AI Will Add $15 Trillion to the World Economy by 2030

Date Posted: February 22, 2019

Read time: 55 min

It’s important for readers to realize that AI is no longer the stuff of science fiction. The technology is already disrupting multiple industries, many of which impact you on a daily basis. Own an iPhone X?

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Photo: bagogames/flickr | Creative Commons Attribution 2.0 Generic (CC by 2.0)

A couple of weeks ago, I introduced you to an exciting new company called GoldSpot Discoveries, conceived and headed by mining visionary Denis Laviolette. GoldSpot is the world’s first exploration company to use artificial intelligence (AI) and machine learning in the discovery process for precious metals and other natural resources. Not yet three years old, it’s already had a number of successes locating optimal target zones.

I’m pleased to inform you now that GoldSpot began trading this week on the TSX Venture Exchange under the ticker SPOT. This is a giant leap forward not just for the company and its team but also AI in general.

It’s important for readers to realize that AI is no longer the stuff of science fiction. The technology is already disrupting multiple industries, many of which impact you on a daily basis. Own an iPhone X? Its facial recognition system is powered by AI. Ever been redirected by Google Maps because of an accident or construction ahead? You guessed it: AI.

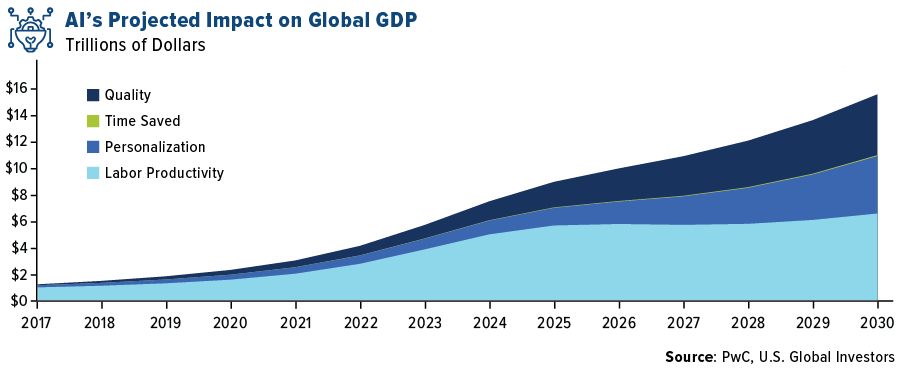

And those are just a couple of small examples. By one estimate, AI contributed a whopping $2 trillion to global GDP last year. By 2030, it could be as much as $15.7 trillion, “making it the biggest commercial opportunity in today’s fast changing economy,” according to a recent report by PwC.

AI: The “New Electricity”

Not every industry and sector will be affected equally, but none will go untouched.

“AI is the new electricity,” says Chinese-English computer scientist and entrepreneur Andrew Ng. “I can hardly imagine an industry which is not going to be transformed by AI.”

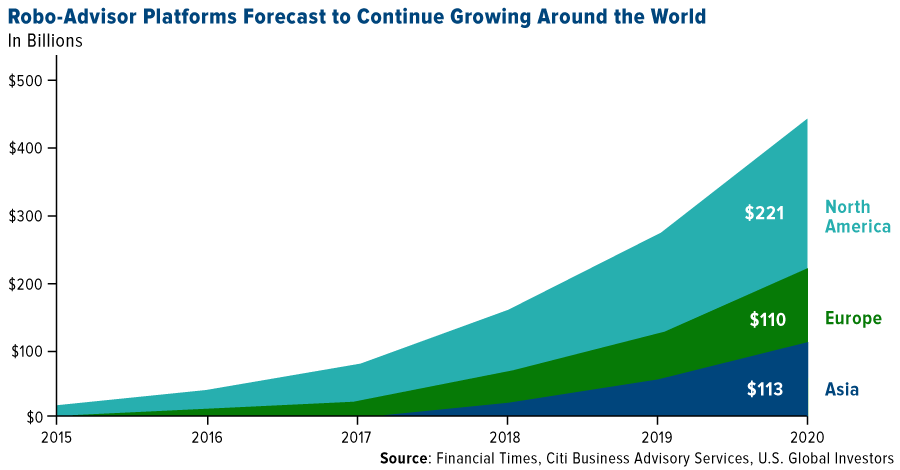

Among the industries that have been fastest to adopt AI, according to PwC, are health care, automotive and financial services. Earlier and more accurate diagnostics, powered by AI, means earlier treatment of life-threatening diseases. Once on the market, self-driving cars will free up an estimated 300 hours the typical American spends driving every year. And more and more people are putting their trust in robo-advisors to manage their wealth.

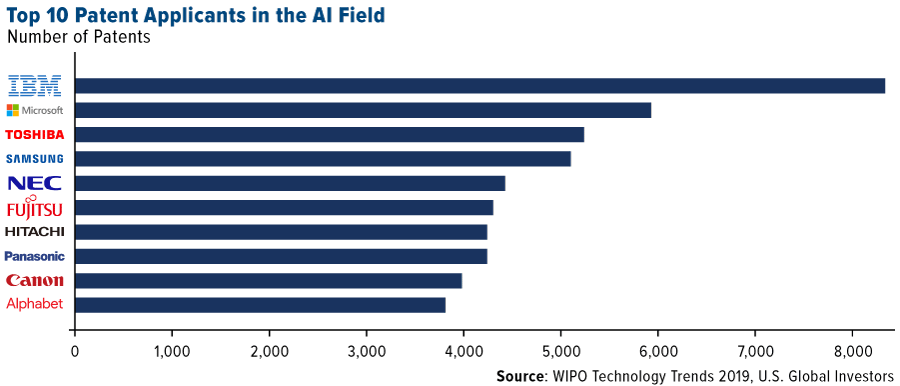

AI patents have surged in the past five years alone, according to the World Intellectual Property Organization (WIPO). From 2013 to the end of 2017, the number of patents grew nearly three times, from 19,000 to more than 55,600.

The massive increase in patenting “means we can expect a very significant number of new AI-based products, applications and techniques that will alter our daily lives—and also shape future human interaction with the machines we created,” comments WIPO Director-General Francis Gurry.

A majority of the top 500 applicants are from China, the U.S. and South Korea. Only four are from Europe. At the top of the list sits IBM, with an incredible 8,290 inventions (so far), followed by Microsoft, which has 5,930 patents to its name.

