Getting In on the Ground Floor With World-Class Companies

Date Posted: March 1, 2019

Read time: 53 min

This week I had the privilege of attending BMO's 28th Annual Global Metals & Mining Conference in Hollywood, Florida, along with portfolio manager and precious metals expert Ralph Aldis.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

This week I had the privilege of attending BMO’s 28th Annual Global Metals & Mining Conference in Hollywood, Florida, along with portfolio manager and precious metals expert Ralph Aldis. The BMO conference is an epic event that brings together the “who’s who” of mining and natural resources—think Pierre Lassonde, Robert Friedland, Marin Katusa and many, many more.

Sentiment was cautiously bullish on gold and precious metals, while mega-mergers and takeovers were top of mind for many attendees and presenters. I’m not exaggerating when I say that the news of Barrick Gold’s bid for rival Newmont Mining dominated the buzz. In case you’re not aware, Barrick is currently seeking to persuade shareholders to support its $18 billion hostile takeover of the Colorado-based miner.

|

|

This latest round of industry consolidation follows the Barrick-Randgold Resources merger, announced back in September, as well as Newmont’s own deal with Goldcorp in January. If Barrick is successful in its bid, however, Newmont must break off the $10 billion deal with Goldcorp.

Even before all of this began, Barrick was the world’s largest gold producer, with a market cap of nearly $21 billion. If it manages to acquire Newmont, it would become an untouchable behemoth.

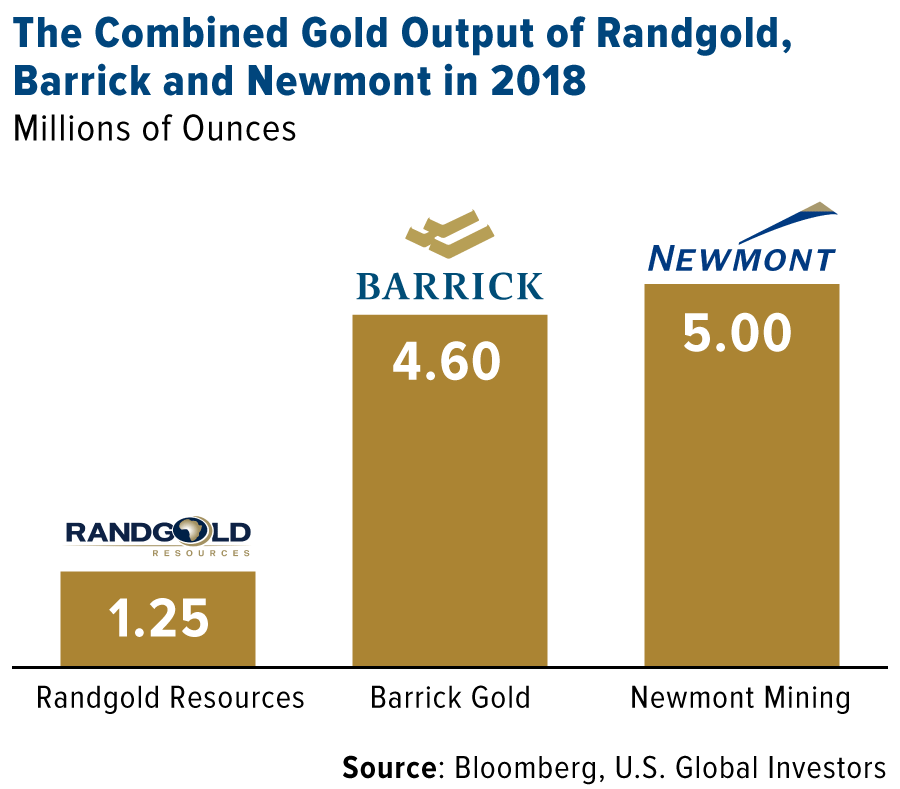

Here’s an illustration of just how big the resultant company would be: World gold output stood at 158 million ounces last year, and of that, Barrick, Randgold and Newmont produced a combined 10.85 million ounces. Those three companies alone, then, were responsible for one out of every 14 ounces or so worldwide.

I have so much more to say on this, but for now, I invite you to watch my interview with Kitco News’ Daniela Cambone, direct from the BMO conference. Click here to see it!

A Record of Early-Stage Investing

The metals and mining industry could be undergoing some dramatic changes in the near future. It’s important for investors to get in on the ground floor when this happens.

Back in 2017, we were seed investors in HIVE Blockchain Technologies, the world’s first publicly traded cryptocurrency mining firm. We also recognized the value of the disruptive jewelry manufacturer Mene, and were able to make a private investment months before it was listed on the TSX Venture Exchange. More recently, I introduced you to GoldSpot Discoveries, the very first company to harness the power of artificial intelligence (AI) in the mineral exploration process. We made a sizeable allocation in the company, and I was named chairman of the board.

We’re not new to any of this, of course. I’m proud of our track record of getting in early with a number of now-phenomenally successful companies. We were among the original financers of American Barrick Resources, before it changed its name to Barrick Gold in 1995. Ditto for Wheaton River Minerals, now known as Wheaton Precious Metals—one of our favorite royalty and streaming companies.

This is just one among many reasons why I believe active management still plays an essential role in investors’ portfolios. It also brings to mind the concept of “synchronicity.”

Be Mindful of Meaningful Connections

The word “synchronicity” was first coined by the Swiss psychoanalyst Carl Jung, a disciple of Sigmund Freud. It says that events are meaningful coincidences if they occur with no causal connection yet seem to be meaningfully related.

