It’s Time We Talked About Modern Monetary Theory (MMT)

Date Posted: June 28, 2019

Read time: 56 min

Fans of the improvisational comedy program Whose Line Is It Anyway? may recall host Drew Carey describing it as "the show where everything's made up and the points don't matter."

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Fans of the improvisational comedy program Whose Line Is It Anyway? may recall host Drew Carey describing it as “the show where everything’s made up and the points don’t matter.”

Interestingly, if we replace “show” with “economic doctrine,” and “points” with “money,” we end up with a near-accurate description of modern monetary theory (MMT).

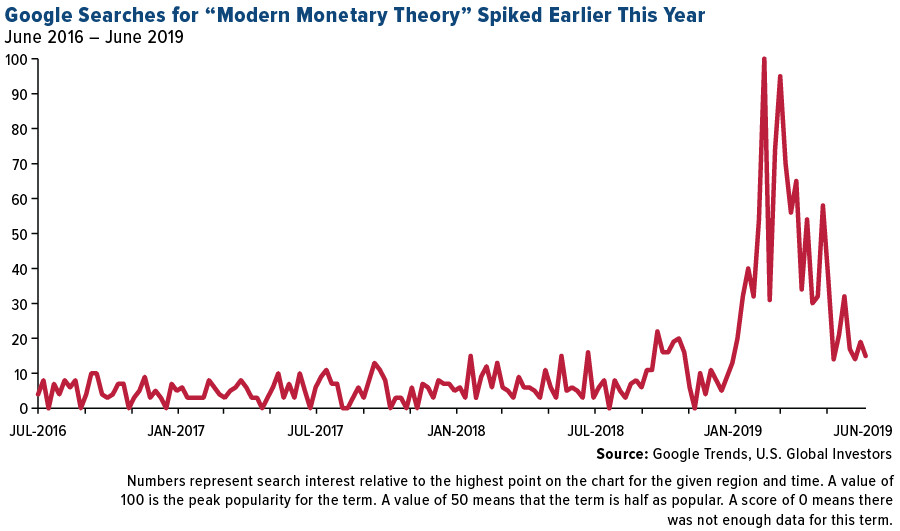

You may have noticed MMT trending in the news in the past few months, thanks in large part to the fact that it’s supported by a number of far-left socialist politicians such as Bernie Sanders and Alexandria Ocasio-Cortez (AOC).

I’m bringing it up now because the first round of Democratic presidential debates were held this week, and if you happened to tune in, you were likely treated to some policy proposals that seem to fall into the MMT camp, even if the term was never uttered. Think “Medicare for all,” free college tuition and the wholesale cancellation of $1.6 trillion in student loan debt. Then there’s the Green New Deal, which AOC recently admitted could cost upwards of $10 trillion.

How would these and other huge federal programs ever be paid for? As I see it, there are two main ways. The first is to raise everyone’s taxes and create whole new ones out of thin air—a “wealth tax,” for instance. The problem is that this method is politically unpopular, as you know.

The second way is much more appealing, to some: Simply print as much money as the program calls for, and then spend it.

That’s the basic idea behind MMT. Remember, everything’s made up, and the money doesn’t matter.

Unlimited Money Printing = Volatile Inflation

You see, advocates of MMT insist that because fiat currency is ultimately a creation of the state, governments can and should print as much of it as needed to fund massive public works, guarantee government jobs for the unemployed and much more. And since a government can never run out of money, the theory says, it can never default on its debts. Deficits are meaningless.

Anyone who’s studied macroeconomics knows that unfettered money printing on this scale is a recipe for runaway hyperinflation. Look at Weimar Germany in the 1920s, or Zimbabwe a decade ago. Today, Venezuela is facing a head-spinning inflation rate of 10 million percent, according to the International Monetary Fund (IMF).

Could such inflation happen in the U.S.?

“If MMT becomes policy, then we can expect a similar bout of high and volatile inflation leading to negative real returns for bonds and cash,” writes Chris Brightman, head of research and investment management at Research Affiliates.

But, as Brightman explains in a paper titled “Dismiss MMT at Your Peril,” the hyperinflation may be by design in order to “level the playing field”:

Unexpected inflation shocks cause the prices of stocks and bonds to plummet. Proponents of MMT may interpret destruction of financial wealth as necessary and beneficial because few of the bottom 160 million [Americans] hold stocks or bonds. A burst of inflation will help level the playing field.

If hyperinflation destroys stocks and bonds, not to mention cash, what can investors do to protect their wealth?

“Real assets provide a measure of inflation protection,” Brightman says. “TIPS [Treasury Inflation-Protected Securities], commodities and REITS [real estate investment trusts] may appreciate as and when investors attempt to reposition for an inflationary regime.”

This is one of the reasons why I always recommend a 10 percent weighting in gold—to hedge against government policy. That includes 5 percent in gold bullion and jewelry, and 5 percent in high-quality, well-managed gold stocks and funds.

