Investor Alert

Gold Is Now the Second Most Liquid Asset on Earth

Date Posted: October 1, 2021

Read time: 45 min

Press Release: U.S. Global Investors Announces a 50% Increase in Monthly Dividend

Contrary to popular belief, what’s good for the goose is not always good for the gander.

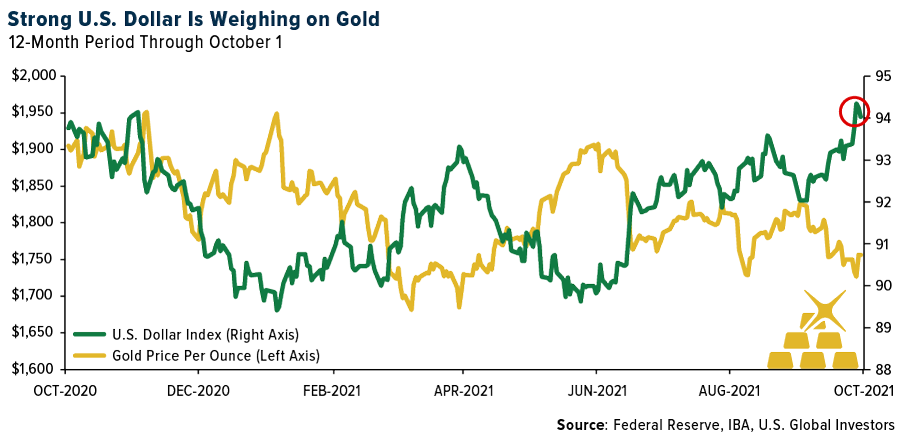

This week the U.S. dollar advanced against a basket of foreign currencies to hit its highest level in about a year. For consumers and importers, this is good news, as it means the greenback offers greater purchasing power.

For exporters, on the other, and for the price of gold and other commodities that are priced in U.S. dollars, this is a headwind. In the chart below, you can see that gold and the dollar share an inverse relationship. When the dollar strengthens, the yellow metal falls; when it weakens, gold soars. It’s important for investors to recognize this relationship because it can help them manage their expectations.

It’s also important for investors to keep in mind that gold continues to be one of the most heavily traded assets on the planet, in case they were wondering if Bitcoin is stealing some of its thunder as a store of value.

I often tell people that gold is the fourth most liquid asset, but the most recent data from the World Gold Council (WGC) shows that it’s actually the second most liquid asset following S&P 500 stocks. The precious metal’s average daily trading volume for the one-year period through September 28 was $183 billion, compared to the S&P 500 with nearly $235 billion in average daily volume. That dollar amount is enough to beat currency swaps as well as all government and corporate debt. The WGC measures gold’s liquidity by looking at data provided by global commodity exchanges, over-the-counter (OTC) markets and gold-backed ETFs.

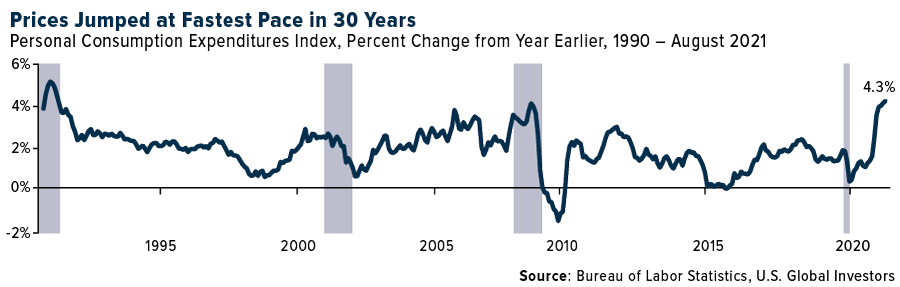

Inflation Surging at Fastest Pace Since 1991. Will Gold Benefit?

Gold traded slightly up today following the release of economic data showing that consumer prices jumped the most in 30 years. The personal consumption expenditure (PCE) index, which reflects changes in the prices of goods and services purchased by U.S. consumers, rose 4.3% year-over-year in August, the ninth straight month of accelerating inflation.

The PCE, by the way, is the Federal Reserve’s preferred measure of inflation. Fed Chair Jerome Powell, who earlier this year predicted inflation would be “transitory,” admitted this week during a Senate hearing that the bottlenecks and supply shortages that have contributed to higher prices were “frustrating,” and that we should see more of the same pressures into next year.

It’s not just the price of consumer goods that are soaring right now. Home prices, as measured by the S&P CoreLogic Case-Shiller National Home Price Index, rose 19.7% in the year ended July 2021, the highest annual rate since the index began in 1987. Apartment rents around the U.S. are also heating up. According to Zillow, the average listed rent in August was up 11.5% compared to last year, which some cities in Florida, Georgia and Washington seeing increases of more than 25%.

Oil at Multiyear Highs Despite the Stronger Dollar

Because it’s priced in U.S. dollars, oil ordinarily tumbles when the greenback strengthens, but that wasn’t the case this week. Brent crude, the international benchmark, briefly topped $80 a barrel on Tuesday for the first time in nearly three years due to ongoing supply disruptions. As you can see below, Brent was trading well above both its 50-day and 200-day moving averages, which is a bullish sign.

