Investors Are Piling Into Safe Havens on Coronavirus Fears

Date Posted: February 21, 2020

Read time: 51 min

U.S. factories rebounded strongly in February, suggesting the manufacturing recession may finally be behind us after the industry contracted for six straight months.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

U.S. factories rebounded strongly in February, suggesting the manufacturing recession may finally be behind us after the industry contracted for six straight months. The Philadelphia Fed Manufacturing Index jumped an incredible 20 points to 36.7, its highest reading since May 2017, while New York’s Empire State Manufacturing Survey rose more than eight points to 12.9, a nine-month high.

We won’t get the Institute for Supply Management’s (ISM) U.S. manufacturing purchasing manager’s index (PMI) until the start of March, but I see the positive regional surveys as a sign that the PMI could beat expectations.

The news also bodes well for President Donald Trump’s reelection bid. The weak U.S. PMI, under pressure from the U.S.-China trade war, has been the one significant drawback in an otherwise solid economy and stock market.

But now we may find ourselves in a “out of the frying pan and into the fire” scenario: The “Phase One” trade deal between China and the U.S. was signed last month just as we began to see the first reports on the novel coronavirus, now known as COVID-19. As of Friday evening, the virus had spread to more than 75,500 within China, and as many as 1,200 outside the country. And although the recovery rate looks promising—more than 18,000 people have survived infection in China, compared to 2,200 deaths—there’s concern that people may be underestimating the risk.

A $1.1 Trillion Hit to the World Economy?

In a note to clients this week, analysts at Oxford Economics said they believe that the threat COVID-19 poses to the world economy is currently underappreciated. In a worst-case scenario in which the infection escalates into a full-blown pandemic, as much as $1.1 trillion could be wiped from the global economy in the first half of the year alone.

Again, this is a worst-case scenario, but consider the economic effects if most major cities around the world were placed on lockdown as Wuhan is right now. Lower discretionary spending, lower demand, lower productivity and lower investment would all be likely consequences.

The U.S. and eurozone would enter, as Oxford Economics lead economist Adam Slater puts it, “technical recessions.”

I’m not as much of an alarmist as Oxford is, but as I told Daniela Cambone this week, COVID-19 is already bigger than SARS and, in many ways, more closely resembles 9/11 because travel has been suspended. Wuhan, China, where the virus originated, is home to more than 11 million people. That’s four Chicagos. Shipping lines and ports have been impacted. Alphaliner, a shipping consultancy, estimates that 46 percent of scheduled departures from Asia to North Europe have been cancelled in the past four weeks.

The Chinese government is taking action, though, with the Ministry of Commerce enhancing support for trade financing, according to China Daily. The article reads that China will “give full play to the role of export credit insurance to help companies cope with the impact of the novel coronavirus epidemic.”

Seeking Safety: Gold Miners at 52-Week Highs

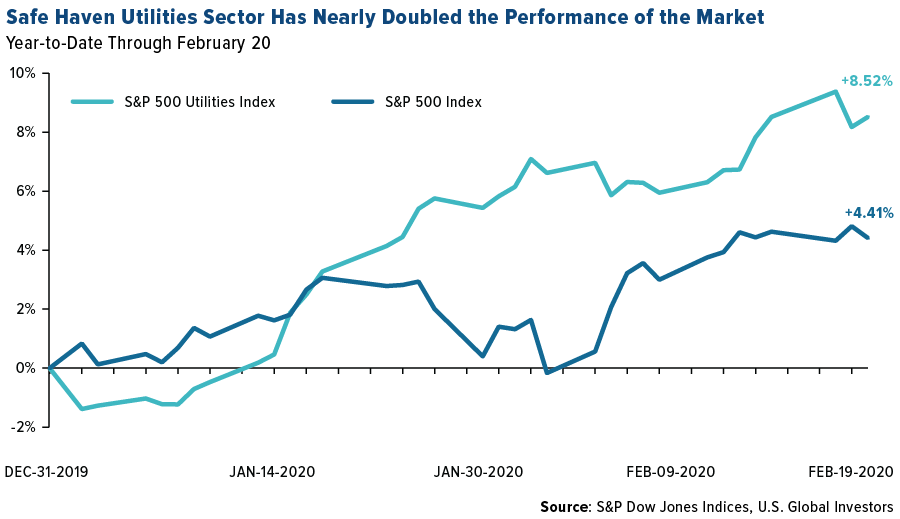

It’s for this reason we’re seeing investors rotate into perceived safe havens and defensive stocks, starting with utilities. Energy producers were up 8.5 percent year-to-date through February 20, nearly double the performance of the S&P 500 Index over the same period.

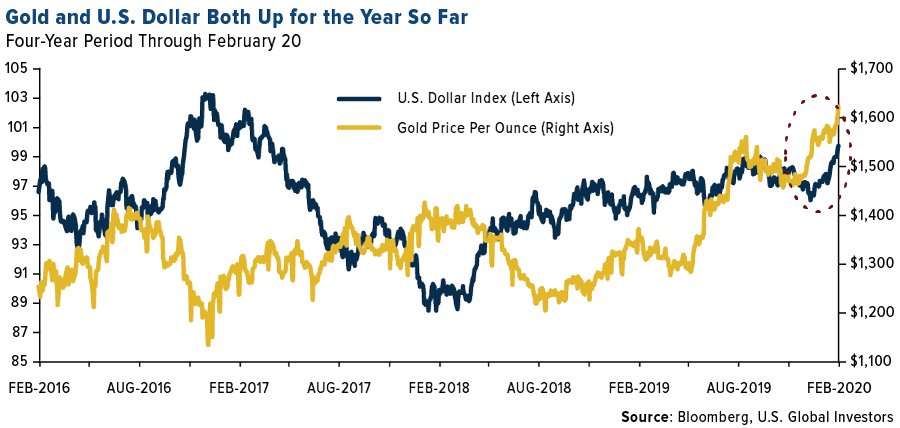

Gold, which I believe to be the ultimate safe haven, rose for the ninth straight day on Friday, crossing above $1,650 an ounce for the first time in seven years. This comes in defiance of a stronger U.S. dollar, which has been edging closer to the psychologically important 100 mark relative to other world currencies. It’s rare to see both assets go up at the same time—the four-year chart below makes that clear—but COVID-19 has spurred the flight to safety and quality, of which gold and the greenback can be considered.

