index. Stocks in Europe have rebounded this year in line with their U.S. counterparts, but are still trading near 2013 lows with further potential to climb higher. This week’s Federal Reserve decision to leave rates unchanged, along with its dovish tone, is very positive for emerging market equities and currencies.

- European leaders gave Theresa May a two-week extension to work on a Brexit deal. If she cannot get her deal approved by parliament next week, she will have to decide by April 12 whether to accept a no deal for Brexit or ask for a longer extension. For now, it looks like the U.K. is saved from a hard Brexit until April 12. The Brexit date was previously set for March 29.

Threats

- Eurozone’s preliminary manufacturing PMI fell to 47.6 in March from 49.3 in February. Germany’s manufacturing PMI fell to 44.7, the lowest since 2012 and well below consensus for a 48 reading. France’s PMI dropped below the 50 level that separates growth from contraction.

- According to one Bloomberg article titled “European Banks to Underperform as Cracks Run Deep” by Heather Burke, European banks are poised to underperform this year. Earnings growth is expected to stall this year, as the euro area economy slows. A slow down in growth and low yields are a toxic combination for banks.

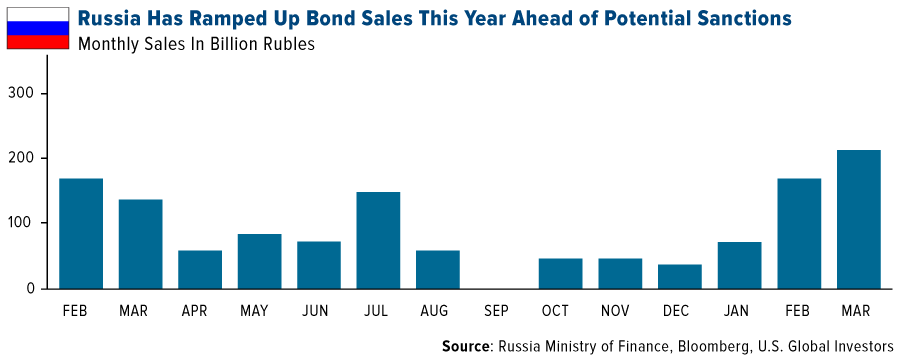

- Russia is preparing to offer 16-year bonds at $3 billion paying 5.1 percent and some euro-denominated bonds as well. The country has been increasing its sale of bonds, ahead of a possible U.S. decision to block Russia’s access to dollar financing. After a placement in dollars and euros, Russia may sell bonds on the Moscow exchange, denominated in Chinese yuan.

China Region

Strengths

- The top country index for the week was the Philippines Stock Exchange Index, which climbed 2.97 percent, narrowly nudging out China’s Shanghai Composite, which gained 2.73 percent.

- Consumer goods took the top performing sector award for the Hang Seng Composite Index, closing out the week 3.40 percent higher.

- Singapore’s non-oil domestic exports came in significantly better than expectations, a 16.0 percent year-over-year gain for the February measurement period, beating analysts’ anticipated 4.3 percent print and rising from the prior month’s decline of 5.7 percent.

Weaknesses

- Vietnam’s Ho Chi Minh Stock Index fell by 1.53 percent, while Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite Index fell 83 basis points.

- Utilities earned the worst performing sector award for the Hang Seng Composite Index for the week, falling by 2.35 percent.

- Taiwan’s year-over-year export orders declined by 10.9 percent, missing estimates for a 5.6 percent decline and slowing even from the prior month’s 6.0 percent decline.

Opportunities

- The U.S. Federal Reserve announced an expectation of no further rate hikes this year, with indications for only one in 2020 at this point, which leaves open the possibility of less pressure on emerging markets in the interim stretch. The offset to this possibility is, of course, a stronger dollar if we see global economic slowdown such that the growth rates weighed on EM anyway. But all else equal, a Fed on hold may well remove some of the concerns on a stronger dollar.

