Congress and the Fed Just Opened the Stimulus Floodgates

Date Posted: March 27, 2020

Read time: 57 min

Extraordinary times call for extraordinary measures, as they say, and this past week has been nothing if not total confirmation of that adage. As of Friday morning, the number of confirmed coronavirus cases in the U.S. stood at more than 86,000. That's now more than any other nation on earth, including China. New York City, home to roughly half of all U.S. cases, appears to have become the new global epicenter of the pandemic.

U.S. Global Investors Continues GROW Dividends

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Extraordinary times call for extraordinary measures, as they say, and this past week has been nothing if not total confirmation of that adage.

As of Friday morning, the number of confirmed coronavirus cases in the U.S. stood at more than 86,000. That’s now more than any other nation on earth, including China. New York City, home to roughly half of all U.S. cases, appears to have become the new global epicenter of the pandemic.

Hospitals in the hardest-hit areas of the countries “have passed a tipping point,” writes the Wall Street Journal, with New York having to quickly set up makeshift treatment centers and morgues to meet the spread of infection.

The news comes at a time when President Donald Trump is weighing whether the “cure”––social distancing, business closures and more––is worse than the problem itself.

To be clear, the “cure” has taken an unprecedented toll on the U.S. and world economies.

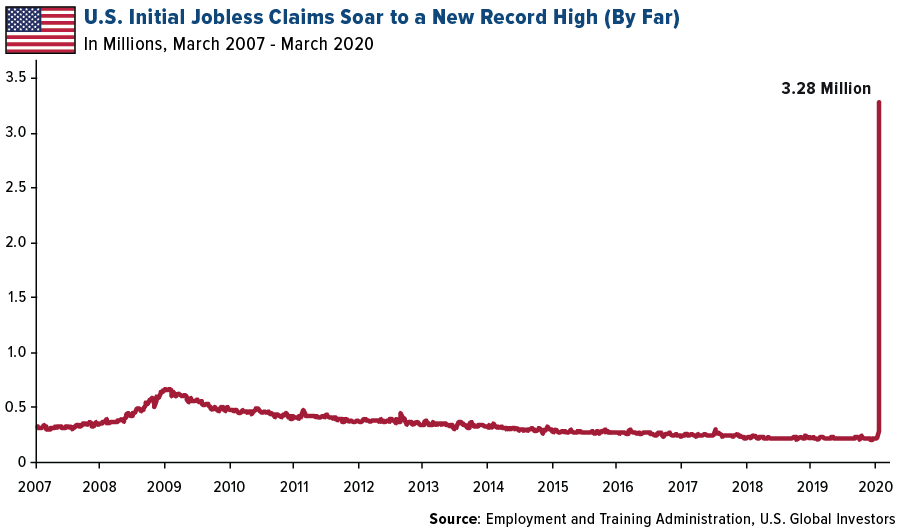

Initial jobless claims soared to a new record high of 3.28 million people as layoffs around the country have accelerated. As recently as February, the weekly figure was little more than 200,000, a historically low number, showing just how rapid the economic deterioration has been. The tidal wave of people seeking jobless benefits this week was so great, in fact, that state-run unemployment websites reportedly couldn’t handle the traffic and were crashing.

In a press conference following the data’s release, Treasury Secretary Steven Mnuchin called the jobless number “not relevant,” saying that the president “is protecting those people.”

Indeed, “protection” is on the way, with Congress and the Federal Reserve both opening the stimulus floodgates as we’ve never seen before.

Trillions in Assistance Headed to U.S. Families and Businesses, Including Airlines

On Friday, Congress approved and President Trump signed into law a $2.2 trillion emergency economic stimulus package, the largest in U.S. history, meaning sometime soon, most American adults will be receiving a one-time payment of $1,200 in cash. (The median personal income in the U.S. as of last year was around $40,000, well below the $75,000 cutoff point to receive the full amount.) On top of that, families will receive $500 per child.

Remarkably, the final vote in the Senate for the landmark bill was a unanimous 96 to 0, which demonstrates to me just how united lawmakers are in getting help to struggling families and businesses. In 2009, when the Senate voted in favor of the $787 billion stimulus bill to mitigate the impact of the financial crisis, the tally was 60 to 38––just barely enough to pass.

Included within the stimulus package is $50 billion in earmarked liquidity for coronavirus-hit domestic airlines. This includes $25 billion in loans and guarantees for passenger carriers and $25 billion in direct grants.

I’m pleased to see that airline stocks have bounced off their lows as deep-value investors such as Warren Buffett have sought discounted exposure to an industry that I believe most people consider essential in today’s interconnected world. Some 2.8 million passengers flew every day in and out of U.S. airports in 2019, according to the Federal Aviation Administration (FAA). The industry also generated a whopping 10.6 million U.S. jobs, or 1 out of every 15 jobs.

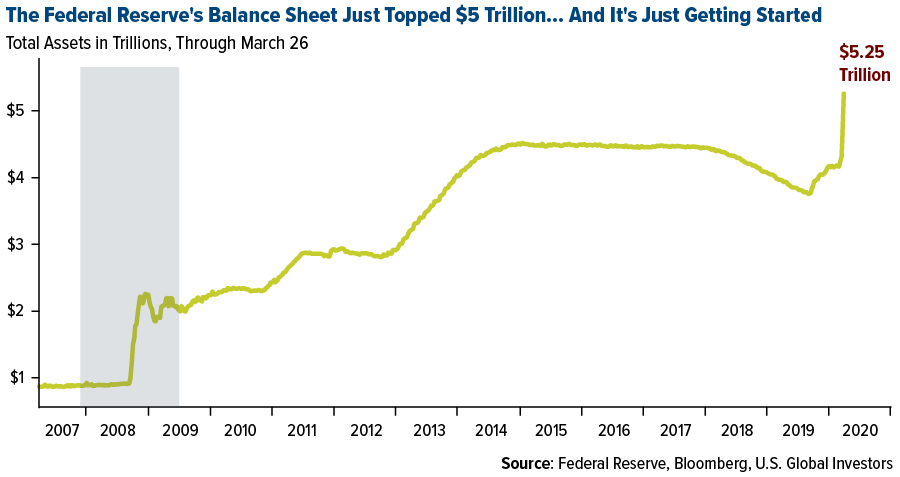

As for the Federal Reserve, the central bank is poised to “spray trillions of dollars into the U.S. economy,” according to Bloomberg. As of March 26, the size of the Fed’s balance sheet had shot up to a never-before-seen $5.25 trillion, far beyond anything it did in the months and years following the financial crisis.