Gold mining stocks have also broken out, with several hitting new 52-week highs this week, including Newmont Mining, Barrick Gold, Yamana Gold and Kinross Gold. Gold royalty and streaming companies, including Franco-Nevada and Wheaton Precious Metals, also hit fresh 52-week highs. Junior miners weren’t left out of the rally, either. The MVIS Global Junior Gold Miners Index climbed to a 52-week high, up more than 58 percent from its recent low in May.

For more on gold mining stocks, watch my interview with SmallCapPower’s Mark Bunting by clicking here!

Gold Market

This week spot gold closed at $1,643.07, up $59.01 per ounce, or up 3.73 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 8.35 percent. The S&P/TSX Venture Index came in up 1.94 percent. The U.S. Trade-Weighted Dollar rose 0.20 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-18 | Germany ZEW Survey Expectations | 21.5 | 8.7 | 26.7 |

| Feb-18 | Germany ZEW Survey Curent Situation | -10 | -15.7 | -9.5 |

| Feb-19 | Housing Starts | 1428k | 1567k | 1626k |

| Feb-19 | PPI Final Demand YoY | 1.60% | 2.10% | 1.30% |

| Feb-20 | Initial Jobless Claims | 210k | 210k | 206k |

| Feb-20 | Eurozone CPI Core YoY | 1.10% | 1.10% | 1.10% |

| Feb-25 | Hong Kong Exports YoY | -4.40% | — | 3.30% |

| Feb-25 | Conf. Board Consumer Confidence | 132 | — | 131.6 |

| Feb-26 | New Home Sales | 713k | — | 694k |

| Feb-27 | GDP Annualized QoQ | 2.10% | — | 2.10% |

| Feb-27 | Durable Goods Orders | -1.50% | — | 2.40% |

| Feb-27 | Initial Jobless Claims | 211k | — | 210k |

| Feb-28 | Germany CPI YoY | 1.70% | — | 1.70% |

Strengths

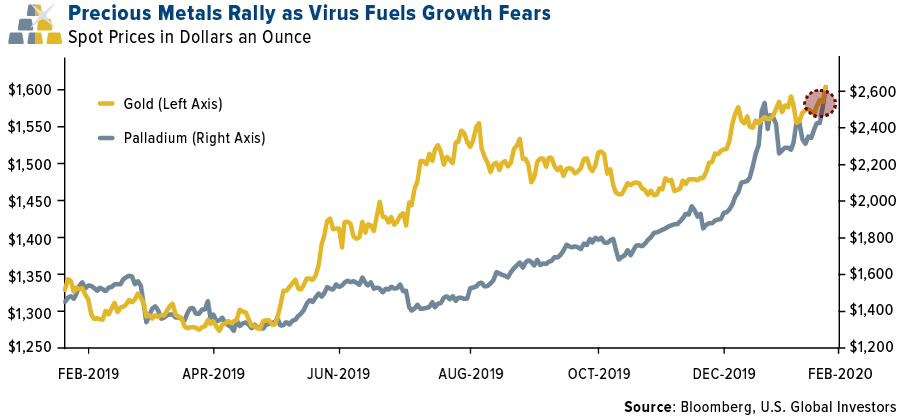

- The best performing metal this week was palladium, up 11.52 percent as precious metals had a stellar week. Gold hit a seven-year high this week, holding above $1,600 an ounce to the highest since February 2013 largely on coronavirus fears. The metal also rose on speculation that the Federal Reserve will ease monetary policy before year-end. Gold remained strong even as the U.S. dollar also held strong, as the two historically have traded inversely. Palladium futures contracts rose as much as 8 percent on Tuesday as investors flocked to safe haven assets. Edward Meir, an analyst at ED&F Man Capital Markets, said in an interview with Bloomberg that palladium is “like the Tesla stock of commodities.” The metal hit an all-time high of $2,504.50 an ounce on Tuesday and then $2,835 on Wednesday.

- Even though gold jewelry buying is down in India, the world’s second largest consumer, gold exchange-traded funds (ETFs) are gaining popularity, reports Bloomberg. The Association of Mutual Funds in India writes that Indians invested the most in gold ETFs in more than seven years in the month of January. Total assets managed by the 11 funds available rose to $870 million, which is 31 percent higher than a year earlier. However, that figure is still half of the all-time high reached in January 2013. Demand for physical gold in the country has fallen in recent months due to higher prices.

- Several miners announced strong earnings this week. Kirkland Lake Gold reported record production of 279,742 ounces and record adjusted net earnings of $185.3 million in the fourth quarter. Kirkland CEO said the company plans on doubling the quarterly dividend in the second quarter of 2020, reports Kitco News. Newmont Corp. reported that its fourth quarter adjusted net profit nearly doubled from the same time a year ago to $410 million. This increase was largely due to the acquired Goldcorp assets and higher gold prices. First Majestic Silver reported that it produced a record 25.6 million silver ounces last year and hit record revenues of $363.9 million, up 21 percent from 2018. Lastly, Sibanye-Stillwater reported an 80 percent increase in full year earnings. The miner said strikes disrupted operations in the first half of 2019, but rebounded in the second half of the year due to higher metal prices.

Weaknesses

- The worst performing metal this week was platinum, still up 1.11 percent. Anglo American, the parent company of De Beers, published year-end results and showed that moving to online sales cut the diamond maker’s revenue by 45 percent.

- Bloomberg reports that a Berlin court convicted three men of stealing a 100-kilogram solid gold coin worth $4 million in 2017. The coin is called the “Big Maple Leaf” and was stolen from the Berlin Bode Museum. It was issued by the Royal Canadian Mint in 2007 and was the biggest gold coin at the time – as big as a car tire. Police have not found the coin and assume it was cut into pieces for selling in smaller parts.

- OceanaGold Corp reported a smaller fourth quarter net profit than the same time a year ago, as revenue was hurt by the suspension of operations at its Didipio mine in the Philippines, writes Kitco News. Operations were halted due to restrictions on material movements imposed by local government. Oceana is working with the government to renew an agreement. The company did report strong gold production of 108,151 ounces in the fourth quarter, an increase of 20 percent from the prior quarter.

