New Beginnings With the Year of the Rat

Date Posted: January 24, 2020

Read time: 53 min

It's been a whirlwind couple of weeks! From Switzerland to Vancouver to Boston, I went from being student to teacher. I'm grateful for the opportunity to learn from others and to share my own story.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

It’s been a whirlwind couple of weeks! From Switzerland to Vancouver to Boston, I went from being student to teacher. I’m grateful for the opportunity to learn from others and to share my own story.

As I told you in last week’s Investor Alert, I attended the Crypto Finance Conference in St. Moritz, Switzerland, where I got to hear from not just the Winklevoss twins but also Arthur Hayes, cofounder and CEO of cryptocurrency exchange BitMEX.

Arthur has such an inspirational story. A graduate of Wharton School of Business, he moved to Hong Kong to work as an equity derivatives trader and market-maker. After losing his job in 2013, the 33-year-old decided he was done with banking and turned his sites toward bitcoin—which had just crossed above $1,000 for the first time, ending the year up a remarkable 5,870 percent.

Like any new idea, BitMEX was a longshot. Today it’s one of the biggest crypto exchanges in the world. In the past 12 months, the platform has seen a mindboggling $1.13 trillion in trading volume.

Bullish on Copper and Gold

The next leg of my trip took me to Vancouver, where I was the keynote speaker at the Vancouver Resource Investment Conference (VRIC), attended by more than 4,000 investors. This was the conference’s 25th anniversary.

Sentiment for gold and other key metals was high, with the yellow metal starting the year above $1,500 an ounce for the first time since 2013. As I told Commodity-TV’s Jochen Staiger on the sidelines of VRIC, I’m especially bullish on copper. Like gold, copper is facing significant supply shortages as there aren’t any new large mine projects being developed or going into production. Meanwhile, the red metal will continue to be in hot demand as we move to electrify everything.

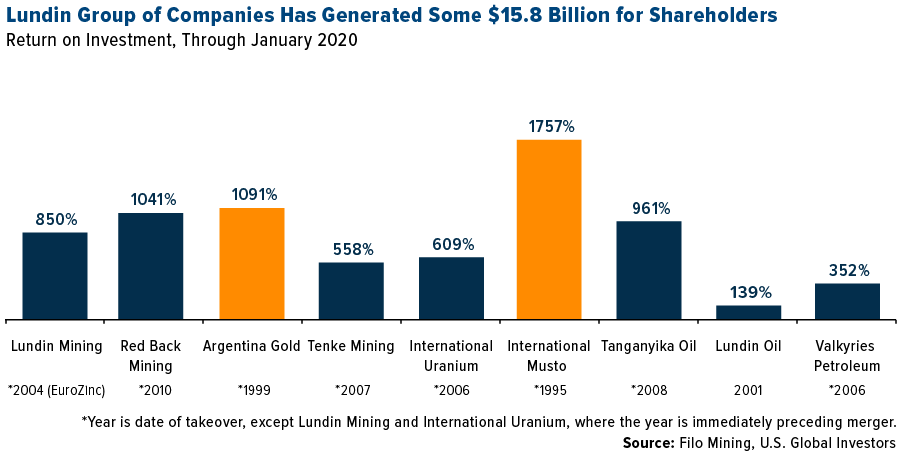

Speaking of copper, one of the more eye-opening presentations was conducted by the Lundin Group of Companies, including Filo Mining and Lundin Gold. In a press release dated January 22, Lundin Mining announced that the company successfully achieved its 2019 guidance for all metals at all operations, with copper production at its Candelaria project increasing 9 percent year-over-year.

Thanks to strategic acquisitions and excellent corporate governance, Lundin has managed to generate an astounding $15.8 billion for shareholders over the years.

Chinese Gold Purchases Muted

As for gold, the normally reliable Love Trade during China’s Lunar New Year has been impacted by the deadly coronavirus, which was first reported in the central Chinese city of Wuhan—population 11 million—but has since spread to other areas of the country, not to mention the U.S. Travel and spending in general have largely been restricted, with the Chinese government’s recent travel ban affecting as many as 35 million people. Today we even learned that Shanghai Disneyland has temporarily closed its doors in an effort to curb the outbreak.

Gold consumption in China, the world’s largest consumer of the yellow metal, fell 13 percent year-over-year in 2019, the China Gold Association announced this week, with sales of jewelry, gold bars and coins falling sharply on higher prices.

I’ll have more to say on China later.

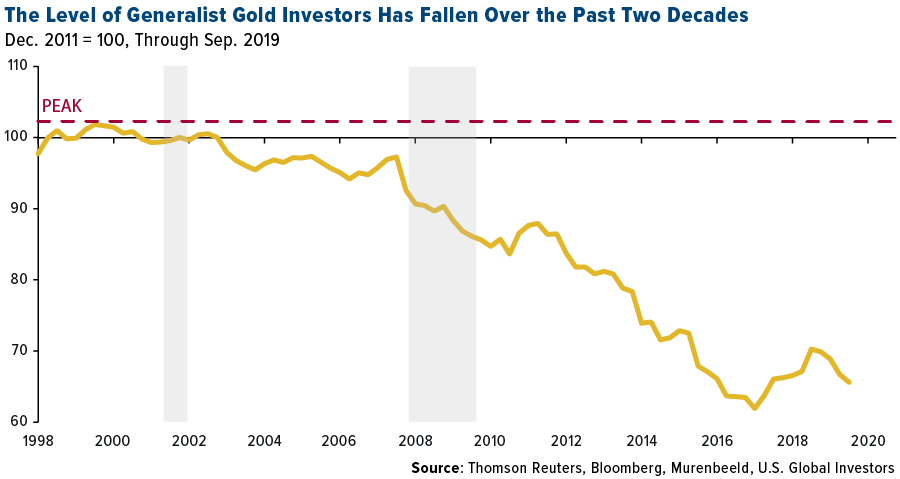

What’s missing in the gold market today, as I told Kitco News’ Daniela Cambone at VRIC, is the generalist investor. Holdings in gold-backed ETFs hit a new record high at the end of last year, but according to a Murenbeeld presentation, generalists are increasingly not participating—a reverse scenario of what we’re seeing in cryptocurrencies.

Happy Year of the Metal Rat!