What this means is that U.S. exporters are faced with the double-whammy of a stronger dollar and higher fuel costs.

The largest publicly traded exporting company in the U.S. is International Paper. The Memphis-based company, which manufactures paper and packaging goods, shipped close to 220,000 twenty-foot equivalent units (TEUs) in 2020, according to the Journal of Commerce (JOC). That’s second only to the privately held Koch Industries, which was responsible for exporting more than 280,000 TEUs last year. Koch is a massive conglomerate that, like International Paper, focuses a large part of its business on paper and pulp products.

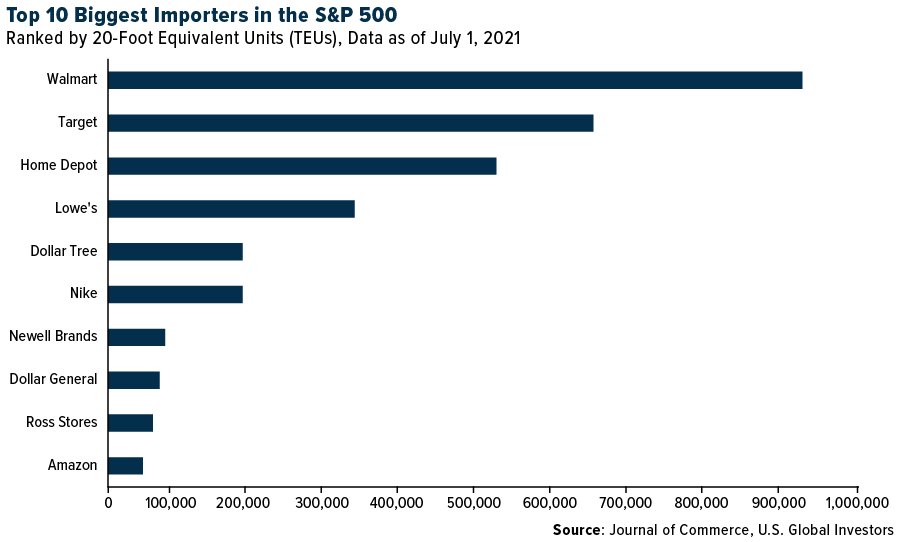

Again, a strong greenback is a tailwind for companies that do a lot of importing. Below are the S&P 500 companies that do the most importing, with Walmart topping the list at a jaw-dropping 930,000 TEUs.

For Airlines, Higher Fuel Costs Are Just More Fud (Fear, Uncertainty and Doubt)

Like a lot of analysts, I see the recent surge in oil prices as a short-term headwind, and already there’s been some contraction due to the stronger dollar and bigger-than-expected inventory build.

As such, this could be an attractive buying opportunity for airline stocks as the share of people fully vaccinated against Covid in high-income countries continues to increase.

I’ll be blunt: When it comes to airlines, the oil price increase is just more FUD (fear, uncertainty and doubt). It’s true that fuel is one of the airline industry’s biggest fixed costs, but what’s important for investors to understand is that higher oil prices have historically helped carriers demonstrate a certain level of capacity growth restraint. Unprofitable routes have been cancelled, for instance, which has contributed to higher load factors.

Plus, I would recommend investors pay more attention to airlines’ ancillary revenues, which play an increasingly important role in driving sales and cash flow. More and more, these revenues help offset higher fuel costs, something that was not necessarily the case 10 years ago when oil was above $100. In 2020, ancillary fees fell in absolute terms, but they represented a bigger piece of airlines’ total revenue.

Right now, vaccination rates and government policy are in the pilot’s cabin, so that’s what investors should be focused on instead.

Before the delta variant, leisure air travel had already returned to 2019 levels. Now that vaccination rates look good in most high-income countries and international travel restrictions are being lifted, I expect to see business travel make some progress.

Speaking for myself, I was recently able to attend the Gold Forum Americas conference in Denver, and I’ll be in Dubai later this month at the AIM Summit. Obviously more progress needs to be made before we’re back to normal pre-pandemic life, so I think this is a very attractive time to start participating with airlines.

Speaking of the AIM Summit… If you’ll be in the Dubai area on October 12, make sure to catch my panel on mining Bitcoin with sustainable energy. Apply to attend by clicking here!

Index Summary

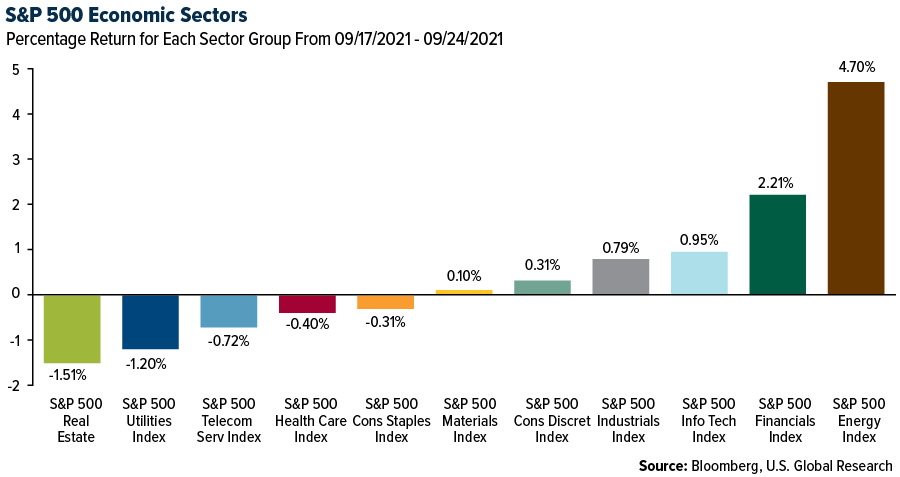

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.36%. The S&P 500 Stock Index fell 1.97%, while the Nasdaq Composite fell 3.20%. The Russell 2000 small capitalization index lost 0.18% this week.

