Gold Gets a Boost of Rocket Fuel From Negative Bond Yields. What’s Next for the Yellow Metal?

Date Posted: June 21, 2019

Read time: 49 min

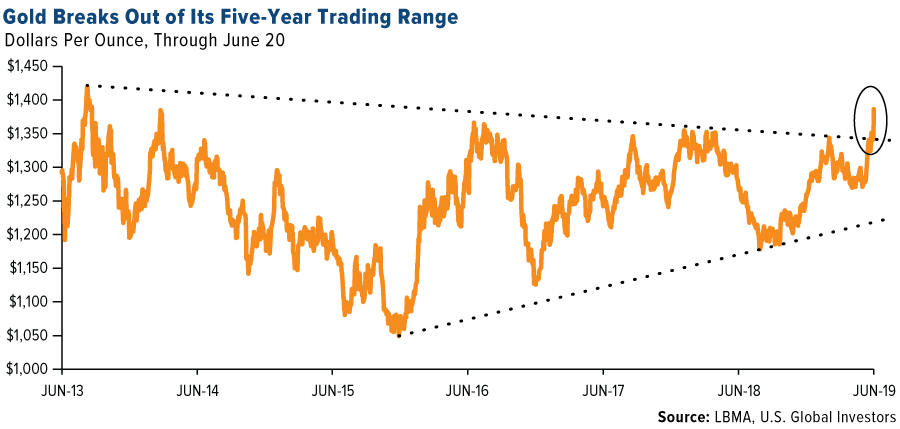

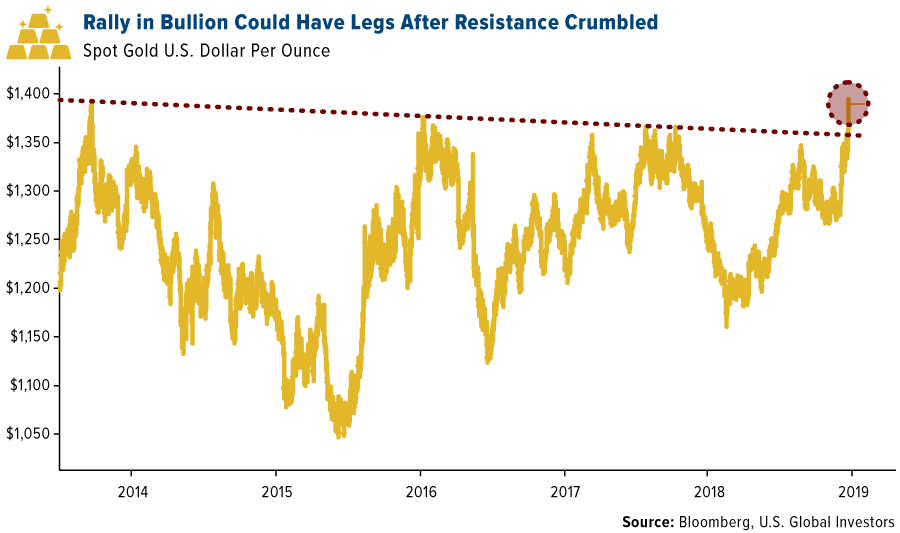

After breaking out of a five-year trading range this week, gold surged above $1,400 for the first time since 2013 on expectations of a U.S. rate cut. Meanwhile, the global pool of negative-yielding bonds hit a fresh record high $13 trillion.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Ladies and gentlemen, we have liftoff!

After breaking out of a five-year trading range this week, the price of gold surged above $1,400 an ounce for the first time since 2013 on expectations of a U.S. rate cut. The 10-year Treasury yield fell to around 2 percent, its lowest level since November 2016. Meanwhile, the pool of negative-yielding government bonds around the world hit a fresh record high of $13 trillion.

Gold “may finally be off the leash,” Bloomberg’s commodities columnist David Fickling wrote on Thursday after the yellow metal rallied above $1,350, a number that for the past six years has filled gold bulls with “dread.” In this week’s Frank Talk Live video, I shared my belief that gold would continue to rally if it broke above that key resistance level. Like billionaire hedge fund manager Paul Tudor Jones, I believe gold can now make it as high as $1,700 an ounce “rather quickly” as more generalist investors decide to participate.

And even if gold’s price did hit $1,700, it would still be well within its DNA of volatility. The truth is that it’s a non-event for gold to go plus or minus 20 percent over any rolling 12-month period.

Lower yields have reportedly caught many analysts by surprise. In January of this year, not a single economist among the 69 surveyed by the Wall Street Journal predicted that yields would drop below 2.5 percent by June. The average forecast had been closer to 3 percent.

Some market-watchers are now looking to 1 percent yields. Writing for Bloomberg, longtime financial analyst Gary Shilling says he’s “more confident than ever in that [1 percent] forecast,” due to “chronic low inflation” and the likelihood that the next recession is “already underway.”

Falling bond yields, as I’ve explained many times before, have historically supported the price of gold.

