Gold Glimmers as the Pool of Negative-Yielding Debt Surges

Date Posted: March 15, 2019

Read time: 55 min

Low to negative-yielding debt has historically been constructive for gold prices. The yellow metal doesn'thave a yield, but in the past it's been a tried-and-true store of value when other safe haven assets...

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

It’s been a tragic week, to say the least. It began with a fluke Ethiopian Airlines crash, which led to the grounding of all Boeing 737 MAX 8 jets worldwide, and ended with a hateful terrorist attack in Christchurch, New Zealand. On behalf of everyone at U.S. Global Investors, I want to extend my deepest sympathies to all those who were affected.

I’ll have more to say on airlines in a moment.

For now, I want to share with you a tweet by Lisa Abramowicz, a reporter for Bloomberg Radio and TV who often comments on the “fear” market.

“The pool of negative yielding debt has risen to a new post-2017 high of $9.2 trillion,” she writes. “Mind boggling at a time when the global economy is supposedly still recovering.”

Since Lisa tweeted this on Wednesday, the value of negative-yielding bonds has ticked up even more, to $9.32 trillion. This is still below the 2016 high of $12.2 trillion, but, as Lisa said, mind-boggling nonetheless. It also indicates that investors fear global economic growth is slowing.

The yield on Japan’s 10-year government bond is back in negative territory, trading at negative 3 basis points (bps) today, while Germany’s was trading at a low, low 8 bps.

As I’ve explained to you before, low to negative-yielding debt has historically been constructive for gold prices. The yellow metal doesn’t have a yield, but in the past it’s been a tried-and-true store of value when other safe haven assets, such as government bonds, stopped paying you anything. In the case of Japanese bonds right now, investors are actually paying the government—and that’s before you factor in inflation.

This is just one of many reasons why I recommend a 10 percent weighting in gold, with 5 percent in physical bullion and jewelry, the other 5 percent in high-quality gold stocks and funds. Remember to rebalance at least once a year.

For more on gold, watch my interview this week with Daniela Cambone, live from Kitco’s New York studio! Click here!

Aircraft Are Safer, Easier to Fly

Back to the Ethiopian flight. I’m confident we’ll soon learn what malfunctioned in the 737 MAX—both this week and in October during Indonesia’s Lion Air flight—so that accidents like this may never happen again.

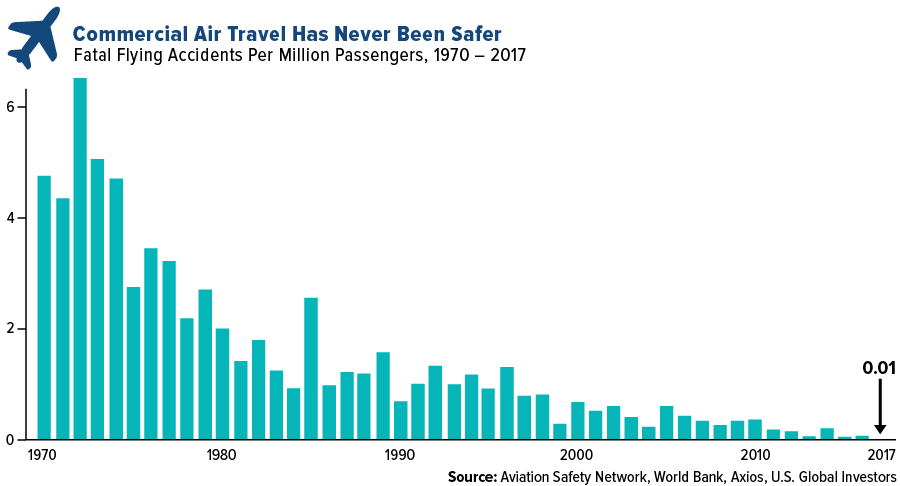

Having said that, I think it’s important to keep in mind that commercial air travel today has never been safer in its approximately 100-year history. In 2017, the safest year for aviation on record, not a single life was lost in a commercial plane crash, despite more than 4 billion people around the world taking to the skies on scheduled passenger flights. You would be hard-pressed to find another major global industry, one that operates 24/7, with such an impressive safety track record.

This is all largely thanks to continuous improvements in aviation technology. Over the decades, aircraft have progressively gotten safer and easier to fly, according to one aeronautics professor at MIT.

“The automation systems that we have on airplanes have demonstrably made airplanes safer,” R. John Hansman, director of MIT’s International Center for Air Transportation, told Boston’s WBUR radio station this week.

And the technological advancements continue today, with artificial intelligence (AI) and the internet of things (IoT) already starting to change the way we fly.

Consider Aireon. Founded in 2011, the aerospace tech firm is responsible for developing a next-generation airline tracking and surveillance system that has the capacity to measure every aircraft’s speed, heading, altitude and position—all in real-time. Using as many as 66 satellites, Aireon’s team gathers data broadcast by tiny transponders, which all U.S. and European planes will be required to carry by next year.

It was the company’s data, in fact, that ultimately convinced the Federal Aviation Administration (FAA) to join the rest of the world in temporarily grounding the 737 MAX.

“Take a Ride on the Airline Stocks,” Writes the National Bank of Canada

In light of the accident, a number of research houses and brokerage firms released notes to investors this week reassuring them that Boeing’s troubles should have only minimal impact on the airline industry as a whole.

Shares of Boeing, the largest company in the Dow Jones Industrial Average by market cap, surged as much as 2.5 percent today after it was announced that the jet manufacturer plans to roll out a software update for the MAX 8 and 9 within the next 10 days—much sooner than initially expected.

Analysts at Raymond James point out that the “737 MAX 8/9 aircraft are still a small part of overall fleet for most U.S. airlines, which in off-peak travel season can likely be covered by higher utilization of existing fleet or delays in certain aircraft retirements.”

Vertical Research’s Darryl Genovesi, an expert in airline revenue, says that he believes the 737 MAX grounding will have an “immaterial” effect on U.S. airlines’ first-quarter earnings per share (EPS). And if the grounding is extended into the second quarter, or into the second half of the year, we may even see higher EPS due to a supply demand imbalance.