- The Hang Seng Composite gained 1.13% this week; while Taiwan was down 3.99% and the KOSPI fell 3.39%.

- The 10-year Treasury bond yield rose 1 basis point to 1.466%.

Airline Sector

Strengths

- The best performing airline stock for the week was Bombardier, up 8.9%. U.S. demand, as measured by the seven-day average TSA passenger throughput, modestly improved for the week ending Thursday, September 23. The passenger throughput was up by 2.5 points relative to last week on a year-to-year basis.

- System net sales declined 60.1% versus 2019 for the week, which is slightly better than the recent downtrend in the low to mid-60% range. Demand in both corporate and leisure channels was also a bit better than the recent trend, showing that the delta variant impact is likely waning.

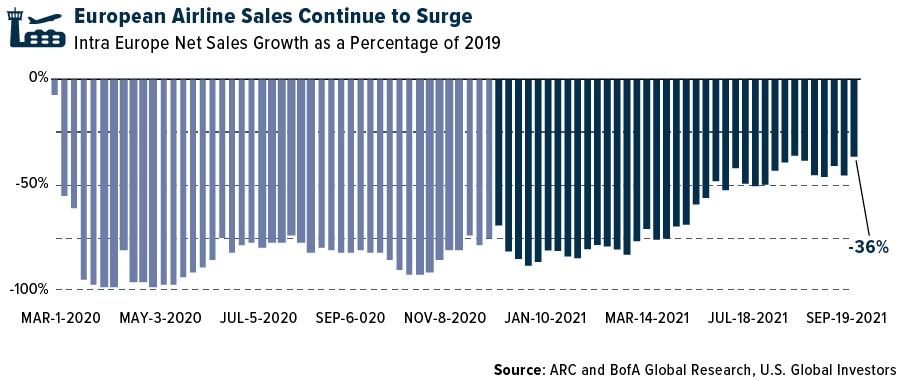

- European airline bookings showed a strong increase in the week, with both intra-European and international net sales reaching their highest post-pandemic levels. Intra-Europe net sales increased by 9 points to -36% versus 2019 (and versus -45% in the prior week) and were up by 24% week-on-week, following a dip in the prior week.

Weaknesses

- The worst performing airline stock for the week was Bangkok Airways, down 5.7%. . There are some declines in U.S. capacity. November capacity was cut 3%, now at -12% versus 2019 (and versus +2% a month ago). United Airlines was the main driver as it cut ASMs by 10% versus last week. December capacity was reduced 2%, now at -8% versus 2019 (also +2% a month ago) with United and Southwest Airlines as the main drivers as they cut ASMs by 6% and 4%, respectively, versus last week.

- According to CNBC, Southwest Airlines is about halfway to its goal of hiring 5,000 workers this fall, but incoming CEO Bob Jordan noted that hiring continues to be a major challenge. This past summer Southwest customers experienced hundreds of cancellations and delays across the network due to technical difficulties, bad weather and labor shortages. The airline is not alone in its search for employees as the labor shortage has taken a toll on the entire airline industry. If Southwest is unable to meet its March schedule due to hiring challenges, management is willing to modify the schedule. This comes a month after Southwest announced it will be trimming its fall schedule to better align with its employee operations

- United Airlines said it would terminate about 320 employees for refusing to comply with its vaccination requirement, putting the company at the forefront of the battle over vaccine mandates, as the economy moves through a bumpy pandemic recovery.

Opportunities

- According to recent data, demand in both domestic leisure (bookings through online channels) and corporate (bookings through large travel agencies) channels stepped up to -1.3% (versus -8.9% last week) and -55.3% (versus -61.2% last week), respectively. Corporate pricing remains ahead of leisure pricing at -26.9% versus 2019 levels, while leisure is -31.3% versus 2019, likely due to the price sensitivity of the leisure traveler.

- U.S. airlines’ trailing seven-day website visits are up 5% for the week compared to up 3% last week. This week the biggest gainer was Alaska Air, which improved to +21% versus 2019 levels (and versus -5% last week) due to its buy-one-get-one (“BOGO”) free ticket deal for fall travel.

- Delta Air Lines wants other airlines to share their “no fly” lists of unruly passengers to help protect employees across the industry. In an internal memo published last week, employees at Delta stated the airline has had more than 1,600 people on its “no fly” list and that it has submitted more than 600 banned names to the FAA in 2021 as part of the Special Emphasis Enforcement program. In order to commit to the safety of employees amid increasing rates of unruly passengers, Delta also asked other airlines to share their “no fly” lists, since a list of banned customers does not matter if that same customer can fly with another airline.