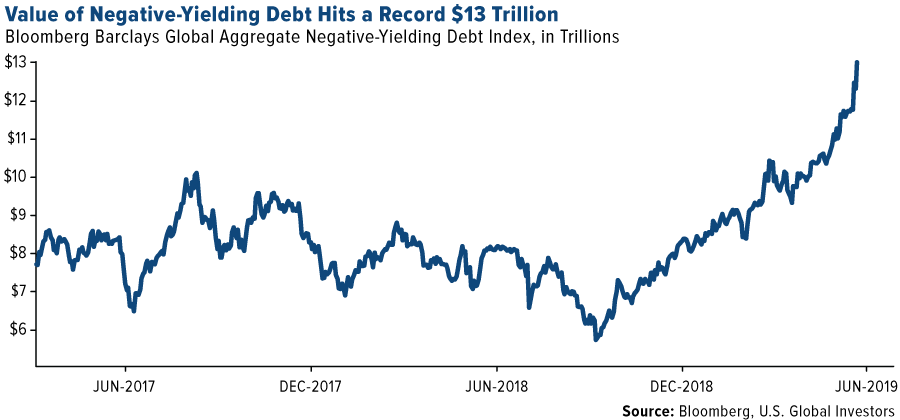

A Record $13 Trillion in Negative-Yielding Debt

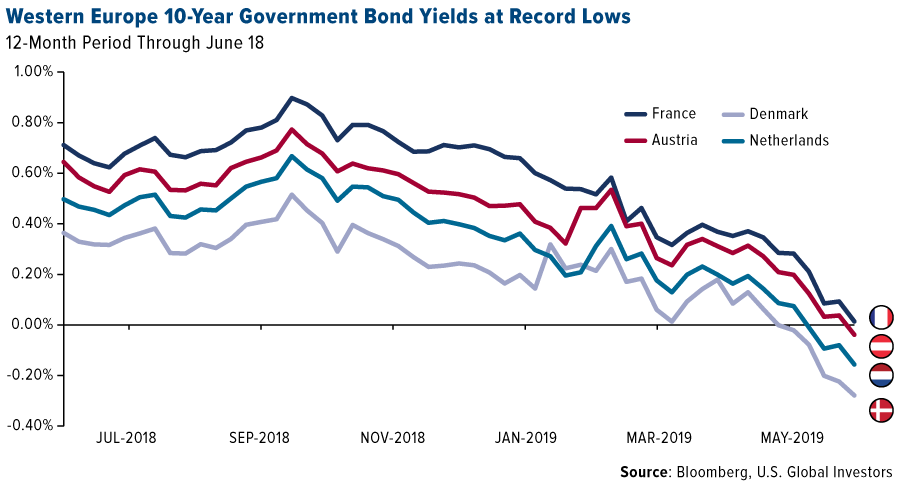

That’s especially the case when yields turn negative, as they have all across Western Europe this week following hints that the European Central Bank (ECB) could initiate a new round of quantitative easing (QE). At the annual ECB conference in Sintra, Portugal, on Tuesday, chief banker Mario Draghi stated that in the absence of economic improvement or a lift in inflation, “additional stimulus will be required.”

A number of European countries’ intermediate government bond yields sagged to record lows. French and Swedish 10-year yields fell below 0 percent for the first time ever. Close to 100 percent of all debt issued by the Swiss government, from one-month to 20-year maturities, now carries a negative yield. That’s closely followed by Sweden (91 percent of all debt), Germany (88 percent), Finland (84 percent) and the Netherlands (84).

Altogether, a jaw-dropping $13 trillion in global government debt—a new record—is now offering sub-zero yields. This means that investors are guaranteed to end up with less than the bond’s principal amount if held until maturity.

We could see increased foreign demand for U.S. Treasuries because of this, which would push bond yields even lower.

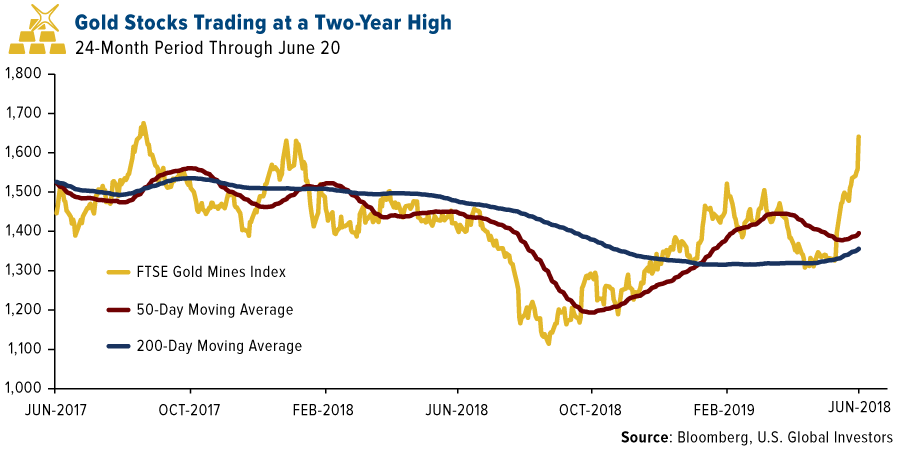

Gold Stocks Trading Higher

Gold stocks also rallied this week, with the FTSE Gold Mines Index advancing more than 5.3 percent on Thursday, its best one-day gain since January 2017. The group is now beating the market for 2019, as of June 21.

Among the companies with the biggest moves this week were Eldorado Gold, closing up 12 percent on Thursday in Toronto trading; Coeur Mining (up 11.1 percent); Yamana Gold (9.5 percent); Hecla Mining (7.6 percent); and IAMGOLD (up 6.7 percent).

As rates look ready to decline, I believe it could be prudent right now to make sure you have adequate exposure to gold. I always recommend a 10 percent weighting, with 5 percent in bullion and gold 24-karat jewelry, the other 5 percent in well-managed gold stocks, mutual funds and ETFs.

Why are billionaires hungry for gold? Watch my interview with Kitco’s Daniela Cambone by clicking here!

Gold Market

This week spot gold closed at $1,399.02, up $57.17 per ounce, or 4.26 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 7.61 percent. The S&P/TSX Venture Index came in up just 0.80 percent. The U.S. Trade-Weighted Dollar fell 1.40 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-18 | Eurozone CPI Core YoY | 0.8% | 0.8% | 0.8% |

| Jun-18 | Germany ZEW Survey Current Situation | 6.1 | 7.8 | 8.2 |

| Jun-18 | Germany ZEW Survey Expectations | -5.6 | -21.1 | -2.1 |

| Jun-18 | Housing Starts | 1239k | 1269k | 1281k |

| Jun-19 | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | 2.50% |

| Jun-20 | Initial Jobless Claims | 220k | 216k | 222k |

| Jun-25 | Hong Kong Exports YoY | -4.5% | — | 2.6% |

| Jun-25 | New Home Sales | 685k | — | 673k |

| Jun-25 | Conf. Board Consumer Confidence | 131.0 | — | 134.1 |

| Jun-26 | Durable Goods Orders | -0.2% | — | -2.1% |

| Jun-27 | Germany CPI YoY | 1.5% | — | 1.4% |

| Jun-27 | GDP Annualized QoQ | 3.2% | — | 3.1% |

| Jun-27 | Initial Jobless Claims | 220k | — | 216k |

| Jun-28 | Eurozone CPI Core YoY | 1.0% | — | 0.8% |

Strengths

- The best performing metal this week was gold, up 4.26 percent. Gold traders and analysts were surprisingly neutral on their price outlook for the yellow metal after it hit a five-year high this week and broke above $1,400 per ounce. Bullion got a huge boost after the Federal Reserve kept interest rates unchanged on Wednesday and signaled a readiness to cut rates due to increased economic uncertainties.