As you might imagine, the U.S. government wants to ensure that the country remain competitive against Asia. This very month, President Donald Trump signed an executive order urging federal agencies to prioritize AI investments in research and development. The American AI Initiative, as it’s called, says that these measures are “critical to creating the industries of the future, like autonomous cars, industrial robots, algorithms for disease diagnosis and more.”

“I want 5G, and even 6G, technology in the United States as soon as possible,” Trump tweeted this week, presumably in response to news that Chinese telecommunications firm ZTE could be first to bring fifth-generation cellular technology to market. “American companies must step up their efforts or get left behind. There is no reason that we should be lagging behind on… something that is so obviously the future.”

Bringing AI to the Miners

Interestingly enough, the industry that’s been slowest to adopt AI is manufacturing, including industrial products and raw materials, according to PwC.

The metals and mining industry has been especially resistant to adoption, with spending on innovation far below that of other industries.

To be fair, not every miner has been behind the curve. For more than 10 years now, Rio Tinto has been using AI-powered autonomous trucks to haul materials, reducing fuel consumption and increasing safety in the process. The London-based producer also uses autonomous loaders and drills, and its highly anticipated “intelligent mine” in Western Australia is slated to begin operations in 2021.

But much more could be done, Denis says, especially when it comes to utilizing the mountains of data already at our fingertips. Miners were “paying for all this data, but no one was really doing anything with it,” he told me earlier this month.

Speaking to the Wall Street Journal in December, Denis commented that he had seen “an awful lot of posturing” when it came to miners claiming to be interested in modernizing operations and integrating AI. “They say they are working on this internally, then you find out they haven’t got anywhere.”

This is precisely why he conceived of GoldSpot Discoveries. I’m fully convinced that mining’s future belongs to AI, with Denis and GoldSpot leading the way. I invite you to learn more by visiting the company’s website by clicking here!

Gold Market

This week spot gold closed at $1328.25, up $6.70 per ounce, or 0.51 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.39 percent. The S&P/TSX Venture Index came in up just 1.19 percent. The U.S. Trade-Weighted Dollar fell 0.38 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-19 | Germany ZEW Survey Current Situation | 20.0 | 15.0 | 27.6 |

| Feb-19 | Germany ZEW Survey Expectations | -13.6 | -13.4 | -15.0 |

| Feb-21 | Germany CPI YoY | 1.4% | 1.4% | 1.4% |

| Feb-21 | Initial Jobless Claims | 228k | 213k | 239k |

| Feb-21 | Durable Goods Orders | 1.7% | 1.2% | 1.0% |

| Feb-22 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.1% |

| Feb-26 | Hong Kong Exports YoY | -2.8% | — | -5.8% |

| Feb-26 | Housing Starts | 1250k | — | 1256k |

| Feb-26 | Conf. Board Consumer Confidence | 124.1 | — | 120.2 |

| Feb-27 | Durable Goods Orders | — | — | 1.2% |

| Feb-28 | Germany CPI YoY | 1.5% | — | 1.4% |

| Feb-28 | Initial Jobless Claims | 225k | — | 216k |

| Feb-28 | GDP Annualized QoQ | 2.5% | — | 3.4% |

| Feb-28 | Caixin China PMI Mfg | 48.7 | — | 48.3 |

| Mar-1 | Eurozone CPI Core YoY | 1.1% | — | 1.1% |

| Mar-1 | ISM Manufacturing | 56.0 | — | 56.6 |

Strengths

- The best performing metal this week was palladium, up 4.74 percent with platinum on its heels up 4.32 percent with the South African mining industry warning of a week-long strike threat. Gold makes a second consecutive weekly gain. Futures of the yellow metal rose as much as 1.6 percent on Tuesday to the highest for a most-active contract since April, writes Bloomberg. Earlier in the week, gold posted its biggest decline in three months after Fed minutes were released, then recovered on news of positive trade talks between the U.S. and China. Gold traders were neutral on the precious metal in this week’s survey by Bloomberg.

- Swiss gold exports rose 29 percent in January to 65.2 tons, up from 50.6 tons in December. Russia increased its official gold holdings to 68.1 million troy ounces, valued at $89.5 billion at the end of January, versus $86.9 billion at the end of December. Kazakhstan also boosted its gold holdings last month to 11.36 million ounces, up from 11.27 million in December. Turkey, however, saw its holdings decline. Its central bank gold reserves slipped slightly by $20 million from the previous week.

- Peru shut down the country’s largest illegal mining zone after years of unregulated mining destroying the surrounding environment. Bloomberg reports that the government sent 1,500 employees to shut down the La Pampa operation in southeast Peru. Illegal mining has long been an issue in the nation, accounting for 7.1 percent of gold output.

Weaknesses

- The worst performing metal this week was gold, which was still up 0.51 percent. After the Fed released minutes of its January meeting, gold fell from a 10-month high on Wednesday. The minutes called into question expectations that the central bank will hold off on rate hikes, which is historically positive for the yellow metal. Fortunately, gold recouped that loss later in the week. Scotiabank analyst Trevor Turnbull wrote that New Gold has “no good options” in the near-term until its Rainy River mine shows some strength. Turnbull said that a potential sale of its operating assets or equity raise wouldn’t be an option for the company at this time. New Gold has seen recent turbulence with the stock falling 26 percent on February 14 after reporting fourth quarter results and its 2019 outlook.

- AngloGold Ashanti Ltd. will be making a decision on its Mponeng mine, the world’s deepest, on whether or not to spend significant capital to extend its life beyond eight years. The number three gold miner rose as much as 10 percent in New York on the news of potentially shutting a higher cost mine. If investors checked AngloGold’s website to value the underlying assets which support the company’s share price, they would be sorely disappointed by lack of disclosure the company provides about its assets. There is no Resource/Reserve Statement prominently displayed and when an investor examines the individual summary of each mine, AngloGold just mentions the number of ounces it thinks there is remaining at the mine. There is no detail on ore tonnage and grades which factor into the risks associated with a mine.