Jung conceived of synchronicity after he observed a curious incident. A client described to him a dream she had the previous night of a golden scarab—a very expensive piece of jewelry. The very next day, while meeting with the same client, an insect struck his office window. Upon closer inspection, Jung saw that it was a scarab beetle, which closely resembled the piece of jewelry from his client’s dream. The insect is very rare in Jung’s native Switzerland. “Here is your scarab,” he reportedly told her.

|

|

| Photo by: Chrumps, CC BY-SA 3.0 |

The two events—the dream and the insect encounter—cannot reasonably be called causally connected. But they’re meaningfully related.

Synchronicity was one of many topics we discussed this year at Harvard Business School, where I go every year along with as many as 150 CEOs from dozens of different countries.

The theme really rang true for me and many of my fellow CEOs. Many of us believe that luck, ambition and positive thinking all play a role in our lives and business decisions, and have helped us get where we are today.

I feel grateful and blessed every day that I’m in a position to find solutions, to stay curious to learn and improve and to find opportunities—opportunities such as HIVE, Mene, GoldSpot and many more.

I wish you all a joyful weekend!

Gold Market

This week spot gold closed at $1,293.40, down $34.85 per ounce, or 2.62 percent, likely on Venezuelan gold sales. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.44 percent. The S&P/TSX Venture Index came in slightly higher by 0.30 percent. The U.S. Trade-Weighted Dollar fell 0.05 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-26 | Hong Kong Exports YoY | -2.8% | -0.4% | -5.8% |

| Feb-26 | Housing Starts | 1256k | 1078k | 1214k |

| Feb-26 | Conf. Board Consumer Confidence | 124.9 | 131.4 | 121.7 |

| Feb-27 | Durable Goods Orders | — | 1.2% | 1.2% |

| Feb-28 | Germany CPI YoY | 1.5% | 1.6% | 1.4% |

| Feb-28 | Initial Jobless Claims | 220k | 225k | 217k |

| Feb-28 | GDP Annualized QoQ | 2.2% | 2.6% | 3.4% |

| Feb-28 | Caixin China PMI Mfg | 48.5 | 49.9 | 48.3 |

| Mar-1 | Eurozone CPI Core YoY | 1.1% | 1.0% | 1.1% |

| Mar-1 | ISM Manufacturing | 55.8 | 54.2 | 56.6 |

| Mar-5 | New Home Sales | 583k | — | 657k |

| Mar-6 | ADP Employment Change | 190k | — | 213k |

| Mar-7 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Mar-7 | Initial Jobless Claims | 225k | — | 225k |

| Mar-8 | Housing Starts | 1170k | — | 1178k |

| Mar-8 | Change in Nonfarm Payrolls | 188k | — | 304k |

Strengths

- The best performing metal this week was palladium, up 2.81 percent with continued price strength. Gold traders were split between bullish, bearish and neutral on the yellow metal this week as prices struggled to recover and posted a monthly loss for February. Lawmakers in Romania are drafting legislation aiming to repatriate the country’s gold stored in the United Kingdom. The bill is to amend a Romanian central bank law that allows only 5 percent of its gold reserves abroad. This is a positive signal of countries wanting to hold their gold domestically. Palladium saw a seventh monthly gain in February and is up an amazing 83 percent since mid-August. The precious metal has been rallying due to a supply shortage as car manufacturers increasingly need palladium to meet emission standards.

- Another precious metal getting attention as of late? Platinum. In the month of February, platinum saw the biggest inflows into ETFs in almost six years. The palladium rally has helped renew investor interest in its sister metal. Impala Platinum Holdings, the world’s second largest platinum miner, made a significant reduction in its debt and share prices rose more than 9 percent on Thursday to the highest since October 2016.

- Kitco News reports that the drama between the world’s two largest mining companies intensified this week. Newmont Mining rejected an all-stock merger proposed by Barrick Gold. Newmont released a statement saying that it prefers to move forward with its acquisition of Goldcorp, with that new company surpassing Barrick to become the world’s largest miner.

Weaknesses

- The worst performing metal this week was silver, down 4.74 percent on hedge funds cutting their net long position by about 10 percent this past week. American Eagle gold coin sales fell 81 percent in February to just 12,500 ounces after posting a two-year high in January, according to U.S. Mint data. This comes as spot gold prices hit their highest level since April on February 20, and then slid to post the first monthly loss in five, writes Bloomberg. The London Bullion Market Association reported that gold trading in January declined to an average 19.6 million ounces per day, a 17 percent drop from the previous month. Gold suffered a narrow loss in February after four straight months of gains. Michael McCarthy, chief market strategist at CMC Markets, said that the “U.S. dollar strength is a key danger for gold, and the technical picture for gold has deteriorated with the failure around $1,340.”

- Turkey continues to sell its gold reserves. Central bank data from Ankara shows that reserves fell 4.5 tons month-over-month in January to 440.8 tons. At least eight tons of gold were removed from Venezuela’s central bank last week, according to unidentified government sources who did not say where the gold was going to. In 2018, 23 tons of Venezuelan gold was transported to Istanbul, and some speculate that is the same place this going is going to as well.

- Centamin Plc, an Egyptian gold miner, saw its shares fall as much as 22 percent on Monday after forecasting production estimates below analyst expectations. The company forecast production from 490,000 to 520,000 ounces in 2019, which is less than the amount mined in 2017.

Opportunities

- According to Australia & New Zealand Banking Group Ltd, palladium consumption by the auto sector will grow 1.1 percent in 2019 due to stricter environmental laws requiring more usage of the metal. This comes despite the recent contraction in car sales in both Europe and China. Strategists Daniel Hynes and Soni Kumari wrote in a report that “with emission regulations getting tighter across major countries, we see higher loadings requirements offsetting a slowdown in the auto sector’s palladium demand.” Bloomberg reports that Impala Platinum Holdings plans to start building a new palladium mine that could begin producing as early as 2024. The miner plans to start work on the Waterberg project in South Africa in 2021, says CEO Nico Muller. Anglo American Platinum Ltd, the world’s top platinum miner, is looking at plans to boost its palladium output through the expansion of one of its current mines.

