Gold Projected to Beat the Market in 2020: CLSA

Date Posted: February 7, 2020

Read time: 60 min

Gold will outperform the S&P 500 Index in 2020. That's one of several projections made by CLSA in its just-released "Global Surprises 2020" report.

U.S. Global Investors Announces Quarterly Results Webcast

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Gold will outperform the S&P 500 Index in 2020. That’s one of several projections made by CLSA in its just-released “Global Surprises 2020” report.

The Hong Kong investment firm has an impressive track record when it comes to making market predictions—last year it had a 70 percent hit rate—so it may be prudent to take this one seriously.

I’ll have more to say on this in a moment. First I want to share with you an eye-opening conversation I had this week at Harvard Business School (HBS), where I’ve been attending the annual CEO Presidents’ Seminar and going over case studies involving Netflix, Amazon and more.

As you know, the coronavirus has disrupted day-to-day life in many parts of China and the surrounding region. That includes Hong Kong, whose economy is being served a one-two punch from not just the outbreak but, before that, the months-long protests.

I overheard that the Hong Kong protests go much deeper than a local spat between young college students and the police. Global forces have gotten involved and are actively financing the side they hope to see “win.”

A large number of the protesters, for instance, received training in Oslo, Norway—at the Oslo Freedom Forum—on how best to mobilize activists, keep ranks, deal with police and more. They returned to Hong Kong with a new set of strategies that perpetuated their demonstrations for months, until the coronavirus outbreak brought things to a halt.

Not only that, but the Hong Kong activists’ strategies are being embraced and mimicked by other demonstrators around the world, including those in Spain’s Catalan region. As some people said, young activists there, who seek independence from Spain, have lately copied many of the Hongkongers’ techniques, going so far as to march with umbrellas and occupy Barcelona’s international airport.

Of course, this level of organization and training requires financing from someone with deep pockets. Some believe it could be George Soros, who has a history of supporting similar civil movements around the globe through his Open Society Foundations.

At his annual dinner at the World Economic Forum (WEF) in Davos, Switzerland, the 89-year-old billionaire investor praised the Hong Kong protesters, telling attendees that it’s been a “most successful rebellion,” and that it has “the overwhelming support of the population.”

I don’t know if Soros is personally involved, but it’s worth reminding readers that back in 1998, he tried and failed to break the Hong Kong dollar’s peg to the U.S. dollar. Could he be trying the same right now? Again, I don’t know, but it raises additional uncertainty as well as the question of how much is happening behind the scenes.

Gold: A Valuable Portfolio Hedge to Macro Uncertainty

That brings us back to gold. Writes CLSA’s head of research Shaun Cochran: “If investors are concerned about the role of liquidity in recent equity market strength… gold provides a hedge that could perform across multiple scenarios.”

Indeed, gold is one of the most liquid assets in the world with an average daily trading volume of more than $112 billion, according to the World Gold Council (WGC). That far exceeds the Dow Jones Industrial Average’s daily volume of approximately $23 billion.

The yellow metal, Cochran adds, can be particularly useful in an era of perpetually loose monetary policy: “[I]n the event that growth disappoints the market’s expectations, gold is positively leveraged to the inevitable policy response of lower rates and larger central bank balance sheets.”

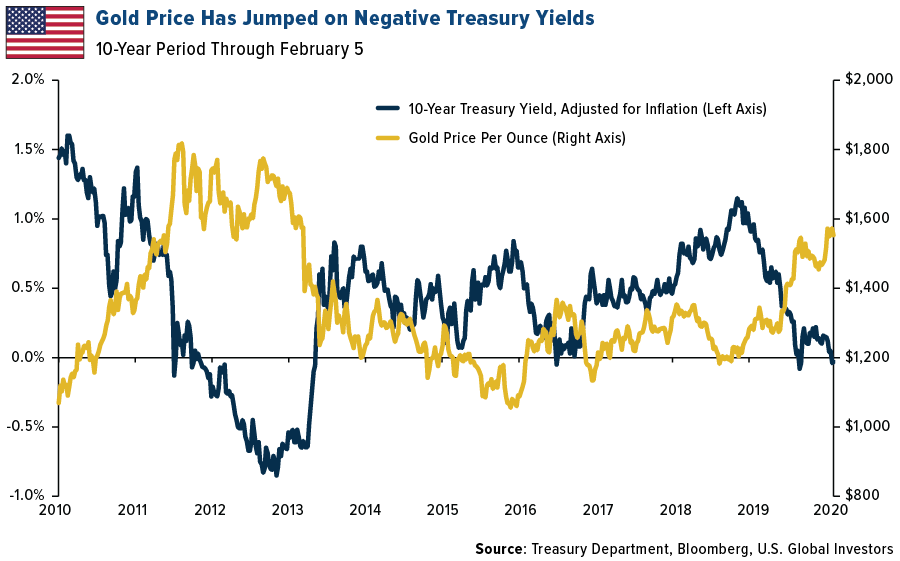

As I’ve pointed out many times before, gold has traded inversely with government bond yields. The recent gold rally has largely been driven by the growing pool of negative-yielding government debt around the world, now standing at $13 trillion. Here in the U.S., the nominal yield on the 10-year Treasury has remained positive, but when adjusted for inflation, it’s recently turned negative, despite a strengthening economy. What’s more, the Federal Reserve’s balance sheet has begun to increase again. It now holds about 30 percent of outstanding Treasury debt, up from about 10 percent prior to the financial crisis.

I can’t say whether gold will beat the S&P this year or next, but what I do know is that the yellow metal has been a wise long-term investment. For the 20-year period through the end of 2019, gold crushed the market two-to-one, returning 451.8 percent compared to the S&P’s 223.6 percent. That comes out to a compound annual growth rate (CAGR) of 8.78 percent for gold, 4.03 percent for the S&P.

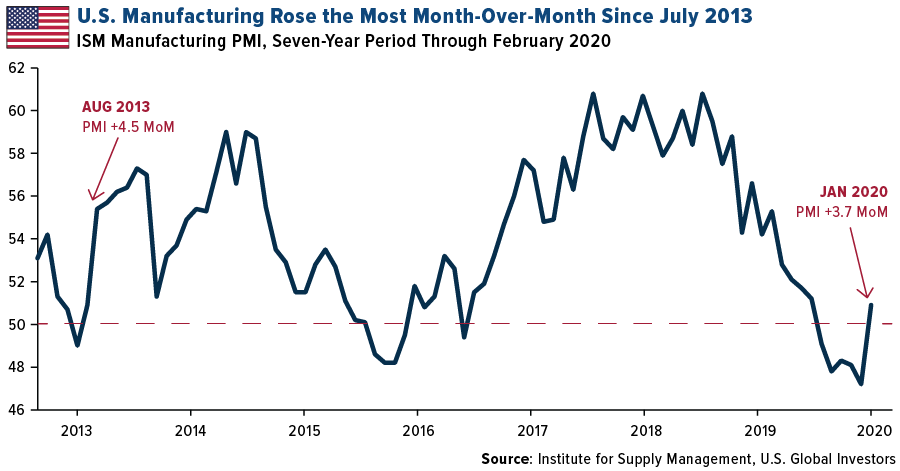

Manufacturing Turnaround Has Begun

U.S. manufacturers started 2020 on stronger footing, a welcome turnaround after contracting for five straight months. January’s ISM manufacturing purchasing manager’s index (PMI) clocked in at 50.9, indicating slight growth. Up from 47.2 in December, this represents the biggest month-over-month jump since August 2013, when the PMI increased to 55.4 from 50.9 in July.