- Just months after the mega merger of Barrick and Randgold was confirmed, Barrick is said to be looking again at a possibility of taking over Newmont, which just announced its own huge deal with Goldcorp. According to sources familiar with the matter, Barrick has looked on and off at the feasibility of an offer for Newmont for some time, including in recent months, writes Bloomberg. Could the gold industry need to “cool off” for some time after two giant mergers? Or is Barrick simply expressing jealousy of Newmont’s deal which places it as the largest gold miner, leapfrogging Barrick? Mergers aren’t easy and perhaps Barrick should think twice about a ménage à trois relationship with Newmont.

Opportunities

- Gold might be getting more recognition from mainstream investors. Bernstein Quants have joined the mix of gold bulls, as miners have gained almost twice the pace of bullion so far this year. Bloomberg writes that Bernstein strategists led by Inigo Fraser Jenkins are seeing a laundry list of reasons to like gold and gold miners just now. Gold’s mysterious rally could be due to liquidity, writes Bloomberg’s Kyoungwha Kim. “Expectations of improving liquidity may be fueling gold’s rally once again.” Mark Cudmore noted that ballooning balance sheets at major central banks could have already foretold what is going to happen to bullion next.

- The price of palladium hit a record high on Wednesday after surging 1.7 percent to $1,505.46 an ounce – breaking above the key $1,500 level. Rules requiring stricter car emissions have tightened global demand for the metal as palladium is a key component for car manufacturers in the new technology. According to Johnson Matthey Plc, a key maker of auto catalysts, the global palladium deficient is set to “widen dramatically” this year. The world’s only “pure-play” for palladium, North American Palladium Ltd., has been the biggest beneficiary, crossing above the C$1 billion mark for the first time in eight years this week.

- Bloomberg’s Eddie van der Walt writes that the gold rally could have further to go if hedge fund managers ramp up their bullish bets after last year’s big short. The chart below shows that money managers remain only modestly allocated to the metal, according to futures positions. “Reluctance lingers, and the risk is that with many market participants waiting to buy dips, there could be a lot of catching up to do if positive catalysts extend,” writes Joni Teves, strategist at UBS Group.

Threats

- In a note to investors this week, Morgan Stanley’s Macro Strategy Group lifted its September recommendation to be long gold, despite expectations of a weaker U.S. dollar and lower real interest rates in 2019. The research group bases its decision on two factors. One, because the price of gold has risen “materially” in recent months, it’s left little upside to Morgan Stanley’s earlier forecast of $1,350 an ounce by year’s end. And two, the target of $1,350 is “a price level gold has struggled to break on a sustained basis for the better part of five years.” If the precious metal manages to break above the target price, the analysts write, “We may need to revisit our view.”

- An old deal made with Nicolas Maduro’s regime in Venezuela is causing headaches for Citigroup. According to Bloomberg, the investment bank struck a $1.1 billion swaps contract backed by gold before additional U.S. sanctions were imposed on Maduro’s government, and now Citigroup bankers are holding high-level talks with the U.S. Treasury to determine if the contract can still move forward without violating sanctions. “The sale of gold is another revenue source that the Maduro regime is using, and I know for a fact that Citibank has had multiple meetings with Treasury [officials] seeking guidance, trying to figure out how to avoid exposure,” Florida senator Marco Rubio is quoted as saying.

- A gold correction could be in the cards, writes Bloomberg’s Benjamin Dow. The price of gold made some positive gains this month, even nearing its 2018 highs. However, the 10-year breakeven rate, which measures the difference between the 10-year Treasury bond and Treasury Inflation Protected Securities (TIPS), is down around the same level as in November 2016. “This disconnect,” according to Dow, “suggests the gold price may not be telling the truth.”

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.57 percent. The S&P 500 Stock Index rose 0.62 percent, while the Nasdaq Composite climbed 0.74 percent. The Russell 2000 small capitalization index gained 1.33 percent this week.

- The Hang Seng Composite gained 3.67 percent this week; while Taiwan was up 2.56 percent and the KOSPI rose 1.57 percent.

- The 10-year Treasury bond yield fell 1 basis point to 2.653 percent.

Domestic Equity Market

Strengths

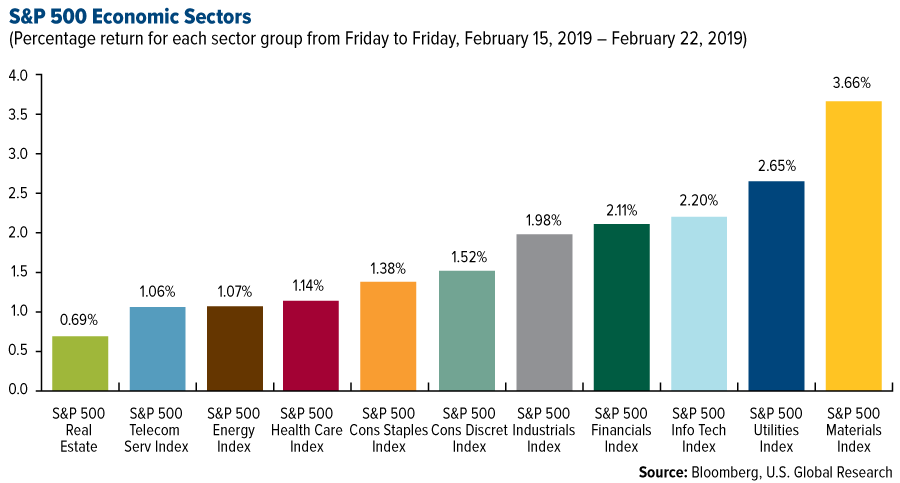

- Materials was the best performing sector of the week, increasing by 3.66 percent versus an overall increase of 1.56 percent for the S&P 500.

- Garmin was the best performing stock for the week, increasing 16.36 percent.

- Garmin soared to an 11-year high. The maker of fitness and navigation devices rose 17 percent Wednesday, to its best level since January 2008, after delivering strong fourth quarter results and forecasting full-year revenue and profits above Wall Street estimates.

Weaknesses

- Real estate was the worst performing sector for the week, but still up slightly 0.69 percent versus an overall increase of 1.56 percent for the S&P 500.

- Kraft Heinz was the worst performing stock for the week, falling 26.17 percent.

- Kraft Heinz fell as much as 28 percent this week after the company announced a $12.6 billion loss for the fourth quarter (compared to an $8 billion profit a year earlier) as it experienced higher operating costs and wrote down the value of the Kraft and Oscar Mayer names by $15.4 billion. The company also announced that the Securities and Exchange Commission (SEC) is investigating the company’s "accounting policies, procedures, and internal controls" related to vendor agreements.