- Central banks continue to show their love for gold. Kazakhstan raised its gold holdings to 11.93 million ounces in May, up from 11.79 million ounces in April. Russia’s climbed from 70.2 million ounces to 70.42 in May. Turkey was also up to 16.03 million ounces in May from 15.99 in April. Additionally, Turkey saw its gold reserves rise $167 million this week from the previous week.

- Illegal gold mining in Ghana is now being cracked down on. A veteran NASA engineer developed a software tool that is capable of identifying illegal mines from satellite photos, making it easier to find and shut down illegal operations. Refiners are also taking steps to reduce illegal mining. Reuters reports that Metalor, one of the world’s largest gold refineries, said on Monday that it would only work with gold from large industrial mines in order to reduce the risk of illegality in its supply chain of the metal. Gold Fields Ltd. announced that its mine in Western Australian will become one of the nation’s first mining operations to be predominantly powered by renewable energy.

Weaknesses

- The worst performing metal this week was platinum, up just 0.51 percent as hedge funds boosted their new bearish positioning to a 9-month high. Fed Chairman Jerome Powell regularly receives attacks from President Donald Trump on interest rates and Fed policy. The President has now threated to remove Powell as chair. Even though many think the president cannot outright fire Powell, White House lawyers have put together a framework for the president to demote Powell and leave him as just a governor.

- Bloomberg reports that sentiment among U.S. homebuilders unexpectedly fell for the first time this year, suggesting that lower mortgage rates aren’t giving housing a boost. The Empire State manufacturing index plunged in June by the most on record, which adds to signs that continued tariffs are hitting manufacturers and the broader economy.

- Barrick Gold continues its bid for Acacia Mining in what might not be the best deal in the space. Barrick was initially down 1.3 percent in the premarket on Wednesday after it said it is proposing to engage “intensively” with Acacia’s minority shareholders.

Opportunities

- President Trump might be starting a currency “war,” in addition to the ongoing trade war. After the European Central Bank (ECB) announced it was prepared to cut interest rates further below zero, Trump published a series of tweets accusing the bank of unfair competition. Trump has spoken of reigning in the dollar, which would likely be positive for the price of gold, as the two have historically had an inverse relationship.

- Gold is heading for its best week in three years with it set to close near $1,400 per ounce – a level not seen since 2013. Citigroup says that “bullish gold fever [is] justified” after the Fed meeting. It also raised its 3-month price target to $1,450, up from $1,400 in January.

- Bloomberg’s Eddie van der Walt writes that “with central banks around the world turning more dovish, the latest move may just be the start” in regards to gold breaking above its resistance level. Evercore ISI, which isn’t usually a gold bull, released a recommendation this week on the yellow metal to “either way, buy gold.”

Threats

- Despite gold’s recent price breakout, junior miners are still having a hard time finding sources of capital, as gold is down around 28 percent below its peak earlier this decade. Andrew Kaip, an equity analyst at BMO Capital Markets, said that “large banks aren’t willing to lend debt to companies that don’t have revenue.” Small gold miners often don’t have revenue and need to find capital for exploration and building out mines. However, if gold keeps moving higher it will be very positive for juniors seeking funding.

- A threat for consumers in general, politicians and analysts are waking up and noticing the negative effect that big tech has on everyday Americans. Representative David Cicilline of Rhode Island, who opened an investigation into competition in the tech industry, said that big tech companies like Facebook and Google have had “devastating effects” on everyday Americans due to them having much of users’ private information and selling to the highest bidders. Should the government pursue antitrust to its logical conclusion that “Big Tech” gets turned into regulated utilities they would no longer be able to own their own platform and participate in it. New regulation is coming for the tech giants as the government realizes the monetization of your privacy is wrong.

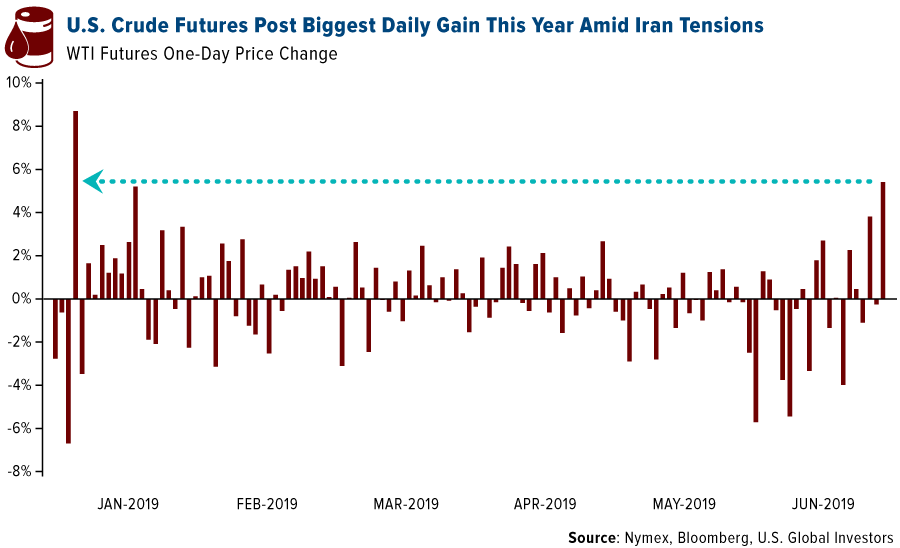

- Tensions continue to rise in the Middle East after Iran shot down an American drone this week. President Trump ordered, and then called off, a limited airstrike that was intended to target three infrastructure sites related to the missile launch.