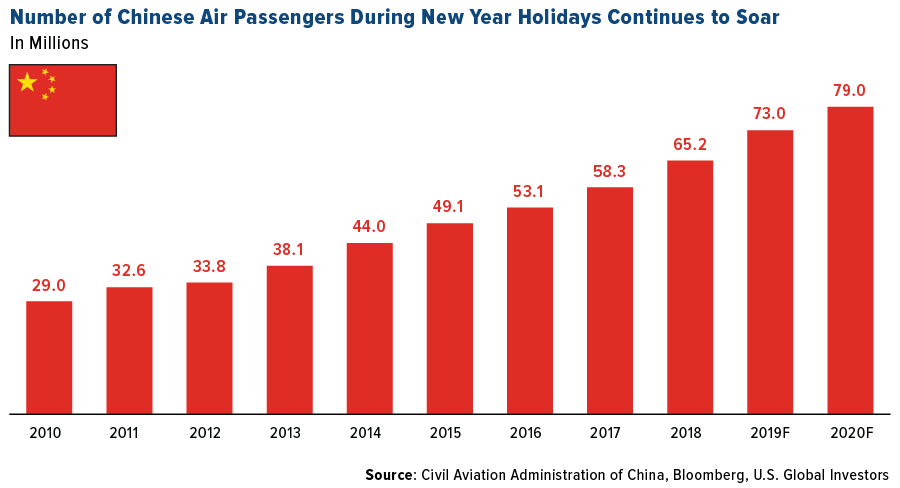

Tomorrow marks the Chinese Lunar New Year, a time when as many as 400 million people ordinarily travel to visit family and go on vacation. Before the coronavirus struck, 3 billion trips were estimated to take place during the 16-day celebration, while some 79 million passengers were expected to take flights, up more than 8 percent from 73 million a year earlier. The new Daxing International Airport in Beijing was to handle nearly 2 million flights.

When I flew through Zurich to attend the crypto conference, I happened to see multiple kiosks and signs proclaiming “Happy Year of the Rat,” an indication of just how broad and far-reaching China’s influence is—as well as how quickly viruses can spread in today’s uber-connected world.

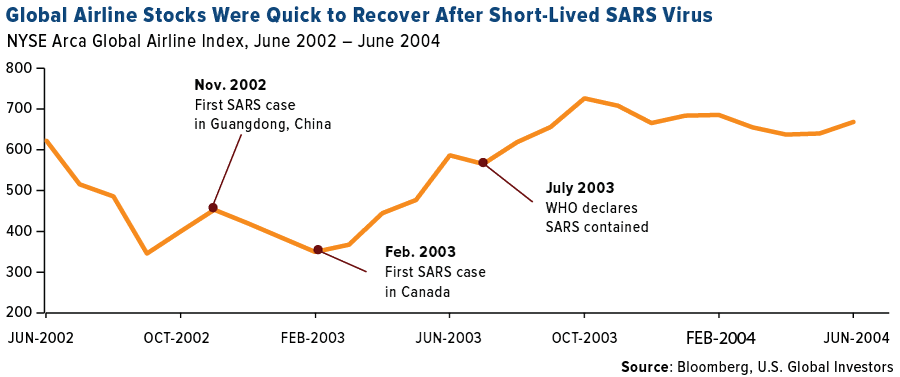

If investors are seeking a precedent to compare to the recent coronavirus, they need only look bad 10 years, when the H1N1 Swine flu made it the U.S. via Mexico. An estimated half a million people died as a result of the virus, 12,000 in the U.S. alone. Major U.S. carriers were impacted, with Delta Air Lines reporting between $125 million and $150 million in lost revenue, according to a note this week from Credit Suisse. But the virus was relatively short-lived, and the industry promptly recovered.

Before that, in 2003, was the SARS epidemic. Air traffic to China fell by nearly half year-over-year in the second quarter of that year, which may have had a negative impact on airline earnings. Credit Suisse points out it’s hard to estimate SARS’ impact on airlines since there was also the Iraq War, not mention a weak macro environment at the time. Again, airlines were quick to recover once the threat of the virus dissipated, and carriers were citing normalization of trends, including capacity growth, in the second half of 2003.

Our own airlines ETF has very little exposure to Asia. The only Asian carrier in the ETF, in fact, is Japan Airlines. It does not own Airports of Thailand, down 4 percent year-to-date through January 24, or Beijing Capital International Airport, down more than 15 percent.

Again, it’s the Year of the Rat, the first sign of the Chinese Zodiac, following 2019’s pig. Speaking of which, pork price inflation in China fell in December, to 97 percent from November’s 110 percent year-over-year, as the African swine fever has wiped out some 40 million pigs. But according to Chinese officials, the fever has come into control, and the number of new pigs jumped the most in a decade last month.

Because it’s the first of the 12 zodiacs, the Year of the Rat is seen as a time of beginnings and renewals. That brings me hope, especially paired with the recent positive development in the U.S.-China trade war. To all of my friends and family, readers and shareholders, I want to wish you a Happy New Year!

To watch my interview with Daniela Cambone at VRIC, click here!

January 24, 2020Generalist Investors Warming Up To Gold |

January 22, 2020Frank Holmes Bullish on Copper – Commodity-TV |

January 9, 2020Gold Fund Manager’s Top 2020 Mining Picks |

|||

Gold Market

This week spot gold closed at $1,571.53, up $14.29 per ounce, or 0.92 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.49 percent. The S&P/TSX Venture Index came in off 0.47 percent. The U.S. Trade-Weighted Dollar rose 0.29 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-21 | Germany ZEW Survey Current Situation | -13.5 | -9.5 | -19.9 |

| Jan-21 | Germany Survey Expectations | 15.0 | 26.7 | 10.7 |

| Jan-23 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jan-23 | Initial Jobless Claims | 214k | 211k | 205k |

| Jan-27 | New Home Sales | 730k | — | 719k |

| Jan-28 | Durable Goods Orders | 1.0% | — | -2.1% |

| Jan-28 | Conf. Board Consumer Confidence | 128.0 | — | 126.5 |

| Jan-29 | FOMC Rate Decision (Upper Bound) | 1.75% | — | 1.75% |

| Jan-30 | Hong Kong Exports YoY | 4.0% | — | -1.4% |

| Jan-30 | Germany CPI YoY | 1.7% | — | 1.5% |

| Jan-30 | GDP Annualized QoQ | 2.2% | — | 2.1% |

| Jan-30 | Initial Jobless Claims | 213k | — | 211k |

| Jan-31 | Eurozone CPI Core YoY | 1.2% | — | 1.3% |

Strengths

- The best performing metal this week was gold, up 0.92 percent. Gold traders and analysts were split between bullish and neutral outlooks on gold ahead of next week’s Federal Reserve meeting, according to the weekly Bloomberg survey. Commodity ETF inflows topped $2 billion last week, expanding more than fourfold for a fifth straight week of inflows. Bloomberg reports that precious metals ETFs led the inflows.

