Ivanhoe Set to Begin Production at World’s Second-Largest Copper Project

Date Posted: September 11, 2020

Read time: 52 min

Copper has had an incredible run, surging 45 percent since its March low on plunging global inventories and the prospect of heightened usage by China, its biggest purchaser. It's also been a good year for one of the world's top explorers of the red metal, Ivanhoe Mines, which just this week released stellar economic results of its tier-one Kamoa-Kakula Copper Project in the Democratic Republic of the Congo (DRC).

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Copper has had an incredible run, surging 45 percent since its March low on plunging global inventories and the prospect of heightened usage by China, its biggest purchaser. It’s also been a good year for one of the world’s top explorers of the red metal, Ivanhoe Mines, which just this week released stellar economic results of its tier-one Kamoa-Kakula Copper Project in the Democratic Republic of the Congo (DRC).

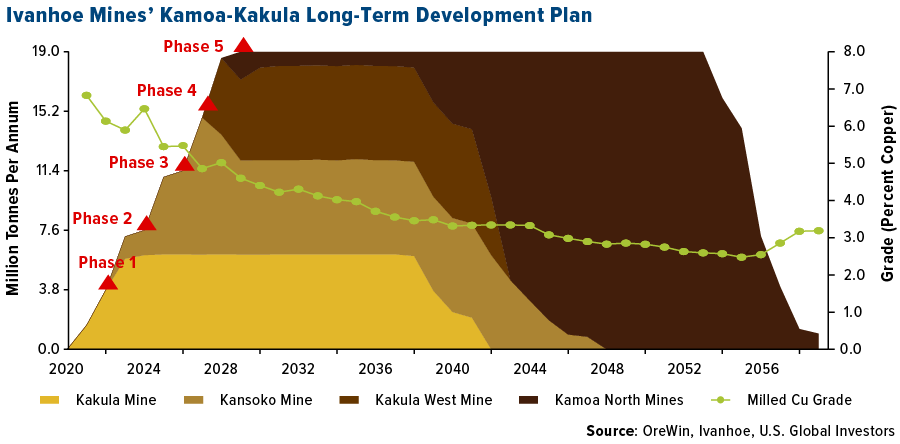

One of our favorite natural resource companies, Ivanhoe has returned more than 146 percent in the past six months alone as investors anticipate the start of production at the Kakula Mine, which has the potential to become the world’s second-largest copper mining complex, with annual output projected to be 800,000 metric tonnes a year.

We now know approximately when phase one of mining is set to begin. The company is fully funded to begin operations in the third quarter of 2021, according to a press release dated September 8.

“Kakula is on track to begin production in under one year from now, which, considering we’ve been working in Africa for 27 years now, feels like tomorrow morning,” commented Robert Friedland, Ivanhoe’s billionaire founder and co-chairman.

It’s impossible to overstate how exciting the news is. As many of you know, a new mine of this scale and quality doesn’t come online too often these days. The copper grade at Kakula is ultra-high at 6.6 percent over the first five years of production, a grade “that is an order of magnitude higher than the majority of the world’s other major copper mines,” according to Robert.

Sure to please ESG investors, operations at the complex will be powered by clean, renewable hydropower, allowing the company to achieve its goal of becoming the world’s “greenest” copper miner.

As you can see in the chart above, production will continue to ramp up in phases until full processing capacity is reached sometime between 2028 and 2030. This makes Ivanhoe a true long-term play on copper, a metal that should only increase in importance as the “electrification of everything” trend accelerates.

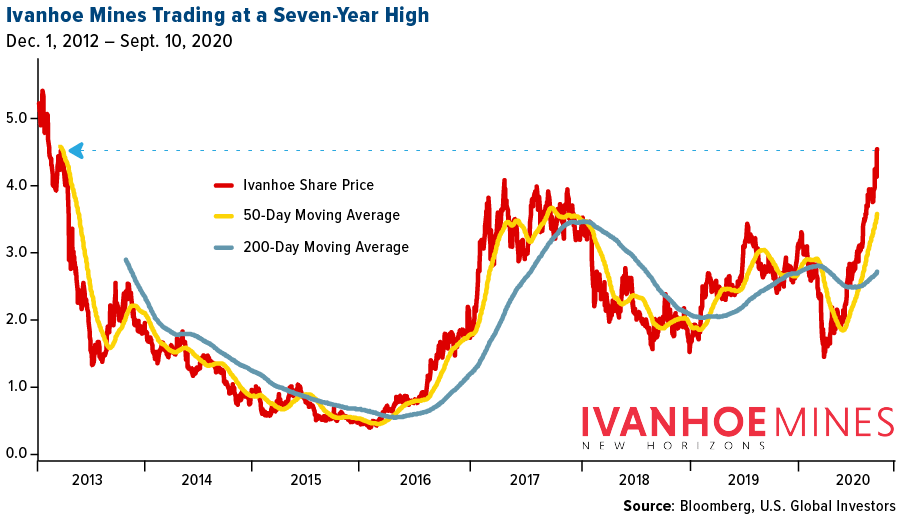

Like copper, shares of Ivanhoe have been on a tear since mid-March. Its stock jumped more than 8 percent on Wednesday following the positive news, its biggest single-day increase since May. The company is now trading at its highest level in seven years, with the best still yet to come. This week, Canaccord Genuity raised its 12-month price target to C$7.00 ($5.30), a 20 percent increase from where it stands today.

Copper Price May Soar on “Historic Squeeze”

If you recall, Robert visited our office in January 2018. He told us then that you’ll need a telescope to see copper prices in 2021.

He may have been on to something.

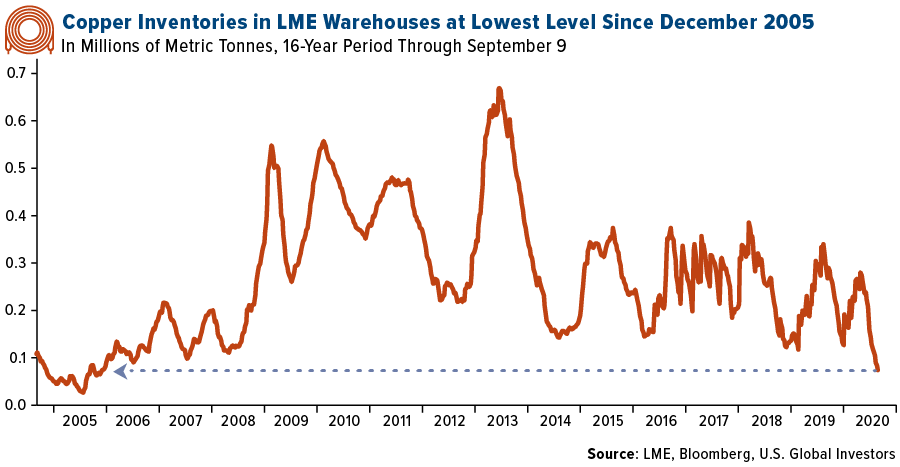

Copper’s supply-demand profile looks incredibly favorable, with the pace of China’s new orders running red hot. Meanwhile, copper inventories in warehouses monitored by the London Metal Exchange (LME) have fallen to a 15-year low.