June 19, 2019Facebook’s Libra Cryptocurrency Is the Future of Fintech |

June 19, 2019Frank Holmes Believes Gold Will Break $1,400 |

June 17, 2019Billionaire Investor: "Gold Has Everything Going For It" |

|||

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.41 percent. The S&P 500 Stock Index rose 2.15 percent, while the Nasdaq Composite climbed 3.01 percent. The Russell 2000 small capitalization index gained 1.80 percent this week.

- The Hang Seng Composite gained 5.00 percent this week; while Taiwan was up 2.65 percent and the KOSPI rose 1.44 percent.

- The 10-year Treasury bond yield fell 2 basis points to 2.057 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing 5.16 percent compared to an overall increase of 2.34 percent for the S&P 500 Index.

- News Corp. was the best performing stock for the week, increasing 14.37 percent.

- Slack went public through the unorthodox method of direct listing, with its stock price soaring 50 percent on its first day of trading.

Weaknesses

- Consumer staples was the worst performing sector for the week, increasing 0.10 percent compared to an overall increase of 2.34 percent for the S&P 500.

- Carnival Corp. was the worst performing stock for the week, falling 12.22 percent.

- Shares of Carnival sank as much as 10 percent, the most in more than three months, after the company slashed its full-year profit forecast during its second quarter-earnings release Thursday. This is the second time in three months the company has lowered its yearly outlook.

Opportunities

- Shares of Allergan have been climbing this week after an analyst at Evercore ISI stated that a break-up of the company’s business may be in the cards. The analyst also stated that the company is likely to provide an update on the split in the next couple of months. The analysis was based on a conference call with the company’s vice president of investor relations on Tuesday. Some analysts believe that splitting of Allergan’s business, if it materializes, would be a positive and has in fact been debated on for long. Moreover, activist investors have long been pushing for a separation of chief executive officer and chairman positions, both currently held by Brent Saunders.

- After years of struggling, oilfield service companies are beginning to raise prices for their products and services, according to a new report from research firm Rystad Energy. “After losing pricing power in 2015 and 2016, oilfield service companies have since regained some of the lost ground, thanks first and foremost to industry consolidation among players that has concentrated the market over the past couple of years,” says Rystad’s chief of oilfield service research.

- Boeing could win more business after its bumper IAG deal. The aviation giant is in talks to sell more of its grounded 737 Max aircraft after British Airways-owner IAG signed a letter of intent to buy 200 of them, according to Reuters.

Threats

- Lufthansa stock is tanking. Shares in the German airline plunged 11 percent after it issued a profit warning, saying its Eurowings unit is likely to suffer from intense competition in the budget airline industry.

- Broadcom took a $2 billion hit following Trump’s Huawei ban. In its earnings report, Broadcom CEO Hock Tan attributed the slowdown to “geopolitical uncertainties” and “the effects of export restrictions on one of our largest customers.”

- The FBI is reportedly investigating Deutsche Bank for flouting money-laundering rules. Some of the transactions in question are connected to Jared Kushner, Donald Trump’s son-in-law, the New York Times reported.

The Economy and Bond Market

Strengths

- Sales of previously owned U.S. homes rebounded in May to a three-month high as all regions gained amid lower interest rates and a labor market that remains strong. Contract closings rose to a 5.34 million annual rate, topping projections and climbing 2.5 percent from April’s upwardly revised pace, the National Association of Realtors said Friday. The median sales price rose 4.8 percent from a year earlier to $277,700.

- The Federal Reserve held rates steady at the conclusion of its policy setting meeting June 19, but committed itself to acting “as appropriate to sustain the expansion.” The Fed elected to keep the benchmark interest rate within its target range of 2.25 percent to 2.5 percent, but new economic projections show more Fed officials seeing the case for a rate cut — or two — by the end of 2020.

- U.S. jobless claims fell more than expected last week, pointing to underlying market strength despite a sharp slowdown in job growth in May. Initial claims for state unemployment benefits dropped 6,000 to a seasonally adjusted 216,000 for the week ended June 15, the Labor Department said on Thursday.

Weaknesses

- A gauge of U.S. factories fell in June to its lowest level since late 2009 and hovered just above the threshold between expansion and contraction. This is just the latest signal that the American industrial sector is losing momentum amid rising uncertainty. The IHS Markit Manufacturing Purchasing Managers’ Index (PMI) slipped to 50.1 from 50.5, according to a preliminary report Friday that trailed most estimates in Bloomberg’s survey of economists. A separate gauge for service providers edged down to a three-year low of 50.7, also falling short of projections.

- A survey of economic conditions in the U.S. was flat in May, suggesting somewhat slower growth in the months ahead. The leading economic index had risen three months in a row before going flat last month. Hiring slowed and U.S. trade talks with China broke down in May, triggering a temporary pullback in stock prices. “While the economic expansion is now entering its 11th year, the longest in U.S. history, the LEI clearly points to a moderation in growth toward 2 percent by year end,” said Ataman Ozyildirim, director of economic research at the Conference Board, publisher of the report.

- Tariffs on Chinese goods have cost U.S. consumers at least $22 billion since the trade war began, according to a report by free-trade group Tariffs Hurt the Heartland. Senator Chuck Grassley’s office has given a similar figure. The estimate doesn’t account for Trump’s latest tariff hikes on $200 billion Chinese goods in May, so the current total is likely to be much higher.

Opportunities

- U.S. inflation expectations are rising after the Fed signaled it’s ready to lower borrowing costs and as oil surges. The five-year breakeven rate—which represents investors’ view on the annual inflation rate through 2024—has rebounded from the lowest level since 2016 as traders bet on a rate cut next month. Driving breakevens higher is the belief that “easing policy would boost growth,” said Gennadiy Goldberg, a strategist at TD Securities. With risk assets and oil rallying, that suggests breakevens “could continue to do well near-term.” Inflation data from the eurozone and the United States next week will be closely watched.