Time to Buy the Gold Miners?

As I’ve discussed plenty of times before, such massive levels of money printing has historically been supportive of gold. In September 2011, when the Fed was rapidly expanding its balance sheet, the precious metal’s price hit its all-time high of $1,900 an ounce.

With real rates already below 0 percent, the Fed has little choice right now than to jump directly to extreme measures. That means loading up on Treasuries and mortgage-backed securities (MBS) “in the amount needed,” as the central bank put it in a press release dated March 23.

I believe this policy will once again be constructive for gold, and so it may be prudent to consider buying not just physical gold, but also the gold miners.

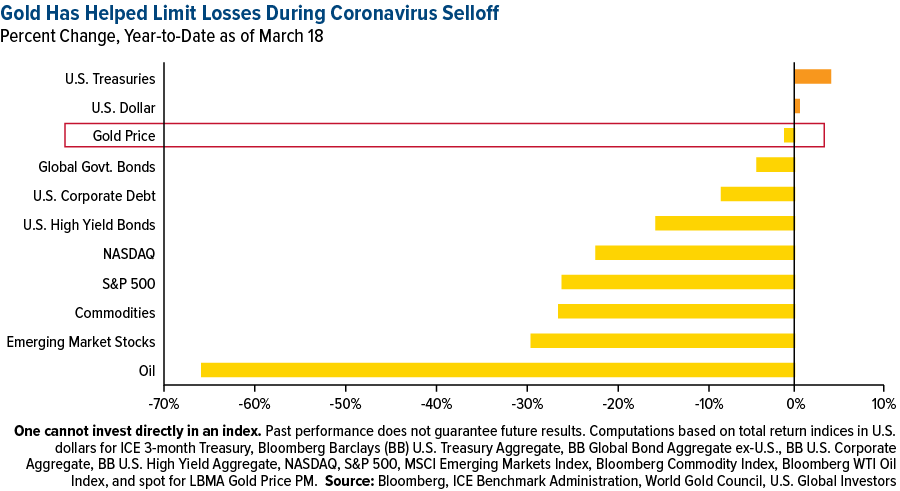

The strategy has been a good one so far this year, as you can see in the chart below. Compared to other major assets, gold’s decline was minimal year-to-date through March 18, helping investors limit net losses in their portfolios.

As for gold mining companies, shares have fallen with the broader stock market, but I believe producers are beginning to look very attractive as investors take note of the revenue and free cash flow they’re generating because of higher metal prices. On Monday, the price of gold ended the day up $83 an ounce, or 5.6 percent––the biggest single-day dollar amount gain in the history of gold trading. The previous record was set on October 25, 2011, when it advanced $70 an ounce.

We’ll see the final results when gold and precious metal miners report quarterly earnings, but if you’re asking for my opinion now, I think they’re in a good position to beat expectations.

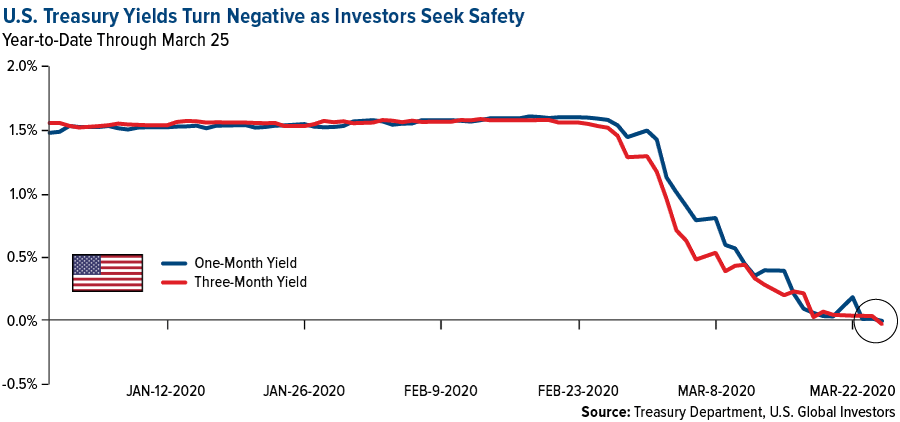

Short-term Treasury yields dipped below 0 percent on Monday, meaning if you held them to maturity, you would be guaranteed a loss. I believe investors seeking a safe haven right now would be better off buying gold and gold mining stocks.

Once-in-a-Lifetime Buying Opportunities

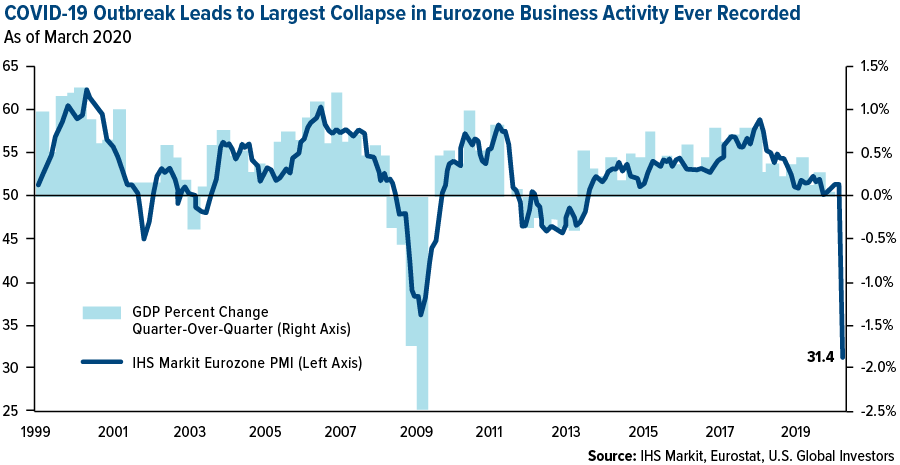

And if it’s equities you’re looking for, there couldn’t be a better time than now to go bargain hunting. Business activity in the eurozone collapsed at the fastest rate ever recorded by IHS Markit in March. The composite purchasing manager’s index (PMI), which includes both the manufacturing and services sectors, plunged from 51.6 in February to 31.4, the lowest reading on record since the series began––lower even than during the global financial crisis.

