Gold Royalty Companies Report a Strong First Quarter on Higher Metal Prices

Date Posted: May 8, 2020

Read time: 52 min

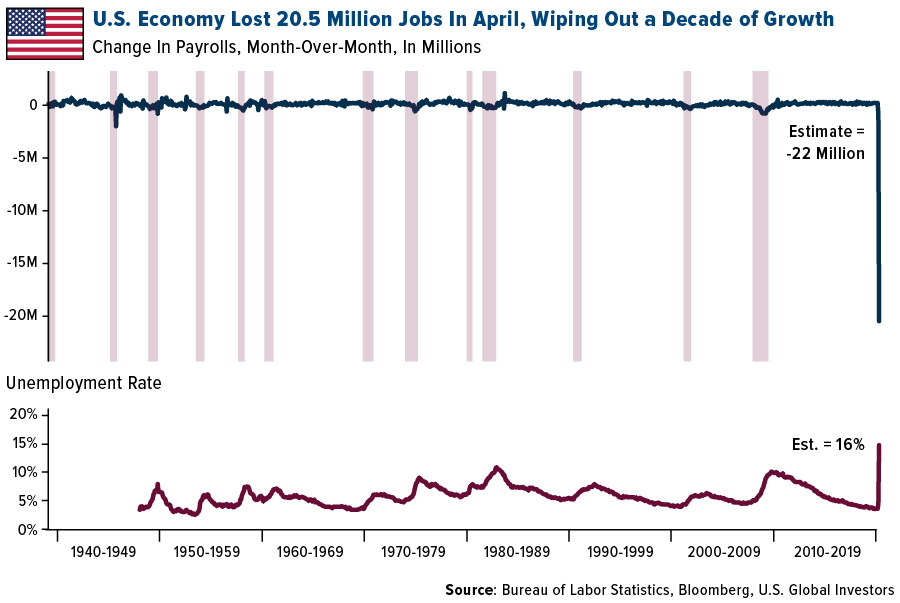

A month is all it took to wipe out a decade of jobs growth. U.S. employers cut an unprecedented 20.5 million jobs in April, the most in history, while the unemployment rate rocketed up to 14.7 percent. As of this week, a head-spinning 33.5 million Americans, or one out of every five workers in the U.S. labor force, have lost their jobs as a result of coronavirus lockdown measures.

U.S. Global Investors Announces Quarterly Results Webcast

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

A month is all it took to wipe out a decade of jobs growth.

U.S. employers cut an unprecedented 20.5 million jobs in April, the most in history, while the unemployment rate rocketed up to 14.7 percent. As of this week, a head-spinning 33.5 million Americans, or one out of every five workers in the U.S. labor force, have lost their jobs as a result of coronavirus lockdown measures.

With so many people out of work as we head into the second quarter, the next earnings season for S&P 500 companies is undoubtedly going to be one for the history books. FactSet reports that Wall Street analysts have already cut their second-quarter earnings estimates by 28.4 percent, the largest such decline on record.

Meanwhile, we’re seeing corporations file for bankruptcy protection at an accelerated clip. As of May 7, an estimated 78 public and private firms with liabilities greater than $50 million have declared bankruptcy so far in 2020, including iconic brands J.Crew and Neiman Marcus. This puts businesses on track to meet and even surpass the 271 bankruptcies that occurred in 2009.

Negative Rates in the U.S.?

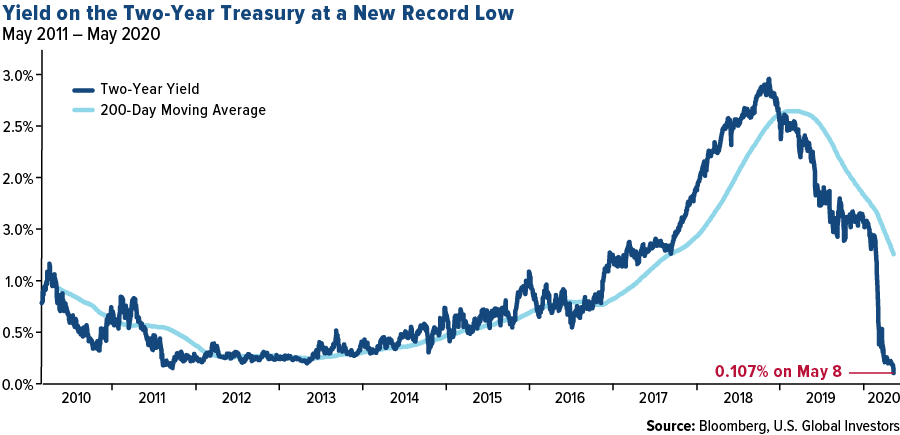

Against this backdrop, yields on the two-year and five-year Treasury fell to fresh record lows today as the fed funds futures market continues to price in negative interest rates by early 2021.

If you recall, Alan Greenspan himself, former Federal Reserve chairman, said it was “only a matter of time” before negative rates spread to the U.S. That was back in September.

Greenspan’s prediction may well come true sooner than even he expected. With the two-year Treasury yield dipping to an anemic 10 basis points, the next test is 0 percent (or less!).

And remember, this is the nominal yield. Adjusted for inflation, it’s already turned negative.

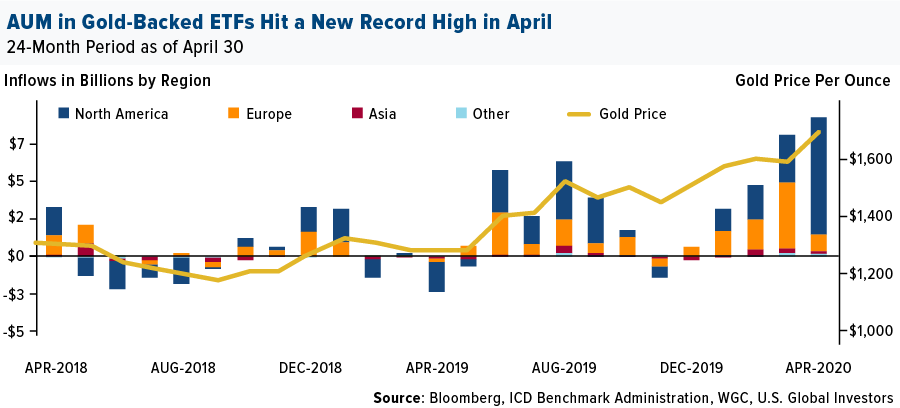

Record Inflows Into Gold-Backed ETFs

To be clear, I’m not advocating for or in favor of negative U.S. rates. As others have pointed out, subzero rates don’t guarantee an economic recovery. They haven’t appeared to help the Japanese or European economies in any way. Instead, they only seem to punish people with savings accounts, forcing them to spend their money or else see their balances slowly melt away.

