Are We Heading for a Second Wave of Lockdowns?

Date Posted: June 19, 2020

Read time: 48 min

That's Dr. Sam Parnia, a doctor and professor at the Grossman School of Medicine at New York University. What he was reacting to is news that a cheap drug, dexamethasone, has reportedly been shown to reduce deaths among COVID-19 patients on ventilators by as much as one-third.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

“I cannot emphasize how important this could be.”

That’s Dr. Sam Parnia, a doctor and professor at the Grossman School of Medicine at New York University. What he was reacting to is news that a cheap drug, dexamethasone, has reportedly been shown to reduce deaths among COVID-19 patients on ventilators by as much as one-third.

“It’s a huge breakthrough, a major breakthrough,” Dr. Parnia said of the study conducted by scientists at the University of Oxford.

The 60-year-old anti-inflation medicine is manufactured by a number of companies, including Mylan and Merck, and is widely available in pharmacies and hospitals around the world.

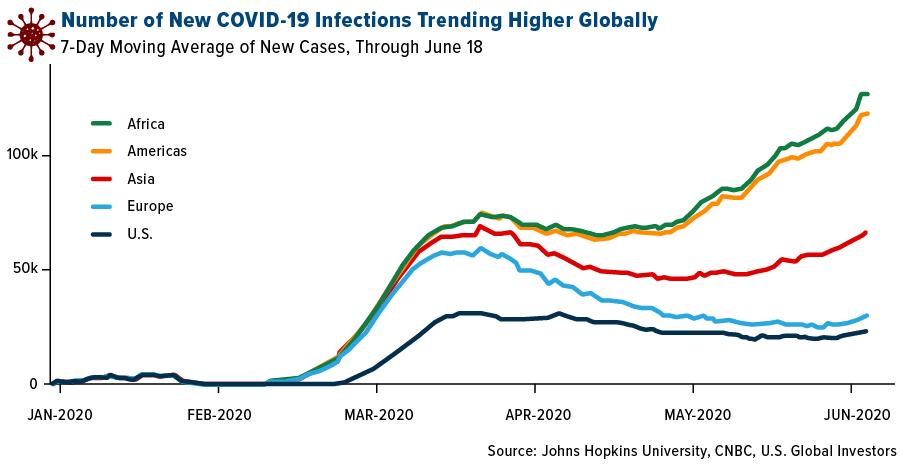

The discovery—if it’s everything the researchers say it is—comes just as new coronavirus cases and hospitalizations are spiking again in several countries, including the U.S.

California, which now requires mask-wearing outside of the home, had its biggest one-day jump in infections. Arizona, Florida and Texas are also turning into new hotspots.

The threat is such that some companies are closing stores again after reopening. Apple announced it would be closing 11 locations in Florida, North Carolina, South Carolina and Arizona.

Our hometown of San Antonio recently had its largest one-day caseload, and hospitalizations are on the rise, particularly among veterans. Today the Audie L. Murphy Memorial Veterans Hospital, not a 10-minute car ride from our office, reported its highest number of coronavirus inpatients since the crisis began.

Fear and Loathing in the Age of COVID-19

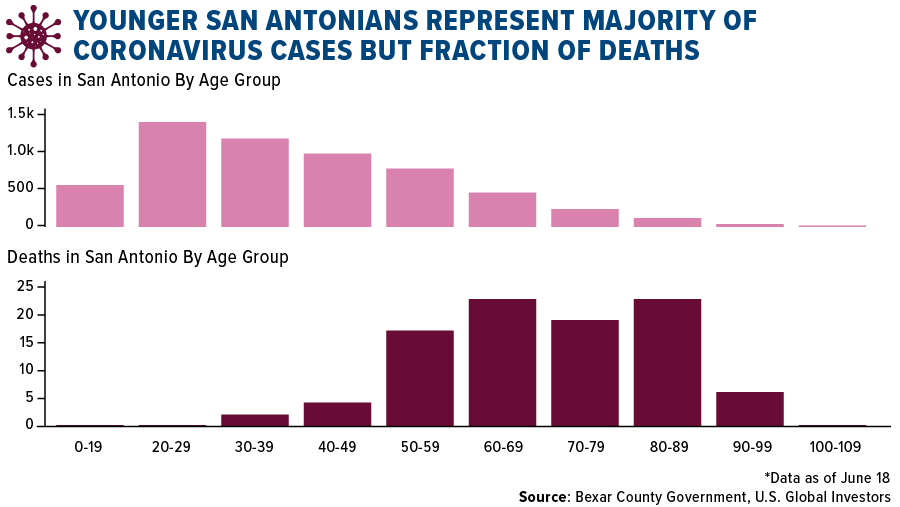

The data is scary and can be paralyzing—if you let it. As I’ve said a number of times, it’s important to keep things in perspective while also being smart and cautious. The average age of death in confirmed COVID-19 cases is 82, according to figures from Massachusetts, and San Antonio’s data appears to show similar results.

Below are COVID-19 cases and deaths in San Antonio by age. As you can see, people under the age of 49 make up a vast majority of total infections in the city, and yet they represent a very small fraction of deaths due to coronavirus-related complications. Meanwhile, the group with the most deaths are those aged 80 to 89, even though they have 13.5 times fewer cases than the 20-to-29 bunch.

But even if an older person contracts the virus, it’s not automatically a death sentence. Of the 103 San Antonians aged 80 to 89 who tested positive, only 22 died as a result, or a little more than one in five.

I understand this is an uncomfortable subject, and I don’t mean to minimize the risk. My intent is simply to share the facts so we can better manage our expectations.