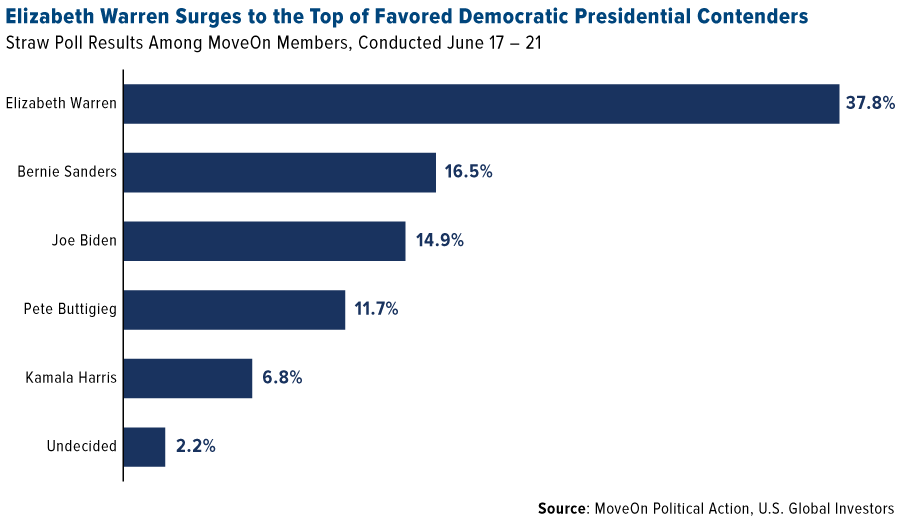

You may question whether MMT could become policy here in the U.S., as it would fundamentally rewrite the rules of how capitalism and free markets operate. I question it as well, but there’s no denying the groundswell of interest and support. It was recently reported that a new 600-page, $70 textbook on MMT, Macroeconomics, sold out of its initial printing. And a MoveOn straw poll of progressive voters this week showed that far-left candidate Elizabeth Warren was highly favored to win the Democratic nomination, with a 21-point lead over Sanders.

Fed Factory Gauges Drop

There are other reasons to make sure you have exposure to gold, of course. This week, all five regional Federal Reserve manufacturing indexes declined in June, the first time in six months that we saw a simultaneous drop, according to Bloomberg. This weakness is yet the latest sign that global economic deceleration and trade tensions are impacting manufacturing.

Among those who see trouble ahead is billionaire hedge fund manager Paul Singer. His firm, Elliott Management, which manages some $34 billion, has one of the most impressive long-term track records, generating a compound annual growth rate (CAGR) of 13.5 percent since its inception in 1977, with only two down years.

This week at the Aspen Ideas Festival, Singer said that he believed the global economy is likely heading toward a “significant market downturn,” perhaps as much as 30 percent to 40 percent.

“The global financial system is very much toward the risky end of the spectrum,” Singer commented, adding that global debt and derivatives are at an all-time high.

Instead of singling out the U.S.-China trade war as the catalyst for this potential slowdown, he criticized global monetary policy that currently favors lower interest rates and has created an imbalance with fiscal policy.

What banks should have done, Singer suggested, “and what they should do now, is try to restore the soundness of money. They should not be cutting rates right now. They should be calling on the congresses and parliaments around the developed world to take steps to deal with the economic slowdown in growth.”

All of this is up in the air, of course. President Donald Trump and Chinese President Xi Jinping are scheduled to meet this weekend at the G20 meeting in Osaka, Japan. Meanwhile, Trump has ratcheted up his attacks on Federal Reserve Chairman Jerome Powell for not easing fast enough. On Wednesday, the president told FOX Business that the U.S. “should have Draghi instead of our Fed person,” referring to Mario Draghi, president of the European Central Bank (ECB), who recently hinting that a new round of quantitative easing (QE) could be in the works.

But back to Paul Singer. I’ve seen him speak before, and he’s discussed at length that he likes gold for its diversification benefits. This is in line with fellow billionaire hedge fund manager Paul Tudor Jones, who recently said that gold is his favorite trade in the next 12 to 24 months.

Looking for someone to make sense of the markets? Subscribe to Frank Holmes’ award-winning Frank Talk CEO blog! Click here to sign up!

Gold Market

This week spot gold closed at $1,399.60 up $11.24 per ounce, or 0.80 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.83 percent. The S&P/TSX Venture Index came in slightly down 1.43 percent. The U.S. Trade-Weighted Dollar fell 0.04 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-25 | Hong Kong Exports YoY | -4.5% | -2.4% | -2.6% |

| Jun-25 | New Home Sales | 684k | 626k | 679k |

| Jun-25 | Conf. Board Consumer Confidence | 131.0 | 121.5 | 131.3 |

| Jun-26 | Durable Goods Orders | -0.3% | -1.3% | -2.1% |

| Jun-27 | Germany CPI YoY | 1.4% | 1.6% | 1.4% |

| Jun-27 | Initial Jobless Claims | 220k | 227k | 217k |

| Jun-28 | Eurozone CPI Core YoY | 1.0% | 1.1% | 0.8% |

| Jun-30 | Caxin China PMI Mfg | 50.1 | — | 50.2 |

| Jul-1 | ISM Manufacturing | 51.0 | — | 52.1 |

| Jul-3 | ADP Employment Change | 140k | — | 27k |

| Jul-3 | Initial Jobless Claims | 220k | — | 227k |

| Jul-3 | Durable Goods Orders | — | — | -1.3% |

| Jul-5 | Change in Nonfarm Payrolls | 163k | — | 75k |

Strengths

- The best performing metal for the week was platinum, which gained 3.02 percent. Both platinum and palladium seem to be playing catch up to gold’s strong move last week. Gold extended its rally this week, pushing past $1,400 an ounce and fueling investors to pour cash into funds backed by the yellow metal. As Bloomberg reports, gold is set for its best month since the Brexit vote and comes ahead of the highly anticipated G20 meeting. Exchange-traded funds added 70,951 ounces of gold to their holdings in the last trading session, bringing this year’s purchases to 2.96 million ounces.

- On the prior Friday, investors added a net $1.57 billion to State Street’s gold shares ETF, reports Bloomberg, increasing the fund’s assets by 4.6 percent to $35.9 billion and riding the new week with further gains. This was the biggest one-day increase in at least a year. Central banks are also gobbling up gold – with holdings worth $22.8 billion as of June 21, according to weekly figures.

- Gold’s rise to a six-year high might be reflective of its status as a “positive yielding asset,” writes Bloomberg, particularly in relation to much of the world’s debt yielding less than zero. In fact, below-zero debt now makes up almost 40 percent of the value of all government bonds outstanding –a very profound shift. “As long as the capital gain is good enough, it doesn’t matter if the yields are underwater”…when seen in this light, Bloomberg explains, there’s a more straightforward choice between gold and sovereign debt. As Ambrose Evans-Pritchard writes, “The old refrain that gold is dead money because it pays no yield has lost its sting.”