Some analysts see the same market conditions developing that propelled the price of copper up 450 percent between 2000 and 2011, during China’s industrial explosion. As I recently shared with you, manufacturing activity is expanding at a rapid pace, as measured by the purchasing manager’s index (PMI).

Citigroup is extremely bullish, telling clients this week that a price of $8,000 per ton is possible.

With Kakula set to begin production, Ivanhoe is very well-positioned to ride the wave higher.

Greenspan and Druckenmiller Sound the Alarm Over Inflation

Late last month, I asked whether the headline consumer price index (CPI), the government’s preferred measure of inflation, was “fake news.” According to the Bureau of Labor Statistics (BLS), consumer prices rose only 1.3 percent year-over-year in August. An alternate measure, which uses the 1980 methodology for inflation, puts the increase at closer to 9 percent.

Some of you took a poll on our site asking whether you believe the CPI is an accurate reflection of changes in price. An overwhelming majority of you, 86 percent, said that inflation is happening at a much faster rate than what’s being reported.

Now, former Federal Reserve Chairman Alan Greenspan and billionaire investor Stanley Druckenmiller are both sounding the alarm over the prospect of rising inflation.

Speaking to CNBC on Thursday, Greenspan said his biggest concerns going forward were inflation and the expanding budget deficit. “My overall view is that the inflation outlook is unfortunately negative and that’s essentially the result of entitlements crowding out private investments and productivity growth,” the “Maestro” told the network.

Greenspan has long criticized the rising cost of entitlements such as Medicare and Medicare, calling them a drain on capital reserves.

Also speaking to CNBC this week, Druckenmiller said he believes inflation (as measured by the CPI) could hit between 5 percent and 10 percent in the next four to five years, thanks in large part to the Fed’s unprecedented levels of money-printing.

Near-zero rates have sent valuations soaring, according to Druckenmiller, who says that the market is “in a raging mania.”

“Everyone loves a party, but inevitably after a big party there is hangover,” he added.

Current Fed Chair Jerome Powell recently unveiled the central bank’s new approach to managing inflation, saying changes in prices would average 2 percent over time. The implication is that the Fed would allow inflation to run hot in some instances. To get there, rates will likely remain at zero for some time longer.

$25 Trillion in Bank Assets, $20 Trillion in Stimulus Spending

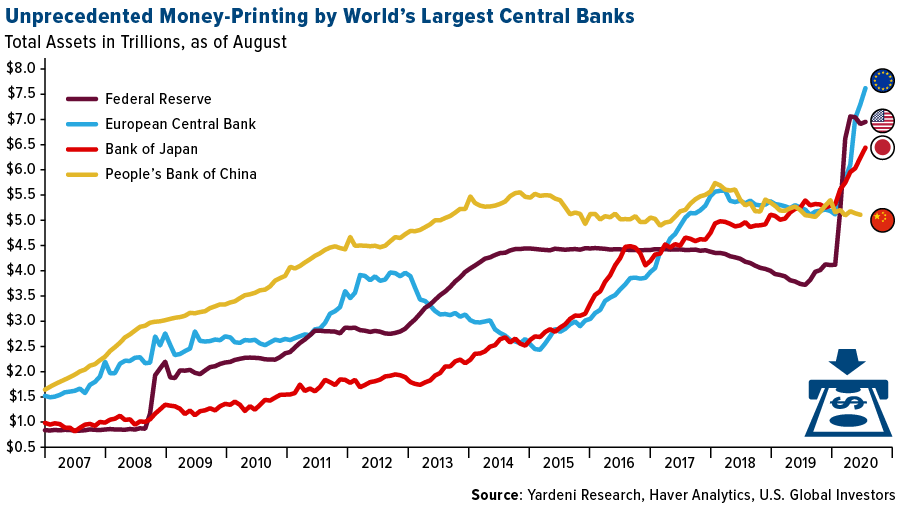

Meanwhile, the amount of assets on the Fed’s balance sheet has surged to more than $7 trillion. Combined with balance sheets of other major central banks—the European Central Bank (ECB), Bank of Japan (BoJ) and People’s Bank of China (PBOC)—total assets are currently above an unbelievable $25 trillion.

On the fiscal side, world governments have so far announced $20 trillion in stimulus measures in response to the global pandemic.

Much of this new cash has flowed into ETFs, whose assets under management (AUM) have hit $7 trillion for the first time ever. Global investors have ploughed as much as $428 billion into ETFs so far in 2020 through the end of August, a 57 percent increase from the same eight months last year, according to the Financial Times.

Citi Raises Average Gold Price Forecast to $2,500

But with the risk of currency devaluation higher now than it’s been in recent memory, it’s crucial that investors get exposure to gold and other hard assets using the 10 Percent Golden Rule.

Coincidentally, Greenspan and Druckenmiller are both fans of the yellow metal as a portfolio diversifier, not to mention other heavyweights including Bridgewater’s Ray Dalio, Paul Singer and Paul Tudor Jones. And don’t forget that none other than Warren Buffett himself, who has long derided the asset, took a stake in a gold producer for the first time, disclosing a $565 million position of Barrick Gold as of June.

Shares of Barrick are up close to 64 percent so far in 2020.

The price of gold is around 6 percent off its all-time high, making now an incredible buying opportunity. Today, analysts at Citi raised their 2021 gold price forecast some $300 an ounce and believe the metal could average $2,500 in 2021, with a target of $2,200 over the next three months and one of $2,400 over the next six to 12 months. A weaker U.S. dollar and heightened macro uncertainty should serve as support, Citi says.