We fear what we don’t understand, and fear often triggers us to make decisions we later regret. Nearly one-third of investors at Fidelity who were over the age of 65 sold all of their stocks between February and May. Tragically, many got out right at the bottom. Think of Warren Buffett, 90 in August, who unloaded his entire airline holdings soon before they began to take off.

Meanwhile, a great number of millennials trading on Robinhood accurately called the market bottom, with accounts surging just as stocks began to rally.

Vacation, Had to Get Away

The U.S. isn’t the only country that’s reopening, of course—a fact that can easily be seen by the sharp rebound in global fossil fuel emissions. After falling as much as 17 million metric tons per day by early April as world governments enforced lockdowns and travel restrictions, emissions have crept back up and are presently down about 4 million metric tons from the pre-pandemic period.

People are beginning to travel again and go on holiday. According to the Transportation Security Administration (TSA), more than 576,000 people boarded commercial airlines on June 18, marking a new high in the coronavirus era. This week Hong Kong Disneyland reopened for the first time since January, following the opening of Shanghai Disneyland last month.

Elsewhere in China, a coronavirus outbreak in Beijing has been “brought under control,” according to the country’s chief epidemiologist, by locking down residential areas and schools.

My Big Fat Indian Wedding

Like the U.S., India is seeing a surge in coronavirus cases this week and—again, like the U.S.—will not initiate another lockdown. Some 12,880 people tested positive on Thursday, a record one-day number. Instead of locking down the Indian economy, Prime Minister Narendra Modi is encouraging people take up yoga to build a “protective shield” against the virus.

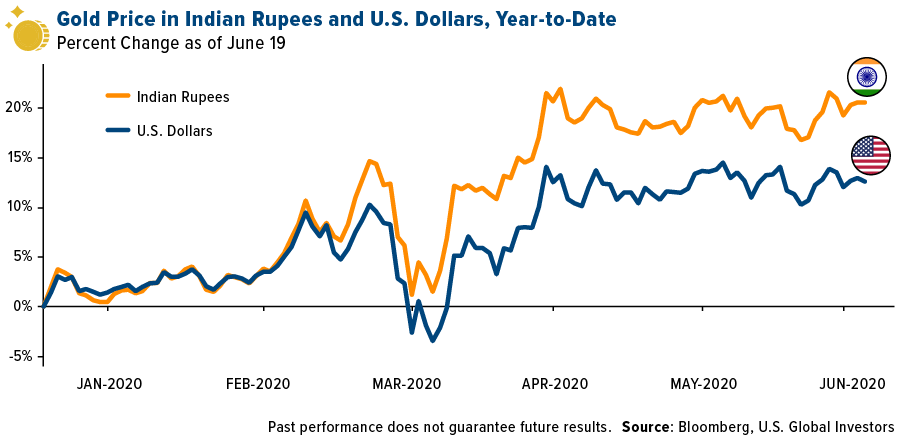

This made me wonder how the virus might impact the upcoming Indian wedding season. As I’ve written about many times before, the $50 billion Indian wedding industry is a huge source of global gold consumption, as weddings are considered an auspicious time to give and receive gifts of gold. Gold jewelry, in particular, is often an essential part of the dowry.

Indian weddings have a long history of being grand affairs, with attendance sometimes reaching into the hundreds and even thousands, the total cost into the tens of thousands.

But with many popular venues limiting wedding sizes, Indian couples are postponing tying the knot at a record rate.

What does this mean for the gold market? I’ll give you my thoughts in a special Frank Talk next week, so make sure you’re subscribed.

On a final note, I would like to invite you to join us in our next can’t-miss airline webcast, to be held on Monday, June 22, at 1:00 P.M. Central time. To register for the event, just send us an email at info@usfunds.com with “Airlines Webcast” in the subject line!

Gold Market

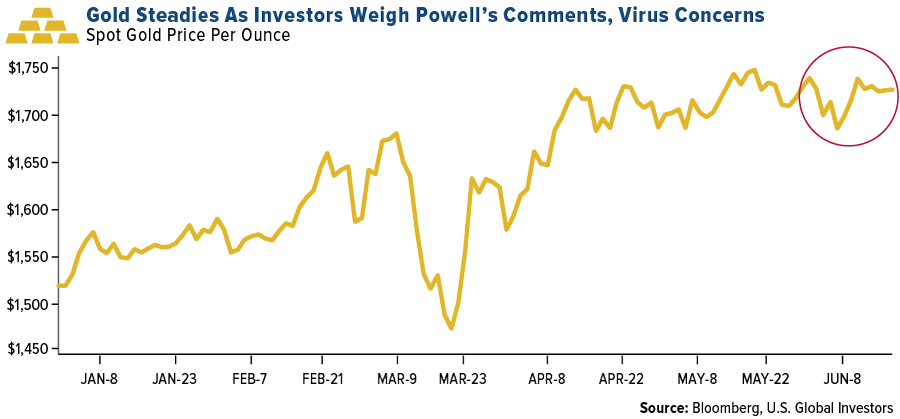

This week spot gold closed at $1,742.47, up $11.72 per ounce, or 0.68 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.00 percent. The S&P/TSX Venture Index came in up 1.96 percent. The U.S. Trade-Weighted Dollar rose 0.32 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-16 | Germany CPI YoY | 0.60% | 0.60% | 0.60% |

