Bitcoin Has Its Best Start to a Year Since 2012 as Market Banks On Institutional Investors

Date Posted: January 17, 2020

Read time: 53 min

Among the biggest contributors to the bitcoin rally is the hope that 2020 could finally see institutional investors move into the digital field en masse, prompted by growing client demand and more attractive ways to get exposure.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Besides its breathtaking mountains, world-famous chocolate and wartime neutrality, Switzerland is perhaps best known for its commitment to financial privacy. Banking secrecy became law in 1934, making it a crime for Swiss banks to disclose accountholder information of any kind to third parties.

Although such privacy laws have been impacted in recent years—mostly by U.S.-led global efforts to counter money laundering and tax evasion—Swiss banks still enjoy a reputation for being secure and discreet, and they continue to attract assets from all over the world.

It’s appropriate, then, that the country should host the world’s most private conference on what’s potentially the most private asset class: cryptocurrencies. This week, hundreds of crypto investors, experts and enthusiasts from all around the globe descended on the legendary skiing resort town of St. Moritz to attend and learn at the Crypto Finance Conference.

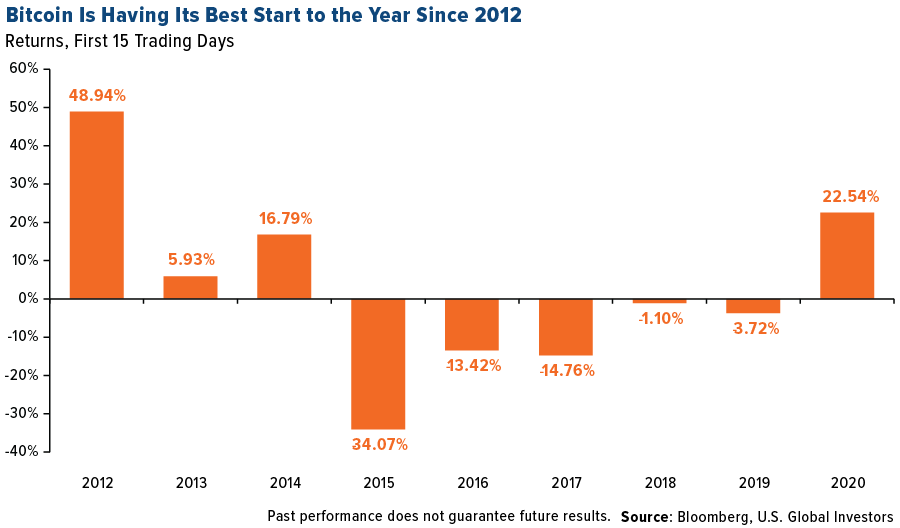

The conference’s timing couldn’t have been more perfect. Bitcoin had its best start to the year since 2012, rising more than 22 percent in the first 15 days.

Among the biggest contributors to the rally, as I see it, is the hope that 2020 could finally see institutional investors move into the digital field en masse, prompted by growing client demand and more attractive ways to get exposure than direct ownership of coins. Earlier in the week, the Chicago Mercantile Exchange (CME) launched one such product, a bitcoin options contract, which reportedly had a successful first day of trading with a total of 55 contracts, worth 275 bitcoin, or the equivalent of $2.4 million.

Who Will Be First With a Bitcoin ETF?

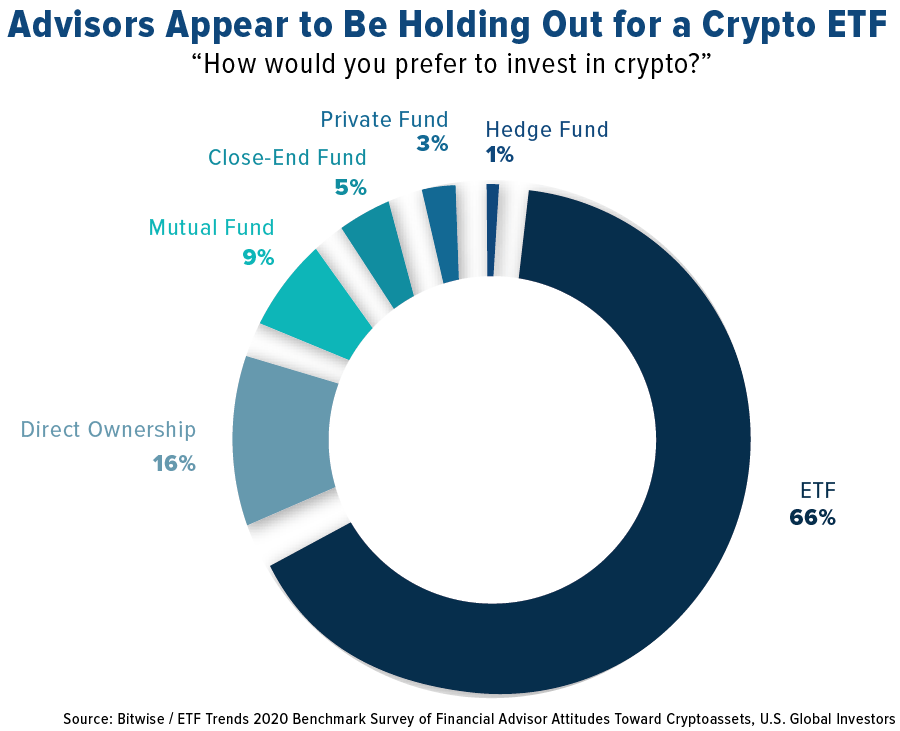

Advisors, though, may be holding out for an exchange-traded fund (ETF) backed by cryptos such as bitcoin, if a recent survey is any indication. As much as 65 percent of respondents to a survey conducted by crypto indexer Bitwise and ETF Trends said that a crypto ETF was their preferred method of getting exposure, followed by a distant 16 percent preferring direct ownership and an even more distant 9 percent preferring a mutual fund.

At the moment, no such ETF is available because the Securities and Exchange Commission (SEC) has yet to approve one. Bitwise, in fact, withdrew its proposal for a bitcoin ETF this week, with Bitwise global head of research Matt Hougan telling The Block that the firm intends “to refile our application at an appropriate time.”

It’s no exaggeration to say that a bitcoin ETF is highly anticipated.