I maintain my call for $4,000 gold in the next three years due to record stimulus spending and money-printing, which may lead to extreme currency debasement. Get my full thoughts by watching my interview with CNBC below, and make sure to like and subscribe to our YouTube channel!

Gold Market

This week spot gold closed at $1,941.99, up $11.08 per ounce, or 0.57 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.51 percent. The S&P/TSX Venture Index came in up 0.46 percent. The U.S. Trade-Weighted Dollar rose 0.57 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-4 | Change in Nonfarm Payrolls | 1350k | 1371k | 1734k |

| Sep-10 | ECB Main Refinancing Rate | 0.00% | 0.00% | 0.00% |

| Sep-10 | PPI Final Demand YoY | -0.30% | -0.20% | -0.40% |

| Sep-10 | Initial Jobless Claims | 850k | 884k | 884k |

| Sep-11 | Germany CPI YoY | 0.00% | 0.00% | 0.00% |

| Sep-11 | CPI YoY | 1.20% | 1.30% | 1.00% |

| Sep-14 | China Retail Sales YoY | 0.00% | — | -1.10% |

| Sep-15 | Germany ZEW Survey Expectations | 69.5 | — | 71.5 |

| Sep-15 | Germany ZEW Survey Current Situtaion | -72 | — | -81.3 |

| Sep-16 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Sep-17 | Eurozone CPI Core YoY | 0.40% | — | 0.40% |

| Sep-17 | Housing Starts | 1480k | — | 1496k |

| Sep-17 | Initial Jobless Claims | 850k | — | 884k |

Strengths

- The best performing precious metal for the week was platinum, up 2.91 percent. The price of gold saw a small uptick on Thursday after the producer price index (PPI) increased 0.3 percent in August and the Labor Department said 884,000 Americans filed for first-time jobless claims in the most recent week. The metal notched a small weekly gain of 0.57 percent. Reuters reports that Thailand’s central bank will allow gold trading in U.S. dollars soon as it tries to curb the impact of growing gold demand on the baht currency.

- Silver, known for its massive and rare price spikes, could be on its way to another boom. The white metal’s gains are nearly double that of gold for 2020. Retail investors have added more than 8,800 tons of the metal to ETFs so far this year. Bloomberg notes than Robinhood buyers of the largest silver ETF have more than doubled in the month leading to August 13.

- The Turkish Treasury and the Istanbul Gold Refinery will allow selected jewelers to collect gold from citizens and deposit it at state banks in a new effort to coax gold into its financial system. It is estimated that “under-the-mattress” stashed gold is valued around 40 percent of Turkey’s GDP. According to Esen, an estimated 5,000 tons of gold are stored outside of the financial system. Gold is popular in the country as a protection against inflation and traditional gift for holidays and celebration – especially as the lira as gone through wild price swings.

Weaknesses

- The worst performing precious metal for the week was silver, down 0.48 percent.

- The 120-day rolling correlation between gold and the Bloomberg Barclays gauge of emerging-market dollar bonds fell below zero for the first time since July 2016 this week – signaling that the two assets have stopped responding in the same way to the dollar’s moves. While the gold rally is looking “tired and ripe for a correction,” emerging-market bonds are extending gains to a sixth month, reports Bloomberg.

- As demand for physical gold as a haven asset has jumped, so too has the cost and logistics of insuring it. Bloomberg Businessweek notes that as the price of gold rises, the number of insurable ounces at each storage site decreases, since insurers place a cap on how much financial exposure they’ll assume for each vault. Ludwig Karl of Swiss Gold Safe, which manages vaults in the Alps, said “you could put all the gold in the world in a large storage space, but you would never be able to get the insurance for it.” Although positive that demand is rising, is it a small weakness that insurance and storage difficulties could detract new buyers.

Opportunities

- Gold-backed ETFs saw a ninth-straight month of inflows in August, driven by growing appetite in Asia. Collectively, 39 tons of bullion, equivalent to $2.1 billion, were added to ETFs in August with 7 tons coming from Asia.

- A diamond the size of an egg is being put up for auction next month and is expected to fetch $12 million to $30 million. Kitco News reports that Sotheby’s is selling a 102.39-carat diamond – the second largest oval diamond of its kind to be offered at auction. The largest ever, a 118.28-carat stone set a record $30.8 million price in 2013.

- Talley Leger, investment strategist at Invesco, said in a commentary that the end to gold’s bull run looks increasingly unlikely, reports Kitco News. Leger says for the gold market to lose steam, the U.S. economy would have to overheat enough to force the Fed to drastically raise interest rates, which would boost the dollar. “In our view, the Fed seems determined to protect this budding upturn by keeping interest rates low for the foreseeable future.” Lower rates boost gold’s appeal since it is a non-interest-bearing asset.

Threats

- A flurry of new investors to the gold mining space has Newmont Corp. warning against dodgy deals. The SEC warns investors of “mini-tender” offers: “Some bidders make mini-tender offers at below-market prices, hoping they will catch investors off guard if the investors do not compare the offer price to the current market price.” Newmont explains that these are offers to acquire less than five percent of a company’s outstanding shares and avoid many of the investor protections afforded for larger tender offers.

- James Steel, chief precious metals analyst at HSBC, said a rise in international trade could create an unfavorable market for gold. Steel points out that an increase in trade is a positive sign for global economic growth and geopolitical stability, which decreases the appeal of gold. “The outlook for trade is better than it was, but is still contracting that is good for gold,” Steel said on an LBMA webinar this week.

- LVMH (Moet Hennessy Louis Vuitton) said it will walk away from its planned $16 billion takeover of Tiffany – a hit to the jewelry and luxury goods industry. LVMH said that its board received a letter from the French foreign ministry asking it to delay the acquisition to beyond January 2021 due to the threat of additional U.S. tariffs. At the same time, LVMH said Tiffany asked to extend the deadline to December 31 from the original date of November 24. Now Tiffany is suing to force the deal through – which was set to be the largest transaction ever in the luxury sector.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.22 percent. The S&P 500 Stock Index fell 3.23 percent, while the Nasdaq Composite fell 5.28 percent. The Russell 2000 small capitalization index lost 3.01 percent this week.

- The Hang Seng Composite lost 2.75 percent this week; while Taiwan was down 0.64 and the KOSPI rose 0.03 percent.

- The 10-year Treasury bond yield rose 3 basis points to 0.667 percent.

Domestic Equity Market

Strengths

- Materials was the best performing sector of the week, increasing by 0.82 percent versus an overall decrease of 2.48 percent for the S&P 500.