I believe this is a huge contributor to why we’re seeing higher gold prices right now. The yellow metal has surged above $1,700 an ounce, trading at nearly $1,710 today, or 34 percent above its per-ounce price a year ago.

Yes, gold doesn’t pay dividends or interest, but then neither do Treasury bonds right now. And with S&P 500 companies losing revenue, an estimated $37 billion in dividends could be cut or suspended this year. Royal Dutch Shell recently cut its dividend for the first time since World War II. This week, Disney became the latest blue-chip to suspend its dividend, despite the runaway success of its new streaming platform, Disney+.

Meanwhile, gold royalty company Franco-Nevada raised its quarterly dividend 4 percent, from $0.25 per share to $0.26 per share, marking the 13th annual consecutive dividend increase.

Rising investor appetite for gold is reflected in the fact that assets under management (AUM) in global gold-backed ETFs reached a new record high in April, according to World Gold Council (WGC) data. AUM stood at $184 billion as of April 30, with holdings also hitting a new all-time high of 3,355 metric tons. Assets in such ETFs grew in 11 of the 12 previous months, adding 80 percent to total AUM.

Although demand for gold jewelry has been negatively impacted by the COVID-19 crisis, “history suggests that the likely strength of investment demand may offset this weakness,” the WGC writes in its April report.

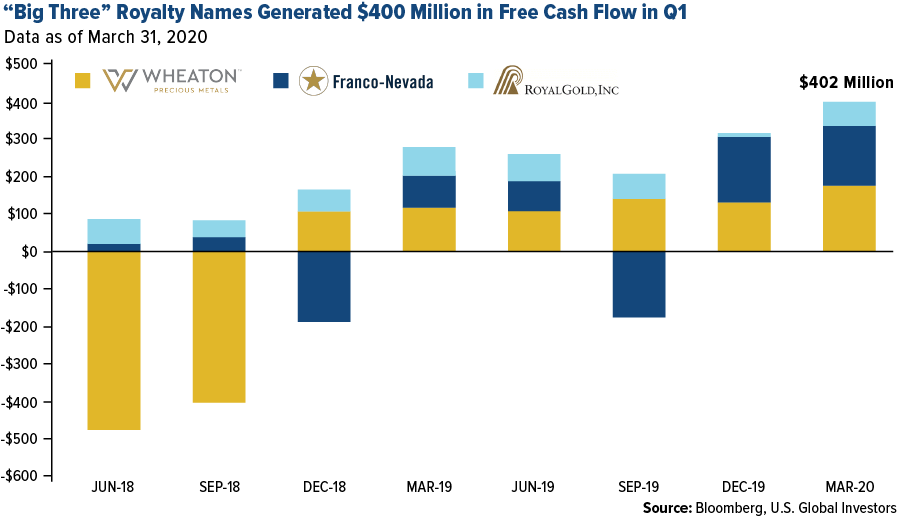

Gold Royalty Companies Report $400 Million in Free Cash Flow

For more than a couple of months now, I’ve said that gold mining companies will have a strong first (and second) quarter thanks to higher metal prices. Stock prices, as you know, are largely driven by revenues and free cash flow (FCF).

FCF is what companies have in the bank after paying operating costs, taxes and other expenses. The higher the cash flow, the better the company can expand its business and reward shareholders.

Longtime readers of the Investor Alert and Frank Talk are probably aware that we like gold royalty companies here at U.S. Global Investors, and in the first quarter of 2020, the “big three” royalty names—Wheaton Precious Metals, Franco-Nevada and Royal Gold—collectively generated a remarkable $402 million in positive free cash flow.

Looking ahead, Raymond James analysts project Franco-Nevada delivering earnings per share (EPS) of $1.91, up from $1.82 in 2019. If Bank of America is right and the price of gold rises to $3,000 an ounce in the next 18 months, Franco’s EPS could be as much as $2.29, according to Raymond James.

As for Royal Gold, Raymond James rates the company as Outperform, seeing EPS of $2.90 this year, up from $1.48 last year. The company’s “high-margin metal sales” can be expanded with “minimal” general and administrative costs, analysts Brian MacArthur and Chris Law write, adding that Royal Gold has a “high-quality, diversified asset base in lower-risk jurisdictions, as well as a flexible balance sheet to support future investments and a growing dividend.”

Curious to learn more about gold royalty companies? Just email us at info@usfunds.com with the subject line “Seeking Info on Gold Royalty Companies.”

May 6, 2020Why Buffett Was Wrong to Dump Airlines |

May 4, 2020Texas Leads the Nation in Reopening Its Economy |

April 29, 2020These 10 U.S. States Are Best Prepared for a Deep Recession |

|||

Gold Market

This week spot gold closed at $1,702.70, up $2.28 per ounce, or 0.13 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.14 percent. The S&P/TSX Venture Index came in up 4.02 percent. The U.S. Trade-Weighted Dollar rose 0.68 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-4 | Durable Goods Orders | -14.4% | -14.7% | -14.4% |

| May-6 | ADP Employment Change | -20,550k | -20,236k | -149k |

| May-7 | Initial Jobless Claims | 3,000k | 3,169k | 3,846k |

| May-8 | Change in Nonfarm Payrolls | -22,000k | -20,500k | -870k |

| May-12 | CPI YoY | 0.4% | — | 1.5% |

| May-13 | PPI Final Demand YoY | -0.3% | — | 0.7% |

| May-14 | Germany CPI YoY | 0.8% | — | 0.8% |

| May-14 | Initial Jobless Claims | 2,500k | — | 3,169k |

| May-14 | China Retail Sales | -5.9% | — | -15.8% |

Strengths

- The best performing metal this week was silver, up 3.34 percent. Gold rebounded on Thursday to steady around $1,700 an ounce as economic data worsened. Unemployment surged to nearly 15 percent in the U.S. Bloomberg notes that the number of Americans filing for unemployment was above 3 million for the seventh straight week, boosting demand for havens as the economic situation continues to deteriorate. According to Bloomberg data, holdings in gold-backed ETFs surged about 3,000 tons to an all-time high this week. Inflows in 2020 so far have already surpassed the volume added in all of 2019.

