Here’s Why the Number of Conventional Oil Discoveries Just Hit a 70-Year Low

Date Posted: October 4, 2019

Read time: 56 min

Will he or won't he? That seems to be the question on a lot of traders and investors' minds today with regard to Federal Reserve chair Jay Powell. An October rate cut appeared back on the table after disappointing economic news was released mid-week. But Friday's mostly-positive employment report may have dashed those chances.

Press Release: U.S. Global Investors Continues GROW Dividends

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Will he or won’t he?

That seems to be the question on a lot of traders and investors’ minds today with regard to Federal Reserve chair Jay Powell. An October rate cut appeared back on the table after disappointing economic news was released mid-week. But Friday’s mostly-positive employment report may have dashed those chances.

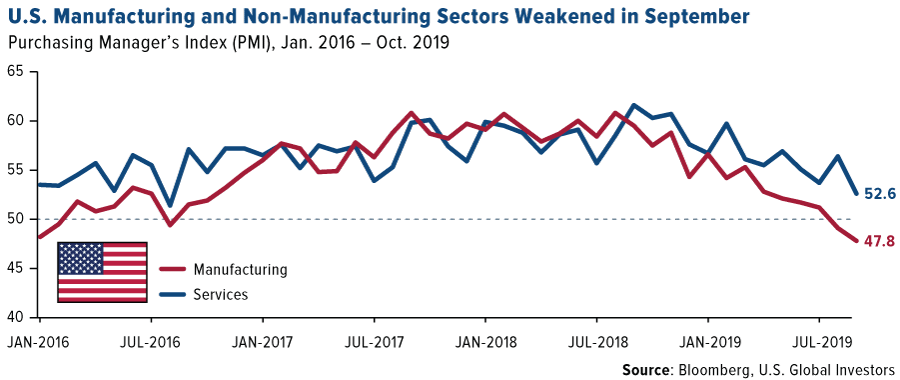

First, the “bad” news. The Institute for Supply Management (ISM) reported this week that both the U.S. manufacturing and non-manufacturing sectors weakened in September. The non-manufacturing, or services, purchasing manager’s index (PMI) fell to 52.6, down from August’s 56.4, representing the lowest reading since August 2016.

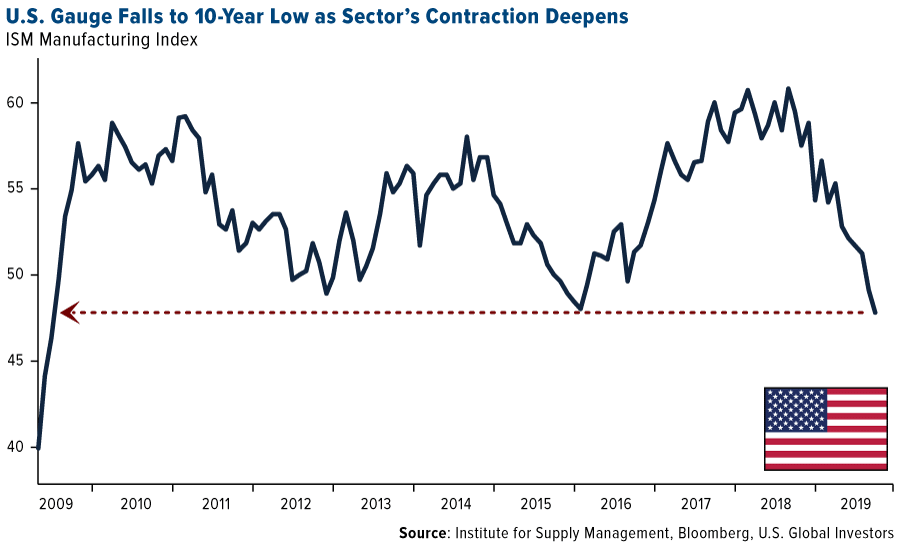

The manufacturing PMI, meanwhile, contracted for the second straight month in September, as I mentioned in this week’s Frank Talk. The gauge came in at 47.8, a 10-year low.

According to one company that makes electrical equipment, appliances and components, the U.S. economy “seems to be softening. The tariffs have caused much confusion in the industry.”

The weakness in manufacturing turned up also in ADP’s employment report, which showed that the sector added only 2,000 net new jobs last month. This made manufacturing the second weakest area of the U.S. economy in September, following only natural resources and mining, which lost 3,000 jobs on net.

Economists and market-watchers were bracing for the worst leading up to Friday’s “official” employment report. And while the actual number of jobs added in September—136,000—wasn’t particularly inspiring, markets seemed to like the fact that the unemployment rate fell to 3.5 percent, an incredible 50-year low.

So the economic expansion, already the longest in U.S. history, continues unabated. But the question still stands: Will he or won’t he? The poor manufacturing data certainly gives Powell license to cut rates another 25 basis points (bps) this month. At the same time, does it really make sense for him to do so with unemployment at its lowest level since the beginning of the Nixon administration?

Powell & Co. have some time yet to decide, as the next Federal Open Market Committee (FOMC) meeting is scheduled for October 30.

Conventional Oil and Gas Discoveries at a 70-Year Low

It wasn’t just stocks that responded favorably to the jobs report. Oil prices traded up on Friday after being knocked down for eight straight days, a losing streak we haven’t seen in more than two years. Concerns about a slowing global economy, falling demand and signs of excess supply despite recent production cuts by the Organization of Petroleum Exporting Countries (OPEC) weighed on oil prices before Friday’s turnaround.

Also putting pressure on oil is Norway’s massive divestiture of fossil fuel equities. The country’s pension fund, the world’s largest at $1.1 trillion, just got the go-ahead from the Norwegian government to sell as much as $5.9 billion worth of oil and gas stocks. As I shared with you before, oil and gas stocks are what made the wealth fund what it is today. In fact, it was set up specifically to invest in the country’s lucrative North Sea oilfields.

In any case, the $5.9 billion doesn’t represent the fund’s entire oil and gas position, but the plan is for it to exit all stocks categorized as “crude producers” over time, according to Norway’s finance minister.