This may also mark the end of the recent manufacturing bear market, prompted by the trade war between the U.S. and China. Although relations between the world’s two biggest superpowers remain strained, to say the least, we’ve seen improvements lately that hint at better days. Both sides signed a “Phase One” agreement in mid-January, and this week, China announced it would be cutting tariffs in half on as much as $75 billion of U.S.-imported products.

The coronavirus is a new development that has disrupted global trade, but there’s reason to be optimistic, as the PMI makes clear.

To read my full comments on the coronavirus, and its impact on Chinese and Hong Kong stocks, click here!

Gold Market

This week spot gold closed at $1,570.44, down $18.72 per ounce, or 1.18 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.34 percent. The S&P/TSX Venture Index came in off just 0.18 percent. The U.S. Trade-Weighted Dollar surged 1.36 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-2 | Caixin China PMI Mfg | 51.0 | 51.5 | 51.5 |

| Feb-3 | ISM Manufacturing | 48.5 | 50.9 | 47.8 |

| Feb-4 | Durable Goods Orders | 2.4% | 2.4% | 2.4% |

| Feb-5 | ADP Employment Change | 157k | 291k | 199k |

| Feb-6 | Initial Jobless Claims | 215k | 202k | 217k |

| Feb-7 | Change in Nonfarm Payrolls | 165k | 225k | 147k |

| Feb-13 | Germany CPI YoY | 1.7% | — | 1.7% |

| Feb-13 | CPI YoY | 2.5% | — | 2.3% |

| Feb-13 | Initial Jobless Claims | 210k | — | 202k |

Strengths

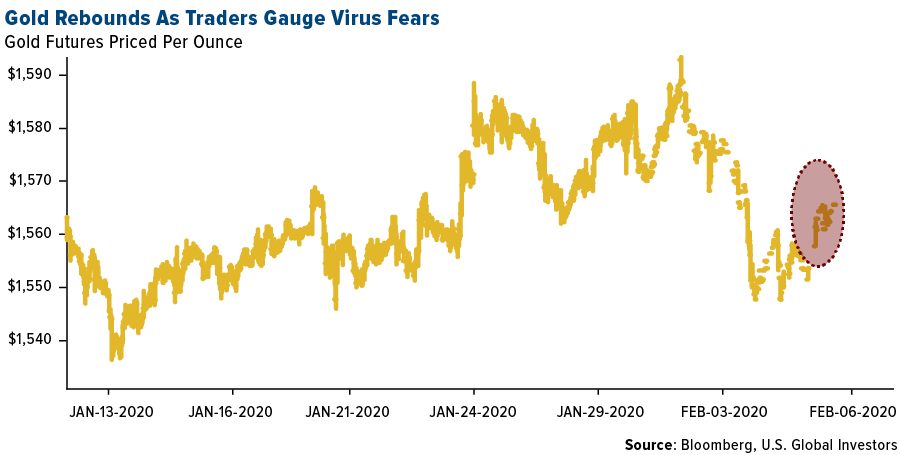

- The best performing metal this week was palladium, up 1.44 percent as Jeffrey Currie, head of global commodities research at Goldman Sachs, commented he sees the potential for palladium to test $3,000. With Friday’s gain, gold saw a third straight day of positive momentum as concerns of economic fallout surrounding coronavirus outweighed stronger-than-expected U.S. job gains. Holdings in gold-backed ETFs surpassed the record set in 2012, hitting 2,573.9 tons on Monday, according to Bloomberg data.

- Russia’s gold reserves grew in January to $562.3 billion, up from $554.4 billion in December. China’s gold reserves remained flat over the same time period. Turkey’s holdings in gold rose $680 million from the previous week to now total $27.5 billion as of January 31.

- Calibre Mining Corp announced initial drill results from its El Limon project in Nicaragua, including 18.65 grams per ton of gold over 5.1 meters. CEO Russell Ball said in the press release: “We ramped up the program significantly in January and I am confident that our 2020 drilling campaign will deliver positive results in this world-class, low sulfidation epithermal district.”

Weaknesses

- The worst performing metal this week was silver, down 1.89 percent despite hedge funds boosting their bullish positioning in the metal this past week. The price of gold fell early in the week over fears that the coronavirus would hamper Chinese demand for the yellow metal. Analysts at Citigroup Inc. wrote in a note this week that “retail coin and jewelry demand in Asia is a negative risk for gold markets, particularly in China where gold premiums have started to soften given GDP downgrades and coronavirus risks.” China is the world’s top consumer of gold.

- India’s gold imports fell to 21.7 tons in January from 45.9 tons a year earlier – a drop of 53 percent. Bloomberg writes that record-high domestic prices and a slowdown in economic growth are behind dramatic decrease. The World Gold Council (WGC) recently showed that full-year purchases fell 14 percent in 2019. Americas Gold and Silver Corp., a North American precious metals producer, said that it has temporarily stopped mining and processing at its Cosala Operations in Mexico due to a blockade by workers at the facility. JPMorgan Chase & Co might face criminal charges and be subject to fines regarding its involvement with alleged manipulation in the precious metals market, reports Bloomberg News.

- According to a report by law firm Bryan Cave Leighton Paisner, private equity investments in mining fell to $500 million in 2019, down from $2 billion the year prior – a drop of 75 percent. The firm said private equity is now focused on raising additional funds for existing investments rather than looking for new deals.

Opportunities

- The London Bullion Market Association (LMBA) released its gold price forecasts for 2020 and the consensus is looking for double-digit increases. The average forecast is $1,558.90 an ounce, with the highest at $2,080 and the lowest at $1,300. Analysts are expecting more volatility, as the range between the high and low prices is $780, much bigger than last year’s range of $325.

- Anglo American Platinum Ltd. CEO Chris Griffith said in an interview this week that the rally in palladium isn’t a bubble because there is still a supply deficit of about 1 million ounces. “That’s a massive shortfall, and that’s making prices rise.” Griffith added that prices will be supported until automakers start substituting palladium with platinum.

- Bloomberg reports that AngloGold Ashanti Ltd. is moving away from South Africa and instead toward the Americas. The world’s third largest gold producer is looking at projects in Colombia and Nevada, according to CEO Kelvin Dushnisky. “The market will always be receptive to good projects, and there are quality assets. The reason we want to bring them into production is part of our objective to bring new, longer life, lower-cost operations.” AngloGold has just one mine left in South Africa and is looking for a buyer. Angolan state-owned diamond mining company Endiama EP is looking at selling as much as 30 percent of its shares in an IPO in 2022, reports Bloomberg.

Threats

- Barrick Gold CEO Mark Bristow confirmed that the company is not planning on merging with Freeport-McMoran, but that he is interested in Grasberg mine in Indonesia. Bristow said “if you’re going to be a world-class gold miner, you’re going to have to accept copper. In ten years’ time the most strategic metal on this planet is copper, if you believe the EV story, and I do.” The Freeport Grasberg mine in Indonesia is a tier-one copper asset because it is high grade and has a long life. However, the mine might not be the best potential acquisition, as Indonesia likely would not be considered a tier-one location by the market.