- Turkey’s gold reserves rose $159 million from the previous week. The country’s holdings are now worth $28.1 billion as of January 17 – a 38 percent increase year-over-year.

- The number of worker deaths at mines in South Africa fell to the lowest on record in 2019 – a sign that safety is improving in some of the world’s deepest and least-mechanized mines. The Department of Mineral Resources and Energy said in a statement that there were 51 fatalities last year, down from 81 the year prior. Barrick Gold and the government of Tanzania signed an accord to a long-running dispute where confiscated resources will be released to Barrick’s subsidiary, now called Twiga Minerals Corp., for export.

Weaknesses

- The worst performing metal this week was palladium, down 2.88 percent. According to the China Gold Association, gold output in China fell 5.2 percent year-over-year to 380 tons in 2019. Gold consumption also fell 12.9 percent to 1,003 tons. China is the top producer and consumer of the yellow metal globally. Lower demand could be attributed to the number of births falling to the lowest since 1961 and the number of marriages falling to the lowest since 2007.

- Ghana is delaying the initial public offering and sale of $750 million of shares in a gold mining fund/royalty company as the government reviews the rules and processes related to mineral royalty payments, reports Bloomberg. The IPO will be delayed until March, according to sources, and the fund will be structured to receive royalties and pay dividends.

- Power cuts by South African energy producer Eskom cost Anglo American Platinum 38,000 ounces in lost output in 2019. Power outages forced mines to shut down and impacted production throughout the year. Despite the challenges, total platinum-group metal production grew 9 percent year-over-year to 1.15 million ounces. Australia’s Resolute Mining announced it will be raising AUD196 million to repay a loan. The company’s shares slipped on the news. Resolute said it will place 22.7 million new shares at the same price to raise AUD25million. This reinforces the trend that when investors see gold companies with debt, the right share price valuation adjustment step is for investors is to repay debt with common at the current share price to arrive at diluted price targets.

Opportunities

- David Rosenberg, well-known economist, expressed his bullishness on gold in an interview with Bloomberg this week: “Gold is a place you want to be. I think that it’s partly because it’s inversely correlated with interest rates. But it’s also an insurance policy when things go wrong. There’s no such thing as a no-brainer, but this is close.” Jeff Currie, head of global commodities research at Goldman Sachs, gave three reasons to hold gold in a Bloomberg interview: 1) it’s a good hedge against political risk, 2) de-dollarization and 3) a drop in investment, which leads to a savings glut.

- Palladium saw a weekly decline after rallying for four weeks, but it could present a buying opportunity. Citigroup says that any substantive pullback from current levels would represent a buying opportunity since “our baseline is that 2020 will be a year of very strong palladium pricing.” Metals Focus estimates that global palladium inventories equal about 14 months of demand and stockpiles have fallen by half in the past decade – this should support high prices.

- Morgan Stanley research from Ridham Desai and Sheela Rathi shows that gold was India’s best performing asset class in 2019. They found that a portfolio that equal weights gold and equities has delivered reasonably strong returns with lower average annual drawdown than gold or equities standing alone over the past 25 years. According to the All India Gem & Jewellery Domestic Council, gold imports by India may rebound in 2020 after hitting a three-year low. Gold imports to the world’s second largest consumer fell last year largely due to prices rising by nearly 25 percent. The group forecasts imports of 750 tons, compared to an estimated 690 tons last year.

Threats

- Bloomberg reports that U.S. prosecutors are starting to build cases against traders suspected of manipulating markets as long as a decade ago. Cases involving conduct older than five years are already under way, after an obscure legal ruling extended the statute of limitations for spoofing cases. Spoofing is when someone places and then cancels large numbers of buy or sell orders with the aim of fooling others about supply and demand.

- Scott Minerd, chief investment officer of Guggenheim Partners, said in an interview that the Federal Reserve is “inflating a bubble” in credit, reports Bloomberg. “Asset prices go up on an escalator and they go down in an elevator.” Head of Dutch bank ABN Amro Bank NV said at the World Economic Forum in Davos this week that negative rates are “not a good place to be.” The head of Deutsche Bank AG said the European Central Bank “missed the exit” from negative rates when growth was stronger.

- Gold producers were hit with a surprise new fee. The Department of Energy issued a mercury fee rule where producers must pay a fee of $37,000 per metric ton of mercury stored. The rule was issued without documents to support its calculations. Gold producers are fighting this new rule, led by Nevada Gold Mines LLC.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.22 percent. The S&P 500 Stock Index fell 1.03 percent, while the Nasdaq Composite fell 0.79 percent. The Russell 2000 small capitalization index lost 2.18 percent this week.

- The Hang Seng Composite lost 4.04 percent this week; while Taiwan was up 0.24 percent and the KOSPI fell 0.20 percent.

- The 10-year Treasury bond yield fell 13 basis points to 1.69 percent.

Domestic Equity Market

Strengths

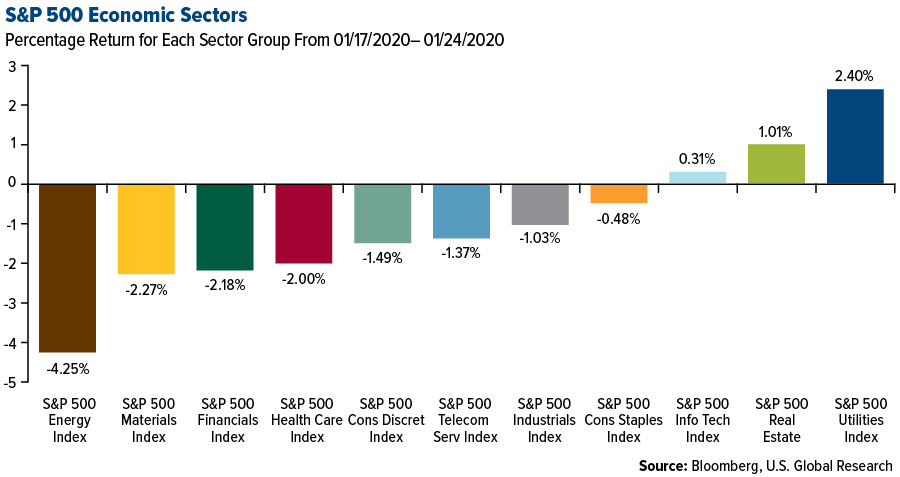

- Utilities was the best performing sector of the week, increasing by 2.40 percent versus an overall decrease of 1.03 percent for the S&P 500.