Opportunities

- Pinterest has reportedly filed for an initial public offering (IPO) that could value the company at $12 billion. The social media company has filed a confidential S-1 and has its eye on a June IPO, according to the Wall Street Journal.

- Goldman Sachs and Apple are partnering to launch a new iPhone-linked credit card, the Wall Street Journal reported on Thursday. The card will reportedly give customers additional features in Apple’s wallet app and allow them to "set spending goals, track their rewards, and manage their balances."

- After beating Wall Street’s estimates, Roku is in "a strong position" to take on Amazon and other rivals, says its Chief Financial Officer. Roku, which has transformed itself into an ad-based business, is in a prime position to compete in the free streaming video market, says its CFO Steve Louden.

Threats

- Senator Mark Warner blasted Google for its hidden Nest microphone. He told Business Insider in a statement that federal agencies and Congress "must have hearings to shine a light on the dark underbelly of the digital economy." Furthermore, a major privacy advocacy group is calling on the FTC to force Google to divest the Nest business after it failed to let consumers know about a hidden microphone. The longtime privacy advocacy group, the Electronic Privacy Information Center (EPIC) is calling on the Federal Trade Commission (FTC) to take action.

- The sale of one of Walmart’s biggest assets is under threat. Walmart’s sale of Asda to the grocer Sainsbury’s is on the rocks after the UK Competition and Markets Authority warned the deal could increase prices and decrease quality.

- A corner of the market that was red hot during the latest recession might not work in the next recession. The catering industry was a beacon of strength during the Great Recession, but investors will have to look elsewhere during the next downturn, according to Bernstein.

The Economy and Bond Market

Strengths

- The IHS Markit U.S. Services purchasing managers’ index (PMI) saw an improvement, rising to an eight-month high of 56.2 for the February flash reading. This is the sharpest upturn in activity since June 2018.

- Overall orders for durable goods increased 1.2 percent in December. That reflected a 3.3 percent rise in demand for transportation equipment.

- In a signal of labor market tightness, the number of Americans filing applications for new unemployment benefits fell last week, reports Morningstar. Initial jobless claims decreased by 23,000 to a seasonally adjusted 216,000 in the week ended Feb. 16, the Labor Department announced. Economists surveyed by The Wall Street Journal expected 227,000 new claims last week.

Weaknesses

- Existing home sales fell for the third month in a row, according to the latest report from the National Association of Realtors. Total existing home sales fell 1.2 percent from December to a seasonally adjusted rate of 4.94 million in January. Sales are now 8.5 percent below the rate in January 2018.

- The recently ended government shutdown has thrown a wrench in the latest reading of the leading economic index run by the Conference Board. The reading fell 0.1 percent in January, reports MarketWatch. “Three of the 10 components – building permits and new orders for consumer and capital goods – were missing due to the 35-day partial federal shutdown,” the article reads.

- Adjusted for seasonal influences, the IHS Markit Flash U.S. PMI fell to 53.7 in February from 54.9 in January. This signals the slowest improvement in business conditions since September 2017, according to IHS Markit.

Opportunities

- On Tuesday the Conference Board will release its barometer of consumer confidence. The index is forecast to increase in February from 120.2 to 125.0. If confirmed, it would end a steep three-month decline.

- The deadline that would end a 90-day U.S.-China trade truce is scheduled for next week, March 1, and hopes are high that some kind of trade deal is reached by then, writes Reuters. If not, markets hope the deadline will be postponed.

- Fed Chair Jerome Powell will testify in the House of Representatives and Senate on February 26 and 27, reports Reuters. He is expected to give his take on the economic outlook and monetary policy at this time.

Threats

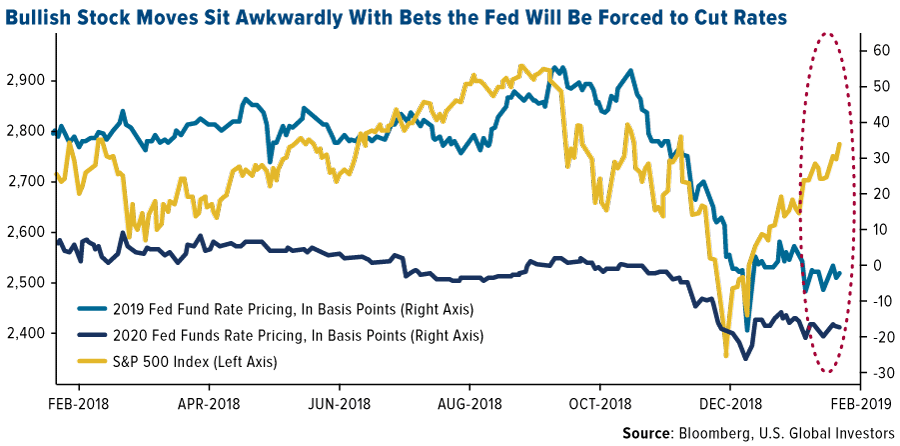

- In an article this week, Bloomberg highlights the ever-changing clash between stocks and bonds. Treasury yields are showing signs that an economic slowdown is in the works, while equity bulls are cheering the business cycle. “The S&P 500 is on track for the best two-month run since 2010, fueled by the most economically sensitive sectors, even as 10-year U.S. Treasury yields hover close to the lows plumbed during the recent global market meltdown,” the article reads. The futures market is pricing in interest rate cuts and growth angst is feeding haven demand for longer-dated debt. “It’s all adding to fears that the fast re-rating of stocks after the overwrought correction in 2018 has gone too far,” Bloomberg explains.

- On Thursday U.S. GDP numbers will be released. Growth is expected to slow from an annualized rate of 3.4 percent in the third quarter to 2.4 percent in the December quarter.