Opportunities

- Egypt is hoping for a gold rush as it eases restrictions for mining companies. Bloomberg reports that mining companies have long complained that the country, whose mineral wealth is largely underexplored, has a system of royalties and profit-sharing agreements that make it hard to operate. Last month Egypt dropped the requirement that miners form joint ventures with the government and limited levies. Aton Resources Inc. obtained mining rights in the country last week, which is the first since Centamin Plc achieved rights more than 10 years ago.

- Citigroup continues to update its bullish forecast for gold, reports CNBC. The firm said in a note on Wednesday that it believes market jitters will prompt invests to flee to safe haven assets, which could push gold prices to $1,700 an ounce in the next six to 12 months and $2,000 in the next 12 to 24 months. Ed Morse, lead analyst of the report, says “gold should perform as a convex macro asset market hedge, resilient during ongoing risk market rallies but a better hedge during sell-offs and volatility spikes.”

- The trend for more sustainable jewelry continues to grow. A new brand called Do Amore creates custom engagement rings that are sustainably and ethically sourced, both the diamonds and metals, and the proceeds from purchases contribute to providing water to an underserved area. Bloomberg reports that more brands are highlighting the use of recycled gold and platinum and minimal carbon emissions to appeal to the millennial and Gen Z age groups. Do Amore uses recycled metals and lets customers see which countries they source materials from.

Threats

- Nedbank CIB mining analyst Arnold Van Graan told S&P Global Platts in an interview that the palladium market isn’t necessarily a bubble, but that the price is overdone and there could be a correction. Van Graan said “I think we are going to correct to what is a sustainable price level.”

- The coronavirus continues to remain a threat to global growth and many industries. Demand for gold jewelry has already been hit in China, where buyers are staying home and avoiding public places. IMF managing director Kristalina Georgieva said on Thursday that it is still too early to assess the impact the virus will have.

- Economists say that the Federal Reserve needs to outline its plan for fighting the next downturn. Stephen Cecchetti, Michael Feroli, Anil Kashyap, Catherine Mann and Kermit Schoenholtz wrote in a paper for a University of Chicago Booth School of Business monetary policy forum that “going forward, low global bond yields likely will hamper any attempt to lower safe interest rates using either old or new monetary policy tools.” Bloomberg reports that the benchmark policy rate is now between 1.5 percent and 1.75 percent and inflation rose just 1.6 percent in 2019. The economists added, “If long-term nominal yields are already at very low levels when activity begins to slow, then the scope for using policies that aim at interest rates will naturally be limited.”

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.38 percent. The S&P 500 Stock Index fell 1.31 percent, while the Nasdaq Composite fell 1.59 percent. The Russell 2000 small capitalization index lost 0.52 percent this week.

- The Hang Seng Composite lost 1.36 percent this week; while Taiwan was down 1.09 percent and the KOSPI fell 3.60 percent.

- The 10-year Treasury bond yield fell 12 basis points to 1.47 percent.

Domestic Equity Market

Strengths

- Real estate was the best performing sector of the week, increasing by 1.11 percent versus an overall decrease of 1.07 percent for the S&P 500.

- E*TRADE Financial Corp was the best performing S&P 500 stock for the week, increasing 19.62 percent.

- Stamps.com gained more than $1 billion in market capitalization this week, in a move unsuspected by Wall Street analysts. Shares in the Internet-based mailing and shipping firm surged as much as 63 percent Thursday after the company announced earnings results that far exceeded analysts’ expectations.

Weaknesses

- Information technology was the worst performing sector for the week, decreasing by 2.05 percent versus an overall decrease of 1.07 percent for the S&P 500.

- ViacomCBS Inc. was the worst performing S&P 500 stock for the week, falling 19.21 percent.

- Shares of LivePerson plunged by 24 percent on Friday after the company said in a late filing on the previous day that fourth quarter net loss widened, missing estimates, and announced the departure of CFO Chris Greiner.

Opportunities

- NXP’s rising-star rating momentum continues with an upgrade to BBB at S&P and positive outlook at Fitch, which likely will result in lower borrowing costs as spreads further compress toward NXP’s technology peer group.

- Tesla’s next Gigafactory is back on track after a German court threw out an environmental challenge, writes Business Insider. A judge removed an injunction preventing Elon Musk’s electric-car startup from clearing forest to build its massive assembly plant.

- John Deere reported an unexpected rise in quarterly profits, reports CNBC. The farm-equipment titan posted a 4 percent rise in net income as the U.S. farm sector showed early signs of stabilizing.

Threats

- As demand plummets due to the coronavirus, airlines project that this could be their worst year since the global financial crisis. The International Air Transport Association (IATA) expects global air-traffic demand this year to be 4.7 percent lower than it previously predicted.

- Apple could lose out on $4 billion in sales as the coronavirus affects its ability to produce sufficient iPhones and AirPods, according to Business Insider. Analysts say Apple’s facilities in China have reopened "more slowly than expected." Additionally, Apple’s plans to launch a new iPad Pro model early this year could be delayed thanks to the coronavirus.

- The European Union is planning an industrial-data push and rules to rein in U.S. tech giants. The European Commission laid out proposals to exploit regional data, govern artificial intelligence, and constrain the likes of Facebook, Google and Amazon.

The Economy and Bond Market

Strengths

- The economy showed some more sizzle at the start of 2020, pointing to steady growth in the next several months, according to an index that measures the nation’s economic health. The leading economic index jumped 0.8 percent in January, the Conference Board said Thursday, increasing twice as much as Wall Street predicted.

- The number of Americans who applied for unemployment benefits rose slightly in mid-February, but the rate of layoffs in the U.S. economy doesn’t show signs of rising. Initial jobless claims edged up by 4,000 to 210,000 in the seven days ended February 15, the government said Thursday. Economists polled by MarketWatch had forecast a 210,000 reading.

- Building permits jumped to the highest level since 2007 as low mortgage rates and a solid labor market continued to fuel housing demand.

