Are Central Bank Digital Currencies the Future of Money?

Date Posted: April 23, 2021

Read time: 51 min

Some major changes could be coming soon to a central bank near you, with an estimated 90% of them at some stage of developing a central bank digital currency, or CBDC. In October 2020, the Bahamas became the first economy to introduce its own CBDC, the Sand Dollar, but many more national currencies are expected to be rolled out in the coming years.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Today we had the pleasure of participating in the (virtual) ringing of the NYSE closing bell to celebrate the six-year anniversary of the launch of our airlines ETF. It’s been an incredible journey, and we extend our gratitude to everyone who helped make it possible. Wheels up!

In case you missed it, you can watch the replay of the bell ringing by visiting nyse.com/bell!

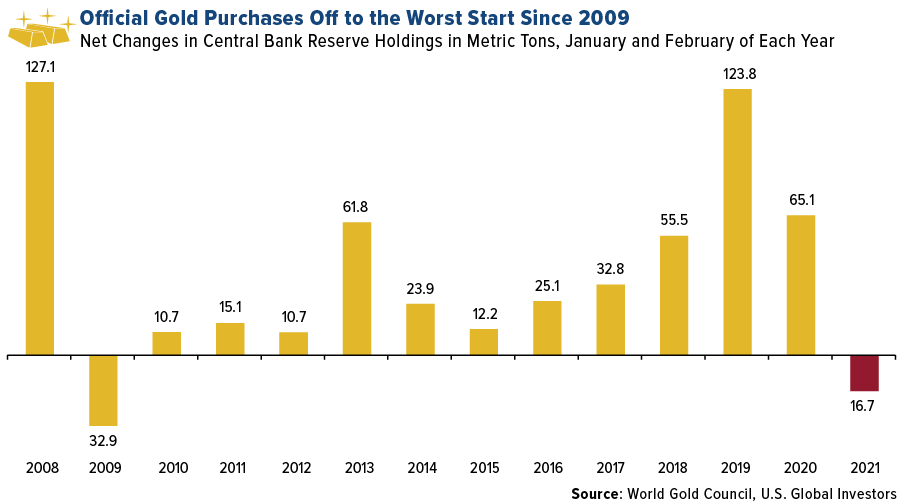

Central Banks Have Been Net Sellers of Gold So Far this Year

Some major changes could be coming soon to a central bank near you, with an estimated 90% of them at some stage of developing a central bank digital currency, or CBDC. In October 2020, the Bahamas became the first economy to introduce its own CBDC, the Sand Dollar, but many more national currencies are expected to be rolled out in the coming years.

I have much more to say on this, but first, let’s get an update on official gold purchases. Since 2010, central banks have been net buyers of the yellow metal as they seek to mitigate risk and hedge against their very own monetary decisions.

That being so, 2021 is off to a rough start in terms of official purchases. Central banks were net sellers in January and February for the first time in over a decade, unloading some 16.7 metric tons, according to the World Gold Council (WGC). This has contributed to gold’s poor performance so far this year, falling 6.5% through today. Turkey was the biggest seller, dumping 11.7 tons in February alone.

Not all central banks were sellers. India bought 11.2 tons in February, Uzbekistan 7.2 tons. Serbia has been accumulating gold every month since February 2019.

The Magyar Nemzeti Bank (MNB), the central bank of Hungary, announced earlier this month that it tripled its holdings from 31.5 metric tons to 94.5 tons, putting Hungary first among Central and Eastern European (CEE) countries in terms of gold reserves per capita.

“As it carries no credit or counterparty risks, gold facilitates reinforming trust in a country in all economic environments, which still renders it one of the most crucial reserve assets worldwide,” the bank wrote in a press release.

China to Allow Large Gold Imports

When it comes to gold policy, though, the big news is that China is now allowing domestic and international banks to import large amounts of the precious metal into the country in an effort to support prices. According to reporting by Reuters, an estimated 150 metric tons worth $8.5 billion will be shipped into China as soon as this month or next.

For the sake of comparison, in 2019 China imported around 75 tons per month, or $3.5 billion.

The country is already the world’s largest importer of the metal, so this is an important development that I believe could help the gold price stay buoyant.

Old Meets New: Will Cash Take the Digital Dive?

Besides holding gold—one of the oldest known assets, having been mined for over 5,000 years—many central banks are now on a path to introduce their own digital currencies, something our ancestors could never have conceived.

More than 60 central banks right now are believed to be exploring the idea of CBDCs, including retail tokens that would be used by citizens as well as wholesale applications for financial institutions. But first, what is a CBDC, and what isn’t it?

|

Simply put, CBDCs are digital payment instruments that, like traditional fiat currency, are issued by a central bank and denominated in the national unit of account. The hope is that they will allow for safe and secure transactions and provide a transparent audit trail while also featuring a level of confidentiality.

Another benefit? No more having to break bills. Many people have shied away from using dirty paper cash during the pandemic, but in years past, Americans would lose some $62 million every year in loose change.

For now, CBDCs appear to be designed not to replace traditional cash but to supplement it. Nor do they seem to threaten the growing popularity of cryptocurrencies such as Bitcoin, whose price is far too volatile to be used as an everyday medium of exchange. Last week, Federal Reserve Bank of Dallas President Robert Kaplan called Bitcoin a “store of value,” like gold, rather than a currency.

Having said that, many merchants now accept Bitcoin as payment, the most notable, perhaps, being Tesla. Visa and PayPal already let customers use cryptos to settle transactions, and this week, PayPal-owned Venmo said it will permit crypto trading. Miami mayor Francis Suarez wants to allow residents to pay their taxes in Bitcoin.