Weaknesses

- The worst performing metal the week was silver, which fell 0.19 percent, coming down slightly on expectations of reduced economic activity. In a weekly Bloomberg survey, gold traders and analysts turned bearish amid concerns that the metal is due for a correction after rallying to a six-year high. The yellow metal hit the pause button as comments from the Federal Reserve dampened expectations over the scale of interest rate cuts. According to Bloomberg, Indian brides probably won’t wear quite as much this year. Record high prices and low rainfall are to blame for the slack in demand.

- U.S. jobless claims increased by more than expected, reports Bloomberg, reaching the highest level in seven weeks. Jobless claims rose by 10,000 to 227,000 in the week ended June 22, announced the Labor Department. Despite the national increase, jobless claims remain near historically low levels.

- U.S. new home sales fell in the month of May, reports Bloomberg, dropping by 7.8 percent to a 626,000 annual rate. In the month of April, home-price gains in 20 U.S. cities decelerated for a thirteenth straight month. This is the weakest pace since 2012, indicating further moderation in the housing market, the article continues.

Opportunities

- Federal Reserve Chairman Jerome Powell said that the downside risks to the U.S. economy have increased recently, reports Bloomberg, which reinforces the case among policy makers for somewhat lower interest rates. In another opportunity in the gold space, the drawdown in Comex gold inventories signals a potential shortage of physical supply that adds further weight to the metal’s bull market, writes Bloomberg. “Gold stockpiles tend to move in tandem with prices, but now they are diverging, which signals signs of a gold shortage that may deepen thanks to voracious demand for ETFs that have to be backed by physical bullion,” the article continues.

- At the moment, gold is nothing but a bond alternative, writes Bloomberg. For this reason, the yellow metal has the scope to run toward $1,500. With central banks turning dovish in recent weeks, the amount of negative-yielding bonds pushed to a record $13 trillion. On a 30-week basis, the correlation of this measure with the price of gold rose to 0.7. Why is that? The opportunity cost of owning non-yielding gold falls when bond holders are effectively taxed. Now investors are looking outside their usual refuges as they hunt for stable assets that provide at least a modicum of return, Bloomberg continues. As Bruno Braizinha, BofA’s director of U.S. rates strategy put it, a world starved of yield “implies a tectonic shift in asset allocation,” with greater appetite for emerging-market investments.

- According to a report dated June 24, gold has risen to Morgan Stanley’s top commodity pick on a six-month view. Similarly, RBC Mining and Materials Equity Team says it is taking a more constructive outlook on the yellow metal into the second quarter of 2019 and 2020, raising average price estimates to $1,350 an ounce. Finally, Goldman Sachs Group says that gold doesn’t need fear to prosper. The bank wrote in a report that while a gradual brightening of prospects for the world economy in the second half of 2019 and receding worries of a recession could lead to lower “fear”-driven demand for gold, that will likely be offset by a positive “wealth” effect.

Threats

- Even as U.S. stocks remain near record highs, a growing cohort of investors say they are ready to throw in the towel, reports Bloomberg. According to the latest reading from the Conference Board’s sentiment indicator, the number of Americans expecting equities to decline over the next year jumped the most since 2007 and for the first time since January exceeds those who expect gains. In addition, consumer confidence dropped in the month of June, well below the range of consensus forecasts, reports Bloomberg. Confidence dropped 10 points to 121.5, raising a potential red flag regarding households’ willingness to drive growth beyond trend over the next several months.

- Merrill Lynch’s commodities unit and Morgan Stanley were sued by a group of traders claiming the companies used a tactic known as spoofing to manipulate the market for precious metals futures, writes Bloomberg. The suit was filed a day after Merrill agreed to pay $36.5 million to settle claims by U.S. officials that its commodities division manipulated the price of precious metals futures over a six-year period. The 2010 Dodd-Frank Act made it illegal to place orders with no intention of executing them and since the laws were passed, the government has prosecuted almost a dozen criminal cases, and the CFTC initiated 15 civil complaints in 2018. That is up from nine in 2017, and before then, the regulator averaged about one a year.

- BNP Paribas sees the period at end of 2019 and into 2020 as more favorable for average higher gold prices, writes Bloomberg, but the bank is cautious about further upside potential from current levels in the short term. The gold market has currently been fueled by markets pricing in an interest rate cut as soon as next month, but any hint that this may not happen, could lead to a sharp pullback for prices already at the highest in six years. In a related note, Bloomberg points out that gold and real yields have never been as tightly bound as they are now, which likely means the metal’s rally has squeezed as much as it can from the bond market, which has priced in a fair amount of rate cuts. For gold to climb further, the article explains, it will need help from the dollar.

Index Summary

- The major market indices finished mostly down this week. The Dow Jones Industrial Average lost 0.45 percent. The S&P 500 Stock Index fell 0.54 percent, while the Nasdaq Composite fell 0.32 percent. The Russell 2000 small capitalization index gained 1.11 percent this week.

- The Hang Seng Composite gained 0.34 percent this week; while Taiwan was down 0.68 percent and the KOSPI rose 0.24 percent.

- The 10-year Treasury bond yield fell 5 basis points to 2.00 percent.

Domestic Equity Market

Strengths

- Materials was the best performing sector of the week, increasing 1.47 percent versus an overall decrease of 0.54 percent for the S&P 500.

- Allergan was the best performing stock for the week, increasing 27.99 percent.

- Global M&A volume reached $842 billion in the second quarter, reports Reuters. This quarter’s volume would have been significantly lower were it not for U.S. mega deals. Mergers between AbbVie and Allergan, Raytheon and United Technologies, as well as Occidental and Anadarko meant the U.S. accounted for more than half of global M&A volumes.