Genovesi writes that Vertical’s models indicate that, in the event of an extended grounding, “system RASM [revenue per available seat mile] would increase by ~200 bps… This would be ~3 percent accretive to second-quarter EPS, on average, across the group including a ~9 percent EPS boost for Alaska Airlines, JetBlue and Spirit Airlines and low-single-digit boost for American Airlines, Delta Air Lines, United Continental and Allegiant Air, partially offset by a low-single-digit EPS reduction for Southwest Airlines.”

Southwest has the largest number of 737 MAX 8s in the world, with a reported 34 planes in its fleet.

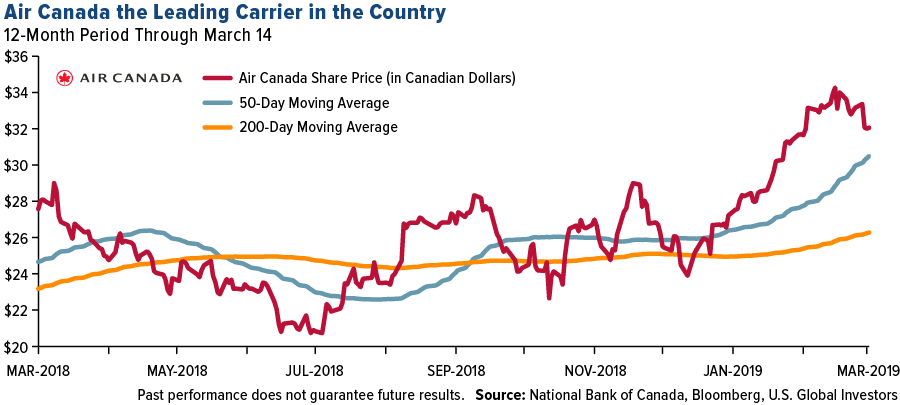

Finally, looking at the Canadian market, the National Bank of Canada says that both Air Canada and WestJet Airlines “remain constructive despite the recent turbulence.”

“The negative news has not changed the overall positive trend in [Air Canada’s] stock,” analyst Dennis Mark writes.

Got FOMO (fear of missing out)? For the latest expert commentary on commodities and capital markets, be sure to subscribe to U.S. Global Investors’ YouTube page by clicking here!

Gold Market

This week spot gold closed at $1,302.43, up $4.03 per ounce, or 0.1 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.31 percent. The S&P/TSX Venture Index came in up 1.57 percent. The U.S. Trade-Weighted Dollar fell 0.77 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-12 | CPI YoY | 1.6% | 1.5% | 1.6% |

| Mar-13 | PPI Final Demand YoY | 1.9% | 1.9% | 2.0% |

| Mar-13 | Durable Goods Orders | -0.4% | 0.4% | 1.3% |

| Mar-14 | Germany CPI YoY | 1.6% | 1.5% | 1.5% |

| Mar-14 | Initial Jobless Claims | 225k | 229k | 223k |

| Mar-14 | New Home Sales | 662k | 607k | 652k |

| Mar-15 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Mar-19 | ZEW Survey Current Situation | 13.0 | — | 15.0 |

| Mar-19 | ZEW Survey Expectations | -11.0 | — | -13.4 |

| Mar-19 | Durable Goods Orders | — | — | 0.4% |

| Mar-20 | FOMC Rate Decision (Upper Bound) | 2.5% | — | 2.5% |

| Mar-21 | Initial Jobless Claims | 225k | — | 223k |

Strengths

- The best performing metal this week was palladium, up 2.42 percent, despite speculators cutting their bullish view to a four-month low. Gold traders were bullish this week, after two weeks of being neutral on the outlook for the yellow metal, on the expectation that central bank policies will help spur demand, according to the weekly Bloomberg survey. Gold climbed back above the $1,300 per ounce level this week as the dollar retreated. Investors also considered the risks of the ongoing trade war and Britain’s imminent departure from the European Union (EU). Commodity ETFs recovered their losses from last week with inflows of $177 million for the week ended March 14. Bloomberg data shows that precious metals funds had inflows of $270 million versus $732 of outflows last week.

- According to India’s Association of Gold Refineries & Mints, 2019 gold dore imports are seen at 280 tons, versus 260 tons a year ago. Bloomberg reports that the country’s 23 refineries are increasingly buying dore from overseas supplies such as Ghana, Peru, Brazil and Bolivia. Gold prices also rose in India this week on the news of increased jewelry demand.

- The $12 million retirement package for outgoing Goldcorp chairman Ian Telfer is at the center of the mega merger between Newmont and Goldcorp. Several industry players have expressed their discontent and even outrage about the payment, as Goldcorp performance has been poor since Telfer joined the management team three years ago. Although the deal will likely go through, it is positive to see strong backlash from this big payout, as it is not in the best interests of shareholders.

Weaknesses

- The worst performing metal this week was silver, down just 0.33 percent, as money managers cut their bullish view to an 11-week low. Turkey’s gold reserves fell from the previous week in a continued pattern of selling reserves. Central bank holdings were down $536 million from the prior week, according to data as of March 8. The nation’s reserves are down 19 percent year-over-year.

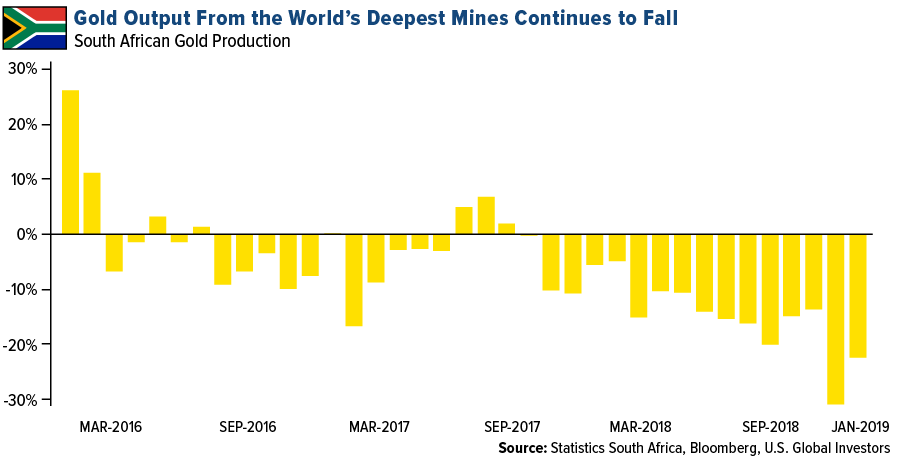

- South Africa, once the world’s top producer, just experienced its 16th straight month of falling gold output. The nation’s output declined 22.5 percent from a year earlier, compared with a 31 percent drop in December, according to Statistics South Africa. The nation is also struggling with rising electricity costs. This week the nation’s energy regulator said that Eskom Holdings can raise prices by 9.4 percent by April 1, taking the total increase to 13.8 percent, reports Bloomberg. This electricity increase adds to miners’ already rising costs.