- Sibanye Gold Ltd. CEO Neal Froneman expressed that South Africa’s president is running out of time to attract investments in the country’s mining industry, reports Bloomberg. “There has been a distinct lack of turnaround, if anything we have gone backward.” Sibanye is increasingly looking at doing business in West Africa, the Americas and Australia due to the risks of weak economic growth and high debt in his home country.

- The Commerce Department announced on Monday that the Trump administration is moving ahead with new rules that would clear the way for the U.S. to apply punitive tariffs on goods from countries accused of having undervalued currencies, reports Bloomberg News. The rules would allow the U.S. to impose duties on goods from countries accused of manipulating their currencies, even in cases the country hasn’t been found guilty of doing so by the U.S. Treasury.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.00 percent. The S&P 500 Stock Index rose 3.17 percent, while the Nasdaq Composite climbed 4.04 percent. The Russell 2000 small capitalization index gained 2.65 percent this week.

- The Hang Seng Composite gained 4.58 percent this week; while Taiwan was up 1.02 percent and the KOSPI rose 4.39 percent.

- The 10-year Treasury bond yield rose 7 basis points to 1.583 percent.

Domestic Equity Market

Strengths

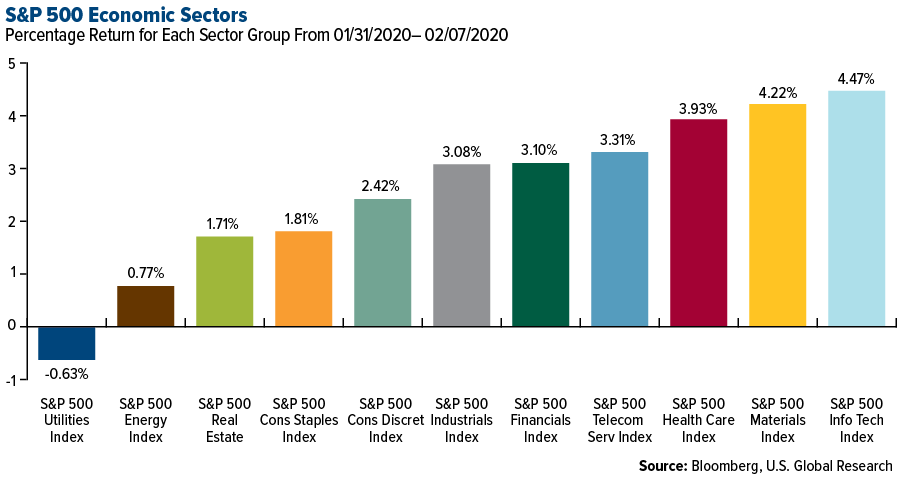

- Information technology was the best performing sector of the week, increasing 4.47 percent compared to an overall increase of 3.26 percent for the S&P 500 Index.

- Biogen was the best performing S&P 500 stock for the week, increasing 25.98 percent.

- Shares of Unisys jumped 49 percent intraday on Thursday after Science Applications International Corp. (SAIC), which provides information technology and government support services, said on Thursday it plans to acquire the company’s federal government business in an all-cash deal valued at $1.2 billion. Unisys Federal, a unit of Unisys, provides various IT services to federal civilian agencies and the Department of Defense. SAIC said the acquisition will help improve its services in government priority areas, as well as expand its portfolio of intellectual property and technology-driven offerings.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing 0.63 percent.

- NortonLifeLock was the worst performing S&P 500 stock for the week, falling 30.58 percent.

- Shares of Plantronics tumbled more than 30 percent on Wednesday after the headset and videoconferencing hardware provider reported its fiscal third-quarter results. Both revenue and earnings declined sharply, with revenue coming in below analyst expectations. Plantronics reported third-quarter revenue of $384.5 million, down 23.4 percent year-over-year, and $14.7 million below the average analyst estimate.

Opportunities

- Energy producers have almost completed a 20-year round trip relative to technology companies within the S&P 500 Index. The ratio between their S&P 500 industry-group indexes fell this week to its lowest level since March 2000, when an internet-driven bull market peaked. The low followed the ratio’s 87 percent retreat from a high in July 2008, when oil traded at a record $147.27 a barrel in New York. “Can energy stage a rally while tech falls? We think so,” Jonathan Krinsky, chief market technician at Bay Crest Partners, wrote in a report that highlighted the ratio.

- The three biggest U.S. drug distributors, mired in litigation over their role in the opioid crisis, got more good news this week with an upgrade on Wall Street from an analyst at Baird. “Yes, no kidding, we’re back on board,” analyst Eric Coldwell wrote in a research note upgrading Cardinal Health Inc., AmerisourceBergen Corp. and McKesson Corp. to outperform from neutral. The three had a healthy run this week as fears that the Trump administration would push forward on a plan to rein in rising Medicare drug costs by tying them to international prices faded. AmerisourceBergen was up nearly 10 percent since Monday while McKesson advanced 11 percent. Cardinal Health jumped 17 percent and was on track to have its biggest five-day gain since 2004 after a guidance increase that beat the highest analysts’ estimates.

- Ericsson and Nokia were top performers on the Stoxx 600 Tech Index, rising as much as 5 percent and 5.7 percent respectively after U.S. Attorney General William Barr said the U.S. should consider investments in the two companies to speed up development of 5G alternatives to Chinese technology.

Threats

- Analysts predicted more tough times for luxury companies after Burberry Group Plc scrapped its full-year guidance because of coronavirus concerns. Coronavirus worries were already weighing on Burberry, which gets about 40 percent of sales from China’s shoppers. The stock is now down about 10 percent since the end of last year.

- Intelsat SA was cut to underweight from neutral at JPMorgan, which wrote that it saw “little to no fundamental equity value” in the stock after the firm examined a C-band proposal from Federal Communications Commission (FCC) Chairman Ajit Pai. JPMorgan wrote this plan was “well below” its estimate and analyst Philip Cusick noted that the money would come over time, rather than up front, “rendering Intelsat’s equity worth little given its debt load, its leverage, and its very challenged fundamental satellite business.”

- Big banks will need to contend with harsher scenarios in this year’s Federal Reserve stress tests, analysts say. That may mean some risk for Goldman Sachs Group Inc., Morgan Stanley and Citigroup Inc., while PNC Financial Services Group might fare well. Banks will have to submit their stress test plans by April 6, and the results will be announced by June 30.

The Economy and Bond Market

Strengths

- The U.S. labor market started 2020 off strong, adding a stronger-than-expected 225,000 workers in the month of January, after an upwardly revised 147,000 gain the prior month, according to the Labor Department on Friday.

- U.S. factory activity unexpectedly rebounded in January after contracting for five straight months, writes the NY Times, amid a surge in new orders. This news offers hope that a prolonged slump in business investment has probably bottomed out. The Institute for Supply Management (ISM) said on Monday its index of national factory activity increased to a reading of 50.9 last month, the highest level since July.

