Copper Well Positioned to Lead the Next Resource Cycle

Date Posted: May 3, 2019

Read time: 56 min

The world is on a path to vast shortages in copper, nickel, lithium and other important minerals that are necessary to build the batteries in electric vehicles. So says Tesla's global supply manager, according to Reuters.

Press Release: U.S. Global Investors Announces Quarterly Results Webcast

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Summary

- Ivanhoe’s high-grade Kamoa-Kakula copper mine to come online soon.

- Once again, bitcoin won’t replace gold.

- Peak gold is closer than you think.

The world is on a path to vast shortages in copper, nickel, lithium and other important minerals that are necessary to build the batteries in electric vehicles. So says Tesla’s global supply manager, according to Reuters.

The comment comes as the electric car maker broke ground in Shanghai for its first overseas “Gigafactory.” Tesla’s first battery factory, in Reno, Nevada—the largest in the world—is still in expansion mode and aims to produce as many as 105 gigawatt hours (GWh) of battery cells and 150 GWh of battery packs by next year.

All combined, that’s a lot of copper that will need to come down the pipeline very soon.

But some analysts now say that capacity isn’t quite there yet to feed global demand, and the industry could be running in deficit by 2021. Commodities analyst firm CRU Group expects copper supply to be short some 41,000 tons that year and 270,000 tons a couple of years later.

Meaning: We could be looking at another commodities super-cycle, with the red metal leading the way.

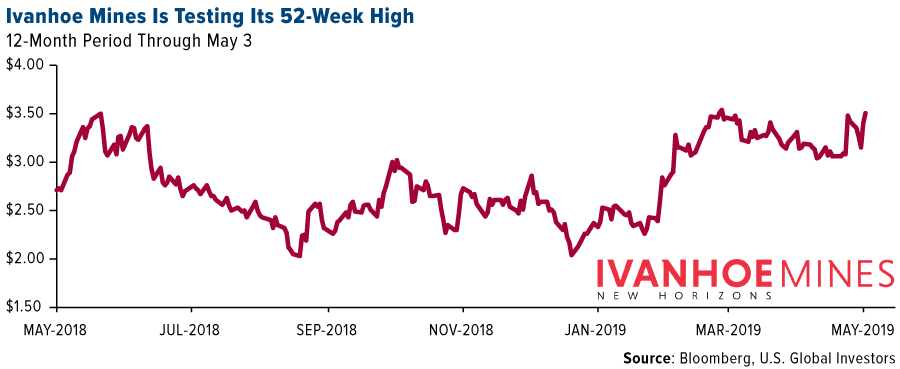

“You’re going to need a telescope to see copper prices in 2021,” my friend Robert Friedland, billionaire founder and executive chairman of Ivanhoe Mines, told us last year during a visit to our office.

This week I had the opportunity to hear Robert speak at the Royal Bank of Canada (RBC), where he explained that investment in metals and mining must increase to meet the unique demands of the future. I also caught up with Ivanhoe executive vice chair Egizio Bianchini, who previously served as vice chair and co-head of metals and mining at BMO Capital Markets.

|

Robert and I are in agreement: The trend toward mass electrification—of everything from vehicles to renewable energy—favors copper, and investors might want to consider getting in now.

Ivanhoe remains my favorite. I own the stock personally. The Vancouver-based miner is nearing the start of production at its long-awaited, high-grade Kamoa-Kakula project in the Democratic Republic of Congo, which has recently gone through leadership change. Ore grades are off the charts. The Kamoa-Kakula deposit—“unquestionably the best copper development project in the world,” as Robert describes it—was fast-tracked after China’s CITIC Metal invested more than $450 million, or nearly $3 a share, late last month.

If fears of a bear market or economic recession are keeping you up at night, I think high-quality resource stocks like Ivanhoe are where you want to be because they’ve historically held up very well.

I’m also heartened to hear that infrastructure might soon be moved to the top of the U.S. government’s priorities, which would be a boon to copper and other base metals. President Donald Trump recently met with Democratic congressional leaders and agreed to a $2 trillion infrastructure package to overhaul U.S. roads, highways, bridges, railroads and waterways. Where this money will come from, I don’t know, but it’s a start.

India’s prime minister, Narendra Modi, made a similar pledge in April, promising as much as $1.44 trillion in infrastructure spending should he win reelection next month.

Once Again, Bitcoin Won’t Replace Gold

Moving on to another metal, a new TV and social media ad blitz is urging investors to “drop gold” in favor of bitcoin. Maybe you’ve seen it. The ad, from crypto investment firm Grayscale, tries to make the case that investing in gold is tantamount to “living in the past,” and that bitcoin is the more logical investment in today’s digital world.

Nonsense.

I’ve commented on the comparison between the two asset classes before. As much as I believe bitcoin has a bright future, I couldn’t agree less with the idea that it will replace gold in people’s portfolios.

Gold is a tangible, time-tested commodity and currency—the best possible candidate for money among all of the known elements, in fact. It’s highly liquid. In 2018, daily trading volume averaged an incredible $112 billion, the sixth largest of any asset class for the year. Gold transactions don’t require electricity or computer technology, and it has a number of other applications besides trading and investing—think jewelry, electronics, dentistry and more.

The same can’t be said of bitcoin or any other digital coin.

That’s not to demean bitcoin. I’m only saying that the two assets are very different. It baffles me that some people continue to try branding bitcoin as a digital replacement for gold. This isn’t the same as upgrading from analog VHS to 4K Blu-ray.

As you know by now, I recommend a 10 percent weighting in gold, split evenly between physical bullion and gold mining stocks. I wouldn’t advise the same percentage weighting in bitcoin, which is much more speculative and volatile. Whereas gold has a daily standard deviation of only ±1 percent—approximately the same as the market—bitcoin’s is closer to ±5 percent. The difference in volatility is even greater for the 10-day

| One Day | Ten Day | |

|---|---|---|

| Gold Bullion | ±1% | ±2% |

| S&P 500 Index | ±1% | ±3% |

| Ethereum | ±5% | ±16% |

| Bitcoin | ±4% | ±12% |

| Past performance does not guarantee future results. Source: Bloomberg, U.S. Global Investors | ||

What’s Supporting Gold Right Now?

Gold tested its 2019 low of around $1,266 an ounce this week, but some recent developments should be supportive of prices going forward.

For one, the pool of negative-yielding government bonds in Europe continues to surge. So far this year, it’s climbed some 20 percent to around $10 trillion, the highest level since 2016, according to Deutsche Bank. And it’s not just government debt. According to Tradeweb, nearly a quarter of the $3.6 trillion worth of investment-grade corporate debt in Europe carries a negative yield. This is constructive for gold, which has been trading closely with the amount of negative-yielding debt.

