Investor Alert

Fossil Fuels Are Under Siege. Is Misinformation to Blame?

Date Posted: September 17, 2021

Read time: 45 min

It’s becoming more and more difficult to be in the fossil fuel business. On both sides of the Atlantic, lawmakers and unelected bureaucrats are turning up the heat, so to speak, on companies over the issue of climate change.

In the U.S. House of Representatives, Democrats have launched an inquiry into whether oil companies have participated in so-called “climate disinformation.” This week, letters were sent to top executives of Exxon Mobil, BP, Chevron and Royal Dutch Shell seeking records, and hearings are scheduled for next month.

Meanwhile, the Securities and Exchange Commission (SEC) is expected to propose a series of new disclosure requirements all publicly traded companies must make, possibly as soon as year-end, to inform investors about potential climate risks associated with their business.

In Europe, the strategy appears to be to choke off any and all lending to the fossil fuel industry. Next year, the European Central Bank (ECB) is expected to look into the trading operations of major banks in what’s being called a climate “stress test,” and at least one big activist investor group, ShareAction, is pressuring lenders to cut all ties to fossil fuels.

Of course, none of this accounts for the fact that fossil fuels still supply around 80% of the world’s energy.

Or that many leading oil and gas producers are investing billions in renewable energy, including wind and solar, and energy storage technology. Chevron, in fact, just unveiled plans to triple its investment in lower carbon energies to $10 billion through 2028.

Could Climate Scientists Be Held Liable?

Climate change was top of mind at the Gold Forum Americas conference I attended and spoke at this week in Denver.

In conversations I had with some of my peers, the question was raised whether certain scientists could be held financially liable for spreading their own “climate disinformation,” which has sown fear and prompted policymakers to enact new draconian taxes and regulations.

Here’s how one colleague put it: In nearly every other profession—from physician to engineer to money manager—there are mechanisms in place to hold bad actors accountable. Why is that not the case with scientists, who may make promissory or misleading statements that materially impact individuals and businesses?

The idea sounds farfetched, but it’s not completely unheard of. In 2012, an Italian court found six seismologists guilty of manslaughter for failing to give proper warning of an earthquake that killed some 300 people. This ruling was overturned in 2014, but it had the effect of putting public facing scientists around the world on high alert.

To be clear, I don’t support charging scientists with crimes. Modern technology, as advanced as it is, still cannot successfully predict earthquakes with any degree of certainty.

Fewer, Not More, Hurricanes Making Landfall in the U.S.

Perhaps the same is true of the climate. We are led to believe that climate change is responsible for causing more hurricanes, for instance, but if you look at the Environmental Protection Agency’s (EPA) own data, you’ll find that the number of North Atlantic hurricanes that strike the U.S. every year has been trending down over the past 120 years. To date, the deadliest natural disaster in U.S. history remains the Great Galveston hurricane, which pummeled the Texas city in 1900, several years before Henry Ford even began mass producing the Model T.

I’m bringing all of this up not to pick a fight. I happen to believe a majority of climate scientists do honest work and have good intentions. The problem is that they also have the ear of some agenda-driven politicians and bureaucrats who actively seek out new reasons to make it more difficult to run an energy or mining company.

U.S. on the Verge of Becoming the Least Vaccinated G7 Country

Up until this point, I haven’t said anything about the media’s role in spreading FUD, or fear, uncertainty and doubt. The cause of a lot of people’s apprehensions can be laid at the feet of not just cable news channels, which sensationalize everything, but also social media platforms, which have allowed misinformation to run wild.

Here, I’m talking specifically about misinformation related to vaccines.

This topic also came up in Denver. I’m fully vaccinated against Covid and have even received a third booster shot, but many of my colleagues haven’t gotten their first jabs. When I ask why, they invariably say it’s because they don’t trust the government.

If that’s the case, I say, do they own gold or Bitcoin?

That aside, I believe the vaccine is our best hope to get back to life as it was before the pandemic. The planes and airports were packed on my way to and from Denver, but Transportation Security Administration (TSA) data shows that commercial air traffic is still down around 25% from the same time in 2019. That’s partly due to the fact that too many Americans are choosing not to get vaccinated.

In fact, the U.S. is about to become the least vaccinated high-income G7 country. Despite the U.S. having the largest stockpile of Covid vaccines, and despite it having a dramatic head start, the country will soon have the lowest vaccination rate of any G7 nation after Japan surpasses it, probably this weekend.

Ancillary Fees Helped Keep Airlines Afloat in 2020

I’ll end with some positive financial news from 2020. In a year when air traffic was clobbered by the pandemic, airlines managed to keep the lights on thanks in large part to ancillary fees. Like sales in general, ancillary fees fell in absolute terms, but they represented a bigger piece of airlines’ total revenue last year.