- Intel Corp. was the best performing S&P 500 stock for the week, increasing 14.88 percent.

- Intel surged towards its highest close since September 2000 on Friday following Thursday’s fourth quarter-results. The company reported revenue of $20.2 billion, up 8 percent year-over-year and above the consensus estimate of $19.2 billion. The company also announced the board approved a 5 percent cash dividend increase to $1.32 a share on an annual basis.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 4.25 percent versus an overall decrease of 1.03 percent for the S&P 500.

- Cabot Oil & Gas Corp. was the worst performing S&P 500 stock for the week, falling 12.91 percent.

- Synchrony Financial was down nearly 10 percent during trading on Friday, making it the worst performer of the S&P 500. The company reported fourth-quarter net interest income of $4.03 billion, down from $4.33 billion a year earlier.

Opportunities

- Global Payments Inc. climbed to a fresh record Friday after Credit Suisse designated the stock a top pick. The company is set for higher revenue and margin expansion, with the most exposure to the fastest-growing aspects in the financial payments world, analysts wrote in a note on payments and fintech stocks.

- Davita was upgraded to a buy from neutral by Goldman Sachs analyst Stephen Tanal, citing higher potential multiples and upward estimate revisions, driven by the impact of the 2021 ESRD rule change on DVA’s revenue per dialysis treatment. Tanal raised his PT to a Street high $97 from $72, according to the note.

- Alphabet’s price target was raised to a Street-high view of $1,769 from $1,546 at KeyBanc Capital Markets, which cited an improved view toward online advertising.

Threats

- Health care stocks led the market lower on Friday on growing fears that upcoming elections may ignite lawmakers to take action on the increasing cost of medicines in the U.S.

- Ericsson’s shares fell 9 percent on Friday, its worst day since the Swedish firm’s earnings miss last July, with analysts disappointed by the company’s lower gross margin and higher operating expenses.

- Remy Cointreau SA’s decision to halt guidance amid the spread of a new coronavirus in China concerned analysts for the quarters to come after the liquor maker reported sales that fell short of their expectations. “There’s increasing uncertainty everywhere,” Citigroup Inc. analyst Simon Hales wrote in a note to clients. “Absence of guidance is problematic.”

The Economy and Bond Market

Strengths

- The number of Americans filing for unemployment benefits increased less than expected last week, suggesting the labor market continues to tighten even as job growth is slowing. Initial claims for state unemployment benefits rose 6,000 to a seasonally adjusted 211,000 for the week ended January 18.

- The IHS Markit Flash Services PMI strengthened for the third month in a row to highest level since last March – rising to 53.2 from 52.8 in December.

- U.S. existing-home sales rose in December to set their best pace since early 2018, according to new data from the National Association of Realtors. Sales of previously owned homes gained 3.6 percent last month after a moderate decline in November, reaching an adjusted annual rate of 5.54 million. The median sale price jumped to $274,500, a 7.8 percent increase from a year earlier as construction of new homes was outpaced by buyer demand.

Weaknesses

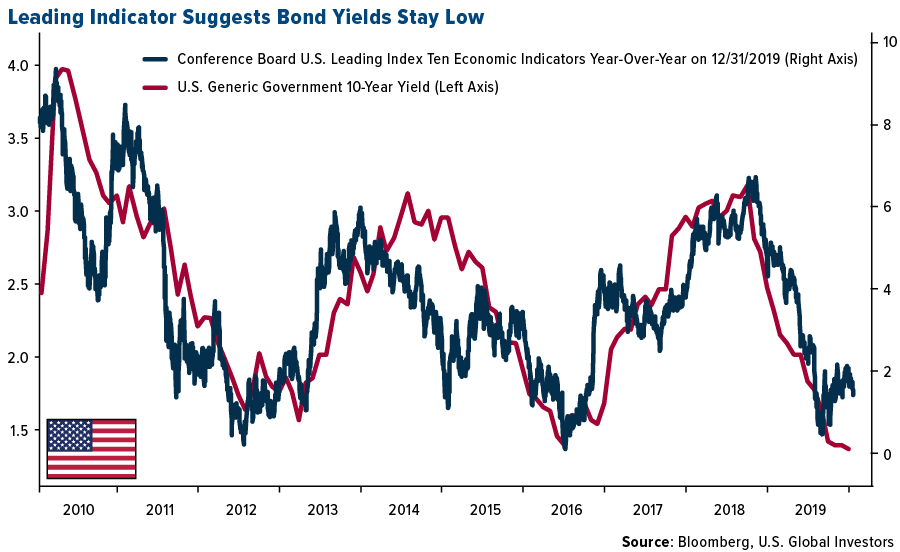

- The leading economic index fell 0.3 percent in December to mark the fourth decline in the past five months, according to the Conference Board. The drop in the index largely stemmed from an increase in jobless claims and a decline in building permits for new houses, slowing the economy toward the end of 2019.

- The IHS Markit Flash Manufacturing PMI fell to a 3-month low in January to 51.7, down from 52.4 in December. Manufacturing firms noted a slower improvement in operating conditions and both domestic and foreign client demand softened.

- World markets dropped amid reports in the U.S., France, Japan, South Korea and Singapore of confirmations of coronavirus cases, sounding fear alarms of the epidemic spreading globally.

Opportunities

- Investors will be looking for recent strength in housing data to continue when the December new home sales data is released on Monday.

- The personal income and outlays report for December will be closely watched next Friday, with another solid increase in personal income and consumption forecast.

- The Treasury’s reintroduction of its 20-year bond should be a “positive development” for tax-exempt and non-callable taxable municipal bonds, Barclays Plc analysts said in a report. “In the medium term, we might see some pick-up in investor demand for securities” in this part of the curve after the reboot of 20-year Treasuries as investors will have a “convenient maturity-matched UST hedging tool,” they said.

Threats

- It’s more likely that 10-year Treasury yields will fall toward 1.6 percent than rise to 1.9 percent. The latest sign is from the Conference Board’s Leading Indicator index, which has shown no signs of a meaningful recovery after peaking in August, suggesting business activity has failed to regain any momentum. Indeed, economic data has been lackluster except for housing, and that’s being supported by low mortgage rates. In addition, demand for Treasuries may rise as investors hedge against the risk in the equity markets amid concerns the coronavirus outbreak in China could spoil the nascent economic stability in the country, which is one of the key ingredients in the global reflation thesis.