| Jun-16 | Germany ZEW Survey Expectations | 60 | 63.4 | 51 |

| Jun-16 | Germany ZEW Survey Current Situation | -82 | -83.1 | -93.5 |

| Jun-17 | Eurozone CPI Core YoY | 0.90% | 0.90% | 0.90% |

| Jun-17 | Housing Starts | 1100k | 974k | 934k |

| Jun-18 | Initial Jobless Claims | 1290k | 1508k | 1566k |

| Jun-23 | New Home Sales | 630k | — | 623k |

| Jun-25 | Durable Goods Orders | 10.90% | — | -17.70% |

| Jun-25 | GDP Annualized QoQ | -5.00% | — | -5.00% |

| Jun-25 | Initial Jobless Claims | 1300k | — | 1508k |

Strengths

- The best performing precious metal for the week was silver, up 0.83 percent as hedge funds boost their net long position to a 14-week high. Swiss exports of gold to the U.S. hit another high in May to 126.6 tons. ETFs added 27,739 troy ounces of gold to their holdings on Thursday, marking the sixth straight day of inflows. Bloomberg notes that total gold held by ETFs rose 22 percent this year to 100.9 million ounces.

- Goldman Sachs raised its 12-month price forecast for gold to $2,000 an ounce. Analysts including Mikhail Sprogis said in a note that “gold investment demand tends to grow into the early stage of economic recovery, driven by continued debasement concerns and lower real rates.” The bank added that it estimates fear-driven demand for bullion has boosted prices by 18 percent this year.

- Gold has traded in a narrow range for the past month. The two biggest factors for the metal are comments from the Fed and COVID-19. The yellow metal has held its gains for the year on the wave of unprecedented stimulus to support the economy and concerns of the number of virus infections rising. Gold then had a surprise rally on Friday and finished the week back in the $1,755 range.

Weaknesses

- The worst performing precious metal for the week was palladium, down 1.08 percent, despite the positive news that it should remain in deficit this year. Traders were rotating positions to silver with expectations that industrial uses for palladium will still be soft in the near term.

- Although gold and silver are in favor with ETF investors, money managers’ net long positions in Comex futures and options for the metals are down by more than 50 percent this year, according to Bloomberg. Commerzbank AG says gold positions have fallen for five of the past six weeks, which explains why prices are stuck in a range despite strong demand from ETFs.

- Gold retreated early in the week after the U.S. dollar strengthened on concern that a second wave of COVID-19 infections could hurt the economic recovery. Equities fell on Monday on news that Beijing reported new virus cases. “The sell-off happening in other assets is rubbing off on gold as well,” Gnanasekar Thiagarajan, director of Commtrendz Risk Management Services, told Bloomberg.

Opportunities

- Anglo American Platinum CEO Natascha Viljoen said the palladium market should remain in deficit in 2021 and sees a small deficit for this year. The metal producer also said it is targeting 70 percent of output capacity by the end of June with potential for that to rise to 90 percent in the second half of this year.

- Cardinal Resources announced that it has entered into an agreement with Shandong Gold where Shandong will acquire 100 percent of the issued and outstanding shares in Cardinal in cash. K92 Mining provided an update on operations amid the COVID-19 state of emergency in Papua New Guinea. The miner said its gold production is one track to exceed production in the first quarter, despite lower running time due to shutdowns.

- Advisors to the world’s wealthiest are urging them to hold more gold in their portfolio. Reuters reports that some private banks are now channeling up to 10 percent of client portfolios into gold as central bank stimulus reduces bond yields. Nine private banks spoken to by Reuters said they had advised clients to increase their allocation to the yellow metal.

Threats

- A growing worry in the economy is that job losses could become permanent from the coronavirus effects. Bloomberg Economics research highlights that about 50 percent of job losses came from the lockdown and weak demand, 30 percent from the reallocation shock and 20 percent from high unemployment benefits encouraging workers to stay home. Federal Reserve Bank of Minneapolis Neel Kashkari commented that his base case is that a second wave of virus comes this fall and the unemployment rate could go higher.

- Evercore ISI research showed that total macro risk has climbed to a new all-time high in its 14-year model. The research says, “volatility associated with changes in S&P correlation now accounts for more than half of total macro risk, followed by the risk influence of credit spreads and the U.S. dollar.”

- Veteran investor Jeremy Grantham said in an interview on CNBC this week that the U.S. stock market is in a bubble and that investing in the market now is “simply playing with fire.” Bloomberg notes that the S&P 500 index has risen almost 40 percent from its March 23 low. Grantham added that “it is a rally without precedent – the fastest in this time ever and the only one in the history books that takes place against a background of undeniable economic problems.”

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.04 percent. The S&P 500 Stock Index rose 1.86 percent, while the Nasdaq Composite climbed 3.73 percent. The Russell 2000 small capitalization index gained 2.23 percent this week.

- The Hang Seng Composite gained 2.21 percent this week; while Taiwan was up 1.05 percent and the KOSPI rose 0.42 percent.

- The 10-year Treasury bond yield fell 2 basis points to 0.691 percent.

Domestic Equity Market

Strengths

- Health care was the best performing sector of the week, increasing by 3.14 percent versus an overall increase of 2.06 percent for the S&P 500.

- Incyte Corp was the best performing S&P 500 stock for the week, increasing 14.48 percent.

- Evercore ISI analyst C.J. Muse raised the price target on Lam Research to $400 from $350 and kept an Outperform rating on the shares. With expectations for beats and raises this coming earnings cycle led by relatively unchanged demand trends and ongoing equipment shortages, coupled with wafer fab equipment positioned to move higher in both 2020 and 2021 on sustained foundry spending and increasing capex from Intel and memory, semi equipment stocks are "primed to outperform" into the second half of 2020 and beyond, Muse told investors in a research note.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 2.39 percent versus an overall increase of 2.06 percent for the S&P 500.