- In other news on South Africa’s Eskom, Citi Research analysts said in a note this week that “Eskom has run out of positive catalysts” and that they believe “it is an optimal moment to enter a short.” Goldman Sachs calls the company the “biggest single threat to South Africa’s economy.” The nation’s construction industry is also struggling. Group Five’s stock was suspended on Tuesday after 45 years of trading due to its filing for bankruptcy protection. Bloomberg’s Janice Kew writes that “the current mix of a depressed South African economy, high levels of national debt and low infrastructure spending is proving toxic as contracts dry up.”

Opportunities

- Jim Gallagher, CEO of North American Palladium, says that palladium cannot be replaced with platinum in gasoline-fueled cars. Palladium has unique chemical properties that make it a better choice for use in vehicle pollution-control devices than platinum, writes Bloomberg. This is positive for the precious metal, which has surged 22 percent so far this year as manufactures scramble to get their hands on it. Fiat Chrysler is recalling almost 862,520 gasoline-fueled vehicles and replacing the catalytic converters on all of those would require an additional 77,000 ounces of palladium, which could further contribute to a supply shock. Citigroup predicts that consumption of palladium will trail production by 545,000 ounces this year.

- Barrick and Newmont Mining entered into a historic joint venture at their operations in Nevada that will unlock $5 billion in synergies. In a statement released this week, Barrick CEO Mark Bristow said that “we listened to our shareholders and agreed with them that this was the best way to realize the enormous potential of the Nevada goldfields.” The joint Nevada operations will create the world’s single largest gold producer. Catherine Raw will run the joint venture and continue on as the chief operating officer of Barrick’s North American business.

- Newcrest Mining, the third largest gold producer by market value, agreed to a $806.5 million deal to acquire a 70 percent joint-venture interest on a copper and gold mine owned by Imperial Metals in British Colombia, reports Bloomberg. Newcrest chief executive Sandeep Biswas said that the company’s balance sheet did not restrict it from further purchases after the deal, signaling that more M&A activity should continue in the space.

Threats

- Inflation sentiment won’t be running on fumes any longer, writes Bloomberg’s Carl Riccadonna, in part due to crude oil being up 27 percent year-to-date and further price appreciation appearing likely. There is a 92 percent correlation between gasoline prices and year-ahead inflation expectations, which signals that rising crude should lift inflation. Riccadonna writes that heightened anxiety about inflation at the end of last year might have been overdone, as the drop in gas prices exceeded the usual seasonal decrease.

- The gold price increase could be stymied by positive data, according to Tapan Patel, senior analyst at India’s most valuable bank, HDFC Bank. Patel said “things look to be settling down” and that “we can expect the risk appetite to come down and see investors shifting to the dollar from gold.” The bank forecasts that gold will trade between $1,240 and $1,380 an ounce this year.

- The Commodity Research Bureau’s Raw Industrials Index has failed to match the post-Christmas rise in stocks and junk bonds. Bloomberg writes that the stall in the gauge signals that the rally in risk assets might have gone too far. According to strategists at Morgan Stanley, the stalling gauge has led to turning points in risks assets in recent years.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.57 percent. The S&P 500 Stock Index rose 2.89 percent, while the Nasdaq Composite climbed 3.78 percent. The Russell 2000 small capitalization index gained 2.08 percent this week.

- The Hang Seng Composite gained 2.29 percent this week; while Taiwan was up 1.93 percent and the KOSPI rose 1.81 percent.

- The 10-year Treasury bond yield fell 4 basis points to 2.592 percent.

Domestic Equity Market

Strengths

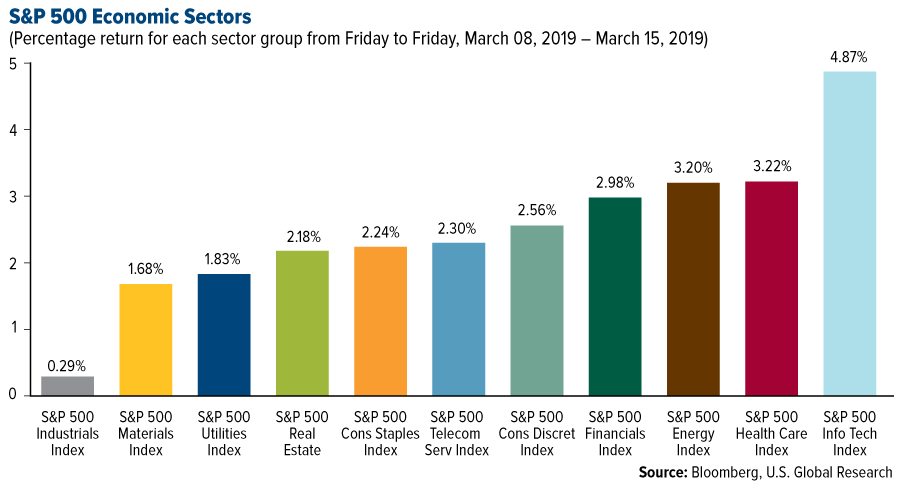

- Information technology was the best performing sector of the week, increasing by 4.87 percent versus an overall increase of 2.82 percent for the S&P 500.

- Nvidia was the best performing stock for the week, increasing 12.73 percent.

- Shares of Ulta Beauty rose this week after beating quarterly estimates, reports TheStreet.com. The cosmetics retailer saw its stock go up 8.68 percent to $339.65 a share in late morning trading Friday, an all-time high. Earnings per share for the fourth quarter were $3.61, beating estimates of $3.56. Per-share earnings rose 31 percent from a year earlier and revenue was $2.12 billion, beating analysts’ estimates of $2.11 billion, the article continues.