Weaknesses

- Real estate was the worst performing sector for the week, decreasing by 2.73 percent versus an overall decrease of 0.54 percent for the S&P 500.

- Bristol-Myers Squibb was the worst performing stock for the week, falling 8.09 percent.

- Glencore’s mining disaster is getting worse, reports Business Insider, as the number of artisanal miners killed rose to 43 on Friday. A landslide at a copper and cobalt mine run by Glencore led to the deaths, and the search for missing workers continues, according to local officials.

Opportunities

- Shares of Western Digital climbed 7.9 percent on Wednesday after Craig-Hallum upgraded the data storage device company’s stock to buy from hold with a price target of $54, writes TheStreet. The upgrade followed Micron Technology’s "positive commentary and announced steps targeting supply growth discipline," writes analyst Christian Schwab in a note to investors.

- Velodyne Lidar, which sells technology for autonomous vehicles, has hired bankers for an initial public offering (IPO), according to people familiar with the process. The company, which makes a laser technology that helps self-driving cars detect the objects around them, is working with Bank of America Merrill Lynch, Citigroup, Royal Bank of Canada and William Blair for a potential public float, Business Insider reports.

- Amazon continues to add options for its customers to receive their packages, reports CNBC, and on Thursday the company added another alternative for U.S. customers. The new option is called Counter and will allow customers to pick up packages at pharmacy Rite Aid.

Threats

- Boeing 737 Max pilots are suing, reports MSN, with over 400 joining the class-action lawsuit. The lawsuit accuses the aviation giant of “unprecedented cover-up” of the “known design flaws.”

- Intel reportedly plans to slash chip prices, and analysts say the move makes sense at a time when the tech giant is falling behind its competitor AMD, writes Business Insider. Analysts say Intel has lost its manufacturing technology edge which rivals like AMD have historically struggled to match.

- California’s governor warned Facebook, YouTube and other social media giants that government regulation is coming. Governor Gavin Newsom cautioned the tech industry of impending federal regulation in a recent interview with Axios. Additionally, a U.S. Senator asked the Federal Trade Commission (FTC) to "take all necessary steps" to ensure YouTube is held accountable for violating children privacy laws.” YouTube is reportedly under investigation by the FTC for its handling of children’s videos and could face fines for breaking children’s privacy laws.

The Economy and Bond Market

Strengths

- Orders with U.S. factories for business equipment rebounded in May with the largest increase in four months, signaling corporate investment is holding up despite tensions with major trading partners fueling uncertainty about the outlook. A proxy for business investment, non-military capital goods orders excluding aircraft rose 0.4 percent after a 1 percent decline in the prior month, according to Commerce Department figures Wednesday that exceeded estimates.

- The core personal consumption expenditures price gauge, which excludes food and energy, rose 0.2 percent from the prior month and 1.6 percent from a year earlier, according to a Commerce Department report Friday. The annual gain was just above the median estimate in a Bloomberg survey, and the three-month annualized increase advanced to about 2 percent, a five-month high. Purchases, which make up the majority of the economy, rose 0.4 percent from April, slightly below estimates, following an upwardly revised 0.6 percent gain in April.

- Personal income increased 0.5 percent for a second month, topping forecasts, though wages and salaries climbed at the slowest pace in six months. Stronger consumer spending and higher incomes should support future growth as the expansion becomes the longest in U.S. history in July.

Weaknesses

- U.S. consumer confidence fell in June to the lowest level since September 2017 as Americans became less upbeat about the economy and labor market amid trade tensions with China and Mexico. The Conference Board’s index declined to 121.5, lower than all forecasts in a Bloomberg survey, data showed Tuesday. The median projection called for a reading of 131. A gauge of the present situation decreased to a one-year low of 162.6, while the measure of expectations fell to 94.1. A separate gauge showed the share of those who said jobs were hard to get climbed to 16.4 percent, the highest since November 2017.

- Filings for U.S. unemployment benefits increased by more than expected to a seven-week high, a possible sign of strains in the labor market that could factor in to the Federal Reserve’s debate over whether to cut interest rates next month. Jobless claims rose by 10,000 to 227,000 in the week ended June 22, according to Labor Department figures released Thursday that exceeded all estimates in Bloomberg’s survey of economists. The four-week average, a less-volatile measure, increased to 221,250, the highest in more than a month.

- Sales of new U.S. homes fell to a five-month low in May, adding to signs of weakness in the sector despite lower mortgage rates. Single-family home sales dropped 7.8 percent to a 626,000 annualized pace that missed all estimates in Bloomberg’s survey of economists, government data showed Tuesday. The median sales price decreased 2.7 percent from a year earlier to $308,000.

Opportunities

- The official employment data will be out next Friday. Forecasts point to a solid report, with nonfarm payrolls expected at 165k, the unemployment rate steady at 3.6 percent, and a slight acceleration in average hourly earnings.

- The U.S. non-manufacturing survey will come out next Wednesday. The service sector has held up better than manufacturing this year and investors hope to see this trend continue.

- The early part of next week will be dominated by the events that will unfold over the weekend, namely the outcome of G20 meetings and trade talks between the U.S. and Chinese presidents. Ahead of the talks, Trump has already indicated that a trade deal with China was possible this weekend. However, Trump also warned that he’s prepared to impose tariffs on most remaining Chinese imports if they don’t agree. So, it looks like the outcome of the meetings will likely be a binary one. If they make progress, then a delay in raising tariffs or cancelling some of the previously announced-levies are likely, and talks could resume between the two nations in July. However, if trade talks falter, it will be plan B: more tariffs on Chinese goods.

Threats

- A third Federal Reserve regional bank factory survey weakened in June, adding to signs of waning momentum in manufacturing amid heightened trade tension. The Dallas Fed’s gauge of manufacturing in Texas slumped to a three-year low of minus 12.2 as more firms saw conditions worsen, according to a report Monday that also showed further deterioration in the six-month outlook. The main reading was well below the minus 2 median projection following minus 5.3 in May and weaker than all estimates in a Bloomberg survey of economists. The fourth-straight monthly drop is the latest sign President Trump’s trade war with China is weighing on the expansion and follows Fed officials last week downgrading their assessment of the economy while citing greater uncertainty about the outlook.

