Investor Alert

Don’t Fall for FUD: Fear, Uncertainty and Doubt

Date Posted: August 20, 2021

Read time: 44 min

So many headlines right now are instilling FUD in investors' minds, which stands for Fear, Uncertainty and Doubt--from the Taliban takeover in Afghanistan, to fears over cryptocurrency, and the delta variant disrupting travel plans across the globe.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

So many headlines right now are instilling FUD in investors’ minds, which stands for Fear, Uncertainty and Doubt—from the Taliban takeover in Afghanistan, to fears over cryptocurrency, and the delta variant disrupting travel plans across the globe.

Don’t let yourself fall for FUD.

There’s no reason to be fearful of cryptocurrency, for example. Many like to say “only bad guys” use these digital assets, but if that’s true, then why are over 100 million people using it today? These people aren’t criminals, they’re consumers and investors, using it on PayPal and Venmo.

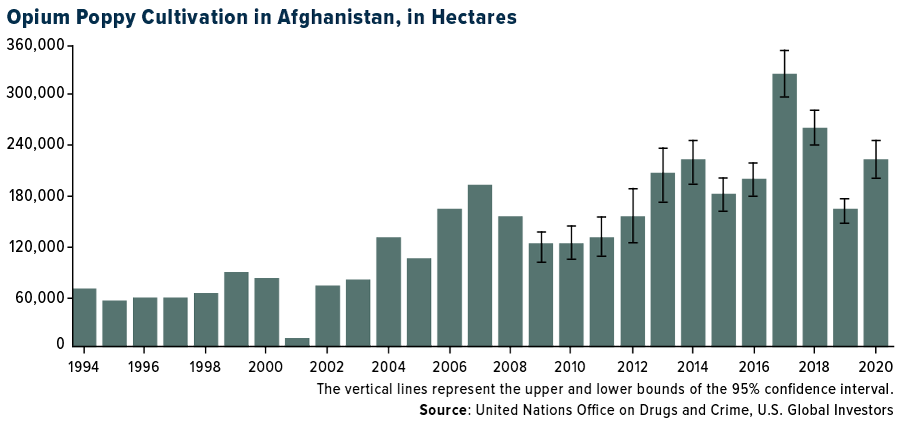

Afghanistan’s Poppy Production Could Be Good for Gold

After 20 years, the longest war in U.S. history is finally coming to a (clumsily handled) close. The war on Afghanistan’s opium poppy production, on the other hand, looks set to escalate, at a potentially great expense to taxpayers.

In case you don’t know, Afghanistan produces a lot of stuff. The United Nations Office on Drugs and Crime (UNODC) estimates that the country is responsible for a whopping 85% of global poppy supply, much of which is used to make morphine, codeine and heroin.

The Taliban “officially” banned poppy cultivation in 2000—but soon realized it couldn’t do without the crop. Poppy is “an attractive insurance policy,” a recent inspector general report says. It’s “lightweight, easy to transport, lucrative and it can be stockpiled to await more favorable market or security conditions.”

Since 2002, the U.S. has spent some $9 billion fighting the Taliban’s narcotics trafficking. Nevertheless, cultivation has continued to ramp up. Last year, the area used to grow opium poppy in Afghanistan increased 37% from 2019—even after U.S. air strikes destroyed a quarter of Taliban-run poppy fields in 2018.

Now that the U.S. military is on its way out, do you think things will improve? I’m guessing no. Billions more will likely need to be spent to combat poppy cultivation and exporting, the Taliban’s number one source of financing.

Gold and Bitcoin Have No Counterparty Risk

This is yet another reminder that U.S. taxpayers and investors need their own “attractive insurance policy” against freewheeling government spending and currency debasement.

For my money, gold is such an asset, as it has no counterparty risk. The more money that’s printed to cover government spending, the more valuable I believe gold becomes.

The same is true of Bitcoin, which many perceive as “digital gold.” But as I told Michael Saylor during this week’s webcast, I don’t think Bitcoin should represent more than 2% to 5% of your portfolio right now. The crypto has incredible upside potential, but as it’s only been around since 2009, it lacks gold’s centuries-long track record as a store of value.

Risk is precisely the reason why Palantir Technologies decided to make an investment in gold. The data analytics firm, founded in part by billionaire Peter Thiel, announced this week that it had stockpiled as much as $50 million worth of gold bars in preparation for “a future with more black swan events.” What’s more, Palantir—named for the all-seeing crystal balls in Lord of the Rings—is also allowing customers to pay for its software in gold.

Palantir’s decision “is only the beginning of what will soon be many major corporations diversifying their U.S. dollar cash into gold,” the National Inflation Association (NIA) wrote in a note to subscribers.

Is Gold Being Manipulated?

That said, Bitcoin is trending up—today it briefly jumped above $49,000 for the first time since May—while gold has continued to trade in a very narrow range since last Monday’s flash crash, which saw the yellow metal plunge below $1,700 an ounce.