If you recall, I explored the feasibility of launching such a product a couple of years ago, ultimately deciding that the regulatory hurdles were too prohibitively high. Instead, we elected to bring to market the world’s first publicly traded crypto-mining firm, HIVE Blockchain Technologies. More than two years after its debut on the TSX Venture Exchange, investors continue to use it as a proxy for digital assets.

This week HIVE announced an incredible 20 percent increase in newly mined Ether coins compared to the last 15 days of December 2019. That’s thanks to the completion of the company’s Ethereum network upgrade dubbed the “Muir Glacier.” You can read more about the development by clicking here.

Winklevoss Twins: Time to Get On Board With Bitcoin

There was a number of notable presenters at the conference, including J. Christopher Giancarlo, former commissioner of the Commodity Futures Trading Commission (CFTC), who reminded the audience that innovation must come before regulation. And yet the European Union (EU) has it backwards, putting rules in place that hamper innovation before it even has a chance to begin.

The biggest rock stars in attendance by far were the Winklevoss twins, Cameron and Tyler, cofounders and president/CEO of crypto exchange Gemini. During their “fireside chat,” the two bitcoin perma-bulls urged conference-goers to start “building up bitcoin reserves” in anticipation of significantly higher prices.

In particular, they targeted gold investors, saying they “think bitcoin will disrupt gold.”

“Once the likes of Tesla’s Elon Musk or Amazon’s Jeff Bezos start mining gold on asteroids, which will happen within 25 years, gold’s value will change,” Tyler Winklevoss told the audience.

With all due respect to Tyler and his brother, I don’t happen to agree that bitcoin will replace gold anytime soon, as I’ve explained before. For one, unlike bitcoin, gold has a number of uses outside of its roles as investment, currency and a wealth preservation vehicle. Two, the yellow metal can be traded without electricity, internet or WiFi. This makes gold especially valuable in situations where power and telecommunications services are unexpectedly unavailable, such as during or after a natural disaster.

Some Relief in U.S.-China Trade Spat, But More Work Is Needed

On a final, unrelated note, you’re probably aware by now that, after more than 18 months since the start of the U.S.-China trade war, a meaningful agreement was finally reached between President Donald Trump and Chinese trade representatives. Although U.S.-imposed tariffs on China-imported goods still remain largely in place—presumably those will come off after a second round of negotiations—this is a positive step toward normalizing trade between the two superpowers.

The visual below, courtesy of Caixin Global, lays out exactly what China has agreed to. Over the next two years, the Asian country will be expected to purchase no less than $200 billion worth of U.S. goods and services, including $77.7 billion in manufactured goods and $32 billion in agriculture.

That’s a tall order, to be sure. In 2017, American exports to China were valued at $130 billion, the most ever, according to the Census Bureau. This leaves a $70 billion purchasing gap that China will need to fill somehow.

Washington and Beijing have also agreed to a “dispute settlement mechanism” to help resolve potential disputes during the implementation phase of the agreement.

Interestingly, the market didn’t respond too strongly on the news, gaining just under half a percent at its session high on Wednesday. This tells me that investors have already priced in the first phase, which, again, does not provide tariff relief. Perhaps not until the so-called Phase 2 of the trade deal is signed will we start see to see significant recovery in the U.S. manufacturing sector.

Curious to know which commodity was the top performer for 2019? Explore the recently updated Periodic Table of Commodity Returns by clicking here!

Gold Market

This week spot gold closed at $1,557.24, down $5.10 per ounce, or 0.33 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.29 percent. The S&P/TSX Venture Index came in up 0.37 percent. The U.S. Trade-Weighted Dollar rose 0.28 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-14 | CPI YoY | 2.3% | 2.3% | 2.1% |

| Jan-15 | PPI Final Demand YoY | 1.3% | 1.3% | 1.1% |

| Jan-16 | Germany CPI YoY | 1.5% | 1.5% | 1.5% |

| Jan-16 | Initial Jobless Claims | 218k | 204k | 214k |

| Jan-16 | China Retail Sales YoY | 7.9% | 8.0% | 8.0% |

| Jan-17 | CPI Core YoY | 1.3% | 1.3% | 1.3% |

| Jan-17 | Housing Starts | 1380k | 1608k | 1375k |

| Jan-21 | Germany ZEW Survey Current Situation | -13.5 | — | -19.9 |

| Jan-21 | Germany Survey Expectations | 15.0 | — | 10.7 |

| Jan-23 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Jan-23 | Initial Jobless Claims | 214k | — | 204k |

Strengths

- The best performing metal this week was palladium, up 17.92 percent on tight supplies and strong demand. One-week lease rates for palladium rose for a seventh day to 32.56 percent. The majority of gold traders and analysts were bullish on gold in the weekly Bloomberg survey, as attention turns to the next stage of the U.S.-China trade deal. Turkey’s gold reserves rose $478 million from the previous week to total $27.9 billion as of January 10, according to data from the central bank. South African gold output rose for the first time in more than two years in November, according to Statistics South Africa. Output rose 5.2 percent from a year earlier, compared to a 1.4 percent contraction in October. Producers have been able to take advantage of higher gold prices.

- Palladium has surged to a whopping $2,500 an ounce and had its biggest one-day increase since 2008 on Friday. Bloomberg data shows that the metal jumped as much as 9.3 percent on Friday to $2,528.51. Palladium has added over 70 percent in the last 12 months, driven by a combination of tight supply and strong demand for use in autos to meet emission standards.

- BloombergNEF says that mines, especially those in remote locations with high energy costs, can now develop onsite renewable energy as a cost-effective way to reduce carbon emissions and electricity costs. According to BNEF, an off-grid copper mine in Western Australian could use onsite renewables to meet up to 40 percent of its electrical demand at a lower or equal cost to diesel generation. Renewable energy costs continue to fall, with solar down 11 percent and wind down 6 percent in the last year.

Weaknesses

- The worst performing metal this week was silver, down 0.41 percent. Gold was under pressure early this week before the signing of phase one of the trade deal between the U.S. and China. “Investors who bought gold for the trade uncertainty will likely take profit,” said ABN Amro strategist Georgette Boele to Bloomberg. The SPDR Gold Shares saw more than $1 billion of outflows last week – the most since 2016. Russia’s gold buying spree has slowed. Russia purchased 149 tons of gold in the first 11 months of 2019, which is 44 percent less than the year before.

