Global Debt, Trade Deficits and the Psychology of Politicians

Date Posted: September 6, 2019

Read time: 55 min

A couple of years ago, I shared with you an observation made by Ben Bernanke. This was at a SkyBridge Alternatives (SALT) hedge fund conference in Las Vegas. The former Federal Reserve chairman said that, in many unexpected ways, President Donald Trump's presidency so far resembles that of Jimmy Carter's.

Press Release: U.S. Global Investors Reports Financial Results for the 2019 Fiscal Year

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

A couple of years ago, I shared with you an observation made by Ben Bernanke. This was at a SkyBridge Alternatives (SALT) hedge fund conference in Las Vegas. The former Federal Reserve chairman said that, in many unexpected ways, President Donald Trump’s presidency so far resembles that of Jimmy Carter’s.

At first blush, Trump and Carter couldn’t be more different from one another. But Bernanke raised some interesting parallels. Among them: Both men were Washington outsiders, having run family businesses. Both arrived in the capital hoping to disrupt the status quo, take on the “beltway party” and “drain the swamp.” Both men tended to pick fights with members of their own parties and had difficulties getting key components of their agendas passed.

Of course, this is just one man’s opinion, and this week I came across another opinion at the Cornerstone Macro Conference in New York City. Before moving on, I want to thank Cornerstone CEO Nancy Lazar for another successful, thought-provoking conference. Like U.S. Global Investors, the analysts at Cornerstone believe that government policy is a precursor to change, and they closely track the purchasing manager’s index (PMI).

One of the speakers I was privileged to hear was Paul Gigot, the Pulitzer Prize-winning editor of the Wall Street Journal’s editorials page. Gigot spoke specifically of Trump’s leadership style, comparing it to Ronald Reagan’s.

|

Reagan was more strategic than Trump, whereas Trump is more tactical than Reagan. But neither president, according to Gigot, is fond of sitting down and diving into pages’ worth of briefing notes. Instead, they prefer to invite around three of their top Cabinet members and advisors to provide a rundown of the news and debate certain topics. Trump then makes a decision with his gut, Gigot says.

Involving trade, Trump’s three “wise men” are Larry Kudlow, director of the National Economic Council (NEC); Peter Navarro, director of the two-year-old Office of Trade and Manufacturing Policy (OTMP); and Treasury Secretary Steven Mnuchin.

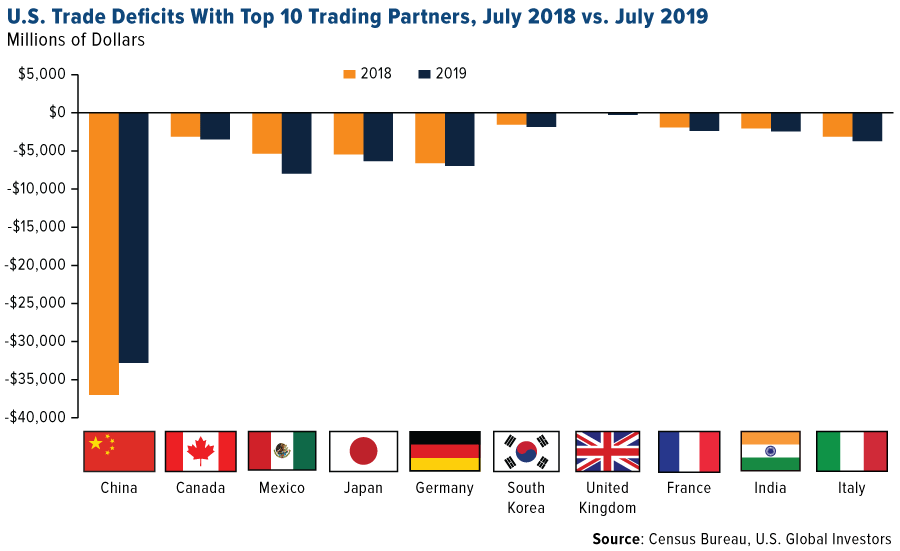

Gigot pointed out how Mnuchin prepares for his meetings with Trump. No other secretary, he says, comes in with a “cheat sheet” of trade deficits for nearly every country the U.S. does business with. Mnuchin can then fire off the data when Trump asks for it.

Take a look at the chart below. It shows the U.S. trade balance with its top 10 trading partners, comparing July 2019 to the same month year earlier. In all but one case (China), trade has fallen further into deficit from 12 months ago.

Could Heating Oil Prices Derail Trump’s Reelection?

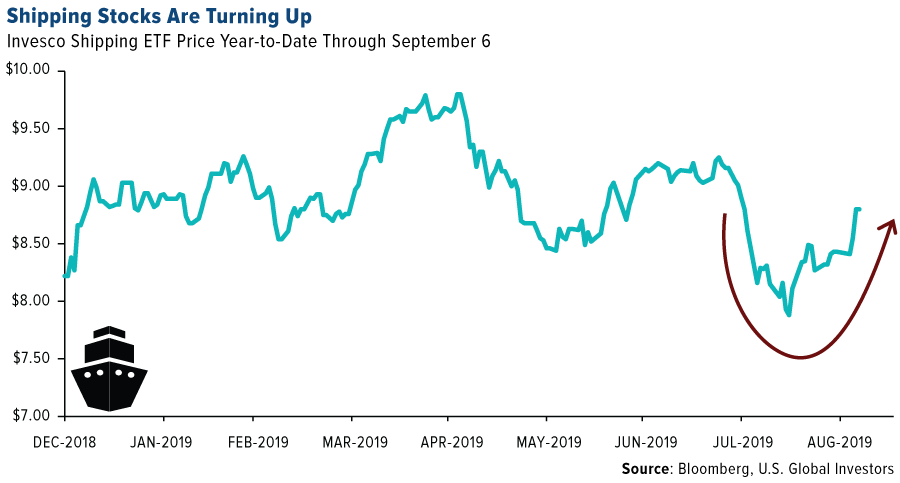

In another presentation, international energy consultant Robert McNally pointed to the one thing that could derail Trump’s reelection bid: IMO 2020.

IMO, in case you don’t know, stands for International Maritime Organization. Beginning January 1, 2020, all ships will need to slash sulfur oxide emissions by over 80 percent, to no more than 0.50 percent of all emissions. They must do this by switching to low-sulfur—and yet costlier—fuels, which is likely to have the effect of making shipping more expensive.