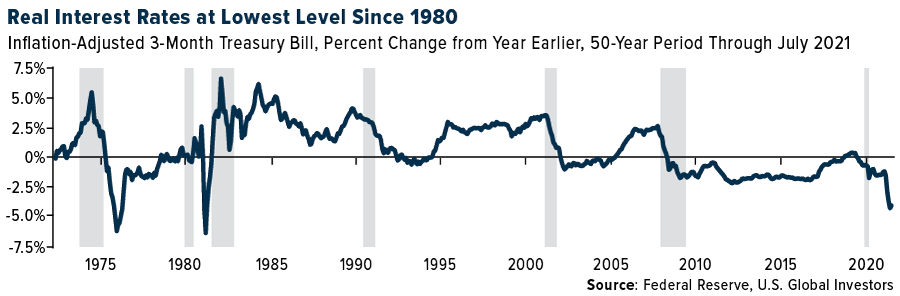

The stronger dollar bears a lot of responsibility for gold’s woes. But something doesn’t add up when inflation is running at 5.4% year-over-year and real rates remain deeply negative. By one measure, rates are lower now than they’ve been since 1980, the same year gold hit its all-time high when adjusted for inflation.

Are investors betting that inflation will be “transitory,” as Federal Reserve Chair Jerome Powell insists?

Or is gold being manipulated?

If you talk to Chris Powell (no relation to Jay), secretary and treasurer at the Gold Anti-Trust Action Committee (GATA), the answer to the latter question is an emphatic yes.

Back in 2019, Chris told me that gold manipulation is largely done through the futures markets and the London over-the-counter (OTC) market. “The mechanisms are gold swaps and leases between central banks and bullion banks, and through the sale of futures contracts,” he said.

When I asked him where he thought gold would be were it not for the kind of institutional manipulation he’s observed, Chris wisely said that the “true value of gold is whatever our free market wants it to be.”

If gold is being suppressed, as Chris and others believe, with G7 countries and central bankers continuing their modern monetary theory (MMT) experiment, the spring effect has the potential to be even greater. We could see gold at $2,000 to $2,400 an ounce.

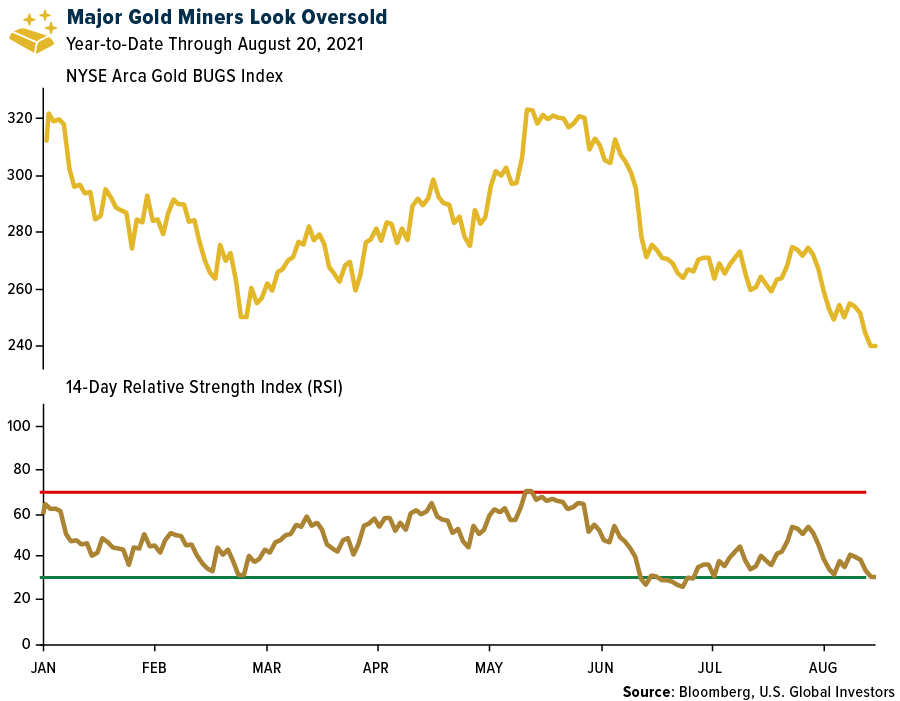

Gold Miners Could Be a Buy

No surprise, but gold miners are also down, as much as 20% for the year so far. Based on the 14-day relative strength index (RSI), the NYSE Arca Gold BUGS Index shows that producers are oversold right now, meaning they could be a buy in anticipation of higher metal prices.

If I were investing, I would focus on the royalty and streaming companies such as Franco-Nevada, Wheaton Precious Metals and Royal Gold. As I’ve explained several times before, these companies provide many of the benefits of the gold mining industry without a lot of the risks.

Recent earnings are evidence of that. Take Franco-Nevada. Despite lower gold prices, the Toronto-based company reported record sales of $347 million during the second quarter, an increase of 78% from the same quarter a year earlier. Adjusted net income came in at $182 million, almost double the income from a year ago.

This sets Franco up for a record year, says Paul Brink, president and CEO, adding that the company’s royalty business model “is particularly attractive during periods of industry cost inflation.”

Missed the webcast this week with Michael Saylor? Read my top 10 takeaways by clicking here!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.11%. The S&P 500 Stock Index fell 0.59%, while the Nasdaq Composite fell 0.73%. The Russell 2000 small capitalization index lost 2.50% this week.

- The Hang Seng Composite lost 6.24% this week; while Taiwan was down 3.77% and the KOSPI fell 3.49%.