- The Treasury Department monthly budget released on Monday shows that the U.S. budget deficit widened to $356.6 billion in the first three months of fiscal 2020 and is on pace to exceed $1 trillion by year-end. A deficit of that amount would be the highest since the financial crisis when the government boosted spending.

- According to Bloomberg data, shareholder activists launched 518 new campaigns in 2019, up slightly from 512 campaigns in 2018. Vinson & Elkins, known for its energy-related work, said “2019 was the busiest year our shareholder activism defense practice has ever had.” Endeavour Mining Corp announced that it has closed merger talks with fellow Africa-focused gold miner Centamin Plc this week after it didn’t receive enough information in the due diligence process to make a formal offer.

Opportunities

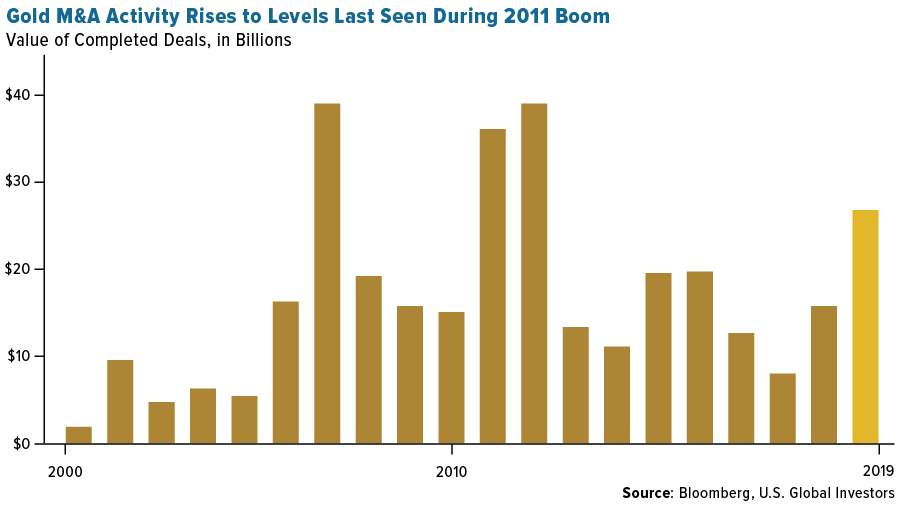

- Bridgewater Associates’ Greg Jenson told the Financial Times this week that gold could spike 30 percent as central banks allow inflation and political fears mount. “There is so much boiling conflict, that gold being part of a portfolio makes sense to us,” Jensen said. This would mean a gold rally to more than $2,000 an ounce. Peak gold could be more distant in the future than originally thought due to increased exploration spending. 2019 saw a flurry of gold M&A activity and a return to levels last seen during the 2011 boom. There was around $26.5 billion worth of completed deals last year.

- Palladium might continue to see its price boom. Joni Teves at UBS said in a note this week that the price forecast was raised to an average of $2,200 in 2020, up from $1,875. HSBC is also bullish, raising its near-term palladium price forecast by over 30 percent.

- According to five fund managers interviewed by Bloomberg, gold’s price increase, “combined with capital discipline among the larger miners, is generating a bonanza of free cash flow while mergers could spark share gains among smaller players.” Catalysts for more gains include a weaker dollar, lower-for-longer interest rates and the U.S. presidential election. RBC Global Asset Management’s Chris Beer said “I have covered the gold sector for more than 20 years and I have never seen this kind of cash flow generation.” Roxgold released strong exploration and drilling results this week and RBC Capital Markets commented that it expects to see a positive reaction from the company’s shares. Red Cloud Research released a note this week saying that it has initiated coverage of Group Ten Metals, which holds the second biggest land package in the prolific Stillwater Igneous Complex of southern Montana. “Group Ten is our favorite PGM explorer in the public domain and we expect big things from this currently small company.”

Threats

- Alastair Pinder at HSBC released a note this week warning that equity markets have been showing signs of exuberance and that global equity markets “may have moved too much, too soon.” Stifel also released a report this week commenting about the risks of unlimited free money. Morgan Stanley said in a note on Monday that the top five publicly-traded American companies now make up a record 18 percent share of the S&P 500 – higher than the tech bubble. Oaktree Capital Group LLC Co-Chairman Howard Marks said in an interview on Bloomberg TV this week that the odds are against investors now. “We’re in the longest bull market, the longest expansion in history, profits are not rising, stock prices are, and it’s what we call a liquidity-driven rally.”

- Several top U.S. automakers are reducing production and cutting jobs in a warning sign of a slowdown in the auto industry. Bloomberg reports that Fiat Chrysler is sending workers home at four factories, Ford has two factories operating on fewer shifts and General Motors might dial back output just after enduring its long strike. American consumers are finding new cars less affordable as the average sticker price approaches $35,000. A greater volume of car purchases last year went to rental companies and other fleet purchasers, rather than individual consumers.

- According to Bank of America Global Research analysis of income migration data, in 2018, low- and lower-tax states gained $32 billion more in adjusted gross income than higher tax states. This is evidence that President Trump’s SALT cap has fueled a wealth exodus from high-tax states. Bloomberg reports that states like Florida and Texas, with no income tax, are seeing more people move there while New York, California, Connecticut and New Jersey, which had the highest average SALT deductions, lost nearly 455,000 people in the last 12 month measurement period, according to U.S. Census data.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.82 percent. The S&P 500 Stock Index rose 1.97 percent, while the Nasdaq Composite climbed 2.29 percent. The Russell 2000 small capitalization index gained 2.53 percent this week.