- As heightened trade tensions force central banks around the world to take a dovish turn, the U.S.-China trade talks will be the limelight at the G20 summit in Japan next week. The planned meeting between President Trump and Chinese President Xi will be the highlight of the week as investors will be hoping for a thaw in the strained relations between the two countries.

- Citigroup municipal analysts led by Vikram Rai said that bonds sold to buy natural gas for utilities under long-term contracts may look attractive to investors seeking higher yielding tax-exempt debt. Municipal gas and electric utilities can use the tax-exempt bond market to lock in discounted pricing on a fixed quantity of natural gas over decades. “Municipal investors who buy these bonds can get corporate exposure without the associated volatility. And, in an environment of compressed spreads, the yields offered by these bonds are attractive.”

Threats

- A U.S. business conditions gauge compiled by Morgan Stanley dropped this month by the most on record to the lowest since 2008, adding to recent signs that the world’s largest economy is slowing. Indicators from services to manufacturing and hiring all cooled, dragging the headline index to 13, far below the 33 threshold consistent with positive real economic growth, economists led by Ellen Zentner wrote in a note. “The decline shows a sharp deterioration in sentiment this month that was broad-based across sectors,” they said. Morgan Stanley’s conclusions dovetail with recent data from job growth to inflation that all point to a cooling American economy.

- China trimmed its holdings of U.S. Treasuries to the lowest in almost two years as the months long trade conflict drags on between the world’s two largest economies. China’s portfolio of U.S. Treasury holdings fell by $7.5 billion in April to $1.1 trillion, according to Treasury Department figures released Monday. Importantly, the latest numbers were collected before tensions between Washington and Beijing escalated to a new level in May, when talks collapsed and President Trump raised tariffs on $200 billion of Chinese goods.

- Traders are piling into U.S. debt. The 10-year Treasury yield fell below 2 percent for the first time since 2016 this week, signaling investors are concerned about global economic growth and trade tensions.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was WTI crude oil, which gained 9.77 percent. U.S. crude futures saw their biggest daily gain so far in 2019 on Thursday after Iran shot down an American drone and geopolitical tensions soared even higher. WTI futures rose 5.4 percent on the day. Bloomberg reports that the chances of South Korea buying more U.S. crude rose due to the oil tanker attacks last week in the same region. Additionally, the U.S. Energy Information Administration (EIA) released data that shows gasoline demand hit a record high of 9.93 million barrels per day last week.

- Several other commodities had a great week – copper, gold, palladium and iron, to name a few. After the Fed pivoted and indicated rate cuts are coming, copper traders turned to bullish. The red metal is also up due to a big mine strike at one of Codelco’s properties. Gold broke above $1,400 and palladium saw its biggest weekly gain in 14 months. It actually saw the largest advance of any major metal this year, reports Bloomberg. Lastly, iron ore was up after Rio Tinto Group cut its output guidance and China continues to see depleting stockpiles at its ports. Contracts on iron were up more than 15 percent in the last two weeks.

- Electric vehicle sales in California remained steady in the first quarter of this year despite the removal of the tax credit. Sales were up 31 percent year-over-year with 36,000 vehicles sold.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 8.21 percent. Natural gas futures fell to their lowest seasonal level since 1995 after U.S. stockpiles rose by more than expected, reports Bloomberg. Gas is the second-worst performer for commodities so far this year and the record summer heat is not expected to boost consumption by enough.

- Equinor ASA, a Norwegian energy company, drilled another dry well that has cast doubt on the ability of Norway to develop a new oil province. Bloomberg’s Mikael Holter writes “all four wells drilled in Norway’s most-recently opened exploration region have now either been dry or failed to find sufficient resources for a commercial development.”

- Solar installer and wind-turbine technician are two of the fastest growing professions in the U.S. as more clean energy projects are being developed. However, there’s a big lack of gender diversity in this growing green workforce. In fact, diversity in renewable energy is worse than the fossil fuel industry, reports Bloomberg.

Opportunities

- Anadarko sees potential for Mozambique to become one of the largest LNG suppliers in the world, as the company approved a $25 billion project in the African nation, reports Bloomberg. Company CEO Al Walker said that over time the project will double the nation’s GDP.

- In green energy news, BloombergNEF predicts that nearly half of the world’s electricity will come from wind and solar by 2050. New York State passed the most aggressive clean energy target in the nation that seeks to significantly boost solar and wind capacity. GM is considering bringing the Hummer back to life by creating an electric version of the gas-guzzler, according to sources familiar with the matter.

- Japan’s largest producer of nickel, Sumitomo Metal Mining Co., says that the nickel market is facing a deficit of 51,000 tons this year due to China’s growing stainless steel output, reports Bloomberg. The estimate is wider than an earlier one of 35,000 tons.

Threats

- Geopolitical tensions continue to grow between Iran and the U.S. An American drone was shot down by Iran early this week then a retaliatory airstrike was called off last minute against Iran. Some airlines have announced that they will avoid flying over Iranian airspace in response. This is a threat to oil as the region is a major transit point.

- A spokesperson for the National Development and Reform Commission in China said in a briefing this week that new policies on rare earth metals will be implemented to ensure maximum advantage is taken of the value of the strategic minerals. This could lead to China dominating even further the production of rare earths.

- Russia’s Druzhba pipeline is being halted again due to Poland finding the Russian oil to contain organic chlorides, which can damage refineries. After an initial contamination incident in April, Russian pipeline operator Transneft PJSC had hoped to fully resolve the crisis by July 1. However, the restoration of full pipeline flows could be delayed after the second incident this week.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 3.6 percent. Equites trading on the Istanbul exchanged rose after the U.S. Federal Reserve announced its readiness to cut rates. Turkey is a highly dollar-indebted country, and the prospect of lower rates creates positive sentiment among investors.

- The Russian ruble was the best performing currency this week, gaining 2.3 percent against the dollar. The ruble appreciated with the price of Brent crude oil, which has gained 7 percent in the past five days.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1 percent. Banks lost 7.5 percent in the past five days, after gaining 35 percent in just one month.