As a reminder, this is preliminary data. We’ll have the final results next week, but I don’t expect to see much change.

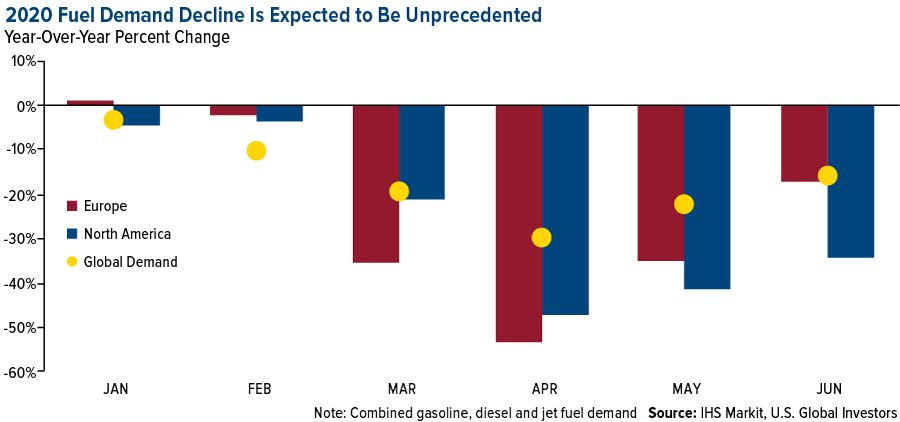

Take a look at the impact the virus may have on global fuel demand. IHS Markit has modeled out what it believes will be fuel consumption declines on a scale that’s never occurred before, due to widespread restrictions on travel that’s deeply affected commerce. Although this is a pandemic, “demand destruction will be most severe in Europe and North America,” writes Rob Smith, director of IHS Markit’s Refining and Marketing group. In April, European and North American fuel demand could drop by half (or more!) compared to the same month in 2019.

“Most airlines are culling their flight schedule by upwards of 50 percent,” Smith says, “with most European airlines cancelling better than 90 percent of their flights. And speaking of Europe, commuter vehicle traffic in heavily affected cities like Milan, Paris and Madrid has fallen as much as 80 percent after lockdown measures took effect. Meanwhile, vehicle mileage in the U.S. is “only” expected to contract by 55 percent.”

“The global auto industry,” IHS Markit continues in a press release dated March 26, “is expected to witness an unprecedented and almost instant stalling of demand in 2020, with global auto sales forecast to plummet more than 12 percent from 2019, to 78.8 million units.”

As I said earlier, these could be buying opportunities!

Interested in learning more on the gold market? Watch my interview with Investing New Network (INN) by clicking here!

March 26, 2020America Will Come Out of This Stronger Than Ever. It’s Done It Before |

March 23, 2020The World Responds to Its New Threat: A Virus |

March 23, 2020A $10 Trillion Response to the Global Pandemic |

|||

Gold Market

This week spot gold closed at $1,628.16, up $129.51 per ounce, or 8.64 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher/lower by 17.29 percent. The S&P/TSX Venture Index came in up 8.99 percent. The U.S. Trade-Weighted Dollar fell 4.40 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-24 | New Home Sales | 750k | 765k | 800k |

| Mar-25 | Durable Goods Orders | -0.9% | 1.2% | 0.1% |

| Mar-25 | Hong Kong Exports YoY | -20.0% | 4.3% | -22.7% |

| Mar-26 | GDP Annualized QoQ | 2.1% | 2.1% | 2.1% |

| Mar-26 | Initial Jobless Claims | 1700k | 3283k | 282k |

| Mar-30 | Germany CPI YoY | 1.3% | — | 1.7% |

| Mar-31 | Eurozone CPI Core YoY | 1.1% | — | 1.2% |

| Mar-31 | Conf. Board Consumer Confidence | 114.0 | — | 130.7 |

| Mar-31 | Caixin China PMI Mfg | 45.0 | — | 40.3 |

| Apr-1 | ADP Employement Change | -125k | — | 183k |

| Apr-1 | ISM Manufacturing | 46.0 | — | 50.1 |

| Apr-2 | Initial Jobless Claims | — | — | 3283k |

| Apr-2 | Durable Goods Orders | — | — | 1.2% |

| Apr-3 | Change in Nonfarm Payrolls | -81k | — | 273k |

Strengths

-

The best performing metal this week was palladium, up 37.90 percent, essentially regaining all the losses from the prior two weeks. Platinum and silver also rebounded strongly. Gold headed for its biggest weekly gain since 2008 while platinum and palladium were on track for their biggest weekly increases on record. It was a smashing week for precious metals due to supply concerns over mine shutdowns in top producing South Africa. Palladium surged more than 20 percent on Tuesday, its biggest ever gain, after South Africa announced a 21-day coronavirus lockdown. Dmitry Glushakov, head of metals and mining research at VTC Capital, said the country “accounts for some 70 percent of global platinum mined supply and 35 percent of palladium, with a 21-day lockdown possibly resulting in a 4 percent and 2 percent of 2020 supply reduction respectively.”

- CME Group is planning to offer a new futures contract with expanded delivery options that include 100-troy ounce, 400-troy ounce and one-kilo gold bars, reports Bloomberg News. Derek Sammann, senior managing director and global head of commodity and options products for CME Group, said that “this time of unprecedented market conditions has led to growing demand for a broader range of delivery needs for our clients worldwide.” Silver demand is finally seeing some love. The Perth Mint reported a surge in demand, so much so, that it is diverting production resources to meet demand for the popular one ounce Silver Kangaroo coin. The U.S. Mint sold out of American Eagle silver coins and the closing of the Royal Canadian Mint has squeezed supply even further.

- Gold had its best two-day gain since 2016 on Monday, climbing 3.8 percent since last Thursday, after the Fed announced a huge second wave of initiatives to support the U.S. economy. Ole Hansen, head of commodity strategy at Saxo Bank A/S, says “it’s a really aggressive message made by the Fed” and is a long-awaited relief for risk-on assets and gold, which had suffered recently from deleveraging. Economic damage expected from the virus has boosted bullion’s safe haven appeal.