- JPMorgan is bullish on gold as a hedge against rising inflation. Strategists led by John Normand wrote in a note last week that “TIPS and gold seem like the most durable inflation hedges for a unique macro environment when the Fed’s reaction function isn’t the only regime change impacting real assets.” Bloomberg’s Joanna Ossinger writes that “the Fed appears to be considering trying to let inflation run hotter than its 2 percent target to make up for years below that level.”

- Heraeus wrote this week the geopolitical risks should keep central banks buying gold. IMF data shows that at the end of 2018 central bank gold reserves reached their highest level since 1997 at 33,800 tons. The company writes that current geopolitical risks and growing concern about the U.S. dollar should drive more purchases of gold as a hedge against instability and a way to diversify.

Threats

- In regards to Barrick’s attempt to takeover Newmont, Doug Groh, a portfolio manager at Tocqueville Asset Management had some harsh words. “It seems arrogant on Barrick’s behalf to assume shareholders will believe in the value creation of the merged Barrick-Newmont entity as the offset to a premium that’s not paid in the marketplace directly in the bid. It’s cheeky on their part to assume shareholders are so naïve as to assume premium value will come through their execution.” According to Bloomberg Intelligence analyst Andrew Cosgrove, the top 20 holders in Barrick, who own 55 percent of total shares outstanding, also own 91 percent of Newmont’s shares. This fact makes it clear that Barrick’s management may have a hard time fighting against shareholders if they support Newmont and demand a higher premium. Another potential issue regarding this potential merger? Review by the Federal Trade Commission and Department of Justice about it possibly substantially lessening competition in the gold mining space in the United States. Would America want its largest domestically based gold company to be taken over by foreign hands? Barrick would dominate Nevada, potentially stifling competition in the nation’s biggest gold mining state.

- Goldcorp could be left at the altar, so to speak, if Newmont merges with Barrick. Under that proposed merger, Newmont would need to abandon its already planned acquisition of Goldcorp. Additionally, Barrick would need to sell several small Australian miners as a part of the deal. But would anyone be there to buy them? Or will the other miners allow Barrick to struggle to rationalize its assets instead of helping it turn noncore assets into cash?

- The Environmental Project Agency (EPA) is facing negligence claims after workers triggered the release of millions of gallons of mining wastewater and toxic sediment into the Animas River in New Mexico. The 2015 Gold King Mine spill occurred when the EPA accidentally opened a passage leading into the mine when trying to identify actions needed to address contamination flowing from the site, writes Bloomberg. The government isn’t required to clean up their spill.

February 25, 2019AI Will Add $15 Trillion to the World Economy by 2030 |

February 21, 2019Would You Do This to Pay Zero Income Taxes for Life? |

February 19, 2019Will 2019 Be the Year of King Copper? |

|||

Index Summarys

- The major market indices finished mix this week. The Dow Jones Industrial Average lost 0.02 percent. The S&P 500 Stock Index rose 0.39 percent, while the Nasdaq Composite climbed 0.90 percent. The Russell 2000 small capitalization index lost 0.03 percent this week.

- The Hang Seng Composite rose 0.06 percent this week; while Taiwan was 0.64 percent and the KOSPI 0.19 percent.

- The 10-year Treasury bond yield rose 10 basis points to 2.76 percent.

Domestic Equity Market

Strengths

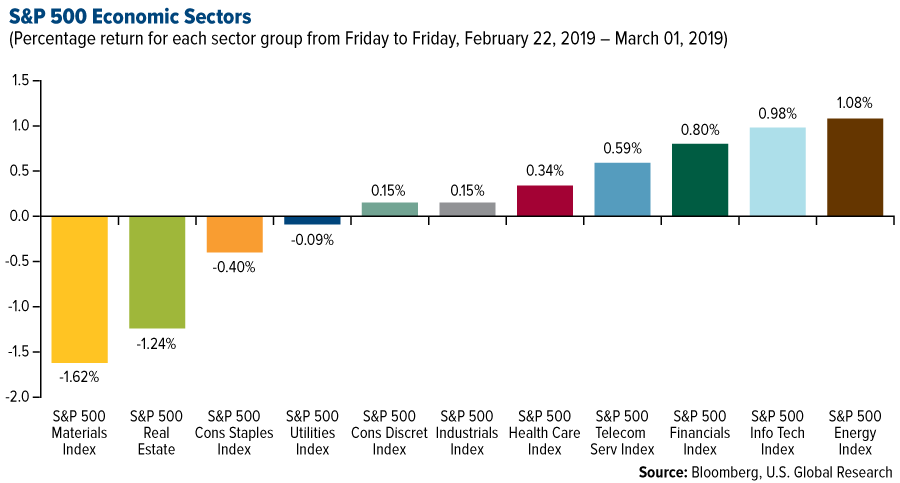

- Energy was the best performing sector of the week, increasing by 1.08 percent versus an overall increase of 0.41 percent for the S&P 500.

- Gap was the best performing stock for the week, increasing 19.18 percent.

- Roche announced this week that it is buying Spark Therapeutics for $4.3 billion. The deal will pay Spark shareholders $114.50 a share, which is a 122 percent premium to the closing price last Friday.

Weaknesses

- Materials was the worst performing sector for the week, increasing by 1.62 percent versus an overall increase of 0.41 percent for the S&P 500.