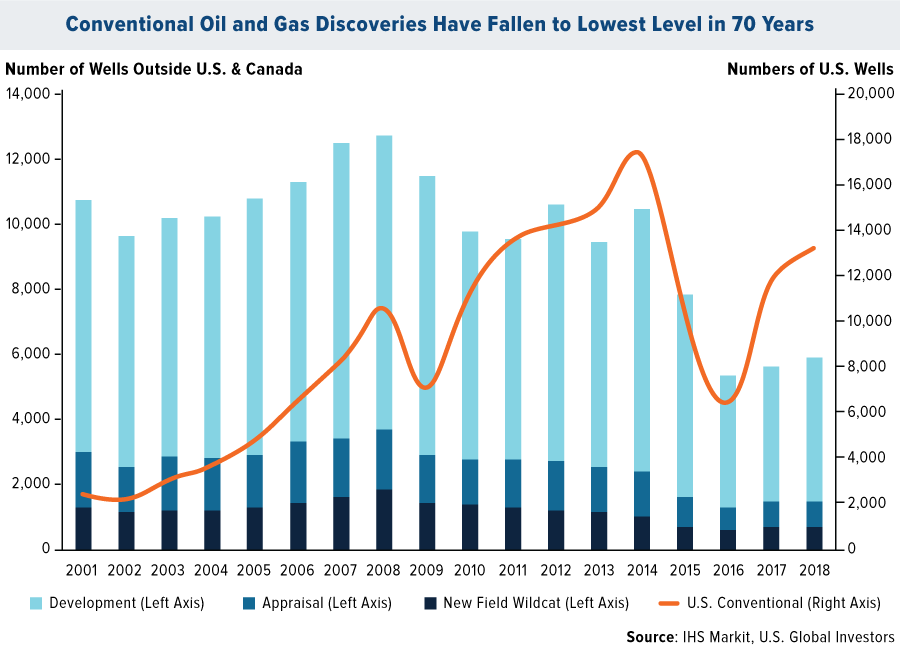

In other oil-related news, IHS Markit released an eye-opening report this week suggesting that conventional drilling and exploration may be at death’s door. In the past three years, oil and gas discoveries made by conventional means have fallen to a seven-decade low. What’s more, “a significant rebound is not expected,” the report’s authors write.

The decline in conventional discoveries, IHS Markit writes, comes as a result not just of lower oil prices—which has discouraged some investors from backing costly “wildcat,” or unproven, drilling projects. Competition from short-term, less costly “unconventional” drilling (shale and fracking) has also made a sizeable impact, especially here in the U.S.

I’ve written many times before on the American success story that is fracking. It’s instrumental in making the U.S. the world’s largest oil producer. The country just produced 12.4 million barrels per day (bpd) in the week ended September 27, according to the Energy Information Administration (EIA). That’s just a hair below the record U.S. high of 12.5 million bpd, reached in August.

The biggest downside to having fewer conventional discoveries, according to IHS Markit, is that it could limit future global reserves and, in effect, drive up fuel costs.

Near-Record Inflows Into Precious Metals

Economic conditions still look strong in the U.S., and according to Larry Kudlow, President Donald Trump’s chief economic advisor, there could be some “positive surprises” next week when U.S. and Chinese trade negotiators meet next week.

Nevertheless, many investors are seeking safety from a potential pullback by piling into Treasuries as well as funds that invest in gold and precious metals. Such funds took in a total of $2.8 billion in the week ended September 25, the second biggest weekly amount on record, according to the Bank of America Merrill Lynch.

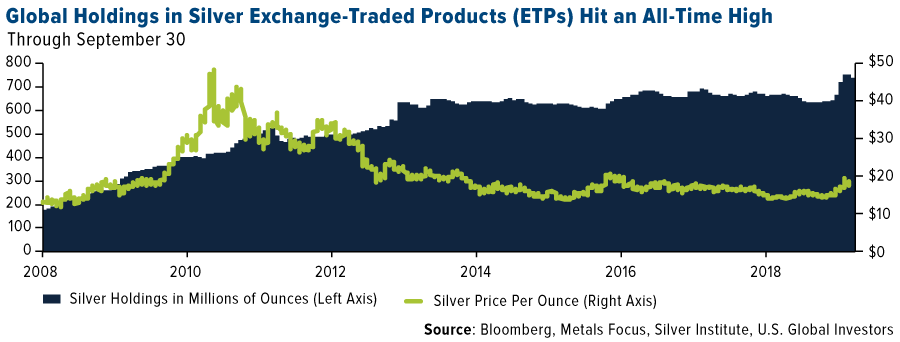

It’s not just gold that’s seeing inflows. Holdings in global silver exchange-traded products (ETPs) hit a new record high in mid-August when precious metal prices were heading higher. According to Metals Focus data, investments in ETPs rose to 706.2 million ounces, or $11.5 billion.

Although gold ended the month of September down some 3.7 percent, it was up almost as much in the third quarter, helping improve risk-adjusted returns. Throughout much of the quarter, stocks traded sideways, a trend that CLSA forecasts will “remain intact into year-end with immediate downside risk through October for the majority of markets.”

To manage risk, CLSA recommends investors buy the dips in gold, writing that they’re attractive buying opportunities “in anticipation of a resumption of the initial base breakout.”

REMINDER: Upcoming Gold Webcast

Speaking of gold… Remember to mark your calendars for October 31 at 2:00pm Eastern time (ET)!

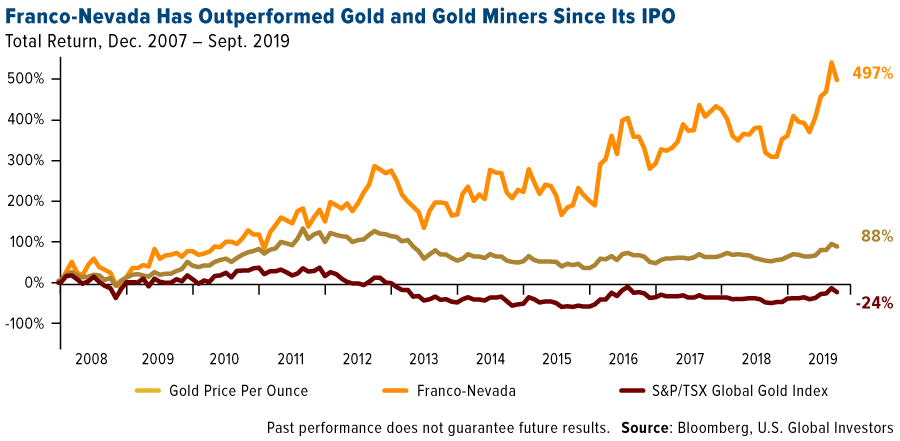

I’ll be taking part in a gold opportunity webcast hosted by Tom Lydon of ETF Trends. I’ve done countless webcasts in the past, but I’m particularly excited for this one because we’ll be joined by my longtime friend, mining legend Pierre Lassonde.

Pierre, as many of you know, is co-founder of the pioneering gold royalty company Franco-Nevada. Pierre likes to call Franco “the GOLD investment that WORKS.” He’s not joking! Since debuting in December 2007, Franco has outperformed both gold bullion and gold miners by a significant margin.

It should be an interesting discussion! If you’d like to listen in, shoot us an email at info@usfunds.com.