Weaknesses

-

The worst performing metal this week was gold, up 8.64 percent. The gold market was thrown in a frenzy this week as investors rushed to get their hands on the metal amid a supply crunch. Logistical disruptions led to a wide divergence of prices in the U.S. and London. Contracts for delivery in New York were trading at a $60 premium to London – the highest premium since the 1980s. Bloomberg reports that most banks and traders ship gold around the world on commercial flights. But with most flights canceled and refineries closing due to lockdowns, it has become more challenging to buy and sell the metal.

- Metalor’s gold refinery in Singapore is running at much-reduced capacity due to a manpower shortage. There is a movement-control order in Malaysia where many workers live. Switzerland’s gold refining hub, the biggest in Europe, halted output. Ludwig Karl, a board member of Swiss Gold Safe, an operator of high security vaults, said “It’s absolutely crazy what’s going on. Right now, if somebody wants to buy gold, I wish them all the best in finding it. Most of the bullion dealers are closed.”

- The All India Gem and Jewellery Domestic Council estimates that total purchases of gold jewelry in India are set to fall 30 percent in 2020. Demand had already been hit for months due to high domestic prices and slow economic growth. But now with the added virus threat and the entire county on lockdown, demand could fall to the lowest since 1995. The lockdown will prevent gold shops from opening and a drop in the rupee is keeping local gold prices elevated, reports Bloomberg.

Opportunities

- Gold may reach $2,500 per ounce in the third quarter due to Fed stimulus, says B Riley FBR analysts led by Adam Graf in a note this week. “Regardless of how much longer recession conditions will continue and how much further general equity markets might retreat, extreme monetary and fiscal stimulus policies enacted on a global basis will have repercussions.” Graf upgraded Royal Gold to buy from neutral and recommends that investors be overweight gold and gold equities, reports Bloomberg.

- Goldman Sachs Group said gold bullion is at an inflection point and it is time to buy as the metal extended its rally on a fresh wave of stimulus measures. Goldman says the Fed’s move will help alleviate the funding stress that had driven gold lower and that investors would now pivot to focus on the expansion of its balance sheet, just as it did in 2008, reports Bloomberg. The U.S. finally passed its $2.2 trillion stimulus package on Friday – growing the deficit even further. Lastly, the analysts highlighted the rise in deficits of developed economies and how “this will likely lead to debasement concerns similar to the post Global Financial Crisis period.”

- While ounces produced may be down in 2020 due to the lockdowns, the margins for gold miners may be better, writes Michael McCrae of Kitco News. One-third of NYSE-listed senior gold miners have withdrawn 2020 production guidance as more and more mines are taken offline. Although this setback could be negative, miners are actually in good shape to weather the downturn, especially with oil prices as low as they are. Additionally, gold miners are “cashed up” due to gold performing well in 2019.

Threats

- The Rand Refinery in South Africa will operate at reduced capacity during the nation’s 21-day lockdown. If the refinery has to do a complete shutdown, it would have a domino effect on the production across the continent. With the refinery closed, mines would stockpile their mined gold on the surface, which would create heightened security risks.

- Treasury holdings by foreign central banks held in custody at the New York Fed fell $31 billion to a two-year low of $2.9 trillion in the week ended March 18. Bloomberg reports that this is likely due to Middle Eastern countries raising cash to balance their budgets as oil prices plummet. Ye Xie, markets reporter, writes that “with low oil prices and shrinking current accounts in emerging markets and China, President Trump can’t count on foreign central banks to take on more Treasuries.”

- President Trump said that he wants the U.S. economy to “reopen” by Easter, but it could end up having severe health and economic consequences after recently implementing strict social distancing policies and shutdowns. The President, and others, fear that the economic consequences of such a long shutdown will be severe, but the number of lives that could be lost if the virus continues to spread rapidly would also be severe. The U.S. became the country with the most number of cases of COVID-19 this week. Nearly half of all Americans have been ordered to stay at home and avoid contact with others and each state is individually determining lockdown measures.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 12.84 percent. The S&P 500 Stock Index rose 10.26 percent, while the Nasdaq Composite climbed 9.05 percent. The Russell 2000 small capitalization index gained 11.65 percent this week.

- The Hang Seng Composite gained 3.95 percent this week; while Taiwan was up 5.03 percent and the KOSPI rose 9.68 percent.

- The 10-year Treasury bond yield fell 16 basis points to 0.686 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing 17.68 percent compared to an overall increase of 10.26 percent for the S&P 500.

- Boeing was the best performing S&P 500 stock for the week, increasing 70.51 percent.

- U.S. stocks weathered a late Friday plunge to post their best week in over 10 years, buoyed by an unprecedented stimulus package meant to blunt the economic impact of the coronavirus pandemic. The S&P 500 Index climbed 10 percent this week, its biggest gain since March 2009, on the strength of a record three-day rally. Nonetheless, the index remains 25 percent below its February record.

Weaknesses

- Communication services was the worst performing sector for the week, increasing 5.50 percent compared to an overall increase of 10.26 percent for the S&P 500.

- Nordstrom was the worst performing S&P 500 stock for the week, falling 10.36 percent.

- S&P Global Ratings and Moody’s Investors Service are downgrading U.S. companies at the fastest pace in more than a decade as debt-saddled corporations and entire industries struggle with a dramatic slump in demand brought on by the coronavirus pandemic. Downgrades are outpacing upgrades at the two biggest credit-rating firms by more than three to one to start the year, the most on a quarterly basis since the depths of the financial crisis, according to data compiled by Bloomberg. At the same time, risk premiums on investment-grade bonds have surged, while junk yields breached 10 percent for the first time in more than eight years. From autos to oil, investment grade to high yield, few parts of the American credit landscape have been spared the onslaught of downgrades that has accompanied the Covid-19 outbreak.

Opportunities

- Walmart upped its minimum wage in e-commerce warehouses by $2 as orders surge on virus worries. The hike boosts entry-level pay to between $15 and $19 an hour from now through May 25.