Weaknesses

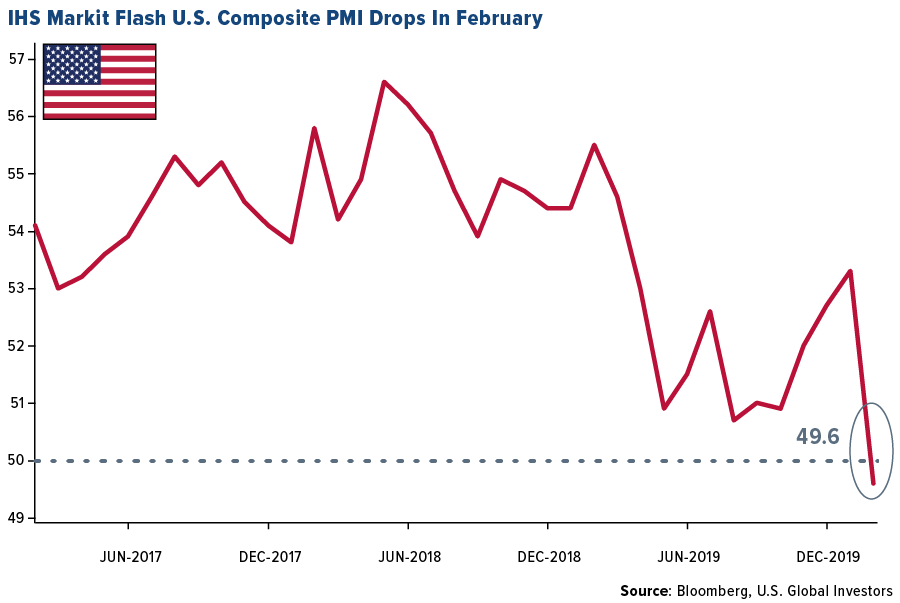

- U.S. business activity shrank in February for the first time since 2013 as the coronavirus hit supply chains and made firms hesitant to place orders, a warning sign that the outbreak is starting to dent the world’s largest economy. The IHS Manufacturing PMI, which measures composite output at factories and service providers, fell by 3.7 points to 49.6, the lowest level since October 2013, when the U.S. government shut down, according to preliminary figures released Friday. Readings below 50 indicate contraction.

- The National Association of Realtors said on Friday that existing home sales declined 1.3 percent to a seasonally adjusted annual rate of 5.46 million units last month. December’s sales pace was revised down to 5.53 million units from the previously reported 5.54 million units.

- After a solid start with steady rises in 2020, mortgage applications have taken a hit this week. According to the Mortgage Bankers Association, mortgage applications decreased 6.4 percent from last week, which saw a 1.1 percent increase.

Opportunities

- The economic calendar in the U.S. next week includes durable goods orders, consumer confidence and the second reading of fourth-quarter GDP. Most of these measures have fared well recently, and the expectation is for a continuation of strength.

- Governments across the world are starting to use more fiscal firepower to boost economies, though the shift may not be happening fast enough to appease central bankers who say they’re sick of carrying the burden of stimulus alone. In more than half of the world’s 20 biggest economies, analysts now expect looser budgets this year than they did six months ago, according to a Bloomberg survey of economist forecasts.

- The more concerns about the virus impact on foreign economies intensify, the more the dollar is likely to shine since the U.S. economy is better protected from a slowdown in China and U.S. authorities have policy room to react to any shock, unlike Europe or Japan.

Threats

- How to cope with the economic impact of the coronavirus is likely to be a key topic at this weekend’s meeting of Group of 20 finance chiefs. While the consensus of economists remains for a short-term hit to demand in China and then globally, followed by a rebound, that could prove too optimistic given Chinese factories are still operating around half their capacity and many workers remain housebound. The partial shutdown of the world’s second biggest economy is having an effect elsewhere by weakening trade, fraying manufacturing supply chains, reducing tourism and fanning investor uncertainty.

- U.S. 10-year yields fell below 1.5 percent this week to the lowest since September. The gap between two and 20-year yields has also compressed to within 11 basis points of inversion. This is concerning for the Federal Reserve, signaling that current monetary policy isn’t sufficient to boost longer-term growth and inflation.

- Long-term U.S. inflation expectations have fallen to the lowest since 2016, as per five-year five-year forward breakeven rates. This is concerning for the economy’s growth outlook.

Energy and Natural Resources Market

Strengths

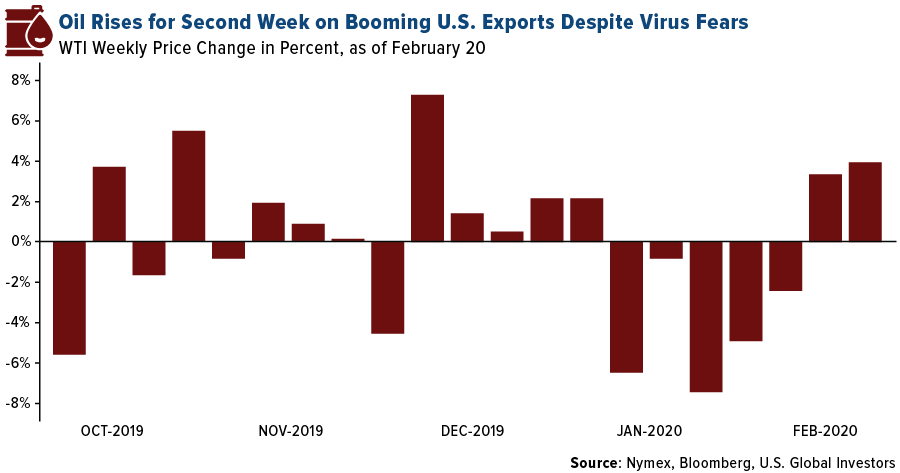

- The best performing major commodity for the week was palladium, which gained 11.52 percent as investors flock to safe haven assets. Oil had a second strong week after U.S. crude exports surged by more than expected to the equivalent of more than one-fourth of the nation’s output to foreign buyers, reports Bloomberg. U.S. stockpiles also rose by just 415,000 barrels last week, below the 3.2 million barrel forecast. Oil was also supported by supply disruptions out of Venezuela and Libya.

- U.S. Agriculture Secretary Sonny Perdue announced an initiative by the USDA to reduce the environmental impact of farming. Bloomberg reports that 21 farm groups announced a coalition on environmental sustainability, including the American Farm Bureau and the National Pork Producers Council. Perdue said there will be voluntary conservation incentives and efficiency improvements. Although the initiative does not include the phrase “climate change” or tout new regulations, it is a major step forward toward greener practices. The goal is to increase farm production by 40 percent while reducing the environmental footprint by half by 2050.