Low-budget carriers appeared to benefit the most. Non-ticket sales were nearly 56% of Hungary-based Wizz Air’s total sales, the highest of any other company. Spirit Airlines was a close second, followed by Allegiant Air, Frontier Airlines and Ryanair.

More good news came out of Ryanair this week. The Irish low-cost carrier announced that it was lifting its growth target to 50% over the next five years, up from a previous target of 33%. This would mean Ryanair would carry more than 225 million passengers a year by 2026, after expanding into markets such as Italy, Scandinavia and Morocco. By this winter, the carrier hopes to operate about 90% of its pre-Covid capacity. Wheels up!

Curious to know the world’s top 10 airlines of 2021? Click here to see the countdown!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.07%. The S&P 500 Stock Index fell 0.58%, while the Nasdaq Composite fell 0.47%. The Russell 2000 small capitalization index gained 0.42% this week.

- The Hang Seng Composite lost 4.93% this week; while Taiwan was down 1.13% and the KOSPI rose 0.47%.

- The 10-year Treasury bond yield rose 2 basis points to 1.368%.

Airline Sector

Strengths

- The best performing airline stock for the week was Sun Country, up 16.1%. European airline bookings showed a strong increase this week, with both intra-Europe and international net sales reaching their highest post-pandemic levels. Intra-Europe net sales were up by 5 points to -41% versus 2019 (versus -46% in the prior week) and increased by 7% on a week-on-week basis. International net sales improved by 6 points to -69% versus 2019 (versus -75% in the prior week), with 3% week-to-week growth. This drove a 7-point increase in system-wide sales for flights booked in Europe to -61% versus 2019 (versus -68% in the prior week).

- Brazilian airline GOL announced that it has agreed to expand its commercial cooperation with American Airlines through an exclusive codeshare agreement for the next three years, reports Reuters, deepening the relationship between both airlines. More importantly, as part of the agreement, GOL will receive an equity investment of $200 million from American. American will have a 5.2% stake in the company.

- Credit Suisse is seeing an initial, compelling stage of recovery for airlines, but specifically highlights that it expects to see continued attractive market share gains from Ryanair (as its competitors struggle to recover as quickly). The group’s global LCC penetration model suggests that Ryanair’s market share could head toward 25% as it leverages network and efficiency gains, while competitors grapple with the challenges of restructuring cost bases as supplier costs and labor costs rise.

Weaknesses

- The worst performing airline stock for the week was China Southern, down 10.8%. There were some small reductions in September schedules which slightly reduced total capacity for the month to -9% sequentially (versus -8%) and -18% versus 2019 levels (versus -17%). November and December schedules had more consistent reductions take place with November capacity 3% lower. October capacity continues to trend to -16% versus 2019, while November is now -8% (versus -5%) and December is -3% (versus +1%).

- October traffic worsened meaningfully to -39% from -22% versus 2019 levels, while the latest week for November was -29%. International routes saw similar traffic trends with October being down 61% versus 53% in the prior week.

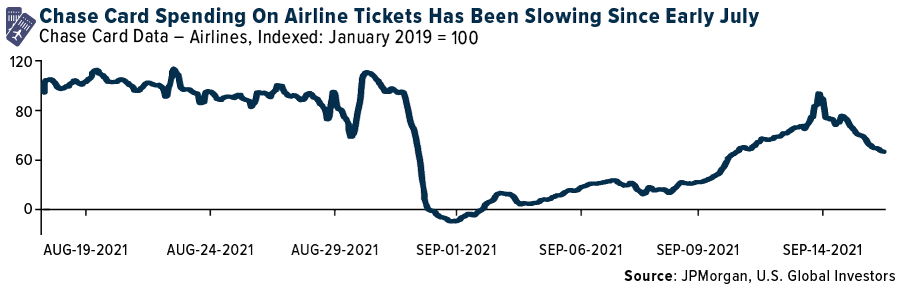

- According to JPMorgan, airline credit card spending has been under pressure since the third week of July, synchronized with delta variant headlines turning undeniably grim. Week-on-week spend data turned negative on July 18 and has continued to contract since.

Opportunities

- The U.K. may remove mandatory testing for travelers via an announcement by the prime minister, reports Bloomberg. By removing the expense related to testing, this could help demand for shorter, off-peak trips (such as over a weekend or during the winter).

- For easyJet, the 1.2 billion British Pound (GBP) rights offering will boost the company’s balance sheet and enhance its ability to compete with legacy carriers at primary airports (leverage falls to 1X net debt/EBITDA). The U.K. government’s plans to potentially remove the traffic light system and expensive PCR tests for vaccinated travelers would also be a positive for easyJet.

- Bloomberg has reported a potential valuation of EUR 3.5 billion-5 billion for Lufthansa Technik (LHT), as deliberations between the company and its advisors continue over whether to pursue a sale or an initial public offering (IPO).