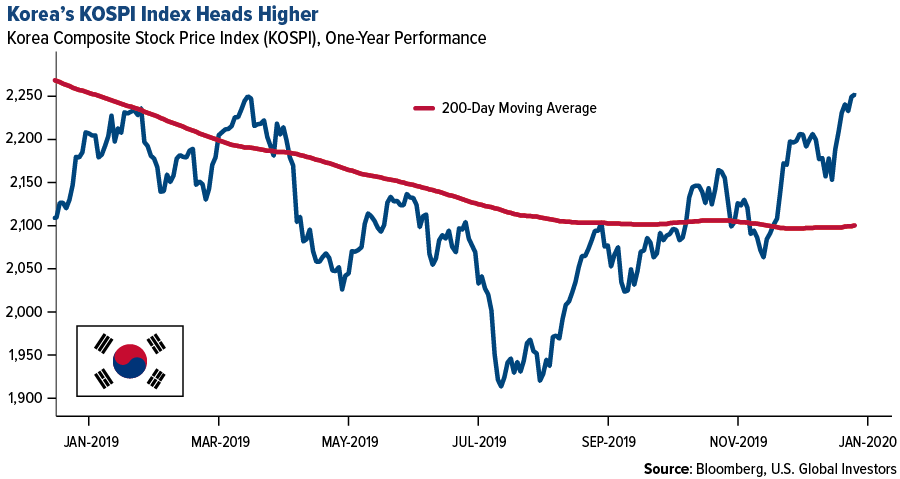

- The Hang Seng Composite gained 1.81 percent this week; while Taiwan was up 0.55 percent and the KOSPI rose 2.00 percent.

- The 10-year Treasury bond yield remained essentially flat this week.

Domestic Equity Market

Strengths

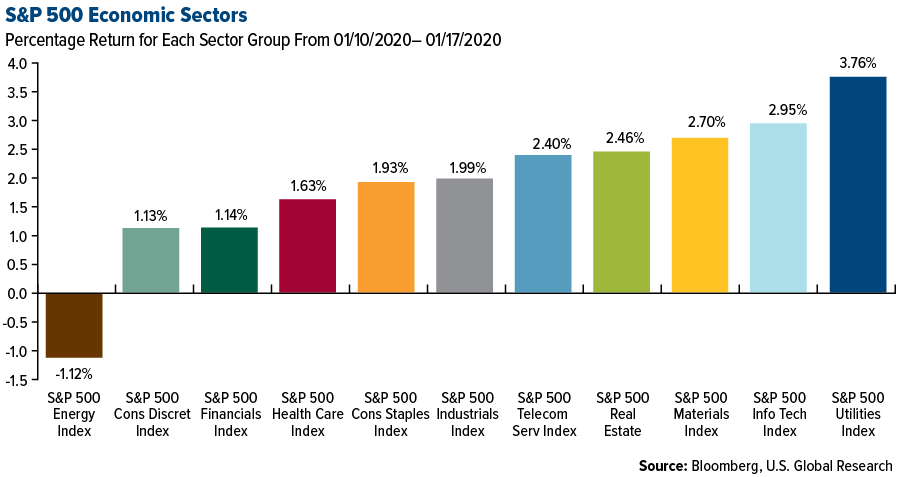

- Utilities was the best performing sector of the week, increasing 3.76 percent compared to an overall increase of 1.96 percent for the S&P 500.

- Perrigo was the best performing S&P 500 stock for the week, increasing 18.73 percent.

- Private equity giant KKR & Co. took the unusual step to disclose plans to push for changes at Dave & Buster’s Entertainment Inc. Shares in the restaurant chain soared as much as 16 percent to the highest level since June.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 1.12 percent compared to an overall increase of 1.96 percent for the S&P 500.

- Bank of New York Mellon was the worst performing S&P 500 stock for the week, falling 8.63 percent.

- Vail Resorts slumped after saying the North American ski season is off to a slower start this year, confirming Wall Street concerns.

Opportunities

- Apple Inc.’s price target was raised 24 percent at Morgan Stanley to a level below only one other Wall Street bank, the latest sign of confidence in the company. According to the analyst, Apple should benefit from a potential reduction in the amount of time customers are taking to replace their smartphones.

- Brookfield Property Partners rose the most since June 4 on Friday after S&P Dow Jones Indices announced that the company will replace Encana in the S&P/TSX 60 Index next week.

- Forest products stocks rose after U.S. housing starts for December surged to the highest in 13 years. Analysts from the Canadian Imperial Bank of Commerce (CIBC) wrote that they expect “spring selling season this year and lumber prices to respond positively to near-term housing data.”

Threats

- Companies that help transport goods and materials ranging from coal to cars are off to a turbulent start this year, after a host of disappointing quarterly results and weak outlooks for 2020.

- Southwest Airlines was downgraded to hold from buy at Deutsche Bank, as analyst Michael Linenberg expects another year of “sub-par growth,” as the carrier pulls Boeing’s 737 Max aircraft from its schedule through June 6.

- Things won’t pick up for smaller grocers like Sprouts Farmers Market and United Natural Foods anytime soon and there’s “plenty of potential downside from here,” according to Wells Fargo analyst Edward Joseph Kelly, who cut both stocks to underweight from equal weight.

The Economy and Bond Market

Strengths

- The number of Americans who applied for unemployment benefits in early January fell for the fifth week in a row, writes MarketWatch, giving a clean bill of health to strong U.S. labor market as 2020 got underway. Initial jobless claims declined by 10,000 to 204,000 in the seven days ended Jan 11, the government said Thursday.

- U.S. consumer sentiment remained elevated in January as record stock prices and a strong job market buoy Americans, reports Bloomberg, suggesting spending will continue its steady gains. The University of Michigan’s preliminary sentiment index for January edged down to 99.1 from a seven-month high of 99.3 in December, data showed Friday. The gauge of current conditions increased slightly to 115.8 while the expectations index ticked down to 88.3.