- Tapestry was the best performing S&P 500 stock for the week, increasing 10.92 percent.

- Peloton stock jumped this week after turning its first quarterly profit. Shares rose as much as 13 percent in pre-market trading on Friday.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 6.43 percent versus an overall decrease of 2.48 percent for the S&P 500.

- Apache was the worst performing S&P 500 stock for the week, falling 18.60 percent.

- Shares in Slack sunk almost 20 percent after reporting showed how the pandemic and its rivalry with Microsoft put pressure on its growth. Compared to other remote work beneficiaries like Zoom, Slack’s numbers have been underwhelming to many observers.

Opportunities

- Chinese technology giant Baidu is in talks with investors to raise $2 billion for a new biotech startup, reports Reuters. The spin-out firm would use Baidu’s AI technology to find and develop drugs, as well as diagnose early-stage cancer, anonymous sources told Reuters.

- Billionaire Howard Marks says real estate, retail, entertainment and hospitality stocks are the real opportunities for investors now, writes Business Insider. Investors shouldn’t worry about Wall Street’s recent tech-sell off and noted markets "can’t tell what lies ahead," he said.

- Warren Buffett’s Berkshire Hathaway will invest over $550 million into Snowflake when the cloud-data company goes public. The famed investor’s company has agreed to buy $250 million of stock in a private placement and over $300 million worth from Snowflake’s former CEO.

Threats

- Veteran bull Ed Yardeni says stocks can fall another 10-15 percent, writes Business Insider, but the market will then make a ‘comeback’. "I’m actually somewhat comforted by the market taking a break here. It’s a healthy development," the economist said of last week’s sell-off.

- Goldman Sachs says Wall Street’s fear gauge is flashing a warning sign unseen since the dot-com crash in 2000. Strong volatility in technology stocks and investor concerns over the U.S. election results are key factors pushing the volatility index higher, analysts said.

- Jeffrey Gundlach says the day-trading boom is “downright terrifying,” specifically noting that an increase in trades-per-account on online brokerage platforms was worrying. Additionally, a Wall Street expert says the emerging “species” of risk-loving day traders is threatening to upend an already vulnerable stock market. "Right now, anyone trying to trade this market needs to better understand this new species of trader," Academy Securities’ Peter Tchir said.

The Economy and Bond Market

Strengths

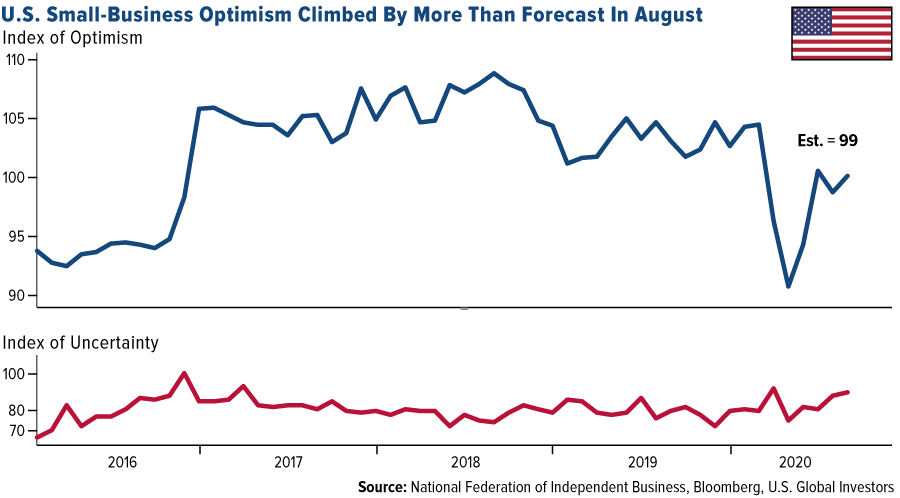

- There’s a growing sense of optimism among America’s small-business owners, though uncertainty remains, according to the latest data from the National Federation of Independent Business (NFIB). The group’s index of sentiment increased by 1.4 points to 100.2 in August—still below this year’s high of 104.5 reached in February—beating the median estimate in a Bloomberg survey of economists.

- Sentiment among U.S. consumers improved the most in 11 years last week as the economy slowly improves, but it remains well below levels seen before the onset of the coronavirus pandemic. The Bloomberg Consumer Comfort Index rose 2.7 points to 47.8 last week, data released Thursday show. This is the largest one-week improvement since April 2009.

- Goldman Sachs upgraded its third-quarter U.S. GDP forecast to 35 percent after a stronger August jobs report, making it by far the most bullish bank on Wall Street.

Weaknesses

- The number of Americans who applied for unemployment benefits through state and federal programs rose in early September for the fourth week in a row, signaling that a gradual improvement in the labor market during the summer has stalled. Initial jobless claims filed traditionally through state employment offices were unchanged at a seasonally adjusted 884,000 in the week of August 30 to September 5, the Labor Department said Thursday. Economists polled by MarketWatch had forecast new claims to fall to 840,000.

- Prospects for any additional stimulus to address the coronavirus pandemic’s devastating toll before the election darkened considerably on Thursday, when a whittled-down Republican plan failed in the Senate on a partisan vote. Democrats voted unanimously to block the proposal from advancing, calling it inadequate to meet the mounting needs for federal aid, in the latest indication of a lack of political will to reach an agreement, even as critical federal aid for individuals and businesses has run dry. It was a nearly party-line vote whose outcome was never in doubt. The proposal amounted to a fraction of the $1 trillion plan Republicans had offered in negotiations with Democrats, who in turn are demanding more than twice as much.

- The U.S. budget deficit hit an all-time high of $3 trillion for the first 11 months of this budget year, the Treasury Department said Friday. The ocean of red ink is a product of the government’s massive spending to try to cushion the impact of the coronavirus-fueled recession. The deficit from October through August is more than double the previous 11-month record of $1.37 billion set in 2009. At that time, the government was spending large sums to get out of the Great Recession triggered by the 2008 financial crisis.

Opportunities

- The September industrial surveys as well as the University of Michigan’s preliminary consumer sentiment gauge next week will provide fresh looks at how business and consumer confidence are shaping up ahead of the November elections.