Threats

- Raymond James downgraded Azul Airlines and GOL to “underperform” from “neutral” on valuation and COVID-driven uncertainties. In its view, these leading Brazilian airlines have done an impressive job adjusting operations, negotiating liabilities, and sustaining liquidity throughout the pandemic. However, the group does see limited upside to current valuation levels and notes the “COVID bill” in Brazil can still impact cash flow.

- Daily website visits for European Union (EU) airlines fell by 4 points to -22% (versus -18% in the prior week). Iberia showed the largest decline by 14 points, followed by Wizz Air at a decline of 10 points. All other airlines, except British Airways, showed declines.

- The consensus is growing among management teams that the corporate recovery is likely pushed back to 2022 from this fall, given the return-to-office delays of major companies. Corporate demand has been down in the 50-60% range versus 2019 since June, after being down 90% in January and down over 70% in May. Delta Air Lines mentioned last week that it sees a 90–120-day delay in corporate recovery.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was the Czech Republic, gaining 1.6%. The best performing country in Asia this week was India, gaining 1%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 0.53%. The Pakistani rupee was the best performing currency in Asia this week, gaining 0.30%.

- Eurozone’s industrial production increased by 1.5% month-over-month in July, above the expected reading of 0.60%. Year-over-year industrial production increased by 7.7%, above the expected 6.0%.

Weaknesses

- The worst performing country in emerging Europe for the week was Turkey, losing 1.8%. Hong Kong, losing 4.95%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 2%. The Thailand baht was the worst performing currency in Asia this week, losing 1.7%.

- China released weaker economic data this week. Money supply growth slowed further, to 4.2% year-over-year in August from 4.9% in July. Retail sales grew by 2.5% in August on a year-over-year basis below the expected 7%. Industrial production increased in August by 5.3% year-over-year versus the expected 5.8%.

Opportunities

- Chinese women will be the main drivers of an expected $5.3 trillion boom in consumer spending over the next two decades as their income rises, UBS Group AG said. Consumption growth through 2030 will be 80% driven by expansion in women’s income. This should benefit international companies in luxury, cosmetic, sportswear, auto, travel, lodging and leisure.

- Southeast Asia, which in August had the world’s worst COVID-19 death rates, has seen its cases begin to decline. Daily cases have dropped 30% from the peak seen a month and a half ago and fatalities have fallen below 14,400 patients a day, half of their highest level, according to analysis of seven-day averages based on data from Johns Hopkins University. Some of the countries in the region started to lift restrictions and open their economies.

- The second line of gas pipeline, North Stream 2, connecting Russia with Germany has been completed. The pipeline now needs to be tested and certified, with the timeline remaining unclear. Earlier, it was reported that gas supplies via the first line of NS 2 might start on October 1, and both lines could be working by December 1.

Threats

- Hong Kong stocks continue to trade lower. This week the Hong Kong Exchange saw a bigger decline in Macau gaming stocks on fears that the government could introduce tighter gaming regulations. Some Macau stocks lost a third of their value on Wednesday. Shares of Wynn Macau declined by 29%, Sand China 32.5%, and MGM China 26.8%.

- Analysts are increasingly expecting a managed collapse of the Chinese real estate developer Evergrande that seeks to protect smaller investors rather than a bailout with bondholders taking a haircut. Some unverified documents showed wide bank exposure with liabilities extending to more than 128 banks and more than 121 non-bank institutions, FactSet reported.

- Central banks in central emerging Europe most likely will continue to hike rates. The Czech Republic, Russia and Hungary have been raising rates due to above-target inflation. Poland will likely join the tightening policy and Hungary will likely hike again next week.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was uranium, up 12.62%. According to Bloomberg, top uranium miner Kazatomprom said it may supply the metal to Sprott Inc., the investment firm whose aggressive bets on the market have helped drive a surge in prices. Coal prices continue to move higher. The price of metallurgical coal continues to rise sharply due to a decrease in supply in China because of a coal mine accident in Shanxi and environmental regulations.

- Lumber pricing continued to make gains while mills extended order files. Lumber ended the week up 8% at $460, down 62% relative to the second quarter of 2021, down 52% year-over-year and up 73% this year. Trading was up once again although sales activity slowed as some mills remained off market due to the aftermath of Hurricane Ida. Pricing for North Central 7/16” ended the week up 1% at $440, down 42% relative to the second quarter of 2021, down 34% year-over-year and up 111% this year.

