Airline Stocks Just Posted Their Best Week on Record

Date Posted: June 5, 2020

Read time: 57 min

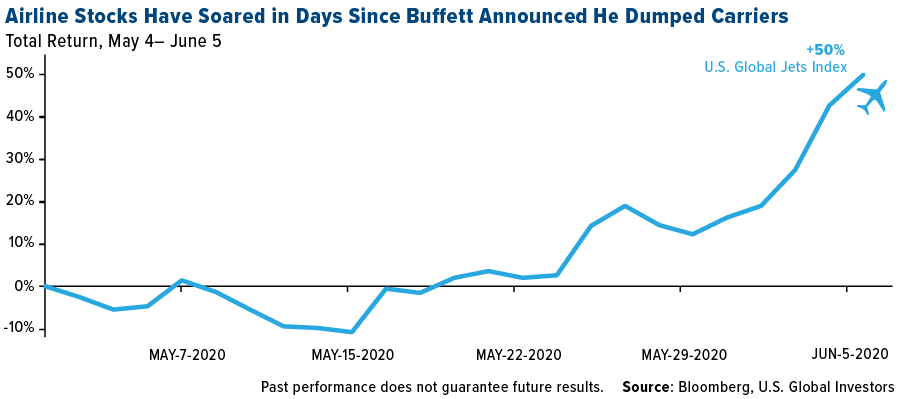

Warren Buffett "should have kept airline stocks because the airline stocks went through the roof today," President Trump said this week. It's a good thing that investors chose not to follow Buffett's lead, as airline stocks are up 50% since his exit.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Today I’d like to start by lending my voice in support of those who seek to bring attention to and rectify the deeply rooted societal inequities that contributed to the senseless killings of George Floyd, Breonna Taylor, Ahmed Aubrey and others. Racism has no place in America. Full stop.

Many Americans understand and empathize with the outrage, even if they don’t necessarily agree with the looting and violence that have defined some of the protests.

A vast majority of the demonstrators want only to exercise their First Amendment rights peacefully, and it’s unfortunate when a few bad actors are allowed to hijack the protests.

Like the coronavirus pandemic and economic downturn, the civil unrest has generated a lot of fear and uncertainty among Americans.

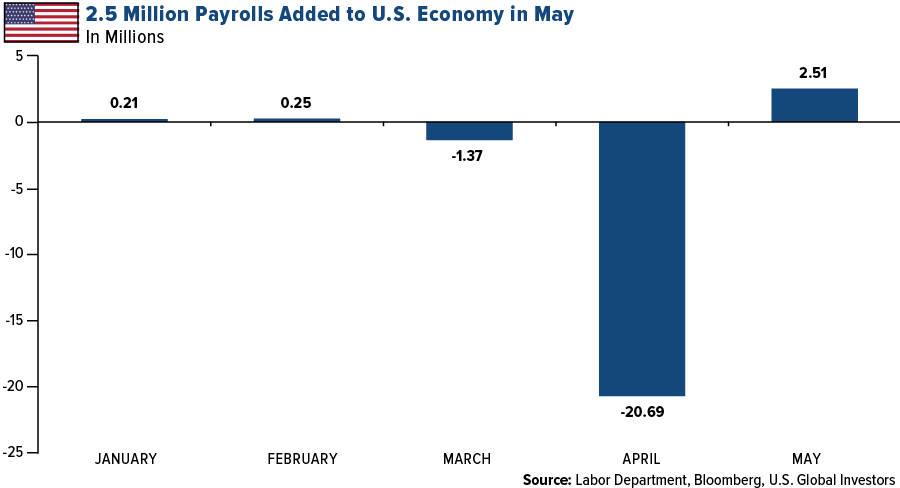

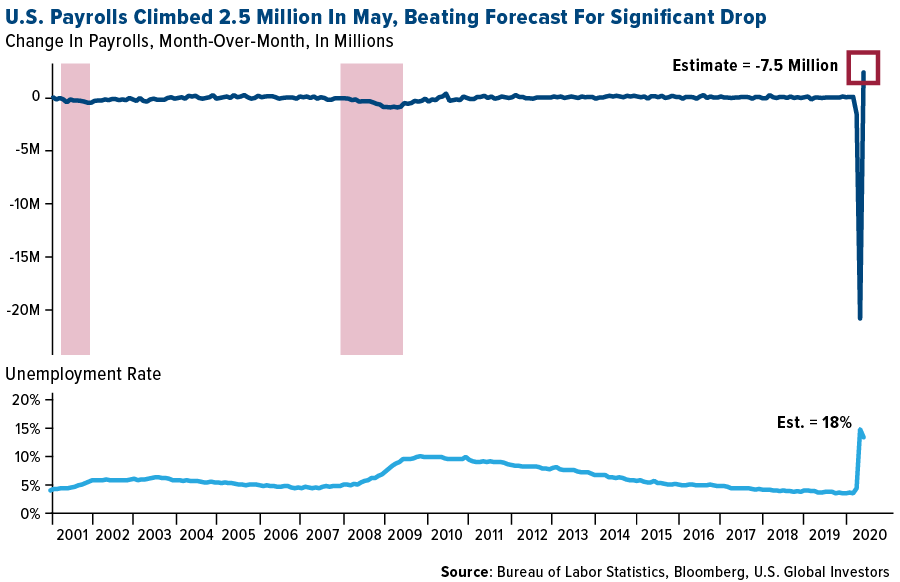

But there are signs that the worst is behind us. The daily rate of new coronavirus cases in the U.S. has been steadily decreasing. And today, the Labor Department reported that the U.S. added a staggering 2.5 million payrolls in May, suggesting a strong economic recovery is underway.

Much work still needs to be done, but I’m equally confident a satisfactory solution to the unrest can be reached.

Airline Investors Rebuff Buffett

President Donald Trump addressed the blowout jobs numbers in a press conference today, comparing the U.S. economy to a “rocket ship.” Economists had been expecting the unemployment rate to jump higher in May, possibly to as much as 20 percent, but it ended up falling last month, from 14.7 percent in April to 13.3 percent.

Trump praised the domestic airline industry, saying carriers are recovering nicely with the economic reopening. On Thursday, shares of American Airlines stock exploded an unbelievable 41 percent, the most on record for a single day, after the carrier said it would increase July flights 74 percent compared with this month. Meanwhile, more and more planes are returning to the sky, with the number of parked passenger aircraft dropping below 50 percent of all fleets in the U.S., Europe and China, according to Bloomberg.

A one-time airline operator himself, Trump also singled out Warren Buffett, who announced in early May that he sold his positions in the four major carriers due to the spread of the coronavirus.

Buffett “should have kept airline stocks because the airline stocks went through the roof today,” the president said.

He’s not wrong. I normally urge investors to follow the money, but it’s a good thing that they chose not to follow Buffett’s lead this time. Since we learned of his departure, investors have flooded into airline equities, pushing them up 53.5 percent in intraday trading Friday.

In fact, the S&P 500 Airlines Index just increased 35 percent this week alone, its “biggest on record and seven times the broader stock market’s five-day gain,” writes Bloomberg’s Nancy Moran.

As I shared with you last month, a recovery in commercial air travel is well underway. At the end of each business day, the Transportation Security Administration (TSA) reports on the number of passengers it screened in U.S. airports. As of yesterday, that number was more than 391,882, a 350 percent increase in volume from the low of 87,500 on April 14. Wheels up!