- Building permits and housing starts will be released on Tuesday, together with the S&P CoreLogic Case-Shiller 20-City Home Price Index. The unimpressive data released this week on existing home sales does not foreshadow better results.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was copper, which gained 5.32 percent. Bloomberg reports that oil has extended its gains from a three-year high on signs that the U.S. and China are close to an end to the trade war. Crude oil has gained around 25 percent so far this year due to OPEC supply output cuts. American shale operators forecast double-digit output growth, even as companies are cutting budgets, but that has been offset by production cuts from OPEC, as growing oil supply can lead to lower prices. Noble Energy saw its shares rise as much as 4.2 percent after it lowered its budget for the year. The Kremlin reported this week that Russian President Vladimir Putin and Saudi Arabia’s Salman Bin Abdulaziz had a phone conversation in which both leaders confirmed their readiness to extend cooperation in the oil market.

- Many of the largest miners routinely buy back their own shares, however Anglo American Plc does not and could be changing that position. Anglo has focused in recent years on improving its balance sheet and investing in growth, writes Bloomberg. The company reported adjusted profit of $3.24 billion this week, which beat the average analyst estimate of $3.06. CEO Mark Cutifani said in an interview with Bloomberg TV that it is a “very active conversation and all options are open” in regards to the possibility of share buyback.

- Demand for lithium has increased 21 percent annually and Albermarle says the market for the metal will be tight over the long term. The world’s top lithium producer estimates demand to be at 475,000 tons by 2021. Citigroup Inc. said in a note this week that China is likely to allocate around $444 of fixed subsidies for solar in 2019, leading to solar panel manufacturers rising on Tuesday. The bank estimates that capacity for solar could rise by 42 gigawatts in 2019.

Weaknesses

- The worst performing major commodity for the week was Powder River Basin, which fell 9.16 percent on fears Europe will turn its back on coal and favor clear LNG imports. Canadian pipeline-operator Enbridge Inc. reported that rationing on its heavy oil lines would increase in March, sending heavy Canadian crude prices to their biggest discount against New York futures this year, reports Bloomberg. The company said that crude shipments through its Mainline pipelines, Canada’s largest export pipeline system, would be apportioned 41 percent next month, up from 39 percent this month.

- BHP Group said in its commodity outlook this week that even though there is strong demand for LNG, the global LNG market is likely fully supplied until mid-2020s. The company did say that there is potential for the market to tighten sooner, with new projects necessary after the mid-2020s. BHP estimates that global nameplate capacity increased by 4.2 bcf/d in 2018. LNG in North Asia, the world’s biggest market for the fuel, fell to the lowest in 17 months as peak demand season saw warmer than usual temperatures, reports Bloomberg.

- An Andarko Petroleum Corp. convoy in northern Mozambique was attacked on Thursday and was one of at least six raids that occurred in the area. At least three contractors were killed and four people were injured in the attacks on convoys traveling to gas projects. Bloomberg writes that this is the first significant coordinated attack and the first time an oil and gas company has been targeted. A truck carrying sulphuric acid to a copper and cobalt mine owned by Glencore Plc in the Democratic Republic of Congo crashed and spilled its contents onto two vehicles killing at least 18 people.

Opportunities

- Pinnacle West Capital Corp., based in Arizona, plans to add 850 megawatts of battery storage and at least 100 megawatts of new solar power by 2025, reports Bloomberg. The company currently has less than 10 megawatts of battery storage in its system. Yayoi Sekine, an analyst at BloombergNEF, says that the plans to add that much additional storage are the “biggest planned deployment by a single utility.” One of the world’s biggest sellers of coal, Glencore Plc, has given in to global emissions-reduction plans and announced this week that it is promising to cap production around current levels of 145 million metric tons a year. Other companies have made commitments to cleaner energy in recent years. Bloomberg writes that BHP Group appears to be committed to its huge steelmaking coal mines and is less attached to the mines producing thermal coal in power generation.

- Oil and gas companies operating in Norway expect to increase investments by 14 percent this year after oil prices recovered, writes Bloomberg. The companies plan to invest $20 billion this year, which is slightly lower than estimates from November. This is a positive turnaround after Norwegian oil investments tanked when crude prices collapsed in 2014. Technological innovations could lead to Chinese smelters boosting their zinc production, with the nation’s output set to climb 6 million tons in 2019, the highest since 2017, says Goldman Sachs. In 2018, there was a supply shortage of the metal, with production at 13.3 million tons and consumption of 13.7 million tons. Bloomberg writes that a higher supply can push up the fees charged by smelters to turn ore into metal.

- Copper rose for a sixth straight day on Wednesday to break above its 200-day moving average for the first time since June. The red metal had been stuck in a trading range for months, but is now breaking out due to renewed concerns of a supply shortage, writes Bloomberg. ANZ Banking Corp. analysts wrote in a report this week that copper could hit $7,000 per ton in the second half of this year on rising demand from China. In the fourth quarter of last year electric vehicles were over 7 percent of car sales in China. Growing prospects of a trade deal between the U.S. and China have also helped lift copper prospects.

Threats

- Reuters reported on Thursday that customs officials in China’s northern port of Dalian have banned the import of Australian coal. The basic resources index fell 0.6 percent and many of Asia’s emerging currencies and the Australian dollar fell on the news. The ban could be in response to Australia banning Chinese telecommunications giant Huawei Technologies and its 5G network on security concerns. The Dalian port previously only took about 2 percent of Australia’s coal exports. China’s foreign ministry said that the report that it has banned imports is false.

- The government of Mexico announced that it has approved the use of hydraulic fracturing for the nation’s oil company, Petroleos Mexicanos, to tap into local natural gas reserves, reports Bloomberg Law. Although a common practice in Texas to extract oil from the ground, Mexico has less experience with fracking due to a lack of infrastructure to supply water to wells. Access to water rights will be the main challenge, as Mexican law gives agriculture a higher priority to water access than industrial users. The world’s largest copper producer, Chile, is squeezing water rights for miners after decades of depletion of fresh-water reserves. The nation’s water authorities will double the number of prohibition areas to at least 70 from 30.

- The major dam collapse in Brazil last month has sparked renewed discussions on global dam safety. Bloomberg writes that there have been at least 50 dam failures globally in the last decade, with 10 of those considered major. This week BHP Group CEO Andrew Mackenzie said there is a need for a “nuclear level of safety” at dams and that his company would welcome an international and independent body to oversee damn integrity. The mining industry is largely self-policed and laws can vary from country to country. Although increased safety regulations are positive, it could lead to potential price increases for maintenance and construction of dams at mining projects moving forward.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 3.3 percent. Shares of the National Bank of Greece and Piraeus Bank both appreciated by 20 percent. The Greek government came to an agreement with the four systemic banks on the new personal bankruptcy law. The agreement should be positive for the banking sector as it will help to reduce the number of defaulters in the system.