Weaknesses

- Industrials was the worst performing sector for the week, increasing by 0.29 percent versus an overall increase of 2.82 percent for the S&P 500.

- Boeing was the worst performing stock for the week, falling 10.31 percent.

- Boeing’s stock fell sharply throughout the week following the tragic Ethiopian Airlines plane crash on Sunday that killed 157 passengers and crew on board. The company’s stock fell further as more nations and airlines grounded its 737 MAX 8 planes. Over the past two days, shares fell over 11 percent.

Opportunities

- Investors who have shunned risky assets since Christmas better start embracing them, according to JPMorgan Chase strategists led by Marko Kolanovic. The firm advised clients to boost holdings in commodities while cutting exposure to safer assets such as government bonds, writes Bloomberg. “A U.S.-China trade agreement appears likely and major central banks around the world have adopted a more dovish stance, all setting the stage for an economic rebound in the second half of 2019,” the team said.

- BMO’s Matthew Luchini says Gilead Sciences is a “buy,” citing its HIV franchise that "should be dominant for at least the next several years."

- Semiconductor stocks gained after Broadcom called for a bottom in the semi business in the second quarter, reports Seeking Alpha. In addition, Lam Research received a Citi target bump from $177 to $215, citing a recent pickup in NAND equipment orders, the article continues.

Threats

- Massachusetts Senator Elizabeth Warren has proposed a plan to break up some of the leading technology companies, reports Business Insider. This would include names like Amazon, Google and Facebook. The Democratic 2020 presidential candidate argues that massive tech mergers smother competition and undermine democracy.

- Facebook is reportedly under criminal investigation over data-sharing deals, reports Business Insider. Deals that gave Apple, Amazon and other companies access to user data that included things like friends lists, contact information and even private messages – many times without the users’ consent.

- A former employee at Tesla has filed a whistleblower tip with the SEC claiming that the company hacked employee cellphones and computers, according to Meissner Associates. The new tip also claims that a proposal to take Tesla private in 2018 was discussed and viewed with skepticism by "many" Tesla employees before CEO Elon Musk tweeted about it in August.

The Economy and Bond Market

Strengths

- Orders for durable goods rose in January for the third month in a row, and business investment posted the biggest increase since last summer, indicating a key segment of the economy is still expanding at a steady pace. Orders rose 0.4 percent in January, according to a government report delayed because of the partial federal shutdown earlier this year. Economists surveyed by MarketWatch had forecast a 0.1 percent decline.

- Consumer sentiment had a further bounce in March, according to the University of Michigan index released Friday. The index jumped to 97.8 in March from 98.3 in the prior month. Economists polled by MarketWatch forecast a 95 reading. This is the second straight month of improving sentiment after the index fell to 91.2 in January.

- In a report that was late due to the recent government shutdown, the U.S. Commerce Department on Monday said that core retail sales rose 0.2 percent in January from December. Economists expected growth to stay flat.

Weaknesses

- Industrial production edged up 0.1 percent in February, the Federal Reserve reported Friday. The gain was below Wall Street expectations of a 0.4 percent rebound after a sharp drop in the prior month.

- Sales of new U.S. homes slumped 6.9 percent in January, a possible sign that buyers paused during the government shutdown. The Commerce Department says that new homes sold at a seasonally adjusted annual rate of 607,000 in January, down from 652,000 in December. The partial government shutdown during January as well as a battered stock market appears to have hurt sales, even as lower mortgage rates eased affordability pressures and boosted buyer interest.

- The number of Americans filing applications for unemployment benefits increased more than expected last week, suggesting the labor market was slowing, but probably not to the extent implied by a near-stall in job growth in February. Initial claims for state unemployment benefits rose 6,000 to a seasonally adjusted 229,000 for the week ended March 9, the Labor Department said on Thursday.

Opportunities

- Some of the most interest-rate-sensitive U.S. stocks are signaling that bond yields won’t move up any time soon, according to Renaissance Macro Research. The firm compared a ratio of bank and utility stocks within the S&P 1500 Composite Index, with the yield on 10-year Treasury notes. The ratio peaked in March of last year and then dropped 28 percent through Tuesday. “We’re not banking on higher yields,” Renaissance wrote.

- According to Bloomberg Economics, for the first time in years, the U.S. is entering its key spring house-hunting season with buyers holding the upper hand. Nowhere is the shift more pronounced than in once-hot areas such as Seattle, San Francisco and Denver, where bidding wars are vanishing, time-on-market is climbing and prices are flattening, or even falling. Western cities, the center of the recent housing boom, are now leading the slowdown.

- In a note to clients, the division of municipal investments at BlackRock said it favors the shortest and longest dated municipal securities. “We favor a long duration stance with respect to municipal bond positioning, employing a barbell yield curve strategy with concentrations in maturities of 0-2 and 20+ years,” analysts said.

Threats

- Federal Reserve Chairman Jerome Powell says America’s workforce faces serious challenges, writes Bloomberg News’ Jeanna Smialek. Education levels are climbing only slowly, and both globalization and drug addiction are taking a toll on the labor market. “When you have people who are not taking part in the economic life of a country in a meaningful way, who don’t have the skills and aptitudes to play a role or who are not doing so because they’re addicted to drugs, or in jail, then in a sense they are being left behind,” Powell told CBS News’ “60 Minutes” in an interview.

- The main tax revenue for U.S. states declined by an average of almost 2 percent during the last three months of 2018 from the same quarter a year earlier, according to preliminary data from the Urban Institute, marking the first drop since the second quarter of 2016. The steeper-than-expected drop threatens to leave some states facing budget shortfalls in the current fiscal year, which ends in June for most governments.