Buying the Gold Dips Looks Attractive

It’s risk-on again for investors. Thanks to the unexpectedly strong U.S. jobs report, stocks rallied strongly on Friday, with gains led by energy producers Occidental Petroleum, Apache and Marathon Oil, as well as cruise lines such as Royal Caribbean, Carnival and Norwegian.

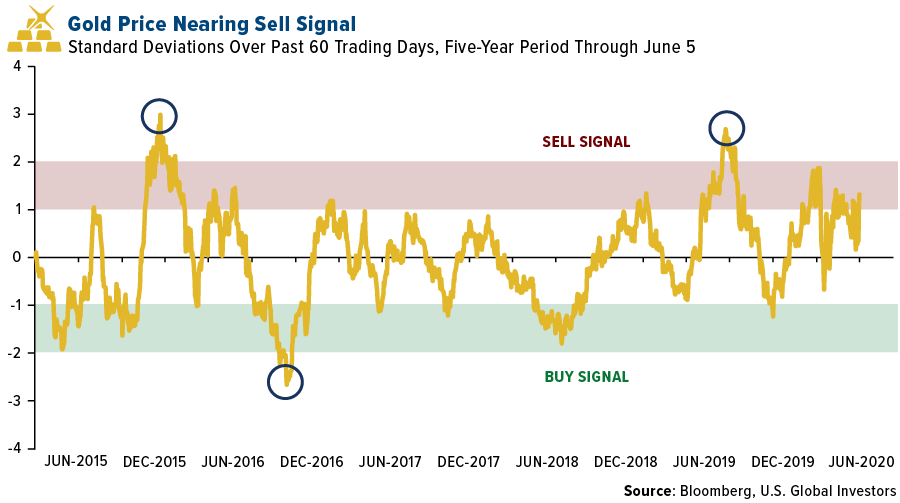

Gold sold off as a result, its price tumbling close to 2.5 percent. This marked the precious metal’s worst one-day decline since the end of March.

Based on fundamentals, the selloff was rational. Gold’s 60-day standard deviation over the past five years shows that the metal was nearing a sell signal in morning trading.

When it comes to selecting gold and precious metal mining stocks, we take a quant approach, focusing on a number of different factors.

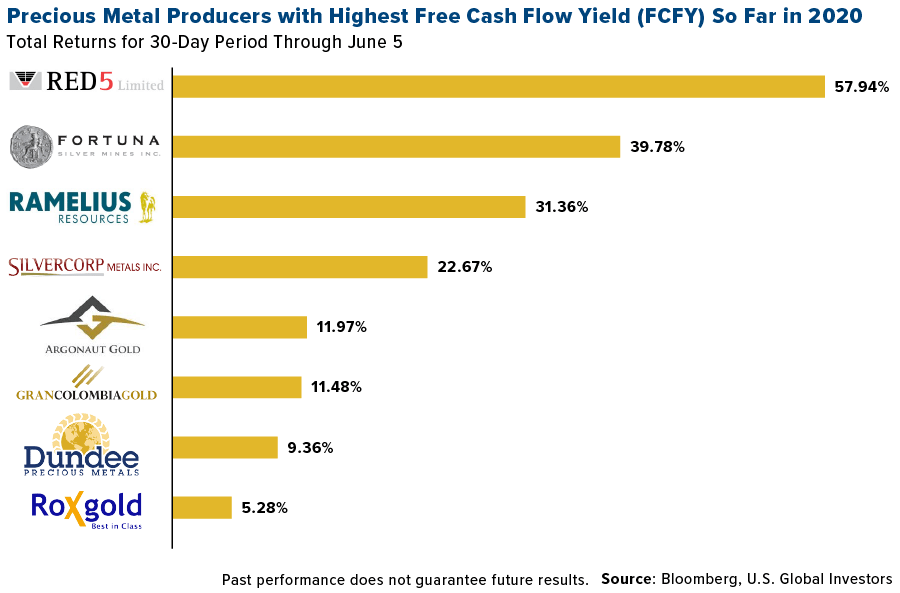

Among those factors is free cash flow yield (FCFY), one of the best profitability indicators. General gold equity investors look for high free cash flow, which is why Newmont was one of the best performing S&P 500 stocks until recently.

I did some data mining on some of my favorite mining stocks and found that, year-to-date, the top 10 producers with a market cap between $200 million and $1 billion had a remarkable average of 33.2 in FCFY.

Australia-based Red 5 Limited was the best performing mining stock of the past 30 days, up almost 58 percent. This was followed by Fortuna Silver Mines, up nearly 40 percent, and Ramelius Resources, up 31 percent for the month.

Interested in learning more about investing in airlines in the age of COVID-19? Register for our FREE webinar, taking place June 17 at 1:00 Central time, by clicking on the banner below!

Gold Market

This week spot gold closed at $1,684.38, down $45.89 per ounce, or 2.65 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.36 percent. The S&P/TSX Venture Index came in up 0.57 percent. The U.S. Trade-Weighted Dollar fell 1.40 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-31 | Caixin China PMI Manufacturing | 49.6 | 50.7 | 49.4 |

| Jun-1 | ISM Manufacturing | 43.8 | 43.1 | 41.5 |

| Jun-3 | Durable Goods Orders | -17.20% | -17.70% | -17.20% |

| Jun-3 | ADP Employment Change | -9000k | -2760k | -19557k |

| Jun-4 | Initial Jobless Claims | 1833k | 1877k | 2126k |

| Jun-4 | ECB Main Refinancing Rate | 0.00 | 0.00% | 0.00% |

| Jun-5 | Change in Nonfarm Payrolls | -7500k | 2509k | -20687k |

| Jun-10 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Jun-10 | CPI YoY | 0.30% | — | 0.30% |

| Jun-11 | Initial Jobless Claims | 1600k | — | 1877k |

| Jun-11 | PPI Final Demand YoY | -1.30% | — | -1.20% |

Strengths

- The best performing precious metal for the week was palladium, up 0.77 percent. ETFs added 241,076 troy ounces of gold to their holdings on Monday, bringing net purchases for the year to 17.2 million ounces, according to Bloomberg data. Total gold held by ETFs rose 21 percent this year to 100.2 million ounces – the highest level since June 2019. However, on Thursday the amount of bullion held in ETFs fell slightly, the first drop in 30 trading days. Silver is also seeing some love. ETFs added 4.62 million troy ounces of silver to their holdings on Monday. Total imports of gold to the U.S. topped $7.2 billion in May, the highest in records going back to 2003, according to the U.S. Census Bureau.

- Pandora A/S, the world’s biggest jewelry firm, announced that it will stop relying on newly minted gold and silver and instead use only recycled precious metals starting in 2025. CEO Alexander Lacik of the Copenhagen-based company said in a statement that “metals mined centuries ago are just as good as new…the need for sustainable business practices is only becoming more important.” Bloomberg notes that Pandora shares jumped 5 percent when trading began on Tuesday.

- Gold sales in China rose 54 percent in May from April, according to a survey from China Gold Association. The World Gold Council said in April that demand for gold jewelry, bars and coins in China will likely pick up in the second quarter after a big drop in the first quarter due to lockdowns. Perseus Mining announced a $60 million takeover of neighbor Exore Resources amid more deal-making in the gold sector, reports Bloomberg. Perseus will gain control of Exore’s gold project in northern Ivory Coast and a 2,000 square kilometer land package.

