October Is Already Living Up to Its Reputation as the “Jinx Month”

Date Posted: October 2, 2020

Read time: 53 min

October has historically been the most volatile month for stocks, and so far this month is shaping up to be just as choppy. With only around 30 days remaining before the election, President Donald Trump tests positive for COVID-19.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

For the past several months, I’ve been watching “Resurrection: Ertugrul” on Netflix.

It’s a Turkish television series that first aired in 2014. Set in the 13th century, the series centers around the titular Ertugrul, the father of Osman, who founded the Ottoman Empire.

Some viewers have called the show the Turkish “Game of Thrones,” and for good reason. It’s full of adventure and excitement as well as intrigue and corruption.

It’s also controversial within the Arab world for showing why the Middle East has so many problems to this day. A number of Arab countries have actually banned it because they believe Turkey’s president Recep Erdogan may see himself as a modern day Ertugrul, out to create a new Ottoman Empire.

In the show, members of the Byzantines, Mongols and Templars are all pressuring their leaders to fight one another, which is reminiscent of the fighting we still see to this day between the Sunnis and Shias.

It also reminds me of America’s political landscape right now. Outside influences are actively trying to “divide and conquer” by weakening the fiber that holds us together. China steals U.S. technology while Russia continues to try to undermine our elections. (More on that later.) Many people believe disinformation is worse now than it’s ever been.

It’s kind of like how Hong Kong protestors were sent to Oslo, Norway last year to be trained to mobilize activists, keep ranks, deal with police and more.

The reason I’m sharing this with you is that investors should try to avoid getting distracted by the feuding political parties within the U.S. A lot of the infighting is being fueled by outside actors, who thrive on the chaos and the division. Russia’s Putin and China’s Xi Jinping are delighted that we’re so divided right now.

In any case, I’m about 90 percent of the way through “Ertugrul.” It’s not short—there are about 450 episodes—but I highly recommend it to fans of world history who are looking for something different. If you’ve already watched it, I’d love to know what you think! Drop me an email at info@usfunds.com.

Will October “Jinx” Investors?

They don’t call it the “jinx month” for nothing.

October has historically been the most volatile month for stocks, and so far this month is shaping up to be just as choppy.

For one, we’re only 30 days away from the general U.S. election. In “normal” times this has been enough to roil markets, but this year the uncertainty is being compounded by the pandemic. Not only has President Donald Trump questioned the integrity of voting by mail, but today we learned that he and the First Lady have tested positive for COVID-19. Trump reportedly has a cough and fever, while Melania is said to be asymptomatic.

In a note to clients today, Evercore ISI’s Sarah Bianchi writes that Trump’s diagnosis actually increases the odds that a stimulus deal can be reached between the White House and Congress “as it refocuses the conversation on the virus and gives [House Speaker Nancy] Pelosi more leeway to worry less about the election implications of passing a bill.” This would be positive especially for domestic airlines, which were set to begin furloughing workers this week as aid ran out.

Analysts at Wolfe Research seemed to agree with this assessment and added that they believe this development could help the Democrats’ chances of winning the White House and Congress next month since it may “make many voters question [Trump’s] ability to handle the virus effectively.”

I wish the president and his wife a full and speedy recovery.