Some central banks are ahead of others in launching a CBDC. Like I said, the Bahamas has the Sand Dollar, while Cambodia has the Bakong. Gold-loving China has reportedly been working on a digital yuan since 2014, and recently it doled out millions of dollars’ worth of the prototype currency to people in Shenzhen and other cities to test drive. Meanwhile, Britain’s Treasury and the Bank of England (BOE) announced this week the creation of a taskforce to look into what some people are calling the “britcoin.”

No Cash, No Problem

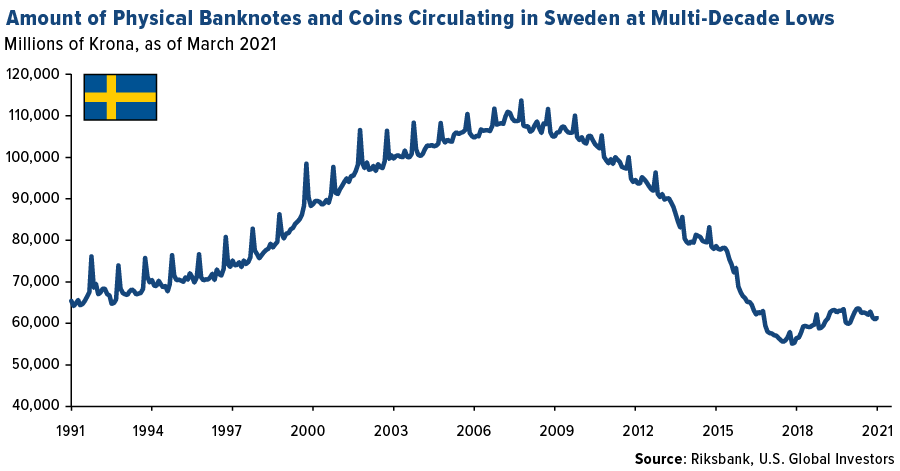

Transitioning to digital currencies is easier when the country already has a history of preferring online payments to paper cash. Take Sweden and Norway, two of the most cashless societies. Both Nordic countries are currently working on their own CBDCs.

As some of you may know, Sweden was the world’s first country, in 1666, to issue paper money. Today, it’s set to become one of the first to introduce a digital token, the e-krona, possibly as early as November 2022. The move follows years of declines in the amount of banknotes and coins circulating in the Swedish economy. Only around 6% of transactions are believed to be made using physical cash.

In neighboring Norway, that figure is even lower at between 3% and 4%. In a press release published yesterday, the Norges Bank says it plans to “test technical solutions for a central bank digital currency (CBDC) over the next two years.”

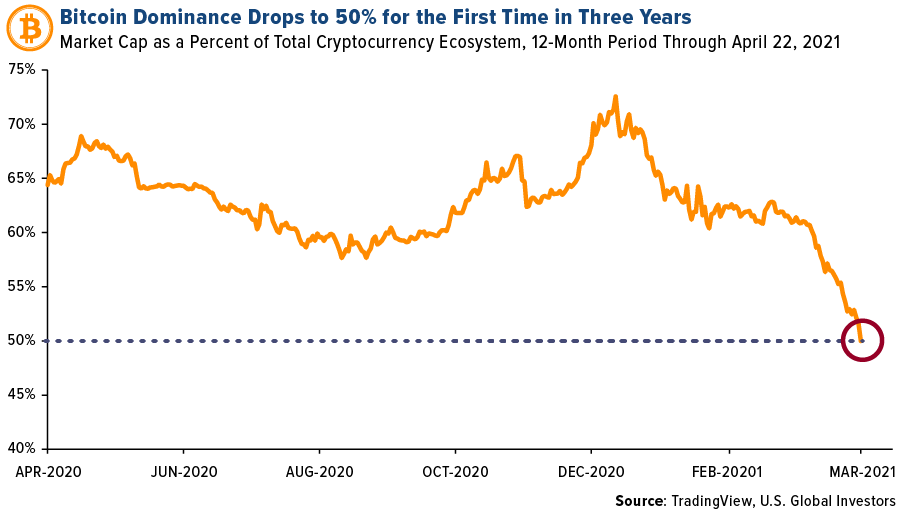

Bitcoin Dominance Drops, Opening the Door to Other Cryptos

Again, CBDCs are not expected to compete with cryptos such as Bitcoin, which is taking its place as a tradeable asset like gold.

The world’s largest cryptocurrency is well off its all-time high, dipping below $50,000 today for the first time since early March in response to news that President Joe Biden is expected to propose a hike in the capital gains tax to as high as 43.4%. Investors clearly had some feelings about this proposal: Stocks fell close to 1% on Thursday.

In any case, Bitcoin’s weakness could very well be other cryptos’ boon. For the first time in three years, its market cap as a percent of the total cryptocurrency ecosystem dropped to 50% this week as its price slid. When this has happened in the past, according to Cointelegraph, other coins have moved in to pick up the slack, with gains led by Ether. Indeed, Ether hit a new all-time high of $2,583 yesterday as analysts predict further advances on a scheduled drop in supply.

April 22, 2021Airline Industry Highs and Lows: First Quarter 2021 |

April 19, 2021Manufacturers Expand at Fastest Pace in 50 Years… |

April 14, 2021Top 10 Countries with the Largest Shipping Fleets |

|||

Gold Market

This week spot gold closed the week at $1,777.20, up $0.69 per ounce, or 0.04%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.14%. The S&P/TSX Venture Index came in off 1.65%. The U.S. Trade-Weighted Dollar fell 0.79%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-22 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Apr-22 | Initial Jobless Claims | 610k | 547k | 586k |

| Apr-23 | New Homes Sales | 885k | 1021k | 846k |

| Apr-26 | Durable Goods Orders | 2.5% | — | -1.2% |

| Apr-27 | Hong Kontg Exports YoY | 15.0% | — | 30.4% |

| Apr-27 | Conf. Board Consumer Confidence | 112.0 | — | 109.7 |

| Apr-28 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Apr-29 | Germany CPI YoY | 1.9% | — | 1.7% |