- U.S. services sector activity picked up in January, with industries reporting increases in new orders, writes Reuters, suggesting the economy could continue to grow moderately this year even as consumer spending is slowing. The Institute for Supply Management (ISM) said on Wednesday its non-manufacturing activity index increased to a reading of 55.5 last month, the highest level since August.

Weaknesses

- For the full year of 2019, U.S. construction spending totaled $1.303 trillion, down 0.3 percent from the 2018 total. Private residential spending declined 4.7 percent for the year, private nonresidential spending was flat, and public construction spending increased 7.1 percent.

- The Federal Reserve has warned that "spillovers" from the coronavirus outbreak are risky to both the global and U.S. economic outlook, reports TheStreet. It added that the recent emergence of the coronavirus could lead to disruptions in China that spill over to the rest of the global economy.

- Economic activity shrank in eight states and was stagnant in three others during the fourth quarter, according to the latest data from the Federal Reserve Bank of Philadelphia. West Virginia’s economy contracted most, reports Bloomberg, while a decline in neighboring Pennsylvania was among the worst in the nation, based on state coincident economic indexes. Economies in Delaware, Iowa, Montana, Missouri, Oklahoma, and Vermont also decline compared with three months earlier.

Opportunities

- CPI inflation has been diverging from PCE inflation – the Fed’s preferred inflation metric – in recent months and the headline rate is forecast to have edged up further in January to 2.4 percent year-on-year. However, the core rate is expected to have moderated slightly to 2.2 percent.

- Democrats signaled that they would deliver a big boon to the municipal bond market if they’re able to get their infrastructure plans through Congress. Key committees of the House of Representatives released a framework for a $760 billion infrastructure plan for roads, railways and airports that would help spur sales of state and local government debt.

- Citigroup analysts said in a note to clients that municipal bonds may return more than 8 percent in 2020 as cash continues surging into the market. “The ongoing intense, prolonged rally, has led to gluttonous demand for tax-exempt paper, which has engendered strong performance, and is leading to more demand,” the analysts wrote. Citigroup is the second biggest municipal bond underwriter.

Threats

- China’s central bank may have managed to stabilize the markets by injecting billions of dollars into the financial system, but investors will still be keeping a close watch on how successful authorities are in curbing the spread of the coronavirus. The longer it takes to bring the situation under control, the longer many businesses will remain shut, hence the bigger the disruption to the domestic economy and to global supply chains.

- January retail sales figures on Friday will be important as they are seen as a reliable barometer of consumer spending. Retail sales are forecast to have increased by 0.3 percent month-on-month in January, reports FXStreet. However, a miss in the retail sales numbers would pose a major downside risk as it would raise concerns about the health of the U.S. consumer amid a weak global economic environment.

- Attorney General William P. Barr said Thursday that China’s dominance of 5G telecommunications networks was one of America’s top national security and economic threats, reports the NY Times, amplifying warnings issued for years by intelligence officials but that President Trump has sometimes undermined. Mr. Barr said that allowing China to establish dominance was not only a “monumental danger” as Beijing could use the technology for monitoring and surveillance, but also that “the stakes are far higher than that.”

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, which gained 8.03 percent on concerns over declining stockpiles and weak production from Malaysia. Equinor ASA, the Norwegian state-controlled oil producer, is for the first time setting a target for carbon emission cuts that also includes the end use of the product it sells. Bloomberg reports that the company initially resisted the move, but succumbed to pressure from shareholders and investors. “We need to build a business that is resilient, that is competitive and can offer consistent cash-generation capacity through the energy transition,” said CEO Eldar Saetre in a Bloomberg TV interview.

- In more green news, California homebuilders are rushing to get ahead of the new state mandate that requires almost all new homes to have solar power. According to the Construction Industry Research Board, permits issued for new single-family homes rose 56 percent in December from a year earlier. BloombergNEF research shows that emissions from electricity generation in Spain were 23 percent lower in 2019 than the year before, largely due to a reduction in output by coal power plants. Less than a month after announcing it would cut coal investments, BlackRock Inc. cut its 5 percent stake in Peabody Energy Corp, the U.S.’s biggest coal miner.

- According to China’s Ministry of Finance, China will cut tariffs in half on $75 billion of imports from the U.S. on February 14, reciprocating what the U.S. is doing and satisfying part of the Phase One trade deal. Although tariffs will still remain on both sides, many are dropping to 5 percent from 10 percent and others from 5 percent to 2.5 percent.

Weaknesses

- The worst performing major commodity for the week was iron ore, which fell 11.15 percent as steel production in China has been curtailed. Bloomberg reports that according to people with inside knowledge of China’s energy industry, demand for oil in China has dropped by about three million barrels a day, or 20 percent of consumption. The price of oil has been hit particularly hard by the coronavirus fears hampering demand for commodities. John Kilduff, a partner at Again Capital LLC, said “it is truly a black swan event for the oil market” and that “if there are no further production cuts, there will only be more price losses.” Additionally, China refiners are processing 15 percent less crude than before the outbreak. Russia is expected to announce soon whether or not it plans to cut production.

- Another consequence of the coronavirus outbreak is disrupted trade, as Chinese companies have started walking away from purchase contracts. Bloomberg reports that a Chinese buyer of LNG and a copper importer declared force majeure, which means they are reneging on deals as the virus hampers their ability to take deliveries. Jan Stuart, global energy economist at Cornerstone Macro, said “this is an entirely different risk, especially in commodities where China’s role dominates.” China consumes more iron than the rest of the world combined and is also a giant consumer of coal, LNG and crude oil.

- According to Norsk Hydro ASA, a top aluminum producer, demand is forecast to remain stagnant in 2020. The aluminum market sharply slowed down in 2019 due to the trade war, falling car sales and slow European economies, reports Bloomberg. Norsk Hydro CEO said that it is too early to estimate the impact of the coronavirus, but they do expect weak demand in the first quarter and through the year.

Opportunities

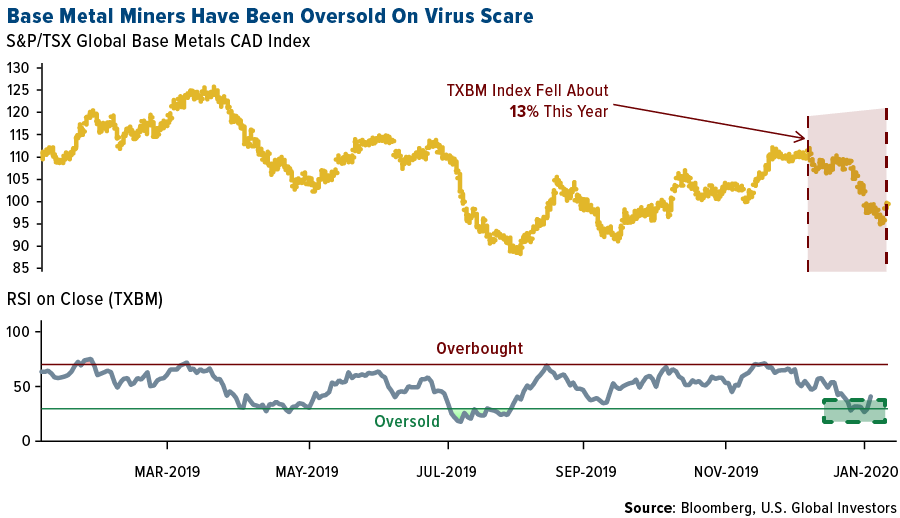

- Bloomberg’s Aoyon Ashraf writes that the entry point for investing in metals and miners might be here, but that analysts recommend caution. According to the relative strength indicator, base metal miners have been oversold on the coronavirus scare. BMO’s Colin Hamilton and Jackie Przybylowski wrote in a note that they feel “there will be an opportunity to increase industrial metals exposure, but only after the spread of the virus is under control.”