2016 All Over Again: Russian Hackers and Brexit Jitters

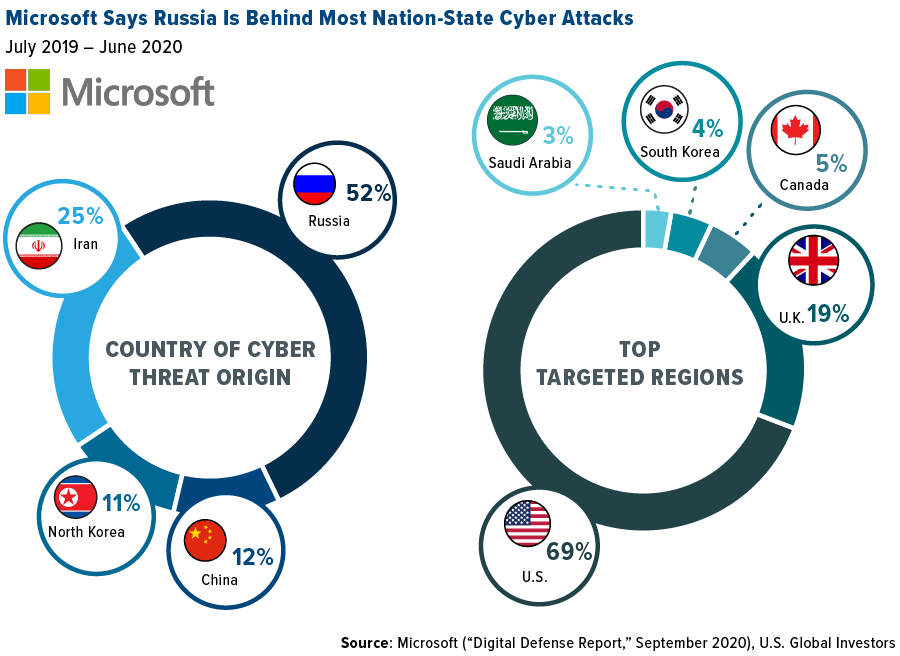

Then there’s the persistent cyber-attacks the U.S. receives from adversarial nation-states. Last month, Microsoft revealed that Russian hackers are once again trying to undermine the U.S. election. As many as 200 organizations tied to the election have been infiltrated, according to Microsoft.

This week the tech giant went further, releasing a new report that shows that Russia is the number one source of cyber threats, representing a little over half of all attacks worldwide. The country is followed by Iran, China and North Korea. The U.S. is hit the hardest, but other countries get targeted as well, including the United Kingdom, Canada, South Korea and Saudi Arabia. Microsoft is in a unique position to report on this since it has billions of customers across the globe, allowing it to “aggregate security data from a broad and diverse spectrum of companies, organizations and consumers.”

And speaking of the U.K., Brexit is back in the news. The transition period ends on December 31, and yet a trade deal with the European Union (EU) has still not emerged. The 27-member bloc is now taking legal action against the U.K. for supposedly breaching the withdrawal agreement both sides signed last year.

Meanwhile, U.S. lenders are moving an estimated $1.5 trillion in assets from the U.K. to continental Europe ahead of the year-end deadline. “London’s standing as the one-stop shop for American banks doing business in Europe is slipping,” writes the Wall Street Journal.

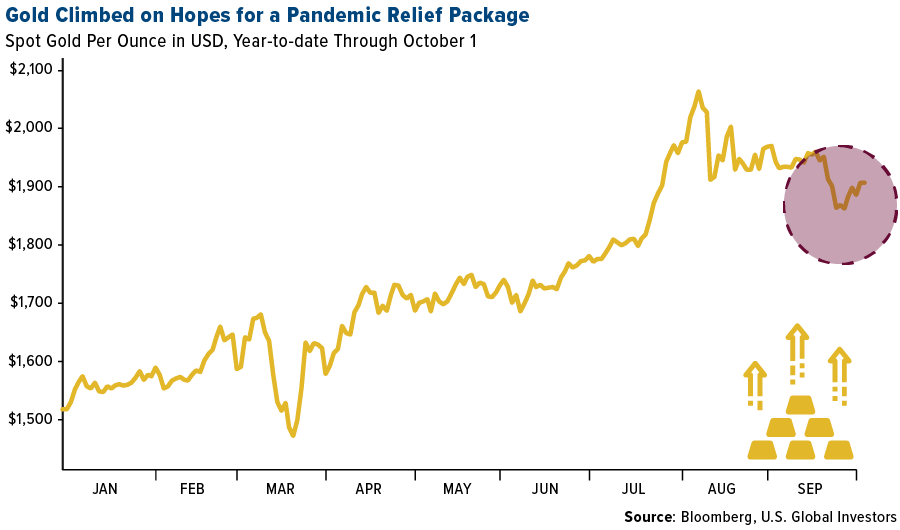

Gold Back Above $1,900. What Could Send It Higher?

All of these risk factors could be constructive for the price of gold. The metal closed above $1,900 an ounce yesterday as the U.S. dollar lost some ground for the fourth straight day, and there could be further upside potential as we head closer to the election.