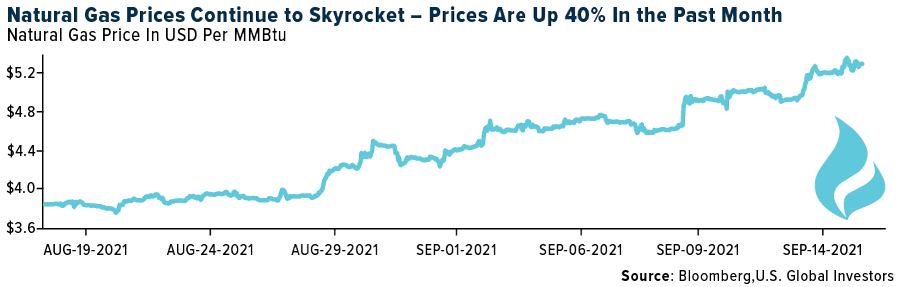

- Natural gas markets continue to spike higher. So far in 2021, producer discipline has left supply relatively stagnant while rising exports (liquefied natural gas and the pipeline to Mexico) have led to higher demand. This has driven Henry Hub over $5, the highest seasonal price since 2008.

Weaknesses

- The worst performing commodity for the week was iron ore, falling 11.89%. Iron ore prices fell again this week, as low buying activity weighed on prices. S&P Global Platts notes that Chinese steel production cuts have picked up in September and should increase further as cumulative production moves toward the production cap. Chinese blast furnace utilization fell 0.6% to 73.6%. On the supply side, weekly exports of iron ore from major producers fell 10% this week despite no notable disruptions, although the decline may in part be due to the Typhoon Chanthu, which is impacting freight rates according to Platts. Using previous downturns as a guide, $70 to $85 per ton is the level where the iron ore market should start to re-balance, as higher-cost producers are squeezed, according to T. Rowe Price’s investment analyst Tom Shelmerdine.

- Trade sources indicate that polyethylene production that remains shut down is still at 9% of U.S. capacity, unchanged from the prior week. Last week, PVC prices and margins continued to remain high at $1,400 per ton on supply crunch concerns amid persisting U.S. plant shutdowns. According to Platts news last Friday, around 40% of PVC capacity in the U.S. had been shut after Hurricane Ida.

- The Chilean Copper Commission Cochilco has revised its average copper price projection to $4.20 per pound for 2021, according to a presentation on Tuesday, September 14. This is lower than its previous prediction in May when it put the average at $4.30 per pound. The forecast for 2022 remains at $3.95 per pound. Cohilco said the slowdown in the Chinese economy and growing expectations that the United States Federal Reserve will soon withdraw stimulus measures were negative price factors behind the revision.

Opportunities

- China’s leading copper producer, Jiangxi Copper, will develop the Mes Aynak copper mine in Afghanistan with Metallurgical Corp of China when conditions allow, the company said. Due to the unstable situation in Afghanistan, there has not yet been any substantial construction at the mine, but the two companies are monitoring the situation and will push forward with the project when they can, reports Jiangxi Copper.

- Bank of America held a conference call with Melih Keyman, CEO of Keytrade, a global fertilizer trader. Mr. Keyman remains constructive on all three primary nutrients due largely to robust grain-driven demand, tight global inventories, high freight rates ($60USD/ton now versus $20USD/ton one year ago), and greater than normal trade disruption from government actions. Phosphate prices have gone from 10-year lows to 10-year highs in the last 20 months, and Mr. Keyman expects prices to be sustained over the next several months or more. Even with currently high prices, demand destruction has yet to occur in most major regions and inventories remain low.

- Chilean copper miner Codelco’s management and the Sindicato de Unión Plantas (Suplant) trade union reached a new collective wage agreement on Friday, September 10. The Suplant union, which represents employees at the company’s Andina concentrator plant, rejected the last offer that came within the standard negotiation period and started its strike on August 17, a few days after two other unions at Andina had started their own separate strikes. The other unions, SIIL and SUT, reached agreement with Codelco on Thursday, September 2. Counted together, the three unions represent more than 1,300 of the 1,437 workers at Andina.

Threats

- The Baltic Dry Index, which tracks the cost to ship major raw materials including coal and iron ore by sea, has climbed to its highest level since late-2009. The index has been rising since bottoming out in mid-2020 due to strong demand on increased consumer spending, as well as supply constraints related to COVID-19 and a lack of investment in new capacity following the last down cycle, states The Economist. While the strong demand is a positive signal for metals end-use, rising shipping prices and constraints could signal that further logistical challenges and cost inflation are on the horizon. Spot rates for container ships to move finished products have surged for the last 20-weeks and now stand 731% over their seasonal average of the last five years, according to Drewry Shipping.

- Russia’s Finance Ministry is focusing on extraction taxes again to raise money from mining and metals companies, according to the three people who took part in the discussions. The ministry’s latest proposal includes an increase in the base rate for the mineral extraction tax and a link to raw material prices starting from 2022, the people said.