| Apr-29 | Initial Jobless Claims | 550k | — | 547k |

| Apr-29 | GDP Annualized QoQ | 6.5% | — | 4.3% |

| Apr-30 | Eurozone CPI Core YoY | 0.8% | — | 0.9% |

Strengths

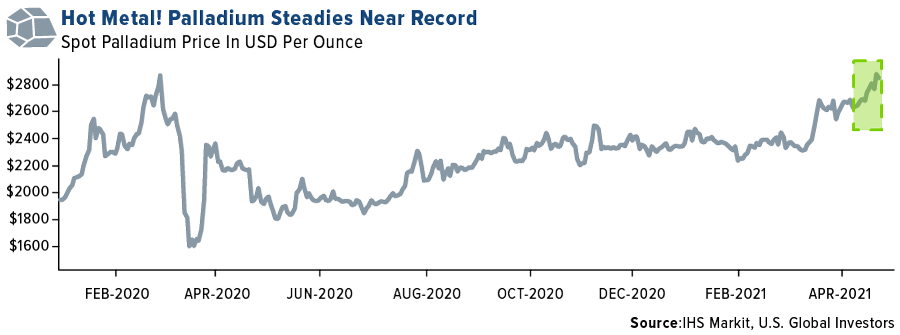

- The best performing precious metal for the week was palladium, up 3.01%. Gold rose above its 50-day moving average on Monday as the 10-year Treasury yield and U.S. dollar trended lower. Bullion hit a seven-week high of $1,785 an ounce.

- Palladium rose as much as 4.8% on Wednesday to $2,895.96 an ounce – a new record high. The metal is up more than 17% so far this year. Palladium is used in catalytic converters to cut emissions in gas vehicles and the market has been in a production deficit for several years.

- De Grey Mining shares finished Friday’s trading session up 20.22% on reporting strong mineralization with visible gold in the core from the McLeod lode of the Crow zones within the Hemi Gold Discovery in Western Australia.

Weaknesses

- The worst performing precious metal for the week was gold, still up slightly by just 0.04%. Interesting to note that in recent weeks every precious metal has finished with positive week over week gains. Gold fell the most in a week on Thursday morning after better-than-expected U.S. jobs data. Initial jobless claims decreased to 547,000 in the week ended April 17, according to the Labor Department, marking a new pandemic low.

- PT Archi Indonesia has postponed its planned IPO of as much as $500 million due to weak gold prices and falling stocks, reports Bloomberg. The gold miner is a unit of conglomerate Rajawali Group and would have been the biggest Indonesian IPO since 2011. Gold is down 14% from its record high in August and the Jakarta Stock Exchange Composite Index is down 7% from a three-year high in January.

- Central bank gold purchases are off to the worst start to the year since 2009. According to the World Gold Council, net changes in central bank reserve holdings for January and February were negative 16.7 metric tons. This is compared to 65.1 tons for the same period a year earlier.

Opportunities

- India’s gold imports from Switzerland rose to the highest in nearly eight years last month, a strong sign that Asian consumer demand has returned. India, the world’s number two consumer, imported 82.6 tons from Switzerland in March. “These latest numbers certainly demonstrate the degree of pent-up demand in the country after the implosion in 2020,” Rhona O’Connell, an analyst at StoneX, wrote in a note. China’s gold imports also surged in March to 38,584 kilograms, according to data from General Administration of Customs. The figure is the highest since January 2020 and up from just 6,272 kilograms in February.

- Sandvik, a mining equipment, machine tooling and materials technology company, said order intake rose organically in the first quarter by 12% to $2.97 billion. CEO Stefan Widing said demand was driven by strong momentum in mining and continued improvement in short-cycle business. Kitco News notes mining accounts for 40% of the company’s revenues.

- Palladium approached all-time highs again this past week. Auto demand is picking up with lockdowns being relaxed across the U.S, but palladium is facing its 10th successive year of supply falling short of demand, thus the positive market dynamics that could keep palladium in the spotlight longer than anticipated. In addition, there are only a limited number of miners with exposure to PGM deposits.

Threats

- Newcrest Mining CEO Sandeep Biswas said in a media briefing this week that although there is likely to be further consolidation in the gold industry, current valuations make it a tough market to find compelling targets. “At the moment, with valuations where they are, it’s going to be very hard to get the sort of returns you’re after,” Biswas said. “You’d be talking single-digit IRRs (investment rates of return), whereas typically we look at double-digit IRRs as a target for ourselves.”

- Canadian miner Alamos Gold is pursuing a $1 billion claim against Turkey for preventing a mining project from moving forward, according to a company press release. The company will file an investment treaty claim against the country for “expropriation and unfair and inequitable treatment” concerning its Kirazli gold mine. The Turkish government did not renew mining licenses for the project in October 2019 and a year later cancelled a forestry permit. Alamos has operated for a decade in Turkey and expects to take a $215 million impairment charge in the second quarter.

- China, one of the main drivers of copper prices could fade. The government is reducing its construction stimulus, which is generally negative for materials. There appears to be an absence of government buying right now. Output from South American mines is increasing as vaccines are rolled out.