- HP Inc. was the worst performing stock for the week, falling 17.44 percent.

- Weight Watchers plummeted this week following the release of its earnings guidance coming in well short of expectations, reports Business Insider. Shares of the diet program provider fell 30 percent Tuesday after the company said it saw full-year earnings of $1.25 to $1.50 a share, well shy of the $3.36 that analysts surveyed by Bloomberg were expecting.

Opportunities

- U.S. companies are finally listening to stock and bond investors that have been pressing corporations to cut their debt loads, writes Bloomberg News’ Molly Smith. “General Electric is selling its biopharmaceutical business to Danaher for more than $21 billion, and using the money to pay down borrowings. Kraft Heinz said last week it was slashing its dividend and using the proceeds of asset sales to reduce its liabilities,” the article reads.

- Gap is spinning off Old Navy into a separate public company, the mall store operator announced this week. Gap’s shares soared 20 percent late Thursday after the struggling retailer said it was making the transaction, which should be complete in 2020.

- Martha Stewart is taking an advisory role in a cannabis company, reports Yahoo! Finance. Stewart and the Canadian cannabis producer Canopy Growth Corporation are teaming up to develop a new line of product offerings for CBD and other cannabinoid uses for both humans and animals.

Threats

- Many American companies are increasingly pessimistic on China due to the trade war, according to one Bloomberg headline this week. Outlooks have shifted from “cautious pessimism” to “cautious optimism,” according to the latest survey conducted by the American Chamber of Commerce. Despite firms seeing the Chinese market as a high priority still, the article continues, nearly three-quarters expect China-U.S. relations to deteriorate or stay the same, at best, in 2019.

- More than three-quarters of business economists expect the U.S. to enter a recession by the end of 2021, according to Bloomberg. According to a semiannual National Association for Business Economics survey released Monday, the numbers are as follows: 10 percent saw a recession beginning this year, 42 percent project one next year, while 25 percent expect a contraction starting in 2021.

- Elon Musk warned that Tesla won’t be profitable in the first quarter, writes CNBC. "We do not expect to be profitable in Q1, but profitability in Q2 is likely," Musk said Thursday.

The Economy and Bond Market

Strengths

- The U.S. economy grew faster than expected in the fourth quarter as business investment picked up, suggesting growth could be stronger for longer. Gross domestic product (GDP) expanded at an annualized pace of 2.6 percent for the period October to December, Commerce Department data showed Thursday, more than the 2.2 percent median estimate in a Bloomberg survey.

- Consumer confidence surged in February after the government reopened. The rise in sentiment should assuage fears that consumer spending is poised for a sharp slowdown in the first quarter. The current conditions index also moved higher, signaling that the strong labor market and increasing pace of wage gains has consumers feeling optimistic.

- New orders for manufactured durable goods increased 1.2 percent in December to $254.4 billion, following a 1.0 percent November rise, according to the U.S. Census Bureau. Transportation equipment drove the increase, growing 3.3 percent to $90.2 billion over the month. December’s pace was the fastest since June.

Weaknesses

- Consumer spending, which accounts for more than two-thirds of U.S. economic activity, dropped 0.5 percent in December. That was the biggest decline since September 2009.

- Home prices in 20 cities rose in December at the slowest pace in four years, continuing to decelerate as buyers balked at purchases amid still-elevated housing costs. The S&P CoreLogic Case-Shiller Home Price Index of property values increased 4.2 percent from a year earlier, after a downwardly revised 4.6 percent in the prior month, below the median estimate of economists. Nationally, home prices climbed 4.7 percent, the least since 2015.

- More than a decade has passed since young Americans faced debt levels this high. Debt among 19 to 29-year-old Americans exceeded $1 trillion at the end of 2018, according to the New York Federal Reserve Consumer Credit Panel. That’s the highest debt exposure for the youngest adult group since late 2007.

Opportunities

- President Donald Trump said he’ll extend a deadline to raise tariffs on Chinese goods beyond this week, citing “substantial progress” in the latest round of talks that wrapped up yesterday in Washington. “The U.S. has made substantial progress in our trade talks with China on important structural issues including intellectual property protection, technology transfer, agriculture, services, currency, and many other issues,” Trump said on Twitter. “As a result of these very productive talks, I will be delaying the U.S. increase in tariffs now scheduled for March 1.”

- Investors can look to a tax-season strategy to pick up extra returns with variable-rate municipals, which are largely insulated from risk because they can be resold to banks at full face value. The securities have benefited from a seasonal quirk during the past two years: Because they’re easy to sell, investors frequently do so to cover their tax bills. As a result, yields tend to rise ahead of the April filing deadline. Floating-rate debt issued by state and local governments is yielding about 1.75 percent, according to the SIFMA Municipal Swap Index. That’s more than those on tax-exempt bonds maturing between one and five years.

- The volume of new municipal-bond sales in March will be slightly less than the amount of money investors will receive from interest payments and securities that are being paid off, Citigroup analysts said in a report. The bank forecasts $33.2b of debt sales, while $26.4b will mature or be paid off early. Investors will get another $8.5b from interest payments. That supply/demand balance should help keep a steady bid on the muni market.

Threats

- According to Bloomberg Economics, even a relatively swift resolution to the trade war may be too little too late to prevent a drop in global exports. World trade volumes fell in December, the first drop since the beginning of 2016. Even if tensions with China ease, uncertainty on auto tariffs adds new risks for Europe and Japan, Brexit threatens to disrupt U.K. and European trade flows, and the cloud of uncertainty on trade policy will be difficult to dispel.