- South Africa’s Rand Refinery Ltd., Africa’s largest refinery, said it is restarting gold smelting as the country eases a national lockdown. Rand’s CEO Praveen Baijnath said, “We have established a good routine and have been able to ensure that product from our mining clients is shipped to us and that refined product makes its way to bullion banks and end user customers.” Swiss refineries are also ramping up production, which should ease supply concerns that caused gold prices to diverge widely in April.

- Traders are pricing in the possibility that the Federal Reserve will cut its policy rate to below zero by early 2021. This could bode well for gold, as it historically has an inverse relationship with rates. Chinese buyers of gold mining projects took their second bite at the apple this year with Shandong Gold Mining agreeing to buy TMAC Resources at a 52 percent premium to its 20-day trailing average price. A new milling and treatment plant are likely needed to process the TMAC ores as their original engineering design had failed to economically recover enough gold from the circuit. This transaction follows on the heels of Silvercorp’s takeout offer for Guyana Goldfields, another failed project with improper mine planning and engineering design; taken under by braver soul.

Weaknesses

- The worst performing metal this week was palladium, down 1.34 percent despite hedge fund managers raising their net bullish positioning and Bank of America Merrill Lynch forecasting a deficit now for both palladium and platinum on reduced South African supplies. Spot gold trading fell in April due to market disruptions and a disconnect between prices in London and New York. According to the London Bullion Market Association (LBMA), trading volumes fell to 743.5 million ounces last month, down from 1.33 billion in March. Bloomberg notes that trading should return to normal in May as major refineries ramp up projection.

- Swiss refiner Valcambi SA tried for five days straight in April to move a shipment of gold out of Hong Kong, reports Bloomberg. With global air travel at a standstill, the precious metals industry is searching for alternative ways to transport the metal. Limited flights are prioritizing protective equipment, medical items and food over bullion, according to Baskaran Narayanan, vice president of Brink Asia Pacific. India’s gold imports totaled just 60 kilograms in April, down from 13 tons in March. This is about a 99.5 percent drop as the coronavirus curbs air transport for gold.

- Barrick Gold lowered is output forecast after running into a conflict with the government of Papua New Guinea. About 5 percent of the miner’s production comes from the Porgera gold mine in the country.

Opportunities

- Mawson Resources said that it has tripled the size of its Sunday Creek gold project in Australia. The company said its plans to commence geophysical surveys followed by diamond drilling during the second half of this year. Americas Gold and Silver announced a C$25 million bought deal offering. Bloomberg reports that investors led by Pierre Lassonde and Eric Sprott have said they intend to subscribe for shares in the offering totaling C$8.75 million.

- RBC Capital Markets has raised its outlook for gold. Their base-case outlook that has a 50 percent probability is that gold will average $1,663 for 2020 and that the fourth quarter will be the strongest. The high scenario, with a 40 percent probability, is that gold could average $1,788 an ounce, up from prior estimates of $1,614.

- Paul Tudor Jones is buying bitcoin as a hedge against financial instability and money printing. Jones said bitcoin “reminds me of gold when I first got into the business in 1976.” The investor said he remains a big fan of gold and predicts it could rally to $2,400 an ounce or even $6,700 “if we went back to the 1980 extremes,” reports Bloomberg.

Threats

- According to Morgan Stanley analysts including Christopher Nicolson, the plans of South African platinum-group miners to ramp up output could depress prices due to weaker automaker demand. “We see the PGM market moving closer to balance in 2021-22. Given the simultaneous disruption to both supply and demand, the 2020 market balance has become somewhat of a moving target.” Car demand has been hit drastically due to the coronavirus-induced economic harm.

- HSBC reported a $1 million loss in metals trading revenue in the first quarter, compared with a $38 million profit for the same period last year. The bank said that it decreased due to “market volatility and unfavorable valuation adjustments on exchange for physical transactions.” Bloomberg reports that the bank cited in a filing “delivery disruptions in the gold market” as one reason why it breached its value-at-risk limits 12 times in March. HSBC normally only expects this to occur two or three times a year.

- Although the worst of the coronavirus might have already been seen, as more economies reopen more cases and deaths are likely to occur. Internal leaked documents showed the Trump administration projects about 3,000 daily deaths in the U.S. by early June according to the Centers for Disease Control and Prevention (CDC). As President Trump pushes states to ease restrictions to get businesses back up and running, the CDC warns that “there remains a large number of countries whose burden continues to grow.” National Economic Council Director Larry Kudlow said a second wave of Covid-19 will not require a shutdown. Currently the U.S. government, across all agencies, approximates the cost of a single human life at $10 million. Unfortunately, we have to live with the choice of how many lives we can save versus how much economic damage is inflicted on society, a sobering calculation.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.56 percent. The S&P 500 Stock Index rose 3.50 percent, while the Nasdaq Composite climbed 6.00 percent. The Russell 2000 small capitalization index gained 5.49 percent this week.

- The Hang Seng Composite lost 0.63 percent this week; while Taiwan was up 1.20 percent and the KOSPI fell 0.09 percent.

- The 10-year Treasury bond yield rose 6 basis points to 0.679 percent.

Domestic Equity Market

Strengths

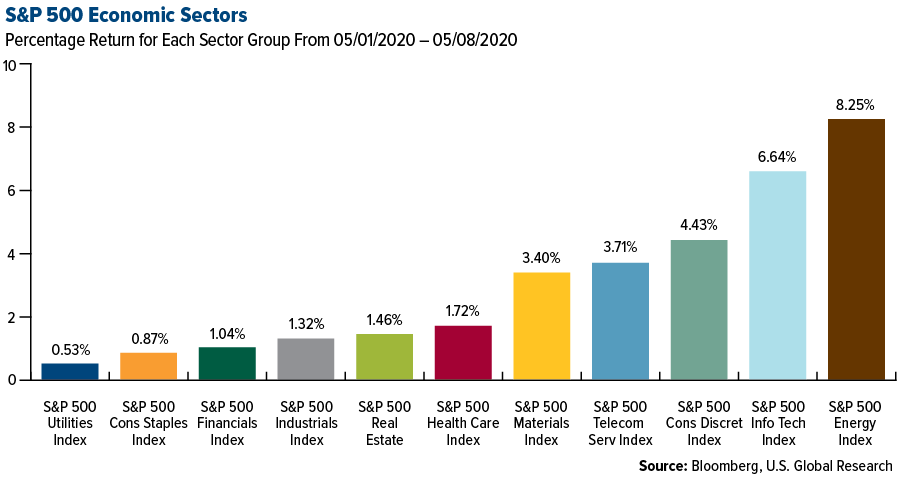

- Energy was the best performing sector of the week, increasing by 8.25 percent versus an overall increase of 3.53 percent for the S&P 500.

