Look Which Precious Metal Is Beating Warren Buffett…

Date Posted: September 13, 2019

Read time: 59 min

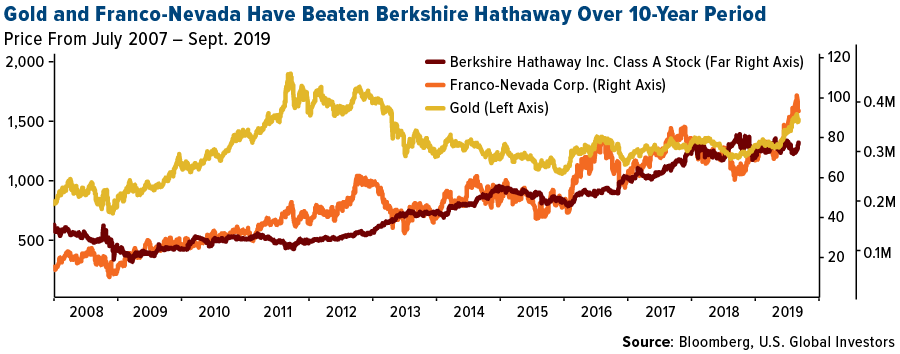

Way back in January, I showed you that the price of gold had beaten the S&P 500 Index over a number of different time periods, including the month, quarter, year... and even the century (so far!).

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

I want to begin this week by extending my most heartfelt condolences to my longtime friend Bob Moriarty, founder and editor-in-chief of 321gold.com. This week Bob lost his wife Barbara to a heart attack after 29 wonderful years of marriage. According to Bob, she was “the genius of 321gold.” Having known Barbara for years, I can say that she was much more than that—charming, gregarious and very, very funny. She is survived by Bob, her daughters and granddaughters. To my friend, on behalf of everyone at U.S. Global Investors, I wish you comfort and peace through your cherished memories. She will be greatly missed!

There are two headline items that transpired this week that I want to make sure all of my readers are aware of.

1. Passive indexing has surpassed active investing.

2. There has been a massive rotation from growth stocks to value stocks, with big moves in financials, energy and materials.

As we look at both pieces of news, we keep our analysis at U.S. Global Investors heavily focused on GARP investing – which is growth at a reasonable price. We consider ourselves more value investors as well. I encourage you to do a little research on these items, and stay tuned to my Frank Talk blog this week for a more in-depth discussion. For now, I’d like to turn your attention to Warren Buffett.

Way back in January, I showed you that the price of gold had beaten the S&P 500 Index over a number of different time periods, including the month, quarter, year… and even the century (so far!).

It was brought to my attention recently—in a tweet by Charlie Bilello, director of research at Pension Partners—that the yellow metal has also outperformed arguably the greatest living investor, Warren Buffett.

For the 20-year period, gold has returned more than 485 percent, beating Warren’s Berkshire Hathaway, which was up 426 percent. Not only that, gold royalty and streaming company Franco-Nevada, has beaten Buffett too.

Visionary: Pierre Lassonde

|

The royalty model is one I believe strongly in and have written about often.

Pierre Lassonde, chair and co-founder of Franco-Nevada, has helped the company serve a very special role in the mining industry, one that many investors fail to realize the significance of. For example, as evidenced in the chart above, many gold royalty companies have outperformed the yellow metal itself.

They have a robust business model and their ability to generate revenue in times when the gold (or other previous metal) price is both rising and falling is what makes them attractive.

I look forward to Pierre joining our upcoming webcast on opportunities in the space on October 31, in collaboration with ETF Trends.

Back to Buffett: He’s No Stranger to Silver

|

Buffet, an infamous gold bear, was actually a silver bull for a time. The Midwest, where Buffett is from, has a historical affinity for silver over gold. In 1997 and 1998 Buffet and Berkshire amassed a record silver stockpile of 129.7 million ounces, which actually caused a shortage of the metal and drove up lease rates. In the 1998 Berkshire Hathaway letter to shareholders, Buffet wrote that in the prior year the company’s silver position “produced a pre-tax gain of $97.4 million for us.”

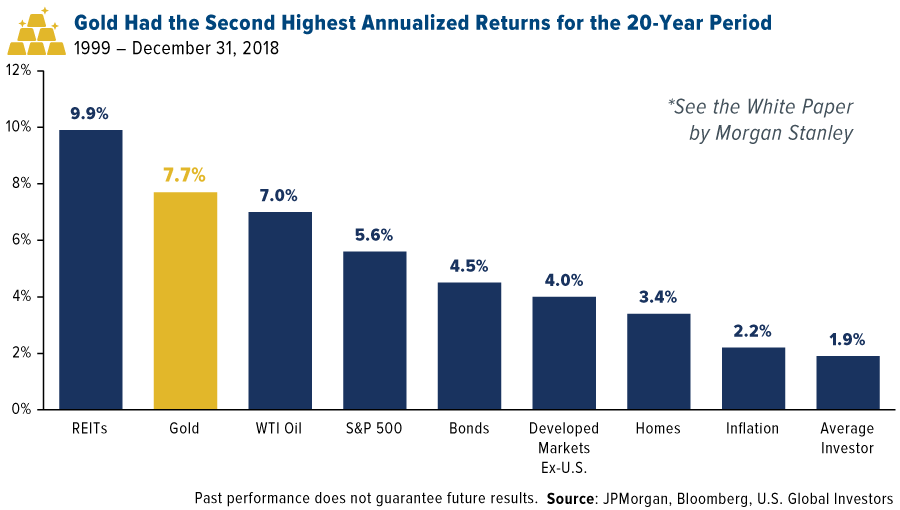

Buffet bought silver when it was under $5 an ounce and sold around the $13 mark in 2006. Turns out Buffet was early to sell, as silver hit its peak of $50 just a few years later in 2011. Why make a big bet on silver and shy away from gold? Especially since gold has been the second best performing asset class, behind REITs, for the 20 year period. Perhaps Buffett will rethink his strategy.

Granted, gold saw an unusually strong rally in the 2000s, while equities were knocked down hard during the dotcom bubble and financial crisis.

But that’s precisely my point. Those who had the prudence to diversify their portfolios during this period—and not just in gold but also bonds, real estate and more—were in much better shape than some other investors.