Gold Market

This week spot gold closed at $1,504.75, up $7.70 per ounce, or 0.51 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.95 percent. The S&P/TSX Venture Index came in off 1.90 percent. The U.S. Trade-Weighted Dollar fell 0.27 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-29 | Caixin China PMI Mfg | 50.2 | 51.4 | 50.4 |

| Sep-30 | Germany CPI YoY | 1.3% | 1.2% | 1.4% |

| Oct-1 | Eurozone CPI Core YoY | 1.0% | 1.0% | 0.9% |

| Oct-1 | ISM Manufacturing | 50.0 | 47.8 | 49.1 |

| Oct-2 | ADP Employment Change | 140k | 135k | 157k |

| Oct-3 | Initial Jobless Claims | 215k | 219k | 215k |

| Oct-3 | Durable Goods Orders | — | 0.2% | 0.2% |

| Oct-4 | Change in Nonfarm Payrolls | 145k | 136k | 168k |

| Oct-8 | PPI Final Demand YoY | 1.8% | — | 1.8% |

| Oct-10 | CPI YoY | 1.8% | — | 1.7% |

| Oct-10 | Initial Jobless Claims | 218k | — | 219k |

| Oct-11 | Germany CPI YoY | 1.2% | — | 1.2% |

Strengths

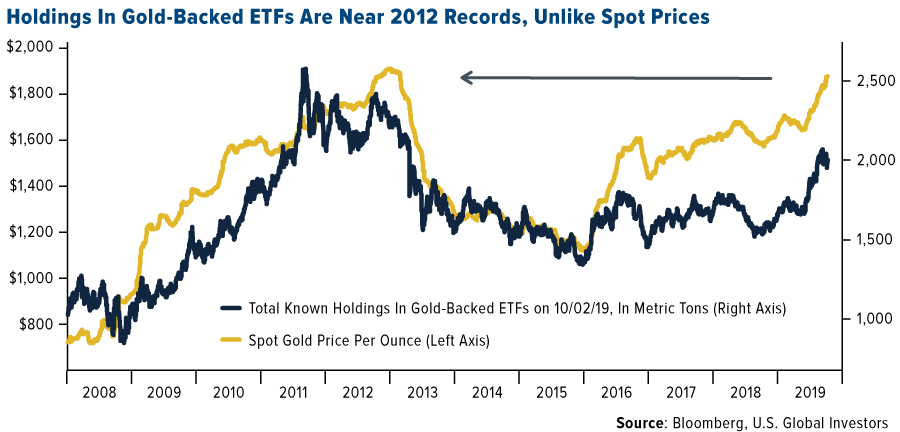

- The best performing metal this week was gold, up 0.51 percent. Gold traders and investors are positive on future gold prices in this weeks’ Bloomberg survey. For the first time in a month the gold bulls outnumbered the combined bearish and neutral responses. ETFs added 39,919 troy ounces of gold to their holdings on Thursday, marking the 14th straight day of inflows, according to Bloomberg data. This year’s net purchases now total 10.3 million ounces. As seen in the chart below, holdings in gold-backed ETFs are near 2012 records, while the price of gold is taking longer to catch up. The yellow metal rallied the most in a month on Wednesday after U.S. private companies’ payrolls rose less than forecast, reports Bloomberg. This builds the case for the Fed cutting rates again this year.

- For the quarter ended September 30, gold beat stocks. The yellow metal returned 3.8 percent while the S&P 500 returned just 1.7 percent. Plus, gold outperformed bonds with the Bloomberg U.S. Treasury Bond Index seeing a 2.4 percent gain. Gold had its fourth straight quarter of positive gains, which is the longest run in eight years. Palladium also shone, hitting a new record of $1,701.93 an ounce on Monday and returning almost 10 percent in the third quarter. Turkey continues to be a big buyer of the metal. The central bank’s gold holdings rose $196 million from the prior week, and are up 47 percent year-over-year.

- In mining company news, Gold Fields Ltd. exercised its option to buy a larger stake in Cardinal Resources Ltd. Previously Gold Fields owned approximately 11.1 percent of outstanding Cardinal shares and now owns 16.4 percent, according to a company statement. Gold Fields operates mines in Ghana, where Cardinals’ shovel ready assets are.

Weaknesses

- The worst performing metal this week was platinum, down 5.46 percent, with the majority of those losses coming in on the last day of the third quarter. India imported just 13.5 metric tons of gold in September, down from 93.8 tons a year earlier. This 86 percent year-over-year slump is significant, as India is the world’s second largest consumer of the metal. Higher gold prices have impacted buying, with gold futures in Mumbai rising 22 percent this year. However, demand is expected to rise in the 15 days before the Diwali festival, where Hindus consider it an auspicious time to buy gold for gift-giving. U.S. Mint data shows that American Eagle gold coin sales fell 8.3 percent in September from a month earlier, declining to 5,500 ounces.

- Gold’s volatility hit highs this week as traders struggle to read conflicting market signals. A measure of 90-day volatility rose to the highest since February on Tuesday, trading within a range of $77.80, which is the widest five-day scope since late June, reports Bloomberg. Ever-changing updates in U.S.-China trade negotiations have been a big contributor to the metal’s price swings.

- In a new sign of potential economic downturn, U.S. hiring missed projections and wage gains cooled in September even as the jobless rate fell to a half-century low. Bloomberg’s Katia Dmitrieva writes that “the jobs report caps a week of U.S. economic data that whipsawed stocks and sent already-low Treasury yields tumbling, led by a key manufacturing gauge that sank deep into contractions with the worst reading in a decade.”

Opportunities

- According to Wood Mackenzie, peak gold supply is coming if miners do not increase their spending on exploration and find new resources. Analysts wrote in a note that “exploration budgets were slashed following the fall in gold price from the highs in 2011 and 2012 and they have since failed to recover.” Tighter supply supports forecasts of gold bulls such as David Roche, president and global strategist of Independent Strategy, who said that gold could hit $2,000 an ounce by year end.

- Palladium has been the precious metal winner for almost four years and could have further to run. Spot prices are up 33 percent in 2019 and look poised to keep going as forecasts show the world will remain in deficit for the ninth year in 2020. Top miner MMC Norilsk Nickel PJSC sees the deficit continuing to widen due to a lack of mine investment. Sister metal platinum is finally starting to see prices rise, which should be positive for top miners Impala Platinum Holdings and Sibanye Gold Ltd. With metal prices rising, companies are luckily being cautious about spending. Miners are focusing on being more efficient and practicing smart capital discipline as they are aware that prices can easily take a turn.

- Southeast Asia’s largest bank DBS Group is bullish on gold. Bloomberg reports that in the bank’s fourth quarter asset allocation report it recommends dividend shares and gold, in addition to stocks, which look attractive in the world of negative-yielding bonds. CEO Hou Wey Fook writes that “against the backdrop of an unpredictable tug-of-war between easy monetary policies and geopolitics, gold will be favored as an effective portfolio diversified and to enhance risk-adjusted returns.”

Threats

- A Dutch pension fund is a growing example of conservative investors moving away from traditional assets to get a return. The Netherlands’ biggest pension fund is moving away from government bonds and into riskier assets in hopes of getting better returns as bonds are yielding less and less. Bloomberg writes that there is a boom in alternative assets such as private equity, property and infrastructure. Elliot Hentov, head of policy research at State Street Global Advisors, says “it’s a low-yield environment, everyone is piling in.” Perhaps more investors will pile into gold?

- Last week news broke that the Trump administration was discussing ways to limit U.S. investors’ portfolio flows in China and potentially delist Chinese companies from U.S. stock exchanges. The threat here is that this kind of talk demonstrates the U.S. is not trying to actually make a deal with China to end the trade war. In an essay about the topic, Ray Dalio writes that the International Emergency Economic Powers Act of 1977 could empower the president to unilaterally impose capital and FX controls to deal with a threat from outside the U.S.