- Fortinet was the best performing S&P 500 stock for the week, increasing 31.15 percent.

- Video game companies like Activision Blizzard and Electronic Arts reported strong results for the first quarter. The increase was partially due to users looking for entertainment options during lockdowns, with EA seeing strong crowds for online tournaments.

Weaknesses

- Utilities was the worst performing sector for the week, increasing by 0.53 percent versus an overall increase of 3.53 percent for the S&P 500.

- Westrock was the worst performing S&P 500 stock for the week, falling 12.45 percent.

- J.Crew filed for bankruptcy this week. The retailer said it reached an agreement with lenders to convert around $1.65 billion of its debt into equity.

Opportunities

- HSBC is set to buy out its life insurance joint venture partner in China. The move will allow London-headquartered HSBC to further expand its footprint in the world’s second-largest economy.

- Two of the UK’s largest telecom companies, Virgin Media and O2, have merged. The deal between Liberty Global and Telefónica creates the UK’s largest phone and internet operator with the new company valued at $38 billion, according to Bloomberg.

- Scandinavian airline SAS said it signed a $336 million three-year revolving credit facility agreement with 90 percent of it guaranteed by Sweden’s and Denmark’s governments.

Threats

- California is suing Uber and Lyft, accusing the ride-hailing companies of misclassifying their drivers. A consortium of city attorneys from the state’s largest cities accused the firms of misclassifying their workers as contractors in order to avoid paying certain benefits.

- The UK and U.S. have issued a joint warning that cyber-spies are targeting the health sector. Hackers linked to foreign states could be trying to steal data related to COVID-19 vaccine research.

- Disney’s profit plunged 91 percent last quarter as the coronavirus shut down most of its business. However, Disney Plus roughly doubled its subscribers to 54.5 million this year.

The Economy and Bond Market

Strengths

- New York is “finally ahead of the virus,” Governor Andrew Cuomo said. Total hospitalizations are down to 8,196, from more than 18,000 at the peak, writes Bloomberg News. The daily death toll is at about 200, down from a high of nearly 800.

- Director of the United States National Economic Council Larry Kudlow said on Friday that 2021 will be a “fabulous” economic recovery if President Trump’s policies continue. “Let’s use a free enterprise system, let’s use incentives, let’s reward success; that’s the president’s philosophy and I think that’s going to be his policies,” Kudlow told America’s Newsroom. “And that’s why the second half of this year should grow by 20 percent,” he added. Kudlow also said Trump wants “lower taxes and regulations, strong energy sector, and fair and reciprocal trade.”

- If there was a smidgen of a silver lining in a dismal April jobs report, it’s that the lion’s share of unemployed Americans were temporarily laid off from their jobs, reports Business Insider. Nearly 80 percent were classified as furloughed, indicating the pandemic-induced shutdown of the economy so far isn’t leading to widespread and permanent losses, government data showed Friday.

Weaknesses

- U.S. payrolls plunged by 20.5 million in April, pushing the unemployment rate to its highest since just after the Great Depression. The jobless rate — which was at a 50-year low just a few months ago — more than tripled to 14.7 percent from 4.4 percent a month earlier, according to a Labor Department report Friday.

- Around 3 million more workers filed for unemployment benefits for the first time last week, down slightly from 3.8 million the previous week. More than 33 million Americans have now filed for initial jobless claims since the coronavirus pandemic ripped through the economy, according to data released Thursday by the Department of Labor. Continuing claims, or the number of people receiving ongoing benefits, is now at more than 22 million, far surpassing the recessionary peak of 6.6 million.

- Moody’s revised the outlook for U.S. local governments to negative from stable as the duration and intensity of the of the pandemic’s impact on the economy grows, according to a research report authored by Natalie Claes. “State actions to balance their fiscal 2021 budgets on the back of local governments by reducing transfers will negatively affect the sector,” she wrote.

Opportunities

- The Federal Reserve is considering rolling out new emergency lending facilities designed for colleges, universities and nonprofit medical institutions, Philadelphia Fed President Patrick Harker said. “We know that this crisis is severely harming the nonprofit sector as well,” Harker said Thursday in remarks prepared for a virtual event with the Chicago Council on Global Affairs. “As a recovering academic and university president myself, I’m acutely aware of the stress this crisis is inflicting on, for instance, the higher-education sector.”

- Federal Reserve Chairman Jerome Powell will talk about the economic outlook next week, the central bank announced Friday. Powell will talk to the Peterson Institute for International Economics via webcast on Wednesday at 9 a.m. Eastern. A recent poll by Gallup found that 58 percent of the public has a good deal of confidence in the Fed chairman.

- Next week the Empire State Manufacturing Index is expected to rebound slightly which would be a welcome development given the dire economic numbers lately.

Threats

- An analysis backed by data from the Congressional Budget Office contends the pandemic could trigger state budget shortfalls of $650 billion over three years, Bloomberg Law reported. The Center on Budget and Policy Priorities, a progressive think tank, on Wednesday issued a new estimate of the coronavirus outbreak’s impact on the states based on recent CBO data and updated projections from economists at Goldman Sachs.

- The “investor class” will have to pay for the ballooning debt stemming from the Covid-19 crisis, according to Jim Millstein, the co-chairman of Guggenheim Securities who led restructuring efforts at the U.S. Treasury Department after the financial crisis. An article in Advisor Perspectives summarizes, “There is one clear implication: The era of tax cuts is over,” Millstein said Monday in a Bloomberg Television interview. It’s “inevitable” that the wealthy will face greater taxes, he said. “People who have been fortunate enough to be able to make significant incomes are going to have to make a greater contribution.” He said unprecedented support by the U.S. Federal Reserve to backstop credit markets has benefited investors in a way they’ll eventually have to pay back.