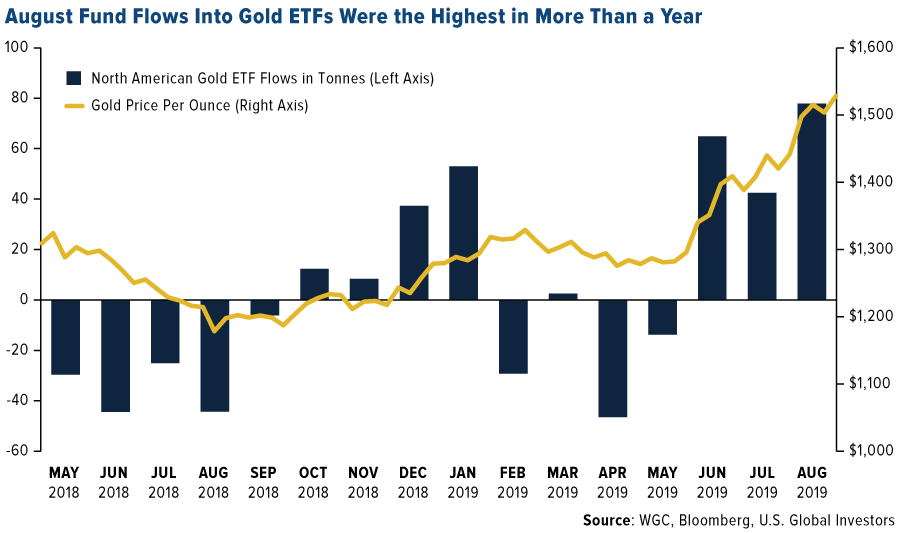

We’re seeing greater appetite for gold and gold-backed investments right now as concerns of a global economic slowdown gain momentum. Not only has the price of gold been up for five of the past six months—it’s down so far in September—but August fund flows into bullion-backed ETFs were the highest in more than a year. North American gold ETFs rose by nearly 78 tonnes (2.7 million ounces) last month, totaling 122.3 tonnes worldwide, according to the World Gold Council (WGC).

In India, gold ETFs attracted the most money in more than six years “as investors poured in money seeking safe havens amid record high domestic prices and a slowdown in the economy,” Bloomberg reports this week. August net inflows rose to 1.45 billion rupees ($20 million), the most since December 2012.

Russia’s Gold Stash Is Now Worth More Than $100 Billion

Retail investors aren’t the only ones in accumulating mode. Central banks, led by those in China and Russia, continue to load up on the yellow metal to diversify away from the U.S. dollar. Russia has quadrupled its gold reserves in the past decade, according to Bloomberg, and in the past year the reserves’ value has jumped 42 percent to $109.5 billion.

“There is a massive substitution of U.S. dollar assets by gold—a strategy which has earned billions of dollars for the Bank of Russia just within several months,” comments Vladimir Miklashevsky, a strategist at Danske Bank.

Meanwhile, China has added some 100 tonnes of gold to its reserves since it resumed purchases in December as a way to hedge against the trade war with the U.S.

I’ve made this point before, but it’s worth repeating: China’s official gold holdings represent only 2.8 percent of its foreign reserves as of this month. This is one of the lowest percentages among world banks. Gold held by the U.S., by comparison, represents more than three quarters of its total foreign reserves. What this means is that the People’s Bank of China (PBOC) still has mountains of gold to buy before its finances are adequately diversified. I can see China’s activity lending support for the price of gold for a long time to come.

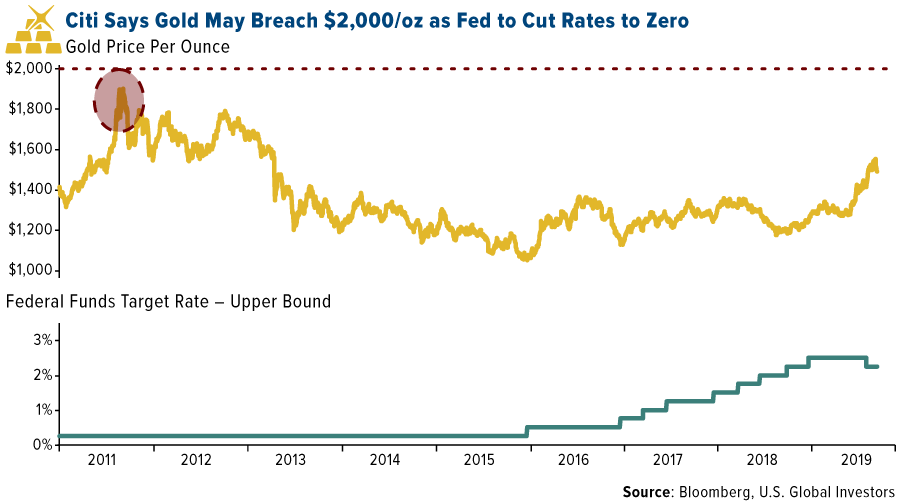

Citigroup: Gold Could Hit $2,000 “in the Next Year or Two”

Speaking of support, perceived risks of a global recession and the likelihood that the Federal Reserve will lower rates to 0 percent could be enough to push gold up to a record $2,000 an ounce, according to Citigroup.

“We expect spot gold prices to trade stronger for longer, possibly breaching $2,000 an ounce and posting new cyclical highs at some point in the next year or two,” Citi analyst Aakash Doshi wrote in a note dated September 10, and reported by Bloomberg.

I agree with Citi’s projection. This very week I joined fellow goldwatchers Peter Schiff and Imaru Cassanova on Liz Claman’s Countdown to the Close, and I pointed out that gold is looking more and more attractive as central banks pursue easy money policies. When governments offer you a negative rate of return, that automatically makes gold much more appealing. What’s more, I think this easing cycle has just begun.

You can watch the full interview by clicking here.

Cornerstone: Regulatory Costs “Would Go Up Sharply Under Democrats”

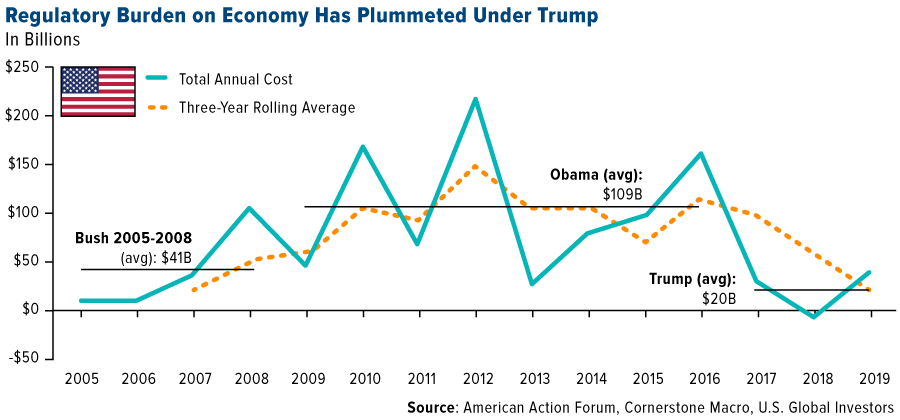

On a final note, Cornerstone Macro sent out an eye-opening note this week that details what might happen to regulatory costs on the private sector should one of the Democrats manage to win the White House in 2020. Spoiler alert: They would likely rise.

According to Cornerstone analysts, the creation of new regulatory costs are significantly down under Trump, who made deregulation a major campaign promise. Since Trump’s inauguration in January 2017, new government rules have added $20 billion on average per year. That might sound like a lot, but it’s 82 percent less than the $109 billion on average that were created every year during Barack Obama’s presidency.