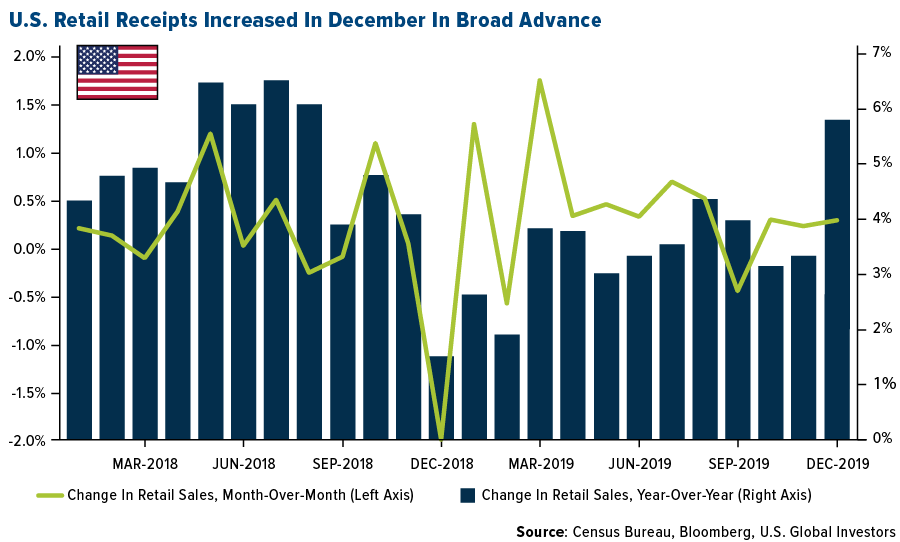

- U.S. retail sales strengthened in December, thanks to a late holiday-shopping rush that wrapped up a more-moderate year of spending at the nation’s merchants. As reported by Bloomberg, the value of receipts at retailers rose 0.3 percent, matching the prior month’s revised gain, and climbed 5.8 percent from December 2018, Commerce Department figures showed Thursday. Stronger sales occurred in all major categories except motor vehicle dealers. Excluding autos, retail purchases climbed 0.7 percent from the prior month, the most since July.

Weaknesses

- Industrial production fell 0.3 percent in December, the third decline in the past four months, the Federal Reserve reported Friday. For the fourth quarter as a whole, industrial production was down at a 0.5 percent annual rate, reports MarketWatch. Production was down in three of the four quarters of 2019. Output was down 1 percent on a year-over-year basis.

- The Federal Reserve Bank of Atlanta’s GDPNow Index latest forecast suggests U.S. GDP will expand 1.79 percent in the fourth quarter, a slowdown from previous quarters.

- A measure of U.S. bank lending is showing signs of stalling, suggesting the American economy could face headwinds in 2020. U.S. commercial and industrial lending fell by $9 billion last month to $2.35 trillion, the biggest drop since March 2017, according to Federal Reserve Bank of St. Louis data.

Opportunities

- This week, the US and China signed off the Phase 1 trade deal, ending two years of escalating trade tensions. The U.S. will roll back only a small part of tariffs implemented since January 2018, but the end to escalation is likely to benefit business and consumer confidence across the world and reduce downside risks to the global economy.

- Existing home sales released next Wednesday should end 2019 on a positive note, rising in December on the back of the previous month’s decline.

- U.S. central bankers on Wednesday expressed confidence they have borrowing costs at the right level to sustain growth and lift inflation to healthier levels, despite what businesses say is a lingering drag from uncertainty over U.S. trade policy.

Threats

- At the heart of President Donald Trump’s "monster" trade deal is a commitment by China to $200 billion in additional imports from the U.S. in the next two years. Bloomberg Economics has crunched the numbers on what would be required to make that happen. The targets for goods exports are extremely stretching. For 2020, they imply an 81 percent increase in China’s imports in the target categories, relative to the 2017 baseline that the deal specifies. The deal stipulates a relatively narrow set of goods categories that are expected to generate the increase in Chinese imports. That will make it even harder to hit an already-stretching target.

- Barclays’ macro outlook implies modestly slower growth in disposable income as slower employment growth and weak trends in manufacturing limit hours and income.

- The Leading Economic Index, released Thursday, is forecasted to post a decline in December.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was lead, which gained 4.48 percent as metal stockpiles tracked by the London Metal Exchange posted their biggest drop since 1995. Copper in London posted the longest string of gains in more than two years on Tuesday due to optimism on global growth and China reporting higher imports and exports, reports Bloomberg News. The red metal is set for a second weekly advance. Orders for LME nickel surged by 27,186 over the past eight days as of Thursday – the longest streak of gains since January 2013. Lithium producers rose after China announced that it would not further cut subsidies for electric vehicles. Bloomberg writes that lithium miners including Albermarle Corp, Livent Corp and SQM all rose more than 4 percent on the news.

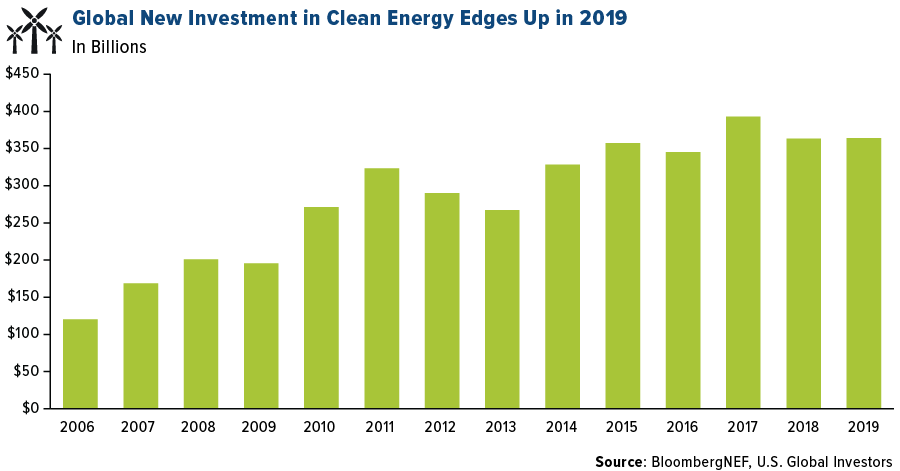

- BloombergNEF reported that global investment in renewable energy increased 1 percent in 2019 to $282 billion. Increases were led by spending in the U.S. and on offshore wind farms in Europe and Asia. Even as President Donald Trump seems to not support green energy, U.S. investment in the space rose to a record last year. A total of $55.5 billion was spent on solar and wind energy, an increase of 28 percent, as companies rush to take advantage of federal tax credits.

- China’s largest offshore oil and gas explorer, CNOOC Ltd., said it will raise spending in 2020 to the most since 2014 and revised output targets up by almost 3 percent for this year and next. Bloomberg News reports that state producers are facing government mandates to expand domestic output and enhance energy security.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 9.17 percent on forecasts of above average temperatures and abundant supplies of shale gas saturating the market. Natural gas futures sank below $2 per million British thermal units for the first time in almost four years as forecasts showed cold weather vanishing next week in the U.S. Natural gas was one of the worst performing commodities in 2019 and the 2020 outlook doesn’t look much better as production far exceeds demand for the heating fuel.