- Next week kicks off with the ISM manufacturing PMI for June. Investors are bracing for confirmation of the trend in manufacturing data deteriorating.

- Signals of a U.S. recession are being sent by employment-survey data and Treasury yields, according to strategists at Societe Generale SA. The “jobs hard to get” component of the Conference Board’s monthly consumer-confidence survey points that way, they wrote in a report Thursday. The index jumped this month by 4.6 percentage points, the most since February 2009. They also cited a widening of the yield gap between 10-year Treasury notes and 30-year bonds, which set an 11-year low last July.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was coffee, which gained 8.47 percent. Low prices have encouraged renewed investor buying. Oil had another great week as well. Futures rose as much as 3.6 percent on Wednesday and oil jumped to a four-week high after the U.S. Energy Information Administration (EIA) reported that domestic inventories fell by 12.8 million barrels last week, representing the largest decline since September 2016. Hedge funds are backing oil with bets on rising U.S. crude prices jumping 13 percent in the week ended June 18, reports Bloomberg. Tensions between the U.S. and Iran continue to grow, which is positive for the price of oil.

- Clean energy sources supplied more of American’s electricity than coal did in April – the first time ever, according to the EIA. Bloomberg reports that hydroelectric dams, solar panels and wind turbines generated 68.5 million megawatt-hours of power, while coal generated 60 million. This is a clear sign of renewables moving into the mainstream.

- Thanks to sanctions against Venezuela and Iran, U.S. oil has gained a larger foothold in Asian markets, and specifically China, the world’s biggest consumer. According to Bloomberg, American oil exports to China surged nearly 65 percent from April to May, while exports to South Korea were three times as much from the same time a year ago. “It’s the U.S. intention to fill the supply gap of sanctioned supplies from Iran and Venezuela,” commented Guo Chaohui, an analyst at China International Capital. In related news, the U.S. is projected to account for around a quarter of world oil and gas production by the early 2030s as fracking technology improves, according to Rystad Energy and reported by Bloomberg. The combined U.S. output from shale of crude oil, condensate and natural gas liquids could reach as much as 25 million barrels per day.

Weaknesses

- The worst performing major commodity for the week was palm oil, which fell 6.66 percent, a seven-month low, on weaker demand. Iron ore futures in Asia dropped on Monday after Vale SA brought its Brucutu mine back online. This restores almost one third of the capacity that was shut down after the deadly dam disaster in January. Bloomberg reports that iron ore in Singapore fell 2.2 percent, extending a decline from a five-year high.

- On Monday the U.S. Supreme Court turned away an appeal that challenges President Donald Trump’s use of national security to justify the imposition of steel tariffs. A steel industry trade group and two of its members filed an appeal saying that the $4 billion in steel tariffs imposed by the President offers such broad discretion that it violates the Constitution.

- A fire at Clearway Energy’s solar farm in California that burned 1,127 acres earlier this month was started by a bird, according to the state’s fire department. Fires caused by birds are not uncommon at solar facilities, as the animals can either fly into beams or land on the wrong two wires at the same time. In addition, a landslide that killed dozens at Glencore’s mine in the Democratic Republic of Congo has pointed the spotlight on illegal mining. The company estimates that approximately 2,000 “unauthorized people” enter the site every day, Bloomberg reports.

Opportunities

- BMW announced this week that it will aim to increase electric car sales by 30 percent each year until 2025 and to push forward its initial plan to launch 25 new products to 2023 from 2015 originally. Bloomberg reports that the automaker boosted sales of EVs by 23 percent in 2018.

- Frackers are now using natural gas as an alternative to diesel engines due to the oversupply of gas. Some explorers are using “e-fracking”, which uses gas from its own wells to rub turbines for electric motors. Wells Fargo estimates that this practices cuts around $1 million a month in fuel costs and it lessens the excess gas burned off at the well site.

- National Petroleum Construction, an Abu Dhabi-based company that builds for Saudi Aramco, is diversifying into wind power as it is bidding for projects in the North Sea, said the company’s CEO in an interview. Bloomberg reports that Chevron Phillips Chemical Co will be partnering with Qatar Petroleum to build the Middle East’s largest ethylene plant.

Threats

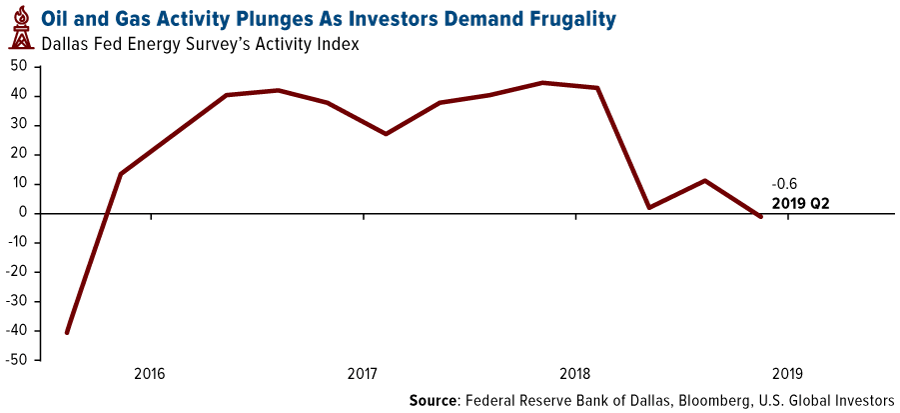

- According to the Federal Reserve Bank of Dallas, activity in the oil and gas industry turned negative in the second quarter for the first time since 2016. The three-year expansion has stalled, driven by drillers and oilfield servicers struggling to lure back investors who are demanding companies be more frugal, writes Bloomberg’s Ryan Collins.