There are some serious implications here, Cornerstone points out.

“If Democrats win the White House next year, the regulatory burden is likely to be at least as high as it was under Obama even if a relatively more moderate Democrat wins the nomination and Democrats don’t have the votes in the Senate to pass new legislation,” Cornerstone says. “Under the right conditions, the regulatory costs could be considerably higher than they were under Obama.”

Where are the conservative Democrats when you need them versus the radical Democrats? As I heard at a dinner recently in New York at the Cornerstone conference, the radical Democrats appear to push European socialist ideals as a new rule or regulation.

As we state in all of our prospectuses here at U.S. Global Investors, government policy is a precursor to change. Cornerstone says that there’s growing support among Democratic presidential contenders for a more aggressive approach to antitrust enforcement and criminal prosecutions of companies and top corporate leaders. Some have called for revitalized organized labor.

I’m not bringing any of this up to be partisan. We’re more concerned about government policy than politics. But I think investors should be aware of the potential for higher costs to U.S. businesses in the coming months.

For these reasons I like to remind investors to pay attention not only to gold, but also to tax-free, short-term municipal bonds, as I believe they remain the best place to park your cash.

Are you following my award-winning CEO blog, Frank Talk? Click here to subscribe.

Gold Market

This week spot gold closed at $1,487.86, down $18.85 per ounce, or 1.25 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 6.51 percent. The S&P/TSX Venture Index came in up just 0.11 percent. The U.S. Trade-Weighted Dollar fell 0.22 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-11 | PPI Final Demand YoY | 1.70% | 1.80% | 1.70% |

| Sep-12 | Germany CPI YoY | 1.40% | 1.40% | 1.40% |

| Sep-12 | ECB Main Refinancing Rate | 0.00% | 0.00% | 0.00% |

| Sep-12 | CPI YoY | 1.80% | 1.70% | 1.80% |

| Sep-12 | Initial Jobless Claims | 215K | 204K | 217K |

| Sep-15 | China Retail Sales YoY | 7.90% | — | 7.60% |

| Sep-17 | Germany ZEW Survey Current Situation | -15 | — | -13.5 |

| Sep-17 | Germany ZEW Survey Expectations | -37.8 | — | -44.1 |

| Sep-18 | Eurozone CPI Core YoY | 0.90% | — | 0.90% |

| Sep-18 | Housing Starts | 1250 | — | 1191k |

| Sep-18 | FOMC Rate Decision (Upper Bound) | 2.00% | — | 2.25% |

| Sep-19 | Initial Jobless Claims | 215k | — | 204k |

Strengths

- The best performing metal this week was palladium, up 4.41 percent. Central banks continue to stock up on gold – led by Russia, the world’s top buyer for seven consecutive years. Russia’s central bank quadrupled its gold holdings in the last decade and has diversified away from U.S. assets. According to Bloomberg, the value of the nation’s gold surged 42 percent in the past year to $109.5 billion due to higher prices. Russia is also a top miner and saw its gold production rise 11 percent in the first half of 2019 from the same period last year to 142.2 tons. China is also growing its gold reserves. The People’s Bank of China (PBOC) has raised its bullion holdings for a ninth consecutive month, adding 5.91 tons in August, reports Bloomberg.

- Although gold demand in India is down due to higher prices, demand for gold ETFs is rising. Inflows into gold ETFs were the highest in six years in August at 1.45 billion rupees, or $20 million, according to the Association of Mutual Funds in India. N.S. Venkatesh, CEO of AMFI, said that the increase in gold prices might have influenced investors to think it is good to invest in paper gold rather than the physical metal.

- The World Gold Council (WGC) released a list of Responsible Gold Mining Principles that companies need to follow if they want to be recognized for responsible mining, which is of growing importance to shareholders and consumers. It is a list of 10 principals aimed at improving environmental, social and governance strategies of mining companies. Terry Heymann, chief financial officer, told Kitco News in an interview that “this is a significant collective achievement for the mining sector and sets out clear expectations for the investment community.”

Weaknesses

- The worst performing metal this week was silver, down 3.94 percent. After a big price swing to below $1,500 an ounce and three back-to-back weeks of losses, some investors are doubting gold’s rally. Last Friday the yellow metal fell to a two-week low just two days after hitting a six-year high. Gold ended this week down 1.29 percent. Bloomberg reports that a measure of 60-day volatility in gold futures climbed to the highest since February 2017. On Monday bullion futures fell as much as 1.1 percent, but then rose slightly on Thursday after the ECB announced cuts to eurozone interest rates.

- According to a report by law firm Bryan Cave Leighton Paisner, private equity investments in the gold mining space fell by 29 percent in the first half of 2019 to $149 million from a year earlier. The data shows that there were just nine private equity deals in the time period, which is down from 13 years ago.

- Continued unrest and protests in Hong Kong are hurting its reputation as the main physical gateway of gold to China, which is the world’s largest consumer. Reuters reports that the geopolitical situation is spooking tourists and subduing jewelry sales due to concerns of how to ship gold out of the city. J. Robart & Co., A Hong-Kong based bullion house, said that “on the individual investor level, we see more clients opting to store their gold in what they consider as safer jurisdictions.”

Opportunities

- The U.K.’s Royal Mint Ltd. is planning to launch a gold ETF in early 2020 in response to rising demand from investors. The Financial Times reports that this would be the first time in its history that the Royal Mint would offer a financial product traded on a stock exchange, and would be the first European sovereign mint to launch a gold-backed exchange-traded commodity. The ETF will be structured as an exchange-traded commodity (ETC), which is a debt security backed by gold stored in the mint’s vault.

- Citigroup came out with a bullish prediction for gold. Analysts, including Aakash Doshi, said in a note this week that “we expect gold prices to trade stronger for longer, possibly breaching $2,000 an ounce and posting new cyclical highs at some point in the next year or two.” Citigroup says the bold price forecast is driven by factors such as lower nominal and real interest rates, escalating global recession risks, strong central bank gold demand and more.

- On Wednesday President Donald Trump tweeted “the Federal Reserve should get our interest rates down to ZERO, or less, and we should then start to refinance our debt.” President Trump has been critical of the Fed for not lowering interest rates faster, which he sees as necessary to boosting U.S. economic growth, reports Reuters. Historically, lower interest rates have been positive for the price of gold.

Threats

- As discussed above, Citigroup thinks gold could soon top its record high and hit $2,000 an ounce. However, this would be bad for diamonds, according to Citigroup’s Barry Ehrlich. The analyst wrote that compared to gold, diamonds are an inferior store of wealth and are unlikely to benefit from investor flight from fiat currencies into safer havens. Ehrlich added that a weaker global and U.S. economy would hurt demand for diamonds, because a healthy diamond market requires a healthy middle-class consumer, reports Bloomberg.