- The Russian ruble was the best performing currency this week, gaining 1.55 percent against the U.S. dollar. The ruble has historically been highly correlated with the price of oil, which gained 1.1 percent over the past five days, as OPEC looks to curb production further.

- Materials was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 6 basis points. Risk of further sanctions has negatively affected equites trading on the Moscow exchange. The country’s economic development ministry reported Tuesday that Russia has lost $6.3 billion due to sanctions imposed since annexation of Crimea, and that further sanctions would hammer its ailing economy.

- The Turkish lira was the worst performing currency this week, losing 27 basis points against the U.S. dollar. Geopolitical tension between Turkey and the U.S. may increase, as the county confirmed buying S-400 missiles from Russia as early as July and refused to buy Patriot missile defense systems from the U.S.

- Communication services was the worst performing sector among eastern European markets this week.

Opportunities

- Vladimir Putin, is his annual state of the union speech, announced additional social spending that could cost as much at $3 billion a year. Putin wants to raise child support payments and subsidies on housing, as well as introduce new tax breaks for families with more than two children. Russia had a budget surplus of $41 billion last year. Now the country may finally be ready to spend some of the saved money to stimulate economic growth and tackle the problem of 19 million people living under the poverty line.

- If China and the U.S. come to a trade agreement, European equites should benefit. Europe is already feeling the pain from higher tariffs. Preliminary eurozone Manufacturing PMI fell below the 50 level in February, with Germany’s PMI at its lowest level since 2012. The automobile industry in Europe has been negatively impacted by the trade war and prospects of no new taxes and/or tax cuts will hopefully push the PMI back above the 50 level that separates growth from contraction.

- President of Romania, Klaus Iohannis, is a critic of the ruling coalition and announced that he would challenge the government’s budget plan for 2019 in a top court. On Friday, Klaus said that this year’s budget jeopardizes the economy, which is already under pressure due to proposed taxes on banks and energy companies.

Threats

- The Organization for Economic Cooperation and Development (OECD) reported that wealth divisions between Europe’s lower- and middle-income families and upper-income households are at a record high. According to a New York Times article dated February 14, “Europe’s Middle Class Is Shrinking. Spain Bears Much of the Pain.” There are plenty of jobs but many are temporary and/or part-time, not providing long-term, stable sources of income.

- Last week, Michael Calvey, a U.S. citizen and founder of Baring Vostk Capital Partners, was arrested in Russia on fraud charges. He founded Baring Vostok in 1994, investing nearly $3 billion in local companies. His arrest may temper foreign direct investment in Russia.

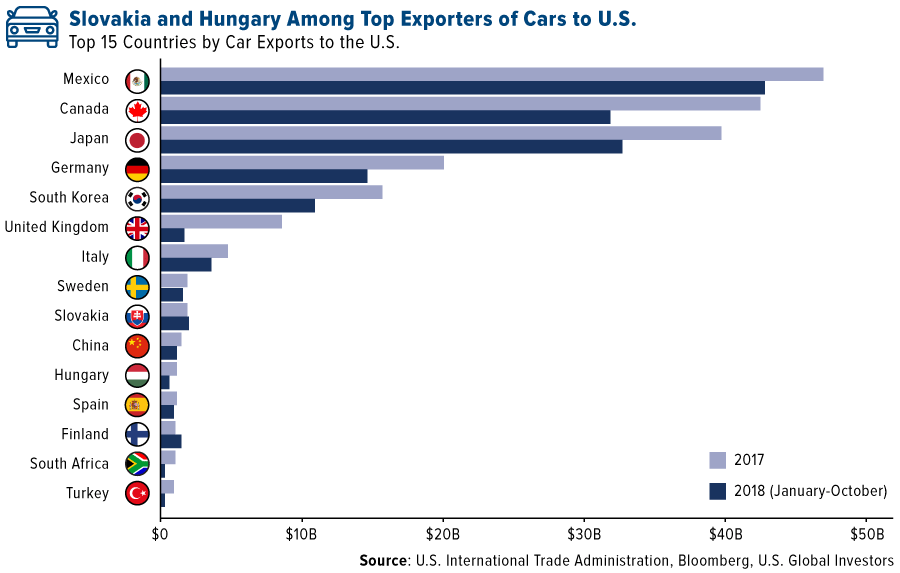

- Jean-Claude Juncker, president of the European Union (EU), says that if President Trump were to impose car tariffs, the EU would retaliate and not feel obliged to abide by its promise to buy more soybeans and LNG from the U.S. The EU has prepared €20B in retaliatory tariffs ($23B) on U.S. goods should the White House impose duties on automobile imports. Slovakia and Hungary are among the exports, selling more than $1 billion of cars each year, so the car tariffs will hit not only Western Europe, but Eastern Europe too. According to a Bloomberg article published on February 19, “Trump’s Car Tariffs Would Hit Eastern Europe.” The direct and indirect value added due to car exports to the U.S. amounted to between 0.5 percent and 0.9 percent of economic output in Hungary, Slovakia and the Czech Republic last year.

China Region

Strengths

- It was a solid week around the region. China’s Shanghai Composite closed up a whopping 4.54 percent for the week, jumping back above its 200-day moving average for the first time in nearly a year. Hong Kong’s Hang Seng Composite (HSCI) closed up 3.67 percent, and Vietnam’s Ho Chi Minh Stock Index closed up 4.00 percent for the week.

- Every single sector in the Hang Seng Composite closed up on the week, with consumer services jumping most of all, rising 6.68 percent and beating out materials—a close second—which rose 6.57 percent.

- Camera module manufacturer Q Technology Group rose nearly 32 percent for the week, the top gainer in the HSCI, as recent shipments demonstrated some recovery and yielded some upgrades to the stock.

Weaknesses

- India’s Nifty and Sensex indices closed up a paltry 65 and 17 basis points, respectively, while the Philippines finished up a mere 69 basis points on the week. What can we say? It was a green one.

- In a positive week for the region, risk-off telecommunications was the worst-performing sector in the HSCI, finishing up a mere 2.61 percent.