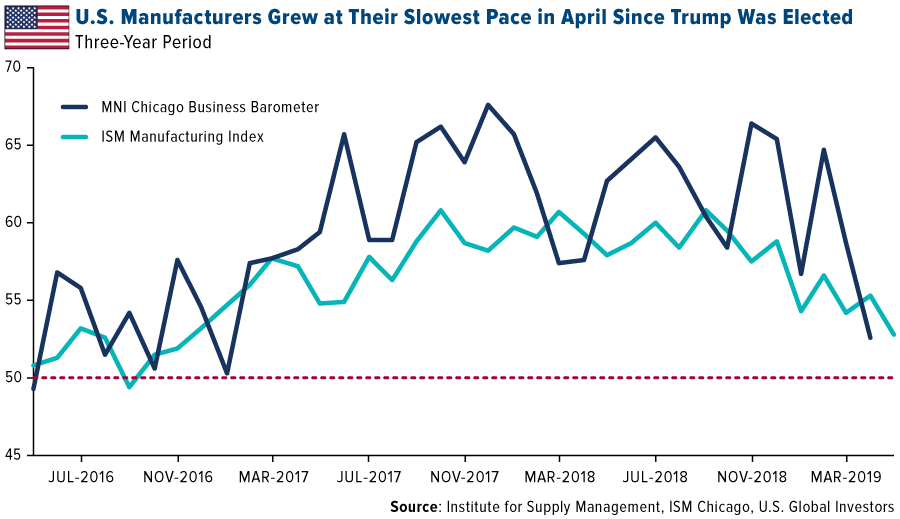

Gold prices jumped a bit this week following the news that the manufacturing sector, both in the U.S. and abroad, continues to slow on global trade concerns.

The Institute for Supply Management (ISM) reported that its U.S. manufacturing index fell sharply in April to 52.8, 2.5 points down from the March reading of 55.3. This is the lowest reading since Donald Trump was elected president in November 2016. Meanwhile, a closely watched barometer of manufacturers in the Chicago metropolitan area fell even more dramatically in April to 52.6, down 6.1 points from 58.7 a month earlier. The WSJ Dollar Index fell a marginal 0.2 percent to 90.45 on the news, which helped support the gold price.

Peak Gold Is Closer Than You Think

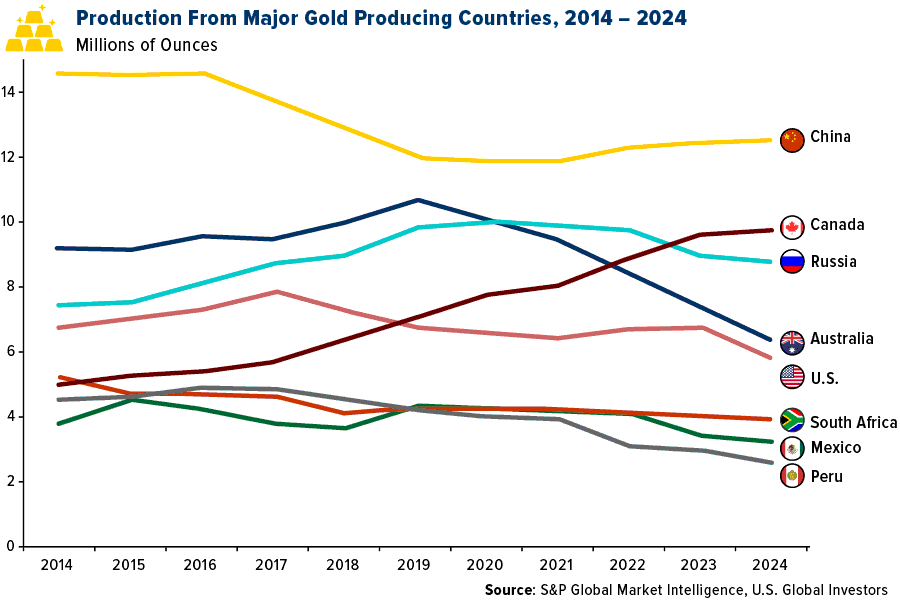

Looking more long term, I think the idea of “peak gold” still makes the case for investing in gold very compelling. This is something I’ve been writing about since as far back as 2010.

Although global gold output is expected to hit a new record high this year—to the tune of 109.6 million ounces, according to S&P Global Market Intelligence—production is seen falling steadily every year thereafter. The only major gold-producing country to increase its production between now and 2024 is expected to be Canada. As a result, it could become the second largest producer after China.

South Africa is currently on an extended losing streak—it recorded its 17th straight month of declines in gold production in February—but Australia is expected to fall the most over the next five years, thanks to faster-than-anticipated depletion of older mines such as St Ives, Paddington, Telfer and others. Today Australia is the second largest gold producer, but by 2024 it could edge down to number four.

The largest Australian gold miner, Newcrest Mining, reported lower production in the first quarter of 2019 relative to the previous quarter. Output stood at more than 623,000 ounces, about 5 percent down from 655,000 ounces in the December quarter.

Central Banks Aren’t Done Adding Gold to Their Reserves

The yellow metal is a finite commodity, one of the many reasons why it’s so highly valued, and it’s about to get even more finite. Demand, meanwhile, is only increasing, as evidenced by central banks’ insatiable consumption.

According to the latest report by the World Gold Council (WGC), gold purchases by central banks totaled 145.5 tonnes in the first quarter. Not only was this the strongest first quarter since 2013, but on a rolling four-quarter basis, demand reached an all-time record high of 715.7 tonnes.

Perhaps the central bank chiefs didn’t see Grayscale’s ad to “drop gold.”

Missed my interview with legendary small-cap resource investor Bob Moriarty? Read it now by clicking here!