- Fitch Solutions said in a report this week that it is likely China will impose restrictions on rare earth exports to the U.S. unless trade tensions are de-escalated, based on historical precedent. Restrictions on exports would immediately impact the U.S. in the form of higher prices, which will hurt industries consuming the metals.

- The Kariba Dam, which forms the world’s largest reservoir and powers Zambia and Zimbabwe, is cutting output amid a drought that has dwindled power to a third. Bloomberg reports that Zambia’s state-owned power utility has unleashing daily blackouts that leave more than 17 million people without power. This raises concerns globally on how climate change is affecting hydropower’s dependability.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 3.6 percent. Banks continue to outperform, gaining 7.4 percent in the past five days. Improving bank profitability and prospects for further economic recovery in the country attract investors to these low valuation assets.

- The Czech koruna was the best performing currency this week, gaining 72 basis points against the U.S. dollar. Central banks left the main rate unchanged at 2 percent, despite global central banks turning dovish.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 1.1 percent. Protests against Prime Minister Andrej Babis continued over allegations of a conflict of interest and criminal fraud case involving European Union funds. Hundreds of thousands of demonstrators filled the streets of Prague last Sunday calling for his resignation. Babis survived a no confidence vote this week.

- The Russian ruble was the worst relative performing currency this week, losing 25 basis points against the U.S. dollar. The ruble was little changed in the past five days, but it is the best performing currency among its emerging market (EM) peers in the second quarter and year-to-date.

- Utilities was the worst performing sector among eastern European markets this week.

Opportunities

- Renaissance Capital, using its five-factor model, identified the best and worst markets over the next 12 months. In EM, Greece, Colombia, South Africa, Argentina, Mexico and Russia screen the best, while Pakistan, India, Chile and Hungary screen the worst. The group likes Russia for the country’s healthy budget surplus, higher FX reserves, less external borrowing and high dividends. Moreover, RenCap’s research team sees Russia cutting policy rates, while Hungary is expected to have the largest rate hikes within emerging markets.

- The U.S. dollar is probably in a bear market, meaning EM currencies are in for a good ride this year despite a weaker outlook for global growth, according to Morgan Stanley. The world’s biggest central banks are switching to a more dovish stance, fueling demand for riskier assets. Morgan Stanley’s favorite currency in Europe, the Middle East and Africa (EMEA), is the Russian ruble.

- Poland might become a European leader in production of lithium-ion batteries for electric mobility, as per Wood & Company research. These investments include an approximately USD $1 billion lithium-ion separators factory planned by South Korea’s SK Innovation, or LG Chem’s PLN 6 billion battery facility, expected to employ 6,000 workers in 2020.

Threats

- Ford Motor Company will eliminate about 20 percent of its workforce across Europe, with Germany, the U.K. and Russia the hardest hit by the cuts. This could be a sign that European carmakers are under pressure due to ongoing trade tensions and new regulations. Expect further challenges in the region.

- Erdogan lost Istanbul again after the re-run of municipal elections last Sunday. On a positive note, Turkey may not see more elections for the next four years. However, while the Turkish lira finally gained against the dollar and equites moved higher, the geopolitical tensions still exist due to country’s open contract with Russia for the delivery of the defense system. First shipments are scheduled for July, and Turkey is risking new sanctions if it takes the delivery.

- Emerging Europe markets (measured by MSCI Emerging Europe Index) gained almost 20 percent year-to-date, beating Western Europe (measured by STOXX 600 Index) and the Unites States (measured by the S&P 500). Recently, the optimism over world leaders discussing global topics during the NATO and G20 meetings has been pushing equites higher. Will the global markets continue to surge next week once the NATO and G20 meetings conclude?

China Region

Strengths

- The best performing indices in the region for the week were Indonesia’s Jakarta Composite, up 79 basis points, and Thailand’s SET Index, up 77.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index since last Friday was consumer goods, which climbed 1.90 percent over the last five days.

- Vietnam’s GDP growth clocked in at 6.71 percent for the year-over-year second quarter, ahead of expectations, though down slightly from the prior reading of 6.79 percent in the first quarter.

Weaknesses

- The worst-performing indices in the region for the week were the Philippines’ PCOMP Index, down 65 basis points, and Vietnam’s Ho Chi Minh Stock Index, which dropped by 96 basis points.

- The poorest-performing sector in Hong Kong’s Hang Seng Composite Index this week was energy, which declined 0.92 percent.

- South Korea’s factory production dropped 0.2 percent in May, down from April’s revised year-over-year gain of 0.2 percent. Month over month, the change was a 1.7 percent decrease, down from a revised 1.9 percent gain.

Opportunities

- President Donald Trump and Chinese President Xi Jinping will sit down tomorrow at the G20 meeting, and the world will be awaiting the results. At immediate stake is the impending implementation of U.S. tariffs on an additional $300 billion of Chinese goods, and with it, perhaps, any chance of salvaging the ongoing talks for the near team. While the stakes are indeed high, lower-level talks began again earlier in the week. Treasury Secretary Steven Mnuchin reminded us that the U.S. and China were—not too long ago—90 percent of the way to a deal, and Vice Premier Liu He did meet with USTR Robert Lighthizer late in the week as well. But the looming question remains: Will Trump implement the tariffs or delay implementation? And similarly, will a new round of talks subsequently ensue? Will any of this get us any closer to a real “deal” that both sides and the market see as acceptable? It is, of course, hard to say, but consensus at this point is for essentially the same play-call as at the December G20 meeting: start up talks again while punting on the immediate implementation of the tariffs. This may allow everyone to be a short-term winner, although significant issues, already much discussed here, still remain.