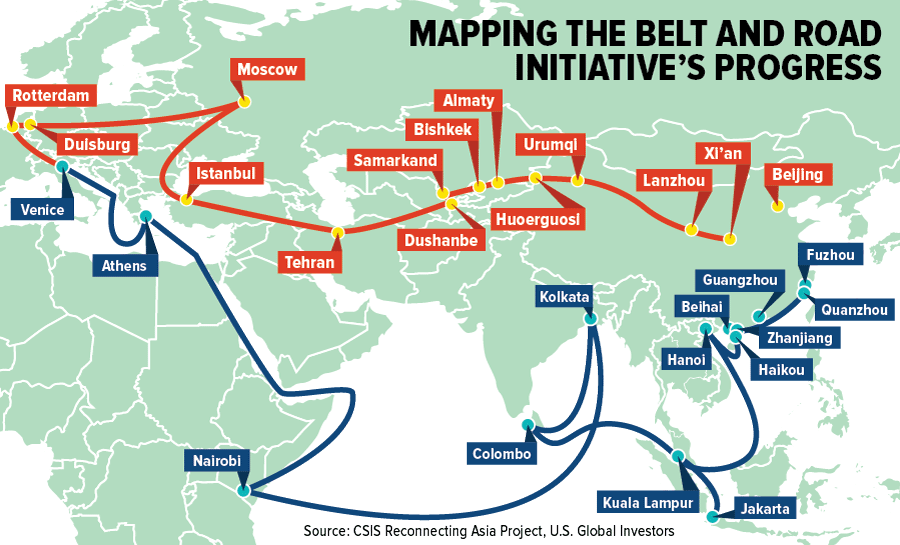

- Even as China has scaled back the pace and progress of some of its recent Belt and Road Initiative projects, the country has also recently called publicly for more assistance in its global projects, encouraging the United States and EU countries, among others, to partner with China in the ambitious BRI. China’s efforts this week focused in particular on Italy, which featured prominently at the western end of the ancient Silk Road and which, and with which, Chinese President Xi Jinping argued, China would like to increase trade and investment. Indeed, Italy and China are tentatively scheduled to sign a memorandum of understanding on the Belt and Road Initiative this weekend. Italy would be the first G7 country to endorse the Belt and Road Initiative, and mark something of a victory for China in making further inroads (beltroads?) on BRI.

- China’s Cnooc Ltd. reported its highest annual profit in four years thanks to robust crude prices while also raising reserves life, Bloomberg News reported this week. Among China’s big three oil companies,” the article continues, “Cnooc is the most sensitive to crude prices as its lack of refining capacity leaves almost all its earnings from exploration and production.” Cnooc also “booked new domestic and overseas reserves,” driving reserve life to 10.5 years from 10.3 years. Net income for 2018 rose to just under 53 billion yuan from just under 25 billion yuan the prior year.

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter remain a collective threat until resolution one way or the other. U.S. President Donald Trump reiterated more than once this week that the current tariffs on China will remain in place for the foreseeable future in order to ensure compliance (read: as leverage) in any “deal” involving agreements or promised progress from China’s end.

- Amid the ongoing U.S.-China trade talks, the United States has “given tacit approval to Taiwan’s request to buy more than 60 F-16 fighter jets,” Bloomberg reported this week, which prompted “a fresh protest from China amid its trade dispute with the U.S.”

- In another possible sign of the tension in talks between the U.S., South Korea, and North Korea, North Korea pulled its staff from a liaison office set up six months ago with South Korea at Gaeseong city.

Blockchain and Digital Currencies

Strengths

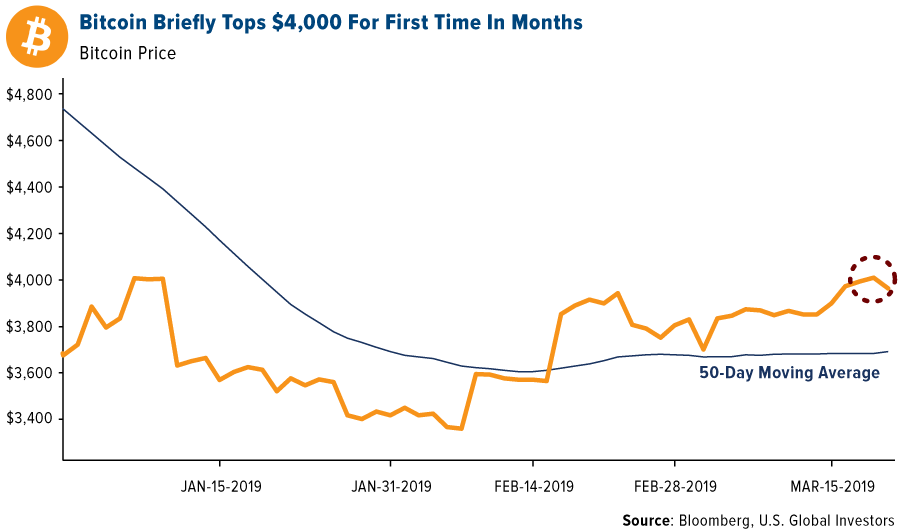

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 22 was doc.com Token, up 317.88 percent. Albeit only briefly, bitcoin broke above the $4,000 mark this week for the first time since early January. In spite of many cryptocurrencies still trading way off their all-time highs, this move could mean we are on the verge of a new wave up, reports Bloomberg.