- H&R Block Inc was the worst performing S&P 500 stock for the week, falling 11.98 percent.

- Wirecard, a German payments processor, said on Thursday that its auditors at EY could not confirm "sufficient audit evidence" of about 1.9 billion euros ($2 billion) in its cash balances, effectively saying that the money is missing. Shares of the fintech group tumbled by over 65 percent in early trading after news of the lost cash.

Opportunities

- Tesla signed a three-year pricing deal with battery cell maker Panasonic. The carmaker’s China car registrations were up 150 percent month on month in May.

- WhatsApp is launching a digital payment system in Brazil in what will be the feature’s first nationwide rollout. The system will use Facebook Pay and will be free to individual users but paid for businesses.

- Shift Technologies Inc., an online retailer for used cars, is in talks to merge with blank-check company Insurance Acquisition Corp., according to people familiar with the matter. The companies could announce a transaction within a month, said the people, who asked to not be identified because the matter isn’t public. Shift is aiming to be valued at more than $500 million in the deal, one of the people said.

Threats

- Veteran investor Jeremy Grantham said in an interview on CNBC this week that the U.S. stock market is in a bubble and that investing in the market now is “simply playing with fire.” Bloomberg notes that the S&P 500 index has risen almost 40 percent from its March 23 low. Grantham added that “it is a rally without precedent – the fastest in this time ever and the only one in the history books that takes place against a background of undeniable economic problems.”

- ‘Don’t confuse day traders with serious investors’: Warren Buffett and Howard Marks will win over time, Princeton economist says. "Legions of new day traders have poured new money into stocks without a care for the risks involved."

- BP slashed its valuation by almost $18 billion as it adjusts to oil’s pandemic era new normal. The oil major said it expects Brent crude to average around $55 per barrel from 2021 through to 2050, 27 percent lower than its previous forecast.

The Economy and Bond Market

Strengths

- Retail sales jumped by the most on record in May after two straight months of sharp declines as businesses reopened, offering new evidence that the recession triggered by the COVID-19 pandemic may be nearing an end. Retail sales jumped 17.7 percent in May compared to a 14.7 drop in April.

- The Conference Board Leading Economic Index (LEI) for the U.S. increased 2.8 percent in May to 99.8, following a 6.1 percent decline in April, and a 7.5 percent decline in March. Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board, said "the relative improvement in unemployment insurance claims is responsible for about two-thirds of the gain in the index.”

- Business activity steadied in New York in June after two months of record contractions, according to the New York Fed’s Empire State Manufacturing Survey. The Empire State Business Conditions Index rose 48 points to negative 0.2 in June. A reading close to zero indicates steadying conditions.

Weaknesses

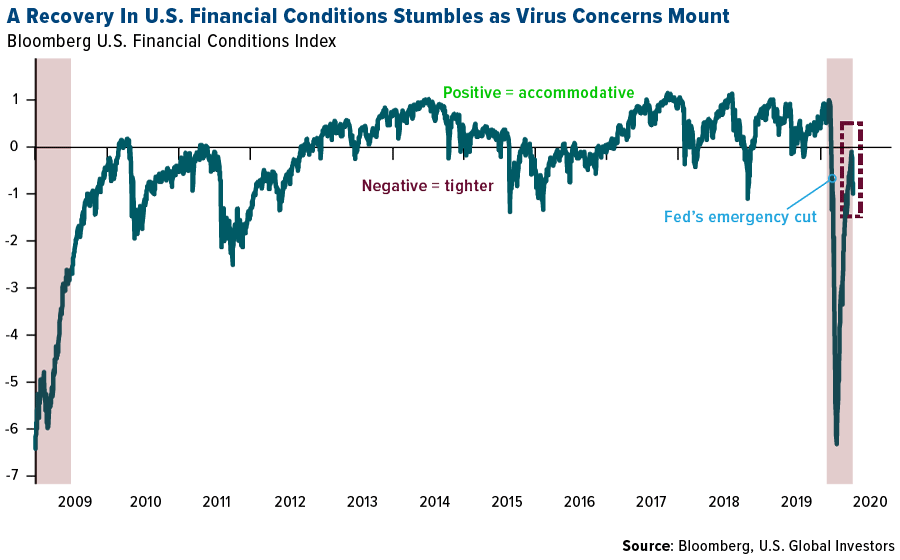

- The Bloomberg U.S. Financial Conditions Index — which tracks the overall level of stress in stocks, bonds and money markets — has turned sharply lower since approaching zero, the dividing line between accommodative and tighter conditions relative to pre-crisis norms. Growing concerns over a potential second wave of coronavirus infections has rattled markets.

- Another 1.508 million Americans filed for unemployment benefits in the week ending June 13, exceeding consensus expectations for 1.29 million. The prior week’s figure was revised higher to 1.57 million from the previously reported 1.54 million jobless claims. While last week marked 11 consecutive week of deceleration, more than 45 million Americans have filed for unemployment insurance over the past 13 weeks.

- A sharp decline in travel will cost governments roughly $17 billion in revenue from taxes on hotel occupancy, corporate profits and other levies in 2020, according to a study by Oxford Economics. The impact has been especially large in California, Florida, New York and Nevada, which are each facing shortfalls of more than $1 billion.