Index Summary

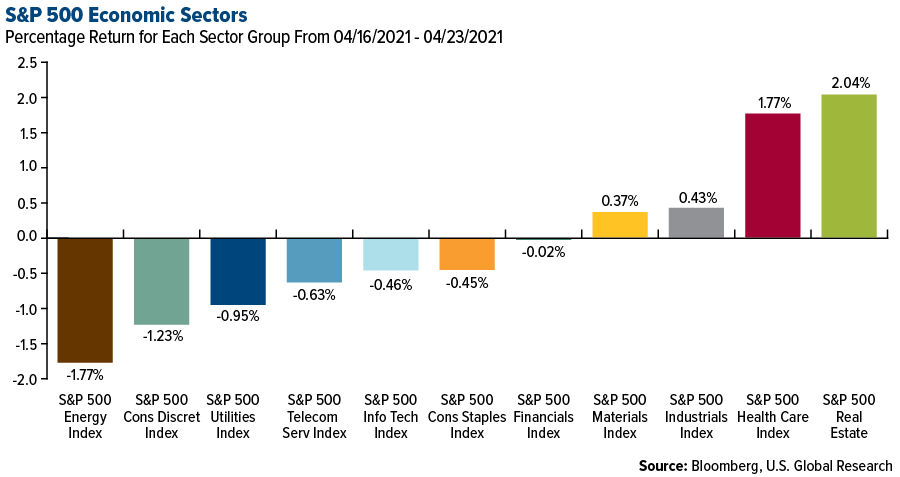

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.46%. The S&P 500 Stock Index fell 0.13%, while the Nasdaq Composite fell 0.25%. The Russell 2000 small capitalization index gained 0.55% this week.

- The Hang Seng Composite gained 1.04% this week; while Taiwan was up 0.82% and the KOSPI fell 0.39%.

- The 10-year Treasury bond yield fell 2 basis points to 1.555%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Solana, rising 34.16%.

- The U.S. House of Representatives passed the Eliminate Barriers to Innovation Act of 2021, which seeks to set up a digital asset working group with representatives from the Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC). The purpose of the group, as per the legislation, is to ensure collaboration between regulators and the private sector, to foster innovation. The goal of the legislation is to seek clarification when the SEC has jurisdiction over digital assets, in the case when they are deemed securities and when the CFTC has jurisdiction, when the digital assets are classified as commodities.

- Grayscale Investments, the world’s largest digital asset manager, reported that it acquired approximately $1 billion in cryptocurrencies in a 24-hour period. Grayscale’s assets under management rose from $44.9 billion to $45.8 billion this week, including increases of $283.3 million and $586.5 million to its Grayscale Bitcoin Trust (GBTC) and Grayscale Ethereum Trust (ETHE), respectively. Meanwhile, Ethereum’s native cryptocurrency ether (ETH) rallied to new all-time highs this week, reaching a record $2,644.04 per token.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Curve DAO Token, down 38.58%.

- Turkish crypto exchange Thodex has come under scrutiny this week as the exchange halted all transactions, stating on its website that it is evaluating an unspecified partnership offer and that the process would take about 4-5 business days. Thodex, before shutting down, had a trading volume of $585 million in cryptocurrencies. Although the exchange’s website says that there is no cause for concern and that the negative news on the internet is not true, Thodex’s executives are deactivating their social media profiles and the platform’s customer support group is unresponsive.

- Bitcoin, which is currently trading below $50,000, showed technical signals of slowing down after it dropped below its 50-day moving average for the first time this year. By the end of this week, it had also slipped below its 100-day moving average. This week’s decline of almost 20% was kicked off last Saturday with $10 billion in long future liquidations and a reduction in the network’s hashrate capacity, which also sent Bitcoin transaction fees to 2018 highs. This short-term bearish sentiment was reflected in Scott Minerd’s, Guggenheim’s CIO, latest interview where he mentioned that the cryptocurrency could fall back to the $20,000 to $30,000 range due to current frothy market conditions, but still remains bullish in the long-term.

Opportunities

- Huobi Technology Holdings, which is a part of Huobi Group, announced that it has launched four digital currency funds targeting $100 million in assets under management by September 2021. The company reported that it has already secured $50 million in commitments across all its proposed funds. Huobi’s funds include a private equity fund that invests in private crypto mining companies, an active fund that invests in a basket of digital assets, and two funds that will invest directly in Bitcoin and Ethereum.

- 3iQ Corp., the Canadian digital asset manager, and investment firm CoinShares launched an ether exchange-traded fund (ETF), which started trading on the Toronto Stock Exchange (TSX) this week. The ETF, called the 3iQ CoinShares Ether ETF, is trading under the ticker ETHQ and will give investors exposure to the daily price movements of ether, Ethereum’s native token, and the opportunity for long-term capital appreciation.

- 21Shares AG, the Switzerland-based investment products provider, announced that it is launching exchange-traded products (ETPs) for the native cryptocurrencies of Stellar and Cardano. The company reported that the Stellar XLM ETP and the Cardano ADA ETP will start trading on the Swiss SIX Exchange on April 26, under the tickers AXLM and AADA respectively. 21Shares said that it is responding to surging customer interest in Stellar and Cardano and has decided to remove Bitcoin Cash and Ripple ETPs from its 21Shares HODL basket ETP.

Threats

- European and British regulators are studying cryptocurrency exchange Binance’s digital stock tokens over its possible non-compliance with securities laws. The zero-commission tokens allow its users to buy fractions of companies’ shares – currently Tesla and Coinbase—and qualifies token holders for returns including dividends. Binance reported that such transactions can only be settled by Binance USD (BUSD), a U.S. dollar stablecoin issued by the exchange. Regulators are arguing that the tokens may not provide sufficiently transparent corporate disclosures, specifically an investment prospectus, and that would be required if the tokens were judged to be securities. Binance claims that the tokens are an official CM-Equity AG product, which is compliant with the European Union’s market rules and banking regulations. Experts are also concerned about the ambiguity over whether Binance itself presents the tokens as securities or derivatives.