Weaknesses

- The worst performing precious metal for the week was gold, down 2.77 percent. Gold tumbled on Friday after better-than-expected U.S. jobs numbers. Payrolls rose by 2.5 million and the jobless rate fell to 13.3 percent from 14.7. Bullion is heading for its longest run of weekly losses since September. The yellow metal’s haven appeal shrunk in May as major economies slowly reopened.

- Gold Fields said in a statement that an employee died at the South Deep mine in South Africa after falling down a reef ore-pass. “This is the first fatality at Gold Fields in a year and comes amid significant improvements in the group’s safety performance over the past six years.” South Africa’s ultra-deep mines are known to be dangerous.

- Central bank net purchases of gold in the first quarter of this year totaled 145 tonnes, which was 8 percent lower than the same period a year ago, according to the World Gold Council (WGC). Six central banks were net buyers, compared with 10 a year ago. Despite lower purchases, the WGC expects buying to pick up in the second half of the year.

Opportunities

- The Brasher Doubloon, the very first gold coin made in the U.S., is being offered privately at a $15 million asking price, according to PCAG Inc. who is marketing the coin on behalf of a collector. The coin dates back to 1787 – 11 years after the Declaration of Independence was signed. Bloomberg notes that the coin was originally worth $15. It went on to sell for $625,000 in 1981, $2.99 million in 2005 and $7.4 million in 2011.

- According to Metals Focus Director Nikos Kavalis, gold could climb near its record high in the second half of 2020 as yields will likely remain low and real rates stay negative. “Even if equities rally further from current levels, we still think allocating to gold makes sense, given what you get for your fixed-income holdings at the moment.” Even as investors’ risk appetite improves, Australia & New Zealand Banking Group has a similar view that gold could hit an all-time high. “The expansion of central banks’ balance sheets shows no sign of abating, while geopolitical tensions escalate. We think those investors who continue to raise their allocation to precious metals are sitting on a gold mine.” JPMorgan shifted its view on gold from underweight to overweight due to central bank stimulus, a weaker dollar and as a hedge against market risks.

- Although gold hasn’t had the best start to the month, it did perform strongly in 2020 through May 14. As seen in the chart below, gold priced in local currency outperformed the respective domestic stock index in that country. For example, in the U.S., gold rose 14 percent through May 14 while the S&P 500 was down 12 percent for the same period. As highlighted in the annual “In Gold We Trust” report by Incrementum, gold often moves in the opposite direction of wider equities and can be a hedge against volatility.

Threats

- Despite better than expected payroll increases in May, local government payrolls fell. According to U.S. Bureau of Labor Statistics data, local government payrolls dropped by 571,000 to 18.3 million in May. Bloomberg notes that in April and May, states and cities have cut more jobs than they did after the last recession. If these job cuts are maintained, it could exert a drag on the country’s economic recovery. States alone are expected to face a $765 billion shortfall over the next three years based on projections by the Center of Budget and Policy Priorities.

- U.S. and China tensions escalated again this week over flights. Responding to China’s announcement on Thursday that limits U.S. carriers to one flight per week each to the county, the U.S. Department of Transportation said it would only permit two flights a week in total from Chinese airlines, reports Bloomberg. Both countries severely limited flights and air traffic in response to the coronavirus pandemic and both seem reluctant to open more flights back up unless the other does so first.

- The outbreak of COVID-19 continues to remain a threat. Latin America has emerged as the new virus epicenter, threatening to disrupt mining operations as more workers test positive for the virus.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 6.81 percent. The S&P 500 Stock Index rose 4.91 percent, while the Nasdaq Composite climbed 3.42 percent. The Russell 2000 small capitalization index gained 8.11 percent this week.

- The Hang Seng Composite gained 7.45 percent this week; while Taiwan was up 4.91 percent and the KOSPI rose 7.50 percent.

- The 10-year Treasury bond yield rose 24 basis points to 0.891 percent.

Domestic Equity Market

Strengths

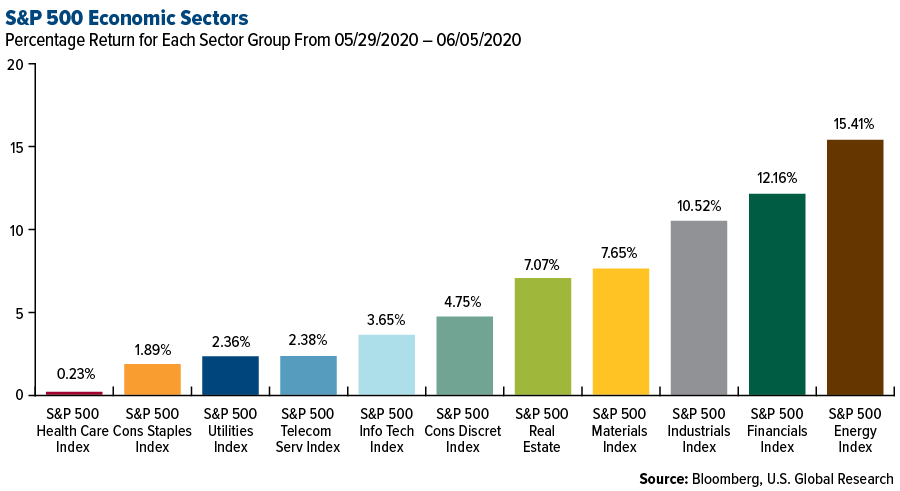

- Energy was the best performing sector of the week, increasing by 15.41 percent compared to an overall increase of 4.84 percent for the S&P 500.

- American Airlines was the best performing S&P 500 stock for the week, increasing 77.05 percent.

- Zoom delivered an "incredible" earnings beat in its first quarter report on Tuesday, as it saw its usage and popularity skyrocket due to coronavirus-related rise in remote work. It also doubled its revenue guidance for the year to $1.8 billion, though some on Wall Street think that that estimate may not have gone far enough.

Weaknesses

- Health care was the worst performing sector for the week, increasing 0.23 percent.

- Incyte Corp was the worst performing S&P 500 stock for the week, falling 8.24 percent.

- U.S. utilities missed sales estimates more than any other sector in the first quarter as stay-at-home orders crippled power demand from businesses and manufacturers. All but two companies in the S&P 500 Utilities Index earned less revenue than analysts forecast, with most of them also reporting a drop from a year earlier. Still, power companies – which are typically seen as insulated from economic downturns – were able to collectively increase year-over-year earnings by 6.3 percent amid lower costs.

Opportunities

- The S&P 500’s biggest-ever gain over 50 trading days “offers a reason to think stock prices may be even higher this time next year,” according to Ryan Detrick, a senior market strategist at LPL Financial LLC. Detrick made the comment in a post Thursday on LPL’s research blog. The index rose for the 50 days ended Wednesday by 40 percent, the most since it was restructured to include 500 companies in 1957, according to data from Bloomberg. Peak gains of more than 20 percent occurred seven times between 1975 and 2009, and the S&P 500 moved higher each time in the next 12 months. The average advance was 17 percent.

- Zynga, once written off as the flailing creator of "FarmVille," has undergone a successful turnaround. The company announced a $1.8 billion acquisition of Turkish gaming company Peak during the pandemic, and has seen a big boost in downloads as users under lockdown turn back to its games.