- CNBC’s Jim Cramer said this week that the migration of money from stocks to safe haven assets, such as gold and bonds, could reach a tipping point. On the Mad Money show, chart analyst Carley Garner says that it’s time for both bond and gold prices to come down, since the number of buyers are running out. Garner added that gold is reaching the overbought territory and that “overbought levels are usually the beginning of the end for a rally.”

- The London Metal Exchange (LME) released plans to allow extended queues for loading out metals, which will enable warehouses to boost profits by holding metals for longer, but consumers will face higher costs as a result, Pratima Desai from Reuters reports. An aluminum consuming firm said “this will help the warehouses improve revenues, but for us it means more expensive metal.” This could potentially hurt consumption if prices rise for consumers.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.58 percent. The S&P 500 Stock Index rose 0.96 percent, while the Nasdaq Composite climbed 0.91 percent. The Russell 2000 small capitalization index gained 4.85 percent this week.

- The Hang Seng Composite gained 2.32 percent this week; while Taiwan was up 0.44 percent and the KOSPI rose 1.99 percent.

- The 10-year Treasury bond yield rose 34 basis points to 1.90 percent.

Domestic Equity Market

Strengths

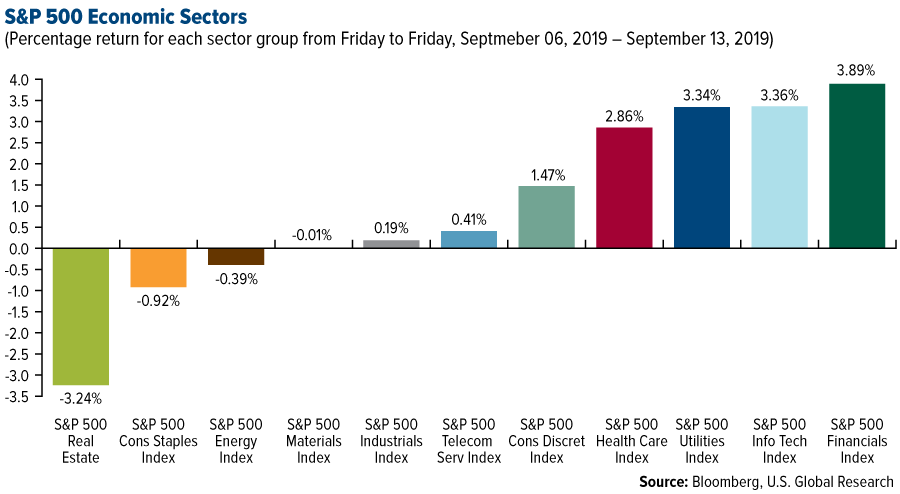

- Financials was the best performing sector of the week, increasing by 3.89 percent versus an overall increase of 0.99 percent for the S&P 500.

- LKQ Corp was the best performing stock for the week, increasing 21.71 percent.

- LKQ’s stock rose 12 percent after an activist investor disclosed that it had taken a substantial stake in the automobile parts company. ValueAct Capital revealed in a U.S. Securities and Exchange Commission filing that it had purchased more than 5 percent of LKQ’s outstanding shares, and the filing included typical language indicating its interest in discussing issues with LKQ management.

Weaknesses

- Real estate was the worst performing sector for the week, decreasing by 3.24 percent versus an overall increase of 0.99 percent for the S&P 500.

- MarketAxess Holdings was the worst performing stock for the week, falling 21.25 percent.

- Moody’s downgraded Ford to “junk” status amid a massive restructuring, reports Business Insider. The credit ratings agency slated Ford’s financial outlook for the year ahead, citing weak earnings and poor cash generation.

Opportunities

- Apple announced three new iPhones at its event on Tuesday: the iPhone 11, iPhone 11 Pro, and iPhone 11 Pro Max. The new iPhones retain their same prices as last year’s designs, but Apple made some significant improvements to each of its top-of-the-line phones. Apple also unveiled the Apple Watch Series 5, which comes in new titanium and ceramic casings and has an always-on display.

- Peloton plans to raise as much as $1.3 billion in an IPO that would double its valuation to $8 billion, reads one Business Inside headline. The maker of internet connected fitness equipment said it intends to sell 40 million Class A shares in the offering.

- The world’s largest brewer, Anheuser-Busch InBev , which shelved a Hong Kong IPO of its Asia Pacific unit in July, is planning to raise about $5 billion from a revived float, people with knowledge of the matter said. It is tentatively looking to price the deal on September 23 and list the unit on September 30, one source said.

Threats

- Fifty state attorneys general have launched an investigation into whether Google has engaged in anticompetitive practices in its ads business. The investigation, announced on Monday from the steps of the Supreme Court in Washington, DC, is being led by Texas Attorney General Ken Paxton.

- California approved a landmark bill to reclassify contractors for companies like Uber and Lyft as employees. The Assembly Bill 5 passed in a 29 to 11 vote in the State Senate and now heads to the State Assembly for passage.

- Alibaba is set for “big challenge,” reports Reuters, as flamboyant chairman Ma departs on Tuesday. Ma will be leaving his handpicked successor a daunting task of steering the $460 billion juggernaut at a time when the market for its core e-commerce business has slowed sharply.

The Economy and Bond Market

Strengths

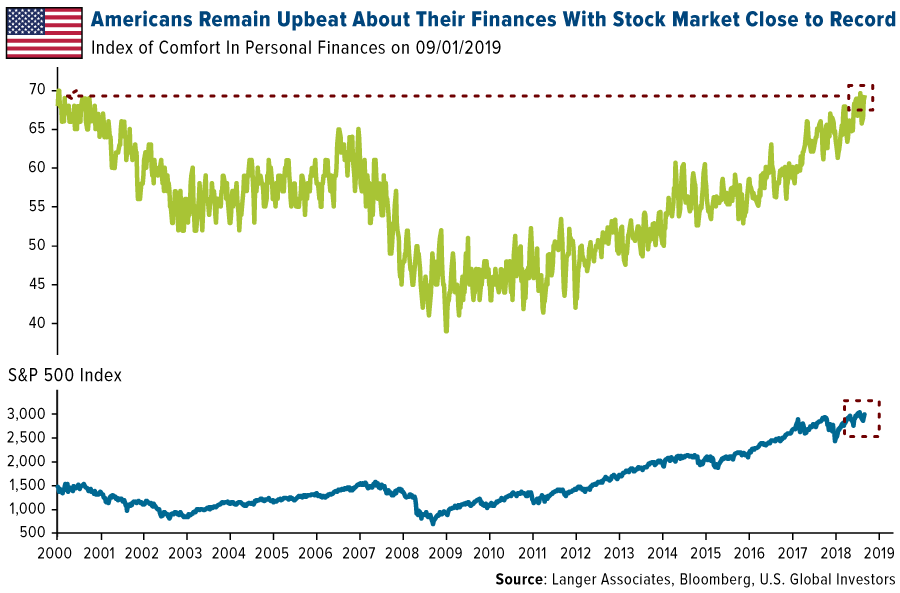

- Americans are cheerful about their finances, according to Bloomberg. Against a backdrop of elevated stocks and steady growth in pay, respondents in Bloomberg’s most-recent report on consumer comfort showed a gauge of sentiment about personal finances advanced in the final week of August to the second-highest level since 2000. Such optimism has the potential of sustaining a robust pace of consumer spending that has been carrying the load for the U.S. economy as businesses contend with the fallout from weaker global demand, trade disputes and lackluster capital investment.