- The big news this week was that the U.S. and China officially signed “phase one” of the trade deal. Although it was meant to be a big positive for commodities, it was largely shrugged off with soybeans, cotton and corn falling on Thursday. China pledged to buy almost $95 billion worth of additional U.S. commodities as part of the deal, but the market isn’t sure that it will happen as there hasn’t been word on how China will execute the plan. Wind turbine contracts signed in the second half of 2019 continued their long-term decline, falling to $700,000 per megawatt, reports BloombergNEF. Turbine margins have fallen along with a 54 percent drop in prices since 2009. As the average capacity of machines sold is rising, buyers are getting more for their money.

- Lundin Petroleum, one of the most active explorers in the Norwegian Arctic, reduced its resource estimates for its Alta discovery in the Barents Seat and said it will not develop the project independently, reports Bloomberg. This is a blow to Norway’s hopes that there would be significant infrastructure and production from the Arctic region. There is potential for vast resources, but only two fields have started production.

Opportunities

- BlackRock Inc., which has around $7 trillion in assets under management, said this week that climate change will upend global finance sooner than they think. CEO Larry Fink wrote in an annual letter to corporate executives that “climate change has become a defining factor in companies’ long-term prospects” and “I believe we are on the edge of a fundamental reshaping of finance.” The asset manager outlined several changes including: making sustainability integral to portfolio construction and risk management, exiting investments that present a high sustainability-related risk and launching new investment products that screen fossil fuels. BlackRock had been under tremendous pressure to address climate concerns and this is positive news for the green movement.

- Germany continues to push for greener energy and has chosen trains over planes, reports Bloomberg. The country launched a $95 billion plan to modernize and expand its railway system and build out capacity to lure travelers from cars and planes. Transportation Minister Andreas Scheuer said “it’ll be the decade of the rail.” Poland, the most coal-reliant country in the EU, used less coal to generate electricity last year than any other year on record, reports Bloomberg. The European Commission will unveil an investment plan aimed at triggering $1.1 trillion worth of investments into making Poland carbon neutral by 2050.

- A new biofuel is emerging in Brazil: animal fat. Brazil launched an initiative this month to increase the use of biofuels and a ranking system in the program found that fuel made from animal fat came out on top, beating sugar-cane ethanol. According to Brazil’s oil regulator, the environmental score for animal fat biodiesel plants were as much as 20 percent higher than for cane ethanol. This gives a greener side to cattle production, which is known for being a big polluter, by reusing the waste from it.

Threats

- The U.S. shale “fracklog”, or number of oil wells that were drilled and never opened for production, has declined. The fracklog has dropped by 10 percent – a sign that explorers are no longer racing to drill wells faster than they can complete them, reports Bloomberg’s David Wethe. According to data from the U.S. Energy Information Administration, the number fell to 7,574 from a high of 8,429 from May to November last year. Haliburton Co., the owner of the world’s biggest fleet of fracking pumps, is expected to report a 29 percent earnings decline from a year earlier in the fourth quarter, according to analysts.

- According to local news reports, China’s Ministry of Finance has hinted at an end to national subsidies for offshore wind after 2021, adding to a string of recent policy changes aimed at reducing renewable subsidies. Bloomberg reports that a 40-gigawatt project pipeline is at risk and could freeze near-term project development if individual provinces do not step in to offer subsidies.

- Uniper SE, one of Germany’s biggest utilities, is set to open a new coal plant, even as the country aims to exit coal by the year 2038. Protesters plan to disrupt the opening of the $1.7 billion Datteln-4 plant in June, which is nine years late and over budget due to a delayed connection to the grid. Bloomberg writes that “the conflict could threaten Chancellor Angela Merkel’s climate legacy as German emission targets lag following a decade of record renewable energy investments.”

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 2.4 percent. Improving geopolitical tensions pushed stocks trading on the Istanbul exchange higher. This week politicians in Berlin are seeking a ceasefire deal in Libya after negotiations failed last week in Moscow.

- The Czech koruna was the best performing currency this week, gaining 30 basis points. All emerging European currencies fell, except the koruna, as the U.S. dollar strengthened. The koruna benefited from higher-than-expected inflation in the Czech Republic as well as the signing of the U.S.-China trade agreement.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 2.1 percent. European Parliament called for additional measures to discipline Hungary and Poland for breaking the rule of law. Shares of OTP Bank recorded significant losses over the past five days among stocks trading on the Budapest exchange.

- The Russian ruble was the worst performing currency in the region this week, losing 94 basis points. Political noise put pressure on the currency. This week, the Prime Minister of Russia resigned and a new cabinet will need to be formed under the new Prime Minister Mikhail Mishustin.

- Energy was the worst performing sector among eastern European markets this week.

Opportunities

- Russian Prime Minister Dimitry Medvedev resigned, and Mikhail Mishustin will be the new Prime Minister. Putin called for a series of constitutional changes that may allow him to stay in power long after he steps down as a President. These changes would require a national referendum, and in order for the referendum to pass smoothly, social spending would increase. In addition, a shrinking population is a threat to Russia’s future, as some new benefits for families were announced already with more to follow.

- After implementing three bailout programs during a decade of severe austerity, Greece will be the euro-area country with the largest fiscal expansion in 2020, according to Moody’s Investors Service. The new government, which came to power last July, has already voted a package of measures that include reductions in taxes for companies and households. Greece also plans to renegotiate its primary surplus targets for 2021 and 2022 with European creditors.

- Bloomberg economists expect a small recovery in the eurozone’s Manufacturing PMI. Preliminary January data may show a small uptick to 46.8 from 46.3 in December. Service PMI is to remain unchanged at 52.8, but Composite PMI should improve, moving away from the 50 level that separates growth from contraction. Preliminary PMI data will come out next Friday.

Threats

- Turkey posted a larger deficit then expected in the month of November of $518 million versus $400 million, after running a surplus for four months. The decrease brought the annualized surplus to $2.7 billion, from a $33.4 billion deficit in the same period last year. It is expected that the Turkey’s current account will slowly fall back into a larger deficit as a more stable lira will support consumer demand and imports. According to the government, the current account will return to a deficit of 1.2 percent of gross domestic product in 2020 and 0.8 percent in 2021 after recording a slight surplus last year.