- The Federal Reserve will wrap up its policy meeting next Wednesday, and the question is whether policymakers will try to make their new “inflation overshooting” framework more credible by hinting at new measures to boost inflation, or whether they think they have done enough for now. Judging by some recent comments from policymakers and the minutes of the July meeting, the Fed is more likely to take the sidelines. The minutes implied there is no rush to strengthen the forward guidance, a view echoed by a few officials lately, who hinted they would like some more clarity on the economy’s path before committing to anything new. Since economic data have remained encouraging, with consumption bouncing back and the jobs market recovering at a healthy clip, there’s little pressure on policymakers to act immediately. After all, there is also an election approaching fast and the outlook for government spending will become clearer after the election, so Fed officials will have a better sense of how much more stimulus is needed.

- Stanley Fischer, former vice chair of the Federal Reserve, says a low-interest rate burden means the Fed can do more to bolster the economy. “The interest burden is way lower than it was in 2008. It means that the Fed can keep going with very cheap money, that it can go on for a much longer time at this rate,” Fischer said in a Bloomberg interview.

Threats

- Next week, August retail sales will provide the first snapshot of consumer spending following the expiration of the $600 top-up to regular unemployment benefits at the end of July. The report will also be instructive because August back-to-school sales inform expectations for the upcoming holiday season.

- Hackers linked to Russia, Iran and China are attacking the Biden and Trump campaigns ahead of the election, Microsoft said. While hackers linked to Russia appeared to be attacking people affiliated with both campaigns, hackers linked to China tended to focus on Biden’s and those aligned with Iran went after Trump’s, Microsoft found.

- China is retaliating against the U.S. for its “naked bullying” of TikTok with a new global security initiative. The data push is a retaliation against the U.S. "Clean Network Initiative" which is aimed at walling off the Chinese internet.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was corn, up 3.21 percent. Copper continues to recover strongly. The red metal has increased 45 percent since its March low due to falling inventories and heightened usage by China. Copper producer Ivanhoe Mines has returned more than 146 percent in the past six months as investors anticipate production at the Kakula Mine, which has the potential to become the world’s second-largest copper mining complex.

- Cold winter forecasts are giving hope to the LNG rally. Bloomberg notes that benchmarks for the fuel in North Asia and Europe have only recently returned to pre-pandemic levels, with the rally supported by unplanned outages and slowly recovering demand. North Asia, one of the world’s top buyers, has a winter outlook colder than previous years, which could support greater demand. The regional benchmark is up 68 percent since early August.

- China announced a five-year plan beginning in 2021 that will call for increases to its huge inventories of crude oil, strategic metals and farm goods. The move is likely an effort to ensure the nation is stocked up in case of another global pandemic or supply chain disruption. This is positive for commodity demand.

Weaknesses

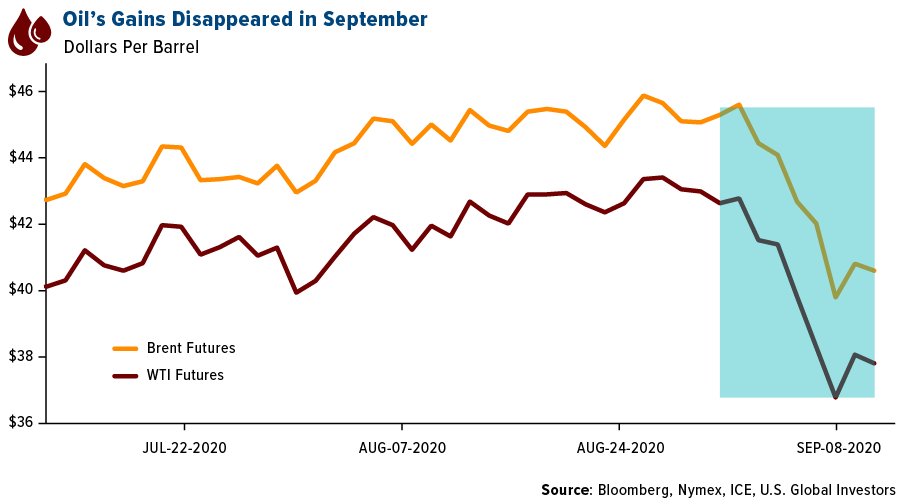

- The worst performing commodity for the week was natural gas, down 13.06 percent. Oil was the second worst performing commodity, down 5.71 percent, and fell below $37 a barrel after the Energy Information Administration (EIA) reported domestic crude stockpiles rose for the first time since mid-July. September saw gains erased for oil, with benchmark futures falling around 13 percent since the end of August. Both WTI and Brent fell sharply and had the first back-to-back weekly losses since the April dive. Oil traders are buying up tankers – a sign of sentiment that another oil glut is coming. Bloomberg notes that Trafigura Group recently booked a dozen supertankers that can hold 24 million barrels of the fuel.

- Rio Tinto Group CEO Jean-Sebastien Jacques is stepping down amid investor backlash over the destruction of ancient Aboriginal heritage sites in Australia in May to open up a new mining area, reports Bloomberg. Two other senior officials are resigning. The miner held talks with 75 investors and indigenous community leaders and found they were unsatisfied with the conclusion that no single individual was at fault for the blasts. This is a sign of how strong of an influence shareholders and the community can have over a company and its leadership.

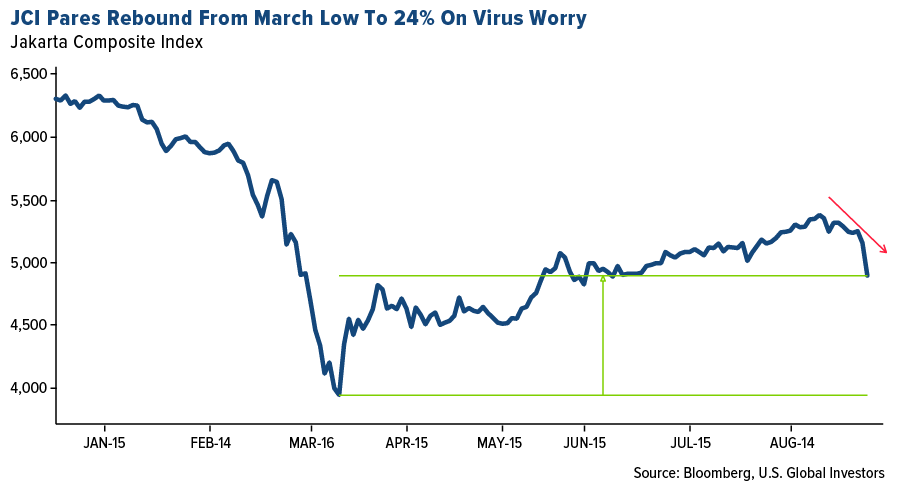

- Indonesia’s capital city Jakarta is being put back on lockdown – surprising investors and threatening to prolong the country’s economic recovery. As coronavirus infections overwhelm hospitals and medical workers, the major city is going back on lockdown to get the virus under control. This is a warning sign to the world that a second wave of lockdowns is possible. Western Europe now has more daily infections than the U.S. and is re-emerging as a global hotspot for the virus.