- Europe’s energy crises are now spreading to the fertilizer industry which has ramifications to produce meat, vegetables and grains, which likely means higher prices for these essential staples. Yara International noted that record high prices for natural gas are consuming their margins to produce ammonia, curtailing their production to about 40%. C.F. Industries Holdings Inc. said it’s halting two U.K. production plants due to skyrocketing costs. Yara trades roughly one-third of the world’s ammonia which is not only used to produce fertilizer, but other industries such as the automobiles, textiles, health care and cosmetics. The U.N. measure of global food prices is already near the highest in a decade.

Domestic Economy and Equities

Strengths

- The Empire State Manufacturing Index for September came in at 34.3, well ahead of the consensus for 17.9 and August’s 18.3 level. Many economists use this data to get a sense of national manufacturing conditions.

- Inflation in the United States has softened. August’s Consumer Price Index (CPI) was reported at 0.3%, below consensus estimates of 0.4%, down from July’s 0.5% print, and the lowest reading since January. Annualized inflation was reported at 5.3% in line with consensus, down from prior 5.4% and the lowest since May. Core inflation was reported at 0.1%, below consensus estimates of 0.3%, down from July’s 0.3%, and the smallest increase since February. Some economists believe that inflation has already passed its peak.

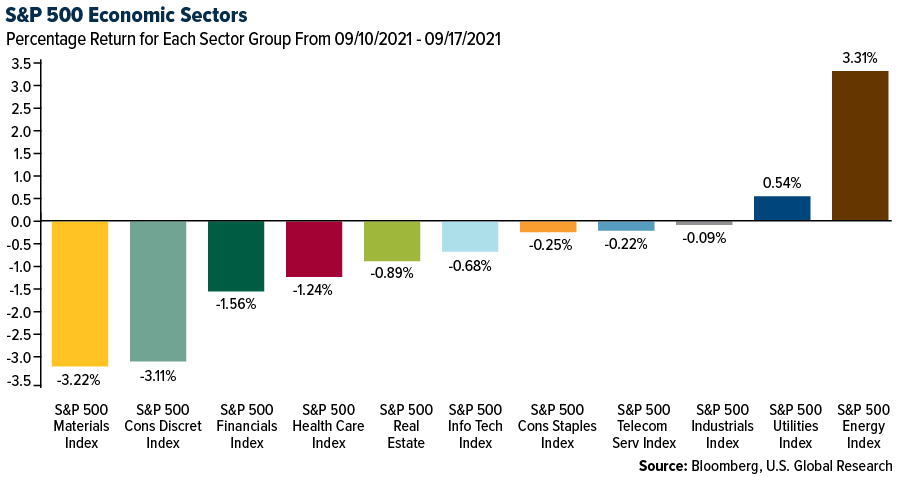

- EOG Resources was the best performing S&P 500 stock for the week, increasing 10.6%. Higher oil price is driving oil equities higher. Brent crude futures closed above $75 per barrel for the first time since August 2 after a U.S. government report showed a bigger-than-expected decline in crude stockpiles.

Weaknesses

- The National Federation of Independent Business (NFIB) Small Business Optimism Index increased slightly in August to 100.1, but 50% of small business owners still have job openings they cannot fill. “As the economy moves into the fourth quarter, small business owners are losing confidence in the strength of future business conditions,” said NFIB Chief Economist Bill Dunkelberg. “The biggest problems facing small employers right now is finding enough labor to meet their demand and for many, managing supply chain disruptions.”

- Industrial production slowed to a 0.4% gain in August from a revised 0.8% in July. Plant closures along the Gulf Coast, as well as lost oil production during last month’s hurricane, shaved 0.3 percentage points from output, the Federal Reserve reported Wednesday.

- Wynn Resorts was the worst performing S&P 500 stock for the week, losing 17.97%. Stocks exposure to Macau sold off sharply this week on fears the government could introduce tighter gambling regulations.

Opportunities

- The Preliminary September Manufacturing Purchasing Managers’ Index (PMI) will be released next week and, most likely, the reading will remain well above the 50 level that separates growth from contraction. The Service PMI should remain strong too, due to increased travel and economic activity following the end of the summer months.

- Initial jobless claims will possibly decline next week. This week the jobless claims rose slightly to 332,000 from 310,000 in August. Louisiana noted the biggest spike in claims led by the labor market disruption due to Hurricane Ida’s impact, as petrochemical plants and refineries remained closed in the aftermath of the hurricane.

- According to FactSet, earnings revision momentum is stalling, but earnings estimates for the third quarter are still up considerably. The bottom-up S&P 500 earnings per share estimate for the third quarter has increased 3.7% over the course of the quarter. This compares to the five-year average decline of 2.9%. In addition, S&P 500 earnings are expected to increase about 28% year-over-year in the third quarter, more than 20% in the fourth quarter and more than 40% for 2021 overall.