- DoubleLine Capital’s Jeffrey Gundlach criticized President Donald Trump for the “shocking” growth in the U.S. debt burden. The Los Angeles-based fund manager noted in a webcast Tuesday the “incredible increase” in corporate and government debt, with federal deficits only poised to grow. He spoke a month after the Treasury Department said total U.S. public debt had climbed to a record above $22 trillion. “This is something that is getting more and more attention, and I think it has to,” said Gundlach, the firm’s chief investment officer. “It’s really shocking that the president ran on the promise of eliminating the national debt, and here it is at $22 trillion and going higher by about $1.5 trillion a year in a growing economy.” The budget deficit could hit 11 percent of gross domestic product (GDP) in the next downturn "and I’ll take the over" said Gundlach, who suggested 13 percent is more likely.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was wheat, which gained 6.82 percent on short covering following five weeks of losses. Oil is set for a weekly gain as OPEC members and allies are scheduled to meet this weekend to discuss extending their pledged output curbs to avert a global glut, reports Bloomberg. New York futures traded near a four-month high at the end of the week and are on course for a 4.4 percent weekly advance. The International Energy Agency (IEA) said that OPEC nations are able to offset the supply shock from the crisis in Venezuela that has seen the nation sharply cut oil production. Goldman Sachs analysts said in a report Thursday that Brent crude is poised to rise above $70 per barrel after reaching its peak forecast of $67.50 three months earlier than expected.

- The base metals to watch this week were zinc, nickel and iron – all due in part to supply concerns. Zinc rose to an eight-month high this week as the market began 2019 already in deficit and the world’s second-largest producer of the metal is considering bankruptcy. Nickel stockpiles fell for a 15th day on Tuesday and the metal is already up 23 percent so far this year. The global iron ore market is set to face a 12 million ton deficit this year as top producer Vale will likely not be able to make up for the losses caused by its fatal dam disaster in January, writes Bloomberg. Credit Suisse estimates that iron ore prices could spike to average $90 a ton in the second quarter.

- Moving on to China news. The world’s top producer of metals churned out record amounts of aluminum and steel in the first two months of the year. Bloomberg reports that crude steel production rose 9.2 percent to 149.58 tons in January-February, which is a record for that time period. The nation’s electric car market saw sales grow 53 percent in February. The China Automobile Manufactures said on Monday that deliveries of new-energy passenger cars rose to 49,000 units last month. Lastly, China’s wind turbine installations are forecast to grow by at least 20 percent this year, according to a forecast by Ming Yang Smart Energy.

Weaknesses

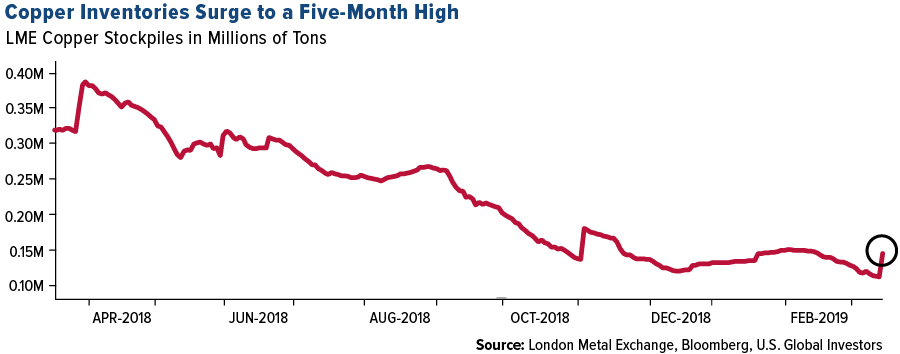

- The worst performing major commodity for the week was natural gas, which fell 2.44 percent with above normal temperatures expected across much of the country next week. LME stockpiles jumped 41,800 tons to 186,425 tons on Friday, driven by inflows throughout Asia, marking the biggest one-day jump since November, reports Bloomberg. The stockpiles were up a whopping 74,650 tons in Thursday and Friday alone, following a surge in Europe. Inventories had been steadily shrinking over the past year as the market heads toward a deficit. Codelco, the world’s second largest copper producer, said that it won’t be able to fulfil its promise to restart operations at two of its smelters in March, according to union leaders. The company said in January that the stoppage would result in production loss of about 218,000 metric tons of copper at its Chuquicamata smelter.

- The coal industry is having a hard time finding capital and is seeing weakening demand for thermal coal. During a panel at the CERAWeek conference in Houston this week, several coal CEOs spoke about industry challenges. Glenn Kellows, CEO of Peabody Energy, said that coal has been “miscast as a Hollywood villain.” Acme Equities, a New-York based holding company, is in talks to buy the 847-megawatt San Juan Generating Station in New Mexico for just $1, after four of its five owners decided to close it, writes Bloomberg’s Will Wade. This comes at a time when the state is pushing for more renewable energy output. Acme plans to spend $400-$800 million to outfit the facility with carbon capture and sequestration technology to capture the polluting gas before it’s released into the atmosphere.

- This week the U.S. government cut its oil production forecast for the first time in six months, reports Bloomberg, as drillers scale back to focus on shareholder returns. The Energy Information Agency (EIA) cut its 2019 forecast to 12.3 million barrels per day, which is 110,000 barrels per day less than its previous forecast. The massive late-winter storm this week in the U.S. heartland is doing damage to crops, livestock and halting mine operations. The extreme weather affected Freeport-McMoRan operations in Colorado.

Opportunities

- In what might be a surprising move for some, Rick Perry, Secretary of Energy, said that he was interested in “getting together and having a conversation” with U.S. Representative Alexandria Ocasio-Cortez, champion of the Green New Deal, about a low-carbon blueprint for the country. At the CERAWeek Conference by IHS Markit this week, Perry said, in regards to Ocasio-Cortez, that “she wants to live in a place where there’s clean air and clean water. So do I. How can we get there?” In a similar tone at the conference, the CEO of BP called for the industry to engage with policymakers as greenhouse gas emissions are expected to rise, reports Bloomberg.

- ExxonMobil aims to reduce the cost of pumping oil in the Permian basin to $15 per barrel and reach a 1 million barrel per day target, according to Staale Gjervik, president of XTO Energy. Bloomberg writes that the shale revolution has made the Permian the world’s largest shale field that has production of over 4 million barrels per day, close to the same amount as Iraq. Royal Dutch Shell is looking for deals to beef up its position in the basin where it lags behind Exxon and Chevron. Wael Sawan, Shell’s deepwater boss, said in an interview this week that “we are definitely actively looking at opportunities.”