- Recent Polish Central Bank data show that local lenders scaled down sales of consumer loans after the European Court of Justice ordered them to partially reimburse upfront fees in case of early repayment. New sales of cash loans to households fell 12 percent to 5.48 zloty in November, the lowest level since February 2018, after dropping 3.8 percent year-over-year in October.

- Reuters reported on European Central Bank (ECB) data Wednesday which showed that eurozone banks increased their net interest income in the first nine months of last year, despite incessant complaints that negative central bank rates are wiping out their most basic form of income. The biggest lenders in the bloc had net interest income of €202.9B in the first three quarters, up from €194.4B a year earlier, the highest nine-month figure since the ECB started supervision in late 2014. Overall income rose but banks’ combined net profit still fell 8 percent, as costs continued to rise and risk provisions surged.

China Region

Strengths

- Korea’s KOSPI jumped 2.00 percent on the week, tops in the region and pushing up to an impressive 52-week high after a long year and steady climb back up over the second half.

- Telecommunications was the top performing Hang Seng Composite Index sector in Hong Kong for the second full week of trading in calendar year 2020, rising 2.85 percent.

- China’s fourth-quarter GDP print clocked in at 6.0 percent on a year-over-year basis, leaving the overall 2019 number well within the governmental guidance and holding steady from the prior third-quarter print. Industrial production and retail sales also came in as mild beats for the last month of 2019, showing what may be a sign of an overall pick-up in the economy.

Weaknesses

- The Philippines Stock Exchange Index dropped 70 basis points for the week, and China’s Shanghai Composite, despite the trade signing ceremony in Washington this week, declined by 54 basis points on the week. Other regional indices were up and finished green.

- Energy was the poorest-performing HSCI sector for this second full week of 2020, dropping by 0.74 percent, the only sector to close in the red.

- Overseas remittances to the Philippines came in lighter than expected at a 2.0 percent year-over-year growth rate for the November (latest) measurement period, below expectations for a 4.6 percent rate and down from the prior reading of 8.0.

Oppurtunites

- Phase One. The Big Uno. Sandwiched right in between the U.S. holidays/calendrical new year and the rapidly-approaching Chinese holidays/Lunar New Year comes the official arrival and signing of the U.S.-China Phase One trade agreement. Cheers everyone, and here’s to the upcoming Year of the Rat!

- Take a gander at Korea’s KOSPI. Some charts speak for themselves, technicians believe, and thus there is no commentary necessary here…

- Taiwan, like (though of course unique from) Hong Kong, dealt Beijing a bit of a slap in the face as Taiwanese incumbent President Tsai Ing-wen was handily re-elected—she remains quite standoffish from the mainland, and Ms. Tsai a surge in her polling numbers throughout the Hong Kong pro-democracy protests against Beijing’s (over?) reach and influence. The election is now wrapped up, the status quo remains, and Taiwan (which you may recall was tops in the region for index performance in 2019, up nearly 29 percent on the year) remains just off its 52-week highs.

Threats

- “Enforceable” is how the U.S. side is referring to promises about a lack of untoward interventions in the Chinese yuan amid the trade deal, signaling that the U.S. mean to play hard ball if necessary on the matter. While this is not, of course—especially in a Phase One honeymoon period—a threat of anything imminent, it remains one to keep in the back of one’s mind heading into the rest of the year as China aims to make good on its purchase promises, as we head into U.S. elections, and as we get closer to the eventual revisiting of China trade issues after the U.S. election outcomes shape up. Of course, the very nature of enforceable deals and agreements between parties is also part of what makes the rule of law and free markets work the world round, so in fact contained within the “threat”-ening language of enforceability is also a seed of expectations for the growth and flowering of productive trade, greater transparency, all amid (perhaps) next and later stages of a larger and more comprehensive deal. (And of course, should yuan strength aid in keeping the dollar at all relatively weaker while trade and perhaps inflation picks up, that could be just the sort of thing at U.S. Global Investors that makes EM and resource and gold investors smile in particular. Time will tell…)

- It is conceivable that following the formal signing of the trade deal and the conclusion of the initial Phase One agreement now, with Asian markets thinning out around the Lunar New Year closures and U.S. holidays now well behind us, that the exuberant markets pause or perhaps retrace to some degree. This is, of course, hardly guaranteed, but again, after a relatively fast and furious December and January-to-date, details of the deal now out, and Asian holidays forthcoming, it is conceivably a realistic sort of threat (even if considered only as the possibility of a pause or change in pace rather than of overall trend).

- While the latest data suggest a possible pick-up in Chinese growth—and China is stimulating, don’t forget—it also remains conceivable that this is not yet the case, or at least not yet convincingly so, and investors will surely be scrutinizing this quarter’s data looking for further signs of progress.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended January 17 was Game Stars, up 577.97 percent.

- Traders and analysts alike were surprised at the start of the week when bitcoin broke out of its already bullish channel to strike at resistance levels near $8,600, reports CoinTelegraph. The leg up on January 14 brought the cryptocurrency’s 24-hour gains to almost 8 percent and hitting a two-month high. Then, by Friday, the popular coin hit $9,000.

- JPMorgan Chase and Co. has entered a partnership with swytchX to use blockchain to help it reach 100 percent renewable energy by the end of 2020, reports S&P Global Platts. This project will allow both companies to track JPMorgan’s energy output, usage and environmental indicators.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended January 17 was QURA GLOBAL, down 98.16 percent.

- According to the latest Texas Investor Guide put out by the State Securities Board, and as reported by CoinTelegraph, Texas regulators have included cryptocurrencies in their list of top threats to investors. They note the digital assets as being extremely volatile and difficult to understand for a non-professional trader, advising potential investors not to contribute to crypto offerings unless they can determine some basic facts about the company and its physical location.

- An announcement on January 15 by Binance’s Japanese support website, reveals that the exchange is restricting access to residents of Japan at an “unspecified later date.” The company was previously headquartered in Japan until exiting Chia and moving its operations to Malta following an official warning by Japanese regulators due to its lack of a national exchange license, explains CoinTelegraph. Currently, there are no restrictions in place and Japanese users can operate normal, but it is said that the restrictions will be implemented gradually.