- Three of the largest Chinese Bitcoin mining hubs—Xinjiang, Inner Mongolia, and Sichuan—are facing regulatory clampdown which could put a big dent in the global hashrate production, which is the computing power to mine bitcoin. China contributes over 65% of the world’s total hashrate, and heavy scrutiny of coal mines in Xinjiang, new regulations on high energy-consuming companies in Inner Mongolia and the end of a local energy policy in Sichuan have unnerved bitcoin miners in the country. An accident at a coal mine in Xinjiang left 21 miners trapped and prompted the region’s government to suspend operations and conduct an inspection of other coal mines in the region. This suspension plunged bitcoin mining power by 30% and pushed bitcoin transaction fees to a record high. Furthermore, China’s highest economic planning agency, the National Development and Reform Commission (NDRC) has decided to shut down and eliminate all crypto mining operations in Inner Mongolia by the end of April.

- Nassim Taleb, a former risk analyst and author, believes that Bitcoin is not a hedge against inflation as there is no connection between the pair. In an interview, he mentioned that you can have hyperinflation and Bitcoin going to zero, and that earlier this year that he sold off his Bitcoin holding due to its volatility, explaining that his stance was based on Bitcoin as a currency and not as a store of value.

Domestic Economy and Equities

Strengths

- Worker filings for jobless benefits declined to 547,000 last week, a new pandemic low that adds to evidence of a strengthening labor market and overall economic recovery. Initial unemployment claims, a proxy for layoffs, fell 39,000 last week from an upwardly revised 586,000 the prior week, the Labor Department said on Thursday.

- The index of U.S. leading economic indicators rose 1.3% in March, the Conference Board said Thursday. All 10 components of the index were positive, suggesting economic momentum in the near term, said Ataman Ozyildirim, senior director of economic research at the Conference Board.

- Equifax was the best performing S&P 500 stock for the week, increasing 20.28%. The company’s shares jumped to a record high after reporting better than expected first quarter earnings and raising its 2021 guidance for revenue and earnings.

Weaknesses

- U.S. home sales fell to a seven-month low in March, pulled down by an acute shortage of properties, which is boosting prices and making owning a house more expensive for some first-time buyers. Existing home sales dropped 3.7% to a seasonally adjusted annual rate of 6.01 million units last month, the lowest level since August 2020, the National Association of Realtors said on Thursday.

- The winter freeze that sent gas and power prices skyrocketing across Texas in February is providing a warning to cities about the risks of global warming: The cost of some extreme weather events can stick around for years. The municipal market generally shrugs off natural disasters because they are usually offset by an influx of federal aid. But the electricity meltdown in the Lone Star State has left cities and local utilities with massive power bills. “What happened in Texas will increase the scrutiny and the awareness of what climate risk means,” said Daniel Rabasco, head of municipal bonds at Mellon Investments. “It’s a wakeup call in terms of the severity of what a climate change impact could be.” The February storm knocked out almost half the state’s electric generating capacity, sending wholesale electricity prices to $9,000 a megawatt-hour and leaving millions without power for days.

- Penn National Gaming was the worst performing S&P 500 stock for the week, decreasing 10.21%. There’s been some concern surrounding the Barstool acquisition and whether it can live up to the hype.

Opportunities

- Blackstone announced record quarterly earnings of $1.75 billion, driven by a strategy of investing in fast-growing companies, which helped push its market capitalization above $100 billion for the first time. The private-equity firm, with $649 billion in assets under management, is the first of its peers to cross that threshold. Analysts say it may also be the first to be included in the S&P 500, a move which could come later this year.

- Silicon Laboratories shares jumped as much as 12% on Friday, after the company agreed to sell its Infrastructure & Automotive business to Skyworks Solutions. Analysts were positive on the news, with KeyBanc upgrading the stock. According to KeyBanc’s analyst, the deal turns Silicon Labs into a pure play internet-of-things company, allowing it to accelerate long-term growth.

- Imax was upgraded to outperform from neutral at Wedbush, which wrote that the large-screen movie-theater company should see strong demand as the economy reopens. “Pent up demand for out-of-home entertainment drove outsized market share for Imax in China, Japan, and elsewhere in Asia over the last several months,” and there should be a similar trend as North America and Europe reopen, the firm wrote.

Threats

- Morgan Stanley downgraded Harley-Davidson to underweight from equal weight, citing several challenges ahead. “We don’t believe investors are focused on the potential headwinds that are around the corner, stemming from electrification, new competition, a potential 200 basis points impact from higher European Union tariffs and an industry in secular decline,” analyst Billy Kovanis writes. Furthermore, the motorcycle industry has not been able to attract the younger generation to riding; their idea of “freedom” has shifted to traveling, from hopping on a motorcycle, he says.

- Piper Sandler stepped away from its bullish stance on Kraft Heinz, citing both cost inflation and the steady march higher of the packaged food giant’s share price since September. “Inflation is hitting many commodity inputs (and freight and even labor) broadly,” analyst Michael Lavery wrote.

- Bank of America’s Derek Hewett downgraded Rocket to neutral from buy, citing expectations for margin pressure stemming from a “less favorable interest rate backdrop and increased competitive intensity.” Most companies in the mortgage finance space should report “solid” first-quarter results, but the outlook for the rest of 2021 is “more challenging,” the analyst writes. The firm’s economists expect benchmark rates to rise this year and into 2022.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was corn, up 10.68%. Corn extended its rise to the highest in almost eight years, leading a rally in crop futures on bets that Chinese demand will increase, rebounding economies throughout the world and adverse weather, which is expected to leave silos depleted.

- Premiums on shipping aluminum to the U.S. Midwest touched record highs, driven by a jump in demand and shipping costs, and a tariff holdover from the Trump administration. Prices to deliver aluminum touched a high of 25.6 cents per pound, surpassing the 24.5 cents per pound it hit in February 2015. Aluminum’s price in London is up almost 20% this year, in its best start since 2008, buoyed by a global economic recovery that is expected to fuel purchases and China, the metal’s biggest producer, deciding to rein in output in a bid to cut emissions.