- North Korean leader Kim Jong Un received a letter from President Trump containing “interesting” and “excellent content,” the WSJ reports North Korean state media as saying, requiring Kim Jong Un’s “serious contemplation.” This comes, of course, on the heels of President Xi’s recent state visit to North Korea, precedes the G20 meeting this weekend, and follows President Xi’s recent diplomatic commitment to the North Korean situation and his encouragement of further North Korean talks with the U.S., so whatever the case with respect to strategic ongoing differences in the nuclear situation, the U.S. and North Korea could be gearing up for another summit or round of talks.

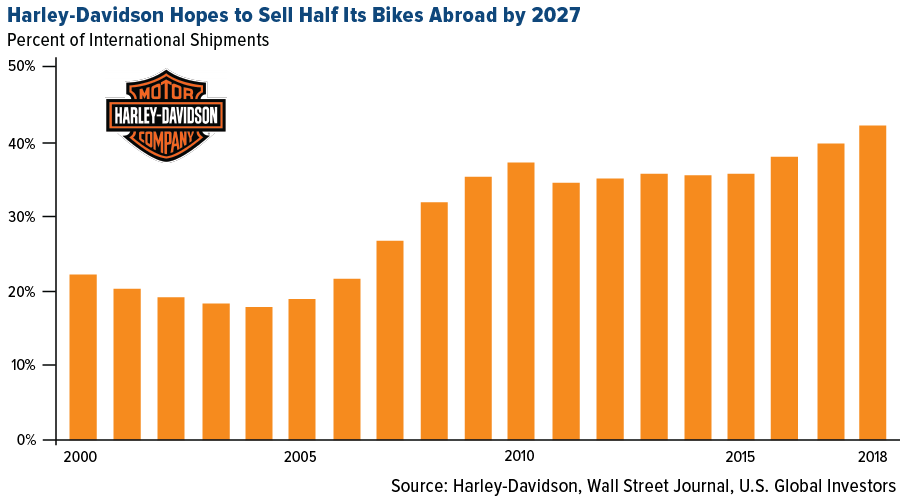

- Iconic American motorcycle brand Harley-Davidson is teaming up with a Chinese manufacturer called Qianjiang Motorcyle to produce a 338 CC bike, the smallest the American company has made in decades, for its fastest-growing market, according to a recent Wall Street Journal story. Harley has stated that it intends to keep all motorcycles sold in the U.S. produced in the United States, but also aims to sell half its bikes abroad by 2027, and this new model, slated to make its debut by the end of 2020, is part of that aim. Qianjiang Motorcycle is majority owned by Chinese auto company Geely, the owner of Volvo (as well as Lotus, Proton and the London Taxi Co./LEVC, to name some others); Geely also holds a significant stake in Daimler. HOG goes to China in the Year of the Pig. That’s got to be worth something, right?

Threats

- The threat of U.S.-China trade war escalation must remain a threat until resolved with more certainty. The stakes remain high this weekend. Even a “can-kicking” will be only just that, and while discussions between the two economic juggernauts are good, some of the core disagreements and concerns may well remain even amid a new truce, which could in turn leave a degree of uncertainty and risk markets will have to work through.

- With more possible uncertainty in markets—though also perhaps some leeway on the monetary policy side—we could see scrutiny of central banking policy step up as risks of policy missteps may increase.

- Bloomberg reported this week that about 56 percent of Chinese consumers are avoiding U.S. products to show support for China, citing a survey by Brunswick.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 28 was XMax, up 686.52 percent.

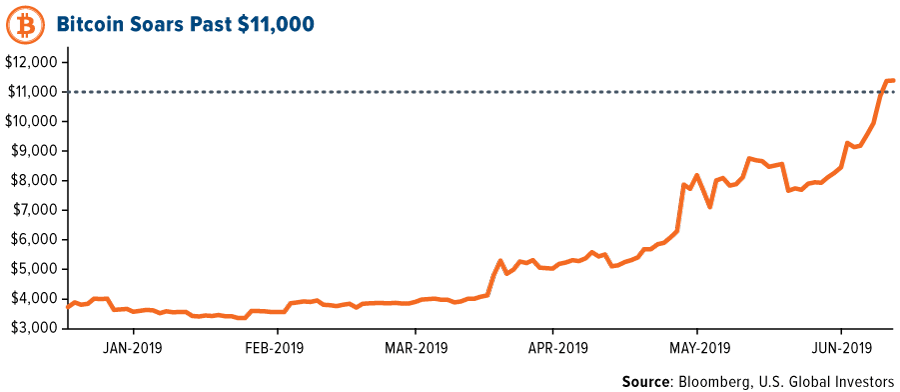

- Bitcoin set a new price high for 2019, reaching as high as $11,304 in early trading on Monday (and going as high as $13,700 mid-week), reports CoinDesk, before conceding a short-term period of profit taking. According to the article, this year’s bull run for the cryptocurrency is likely a combination of traders buying into their own fear-of-missing-out (FOMO) as well as institutions chasing the tail end announcement of Facebook’s project Libra.

- Bitcoin’s surge is benefitting more than the cryptocurrency itself, writes Bloomberg. It is also sending crypto-linked stocks higher. Stocks with exposure to bitcoin, such as Grayscale Bitcoin Trust, Riot Blockchain and DPW Holdings, are rallying in pre-market trading after the digital asset rose above $11,000 for the first time in 15 months.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 28 was M20, down 60.20 percent.

- A new cryptocurrency-mining botnet has been exploiting Android Debug Bridge ports, reports CoinDesk, which is a system designed to resolve app defects installed on a majority of Android phones and tablets.Trend Micro reports that the botnet malware has been detected in 21 countries and is most prevalent in South Korea.

- The popular cryptocurrency exchange Coinbase experienced an outage mid-week, reports CoinDesk, with both its website and API rendered temporarily inaccessible. This all while the price of bitcoin fell over $1,700 in the span of about 15 minutes. According to its website, the trading app Robinhood also reported issues with its crypto trading service this week.