- Deere & Co. reported an unexpected increase in earnings for the fourth quarter and maintained its annual outlook. CEO John May said “farmer confidence, though still subdued, has improved due in part to hopes for a relaxation of trade tensions and higher agricultural exports.” Bloomberg reports that the U.S. Department of Agriculture expects American soybean stockpiles to fall back to pre-trade war levels when China comes back into the market.

Weaknesses

- The worst performing major commodity for the week was nickel, which fell 2.71 percent. As the coronavirus continues to hit China, steelmakers are still churning out the metal that no one wants to buy, according to Bloomberg News. It is difficult for most steelmakers to cut output because blast furnaces are designed to run constantly. Because of this, millions of tons of steel are piling up at mills with no buyers. Kevin Bai, analyst at CRU Group, said “inventories are at critically high levels” and “most mills are still trying to keep running for now though for technical reasons.”

- The Department of Homeland Security said in an alert on Tuesday that hackers used a phishing attack to gain control of a natural gas compressor facility that was forced to shut for two days. The name of the facility was not given. This is another attack in the last few years that has increased concerns about whether U.S. energy facilities are equipped to fend off cyberattacks. Bloomberg News writes that in 2018 several pipeline companies had their electronic systems for communicating with customers shut down after being hit by hackers.

- The Treasury Department Office of Foreign Assets Control sanctioned a unit of Rosneft PJSC for maintaining ties with Venezuela’s Nicolas Maduro and its state-run oil company. Rosneft is Russia’s largest oil producer. The Russia government responded by saying that the sanctions will not affect its relationship with Venezuela, pointing out that doing business with the country is not illegal. The sanctions will likely disrupt supply, which should be positive for oil prices.

Opportunities

- Thailand is normally the main supplier of raw sugar to Indonesia, but after a severe drought cut production, India is ready to step in with its supply. According to a Bloomberg survey of traders and officials, India may sell 250,000 tons of raw sugar to Indonesia by the end of May. India is just behind Brazil as the world’s top producer. India’s director general of estate crops at the Agriculture Ministry said that Indonesia has changed the color specification for raw sugar imports to allow shipments from India.

- Anglo American Plc is moving toward growth after spending nearly $1 billion in share buy backs. The miner is instead focusing on new projects and ramping up production through investments of $3 billion toward a U.K. potash project and $5 billion in a Peruvian copper mine. Bloomberg writes that miners have focused on giving returns to shareholders, but Anglo is setting itself apart by taking a different path. Anglo did write down the value of its coal assets by about $900 million, similar to Glencore’s move.

- While the coronavirus hurts demand for certain commodities, it isn’t hurting demand for rare earth minerals in China. Bloomberg reports that China has increased the first batch of mining quotas for rare earths, which are used heavily in technology. The quota for the country’s top six producers was set at 66,000 tons, according to the Ministry of Industry and Information Technology.

Threats

- EU President Charles Michel said that he wants to limit aid to countries that fail to respect the 2050 deadline for eradicating emissions – putting Poland at risk of losing access to an $8.1 billion transition fund. Bloomberg Green reports that Poland still relies on coal for more than 80 percent of its power generation and is alone among the bloc’s 27 nations in refusing to accept the deadline for carbon neutrality.

- Falling natural gas prices are leading to some of the marginal producers leaving the market. Bloomberg reports that Orsted A/S in Denmark and Iberdrola SA in Spain have already exited the business. New export projects from Australia to the U.S. have flooded the market with new supply of the fuel and warmer temperatures have hurt demand. Frank van Doorn, Vattenfall’s head of trading, said in an interview that “now is a pretty painful moment for the LNG market with such low prices.”

- This week the White House acknowledged that President Trump’s trade stance depressed economic growth and business investments, reports Bloomberg. Chief economist Tomas Philipson told reporters in a briefing on the annual Economic Report of the President that “uncertainty generated by trade negotiations dampened investment.” The U.S. economy grew by 2.3 percent in 2019, versus growth of 2.9 percent in 2018.

February 20, 2020Frank Holmes Says Invest in Gold Using Stocks and Jewelry |

February 19, 2020Why Frank Holmes Is Bullish on Mining Stocks |

February 11, 2020U.S. Global Investors Reports Financial Results for the Second Quarter of 2020 Fiscal Year |

|||

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 2 percent. Hungary’s central bank has been supporting the country’s growth by keeping its main rate fixed at a record low of 90 basis points since November 2016. However, spiking inflation and a weakening currency prompted the monetary policy members to announce possible changes to its low rate policy. OTP Bank reacted positively to the news, gaining 1.1 percent over the past five days.

- The euro was the best performing currency this week, gaining 25 basis points. Preliminary February PMI data released in Europe on Friday surprised to the upside. Eurozone flash manufacturing PMI climbed to 12-month highs, supported by stronger-than-expected manufacturing recovery in Germany and the United Kingdom. Manufacturing PMI in the U.K. was reported at 51.9 (vs. expected 49.7), Germany 47.8 (vs. expected 44.8) and the eurozone manufacturing rose to 49.1 (vs. expected 47.4).

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 3.2 percent. Banks sold off, with shares of National Bank of Greece losing 10 percent and Eurobank 8.5 percent. Banks’ balance sheets had been slowly improving, but Greek banks still are holding toxic debt on their books well above levels that regulators consider safe. According to the European Central Bank (ECB), non-performing loans still account for almost half of all debt.

- The Russian ruble was the worst performing currency in the region this week, losing 80 basis points. The ruble was under some pressure after U.S. Administration imposed sanctions on Rosneft Trading SA (a subsidiary of Rosneft, the biggest state-owned oil company) for its involvement in trading Venezuelan oil. However, the ruble remains attractive to investors as Russia has the highest real rates among major economies.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- The new government in Russia is focused on increasing social spending in the next few years. According to the government plan, the largest amount of money this year will be allocated to support poor families with children. The second-biggest beneficiary will be new mothers, as Russia tries to increase its country’s birth rate. Schools and poor regions will also receive money. Domestic companies like DetskyMir – a children’s store, and food retailers X5 Retail and Magnit, should benefit from higher store traffic.