Gold Market

This week spot gold closed at $1,279.15, down $7.10 per ounce, or 0.55 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.44 percent. The S&P/TSX Venture Index came in off just 0.70 percent. The U.S. Trade-Weighted Dollar fell 0.56 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-29 | Hong Kong Exports YoY | -2.6% | -1.2% | -6.9% |

| Apr-29 | Caixin China PMI Mfg | 50.9 | 50.2 | 50.8 |

| Apr-30 | Germany CPI YoY | 1.5% | 2.0% | 1.3% |

| Apr-30 | Conf. Board Consumer Confidence | 126.8 | 129.2 | 124.2 |

| May-1 | ADP Employment Change | 180k | 275k | 151k |

| May-1 | ISM Manufacturing | 55.0 | 52.8 | 55.3 |

| May-1 | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | 2.50% |

| May-2 | Initial Jobless Claims | 215k | 230k | 230k |

| May-2 | Durable Goods Orders | — | 2.6% | 2.7% |

| May-3 | Eurozone CPI Core YoY | 1.0% | 1.2% | 0.8% |

| May-3 | Change in Nonfarm Payrolls | 190k | 263k | 189k |

| May-9 | Initial Jobless Claims | 220k | — | 230k |

| May-9 | PPI Final Demand YoY | 2.4% | — | 2.2% |

| May-10 | CPI YoY | 2.1% | — | 1.9% |

Strengths

- The best performing precious metal this week was gold, after closing out the week on a strong uptick on Friday. Gold traders were split this week on the yellow metal as it headed for another down week, according to the weekly Bloomberg survey of traders and analysts. However, gold futures rose on Friday after a report showed slower-than-expected U.S. wage gains support the Federal Reserve’s patient stance on interest rate hikes.

- Russia’s central bank emerged as the biggest buyer of gold in April, purchasing 19.4 tons, according to data from the World Gold Council (WGC). China also bought 11.2 tons and Kazakhstan bought 5.4 tons. India is considering reducing the import tax on gold from the current 10 percent to 4 percent. Bloomberg reports that the proposal is being reviewed by the Central Board of Indirect Taxes and Customs.

- Turkey’s central bank turned bullish on gold this week after selling last week. The nation’s central bank reserves rose $51 million from the prior week to now be worth $20.4 billion. The bank introduced a new swap instrument that will allow it to bolster its international reserves by borrowing gold from commercial lenders in the country in exchange for lira, writes Bloomberg’s Kerim Karakaya.

Weaknesses

- The worst performing metal this week was palladium, down 6.29 percent on weak April auto sales and a Reuters survey that indicated prices are expected to fall in 2020. American Eagle gold coin sales fell for a third straight month after hitting a two-year high in January, according to U.S. Mint data. Australia’s Perth Mint also reported that gold coin and bar sales fell in April to just 19,991 ounces, down from 32,757 ounces in March. Bloomberg data shows that commodity ETFs suffered a fifth week of outflows with precious metals funds leading the decline. A program to refund tourists for value-added tax in the United Arab Emirates (UAE) has failed to reverse a slump in gold and jewelry sales. Sales saw a 6 percent year-over-year increase in the first quarter of this year, but that compares poorly to the 23 percent drop in the same period last year, according to WGC data. Reportedly, potential Indian buyers in the UAE are worried about their buying will be reported back to Indian authorities and both the UAE and Saudi Arabia are actively removing expatriates from their borders.

- Gold was on a wild ride this week after Fed Chairman Jerome Powell’s comments. The yellow metal rose sharply on Wednesday after Powell said the Fed will keep rates unchanged, but then those gains disappeared minutes later when Powell said low inflation may be transitory. Bloomberg writes that hedge funds are shorting the VIX at rates not seen in at least 15 years as they’re betting that low volatility will continue, which could be seen as complacent the rise further. It also did not help that the embattled Venezuelan leader Nicolas Maduro remained in power this week, potentially leaving the door open for more gold sales from the county.

- Macquarie Group, Australia’s largest investment bank, will be exiting its 50 employee equities research, sales and syndication business in Canada, reports Bloomberg. The Globe and Mail’s Andrew Willis writes that this retreat signals the streamlining of investment banks. Willis says “the restructuring should be a wakeup call to both small-cap Canadian companies, which traditionally look to independent dealers for capital, and the entire investment-banking community.”

Opportunities

- World Gold Council data shows that central bank gold purchases were the highest in six years in the first quarter of this year with reserves rising 145.5 tons. This marks a 68 percent increase from a year earlier with Russia remaining the largest buyer. The council expects gold jewelry demand to rise only marginally in 2019 and they expect a plunge in the S&P 500 Index to spur safe haven demand later in the year boosting prices to $1,400 per ounce.

- Bloomberg’s Carl Riccadonna writes that analysts should be cautious not to write off the employment cost index (ECI) report as evidence of muted inflation pressures. The year-over-year rate of change in employment costs had the strongest start of any year of the past decade. Riccadonna says “this is a compelling signal that employers’ labor costs are increasing” and that “barring a substantial pickup in capital investment and productivity, price pressures will be passed along the supply chain.”

- Billionaire hedge fund manager Ray Dalio says that central banking as we know it is on its way out and that it is “inevitable” that something like modern monetary theory (MMT) will replace it. Bloomberg’s Ben Holland writes that MMT is the idea that governments should manage their economies through spending and taxes, instead of relying on independent central banks to do it via interest rates. Dalio writes that one of the risks of MMT is that policies could put the power to create and allocate money, credit and spending into the hands of politicians.

Threats

- According to Polymetal CEO Vitaly Nesis, the Russian gold industry is too isolated from the rest of the world to join the global merger and acquisition rush. Nesis said in an interview last week that it doesn’t make sense for Russian gold producers to merge with each other or to make acquisitions abroad.

- Sonal Desai, chief of Franklin Templeton Investments’ $150 billion fixed-income unit, warns of a rate hike later this year. A contrarian to most right now, Sonal believes that 10-year Treasury yields will climb to 3 percent or more this year. Sonal says that “markets are overestimating the Fed’s ability to anchor long-end rates – they’re also over-estimating the Fed’s fear about the underlying real economy.”

- Seven of the world’s biggest diamond miners released figures on everything from emissions to taxes in an attempt to show that man-made diamonds are creating a bigger greenhouse footprint than digging diamonds from the ground. Bloomberg’s Thomas Biesheuvel writes that “the publication of so much information from the industry highlights the growing awareness of the threat posed by diamonds made in laboratories.”

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.14 percent. The S&P 500 Stock Index rose 0.20 percent, while the Nasdaq Composite climbed 0.22 percent. The Russell 2000 small capitalization index gained 1.39 percent this week.

- The Hang Seng Composite gained 1.37 percent this week; while Taiwan was up 1.31percent and the KOSPI rose 0.78 percent.

- The 10-year Treasury bond yield rose 2 basis points to 2.53 percent.