- According to Bloomberg Economics, U.S. residential investment will likely continue to be among the weakest performers, falling by 5.6 percent in the fourth quarter after a 3.6 percent drop in the third quarters. This would cement a negative print in 2018 as a whole, the first such occurrence since 2010. Increases in mortgage rates saw affordability deteriorate and homes sales fall sharply. Single-family construction also declined, especially in the latter part of the year.

- According to Bloomberg Economics, U.S. business fixed investment might not meaningfully rebound from the tepid second quarter result of 2.5 percent as the data suggests prospects for early 2019 are not encouraging. Business investment surged early in 2018 following the 2017 tax overhaul, but sentiment deteriorated as increased trade, political and global uncertainties moderated investment.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was natural gas, which gained 4.82 percent on strong demand in the U.S. Northwest with a winter storm. Nickel is having its best start to the year since 2007 as it rallied toward a six-month high in London. Bloomberg reports that nickel is the best-performing base metal so far this year with a 24 percent gain. The metal has been boosted by a rebound in Chinese prices of stainless steel and London Metal Exchange inventories falling to their lowest since 2013.

- The U.S. imported the least amount of crude oil on a weekly basis in 23 years while Saudi Arabia and Venezuela cut their shipments to unusually low levels, writes Bloomberg’s Jessica Summers. Weekly imports fell to 5.92 million barrels per day, which is the lowest since 1996, while domestic crude production skyrocketed to 12.1 million barrels per day.

- Colombian oil is seeing a boost from sanctions on Venezuelan oil imports. The nation is experiencing a rebirth of oil activity, as it produced 898,965 barrels a day in January, the highest on record since May 2016. Executives at Ecopetrol SA, the nation’s state-controlled oil company, said that they are able to “reliably supply customers” as Venezuelan production continues to fall. Traditional buyers of Venezuelan crude have had to find alternatives, such as Valero Energy, which has bought Canadian crude to fill their gap.

Weaknesses

- The worst performing major commodity for the week was lumber, which fell 4.89 percent as housing growth slows. The Stoxx Europe 600 Basic Resources Index fell as much as 1.9 percent on Thursday after China’s manufacturing PMI contracted further to 49.2, versus expectations of a reading at 49.4. This has revived concerns about an economic slowdown in China, the world’s top user of metals.

- Cobalt prices are in freefall after surging last year on the news that the world would need more of the metal for use in lithium-ion batteries that power electric vehicles. The price surge resulted in oversupply of the metal from the Democratic Republic of Congo. Bloomberg writes that cobalt has fallen more than 60 percent from its peak in April 2018 to now sit around $15.88 a pound.

- According to data from the London Metal Exchange, on-warrant copper stockpiles rose 2.8 percent this week to 22,200 tons, snapping a six-day drop of inventories. Previously, a decline in inventories contributed to rising spot prices of the red metal, but three-month copper was little changed at $6,500 per ton to end the week.

Opportunities

- BHP Group made big changes to its executive leadership board this week. The world’s biggest mining company promoted three women to the executive leadership board, which will now include six men and five women – a gender balance that is unusual in the industry, writes Bloomberg. Shell is looking to expand its position in the Permian basin, which it says is currently “too thin.” Upstream Director Andy Brown said in an interview this week that the idea that there’s a looming oil-supply gap is “totally fictitious” and that Shell’s portfolio would remain profitable even if crude fell as low as $40 a barrel.>

- SQM CEO Ricardo Ramos said that global lithium demand may grow at least 20 percent this year, in a statement accompanying fourth quarter earnings for the Chilean-based chemicals company. SQM, the world’s biggest lithium producer, said that demand grew an estimated 25 percent last year, led by the electric vehicle market, which had market penetration levels of 2 percent in 2018.

- Scientists in Dubai are developing crops that can thrive in salty soils in an effort to increase food production, which the United Nations estimates must grow by 60 percent in the next 30 years. Researchers at the International Center for Biosaline Agriculture are trying to help farmers in the Middle East grow plants known as halophytes, which can flourish in salty and arid environments. The most well-known halophyte is quinoa, which can be used in salads, fodder and biofuels, reports Bloomberg.

Threats

- February temperatures in Europe were unseasonably warm – closer to what early April temperatures should be – which sent natural gas and electricity prices lower this week. Bloomberg Intelligence analyst Elchin Mammodov writes that “mild winter tends to hurt unregulated power generators and energy suppliers by curbing demand and wholesale prices.”

- Energy Secretary Rick Perry warned this week that the recently passed “No Oil Producing and Exporting Cartels Act” could have the unintended effect of raising energy prices. Perry said at a press conference that “I think we need to be really careful before we pass legislation that may have an impact that goes way past its intended consequences.” The legislation would authorize the Justice Department to pursue antitrust action against OPEC for manipulating oil prices, writes Bloomberg.

- Southern California Edison must charge customers an extra $815 million after failing to predict a West Coast heat wave that sent prices skyrocketing to a record in July. Additionally, when it snowed in Pasadena in early February, gas for delivery in Los Angeles traded at almost 10 times the U.S. benchmark. Bloomberg’s David Baker writes that “Southern California’s gas market has become so unpredictable that it’s starting to resemble trading in the Northeast, where pipeline bottlenecks can lead to the world’s highest prices when demand for the heating fuel surges during the winter.”

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 5.3 percent. Banks appreciated the most, supported by a change in the bankruptcy law. Piraeus Bank gained 54 percent and Eurobank’s shares appreciated by 20 percent.

- The Polish zloty was the best performing currency this week, gaining 1 percent against the U.S. dollar. Fiscal stimulus announced by the Polish government strengthened the country’s currency.