Threats

- Labor availability for Delta Air Lines is not about inability to staff or hire. The company received 30,000 applications for 1,500 flight attendant jobs, for example. The time to process and train new employees are the key issues facing the company in this aspect.

- Raymond James revised its U.S. airlines estimates, primarily reflecting the delta variant demand impact. The estimates also reflect lower capacity production into year-end 2021 in response to the demand softness and operational issues, along with incremental cost headwinds.

- The Department of Justice (DOJ) filed an antitrust lawsuit challenging the domestic alliance between American Airlines and JetBlue. They stated that the Northeast Alliance (NEA) will not only eliminate competition within New York and Boston but will also harm air travelers by diminishing JetBlue’s incentive to compete with American elsewhere. The partnership between American and JetBlue, which was announced in July 2020, combines operations at four major airports in Boston and New York, and coordinates all aspects of network planning.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 4.2%. The best performing country in Asia this week was Indonesia, gaining 1.5%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 0.32%. The China renminbi was the best performing currency in Asia this week, gaining 0.33%.

- The final Manufacturing PMI for the Eurozone was reported at 58.6 versus the 58.7 expected. Despite recent corrections in European manufacturing activity, it remains well above the 50 level that separates contraction from expansion.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Poland, gaining 1%.The worst performing country in Asia this week wasTaiwan, losing 4.4%.

- The Hungarian forint was the worst performing currency in emerging Europe this week, losing 1.1%. The Pakistani rupee was the worst performing currency in Asia this week, losing 0.80%.

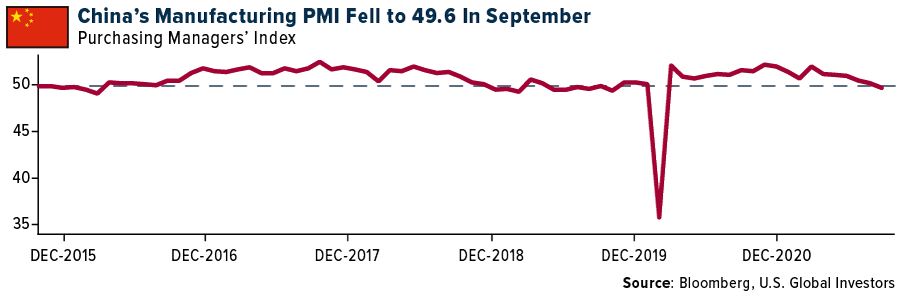

- China released weak economic data. China’s industrial profits slowed down in August to 10.1% year-over-year from 16.4% in July. The spread of the coronavirus, high raw material prices, cost of logistics and chip shortages were all to blame for the slowdown, FactSet reported. The China Manufacturing PMI dropped below the 50 level that separates growth from contraction this week.

Opportunities

- The Social Democrats party won the election in Germany by a narrow margin this past Monday. The German Social Democrats will have to team up with their sister parties to form a government. It could take several months before the new coalition is fully formed. Germany overall has enjoyed great economic conditions over the past few decades, and there appears to still be room for more relaxed fiscal and monetary stimulus. Raffaella Tenconi from Wood & Company does not believe the election results will make a huge difference on the CE4 (Czech Republic, Hungary, Poland, and Romania) countries over the long term, as most of them are already experiencing very loose conditions. For Greece and the Eurozone as a whole, though, this could be a factor that pushes the average GDP growth up in the next five years and beyond.

- Last week, the Russian government announced it had reached an agreement with the largest metals and mining companies on tax changes, implying softer implications on Russian metals and mining profits versus some options discussed previously. There is no change in taxation for precious metals, aluminum-producing raw materials, and diamonds. Most importantly, the progressive tax based on dividends has been put on pause for now.

- The Caixin Service PMI, calculated by the Caixin-Markit Index and based on a survey of approximately 500 small private businesses, will be released next week. It may spike higher, following the official China Service PMI. The China Service PMI, which has a much bigger sample and most of the surveyed companies are state-owned enterprises, was released this week at 53.2 versus the expected 49.8.

Threats

- China continues to support its economy, moving more money into its banking system. The People’s Bank of China (PBOC) also vowed to protect the rights and interest of real estate consumers amid the Evergrande debt crisis. However, it remains to be seen if the heavy indebted real estate company, Evergrande, will be able to pay its upcoming coupon expenditures. The Chinese government most likely will not allow disorganized default, but the real estate market disruption is unaidable at this point.

- After last week’s Turkish central bank surprise decision to cut the one-week repo rate by 100 basis points, the Turkish lira reached its new record low mid-week. The United States warned it could issue new sanctions on the country if Turkey goes ahead with its plan to purchase more military equipment from Russia. The Turkish lira is the world’s worst performing currency, losing 16% year-to-date. And, most likely, it will continue to underperform.

- Eurozone inflation has spiked to 13-year highs. September inflation was released at 3.4% versus the expected 3.3% and August’s 3.0%. The core inflation spiked to 1.9% in September from 1.6% the prior month.