I like to say that government policy is a precursor to change, but in this case, IMO 2020 is a United Nations (UN) resolution. And as always, intentions are good, but this will have unintended consequences.

It’s expected that IMO 2020 will drive up the price of diesel, marine and jet fuels, not to mention heating oil in states such as Pennsylvania, Ohio and New York. The rise in consumer prices could end up weighing on the economy, and this has never reflected well on the incumbent president, whether he’s responsible or not.

McNally calls IMO 2020 a “sleeper” rule. Few people are talking about it right now, but that will undoubtedly change come January. In this respect, it’s not unlike FAS 157—also known as “mark-to-market”—the little-known accounting rule that some say was the cause of 2007-2008 financial crisis.

Below is the Invesco Shipping ETF (SEA), which invests in high dividend-paying companies in the global shipping industry. It’s been trading choppy lately because of the trade wars, but I expect it to turn up the closer we get to January. High-quality shipping companies have a better chance of being compliant, and the penalties will be high for non-compliance, from fines to even jail time for the ship’s captain.

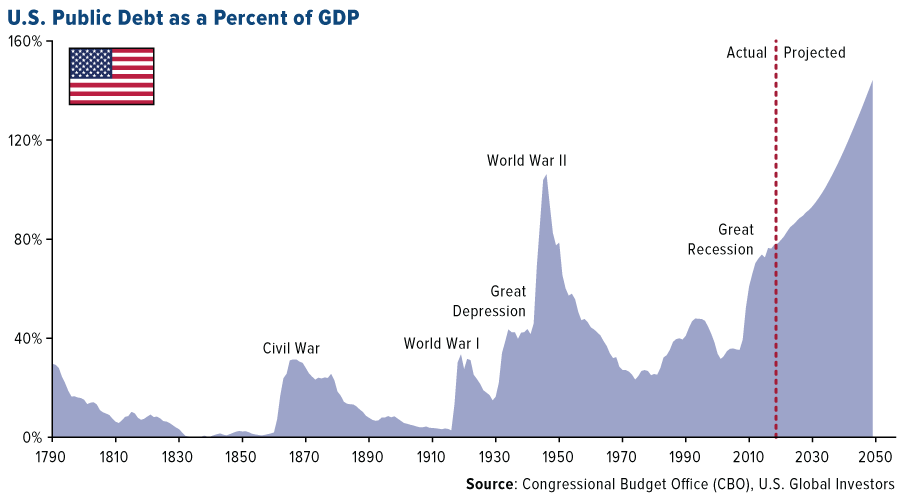

Federal Debt Projected to Hit an Unprecedented 144 Percent of GDP by 2049

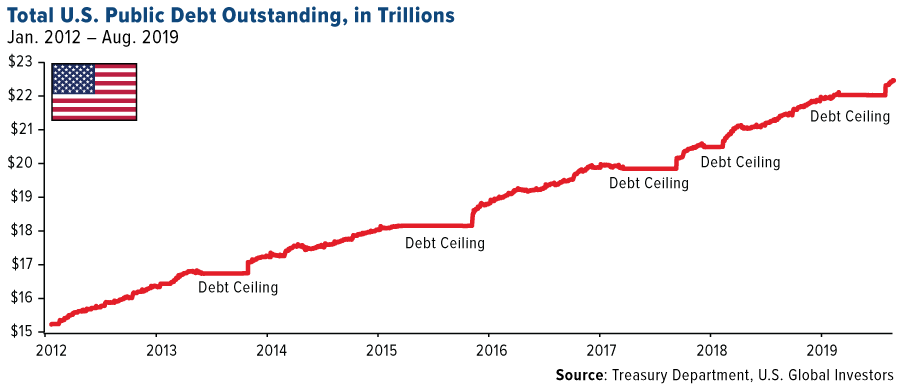

Deficits and federal spending were top of mind for many speakers and attendees at the conference. For the 2020 fiscal year, the federal budget deficit is expected to hit a massive $1 trillion—the first time in U.S. history that it will have expanded so rapidly in a time of peace and economic stability.

The most recent estimate by the Congressional Budget Office (CBO) puts total federal debt at a whopping 144 percent of gross domestic product (GDP) by 2049. This level of debt is not only unprecedented but also unsustainable. It puts everyone’s financial security at risk.

And if you’ve been keeping up with the Democratic presidential debates, things could get even worse.

Medicare-for-all, the Green New Deal, reparations—these programs, while admirable and potentially beneficial, would add trillions more to the already-ballooning national debt.

Remember, it’s the policies that we should be paying attention to, not partisan politics.

Years ago, it might have taken $1 trillion to move the U.S. economy by 2 percent of GDP. What is that number today? It might take $10 trillion or more.

Low, Low Corporate Bond Yields Encourage Record Borrowing

Speaking of debt, you may have heard that a record number of companies this week sought financing in the bond market. It’s no coincidence they rushed to the trough all at once. Average yields for investment-grade corporate debt are near an all-time low right now, making borrowing very inexpensive. Apple, Deere, Walt Disney and Coca-Cola were among the record 49 companies that issued as much as $54 billion through this past Wednesday. Apple alone sold $7 billion, its first bond deal since 2017.

Historic Currency Debasement Calls for a Shot of Gold

This brings me to my final point, and it’s an important one. Yields are at historic and near-historic lows, and they could be heading even lower sooner rather than later. The question you must ask yourself is how you will be positioned going forward.

In a recent blog post, Rick Rieder, chief investment officer at BlackRock, writes that we could be at what he calls the “monetary policy endgame.” In recent years, central banks have deployed nearly everything in their arsenal, including zero and negative interest rates and quantitative easing (QE).

The last stage could very well be extreme currency debasement. For that to happen, rates would need to be taken deeper and deeper into negative territory as economies compete for the weakest currency.

“How should one position for such as endgame?” Rieder asks. The solution, he says, “is to hold an asset that maintains its real value—an asset that cannot be printed.”

Such assets include dividend-paying stocks and “commodity currencies,” including gold, which is limited in supply and expensive to extract.

|

And the worst assets? According to Rieder, these would include “a sovereign bond with a negative yield, closely followed by paper money at zero yield, both with a theoretically infinite supply.”

Again, that’s the power of scarcity, as I discussed last week.

I believe such scarcity, when coupled with the slow debasement of currencies, is enough to push the price of gold up to as high as $10,000 an ounce. As I told Daniela Cambone this week in Kitco News’ New York studio, we aren’t going to see $10,000 gold in the next 12 months. But with yields in freefall, and radical currency debasement estimated to happen by the world’s central banks, where else will investors be able to turn? Real assets that have a limited supply and intrinsic value.