Threats

- The Federal Reserve Bank will meet next week, and policymakers may discuss tapering. The central bank will eventually start withdrawing some of its stimulatory monetary policies, but the big unknown that remains is timing.

- Bloomberg economists predict the Leading Index to increase by 0.5% in August, lower than the 0.9% in July. The Conference Board Leading Economic Index is based on 10 components, among them initial claims for unemployment insurance, manufacturers’ new orders, building permits of new private housing units, stock prices and consumers’ expectations. It is intended to signal swings in the business cycle and to smooth out some of the volatility of individual indicators and is intended to forecast future economic activity.

- U.S. House of Representatives on Monday proposed a substantial roll-back of former President Donald Trump’s tax cuts, including raising the top tax rate on major corporations to 26.5% from the current 21%. Besides increasing corporate taxes, the super-wealthy are likely to see a jump in their income taxes as well as higher capital gains and estate taxes.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Xenon Pay, gaining over 278,000,000%.

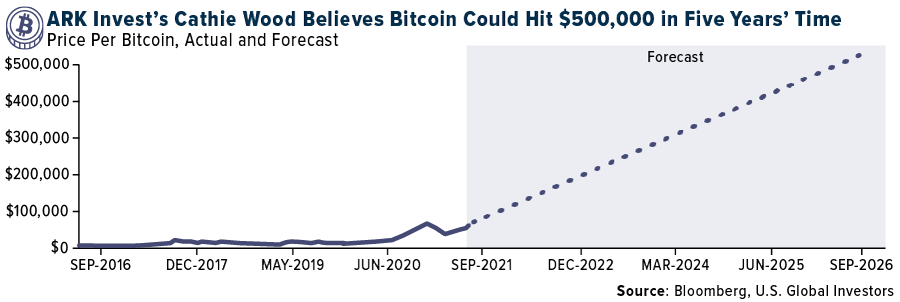

- Seeking fresh ways to bet on digital assets, Cathie Wood’s Ark Investment Management is allowing one of its funds to invest in Canadian Bitcoin ETFs, reports Bloomberg. In a late-Friday filing for the $5.7 billion ARK Next Generation Internet Fund, the firm adjusted its prospectus to include reference to holding exposure to cryptocurrencies. In addition, Wood commented this week at the SALT conference in New York that she believes Bitcoin’s price could rise tenfold to top $500,000 in the next five years, reports Bloomberg.

- Bitcoin has now traded above $10,000 an entire year, reports CoinTelegraph. On September 9, 2020, Bitcoin had slowly edged into the $10k zone and hasn’t returned since in over a year. In fact, by the fourth quarter of 2020, Bitcoin was trading at $28,000 – a 180% increase in value. Many cryptocurrency enthusiasts expect Bitcoin to repeat itself again this year with a 180% increase to $135,000 by the start of 2022.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Channels, down 99.74%.

- According to a central bank official, the Republic of Uzbekistan will never adopt cryptocurrencies like Bitcoin as a payment method, writes CoinTelegraph, alleging that Bitcoin is backed by nothing. Behzod Khamraev, deputy chairman of the Central Bank of Uzbekistan, pointed out that there are about 28 trillion Uzbekistani soms in circulation, and all of those are backed by the central bank’s assets. Uzbekistan officially banned its residents from making payments in cryptocurrencies in late 2019.

- Authorities in the Chinese province of Hebei have reportedly launched a campaign against cryptocurrency mining and trading. According to a quoted announcement by the region’s cyberspace administration, several government agencies are working together to prevent the use of the region’s computing power in the crypto activities which the government considers illegal, reports Bitcoin.com on Thursday. Government agencies and state-run companies in the province which surrounds Beijing have been asked to inspect their information systems and put an end to any use of their computing power to mint digital coins by the end of September, as stated in the South China Morning Post (SCMP).

Opportunities

- Coinbase Global Inc. sought to raise $1.5 billion in its first junk-bond offering at the start of the week, reports Bloomberg, a deal that provides another stamp of approval for cryptocurrency and a sign that the nine-year-old firm is gaining mainstream acceptance (even as regulators ramp up scrutiny). The firm saw such high demand it boosted the original deal size to $2 billion. On Thursday, Bloomberg reported that the junk bonds declined, as new bonds fell for the second day since pricing at par on Tuesday.

- Interactive Brokers Group reported that it launched low-fee cryptocurrency trading on its platform, adding to the growing online retail brokerages to add digital assets to its offerings, reports Yahoo! Finance this past Monday. “As financial markets evolve, sophisticated individual and institutional investors are increasingly seeking out allocations to digital currencies as a means of achieving their financial objectives,” said CEO Milan Galik. Interactive Brokers is partnering with Paxos Trust Company to enable the new service.