- U.S. retail sales advanced in August by more than forecast, writes Investors.com, as Americans hit auto showrooms and kept shopping online, signaling consumers will continue to buoy an economy beset by risks from trade and global weakness. The value of overall sales rose 0.4 percent from the prior month, Commerce Department figures showed Friday.

- The fewest Americans in almost five months filed for unemployment benefits last week, signaling the broad labor market remains healthy despite a slowdown in some parts of the economy. Jobless claims dropped by 15,000 to 204,000 in the week ended September 7, according to Labor Department figures.

Weaknesses

- Treasuries extended their September tumble, sending the benchmark 10-year yield to its highest level since early August, amid stronger-than-expected U.S. economic data. The 10-year yield ended the week at 1.90 percent, up from 1.46 percent at the end of August.

- A measure of underlying U.S. inflation accelerated by more than forecast to a one-year high in August, writes Bloomberg, signaling inflation was already firming ahead of fresh tariffs on Chinese goods this month that may push prices higher for Americans. The core consumer price index, which excludes food and energy, rose 0.3 percent from the prior month and was up 2.4 percent from a year earlier, a Labor Department report showed Thursday.

- President Donald Trump’s trade barriers are driving up prices for U.S. solar power and holding back development, according to Kevin Smith, Lightsource BP’s chief executive officer for the Americas. The San Francisco-based solar developer is paying as much as 60 percent more for solar panels it’s using in the U.S., compared with costs for projects in other parts of the world, Smith said.

Opportunities

- Trump said Thursday that he will delay tariffs on China a day after China removed some of its own — but "it does not mean an end to the trade war." China removed tariffs on 16 American exports on Wednesday. China also said it is encouraging companies to buy U.S. farm products including soybeans and pork, and will exclude those commodities from additional tariffs, in the latest move to ease tensions before the two sides resume trade talks. The Commerce Ministry’s announcement on Friday follows a move earlier this week to exempt a range of American goods from 25 percent extra tariffs put in place last year, as the government seeks to lessen the impact from the trade war.

- U.S. consumer sentiment rebounded in September after a steep drop, reports Bloomberg, signaling that consumers may be poised to keep powering the economic expansion despite gathering uncertainties. The University of Michigan’s preliminary sentiment index rose to 92 from a nearly three-year low of 89.8 in August, data showed Friday.

- In a busy week for central banks, the Fed’s meeting will be the highlight for most traders. The U.S. central bank is widely anticipated to lower the federal funds rate by 25 basis points to a target range of 1.75-2.00 percent on Wednesday.

Threats

- Tuesday’s industrial production numbers for August will be monitored as a gauge of the continued impact from the US-China trade war. July’s industrial production fell 0.2 percent.

- As Bloomberg reports, the likelihood of U.S. recession before the 2020 election has grown, based on changes in the Treasury yield curve, according to Jeffrey Gundlach, the chief executive officer of DoubleLine Capital. “We should be on recession watch before the 2020 election,” Gundlach said Thursday in London. “We’re getting closer but we’re not there yet.” The odds of a U.S. recession before the election are 75%, said Gundlach, reiterating a prediction he made in August.

- Fuel shortages, bankrupted businesses, and riots: those are the official UK government forecasts during a no-deal Brexit chaos, reports Business Insider. A five-page planning document detailing the government’s "planning assumptions" was released under Operation Yellowhammer, the government’s no-deal Brexit plan, after opposition lawmakers passed a motion on Monday compelling it to do so.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was iron, which gained 6.77 percent. Iron ore surged early this week after China announced stimulus measures. The People’s Bank of China says that it will cut the amount of cash banks must hold as reserves to the lowest level since 2007, which will release $126 billion of liquidity. China, the world’s top iron consumer for steel production, saw its imports of the metal jump in August to 94.85 million tons.

- Suncor Energy Inc. announced that it plans to spend $1.1 billion to make its Oil Sands Base Plant more efficient. The company, Canada’s largest oil sands producer, will build two electricity-making cogeneration units that use heat from the base plant’s existing operations to add 800 megawatts of generating capacity and reduce greenhouse emissions, according to CEO Mark Little. “We found a great investment that gets very good returns for shareholders and makes a sizable reduction in environmental effects.”

- BP Plc said that it will install permanent methane detection devices at its new projects, solving an issue that has long been dogged by the energy industry, reports Bloomberg. The devices will be able to immediately pinpoint and quantify leaks of natural gas, which is invisible and odorless. BP says that the wider industry leaks around 3.2 percent of the gas it produces.

Weaknesses

- The worst performing major commodity for the week was silver, which fell 3.94 percent. Oil had a volatile week, falling 2.81 percent, and some traders are frustrated by the uncertainty in what will drive oil prices in either direction. Crude oil plunged as much a 1 percent early this week after President Trump fired one of his most hawkish advisors, national security advisor John Bolton. The International Energy Agency (IEA) cut its forecast for global oil demand growth, again. The new forecast is 10 percent lower than the previous one, citing the economic impact of the U.S.-China trade war. IEA executive director Faith Birol said in an interview with BloombergTV that demand this year will average about 1 million barrels a day of growth.

- Another battery metal is taking a beating after demand for electrics vehicles in China slowed after subsidies were removed, reports Bloomberg. Graphite, which is used in steelmaking and for anodes in vehicles batteries, has fallen 19 percent so far this year and is trading at a more than two-year low, according to Asian Metal Inc. data. Syrah, a top producer of the metal, saw its shares fall 33 percent after it announced plans to curb output from the world’s biggest graphite mine in response to lower prices.

- Major commodity producer Indonesia is considering more export curbs after recently announcing a ban on iron ore. The nation is studying bringing forward bans on other minerals, including bauxite, reports Bloomberg. Indonesia is trying to squeeze more value out of its massive mineral deposits by creating local processing capacity, rather than exporting all its ore for processing abroad.

Opportunities

- Some positive progress was made in the U.S.-China trade war this week with both countries making conciliatory gestures ahead of a new round of negotiations, which could be positive for oil and other commodities. Reuters reports that China is renewing purchases of U.S. farm goods while President Trump delayed a tariff increase on certain Chinese goods. Stephen Brennock from broker PVM said “the upshot is that no further deterioration in the economic environment is expected, hence the downside for oil prices should be limited in the near term.”

- SQM, a top lithium producer, is bullish on the metal. CEO Ricardo Ramos said in a presentation this week that they see lithium prices at $10,000 to $15,000 per ton through 2025 and that the outlook for demand and supply is very positive. The company expects its Chilean output to grow to 150,000 tons by 2025, up from 46,800 tons over the last 12 months. Company shares rose as much as 3.8 percent on Tuesday on the positive outlook.