- According to the U.S. Assistant Secretary of Fossil Energy Steven Winberg, the best way to reduce the amount of natural gas flaring is to build more infrastructure and pipelines to get the fuel to end-users. Winberg said: “pipelines are clearly the answer.” The practice of flaring gas into the air has surged as natural gas production has grown faster than the construction of pipelines to take the gas away.

- After analyzing 15 years of data from 8,000 French manufacturers, economists at the OECD found that when energy costs rise 10 percent, emissions fall 9 percent, reports Bloomberg. The study also found that there is no net loss of employment in the sector. France is a key nation to analyze as it has a 45 euro tax per ton of carbon dioxide. Damien Dussaux, lead author of the OECD paper, said the analysis shows that “the rise in energy prices triggers a reallocation of production and workers from energy-intensive to energy-efficient firms.” Bloomberg’s William Horobin writes that this demonstrates a lesson for governments in balancing climate change and economic demands, where a carbon tax doesn’t necessarily mean a loss of jobs.

Threats

- The Energy and Resources Institute said in a report that India’s steel industry is set to more than triple its carbon footprint by 2050. Due to growing demand, carbon dioxide emissions from the country’s steel industry – the world’s second largest producer – is estimated to increase to 837 million tons over the next 30 years from 242 million tons now. Bloomberg reports that India currently has 977 steel plants and is a strong source of demand.

- According to a report from Jefferies Financial Group Inc., even if countries aggressively tighten regulations, the world will still struggle to recycle just 50 percent of its plastic waste in 10 years. “The impact of plastics leaking into the environment, polluting oceans, and entering the food chain could potentially be almost as big a concern for civil society as climate change.” The report added that almost all of the eight billion tons of plastic ever produced still exist in either a landfill or the environment.

- In December federal regulators approved Florida Power & Light Co.’s request to keep its twin nuclear reactors in operation for 20 more years, which would make them 80 years old at the end of the license. Bloomberg reports that this would make the U.S. the country with the oldest nuclear power plants, which is of concern because reactors were not designed to stay in use for that duration.

Emerging Europe

Strengths

- The Czech Republic was the best relative performing country this week, gaining 3.6 percent. Outperformance of the Prague exchange was attributable to foreign stocks listed on the exchange. Avast PLC, a British cyber-security software company, gained 7 percent over the past five days after losing 22 percent last week due to accusations that it collected data on what many of its users did online and sent it to Jumpshot, which then offered to sell the information to clients. Erste Group, the Austrian bank listed on the Prague exchange, gained 5.3 percent

- The Russian ruble was the best relative performing currency this week, losing 15 basis points. The ruble dropped the most on Friday after the U.S. indicated it may impose sanctions on Russia’s’ state-owned oil producer Rosneft for maintaining its ties with Venezuela. Rosneft is Venezuela’s main shipper of crude.

- Consumer services was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 2 basis points. Romanian’s minority government was ousted just three months after taking power, as the Prime Minister lost a no-confidence vote on Wednesday. Romania has had a lot of political chaos. It has had more prime ministers than any other European Union member-state in the three decades since communism collapsed.

- The Hungarian forint was the worst performing currency in the region this week, losing 1.6 percent. Industrial production dropped 3.7 percent in December on year-over-year basis, with the car industry contracting significantly, as German December factory orders fell at the fastest pace in more than a decade.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

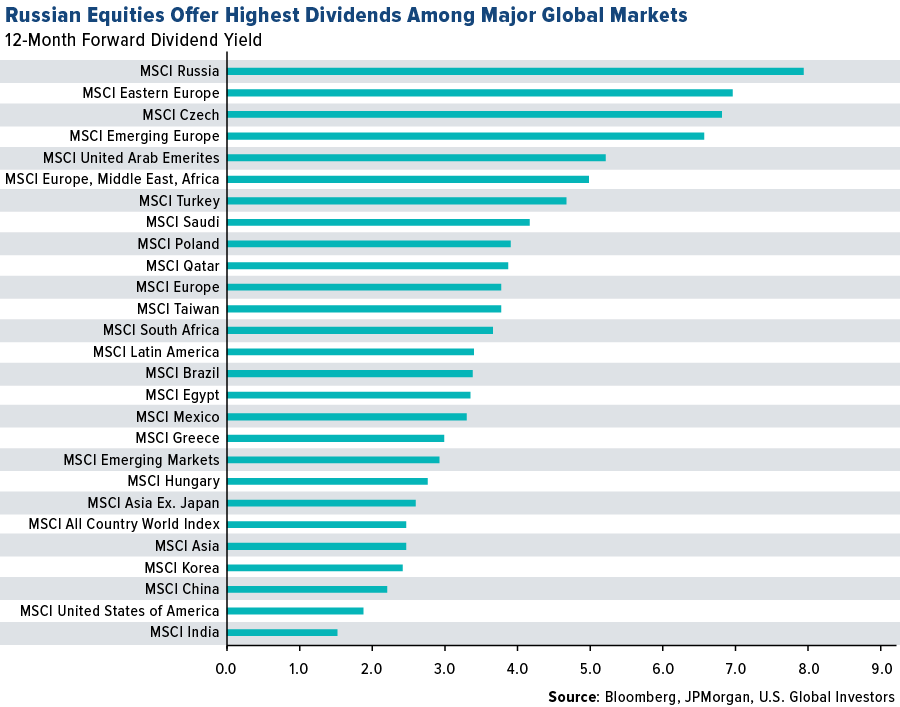

- Russia offers the highest dividend yields among major emerging global markets and JPMorgan recommends investors overweight Russian equites. MSCI Russia yields 7.9 percent, which is above where it stood this time last year, which was 7.2 percent. Most importantly, JPMorgan’s research team thinks that Russia can outgrow CEEMEA dividends going forward.

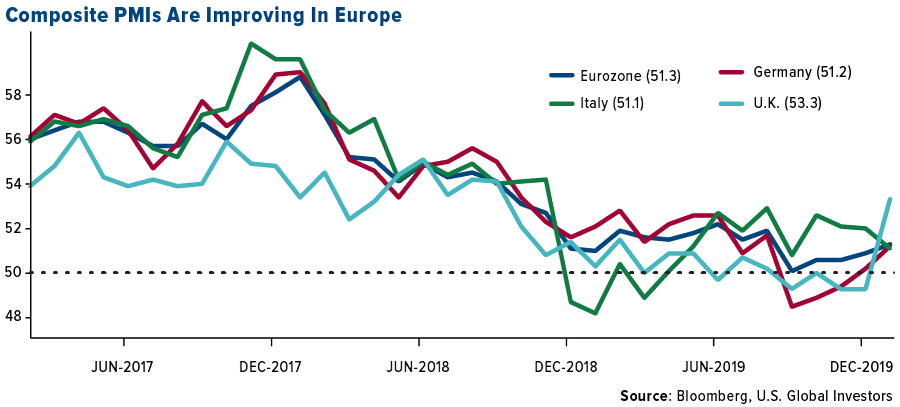

- Composite PMIs, which combine Manufacturing and Service activities in Europe, are improving. The United Kingdom noticed the biggest jump in service PMI in the month of December, pushing the Composite PMI to 53.9, the highest level since September 2018. Germany’s Composite PMI moved higher too, while Italy’s dropped slightly but remains above the 50 level that separates growth from contraction.