Opportunities

- NASA is seeking bids from explorers who are willing to finance their own trips to the moon to collect soil or rock samples without returning any material to earth, reports Bloomberg. The purpose is to establish a legal framework for mining on the moon that would allow NASA to one day collect ice, helium and other materials. The agency said it anticipates paying between $15,000 and $25,000 per moon contract.

- BP and Shell are calling for Texas regulators to end the practice of routine natural gas flaring, which releases harmful carbon dioxide into the air. The shale boom has led to a massive glut of the fuel, and prices are often so cheap that it’s cheaper for producers to burn it rather than pay for pipelines to take it to the market, writes Bloomberg Green.

- Bloomberg reports that Orix Corp is buying a 20 percent stake in Indian renewable energy developer Greenko Energy Holdings for $980 million. “India is a big and attractive market – power demand is growing”, Hidetake Takashi, an executive officer at Orix said in an interview.

Threats

- California’s wildfires rage on. More than 4,800 square miles have burned so far this year – more than the land of Rhode Island, Delaware and Washington D.C., combined. AP reports that at least 19 people have been killed and more than 4,000 structures have been burned across California. The fires are spreading to other states. 1,400 square miles have burned in Oregon and nearly 937 square miles burned in Washington this week.

- African swine fever, a deadly pig disease, has been confirmed in Germany for the first time. The virus kills most infected pigs within 10 days but is not harmful to humans. Germany is a key supplier to China, the largest consumer, and the fear is that China will stop importing pork due to the virus.

- A flurry of new investors to the gold mining space has Newmont Corp warning against dodgy deals. The SEC warns investors of “mini-tender” offers: “Some bidders make mini-tender offers at below-market prices, hoping they will catch investors off guard if the investors do not compare the offer price to the current market price.” Newmont explains that these are offers to acquire less than five percent of a company’s outstanding shares and avoid many of the investor protections afforded for larger tender offers.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 3.4 percent. In June, Romania reported the fastest construction growth in the EU as building sites stayed opened throughout the lockdowns in Romania. Romanian banks outperformed stocks trading on the Bucharest Stock Exchange. Banca Transilvania gained 8.7 percent and shares of BDR-Groupe Societe Generale appreciated by 5.4 percent over the past five days. BRD was raised to a “buy” rating at Wood & Company.

- The Hungarian forint was the best performing currency this week, gaining 84 basis points. The currency gained the most after the European Central Bank (ECB) showed no urgency toward further monetary easing. In addition, the Hungarian opposition called for government action to strengthen the nation’s currency.

- Utilities was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst performing country this week, losing 54 basis points. The country’s income from foreign visitors fell 64 percent in the second quarter of 2020 compared to the same period last year. Czech inflation slowed slightly in August but stayed above the central bank’s tolerance range, due to massive government stimulus supporting consumption. Stock Spirits Group, an alcoholic beverages maker, was the worst performing equity trading on the Prague Stock Exchange, losing 2.4 percent over the past five days.

- The Turkish lira was the worst performing currency in the region this week, losing 80 basis points. The lira continued it downtrend despite costs of funding moving higher, fueled by worsening economic data and increasing geopolitical tensions.

- The health care sector was the worst performing sector among eastern European markets this week.

Opportunities

- The ECB left its main rates and bond-buying program unchanged and the ECB President announced strong economic rebound in the euro area. In context, the ECB revised up its growth forecast slightly. GDP is seen now dropping by 8 percent this year, from the June estimate of negative 8.7 percent. For 2021, the ECB expects euro-area revenue to grow by 5 percent and by 3.2 percent in the year after that.

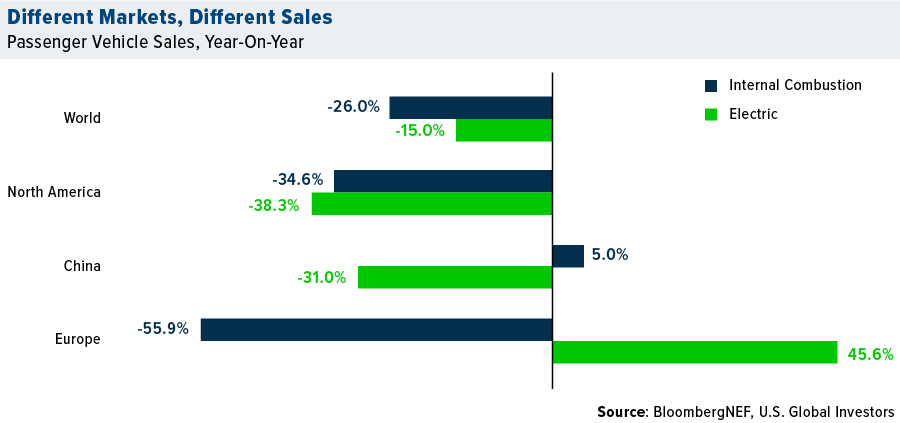

- Europe’s 16 major markets in car sales had the largest fall in the internal combustion sales (down 56 percent year-over-year) and a similarly large increase in the electric vehicles sales (up more than 45 percent). The electric car sales will probably grow further in the years to come, supported by new stimulus programs, new model launches and automakers pushing to hit their carbon dioxide emission targets.

- Bloomberg economists predict euro-area industrial production to improve in July. Data will be released on Monday and the survey estimates a drop of 8.8 percent on a year-over-year basis versus 12.3 percent the prior month. It is continuing its V-shape recovery from a recent low reading in April.

Threats

- According to the World Health Organization and Bloomberg calculations, Western Europe has surpassed the United States in new daily coronavirus infections, re-emerging as a global hotspot. The 27 countries, the European Union plus the United Kingdom, Norway and Iceland and Lichtenstein recorded 27,233 new cases on Wednesday, compared with 26,015 in the U.S. In recent weeks Europe has seen a resurgence in infections especially in Spain, France and Italy.