Domestic Equity Market

Strengths

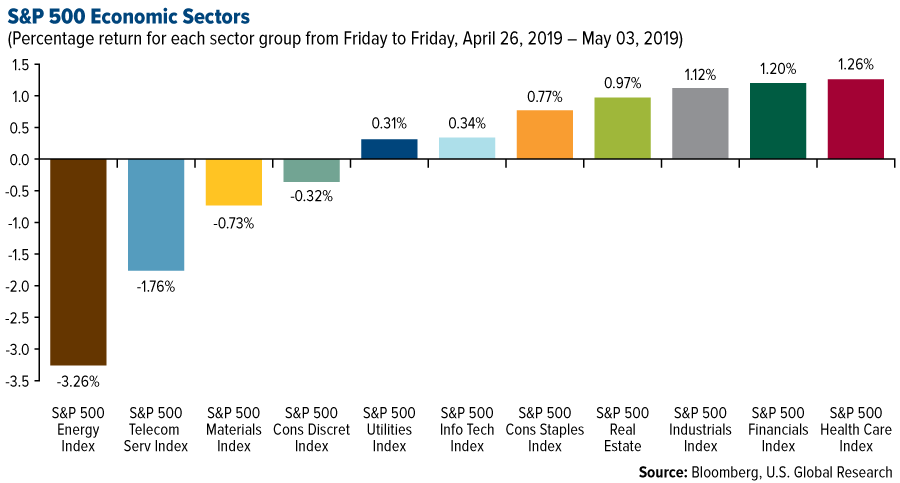

- Health care was the best performing sector of the week, increasing by 1.26 percent versus an overall increase of 0.19 percent for the S&P 500.

- Newell Brands Inc. was the best performing stock for the week, increasing 16.17 percent.

- Disney’s "Avengers: Endgame" smashed box office records for the biggest opening weekend, reports CBS News, bringing in a record $350 million. Ticket sales reached $1.2 billion worldwide, making it the biggest opening in movie history.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 3.26 percent versus an overall increase of 0.19 percent for the S&P 500.

- Fluor Corp. was the worst performing stock for the week, falling 26.50 percent.

- Lyft has had a tough first month of trading, reports Business Insider. Shares of the ride-hailing company plunged 35 percent from their opening print of $87.24 on March 29, setting the tone for rival Uber which is set to hit the public this year.

Opportunities

- According to IHS Markit, the next nine days are set to be some of the most active in the history of the initial public offering (IPO) market. In fact, nearly $10 billion in equity capital is set to be issued, reports Business Insider, the majority of which is related to Uber’s IPO.

- Next month Tesla will start offering a new insurance product to its customers, according to comments from CEO Elon Musk this week. Due to the difficulty of finding replacement parts and qualified body shops, many Tesla owners have dealt with high insurance costs. In addition, Tesla has plans to roll out 1 million robo-taxis by next year, which will allow owners to turn their vehicles into direct competition to Uber and Lyft.

- According to industry news site FreightWaves, Amazon is going after the shipping industry in a big way. The company has launched a trial version of its online-freight-broker platform, which is undercutting prices by over 25 percent.

Threats

- The grounding of the 737 Max aircraft will cost airlines around the world hundreds of millions of dollars, the companies are warning. As reported in Business Insider, analysts say they’ll all want different forms of compensation from Boeing.

- Samsung’s first-quarter operating profits plunged 60 percent, reports Reuters, or $5.4 billion. Slowing demand for TVs and a drop in chip prices can be attributed to the fall.

- On Wednesday, Square reported second-quarter sales and profits guidance that disappointed expectations. Shares fell by as much as 7 percent. This makes the second quarter that the mobile-payments company’s guidance also disappointed investors, writes Business Insider.

The Economy and Bond Market

Strengths

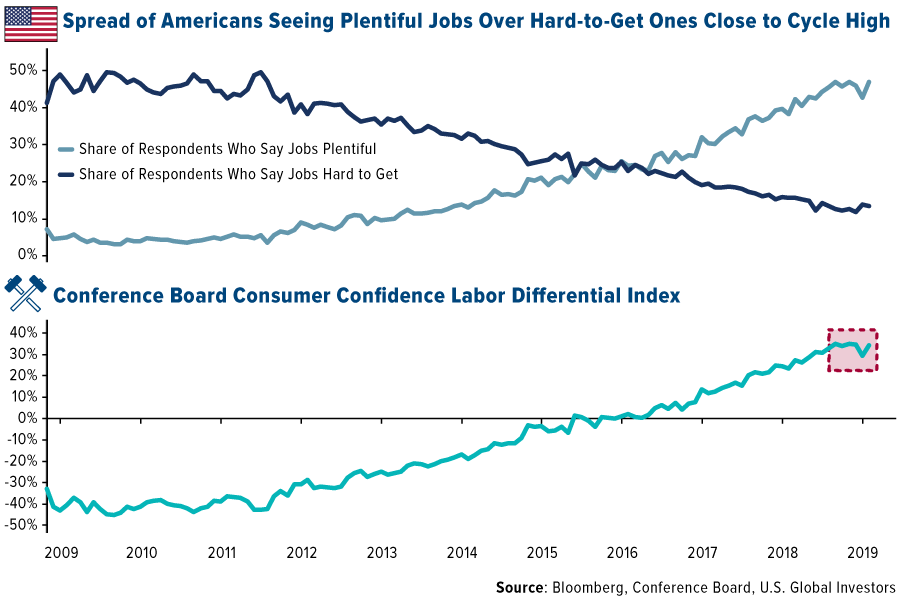

- The winter gloom that impacted Americans’ perception of the job market is turning sunnier; something the Federal Reserve hawks can add to their argument for maintaining a bias toward raising interest rates, rather than lowering them. The Conference Board’s April consumer confidence report shows a sharp rebound in the percentage of respondents saying jobs are plentiful, while those saying jobs are hard to get, fell. The spread between the two, as shown in the labor differential index, is nearly back to a cycle-high reached in November.

- The Federal Reserve held its benchmark interest rate steady on Wednesday, in a range between 2.25 percent and 2.5 percent. Officials are pointing to weaker-than-expected inflation and continued economic growth, reports Wall St. Journal.

- Municipal bonds are off to their best start in five years, as reflected in the Bloomberg Barclay’s benchmark state and local government debt index. The index has returned 3.2 percent since the beginning of January, the most for the first four months of the year since 2014, reports Bloomberg. “The securities have been bolstered by low supply and seemingly unbounded demand, with almost $4 billion flowing into municipal mutual funds in April alone as investors scrambled for tax-exempt debt to offset the federal cap on state and local tax deductions,” the article reads.

Weaknesses

- The ISM manufacturing index fell in April to the weakest level since late 2016, reports Bloomberg, signaling that manufacturing headwinds extended into the second quarter as companies continue to confront uncertainty about trade. The index dropped to 52.8 from 55.3 the prior month, missing all estimates in Bloomberg’s survey.

- The number of people who applied for jobless benefits at the end of April stood at a three-month high of 230,000 for the second week in a row, writes MarketWatch. Economists polled by the news outlet had estimated new claims would fall to seasonally adjusted 215,000 in the seven days ended April 27 from 230,000 in the prior week.