- In this week’s solar news, the state-run Solar Energy of India announced on its website that it is seeking bids for 1,200 megawatts of solar projects and 3,600 megawatt-hours of storage capacity across the country. U.S. companies are hurrying to get billions of dollars’ worth of solar projects on the books to cash in on a federal tax credit that is set to shrink at the end of 2019, writes Bloomberg’s Brian Eckhouse. South Korea’s S-Energy is setting up a solar photovoltaic module manufacturing plant in Egypt to expand its presence in emerging markets. Eni IM, an Italian oil major, is building solar plants in Pakistan and Tunisia to support its upstream operations by providing off-grid power. Lastly, in Chile, Anglo American installed 256 photovoltaic panels to float atop a dam of liquid copper waste at its Los Bronces complex. This is a unique way to generate renewable energy and make use of waste from mining operations at the same time.

Threats

- In private talks this week at the CERAWeek conference in Houston, former OPEC president and current United Arab Emirates (UAE) oil minister told members of the financial community in a meeting that the “NOPEC” legislation would be very bad for shale prices. NOPEC is legislation that is being considered by the U.S. government that would allow it to sue OPEC, which would stop the cartel from working. Bloomberg writes that this would raise production capacity in member nations and cause oil prices to crash. Many are critical of the NOPEC idea, as it would disrupt oil markets heavily.

- The Environmental Protection Agency (EPA) released a plan this week that will expand the U.S. market for corn-based ethanol and place trading restrictions on credits that refiners use to prove they are using biofuel, reports Bloomberg, which has long been a promise of President Trump. Current pollution requirements block the sale of E15 gasoline from June 1 to September 15 in areas where smog is a problem. The new proposal would remove those time restrictions and allow the sale year-round of the fuel, which is gasoline containing 15 percent ethanol.

- Bloomberg reports that Indonesia, the world’s largest exporter of thermal coal, is set to see a production decline for the first time in three years after the government trimmed the production quota of some miners. While several large oil companies are diving into the growing natural gas market, ConocoPhillips, the best-performing oil stock in the S&P 500 Energy Index in the past year, sees too much competition. Chief operating officer Matt Fox said in an interview this week that “we’ve decided not to invest in LNG exports from North America because we believe ultimately the returns from that will be pushed down.”

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 2.60 percent.

- The Russian ruble was the best performing currency this week, gaining 2.25 percent against the U.S. dollar. The currency climbed this week as advancing crude oil prices put it on track for one of the strongest five-day performances among its emerging market peers.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst relative performing country in the region, closing flat this week. The United States, together with the European Union and Canada, slapped new sanctions on more than a dozen Russian officials and businesses on Friday. The measure came in response to the country’s "continued aggression in Ukraine."

- The Turkish lira was the worst performing currency this week, losing 31 basis points against the U.S. dollar. The country’s planned purchase of advanced missile systems from Russia, which spread jitters among investors and uncertainty ahead of municipal elections later this month, is weighing on the currency. Turkey’s economy contracted 3 percent year-over-year in the fourth quarter of 2018, according to official data released on March 11. The lira extended losses after the GDP data.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- Euro-area industrial production witnessed the strongest pick-up in more than a year. A 1.4 percent jump in industrial output, higher than the 1 percent gain forecast, was driven by a rebound in some of the bloc’s largest economies, including France, Italy and Spain. Gains in energy and non-durable consumer goods production were particularly strong, though output was still down 1.1 percent on the year. The euro-area figures offer evidence that momentum may be reviving after a extended slowdown.

- According to Bloomberg economics, Spain’s economy is the brightest star in the euro-region for the past few years, promising to keep shining this year. Companies are continuing to hire and wages are climbing. Higher government spending, notably the recruitment of more public sector workers is helping growth in Spain. France is also staging a recovery. Together, they should help the region’s economy rebound from its lowest point in five years.

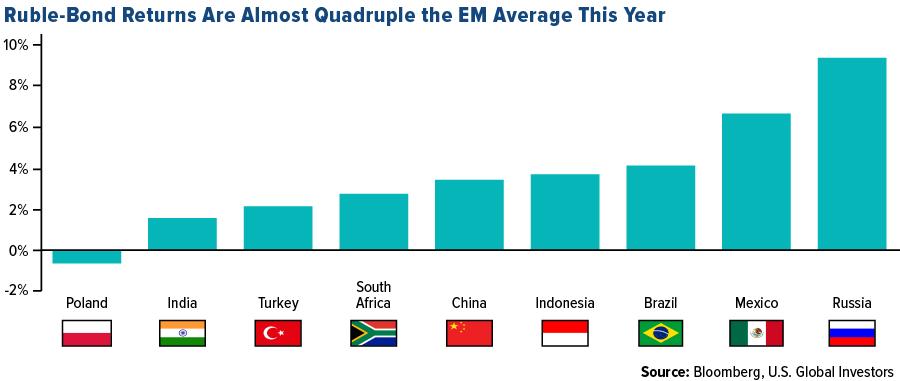

- Yield-hungry investors piled into the Russia Finance Ministry’s latest limitless debt sale, once again shrugging off the lingering risk of U.S. sanctions. Foreigners bought more than half the bonds on offer, according to Konstantin Vyshkovsky, head of the Finance Ministry’s debt department. Russia’s real yields are among the highest in emerging markets this year and the nation’s local bonds have handed investors a return of more than 9 percent, the biggest in the asset class.

Threats

- Poland finance minister Teresa Czerwinska said on Thursday that Polish economic growth will be moderate this year, driven mainly by external factors including Brexit. Poland’s spending splurge before this year’s general elections may increase the inflation above the target level and the central bank may have to embark monetary policy tightening next year. Analysts expect growth in Poland’s $527 billion economy to slow to 3.8 percent this year and 3.3 percent in 2020, which would be the slowest expansion since 2016.

- According to a forecast by leading research group Ifo Institute, Germany’s pace of growth will drop sharply as demand for the country’s products weakens amid a slowing global economy. Germany’s Ifo Institute cut its 2019 growth forecast to 0.6 percent from 1.1 percent. It raised its estimate for expansion in 2020 to 1.8 percent.

- After suffering two crushing defeats by Parliament in less than two months, Prime Minister Theresa May’s Brexit deal was thrown a lifeline last night. If she pulls off a near miracle and gets her deal through parliament before the exit day deadline, the economy would rebound and prompt the BOE to raise rates this year. However, the twists and turns in the Brexit saga in recent weeks have underlined how difficult it is to be confident of any one Brexit outcome. A long delay to the exit day that leads the U.K. to change course remains a real possibility. The uncertainty created by a long extension would keep the economy in the slow lane.