- Gold has been in the spotlight as of late, but other precious metals are making big moves too, specifically silver and platinum. Bloomberg’s Justina Vasquez writes that “investors looking for cheaper entry into havens have helped widen the rally to silver and platinum, which surged in the past few weeks to approach or surpass gold’s 2019 gains.” Silver has surged more than 4 percent since mid-August and gold has fallen. However, as seen in the chart below, silver is still cheap relative to the yellow metal, with the ratio below the historical average of 67. Citigroup is bullish on platinum and predicts that the metal will rally to $1,000 an ounce next year due to improvement in automotive demand.

Threats

- News came out this week that France’s nuclear plants may contain sub-standard parts, sending buyers on a spree of natural gas. In previous years problems with French reactors have kept many out of service for months. Bloomberg reports that the electricity from 58 reactors is essential to the region’s supply and is exported to major markets such as Germany and Britain. Both French and German power prices for the next quarter rose to the most on record, even though operator Electricite de France SA didn’t actually say that the reactors would be halted.

- In other energy headwinds, natural gas-fired plants will soon be undercut by renewable power. Bloomberg reports that by 2035 it will be more expensive to run 90 percent of gas plants than it will be to build new wind and solar farms equipment with storage systems. Natural gas just recently crushed the economics of coal, which is bad news for new natural gas projects underway.

- Although some progress was made on the trade war this week, American farmers are still frustrated. At President Trump’s direction, the Department of Agriculture has given out $28 billion in aid to farmers hurt by slowed demand out of China for their crops. However, the varying payouts have confused and irritated farmers nationwide, according to Reuters interviews. In the second round of payouts the rules changed and now payouts are based on the estimated impact of trade policy – regardless of what an individual farmer actually plants.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 4.1 percent. The central bank cut its main interest rate by another 325 basis points, after a 425 basis point cut back in July. Moreover, President Donald Trump’s decision this week to fire national security advisor John Bolton could be positive for Turkey and the region, as geopolitical tensions are likely to ease.

- The Russian ruble was the best performing currency this week, gaining 2.3 percent against the dollar. While central banks are turning more dovish around the world, the ruble is attracting carry traders searching for higher yielding investments. Two-year Russian government bonds pay around 6.5 percent with inflation only at 4.3 percent. Russia lures investors with a 2 percent real rate, while real rates in other central European countries are negative.

- Consumer staples was the best performing sector among eastern European markets this week. Eurocash, a Polish retailer, was the best preforming equity, gaining more than 6 percent.

Weaknesses

- Greece was the worst performing country this week, losing 1.4 percent. Industrial production declined by 2.1 percent in July, suggesting a slowdown in economic activity. However, most analysts predict that Greek GDP will reach 3 percent in 2020. Wood & Company research team believes that Greece will remain a great reform story with significant upside on the macro level and that lower taxes will soon be announced.

- Hungarian forint was the worst relative performing currency in the region this week, gaining 25 basis points. All emerging Europe currencies appreciated against the U.S. dollar, but the forint recorded the smallest gains among its peers after the European Central Bank (ECB) announced more stimulus. The ECB’s cut in the deposit rate by another 10 basis points did not surprise the market, but the open-ended quantitative easing program was not expected.

- Health care was the worst performing sector among eastern European markets this week. Richter Gedeon NYRT, a Hungarian pharmaceutical producer and distributor, was the worst preforming equity losing more than 3 percent.

Opportunities

- As mentioned above, the ECB delivered a dovish message this week. The bank’s deposit rate was cut by 10 basis points to negative 0.5 basis points, a new quantitative easing plan was restarted at a pace of 20 billion euros per month and a tiering system for banks was announced. Banks will be charged negative rates on only a portion of their deposits at the ECB. More stimulus should help the eurozone economy to recover and move inflation to a higher level.

- Ahead of October’s elections, the Polish government announced a plan to nearly double minimum wages. The minimum wage is set to rise 78 percent to 4,000 zloty (or USD 1,017) at the end of 2023. Adjusted for local price levels, minimum wages are already near those in Spain and the U.S., surpassing those in Hungary and Greece.

- Ukraine and Russia completed a large prisoner exchange this week, which is a potential step that could ease tensions between Moscow and Kiev. 70 prisoners were involved, 35 on each side, including 24 Ukrainian sailors who were detained when their ships were seized in 2018 in the Kerch Strait between Crimea and the Russian mainland.

Threats

- On September 8, Russians voted in local and regional elections where Russia’s ruling party lost multiple seats. United Russia party, which supports Russian President Vladimir Putin, retained its majority of 25 seats in the council, but lost as many as 13 to members of the Communist Party, three to members of “A Just Russia” party and four to members of the liberal Yabloko party. Dissatisfaction with the current ruling party is becoming more visible.

- The ECB cut the deposit rate by another 10 basis points to negative 0.5 percent, which means that banks will have to pay the additional 10 basis points or total of 50 basis points for depositing funds overnight. Negative rates penalize banks for holding cash rather than lending it out. With low demand for loans in the eurozone, banks will have to pay higher fees for parking their excess capital overnight and book higher operational costs.

- The International Energy Agency (IEA) said that growing surplus in the oil market next year will push prices lower. The IEA monthly report said that while the oil market would face a small deficit in the second half of this year, supplies were expected to surge later in 2019 and into 2020. Weaker prices of oil will have a negative effect on Russia as it is the country’s main source of revenue.

China Region

Strengths

- The best performing indices in the region for the week were Hong Kong’s Hang Seng Composite, which climbed 2.32 percent, and Singapore’s FTSE Straits Times Total Return Index, which rose 2.16 percent. China, Taiwan and South Korea were closed later in the week for mid-autumn Festival/Harvest Moon Festival.

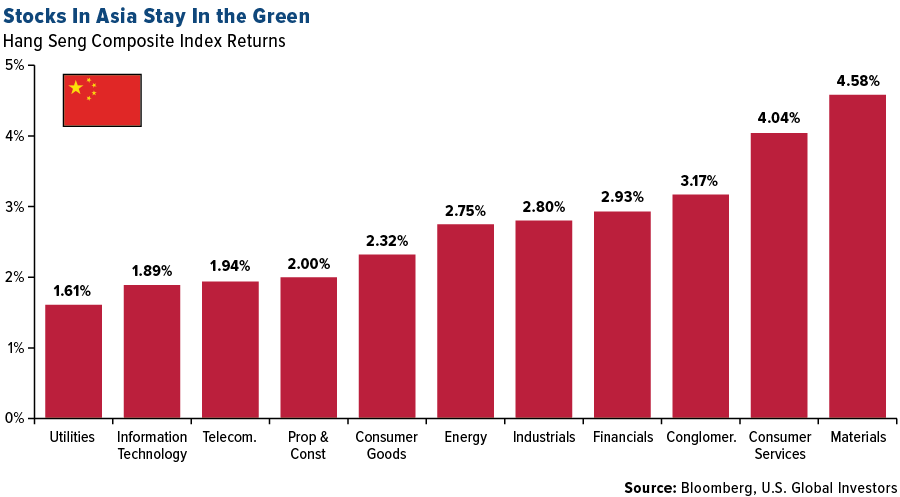

- The best-performing sector in Hong Kong’s Hang Seng Composite Index was materials, which jumped 4.58 percent in a week that saw all HSCI sectors up in the green. Look and see for yourself; it’s all so lush-looking.