To see my entire interview with Daniela, click here!

Gold Market

This week spot gold closed at $1,506.71, down $13.59 per ounce, or 0.89 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.98 percent. The S&P/TSX Venture Index came in off just 0.14 percent. The U.S. Trade-Weighted Dollar fell 0.50 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-1 | Caixin China PMI Mfg | 49.9 | 50.4 | 49.9 |

| Sep-3 | ISM Manufacturing | 51.2 | 49.1 | 51.2 |

| Sep-5 | ADP Employment Change | 148k | 195k | 142k |

| Sep-5 | Initial Jobless Claims | 215k | 217k | 216k |

| Sep-5 | Durable Goods Orders | 2.1% | 2.0% | 2.1% |

| Sep-6 | Change in Nonfarm Payrolls | 160k | 130k | 159k |

| Sep-11 | PPI Final Demand YoY | 1.8% | — | 1.7% |

| Sep-12 | Germany CPI YoY | 1.4% | — | 1.4% |

| Sep-12 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Sep-12 | CPI YoY | 1.8% | — | 1.8% |

| Sep-12 | Initial Jobless Claims | 216k | — | 217k |

Strengths

- The best performing metal this week was platinum, up 1.89 percent. London-based BullionVault said in a report that investors bought gold at the fastest pace in three years, with the number of buyers jumping to 34 percent last month. Its gold investor index rose to an 11-month high of 55 in August, versus 52.6 in July. Investors swarmed toward gold in August. According to data compiled by Bloomberg, inflows into gold-backed ETFs topped 100 tons to hit the highest since February 2013. Even as gold took a big tumble this week, traders and analysts surveyed by Bloomberg are still bullish on the metal.

- Other precious metals had better weeks than bullion. Silver hit a three-year high early in the week and platinum continued its rally. The gold-to-silver ratio also fell to the lowest since August 2018, demonstrating that silver is catching up. In August, silver surged 13.3 percent compared with a 7.6 percent gain for the yellow metal. Turkey was bullish on gold last week. The central banks’ gold holdings rose $1 billion from the prior week to now total $25.7 billion.

- The ISM manufacturing purchasing manager’s index (PMI), an important forward-looking gauge of economic activity in the U.S., has been declining steadily for months now, and in August, it shrank for the first time in three years. The PMI stood at 49.1, down from 51.2 a month earlier, its lowest reading since March 2016. Gold historically performs well in times of economic uncertainty.

Weaknesses

- The worst performing metal this week was silver, down 1.19 percent. Gold posted its biggest loss in more than a year on Thursday, falling as much as 3 percent, as signs of easing trade tensions curbed demand for the metal as a safe haven asset, writes Bloomberg’s Justina Vasquez. Gold and silver miners also took a big tumble when China announced that it had agreed to trade talks with the U.S. early next month. However, some of those losses were erased on Friday morning after the U.S. economy added fewer jobs in August than expected. Later on Friday Fed Chairman Jerome Powell made comments that had little impact on expectations for further easing.

- Bloomberg reports that gold imports by India fell to 14.8 metric tons in August, down 84 percent from 92.1 tons a year earlier. Demand has decreased largely due to high gold prices in the world’s second largest gold consuming nation.

- Newmont GoldCorp announced the pricing of its public offering of $700 million total principal amount of 2.8 percent senior notes due in 2029, according to Zacks Equity Research. The net proceeds of the offering will be used for repayment of outstanding senior notes that are due next month. While refinancing existing debt with cheaper debt makes economic sense, we would rather see the debt load go down to improve the value of the equity.

Opportunities

- RBC Capital Markets Research Analyst James Bell wrote a note raising its forecast on gold. The group noted that the macro outlook for gold has improved materially and that real rates in the U.S. and globally have pushed gold prices to a six-year high. The note emphasizes that generalist investors are still underweight the sector and that we are currently in a “sweet spot” of higher prices without the mandate yet to buy from generalist throwing in the towel. Many of the junior companies share prices will lift with the broadening of the gold market, which just seems to be starting with silver and platinum now getting a bid.

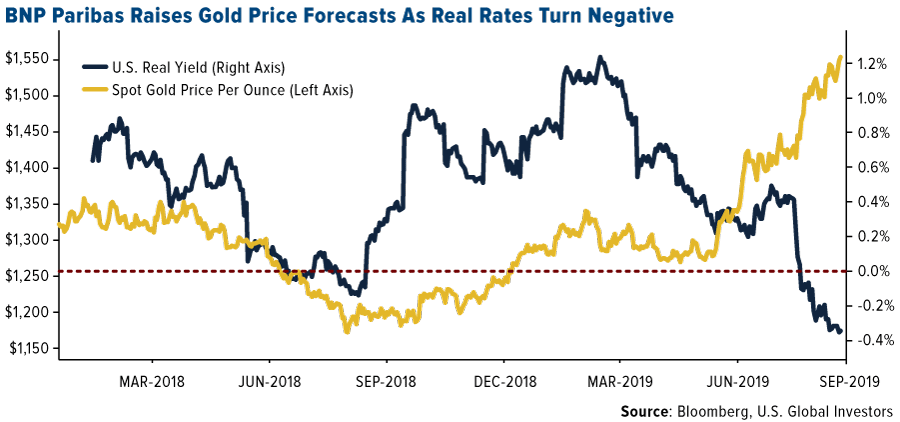

- BNP Paribas SA says that gold will surge above $1,600 an ounce as the Federal Reserve continues to cut interest rates to combat slowing U.S. growth. In the chart below the negative correlation between the gold price and U.S. real rates in clear. With the Fed expected to complete a quartet of cuts, this should be positive for the yellow metal.

- Platinum is riding the precious metals rally, with futures hitting $1,000 an ounce this week, a level last seen in February 2018. According to the World Platinum Investment Council, global platinum demand is forecast to rise 9 percent this year, driven by increased buying from ETFs. WisdomTree lifted its silver outlook and expects to see the white metal at $19.90 by the end of the quarter. These two metals rallying, along with gold, demonstrate that the precious metals rally is broadening.

Threats

- Billionaire hedge fund manager Ray Dalio believes there’s a 25 percent chance of recession this year and in 2020 in the U.S., reports Bloomberg, and that central bankers will be limited in addressing it. Dalio, who continues to advocate gold, says the yellow metal will be in demand as investors seek alternative forms of money as central bank stimulus nears “the limit of its effectiveness.” Earlier in the year he also pointed out flaws with capitalism – specifically pointing to gaps in education, social mobility and income that threaten the health of the economy.