- The number of expected deaths in the U.S. from the coronavirus has doubled because of governors’ push to reopen, New York Governor Andrew Cuomo said as he warned against prematurely ending lockdowns. “There’s a cost of reopening quickly,” Cuomo said Tuesday. “The faster we reopen, the lower the economic cost, but the more lives lost.” The governor cited data from the University of Washington’s Institute for Health Metrics and Evaluation, which has increased its first-wave death projection to more than 130,000 from earlier estimates of about 60,000.

Energy and Natural Resources Market

Strengths

- The best performing commodity this week was crude oil, up 25.23 percent. Oil’s rally resumed on Wednesday with prices doubling over five days. Bloomberg notes that futures in New York rose above $25 a barrel and broke above its 50-day moving average for the first time since January as output cuts take effect. Oil quotas in Texas were dead on arrival, but shale drillers are making their own cuts. Bloomberg reports that Diamondback Energy, Parlsey Energy and Centennial Resource Developament became the latest Permian explorers to say that they were curbing output. Centennial is shutting 40 percent of its output in May and suspending all drilling and fracking. A cut in production could further support oil prices.

- Anglo American Platinum announced it completed repairs at its key Rustenberg plant ahead of schedule and will be fully operational by next week. Credit Suisse upgraded Anglo American to Outperform, saying that it is best placed for a rally and is now at an attractive entry point. The firm added that Anglo has the best environment, social and governance (ESG) score and is the most diversified of the big four miners.

- Westpac, an Australian bank, said it will exit thermal coal by 2030 and will aim to provide A$3.5 billion of new lending to climate change solutions over the next three years. In a climate action document published this week, the bank added that it plans to source the equivalent of 100 percent of its energy consumption from renewable sources by 2025. Total SA announced commitments to eliminate most of its carbon emissions by 2050 despite the negative impacts of plummeting oil demand.

Weaknesses

- The worst performing commodity this week was sugar, down 6.20 percent , likely on Citigroup forecasting sugar supply to shift from deficit to surplus this year. According to Citigroup analysts led by Tracy Liao, the strength in iron ore will fade in the coming weeks and spot prices will fall to around $70 per ton. The sell-off should happen in May due to seasonal weakness in China’s steel demand. The group forecasts a surplus of more than 80 million tons in the second half of this year.

- Crop giant Bunge Ltd., one of the world’s largest agricultural commodities traders, said it expects earnings this year to be lower than previously thought due to shrinking demand from closed restaurants. CEO Greg Heckman said, “We did not experience significant disruptions to our business from COVID-19 in the first quarter, although we did start to see the impact of changing consumer behavior in parts of our edible oils business in March.”

- A gas leak at an LG Chem Ltd. Polymer plant in Southern India killed at least seven people and led to the evacuation of the city of Visakhapatnam. The leak occurred when the company tried to restart the aging plant. With $8.1 billion in spending cuts announced in the Canadian energy sector, Alberta will be hit hardest as their oil sands growth will come to a near standstill.

Opportunities

- According to ethanol producer Green Plains Inc., demand for biofuels will increase after the pandemic. CEO Todd Becker said that people will likely avoid mass transportation in the post-pandemic era and instead drive more. “We believe the future could look a little different as companies and individuals look for ways to avoid mass transit and air travel and drive more, which could be a potential tailwind.”

- Italy’s electricity demand rose on Monday as lockdown restrictions were loosened, signaling economic recovery is underway, reports Bloomberg. Consumption also rose in France and Britain and held steady in Germany and Spain from the previous week. Power demand dropped by as much as 20 percent in parts of Europe as governments kept businesses shut. Countries opening back up “will lead to slightly increased demand and electricity prices will slowly and steadily rise in the future,” according to Somik Das, senior power analyst at GlobalData Ltd.

- Middle Eastern oil producers could make a faster move toward renewables now that solar power is the cheapest kilowatt-hour in the region. According to research by BloombergNEF, solar projects cost only about a 10th of what they did a decade ago due to more affordable equipment and better technology. Benjamin Attia at Wood Mackenzie said that new projects for renewables in the Middle East rely on private funding, rather than government spending, and are therefore insulated from headwinds of lower oil prices. South Korea is considering ramping up its push for renewable energy to 40 percent of the nation’s power by 2034, previously the goal had been 20 percent. Controlling their own energy destiny versus relying on imports of carbon based fuels.

Threats

- The International Energy Agency (IEA) said that nuclear could drop by 3 percent from last year due to lower demand and delays to planned maintenance and construction of projects. Nuclear is known as a stable source of emission-free power, but recent shutdowns to reactors due to reduced power demand could spell long-term trouble as it faces competition from solar and wind.

- China agreed to help get a $4.2 billion coal project in Zimbabwe off the ground. This comes in contrast to financial institutions worldwide stepping away from funding coal projects. Bloomberg notes that this move by China could risk further isolation from the rest of the world at a time when it needs allies to help recover from the pandemic. According to data by Greenpeace, Chinese companies and banks are involved in financing at least 13 coal projects across Africa with another nine in the works.