- Greece’s 10-year government bond yield fell more than four basis points to 1.143 percent, a new record low. Fitch upgraded ratings on Greek bonds last month, but they are still rated “junk” by all major rating agencies. However, the rating revisions may accelerate and soon Greek bonds could meet the European Central Bank’s (ECB) requirement, investment grade rating, to be eligible to participate in the EU’s bond-buying program.

Threats

- Turkey is working on a broad overhaul of laws regulating its banking industry and capital markets. The proposal submitted by the president to the parliament will significantly increase regulatory authorities’ sway over the nation’s lenders, according to Bloomberg news. The central bank will now set fees and commission charged by lenders to clients, increasing the monetary authority’s power over stream that accounts for about 12 percent of total banking revenue.

- Polish President Andrzej Duda on Tuesday signed into law a much-criticized legislation that gives politicians the power to fine and fire judges whose actions and decisions they consider harmful. The same day, the new Disciplinary Chamber of the Supreme Court ruled to suspend Judge Pawel Juszczysnki who has raised questions about some recent politicized judicial appointments, and cut 40 percent of his earning, as a fine.

- Tensions between Russia and Turkey escalated after seven Turkish soldiers were killed in Syria. Turkish President Erdogan asked the President of Syria Assad to pull back forces fighting in Idlib with Russia support by the end of this month. Turkey and Russia have worked hard to improve the strained relationship after Turkey shot down a Russian warplane back in 2015, but the conflict in Syria complicated the delicate relationship between both countries.

China Region

Strengths

- In a snapback week of moderate optimism but somewhat negative headlines, Hong Kong’s Hang Seng closed up 4.58 percent on the week. Korea’s KOSPI jumped 4.39 percent, and the Philippine Stock Exchange PSEi Index climbed 4.26 percent.

- Information technology was the name of the game for Hong Kong’s HSCI snapback this week, jumping 7.71 percent.

- The Markit Philippines Manufacturing PMI came in better than last time, rising to 52.1 from a prior 51.7.

Weaknesses

- Shanghai finished this week’s trading down “only” 3.38 percent since the 23rd of January (the last time the Shanghai Composite traded heading into the holidays), though markets did reopen down significantly further earlier in the week on Monday.

- Utilities barely eked out a gain in Hong Kong, rising 4 basis points as that sector finished out as the weakest relative performer for the HSCI on the week.

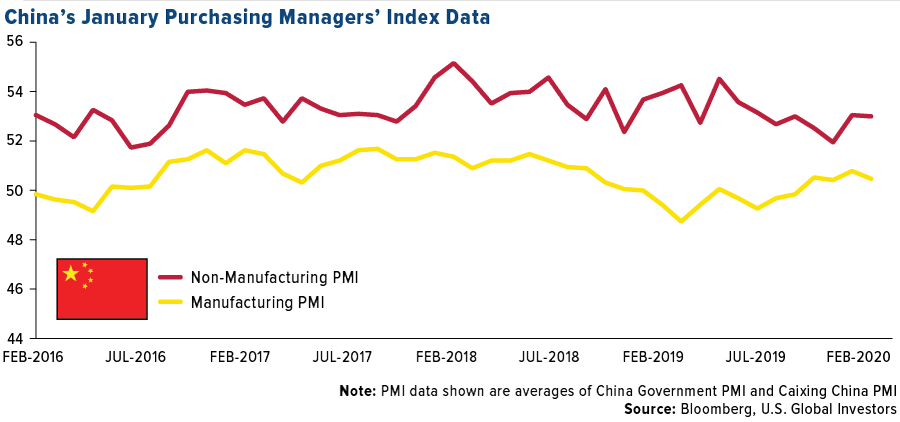

- This week the Caixin China Services PMI came in at a 51.8, a little shy of expectations for a 52.0 print and down from last month’s 52.5. You may also recall that last week we got China’s latest official Manufacturing PMI, which—though measuring the period prior to the exponential increase in coronavirus cases and the New Year holidays—dropped to 50.0, right on the edge of contraction, and that was before the exponential rise in viral cases and the lockdown and holidays.

Opportunites

- Presidents Donald Trump and Xi Jinping reportedly spoke about the Wuhan coronavirus among other things in a telephone conversation this week, but one opportunity may perhaps lie in that the Phase One import levels by China of U.S. exports is supposedly still on.

- And just like that, Korea’s KOSPI is back to little more than 2 percent off of its 52-week highs.

- A quick snapback or reassessment in sentiment and valuation remains possible if and when the coronavirus outbreak peaks and resumption of relative normalcy seems a little closer.

Threats

- Our 2019-nCoV (better known as the Wuhan coronavirus) update of the week brings the sad news that cases confirmed globally are now up to well over 30,000 people with a death count that has surpassed 600. While this week did see the first reports of confirmed deaths outside of China, most of the severe cases and deaths have been in mainland China. This week also saw the tragic death (due to coronavirus infection) of 34 year-old Chinese doctor Li Wenliang, who—along with seven other doctors (that collectively blew the whistle, so to speak, on the Wuhan outbreak)—had been sanctioned by local authorities after alerting people about the disease last month.

- We are now through the Iowa Caucus (or are we?) with New Hampshire in sight and Nevada and South Carolina not too far behind. Super Tuesday looms ominously beyond, and as of right now, no one knows what lurks beyond that. Is this a threat? Hardly. But here’s a conceivable scenario to consider: By the time that coronavirus concerns and domestic political battles play out over the coming weeks (months?), and everyone is getting around to wondering how much to ding first-quarter Chinese growth by (and by extension, perhaps global growth), and wondering about how precisely Phase One is working out, and so on, U.S. domestic politics could start to shift more toward inclusion of a bit of foreign policy discussion and bam, just like that, people could be arguing over who could be tougher on China even as the East Asian behemoth is still licking its wounds. Of course, that’s not to say things play out that way at all. But it’s conceivable. At the end of the day, the point is this: The Phase One honeymoon period may well have been cut short by viral infection, and should markets spend this interim period convalescing, so to speak, the honeymoon stretch could devolve into an unfortunate spat if certain issues go unresolved.

- The U.S. dollar jumped this week to new multi-month highs, hitting levels last seen in October. Amid a degree of risk-off sentiment and virus concerns, this could weigh on emerging markets in the interim.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 7 was Acute Angle cloud, up 190.74 percent.