- The 10-year Treasury bond yield fell 2 basis points to 1.254%.

Airline Sector

Strengths

- The best performing airline stock for the week was Bangkok Airways, up 20.2%. Azul Airlines noted its domestic Brazilian business demand has recovered to 60% of pre-pandemic levels, with the potential to reach 75-85% by year end.

- European airline bookings stepped up this week, with a big improvement in international bookings likely supported by the removal of U.K. quarantine restrictions for U.S. travelers. Intra-Europe net sales were up 3 points to -36% versus 2019 levels (and versus -39% in the prior week), supported by a declining 2019 base with broadly stable bookings week-on-week. International net sales grew by 8 points to -66% versus 2019 levels (versus -74% in the prior week), with an 11% week-to-week increase. System-wide net sales for flights booked in Europe increased by 8 points to -59% (versus -66% in the prior week).

- Allegiant Air reported July 2021 traffic up 7.3% versus 2019 and up 107% year-over-year. Management reported capacity up 16.4% versus 2019, passengers up 6.4% versus 2019, and a load factor of 81.3% (versus 88.2% in 2019).

Weaknesses

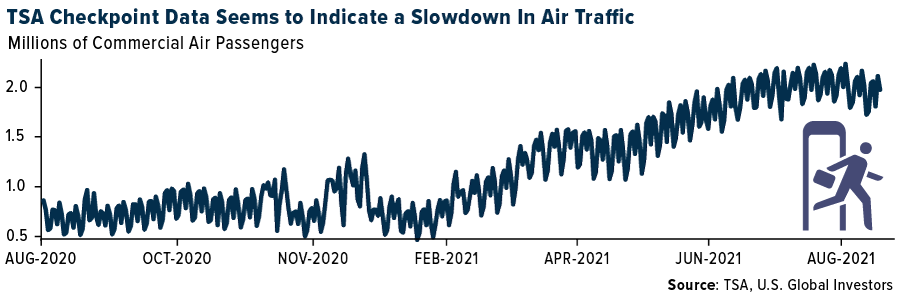

- The worst performing airline stock for the week was Sun Country Air, down 11.0%. More airlines are now noting an impact to bookings and cancellations likely related to increasing COVID-19 cases, specifically linked to the delta variant. There was a further decline in domestic booked traffic for September as well. Booked traffic in the final week for September was -13% versus 2019, compared to -10% last week. The latest September datapoint for corporate bookings is -56% versus -49% last week, and -20% four weeks ago. TSA checkpoint data is also leveling off and trending slightly downward, as can be seen below. In an interview with CNBC, Cowen’s Helane Becker said she believes most travelers feel comfortable flying domestically, but its international travel which seems to be halting.

- Domestic yields were down 20% versus 2019 this week (versus down 15% last week), while September slipped to down 12% from down 5% in August. August international yields were down 24% versus down 23%.

- Spirit Airlines published an investor update, flagging a worsening September quarter revenue environment than previously expected in addition to worse-than-expected costs. Management called out the impact of rising COVID-19 cases in addition to the operational challenges the company has been facing as of late, as the driver of its reduced revenue outlook.

Opportunities

- Alaska Airlines continues its fleet optimization by exercising options early on 12 additional Boeing 737-9 aircraft, which brings the airline’s total firm 737 orders to 93 aircraft, five of which are currently in service. The options exercised are for deliveries in 2023 and 2024.

- The latest American Express Global Business Travel survey shows the majority of clients expect travel to return to normal before the end of 2021. According to the latest update, 98% of clients expect this prior to the end of 2021, and the number of clients ready to travel in the next 30 days is up 47% from where it was in May.

- Southwest Airlines is outlining a path for growth. Next year, the company could take up to 114 aircraft deliveries (assuming options are exercised), which will be used to restore the service cut during the pandemic and due to the 2019 MAX grounding. Management expects growth in 2022 and into 2023 to be fueled by network restoration.

Threats

- Goldman’s pricing study shows that airline fare trends for the holidays have worsened recently. Fares for the Friday departure of Labor Day weekend have turned negative for the first time on a year-over-year basis, and year-versus-2019 performance worsened 10 points from the prior three weeks.

- U.S. airlines’ website visits decelerated to up 2% versus 2019 levels compared to up 6% last week and have been slowly declining since early July. Website data could be a leading indicator of bookings as consumers search for flights before actually booking them.

- Recent data shows a 1% cut in scheduled capacity for each month through year-end. Asia continues to drive the August reduction with a 3% cut (now just at 45% of 2019 levels versus 60% planned a month ago) with China being the main reason as the country is dealing with increasing COVID-19 cases.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 2.6%. The best performing country in Asia this week was the Philippines, gaining 5.8%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 0.25%. The Philippines peso was the best performing currency in Asia this week, gaining 0.58%.

- Hungary’s economy expanded 17.9% in the second quarter from a year earlier, the most since records began in 1996. Analysts expected the figure to read at 16%, (the highest in the European Union after France and Spain), according to a Bloomberg survey.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 1.9%. The worst performing country in Asia this week was Hong Kong, losing 6%.

- The Czech koruna was the worst performing currency in emerging Europe this week, losing 1.4%. The South Korean won was the worst performing currency in Asia, losing 1.5%.