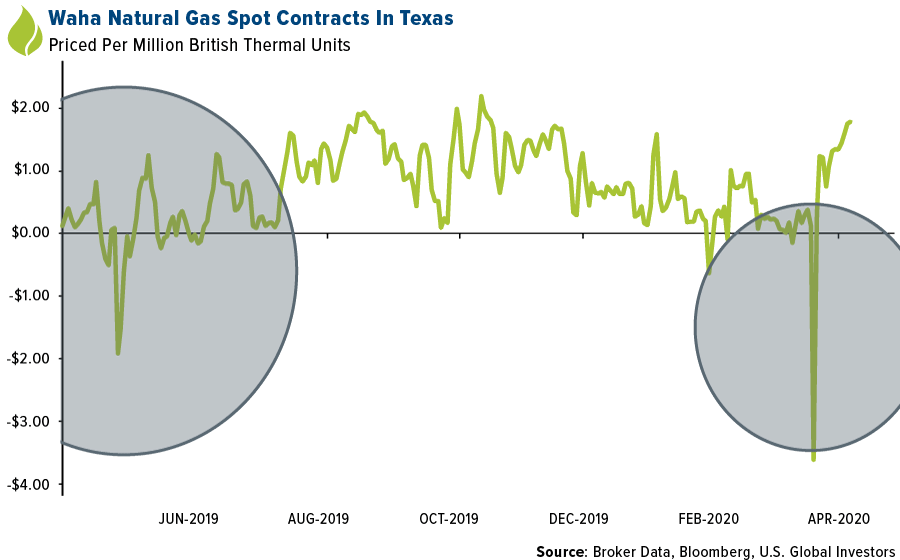

- Some of the world’s biggest gas benchmarks are at the risk of falling negative as storage runs out. Bloomberg reports there are growing concerns that natural gas prices could see the same fate as oil. Four major indexes are already trading near record lows. As seen in the chart below, Waha natural gas spot contracts in Texas went negative as recently as last month. Should inventories hit full capacity globally, especially in Europe, the fuel could potential drop below zero, just as oil did on the same concern. Bloomberg announced on at the end of the week that they had reconfigured the Bloomberg Commodity Index and sub-indices to accommodate negative prices.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 5 percent. The government is preparing a program to boost the economy with significantly higher investment in infrastructure, health care and agriculture; total allocations could top 6 percent of GDP, compared with an average 4 percent in previous years. Ryanair, a low cost airline, announced resuming flights from Bucharest to London on May 15. OMV Petrom, was the best performing stock trading on the Bucharest exchange, gaining 10.8 percent over the past five days.

- The Russian ruble was the best performing currency this week, gaining 2.5 percent. The ruble outperformed it peers with the recovery in oil. The price of Brent crude oil bounced to $30.86 per barrel from $26.44 last Friday.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 3.3 basis points. The Markit PMI reading dropped to 33.4 in April from 48.1 in March. The country’s budget gap widened to 46.2 billion in April from 40.4 billion. Auto makers/distributors Ford Otomotive and Dogus Otomotiv were the worst performing equites trading on the Istanbul Stock Exchange, losing 13 percent each over the past five days.

- The Turkish lira was the worst performing currency in the region this week, losing 1.2 percent. The lira dropped to the lowest level this week surpassing its weakness from August 2018 when the U.S. imposed sanctions on Turkey. The Turkish government banned Citi, UBS and BNP from trading the currency, saying the threesome of the biggest FX banks failed to meet its lira liabilities in lira transactions with the local bank.

- Consumer discretionary was the worst performing sector among eastern European markets this week.

Opportunities

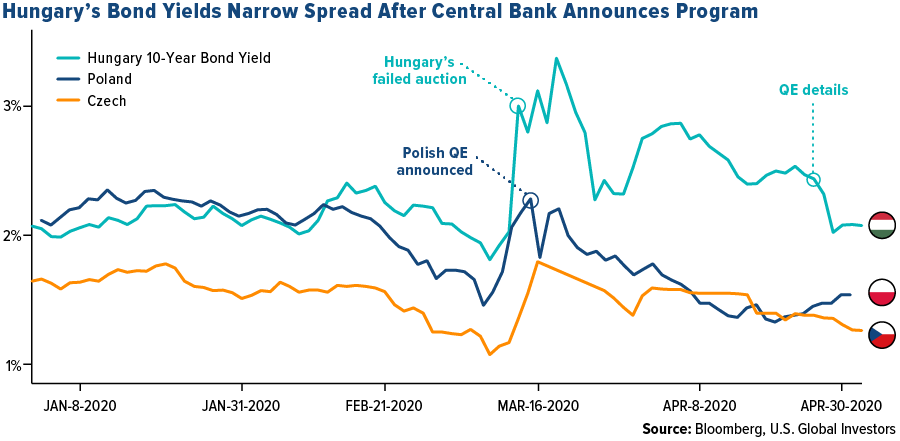

- Hungary started its quantitative bond-buying program this week. The central bank is planning to buy 100 billion forint weekly until 1 trillion is reached. The program is designed to provide money in the system and lower rates. Hungarian 10-year government bonds trade at a premium over Polish and Czech Republic notes and the QE program should help to flatten the yield curve.

- Countries around the world continue to stimulate their economies. The Czech Republic’s central bank cut its main rate by 75 basis points, more than expected, lowering borrowing costs by 2 percent since March and still has more room for easing if needed.

- Reuters reported Thursday that the European Commission has proposed scrapping the usual conditions for member countries to access the European Stability Mechanism (ESM) amid the efforts to revive economies hit by the Covid-19 pandemic. The article says countries drawing on the fund would not face any macroeconomic adjustment program. It added that the proposal discusses "enhanced surveillance" of countries taking credit lines to ensure they use the funds for coronavirus-related health spending, which would end once Brussels confirms the money was used properly.

Threats

- The German constitutional court issued a ruling to which the European Central Bank (ECB) has three months to carry out an assessment of its quantitative easing (QE) program and show that QE is benefiting the economy and does not have adverse fiscal effects over its monetary benefits. The ECB has three months to come up with a rational reason for why it is “proportional” to the ECB’s monetary policy objectives, according to Cornerstone Macro’s research team. It believes this ruling should have no short-term effect on QE, but it may affect the ECB’s ability to deal with future emergencies.

- The European Commission projected that the EU will contract 7.7 percent this year and grow 6.3 percent in 2021, the commission said, which would still leave it some 3 percent below the commission’s previous forecast level by the end of next year. The commission forecasts that by this year’s end, seven eurozone economies will have debts exceeding 100 percent of its gross domestic product, with Greece’s ratio near 200 percent and Italy’s rising to 159 percent from 135 percent.

- Russia surpassed Germany and France in its total number of COVID-19 infections on Thursday, adding more than 11,000 new cases for a total of 177,160. Leonid Fedun, the largest shareholder of Lukoil after CEO Vagit Alekperov, was hospitalized due to complications from the virus. Three government ministers, including Prime Minister Mikhail Mishustin have been diagnosed with the disease. The number of coronavirus cases in Russia most likely will continue to grow, surpassing those in Italy, the United Kingdom and Spain, considering Russia is the most populated country in Europe.

China Region

Strengths

- Vietnam was the best performing country this week, gaining 5.8 percent. Not too liquid, Saigon General Service, was the best performing equity among stocks trading on the Ho Chi Minh City Stock Exchange, gaining 30 percent in the past five days. Prime Minister Nguyen Xuan Phuc lifted social distancing guidelines for almost all localities. As of Friday, Vietnam reported only 288 coronavirus cases and no deaths.