- The stimulus is likely to be very good news for any company in the business of lending money. Among other things, the stimulus provides immediate cash payments to most U.S. households, expands unemployment benefits, and suspends student loan payments for six months. This could benefit credit card lending companies such as American Express, Discover Financial Services and Capital One. <

- SoftBank plans to sell up to $41 billion assets to fund another share buyback and reduce debt. The Japanese tech conglomerate wants to finance a $45 billion buyback, on top of a $4.5 billion buyback it announced earlier this month.

Threats

- percent of its total U.S. workforce as the coronavirus outbreak saps demand for commercial air travel and upends the global economy. There will be a temporary lack of work impacting approximately 50 percent of its U.S. maintenance, repair and overhaul employees for 90 days.

- Facebook’s ad business is being hurt by coronavirus even though the lockdown has caused unprecedented usage. Much of the activity is on unmonetized services, while advertisers are pulling back due to the pandemic.

- General Motors suspended its 2020 outlook, and plans to draw down $16 billion in credit. The auto giant wants to bolster its liquidity as coronavirus weighs on its business.

The Economy and Bond Market

Strengths

- The economy grew by a moderate 2.1 percent in the fourth quarter of last year, the Commerce Department said Thursday in its third and final look at the fourth quarter. Growth was unchanged from its previous estimate, but the components were slightly altered with consumer spending stronger and government spending and business investment lower.

- In an NBC interview, Fed Chairman Jerome Powell said the Fed was prepared to do more and he said those efforts should help the economy emerge in good shape to rebound from a brief downturn. “When it comes to this lending, we’re not going to run out of ammunition, that doesn’t happen. We still have policy room in other dimensions to support the economy. We’re trying to create a bridge from a very strong economy to another place of economic strength,” Powell told NBC’s Savannah Guthrie.

- New orders for long-lasting U.S. manufactured goods unexpectedly rose in February. Orders for durable goods, items ranging from toasters to aircraft that are meant to last three years or more, accelerated 1.2 percent last month. Economists polled by Reuters had forecast durable goods orders dropping 0.8 percent in February. Future orders are set to decline as strict measures to contain the coronavirus pandemic hurt demand.

Weaknesses

- The number of people who filed claims for unemployment insurance in the U.S. last week surged to an all-time high as the coronavirus pandemic spurred layoffs across the country. Weekly jobless claims for the week ending March 21 totaled 3,283,000, the Labor Department reported Thursday, exceeding the consensus analyst forecast of 1.5 million. That was up from 281,000 in the previous week, which already marked a two-year high. The latest number is by far the largest on record for a single week, exceeding the record of nearly 700,000 newly filed jobless claims set in 1982.

- The number of people in the U.S. who have tested positive for COVID-19 has now surpassed the number of cases in China and Italy. There are a total of 97,028 cases and at least 1,475 people have died in the U.S. according to the latest data. The tally is expected to rise as testing grows.

- The International Monetary Fund (IMF) said it expects a global recession this year that will be at least as severe as the downturn during the financial crisis more than a decade ago, followed by a recovery in 2021. Nearly 80 countries have asked the Washington-based IMF for emergency finance, Managing Director Kristalina Georgieva said in a statement Monday following a conference call of Group of 20 finance ministers and central bankers.

Opportunities

- Should economic data and negative virus developments trigger another bout of turbulence in the markets, the U.S. dollar is likely to benefit from safe haven demand and head higher again.

- The non-farm payrolls report next week is predicted to be grim, with the economy expected to have lost jobs for the first time since 2010. Forecasts are for nonfarm payrolls to drop by 123,000 in March, versus a gain of 273,000 in February. The unemployment rate is expected to jump to 3.9 percent.

- Vice President Mike Pence said that the fundamentals of the U.S. economy remain strong despite the coronavirus pandemic that has tanked markets and led to unprecedented layoffs of millions. “While the stock market has ebbed and flowed, and even this week made dramatic moves, President Trump and our entire economic team believe that all the fundamentals continue to be strong,” Pence told CNBC.

Threats

- percent, the Fed’s James Bullard warns. "It is a huge shock and we are trying to cope with it and keep it under control," the St. Louis Fed president told Bloomberg.

- A key data point to watch next week will be the Conference Board’s consumer confidence Index on Tuesday. The consumer is one of the main pillars of the economy, but with people being asked to stay at home, that vital support is expected to disappear over the next few months. Retail sales were already down in February before the U.S. was too impacted by the virus. The consumer confidence index is expected to drop from 130.7 to 111.5 in March.

- The ISM PMIs are likely to be negative next week when released for March. The manufacturing PMI just avoided contraction in February, but is forecast to fall to 44.3 this month, which would be the lowest since 2009.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was uranium, as measured using Uranium Participation Corp as the price proxy, which gained 14.33 percent as there is concern with some uranium mines being impacted supplies could dwindle. Copper had its biggest gain in six years on Tuesday after U.S. and European stocks rallied after measures from the Federal Reserve were released to boost the economy from the coronavirus outbreak. The red metal was up as much as 5.4 percent for the day.

- According to a European Union document obtained by Bloomberg, heads of government met by video on Thursday to consider a proposal that would ensure their emergency measures to help the economy would be compatible with principles set out in the Green Deal. A draft of a statement after the meeting says that “the urgency is presently on fighting the coronavirus pandemic and its immediate consequences. We should, however, start to prepare the means necessary to get back to a normal functioning of our societies and to sustainable growth, integrating the green transition and the digital transformation and drawing all lessons from the crisis.”

- According to customs data, China’s liquified natural gas (LNG) imports from Australia rose to 4.99 tons in the first two months of this year, up from 4.12 million a year earlier. China did not buy any LNG from the U.S. in that same period, continuing a streak of zero purchases since May 2019 due to the trade war, reports Bloomberg. Although negative for U.S. LNG, this is positive for Australia LNG suppliers like Woodside Petroleum Ltd.

Weaknesses

- The worst performing major commodity for the week was crude oil, which fell 4.64 percent. Oil continues to plummet, trading nearly as low as $20 per barrel intraweek, as global demand capitulates. Crude fell deeply on Thursday after a plan for the U.S. government to buy oil for its emergency reserve fell through. Saudi Arabia has held firm that it will not hold talks with Russia on oil output cuts, intensifying the oil price war. Futures in London fell as much as 8 percent to the lowest level since 2003 on Friday morning. Canadian heavy crude oil has now become so cheap that the cost of shipping it to refiners is more than the value of the oil itself. Bloomberg reports that Western Canadian Select crude in Alberta fell to a record low of $5.03 on Friday morning. The big five integrated oil and gas majors have cut 2020 capex spending by $21 billion, or as much as 20 percent of spending planned before the pandemic.