- Tensions between Turkey and Russia over Syria have intensified. This is sparked over growing conflict and a fight for power over the buffer zone in Northern Syria. The president of Turkey asked the Syrian army that receives support from Russia to back out of the area. Turkey and Russia have invested quite a bit of effort in the economic and political relationship over the past three years following the downing of the Russian fighter jet back in 2015. It is difficult to imagine that both countries will be willing to destroy the relationship over the Idlib problem, according to Afacan Funda from BGC Partners. Weakness in stocks trading on the Istanbul exchange may present good buying opportunity, as the economy is seeing signs of recovery.

- Bonds continue to rally in Russia, after the central bank delivered a sixth consecutive interest rate cut earlier in the month. Ten-year yields fell below 6 percent for the first time in a decade this week. Even with 175 basis points of easing in the past year, Russia’s real rates are among the highest in emerging markets. Investors recorded a 34 percent return on local currency bonds last year and the bond rally could continue this year as the central bank signaled more rate cuts.

Threats

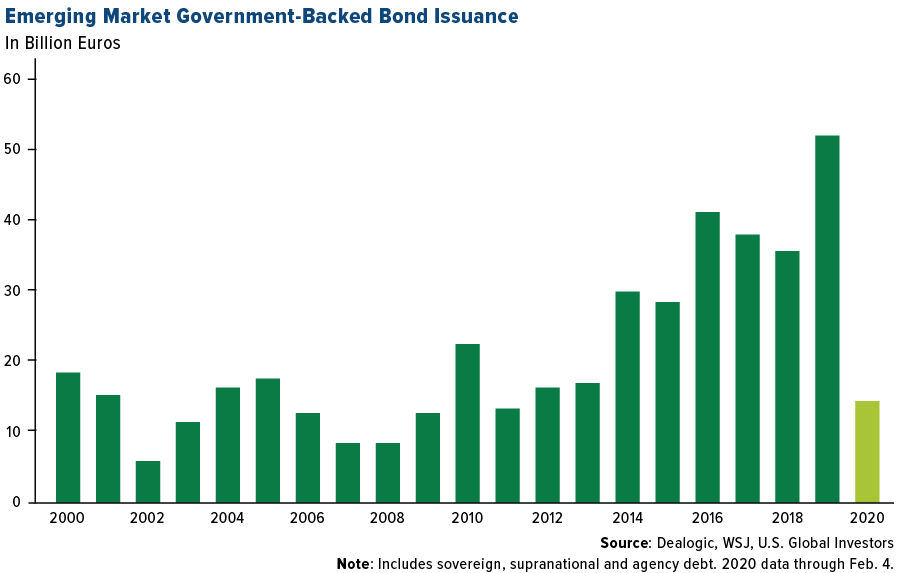

- A surge in euro-based borrowing abroad is weighting the euro currency down, according to a Wall Street Journal article titled “Foreign Borrowing Weakens Euro”. Carry traders are taking advantage of super low rates in euro-area, borrowing in euros and exchanging them for other currencies that are yielding higher rates. Last year, emerging market countries sold a record 52 billion euros of government backed sovereign, supranational and agency debt surpassing the prior record of 41 billion euros from 2016.This year we may see a new record high of bond sells in euros.

- Russia may have to pay a $50 billion arbitration ruling after a Dutch court ruled in favor of the former owners of Yukos Oil Company. Back in 2003 the founder of Yokos, and the richest man in Russia at that time, was sent to prison on charges of tax evasion. Rosneft, Russia’s state owned oil giant, took over most of Yuko’s assets and operates in 25 countries around the world.

- Tesla is allowed to continue building its first assembly plant in Europe, located in a small town of Gruenheide in Germany. The factory could produce as many as 500,000 cars a year and employ 12,000 people. Tesla wants the plant up and running by the middle of next year, challenging European car producers.

China Region

Strengths

- Despite ongoing concerns about coronavirus, China’s Shanghai Composite jumped 4.21 percent on the week, the strongest performer in the region. The Philippines and Indonesia also finished positive, by 1.21 percent and 0.26 percent, respectively, for the week.

- Materials rose 1.51 percent for the week, making it the top-performing sector in the HSCI.

- One strength to note is that as of Friday’s reports, while cases of coronavirus were still climbing elsewhere, Singapore reported more people leaving hospitals than new confirmed cases, marking what could be, one hopes, a turning point. Three new cases were confirmed but five people discharged.

Weaknesses

- South KOSPI backpedaled this week as confirmed coronavirus cases jumped and markets pulled back. The KOSPI was down 3.60 percent for the week.

- Properties & construction was the worst performing sector in the HSCI for the week, declining by 3.17 percent.

- In what is hardly a surprise, car sales for the first half of February this year are reportedly down 92 percent, according to Bloomberg News.

Opportunites

- One continued upside for the city-state of Singapore, following Hong Kong’s protests last year and lingering “2047” concerns for HK, is that law firm Shook Lin & Bok and global valuation and corporate finance advisor Duff & Phelps confirmed—per Bloomberg News—that applications and inquiries from asset managers about opening Singapore offices are on the rise. In addition to natural and growing attraction to Southeast Asia’s rising economic might, the protests of last year in Hong Kong “are a factor that accelerates the decision to open a Singapore office,” one source reported.

- Here’s an idea: while 2019 saw Hong Kong’s tourism and retail sales battered by violent and ongoing protests, and early 2020 has China relatively locked down on coronavirus fears (which of course also extend to Hong Kong by proxy then, and to Macau’s tourism as well), it just may be that retailers and casinos may present timely opportunities at this point or in the near future.

- Tropical Indonesia, which still—at this point—has not reported any confirmed cases of coronavirus, did go ahead and cut interest rates this week as the growth outlook for the region continues to slow. Indonesia’s central bank guidance is now assuming global growth of 3-3.1 percent overall with domestic guidance lowered slightly down to a 5.0-5.4 percent range. But hey, with no reported cases and a supportive central bank for Southeast Asia’s largest economy, perhaps therein lies the opportunity.

Threats

- Coronavirus confirmed case concerns continue. As of Friday, almost 77,000 cases globally are now reported—with, of course, some questions about whether they may be additional cases not yet reported or identified—and some 2,250 deaths, the large majority of which remain in China and especially in Hubei province. Some new cases not apparently linked directly to known China travel are also of concern, says the World Health Organization.