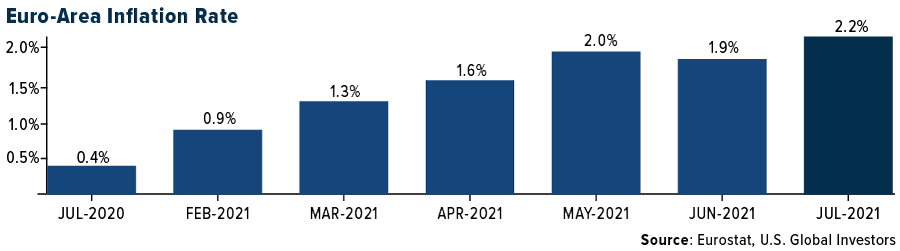

- Eurozone inflation rose to 2.2% in July, its highest rate in almost three years and above the European Central Bank’s target of 2%. The higher rate in July was largely due to a spike in energy prices, which Eurostat said Wednesday rose 14.3% on an annual basis. Inflation, excluding alcohol and tobacco prices, eased to 0.7% from 0.9% in June.

Oppurtunities

- Bloomberg reported that Indian firms have already raised $8.8 billion year-to-date, more than in the past three years and could exceed 2017’s record of $11.8 billion. Some emerging market investors are favoring India as a regulatory safety bet, after China increased the speed of issuing new regulatory policies. This week China said 43 apps violated data transfer rules; they have been given until August 25 to make amendments, otherwise they will be punished in accordance with relevant laws and regulations.

- Reports say that China is willing to help troubled Huarong Asset Management Co., providing the corporation a $7.7 billion cash injection. This bailout will end months of uncertainty over whether Beijing would deem the financial institution too big to fail. This bailout may boost short-term confidence in China’s credit market.

- Europe is pushing forward with its digital COVID certificate, that should simplify travel among European countries. Turkey, the Ukraine and North Macedonia will join the Eurozone’s COVID Certificate Getaway program. Turkish citizens with a vaccine certificate issued by Turkey will no longer be subject to extra pandemic-related measures while traveling to or within Europe. Similarly, Turkey will accept the digital certificate for travel into the country.

Threats

- President Xi of China called for a stronger regulation on high incomes and ask for deeper wealth distribution in the country. A meeting of the Chinese Communist party’s Central Financial and Economic Affair Commission, chaired by President Xi, encouraged high income groups to return more to the society, promoting common prosperity for all.

- According to the Bank of America European fund manager survey for August, less than half of fund managers expect the European economy to improve over the next 12 months, down sharply from 80% in the previous month. Most fund managers are concerned about accelerating inflation in the Eurozone and the spread of the Delta variant of COVID.

- Germany, the largest economy in Europe, will face increased political noise in the next few weeks. Postal voting for Germany’s federal elections began on Monday, six weeks ahead of the September 26 election. Chancellor Angela Merkel will step down following 16 years in power, leaving behind a fractured political landscape in which no party has a comfortable lead.

Energy and Natural Resources Market

Strengths

- Leading indicators continue to signal a year-to-year improvement in U.S. steel demand. Non-residential construction represents the largest consumer of steel, where project starts lead steel demand by 6-12 months. On a national basis, U.S. non-residential building construction starts were up 39% year-to-year in the trailing three months through June.

- European natural gas prices again set records, reports Natural Gas Intelligence, as Russian pipeline imports were poised to fall further next month. This exacerbates fears that the continent would be short of supplies this winter as storage inventories remain low. “European gas fundamentals remain tight, with the persistent weakness of Russian supply as the main source of concern,” Engie Energy Scan analysts said in a note Monday.

- Aluminum in Shanghai surged to the highest close since 2008 after China’s pledge to cut energy intensity exacerbated supply concerns. China, which accounts for more than half of the world’s supply, is urging local governments to adopt strong measures to meet this year’s goal to reduce energy intensity, the National Development and Reform Commission said. The pledge came after 19 provinces including Qinghai, Ningxia and Guangxi missed their targets in the first half.

Weaknesses

- Vine Energy Inc. reported negative revenue of $64.5 million in the second quarter, leading to a $360 million loss for the period, according to a filing with the U.S. Securities and Exchange Commission. The main culprit for the negative revenue was $274 million in unrealized derivative losses in the quarter, along with $24 million in realized losses.

- According to Random Lengths, the Framing Lumber Composite fell by $31 this week to $432, which marks the lowest level since May 2020. Distributors showed little interest in orders as they continue to work down higher-priced inventories, causing weakness across most framing lumber species. In OSB markets, the Composite fell $69 this week to $517.

- China’s crude steel production data showed a decline of 7% year-to-year to the lowest daily rate in 15 months. In addition, prices have fallen 62% and pellet premiums have fallen 40%, while freight rates have increased 20-30%.