- China’s FX reserves number clocked in at a steady $3.107 trillion in August, up from $3.104 trillion in July, coming in slightly above consensus and indicating that outflows—even amid relative yuan weakness for some of that period—are not yet an immediately pressing concern.

Weaknesses

- The worst performing indices in the region were Thailand’s SET Index, which declined by 39 basis points, and Malaysia’s KLCI, which dropped by 15 basis points.

- The laggard sector in Hong Kong’s Hang Seng Composite Index this week was utilities, which rose a paltry 1.61 percent over the last five trading days.

- China’s year-over-year exports headed for the United States dropped by 16 percent for the August measurement period, although notably the decline in total shipments was only 1 percent as Chinese exporters found other recipients for their goods. Analysts had been looking for overall growth in China’s exports.

Opportunities

- In what is becoming a weekly comment, one must say again, “Wow, what a difference a week can make!” After Chinese Premier Li Keqiang argued that the U.S. and China should find solutions to the trade spat—which didn’t actually say much or change anything but did sound moderately hopeful (given, of course, that he could have said nothing or made a negative comment), we saw quite a few steps in just that direction. Baby steps, perhaps, but meaningful ones. By the end of the week, the United States offered to delay the October tariff hike until the 15th, post-Chinese holidays and market closures, and in time for the presumed (TBD on specific dates) “high-level” talks between Vice Premier Liu He’s team and the U.S. team. (Could another delay come? Stay tuned.) Additionally, China played ball and offered more exemptions, and by the end of the week, was looking at U.S. pork and soybeans again. To top it off, late in the week, U.S. President Donald Trump suggested that he is amenable to the idea of some sort of “interim deal” with China, and Xinhua issued statements about needing to resume talks again and continue to provide stability and “enhance trust via positive exchanges.” It looks like we’re into the “on” wave in the “on-again, off-again” cycle …

- Bloomberg News reported this week that China’s State Administration of Foreign Exchange announced it was scrapping the global fund quota for Chinese stocks and bonds, continuing to remove formally another hurdle to foreign investment.

- North Korea fired off another couple of missiles and almost simultaneously announced a willingness to meet with the United States. We’ll call it an opportunity, in a bizarre, North Korea sort of way. While the talks do, in some way, appear to have stalled and slowed down, it was not that long ago that we heard a meeting could very well happen in September, and now we have North Korea continuing to state the same thing, albeit from their angle and talking tough, with some rockets for good measure to ensure attention is paid. Given the history prior to previous meetings and summits, the uptick in saber rattling and tweets and headline-grabbing posturing was in many ways simply prelude, and gave way to warm letters and handshakes. One thinks of two barking dogs, circling carefully if loudly, who subsequently, tolerantly, even Instagram-ably wag their tails, and who knows? Maybe even make friends. North Korea will take time, but dialogue remains positive. And should any thaw in international sanctions or relations ever come to North Korea, opportunities will abound as that pariah nation is thereafter reintroduced and plugged in to the big, broad, global economic machine.

- Also of note this week is the (now-rejected) HKEX (388 HK) ~$37 billion bid for the LSE, perhaps to be taken as a strong vote of confidence in London’s continued status as a post-Brexit financial powerhouse. Nota bene, global investors, nota bene.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. We must note as well that the positive signaling between the two sides in the U.S.-China trade war are positive and at least demonstrative of a will to engage in further high-level talks and look for some kind of deal. The base case amongst analysts still seems to be, at this point, no deal before 2020—which would almost guarantee a run of headline-y ups and downs on the subject until then—although talks will always run the risk of falling apart. (The up- and flip-side of these looming downside potential scenarios remains, of course, that any deal coming sooner or more-rapidly-than-expected resolution of any uncertainty may swing market sentiment quickly to the upside.) This week saw many positive developments in U.S.-China steps toward October holidays, talks and now-delayed tariffs with more exemptions granted, but October 15th is still a long way away, and the larger question comes with respect to the December tariffs. And there is now an even larger question of what, exactly, any “interim deal” is and whether it would, in fact, solve any of those deeper-seated issues, or simply place band-aids over said issues and punt into 2020.

- As unrest has continued in Hong Kong, the city’s year-over-year tourist arrivals declined by nearly 40 percent for August, marking what Bloomberg News observed was the biggest decline since the SARS outbreak in May 2003. However, note that much other business continues apace—Hong Kong remains “Asia’s World City” until it isn’t—and one does well to remember that media reports and attention on, say, flaming rubbish blocking an entrance to a popular MTR station, can lead one to believe that perhaps the whole city is aflame. It isn’t. But there are issues that remain unresolved at this point amid the protests, and as usual, stay tuned.

- Indonesia’s economic growth could slide below 5 percent next year, The World Bank warned this week, noting the island nation’s possible vulnerabilities amid the trade war and the potential for what it called “severe” outflows.

Blockchain and Digital Currencies

Strengths

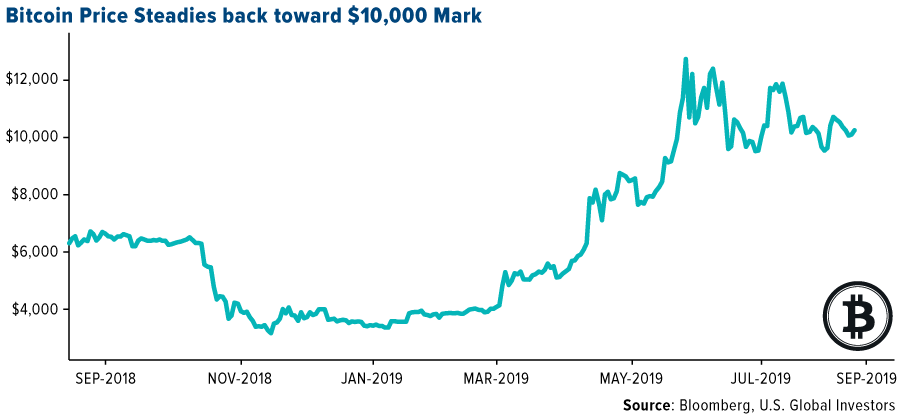

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 13 was Howdoo, up 548.08 percent. Although the price of bitcoin has stalled in the last 10 weeks, the bullish case remains intact with prices hovering well above the historically strong price support, writes CoinDesk.