- The S&P 500 Index rallied to three-month highs this week, while haven assets like the greenback, Treasuries and gold slumped. The Bloomberg Dollar Spot Index is trading below its 200-day moving average for the first time since early March, an indication that “risk-off” momentum may be gaining steam in support of further equity gains.

Threats

- With the S&P 500 Index’s rally extending into a fourth day, a technical gauge is flashing a warning signal. The GTI Global Strength Indicator—a measure of upward and downward movements of successive closing prices—climbed above 70 for the first time since February, just before the coronavirus pandemic sent stocks plunging. Coupled with the equity benchmark’s climb above 3,100 and valuations at 20-year highs, the gauge’s “overbought” status may give traders pause as they navigate the days ahead.

- Facebook is getting slammed by civil rights leaders and losing business as employee strife rages about its stance on Trump’s posts. Civil rights leaders said Mark Zuckerberg "refuses to acknowledge how Facebook is facilitating Trump’s call for violence against protesters."

- Southwest is offering buyout packages, temporary leave to “ensure survival.” The airline, which has not imposed any layoffs or furloughs in its 49-year history, said its flying capacity would probably be down about 30 percent in the fall.

The Economy and Bond Market

Strengths

- The unemployment rate unexpectedly fell to 13.3 percent in May after employers added 2.5 million workers. That compared with a forecast for a loss of 7.5 million jobs. The economy could be picking up faster than expected.

- The Institute for Supply Management headline Purchasing Managers Index (PMI) was 43.1 for May, an increase of 1.6 from 41.5 in April.

- Non-manufacturing activity contracted in May for the second consecutive month, though at a slower pace than April. The index came in at 45.4 in May, up 3.6 percentage points from April and above the consensus forecast of 44.4.

Weaknesses

- An additional 1.877 million Americans filed for unemployment benefits in the week ending May 30, exceeding economists’ estimates for 1.843 million initial jobless claims during the week. The prior week’s figure was revised higher to 2.13 million from the previously reported 2.12 million. Over the past 11 weeks, more than 42 million Americans have filed for unemployment insurance.

- Factory orders fell 13 percent in April, a slightly larger drop than the 11 percent decline in the prior month. Durable goods orders also fell sharply by 17.7 percent.

- The coronavirus shutdowns caused Texas’s sales-tax collections to drop by the most in a decade. The revenue is the biggest source of funds for the state government, which does not have an income tax. With business closed and unemployment surging, those collections in May dropped 13.2 percent from a year earlier to $2.6 billion, the steepest decline since January 2010.

Opportunities

- Investors will be on the lookout next week for the University of Michigan’s preliminary consumer sentiment survey for June, hoping the reopening of the economy will also lift consumer sentiment.

- The Fed is allowing all 50 states to have at least two cities or counties eligible to directly issue notes to the Fed’s Municipal Liquidity Facility, regardless of their size. The central bank also said governors can designate two revenue-bond issuers, like public transit agencies or airports, as eligible borrowers. The intent from the Fed is to make sure that these funds can reach the smaller and poorer communities that need them the most.

- The conference and convention business, gutted by months of lockdown, is planning a comeback, and it could begin as soon as September. Over the last three months, 64 percent of the events were canceled outright and 36 percent were rescheduled, mainly to September and after, according to Cathy Breden, chief operating officer of the International Association of Exhibitions and Events and chief executive of the Center for Exhibition Industry Research.

Threats

- Violence erupted in dozens of cities following the death of George Floyd, a black Minneapolis man who died after a white police officer pressed a knee into his neck for more than eight minutes. The chaos struck as the economy struggles to emerge from its coronavirus-enforced hibernation.

- The U.S. dollar has been the preferred currency in the flight to safety during the pandemic with demand being so strong that it has lost its usual correlation with Treasury yields and economic data.

- The sum of exports and imports as a percentage of U.S. GDP declined to 19.6 percent in April, the lowest since February 1993.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was crude oil, up 10.74 percent. Oil saw a sixth weekly gain after OPEC+ reached a tentative deal to prolong production cuts and U.S. jobs data released on Friday was better than expected. Bloomberg notes that Brent crude rose about $42 a barrel. Iron ore pushed toward $100 a ton as investors weigh the impact of lower supply from Brazil amid a surge in COVID-19 infections in the country. Impala Platinum Holdings said that South African miners are seeing palladium demand from Chinese automakers return to pre-pandemic levels.

- Copper is on course to enter a bull market as prices increase for a third week. The metal rose 1.3 percent on the LME on Friday morning, on course to finish more than 20 percent above the 2020 low. Bloomberg notes the rebound coming as demand returned more strongly than expected in China.

- Total SA said its models show oil demand hitting a plateau around 2030 as Europe and China shift to electric cars. The power market will grow, but the oil market will not, according to CEO Patrick Pouyanne. Bloomberg reports that Total will attempt to gain investors by spending on low-carbon electricity. According to people familiar with the matter, Total is set to buy a stake from SSE Plc in a large wind farm off the Scottish coast.

Weaknesses

- The worst performing precious metal for the week was uranium, down 3.02 percent. 20,000 tons of diesel leaked from a reservoir owned by Norilsk Nickel in Siberia and prompted Russia to declare a state of emergency in the region – five days after the spill occurred. The cause of the spill is yet to be determined, but the company thinks it could be climate change related. Scientists have warned for many years that the thawing of frozen ground in Russia is threatening the stability of buildings and pipelines, notes Bloomberg. There is a growing threat of massive spending to shore up infrastructure amid changing ground temperatures.

- According to Moody’s Investors Service, North American coal miners could see earnings slide by more than 50 percent and thermal coal production could be down more than 25 percent. “Coal consumption will be crushed in 2020. We expect a sharp and sustained slowdown in economic activity will result in lower economic growth, reduced demand for electricity and reduced demand for steel,” analysts led by Benjamin Nelson wrote in a report.

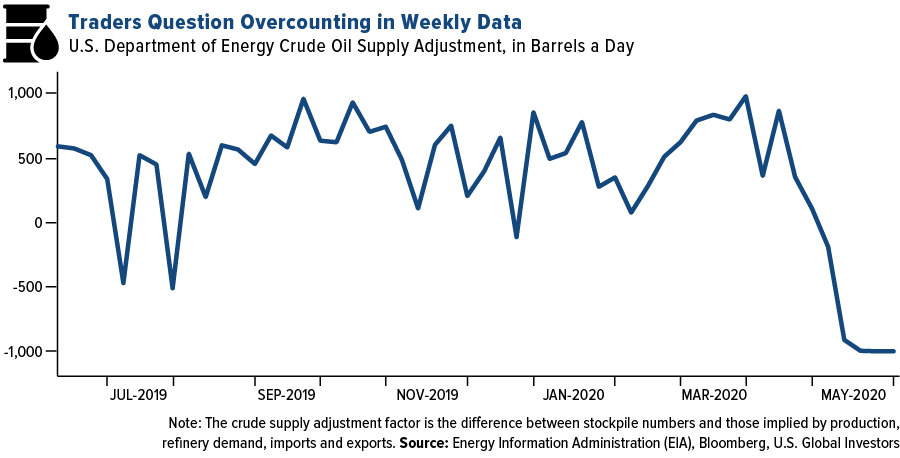

- Oil traders are wondering why the math doesn’t add up with the U.S. inventory data. The excess amount of crude shows up in the U.S. Energy Information Administration’s crude supply adjustment factor that has averaged negative 980,000 barrels daily over the past month – the largest in records going back to 2011. Bloomberg’s Catherine Ngai writes “While daily output fell 700,000 barrels to 11.2 million in May, they believe oil’s plunge into negative territory in April should have led to a steeper decline.”