Opportunities

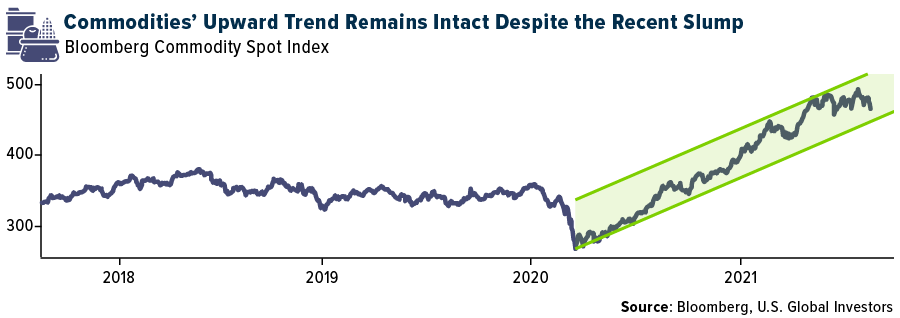

- Commodities remain in an uptrend, despite headwinds from the delta variant. This week’s petroleum inventories update was bullish relative to consensus. "Big Three" petroleum inventories (crude, gasoline, and distillates) fell by 5.2 million barrels, versus consensus estimates for a draw of 3.3 million barrels. Turning to crude, total inventories fell by 3.2 million barrels, versus consensus calling for a draw of 1.3 million barrels and a normal seasonal draw of 1.7 million barrels. Refinery utilization rose to 92.2% from 91.8% last week.

- BHP Group’s deal to merge its oil and gas business with Woodside Petroleum Ltd. will potentially create one of the world’s top-five LNG producers, according to Credit Suisse Group AG. Demand for the gas is expected to grow faster than any other fossil fuel over the next decade, as Asian nations accelerate a shift away from coal to reduce greenhouse gas emissions. BHP’s unit could be valued at more than $15 billion, a person familiar with the details said last month. BHP also approved $5.7 billion (C$7.5 billion) in capital expenditure for the Jansen Stage 1 potash project in the province of Saskatchewan, Canada.

- Sugar prices extended their gains, with recent extreme weather in Brazil continuing to impact supply. Sugar prices have increased after extreme drought and frost damaged crop supply in Center-South Brazil, where most of the world’s supply is produced. The weather conditions, the worst in more than two decades, means the country’s sugarcane crop will be reduced for a second straight year.

Threats

- This week’s drop for iron ore accelerated, with futures sliding as much as 14% to the lowest since December in Singapore. The drop comes on the back of expectations that Chinese steel output and consumption will weaken over the rest of the year, partly as authorities curb pollution. Prices are more than 40% below a record high reached just three months ago.

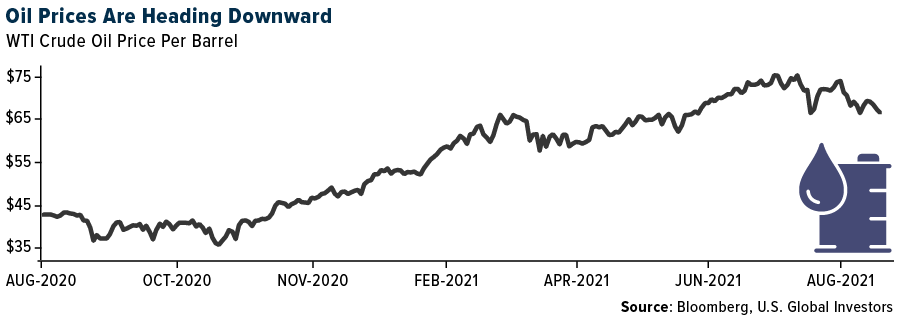

- Oil sank again as Chinese economic data disappointed, and the spread of the delta variant hurt prospects for global demand. West Texas Intermediate (WTI) also slumped as fresh outbreaks in Asia have started weighing on China’s economy, with retail sales growth and industrial output slowing. Cases are also at or near records in nations including Thailand, Vietnam, and the Philippines.

- Copper declined to near a one-month low in London, as the spread of COVID-19 in China weighs on the demand outlook. Base metals have come under pressure in recent weeks as authorities in China race to contain an outbreak of the virus and investors across global markets weigh the risks that localized lockdowns could disrupt both demand and supply in key industrial areas and logistics hubs.

Domestic Economy and Equities

Strengths

- After disappointing prints in June, U.S. Industrial Production and Manufacturing Output was expected to rebound in July, and it did. Industrial Production rose 0.9% month-over-month, way above the expected increase of just 0.5%. Manufacturing output in July rebounded by 1.4% month-over-month (versus just +0.7% as expected) and after June’s unexpected 0.1% decline.

- Unemployment claims declined again this week, providing another sign of the labor market improving. Initial jobless claims dropped to 348,000 from 375,000, below the anticipated 364,000.

- Kroger, a grocery store operator, was the best performing S&P 500 stock for the week, increasing 10%. Bloomberg reported that Warren Buffett’s Berkshire Hathaway purchased shares in the company.

Weaknesses

- Housing starts disappointed expectations in July, falling 7.0% to 1.534 million, while housing permits beat expectations, increasing 2.6% to 1.635 million. JPMorgan research team said that the trends in the starts and permits data have softened lately during a time in which many other housing indicators also have weakened. This cooling has been particularly noticeable in the starts and permits data for single-family units.

- FactSet reported that companies across a wide range of industries continue to flag global supply chain pressures, which act as a headwind on both sales and margins and are expected to persist to the rest of this year. The chip shortage continues to grab the bulk of the headlines.