- De Beers reported a 39 percent drop in its latest diamond sale and demonstrates why this is one of the worst years for the diamond industry in a long time, writes Bloomberg’s Thomas Biesheuval. The industry is suffering from an oversupply of polished gems. De Beers holds 10 sales events each year and sold just $295 million in its eighth sale of the year, according to the company on Thursday. RBC Capital Markets expects the company’s profit will drop by around 40 percent in 2019.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.92 percent. The S&P 500 Stock Index lost 0.33 percent, while the Nasdaq Composite climbed 0.54 percent. The Russell 2000 small capitalization index lost 1.30 percent this week.

- The Hang Seng Composite lost 0.18 percent this week; while Taiwan was up 0.60 percent, and the KOSPI fell 1.43 percent.

- The 10-year Treasury bond yield fell 15 basis points to 1.52 percent.

Domestic Equity Market

Strengths

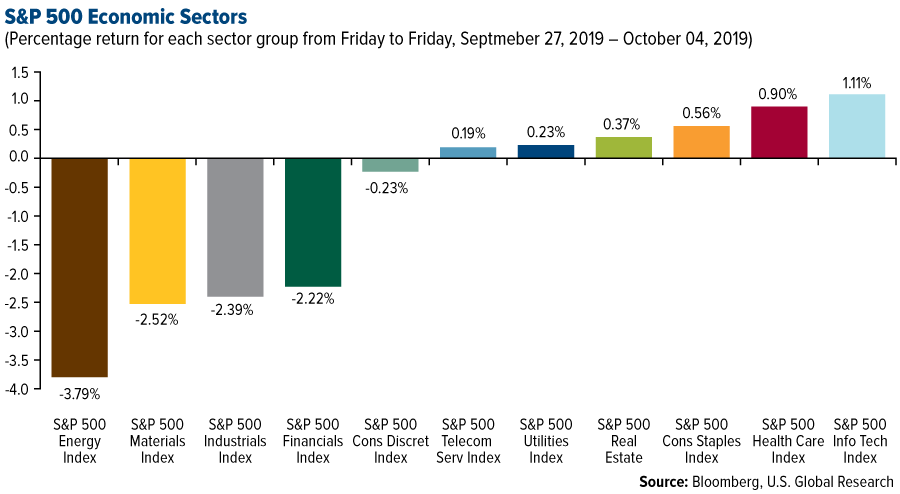

- Information technology was the best performing sector of the week, increasing by 1.11 percent versus an overall decrease of 0.42 percent for the S&P 500.

- Lennar Corp. was the best performing stock for the week, increasing 8.72 percent.

- PepsiCo beat quarterly revenue estimates on Thursday, writes Reuters, as ramped up advertising boosted demand for the company’s sodas and snacks. Net revenue rose 4.3 percent to $17.19 billion in the third quarter ended September 7, beating analysts’ estimates of $16.93 billion, according to IBES data from Refinitiv.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 3.79 percent versus an overall decrease of 0.42 percent for the S&P 500.

- E-Trade Financial Corp. was the worst performing stock for the week, falling 15.87 percent.

- Forever 21, an American fast-fashion retailer, has filed for bankruptcy, reports Business Insider. Linda Chang, the company’s executive vice president, told The New York Times that the retailer would soon cease operations in 40 countries and close up to 350 stores globally.

Opportunities

- Volkswagen’s VW brand expects to raise productivity to more than 6 percent in 2019, reports Reuters. "Our strategy is working. We will improve our productivity by over 6 percent and lower production costs per vehicle for the first time since 2013," VW’s board member for production and logistics, Andreas Tostmann, said in a statement.

- UPS beat out Amazon and Google to become America’s first nationwide drone airline. The U.S. Department of Transportation said on Tuesday it granted its first full Part 135 certification for a drone airline to UPS, meaning it will now be able to operate drones anywhere in the country.

- DraftKings, a fantasy sports site, is looking to raise new funding at a $2 billion valuation in its march to IPO, according to Business Insider. The company has hopes of pushing into the newly opened live sports betting space, which was cracked open last year after the Supreme Court overturned a federal ban on sports betting outside of Nevada.

Threats

- Major U.S. fund managers have billions of dollars at stake in some of the most popular Chinese stocks, exposing them to potential losses should the White House move to de-list Chinese firms from U.S. exchanges. "The proposed measures would completely undermine the international market and would harm the U.S.’s role as a conduit for international capital," Jefferies equity strategist Sean Darby wrote in a client note.

- U.S. focused pot stocks accelerated their losses after the U.S. Centers for Disease Control and Prevention said 77 percent of patients with vaping-related illnesses had used products containing THC.

- The herd mentality is more pronounced than ever in the stock market, as is the risk. So says Bank of America, which studied investors’ tendency to crowd into a small group of favorites by examining the 50 most-favored stocks among hedge funds and mutual funds and seeing how many overlap. Right now, it’s 12 percent, the largest proportion in the bank’s data going back to 2011. Periods of market stress or uncertainty can trigger de-risking and simultaneous selling of crowded trades, with illiquidity on exit exacerbating drawdowns.

The Economy and Bond Market

Strengths

- The U.S. unemployment rate fell to its lowest level in 50 years, the Department of Labor said Friday. The unemployment rate, now at 3.5 percent, fell by 0.2 percent from August to September.

- The U.S. economy is in a good place though it faces some risks, Federal Reserve Chairman Jerome Powell said Friday. “Unemployment is near a half-century low, and inflation is running close to, but a bit below, our 2 percent objective,” he said in the text of opening remarks to a Fed Listens event in Washington. “Our job is to keep it there as long as possible.”

- After a rough month for mortgage rates, borrowers saw a sign of hope and pounced on a small dip in the 30-year fixed rate. Total mortgage application volume was up 8 percent for the week, according to the Mortgage Bankers Association’s seasonally adjusted index. Volume was 58 percent higher than a year ago, when refinances were incredibly weak.

Weaknesses

- A measure of U.S. manufacturing unexpectedly fell deeper into contraction, posting the weakest reading since the end of the last recession as a global slowdown and the U.S.-China trade war increasingly weigh on the sector. The Institute for Supply Management’s factory index slipped to 47.8 in September, the lowest since June 2009, according to data Tuesday. The figure missed all estimates in a Bloomberg survey that had called for an increase from August’s 49.1 reading.

- The Labor Department reported on Friday that the U.S. economy added 136,000 jobs in September, missing consensus forecasts for 145,000 – a fresh sign that the economy is cooling.

- The World Trade Organization (WTO) has downgraded its forecast for global trade growth for this year and next as the repercussions of the U.S.-China trade war and a broader economic slowdown continue to play out. On Tuesday, the WTO said world merchandise trade volume is expected to rise 1.2 percent in 2019 — markedly slower than the 2.6 percent forecast in April. The revised projections come less than two weeks after President Trump called China a "threat to the world" and said there was little urgency for an interim trade agreement.