- Communication services was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 1.6 percent. Richter Gedeon, a pharmaceutical company, declined 5.7 percent, falling the most among stocks trading on the Budapest exchange. The company recently announced weaker fourth quarter results, due to additional impairment for Esmya, a fibroids treatment medication, after being denied approval by the FDA due to concerns over liver damage.

- The Turkish lira was the worst performing currency this week, losing 1 percent against the U.S. dollar. The currency weakened before Monday’s inflation reading and ahead of Wednesday’s central bank meeting. A majority of Bloomberg analysts expect year-over-year inflation to decline to 19.9 percent in February and rates to stay unchanged at 24 percent.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- The Greek government and four systemic banks came into a deal regarding the first-time residential mortgage loans that are under the protection of the ‘Katseli’ law (bankruptcy law). In order for the property to remain under the umbrella of the Katseli law (and avoid repossession by a bank), the outstanding balance of the loan cannot be in excess of EUR 130k, and the value of the asset has to be no more than EUR 250k. Minimum income criteria will also be considered under this new law. This change to the bankruptcy law will decrease the number of defaulters in the system and it will help banks reduce their non-performing loan portfolio.

- Poland’s ruling party announced generous stimulus measures ahead of the scheduled general elections in the fall. The amount to be spent is estimated at 40 billion zloty ($10.5 billion) on family subsidies and pension raises. In addition, income taxes will be cut for workers under 26, and extra money will be spent on transportation infrastructure. Additional social spending should strengthen consumer confidence and boost economic growth.

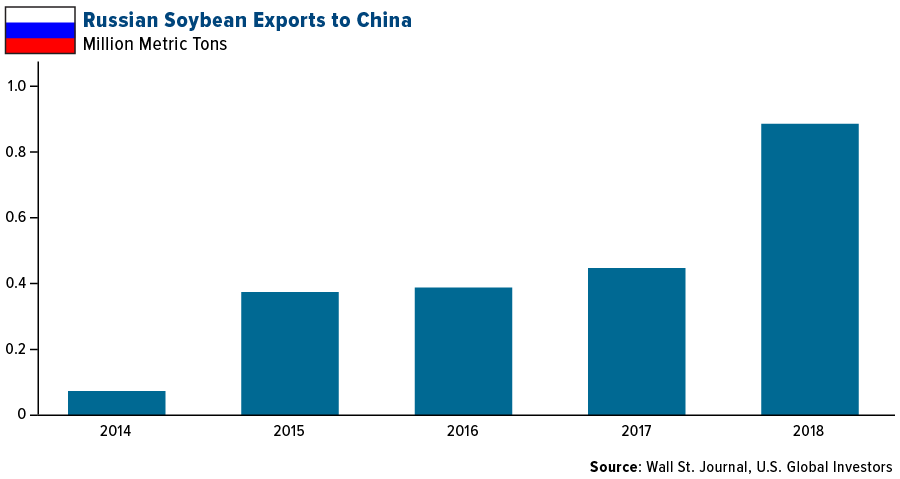

- According to a Wall Street Journal article dated February 21, “Surprise Winners in U.S. – Beijing Trade Spat: Russia Soy Farmers”, Trump’s trade conflict with China has nearly wiped out U.S. soy exports to the country, the bean’s biggest market. Russia has increased its soybeans exports, which have risen more than 10-fold in four years to nearly 1 million tons. There is still more room for Russia to grow its exports to China, according to Chinese government data that shows Russia’s soy exports only make up 1 percent of China’s 90 million-ton annual soy import market.

Threats

- The German current account surplus came in as the world’s largest for the third year in 2018 at $294 billion. Japan has the second largest surplus at $173 billion, and Russia secured third place with a trade surplus of $116 billion. In contrast, the U.S. had the world’s largest current deficit last year of $455 billion (and up $5 billion from the prior year). This data adds ammunition to President Trump’s trade discussion with the eurozone. His plan proposes increasing the tax on car imports from Europe to the U.S. to 25 percent.

- Europe will be watching developments in the U.K. in March, as the country is set to exit the European Union on March 29. On March 12, Theresa May will once again try to pass her Brexit deal through the parliament. If she fails to get support again, then the Brexit date can be extended, but it needs to be approved by all 27 eurozone member states. Regardless of the outcome, deal or no-deal, the world will be watching these political developments in the U.K. this month.

- TD Securities, the Toronto-based investment house, predicts another crisis in the Turkish lira, expecting a 40 percent drop against the U.S. dollar by the third quarter of this year. Crisitan Maggio, the head of emerging market strategy at TD, believes that the lira will be under pressure from a deepening economic contraction, high inflation, and current account deficit, along with a negative banking outlook. He predicts that the central bank will hike rates by 400 basis points between June and July to support the currency.

China Region

Strengths

- China’s Shanghai Stock Exchange Composite Index jumped another 6.77 percent for the week, extending recent gains amid more multi-month highs.

- Financials were the top-performing sector in Hong Kong’s Hang Seng Composite Index, climbing 1.77 percent on the week.

- The Caixin China Manufacturing PMI beat expectations, and, while still technically contractionary, clocked in at 49.9, ahead of analysts’ anticipated 48.5 print and up from the prior month’s 48.3 showing.

Weaknesses

- The Philippines’ PCOMP dropped by 4.02 percent on the week while Korea’s KOSPI, which did not trade this Friday, declined by 1.57 percent for the week.

- Information technology was the worst-performing sector in the HSCI for the week, declining by 1.74 percent.

- China’s Official Manufacturing PMI gauge clocked in at 49.2, short of expectations for a 49.5 print and below last month’s 49.5. The Official Non-Manufacturing PMI (still expansionary, well above 50) also missed, coming in at 54.3, below an anticipated 54.5 and down from the prior month’s 54.7.