- The latest durable goods orders report will be released next Tuesday. With manufacturing data still in disarray, results could disappoint.

- The main highlights of the week will be the Fed meeting and the advance GDP estimate. The U.S. economy is forecast to have grown by an annualized rate of 2.1 percent in the three months to December, the same pace as in the prior quarter. With earlier forecasts predicting a sharp slowdown in the fourth quarter, investors are bracing for a confirmation.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, which retained a 0.85 percent gain. The rise follows a general correction in many commodity prices this week on fears the travel limits in China, regarding the potential spread of the coronavirus, would curb growth. BloombergNEF reports that China has removed tariffs on Chile and Australia on lithium imports. After the Phase One deal was signed with the U.S., China cut imports on a wide range of battery materials including lithium spodumene, carbonate and hydroxide. The provisional tariff for lithium products from Chile and Australia is 0 percent, versus 2 to 5 percent for other countries. Chile supplies 60 percent of China’s lithium carbonate.

- This week Tesla Inc.’s market value climbed above Volkswagen AG’s for the first time – hitting $100 billion. Shares rose as much a 5.9 percent on Wednesday and are up 31 percent since the start of the year. The carmaker has a massive lithium-ion battery that is close to operation in South Australia, where it will support a steady flow of power from a wind farm, reports Bloomberg. Rolls-Royce is also jumping into renewables and batteries. The carmaker acquired a majority stake in a German battery storage developer Qinous.

- Japanese Environment Minister Shinjiro Koizumi questioned the country’s support for a new coal-fired power plant in Vietnam, despite support of the plant from Japan’s financial institutions, reports Bloomberg. Japan is the only nation in the Group of Seven that is still building new coal plants and Koizumi’s comments are a rare case of a high level politician questioning such policies.

Weaknesses

- The worst performing major commodity for the week was WTI crude oil, which fell 7.15 percent. Several commodities had a bad week due to concerns surrounding the spread of China’s coronavirus. The International Energy Agency noted this week that oil could be oversupplied by as much a 1 million barrels per day in the first half of the year. Copper saw its biggest weekly decline since 2018 due to fears that the virus could drag down global growth. Bloomberg reports that nickel led other metals lower on Friday for a weekly loss of more than 6 percent. Oil fell below $55 a barrel on Thursday – a two-month low – over concerns that the coronavirus could erode fuel demand.

- According to estimates from the Met Office, Britain’s official forecaster, the wildfires burning across Australia may have an influence on weather patterns and global ecosystems throughout the year. Estimates show the wildfires will release about 900 million metric tons of carbon dioxide into the atmosphere – almost the same amount as all commercial aircraft in 2018.

- Fabio Schvartsman, former CEO of Vale SA, was charged with 270 counts of homicide caused by a dam collapse in Brazil in January 2019. He is accused of knowing ahead of time of the dam’s safety issues and helping hide them prior to the deadly incident. Schvartsman began his tenure as Vale CEO with a vow never to repeat the 2015 disaster and left his post in March, just after the collapse, which ended up being far worse than the one four years prior. The dam collapse led to a spike in iron ore prices in early 2019 on supply shortage fears.

Opportunities

- Royal Dutch Shell Plc and Equinor ASA are looking to jointly purchase a 49 percent stake in the Bandurria Sur shale field in Argentina owned by Schlumberger Ltd. The interest from two majors comes at a critical moment for the country’s shale industry, which has the potential to rival places like the Permian Basin. Bloomberg’s Jonathan Gilbert writes “the Patagonian oil patch is being held back by infrastructure bottlenecks, abrupt changes in government subsidies, and sovereign risk.”

- Brazil’s agriculture minister Tereza Cristina said at a conference in New Delhi that Brazil sees a “great opportunity” for a partnership with India in the bio-energy sector: “There is huge potential for cooperation between our nations. An increase in ethanol production in India would provide, in addition to the socioeconomic benefits already observed, great environmental gains.” Brazil and India account for about 55 percent of sugarcane production and 35 percent of sugar output, however, there is a big disparity in ethanol production, with Brazil making over 30 billion liters and India at only 1.5 liters in 2018, reports Bloomberg. The partnership between the two nations could boost Indian production and contribute to the establishment of a global biofuel market.

- BloombergNEF estimates show that chemical recycling is set to grow 22 percent a year and reach an annual capacity of 4.1 million metric tons by 2030. Chemical recycling is relatively new where low-grade waste plastics that are landfilled are turned into virgin-grade material. Spain is moving quickly to become coal-free. According to the nation’s grid operator Red Electrica SA, coal’s share in the nation’s electricity fell to less than 5 percent in 2019, down from 14 percent a year earlier. The world’s most profitable hedge fund is now a “climate radical”, reports Bloomberg. Chris Hohn of TCI Fund Management, who has $30 billion in assets, is pushing portfolio companies to dramatically reduce greenhouse gas emissions and says he’ll remove companies from his fund if they don’t. Hohn’s fund had a gain of $8.4 billion in 2019 – making it the most profitable.

Threats

- Warmer winter temperatures hurting consumption and an onslaught of new supply will likely push LNG prices to record lows this year, just after having a terrible 2019. Bloomberg reports that LNG for spot delivery to North Asia is set to hit an all-time low in summer and gas prices in both Europe and the U.S. are at the weakest seasonal levels since 1999. “The gas market can’t stomach the oversupply and warm weather, and it’s getting both,” says Ron Ozer, founder of gas-focused hedge fund Statar Capital LLC.

- Opening arguments began this week in Ohio over whether DuPont caused cancer in two people because of PFAS contamination. The trial is based on allegations that polyfluoroalkyl substances from a DuPont plant in West Virginia caused kidney cancer of a woman and testicular cancer of a man, reports Bloomberg. The case was the subject of a recent movie called “Dark Waters”, which chronicles the struggles of one lawyer to bring suits against DuPont for chemical contamination for years.