- BMO Capital Markets, in its recent precious metals publication, says the rapid rise of precious metals pricing has fueled discussions on whether hedging should be making a comeback. The group explains that after several expensive experiments in hedging concluded over a decade ago, many producers have been reluctant to hedge any appreciable amount of production over a significant duration. The report also takes a look at who is hedging – apparently North American producers “generally have not entered meaningfully into hedges while international producers have.”

- According to the Australian Financial Review, Gold Fields chief executive Nick Holland is accusing the gold sector of misleading investors, pointing to inconsistent reporting of its actual cost structure. "Any growth capital people speak about is in fact largely sustaining capital,” Holland said. “The cost to sustain production is increasing. The industry is mining more tonnes at lower grade to maintain an ounce.”

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.49 percent. The S&P 500 Stock Index rose 1.79 percent, while the Nasdaq Composite climbed 1.76 percent. The Russell 2000 small capitalization index gained 0.69 percent this week.

- The Hang Seng Composite gained 3.63 percent this week; while Taiwan was up 1.53 percent and the KOSPI rose 2.10 percent.

- The 10-year Treasury bond yield rose 6 basis points to 1.555 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 2.64 percent versus an overall increase of 1.77 percent for the S&P 500.

- Tapestry was the best performing stock for the week, increasing 14.72 percent.

- Shares of PVH, the parent of brands such as Tommy Hilfiger and Calvin Klein, climbed 9.1 percent after an SEC filing indicated Chairman and CEO Chirico Emanuel spent nearly $10 million buying 133,155 shares at an average price of just under $75, writes the Motley Fool. The move significantly increased Emanuel’s stake in PVH to 417,351 shares, worth a total of over $33.8 million.

Weaknesses

- Utilities was the worst performing sector for the week, increasing by 0.36 percent versus an overall increase of 1.77 percent for the S&P 500.

- Tyson Foods was the worst performing stock for the week, falling 7.52 percent.

- Slack Technologies Inc. fell 12 percent after its first-ever earnings as a public company were announced, in which it posted a big loss. The stock price plunged to $26 after the bell, which is exactly what Slack had originally priced its shares at when it went public in June.

Opportunities

- It took less than a week for the U.S. equity market to put August’s tumult and frustration behind it. The S&P 500 rallied this week, driven by strong readings on the U.S. economy and news that top Chinese and American officials agreed to restart talks aimed at ending the trade war. The index has retraced almost all of last month’s 1.8 percent loss.

- Amgen Inc. shares could hit a record if an experimental new cancer medicine is able to show improvements in a handful of patients later this week, writes Bloomberg. A medicine known as AMG 510 has already shown early promise as data from June indicated the treatment can lead to responses at low doses, the article explains. AMG 510 targets a lung and colon cancer mutation known as KRAS G12C. Getting a drug to work on KRAS mutations has been the “the white whale of drug discovery,” Amgen’s head of global development has said.

- Facebook has brought its in-app dating feature to the U.S. after launching in 19 other countries, reports Business Insider. Facebook Dating is designed to compete with apps like Tinder and Bumble.

Threats

- Google is reportedly facing a big antitrust probe from “more than half” of the U.S. state attorneys general, and it could be announced as soon as next week. According to The Washington Post, it appears to be another probe looking into whether one of Silicon Valley’s largest companies has become too dominant.

- California legislators are voting on a bill that could force Uber and Lyft to reclassify their drivers as employees rather than independent contractors, potentially devastating their business models. Uber and Lyft have been open about the ramifications to their businesses should the bill become law.

- Oil producers and their suppliers are cutting budgets, staff, and production goals amid a growing consensus that oil and gas prices will stay low for several years. The U.S. has 904 working rigs, down 14 percent from a year ago.

The Economy and Bond Market

Strengths

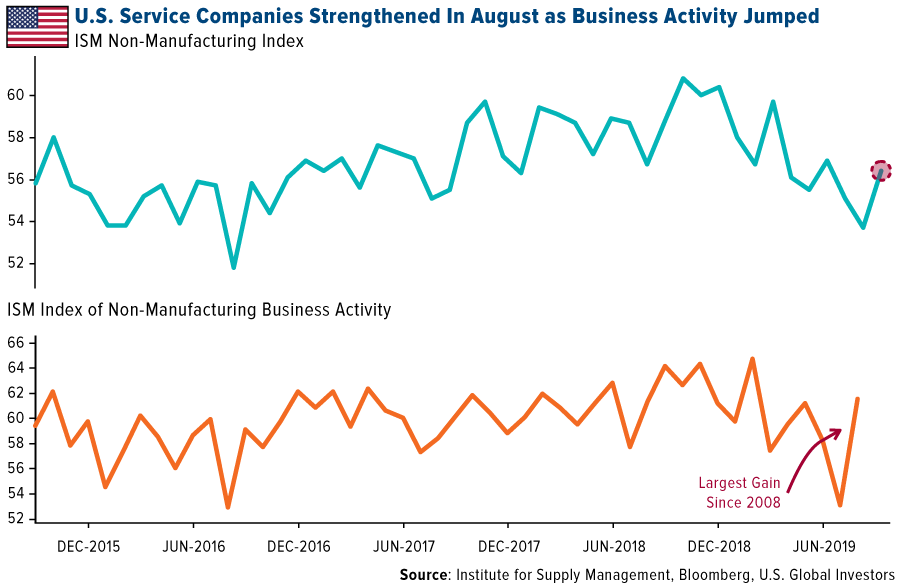

- Growth at U.S. service industries in August comfortably topped expectations on the sharpest monthly rebound in business activity since early 2008, writes Bloomberg. The non-manufacturing index advanced to a three-month high of 56.4, exceeding the most optimistic forecast in a Bloomberg survey of economists, Institute for Supply Management data showed Thursday.

- The unemployment rate held steady at 3.7 percent while average hourly wages rose by an average annual increase of 3.2 percent, according to government figures on Friday. Wage gains and low unemployment helped to fuel strong consumer spending during the spring and summer.

- The U.S. economy grew at a modest pace through much of July and August, writes Bloomberg, with companies remaining upbeat despite disruption caused by international trade disputes, a Federal Reserve survey found. “Although concerns regarding tariffs and trade policy uncertainty continued, the majority of businesses remained optimistic about the near-term outlook,” according to the Federal Reserve’s latest Beige Book.