- Economic confidence in the euro area dropped for a tenth month in April to the lowest in more than two years, reports Bloomberg, indicating the region may struggle to pick up from its recent slump. The headline index, which assesses the mood of households and businesses, fell sharply to its lowest level since September 2016.

Opportunities

- Although President Trump agreed to Democratic leaders’ aim for a $2 trillion infrastructure plan, the pivotal question of where the money will come from still remains. House Speaker Nancy Pelosi and Senate Democratic leader Chuck Schumer will meet with Trump again in three weeks to talk about how to raise the money, reports Bloomberg.

- On Wednesday, the latest round of U.S.-China talks wrapped up in Beijing, reports Bloomberg, with U.S. Treasury Secretary Steven Mnuchin calling the meetings “productive” in a tweet. Negotiations will continue in Washington D.C. next week as the U.S. increases pressure to reach a deal in the next two weeks.

- China announced its plans to remove limits on ownership in local banks and scrap size requirements for foreign firms that operate onshore, reports Bloomberg. One of the changes includes the allowance of overseas insurance groups to set up units in the world’s second-biggest economy, the China Banking and Insurance Regulator said on Wednesday.

Threats

- U.S. regulators told banks and investors that it was okay to make riskier loans to companies. Now they’re having trouble reining in the excesses that resulted, writes Bloomberg. In the first quarter, banks and investors helped bring some of the highest debt levels of this decade to leveraged buyouts and other acquisitions. Lenders are letting companies aggressively massage measures of their profits when posting them for credit investors. All while more and more lender protections are being watered down.

- Italy is trapped in a “perma-recession” with no easy exit, reports Business Insider. The country has a 2 trillion euro debt load that threatens the eurozone itself, analysts told the news outlet.

- A gauge of U.S. service industries unexpectedly dropped for a second month, slipping to the lowest level since August 2017. This is the latest sign of weaker economic momentum at the start of the second quarter. The ISM non-manufacturing index declined to 55.5 in April from 56.1, according to an Institute for Supply Management survey released Friday.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was corn, which gained 3.35 percent as flooding and wet weather are expected to lower crop yields. The Stoxx Europe 600 Basic Resources Index rose as much as 1.2 percent on Friday after falling nearly 8 percent from its April peak. The bounce was largely due to Anglo American’s upgrade. Copper advanced on Friday, trimming a sharp weekly drop, after Codelco, the world’s largest miner of the metal, said the downtrend in prices won’t last long, writes Bloomberg. Chief Commercial Officer Roberto Ecclefield forecast 2.3 percent growth in consumption of copper this year while mine production is expected to fall 0.5 percent.

- Caterpillar announced a 20 percent increase in its quarterly dividend—a record payout. Norway’s Equinor ASA beat profit and cash flow estimates after pumping more oil and gas than predicted, reports Bloomberg. The company’s adjusted net income rose to $1.54 billion in the quarter from $1.47 billion a year earlier.

- Northwest Europe received the most LNG than it ever has in the month of April, with as many as 57 tankers unloading the fuel at terminals in the U.K., Belgium, the Netherlands and western France, likely to Russia’s profound disappointment. Australian conglomerate Wesfarmers has agreed to pay $545 million for a lithium mine and refinery project developer Kidman Resources in order to gain exposure to the electric vehicle battery market, reports Bloomberg.

Weaknesses

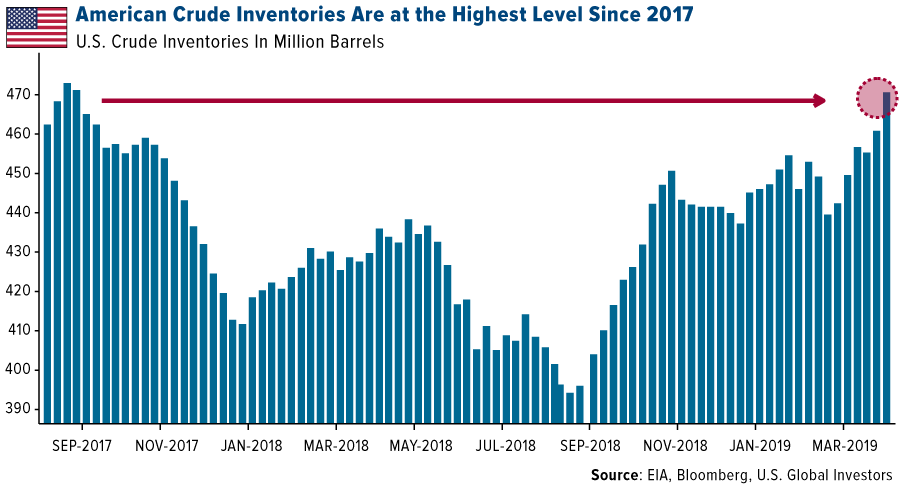

- The worst performing major commodity for the week was palm oil, which fell 5.61 percent on concerns of ample supplies of edible oils and high stockpiles. Oil fell this week as a massive surge in stockpiles allayed worries about supply disruptions around the world, writes Bloomberg. U.S. government data showed that crude oil inventories soared by 9.93 million barrels last week, which is more than four times the amount initially anticipated by analysts. Oil prices slumped 2.9 percent last Friday after President Donald Trump said he had personally pressed OPEC to keep oil prices down. Russia missed its oil production cut target in April and pumped more crude than agreed on under the OPEC deal.

- Aluminum inventories in warehouses tracked by the London Metals Exchange jumped the most since last April. Two aluminum giants, United Co. Rusal and Norsk Hydro ASA, joined a growing list of suppliers cutting their 2019 demand outlooks amid concerns about global growth, writes Bloomberg’s Elena Mazneva. Glencore cut its full-year copper output goal by around 3 percent and lowered production targets for other commodities as the world’s biggest metal trader faces problems across operations.

- According to an investigation by NASA, a metals manufacturer faked test results and provided faulty materials to the space agency, causing more than $700 million in losses and two failed satellite launches, reports Bloomberg. An Oregon-based company called Sapa Profiles falsified thousands of certifications for aluminum parts over 19 years and those bad parts were used in the making of a rocket that was supposed to deliver satellites to space in 2009 and 2011.

Opportunities

- Bloomberg New Energy Finance (BNEF) forecasts battery demand for nickel could increase nine fold by 2030, as battery industry leaders are shifting to high-nickel cathodes to increase battery density. Much of this nickel could come from Indonesia, which already has half of the best performing Tier 1 and Tier 2 assets that produce battery-grade nickel sulfates from lower-grade laterite ores.