Opportunities

- According to Drax Electric Insight’s quarterly report, the U.K.’s sunniest spring on record boosted solar power’s share of the energy mix to a record high. In the month of May, solar supplied an average of 2.6 gigawatts a day, or 33 percent of the country’s electricity. Bloomberg notes that the U.K. has been coal free for 53 days as of May 30.

- Berenberg said in a note that ESG is likely to become a positive differentiator for returns in the mining sector as adherence to these principles gain importance for investors. Analysts say that Polymetal and Petra Diamond are preferred names from an ESG perspective. Other companies that show improving ESG metrics include Anglo Pacific, Base Resources, Kenmare Resources, Resolute Mining and Endeavour Mining.

- Toyota Motor Corp is partnering with five Chinese companies to develop fuel cells for commercial vehicles, as a part of its plan to become a source of energy for electric vehicles. The new entity formed will be called United Fuel Cell System R&D, 65 percent owned by Toyota, and start with an initial investment of $46million. BloombergNEF estimates that annual sales of fuel cells are on track to reach 1 million vehicles by 2035.

Threats

- A report from Wood Mackenzie estimates that aging offshore oil rigs will cost the industry $104.5 billion by 2030. Rystad Energy reported in May that at least 23 platforms a year could be retired. Companies will likely accelerate the closure of aging rigs amid the coronavirus pandemic and record low prices, but they cannot just be abandoned as regulators require proper sealing and environmental upkeep. Marcelo de Assis from Wood Mackenzie says, “abandonment costs will haunt the industry in the years to come, especially if government gets tougher with parent company guarantees.”

- The Trump administration continues to weaken environmental protections and make changes to the Environmental Protection Agency (EPA). Two policies were announced on Thursday cutting reviewing for large infrastructure projects. One of the policies is an executive order from President Trump that instructs agencies to use emergency authorities to bypass bedrock environmental laws and speed federal approvals for highways and oil and gas pipelines. The justification for this is to ease the burden for companies amid the COVID-19 economic downturn. Another proposal includes new guidelines for how the EPA weighs the costs that a regulation places on an industry and its customers versus the health benefits it provides to the public.

- U.S. shale driller Parsley Energy said it is turning oil wells back on just weeks after shutting them. EOG Resources, America’s largest shale-focused producer, said it plans to accelerate output in the second half of this year. The restart of American shale production has analysts concerned that it will complicate OPEC+ efforts to curb supply. Demand has rebounded in China, with tankers idling off the coast waiting to unload, but demand is still uneven in the rest of the world.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 7 percent. Recently, Fitch affirmed Poland’s “Long-Term Foreign Currency Issuer Default Rating” at A- with a stable outlook. In addition, Fitch believes Poland should be relatively resilient to the shock of the COVID-19 pandemic. The European Union predicts that growth in Poland will contract by 4-5 percent in 2020, about half of the euro-area. CCC, a shoe retailer, was the best performing equity trading on the Warsaw Stock Exchange, gaining 47 percent in the past five days supported by optimism over reopening shopping malls.

- The Czech koruna was the best performing currency this week, gaining 3 percent. The currency was supported by stronger economic data. Preliminary annual and quarterly gross domestic product for the first quarter was reported stronger than expected, and retail sales improved slightly in April. Unemployment moved slightly higher from 3.4 percent in April to 3.6 percent in May.

- Utilities was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst relative performing country this week, gaining 1.7 percent. The country underperformed on expectations that Romania may receive its first junk rating with a review from S&P due on late on Friday. The three major agencies have the country at their lowest investment grade, with a negative outlook. Digi Communications, a cable television/data/ telephone/Internet provider, was the worst performing equity trading on the Bucharest Stock Exchange, losing 2 percent over the past five days.

- The Turkish lira was the worst relative performing currency in the region this week, gaining 78 basis points. The lira appreciated but lagged its peers. Investors remain cautious about the outlook in Turkey; in particular, the prospects of a pick-up in inflation, a widening budget and current account-deficit, and the decline in the central bank’s foreign reserves potentially derailing the lira to move higher against the dollar.

- Materials was the worst performing sector among eastern European markets this week.

Opportunities

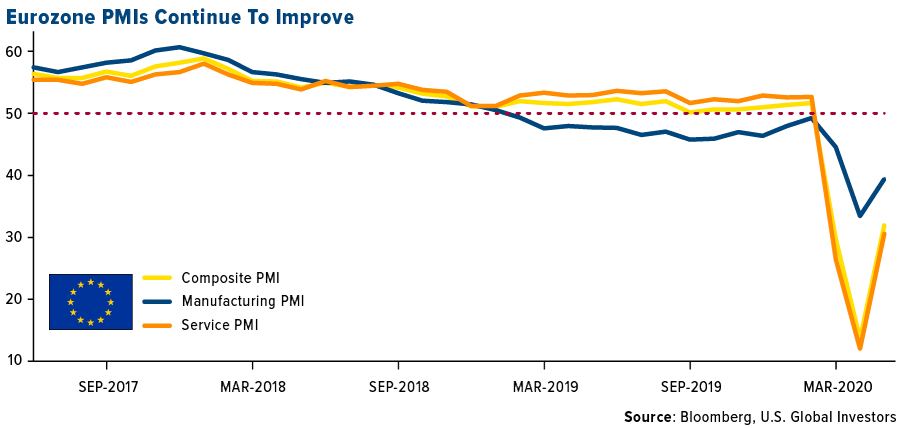

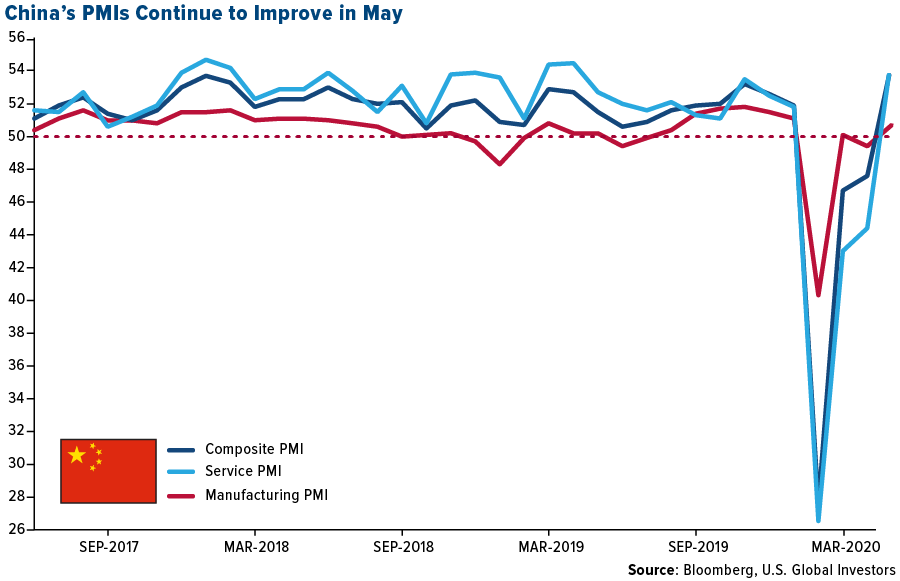

- The IHS Markit flash eurozone composite purchasing managers index rose to a reading of 30.5 in May from 13.6 in April. Service PMI increased to 30.5 from 28.7, and final manufacturing PMI was reported slightly lower at 39.4 versus 39.5. PMIs below the 50 level represent contraction, but they are rebounding as you can see on the chart below.