- The chairman of the Securities and Exchange Commission Jay Clayton told CNBC on Monday that there is progress being made toward a bitcoin exchange-traded fund (ETF), reports MarketWatch. Specifically, when asked whether “the people involved in the bitcoin business…in any way come close to satisfying your concerns,” Clayton said “the short answer is yes, but there’s still work to be done.”

- Binance, the largest crypto exchange by volume, is making its U.S. debut next week, reports CoinDesk. On September 18, Binance.US will open registration and deposits, initiating a rollout of multiple Binance products across America.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 13 was Opennity, down 73.38 percent.

- There is a security hole in various versions of bitcoin’s Lightning Network software that developers are warning could cause users to lose money if not updated, writes CoinDesk. The bug was first made public on August 30 and confirmed on Tuesday afternoon. Although it is unclear how much bitcoin, if any, was lost, CTO of Lightning Labs Olaoluwa Osuntokun warned that multiple Lightning node versions are vulnerable and should be updated immediately.

- The finance minister of France has said the nation will block Facebook’s Libra cryptocurrency in the European Union, reports CoinDesk, over concerns that it poses a threat to the sovereignty of national currencies. “I want to be absolutely clear: In these conditions, we cannot authorize the development of Libra on European soil,” Bruno Le Maire, Economy and Finance Minister of France said.

Opportunities

- On Wednesday, MasterCard announced plans to develop a blockchain-powered cross-border payments platform in partnership with enterprise-focused blockchain firm R3, writes CoinDesk. The payments solution will be backed by MasterCard’s clearing and settlement network, aiming to connect faster payment schemes and banks.

- Coinbase may soon be launching an initial exchange offering (IEO), reports CoinDesk. The cryptocurrency exchange’s head of institutional sales in Asia, Kayvon Pirestani, told a panel on Wednesday that “In a nutshell, Coinbase is carefully exploring not only the IEO space, but also the STOs (security token offerings), but I can’t make any formal announcements right now.”

- A new report from PxC shows that more and more fundraising and M&A deals in the digital currency space are now happening in Asia and Europe, reports CoinDesk, surpassing the previously dominant role of the Americas. A portion of the firm’s analysis found that 41 percent of global fundraising deals in the second quarter of this year took place in Europe.

Threats

- As Facebook continues the development of its Libra cryptocurrency, the social media giant has informed U.S. senators what the initial basket of currencies will be that back Libra. This likely includes the U.S. dollar, euro, yen, British pound and Singapore dollar. China has encouraged governments to include its currency in their reserve holdings, but Virginia Democratic Senator Mark Warner has asked Facebook to commit to excluding it from the Libra basket. Warner says China wants stability to its currency, which many feel the government manipulates.

- Estate planning experts are warning cryptocurrency users to make a plan for digital assets, reports MarketWatch, stating that they may well disappear without a trace if there is no plan to pass them along. The article goes on to explain that investors should appoint a “digital executor” that could be the same person who settles the rest of your estate.

- Although bitcoin recovered from nine-day lows mid –week, CoinDesk reports that sellers still need to observe caution, as the recent pullback lacks volume support and may prove a bear trap.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 235.68 | -12.40 | -5.00% |

| Gold Futures | 1,495.40 | -20.10 | -1.33% |

| Natural Gas Futures | 2.62 | +0.13 | +5.01% |

| S&P/TSX VENTURE COMP IDX | 589.16 | +0.65 | +0.11% |

| 10-Yr Treasury Bond | 1.90 | +0.34 | +21.91% |

| Nasdaq | 8,176.71 | +73.64 | +0.91% |

| Oil Futures | 54.95 | -1.57 | -2.78% |

| Hang Seng Composite Index | 3,672.61 | +83.30 | +2.32% |

| S&P 500 | 3,007.39 | +28.68 | +0.96% |

| DJIA | 27,219.52 | +422.06 | +1.58% |

| Korean KOSPI Index | 2,049.20 | +40.07 | +1.99% |

| Russell 2000 | 1,578.14 | +72.97 | +4.85% |

| S&P Energy | 447.81 | +14.57 | +3.36% |

| S&P Basic Materials | 369.31 | +11.93 | +3.34% |

| XAU | 89.49 | -4.77 | -5.06% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.62 | +0.48 | +22.31% |

| S&P/TSX Global Gold Index | 235.68 | -12.73 | -5.12% |

| 10-Yr Treasury Bond | 1.90 | +0.32 | +20.44% |

| Oil Futures | 54.95 | -0.28 | -0.51% |

| Gold Futures | 1,495.40 | -32.40 | -2.12% |

| S&P 500 | 3,007.39 | +166.79 | +5.87% |

| S&P Energy | 447.81 | +31.54 | +7.58% |

| Hang Seng Composite Index | 3,672.61 | +275.12 | +8.10% |

| DJIA | 27,219.52 | +1,740.10 | +6.83% |

| Korean KOSPI Index | 2,049.20 | +110.83 | +5.72% |

| Nasdaq | 8,176.71 | +402.77 | +5.18% |

| S&P Basic Materials | 369.31 | +21.06 | +6.05% |

| Russell 2000 | 1,578.14 | +110.62 | +7.54% |

| S&P/TSX VENTURE COMP IDX | 589.16 | +11.47 | +1.99% |

| XAU | 89.49 | -3.42 | -3.68% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.62 | +0.30 | +12.73% |

| 10-Yr Treasury Bond | 1.90 | -0.19 | -9.21% |

| DJIA | 27,219.52 | +1,112.75 | +4.26% |

| Oil Futures | 54.95 | +2.67 | +5.11% |

| S&P 500 | 3,007.39 | +115.75 | +4.00% |

| Gold Futures | 1,495.40 | +140.30 | +10.35% |

| S&P Energy | 447.81 | -3.00 | -0.67% |

| Nasdaq | 8,176.71 | +339.58 | +4.33% |

| Korean KOSPI Index | 2,049.20 | -53.95 | -2.57% |

| S&P Basic Materials | 369.31 | +6.63 | +1.83% |

| Russell 2000 | 1,578.14 | +42.33 | +2.76% |

| Hang Seng Composite Index | 3,672.61 | +24.62 | +0.67% |

| S&P/TSX Global Gold Index | 235.68 | +32.23 | +15.84% |

| S&P/TSX VENTURE COMP IDX | 589.16 | -0.08 | -0.01% |

| XAU | 89.49 | +13.50 | +17.77% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2019):

Franco-Nevada Corp.

Eurocash SA

Suncor Energy Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Kuala Lumpur Stock Exchange Composite Index (KLCI) is a broad-based capitalization-weighted index of 100 stocks designed to measure the performance of the Kuala Lumpur Stock Exchange. The Straits Times Index comprises the top 30 SGX Mainboard listed companies on the Singapore Exchange selected by full market capitalization. The Bangkok SET Index is a capitalization-weighted index of all the stocks traded on the Stock Exchange of Thailand. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money.