Opportunities

- White House economic advisor Larry Kudlow said Friday that “positive surprises” could emerge from the trade talks between the U.S. and China next week in Washington. “Coming into this, China has been buying some commodities. A small amount, but perhaps a good sign,” Kudlow said. Trade negotiators from the U.S. and China are set to resume principal-level trade negotiations on Thursday in Washington.

- A trade deal between the United States and India will be positive for global growth, said Borge Brende, president of the World Economic Forum. “I think there is something moving on the trade deal between the U.S. — the largest economy in the world, and India — the fastest growing among the emerging economies,” Brende told CNBC’s Tanvir Gill at the WEF India summit on Thursday. Indian Prime Minister Narendra Modi was in the U.S. for a state visit in September. This week, U.S. Commerce Secretary Wilbur Ross met Indian Finance Minister Piyush Goyal at the WEF summit, said Brende.

- Investors will be on the lookout for signs of inflation when U.S. CPI numbers come out next Thursday.

Threats

- The Fed’s regional banks are delving deeper into how climate change will impact businesses, consumers and the country’s $17 trillion asset banking system. "It’s hard to meet with a business person or a city or a community leader in this state" who doesn’t have questions on climate change, a former Goldman Sachs investment banker and one of 17 Fed policymakers said in response to a question.

- Europe’s manufacturing sector is spiraling downward, with PMI falling to a seven-year low. September’s PMI figure was 45.7, down from August’s 47.0, continuing its decline since the start of the year.

- Americans’ attitudes toward the economy took a sharp turn downward in the third quarter, according to the CNBC All-America Economic Survey, with just 23 percent believing the economy will improve in the next year, the lowest level of optimism in three years.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was sugar, which gained 10.67 percent on further news that Australian and Thailand sugar production may drop too. Last week sugar was stronger on rains in Brazil impacting the sugar cane harvest. Nickel had its best quarter in a decade as investors stocked up on the metal as Indonesia is set to ban exports at year end. The metal was up 38 percent in the quarter ended September 30. Stockpiles of LME nickel, which is a key ingredient in stainless steel, are at the lowest level since 2012. Bloomberg reports that inventories posted a record decline for a second straight day this week. “Even with all the macro headwinds and demand worries, any supply-side shocks can support a strong rally when stocks are low,” says Xiao Fu, head of commodities research at BOCI Global Commodities.

- According to Shell’s vice president for energy transitions, the Houston area is key to testing carbon capture and storage, which is the oil industry’s preferred method of removing greenhouse gasses from the atmosphere. Bloomberg reports that Shell already has one major carbon capture plant in Canada and that federal tax credits could help get projects up and running in the U.S. Chevron announced new targets for cutting greenhouse gases from operations. The company plans to lower upstream oil net emission intensity by 5 to 10 percent and upstream natural gas emission intensity by 2 to 5 percent from 2016 to 2023.

- Hochschild Mining announced that it is acquiring 93.8 percent of the BioLantanidos rare earth deposit in Chile that it doesn’t already own for $56.3 million, reports Bloomberg. The project is expected to be one of the lowest cost rare earth producers and CEO Ignacio Bustamante says it hopes to become a relevant player in the global rare earth market.

Weaknesses

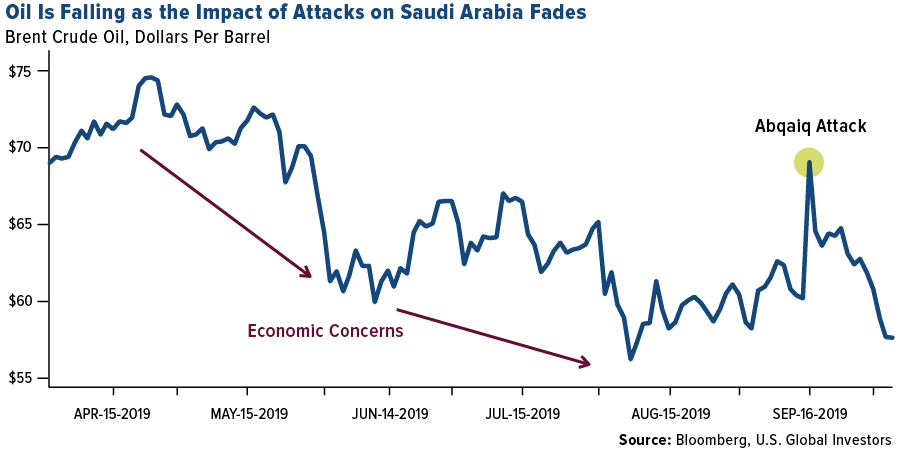

- The worst performing major commodity for the week was crude oil, which fell 5.47 percent. Oil had its biggest weekly decline since the middle of July after experiencing its worst quarter of 2019. Prices spiked the most on record after the news of an attack on Saudi Arabia oil production, but the elevated prices didn’t last as long as expected. Crude fell roughly 7.5 percent in the quarter ended Monday. The fossil fuel also suffered from news that American crude inventories had expanded the most since May and weaker economic data has some concerned that a recession is looming, which would hurt demand.

- Coal also saw a string of bad news globally. Foresight Energy, a U.S. coal miner, missed an interest payment, which is a sign that the company could be on the path to default, reports Bloomberg. So far this year, at least four coal miners have sought bankruptcy protection. The heaviest rains in 25 years have led to lower coal production out of India. Coal India cut shipments 20 percent year over year. In Germany, the government allocated less money than expected in its budget for closing coal-fired power plants. The administration earmarked just 1 billion euros to close 5 gigawatts of coal capacity, which is much lower than the expected 1.2 billion euro costs per gigawatt that utilities need to offset investments that they will need to write off early.

- Copper fell to a four-week low after the U.S. manufacturing PMI hit a 10-year low, which indicates contraction and points to potentially lower demand. “The bigger picture in the base metals market is that investor sentiment is very bearish,” says Caroline Bain, chief commodities economist at Capital Economics.

Opportunities

- Bloomberg reports that Russia’s state oil giant Rosneft tendered to sell a cargo of crude in euros, rather than the U.S. dollar, after doing the same for cargoes of marine diesel and fuel oil. The U.S. dollar is the traditional currency for oil transactions, but amid a growing number of sanctions against Russia, Iran, China and Venezuela, Russia is trying to remove U.S. dollar exposure dependence.

- In literal big news for wind energy, the world’s largest offshore wind farm is set to run on the world’s largest wind turbine, reports Bloomberg. General Electric has agreed to sell its 853-foot turbines to the SSE and Equinor wind farm off the coast of England.

- Clean energy-focused ETFs are some of the best performing funds so far this year. The Invesco Solar ETF, known by ticker TAN, has returned a whopping 58 percent so far this year and has outperformed all other unleveraged ETFs in the U.S., according to Bloomberg data. Two other ETFs are in the top 10 performers this year through September 30.

Threats

- Shipping rates for the largest oil tankers have surged after the U.S. imposed sanctions on six Chinese shipping companies on September 25. Rates from the Arabian Gulf to China are up 66 percent and to India are up 88 percent, reports Bloomberg.

- Continued negative economic data out of Germany, Europe’s largest economy, could spell an impending recession reminiscent of the 2009 crash. Manufacturing activity is at a decade low, according to the IHS PMI reading, and machinery orders declined by 9 percent in the first half of this year. Car companies are struggling due to stricter emission standards and the demise of the combustion engine. Bloomberg’s Chris Bryant writes that “Germany’s economic power was built on the back of its excellent gasoline and diesel cars. Their inevitable demise puts the country’s position as the ‘engine of Europe’ under threat.”

- The U.S. is the second largest player in onshore wind capacity, but it lags behind in harnessing the power of stronger and steadier gusts at sea with offshore wind. Bloomberg Businessweek writes that offshore projects in the U.S. often struggle to get off the ground due to the infamous failure of Cape Wind, after a 16-year battle with the Kennedy family and billionaire Bill Koch over its location just 5 miles from shore. Offshore wind is more expensive than onshore, but prices have fallen 64 percent from 2012 to 2018.

Emerging Europe

Strengths

- Turkey was the best relative performing country this week, losing 1.6 percent. Equites trading on the Istanbul exchange declined, but not as much as other markets. Turkish equites were supported by stronger economic data released this week. Inflation declined and manufacturing PMI ticked up to the 50 level in September from 48 the prior month.

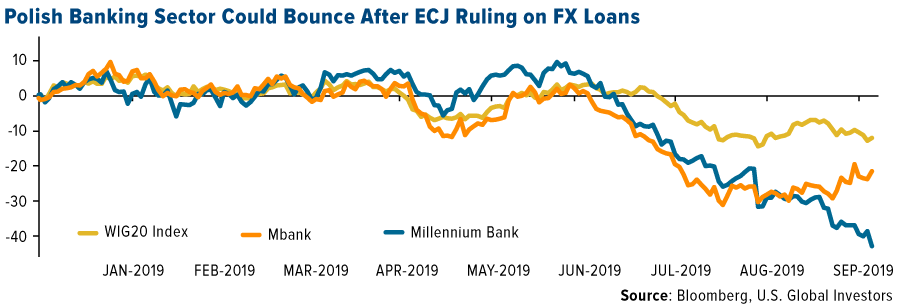

- The Polish zloty was the best performing currency this week, gaining 1.7 percent against the U.S. dollar. The currency appreciated after the European Court of Justice announced a softer ruling on unfair clauses in the FX loans, avoiding the worst-case scenario for Polish banks – a ruling that the initial value of the FX mortgages should be returned.

- Communication services was the best performing sector among eastern European markets this week. Play Communications SA, a Polish mobile phone provider, was the best performing equity gaining more than 2 percent.

Weaknesses

- Greece was the worst performing country this week, losing 5.5 percent. The Greek banking index declined 10 percent in the past five days, as investors were taking profits during the risk-off week. Year-to-date Greek banks gained 70 percent.

- The Turkish lira was the worst performing currency in the region this week, losing 40 basis points. Declining inflation may prompt the central bank to cut rates again soon. The bank already delivered two massive rate cuts this year, trimming by 425 basis points in July and 325 basis points in September.

- Consumer discretionary was the worst performing sector among eastern European markets this week. LPP SA, a Polish retailer, was the worst preforming equity losing 1.4 percent.

Opportunities

- The long-awaited European Court of Justice (ECJ) decision regarding foreign loans in Poland was largely, as expected, in line with an earlier opinion of the adviser to the court. The risk of potentially high FX losses to the bank remains, but given its recent underperformance, the worst-case scenario could be already priced in. Year-to-date Bank Millennium and MBank, which have the highest exposure to Swiss Franc loans, are down 43 percent and 22 percent, while the Warsaw stock exchange lost 13 percent during the same period.

- Turkey released better-than-expected September inflation, taking the annual inflation to 9.3 percent from 15 percent in August. The annual core inflation, excluding volatile goods such as food and energy, was down 7.5 percent from 13.6 percent in August. This drop in inflation can be explained mainly by the high base effect, as inflation in September 2018 was 24.5 percent year-over-year. The decline in inflation may prompt the Turkish central bank to cut rates further to stimulate growth. This week Turkish Finance Minister projected that the country will grow at 5 percent next year, versus just 50 basis points in 2019.

- The U.K. proposed a new Brexit deal to the euro-area. It presented a new plan for avoiding a hard border on the island of Ireland, suggesting for Northern Ireland (a part of U.K.) to stay in the European single market for goods but leave the custom union. If no deal is in place by October 19, Boris Johnson has been bound by law to ask the EU for a delayed departure date. There is no guarantee that the EU will agree to another delay.

Threats

- The euro-area September composite PMI index was revised down to 50.1, the lowest in more than six years. The services PMI was lowered to 51.6. The German composite measure slid deeper into contraction.

- The U.S. imposed new tariffs on as much as $7.5 billion of European exports annually in retaliation for illegal government aid to Airbus. The new plan included a 10 percent tax on jetliners and a 25 percent tax on a range of other items. The new duties, starting October 18, represent the most significant trade action against the EU since the Trump administration hit the bloc with steel and aluminum duties last year. Bloomberg Economics thinks this would deliver a serious blow to Europe’s aircraft industry and hit export orders for U.S. manufacturers. It may also mark an escalation in a trade war with the EU.

- Despite the European Central Bank’s (ECB’s) efforts to revive growth in the euro-area, inflation continues to slide below the ECB’s target. CPI dropped to its lowest monthly rate in almost three years at 0.9 percent in September, while the core reading ticked up from 0.9 percent to 1 percent. Eurostat said headline inflation was dragged down by particularly weak price growth of only 0.3 percent in industrial goods and a 1.8 percent drop in energy prices.

China Region

Strengths

- The best performing index in the region for the week was Taiwan, up 60 basis points. Mainland China was only open on Monday this week.

- The Markit Taiwan Manufacturing PMI jumped up from a prior reading of 47.9 percent to 50.0 for the September reading.

- China’s official Manufacturing PMI print for the September period beat expectations at a 49.8—still contractionary, but up from 49.5 and better than an expected 49.6. The Caixin China Manufacturing PMI also beat, coming in at 51.4, significantly better than consensus expectations of 50.2 called for and up from the prior reading of 50.4.

Weaknesses

- The poorest performing index in the region was India, down 2.96 percent. Mainland China was only open on Monday this week.

- South Korea’s year-over-year industrial production for the August measurement period declined by 2.9 percent, missing expectations for a minor 10 basis point drop and down from the prior reading of 0.6 percent growth.

- Macau gaming revenue for the September period was just over 22 billion patacas (~$2.7 billion), falling to the lowest level in a year.

Opportunities

- In what has of late developed into a regularly weekly comment, there remains opportunity for a degree of resolution to the U.S.-China trade war. With high-level trade talks set and apparently still on schedule for next week, there remains an upcoming window of opportunity. (Of course, beyond those talks looms the already-pushed-back implementation of the October tariff hike on Chinese goods by the President of the United States.) Perhaps at this point the real game is the December tariffs, which loom larger, one suspects, for both economies and certainly may be seen as a potentially pivotal point for the state of trade talks overall. But in the meantime, we do have scheduled talks for next week, China stepped in with amicable purchases of U.S. soy this week on a tariff waiver, and both sides are playing nice for the moment even in the midst of these looming deadlines.

- Third quarter GDP for U.S.-China trade war beneficiary Vietnam clocked in at a rock-solid 7.31 percent year-over-year figure, handily beating expectations for a 6.70 print and well up from the prior revised reading of 6.73 percent, granting global investors more insight on the rising economic power of the Southeast Asian nation. Year-over-year exports were up 9.0 percent in September for Vietnam, and imports jumped to 15.6 percent.

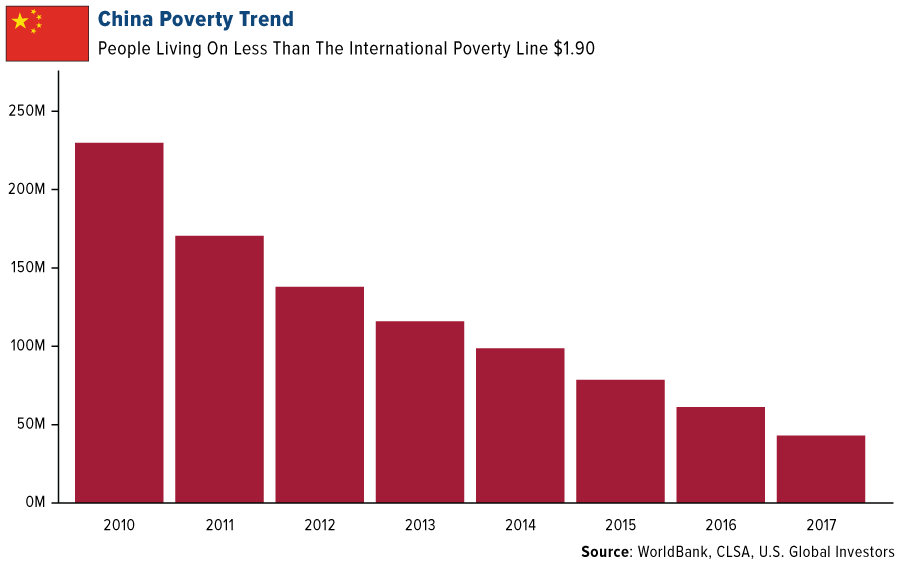

- In the midst of Chinese holidays and the National Day celebrations of the 70th anniversary of the founding of the People’s Republic of China, one would do well to consider that for all the ups and downs and various twists and turns of the last 70 years—not to mention the current spat with the United States of America—China has nonetheless enjoyed phenomenal growth, especially over its most recent decades. And as we here at U.S. Global like to emphasize, part of that story is the steady march forward of a growing middle class of Chinese consumers, amid trends like increasing urbanization, declining poverty, and rising tourism. We tend to focus here oftentimes on the present, and of course, on geopolitical and pragmatic macroeconomic reality, but sometimes it really pays to keep things in perspective and look at how we’ve gotten to where we are at present, appreciating some of the truly phenomenal growth from a longer-term point of view.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. To be sure, we have some positive moves with the resumption of agricultural purchases from China and with upcoming trade talks on the schedule for next week, but as observed already above, looming just beyond there is the bite of October 15th tariff hikes and the larger issue of the new December tariffs. All while this week President Xi Jinping stressed that China is an unstoppable force in his National Day speech and as President Trump argued that he has a number of “options” on China, following hints from the White House recently that the administration reportedly will entertain the idea of restricting portfolio flows to China. Is there a bit of posturing going on amid negotiations and trade talks and a trade war? Yes, naturally. But could the threats escalate? The talks break down? Sentiment get damaged? We’re in the on-again wave of an on-again/off-again cycle in this trade war, and the stakes remain high.

- Unrest continues in Hong Kong, with the first protestor shot by a live round during a National Day protest. Later in the week, HK lawmakers announced an intention to employ an old law on the books from the colonial period banning face masks. Many protestors attempt literally to mask their identities, and of course, there have been numerous deployments of tear gas as well to break up protests. As the protests continue, the effects upon the HK SAR’s economy continue as well, with HK’s year-over-year GDP, retail sales, and tourist arrival data all falling well below those declines of the Umbrella Protests and the 2015-2016 selloff. On his National Day speech, President Xi Jinping called for stability in Hong Kong and the "complete unification" of the nation.

- Another week, another 52-week high in the U.S. dollar. As noted in the past, this could continue to exert a degree of pressure on emerging markets and may well place increased pressure on central banks for timely and appropriate responses.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 4 was Centrality, up 361.84 percent.

- IKEA Iceland has taken part in a commercial transaction on ethereum, reports CoinDesk, using smart contracts and licensed e-money to facilitate the settlement of an order from local retailer Nordic Store. The platform where the transaction was carried out was provided by supply chain management firm Tradeshift, while the “programmable digital cash” came from ConsenSys-backed Monerium. Both Monerium and Tradeshift suggested the “world’s first” transaction shows that “government-regulated, programmable e-money is ready for mainstream markets.”

- A filing with the U.S. Securities and Exchange Commission shows that Stone Ridge Asset Management is planning a bitcoin futures product. On Wednesday, the company filed a prospectus for a cash-settled bitcoin futures fund – called the NYDIG Bitcoin Strategy Fund – reports CoinDesk.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 4 was DUO Network Token, down 78.36 percent.

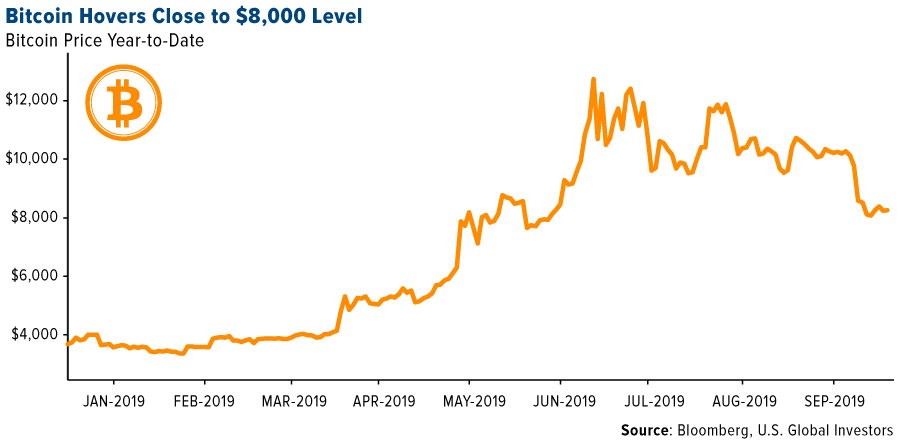

- The price of bitcoin struggled to remain above the $8,000 level as the week started, writes MarketWatch, following its worst weekly price loss of the year. The cryptocurrency has fallen about 34 percent over the past three months. “Bitcoin’s recent price drop is a result of technical and fundamental factors,” Bitpull Capital CEO Joe DiPasquale wrote last week.