Opportunities

- Dish Network, one of the largest U.S. television providers, has published a patent application for a new “anti-piracy management system,” that uses blockchain technology, reports CoinDesk. Published by the patent office Thursday, Dish says the proposal can better monitor and enforce ownership rights, alerting platforms to when content is used without permission.

- In a new report compiled by jobs site LinkedIn, blockchain is listed as the number one “hard skill” for the year 2020, writes CoinDesk. “Last year, cloud computing, artificial intelligence and analytical reasoning led LinkedIn’s global list of the most in-demand hard skills,” LinkedIn wrote in the report. “They’re all on the list again this year, but a skill we weren’t looking at a year ago – blockchain – tops the list of most in-demand hard skills for 2020.”

- The cryptocurrency exchange founded by the Winklevoss twins, Gemini, has created its own insurance company in order to protect clients against the potential loss of coins from its offline vaults, writes CoinDesk, with a possibly record-breaking $200 million coverage limit.

Threats

- Mark Cheng, a Singaporean cryptocurrency consultant, was recently kidnapped in Thailand and tortured for a $740,000 ransom in bitcoin, reports the South China Morning Post and CoinTelegraph. Cheng was on a business trip when a group of masked men grabbed he and associate Kim Lee Yai Wei and pulled them into a nearby truck. Cheng was only able to provide $46,000 to the captors, and was luckily able to escape shortly after.

- On January 16 the Bangkok Post reported that around 20 investors have fallen victim to an alleged cryptocurrency pyramid scheme in Thailand, and are now taking their case to the country’s Department of Special Investigation. Losses total around $2.5 million. As reported by CoinTelegraph, the scheme promised returns of as high as 8 percent weekly, with locals selling off their assets including private land, cars and motorcycles to raise the money for their investments.

- New Hampshire lawmakers in the state legislature have killed a bill that would have allowed state agencies to accept cryptocurrencies as payment for taxes, reports CoinTelegraph. Authorities considered the bill ineffective due to the high volatility of cryptocurrencies, the article explains, and if the bill was adopted, expenditures of the Department of Revenue Administration (DRA) would have surged by an “indeterminable amount” in the fiscal year of 2020.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.82 | +0.00 | +0.16% |

| Oil Futures | 58.68 | -0.36 | -0.61% |

| Hang Seng Composite Index | 3,979.54 | +70.82 | +1.81% |

| S&P Basic Materials | 383.98 | +10.09 | +2.70% |

| Korean KOSPI Index | 2,250.57 | +44.18 | +2.00% |

| S&P Energy | 448.77 | -5.10 | -1.12% |

| Nasdaq | 9,388.94 | +210.08 | +2.29% |

| DJIA | 29,348.10 | +524.33 | +1.82% |

| Russell 2000 | 1,699.64 | +41.99 | +2.53% |

| S&P 500 | 3,329.62 | +64.27 | +1.97% |

| Gold Futures | 1,556.90 | -3.20 | -0.21% |

| XAU | 101.84 | -0.41 | -0.40% |

| S&P/TSX VENTURE COMP IDX | 584.50 | +2.15 | +0.37% |

| S&P/TSX Global Gold Index | 255.74 | +1.08 | +0.42% |

| Natural Gas Futures | 2.00 | -0.20 | -8.99% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,250.57 | +55.81 | +2.54% |

| 10-Yr Treasury Bond | 1.82 | -0.09 | -4.90% |

| Gold Futures | 1,556.90 | +78.20 | +5.29% |

| S&P Basic Materials | 383.98 | +4.87 | +1.28% |

| S&P 500 | 3,329.62 | +138.48 | +4.34% |

| DJIA | 29,348.10 | +1,108.82 | +3.93% |

| Nasdaq | 9,388.94 | +561.21 | +6.36% |

| Oil Futures | 58.68 | -2.25 | -3.69% |

| Hang Seng Composite Index | 3,979.54 | +188.58 | +4.97% |

| S&P/TSX Global Gold Index | 255.74 | +8.25 | +3.33% |

| XAU | 101.84 | +2.29 | +2.30% |

| Russell 2000 | 1,699.64 | +37.90 | +2.28% |

| S&P Energy | 448.77 | -0.06 | -0.01% |

| S&P/TSX VENTURE COMP IDX | 584.50 | +45.79 | +8.50% |

| Natural Gas Futures | 2.00 | -0.28 | -12.34% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 101.84 | +11.82 | +13.13% |

| S&P/TSX Global Gold Index | 255.74 | +17.78 | +7.47% |

| Gold Futures | 1,556.90 | +51.70 | +3.43% |

| DJIA | 29,348.10 | +2,322.22 | +8.59% |

| S&P 500 | 3,329.62 | +331.67 | +11.06% |

| Nasdaq | 9,388.94 | +1,232.09 | +15.10% |

| Korean KOSPI Index | 2,250.57 | +172.63 | +8.31% |

| Natural Gas Futures | 2.00 | -0.31 | -13.55% |

| S&P Basic Materials | 383.98 | +23.01 | +6.37% |

| Russell 2000 | 1,699.64 | +157.79 | +10.23% |

| Oil Futures | 58.68 | +4.75 | +8.81% |

| Hang Seng Composite Index | 3,979.54 | +356.57 | +9.84% |

| S&P/TSX VENTURE COMP IDX | 584.50 | +40.43 | +7.43% |

| S&P Energy | 448.77 | +25.80 | +6.10% |

| 10-Yr Treasury Bond | 1.82 | +0.07 | +4.05% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

CNOOC Ltd.

OTP Bank

SPDR Gold Shares

Roxgold Inc.

Group Ten Metals Inc.

Southwest Airlines Co

The Boeing Co

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy. The Philippine Stock Exchange PSEi Index is composed of stocks representative of the industrial, properties, services, holding firms, financial and mining & oil sectors of the Philippines Stock Exchange. The S&P/TSX 60 Index is a stock market index of 60 large companies listed on the Toronto Stock Exchange. Maintained by the Canadian S&P Index Committee, a unit of Standard & Poor’s, it exposes the investor to ten industry sectors.