- Exports from Thailand dropped more than expected. Analysts were looking for a 2.10 percent decline in year-over-year exports for the January reading. Instead, exports lost 5.65 percent. Non-oil domestic exports missed in Singapore, where an expected year-over-year gain of 7.0 percent came in instead as minus 5.7 percent.

Opportunities

- The tone of the (now-extended) U.S.-China trade talks this week was more optimistic, as both President Donald Trump and Chinese Vice Premier Liu He indicated they think it is “likely” some kind of a deal gets done. Secretary Steven Mnuchin stated that the U.S. and China have reached a final agreement on the issue of currency, and President Trump reiterated that he will likely push back the deadline on the next round of tariff implementation.

- Trump and North Korea’s Kim Jong Un will meet next week in Hanoi, Vietnam for a second summit and will attempt to hammer out more details on what denuclearization will look like and how it will be measured. Talk is good, and progress better; here’s to a peaceful resolution! On National Margarita Day, we can all drink to that.

- While a possible Saudi “pivot” toward Asia may have other implications for the West, it may well hold opportunity for Asia. The Crown Prince’s trip through five Asian nations is already resulting in deals, as Saudi Aramco agreed to set up a joint venture with two Chinese firms to build a $10 billion refining and petrochemical complex, and as the Crown Prince promised billions for projects in Pakistan and India.

Threats

- Technically speaking, the additional tariffs on Chinese goods are set to go into effect in almost exactly one week, almost down to the hour. Of course, that looming deadline may well be extended (and indeed, it is quite consensus at this point that in fact they will be), but the possibility remains. Another possibility is that even though the deadline may be pushed back, “progress” could ultimately be insufficient for one or both parties and result in an eventual resumption of tariff hikes and the resultant further disruptions to trade.

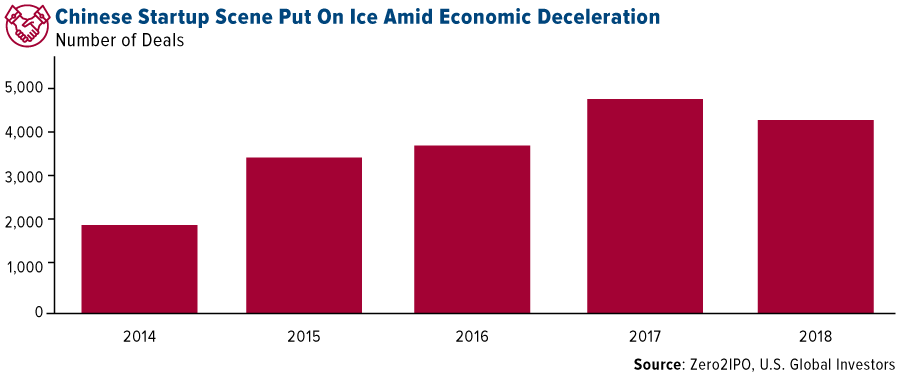

- One recent effect of the deceleration in Chinese growth last year was a decline in the number of deals in the startup scene.

- Central banking policies will remain, well, central over the coming months as a trade deal or no-deal plays out in currency markets and as the U.S. Fed clarifies what exactly a “pause” is.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 22 was Paragon, up 167.8 percent.

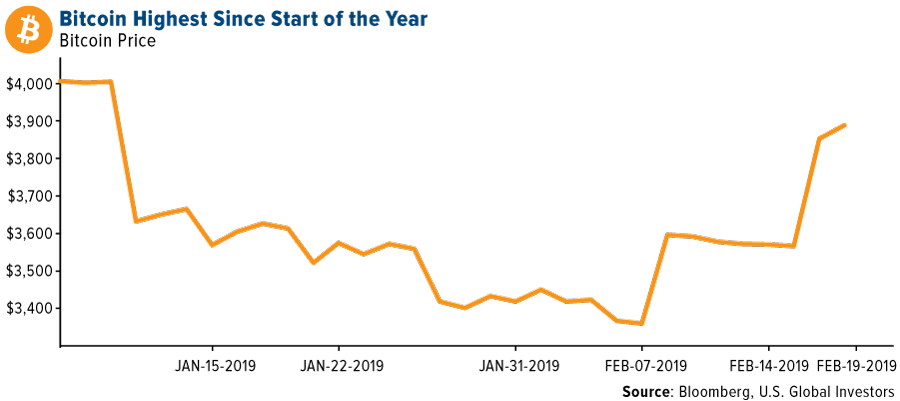

- Bitcoin prices were moving higher this week, looking to extend a win streak that has seen the cryptocurrency trade to the $4,000 mark, reports MarketWatch. “The big level isn’t until $5,000, which coincides with the 200-day moving average,” said Mati Greenspan, senior market analyst at eToro. “If we get a strong break of that, that’s when things start to change.” On Thursday, bitcoin prices were drifting a bit lower, but the digital coin still held up the highest since the start of the year.

- Latin America’s biggest standalone investment bank, Banco BTG Pactual, is the latest to join the world of cryptocurrency assets with its own security token, reports Bloomberg. The bank’s chief technology officer Gustavo Roxo says BTG plans to raise as much as $15 million through an initial coin offering for a token called ReitzBZ. The token will be backed by distressed real estate assets in Brazil.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 22 was ELA Coin, down 74.77 percent.

- Gavin Wells, head of Europe for enterprise blockchain company Digital Asset (DA), is the latest to announce his departure from the company, reports Coindesk. Just over a week ago it was revealed that James Powell, CIO and CTO of engineering at DA, also left the software company.

- Last week JPMorgan announced plans to develop a prototype digital coin, which Bloomberg writes could be the reason pushing bitcoin and other digital currencies higher this week in a delayed boost. Many crypto-specific news outlets, however, have been mocking Bloomberg’s analysis, saying it reveals an epic lack of understanding on the part of mainstream media and the financial industry at large, write CCN.com. CCN Reporter Ben Brown explains that “Bloomberg’s headline tries to draw together two completely unconnected events. The truth is JPM coin has nothing in common with bitcoin. It’s not a threat to bitcoin, nor does it have any attributes that could support bitcoin’s price.”

Opportunities

- It’s time for institutional investors to consider dipping their toes into cryptocurrencies, according to Cambridge Associates, a consultant for pensions and endowments, reports Bloomberg. In a research note published Monday, analysts from the group said that “despite the challenges, we believe that it is worthwhile for investors to begin exploring this area today with an eye toward the long run.”