- New data from both BitPay and Coinbase show that bitcoin usage among merchants is up, reports CoinDesk. According to BitPay Chief Marketing Officer Bill Zielke, the payment processor facilitated $1 billion worth of cryptocurrency transactions in 2019, while a Coinbase spokesperson said that Coinbase Commerce processed $135 million worth of cryptocurrency payments for thousands of merchants in 2019.

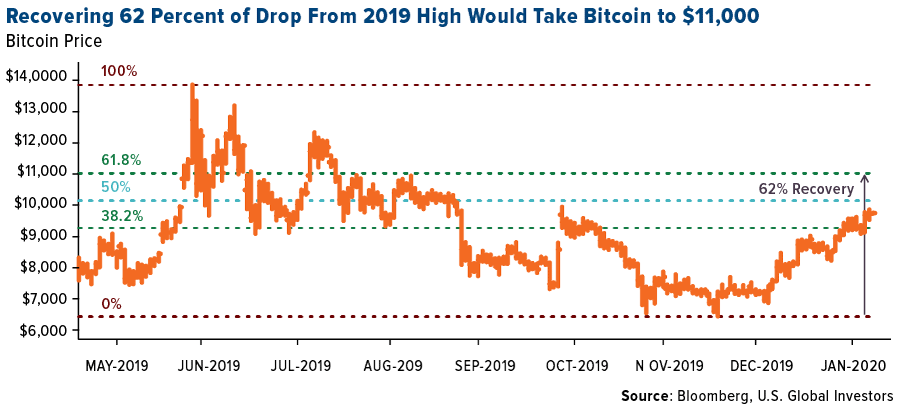

- Fundstrat Global Advisors’ top chartist Rob Sluymer believes that bitcoin is poised to continue its rally to a range of $10,000 – $11,000 based on previous recoveries, reports Bloomberg. “Bitcoin appears to be in a textbook re-acceleration,” Sluymer wrote in a note Wednesday. The pullback should be relatively shallow, followed by “resuming its longer-term uptrend into year-end.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 7 was TCOIN, down 74.02 percent.

- At the start of the week, bitcoin’s price action told a tale of buyer exhaustion, writes CoinDesk, hinting at a more major price pullback ahead. On Monday, the popular digital currency produced a “doji” candle, which indicates bull fatigue and shifting risk in favor of a stronger price pullback.

- Concerns over coronavirus have continued impacting lives and businesses in the China region, with the cryptocurrency industry as no exception, reports CoinDesk. On Thursday, an announcement was released that the TOKEN2049 conference to be held in Hong Kong on March 17-18, has now been rescheduled for October over outbreak concerns. This news comes just days after it was announced that Binance would be forced to postpone its Binance Blockchain Week Vietnam, slated for February 29, the article continues.

Opportunities

- In an announcement on January 30, researchers at the Massachusetts Institute of Technology (MIT) claim to have created a new cryptocurrency-routing scheme to speed up blockchain-based transactions, reports CoinTelegraph. The new solution is called “payment channel networks” (PCN) and is said to not only notably reduce transaction times, but also boost profits and perform with minimal involvement from the blockchain.

- According to one of bitcoin’s best-known supporters, bitcoin is primed for average gains of nearly 200 percent over the next six months, reports CoinTelegraph. Tom Lee, co-founder of Fundstrat Global Advisors, told Yahoo! Finance that one bullish technical factor, in particular, made him “really optimistic” about the digital currency’s short-term potential. “Notably in January – January is usually a weak month, it was a great month for bitcoin, up 26 percent – but it also recovered its 200-day moving average,” Lee said.

- Mike McGlone of Bloomberg Intelligence is tracking parallels between Tesla and Bitcoin in a new edition of Charting Futures. McGlone comments that the pair are the “most significant disruptive technologies on the planet” and therefore it’s no surprise to see their valuations experience massive boom and bust cycles.

Threats

- Chinese manufacturers are seeing rising demand for new equipment ahead of bitcoin’s scheduled halving in May, writes CoinDesk, but if the outbreak of coronavirus isn’t resolved in the near future it could prove difficult to expand or build new machines. General Manager of Canaan Creative’s blockchain arm Kevin Shao told CoinDesk that while there is little doubt miners can maintain the current level of computing power, there is a shortage of new mining machines.

- After being acquitted, now a Japanese court wants a man who infected website visitors with cryptocurrency mining malware to face justice, reports CoinTelegraph. As reported on February 7, the Tokyo High Court overturned a previous ruling which cleared the man of any wrongdoing. “Visitors were not informed of (the mining program) or given the chance to reject it,” The Mainichi news outlet quoted Presiding Judge Tsutomu Tochigi as saying.

- Bitspark, a Hong Kong-based blockchain remittance startup, has abruptly announced its closure, reports CoinTelegraph, citing internal restructuring issues. According to the official statement released February 3, Bitspark users will be able to withdraw their cryptocurrencies from Feb. 3 to March 4 as the platform’s functionality will stay intact over that period. After March 4, however, account logins will be disabled for a period of 90 days, with users being able to withdraw funds via Bitspark customer support, the announcement continues.

Airline Sector

Strengths

- London Heathrow, Europe’s busiest airport, has implemented a drone-blocking system to detect threats entering its airspace. The airport had a string of attempts by drones to enter the area in 2019. The new system, designed by France’s Thales SA, can detect and identify drones as far as 5 kilometers away and is already in use at Paris’s Charles de Gaulle airport.

- Delta Air Lines reported stronger-than-expected fourth quarter earnings, with revenue from business cabin tickets and other premium products rising 9 percent. The carrier was boosted by strong ticket sales and robust domestic demand. Delta has benefited from not flying the Boeing 737 Max, which has negatively impacted other major carriers.

- JetBlue increased the cost for travelers checking a first and second bag by $5 to $35 and $45, respectively. Bloomberg reports that other airlines will likely follow suit and raise prices too. JetBlue was the first major U.S. carrier to charge as much as $30 for checking a single bag, and other airlines quickly copied the move. Although negative for consumers, it is positive for carriers in potentially helping boost ancillary revenues.

Weaknesses

- Kyviv-bound Ukraine International Airlines Flight 752 was accidentally shot down by the Iranian military shortly after taking off from Tehran on January 8 – just days after Iran fired more than a dozen missiles at two Iraqi military bases housing U.S. forces. It took several days for Iran to confirm that two missiles struck the plane and said it was due to human error. All 176 people on board were killed and were mostly Canadian or Iranian nationals. The incident led to several countries diverting flights in the area.

- According to internal communications at Lion Air, the Indonesian airline considered putting its pilots through simulator training in 2017 before flying the Boeing 737 MAX, but abandoned the idea after Boeing convinced them it was unnecessary. Just a year later, a Lion Air 737 Max crashed into the sea and killed all on board, partially due to the pilots’ inexperience with the aircraft. This is another big blow to Boeing who sought to prevent pilot training on the new model, as one of the big selling features was that pilots would not need to undergo such training. Bloomberg reports that internal communications at Boeing showed some employees calling Lion Air “idiots” for requesting the expensive simulator training.

- In late January Boeing unveiled the 777X, a twin engine jet capable of flying 426 passengers with wings so long that the wingtips fold. The plane is longer than the 747 and is the priciest model at $442.2 million each. The successful test flight was a bright spot for the troubled plane maker. However, sales of the 777X have stalled since the Dubai Airshow in 2013 and expected orders from China haven’t materialized. Bloomberg Intelligence aviation analyst George Ferguson says “it is feeling like the plane is too big for most markets, for most airlines.”