- The Indonesia rupiah was the best performing currency this week, gaining 1.8 percent. Emerging market currencies advanced on optimism of re-opening economies and renewed talks between the U.S. and China on a trade deal. On Friday, the bank of Indonesia announced allocation of Rp125 trillion ($8.25 billion) to buy government bonds in the primary market to support the state’s financial needs.

- Semiconductor stocks were the best performing among equites trading on the Hong Kong Stock Exchange.

Weaknesses

- India was the worst performing country this week, losing 6.2 percent. India’s manufacturing PMI fell to 27.4 in April from 51.8 in March. Service PMI plummeted to 5.4 in April from 49.3, leaving the composite PMI at 7.2, the lowest level and well below the 50 mark, that separates growth from contraction. As of today, India reported 57,306 coronavirus cases with 1,899 deaths. Titan, a jewelry maker, was the worst performing equity among stocks in the India Nifty50 Index, losing 14.4 percent in the past five days.

- The Malaysian ringgit was the worst performing currency this week, losing 60 basis points. The currency lost last week’s gains over the past five days. Manufacturing PMI dropped to 31.3 in April from 48.4. Exports and imports declined, but not by as much as expected. The overnight policy rate was left unchanged at 2 percent. Next week’s GDP data will be released and Bloomberg economists predict contraction of 2.5 percent in the first quarter versus expansion of 60 basis points recorded in the fourth quarter of last year.

- Airline stocks were the worst performing among equites trading on the Hong Kong Stock Exchange.

Opportunites

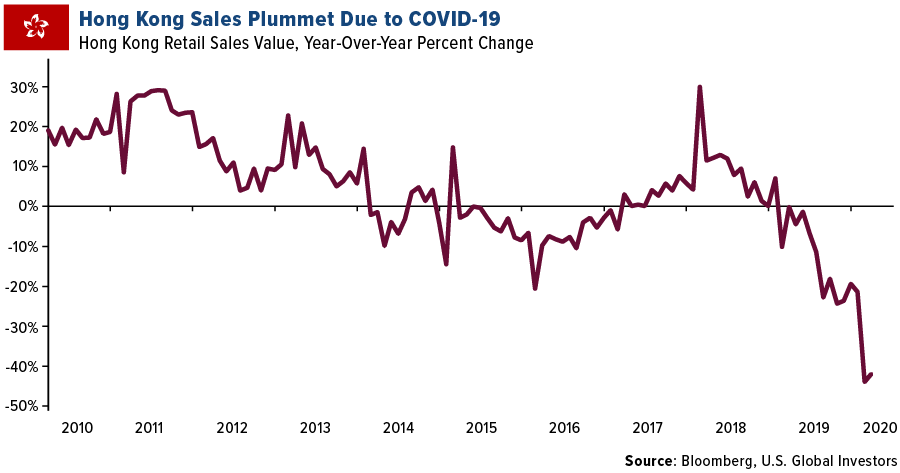

- According to Citigroup, Hong Kong home prices and retail sales have likely hit the bottom in April. Analysts including Ken Yeung wrote in a note that home prices are expected to resume an uptrend in May, rising 5 percent to 10 percent through the end of 2020.

- Hong Kong’s CEO Carrie Lam said on Tuesday that it will soon relax virus restrictions. “The time for some relaxation, some lifting of the restrictions that we put on this social context has come.” This positive news follows the decision for government employees to resume work back at the office on Monday.

- China’s General Administration of Customs said that foreign trade of goods fell by just 0.7 percent year-over-year in April to $352.5 billion. A bigger drop was expected due to the impact of COVID-19. China’s exports rose 8.2 percent year-over-year in April.

Threats

- Hong Kong’s GDP fell by 8.9 percent in the first quarter a year ago, according to advanced estimates from the Census and Statistics Department. Economist estimates compiled by Bloomberg had forecast a drop of only 6.5 percent.

- Retail sales in Hong Kong fell 42 percent in March compared to the same time a year ago. Government data shows that sales dropped to $2.97 billion. Hong Kong’s economy was already in a recession before the pandemic began due to violent anti-government protests in the second half of 2019.

- U.S. and Chinese negotiators might speak next week on progress toward implementing the Phase One trade deal. However, China’s imports fell 14 percent in April. ANZ’s Raymond Yeung says that figure does not bode well for the two countries’ relationships and that “the Trump administration will certainly press for more” imports of American goods.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 8 was Switch, up 1,493.07 percent. As reported by Bloomberg this week, macro investor Paul Tudor Jones is buying bitcoin as a hedge against inflation he sees coming from central bank money-printing. “The best profit-maximizing strategy is to own the fastest horse,” Jones said in a market outlook note. “If I am forced to forecast, my bet is it will be bitcoin.”

- Galaxy Digital CEO Mike Novogratz, who has always held a bullish belief on bitcoin, tweeted over the weekend that he expects “this rally to last,” reports BeingCrypto. Novogratz was referring to the upcoming BTC block-reward halving, and adds that the price rally will mostly be the result of an influx of new investors – signs of which already seem to be forming.

- So far this month, bitcoin is outperforming both gold and stocks, reads one CoinDesk headline. While the popular digital currency has gained nearly 5.9 percent so far in May, gold is down 1 percent and the S&P 500 was down 2.2 percent mid-week, on a month-to-date basis, according to data source Skew.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended May 8 was Okschain, down 90.77 percent.

- Warren Buffett and Berkshire Hathaway are reluctant to spend its $137 billion cash pile, writes CoinTelegraph, with their cautious stance toward the abrupt recovery of the U.S. stock market possibly spoiling the recent bitcoin rally. Although bitcoin has long broken out of its short-term correlation with the U.S. stock market, the article explains, a potential equities correction in the near-term raises the probability of a pullback in all high-risk and speculative assets.

- A respected researcher in the crypto market says he thinks he’s found the reason transactions on the bitcoin network continue to be more expensive for everyone – BitMEX. As reported by CoinDesk, if the crypto derivatives exchange used more efficient technologies when broadcasting transactions, users could save as much as roughly 1.7 bitcoin in fees every day. Since BitMEX broadcasts thousands of transactions at once at the same time every day, it leads to a fee increase each day.