- Occidental Petroleum was the worst performing S&P 500 stock for the week, losing 15%. The company’s share price corrected with oil trading lower.

Opportunities

- The Biden administration said in a letter to lawmakers Thursday that it’s appropriate for expanded unemployment benefits to expire as scheduled in a little more than two weeks. Many Republicans have argued that the expanded unemployed benefits made Americans refuse to return to work; many Democrats, conversely, have argued that low wages are the cause of Americans lack enthusiasm to return to work. The United States has a record level of open jobs with more job openings than the number of people unemployed. It is believed that ending these measures will help companies fill up these open positions.

- Despite the risk-off theme this week, equities have continued to see strong inflows. Bank of America’s Flow Show report noted that global equities attracted $23.9 billion in the week-ended August 18, the most in nine weeks. In addition, the United States equities attracted $12.8 billion, also the largest in nine weeks. Investors are buying at the dips.

- The Federal Reserve’s annual Jackson Hole Symposium will take place next week with Powell set to speak on Friday. His speech may offer more clarity on tapering.

Threats

- The Empire and Philadelphia Federal Manufacturing indexes both declined in August and suggest the national Manufacturing PMI declined as well. The preliminary Manufacturing PMI for August will be released on Monday and Bloomberg economists predict it falling to 63.0 from 63.4 which is still a very strong level.

- Health officials announced on Wednesday that the United States will start widely distributing COVID booster shots beginning the week of September 20 to address the transmissible delta variant that is driving a surge in cases. The booster decision came after a review of a raft of new data from the CDC that showed a worrying drop in vaccine efficacy over time.

- Equities have been trading higher and with the growing number of COVID cases, geopolitical global tensions with Afghanistan, inflation accelerating and confusion regarding Fed tapering in the United States, some correction could follow.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was UNIDOWN, rising 9,858,179%.

- Cardano’s ADA Token is now the world’s third largest cryptocurrency, writes Bloomberg. The token has rallied over 50% amid booming DeFi demand and comes in as the largest cryptocurrency right behind Bitcoin and Ethereum.

- The Economic Times reported this week that India has been ranked second in terms of cryptocurrency adoption, amid a bull run in cryptocurrency assets globally this year. A new report from Chainalysis shows that worldwide crypto adoption grew over 881% in the last year, and countries in the emerging markets sector led ahead of the U.S. and European nations, driven by peer-to-peer platform trading.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Bitcoin Networks, down 97.59%.

- According to a statement distributed to Australian investors by the Australian Securities and Investments Commission (ASIC), many investors have experienced significant losses after trading cryptocurrency financial products such as options, futures, and leveraged tokens. Many of these can be attributed to “excessive leverage, platform outages, or unfair liquidations.” Due to this information, the regulator is now issuing warnings about unlicensed entities that offer these financial products as they gain in popularity.

- Poly Network, the China-based blockchain protocol exploited earlier this month for more than $600 million, said on Thursday that it sent a bounty worth nearly $500,000 to the attacker, reports CoinDesk, and that most of the looted cryptocurrency has now been fully recovered. Unfortunately, the attacker has yet to provide the key needed to unlock the remaining $141 million.

Opportunities

- Walmart Inc. is looking to hire a cryptocurrency expert to develop a blockchain strategy, writes Bloomberg, joining a growing number of major corporations exploring the feasibility of digital currencies like Bitcoin or Ethereum. According to the posted job description, the position will be responsible for “developing digital currency strategy and product roadmap,” and identifying “crypto-related investments and partnerships.”

- HIVE Blockchain Technologies, a public mining company listed on the Nasdaq (HVBT) and Toronto Venture (HIVE) exchanges, announced the appointment of Aydin Kilic as President and Chief Operating Officer of the company this week. Mr. Kilic, who founded Fortress Blockchain Corp. in 2017, will now oversee all of HIVE’s operational activities across its facilities in Canada, Iceland, and Sweden. In the U.S., a top regulator signaled a path towards approval for Bitcoin ETFs. ProShares, Investco, VanEck, Valkyrie Digital Assets, and Galaxy Digital have all filed plans for Bitcoin futures ETFs. Last month, the SEC approved the first U.S. Bitcoin-futures-based mutual fund, which is currently up and trading.

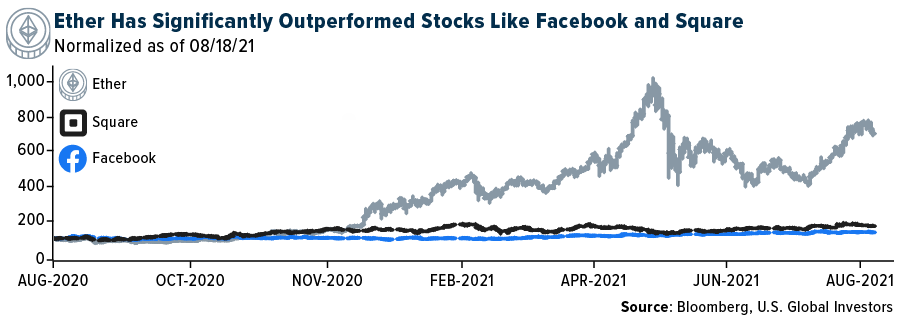

- Jack Dorsey, CEO of Square Inc., and Facebook’s Mark Zuckerberg may be making big plans in the cryptocurrency space, writes Bloomberg, but Ethereum inventor Vitalik Buterin is skeptical if they can gain traction. Buterin casts doubt on Dorsey’s plan for the company to create a new business focused on decentralized financial services that use Bitcoin. As seen in the chart below, Ethereum currently outperforms both Square and Facebook. Time will tell if the opportunity still exists for these names.