- Putin’s biggest critic Alexi Navalny remains in a German hospital, but his condition has improved. He has been taken out of the induced coma and regained his ability to speak, but still long-term effects of his poisoning are not known. Tensions between Russia and Western Europe may increase as Germany claims that Navalny was poisoned by a Soviet-era nerve agent, the same nerve agent that almost killed former Russian spy on Great Britain soil a few years back.

- Eurozone efforts to pressure Belarus to resolve political problems there are being held up by disputes between Cyprus and Turkey. Cyprus told European members that it won’t approve Europe’s proposal to sanction Belarusian officials unless member states also agree to act on Turkey over drilling activities in the Mediterranean Sea.

China Region

Strengths

- The Philippines was the best performing country this week, gaining 3.2 percent. President Rodrigo Duterte signed into law a second pandemic relief measure worth 165.5 billion pesos ($3.4 billion). The Philippines has the most coronavirus infections in Southeast Asia, with 252,964 cases, including 4,108 deaths as of Friday. Holding company Alliance Global Group Inc., was the best performing equity among stocks trading in the iShares Philippines ETF (EPHE), gaining 13.2 percent over the past five days.

- The Thailand baht was the best performing currency this week, gaining 33 basis points. The currency was supported by continued bond inflows.

- Telecommunication stocks were the best performers among those trading on the Hong Kong Stock Exchange.

Weaknesses

- Indonesia was the worst performing market this week, losing 2.9 percent. The government announced another lockdown in Jakarta starting on Monday due to the spike of COVID-19 infections. Real estate company, Lippo Karawaci TBK, was the worst performing equity among stocks trading in the iShares MSCI Indonesia ETF (EIDO), losing 16 percent over the past five days.

- The Indonesia rupee was the worst performing currency this week, losing 2 percent. Currency and equites sold-off on fears of negative economic effects from a new large-scale lockdown being imposed in the country’s capital.

- Health care stocks were the worst performers among stocks trading on the Hong Kong Stock Exchange.

Opportunites

- The Chinese government is taking steps to encourage consumption. A State Council meeting statement stressed measures supporting new industries and patterns to boost new types of consumption to foster the economic recovery. Xinhua reports there are measures to speed up the innovative development of medical education online and contactless consumption patterns.

- According to documents reviewed by Bloomberg News, India is set to offer incentives up to $23 billion to attract companies to set up manufacturing in the nation. The government will offer production-linked incentives to automobile manufacturers, solar panel makers and specialty steel to consumer appliance companies, among others.

- Citigroup Inc. is sending an additional 20 percent of its staff back to work in the office from Hong Kong starting next week. Coronavirus cases in Hong Kong have dropped from record highs.

Threats

- According to data from the American Chamber of Commerce in Shanghai, U.S. companies in China are increasingly worried that trade tensions between the two countries will worsen over several years. A third of companies surveyed said their ability to retain staff has been affected. Reuters notes that half of the firms said they believe sour tensions will last up to three years, up from just 30 percent believing this in 2019.

- The U.S. canceled over 1,000 visas for Chinese nationals deemed security risks, reports Reuters. The Department of Homeland Security is blocking visas for certain Chinese graduate students and researchers with ties to China’s military strategy.

- Indonesia’s capital city Jakarta is being put back on lockdown – surprising investors and threatening to prolong the country’s economic recovery. Bloomberg reports that the Indonesian economy could contract for a third consecutive quarter, instead of earlier expectations for a recovery toward the end of the year, as Jakarta accounts for 20 percent of the economy.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 11 was TAI, up over 9,000 percent.

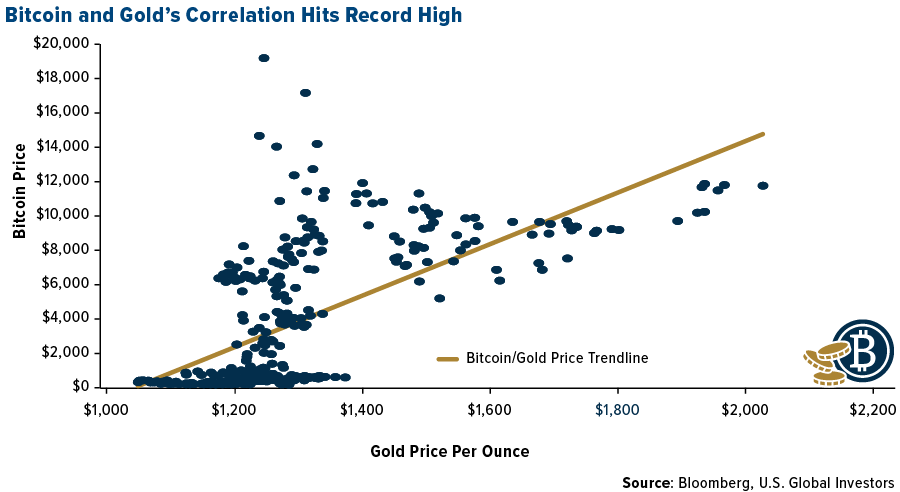

- Bitcoin is now more closely tied to gold than ever before, writes CoinDesk, possible bringing the digital asset greater resilience to risk aversion in the traditional markets. Coin Metrics data, in fact, shows that the 60-day correlation between the two assets is hovering at record highs above 0.5. As the U.S. dollar started taking a beating against other major currencies, the article continues, the positive correlation has strengthened sharply since the start of July.

- Both gold and bitcoin have had a good run among investors seeking a haven or those willing to take a punt on cryptocurrency, writes Bloomberg. But another investment thesis is emerging as a bit more successful over the past year. Instead of buying into either asset, the article continues, those who threw their money behind a basket of companies with exposure to blockchain companies would have returned 54 percent over the past year, even after the rout that has hit global tech stocks the hardest. Guess the old adage remains true: it’s smartest to be selling shovels in a gold rush.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 11 was Based Money, down 99.54 percent.

- As reported by The Straits Times, a major suspect in a high-profile theft case related to bitcoin trading has pleaded guilty as an accomplice in a $360,000 robbery. Pretending to be a bitcoin broker, Syed Mokhtar Syed Yusope and two accomplices stole hundreds of thousands of dollars from a Malaysian man in Singapore, writes CoinTelegraph.