- Elon Musk, founder and CEO of Tesla and SpaceX, discussed his views on cryptocurrency in a podcast with investment firm ARK Invest this week. Musk believes that bitcoin’s structure is “quite brilliant” and thinks that cryptos offer an improved alternative to conventional money. “It [cryptocurrency] bypasses currency controls…Paper money is going away,” Musk said. “And crypto is a far better way to transfer values than a piece of paper, that’s for sure.”

- Facebook is reportedly ramping up its blockchain resources, reports MarketWatch, and CEO Mark Zuckerberg believes the technology could be implemented as an alternative way for users to access, store and manage their private data. “Basically, you take your information, you store it on some decentralized system and you have the choice of whether to log in to different places and you’re not going through an intermediary,” he said in a Facebook live interview.

Threats

- Cryptocurrencies should stop being compared to gold, reports Coindesk. According to a recent report from the World Gold Council (WGC), digital coins are “no substitute” for the yellow metal, arguing that gold is very different from cryptos for a number of reasons. The WGC says gold is less volatile, has a more liquid market and trades in a regulatory environment, among other factors. In a report last month the group also highlighted that the price of bitcoin has been “extremely volatile – some 10 times that of the dollar denominated gold price.”

- Andreas Antonopoulos, the author of two widely acclaimed books on cryptocurrency, offered advice to developers building Ethereum, reports Coindesk. At a conference that drew thousands to Colorado, ETHDenver, he gave a keynote address about the importance of building unstoppable code to hackers and enthusiasts. Speaking in an interview with Coindesk, Antonopoulos said “Be careful of fragmentation…When things get difficult, people become more insular in their thinking and they start magnifying differences instead of focusing on commonalities.”

- Despite bitcoin’s positive week, one expert is cautioning further declines on the horizon, reports MarketWatch. “Bitcoin continues bouncing around in the upper $3K range. But we saw this same behavior at $9K support, $8K support, $7K, $6K, $5K and $4K,” explains Jani Ziedins of the Cracked Market blog. “The lack of a decisive bounce tells us that bitcoin is not grossly oversold yet. That means lower prices are still ahead of us.”

February 20, 2019A Trade War Truce Could Be Imminent |

February 15, 2019The Two Biggest Drivers of Gold Explained |

February 12, 2019U.S. Global Investors Reports Financial Results for the Second Quarter of 2019 Fiscal Year |

|||

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 196.42 | +6.15 | +3.23% |

| Gold Futures | 1,331.00 | +8.90 | +0.67% |

| Natural Gas Futures | 2.70 | +0.08 | +2.97% |

| S&P/TSX VENTURE COMP IDX | 623.27 | +7.34 | +1.19% |

| 10-Yr Treasury Bond | 2.65 | -0.01 | -0.41% |

| Nasdaq | 7,527.55 | +55.14 | +0.74% |

| Oil Futures | 57.18 | +1.59 | +2.86% |

| Hang Seng Composite Index | 3,878.12 | +137.28 | +3.67% |

| S&P 500 | 2,792.67 | +17.07 | +0.62% |

| DJIA | 26,031.81 | +148.56 | +0.57% |

| Korean KOSPI Index | 2,230.50 | +34.41 | +1.57% |

| Russell 2000 | 1,590.06 | +20.81 | +1.33% |

| S&P Energy | 483.41 | -2.48 | -0.51% |

| S&P Basic Materials | 349.17 | +7.76 | +2.27% |

| XAU | 78.61 | +2.97 | +3.93% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.70 | -0.28 | -9.30% |

| S&P/TSX Global Gold Index | 196.42 | +20.46 | +11.63% |

| 10-Yr Treasury Bond | 2.65 | -0.09 | -3.25% |

| Oil Futures | 57.18 | +4.56 | +8.67% |

| Gold Futures | 1,331.00 | +40.80 | +3.16% |

| S&P 500 | 2,792.67 | +153.97 | +5.84% |

| S&P Energy | 483.41 | +26.87 | +5.89% |

| Hang Seng Composite Index | 3,878.12 | +292.29 | +8.15% |

| DJIA | 26,031.81 | +1,456.19 | +5.93% |

| Korean KOSPI Index | 2,230.50 | +102.72 | +4.83% |

| Nasdaq | 7,527.55 | +501.78 | +7.14% |

| S&P Basic Materials | 349.17 | +20.89 | +6.36% |

| Russell 2000 | 1,590.06 | +135.81 | +9.34% |

| S&P/TSX VENTURE COMP IDX | 623.27 | +30.57 | +5.16% |

| XAU | 78.61 | +9.75 | +14.16% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.70 | -1.75 | -39.27% |

| 10-Yr Treasury Bond | 2.65 | -0.41 | -13.41% |

| DJIA | 26,031.81 | +1,567.12 | +6.41% |

| Oil Futures | 57.18 | +2.55 | +4.67% |

| S&P 500 | 2,792.67 | +142.74 | +5.39% |

| Gold Futures | 1,331.00 | +91.30 | +7.36% |

| S&P Energy | 483.41 | -2.41 | -0.50% |

| Nasdaq | 7,527.55 | +555.29 | +7.96% |

| Korean KOSPI Index | 2,230.50 | +160.55 | +7.76% |

| S&P Basic Materials | 349.17 | +12.37 | +3.67% |

| Russell 2000 | 1,590.06 | +101.78 | +6.84% |

| Hang Seng Composite Index | 3,878.12 | +357.82 | +10.16% |

| S&P/TSX Global Gold Index | 196.42 | +24.74 | +14.41% |

| S&P/TSX VENTURE COMP IDX | 623.27 | +20.83 | +3.46% |

| XAU | 78.61 | +11.41 | +16.98% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Piraeus Bank SA

National Bank of Greece SA

New Gold Inc

Barrick Gold Corp

Newmont Mining Corp

North American Palladium Ltd

Citigroup Inc

Glencore Plc

Anglo American Plc

BHP Group Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy. The S&P CoreLogic Case-Shiller 20-City Composite Home Price NSA Index seeks to measures the value of residential real estate in 20 major U.S. metropolitan areas. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The BSE SENSEX (also known as the S&P Bombay Stock Exchange Sensitive Index or simply the SENSEX) is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange. The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market.