Weaknesses

- The Institute for Supply Management’s purchasing managers index fell to 49.1 in August, weaker than all forecasts in a Bloomberg survey of economists, data released Tuesday showed. This unexpected contraction is the first since 2016. The group’s gauge of new orders dropped to a more than seven-year low, while the production index hit the lowest since late 2015.

- U.S. companies’ hiring stumbled in August, likely cementing expectations for a second straight Federal Reserve interest-rate cut. This comes as trade uncertainty and softer global growth weigh on the outlook, reports Bloomberg. Private payrolls rose 96,000, a three-month low, after a downwardly revised 131,000 advance the prior month, according to a Labor Department report Friday. Total nonfarm payrolls climbed a below-forecast 130,000.

- Residential construction spending dropped further off 2018 pace, reports Mortgage News Daily. While construction spending inched up by 0.1 percent in July, to a seasonally-adjusted annual rate of $1.289 trillion compared to $1.288 trillion in June, the July figure is 2.7 percent lower than the rate of spending in July 2018.

Opportunities

- Investors will be watching retail sales next Friday as they have been the backbone keeping the U.S. economy afloat.

- Federal Reserve Chairman Jerome Powell said the most likely outlook for the U.S. and world economy is continued moderate growth, but the central bank was monitoring “significant risks.” “As we move forward, we’re going to continue to watch all of these factors, and all the geopolitical things that are happening, and we’re going to continue to act as appropriate to sustain this expansion,” Powell said Friday in Zurich.

- Global Times, a newspaper of the Communist Party of China (CPC), is proclaiming there might be a real "breakthrough" in the upcoming trade talks between China and the United States scheduled for October, writes IBTimes.com. Editor-In-Chief Hu Xijin on Thursday tweeted, “China and the US announced new round of trade talks and will work to make substantial progress. Personally I think the US, worn out by the trade war, may no longer hope for crushing China’s will. There’s more possibility of a breakthrough between the two sides.”

Threats

- Germany’s recession risk continues to rise as industrial orders dropped significantly, writes Business Insider. Data on Thursday added to Germany’s woes, as new factory orders declined in July and construction fell to its lowest level in five years.

- The U.S. has its own problem with negative-yielding bonds, reads one Bloomberg article this week. Unlike Germany, Japan and other parts of the world, the U.S. still offers its creditors positive returns, the article explains. But the so-called real yield on 10-year Treasury Inflation-Protected Securities last month fell below zero and hit the lowest level since just before President Trump’s election in November 2016. This isn’t the first time the real yield has turned negative. But it’s turned negative at the same time as inflation expectations have been sinking, sounding a double-whammy warning for Wall Street.

- Morgan Stanley sees a Catch-22 for municipal-bond investors: A slowing U.S. economy could be bad for the asset class — and so could a rebounding one. That’s made the bank less optimistic about state and local government debt, which has returned 7.6 percent in 2019, marking the best year since 2014, according to the Bloomberg Barclays Index. The bank’s municipal-securities strategists said in a note to clients Tuesday that further upside may be limited regardless of which direction the economy takes. If the economy accelerates, that could upend bond markets that currently expect the Federal Reserve to cut interest rates again over the next two months. On the other hand, a recession would pose different risks: it could drive up the yields on many government bonds if tax revenue slows, credit ratings are cut and securities that financed speculative projects run into distress.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was natural gas, which gained 8.88 percent on strong demand as weather forecasts show summer’s heat continuing into next week. Zinc is having its best week in a year, gaining 5.5 percent. The metal is rising along with a broader rally in base metals after a move by China to support slowing growth added to strong U.S. economic data, reports Bloomberg. Copper also had a strong week advancing 3.1 percent.

- Nickel continues to have a great year after major exporter Indonesia announced a ban on ore exports two years earlier than expected. The nation expects related exports to more than double by 2024 as the ban on ore shipments will encourage investors to create smelters and electric car battery plants in the country. Nickel is the best performing main base metal so far this year, according to Bloomberg. “We don’t foresee a peak for nickel prices in the short term,” the Shanghai Metals Market said in a note on Tuesday.

- Equinor ASA surged as much as 7.7 percent in Oslo trading on Thursday after the company said it will be capitalizing on the imminent startup of its massive Johan Sverdrup field to kick off a $5 billion stock buyback program, reports Bloomberg. Shareholders had long been awaiting a stock buyback program. Concho Resources Inc. is selling assets in New Mexico to buy back $1.5 billion of its shares. The troubled Permian Basin oil producer is working to win back investor confidence after reducing its output target last month and plunging 22 percent, reports Bloomberg. The company says that selling assets in New Mexico will help cut costs and achieve a previously stated leverage target.

Weaknesses

- The worst performing major commodity for the week was lumber, which fell 4.41 percent. According to a report from Sanford C. Berstein, global electric car sales fell for the first time since China cut its subsidy. Monthly sales fell 14 percent to 128,000 passenger vehicles, with sales falling in China and North America while rising in Europe. Lithium stocks could fall along with these sales, which highlights the importance of government subsidies in growing adoption of this new technology.

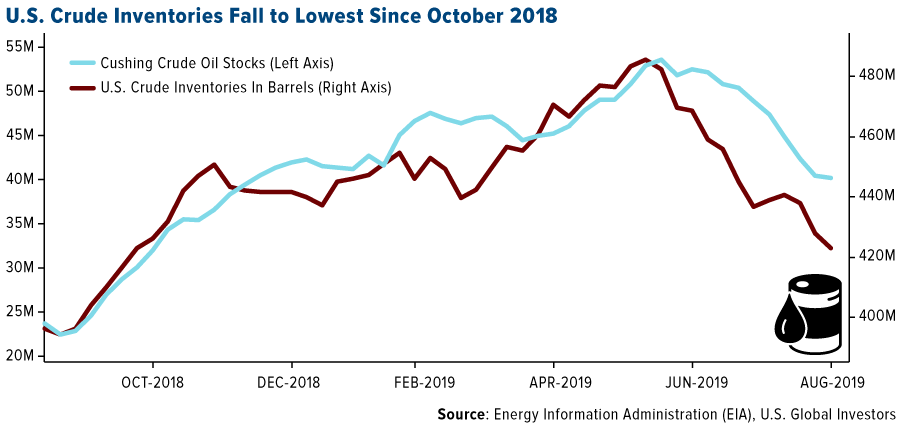

- Crude oil had a volatile week and will end little changed. Oil rose as much as 2.9 percent on Wednesday after U.S. crude inventories fell to the lowest since October 2018 and after Russia said it would curb production this month. Then on Friday morning it fell as much as 2.2 percent as the growing U.S.-China trade tensions weigh on the global economic outlook.