- The Hungarian forint was the worst relative performing currency this week, gaining 83 basis points against the dollar. All emerging Europe currencies gained this week due to the dovish Federal Reserve tone, with the forint gaining less than others, as Hungary’s central bank is set to keep loose financial conditions at a meeting next week.

- Materials was the worst performing sector among eastern European markets this week.

Opportunities

- A day before the Fed decision in the U.S, the European Central Bank (ECB) announced its readiness for future rate cuts and renewed quantitative easing programs if needed. On Wednesday the Fed kept its rates unchanged, but also indicated that is ready to use its policy tools to support economic growth if needed. Central banks around the globe are ready to support growth, which usually translates into higher stock prices.

- Preliminary June PMI readings improved slightly in Europe. French and German manufacturing showed a positive surprise. Germany’s composite PMI stayed at 52.6 in June. France’s PMI rose to 52.9, up from from 51.2 a month ago. Manufacturing PMI for the euro area improved, but remains below the 50 level that separates growth from contraction. However, the Eurozone Composite PMI is above the 50 level, supported by continued strength in Service PMI.

- Russia is on the list of the top 25 countries that are attractive for digital economy exports, as the nation is currently undergoing planned digitalization, according to a joint study by BCG and The Network. Russian digital exports working in Germany may consider moving back home as both countries fight over programmers.

Threats

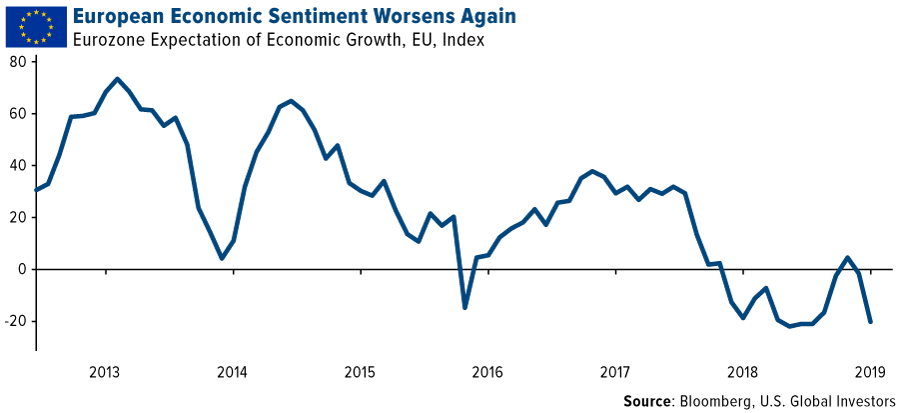

- Economic expectations in the eurozone fell into negative territory again after a short- lived bounce. The ZEW Indicator of Economic Sentiment for the euro area fell to -20.2 in June, down from -1.6 in the prior month. The biggest drop was in Germany, Europe’s largest economy, which is highly sensitive to the ongoing trade tensions and industrial production slowdown.

- The dovish market mood drove more countries’ bond yields below the inflation rate. In central Europe, Poland is the latest victim with the yield on 10-years bonds dropping below the inflation rate. Only Romania and Russia have positive real rates in Eastern Europe.

- Turkish equites may see a correction in the short term due to domestic and international politics. This weekend Turkey will repeat municipal elections in Istanbul and the expectation is that President Erdogan’s AKP party will lose again. Moody’s downgraded 18 Turkish banks, citing high reliance on short-term funding in foreign currencies. The U.S. is also preparing sanctions against Turkey over its purchase of S-400 defense systems from Russia.

China Region

Strengths

- The best performing indices in the region for the week were China’s Shanghai Composite, which jumped 4.49 percent in total return, and Hong Kong’s Hang Seng Composite, which gained 4.37 percent for the week.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index since last Friday was information technology, which surged 6.33 percent, nudging out energy, which jumped to a close second on a 6.29 percent gain.

- Singapore’s non-oil domestic exports beat expectations both month-over-month (mom) and year-over-year (yoy), as mom numbers for May were up some 6.2 percent—better than 5.5 percent expected—while yoy numbers were only down 15.9 percent, ahead of an expected drop of 16.5 percent.

Weaknesses

- The worst-performing indices in the region for the week were India’s NIFTY and SENSEX indices, which declined by 75 and 55 basis points, respectively, while the rest of the region finished up in the green.

- The poorest-performing sector in Hong Kong’s Hang Seng Composite Index this week was, perhaps understandably in a risk-on week, utilities, which climbed a mere 0.46 percent.

- Overseas remittances to the Philippines were lighter than expected for the year-over-year April reading, rising only 4.0 percent, shy of expectations for a 4.6 percent rate and down from the prior reading of 6.6 percent growth.

Opportunities

- The U.S.-China trade war saga continues with a slightly more optimistic note heading into confirmation of an upcoming G20 sit-down between Presidents Trump and Xi and confirmation of lower level talks preceding the meeting. There remain significant obstacles—from strategic geopolitics and economics down to published whitepapers, off-the-cuff comments, and even possibly individual tweets at times—but there nonetheless remains a possibility that the U.S. and China work out some sort of understanding or arrangement that may lead to a more positive market outlook. President Trump has said he’ll make up his mind on tariffs post-G20 next weekend, and with talks supposedly set to start up again heading into the talks, it may be a week of posturing, leaks, and headlines, but there may also be some possible upside on the flipside if the G20 meeting is productive and convincing. Time will tell, and again, the results may be more binary than some would hope (or perhaps not—who knows?), but due to the massive size of the American and Chinese economies and the reverberating sentiment that may surround any deal or lack thereof it seems well worth the while to consider talks and a G20 meeting a reason for at least some possible opportunity.

- As China’s Xi Jinping finished a state visit with North Korea’s Kim Jong Un, President Xi remarked that he wanted to play a “positive and constructive role” in denuclearization of the Korean Peninsula, and, according to press reports citing Xinhua News, President Xi also notably stated that, “The international community hopes that talks between the DPRK and the United States will move forward and bear fruit.”