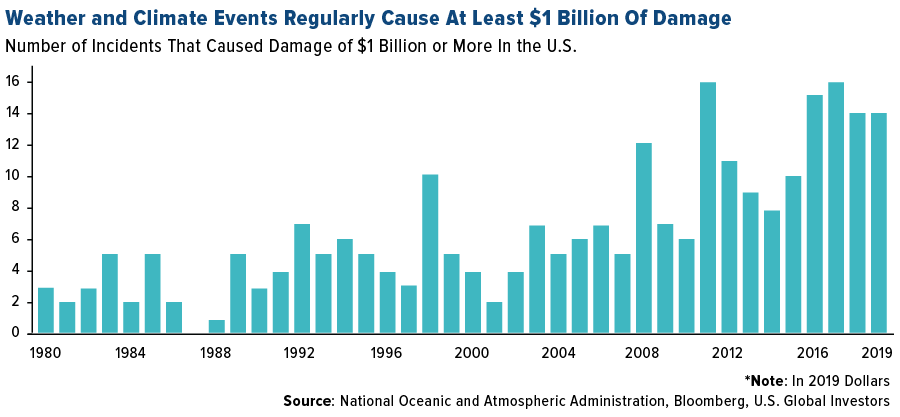

- According to the National Oceanic and Atmospheric Administration, billion dollar disasters caused by weather or climate are a regular occurrence. In 2019 alone, there were 14 incidents that caused damage of $1 billion or more in the United States. Swedish climate activist Greta Thunberg made headlines this week after calling out global leaders at the World Economic Forum in Davos for doing nothing toward curbing climate change.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 1.5 percent. The Greek parliament held presidential elections on Wednesday. Katerina Sakellaropoulou, who was nominated by the ruling conservative New Democracy party, became the first woman president, winning 261 votes out of 300, which is way above the 200 required by the constitution.

- The Hungarian forint and Czech koruna were the best relative performing currencies this week, losing 60 basis points each. All emerging Europe currencies declined over the past five days as the dollar strengthened. The koruna and the forint recorded the smallest losses, supported by strong economic data.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.6 percent. Brent crude oil declined 6.3 percent over the past five days, pushing stocks trading on the Moscow exchange lower. Commodity and metal producers corrected this week on fears of weaker demand due to growing concerns over the impact of the coronavirus. Two passengers on a flight from China to St. Petersburg were hospitalized with a suspected acute respiratory viral infection. The World Health Organization decided not to declare a global health emergency for now, but planned to meet again within 10 days

- The Polish zloty was the worst performing currency in the region this week, losing 1 percent. All emerging European currencies declined as the dollar strengthened over the past five days. The zloty was under more pressure than other currencies due to political developments. Poland’s lawmakers approved legislation that will allow politicians to fire judges who criticize their decisions, as part of the judicial reform plan. President Andrzej Duda is expected to sign it into law. This law has been condemned by the European Union, the United Nations and other international bodies, as well as by Polish legal experts on Poland’s opposition.

- Energy was the worst performing sector among eastern European markets this week.

Opportunities

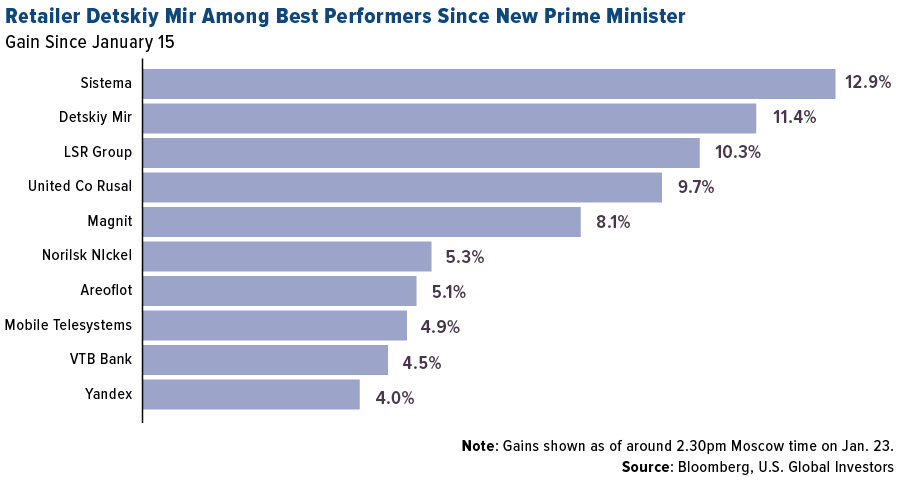

- Russia’s new Prime Minister Mikhail Mishustin has announced his new cabinet. Out of nine Vice Prime Ministers in the cabinet, only three retained their posts, signaling readiness to change. These new members of the cabinet will be more willing to promote growth in the economy and disposable income. Last week Putin announced a proposal to spend $65 billion until 2024 in new benefits for the poor and for families. In addition, Russia may spend $400 billion on infrastructure projects in the next four years. Domestic consumer equites could outperform commodity exporters under the increased spending plan.

- The European Central Bank (ECB) left all rates unchanged and will continue to reinforce the accommodative policy state by buying 20 billion euros per month as long as necessary. ECB President Christine Lagarde announced the beginning of a strategic review on the bank’s monetary policies, the first review since 2003.The review should reveal why inflation has remained below target for many years, and whether the inflation target needs to be changed.

- Eurozone’s preliminary Manufacturing PMI for January came in at 47.8, above the expected reading of 46.8. The largest European economies, including Germany, France and the United Kingdom, saw increases in their manufacturing activity last month. While Service PMIs were reported mostly lower, with France posting the weakest Service PMI at 51.7 versus expected 52.2 due to ongoing strikes against government reforms. The eurozone composite PMI, which combines the manufacturing and service activity numbers, remained unchanged at 50.9.

Threats

- In 2018, President Trump threatened a 25 percent import tariff on every car from the European auto industry. This threat was put on hold while the U.S. focused on negotiating a trade deal with China. Following Trumps’ recent trade agreement with China, talks about additional tariffs on European goods may intensify.

- Russia’s central bank reported a historical record in foreign funds’ flow of $22 billion into Russia’s public debt last year, exceeding the prior record from 2012 of $17.1 billion. Experts say that it will be impossible to maintain the same interest this year, and it may require up to $25 billion of net new flows to avoid ruble depreciation this year.

- Belarus, the post-Soviet country on the east of Poland, relies on Russia for more than 80 percent of its energy needs. Russia stopped supplying oil to its post-Soviet neighbor after December 31 as the two counties had failed to renegotiate an agreed-upon oil price for this year. Russia argues that Belarus should accept greater economic integration if it wants to continue receiving energy resources at Russia’s domestic prices, according to Bloomberg. Will Belarus follow Crimea’s footsteps?