- Thailand’s fourth quarter year-over-year GDP print missed estimates, coming in at only 1.6 percent, down from a prior 2.4 percent and shy of a consensus for 1.9 percent. Thus there is obviously one “threat” to consider specific here to Thailand, of course, but and the greater regional “threat” of a slowdown (and indeed, even a global dent in growth by extension) from coronavirus—but there is also a threat in whether and how and to what extent central banks also act to support their respective governments in timely fashion in the face of uncertainty, which highlights a different, derivative sort of threat to consider for the region.

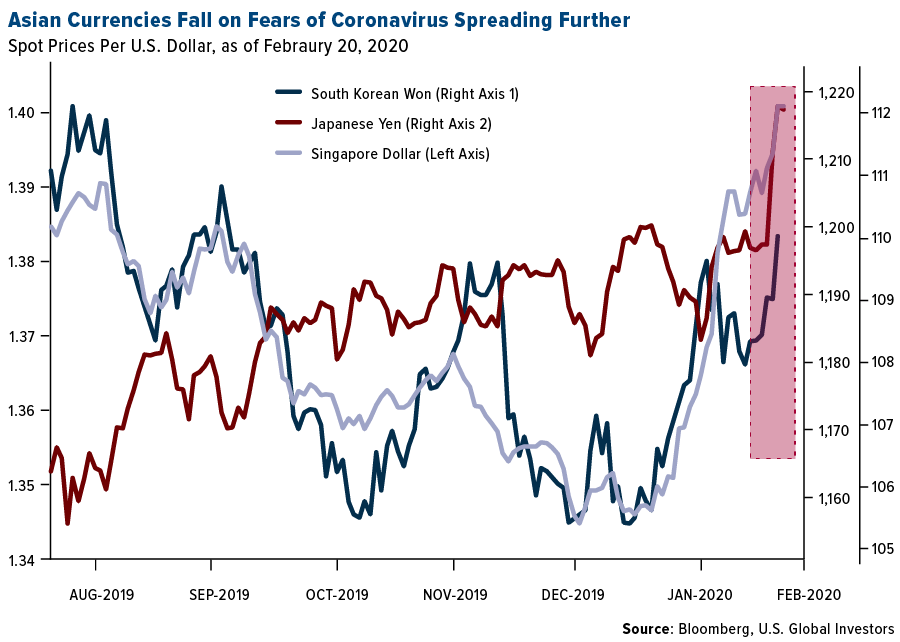

- Perhaps at least somewhat relatedly, that U.S. dollar hasn’t stopped its recent and relatively safe-haven tear to the upside, with the DXY putting in more 52 week highs—almost hitting 100—before pulling back a bit on Friday from its Thursday highs. In the meantime, a number of Asian currencies declined as fears of spreading economic effects from the coronavirus continue.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 21 was Insolar, up 442.70 percent.

- San Francisco-based Coinbase has officially been made a Visa principal member, reports CoinDesk. On its blog Wednesday, the firm said the news marks it as the “first pure-play crypto company” to be approved by the credit card giant.

- Celebrated TV host Max Keiser told host Alex Jones on Infowars that his first prediction of bitcoin reaching $100,000 was now too conservative, reports CoinTelegraph. Keiser has now raised his price target for the first time since 2012, calling for the popular digital currency to hit $400,000. Unfazed by short-term volatility, he said the largest cryptocurrency was “equally as attractive” at current levels as it was at the time of his original forecast.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 21 was CyberMusic, down 97.65 percent.

- On Wednesday, bitcoin took its biggest daily fall in three months, reports CoinDesk, potentially trapping the bulls on the wrong side of the market. Despite the $800 drop, however, the cryptocurrency’s broader trend remains bullish, with prices holding above the higher low of $9,075 (as of Thursday).

- In order to focus more on bitcoin mining ahead of the halving later this year, Riot Blockchain, a Nasdaq-listed crypto firm, plans to sell its exchange, reports CoinTelegraph. In an official announcement from February 20, Riot explains that it has “opted to sunset further development of Riot’s U.S.-based digital currency exchange” in order to focus on crypto mining as part of its updated strategic priorities for 2020.

Opportunities

- Presidential candidate Michael Bloomberg, in a newly published financial reform plan, proposed creating a regulatory framework for cryptocurrencies, reports CoinDesk. “Cryptocurrencies have become an asset class worth hundreds of billions of dollars, yet regulatory oversight remains fragmented and undeveloped,” the proposal said. “For all the promise of the blockchain, bitcoin and initial coin offerings, there’s also plenty of hype, fraud and criminal activity.”

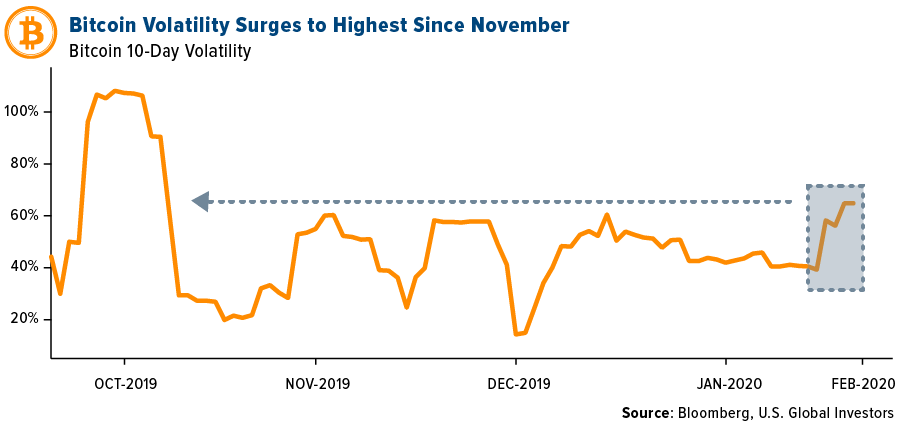

- Bitcoin volatility is back to levels not seen since early November, writes Bloomberg, with the bulls and bears sparring at the $10,000 price level. “It could be a technical move with highly leveraged derivatives positions getting called,” said Emmanuel Goh, who runs crypto-derivatives tracker Skew. The digital currency plunged mid-week, but recovered somewhat after that – trading at $9,537 on Thursday morning.