- The European Central Bank (ECB) intensified its response to the coronavirus recession with a bigger-than-anticipated increase to its pandemic emergency bond-buying program. The program was expended by 600 billion (versus expected 500 billion) for a total of 1.4 trillion. The duration of the program was extended to at least the end of 2021. The ECB’s rates were left unchanged. The regular asset purchase bond-buying program was unchanged at 20 billion per month with the additional 120 billion until the end of the year. In addition, Germany announced a fresh $146 billion stimulus plan to fight the economic impact of coronavirus.

- Card-payment data in Poland shows the economy is reviving. Data from Poland’s biggest bank shows consumers are using their cards more now than before the coronavirus lockdown, pointing to a recovery. The European Union forecast Poland’s gross domestic product to shrink 4.3 percent this year, the least among the bloc’s 27 economies.

Threats

- The Organization of Petroleum Exporting Countries (OPEC) and its allies pledged in April to cut oil output by 9.7 million barrels a day, about 10 percent of the global oil supply. Saudi Arabia and Russia are ready to continue cuts at the current level for an extra month beyond July 1. However, if they cannot come to an agreement with other oil producers, the group’s daily supply curbs will ease to 7.7 million barrels for the rest of the year. A lower oil price presents a threat to Russia as it main revenue comes from the sale of oil and gas. The next OPEC meeting is tentatively planned for June 6-7.

- Russia declared a federal state of emergency in part of Siberia after a massive fuel spill that MMC Norilsk Nickel PJSC said could have been caused by melting permafrost. The May 29 incident may revive concerns about the effects of climate change on infrastructure in the Arctic. Scientists have warned for years that melting permafrost covering more than half of Russia is threatening the stability of buildings and pipelines.

- Gas may be next to trade below zero as the market remains extraordinarily oversupplied. The highest chance of this happening is in August and early September when there is lower demand and higher storage inventories, said Axpo Group. Unlike the oil market, there has been no sign of a coordinated respond to address the glut.

China Region

Strengths

- Philippines was the best performing country this week, gaining 10.7 percent. The government announced more bond buying and is planning to change its law to allow for more stimulus. The cap now is set at 20 percent of the government’s average revenue over the past three years. Bonds have been rallying and have more room to go. JG Summit Holdings Company was the best performing equity among stocks trading on the Philippines Stock Exchange, gaining 28 percent over the past five days.

- The Indonesia rupiah was the best performing currency this week, gaining 4.5 percent. Bloomberg reported that the currency is heading for its best week since 2015, on optimism that the gradual reopening of the economy and improving global risk sentiment will boost inflows into the nation’s high-yield assets.

- Energy was the best performing among equites trading on the Hong Kong Stock Exchange.

Weaknesses

- Pakistan was the worst relative performing market this week, gaining 1.2 basis points. The country’s total coronavirus infections shot up to 90,000 and deaths surged to more than 1,800. Prime Minister Imran Khan on Friday urged the continued awareness about the virus as the country “cannot afford to impose another lockdown.” Indus Dyeing & Manufacturing Company, a yarn manufacturer and distributor, was the worst performing equity among stocks trading on the Karachi Stock Exchange, losing 15 percent over the past five days, (and erasing all gains from the prior week).

- The Indian rupee was the worst performing currency this week, losing 16 basis points. The currency remained mostly flat for the week, brushing off stronger economic data. Annual gross domestic product was reported at 3 percent, higher than the expected 1.6 percent in the first quarter. PMIs remain well below the 50 level that separates growth from contraction, but all moved higher. Service PMI picked up to 12.6, Manufacturing to 30.8 and Composite to 14.8.

- Utilities was the worst performing among equites trading on the Hong Kong Stock Exchange.

Opportunites

- China’s manufacturing PMI came in at 50.6 for the month of May, which was slightly below expectations of 51.0, but still above the 50 level that separates contraction from growth. This marks the third straight month of rising factory output. Among the those surveyed by the National Bureau of Statistics, 81.2 percent have reached more than 80 percent of the normal production level in May.

- Bloomberg reports that mainland China investors have been net buyers of Hong Kong stocks in all but six sessions this year and added $35.4 billion this year as of May 26. The increase in buying coincided with China’s plan to impose security law on the city that sparked an equity crash last week. History shows that mainland buying often picks up when Hong Kong shares tumble. According to Bloomberg calculations, Chinese investors now own 2.9 percent of the total market value of Hong Kong stocks eligible for cross-border trading.

- After testing 10 million residents, the city of Wuhan reported that it found no new cases of COVID-19. Authorities launched a mass testing campaign in mid-May, and reached 9.9 million out of 11 million people, after a cluster of new cases sparked fears of a second wave of infections in the original epicenter of the virus.

Threats

- On Monday, Hong Kong prohibited the annual vigil honoring victims of the pro-democracy Tiananmen Square protests of 1989. The remembrance gathering, held since 1990, had become a major rallying point for Hong Kongers worried about what they see as the overreach of China, notes the New York Times. The city citied the need to enforce social distancing as the reason for the cancellation and comes the week after China moved to enact new security laws on the city.

- China is struggling to attract international investors to its local government notes, where foreign ownership is just 0.01 percent. Banks are typically big buyers of local debt, but banks are now burdened by bad loans and request to keep credit flowing to businesses after the coronavirus pandemic. Zhou Guannan, an analyst with Huachuang Securities Co., said in a Bloomberg interview that “as China’s local government bond market is expanding quickly, regulators need to attract more diversified investors, including foreigners.” Bloomberg notes that issuance will climb to 4.73 trillion yuan in 2020 to help bolster economic growth.

- U.S-China tensions heated up this week over international air travel. President Trump threatened to bar passenger flights from China beginning on June 16 if China did not make changes to its travel restrictions. In March, to stem the spread of COVID-19, China said foreign airlines could operate no more than one weekly flight to the country. The Department of Transportation said that the order had effectively banned U.S. airlines. BBC reports that on Thursday morning China reversed course and will loosen its policy on air travel.

Blockchain and Digital Currencies

Strengths

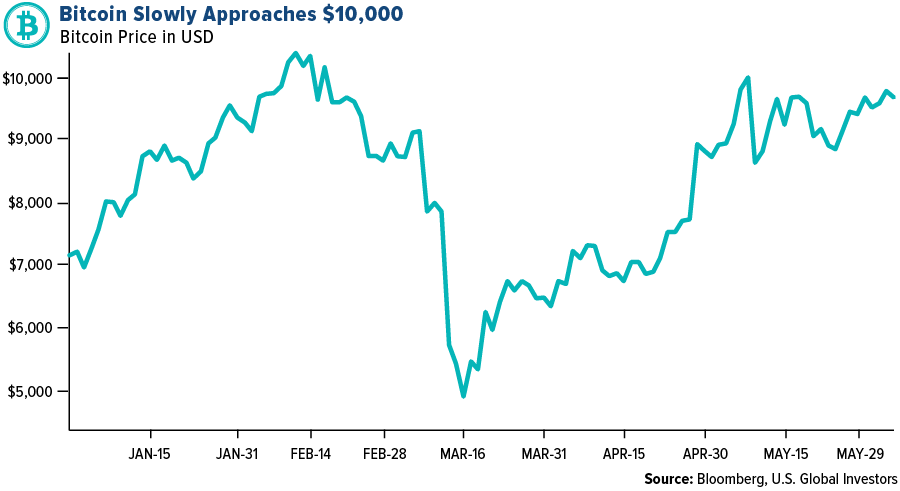

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 5 was DWS, up over 497 percent. Bitcoin hovered over the $9,000 mark this week, slowly inching its way closer to reach $10,000.