China Region

Strengths

- Before closing for the latter days of the week, Vietnam’s Ho Chi Minh Stock Index rose 1.28 percent for the week, while Taiwan’s Capitalization Weighted Stock Index rose 24 bps.

- Telecommunications was the top-performing Hang Seng Composite Index sector in Hong Kong again this week, rising amid the risk-off environment by 2.51 percent.

- South Korea’s preliminary fourth quarter GDP readings looked better than expected, with quarter-over-quarter change at 1.2 percent versus 0.7 percent expected and a 2.2 percent year-over-year reading versus a 1.9 percent consensus. Taiwan also looked stronger than expected, as 2019 YoY GDP finished at a 2.73 percent and ahead of a 2.60 percent consensus, with preliminary fourth quarter readings at 3.38 percent, well ahead of a 2.78 percent consensus. Taiwanese industrial production was better than expected as well, coming in just shy of 6 percent for the YoY December measurement.

Weaknesses

- Hong Kong’s Hang Seng Composite dropped by 4.04 percent for the week.

- Properties and construction was the poorest-performing HSCI sector this week, dropping by 6.50 percent.

- The Chinese renminbi weakened over the course of the week.

Opportunites

- The Lunar New Year is here, and happy Year of the Rat to you all! Don’t let coronavirus get you down, but do consider whether a scare and selloff may represent any sort of buying opportunity given that up until the last few days markets seemed positive and optimistic with improved sentiment on Phase One cheer.

- You know what’s worth bringing up again? Korea’s KOSPI still made new 52-week highs earlier this week.

- U.S. Senator John Cornyn (R-TX) released a letter to his fellow Texans in honor of the Vietnamese Lunar New Year celebration (Tet Nguyen Dan), noting that in the great state of Texas, Vietnamese is actually the third most spoken language, after English and Spanish!

Threats

- Coronavirus, the “China virus,” the “Wuhan virus”—call it what you like—but the world sees this deadly pneumonia-like virus that has already claimed 25 lives in China as a real threat and legitimate health scare. SARS is one acronym everyone’s talking about again and caution is the watchword. China is locking down some 40 million persons and counting—at the start of the Lunar New Year holidays, to boot—and the coronavirus has indeed crossed oceans at this point, with at least three confirmed cases in the United States as well, at least two in France, and, closer to Wuhan, China (where the virus appears to be centered) confirmed cases around the Asia Pacific region elsewhere include (at least!) Hong Kong, Macau, Singapore, Thailand, Japan, Taiwan and South Korea. And make no mistake about it: If one takes SARS as an example from more fairly recent history or—in a less “viral” but similarly disruptive parallel given some of the economic effects and reverberations, Hong Kong’s protests last year as a more recent example—retail sales as well as transports and tourism may well be most likely see the first economic effects of the virus. Note, however, that the World Health Organization (WHO) has, at this point at least and as of their meeting on Thursday, declined to declare the Wuhan coronavirus outbreak a global emergency.

- Relatedly, as we observed last week, following the exuberance of markets heading into the actual signing of the Phase One agreement and their collectively sharp ascent, markets may indeed have been open to some possible retracement—and accordingly it is entirely possible that it may not be over. As more cases are surely going to be reported following incubation periods, lagging lockdowns on travel, etc. the coronavirus may serve to “excuse” further global profit-taking or de-risking.

- At the Davos World Economic Forum this week, Commerce Secretary Wilbur Ross pointed out that the U.S. may well in the “near-term” release new rules on limiting U.S. suppliers to Huawei Technologies. Remember, Phase One is Phase One, not All Said and Done. Sticking points remain, and some will surely endure for the “near-term” and well beyond.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended January 24 was Prometeus, up 154.23 percent.

- The fifth-largest crypto exchange by daily trading volume, Huobi, is launching its first licensed digital asset brokerage known as Huobi Brokerage, reports CoinTelegraph. According to a press release this week, the exchange will now provide brokerage service to its institutional clients with a unique feature allowing the platform to connect with other exchanges and over-the-counter (OTC) desks. The VP of Business at Huobi Group, Ciara Sun, notes that institutional investors and high-net-worth individuals will be the major contributors to growth in the crypto economy in 2020.

- In the first week after going live, bitcoin options from the CME Group more than doubled their traded volume, reports CoinTelegraph. Figures supplied by the company show that options volumes skyrocketed in the seven days since they went live on January 13. As of January 17, volume was 122 contracts.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended January 24 was BenePit Protocol, down 81.66 percent.

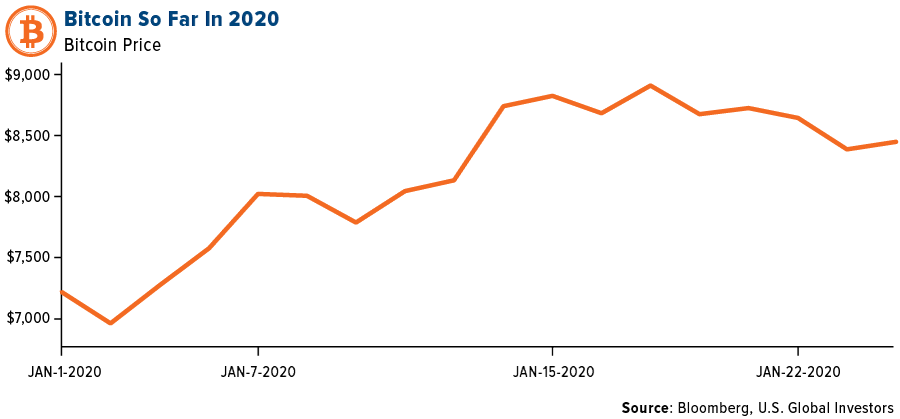

- Over the last 24 hours, and to end another week, bitcoin’s price pullback has gathered steam, reports CoinDesk, erasing a major portion of the cryptocurrency’s recent gains. Notably, bitcoin has now erased nearly 40 percent of the rally from $6,853 to $9,188 witnessed in the 17 days to January 19.

- In an interview this week during the World Economic Forum, billionaire investor Ray Dalio was asked about the global economy, writes Forbes. While his general thesis on what will happen in the coming years matched up with what many bitcoin holders think, Dalio’s advice for those worried about tough economic times ahead is to turn to gold, the article explains, rather than to bitcoin, as a safe haven asset.