- Data released from the World Bureau of Metal Statistics and the International Nickel Study Group show that the nickel market was in deficit in 2019. However, BloombergNEF expects the market to be in surplus in 2020, due to reduced demand for the metal amid COVID-19. Even with disrupted mine production, demand for electric vehicles and batteries are likely to drop.

- Although positive that China is soon lifting the lockdown on Wuhan, the first virus epicenter, it is implementing a new ban: blocking all foreigners from entering the country. Starting on Saturday, China will prevent foreigners, even those with valid visas and work permits, from entry as the virus continues to spread rapidly outside of China. A second wave of virus shock has begun to hit Chinese factories. At first it disrupted supply chains due to internal shutdowns of production, but now the threat of declining external demand is shocking the market as the virus hammers other countries.

Opportunities

- Temporary supply disruptions at mines in the Americas might just be what the copper market needs, writes Bloomberg’s Yvonne Yue Li. Peru and Chile, top copper mining countries, are under lockdowns, forcing major mining companies like Freeport-McMoRan and Newmont to curb production. According to the Bank of Nova Scotia, a two week mining halt in the two countries may result in 325,000 in production loss of copper, or about 1.5 percent of global supply. Copper had its biggest weekly drop last week, but pending supply cuts should help stabilize the market.

- Toyota is set to begin producing much needed face shields and masks at its idled manufacturing facilities in the U.S. Bloomberg reports that the automaker is also closing in on deals with medical-device makers to help them boost production of breathing ventilators and respirator hoods. Although it extended its shutdown of North American factories for two weeks, it is positive that Toyota, along with other manufacturers, are able to step in and help supply the shortage of medical equipment as the virus continues to spread.

- As demand for most fuels and commodities has plummeted globally, demand for one prized metal has skyrocketed: gold. Known as the yellow metal, gold is one of the oldest methods of storing wealth, and so many investors have rushed to get their hands on it during this time of crisis that it is selling out. Three of the world’s largest gold refineries were forced to close after lockdowns were issued. Most gold is transported via commercial flights, but since those are canceled by the thousands, less gold is able to be distributed. It is negative that the market and supply chain has been disrupted, but it has been positive for prices.

Threats

- IHS Markit said that current rates of supply and demand mean that oil inventories will increase by 1.8 billion barrels over the first half of 2020. In as little as three months, the world will run out of places to store all the excess oil created from significantly reduced demand, as there is only an estimated 1.6 billion barrel storage capacity. IHS added that oil supply could exceed demand by a whopping 12.4 million barrels a day in the second quarter.

- According to asset manager Pickering Energy Partners, the U.S. oil and gas industry could see as many as 40 percent of its companies fall into bankruptcy or distress over the next two years due to the market crash. Companies will need to make deep cuts to budgets and 15 percent to 25 percent of workers in the field could lose their jobs. Rystad Energy said that globally, the oil industry will likely lose 1 million jobs in 2020.

- Iron ore has held up better than other industrial commodities throughout the COVID-19 selloff, but that could soon change, according to Citigroup. The bank warned this week that investors should brace for a price drop to $70 a ton. Wood Mackenzie said there’s a risk of $50 per ton iron if the market becomes oversupplied. Iron found strength in tighter mine supply in the first quarter and continued steel output in China. However, assuming the second quarter sees fewer lockdowns, mine output could pick up and steel demand could shrink, reports Bloomberg.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 6 percent. The central bank cut its main rate by an additional 75 basis points, more than the expected 50 basis point cut. Central European Media, a TV operator in central emerging Europe, was the strongest equity trading on the Prague Stock Exchange, gaining 25 percent in the past five days.

- The Polish zloty was the best performing currency this week, gaining 4.2 percent. All emerging European currencies gained as the U.S. dollar corrected sharply. The zloty outperformed most peers as Poland’s Prime Minister said that the country’s stimulus program worth some 10 percent of GDP is adequate at the moment, but the government is ready to add new measures if the crisis deepens. Prime Minister Mateusz Morawiecki predicts a V-shaped recovery in Poland.

- Materials was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 65 basis points. Financial regulators asked banks and insurance companies to retain all profits and not pay out any dividends. According to the latest Bloomberg survey, the Polish economy will expand 0.5 percent in 2020, 2.8 percent 2021 and 2.9 percent in 2022, compared to 3.2 percent growth in 2019. Santander Bank Polska was the weakest equity trading on the Warsaw Stock Exchange, losing 15 percent in the past five days.

- The Russian ruble was the worst relative performing currency in the region this week, gaining 1.3 percent. All emerging European currencies gained as the U.S. dollar corrected sharply, but the ruble underperformed its peers due to weakness in the oil price. Brent crude oil lost 8.2 percent in the past five days and closed below $25 per barrel. Oil corrected more than 5.9 percent on Friday alone after Saudi Arabia confirmed there are no active talks with Russia regarding reinstating production cuts.

- Financials was the worst performing sector among eastern European markets this week.

Opportunities

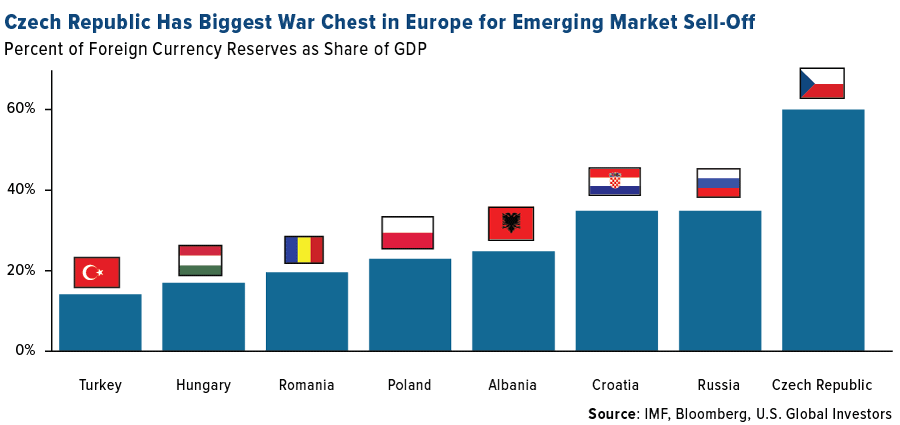

- The Czech Republic has the most money in Eastern Europe to combat currency weakness. The country can easily tap into its large foreign currency reserves to support its currency as it holds the largest reserves in the world relative to the size of its economy – nearly 60 percent.