- The price of bitcoin has risen above $10,000 for the first time in nearly a month, reports CoinDesk. Unfortunately, the reason for the uptick in price comes as protests in U.S. cities continue to intensify.

- According to Bloomberg Intelligence’s latest commodity outlook, gold and bitcoin remain the “top candidates to advance” this year, reports Kitco News. “Among the few assets up in this tumultuous year, gold and bitcoin are building foundations for further price appreciation,” senior commodity strategist Mike McGlone said. “The metal and crypto remain our top candidates to advance in 2020.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended June 5 was DUO Network Token, down 96 percent.

- As reported by CoinTelegraph, the power struggle inside Bitmain appears to have greatly intensified this week, as reports circulated that Micree Zhan hired guards to physically take over the company’s Beijing office. An open letter from Zhan began to circulate on Chinese social media, and in it he claims to have resumed control of the office and urged employees to return to the office as normal work resumes.

- In a new research paper entitled “Blockchain is Watching You,” writers argue that governments and private-entities are quickly learning how to strip away anonymity from Ethereum. As CoinDesk explains, that’s in part because users are making it easy for them. “Careless usage easily reveals links between deposits and withdraws and also impact the anonymity of other users, since if a deposit can be linked to a withdraw, it will no longer belong to the anonymity set,” the authors write.

Opportunities

- As of June 1, cryptocurrency exchanges and payment processors are now legally recognized as Money Service Businesses (MSB) within Canada, reports CoinTelegraph. Crypto firms must now report all transactions exceeding 10,000 Canadian dollars, and register and comply with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

- The Chinese government are no strangers to digital payments, and now they could be making a cryptocurrency to challenge bitcoin, reports Bloomberg. The Chinese government has begun a pilot program for an official digital version of its currency – with the likelihood of a bigger test at the Beijing Winter Olympics in 2022.

- Bloomberg analysts expect bitcoin to revisit its record high in 2020, reports CoinDesk. But what is the prediction based on? As the article reads, the analysts are paying attention to the price action seen over the last 2.5 years and how it looks similar to the patterns over the 2.5 years following bitcoin’s rise to record highs in December 2013.

Threats

- As written by CoinDesk, a lawsuit alleging stablecoin issuer Tether and sister exchange Bitfinex manipulated the bitcoin market is getting bigger. On Wednesday, a 156-page amended suit was filed, continuing to allege that Tether and Bitfinex orchestrated a grand scheme to launder and circulate billions of allegedly unbacked USDT stablecoins through the market, to the detriment of their customers, the article continues.

- One crypto trader is trying to seize nearly 500 bitcoin from Xapo and Indodax, writes CoinDesk, through a new lawsuit that accuses the two crypto exchanges of harboring his stolen funds. The suit accuses Xapo and Indodax of aiding and abetting unauthorized access of a computer in violation of federal code.

- In May of this year, as exchange volumes and crypto market resumes growing, the USDC stablecoin saw its bitcoin trading volume plummet by 78 percent, writes CoinDesk. CryptoCompare goes on to highlight that both USDC and Paxos (PAX) suffered enormous collapse in BTC volume in just a single month.

Airline Sector

Strengths

- Space travel made a big leap forward in May. A private company, SpaceX, for the first time launched two astronauts into orbit nearly a decade after the U.S. government retired the space shuttle program. The Falcon 9, carrying a Crew Dragon capsule, was launched on Saturday May 30, and arrived at the International Space Station the next morning carrying two American astronauts. The successful launch is one step closer toward space tourism and commercial flights. Both SpaceX and Boeing were awarded contracts for the Commercial Crew Program in 2014, and Boeing could soon too achieve the mission of getting astronauts to space.

- The number of passengers screened daily in the U.S. by the Transportation Security Administration (TSA) has steadily been gaining momentum. On May 31, nearly 353,000 people boarded commercial flights in the U.S., up 303 percent from a low of 87,534 people on April 14, and well above the 10-day moving average.

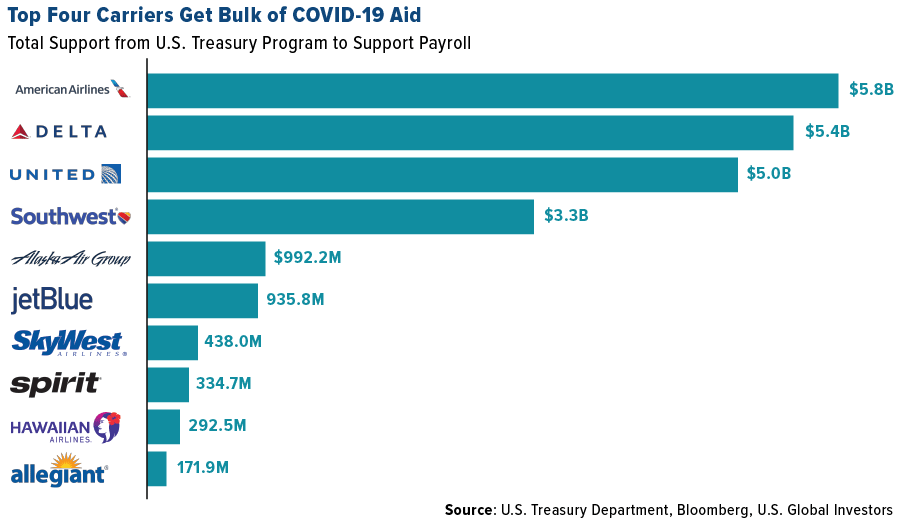

- According to government figures, the bulk of the $25 billion in aid for employees at passenger carriers went to the four biggest airlines: American, Delta, United and Southwest. Bloomberg notes that 90 other companies have received funds under the payroll aid program, including luxury charter carriers. As of May 29, none of the carriers had actually tapped into those funds. Bloomberg reports that the carriers plan to wait until fall and see how the summer travel season goes before deciding to take the government aid. This demonstrates optimism from carriers that travel demand could recover faster than expected.

Weaknesses

- Perhaps the biggest news for the airline industry in May was that legendary investor Warren Buffett sold all his positions in major U.S. carriers. Buffett’s Berkshire Hathaway announced in its annual meeting that sales of shares in Delta, Southwest, American and United made up most of the company’s $6.5 billion April equity sales. At the end of 2019, Buffet’s stakes in the big four carriers neared $10 billion, with greater than 10 percent ownership stakes in Delta and Southwest. “The airline business – and I may be wrong and I hope I’m wrong – but I think its changed in a very major way. The future is much less clear to me,” said Buffett.

- Airbus reported just nine net orders in the month of April and delivered only 14 jetliners. More and more airlines are conserving cash and delaying accepting new planes. Airbus already cut output targets for the year by a third. Rolls-Royce lowered its delivery target for wide-body plane engines by 44 percent for the year. Boeing, which was suffering long before the coronavirus erased travel demand, reported more than 300 cancelled orders so far in 2020.