- In a private meeting with the U.S. SEC, Fidelity Investments urged the regulatory body to approve its Bitcoin exchange-traded fund (ETF), reports Bloomberg, listing the virtues of an idea that the regulator has been slow to embrace. Filings show that executives from Fidelity laid out reasons why the regulator should approve the product, including increased investor appetite for virtual currencies, the growth of Bitcoin holders and the existence of similar funds in other countries.

Threats

- Litecoin gave up a 20% gain and tumbled back following a fake press release sent out by GlobeNewswire at the start of the week, referencing a partnership with Walmart, reports CNBC. GlobeNewswire said that a fraudulent user account was used to issue the release, and then a social media coordinator from Litecoin mistakenly tweeted it from the company’s official account.

- Protests in El Salvador happened this Wednesday over the adoption of Bitcoin as legal tender and recent moves by El Salvadorian President Nayib Bukele to consolidate power, reports Bloomberg. Although the demonstrations were largely peaceful, one group of protesters smashed windows and set fire to a Bitcoin ATM kiosk installed last month ahead of the cryptocurrency’s rollout as legal tender. Along with Bitcoin’s adoption last week, the government has proposed more than 200 changes to the constitution including eliminating a ban on presidential re-election.

- In a statement spoken at the SALT Conference on Wednesday, billionaire Ray Dalio said regulators will try to ‘kill’ Bitcoin if it gains mainstream success. In an article by Yahoo! Finance, Hollerith reports that Dalio believes Bitcoin is a “viable asset class” and “interesting” for diversifying a portfolio. However, if Bitcoin becomes too successful, then regulators will likely ban it.

Gold Market

This week spot gold closed at $1,754.34, down $33.24 per ounce, or 1.86%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.15%. The S&P/TSX Venture Index came in off 1.83%. The U.S. Trade-Weighted Dollar rose 0.71%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-14 | CPI YoY | 5.3% | 5.3% | 5.4% |

| Sep-14 | China Retail Sales YoY | 7.0% | 2.5% | 8.5% |

| Sep-16 | Initial Jobless Cliams | 322k | 332k | 312k |

| Sep-17 | Eurozone CPI Core YoY | 1.6% | 1.6% | 1.6% |

| Sep-21 | Housing Starts | 1,550k | — | 1,534k |

| Sep-22 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Sep-23 | Initial Jobless Claims | 320k | — | 332k |

| Sep-24 | New Homes Sales | 709k | — | 708k |

Strengths

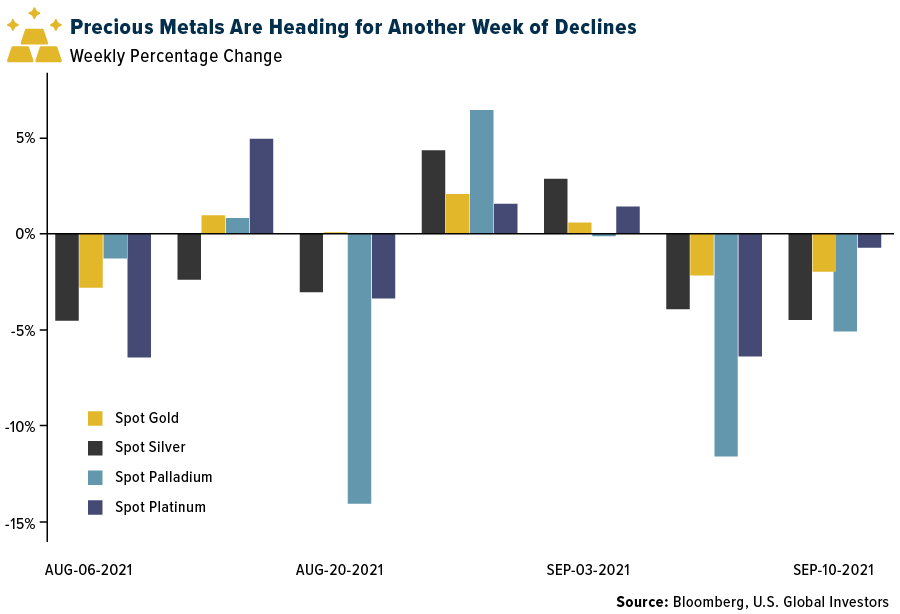

- The best performing precious metal for the week was gold, but still off 1.86%. Sibanye Stillwater, which has transformed itself from a South African gold miner to a platinum-group metals giant, branched out its reach this week to enter into a joint venture to develop the Rhyolite Ridge lithium-boron project in Nevada and have additional exposure to battery metals. Earlier this year, Sibanye bought a stake in a nickel hydrometallurgical processing facility in France.