- Sweden has begun testing an e-krona, writes CoinTelegraph, bringing the country that much closer to the proper release of a central bank digital currency (CBDC). The pilot program will be in operation for one year, until February 2021. The idea is that this blockchain-powered currency would drive conventional payments and banking activities throughout the country, the article explains. Everyday transactions can move to the blockchain rather than swiping a credit card or spending fiat currency.

Threats

- A Chinese crypto exchange known as Fcoin revealed in a post that it will be closing down, reports CoinTelegraph, with founder Zhang Jian stating that it may not be able to pay the $125 million that it owes to users. The exchange claims that the shutdown is not due to a hack or exit scam, but rather due to “internal data errors” and decisions that are too complicated to explain. Binance’s CEO Changpeng Zhao has called Fcoin a Ponzi scheme since 2018.

- The Central Bank of Brazil has announced a plan to launch a new near-instant payment system during November, reports CoinTelegraph, called the Brazilian Instant Payment Scheme (PIX). According to BCB President Roberto Campos, the platform is intended to compete against distributed ledger-based payment systems – facilitating peer-to-peer and business-to-business transactions in 10 seconds or less. “If we think about what has happened in terms of the creation of bitcoin, cryptocurrencies and other encrypted assets, it comes from the need to have an instrument with such characteristics,” Campos said at a launch event in Sao Paulo.

- According to a well-known trader of both cryptocurrency and traditional assets Peter Brandt, the price of XRP may face a 25 percent drop if the recent high breaks down. Brandt warned that a bearish price feature was yet to complete its impact on the market, writes CoinTelegraph, and in a tweet on February 20th Brandt said that a “head and shoulders” pattern in XRP/USD this month had the potential to send prices lower.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.47 | -0.12 | -7.37% |

| Oil Futures | 53.34 | +1.29 | +2.48% |

| Hang Seng Composite Index | 3,765.39 | -51.95 | -1.36% |

| S&P Basic Materials | 378.91 | -1.12 | -0.29% |

| Korean KOSPI Index | 2,162.84 | -80.75 | -3.60% |

| S&P Energy | 405.93 | -3.89 | -0.95% |

| Nasdaq | 9,576.59 | -154.59 | -1.59% |

| DJIA | 28,992.41 | -405.67 | -1.38% |

| Russell 2000 | 1,678.74 | -8.84 | -0.52% |

| S&P 500 | 3,336.12 | -44.04 | -1.30% |

| Gold Futures | 1,645.60 | +59.20 | +3.73% |

| XAU | 111.06 | +9.05 | +8.87% |

| S&P/TSX VENTURE COMP IDX | 581.57 | +11.08 | +1.94% |

| S&P/TSX Global Gold Index | 283.06 | +22.76 | +8.74% |

| Natural Gas Futures | 1.91 | +0.07 | +3.76% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,162.84 | -104.41 | -4.61% |

| 10-Yr Treasury Bond | 1.47 | -0.30 | -16.95% |

| Gold Futures | 1,645.60 | +82.70 | +5.29% |

| S&P Basic Materials | 378.91 | +0.51 | +0.13% |

| S&P 500 | 3,336.12 | +14.37 | +0.43% |

| DJIA | 28,992.41 | -193.86 | -0.66% |

| Nasdaq | 9,576.59 | +192.82 | +2.05% |

| Oil Futures | 53.34 | -3.40 | -5.99% |

| Hang Seng Composite Index | 3,765.39 | -122.46 | -3.15% |

| S&P/TSX Global Gold Index | 283.06 | +22.78 | +8.75% |

| XAU | 111.06 | +7.91 | +7.67% |

| Russell 2000 | 1,678.74 | -5.72 | -0.34% |

| S&P Energy | 405.93 | -30.46 | -6.98% |

| S&P/TSX VENTURE COMP IDX | 581.57 | -3.79 | -0.65% |

| Natural Gas Futures | 1.91 | +0.00 | +0.05% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 111.06 | +17.22 | +18.35% |

| S&P/TSX Global Gold Index | 283.06 | +40.86 | +16.87% |

| Gold Futures | 1,645.60 | +169.50 | +11.48% |

| DJIA | 28,992.41 | +1,226.12 | +4.42% |

| S&P 500 | 3,336.12 | +232.58 | +7.49% |

| Nasdaq | 9,576.59 | +1,070.38 | +12.58% |

| Korean KOSPI Index | 2,162.84 | +66.24 | +3.16% |

| Natural Gas Futures | 1.91 | -0.66 | -25.75% |

| S&P Basic Materials | 378.91 | +7.55 | +2.03% |

| Russell 2000 | 1,678.74 | +94.78 | +5.98% |

| Oil Futures | 53.34 | -5.24 | -8.95% |

| Hang Seng Composite Index | 3,765.39 | +176.95 | +4.93% |

| S&P/TSX VENTURE COMP IDX | 581.57 | +52.54 | +9.93% |

| S&P Energy | 405.93 | -33.75 | -7.68% |

| 10-Yr Treasury Bond | 1.47 | -0.30 | -17.14% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

OTP Bank Nyrt

National Bank of Greece SA

Eurobank Ergasias SA

Rosneft Oil Co.

DetskyMir PJSC

X5 Retail Group

Magnitogorsk Iron & Steel Work

Kirkland Lake Gold Ltd

Newmont Corp

OceanaGold Corp

Anglo American Plc

Yamana Gold Inc

Franco-Nevada Corp

Wheaton Precious Metals Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MVIS Global Junior Gold Miners Index provides exposure to the micro- and small-cap segment of the gold and silver mining sector. Components are considered gold/silver miners when they have the majority of their revenues or reserves in these precious metals. The index is market cap weighted, with holdings capped at a maximum of 8%. The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies. The Index goes up when the U.S. dollar gains "strength" when compared to other currencies. The S&P 500 Utilities comprises those companies included in the S&P 500 that are classified as members of the GICS utilities sector. The Philadelphia Federal Index (or Philly Fed Survey) is a regional federal-reserve-bank index measuring changes in business growth. It is also known as the "Business Outlook Survey." The Empire State Manufacturing Index (ESMI) is a survey given out by the Federal Reserve Bank of New York to manufacturing companies within the state of New York. It measures how the people who run these companies feel towards the economy.