- Commodities are steadily gaining despite the worsening COVID-19 outbreaks in nations like India. The Bloomberg Commodity Spot Index, which tracks the futures price movement of commodities, just hit the highest since 2013, driven by strength across the board: copper closing in on its 2011 high; increased demand for agricultural goods; optimism about travel and recovery of oil demand. If commodities gain during the second quarter of 2021, it will mark a fifth consecutive quarter of gains and would be the best run since 2008.

Weaknesses

- The worst performing commodity for the week was nickel, down 1.84%. Nickel slipped on the futures market after participants offloaded their positions amid weak demand in the spot market.

- Oil is headed for another weekly decline as COVID-19 cases continue to rise in countries like India, tempering optimistic economic data coming out of U.S. and Europe. In India, diesel and gasoline consumption is set to fall by a fifth this month, and traders said that the nation’s largest refiner had refrained from buying West African oil this week, defying their expectations. Meanwhile, the Japanese government has declared a state of emergency a few weeks before the Olympics as Covid-19 cases are increasing. U.S. benchmark crude oil is set for a roughly 2% decline this week.

- Europe, which is home to some of the most sought-after companies involved in renewable energy, is seeing its renewable energy index lagging the wider market. In 2020, the European Renewable Energy Index (ERIXP) gained 92% and is currently witnessing a correction. The gauge has fallen 25% since its January peak, with investors being put off by stretched valuations and rising bond yields. The chart below compares the returns of the Stoxx 600 Europe Index and the ERIXP.

Opportunities

- China’s top copper smelter, Jiangxi Copper Co., expects the metal to hit $10,000 per metric ton. The company’s vice general manager said at an industry conference that the market fundamentals are favoring the increase in price for copper but did not give a time frame. Currently, copper is nearing its 2011 high buoyed by the optimism about growth, spending on green infrastructure and a weaker dollar. Jiangxi’s price target of $10,000 is below the forecast set by Goldman Sachs, Citigroup and Trafigura Group for copper. Although inventories monitored by the London Metal Exchange have doubled since February and stockpiles on the Shanghai Futures Exchange are at an 11-month high, copper bulls expect demand to roar throughout the decade as countries push to decarbonize their existing infrastructure.

- Canadian Imperial Bank of Commerce (CIBC) announced that it is forming a global energy, infrastructure, and transition group within its investment-banking division. The bank expects the group to break down silos between the different teams and provide clients with the broader package of services that are necessary for their energy transition. Roman Dubczak, CIBC’s head of global investment banking, said that this is a natural evolution of the sector and that the bank must shape its business to meet its clients’ objectives and to do so, cross-collaboration and exchange of ideas across teams will be vital.

- U.S. President Joe Biden’s climate summit saw environmental pledges from countries across the globe, sending renewable energy stocks rising around the Asian markets. China announced plans to cut usage of coal through this decade, Japan pledged to achieve a stricter emission target by 2030 and South Korea has decided to halt state-backed financing of coal-fired power plants. Biden announced that he is committed to halve greenhouse emissions by 2030 and double climate aid to developing countries, while China’s President Xi Jinping reiterated the nation’s goal to become carbon neutral by 2060. Shares of companies tied to solar and wind energy rose this week in Asia, while those of coal miners dropped significantly.

Threats

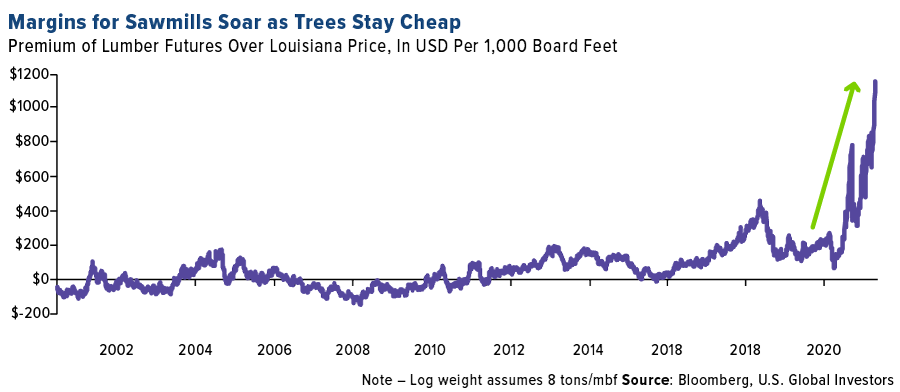

- The U.S. lumber market is facing shortages while the price of lumber products is on the rise. Analysts report that for the first time in recent memory, a lumberyard was the one selling wood to a supplier, pushing the product back up the supply chain and threatening to push wood prices higher. Normally, a wholesale distributor buys lumber from sawmills and sells that to the yards, which in turn sell the product to homebuilders. The premium of lumber futures over the Louisiana price has surged to record level due to an excess demand from consumers who are renovating their homes and buying bigger ones.

- Procter & Gamble Co. (P&G) announced that it is raising the prices of certain consumer products as it battles with higher commodity costs. While reporting its third-quarter earnings, P&G said that with manufacturing expenses climbing, it is set to increase prices of products in the baby care, feminine care and adult incontinence categories starting September. The increase is expected to be in the mid to high-single digit percentages. The company’s Chief Operating Officer Jon Moeller cited higher pulp and oil-related prices as a factor and that across the board, this is one of the bigger increases in commodity costs the company has ever seen.

- Natural Gas is falling out of favor with emissions-wary investors at a quicker pace than coal did, and that is catching some power generators unsuspecting and potentially leaving them stuck with billions of dollars of assets they cannot sell. Executives at European energy companies are reporting that they are already struggling to offload their gas-fired facilities, as cost of renewables has dropped drastically during the past decade and has made gas-fired stations less competitive. Europe plans on reaching net-zero emissions by 2050, which is at odds with plans to build numerous infrastructure projects like pipelines and terminals. Global Energy Monitor, a non-governmental organization that catalogs worldwide fossil fuel projects and share information in support of clean energy, estimates that there is a potential $104 billion stranded-asset risk if these projects are built but no longer needed.