Opportunities

- According to a press release published by the Bank of England on January 21, six major central banks have created a group with the Bank for International Settlements (BIS) to jointly research central bank digital currencies (CBDC). As reported by CoinTelegraph, the institutions will share their experience with other group members as they study potential cases for CBDCs in their respective jurisdictions. The banks include Canada, the U.K., Japan, European Union, Sweden and Switzerland.

- On Tuesday, payments provider Square was granted a patent by the U.S. Patent and Trademark Office, for a new network that enables seamless crypto-to-fate transactions, reports CoinDesk. The payments system allows users to hold different asset types to transact with one another in real-time. According to the filing, the new system could be especially advantageous for the retail sector.

- In a controversial first for the industry, CoinTelegraph reports that U.S. crypto exchange Coinbase will soon hold a million bitcoins in its cold wallets. As of January 1, and according to data from news resource Longhash released January 23, Coinbase’s cold wallets contained around 970,000 BTC ($8 billion).

Threats

- Facebook’s Libra cryptocurrency is starting 2020 looking no closer to release, writes Bloomberg, with authorities in its base in Switzerland raising fresh questions about its suitability as a global currency. Swiss finance minister Ueli Maurer said in late December that the project “has failed” in its current form because the basket of currencies Libra proposed to back the digital currency haven’t been accepted by the issuing national banks.

- Following the exit of Visa and MasterCard, now Vodafone is the latest firm to abandon Facebook’s Libra Association, reports Newsweek, yet another blow to the social network’s cryptocurrency plans. Since it was first announced last June, several large brands have left the project, mostly citing concerns about financial regulation.

- According to a January 22 post by Ripple, its XRP sales continued to drop in the second half of 2019, with sales of the token reaching a historic low in the fourth quarter. Total sales in the fourth quarter accounted for $13.08 million, down more than 80 percent from the $66.24 million reported in the third quarter of 2019.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.69 | -0.13 | -7.35% |

| Oil Futures | 54.37 | -4.17 | -7.12% |

| Hang Seng Composite Index | 3,818.77 | -160.77 | -4.04% |

| S&P Basic Materials | 375.28 | -8.70 | -2.27% |

| Korean KOSPI Index | 2,246.13 | -4.44 | -0.20% |

| S&P Energy | 429.71 | -19.06 | -4.25% |

| Nasdaq | 9,314.91 | -74.03 | -0.79% |

| DJIA | 28,989.73 | -358.37 | -1.22% |

| Russell 2000 | 1,662.59 | -37.05 | -2.18% |

| S&P 500 | 3,295.40 | -34.22 | -1.03% |

| Gold Futures | 1,577.10 | +10.60 | +0.68% |

| XAU | 104.82 | +2.98 | +2.93% |

| S&P/TSX VENTURE COMP IDX | 580.85 | -3.65 | -0.62% |

| S&P/TSX Global Gold Index | 264.32 | +8.64 | +3.38% |

| Natural Gas Futures | 1.89 | -0.11 | -5.54% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,246.13 | +56.05 | +2.56% |

| 10-Yr Treasury Bond | 1.69 | -0.21 | -11.20% |

| Gold Futures | 1,577.10 | +66.50 | +4.40% |

| S&P Basic Materials | 375.28 | -8.63 | -2.25% |

| S&P 500 | 3,295.40 | +72.02 | +2.23% |

| DJIA | 28,989.73 | +474.28 | +1.66% |

| Nasdaq | 9,314.91 | +362.03 | +4.04% |

| Oil Futures | 54.37 | -6.74 | -11.03% |

| Hang Seng Composite Index | 3,818.77 | +30.38 | +0.80% |

| S&P/TSX Global Gold Index | 264.32 | +4.93 | +1.90% |

| XAU | 104.82 | +0.15 | +0.14% |

| Russell 2000 | 1,662.59 | -15.42 | -0.92% |

| S&P Energy | 429.71 | -27.35 | -5.98% |

| S&P/TSX VENTURE COMP IDX | 580.85 | +24.85 | +4.47% |

| Natural Gas Futures | 1.89 | -0.28 | -12.89% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 104.82 | +12.82 | +13.93% |

| S&P/TSX Global Gold Index | 264.32 | +22.03 | +9.09% |

| Gold Futures | 1,577.10 | +60.30 | +3.98% |

| DJIA | 28,989.73 | +2,184.20 | +8.15% |

| S&P 500 | 3,295.40 | +285.11 | +9.47% |

| Nasdaq | 9,314.91 | +1,129.12 | +13.79% |

| Korean KOSPI Index | 2,246.13 | +160.47 | +7.69% |

| Natural Gas Futures | 1.89 | -0.42 | -18.31% |

| S&P Basic Materials | 375.28 | +13.72 | +3.79% |

| Russell 2000 | 1,662.59 | +112.41 | +7.25% |

| Oil Futures | 54.37 | -1.86 | -3.31% |

| Hang Seng Composite Index | 3,818.77 | +210.09 | +5.82% |

| S&P/TSX VENTURE COMP IDX | 580.85 | +38.01 | +7.00% |

| S&P Energy | 429.71 | -5.79 | -1.33% |

| 10-Yr Treasury Bond | 1.69 | -0.08 | -4.47% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2019):

Destkiy Mir

Sistema

Norilsk

Aeroflot

Mobil Tel.

Cabot Oil & Gas Corp.

Anglo American PLC

Resolute Mining Ltd

Royal Dutch Shell PLC

Equinor ASA

Filo Mining Corp

Lundin Gold Inc

Lundin Mining Corp

Delta Air Lines Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Conference Board Leading Economic Index is intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables. These variables have historically turned downward before a recession and upward before an expansion. The percent change year over year of the Leading Economic Index is a lagging indicator of the market directions. The NYSE Arca Global Airline Index (“AXGAL” or “Index”) is a modified equal- dollar weighted index designed to measure the performance of highly capitalized and liquid international airline companies. The Index tracks the price performance of selected local market stocks or ADRs of major U.S. and overseas airlines. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Ho Chi Minh City Stock Exchange or Ho Chi Minh Stock Exchange, located in Ho Chi Minh City, is the largest stock exchange in Vietnam. The Taiwan Capitalization Weighted Stock Index is a stock market index for companies traded on the Taiwan Stock Exchange. The Korea Composite Stock Price Index or KOSPI is the index of all common stocks traded on the Stock Market Division—previously, Korea Stock Exchange—of the Korea Exchange. It is the representative stock market index of South Korea, like the S&P 500 in the United States.