Energy and Natural Resources Market

Strengths

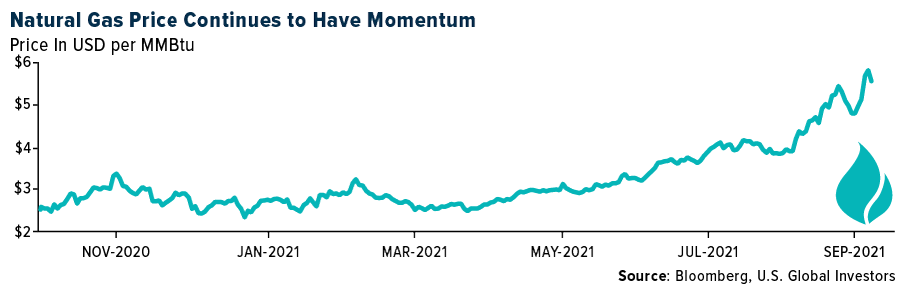

- The best performing commodity for the week was cotton, up 10.6%. Natural gas prices surged to a fresh seven-year high in the U.S. as the expiration of October options added momentum to a rally fueled by escalating concerns about tight winter supplies. Gas for October delivery gained 11%, the biggest daily jump since February, settling at $5.71 per million British thermal units, a level not seen since early 2014.

- Iron ore surged back to near $120 a ton, extending its rebound from the lowest in more than a year as some steel mills looked to build up inventories ahead of a holiday in China. Prices are heading for the longest streak of gains since June, after plummeting to $90 a ton last week.

- Due to a global supply shortage of PVC, the U.S. PVC export price rose to $2,000/ton (up $100/ton compared with the previous week), and the Indian PVC import price rose to $1,800/ton (up $150/ton last week). According to Platts, all U.S. PVC facilities that had been shut down due to Hurricane Ida are back online, but it will likely take several weeks to make up for lost production. Meanwhile, housing starts in the U.S. in August were positive, which suggests strong demand for PVC. In China, 5% to 7% of PVC capacity has apparently been taken offline due to energy restrictions.

Weaknesses

- The worst performing commodity was nickel, down 7.5% for the week. Renewables pricing is under pressure. One reason U.S refiners earnings have been below normalized levels is because higher RIN renewables prices are a headwind to most refiners due to a higher cost of compliance. According to Reuters, the U.S. EPA is proposing big cuts to the conventional biofuel blending requirements.

- According to UBS, even with higher-than-expected 2021 demand, they estimate capacity additions will result in a 200-basis point year-to-year decline in 2022, with utilization rates to 93% for containerboard. With utilization falling, they expect the containerboard industry to lose pricing power. UBS expects kraftliner price weakness starting in late first quarter of 2022 on oversupply, following seasonally strong demand in the fourth quarter. They track 3.7% average containerboard supply growth in 2022 and 2023 from planned expansions, accelerating from 3.1% growth in 2021. U.S. containerboard demand growth is slowing. There is a slowdown in eCommerce as instore took share, and an increase in services spending over goods.

- China crude steel production fell 4% month-to-month in August (-13% year-to-year) to the lowest daily run rate since March 2020. The preliminary data suggests production is down 3% month-to-month in September. Weaker steel production since July is driven by the central government pressuring provinces to materially cut energy consumption and intensity to meet the 2021 target cut of 3% year-to-year.

Opportunities

- Fertilizer prices are improving. Urea prices continued the significant surge upward since the beginning of September, as typical demand seasonality has been met by constrained supply. UAN prices jumped across global benchmarks on recent supply curtailments in Europe. Potash prices moved up on rising demand in Asia and tight supply owing to logistical concerns related to Belarusian exports.

- Goldman Sachs says it continues to view aluminum as the base metal with the most bullish fundamentals over the rest of 2021 and into next year. The market, already in a clear deficit, will head toward progressively larger deficits over the next two to three years.

- Western lumber pricing continued to move higher backstopped by better-than-expected August housing starts while futures maintained a historically high premium over cash. Pricing ended the week up 6% at $498, down 62% relative to the second quarter, down 47% year-to-year, and up 69% year-to-date.

Threats

- China will release 30,000 tons of copper, 50,000 tons of zinc and 70,000 tons of aluminum from state reserves in its fourth batch of sales, according to statements from National Food and Strategic Reserves Administration in China.

- Bank of America Japan expects the earnings of diversified chemical makers to head toward a peak near the end of this year. This is based on a deteriorating demand outlook due to lower GDP forecasts for China, a cyclical peak for petrochemicals (excluding PVC) due to significant capacity increases for various petrochemicals, decreased shipments of automotive materials due to a short-term slowdown in auto production, softening demand for LCD materials and sharply increasing raw material and fuel costs.

- Global steel production for August dipped 3% month-to-month and down 1.4% year-to-year to 156.8 million tons. The slowdown is driven by -13.2% year-to-year Chinese production; production, excluding China, was higher 17% year-to-year.

Domestic Economy and Equities

Strengths

- The U.S. economy expanded at a 6.7% annual pace in the second quarter, the Commerce Department said Thursday, slightly upgrading its estimate of last quarter’s. A key factor in the upgraded growth estimate for the April-June quarter was a slightly higher level of consumer spending, which accounts for roughly 70% of economic activity.