- MP Pension, a $420 billion fund in Denmark, is selling its stakes in the 10 largest oil companies after deciding they haven’t done enough to work toward climate goals, reports Bloomberg. The divestment is around $95 million and means the fund will no longer hold shares in companies such as ExxonMobil, BP and Chevron, the company said in a statement on Tuesday.

Opportunities

- First Cobalt Corp. is planning its first cobalt refinery in Canada, which would be North America’s only such refinery, after securing a $5 million loan agreement with Glencore AG. Bloomberg reports that the company will be able to fund its $37.5 million expansion of the plant, which is scheduled to produce 5,020 metric tons of contained cobalt by 2021 and supply 5 percent of the world’s global cobalt sulfate by 2025.

- Freeport LNG Development LP’s terminal is up and running in Texas and the first cargo has departed, making it the fifth such terminal in the area and further establishing American LNG influence. Bloomberg reports that since the first U.S. LNG export terminal began operating in Louisiana in 2016, the nation has become the world’s third largest supplier of the fuel.

- Major oil conference Oil & Money is rebranding for more climate-minded times, reports Bloomberg. The conference will be renamed the Energy Intelligence Forum, named after the publishing firm that sponsors it. The company said in a statement that “the world needs energy, but the energy industry must find ways to meet those needs in a more sustainable way.”

Threats

- U.S. oil sector bankruptcies are at the highest level in two years and continue to rise. The liabilities of upstream, downstream and oilfield services and equipment firms that have entered bankruptcy is approaching $20 billion this year, writes Bloomberg. Richard Chatterton says that although U.S. crude production is rising, it is not translating into sustainable profit for indebted oil firms.

- Mark Papa, CEO of Centennial Resource Development and chairman of Schlumberger, warns of Permian shale burnout. At a conference this week, Papa said that explorers are being forced into less-productive areas, which will cause U.S. growth in crude production to come in well below forecasts of 1.2 million barrels per day. “We’re seeing a lot of difficulties in growing U.S. oil production” and “in the time frame of six months to three years it’s going to have a profound effect on oil prices.”

- According to figures from the Pilbara Ports Authority, the world’s leading bulk-export port located in Australia, shipments of iron ore expanded to 45.4 million tons in August, which is the most ever for that time of year. Iron has had a volatile year after rising in the first half of the year due to a supply disruption then falling after production ramped back up. Bloomberg reports that there have been signs of potentially slower demand out of the China, which is the world’s largest consumer.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 2.4 percent. Investors’ worries lessened regarding investing in emerging markets after Hong Kong’s leader withdrew the controversial extradition bill that initially sparked the months-long protests. Turkish equites trade at almost a 50 percent discount to the MSCI Emerging Europe Index.

- The Turkish lira was the best relative performing currency this week, losing 2 percent against the U.S. dollar. The lira was supported by stronger economic data. Gross domestic product (GDP) was reported higher than expected in the second quarter and inflation declined further. However, Rabobank’s research team thinks that the disinflationary trend is mainly a function of favorable base effect accompanied by weak domestic demand.

- Industrial was the best performing sector among eastern European markets this week.

Weaknesses

- Czech Republic was the worst performing country this week, losing 50 basis points. There are only 12 stocks trading on the Prague exchange. Komercni Banks AS was the largest negative contributor to the index performance, with shares declining by 2 percent in the past five days. Banks in Europe face declining revenue on prospects of further rate cuts.

- The euro was the worst relative performing currency in the region this week, gaining 40 basis points against the U.S. dollar. Currencies gained in the past five days, but the euro was lagging its peers on prospects of rate cuts. European Central Bank policymakers will meet on September 12.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- Europe saw some positive news flow this week that could lead to less political noise and more economic stability. Italy was able to form a new government and avoid snap elections. The prospects of the U.K. exiting the eurozone without a deal on October 31 are declining. The British pound appreciated against the U.S. dollar. European luxury goods bounced strongly after small positive development in the Hong Kong protests.

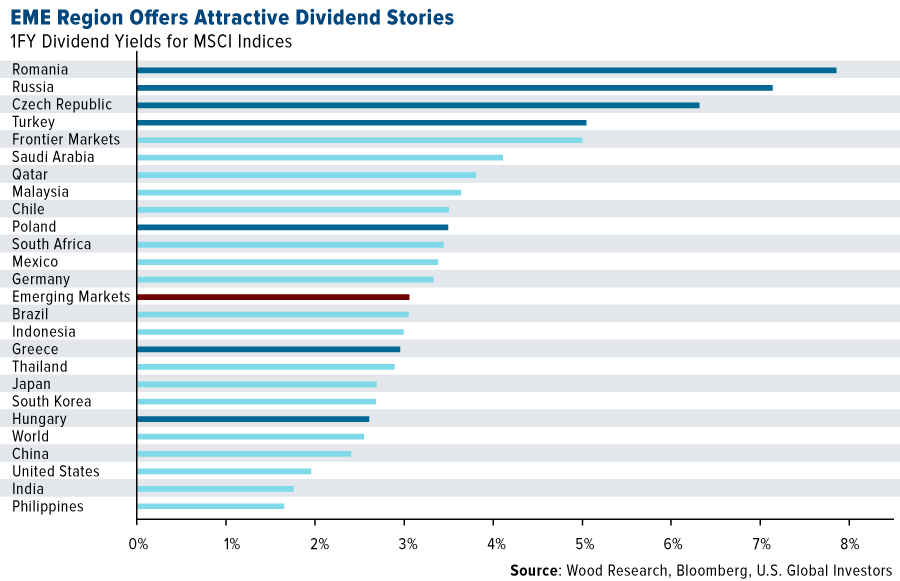

- Wood & Company in its “Yield hunting in WOOD’s universe” report selected 37 dividend stories and advised investors to focus on the EME region. They stressed that the top three markets with the highest dividend yields in the EME Region are Romania, Russia and Czech Republic, which are paying nearly double the average for the Emerging Market and Developed Market universe.

- Mario Draghi, president of the ECB, is expected to deliver a stimulus push next week. More than 80 percent of economists surveyed by Bloomberg predict officials will announce more quantitative easing next week. They see the ECB’s deposit rate being reduced by 10 basis points to a record-low of negative 0.5 percent in September, and expect a second cut of 10 basis points in December.