Threats

- The Chinese central bank’s branch of Shenzhen ordered almost a dozen companies operating in the technology hub to remedy illegal activities related to cryptocurrencies, according to Bloomberg, signaling an intensifying crackdown on digital assets. The People’s Bank of China (PBOC) “cleaned up” 11 firms allegedly involved in illegal activities. China has launched a new campaign against cryptos this year, the article continues, acting against miners and imposing curbs on crypto banking services and trading.

- Japan’s Liquid Global exchange tweeted on Thursday that it has been hacked, reports CoinDesk, and has suspended both deposits and withdrawals. The exchange said that its warm wallets were compromised and that it was moving digital assets offline. Senior researcher at OKLink, Eddie Lang, told CoinDesk that the value of coins stolen could be upward of $90 million.

- Binance, the world’s largest crypto exchange, is still on the quest for legitimacy in the United States, writes the New York Times, pursuing an IPO of its American unit. Unfortunately, after only three months on the job, CEO of Binance Brian Brooks left the company due to “strategic differences.” Brooks, a former regulator, was tasked with helping the company gain a U.S. footing, the article continues. He left following a venture capital investment he was putting together for Bianance.US that fell through.

Gold Market

This week spot gold closed the week at $1,781.11, up $1.37 per ounce, or 0.08%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.96%. The S&P/TSX Venture Index was off 6.34%. The U.S. Trade-Weighted Dollar rose 1.02%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-15 | China Retail Sales YoY | 10.9% | 8.5% | 12.1% |

| Aug-18 | Eurozone CPI Core YoY | 0.7% | 0.7% | 0.7% |

| Aug-18 | Housing Starts | 1,600k | 1,534k | 1,650k |

| Aug-19 | Initial Jobless Claims | 364k | 348k | 377k |

| Aug-24 | New Homes Sales | 700k | — | 676k |

| Aug-25 | Durable Goods Orders | -0.2% | — | 0.9% |

| Aug-26 | Hong Kong Exports YoY | 26.3% | — | 33.0% |

| Aug-26 | Initial Jobless Claims | 352k | — | 348k |

| Aug-26 | GDP Annualized QoQ | 6.6% | — | 6.5% |

Strengths

- The best performing precious metal for the week was gold, up just 0.08%. Gold headed for a weekly gain as investors turned to the haven asset amid concerns over the delta coronavirus variant and weaker economic data. A gauge of New York State manufacturing moderated in August after expanding at an unprecedented pace a month earlier, while a measure of selling prices advanced to a fresh record. Chinese retail sales and industrial output data showed activity slowed due to fresh lockdowns to contain the Covid-19 outbreak there. The data underscored broader concerns over threats to the global recovery from rising prices and virus cases, boosting bullion as a haven asset. Treasury yields and inflation-adjusted real yields also fell, increasing the metal’s appeal.

- Newcrest Mining Ltd., Australia’s largest gold producer, said annual profit rose 55% from a year earlier, with earnings driven by increased production and higher prices. Underlying profit rose to $1.16 billion in the year to June 30 from $750 million a year earlier. This was higher than the consensus of $1.1 billion.

- Aluminum in Shanghai surged to the highest close since 2008 after China’s pledge to cut energy intensity exacerbated supply concerns. China, which accounts for more than half of the world’s supply, is urging local governments to adopt strong measures to meet this year’s goal to reduce energy intensity, the National Development and Reform Commission said. The pledge came after 19 provinces including Qinghai, Ningxia and Guangxi missed their targets in the first half.

Weaknesses

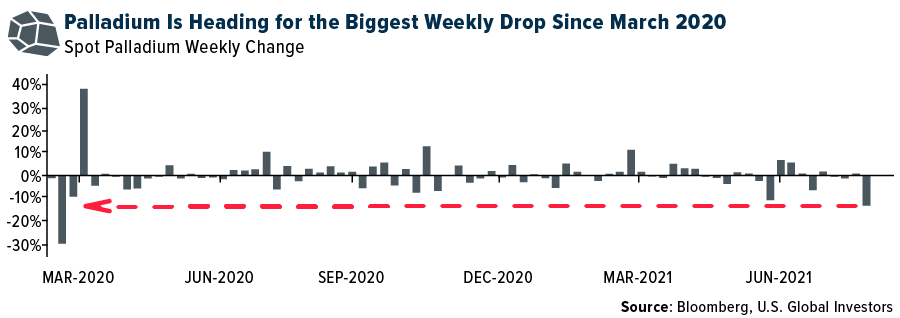

- The worst performing precious metal for the week was palladium, down 14.09%. Palladium headed for its biggest weekly decline since March 2020 as a shortage of automotive chips weighed on demand from carmakers. The metal, 85% of which goes into catalytic converters, was down about 13% this week.