- The Pending Home Sales Index for August rose 8.1% month-over-month, beating estimates for a 1.0% gain and reversing two-straight months of declines.

- Dollar Tree was the best performing S&P 500 stock for the week, increasing 16.4%. Shares gained after the company announced a plan to add more products at slightly higher prices. Dollar Tree said it would start selling products at $1.25 and $1.50 or other prices slightly above $1 in some of its stores.

Weaknesses

- New jobless claims have risen for a third straight week. Initial jobless claims unexpectedly rose to 362,000, above consensus for 335,000. Continuing claims logged 2,802,000, just a bit higher than the consensus for 2,800,000.

- September’s Richmond Fed Manufacturing Index fell into contraction, moving to -3.0 versus consensus for +11.0 and August’s +9.0. Consumer confidence in September came out at 109.3, below consensus for 114.0 and August’s upwardly revised 115.2. Both present situation and expectation components fell during the month.

- Moderna was the worst performing S&P 500 stock for the week, losing 20.3%. Shares declined after Merck’s antiviral pill cut the risk of hospitalization or death related to COVID by 50% in an interim analysis of a late-stage trial.

Opportunities

- One in four companies has instituted a vaccine mandate for U.S. workers, a sharp increase from last month, following President Joe Biden’s directive ordering large employers to require shots or weekly testing. Another 13% of companies plan to put a mandate in place, according to Brian Kropp, chief of human resources research at consultant Gartner.

- Bloomberg economists expect nonfarm payrolls to increase by 500,000 next week pointing to further recovery in the job market. The unemployment rate will likely drop to 5% for September, lower than the 5.2% reported a month ago.

- Manufacturing activity remains strong in the United States. The final September reading for Markit’s Manufacturing PMI came out at 60.7 versus 60.5. The University of Michigan Consumer Confidence and Current Conditions jumped. ISM new orders came out higher than expected in September. Better economic data is pointing to a continuation of economic recovery.

Threats

- Rising Treasury yields and increasing energy prices have pushed equites lower in September. Usually, higher rates and firmer energy prices are seen as positive signs of the economic recovery, but the recent speed of the shift continues to surprise the market. On Thursday, the S&P recorded its first monthly decline since January.

- The energy crunch may push oil above $100 per barrel for the first time since 2014 and spur a global economic crisis, Bank of America said. With monetary and fiscal policy stretched to the limit and energy costs rising as a share of GDP, higher crude may create a macro crisis.

- On Wednesday, the world’s top central bankers warned that supply constraints threatening global economic growth could still get worse, keeping inflation elevated longer. “We see that continuing into next year probably and holding inflation up longer than we had thought,” Powell told the European Central Bank’s Forum on Central Banking. ECB chief, Christine Lagarde, voiced similar concerns.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Gravitoken (GRV), rising over 2,400%.

- Billionaire Orlando Bravo said he owns Bitcoin and is very bullish on the cryptocurrency. At CNBC’s Delivering Alpha conference this week, Bravo stated “How could you not love crypto?” He added that he likes Bitcoin’s finite supply and sees more people using it in the future, according to Bloomberg.

- The city of Miami has earned over $5 million from the launch of the new token MiamiCoin and city officials just voted to approve accessing the funds. MiamiCoin is the first of its kind, and San Francisco seems to be following suit, reports Blockworks.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Capital X Cell (CXC) down 99%.

- Chinese e-commerce giant Alibaba is the next company to wrap up its cryptocurrency-related services in response to the ongoing crackdown in China, writes CoinTelegraph. The company officially announced on Monday that its platform will prohibit sales of crypto miners and suspend categories for blockchain miners and accessories from its website on October 8. Any sellers that list these kinds of products on Alibaba’s platforms after October 15 will face significant penalties, the article explains.

- The Commodity Futures Trading Commission (CFTC) has imposed a $1.25 million penalty to cryptocurrency exchange Kraken. The exchange offered margined retail commodity transactions in digital assets and failed to register as a futures commission merchant. Kraken is not the first crypto exchange sanctioned by the CFTC; in August, FinCEN charged Bitmex $100 million for operating an unregistered derivatives trading platform.

Opportunities

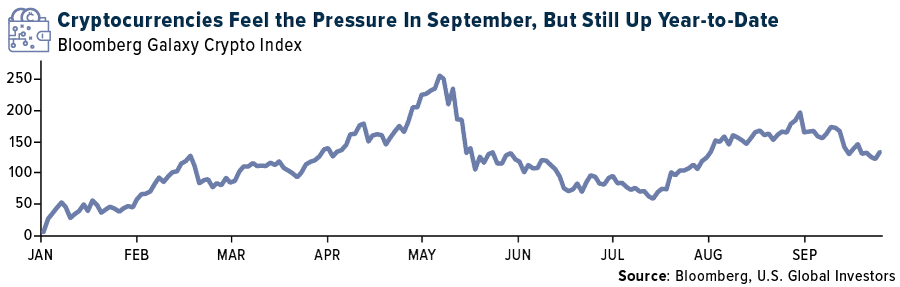

- The cryptocurrency market made a swift comeback from the turbulence last week triggered by China’s latest crackdown, reports Bloomberg, with the likes of Bitcoin and Ether recouping most of their losses at the start of the week. Bitcoin rallied to around $44,000 in Hong Kong on Monday (near the level when the PBOC announced its latest step in reining in crypto Friday), and Ether broke above last week’s level at $3,100, the article continues. Although the group of major cryptos (as represented by the Bloomberg Galaxy Crypto Index) was down slightly in September, they are still up year-to-date.