- Russia’s new cryptocurrency-related law, “On Digital Financial Assets,” in its current form, is essentially providing legal status to digital assets like bitcoin, but prohibits their use for payments in Russia, writes CoinTelegraph. Based on comments from executives at companies like Binance, Paxful and Wirex, however, they aren’t exactly scrambling to adapt to the new law, primarily because of its ambiguous language.

Opportunities

- On Wednesday, Mastercard announced the release of a proprietary tool targeted to central banks that wish to test their Central Bank Digital Currency (CBDC), writes CoinTelegraph. A Bank of International Settlements report notes that over 70 percent of central banks are entertaining the idea of a digital currency of some form. While few have moved into concept and experimentation, MasterCard’s tool aims to make testing simpler, the article continues.

- The price of bitcoin has been ranging from $9,800 to $10,500 for nearly a week following a short fall from nearly $12,100 on September 1, writes CoinTelegraph. Although the cryptocurrency isn’t showing any distinctive price movement, over the medium to long term, traders expect bitcoin to recover and “perceive the ongoing consolidation phase as a healthy pullback.”

- On Thursday, Square announced the launch of what it calls the Cryptocurrency Open Patent Alliance (COPA), reports CoinDesk, a non-profit that wants to stop companies from locking up useful technologies in patents, a practice that Square says hamstrings innovation. In order to become a part of COPA, members must pledge to make their patents freely available to all other members using a shared library.

Threats

- A previously undisclosed vulnerability in the Bitcoin Core software could have allowed attackers to steal funds, delay settlements or split the largest blockchain network into conflicting versions, writes CoinDesk. All of that had the potential to become reality had it not been quietly patched two years ago, according to a paper published by Braydon Fuller – a protocol engineer at Purse. The vulnerability was given a severity level of 7.8 on a scale of 1 to 10.

- As bitcoin falls in tandem with U.S. stocks, Bloomberg writes that technical indicators suggest it could decline even further if it fails to reverse recent downside momentum. “One by one, the dominoes of what were the most popular trades in the market have fallen,” said Brad Bechtel, head of global currency trading at Jeffries LLC. “The market is in a bit of liquidation mode, unwinding many of the popular trades from the summer or from the start of the post-COVID rebound. Bitcoin is one of them.”

- After going offline for 14 hours on August 10 and 11, Polkadot validator Web3Italy has been “slashed” and “chilled,” writes CoinTelegraph. What does this mean? The validator has lost their staked tokens and been temporarily kicked from the network. “This validator was offline when a biggest set of validators failed, all of which for slashed and aren’t being forgiven,” said Web3 Foundation technical educator Bruno Skvorc said. “This validator was collateral damage.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.67 | +0.03 | +4.87% |

| Oil Futures | 37.52 | -3.85 | -9.31% |

| Hang Seng Composite Index | 3,793.82 | -107.21 | -2.75% |

| S&P Basic Materials | 408.16 | +3.84 | +0.95% |

| Korean KOSPI Index | 2,396.69 | +0.79 | +0.03% |

| S&P Energy | 243.58 | -17.60 | -6.74% |

| Nasdaq | 10,853.55 | -604.56 | -5.28% |

| DJIA | 27,665.64 | -627.09 | -2.22% |

| Russell 2000 | 1,498.22 | -46.46 | -3.01% |

| S&P 500 | 3,343.56 | -111.50 | -3.23% |

| Gold Futures | 1,950.40 | +12.60 | +0.65% |

| XAU | 150.34 | -0.59 | -0.39% |

| S&P/TSX VENTURE COMP IDX | 733.71 | +3.36 | +0.46% |

| S&P/TSX Global Gold Index | 380.84 | +2.32 | +0.61% |

| Natural Gas Futures | 2.25 | -0.24 | -9.57% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,396.69 | -35.66 | -1.47% |

| 10-Yr Treasury Bond | 0.67 | -0.01 | -1.33% |

| Gold Futures | 1,950.40 | +1.40 | +0.07% |

| S&P Basic Materials | 408.16 | +14.52 | +3.69% |

| S&P 500 | 3,343.56 | -36.79 | -1.09% |

| DJIA | 27,665.64 | -311.20 | -1.11% |

| Nasdaq | 10,853.55 | -158.70 | -1.44% |

| Oil Futures | 37.52 | -5.15 | -12.07% |

| Hang Seng Composite Index | 3,793.82 | -5.46 | -0.14% |

| S&P/TSX Global Gold Index | 380.84 | +21.91 | +6.10% |

| XAU | 150.34 | +8.66 | +6.11% |

| Russell 2000 | 1,498.22 | -85.02 | -5.37% |

| S&P Energy | 243.58 | -46.49 | -16.03% |

| S&P/TSX VENTURE COMP IDX | 733.71 | +8.00 | +1.10% |

| Natural Gas Futures | 2.25 | +0.10 | +4.51% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 150.34 | +35.50 | +30.91% |

| S&P/TSX Global Gold Index | 380.84 | +67.61 | +21.58% |

| Gold Futures | 1,950.40 | +192.80 | +10.97% |

| DJIA | 27,665.64 | +2,537.47 | +10.10% |

| S&P 500 | 3,343.56 | +341.46 | +11.37% |

| Nasdaq | 10,853.55 | +1,360.82 | +14.34% |

| Korean KOSPI Index | 2,396.69 | +219.91 | +10.10% |

| Natural Gas Futures | 2.25 | +0.44 | +24.05% |

| S&P Basic Materials | 408.16 | +69.72 | +20.60% |

| Russell 2000 | 1,498.22 | +142.00 | +10.47% |

| Oil Futures | 37.52 | +1.18 | +3.25% |

| Hang Seng Composite Index | 3,793.82 | +258.26 | +7.30% |

| S&P/TSX VENTURE COMP IDX | 733.71 | +189.51 | +34.82% |

| S&P Energy | 243.58 | -47.81 | -16.41% |

| 10-Yr Treasury Bond | 0.67 | -0.00 | -0.60% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2020):

Banca Transilvania

Groupe Societe Generale

Ivanhoe Mines Ltd

Barrick Gold Corp

Newmont Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Bloomberg Consumer Comfort Index is based on responses to a weekly, random-sample national telephone survey asking Americans to rate the economy, the buying climate and their personal finances as excellent, good, not so good, or poor. Conducted continuously since late 1985, the reported results reflect a sample size of 1000 consumers, aged 18 or over, using a four-week rolling average of 250 interviews per week. The University of Michigan of Consumer Sentiment Index is comprised of measures of attitudes toward personal finances, general business conditions, and market conditions or prices.