Opportunities

- Next Tuesday, the preliminary Markit PMIs for June could jump higher to reflect the re-opening in most states. Personal income and spending data for May will hit the markets next Friday and are likely to continue the trend of improvement.

- The Trump administration is preparing a nearly $1 trillion infrastructure proposal as part of its push to spur the economy, according to people familiar with the plan. A preliminary version being prepared by the Department of Transportation would reserve most of the money for traditional infrastructure work, like roads and bridges, but would also set aside funds for 5G wireless infrastructure and rural broadband, the people said. An existing infrastructure funding law is up for renewal by September 30, and the administration sees that as a possible vehicle to push through a broader package, the people said.

- The global economy is in a new expansion cycle and output will return to pre-coronavirus crisis levels by the fourth quarter, according to Morgan Stanley economists. “We have greater confidence in our call for a V-shaped recovery, given recent upside surprises in growth data and policy action,” economists led by Chetan Ahya wrote in a mid-year outlook research note on June 14. Predicting a “sharp but short” recession, the economists said they expect global GDP growth will trough at negative 8.6 percent year on year in the second quarter and recover to 3.0 percent by the first quarter of 2021.

Threats

- Although U.S. employment will increase in the coming months, the jobless rate will remain elevated through the end of the year, said Robert Kaplan, president of the Federal Reserve Bank of Dallas. “We’re on our way down right now,” Kaplan said Sunday in an interview on CBS. Kaplan said the rate would end the year at 8 percent or more.

- Markets are likely to remain tuned to virus news in the coming week, as the battle between stimulus-fueled optimism and second wave fears rages on. The progression of virus hospitalizations could tip the scales, either positively or negatively, depending on its evolution.

- A Census Bureau survey of how households are handling their medical needs amid coronavirus- related closures and stay-at-home orders found that millions are going without care. Led by the New York metro area, in the last four weeks to June 9 an estimated 87.7 million nationally delayed getting care, while almost 70.6 million needed it for something unrelated to COVID-19 but didn’t get it.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 16.97 percent as a nationwide shortage of product has come with Covid-19 related shutdowns. Tesla struck a deal to buy cobalt from Glencore, the world’s biggest miner of the battery metal. Cobalt demand is expected to surge as Tesla expands in the coming years to China and Europe and as other carmakers roll out electric vehicles. According to the deal, Glencore could supply as much as 6,000 tons of the metal a year for lithium-ion batteries, reports Bloomberg, citing a person familiar with the matter.

- China increased its budget for renewable power subsidies to $13 billion, which is 7.5 percent more than it spent last year. According to the Ministry of Finance’s website, solar power incentives are set to rise 14 percent compared with last year, while wind is down 3.2 percent. The higher-than-expected solar subsidy increase is positive for photovoltaic equipment value chains and for solar farm operators, reports Bloomberg.

- A big maybe is the giant U.S. infrastructure plan to help boost the economy. On Monday, European construction stocks jumped after reports that the Trump administration is weighting a $1 trillion program. Infrastructure spending is much needed in the U.S. and plans for new developments were put on hold when the coronavirus pandemic struck.

Weaknesses

- The worst performing commodity for the week was wheat, down 4.38 percent on the outlook of plentiful supplies due to optimal weather conditions. According to Global Ports data, weekly exports of iron in the first week of June out of Australia hit an all-time high. Brazil’s iron exports averaged 1.64 million tons a day in the first nine days of June, up significantly from 1.4 million tons in the first five days of the month. Bloomberg notes that iron ore is forecast to average $80 a ton in the second half of 2020 after rising above $100.

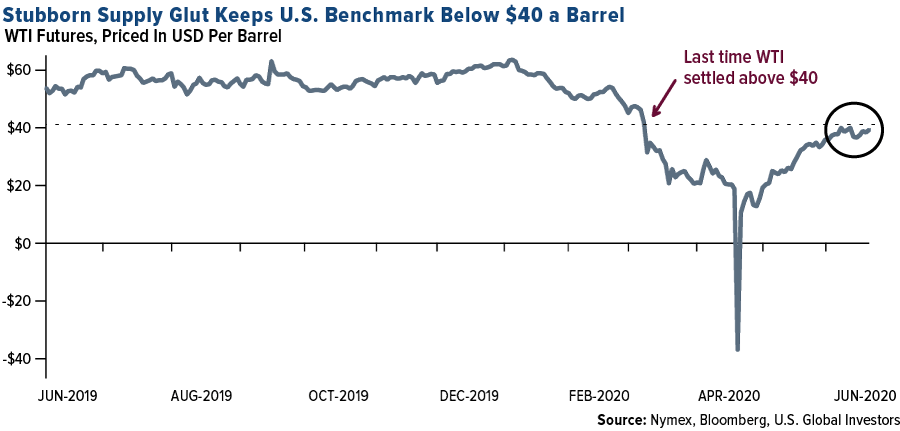

- Despite strong production cuts and growing short-term demand for oil, U.S. inventories continue to climb and hit a record for the second week in a row. Oil has continued to trade around $40 a barrel and the continued threat is of a second wave of COVID-19 infections that would cut short-term demand. However, it was a stronger week for the fuel. Futures in New York did rise above $40 on Friday morning and ended the week up over 9 percent.

- Due to the coronavirus demand wipe-out, BP is making its biggest write down since the Deepwater Horizon disaster. Write offs in the second quarter are estimated to be in a range of $13 billion to $17.5 billion post-tax. According to Baker Hughes data, the number of operating rigs in Africa halved in the month of May. Bloomberg reports that oil exploration will likely to a big long-term hit. In a strange move, Saudi Aramco is set to sell bonds or loan in order to pay its $75 billion in dividends this year, adding to its ever-growing balance sheet.