- Gold shipments from Europe’s key refining hub fell to 94.1 tons last month from 125.9 tons in June, according to the Swiss Federal Customs. Swiss gold imports fell 16% to 141.2 tons. Exchange-traded funds continue to sell, bringing this year’s net sales to 6.79 million ounces, according to data compiled by Bloomberg. The sales were equivalent to $177.2 million at the previous spot price. Total gold held by ETFs fell 6.3 percent this year to 100.3 million ounces.

- India’s new purity standards for gold could hurt demand from the second-biggest consumer just as demand is expected to rebound. Jewelers may find it difficult to fulfill orders during the peak festival season starting next month, as they are facing delays in getting their goods certified under the country’s new hallmarking standards.

Opportunities

- Palantir Technologies said it’s preparing for another “black swan event” by stockpiling gold bars and inviting customers to pay for its data analysis software in gold. The company spent $50.7 million this month on gold, part of an unusual investment strategy that also includes startups, blank-check companies and possibly Bitcoin. Palantir had previously said it would accept Bitcoin as a form of payment before adding precious metals more recently. This could set a trend where CIOs of companies may consider some excess cash in bullion as a way to hedge against broad risks in the economy and inflation gains relative to no real returns on cash or the volatility of cryptocurrencies.

- Gold Fields Ltd. is looking at acquiring assets to replace depleting mines as the company’s new chief executive officer seeks to ensure that output doesn’t decline from a projected peak in three years. A new Chilean operation starting in 2023 plus increasing production from its last South African mine will help the Johannesburg-based producer lift output to 2.7 million ounces by 2024. Gold Field’s dilemma is how to find an asset that the market has not priced correctly. Gold Fields has operations in Africa, South America and Australia and may consider these jurisdictions first.

- Rio2 Limited and Sixth Wave Innovations Inc. entered a contract for further testing of Sixth Wave’s patented IXOS purification polymer to replace carbon in a traditional Carbon-In-Leach (CIL) circuit for recovering the gold. These engineered polymer beads can be reused multiple times whereas the carbon has a shorter recycling life. This IXOS polymer beads can potentially works better by faster absorption efficiency, quicker elution times, and overall absorption kinetics.

Threats

- Teck Resources is suspending its Highland Valley mine in south-central British Columbia due to the wildfire evacuation order. National Bank’s Shane Nagle said the mine contributes 9% to the company’s net-asset-value estimates and the news is a “modest negative” for the stock.

- American Gold & Silver continues to be beset by delays. Relief Canyon continues to struggle with carboniferous ore on the pad, producing only 1,200 ounces in the quarter. To conserve capital, the company is suspending operations until a new path forward can be determined. The Cosalá operation remains under a blockade, and there may not be a restart of operations until 2022.

- Dominic Schnider, head of commodities at UBS Wealth Management, thinks gold and silver could drop closer to $1,600 and $22 an ounce, respectively, in an improving global outlook. Schnider cited the precious metal platinum as a better investment due to industrial demand. In contrast, Goldman Sachs forecasts $2,000 and $30 per ounce for gold and silver, respectively, by year-end.

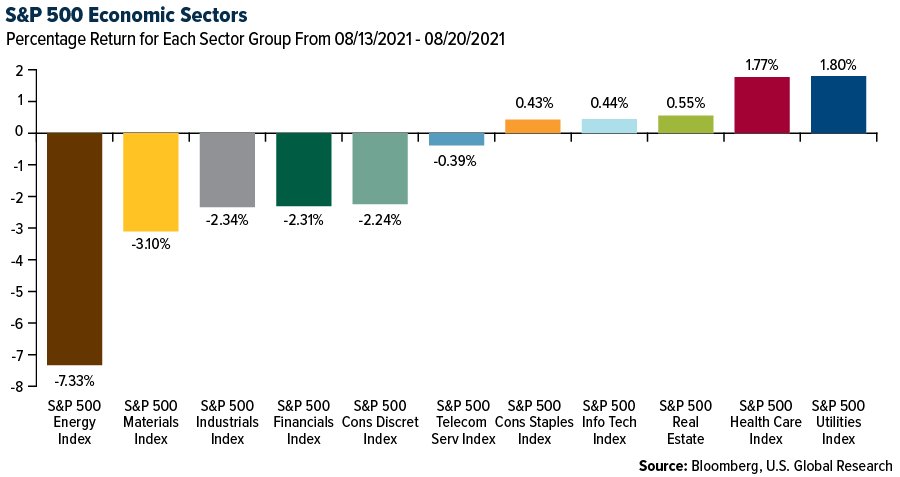

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Alaska Air Group

Allegiant Travel Co.

Azul SA

HIVE Blockchain Technologies

Spirit Airlines

Southwest Airlines

Franco-Nevada Corp.

Wheaton Precious Metals Corp.

Royal Gold Inc.

Gold Fields Ltd.

Sixth Wave Innovations Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The relative strength index (RSI) is a momentum indicator used in technical analysis that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The NYSE Arca Gold Bugs Index is a rules-based, modified equal weighted equity benchmark designed to track the performance of companies involved in the mining of gold ore that do not hedge their production beyond 1.5 years. The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity.