I Believe Gold and Silver Are Just Getting Started

Date Posted: July 24, 2020

Read time: 48 min

The U.S. Mint made an unusual request this week. In a press release dated July 23, the bureau literally begged Americans to start putting coins back into circulation by spending or depositing them.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

The U.S. Mint made an unusual request this week. In a press release dated July 23, the bureau literally begged Americans to start putting coins back into circulation by spending or depositing them.

As you may have noticed, people just aren’t making transactions with coinage like they used to. That’s especially the case now in the age of the coronavirus. With many people sheltering-in-place, billions of dollars in everyday purchases are being made online that in normal times would have happened at the cash register.

This is creating a national coin shortage.

“Until coin circulation patterns return to normal, it may be more difficult for retailers and small businesses to accept cash payments,” the Mint writes, adding that for millions of Americans, cash is the only form of payment. Without coins, retailers can’t break bills.

This crisis, if it can be called that, got me thinking about the velocity of money. In simple terms, money velocity measures the number of times a unit of currency changes hands in a given period of time. As an illustration, imagine you spend $10 on lunch at a restaurant in a strip mall. That same $10 is then used by the restaurant owner to pay the lease, the landlord then uses it to pay its own creditors, and so on.

When the velocity of money increases, it suggests greater economic activity. Money is being spent more freely and rapidly. And when it decreases, it suggests the opposite—that the economy is stagnating or deteriorating. People aren’t spending.

Below is the velocity of M2 money supply, which includes not just cash but also so-called “near money”: savings deposits, money market securities and the like. As you can see, it’s at its lowest level ever, using 60 years’ worth of data.

So what does this mean, and can we blame coin hoarders for this decline? Hardly. Instead, we should be directing the blame at the Federal Reserve, which has flooded the economy with easy money.

Record Money-Printing Has Been Rocket Fuel for the Price of Gold

Never before in its 244-year history has the U.S. economy been so saturated with money. In fact, there’s too much of it. M2 money supply growth is at 24 percent year-over-year, the fastest rate ever.

Obviously the economy isn’t growing that quickly. It’s simply impossible for much of this newly-issued money to be lent out to consumers, and with rates so low, there’s little financial incentive to do so. So it’s just sitting in banks’ excess reserves.

Kind of like how coins are just sitting in people’s couch cushions and mason jars right now instead of being put into circulation.

For many people, this underlines the belief that fiat currency is intrinsically worthless. Because cash is not linked to a hard asset—or, for that matter, anything of value—the central bank is free to print as much of it as it pleases, right out of thin air, regardless of there being a demand for it or not.

And as anyone who’s taken high school economics knows, when supply outpaces demand, the value of any asset plummets.

Dalio and Mobius Urge Investment in Gold

“Cash is trash,” Ray Dalio, founder of Bridgewater Associates, the world’s largest hedge fund firm, said back in January. “There’s still a lot of money in cash.”

Instead, Dalio advocates for a highly-diversified portfolio, one that includes gold and other hard assets that we can’t just print more of.

“I believe that it would be both risk-reducing and return-enhancing to consider adding gold to one’s portfolio,” Dalio wrote last July in an article posted on LinkedIn. That same month, he revealed that gold would be among his top investments at Bridgewater.

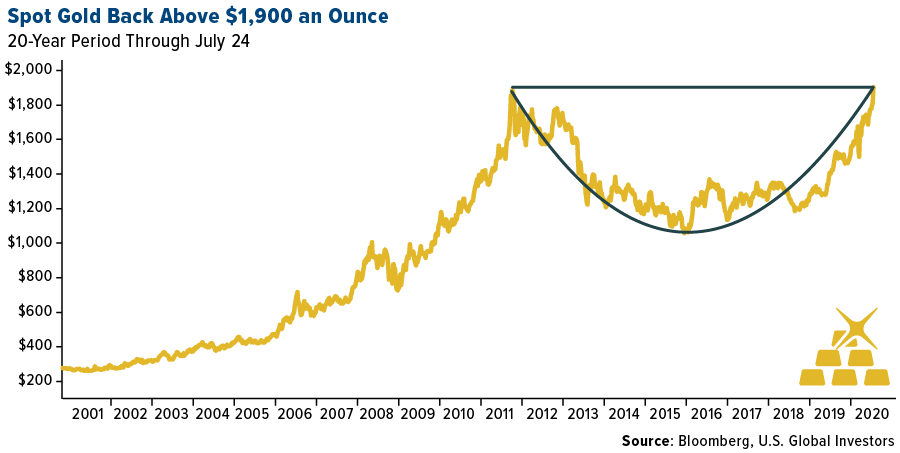

It was a masterful call. Since he wrote the article, spot gold has climbed 35 percent. And today, for the first time since 2011, the precious metal crossed above $1,900 an ounce.

Dalio isn’t the only big-name investor and money manager who’s recently thrown his weight behind gold. Speaking to Bloomberg TV today, emerging markets investor Mark Mobius urged viewers to buy gold now and “continue to buy” as interest rates remain near zero and as COVID-19 continues to impact mine output.

And Jim Reid, research strategist at Deutsche Bank, reportedly described himself as a gold bug recently, adding that he believes “fiat money will be a passing fad in the long-term history of money.” You may consider Reid’s position extreme, so do with it what you will.

Hi Ho Silver!

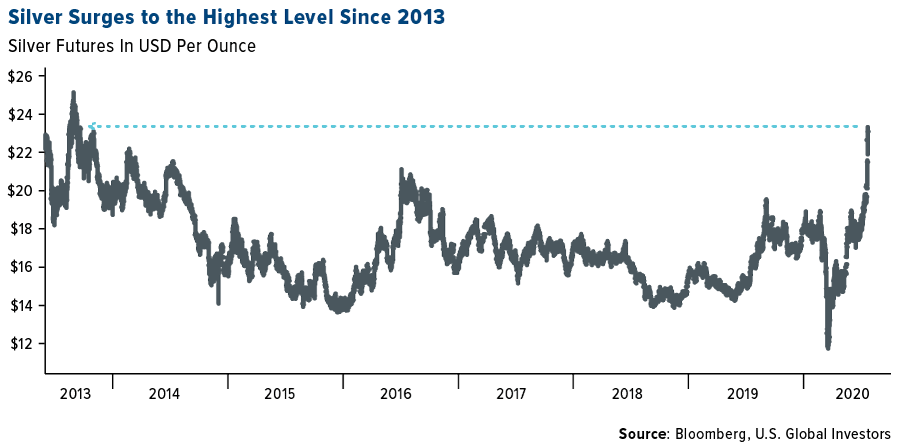

When gold makes moves like this, silver isn’t too far behind. The white metal rose above $23 an ounce on Thursday before trading in the $22.70 range on Friday. Since silver’s 52-week low in mid-March, holdings in silver-backed ETFs have increased by 255 million ounces. Total holdings now stand at a record of just under 860 million ounces, according to Bloomberg data.

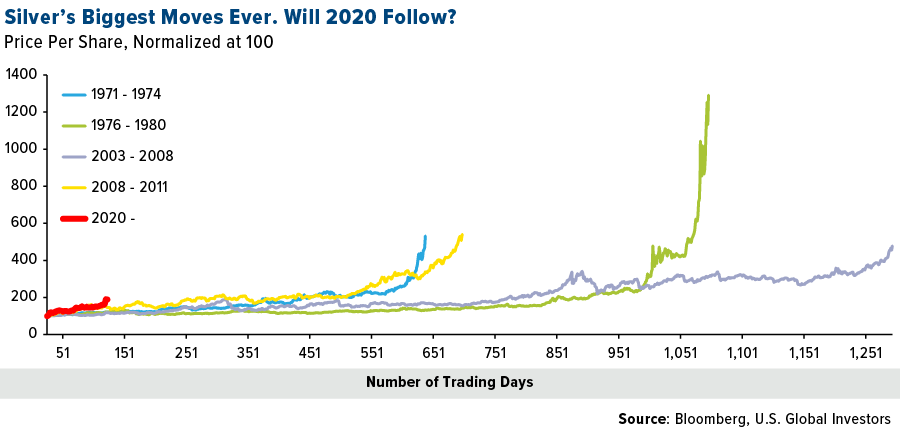

I believe silver is only getting started. As I explain in this video, silver has historically had a higher beta than gold. When gold has gone up 10 percent, silver has gone up 15 percent. The reverse has also been true: When gold has fallen 10 percent, silver has fallen 15 percent.

We all know that past performance is no guarantee of future results, but you can see in the chart below that the white metal could possibly be setting up for another epic run-up. At this stage of the bull market, silver’s current price appreciation is ahead of any previous rally.

I’m pleased to see the ratio between the gold price and silver price fall further off its recent all-time high. This shows that the white metal is acting more competitively against its more expensive cousin.

Mark Your Calendar for July 30…

This upcoming Thursday, July 30, at 9:00am CT, I will be co-hosting a webcast with O’Shares ETF’s Kevin O’Leary—Mr. Wonderful himself. We’ll be discussing internet giants and airline stocks.

Email info@usfunds.com for the free registration details!

Gold Market

This week spot gold closed at $1,902.02, up $91.60 per ounce, or 5.06 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.83 percent. The S&P/TSX Venture Index came in up 2.44 percent. The U.S. Trade-Weighted Dollar sunk 1.66 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-23 | Initial Jobless Claims | 1300k | 1416k | 1307k |

| Jul-24 | New Home Sales | 700k | 776k | 682k |

| Jul-27 | Hong Kong Exports YoY | 4.2% | — | -7.4% |

| Jul-27 | Durable Goods Orders | 7.0% | — | 15.7% |

| Jul-28 | Conf. Board Consumer Confidence | 94.2 | — | 98.1 |

| Jul-29 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Jul-30 | Germany CPI YoY | 0.2% | — | 0.9% |

| Jul-30 | GDP Annualized QoQ | -35.0% | — | -5.0% |

| Jul-30 | Initial Jobless Claims | 1450k | — | 1416k |

| Jul-31 | Eurozone CPI Core YoY | 0.8% | — | 0.8% |

Strengths

- The best performing precious metal for the week was silver, up 17.79 percent. Silver had its biggest weekly gain in nearly 40 years and could keep soaring. The metal hit its highest level since 2013. Mike McGlone, commodity strategist at Bloomberg Intelligence says the white metal could eventually climb to $30 an ounce amid a broad-based bull market for precious metals. McGlone predicts the metal will stay between $20 and $25 for an extended period before moving higher. The Global X Silver Miners ETF had a ninth straight day of inflows and the iShares Silver Trust saw five consecutive days of money flows.

- Gold has rallied an amazing 24 percent so far this year and rose above $1,900 an ounce for the first time since 2011. Investments in U.S.-listed commodity ETFs rose last week for the fifth straight week of inflows, according to Bloomberg data. Precious metals funds saw investment inflows of $3.8 billion in the week ending July 22, which is the second largest weekly inflows ever, according to Bank of American strategists citing EPFR Global data.

- Veteran investor Mark Mobius says that investors should buy gold now and keep buying it as political tensions and worries over global growth fuel the bullion rally. Mobius said in a Bloomberg TV interview this week that “I would be buying now and continue to buy. When interest rates are zero or near zero, then gold is an attractive medium to have because you don’t have to worry about not getting interest on your gold.”

Weaknesses

- The worst performing precious metal for the week was gold, still up an incredible 5.06 percent. With gold positive 24 percent for the year, investors are broadening their exposure across the precious metals space with palladium and platinum both with nearly double digit gains this week too.

- Teck Resources Ltd reported an 82 percent drop in second quarter adjusted profit as the Covid-19 pandemic hurt demand for its products and squeezed prices, reports Kitco News. Miners globally have been faced with challenges in the commodities market, forced mine closures and production cuts. Teck largely produces copper and zinc and suspended its 2020 outlook in April.

- Pan American Silver announced this week that it is moving two of its operations in Peru into care and maintenance after several works at the mines recently tested positive for Covid-19.

Opportunities

- Platinum could rise higher along with gold, according to UBS Group AG. “Our near-term bullish view on gold implies higher platinum prices this year,” said analyst Giovanni Staunovo in a note this week. The bank raised its platinum forecast to $975 an ounce at the end up September, up from $850 an ounce. U.S. imports of platinum from Switzerland more than tripled in June from a month earlier to 3.4 tons – the highest level since October 2006.

- According to Deutsche Bank AG, the close correlation between gold and the Japanese yen has broken down in the new macro environment. A risk-averse environment that leads to easy monetary policy, which in turn triggers a rebound in risky assets, is among the most constructive for a long-gold and short-yen position, writes strategist Alan Ruskin. “Gold then remains the easier long” versus the dollar or yen.

- Gold miners have room to catch up with spot gold. The performance of gold miners relative to the MSCI World Index has widened a gap with spot prices in recent years, signaling plenty of catch-up potential. According to Societe Generale strategist Sophie Huynh, “both fundamentals and positioning look aligned for gold miners to shoot higher.”

Threats

- Gold’s meteoric rise is flashing a warning signal that faith in central banks has disappeared. Bloomberg’s Eddie van der Walt comments: The risk is that top central bankers’ “clay feet are exposed by asset price bubbles and the fear of stagflation. In particular, I’m starting to hear the question: ‘If these people really knew what they’re doing, why is gold going gangbusters?’ The assumption being that there should be no reason to own the metal if growth is steady and inflation is benign.”

- U.S. and China tensions rose dramatically this week. The U.S. ordered China to close its consulate in Houston after accusing it and other Chinese diplomatic missions of economic espionage and visa fraud, reports Wall Street Journal. Beijing then ordered the closure of the American consulate in Chengdu in retaliation on Friday.

- Many see a bubble brewing. According to a Bank of America survey, a majority of fund managers believe tech stocks to be the “most crowded trade” in history. The combined market cap of Apple, Amazon, Microsoft, Google and Facebook now represents close to a quarter of the total S&P 1500 market cap. tech stocks, as measured by the NASDAQ 100, are now more overvalued relative to the S&P 500 than they were during the dotcom bubble, after which the market tumbled nearly 50 percent.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.99 percent. The S&P 500 Stock Index fell 0.02 percent, while the Nasdaq Composite fell 1.06 percent. The Russell 2000 small capitalization index lost 0.02 percent this week.

- The Hang Seng Composite remained flat this week; while Taiwan was up 1.20 percent and the KOSPI rose 0.76 percent.

- The 10-year Treasury bond yield fell 3 basis points to 0.584 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 2.10 percent versus an overall decrease of 0.29 percent for the S&P 500.

- Advanced Micro Devices was the best performing S&P 500 stock for the week, increasing 26.09 percent.

- Twitter stock soared after the company reported adding 20 million users in three months. The popular social media platform grew its daily active users by 34 percent year-on-year to 186 million.

Weaknesses

- Information technology was the worst performing sector for the week, decreasing by 1.54 percent versus an overall decrease of 0.29 percent for the S&P 500.

- FirstEnergy Corp was the worst performing S&P 500 stock for the week, falling 30.04 percent.

- Las Vegas Sands Corp., the world’s largest casino company, is painting a bleak picture of the U.S. gambling capital for investors, writes Bloomberg, saying COVID-19 has devastated the city’s bread-and-butter convention business, with no significant recovery in sight. “We’re in a world of hurt here,” Sands President Rob Goldstein said Wednesday on a conference call, after the company reported a 97 percent drop in second-quarter revenue.

Opportunities

- Bill Ackman’s blank-check acquisition company began trading on Wednesday after raising $4 billion, reports Business Insider. Ackman has not revealed which companies he’s aiming to buy, though he previously said he’s looking for "high-quality, venture-backed businesses."

- Warren Buffett just plowed $800 million into Bank of America, writes Business Insider, boosting his stake to over 11 percent. The billionaire investor and Berkshire Hathaway CEO scooped up nearly 34 million shares in three days.

- Fiat Chrysler and Waymo just announced an exclusive deal for advanced self-driving technology. Waymo will provide its autonomous "driver" technology to FCA’s entire vehicle brand portfolio.

Threats

- Microsoft reported earnings for its fiscal fourth quarter and the full 2020 fiscal year earnings at market close on Wednesday, beating analyst expectations for overall results but missing estimates on its key Azure cloud computing business unit, including its Office products. The firm reported revenue of $38 billion, and earnings per share of $1.46.

- Morgan Stanley warns technology stocks are unusually vulnerable to earnings disasters over the next few weeks and said some tech companies could be hit hard by an earnings miss.

- UBS saw profits slide 23 percent in the second quarter as it warned of credit losses ahead due to COVID-19. The giant Swiss lender was the first major European bank to release second-quarter results, and they showed the impact the pandemic is having on the sector.

The Economy and Bond Market

Strengths

- Sales of new single-family homes raced to a near 13-year high in June as the housing market outperforms the broader economy amid record low interest rates. New home sales rose 13.8 percent to a seasonally adjusted annual rate of 776,000 units last month, the highest level since July 2007.

- Factory activity rebounded in July with the flash manufacturing PMI increasing to a six-month high of 51.3 from a reading of 49.8 in June. Economists had forecast the index for the sector, which accounts for 11 percent of the economy, advancing to 51.5 in July.

- The Conference Board reported its Composite Index of Leading Economic Indicators increased 2 percent during June following a 3.2 percent May rise. Seven of the ten components rose last month, as they did in May.

Weaknesses

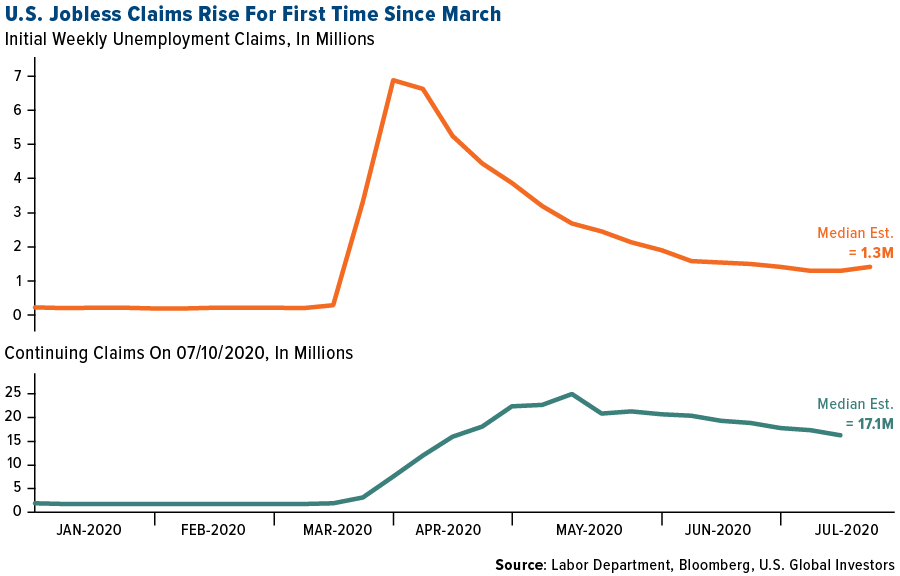

- The labor market recovery is showing signs of a pause just as federal aid winds down. Initial jobless claims climbed to 1.42 million in the week ended July 18, up 109,000 from the prior period and marking the first advance since March. On a non-seasonally adjusted basis, claims actually declined. Continuing claims, which lag initial and measure the overall pool of recipients in state programs, fell to 16.2 million.

- The services sector flash PMI increased to 49.6 from a reading of 47.9 in June. However, service industry firms reported a faster pace of decline in new orders in July. Further, economists polled by Reuters had forecast a reading of 51 for the services sector, which accounts for roughly two-thirds of the U.S. economy. With the reading coming in below 50, the implication is that the service sector is still in contraction.

- Texas Comptroller Glenn Hegar is projecting that the state will have a $4.58 billion shortfall in the 2021 fiscal year because of the Covid-19 pandemic and recent volatility in oil prices, according to a statement from his office on Monday. The shortfall compares with the $2.89 billion surplus originally projected in October.

Opportunities

- Investors, looking to be reassured by the Fed Chair Powell, are expecting the Fed to strengthen its forward guidance on how long the ultra-loose policy will stay in place when it announces its July FOMC decision on Wednesday. Further, they are also looking for Powell to address concerns about the unexpected shrinkage of the Fed’s balance sheet in recent weeks as well as maybe fine tune some of the emergency lending facilities.

- Pimco’s David Hammer and Rachel Betton said in a report Wednesday that the Fed’s move into the $3.9 trillion municipal bond market supports investors moving toward longer-maturity debt that offers higher yields. Debt in the market has an average maturity of 12 years, while the Fed is buying state and local securities maturing in three years or less. “With economic recovery likely to be sluggish and short-term interest rates expected to be near 0 percent for at least a few years, we see value in longer maturities between 15 and 20 years,” they said.

- Durable goods orders out on Monday are forecast for a 6.5 percent monthly gain in June, a continuation of the nascent recovery.

Threats

- Lingering differences among Senate Republicans and the White House stalled the rollout of their proposal for another pandemic relief package this week, and Majority Leader Mitch McConnell said the $1 trillion GOP plan won’t be ready until Monday.

- The coronavirus pandemic may lead to an 8.1 percent decline in GDP in 2020 and persistently elevated unemployment in cities, according to an analysis commissioned by the U.S. Conference of Mayors. The report lays out daunting scenarios for America’s communities that may prove not dire enough, given that it assumes the outbreak will taper this year. Metropolitan areas will suffer a $1.45 trillion drop in economic output in 2020, with the financial effects of the pandemic on par with the Great Recession a decade ago.

- New York’s Metropolitan Transportation Authority (MTA) is considering nearly $1.4 billion of spending cuts and may impose steeper fare increases than planned as ridership may not return to pre-coronavirus levels until almost 2023. The MTA, the largest public transportation system in the nation, is in the midst of a “fiscal tsunami,” that’s wiped away 40 percent of its revenue, Pat Foye, the agency’s chief executive officer, told board members Wednesday. The MTA may impose bigger fare and toll increases, delay pension contributions, freeze wages, and postpone or reduce its record $51.5 billion capital program if Congress fails to allocate more relief funds to the agency, MTA officials warned board members.

Energy and Natural Resources Market

Strengths

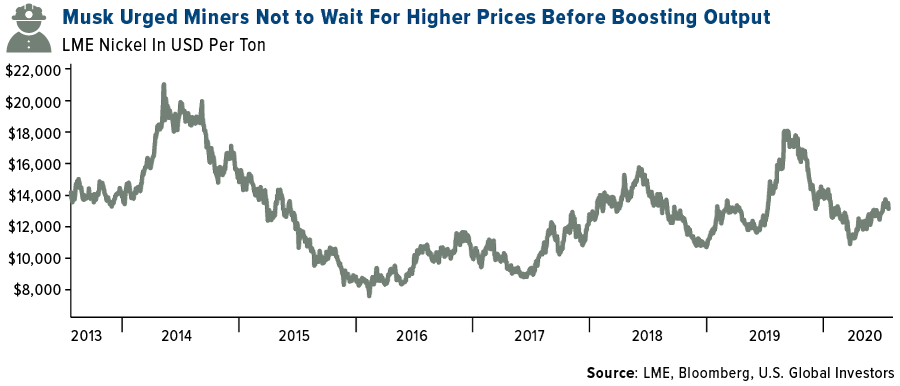

- The best performing commodity for the week was palm oil, rising 6.27 percent to a 5-month high amid increased demand in India and China and expectations that Malaysian supply will fall. Nickel rallied the most in two months on Thursday after Tesla founder Elon Musk urged miners to boost supply of nickel, a critical battery material. Bloomberg notes that nickel climbed as much as 3.2 percent after Musk’s comments on an earnings call.

- World Steel Association data shows the steel output contraction outside of China eased for a second month in June, a small sign of improvement as economies reopen. American steel producers are anticipating higher demand soon, as evidenced by raising prices. U.S. Steel Corp raised prices of benchmark prices by a minimum of $40 a ton on Tuesday.

- Equinor ASA, Norway’s state-controlled oil producer, reported a surprise profit in the second quarter with help from trading gains and a tax change designed to help the local oil industry through the COVID-19 crisis, reports Bloomberg. The company reported adjusted net income of $646 million, which is down from $1.13 billion a year ago, but well ahead of expectations for a $250 million loss.

Weaknesses

- The worst performing commodity for the week was cotton, falling 2.97 percent, marking its biggest loss in 16-weeks with slack demand and the upcoming harvest next month in the U.S., the biggest producer in the world. Copper ended its nine-week rally as base metals fell on Friday morning amid concerns over the U.S. economy and rising tensions with China. The dispute between the world’s two largest economies could have a lasting impact on trade, darkening the demand outlook for industrial metals, writes Bloomberg news.

- GCL-Poly Energy Holdings halted output at its polysilicon plant in China after explosions on July 19 resulted from distillation unit problems. The company said it will likely take one month to make the repairs and restart production, which could result in a spike in global prices for solar materials.

- Schlumberger said it is cutting one-fifth of its workforce after the oil giant posted its worst quarterly sales in 14 years. The company is laying off 21,000 employees, which reduces staffing to an 11-year low. The COVID-19 pandemic has taken a massive toll on the energy industry. CEO Oliver Le Peuch said in a statement that “subsequent waves of potential virus resurgence pose a negative risk to this outlook.”

Opportunities

- Lynas Corp, the key source of rare earths outside China, says it will push ahead with its planned U.S. refinery project with or without support from the government. The company is seeking to build a separation plant for heavy rare earths in Texas. China currently supplies around 80 percent of America’s rare earths imports and Lynas’ new plant would add 10,000 tons of capacity, which is enough to meet the U.S. military needs, reports BloombergNEF.

- The EU launched a hydrogen strategy earlier this month that targets 40 gigawatts of renewable hydrogen capacity in the bloc by 2030. BloombergNEF notes that this plan will require massive infrastructure spending to get hydrogen up and running. The cost is estimated at 27 to 64 billion euros on pipeline spending by 2040. The U.S. Department of Energy award grants to several companies under a new $64 million hydrogen research and development program while Australia shortlisted seven companies for A$200 million in hydrogen grants.

- Chevron has been using solar panels to power pumps at one of its oil fields in San Jose. A 29-megawatt site owned by SunPower Corp is design to provide the oil field with 80 percent of its electricity. Bloomberg reports that Chevron will earn low-carbon fuel standard credits worth around $4 million a year at current prices.

Threats

- More than 20,000 Brazilians are asking for British judges for the right to sue BHP Group, the world’s largest miner, in U.K. courts over a deadly dam collapse five years ago, reports Bloomberg. An eight-day hearing began this week where judges will rule if British courts have jurisdiction over the case. If it moves forward, it would be the largest class action in U.K. history with the group seeking 5 billion pounds in damages.

- The U.S. nuclear industry faced two high profile blows in recent days with bribery scandals at utility giants. Federal officials arrested the speaker of the Ohio House of Representatives on racketeering charges tied to the bailout of two nuclear plants owned by Energy Harbor Corp, reports Bloomberg. Just four days earlier Exelon Corp agreed to pay $200 million to resolve a lobbying probe in Illinois where nuclear plants also receive aid. Nuclear companies have been lobbying the state for aid in recent years as natural gas and renewable energy take prominence.

- A surge in new wind and solar capacity is driving wholesale electricity prices as low as A$40 in parts of Australia, making it difficult for the world’s top coal exporter to make a profit. The country’s coal power plants make up more than half of Australia’s generation mix but are facing increased pressure due to the rise in renewables. Kerry Schott, chair of the Energy Security Board, said at a summit this week that “we’ve got a problem with coal closures.” Schott added that plants are becoming uneconomic and “some have got very tight margins at the moment.”

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 3 percent. The Bank of Russia delivered its smallest interest rate cut in months but left the door open for further reductions. Russia and Turkey are planning to reopen international flights, which should benefit both countries, as Turkey is a popular travel destination for Russian vacationers. Magnit PJSC, a food retailer, was the best performing stock trading in the VanEck Russia ETF (RSX), gaining 18 percent over the past five days.

- The Hungarian forint was the best performing currency this week, gaining 3.6 percent. All currencies of eastern Europe appreciated against the dollar, with the strength in the euro, after the leader of the EU agreed on the long-awaited 750 billion euro recovery fund.

- Consumer discretionary was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 3.5 percent. The central emerging Europe (CEE) region will be a large beneficiary of the 750 billion euro recovery fund that the EU just agreed on, but due to the Czech Republic’s high income and low debt level, it could find itself a net small contributor for the first time. Erste Group Bank, an Austrian bank listed on the Prague Stock Exchange, was the worst performing equity, losing 5.5 percent over the past five days.

- The Russian ruble was the worst relative performing currency in the region this week, gaining 15 basis points. The price of Brent crude oil, which historically has been highly correlated with the price of the country’s currency, was little changed this week.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

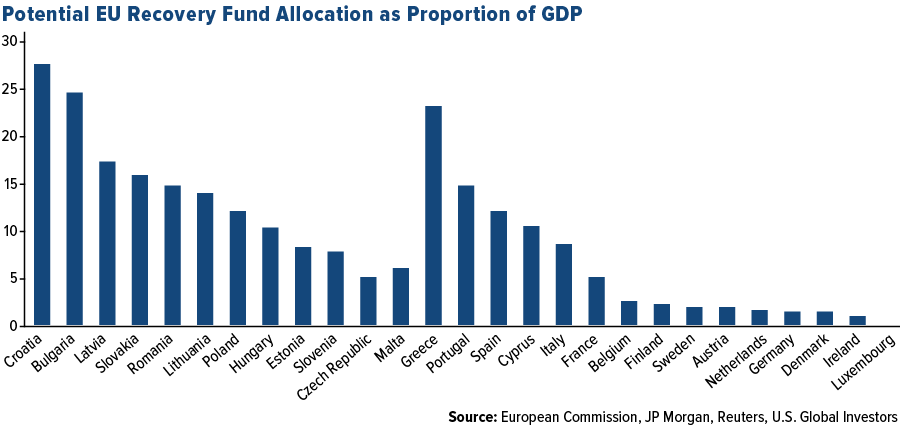

- EU leaders reached an agreement in the pandemic recovery fund. Now 390 billion euros will be distributed among members in the form of grants and the rest will be available as low interest rate loans. The central emerging Europe region will greatly benefit from it, as about 25 percent (187 billion euros) of funds have been provisionally allocated there.

- Bloomberg reported that the euro could turn into a credible safe-haven after the landmark EU recovery fund deal. Citing strategists, some are calling for the euro to race higher in the coming months and say it could potentially trade to $1.3. Positives highlight a new pool of high-quality, euro-denominated bonds that could be used by foreign investors for diversification. Other reports pointed out that greater political cohesion in the bloc could result in Europe’s bonds, currency and stocks becoming bigger features of international portfolios. Additionally, some believe the euro is currently under-represented in global central bank reserves relative to the size of the bloc’s economy.

- Preliminary July PMI data for the eurozone came out stronger, pointing to further recovery as Europe continues to successfully reopen its economy. The Service PMI was reported at 55.1 versus expected 51. Manufacturing PMI was reported at 51.1 versus expected 50.1. Composite PMI crossed well above the 50-level reaching 54.8, a level that was last time seen in June 2018.

Threats

- The FT reported on a report by Link Group, an investors services business, which said British companies cut payouts to shareholders by £22B in the second quarter as they raced to shore up their finances in the face of the economic crash caused by the pandemic. In total, only £16.1billion of dividends were paid in the second quarter, with 176 companies cancelling payouts and 30 more cutting them back – representing about three quarters of companies that normally pay a dividend in the period.

- Eurozone consumer confidence data deteriorated in July despite expectations of an improvement, as most European governments relaxed restrictions on business and travel related to the pandemic. The European Commission said the consumer confidence came in at negative 15 versus consensus of negative 12.4 and a prior month reading of negative 14.7.

- Next week actual GDP data will be released for the euro-area pointing to a very weak first half of this year. Bloomberg Economists predict second-quarter GDP contraction of 8 percent and 14.5 percent contraction on a year-over-year basis.

China Region

Strengths

- India was the best performing country this week, gaining 3 percent. Stocks moved higher, mainly supported by retail investors. This comes despite a stress test conducted by the Reserve Bank of India suggesting that the COVID-19 crisis could push Indian banks’ gross bad loans to the highest in nearly two decades. Reliance Industries, a refinery, was the best performing equity among stocks trading in the NSE Nifty 50 Index (NIFT), gaining 12.3 percent over the past five days.

- The Indonesia rupiah was the best performing currency this week, gaining 1.4 percent. Indonesia’s sovereign bond outlook is positive as concerns over debt monetization fade and room for further policy easing helps to support sentiment, according to Neuberger Berman.

- Industrial stocks were the best performers in the Hong Kong Stock Exchange.

Weaknesses

- Vietnam was the worst performing market this week, losing 4.9 percent. Vietnam’s coastal Da Nang City has quarantined more than 50 people who came into contact with a man who tested positive for COVID-19. The potential case could break Vietnam’s 99-day streak of having no new local community transmissions. The country has reported 412 cases and zero deaths. FLC Faros Construction Company was the worst performing equity among stocks trading in the VanEck Vietnam ETF (VNM), losing 18 percent over the past five days.

- The Chinese renminbi was the worst performing currency this week, losing 2.4 percent. Increased political tensions between the U.S. and China put pressure on the country’s currency. Investors are concerned about Washington and Beijing ordering each other to close consulates. Moreover, Secretary of State Michael Pompeo said Thursday that Chinese leaders were tyrants bent on global hegemony.

- Conglomerate stocks were the worst performers in the Hong Kong Stock Exchange.

Opportunites

- Ant Group, the parent company of China’s largest mobile payment company and backed by Jack Ma, plans to list simultaneously in Hong Kong and on the STAR board in Shanghai. The company was valued at $150 billion in its last funding round and is seeking a valuation of at least $200 billion, according to people familiar with the matter.

- Consumption is rising back to pre-pandemic levels in several Asian nations. Online retail sales have been a big contributor to growth in China, and South Korea posted positive monthly retail sales growth for two consecutive months in April and May, according to CLSA. Japan appears to have bottomed in April and major retailers observed improvements in May.

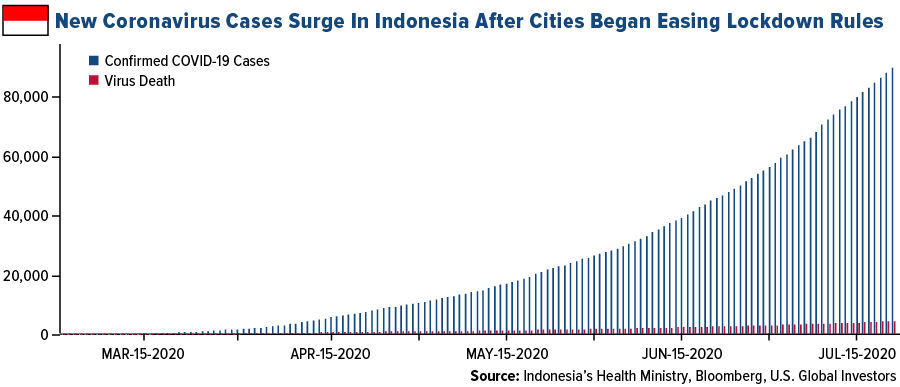

- PT Bio Farma, an Indonesian state-owned drugmaker, plans to begin human trials of Sinovac Biotech Ltd.’s coronavirus vaccine in August and could begin commercial production in early 2021. Indonesia is the world’s fourth-most populous nation and is the worst virus-hit country in Southeast Asia, with a death toll of 4,320 and confirmed cases nearing 90,000. Bloomberg reports that once the vaccine clears the final phase of clinical trials production and distribution can begin without delay from regulators.

Threats

- The U.S. ordered China to close its consulate in Houston after accusing it and other Chinese diplomatic missions of economic espionage and visa fraud, reports Wall Street Journal. China could respond with cuts to the U.S. Hong Kong consulate. This is a major escalation in the feud between two world superpowers.

- Reuters reports that Chinese regulators have seized control of nine troubled insurers, trust companies and securities brokers, signaling that the government is still working to contain hidden risks in the financial sector. The China Banking and Insurance Regulatory Commission said in a statement last week that four insurers and two trust companies would be taken over to “protect the public interest.”

- China is facing widespread floods after heavy rain boosted water levels in the upper reaches of the Yangtze River. More than 20 million people in 24 provinces have been affected by flooding in recent weeks. The economic impact of the environmental disaster has been estimated around $7.1 billion – an 11 percent increase year-over-year from prior flood seasons.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 24 was Aleph.im, up 365.49 percent.

- Tether has reached $10 billion in market capitalization as growth in 2020 picked up, writes CoinTelegraph. The company’s issuance has doubled from $5 billion in just five months since March 2020. Previously reported by CoinTelegraph, a relevant portion of this growth comes from existing fiat on exchanges being transformed into USDT.

- According to its most recent earnings report, out of nearly $8 billion in deposit growth that Signature Bank saw in the second quarter, $1 billion was raked in by the firm’s digital assets team, reports CoinDesk. The crypto industry is often a rich source of low-cost, non-interest-bearing deposits for crypto-friendly banks like Signature, Silvergate Bank and Metropolitan Commercial Bank.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended July 24 was Baz Token, down 91.52 percent.

- Russia passed a major bill this week related to cryptocurrencies, writes CoinTelegraph. The State Duma (Russia’s legislative body) passed the bill “On Digital Financial Assets,” of DFA, to be adopted officially on January 1, 2021. Although the bill does provide a legal definition to digital assets and legitimizes cryptocurrency trading in Russia, unfortunately it still prohibits the use of cryptos such as bitcoin as a payment method.

- Rising congestion on the Ethereum blockchain has driven up transaction fees tenfold this year to the highest since early 2018, writes CoinDesk. This is pressuring the network’s developers to speed up crucial upgrades, while possible creating an opening for competitors to lure away project developers, the article continues.

Opportunities

- VALR, South Africa’s biggest bitcoin exchange by trading volume, raised 57 million rand to held fund further expansion, writes Bloomberg. In an interview, VALR’s chief executive officer Farzam Ehsani said that the proceeds from the capital raise will be used to explore new products for the South African market. This includes collateralized lending and derivative trading, in turn broadening the company’s presence on the continent.

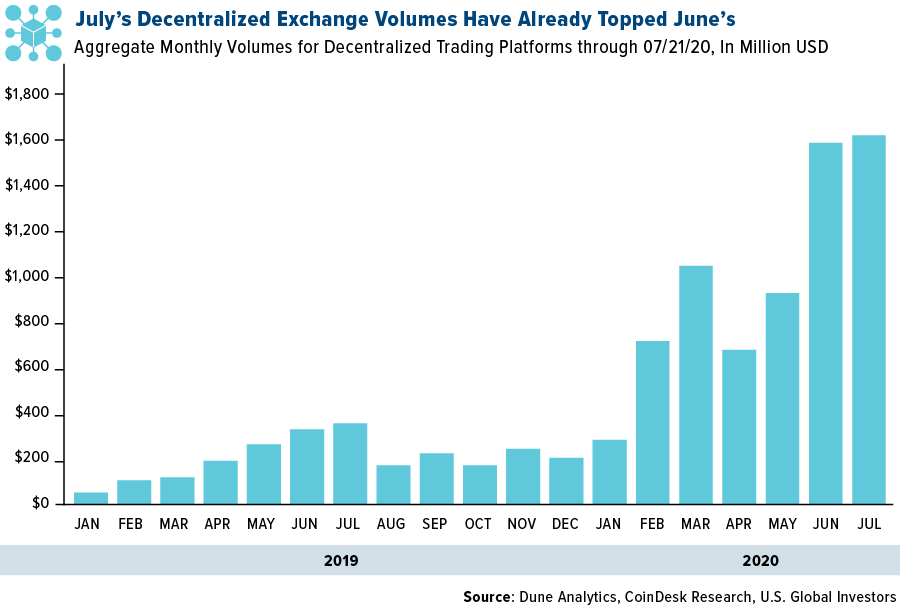

- July’s decentralized exchange volumes have already broken the all-time high set in June, shows data from Dune Analytics. As reported by CoinDesk, total traded volume for July passed $1.6 billion as of Tuesday. “For investors racing to get exposure to the newest decentralized finance (DeFi) projects, decentralized exchanges are the earliest and often only place to make those initial investments,” said Joseph Todaro, managing editor at Blocktown Capital.

- According to people familiar with the mater, PayPal has chosen Paxos to handle the new service’s supply of digital assets. The offering would make PayPal one of the most prominent mainstream companies to offer cryptocurrency purchases, joining fellow publicly-traded payments provider Square and unicorn stock brokerage Robinhood, writes CoinDesk.

Threats

- As reported by CoinDesk, the attackers who compromised Twitter in a massive breach last week might have accessed direct messages from up to 36 accounts – including CoinDesk’s. Twitter Support tweeted the following this week: We believe that for up to 36 of the 130 targeted accounts, the attackers accessed the DM inbox, including 1 elected official in the Netherlands.

- The head of research at Blockchain.com shared an interview this week showing that Indian banks are interested in cryptocurrencies but are also skeptical of heading further into the space due to the regulatory uncertainty. Over the past two years, India has already seen many blockchain and crypto businesses go bust, reports CoinTelegraph, due to the lack of clear regulations and banking support.

- Anthony Ghosn, son of former Renault and Nissan head and fugitive Carlos Ghosn, used Coinbase to pay two men $600,000 in bitcoin to get his father out of Japan last December, reports CoinDesk. U.S. prosecutors said Wednesday that Anthony sent 63 bitcoin to Michael and Peter Taylor, a father and son team who smuggled Carlos Ghosn out of Japan. This week Coinbase gave evidence to Japanese investigators showing a series of transactions between January and May 2020 from Ghosn’s Coinbase account to one belonging to Peter Taylor.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2020):

Tesla Inc, Schlumberger Ltd, BHP Group Ltd, Pan American Silver Corp, Amazon.com Inc, Microsoft Corp, Facebook Inc, Magnit PJSC

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The NIFTY 50 is a benchmark Indian stock market index that represents the weighted average of 50 of the largest Indian companies listed on the National Stock Exchange. The MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across all 23 developed markets countries. It covers approximately 85% of the free float-adjusted market capitalization in each country. The NASDAQ-100 Index is a modified capitalization-weighted index of the 100 largest and most active non-financial domestic and international issues listed on the NASDAQ. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Beta is a measure of the volatility, or systematic risk, of a security or portfolio in comparison to the market as a whole.