- Sirius Minerals announced a $3.8 billion funding package that brings the company closer to building the U.K.’s first potash mine in more than 40 years, reports Bloomberg. The mine is ambitious and ranks among one of Britain’s biggest industrial projects that could bring many jobs to a beleaguered economy in North Yorkshire. The mine could start producing in 2021.

- Floating wind turbines on floating foundations could unlock new markets for offshore wind. BNEF writes that conventional turbines are capped to depths of 50 to 60 meters, but floating turbines could sit in waters over 1,000 meters deep. Currently there are tests close to shore; however, BNEF expects developers to target sits with water at depths greater than 60 meters.

Threats

- After a crucial conduit was contaminated with chemicals last week in Russia’s largest export pipeline, reports are saying that it could take up to six months to repair and restore normal flow. Both branches of the Druzhba pipeline via Belarus into Poland or Ukraine have been closed.

- Bijan Namdar Zanganeh, Iran’s oil minister, has warned that OPEC is in danger of collapse as some nations seek to undermine their fellow members, which could be a direct reference to Saudi Arabia pledging to fill the supply gap created by U.S. sanctions on Iran exports, reports Bloomberg. Zanganeh said “Iran is a member of OPEC for its interests and any threat from member states won’t go unanswered.”

- This week Democratic congressional leaders agreed with President Trump to pursue a $2 trillion infrastructure plan to upgrade highways, railroads, bridges and broadband. However, no details have been released on how the plan would be funded, with some speculating that a gas tax could be proposed. Although positive for America’s infrastructure, a gas tax would be a threat to consumers’ income.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 70 basis points. On the political front, negative news flow on sanctions has slowed this year. Focused on the domestic market, the central bank left its main rate unchanged last week and indicated that a rate cut is possible during the next meeting, due to subediting inflation.

- The Polish zloty was the best performing currency this week, gaining 94 basis points against the U.S. dollar. Polish inflation hit the highest since 2017, raising pressure for the central bank to lift interest rates. April’s inflation came in at 2.2 percent, mainly driven by higher fuel and food prices.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 3 percent. Despite strong economic data released this week, equites trading on the Budapest exchange traded lower. Manufacturing PMI spiked to 54.9 in April from 52.4 in March. Unemployment stayed at a record low of 3.6 percent, gross wages grew by 12.1 percent. MOL, a Hungarian refinery, lost 5.4 percent in the past five days after reporting a small, first-quarter miss.

- The Turkish lira was the worst performing currency this week, losing 51 basis points against the U.S. dollar. Erdogan has pledged to lower rates and inflation. Some analysts expected a rate cut at the next central bank meeting. Geopolitical tension could increase in the summer months as Turkey considers taking the delivery of S-400 missiles from Russia, risking new sanctions from the United States.

- Materials was the worst performing sector among eastern European markets this week.

Opportunities

- Unexpectedly, eurozone growth picked up in the first quarter of the year compared to the last three months of the prior year. The EU’s economy grew by 0.4 percent, faster than the expected 0.3 percent. This improvement could be explained by stronger data out of Italy, where the economy expanded by 0.2 percent, exiting recession. In another boost, unemployment across Europe fell to a 10-year low, and inflation in April spiked to 1.7 percent versus 1.4 percent a year ago, and expected 1.6 percent.

- Europe has seen a slight improvement in manufacturing activity in the month of April. Eurozone manufacturing PMI came in at 47.9 versus 47.5 in March. Slightly stronger readings were reported in the largest European economies: Germany, France and Italy. Within the emerging Europe universe, Greek industrial production is the strongest, with a PMI at 56.6, well above the 50 level that separates contraction and growth.

- Final data for April’s service PMI will be released for the eurozone next week, and expectations are that it will remain unchanged at 52.5. Service PMI has kept the EU’s composite PMI above the 50 level that separates growth from contraction.

Threats

- The Hungarian, Polish and most recently Romanian governments implemented a tax on the banking sector. This week the Czech Republic announced that it could be the next Eastern European country to tax its banking sector as well. Banks in the Czech Republic and Austria’s Erste Bank, which owns operations in the Czech Republic, declined on the announcement and then recovered its losses.

- The leaders of Albania, Bosnia and Herzegovina, Montenegro, North Macedonia, Serbia and Kosovo met in Berlin to discuss EU accession, but were told to solve their internal country problems before applying to join the eurozone. Mr. Macron, the French President, said that he would rather focus on political stability in the region than on the EU enlargement process. The EU has long held out the possibility of bringing western Balkan countries into the bloc to foster economic progress and improve broader regional stability.

- Europe celebrated Labor Day on Wednesday, along with the fifteen-year anniversary of nine European countries joining the eurozone. Among the nine countries were Poland, the Czech Republic and Hungary. The day was filled with peaceful marches and concerts, but some clashes occurred between police and protestors across Europe. In Paris, French police arrested almost 300 participants. More than 100 people were detained in Russia, and most of the arrests took place in St. Petersburg where several hundred people had taken to the streets calling for fair elections. Reports of violence occurred across all of Europe during the May 1 celebrations.

China Region

Strengths

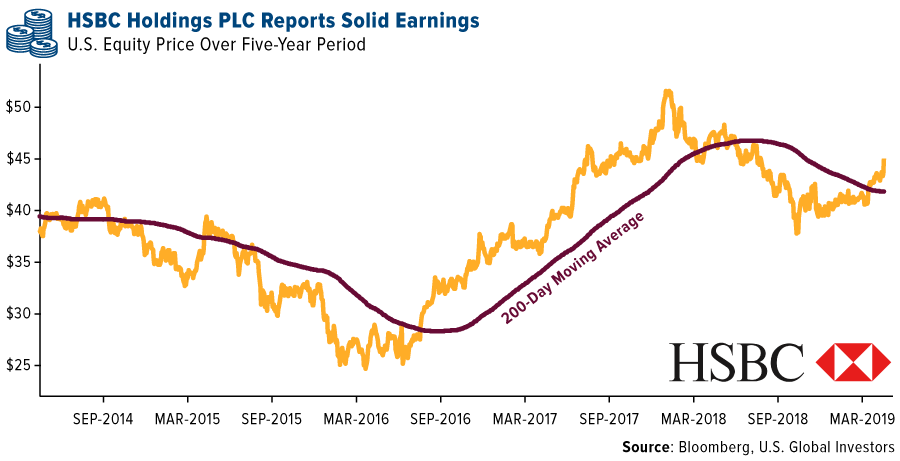

- Financials was the top-performing sector for Hong Kong’s Hang Seng Composite Index this week, climbing 2.64 percent. Index heavyweight HSBC Holdings PLC (HSBA LN/HSBC US/5 HK) reported solid earnings on Friday, which bolstered the sector as a whole.