- Greek government debt will be included in the 750 billion euro Pandemic Bond-Buying Program under a waiver from current rules. The decision would allow the European Central Bank (ECB) to buy up to 12 billion euros of Greek Government Bonds (GGBs), according to Wood & Company. The ECB also recently lifted the ban on Greek banks to purchase GGBs.

- Year-to-date the Warsaw stock exchange has declined by 30 percent, but it has managed to encourage investors to increase activity nevertheless. Currently, the opening of retail brokerage accounts at DM BOS, a domestic brokerage company, exceeds the average prior levels, and clients that ceased to be active some time ago are now coming back.

Threats

- The number of cases of coronavirus in Russia is growing. Last Thursday, Russia reported 200 cases versus this Thursday the number of cases stood at 840. President Putin announced the closure of all stores next week except for groceries in Moscow. All parks and entertainment centers will be closed as well. He also laid out a plan to increase taxes on dividends paid to offshore entities to 15 percent from 2 percent and ordered a 13 percent levy on interest on bank deposits of more than 1 million rubles ($12,600).

- Polish financial watchdog KNF wants banks and insurance companies to retain all profits from past years, regardless of previous decisions, in order to build capital buffers to mitigate the negative impact of the coronavirus. The recent central bank rate cut of 50 basis points will also negatively impact the financial sector. In addition, loan payments might be suspended in Poland for up to a year.

- Wood & Company is predicting a shock in exports and investments in Eastern Europe comparable to what was seen in 2009, and a drop of household spending by 15 percent to 20 percent in the second quarter due to nation-wide lockdowns. Economist Raffaella Tenconi sees a 5 percent drop in GDP this year for most countries under her coverage, followed by a V-shaped recovery in 2021.

China Region

Strengths

- The Philippines was the best performing country this week, gaining 13 percent. Equites outperformed other Asian markets after the government and central bank unveiled steps to support the domestic economy. Robinson Land, a real estate company, was the best performing stock trading on the Philippines Stock Exchange, gaining 27 percent in the past five days.<

- The South Korea won was the best performing currency this week, gaining 3 percent. The won led gains among Asia’s emerging market currencies as South Korea bonds advanced after the central bank pledged unlimited liquidity to financial institutions due to the coronavirus pandemic.

- Telecommunication was the best performing sector among the China iShares MSCI ETF this week.

Weaknesses

- Pakistan was the worst performing country this week, losing 11 percent. The country asked for an additional $1.4 billion from the IMF to help combat the spread of coronavirus. The term of the extra loan would be the same as the $6 billion funding the IMF extended to the South Asian nation last year. Honda Atlas, a car producer, was the worst performing stock trading on the Karachi Stock Exchange, losing 22 percent in the past five days.

- The Pakistani rupee was the worst performing currency in the region this week, losing 5 percent and falling to a record low. The central bank cut its policy rate by 150 basis points – much more than expected.

- Utilities was the worst performing sector among the China iShares MSCI ETF this week.

Opportunites

- China announced that it would lift the lockdown on Wuhan, the city at the epicenter of the coronavirus pandemic, on April 8. This is a big milestone in the battle against COVID-19 and provides hope for other nations facing a growing number of infections that the situation can improve over time.

- On Monday, the Purchasing Manager’s Index (PMI) data will be released for March and the expectation is that there will be improvements. Chinese manufacturing activity slumped to a record low in February of 35.7 as the coronavirus outbreak temporarily shuttered plants and factories and travel restrictions impacted the supply of labor. The expectation is for an increase to 45 in March.

- The Financial Times reported that the People’s Bank of China (PBOC) is in talks with commercial lenders for a reduction in its benchmark deposit rate. The bank has not made a cut since late 2015. If there were a rate cut, it would potentially help banks’ profitability and encourage them to lend cheaper funding to businesses and households.

Threats

- Several countries have had GDP growth estimates slashed after the coronavirus outbreak. Bloomberg Economists estimate that the Chinese economy contracted 20 percent year-over-year in January and February. They now forecast a contraction of 11 percent in the first quarter, but still an expansion of 1.4 percent for the year. Before the virus outbreak, China’s GDP growth for 2020 was forecast at 6 percent.

- The 2020 Summer Olympics have officially been pushed back to an unspecified date in 2021 – dealing a massive blow to Japan’s economy. Olympics host countries often spend years preparing for the major global sports event and rely on the income from increased travel to the country. Japan could lose up to $18 billion from its economy, or about 0.4 percent of GDP, due to the postponement.

- China is soon lifting the lockdown on Wuhan, but it is implementing a new ban: blocking all foreigners from entering the country. Starting on Saturday, China will prevent foreigners, even those with valid visas and work permits, from entry. As the coronavirus outbreak continues to worsen in countries such as Italy and the U.S., China says the ban is a “necessary and temporary” step to prevent further spread. The ban is similar to others imposed against China in January and February when most cases were confined to the country.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 27 was MorCrypto Coin, up 850.54 percent.

- Bloomberg reports that CoinDCX, one of India’s largest cryptocurrency exchanges, has raised $3 million from backers including Bain Capital Ventures. This is a sign that global investors are drawn to the sector after a positive decision from the country’s Supreme Court three weeks ago. CoinDCX says that the number of users has grown 10-fold since the decision was made.

- A report by derivatives analysis firm Acuiti––in partnership with other exchanges, Bitstamp and the Chicago Mercantile Exchange (CME)––shows growing interest in listing cryptocurrency assets among institutions. CoinTelegraph reports that the study found that 17 percent of traditional trading firms have already adopted crypto assets and that 45 percent of the firms that do not currently support crypto plan to revisit the idea within the next six months.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 27 was Storeum, down 87.93 percent.