Oppurtunites

- Bloomberg reports that the International Air Transport Association (IATA) formed a partnership with Xpansiv CBL Holding Group to develop the Aviation Carbon Exchange, which aims to limit airline emissions. Commercial aviation accounts for 2 percent of the world’s greenhouse emissions and has faced growing scrutiny to adopt greener practices. Xpansiv is an emissions marketplace and saw millions of tons of carbon traded on its platform in January alone. Several airlines have already taken steps to reduce their carbon footprints, with JetBlue announcing that it hopes to become carbon neutral on all domestic flights by July through using an alternative fuel source.

- Norwegian Air is now improving profitability after years of high debt. The airline said its unit revenue rose by 21 percent in December – the ninth straight monthly increase – and 2019 unit revenue was up 7 percent. Bloomberg reports that the company turned around its strategy of aggressive growth and now vows to reduce capacity and focus on profitability.

- India continues to be one of the fastest growing aviation markets and competition is heating up in the country. Singapore Airlines is preparing to add more Boeing jets in India to compete with Emirates. Bloomberg writes that Vistara, which is Singapore Air’s Indian joint venture, is considering adding more 787 Dreamliner jets to add flights to destinations as far away as the U.S. Singapore Airlines is also facing growing competition from budget carriers in Southeast Asia.

Threats

- The biggest threat to emerge for the airline sector in January 2020 was the spread of the coronavirus, declared a global health emergency. In attempting to prevent the disease from spreading further outside of China, many airlines suspended flights to the country for several weeks. This could hurt global travel demand for several months.

- U.K. airline Flybe Group Plc struck a rescue deal with the government to keep the airline from bankruptcy and liquidation, reports Bloomberg. The airline serves more British towns and cities than any other and would leave many routes without flights. Flybe is one of the largest operators of Q400 turboprop planes and employs around 2,400 people. Industry consultant John Strickland says many of the routes have marginal economics and small airports, so other carriers such as British Airways or EasyJet might be hesitant or unable to fill the void due to their larger airplanes.

- Boeing’s troubles continue and airlines don’t expect the 737 Max jet to return to service until summer or later. Southwest, which is the most impacted by the groundings because it flies the most jets, said growth has been stalled and didn’t give a 2020 capacity outlook. The airline said in a statement that the cost to fly each seat a mile will increase 6 percent to 8 percent in the first quarter of 2020 due to reduced flights and seat capacity. The carrier reached a confidential settlement with Boeing after incurring $828 million in 2019 damages, reports Bloomberg.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.51 | -0.18 | -10.62% |

| Oil Futures | 51.62 | -2.57 | -4.74% |

| Hang Seng Composite Index | 3,587.47 | -231.30 | -6.06% |

| S&P Basic Materials | 361.99 | -13.29 | -3.54% |

| Korean KOSPI Index | 2,119.01 | -127.12 | -5.66% |

| S&P Energy | 405.45 | -24.26 | -5.65% |

| Nasdaq | 9,150.94 | -163.98 | -1.76% |

| DJIA | 28,256.03 | -733.70 | -2.53% |

| Russell 2000 | 1,614.06 | -48.17 | -2.90% |

| S&P 500 | 3,225.52 | -69.95 | -2.12% |

| Gold Futures | 1,592.40 | +14.20 | +0.90% |

| XAU | 103.94 | -0.88 | -0.84% |

| S&P/TSX VENTURE COMP IDX | 575.18 | -6.58 | -1.13% |

| S&P/TSX Global Gold Index | 266.69 | +2.13 | +0.81% |

| Natural Gas Futures | 1.84 | -0.05 | -2.69% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,119.01 | -78.66 | -3.58% |

| 10-Yr Treasury Bond | 1.51 | -0.41 | -21.52% |

| Gold Futures | 1,592.40 | +63.10 | +4.13% |

| S&P Basic Materials | 361.99 | -23.86 | -6.18% |

| S&P 500 | 3,225.52 | -5.26 | -0.16% |

| DJIA | 28,256.03 | -282.41 | -0.99% |

| Nasdaq | 9,150.94 | +178.33 | +1.99% |

| Oil Futures | 51.62 | -9.44 | -15.46% |

| Hang Seng Composite Index | 3,587.47 | -240.08 | -6.27% |

| S&P/TSX Global Gold Index | 266.69 | +5.39 | +2.06% |

| XAU | 103.94 | -2.98 | -2.79% |

| Russell 2000 | 1,614.06 | -54.41 | -3.26% |

| S&P Energy | 405.45 | -51.01 | -11.18% |

| S&P/TSX VENTURE COMP IDX | 575.18 | -2.36 | -0.41% |

| Natural Gas Futures | 1.84 | -0.35 | -15.85% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 103.94 | +8.32 | +8.70% |

| S&P/TSX Global Gold Index | 266.69 | +16.87 | +6.75% |

| Gold Futures | 1,592.40 | +65.50 | +4.29% |

| DJIA | 28,256.03 | +1,209.80 | +4.47% |

| S&P 500 | 3,225.52 | +187.96 | +6.19% |

| Nasdaq | 9,150.94 | +858.58 | +10.35% |

| Korean KOSPI Index | 2,119.01 | +35.53 | +1.71% |

| Natural Gas Futures | 1.84 | -0.79 | -30.04% |

| S&P Basic Materials | 361.99 | -2.74 | -0.75% |

| Russell 2000 | 1,614.06 | +51.61 | +3.30% |

| Oil Futures | 51.62 | -2.56 | -4.72% |

| Hang Seng Composite Index | 3,587.47 | -44.67 | -1.23% |

| S&P/TSX VENTURE COMP IDX | 575.18 | +36.81 | +6.84% |

| S&P Energy | 405.45 | -21.21 | -4.97% |

| 10-Yr Treasury Bond | 1.51 | -0.19 | -10.99% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

Delta Air Lines Inc

JetBlue Airways Corp

Boeing Co/The

easyJet PLC

Southwest Airlines Co

Equinor ASA

Rosneft

Calibre Mining Corp

Americas Gold & Silver Corp

Anglo American PLC

AngloGold Ashanti Ltd.

Freeport-McMoRan Inc

McKesson Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P/TSX Global Base Metals Index is a subset of the S&P/TSX Global Mining Index. It is an investable index of companies that have North American equity listings and are involved in the production or extraction of base metals. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Compound annual growth rate (CAGR) is a business and investing specific term for the geometric progression ratio that provides a constant rate of return over the time period. The "core" PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices. The Stoxx Europe 600 Technology index aims to reflect the performance of large, mid and small-cap companies from developed European countries classified by ICB as members of the Technology sector. The Korea Composite Stock Price Index, or KOSPI, is the index of all common stocks traded on the Stock Market Division—previously, Korea Stock Exchange—of the Korea Exchange. The PSE Composite Index, commonly known previously as the PHISIX and presently as the PSEi, is a stock market index of the Philippine Stock Exchange consisting of 30 companies. A basis point is one hundredth of one percent, used chiefly in expressing differences of interest rates.