- China’s Industrial Company Profits climbed 14 percent year-over-year for the March measurement period, notching a gain after declines over the last couple of months.

- First quarter Hong Kong GDP expanded 1.2 percent quarter-over-quarter, outpacing analysts’ expectations for a 0.7 percent rate of growth.

Weaknesses

- Indonesia’s Jakarta Composite fell by 1.19 percent. China’s Shanghai Composite declined by 29 basis points in its holiday-shortened week, while Vietnam’s Ho Chi Minh Stock Index dropped by 55 basis points. India’s NIFTY fell by 36 basis points and the SENSEX by 27 basis points.

- The worst-performing sector in Hong Kong’s Hang Seng Composite Index was Materials, which declined by 2.80 percent.

- China’s official Manufacturing and Non-manufacturing PMIs both missed expectations, as did the Caixin China Manufacturing PMI. The official Manufacturing PMI clocked in—still in expansionary territory—at 50.1 for April, below consensus of 50.5, while the Non-manufacturing came in at 54.3, shy of an expected 54.9. The Caixin Manufacturing PMI registered at 50.2, missing analysts’ expected showing of 50.9. We’ll get the Caixin Services reading early next week. Expectations are for a 54.6 print.

Opportunities

- Secretary. Mnuchin and USTR Lighthizer returned to Beijing this week for more talks with Chinese Vice Premier Liu He, and talks in Washington are scheduled for next week. Reports late in the week suggested that an end to the trade talks could come potentially as soon as the end of next week, and there has been messaging lately that for better or for worse, talks need to conclude soon because both sides have an interest in moving on one way or the other. We continue to receive reports from Mnuchin that the talks are both productive as well as nearing conclusion. The Trump administration has also attempted to send a message that it remains prepared to walk if there is no deal to be had or it is not substantial enough, but at this point it seems we may receive something more decisive on a timeline as early as next week. Given market positioning and the “consensus”, both sides are said to have reached around certain language and enforceability—as well as continued rumors of various concessions on both sides—it does appear there are some reasons to be optimistic. Watch for headlines next week as talks resume in Washington, with the possibility of a signing summit down the road if things go well.

- Indonesia’s official vote count remained comfortably in favor of incumbent JokoWi this week with the majority of votes now having been counted. With Joko Widodo running somewhere around 56 percent of the votes—well ahead of challenger Prabowo Subianto’s roughly 44 percent—the Indonesian election looks closer to an official call (although, as mentioned last week, the day-of polls and surveys have historically been highly accurate, and these also projected collectively a JokoWi re-election).

- A continued decline in crude oil prices could benefit major net importers around the region like Indonesia and India.

Threats

- As has been customary of late given the potentially binary nature of the trade talks, it must be said: U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter remain a collective threat until resolution one way or the other amid the dispute. While there were several reiterations from the Trump administration this week that the U.S. is prepared to walk away, so too there was some telegraphing that we are closing the gaps. One question will be whether we have, as some media were reporting by Thursday, hit an “impasse” in the talks, while another question will be whether any “deal” represents all the market thinks it ought to be. Markets can be, of course, notoriously fickle at times. Thus, once again, the devil will be in the details, and as we’ve said before, it ain’t over ‘till it’s over …

- The Huawei saga continues this week as Vodaphone released a report alleging it discovered “vulnerabilities in equipment made by Huawei,” as the WSJ reported. Huawei continues to deny U.S. allegations that the company’s equipment could be used for spying, even as the U.K seems prepared to go ahead with Huawei and as the U.S. continues to argue that the incorporation of Huawei infrastructure into nations with whom the U.S. shares intelligence could jeopardize such arrangements.

- The U.S. dollar remains strong, which could conceivably pose a threat to emerging markets. Hong Kong, of course, notably remains pegged to the U.S. dollar.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 3 was Diruna, up 455.76 percent.

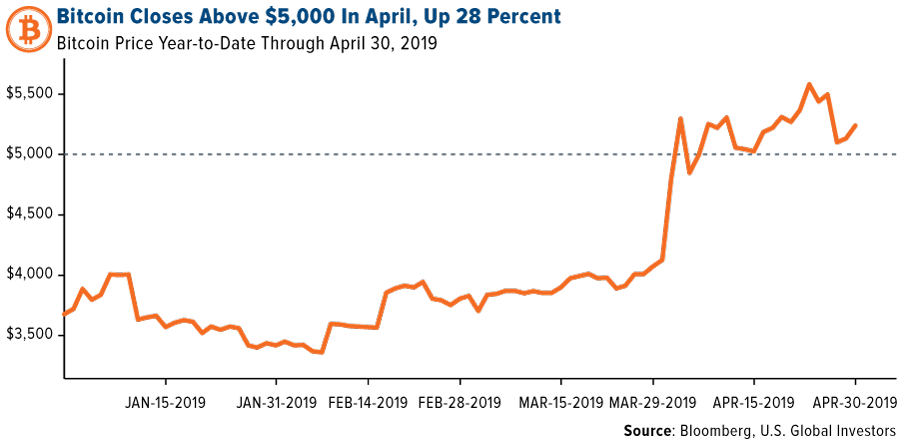

- Bitcoin ended the month of April with double-digit gains, reports CoinDesk, up 28 percent. Bullish developments on the digital currency’s monthly chart, paired with a bounce from the historically strong 30-day moving average support, could indicate scope for a rally to $6,000 in the next few weeks, the article continues.

- A blockchain-powered marketplace for precious metals, Tradewind, has hired a senior executive from JPMorgan to be the startup’s first-ever CEO, reports CoinDesk. Launched back in March 2018, Tradewind set out to put gold trading on the blockchain. By appointing Michael Albanese (who has over 20 years of experience in major financial institutions) to the position of CEO, the company is confident his expertise will aid in expanding its product offering and client base.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended May 3 was Digitex Futures, down 57.21 percent.

- On Monday, Galaxy Digital Holdings posted an annual loss of $272.6 million in 2018, reports MarketWatch, thanks in part to a loss of $101.4 million in digital assets. The price of bitcoin fell over 60 percent in 2018, but billionaire owner Mike Novogratz says he is already seeing the benefits of the early 2019 cryptocurrency rally.

- Bitcoin traded at a $300 premium this week on the Bitfinex exchange, reports Bloomberg. The increased demand for bitcoin comes amid speculation that investors are exiting the Tether stablecoin on allegations that “Tether and the operator of the Bitfinex exchange participated in a cover-up to hide nearly $1 billion in losses in corporate and client funds,” the article explains. Bloomberg Intelligence analyst Mike McGlone reasons, “What’s the first thing you’re going to buy if you don’t want too much broad crypto exposure? Bitcoin.”