- One of the world’s largest distributors of electronic components and services, Avnet, is now accepting cryptocurrency payments via BitPay, reports Coindesk. The Fortune 500 firm will now be the third largest technology company in the U.S. (following Microsoft and Dell) to accept bitcoin payments, an Avnet spokesperson said. According to the company, cryptocurrency payments can reduce the “time, cost and complexities of bringing products to market.”

- BlockFi’s interest-yielding deposit accounts, which launched in beta in January, are now fully live this month and have attracted more than $35 million in cryptocurrency, reports CoinDesk. The company is flexible in how it uses depositors’ funds and the interest rate it pays them. For example, institutional investors borrow crypto at individualized terms, at interest rates from 4 to12 percent, and BlockFi can call in the loans at any time.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 22 was Cosmos, down 51.41percent.

- Bitcoin is in the longest slump of its 10-year history, writes Wall St. Journal this week. Not only was the price of bitcoin down around 80 percent this week from its trading peak of $19,800 in December 2017, but the total market value of all cryptocurrencies outstanding is also down 85 percent from its peak in January 2018. Research firm TradeBlock adds that volumes on the largest U.S. exchanges have been falling steadily for the past 15 months as well.

- As interest in cryptocurrency trading has continued to dry up since the 2017 mania, Cboe Global Markets has decided to stop listing bitcoin futures, reports CNBC. While the exchange says it “does not currently intend” to list additional bitcoin futures for trading, it will not fully close the door on cryptos. Active bitcoin contracts are still available to trade, although the last of them expires in June, the article continues.

Opportunities

- The cryptocurrency-based cross-border payments race is heating up, writes MarketWatch. On Monday IBM Corp. announced that its Blockchain World Wire initiative has entered production and will support instantaneous foreign exchange payment and settlement in more than 70 countries, supporting close to 50 currencies.

- Data provider CoinMarketCap launched two cryptocurrency benchmark indices on Wednesday on financial data feeds from Nasdaq Global Index Data Service, Bloomberg Terminal, Thomson Reuters Eikon and Germany’s Borse Stuttgart, as well as on its own platform, reports Coindesk. According to the company, the benchmark indices will cover the top 200 cryptocurrencies by market capitalization, one including bitcoin and other without. “These indices will promote greater accessibility to cryptocurrency data in an easier-to-digest format,” CEO Brandon Chez explained.

- Former secretary-general of NATO and prime minister of Denmark, Anders Fogh Rasmussen, is joining blockchain identity startup Concordium as a strategic advisor, reports Coindesk. Concordium is building an identity (ID) and know-your-customer (KYC)-validating, regulatory compliant blockchain network, and chairman Lars Christensen says that Rasmussen will play a “pivotal” role in the firm’s global expansion plans, the article continues.

Threats

- For the first time in over seven months, bitcoin’s share of the total cryptocurrency market is on the verge of falling below 50 percent, writes Coindesk. Prior to 2017, the digital coin’s dominance rate was over 70 percent, the article continues, but it began to deflate as new cryptos were created and sold to investors in initial coin offerings. Data from CoinMarketCap shows that bitcoin accounted for 50.54 percent of the total capitalization of the entire market as of March 17.

- Officials in Dubai removed the United Arab Emirates’ very first bitcoin ATM from a hotel only two day after it was installed, according to travel blog Lovin Dubai. The machine was marketed as being anonymous, which ran up against the country’s anti-money laundering (AML) and know your customer (KYC) laws. Representatives of Amhora, the company responsible for the ATM, said it would work with officials to get the machine up and running again.

- On Thursday, Dallas News reported that Jared Rice Sr., founder of cryptocurrency bank AriseBank, has pleaded guilty to one count of securities fraud in federal court this week, writes CoinDesk. Rice was arrested last year and admitted to scamming investors out of $4.2 million by selling AriseCoin tokens and promising that customers would receive Visa credit cards and accounts insured by the Federal Deposit Insurance Corporation (FDIC), the article continues.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 199.05 | +5.63 | +2.91% |

| Gold Futures | 1,319.50 | +10.60 | +0.81% |

| Natural Gas Futures | 2.76 | -0.04 | -1.25% |

| S&P/TSX VENTURE COMP IDX | 637.82 | +10.05 | +1.60% |

| 10-Yr Treasury Bond | 2.44 | -0.15 | -5.91% |

| Nasdaq | 7,642.67 | -45.86 | -0.60% |

| Oil Futures | 58.82 | +0.30 | +0.51% |

| Hang Seng Composite Index | 3,897.39 | +14.86 | +0.38% |

| S&P 500 | 2,800.71 | -21.77 | -0.77% |

| DJIA | 25,502.32 | -346.55 | -1.34% |

| Korean KOSPI Index | 2,186.95 | +10.84 | +0.50% |

| Russell 2000 | 1,505.92 | -47.62 | -3.06% |

| S&P Energy | 484.86 | +0.02 | +0.00% |

| S&P Basic Materials | 340.33 | -7.02 | -2.02% |

| XAU | 77.38 | +1.33 | +1.75% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.76 | +0.12 | +4.70% |