- The Commodity Futures Trading Commission (CFTC) released its view on what it means to take “actual delivery” of a digital asset––a significant step in defining a blurry line between crypto futures and trading in the spot market. However, Bloomberg reports that the guidance means there could be penalties for trades that don’t let the buyer take physical possession and control of a coin within 28 days. The CFTC has said it considers Bitcoin and Ether to be commodities and that any derivatives on them fall under its jurisdiction. The guidance might force some major U.S. trading platforms to rethink business lines or risk enforcement actions.

- According to Fundstrat Global Advisors, Bitcoin might take months to recover after trading 40 percent below its mid-February high. The firm notes that Bitcoin lost more than $3,000 in 16 hours in mid-March and its price action is now “badly compromised.” Technical strategist Rob Sluymer says “lower highs and lower lows are in place for Bitcoin, leaving in a compromised, potentially vulnerable longer-term profile.”

Opportunities

- Billionaire investor Mike Novogratz said in a CNBC TV interview this week that he has used the recent Bitcoin slide as a buying opportunity. The founder of Galaxy Digital Holdings said “if there was ever a time––debasement of fiat currencies, monetization of trillions of dollars of debt––this is the time for Bitcoin.” Bloomberg reports that Novogratz also said he might continue to buy the dips in Bitcoin and gold.

- Lukka, a cryptocurrency accounting company, launched the Lukka Library, an interactive collection of academic papers addressing legal, accounting and tax questions regarding crypto assets, reports CoinTelegraph. The release of this major resource is a positive step in helping crypto users properly account for their crypto assets and demonstrates growing interest in the space to comply with all rules and regulations.

- Binance announced on Thursday that it is entering the crypto debit card space with an official Binance Card issued by Visa. The card will initially be available in South East Asia for testing and will allow users to spend their cryptocurrencies by converting them into fiat currency and working off of established debit card networks, reports CoinTelegraph. Josh Goodbody, head of growth at Binance Card, says that “users can deposit BNB and BTC to their Binance Cards directly from their Binance.com wallet or any other crypto wallet.”

Threats

- According to the U.S. Department of Justice, Venezuelan President Nicolas Maduro used cryptocurrency to hide transactions related to illegal drug activity, reports CoinDesk. The indictment against Maduro and 14 other officials is aimed at stopping an alleged multi-billion dollar cocaine trafficking ring that invovled drug runners, Colombian revolutionaries and narco-terrorism.

- Several data analytics sites show that the Bitcoin network hash rate has fallen 45 percent from its 2020 peak. CoinTelegraph reports that the hash rate sank 136.2 quintillion hashes per second on March 1 to 7.5.7 hashes per second on Thursday. A higher hash rate demonstrates greater competition among miners, but due to volatile prices and the global pandemic shutting businesses globally, the rate has fallen steeply.

- In California Governor Gavin Newsom’s speech on Thursday about how the state is combating the spread of COVID-19, he warned about crypto-fraudsters taking advantage of people during this panicked time. “People claiming that we need to send them the equivalent of Bitcoin in advance to get some materials before they can send them.” The CFTC also recently cautioned the public about scammers that use major news events to add credibility to their schemes.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.69 | -0.16 | -19.10% |

| Oil Futures | 21.56 | -0.87 | -3.88% |

| Hang Seng Composite Index | 3,240.03 | +123.06 | +3.95% |

| S&P Basic Materials | 278.30 | +24.14 | +9.50% |

| Korean KOSPI Index | 1,717.73 | +151.58 | +9.68% |

| S&P Energy | 217.56 | +23.63 | +12.18% |

| Nasdaq | 7,502.38 | +622.86 | +9.05% |

| DJIA | 21,636.78 | +2,462.80 | +12.84% |

| Russell 2000 | 1,131.99 | +118.10 | +11.65% |

| S&P 500 | 2,541.47 | +236.55 | +10.26% |

| Gold Futures | 1,650.90 | +162.80 | +10.94% |

| XAU | 81.81 | +11.69 | +16.67% |

| S&P/TSX VENTURE COMP IDX | 388.58 | +32.04 | +8.99% |

| S&P/TSX Global Gold Index | 241.90 | +28.52 | +13.37% |

| Natural Gas Futures | 1.63 | +0.03 | +1.87% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 1,717.73 | -359.04 | -17.29% |

| 10-Yr Treasury Bond | 0.69 | -0.65 | -48.77% |

| Gold Futures | 1,650.90 | +2.00 | +0.12% |

| S&P Basic Materials | 278.30 | -72.75 | -20.72% |

| S&P 500 | 2,541.47 | -574.92 | -18.45% |

| DJIA | 21,636.78 | -5,320.81 | -19.74% |

| Nasdaq | 7,502.38 | -1,478.40 | -16.46% |

| Oil Futures | 21.56 | -27.17 | -55.76% |

| Hang Seng Composite Index | 3,240.03 | -439.60 | -11.95% |

| S&P/TSX Global Gold Index | 241.90 | -36.73 | -13.18% |

| XAU | 81.81 | -25.54 | -23.79% |

| Russell 2000 | 1,131.99 | -420.77 | -27.10% |

| S&P Energy | 217.56 | -141.38 | -39.39% |

| S&P/TSX VENTURE COMP IDX | 388.58 | -157.02 | -28.78% |

| Natural Gas Futures | 1.63 | -0.19 | -10.27% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

Royal Gold Inc, Newmont Corp, Freeport-McMoRan Inc, Santander Bank Polska SA, Woodside Petroleum Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Barclays US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. The Bloomberg Barclays US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. The Bloomberg Barclays US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. The MSCI Emerging Markets Index captures large and mid cap representation across 26 Emerging Markets (EM) countries. With 1,401 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity. The Bloomberg WTI Crude Oil Subindex is a single commodity subindex composed of futures contracts on crude oil. It reflects the return of underlying commodity futures price movements only and is quoted in USD. Free cash flow (FCF) represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. U.S. consumer confidence index is an economic indicator published by The Conference Board to measure consumer confidence, which is defined as the degree of optimism on the state of the U.S. economy that consumers are expressing through their activities of savings and spending.