Opportunities

- Nasdaq is adding another cryptocurrency index, writes CoinDesk, this time for the world’s third-largest digital currency, XRP. Beginning May 1, Nasdaq will offer “real time” index information for XRP through its partnership with New Zealand-based blockchain data and research firm Brave New Coin.

- CoinMarketCap, a popular cryptocurrency data provider, has formed an alliance dubbed the Data Accountability & Transparency Alliance (DATA), that will discuss ways to tackle concerns over crypto data reporting in its current state, reports CoinDesk. DATA will work with major exchanges on the initiative and has notable members at launch which include Binance, Bittrex, OKEx and Huobi, to name a few.

- The central banks of Canada and Singapore announced Thursday that they successfully settled a trial of cross-border payments using blockchain technology and central bank digital currencies, reports CoinDesk. The trial is the first of its kind and according to the two banks, shows “great potential to increase efficiencies and reduce risks for cross-border payments.”

Threats

- The recent rally in the price of bitcoin might be losing steam, reports Bloomberg. A popular indicator that is used to detect trend reversals, the GTI Vera Convergence Divergence Indicator, sent its first sell signal since mid-March, the article continues. As the coin touches its highest levels of the year so far, this shift could suggest further downside may be ahead.

- A crypto ATM operator, CoinFlip, has postponed its plans to add the Tron version of USDT to more than 180 of its machines following fraud allegations by the New York Attorney General against the companies behind the stablecoin, reports CoinDesk. “We want to make sure Tether and Bitfinex are operating 100 percent lawfully before offering their products with our customers,” said co-founder and CEO of CoinFlip Daniel Polotsky.

- In a new report for its clients, Moody’s reviews the pros and cons of blockchain technology for financial firms, explaining how businesses like banks can leverage it to their benefit. As CoinDesk reports, in the document Moody’s does emphasize the difference between public and private blockchains, warning that private chains might not be as strong, or absent all together. “Private/centralized blockchains are more exposed to fraud risk because system design and administration remains concentrated with one or few parties,” the April 25 report continues.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 178.44 | -8.13 | -4.36% |

| Gold Futures | 1,279.60 | -9.20 | -0.71% |

| Natural Gas Futures | 2.56 | -0.01 | -0.23% |

| S&P/TSX VENTURE COMP IDX | 606.42 | -4.27 | -0.70% |

| 10-Yr Treasury Bond | 2.53 | +0.03 | +1.08% |

| Nasdaq | 8,164.00 | +17.60 | +0.22% |

| Oil Futures | 61.84 | -1.46 | -2.31% |

| Hang Seng Composite Index | 4,018.04 | +54.18 | +1.37% |

| S&P 500 | 2,945.62 | +5.74 | +0.20% |

| DJIA | 26,504.95 | -38.38 | -0.14% |

| Korean KOSPI Index | 2,196.32 | +17.01 | +0.78% |

| Russell 2000 | 1,614.02 | +22.20 | +1.39% |

| S&P Energy | 474.50 | -15.97 | -3.26% |

| S&P Basic Materials | 354.79 | -2.58 | -0.72% |

| XAU | 68.79 | -3.86 | -5.31% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.56 | -0.12 | -4.37% |

| S&P/TSX Global Gold Index | 178.44 | -14.48 | -7.51% |

| 10-Yr Treasury Bond | 2.53 | +0.00 | +0.04% |

| Oil Futures | 61.84 | -0.62 | -0.99% |

| Gold Futures | 1,279.60 | -15.70 | -1.21% |

| S&P 500 | 2,945.62 | +72.22 | +2.51% |

| S&P Energy | 474.50 | -13.43 | -2.75% |

| Hang Seng Composite Index | 4,018.04 | -2.00 | -0.05% |

| DJIA | 26,504.95 | +286.82 | +1.09% |

| Korean KOSPI Index | 2,196.32 | -6.95 | -0.32% |

| Nasdaq | 8,164.00 | +268.44 | +3.40% |

| S&P Basic Materials | 354.79 | -3.81 | -1.06% |

| Russell 2000 | 1,614.02 | +53.11 | +3.40% |

| S&P/TSX VENTURE COMP IDX | 606.42 | -20.96 | -3.34% |

| XAU | 68.79 | -6.63 | -8.79% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.56 | -0.25 | -9.03% |

| 10-Yr Treasury Bond | 2.53 | -0.10 | -3.95% |

| DJIA | 26,504.95 | +1,505.28 | +6.02% |

| Oil Futures | 61.84 | +8.05 | +14.97% |

| S&P 500 | 2,945.62 | +241.52 | +8.93% |

| Gold Futures | 1,279.60 | -52.00 | -3.91% |

| S&P Energy | 474.50 | +3.69 | +0.78% |

| Nasdaq | 8,164.00 | +882.26 | +12.12% |

| Korean KOSPI Index | 2,196.32 | -8.53 | -0.39% |

| S&P Basic Materials | 354.79 | +20.81 | +6.23% |

| Russell 2000 | 1,614.02 | +114.60 | +7.64% |

| Hang Seng Composite Index | 4,018.04 | +295.95 | +7.95% |

| S&P/TSX Global Gold Index | 178.44 | -13.04 | -6.81% |

| S&P/TSX VENTURE COMP IDX | 606.42 | -16.30 | -2.62% |

| XAU | 68.79 | -7.51 | -9.84% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Anglo American Plc

Equinor ASA

MOL Hungarian Oil & Gas PLC

HSBC Holdings Plc

Ivanhoe Mines Ltd

Polymetal International Plc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Consumer Confidence Index (CCI) is an indicator which measures consumer confidence in the Economy.

The ISM manufacturing composite index is a diffusion index calculated from five of the eight sub-components of a monthly survey of purchasing managers at roughly 300 manufacturing firms from 21 industries in all 50 states.

The Bloomberg Barclays U.S. Municipal Index covers the USD-denominated long-term tax exempt bond market.

The STOXX Europe 600 Index, covering the 600 largest companies in Europe, is divided into 19 supersectors according to the ICB industry classification and reflects the exposure to a certain sector in terms of free-float market capitalization.

The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange.

The SSE Composite Index also known as SSE Index is a stock market index of all stocks that are traded at the Shanghai Stock Exchange.

The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market.

The BSE SENSEX is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange.

The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange.

The standard deviation is a statistic that measures the dispersion of a dataset relative to its mean and is calculated as the square root of the variance.