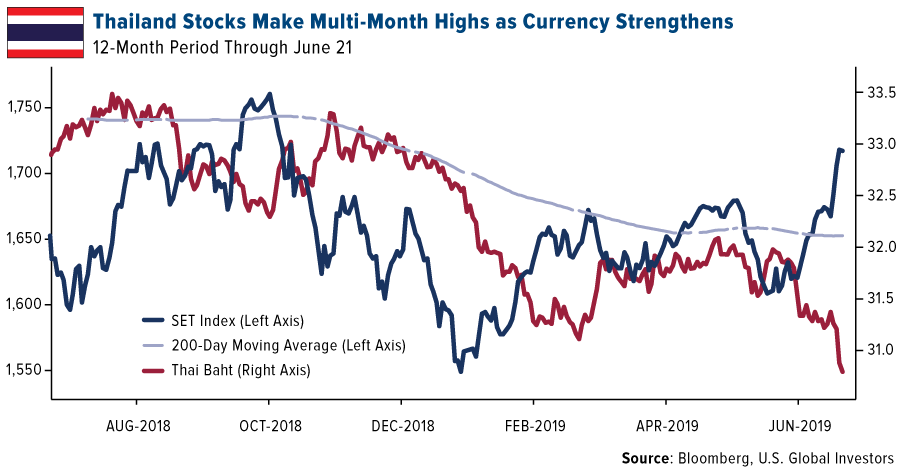

- Thailand’s SET Index jumped to multi-month highs over the last few trading days even as the baht has continued to strengthen (fall).

Threats

- The threat of U.S.-China trade war escalation must remain a threat until resolved with more certainty. To be sure, at the moment there seems to be some optimism about the upcoming G20 summit, or the possibility of delays in implementation of tariffs, and so forth, but at the end of the day this just punts on the central issues and could extend uncertainty. Of course, if there is full or partial resolution, that is a positive, but this trade war has already dragged on over two different calendar years—will it likely be solved in a single sit-down all of a sudden? All progress is useful, but any steps backward thereafter or escalation would be a negative, for sure.

- The Hong Kong protesters continue to stand up not only to the controversial extradition bill (which has been “suspended” but which many want dead and fully off the table) but also to Carrie Lam, the CEO of the Hong Kong SAR, as some of the vocal protesters demand—but have not received—her resignation. All of this also ratchets up pressure on China’s Xi Jinping, who faces a delicate balance between a slowing domestic economy, high profile trade war confrontation from the U.S. and President Donald Trump, and HK’s democratic defiance. Bear in mind that President Xi has also assumed the most concentration of power in decades in China, which means that when everything’s going well, he looks really good, but when things are going less well, it’s presumably harder to pass the blame. All eyes will be on the upcoming G20 meeting.

- Goldman Sachs reportedly offered to pay some $241 million to settle the 1MDB scandal, a recent Bloomberg News article reports Malaysian PM Mahathir Mohamad as saying, but the PM called the amount “little” compared to what would be “reasonable” in his mind. His number? More like some $593 million at least, which the bank supposedly made on the 1MDB debt sales. While the two sides do indeed sound closer to some kind of settlement, the numbers are big and still reasonably far apart.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 21 was MSD, up 396.47 percent.

- Over the weekend, bitcoin rose above $9,000, reports CoinDesk, taking cumulative year-to-date gains to more than 150 percent. On Sunday, the leading crypto by market value clocked a 13-month high of $9,391 on Bitstamp.

- An open banking platform, Token, says it raised $16.5 million in funding from big tech firms. Token has recently partnered with Mastercard and says the partnership represents “the first movement in open banking by a large infrastructure provider”, reports CoinDesk.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 21 was Jewel, down 65.02 percent.

- Bitmain is suing three former employees who started a rival mining pool known as Poolin, reports CoinDesk. Poolin co-founders allegedly violated their non-complete agreements and now Bitmain is seeking $4 million in damages.

- In a report released on Wednesday from Ernst & Young, the firm alleges that the late founder of QuadrigaCX, Gerald Cotton, transferred millions in crypto out of customer accounts and into other exchanges in order to finance his personal lifestyle. CoinDesk reports that Cotton stole around $200 million from his customers.

Opportunities

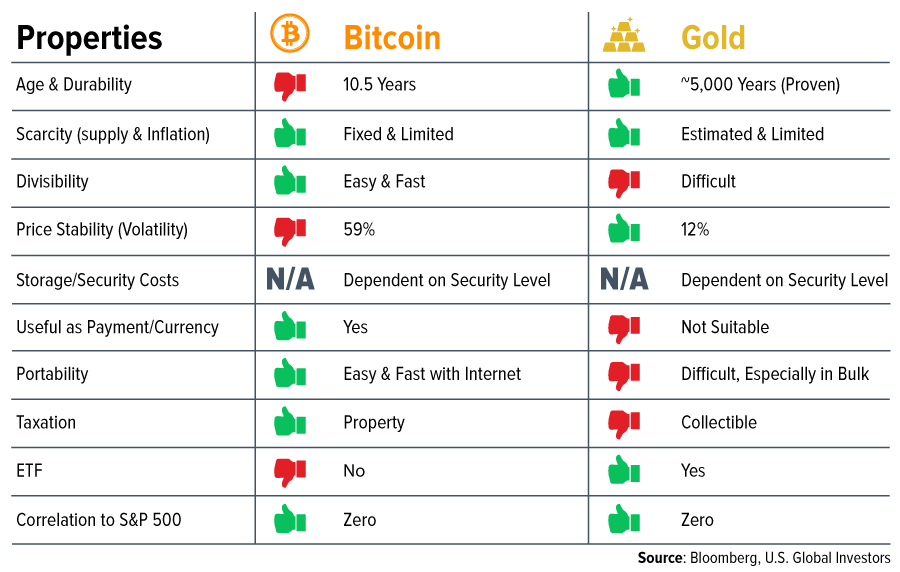

- Rather than positioning bitcoin and gold as polar alternative assets, Bloomberg analyst Morgan Barna believes they can complement each other in a portfolio. “Bitcoin is more transportable and divisible, and more applicable as a currency,” Barna reasons. “But gold is more stable, with a proven track record.” Both offer almost zero correlation to traditional asset classes.