Opportunities

- Shell and IBM partnered to launch a digital services marketplace for mining companies called Oren. This is Shell’s first move into the mining business and is one of many oil majors exploiting its software analytics. Bloomberg’s Danya Liu writes that “digitization in mining will grow because of its potential to improve yield, safety and sustainability. Entering the space now puts Shell in a position to capture market share as technology adoption accelerates.”

- Bloomberg reports that the Delbrook Resource Opportunities Master Fund LP, a hedge fund, has risen 36 percent so far this year by trading precious metal miners. The fund is significantly outperforming its benchmark due to what the company says is taking advantage of dislocations in high-quality mid-cap precious metals producers versus larger-cap peers.

- According to Goldman Sachs, spending on renewable power is set to overtake oil and gas drilling for the first time in 2021 and clean energy affords a $16 trillion investment opportunity through 2030. Analysts wrote in a note that renewables including biofuels will account for around a quarter of all energy spending in 2021, up from 15 percent in 2014. Green energy infrastructure could draw $1 trillion to $2 trillion a year and create 15 to 20 million jobs globally, reports Bloomberg.

Threats

- The International Energy Agency (IEA), OPEC and the U.S. Energy Information Administration (EIA) have all updated their oil market forecasts recently and they all three agree that global consumption will fall between 16 and 18 percent year-over-year in the second quarter of this year. This compares with a decline of just 3.4 percent during the worst during of the 2008 to 2009 financial crisis, notes Bloomberg.

- As for overall energy demand, growth was slowing even before the coronavirus pandemic spread globally, according to BP. The company’s annual Statistical Review of World Energy report showed that growth in primary energy consumption slowed to 1.3 percent in 2019, almost half the rate of 2018.

- The EPA said that it will not set national drinking water standards for perchlorate, which is a rocket fuel chemical. Bloomberg Law reports that this could result in a legal challenge. The EPA was bound by a consent decree in 2016 that it must issue drinking water regulation for the chemical by December 19, 2020. However, those regulations were never instated, and an EPA spokesperson said the consent decree no longer applies.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 3.3 percent. Global risk-on sentiment has helped Turkish equites to nearly erase 2020 losses. The Istanbul Stock Exchange has climbed 23 percent since March 23 and is now in overbought territory. Dogus Otomotive, a car distributor, was the best performing equity trading on the Istanbul Stock Exchange, gaining 26 percent in the past five days.

- The Russian ruble was the best performing currency this week, gaining 50 basis points. The currency gained along with oil as OPEC has agreed to extend production cuts until the end of July. Brent crude oil gained 9 percent in the past five days. The Central Bank of Russia cut its main rate by 100 basis points and signaled more easing ahead. Despite another larger rate cut, Russia still has the highest real rates among central emerging European peers.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 33 basis points. The European Union’s highest court ruled on Thursday that Hungary’s restrictions on the financing of civil-society organizations are unlawful. The European Court of Justice found that a 2017 law that required nongovernmental organizations that received foreign financing to identify themselves as such and to disclose their donors had “introduced discriminatory and unjustified restrictions.” To comply with the decision, Hungary would have to repeal the law as written or could face sanctions. The worst performing stock trading on Budapest Stock Exchange was MOL, a Hungarian refinery, losing 2.5 percent in the past five days.

- The Polish zloty was the worst performing currency in the region this week, losing 1.1 percent. The currency declined on weaker economic data. The central bank left its main rate unchanged at a record low 10 basis points. The government announced that it would not suspend a banking tax.

- Financial was the worst performing sector among eastern European markets this week.

Opportunities

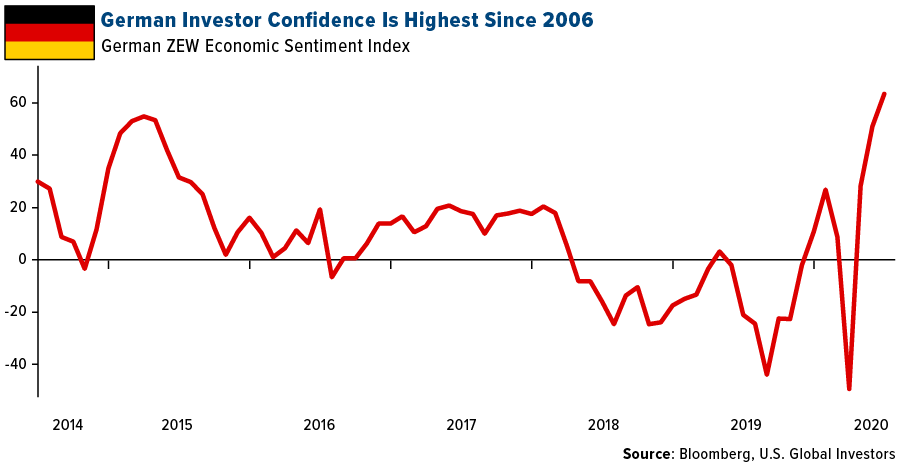

- Germany’s ZEW survey of investor expectations rose to 63.4 in June from 51. The current situation measure improved to negative 83.1 from negative 93.5. "There is growing confidence that the economy will bottom out by summer 2020," ZEW President Achim Wambach said.