Airline Sector

Strengths

- The best performing airline stock for the week was Avianca, up 10.2%. This week Southwest reported quarterly earnings 7% higher than expectations and revenues in March 5% higher than expectations. Due to increased demand, the airline is also adding flights in June.

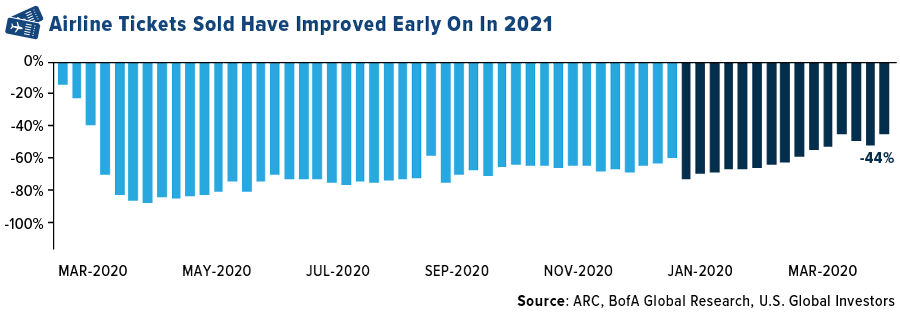

- Ticket sales, a primary indicator for future travel, showed sharp improvement early in 2021, reports Bank of America (BofA). Website visits are down only 22% versus year-ago levels and are showing continued improvement. According to BofA, ticket sales are down only 38% versus a year ago. The source of the surge is leisure bookings, which are down only 5% from year-ago levels. Alaska Airlines, in its recent quarterly report, guided second-quarter revenues to be down 32-37%, versus down 58% in the first quarter.

- Capacity is continuing to increase, illustrating a return to normal. Capacity has shown sequential growth of 5-6% from March to May, according to Stifel. American Airlines, in its most recent quarterly earnings release, indicated that capacity would be down 20-25% in the second quarter, as opposed to a consensus of down 53%.

Weaknesses

- The worst performing airline stock for the week was Singapore Airlines, down 6.9% as the company indicated that it may increase capital further in 2021. In addition, the French government indicated that it would not increase its stake in the carrier. United Airlines reported a quarterly loss of $(7.50) with revenues down 66%, worse than expectations. Cash burn was about $9 million per day, and the airline still has liquidity of $21 billion.

- Mesa Air reported March operating results this week as well, and they were below expectations. Block hours, which is the time from the moment an aircraft door closes at departure of a revenue flight until the moment the aircraft door opens, were 3% below consensus. Some of this can be explained by nearly 3,000 block hours being cancelled due to adverse weather. Estimates are being reduced for the second quarter due to an underlying slowdown in block hours.

- Recent air travel demand by geography is indicating that demand has moderated in the South and Midwest, likely due to increasing COVID cases in these regions. Strength remains, however, in the East and West.

Opportunities

- According to ISI, the airline industry is showing signs of future improvement. They indicated that their airline ratings survey rose from a 22.5 to 23.8 and has been increasing over the past two months to the highest reading since March 2020. The group also indicated that vaccinations are continuing, which is critical for reopening. In fact, 39% of citizens have received one dose, with 51% of adults and 82% of people 65 and older having received one dose.

- European bookings are indicating that there may be an airline recovery continuing into the summer. The European Union is working on a digital green certificate that would allow citizens of the EU to travel freely. EasyJet is ramping up capacity for the summer, and Ryanair is expecting very little restrictions on EU travel in June.

- Bank of America did a global travel survey which for the first time indicated a more optimistic tone from business travelers. It indicated that business travel could return to normal over time with 40% taking their first business trip in 2021. Nearly 40% of respondents could make their first international trip in 2022. In Europe, two-thirds or people expect to travel by plane this year, and 72% expect to travel for business this year.

Threats

- According to UBS, global travel restrictions continue to affect 83% of routes as of April 6. This study is rather exhaustive and covers 247 countries and 60,000 travel routes. Nearly 93% of routes in the G20 have some kind of restriction and almost 100% of intra-EU routes have some form of restriction too.

- Long-haul international travel has not shown significant improvement. Delta has said that long-haul demand has only recovered to 15-25% of normal. It does not expect significant improvement in trans-Atlantic and South American travel until late 2021, and trans-Pacific travel until late 2022.

- Stifel has developed a proprietary air travel demand model that is a leading indicator of passenger traveler counts. Passenger traveler count is expected to be down 43% year-over-year based on the most recent data, and this is 5% lower year-over-year than recent readings. This is likely due to the end of summer travel. Leisure passenger counts are at 80% of normal levels.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 55 basis points. The best performing country in Asia this week was China, gaining 1.8%.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 70 basis points.The Taiwanese dollar was the best performing currency in Asia this week, gaining 60 basis points.

- Eurozone’s preliminary PMIs improved in April. The service PMI crossed above the 50 level that separates growth from contraction. Manufacturing PMI strengthened to 63.3, while composite PMI, that combines service and manufacturing, moved up to 53.7 versus an expected 52.9.

Weaknesses

- The worst performing country in emerging Europe for the week was Turkey, losing 4.4%. The worst performing country in Asia this week was India, losing 2.5%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 3.5 %. The Thailand baht was the worst performing currency in Asia, losing 80 basis points.

- On Friday, India reported 332,730 new daily COVID cases, with more than 16 million in total. It is the second worst affected nation in the world currently, lagging only the United States. But while the U.S. caseload is twice as high, the death rate is much lower. India is struggling with a second wave of the virus, raising more fears about its overwhelmed health care system.