- Cryptocurrency derivatives exchange Bitget is the first ever sleeve partner with famous European soccer club Juventus, reports Bitcoinist. This is further proof of the undeniable trend that sports are getting increasingly connected with cryptocurrencies.

- Switzerland’s Financial Market Supervisory Authority (FINMA) has approved the first Swiss crypto fund. The fund is managed by asset manager Crypto Finance and custodied by Seba Bank. “This is the first time that FINMA has approved a Swiss fund that invest primarily in crypto-assets” said a regulator and reported by Bitcoin.com

Threats

- Virgil Griffith, Ethereum developer, has plead guilty to violating U.S sanction law. Griffith was arrested in 2019 after giving a presentation at a North Korean cryptocurrency conference. He was released on bail in 2020, but currently resided in jail for violating his bail conditions. He will be sentenced in January 2022, according to Coindesk.

- The State of Tennessee has received reports about pyramid schemes on cryptos like Bitcoin, Ethereum, and Dogecoin. The investments are in fraudulent Bitcoin futures that come from shell companies. The state attorney has vowed to take action and apprehend the criminals, writes Cryptopolitan.com.

- Due to the ongoing crypto crackdown by the CCP, one of the world’s largest crypto exchanges by trading volume, Huobi is relocating its operations out of the country. Chinese censors started blocking social media and internet results for “Huobi” and other crypto exchanges, writes CoinTelegraph.

Gold Market

This week spot gold closed the week at $1759.48, up $9.06 per ounce, or 0.5%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.2%. The S&P/TSX Venture Index came in off 1.7%. The U.S. Trade-Weighted Dollar rose 0.8%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-27 | Durable Goods Orders | 0.7% | 1.8% | -0.1% |

| Sep-28 | Hong Kong Exports YoY | 26% | 25.9% | 26.9% |

| Sep-28 | Conf. Board Consumer Confidence | 115 | 109.3 | 113.8 |

| Sep-29 | Caixin China PMI Mfg | 49.5 | 50 | 49.2 |

| Sep-30 | Germany CPI YoY | 4.2% | 4.1% | 3.9% |

| Sep-30 | Initial Jobless Claims | 330k | 262k | 351k |

| Sep-30 | GDP Annualized QoQ | 6.6% | 6.7% | 6.6% |

| Oct-1 | Eurozone CPI Core YoY | 1.9% | 1.9% | 1.6% |

| Oct-1 | ISM Manufacturing | 59.5 | 61.1 | 59.9 |

| Oct-4 | Sentix Investor Confidence | 18.6 | — | 19.6 |

| Oct-4 | Factory Orders | 1.0% | — | 0.4% |

| Oct-5 | Markit Eurozone Services PMI | 56.3 | — | 56.3 |

| Oct-5 | Markit Hong Kong PMI | — | 53.3 | |

| Oct-5 | PPI YoY | 13.5% | — | 12.1% |

| Oct-5 | Markit US Services PMI | 54.4 | — | 54.4 |

| Oct-6 | Retail Sales YoY | 0.4% | — | 3.1% |

| Oct-7 | Initial Jobless Claims | 348k | — | 362k |

| Oct-8 | Caixin China PMI Services | 49.2 | — | 46.7 |

| Oct-8 | Unemployment Rate | 5.1% | — | 5.2% |

Strengths

- The best performing precious metal for the week was gold, up 0.5%. Agnico Eagle announced it entered into an agreement to acquire Kirkland Lake in a merger of equals. The combined company will have annual production of 3.4 million ounces and reserves of 48 million ounces in mining-friendly jurisdictions (mainly Canada and Australia). Agnico Eagle estimates pre-tax synergies of $800 million over five years and $2 billion over 10 years, implying annual synergies of $200 million, with most of the synergies in Canada. The combined company will have the highest quality portfolio, in terms of lowest costs, best jurisdictions and ESG performance, among senior gold companies.

- For $50 million, Maverix agreed to acquire a gold stream from Auramet that will deliver 5,000 ounces of gold to Maverix per year. Maverix will make ongoing cash payments equal to 16% of the spot gold price for each gold ounce delivered. After a total of 50,000 ounces of gold have been delivered to the stream, Auramet will have the option to terminate the stream for a cash payment of $5 million less certain cash flows related to the stream.

- According to Stifel, Pure Gold, on the back of the recently completed C$23 million equity financing, has significantly improved its balance sheet. Based on Stifle’s estimates, Pure Gold will remain compliant with its debt covenants as long as gold prices remain above $1,400 an ounce, with spot prices currently at $1,750.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.7%. Gold slid on a stronger dollar and higher Treasury yields as Federal Reserve officials talked up the prospect of tapering asset purchases. The benchmark 10-year U.S. yield rose to the highest since June on Tuesday, diminishing the allure of non-interest-bearing bullion. European stocks and U.S. futures both sold off, stoking demand for the dollar which climbed to the highest in more than six weeks. The turbulence in markets follows comments on tapering from prominent Fed officials. Governor Lael Brainard and New York Fed President John Williams both said it may soon be time to scale back asset purchases, though also highlighted the impact of the recent resurgence in virus cases. Bullion has struggled this year as central banks signal the stimulus brought in to combat the pandemic will be reined in. It’s now trading near the lowest in more than six weeks, with most of the decline occurring following a Fed meeting at which Chair Jerome Powell said tapering could start soon.