- The month of September has not been pretty for the crypto-markets, writes Binance.com. In explaining bitcoin’s price drop in particular, the article explains that it could be the general indifference toward the much-hyped release of Bakkt, as BTC prices fell over $1,000 a day or so after trading began. “Bakkt was touted by many ‘crypto-observers’ as an additional primary channel to bring large institutional flows into cryptocurrency and digital asset markets. It may certainly still do so in the future… Short-term wise though, Bakkt’s disappointing start seems to have been a contributing factor to the recent price decline.”

Opportunities

- Did you know that the world’s most-used cryptocurrency isn’t bitcoin? As reported by Bloomberg, bitcoin, which accounts for around 70 percent of all the digital-asset world’s market value, doesn’t come out on top. Data from CoinMarketCap.com shows that the token with the highest daily and monthly trading volume is actually Tether.

- Morningstar Credit Ratings, whose parent company is Morningstar Inc., is making moves into the industry of assets issued on the blockchain, reports Forbes. The Chicago-based company is challenging Fitch and the other “Big Three” ratings agencies for pole position in the race to bring credibility to assets issued on a blockchain, the article explains, also known as cryptoassets.

- In a letter sent to Fed Chairman Jerome Powell, two U.S. lawmakers have outlined concerns they have about risks to the U.S. dollar, should another country or private company create a widely used cryptocurrency. As reported by CoinDesk and Bloomberg Law, the two lawmakers also inquired whether the central bank is looking into creating its own version. “We are concerned that the primacy of the U.S. dollar could be in long-term jeopardy from wide adoption of digital fiat currencies,” the Congressmen wrote.

Threats

- According to an article in the Wall St. Journal this week, cracks are beginning to form in the coalition that Facebook Inc. assembled in order to build a global cryptocurrency-based payments network. Following backlash from U.S. and European government officials, Visa Inc., Mastercard Inc. and other financial partners that initially signed on to help build and maintain the Libra payments network, are reconsidering their involvement.

- CoinDesk writes that former chief technology officer and co-founder of NiceHash, a mining power marketplace, has reportedly been arrested in Germany over U.S. charges that he is part of a hacking organization responsible for the theft of millions of dollars. The U.S. Department of Justice has released a warrant for his extradition, and according to Slovenian news site 24UR.com, Matjaz Skorjanec was apprehended by German federal police last Monday.

- As reported by Bloomberg and CoinDesk, executives from some of the biggest American banks told the Federal Reserve that Facebook’s Libra cryptocurrency would post a threat on monetary policies in the U.S. “Facebook is potentially creating a digital monetary ecosystem outside of sanctioned financial markets – or a ‘shadow banking’ system,” banks said, according to minutes of this month’s Federal Advisory Council meeting.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 245.78 | +3.99 | +1.65% |

| Gold Futures | 1,509.70 | +3.30 | +0.22% |

| Natural Gas Futures | 2.35 | -0.05 | -2.12% |

| S&P/TSX VENTURE COMP IDX | 558.76 | -10.82 | -1.90% |

| 10-Yr Treasury Bond | 1.53 | -0.16 | -9.33% |

| Nasdaq | 7,982.47 | +42.85 | +0.54% |

| Oil Futures | 52.84 | -3.07 | -5.49% |

| Hang Seng Composite Index | 3,488.11 | -6.35 | -0.18% |

| S&P 500 | 2,952.01 | -9.78 | -0.33% |

| DJIA | 26,573.72 | -246.53 | -0.92% |

| Korean KOSPI Index | 2,020.69 | -29.24 | -1.43% |

| Russell 2000 | 1,500.70 | -19.77 | -1.30% |

| S&P Energy | 423.76 | -16.69 | -3.79% |

| S&P Basic Materials | 352.92 | -9.11 | -2.52% |

| XAU | 91.11 | +0.04 | +0.04% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.35 | -0.09 | -3.76% |

| S&P/TSX Global Gold Index | 245.78 | -23.63 | -8.77% |

| 10-Yr Treasury Bond | 1.53 | +0.06 | +4.02% |

| Oil Futures | 52.84 | -3.42 | -6.08% |

| Gold Futures | 1,509.70 | -50.70 | -3.25% |

| S&P 500 | 2,952.01 | +14.23 | +0.48% |

| S&P Energy | 423.76 | -1.84 | -0.43% |

| Hang Seng Composite Index | 3,488.11 | -65.15 | -1.83% |

| DJIA | 26,573.72 | +218.25 | +0.83% |

| Korean KOSPI Index | 2,020.69 | +32.16 | +1.62% |

| Nasdaq | 7,982.47 | +5.60 | +0.07% |

| S&P Basic Materials | 352.92 | -2.03 | -0.57% |

| Russell 2000 | 1,500.70 | +15.94 | +1.07% |

| S&P/TSX VENTURE COMP IDX | 558.76 | -34.17 | -5.76% |

| XAU | 91.11 | -10.65 | -10.47% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.35 | +0.06 | +2.75% |

| 10-Yr Treasury Bond | 1.53 | -0.43 | -21.78% |

| DJIA | 26,573.72 | -392.28 | -1.45% |

| Oil Futures | 52.84 | -4.50 | -7.85% |

| S&P 500 | 2,952.01 | -43.81 | -1.46% |

| Gold Futures | 1,509.70 | +76.80 | +5.36% |

| S&P Energy | 423.76 | -42.57 | -9.13% |

| Nasdaq | 7,982.47 | -187.76 | -2.30% |

| Korean KOSPI Index | 2,020.69 | -88.04 | -4.18% |

| S&P Basic Materials | 352.92 | -18.10 | -4.88% |

| Russell 2000 | 1,500.70 | -71.42 | -4.54% |

| Hang Seng Composite Index | 3,488.11 | -344.98 | -9.00% |

| S&P/TSX Global Gold Index | 245.78 | +24.65 | +11.15% |

| S&P/TSX VENTURE COMP IDX | 558.76 | -29.07 | -4.95% |

| XAU | 91.11 | +7.06 | +8.40% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Play Communications SA

LPP SA

Royal Dutch Shell PLC

Hochschild Mining PLC

Equinor ASA

Franco-Nevada Corp.

Gold Fields Ltd

Cardinal Resources Ltd

MMC Norilsk Nickel PJSC

Impala Platinum Holdings Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Caixin China General Manufacturing Purchasing Managers’ Index (PMI) is closely watched by investors as one of the first available indicators every month of the strength of the Chinese economy. A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001). The ISM Manufacturing PMI is a composite index that gives equal weighting to new orders, production, employment, supplier deliveries, and inventories. The Non-Manufacturing ISM Report on Business is a purchasing survey of the United States service economy, published by the Institute for Supply Management since June 1998. The S&P/TSX Global Gold Index is designed to provide an investable index of global gold securities. Eligible Securities are classified under the GICS Code 15104030 which includes producers of gold and related products, including companies that mine or process gold and the South African finance houses which primarily invest in, but do not operate, gold mines. Bloomberg U.S. Treasury Floating Rate Bond Index is a rules-based, market-value weighted index engineered to measure the performance and characteristics of floating rate coupon U.S. Treasuries which have a maturity greater than 12 months.