| S&P/TSX Global Gold Index | 199.05 | +0.46 | +0.23% |

| 10-Yr Treasury Bond | 2.44 | -0.21 | -7.94% |

| Oil Futures | 58.82 | +1.90 | +3.34% |

| Gold Futures | 1,319.50 | -34.90 | -2.58% |

| S&P 500 | 2,800.71 | +16.01 | +0.57% |

| S&P Energy | 484.86 | -4.52 | -0.92% |

| Hang Seng Composite Index | 3,897.39 | +76.02 | +1.99% |

| DJIA | 25,502.32 | -452.12 | -1.74% |

| Korean KOSPI Index | 2,186.95 | -42.81 | -1.92% |

| Nasdaq | 7,642.67 | +153.60 | +2.05% |

| S&P Basic Materials | 340.33 | -8.85 | -2.53% |

| Russell 2000 | 1,505.92 | -75.74 | -4.79% |

| S&P/TSX VENTURE COMP IDX | 637.82 | +15.49 | +2.49% |

| XAU | 77.38 | -2.04 | -2.57% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.76 | -0.82 | -22.97% |

| 10-Yr Treasury Bond | 2.44 | -0.37 | -13.22% |

| DJIA | 25,502.32 | +2,642.72 | +11.56% |

| Oil Futures | 58.82 | +12.94 | +28.20% |

| S&P 500 | 2,800.71 | +333.29 | +13.51% |

| Gold Futures | 1,319.50 | +39.00 | +3.05% |

| S&P Energy | 484.86 | +65.41 | +15.59% |

| Nasdaq | 7,642.67 | +1,114.26 | +17.07% |

| Korean KOSPI Index | 2,186.95 | +126.83 | +6.16% |

| S&P Basic Materials | 340.33 | +32.74 | +10.64% |

| Russell 2000 | 1,505.92 | +179.92 | +13.57% |

| Hang Seng Composite Index | 3,897.39 | +470.85 | +13.74% |

| S&P/TSX Global Gold Index | 199.05 | +17.83 | +9.84% |

| S&P/TSX VENTURE COMP IDX | 637.82 | +100.81 | +18.77% |

| XAU | 77.38 | +7.59 | +10.88% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Akbank T.A.S.

Turkiye Garanti Bankasi AS

BP PLC

BHP Group Ltd

Royal Dutch Shell PLC

BHP Group Ltd

Luminex Resources Corp

Lundin Gold Inc

St. Barbara Ltd

Franco-Nevada Corp

Roxgold Inc

Golden Star Resources Ltd

Citigroup Inc

Wheaton Precious Metals Corp

Anglo American Plc

CNOOC Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Dollar Spot Index (BBDXY) tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar.

The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy.

The Bloomberg Consumer Comfort Index is a weekly, random-sample survey tracking Americans’ views on the condition of the U.S. economy, their personal finances and the buying climate.

The Business Roundtable CEO Economic Outlook Index is based on a survey — conducted quarterly since the fourth quarter of 2002 — of our member CEOs’ plans for hiring and capital spending, and their expectations for sales, over the next six months.

The MSCI Europe Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe. As of September 2002, the MSCI Europe Index consisted of the following 16 developed market country indices: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom.

MSCI World Index is a capitalization weighted index that monitors the performance of stocks from around the world.

The ZEW Economic Sentiment is a monthly economic survey. It’s an aggregation of the sentiments of approximately 300 economists and analysts, used as an indicator of the economic future of Germany for the next six months.

The S&P 500 Low Volatility Index measures performance of the 100 least volatile stocks in the S&P 500. The index benchmarks low volatility or low variance strategies for the U.S. stock market.

The Philippine Stock Exchange PSEi Index is composed of stocks representative of the industrial, properties, services, holding firms, financial and mining & oil sectors of the Philippines Stock Exchange.

The FTSE Bursa Malaysia Index Series is a broad range of real-time indices, which cover all eligible companies listed on the Bursa Malaysia Main and ACE Markets. The indices are designed to measure the performance of the major capital segments of the Malaysian market, dividing it into large, mid, small cap, fledgling and Shariah-compliant series, giving market participants a wide selection and the flexibility to measure, invest and create products in these distinct segments.