- A Pakistan International Airlines flight with 99 people on board crashed into a residential neighborhood on May 22 after pilots reported losing power from both engines as the plane neared landing, reports Bloomberg. At least two passengers survived the crash and many on the ground were killed or injured. The flight was from Lahore to Karachi, Pakistan and was on a A320 narrow-body jet that entered service in 2004.

Opportunities

- Despite Buffett exiting the airline space, investors and traders are not deterred from investing in airlines, viewing it as an attractive buying opportunity. The U.S. Global Jets ETF (JETS), which invests in global airlines, airport operators and manufacturers, saw strong inflows even after the Buffett news was released. From May 1 to May 27, investors added $182.14 million to JETS – a sign that investors are betting on a travel turnaround.

- Private air travel could be making a comeback, according to Signature Aviation Plc. CEO Mark Johnstone said “encouragingly, we have seen some early signs of an improvement.” The company said flight activity that fell 77 percent in April from a year earlier was down only two-thirds in the first 13 days of May.

- Airlines are taking big precautions to help make passengers feel safe flying again. JetBlue was the first major carrier to require all employees and travelers to wear a face mask throughout the journey, and other carriers quickly followed suit. Delta is one of many leaving middle seats unoccupied to increase the distance between passengers. Airlines are also allowing passengers to reschedule their trips for free if a plane reaches a certain capacity level. Hopefully these measures, along with the falling number of COVID-19 infections, will get more people in the skies.

Threats

- The International Air Transport Association (IATA) warned that demand for flights will lag behind pre-coronavirus forecasts for at least five more years. Brian Pearce, the group’s chief economist said that global traffic will still be 10 percent below original estimates in 2025. The IATA doesn’t expect travel rebounding to 2019 levels until 2023 at the earliest.

- American Airlines and EasyJet both plan to cut management and staff by 30 percent. These are just a few of the carriers announcing massive job cuts to stem losses from drastically reduced travel. Delta Airlines is offering new retirement programs to entice workers to leave voluntarily as it anticipates a slow recovery in demand. Latam Airlines, the top South American carrier, has filed for bankruptcy and more carriers could be headed in the same direction soon. Boeing CEO Dave Calhoun said on NBC that the travel recovery is going to be slow and there is a risk that a major American airline could fail.

- U.S. and China tensions heated back up in May. China will allow chartered passenger flights from eight countries as it loosens restrictions on inbound travel, but the U.S. will not be included, reports Bloomberg. Although positive that China, and other countries, are easing coronavirus travel restrictions, this is negative for U.S. carriers in losing out on service to the populous nation.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.89 | +0.24 | +36.45% |

| Oil Futures | 39.10 | +3.61 | +10.17% |

| Hang Seng Composite Index | 3,569.02 | +247.44 | +7.45% |

| S&P Basic Materials | 375.02 | +26.64 | +7.65% |

| Korean KOSPI Index | 2,181.87 | +152.27 | +7.50% |

| S&P Energy | 336.52 | +44.93 | +15.41% |

| Nasdaq | 9,814.08 | +324.21 | +3.42% |

| DJIA | 27,110.98 | +1,727.87 | +6.81% |

| Russell 2000 | 1,507.15 | +113.12 | +8.11% |

| S&P 500 | 3,193.93 | +149.62 | +4.91% |

| Gold Futures | 1,687.70 | -64.00 | -3.65% |

| XAU | 114.87 | -5.23 | -4.35% |

| S&P/TSX VENTURE COMP IDX | 556.91 | +3.14 | +0.57% |

| S&P/TSX Global Gold Index | 303.78 | -24.83 | -7.56% |

| Natural Gas Futures | 1.80 | -0.05 | -2.49% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,181.87 | +324.79 | +17.49% |

| 10-Yr Treasury Bond | 0.89 | +0.19 | +26.56% |

| Gold Futures | 1,687.70 | -8.80 | -0.52% |

| S&P Basic Materials | 375.02 | +59.17 | +18.73% |

| S&P 500 | 3,193.93 | +345.51 | +12.13% |

| DJIA | 27,110.98 | +3,446.34 | +14.56% |

| Nasdaq | 9,814.08 | +959.69 | +10.84% |

| Oil Futures | 39.10 | +15.11 | +62.98% |

| Hang Seng Composite Index | 3,569.02 | +175.61 | +5.18% |

| S&P/TSX Global Gold Index | 303.78 | -42.63 | -12.31% |

| XAU | 114.87 | -3.02 | -2.56% |

| Russell 2000 | 1,507.15 | +244.15 | +19.33% |

| S&P Energy | 336.52 | +60.85 | +22.07% |

| S&P/TSX VENTURE COMP IDX | 556.91 | +78.09 | +16.31% |

| Natural Gas Futures | 1.80 | -0.14 | -7.25% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 114.87 | +10.17 | +9.71% |

| S&P/TSX Global Gold Index | 303.78 | +22.56 | +8.02% |

| Gold Futures | 1,687.70 | +12.20 | +0.73% |

| DJIA | 27,110.98 | +989.70 | +3.79% |

| S&P 500 | 3,193.93 | +169.99 | +5.62% |

| Nasdaq | 9,814.08 | +1,075.49 | +12.31% |

| Korean KOSPI Index | 2,181.87 | +96.61 | +4.63% |

| Natural Gas Futures | 1.80 | +0.03 | +1.75% |

| S&P Basic Materials | 375.02 | +30.97 | +9.00% |

| Russell 2000 | 1,507.15 | +28.33 | +1.92% |

| Oil Futures | 39.10 | -6.80 | -14.81% |

| Hang Seng Composite Index | 3,569.02 | -148.96 | -4.01% |

| S&P/TSX VENTURE COMP IDX | 556.91 | +35.64 | +6.84% |

| S&P Energy | 336.52 | -1.07 | -0.32% |

| 10-Yr Treasury Bond | 0.89 | -0.02 | -2.52% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2020):

American Airlines Group Inc

Delta Air Lines Inc

United Airlines Holdings Inc

Southwest Airlines Co

Alaska Air Group Inc

JetBlue Airways Corp

Spirit Airlines Inc

SkyWest Inc

Hawaiian Holdings Inc

Allegiant Travel Co

Airbus SE

CCC

TOTAL SA

Impala Platinum Holdings Ltd

MMC Norilsk Nickel PJSC

Polymetal International PLC

Resolute Mining Ltd

EOG Resources Inc

Gold Fields Ltd

Exore Resources Ltd

Pandora A/S

Red 5 Ltd

Ramelius Resources Ltd

Silvercorp Metals Inc

Argonaut Gold Inc

Gran Colombia Gold Corp

Dundee Precious Metals Inc

Roxgold Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Eurozone Markit Composite PMI reports on manufacturing and services are based on surveys of over 300 business executives in private sector manufacturing companies and also 300 private sector services companies. Standard and Poor’s 500 Airlines Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. Standard and Poor’s 500 Utilities Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 30, 1994. The Bloomberg Dollar Spot Index tracks the performance of a basket of ten leading global currencies versus the U.S. Dollar. Each currency in the basket and their weight is determined annually based on their share of international trade and FX liquidity. The BBDXY Index data starts from Dec 31, 2004 with a base level of 1000. The GTI Global Strength Indicator indicates whether the underlying entity is oversold or overbought. The indicator ranges from 0 to 100, the former indicating a high oversold condition.