- Both Microsoft and Salesforce are among the eight new members announced on Tuesday to have joined the Hyperledger blockchain consortium, reports CoinDesk. These companies will pay dues based on their size to Hyperledger, the article explains, an umbrella project for various business blockchains run by the Linux Foundation, and will build applications using the software.

- An increasing supply in the broader cryptocurrency market is favoring bitcoin, writes Bloomberg’s Mike McGlone. Bitcoin doesn’t have a supply overhang, he explains, allowing it to gain status as a digital version of gold with limited supply.

Threats

- Facebook is preparing to introduce its Libra currency, as many news outlets have reported, and released a paper outlining the venture on Tuesday. While this cryptocurrency could be worth billions, Bloomberg reporter Lionel Laurent explains that it also poses a double threat. Mark Zuckerberg’s new digital asset may strengthen his stranglehold on our user data, Laurent’s says. In addition, it could pose a threat to financial stability.

- Binance, one of the top cryptocurrency exchanges, pre-announced a soon-to-come $81 million or so bitcoin transaction on Twitter, reports Bloomberg. In the tweet, the company notes “no need to FUD” – which essentially means no need to fear. “That’s atypical,” said David Tawil of ProChain Capital speaking about the broadcast. “With Binance (along with the entire industry) looking toward regulatory compliance and SEC approval, I’m not sure if this announcement was the smartest thing.”

- The V20 Summit is coming up next week where representatives from various countries will asses the course of new legal action proposed by the international Financial Action Task Force (FATF). While regulation of cryptos is positive, there could be too much regulation. “What we are hearing from industry is that the new rules may have the opposite effect to which they were intended, effectively forcing crypto transactions off the controlled platforms, which are currently one of the best avenues we have in gaining visibility over financial crime,” said Roger Wilkins, FTAF ex-president.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 205.10 | +5.69 | +2.85% |

| Gold Futures | 1,344.60 | -1.50 | -0.11% |

| Natural Gas Futures | 2.39 | +0.05 | +2.27% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -9.57 | -1.60% |

| 10-Yr Treasury Bond | 2.09 | +0.00 | +0.10% |

| Nasdaq | 7,796.66 | +54.56 | +0.70% |

| Oil Futures | 52.53 | -1.46 | -2.70% |

| Hang Seng Composite Index | 3,620.02 | +26.25 | +0.73% |

| S&P 500 | 2,887.01 | +13.67 | +0.48% |

| DJIA | 26,089.61 | +105.67 | +0.41% |

| Korean KOSPI Index | 2,095.41 | +23.08 | +1.11% |

| Russell 2000 | 1,522.44 | +8.05 | +0.53% |

| S&P Energy | 447.48 | -2.21 | -0.49% |

| S&P Basic Materials | 360.98 | +1.78 | +0.50% |

| XAU | 75.81 | +1.48 | +1.99% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.21 | -8.11% |

| S&P/TSX Global Gold Index | 205.10 | +22.96 | +12.61% |

| 10-Yr Treasury Bond | 2.09 | -0.29 | -12.17% |

| Oil Futures | 52.53 | -9.49 | -15.30% |

| Gold Futures | 1,344.60 | +40.90 | +3.14% |

| S&P 500 | 2,887.01 | +36.05 | +1.26% |

| S&P Energy | 447.48 | -23.94 | -5.08% |

| Hang Seng Composite Index | 3,620.02 | -150.49 | -3.99% |

| DJIA | 26,089.61 | +441.59 | +1.72% |

| Korean KOSPI Index | 2,095.41 | +2.63 | +0.13% |

| Nasdaq | 7,796.66 | -25.49 | -0.33% |

| S&P Basic Materials | 360.98 | +21.80 | +6.43% |

| Russell 2000 | 1,522.44 | -25.83 | -1.67% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -20.57 | -3.39% |

| XAU | 75.81 | +7.51 | +11.00% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.47 | -16.29% |

| 10-Yr Treasury Bond | 2.09 | -0.55 | -20.75% |

| DJIA | 26,089.61 | +379.67 | +1.48% |

| Oil Futures | 52.53 | -6.08 | -10.37% |

| S&P 500 | 2,887.01 | +78.53 | +2.80% |

| Gold Futures | 1,344.60 | +37.00 | +2.83% |

| S&P Energy | 447.48 | -37.76 | -7.78% |

| Nasdaq | 7,796.66 | +165.75 | +2.17% |

| Korean KOSPI Index | 2,095.41 | -60.27 | -2.80% |

| S&P Basic Materials | 360.98 | +14.33 | +4.13% |

| Russell 2000 | 1,522.44 | -27.19 | -1.75% |

| Hang Seng Composite Index | 3,620.02 | -238.07 | -6.17% |

| S&P/TSX Global Gold Index | 205.10 | +12.28 | +6.37% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -36.10 | -5.79% |

| XAU | 75.81 | +0.48 | +0.64% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Coeur Mining Inc.

Yamana Gold Inc.

Hecla Mining Co.

IAMGOLD Corp.

Gold Fields Ltd

Barrick Gold Corp

Acacia Mining Plc

Equinor ASA

The Boeing Co.

Deutsche Lufthansa AG

Broadcom Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The FTSE Gold Mines Index Series encompasses all gold mining companies that have a sustainable and attributable gold production of at least 300,000 ounces a year, and that derive 75% or more of their revenue from mined gold. The Bloomberg Barclays Global Aggregate Negative Yielding Debt Market Value Index measures the stock of debt with yields below zero issued by governments, companies and mortgage providers around the world which are members of the Bloomberg Barclays Global Aggregate Bond Index. The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables. The Empire State Manufacturing Index rates the relative level of general business conditions New York state. A level above 0.0 indicates improving conditions, below indicates worsening conditions. The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. Sensex, otherwise known as the S&P BSE Sensex index, is the benchmark index of the Bombay Stock Exchange (BSE) in India. A basis point is one hundredth of one percent, used chiefly in expressing differences of interest rates. The SET Index is a Thai composite stock market indexwhich is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year.