- Following good first quarter results, Alex Boulougouris, a banking analyst at Wood & Company, increased his estimates for Greek banks. He argues that recent developments despite Greek banks being removed from the MSCI Emerging Europe Index at the last rebalancing are positive. In particular, the frontloading of COVID-19 loan loss provisions, the benefit from the targeted longer-term refinancing operations (TLTRO) on net interest income and the relaunch on the securitization transactions by Alpha and Piraeus Bank.

- President Donald Trump announced his plan to withdraw troops from Germany unless Chancellor Angela Marker boosts defense spending. The move to cut troops by more than a quarter to 25,000 is a sign of deteriorating relations between the two countries. At the same time, there is a speculation that Trump may increase the number of U.S. troop present in neighboring Poland, which meets America’s target for defense spending at 2 percent of gross domestic product.

Threats

- The Czech government approved a plan to widen the 2020 budget deficit target for the third time, which stands at 9 percent of GDP. Compared with the original budget for this year, which targeted a deficit of 40 billion koruna, the latest amendment sees revenue lower by 213 billion koruna and expenditures rising by 246 billion koruna, according to the finance minister. The record stimulus includes worker compensation, more money for hospitals, commercial rent subsidies and financial aid for municipalities.

- Reuters reported that Germany’s Economy Ministry said economic output will fall further in the second quarter than in the first, and warned that the recovery in the second half of the year and beyond would be sluggish. Germany left its GDP forecast unchanged at 6.3 percent contraction this year.

- Russia sentenced American Paul Whelan to 16 years in prison for spying. Whelan was arrested in December 2018 while attending a wedding in Moscow after receiving a flash drive with “state secrets” that he says he thought contained holiday pictures, Bloomberg reported. His family said that they believe that now Whelan has been sentenced Russia will try to use his as a bargaining chip to gain U.S. concessions.

China Region

Strengths

- India was the best performing country this week, gaining 2.8 percent. Despite the deadly border incident with China this week, local equities moved higher. Bloomberg reported that 20 Indian soldiers have died after violence broke out Monday afternoon and went until midnight on the Tibetan plateau with an unknown number of Chinese casualties. Bajaj Finserv, an insurance company, was the best performing equity among stocks trading on the NSE Nifty 50 Index, gaining 11.6 percent in the past five days.

- The Philippine peso was the best performing currency this week, gaining 45 basis points. The government is planning to introduce new taxes as a part of its commitment to a 9 percent fiscal deficit limit. The increase in taxes will help the government to bring in more revenue, but it could also slow down the economic recovery.

- Healthcare was the best performing sector in the Hong Kong Stock Exchange.

Weaknesses

- Pakistan was the worst performing market this week, losing 3.5 percent. Equites sold off on news of the deadly border fight between India and China and the spiking number of coronavirus cases in Pakistan. On Thursday, Pakistan recorded its deadliest day of coronavirus with 136 deaths. IGI Holdings was the worst performing equity among stocks trading on the Karachi Stock Exchange, losing 17.6 percent in the past five days.

- The Pakistani won was the worst performing currency this week, losing 1.6 percent. The currency weakened with local equites on pandemic concerns and increased regional geopolitical tension.

- Telecommunication was the worst performing sector in the Hong Kong Stock Exchange.

Opportunites

- Reuters reported that U.S. Secretary of State Mike Pompeo met with Yang Jiechi, China’s top diplomat in Hawaii this week for their first in-person meeting since 2019. Pompeo stressed “the need for fully-reciprocal dealings between the two nations across commercial, security, and diplomatic interactions.” After the meeting, China agreed to honor of its commitments under the phase one trade deal, including buying $36.5 billion worth of American agriculture products.

- China is encouraging financial institutions to make interest concessions as appropriate to businesses to keep economic fundamentals stable. CLSA recommends an overweight of Chinese banks due to the strong provisions and expects the People’s Bank of China (PBOC) to further cut rates and the deposit benchmark rate in the third quarter.

- Although COVID-19 cases are increasing, global experts have found that its unlikely food trade is responsible for causing a fresh outbreak in Beijing. Bloomberg notes that the new outbreak was blamed on imported salmon after a food market said the virus had been traced to a chopping board for this fish. The findings should provide relief for exporters of seafood whose sales to China had already fallen 30 percent in the first four months of the year.

Threats

- Geopolitical tensions between North and South Korea escalated dramatically this week. North Korea destroyed an office building housing the joint liaison office, located in a North Korean border town, that was constructed just two years ago. The country said the destruction was in response to South Korea sending anti-North Korean propaganda across the border via balloons and drones.

- According to the Institute for Management Developed (IMD) survey, both China and the U.S. have fallen lower on the World Competitiveness Rankings for this year. The U.S. fell seven places to the 10th spot while China fell six places to the 20th spot. IMD says the trade war between the two nations has made them both less competitive.

- Beijing reported 106 COVID-19 infections over the weekend. Bloomberg reports that on Tuesday the city closed several food markets and put 30 housing compounds under lockdown to try and stem the spread of the virus. Globally, the number of positive infections is trending back upward, especially in the U.S. and South America. This is creating concern that a second wave of infections will hamper the global economic recovery.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 19 was Acash Coin, up over 9,000 percent.

- A survey conducted by The Tokenist, shows that people all over the world are increasingly interested in bitcoin over traditional asset classes, writes BitcoinExchangeGuide.com. The survey polled over 4,800 respondents in 17 countries and revealed that 45 percent prefer to own bitcoin over stocks, real estate and gold – an increase of 13 percent from 2017. “Belonging to the age group 18-65, millennials’ confidence in bitcoin has ‘increased dramatically.’”