- Franco-Nevada CEO Paul Brink reiterated that the company expects to grow production from 600,000 gold equivalent ounces (GEO) in 2021 to 650,000 GEO in 2025, with the biggest driver being Cobre Panama, expanding to 100 million tonnes per year in 2023. The company is currently growing its cash balance $1 billion each year.

- Endeavour Mining CEO Sebastien de Montessus said the company is on track to achieve the top end of 2021 guidance (1,365-1,495 thousand ounces), with production benefiting from higher grades at Hounde (Kari Pump) and a late start to the rainy season.

Weaknesses

- The worst performing precious metal for the week was silver, down by 5.72%. Silver fell to its lowest level since December as stronger than expected retail sales across almost all categories more than offset the weaker automobile sales. Last week, ETFs reduced their silver holdings by 1.4 million troy ounces, platinum holdings by 35,666 troy ounces and palladium holdings by 15,297 troy ounces.

- Platinum and its sister metals palladium and rhodium — used in pollution-cutting catalytic converters — have all suffered sharp drops in recent weeks as carmakers shutter plants and trim output guidance. The price slump is a big contrast with the booming performance earlier in the pandemic, which was driven by supply shortages and hopes of a stimulus-led economic recovery. Rhodium, the most expensive precious metal, has suffered the most as its demand comes almost entirely from the auto sector. Palladium isn’t far behind, having this week dropped through $2,000 an ounce for the first time since July 2020.

- New Gold provided an update at its Rainy River mine in Ontario, Canada. Gold production at Rainy River is now expected to be between 235,000 and 250,000 ounces, reflecting the impact of prior disclosed negative grade reconciliation. National Bank Financial lowered its price target form C$2.50 to C$2.00 on the update.

Opportunities

- OceanaGold’s Didipio restart is progressing ahead of plan, with inventory sales of approximately 40% for $25 million and 65% of the workforce expected to be rehired by end of the third quarter. The company expects the asset to be fully ramped within 10 months.

- AngloGold announced that it has entered a definitive agreement to acquire Corvus Gold following the proposal announced on July 13. Under the agreement, AngloGold will pay C$4.10 per share in cash for the 80.5% of the shares it does not already own in a deal worth $370 million. The offer price is at a 59% premium to the share price on 5 May 2021, the day before AngloGold entered a $20 million unsecured loan facility and a 90-day exclusivity period.

- Americas Gold and Silver announced work had restarted at the Cosalá operation in Mexico, and the company expects to start shipping concentrate before the end of October after the 20-month blockade was lifted. Cosalá is a significant component of its valuation, so if the company can deliver on the plan, the market would likely rerate the stock higher.

Threats

- Centerra CEO Scott Perry reiterated the company’s revised 2021 guidance of 290,000 ounces, following derecognition of Kumtor. The company remains open to discussions with the Kyrgyz government (potentially taking back the government’s stake in Centerra and subsequently canceling those shares) but is also considering all legal options.

- Newmont CEO Tom Palmer noted that the Yanacocha Sulfides full funds decision has been deferred to late 2022 from late 2021 due to ongoing COVID-19 related issues in Peru (including low vaccination rates). In a Bloomberg interview this week, the CEO noted that labor tightness, higher energy prices and higher materials prices are pushing the company’s overall costs up by 5%.

- Gold fell, pressured by rising Treasury yields as lower-than-expected U.S. inflation data eased concerns over the Federal Reserve starting to reduce stimulus. The yield on the 10-year Treasury rebounded after dipping to a three-week low, reducing demand for bullion that generates no interest. The U.S. consumer price index (CPI) rose 0.3% in August from July, the smallest gain in seven months, data released Tuesday showed. The inflation print Tuesday offered some validation of the view held by Fed Chair Jerome Powell that high inflation caused by the economy reopening was transitory, alleviating worries that the central bank will be forced to soon tighten policy.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Delta Air Lines

American Airlines

Ryanair Holdings

easyJet PLC

Azul SA

Wizz Air Holdings

Spirit Airlines Inc.

Allegiant Travel Co.

Southwest Airlines Co.

Alaska Air Group Inc.

easyJet PLC

Hawaiian Holdings Inc.

United Airlines Holdings Inc.

Sibanye Stillwater

Franco-Nevada

Endeavor Mining

OceanaGold Corp.

AngloGold Ashanti

Corvus Gold Inc.

Centerra Gold

Newmont Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Empire State Manufacturing Index rates the relative level of general business conditions New York state. A level above 0.0 indicates improving conditions, below indicates worsening conditions. The reading is compiled from a survey of about 200 manufacturers in New York state. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The National Federation of Independent Business (NFIB) Small Business Optimism Index is a composite of ten seasonally adjusted components. It provides a indication of the health of small businesses in the U.S., which account of roughly 50% of the nation’s private workforce.