- Wheaton Precious Metals CEO Randy Smallwood says it’s getting “tougher and tougher” for mines to get approval and to get developed, posing the biggest challenge for his company to spend money. Without mines getting developed, and with exploration having a harder time finding new greenfield precious metals deposits, Smallwood says the company won’t have too many other options than to boost the dividend, considering all the cash it is earning.

- Palladium and platinum, precious metals that are used in catalytic, are heading for their fifth straight monthly declines due to the semiconductor shortage that’s curbed automobile production. Palladium is down 23% so far in September, poised for the biggest monthly drop in 13 years.

Opportunities

- Brixton Metals announced new assay results from additional surface rock samples on the Trapper Target. Rock grab sample D131206 assayed 135.5 grams per tonne of gold and 172 grams per tonne of silver. Six rock grab samples returned greater than 10 grams per tonne gold.

- According to Bank of America, news emerged that China is planning to further consolidate its rare earth industry, combining the existing six state-owned enterprises to just two, split between northern and southern regions. Analysts believe this will eventually result in an almost even split on a total rare earth oxide basis, albeit with virtually all heavy rare earth production in the south. While details remain limited at this stage, the bank believes consolidation is aimed at further cleaning up environmental compliance, particularly among heavy rare earth producers. It also believes consolidation will inevitably lead to further supply insecurity, adding further impetus to efforts to onshore supply chains in the U.S. and Europe. This can only be positive for pricing.

- South Africa’s mining industry has given its backing to moving the continent’s most developed economy away from coal but said it must be done gradually and responsibly. South Africa’s economy expanded over the last century through the development of the world’s biggest gold and platinum reserves, which require significant and reliable power supply.

Threats

- Hunan Gold has faced some recent production issues. Two of the company’s units suspended production at concentrating mills recently due to local power curbs, the company said in a statement to the Shenzhen Stock Exchange.

- The mining sector’s tax contribution to the Peruvian economy is lower than other industries, Minister of Energy and Mines Iván Merino told the Congressional Budget and General Account Committee. Mining and hydrocarbon operations account for a high percentage of Peruvian exports and gross domestic product, yet their tax share is just over 21% while other sectors generate 40%, Merino said.

- Centerra Gold said that it filed an application seeking urgent interim measures in its international arbitration against the Kyrgyz Republic and Kyrgyzaltyn OJSC to address alleged operational and safety issues at the Kumtor gold mine. Centerra’s filing seeks to prevent the Kyrgyz Republic and the state-owned gold refiner from damaging the mine’s value and long-term viability, the company said in a statement. “Statements by Kyrgyz officials since the government’s illegal seizure of the Kumtor mine indicate that they are departing from the approved mine plan in ways that will cause irreversible damage. Based on recent reports, the government has also failed to adequately protect the mine’s infrastructure from flooding and other threats and may be facing production difficulties,” said Centerra COO Dan Desjardins in the statement.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2021):

Alibaba Group Holdings

United Airlines

Southwest Airlines

Alaska Air

Delta Air Lines

Wizz Air Holdings Inc.

Spirit Airlines Inc.

Allegiant Travel Co.

Ryanair Holdings PLC

Azul SA

easyJet PLC

Hawaiian Holdings Inc.

American Airlines Group Inc.

The Home Depot Inc.

Nike Inc.

Amazon.com Inc.

Kirkland Lake Gold Ltd.

Maverix Metals Inc.

Pure Gold Mining Inc.

Wheaton Precious Metals Corp.

Brixton Metals Corp.

Centerra Gold Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Bloomberg Galaxy Crypto Index (BGCI) is designed to measure the performance of the largest cryptocurrencies traded in USD.

The Caixin China General Services PMI (Purchasing Managers’ Index) is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private service sector companies. The index tracks variables such as sales, employment, inventories, and prices.

The European PMI Manufacturing Index is derived from original national surveys of manufacturing and service sector business conditions conducted by NTC Research.

CE4 comprises of the main central European nations, which are the Czech Republic, Hungary, Poland, and Romania.

The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies.

The PCE price index, released each month in the Personal Income and Outlays report, reflects changes in the prices of goods and services purchased by consumers in the United States. Quarterly and annual data are included in the GDP release.

The S&P CoreLogic Case-Shiller Home Price Indices are the leading measures of U.S. residential real estate prices, tracking changes in the value of residential real estate nationally.

The Pending Home Sales Index (PHS), a leading indicator of housing activity, measures housing contract activity, and is based on signed real estate contracts for existing single-family homes, condos, and co-ops.

The Richmond Manufacturing Index is an index of manufacturing activity in the Fifth Federal Reserve District, which covers Maryland, North Carolina, the District of Columbia, Virginia, most of West Virginia, and South Carolina..