Opportunities

- In an interview on Radio One, Malta’s Prime Minister Joseph Muscat announced that every rental contract in Malta would be registered on the blockchain, reports CoinDesk. The initiative ensures security, prevents record tampering and ensures only authorized persons can access the records, said Muscat.

- On Tuesday, the Commodities Futures Trading Commission (CFTC) approved LedgerX’s application for a designated contract market (DCM) license, meaning the company can now offer physically settled bitcoin futures contracts, reports CoinDesk. In physically settled futures the buyer receives the underlying commodity when a contract expires.

- Digital contract management startup Clause has raised $5.5 million in a Series A round, reports CoinDesk, led by crypto merchant bank Galaxy Digital. Clause offers blockchain-based solutions to facilitate the creation, storage and maintenance of digital contracts for businesses. However, as the article explains, it also offers clients these same services independent of blockchain technology – by using existing platforms such as Stripe or PayPal.

Threats

- Australia’s Central Bank Chief Philip Lowe is very skeptical of Facebook’s new cryptocurrency Libra, reports CoinDesk. “There’s a lot of water under the bridge before Facebook’s proposal becomes something we’re using all the time,” Lowe declared during a pess conference. “There are a lot of regulatory issues that need to be addressed and they’ve got to make sure there’s a solid business case.”

- Scammers are targeting Libra fans with fake websites, reports CoinDesk. According to the article, despite the fact Libra isn’t public yet, would-be investors have been caught in supposed Libra pre-sales.One fake website looks like a mirror image of Facebook’s legitimate website calibra.com, with the same marketing materials, wording, fonts, color schemes, etc.

- Six individuals have been arrested for stealing over $27 million in cryptocurrency from thousands of victims, European law enforcement agency Europol said in a press release on Wednesday. As CoinDesk reports, the criminal endeavor involved a “typosquatting” scam in which a “well-known” online crypto exchange was cloned in order to gain access to victims’ crypto wallet login details and steal funds.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 205.10 | +5.69 | +2.85% |

| Gold Futures | 1,344.60 | -1.50 | -0.11% |

| Natural Gas Futures | 2.39 | +0.05 | +2.27% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -9.57 | -1.60% |

| 10-Yr Treasury Bond | 2.09 | +0.00 | +0.10% |

| Nasdaq | 7,796.66 | +54.56 | +0.70% |

| Oil Futures | 52.53 | -1.46 | -2.70% |

| Hang Seng Composite Index | 3,620.02 | +26.25 | +0.73% |

| S&P 500 | 2,887.01 | +13.67 | +0.48% |

| DJIA | 26,089.61 | +105.67 | +0.41% |

| Korean KOSPI Index | 2,095.41 | +23.08 | +1.11% |

| Russell 2000 | 1,522.44 | +8.05 | +0.53% |

| S&P Energy | 447.48 | -2.21 | -0.49% |

| S&P Basic Materials | 360.98 | +1.78 | +0.50% |

| XAU | 75.81 | +1.48 | +1.99% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.21 | -8.11% |

| S&P/TSX Global Gold Index | 205.10 | +22.96 | +12.61% |

| 10-Yr Treasury Bond | 2.09 | -0.29 | -12.17% |

| Oil Futures | 52.53 | -9.49 | -15.30% |

| Gold Futures | 1,344.60 | +40.90 | +3.14% |

| S&P 500 | 2,887.01 | +36.05 | +1.26% |

| S&P Energy | 447.48 | -23.94 | -5.08% |

| Hang Seng Composite Index | 3,620.02 | -150.49 | -3.99% |

| DJIA | 26,089.61 | +441.59 | +1.72% |

| Korean KOSPI Index | 2,095.41 | +2.63 | +0.13% |

| Nasdaq | 7,796.66 | -25.49 | -0.33% |

| S&P Basic Materials | 360.98 | +21.80 | +6.43% |

| Russell 2000 | 1,522.44 | -25.83 | -1.67% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -20.57 | -3.39% |

| XAU | 75.81 | +7.51 | +11.00% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.47 | -16.29% |

| 10-Yr Treasury Bond | 2.09 | -0.55 | -20.75% |

| DJIA | 26,089.61 | +379.67 | +1.48% |

| Oil Futures | 52.53 | -6.08 | -10.37% |

| S&P 500 | 2,887.01 | +78.53 | +2.80% |

| Gold Futures | 1,344.60 | +37.00 | +2.83% |

| S&P Energy | 447.48 | -37.76 | -7.78% |

| Nasdaq | 7,796.66 | +165.75 | +2.17% |

| Korean KOSPI Index | 2,095.41 | -60.27 | -2.80% |

| S&P Basic Materials | 360.98 | +14.33 | +4.13% |

| Russell 2000 | 1,522.44 | -27.19 | -1.75% |

| Hang Seng Composite Index | 3,620.02 | -238.07 | -6.17% |

| S&P/TSX Global Gold Index | 205.10 | +12.28 | +6.37% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -36.10 | -5.79% |

| XAU | 75.81 | +0.48 | +0.64% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

Boeing

Ford Otomotiv Sanayi AS

Geely Automobile Holdings Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Dallas Fed Energy Survey is conducted by the Federal Reserve of Dallas quarterly to obtain a timely assessment of energy activity among oil and gas firms located or headquartered in the Eleventh District. Firms are asked whether business activity, employment, capital expenditures and other indicators increased, decreased or remained unchanged compared with the prior quarter and with the same quarter a year ago. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. The Consumer Confidence Index (CCI) Survey is an index by The Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future. The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange. The SET Index is a Thai composite stock market index which is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year. The Philippine Stock Exchange PSEi Index is a capitalization-weighted index composed of stocks representative of the Industrial, Properties, Services, Holding Firms, Financial and Mining & Oil Sectors of the PSE. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. A basis point is one hundredth of one percent, used chiefly in expressing differences of interest rates.