Opportunities

- Announced on Tuesday, the highly specialized world of digital identity is opening itself to a wider audience, writes CoinDesk. The Trust over IP (ToIP) Foundation is backed by governments, nonprofits and private-sector firms, with key players like Mastercard and IBM. The ToIP Foundation is a move to rein together core issues that matter to all of them, as well as creating appropriate technologies.

- Bitcoin halvings, which slow down the rate at which new tokens are created, writes Bloomberg, happen once every four years or so. Next week, its third such event is set to occur. Bitcoin seems to, once again, be staging a comeback with “evangelists pegging their hopes” on this technical event as the new catalyst.

- Jenny Ta, a serial entrepreneur and Wall St. veteran, has launched a crypto-powered social media network and marketplace platform that promises it won’t sell users’ data, reports CoinTelegraph. The platform known as CoinLinked launched on May 7, featuring a utility token that rewards its users for activity, and can also be redeemed for discounts on CoinLinked’s marketplace.

Threats

- Telegram told investors in its TON blockchain project that it is contractually obligated to pay back 72 percent of their investments after missing an April 30 launch date, reports CoinDesk. Just last week, the company told investors they could be repaid in gram tokens – however, that crypto option has now been deemed infeasible. “Unfortunately, based on more recent discussions with relevant authorities and our counsel, we have made the difficult decision not to pursue an option involving grams or another cryptocurrency due to its uncertain reception from the relevant regulators,” reads a letter shared with CoinDesk.

- Hackers have infected the IT infrastructure of the largest private hospital in Europe with ransomware, reports CoinTelegraph. On May 6, cybersecurity news outlet KrebsonSecurity wrote that hackers compromised the IT systems of Germany-based private hospital, Fresnius. The ransomware, known as Snake, was discovered earlier this year, and is being actively used to target large businesses.

- Micree Ketuan Zhan, former co-founder of Bitmain who was ousted by his rival co-founder Wu Jihan last October, was recently granted the right to recover his status as the legal representative of Beijing Bitmain Technology, reports CoinDesk. On Friday, Zhan attended the Beijing Haidian District Justice Bureau to collect his new registration license as part of the recovery process. However, as the bureau attempted to hand over the license to Zhan, Bitmain’s CEO Liu Luyao abruptly took possession of it saying, “The business license is company property, how can it fall into the hands of an individual?” The tensions later escalated into a physical confrontation.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.68 | +0.07 | +10.59% |

| Oil Futures | 24.60 | +4.82 | +24.37% |

| Hang Seng Composite Index | 3,426.89 | -21.70 | -0.63% |

| S&P Basic Materials | 330.32 | +10.85 | +3.40% |

| Korean KOSPI Index | 1,945.82 | -1.74 | -0.09% |

| S&P Energy | 294.75 | +22.47 | +8.25% |

| Nasdaq | 9,121.32 | +516.37 | +6.00% |

| DJIA | 24,331.32 | +607.63 | +2.56% |

| Russell 2000 | 1,329.64 | +69.16 | +5.49% |

| S&P 500 | 2,929.80 | +99.09 | +3.50% |

| Gold Futures | 1,708.70 | +7.80 | +0.46% |

| XAU | 122.09 | +4.73 | +4.03% |

| S&P/TSX VENTURE COMP IDX | 491.97 | +18.88 | +3.99% |

| S&P/TSX Global Gold Index | 352.17 | +9.90 | +2.89% |

| Natural Gas Futures | 1.83 | -0.06 | -3.28% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 1,945.82 | +138.68 | +7.67% |

| 10-Yr Treasury Bond | 0.68 | -0.09 | -12.16% |

| Gold Futures | 1,708.70 | +24.40 | +1.45% |

| S&P Basic Materials | 330.32 | +20.37 | +6.57% |

| S&P 500 | 2,929.80 | +179.82 | +6.54% |

| DJIA | 24,331.32 | +897.75 | +3.83% |

| Nasdaq | 9,121.32 | +1,030.42 | +12.74% |

| Oil Futures | 24.60 | -0.49 | -1.95% |

| Hang Seng Composite Index | 3,426.89 | +119.42 | +3.61% |

| S&P/TSX Global Gold Index | 352.17 | +88.62 | +33.63% |

| XAU | 122.09 | +32.39 | +36.11% |

| Russell 2000 | 1,329.64 | +137.97 | +11.58% |

| S&P Energy | 294.75 | +32.29 | +12.30% |

| S&P/TSX VENTURE COMP IDX | 491.97 | +83.08 | +20.32% |

| Natural Gas Futures | 1.83 | +0.04 | +2.52% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 122.09 | +18.67 | +18.05% |

| S&P/TSX Global Gold Index | 352.17 | +90.42 | +34.54% |

| Gold Futures | 1,708.70 | +132.90 | +8.43% |

| DJIA | 24,331.32 | -5,048.45 | -17.18% |

| S&P 500 | 2,929.80 | -415.98 | -12.43% |

| Nasdaq | 9,121.32 | -450.83 | -4.71% |

| Korean KOSPI Index | 1,945.82 | -282.12 | -12.66% |

| Natural Gas Futures | 1.83 | -0.03 | -1.83% |

| S&P Basic Materials | 330.32 | -52.55 | -13.73% |

| Russell 2000 | 1,329.64 | -347.82 | -20.73% |

| Oil Futures | 24.60 | -26.35 | -51.72% |

| Hang Seng Composite Index | 3,426.89 | -337.52 | -8.97% |

| S&P/TSX VENTURE COMP IDX | 491.97 | -86.03 | -14.88% |

| S&P Energy | 294.75 | -116.89 | -28.40% |

| 10-Yr Treasury Bond | 0.68 | -0.97 | -58.70% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2020):

Ryanair Holdings PLC

OMV Petrom SA

Ford Otomotive Sanayi SA

Lukoil PJSC

Anglo American Plc

Barrick Gold Corp

Mawson Resources Ltd

Americas Gold & Silver Corp

Franco-Nevada Corp

Royal Gold Inc

Wheaton Precious Metals Corp

TMAC Resources

Silvercorp Metals

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The index was created with a base index value of 100 as of July 28, 2000 The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index represents 20 commodities, which are weighted to account for economic significance and market liquidity. The Empire State Manufacturing Index is an index based on the monthly survey of manufacturers in New York State conducted by the Federal Reserve Bank of New York. The index summarizes general business conditions in New York State.