Threats

- The incoming head of the EU executive arm, Ursula von der Leyen, is promising new laws on artificial intelligence and the use of big data within 100 days of taking office on November 1. Alphabet Inc.’s Google has been fined a total of $9.4 billion in three separate EU probes. She is in favor of fair taxes on the tech giants, which will further strain the already delicate U.S. – EU relationship.

- Bloomberg economists predict the Sentix Investor Confidence Index in the euro area to fall deeper into negative territory next week. The data could come out even worse for the German economy, the largest in Europe, that is highly dependent on exports and the Chinese sales market.

- More political noise could emerge in Turkey, as former economy minister Ali Babacan is planning to establish his own political party by the end of this year to challenge President Erdogan’s 16-year rule. Babacan broke with the ruling AKP Party days after Erdogan let go the central bank chiefs in July.

China Region

Strengths

- The best performing indices in the region for the week were China’s Shanghai Composite, which gained 3.95 percent on the week, and Hong Kong’s Hang Seng Composite Index, which jumped 3.63 percent for the week. Despite some continued headwinds both locales enjoyed a bit of respite and some positive news.

- The best performing sector in Hong Kong’s Hang Seng Composite Index was information technology, which bounced back and gained 5.29 percent for the week.

- Most of China’s PMI data came in a little better than consensus anticipated. Official Manufacturing PMI clocked in at only 49.5, slightly below estimates for 49.6 and still in contractionary territory, but the Caixin China Manufacturing PMI, on the other hand, was expected to come in at 49.8 and instead beat, delivering a 50.44 print, rising to an expansionary level again from the prior reading of 49.9. China’s official non-manufacturing PMI also beat slightly, with a 53.8 print versus expectations for 53.7, while the Caixin China Services PMI came in this week at a 52.1, up from the prior reading of 51.6.

Weaknesses

- The worst performing indices in the region were India’s NIFTY and SENSEX indices, which declined by 70 and 94 basis points, respectively.

- The poorest performing sector in Hong Kong’s Hang Seng Composite Index this week was the more risk-off utilities sector, which closed down 62 basis points on the week and was the only sector to finish in the red.

- The Markit Indonesia Manufacturing PMI declined to 49.0, down from the prior contractionary reading of 49.6.

Opportunities

- As noted last week, a lot can change in a week with respect to the U.S.-China trade war. While the September 1 tariffs did indeed kick into effect, most analysts remain more focused upon those looming in December and of course, on the question of the hikes approaching on October 1. This week did see a positive development in the confirmation of high-level talks now set for some time in October, and the announcement of lower level talks leading into them.

- Momentum shifted higher this week and out of the U.S.’s recent August range trade as Hong Kong CEO Carrie Lam formally killed the extradition bill and met one key demand of the protestors. As a degree of buying ensued and U.S.-China talks looked to be set for October, the question of whether Hong Kong is “oversold” and “undervalued” began to arise among market analysts. And indeed, while it’s probably too soon to say whether the big picture has really changed—Carrie Lam, after all, is still CEO, and other protestor demands remain unmet, etc.—it is worth noting that Investor Alert has called consistent attention to the relatively low price-to-earnings ratio for Hong Kong’s blue chip Hang Seng Index, which has now risen modestly, closing the week at 10.40.

- China announced a broad-based 50 basis point cut in the reserve ratio requirement for its banks, as well as delivering a more targeted 100 basis point cut for eligible regional banks, Bloomberg News reported on Friday in an article quotably entitled “PBOC Unleashes Stimulus with RRR Cut, More to Come.”

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation remains a threat until it isn’t. It seems likely that the cycle of delays and talks and hikes/counter-hikes could continue, with fits and starts, into 2020 and possibly even through the U.S. election. Of course, they could always collapse well before then too, and at present, the U.S. is set to hike in October and introduce new tariffs in December. Given the tariffs already in place, escalation remains a potential reality that must be borne in mind. Larry Kudlow advised that negotiations could go on for a while…

- Once again, unrest continues in Hong Kong and the uncertainty means Hong Kong’s political (and economic) status remains somewhat on the table, even as Fitch downgraded the city this week to AA from AA+, with a negative outlook.

- Recent news reports have highlighted that as China’s economy has slowed down, Chinese outbound tourism around the region has also declined accordingly, and even Macau’s gross gaming receipts for the August measurement period were down 8.6 percent year over year, lower than the consensus estimate.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 6 was Molecular Future, up 772.02 percent.

- After the Securities and Exchange Commission (SEC) has so far made it impossible for VanEck Securities and SolidX Management to launch an ETF that invests in bitcoin, now the duo have found a workaround for some large investors. As reported by Bloomberg, the two companies announced Tuesday that through Rule 144A of the Securities Act of 1933, they’ll be issuing shares in the VanEck SolidX Bitcoin Trust to qualified institutional buyers.

- One of the earliest companies to pitch blockchains to enterprises, Factom, is participating in a U.S. government-funded trial of the technology to protect the national power grid, reports CoinDesk. TFA Labs announced Thursday it is experimenting with Factom’s protocol to validate that devices on the grid aren’t infected with malware. Backed by a nearly $200,000 grant from the U.S. Department of Energy (DOE), the project aims to improve the security of millions of devices on the power grid.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 6 was Custody Token, down 96.30 percent.

- According to one MarketWatch headline this week, ransomware is threatening to take more businesses and governments “hostage.” In the report that outlines how these attacks have evolved, it explains that cybercriminals have shifted to more sophisticated techniques to cover their tracks, particularly how they are paid. “Now almost all ransomware attackers demand payments in some type of cryptocurrency such as bitcoin, making it more difficult to identify who the actual person behind the keyboard is,” the article continues.

- Mark Mobius of Mobius Capital Partners told CNBC’s Squawk Box this week that cryptocurrencies, like fiat, are backed by faith and only hold utility as far s others are willing to use them, reports CoinDesk. The major investor also remains cautious about blockchain. “I belive blockchain is a very high-risk situation,” Mobius said, explaining that the technology itself remains open to attacks.

Opportunities

- Legacy Trust, a cryptocurrency custody provider, is launching one of the first digital assets-based pension plans, writes CoinDesk. “We envisage that this will appeal to businesses who are active in the digital assets space, and who want to offer additional benefits to their employees to retain talent and recognize achievement,” Legacy Trust CEO Vincent Chok said.