China Region

Strengths

- The top performing country in the Asia region this week was India, climbing 3.69 percent.

- Telecommunications was the top performing sector in the Hang Seng Composite Index, closing out the week 4.78 percent higher.

- Retail sales in Singapore bounced back from their December period decline, rising 7.6 percent year-over-year for the January period.

Weaknesses

- The worst performing country in the Asia region this week was Thailand, which fell by 0.28 percent.

- Materials was the worst performing sector for the Hang Seng Composite for the week, still up slightly 0.05 percent.

- India’s year-over-year industrial production declined to 1.7 percent growth, down from last month’s 2.4 percent and shy of analysts’ estimates for a 2.1 percent pace.

Opportunities

- In a Wall St Journal story this week (“Starbucks Races Rival in China”) highlighting China’s up-and-coming Starbucks challenger Luckin Coffee, a handful of major points deserve to be passed on. First, Luckin, which was only founded in 2017, has now raised more than $1 billion and opened some 2,000 stores across China, mainly offering delivery or pickup, with “many just feet away from a Starbucks café.” Second, “Annual coffee consumption per capita in China is roughly 5 to 6 cups per household, compared with the more than 300 cups per capita consumed by Americans annually.” Finally, Luckin could file for an IPO in the United States “as soon as the first half of this year.”

- A U.S.-China trade deal remains possible, and while the devil, so to speak, will surely be in the details, a removal of uncertainty and resolution on the trade front would likely be welcomed by markets.

- “Indonesian and Philippine elections in April and May, respectively, may aid equity investors,” Bloomberg News reported this week, citing a JPMorgan note, “because their markets historically gain before votes as governments offer cash handouts and other industry-specific subsidies.”

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter continue to be a collective threat until resolution one way or the other. U.S. President Donald Trump and Chinese President Xi Jinping will not meet this month, Secretary Mnuchin confirmed on Thursday.

- Bloomberg News reports that the delay in approving the Philippine budget prompted authorities to cut growth targets for this year and next. GDP may expand 4.2 percent to 4.9 percent in 2019 if the fiscal plan isn’t passed, the article highlights Economic Planning Secretary Ernesto Pernia as saying; that range would be the weakest pace since the 3.7 percent expansion in 2011.

- The U.S. dollar remains a scant hop-skip-and-a-jump away from new 52-week highs (roughly 1 percent or so), leaving emerging markets subject to possible dollar pressures should the dollar break out and run higher. While the U.S. Federal Reserve has promised a patient pause, data dependency will lead where it will lead, and as Europe stimulates, China stimulates, and the United Kingdom attempts to work out what exactly Brexit looks like, U.S. dollar strength could be, or develop into more of, a possible headwind.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 15 was Ormeus Coin, up 853.90 percent.

- Investment management company Invesco, in partnership with Elwood Asset Management, launched a blockchain exchange-traded fund (ETF) on the London Stock Exchange on Monday, reports Coindesk. The Invesco Elwood Global Blockchain UCITS ETF is designed to target companies with the potential to generate “real earnings” from blockchain technology, according to the announcement released by Elwood.

- While delivering the keynote speech at the Australian Financial Review Business Summit last week, Niall Ferguson (the prominent British historian and author of “The Ascent of Money”) retracted his critical appraisal of the crypto industry, reports Bitcoin.com. Ferguson said he was “very wrong to think there was no use for a form of currency based on blockchain technology.” Another renowned stock market analyst is also jumping on the crypto train, reports Cash. In a recent interview, 73-year-old Marc Faber revealed that he purchased bitcoin for the first time in late February.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 15 was Game Stars, down 48.58 percent.

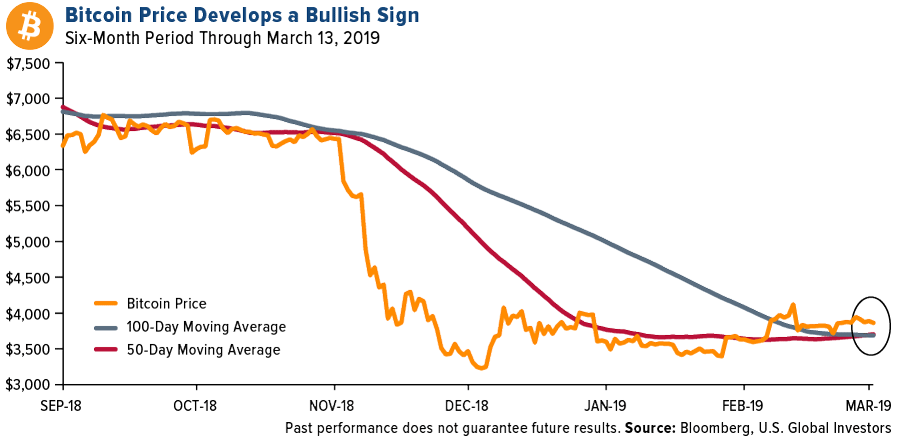

- According to the Bitcoin Moving Average Convergence Divergence indicator, a recent rally seen in the popular digital currency could be winding down, reports Bloomberg. The indicator is steadily falling, the article explains, after logging its first positive returns in seven months during February and rising off its 52-week lows. As long-term buying demand for bitcoin deteriorates, selling pressures could intensify.

- Agustin Carstens, head of Bank for International Settlements, is one of the fiercest critics of cryptocurrencies, reports Bitcoin Exchange Guide. At the beginning of 2019, Carsten said that bitcoin and altcoins are “a bubble, a Ponzi scheme and an environmental disaster.” In his latest attack on the industry, he told a Swiss-German newspaper that the digital currency is a “fraud” and is quoted as saying “stop trying to create money!”

Opportunities

- The cryptocurrency unit of Kakao, Ground X Corp., has raised $90 million through a private coin offering, reports Bloomberg. The company is planning another round targeting a similar sum starting March 12, as it gears up to launch its blockchain platform in June, the article continues.

- Facebook is reportedly developing a cryptocurrency that could be part of a multibillion-dollar revenue opportunity, according to Barclay’s internet analyst Ross Sandler. As CNBC specifies in a recent article, Sandler forecasted as much as $19 billion in additional revenue by 2021 from “Facebook Coin.”