Opportunities

- MSCI Inc. announced a decision to boost the weighting of China’s stocks in its widely-used global benchmark indices, which could bring further inflows into China’s domestic A-share market—potentially tens of billions of dollars—over the year. This marks the further internationalization of China’s economy and the renminbi.

- The United States and China continue their trade talks, even as tonight’s original 11:59 pm deadline has now been rolled back indefinitely for the course of what are deemed to be productive talks. The latest news, as of the end of this week and time of writing, is that the U.S. and China are nearing some broad agreements that may constitute something like a (reportedly) 150-page document with a potential formal signing ceremony possibly coming sometime as early as the middle of March. As usual, the situation remains fluid and headlines abound. Stay tuned, but there definitely appears to be an increasingly optimistic tone.

- In the background (literally) of the Trump-Kim summit this week, Vietnam demonstrated its rising potential and sizzling growth (fourth quarter GDP was over 7 percent) while it played host to the talks, held in Hanoi. And sure, while one can argue North Korea’s situation is different for a number of reasons and in a number of ways, or debate the legitimacy of any parallels, and so on, one can also just stop and marvel at Vietnam’s growth, unencumbered by any analysis whatsoever of North Korea. There you go. Bask in the growth. Now, if you want to go back to analysis of North Korea, go right ahead, but please, make sure to appreciate the host nation for the summit on its own terms, first.

Threats

- As usual with major and possibly binary events, the flipside of the deal/no-deal “coin” on China trade talk optimism is the possibility of a collapse in talks, reintroduction of tariff deadlines and escalation. Some of the issues at hand—intellectual property and technology transfers particularly come to mind—reportedly remain big sticking points with potentially longer-term (and, one imagines, implied geopolitical) effects. So the stakes remain high.

- This week’s summit between North Korea’s Kim Jong Un and U.S. President Donald Trump ended without any concrete progress or resolutions, although the talks reportedly ended amicably enough and with agreements to keep talking. While both the bar and expectations for concrete progress were admittedly low after the first summit and following White House hints, the two sides ended up far enough apart that President Trump apparently decided to call off the talks and nix the possibility of a deal at present. North Korea reportedly wanted sanctions lifted entirely; the President declined to acquiesce and walked away when North Korea would not agree to taking further and more comprehensive steps toward denuclearizing. While there are of course very obvious threats to a nuclear North Korea, and while there do not appear to be any imminent threats or announcements of a resumption of testing, etc., one potential side effect to a no-deal scenario may be felt at home by South Korea’s President Moon. Moon has staked quite a lot on making progress with North Korea, and, while there have indeed been some inroads, it remains possible that Mr. Moon may end up stymied on this front and suffer politically at home as ratings drop.

- Canada has now officially ordered the start of the extradition hearings against Huawei’s CFO Meng Wanzhou, Bloomberg News reported late on Friday, even as Huawei’s technology and reach is gaining share around the world as it looks increasingly at 5G.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 1 was SnapCoin, up 487.36 percent. In a New York Times op-ed, Venezuelan economist Carlos Hernandez writes that “bitcoin has saved my family.” Hernandez claims that, with annual inflation at 1.7 million percent and geopolitics in chaos, he owns no local currency and instead relies exclusively on bitcoin to buy milk and other essentials. The entire process of converting bitcoin into bolivars, he says, takes about 10 minutes. What’s more, cryptocurrencies helped his brother escape the beleaguered South American country last year. When his brother sends money home from abroad, he does so in bitcoin, which is “cheaper, faster and safer” than traditional money transfer methods.

- At the start of the week Coinbase announced its listing of XRP, the digital currency that runs on the Ripple protocol, reports MarketWatch. Despite little price reaction, market analysts have touted the news as a further step in the maturation of the opaque industry, the article continues.

- Switzerland-based Pangea Blockchain Fund launched its blockchain fund this week after securing $22 million in seed money, key investors of which include Bitcoin.com CEO Roger Ver. “Our team’s investment thesis is based on the profoundly important reality that blockchain will fundamentally alter the way society collaborates, transacts, governs and brings new concepts to life,” said Blockchain Investment Advisory Sagl co-founder James Duplessie.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 1 was AiLink Token, down 63.93 percent.

- Warren Buffett still isn’t impressed by bitcoin, reports MarketWatch. In an interview with CNBC on Monday, and on the heels of his annual letter to clients, Buffett commented that bitcoin has no unique value at all, even referring to the digital currency as a “delusion.”

- A New York man was charged this week with cheating investors out of millions of dollars by selling fake cryptocurrencies he falsely claimed were backed by gold. Between 2014 and 2017, Randall Crater, founder of Las Vegas-headquartered My Big Coin Pay, allegedly told investors that “My Big Coins” could be exchanged for paper currency when in fact they had no actual value. The incident could rattle some investors’ confidence in the credibility of the crypto market.

Opportunities

- At this week’s Mobile World Congress in Barcelona, Samsung announced that its new Galaxy S10 series smartphone will have wallet functions for Ethereum, bitcoin, the COSMEE token and Enjin’s coin (ENJ). It’s rumored that the Enjin wallet will come pre-installed on Samsung’s new phone, which is projected to be used by more than 31 million people. The price of ENJ surged as much as 130 percent for the day in response.

- Blockchain firm ThunderCore has raised $50 million to build what it predicts will be a “more nimble, cheaper and faster blockchain platform,” according to an interview with VentureBeat. ThunderCore CEO Chris Wang says that the project could lead to a “cheaper and faster version of bitcoin with smart contracts,” adding: “We can be 100 times faster than Ethereum and bitcoin.”