- According to an executive at Apple, the tech giant is “watching cryptocurrency,” reports CoinDesk. At a private San Francisco event, Apple Pay vice president Jennifer Bailey told CNN “We think blockchain has interesting, long-term potential.” In February, Apple submitted a filing to the SEC containing rare details about the computing giant’s interest in blockchain tech, the article continues.

- Square’s co-founder Jack Dorsey says that cryptocurrency adoption will help transform his company’s development, reports CoinDesk. “In the long term (cryptocurrencies) will help us be more and more like an internet company where we can launch product,” Dorsey said in an interview with the Australian Financial Review. “The whole world can use it, instead of having to go from market to market, to bank to bank to bank and from regulatory body to regulatory body.”

Threats

- On Monday, Yves Mersch, a member of the European Central Bank (ECB) executive board outlined problems with the planned cryptocurrency Libra, reports MarketWatch, the latest in a series of warnings from government officials. “I sincerely hope that the people of Europe will not be tempted to leave behind the safety and soundness of established payment solutions and channels in favor of the beguiling but treacherous promises of Facebook’s siren call,” Mersch said.

- According to an article by Bloomberg, the notion that more people are trading cryptos could be wrong. Crypto data tracker TokenAnalyst reports that fewer people have been sending bitcoin to major exchanges in recent months. After peaking in 2017, the number of unique addresses sending to popular exchanges such as Binance and Bitfinex has been declining.

- JPMorgan says that despite stablecoins being the fastest growing subset of cryptocurrencies, designed to avoid large fluctuations of bitcoin and ether, they could actually fail to function properly in times of stress. As reported by Bloomberg, while the total value of all stable coins is less than $5 billion, the low-volatility tokens are poised for rapid growth. However, they are vulnerable to bottlenecks and seizures “because they lack the same short-term liquidity facilities common in other payments systems.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 248.08 | -15.16 | -5.76% |

| Gold Futures | 1,513.90 | -15.50 | -1.01% |

| Natural Gas Futures | 2.49 | +0.21 | +9.02% |

| S&P/TSX VENTURE COMP IDX | 588.51 | -0.85 | -0.14% |

| 10-Yr Treasury Bond | 1.56 | +0.06 | +3.81% |

| Nasdaq | 8,103.07 | +140.19 | +1.76% |

| Oil Futures | 56.62 | +1.52 | +2.76% |

| Hang Seng Composite Index | 3,589.31 | +125.87 | +3.63% |

| S&P 500 | 2,978.71 | +52.25 | +1.79% |

| DJIA | 26,797.46 | +394.18 | +1.49% |

| Korean KOSPI Index | 2,009.13 | +41.34 | +2.10% |

| Russell 2000 | 1,505.15 | +10.31 | +0.69% |

| S&P Energy | 433.24 | +11.15 | +2.64% |

| S&P Basic Materials | 357.38 | +3.10 | +0.88% |

| XAU | 94.26 | -4.72 | -4.77% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.49 | +0.41 | +19.59% |

| S&P/TSX Global Gold Index | 248.08 | -5.87 | -2.31% |

| 10-Yr Treasury Bond | 1.56 | -0.18 | -10.37% |

| Oil Futures | 56.62 | +5.53 | +10.82% |

| Gold Futures | 1,513.90 | -5.70 | -0.38% |

| S&P 500 | 2,978.71 | +94.73 | +3.28% |

| S&P Energy | 433.24 | +4.16 | +0.97% |

| Hang Seng Composite Index | 3,589.31 | +120.68 | +3.48% |

| DJIA | 26,797.46 | +790.39 | +3.04% |

| Korean KOSPI Index | 2,009.13 | +99.42 | +5.21% |

| Nasdaq | 8,103.07 | +240.25 | +3.06% |

| S&P Basic Materials | 357.38 | -0.08 | -0.02% |

| Russell 2000 | 1,505.15 | +4.46 | +0.30% |

| S&P/TSX VENTURE COMP IDX | 588.51 | -8.82 | -1.48% |

| XAU | 94.26 | -1.79 | -1.86% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.49 | +0.17 | +7.19% |

| 10-Yr Treasury Bond | 1.56 | -0.56 | -26.58% |

| DJIA | 26,797.46 | +1,076.80 | +4.19% |

| Oil Futures | 56.62 | +4.03 | +7.66% |

| S&P 500 | 2,978.71 | +135.22 | +4.76% |

| Gold Futures | 1,513.90 | +159.90 | +11.81% |

| S&P Energy | 433.24 | -14.61 | -3.26% |

| Nasdaq | 8,103.07 | +487.52 | +6.40% |

| Korean KOSPI Index | 2,009.13 | -59.98 | -2.90% |

| S&P Basic Materials | 357.38 | +0.68 | +0.19% |

| Russell 2000 | 1,505.15 | +1.61 | +0.11% |

| Hang Seng Composite Index | 3,589.31 | -4.46 | -0.12% |

| S&P/TSX Global Gold Index | 248.08 | +46.93 | +23.33% |

| S&P/TSX VENTURE COMP IDX | 588.51 | -6.69 | -1.12% |

| XAU | 94.26 | +19.85 | +26.68% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2019):

Equinor ASA

Concho Resources Inc

Chevron Corp

Freeport-McMoRan Inc

Gold Fields Ltd

Newmont Goldcorp Corp

Tyson Foods Inc.

Amgen Inc.

Invesco Shipping ETF

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MSCI Emerging Markets Europe Index captures large and mid-cap representation across 6 Emerging Markets countries in Europe. With 72 constituents, the index covers approximately 85 percent of the free float-adjusted market capitalization in each country. The Sentix Investor Confidence Index rates the relative six-month economic outlook for the euro zone. The data is compiled from a survey of about 2,800 investors and analysts. A reading above zero indicates optimism; below indicates pessimism. BullionVault’s Gold Investor Index measures the balance of private investors buying gold to start or grow their holding across the month over those reducing or selling them entirely. A reading of 50.0 means the number of people buying gold across the month was perfectly balanced by the number of sellers. The Bloomberg Barclays 3-Year Municipal Bond Index is a total return benchmark designed for short-term municipal assets. The index includes bonds with a minimum credit rating BAA3, are issued as part of a deal of at least $50 million, have an amount outstanding of at least $5 million and have a maturity of 2 to 4 years. The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. Sensex, otherwise known as the S&P BSE Sensex index, is the benchmark index of the Bombay Stock Exchange (BSE) in India. The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.