- As Coindesk reports this week, a widely-followed bitcoin price indicator could soon turn bullish for the first time in seven months. The cryptocurrency’s 50-day moving average (MA) is about to move above the 100-day MA. While the bullish crossover is technically a lagging indicator, the article explains that the current slope of the Mas is signaling bearish exhaustion.

Threats

- According to Paul R. Brody, Global Blockchain Innovation Chief at Ernst and Young (EY), there is no practical application for bitcoin and other cryptocurrencies. He says crypto-fiat, and not bitcoin, is the future of money. “Most people and companies earn their revenue and spend their money in local currency,” Brody explained. “We believe the future of business transactions on the blockchain are tokenized fiat currencies – basically blockchain-linked dollars, euros, yen, rupees and so on.”

- On Wednesday, the Basel Committee on Banking Supervision, a group of international banking authorities, issued a statement warning that the growth of cryptocurrencies poses a number of risks to banks and global financial stability, reports Coindesk. According to the statement, the potential risks for banks include liquidity, credit and market risks, operational risk, money laundering and terrorist financing risk.

- The size of bitcoin’s average daily gain has reduced quite significantly since mid-February, reports Bitcoin Exchange Guide, pointing to the fact that the digital asset’s recent price rally could finally be nearing completion. “The entire industry is ripe to resume a path to lower prices. Conditions are akin to November, just prior to the collapse,” Bloomberg analyst Mike McGlone said. “Prices are consolidating within narrowing ranges, with a few sharp bear-market rallies that appear fleeting.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Oil Futures | 58.42 | +2.35 | +4.19% |

| Nasdaq | 7,688.53 | +280.39 | +3.78% |

| S&P Energy | 484.84 | +15.07 | +3.21% |

| S&P 500 | 2,822.48 | +79.41 | +2.89% |

| Hang Seng Composite Index | 3,882.53 | +86.87 | +2.29% |

| Russell 2000 | 1,553.54 | +31.65 | +2.08% |

| Korean KOSPI Index | 2,176.11 | +38.67 | +1.81% |

| S&P Basic Materials | 347.35 | +5.75 | +1.68% |

| DJIA | 25,848.87 | +398.63 | +1.57% |

| S&P/TSX VENTURE COMP IDX | 627.63 | +9.55 | +1.55% |

| Gold Futures | 1,301.60 | +2.30 | +0.18% |

| XAU | 76.05 | +0.03 | +0.04% |

| S&P/TSX Global Gold Index | 193.27 | -1.98 | -1.01% |

| 10-Yr Treasury Bond | 2.59 | -0.04 | -1.44% |

| Natural Gas Futures | 2.80 | -0.07 | -2.44% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.80 | +0.22 | +8.54% |

| Oil Futures | 58.42 | +4.52 | +8.39% |

| Nasdaq | 7,688.53 | +268.15 | +3.61% |

| S&P/TSX Global Gold Index | 193.27 | +6.46 | +3.46% |

| S&P/TSX VENTURE COMP IDX | 627.63 | +17.64 | +2.89% |

| XAU | 76.05 | +2.01 | +2.71% |

| S&P Basic Materials | 347.35 | +8.65 | +2.55% |

| S&P 500 | 2,822.48 | +69.45 | +2.52% |

| Hang Seng Composite Index | 3,882.53 | +60.33 | +1.58% |

| S&P Energy | 484.84 | +7.27 | +1.52% |

| DJIA | 25,848.87 | +305.60 | +1.20% |

| Russell 2000 | 1,553.54 | +10.59 | +0.69% |

| Gold Futures | 1,301.60 | -13.50 | -1.03% |

| Korean KOSPI Index | 2,176.11 | -25.37 | -1.15% |

| 10-Yr Treasury Bond | 2.59 | -0.11 | -4.11% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| S&P/TSX VENTURE COMP IDX | 627.63 | +70.67 | +12.69% |

| Oil Futures | 58.42 | +5.84 | +11.11% |

| XAU | 76.05 | +7.30 | +10.62% |

| Hang Seng Composite Index | 3,882.53 | +315.70 | +8.85% |

| Nasdaq | 7,688.53 | +618.19 | +8.74% |

| Russell 2000 | 1,553.54 | +120.84 | +8.43% |

| S&P/TSX Global Gold Index | 193.27 | +14.27 | +7.97% |

| S&P Basic Materials | 347.35 | +24.84 | +7.70% |

| S&P 500 | 2,822.48 | +171.94 | +6.49% |

| DJIA | 25,848.87 | +1,251.49 | +5.09% |

| Korean KOSPI Index | 2,176.11 | +80.56 | +3.84% |

| Gold Futures | 1,301.60 | +48.00 | +3.83% |

| S&P Energy | 484.84 | +17.79 | +3.81% |

| 10-Yr Treasury Bond | 2.59 | -0.32 | -11.05% |

| Natural Gas Futures | 2.80 | -1.33 | -32.23% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

The Boeing Co.

Alaska Air Group Inc.

American Airlines Group Inc.

Delta Air Lines Inc.

United Continental Holdings Inc.

Southwest Airlines Co.

Spirit Airlines Inc.

Allegiant Travel Co.

JetBlue Airways Corp.

Air Canada

San Juan Basin Royalty Trust

Freeport-McMoRan Inc

BP Plc

Peabody Energy Corp

Royal Dutch Shell Plc

Chevron Corp

Anglo American Plc

Citigroup Inc

Barrick Gold Corp

Newcrest Mining Ltd

North American Palladium Ltd

Newmont Mining Corp

Lam Research Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Barclays Global Aggregate Negative Yielding Debt Market Value Index measures the stock of debt with yields below zero issued by governments, companies and mortgage providers around the world which are members of the Bloomberg Barclays Global Aggregate Bond Index.

Earnings per share (EPS) is the portion of a company’s profit allocated to each share of common stock. Earnings per share serve as an indicator of a company’s profitability.

The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of U.S. consumer confidence levels conducted by the University of Michigan. It is based on telephone surveys that gather information on consumer expectations regarding the overall economy. The S&P 500 Energy Index comprises those companies included in the S&P 500 that are classified as members of the GICS sector.

The Commodity Research Bureau (CRB) Raw Industrials Index tracks several commodities and acts as a representative indicator of today’s global commodity prices.