- According to new research by Global Market Insights, blockchain technology in the global health care market is poised to exceed $1.64 billion by 2025, as reported by MarketWatch. The report points out that growing occurrence of medical data breaches will likely result in greater adoption of blockchain technology in health care.

Threats

- The Ethereum network has a scaling issue, writes Martin Weiss of Weiss Ratings in a report for the U.S. Commodity Futures Trading Commission (CFTC). Running at full capacity, the network currently processes fewer than half a million transactions every day, meaning between 40,000 to 50,000 transactions are unable to “make it through traffic jams.” Meanwhile, Ethereum’s closest competitor, EOS, is able to process some 5.5 million transactions a day, or 11 times more. When the Ethereum network is running at full capacity, according to Weiss, “it tends to drive up fees,” which, in turn “can compound the problem by discouraging economic activity on the ledger, further reducing the volume of transactions.”

- A recent survey found that a significant percentage of investors in alternative assets believe cryptocurrencies are a bubble. During this week’s Cayman Alternative Investment Summit (CAIS), 45 percent of investors said digital currencies are a bubble, compared to U.S. equities (20 percent), the leveraged loan market (19 percent) and private credit (16 percent).

- Bitcoin’s rally for the month of February seems to be coming up short yet again, reports Bloomberg. At the start of the week the popular digital currency fell as much as 5.4 percent, after closing just shy of its $4,000 resistance level at the close of last week.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.85 | +0.13 | +4.71% |

| 10-Yr Treasury Bond | 2.76 | +0.11 | +4.11% |

| S&P Energy | 488.65 | +5.24 | +1.08% |

| Nasdaq | 7,595.35 | +67.81 | +0.90% |

| S&P 500 | 2,803.69 | +11.02 | +0.39% |

| S&P/TSX VENTURE COMP IDX | 625.16 | +1.89 | +0.30% |

| Korean KOSPI Index | 2,234.79 | +4.29 | +0.19% |

| Hang Seng Composite Index | 3,880.61 | +2.49 | +0.06% |

| DJIA | 26,026.32 | -5.49 | -0.02% |

| Russell 2000 | 1,589.63 | -0.43 | -0.03% |

| S&P Basic Materials | 343.50 | -5.67 | -1.62% |

| Oil Futures | 55.77 | -1.49 | -2.60% |

| Gold Futures | 1,292.50 | -40.30 | -3.02% |

| S&P/TSX Global Gold Index | 188.37 | -8.27 | -4.21% |

| XAU | 74.04 | -4.57 | -5.81% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Russell 2000 | 1,589.63 | +102.69 | +6.91% |

| Nasdaq | 7,595.35 | +412.27 | +5.74% |

| Hang Seng Composite Index | 3,880.61 | +207.56 | +5.65% |

| S&P 500 | 2,803.69 | +122.64 | +4.57% |

| S&P Energy | 488.65 | +21.16 | +4.53% |

| DJIA | 26,026.32 | +1,011.46 | +4.04% |

| 10-Yr Treasury Bond | 2.76 | +0.09 | +3.17% |

| Oil Futures | 55.77 | +1.54 | +2.84% |

| Korean KOSPI Index | 2,234.79 | +28.59 | +1.30% |

| S&P Basic Materials | 343.50 | +4.30 | +1.27% |

| S&P/TSX Global Gold Index | 188.37 | +0.27 | +0.14% |

| Natural Gas Futures | 2.85 | -0.01 | -0.32% |

| Gold Futures | 1,292.50 | -23.00 | -1.75% |

| S&P/TSX VENTURE COMP IDX | 625.16 | +9.96 | +1.62% |

| XAU | 74.04 | -0.49 | -0.66% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 188.37 | +23.09 | +13.97% |

| Hang Seng Composite Index | 3,880.61 | +320.29 | +9.00% |

| Oil Futures | 55.77 | +4.32 | +8.40% |

| Korean KOSPI Index | 2,234.79 | +120.69 | +5.71% |

| Gold Futures | 1,292.50 | +56.20 | +4.55% |

| Nasdaq | 7,595.35 | +322.27 | +4.43% |

| Russell 2000 | 1,589.63 | +64.24 | +4.21% |

| DJIA | 26,026.32 | +687.48 | +2.71% |

| S&P 500 | 2,803.69 | +65.93 | +2.41% |

| S&P Basic Materials | 343.50 | +3.84 | +1.13% |

| S&P Energy | 488.65 | +1.05 | +0.22% |

| 10-Yr Treasury Bond | 2.76 | -0.27 | -8.87% |

| Natural Gas Futures | 2.85 | -1.80 | -38.76% |

| S&P/TSX VENTURE COMP IDX | 625.16 | +34.04 | +5.76% |

| XAU | 74.04 | +9.24 | +14.26% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Piraeus Bank

Barrick Gold Corp

Newmont Mining Corp

Centamin Plc

Anglo American Platinum Ltd

BHP Group Ltd

Royal Dutch Shell Plc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P CoreLogic Case-Shiller U.S. National Home Price Index is a composite of single-family home price indices for the nine U.S. Census divisions.

The SIFMA Municipal Swap index is a 7-day high-grade market index comprised of tax-exempt VRDOs reset rates that are reported to the Municipal Securities Rule Making Board’s (MSRB’s) SHORT reporting system. The index is calculated on an actual/actual basis.

The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 17 countries of the European region. The STOXX Europe 600 basic resources index is a subset of the index, tracking companies in the resources sector.v

The Philippine Stock Exchange PSEi Index is a capitalization-weighted index composed of stocks representative of the Industrial, Properties, Services, Holding Firms, Financial and Mining & Oil Sectors of the PSE.