Opportunities

- Greece announced fiscal measures and cut the corporate tax rate to 22% from 24%. The country will allow restaurants to reopen (for outside seating only) starting May 3, and schools will reopen May 10. Greece will benefit from stronger tourism this year compared to the prior year. Wood & Company, an emerging Europe broker, is recommending overweighting the Greek market.

- The travel sector received a boost in Europe amid news that COVID passports will be made available this summer. Telegraph reported that the travel industry has been told by the U.K. that government passports will be made available to prove people have been fully vaccinated as early as next month. It said the Department for Transport wants an official certification scheme that gives British travelers a document they can show at borders overseas in place by May 17. Many countries in Europe are open to the idea to pass the quarantine for passengers fully vaccinated.

- Thailand aims to sell only zero-emission vehicles in the country by 2035, reports Bloomberg, planning to substantially expand its electric car production. The automotive industry is one of Thailand’s most important sectors. It contributes to about 10% of the economy, employs 850,000 workers, and supports industries from iron and steel to petrochemicals and plastic. Thailand sets a target to have electric vehicles account for 50% of all new car registrations by the end of the decade, up from 30%previously.

Threats

- Looking at China’s quarter-over-quarter gross domestic product (GDP) growth, the first three-months of this year recorded the slowest GDP growth in a decade. The stable growth over the past 10 years may be over and the Asian nation’s economy could slow down.

- Turkey’s relationship with the U.S. may deteriorate from here. Reportedly, U.S. President Biden is to recognize mass killings of Armenians in 1915 as a genocide. This is likely to trigger harsh reaction from the Turkish government. The Turkish lira was the wort performing currency this week among its European peers and if the U.S. administration goes ahead with the move, the lira may sink even further. The announcement is expected tomorrow.

- Bloomberg reported that U.S. Congress is moving with increasing urgency on bipartisan legislation to confront China and bolster U.S. competitiveness in technology and critical manufacturing. The U.S. Senate Foreign Relations Committee voted 21-1 to approve a bill aimed at China on several fronts.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.56 | -0.03 | -1.71% |

| Oil Futures | 62.13 | -1.00 | -1.58% |

| Hang Seng Composite Index | 4,575.00 | +46.88 | +1.04% |

| S&P Basic Materials | 520.87 | +1.93 | +0.37% |

| Korean KOSPI Index | 3,186.10 | -12.52 | -0.39% |

| S&P Energy | 358.74 | -6.45 | -1.77% |

| Nasdaq | 14,016.81 | -35.53 | -0.25% |

| DJIA | 34,043.49 | -157.18 | -0.46% |

| Russell 2000 | 2,275.04 | +12.37 | +0.55% |

| S&P 500 | 4,180.05 | -5.42 | -0.13% |

| Gold Futures | 1,776.20 | -4.00 | -0.22% |

| XAU | 148.53 | -0.63 | -0.42% |

| S&P/TSX VENTURE COMP IDX | 930.63 | -13.83 | -1.46% |

| S&P/TSX Global Gold Index | 312.86 | +0.24 | +0.08% |

| Natural Gas Futures | 2.72 | +0.04 | +1.64% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,186.10 | +189.75 | +6.33% |

| 10-Yr Treasury Bond | 1.56 | -0.05 | -3.42% |

| Gold Futures | 1,776.20 | +40.70 | +2.35% |

| S&P Basic Materials | 520.87 | +39.29 | +8.16% |

| S&P 500 | 4,180.05 | +290.91 | +7.48% |

| DJIA | 34,043.49 | +1,623.43 | +5.01% |

| Nasdaq | 14,016.81 | +1,054.92 | +8.14% |

| Oil Futures | 62.13 | +0.95 | +1.55% |

| Hang Seng Composite Index | 4,575.00 | +209.95 | +4.81% |

| S&P/TSX Global Gold Index | 312.86 | +29.68 | +10.48% |

| XAU | 148.53 | +14.83 | +11.09% |

| Russell 2000 | 2,275.04 | +140.78 | +6.60% |

| S&P Energy | 358.74 | -11.77 | -3.18% |

| S&P/TSX VENTURE COMP IDX | 930.63 | -15.88 | -1.68% |

| Natural Gas Futures | 2.72 | +0.21 | +8.18% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 148.53 | +7.29 | +5.16% |

| S&P/TSX Global Gold Index | 312.86 | +0.58 | +0.19% |

| Gold Futures | 1,776.20 | -95.60 | -5.11% |

| DJIA | 34,043.49 | +2,867.48 | +9.20% |

| S&P 500 | 4,180.05 | +326.98 | +8.49% |

| Nasdaq | 14,016.81 | +485.89 | +3.59% |

| Korean KOSPI Index | 3,186.10 | +25.26 | +0.80% |

| Natural Gas Futures | 2.72 | +0.23 | +9.35% |

| S&P Basic Materials | 520.87 | +50.44 | +10.72% |

| Russell 2000 | 2,275.04 | +133.62 | +6.24% |

| Oil Futures | 62.13 | +9.00 | +16.94% |

| Hang Seng Composite Index | 4,575.00 | -202.88 | -4.25% |

| S&P/TSX VENTURE COMP IDX | 930.63 | -8.58 | -0.91% |

| S&P Energy | 358.74 | +39.62 | +12.42% |

| 10-Yr Treasury Bond | 1.56 | +0.45 | +40.47% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2021):

Southwest Airlines

American Airlines

United Airlines

Mesa Air Group

Ryanair

Delta Air Lines

Tesla Inc.

Visa Inc.

De Grey Mining Ltd.

The Blackstone Group Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Jakarta Stock Price Index is a major stock market index which tracks the performance of all companies listed on the Indonesia Stock Exchange.

The Bloomberg Commodity Total Return index is composed of futures contracts and reflects the returns on a fully collateralized investment in the BCOM.

The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd.

The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables.

The ERIX index selects the largest companies in the areas of renewable energy such as wind, solar, biomass and water energy.