- In an official statement on Thursday, Russia’s Federal Service for Supervision of Communications, Information Technology and Mass Media, has officially lifted the two-year ban on Telegram, writes CoinTelegraph. The announcement by local authorities apparently comes in response to a recent statement from Telegram CEO Pavel Durov, claiming that the Telegram team has been actively combating terrorism and extremism on the messenger while ensuring user privacy.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended June 19 was FuturoCoin, down 97.18 percent.

- A new report from the U.S. Department of Justice’s Office of the Inspector General, notes that even years after one of its agents stole $700,000 in bitcoin back in 2015, the Drug Enforcement Administration (DEA) failed to adequately police its undercover agents’ handling of cryptocurrency, writes CoinDesk. According to the report, some of the problems manifested in the “relative uniqueness of crypto money-laundering,” but the DEA did not adapt itself to these new challenges. In fact, its record keeping was so poor that investigators struggled to match up transaction information with activities.

- Ebang, a Chinese bitcoin miner manufacturer, estimates it incurred a net loss of $2.5 million on a revenue of $6.4 million for the first quarter of 2020, according to CoinDesk. This financial disclosure was posted mid-week in an update to the firm’s IPO prospectus filed with the SEC.

Opportunities

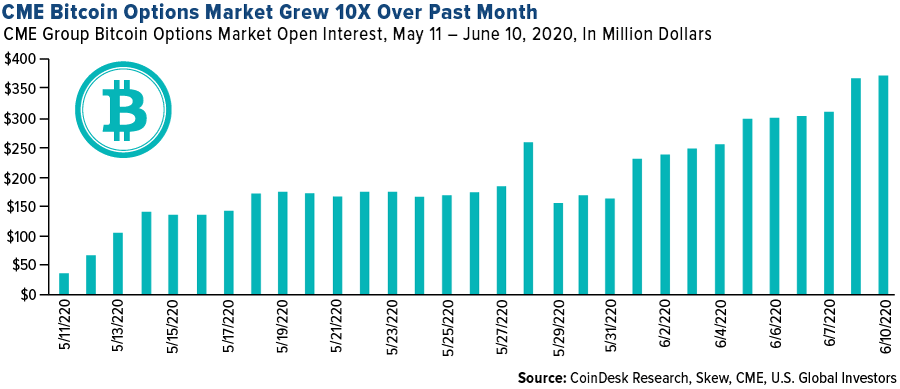

- The total open interest for CME bitcoin options increased more than tenfold, reports CoinDesk, from $35 million on May 11 to $373 million on June 10. It also made a new all-time high on six consecutive days from June 5-10. According to the article, significant growth in CME futures points to rapidly growing interest by institutional investors in trading regulated bitcoin derivatives products.

- The Bank of Canada is preparing to design its own central bank digital currency (CBDC), as revealed in plans in a June 11 job posting. As reported by CoinDesk, the central bank says it is “reinventing central banking and radically rethinking the nature of Canada’s cash. “The Bank of Canada is embarking on a program of major social significance to design a contingent system for a CBDC, which can be thought of as a banknote, but in digital form,” the bank wrote.

- A startup bitcoin financial services firm known as River Financial Inc. said its number of clients has doubled every month this year, writes Bloomberg. The increase in clients is fueled by what the startup calls “bitcoin boomers,” or new cryptocurrency investors over the age of 55. In fact, these bitcoin boomers have accounted for 77 percent of River Financials’ volume growth.

Threats

- A major German fintech company, WireCard, which issues Crypto.com’s debit cards, allegedly misrepresented over $2 billion in cash reserves, reports CoinTelegraph. Financial Times wrote on June 18 that auditors from EY “could not confirm the existence of 1.9 Billion Euros in cash,” or about $2.1 billion. A statement from WireCard reads that a trustee of the company’s bank accounts attempted to deceive the auditor and falsely indicate the existence of the cash balance.

- The newest release of the Bancor decentralized exchange appears to have a critical vulnerability, and is now hacking itself to save user funds from malicious actors, writes CoinTelegraph. Users who traded on Bancor and gave a withdrawal approval to its smart contract are urged to revoke it through a specialized website, the article continues. That website is approved.zone.

- WisdomTree Investments is looking to start a bitcoin exchange-traded fund (ETF), writes Bloomberg, but unfortunately will face an uphill battle for approval. The SEC has turned down prior proposals for cryptocurrency ETFs, so the New York-based asset manager will surely face hurdles with its proposal as well. The firm’s plan is to launch a fund that could invest as much as 5 percent of its net assets in bitcoin futures traded on the Chicago Mercantile Exchange.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2020):

Cardinal Resources Ltd

K92 Mining Inc

MOL Hungarian Oil & Gas PLC

Alpha Bank AE

Merck & Co Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Pakistan Stock Exchange (Karachi Stock Exchange) KSE-100 Index comprises the top company from each of the 34 sectors on the PSX, in terms of market capitalization. The NIFTY 50 is the flagship index on the National Stock Exchange of India, computed using a float-adjusted, market capitalization weighted methodology. The MSCI Emerging Markets Europe Index captures large and mid-cap representation across 6 emerging markets countries (Czech Republic, Greece, Hungary, Poland, Russia and Turkey) in Europe. With 70 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables. These variables have historically turned downward before a recession and upward before an expansion. The Empire State Business Conditions Index is a monthly survey of manufacturers in New York state conducted by the Federal Reserve Bank of New York. The index summarizes general business conditions in the state. The Bloomberg U.S. Financial Conditions Index tracks the overall level of stress in stocks, bonds and money markets.