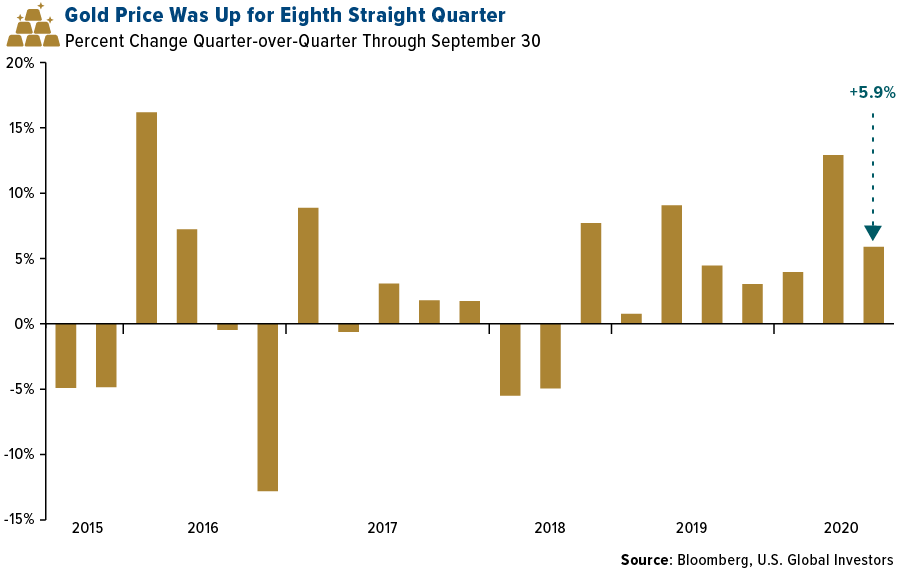

Gold has had an incredible run. It rose for the eighth straight quarter at the end of September, increasing around 6 percent. This marks the longest such streak for gold since the bull run nearly 10 years ago, when it gained for 12 straight quarters between the end of 2008 to 2011.

Gold was positive for the quarter, but it fell more than 4 percent during September, its worst month since November 2016 and worst September since 2014. As many of you may know, September used to be among the strongest months for gold, due mainly to seasonal buying in India, but lately the month has failed to deliver. You have to go back to 2016, in fact, to find the last time gold was positive in September.

So what could propel the price of gold higher? Most of the drivers are in place—negative real rates, unprecedented money-printing, geopolitical uncertainty.

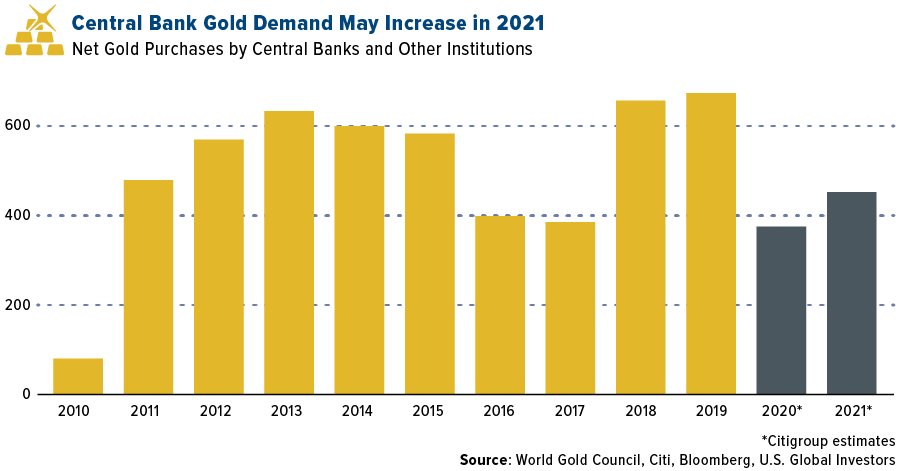

As I see it, two big factors are missing. One, central banks have been limiting their purchases this year, but Citigroup is projecting this won’t be for long. Banks bought some 375 metric tons this year, down significantly from the previous two years. However, Citi sees this amount going up to about 450 tons in 2021.

Number two is inflation. The U.S. has been stuck under 2 percent inflation for years now, which has prompted the Federal Reserve to keep rates near zero for some time longer.

But that’s only if you believe the consumer price index (CPI) is truly an accurate measure of inflation. Some economists and investors have raised questions whether the CPI is “fake news.” That’s the topic of one of my most recent YouTube videos, which you can watch below.

Global Factories Are Back in Business

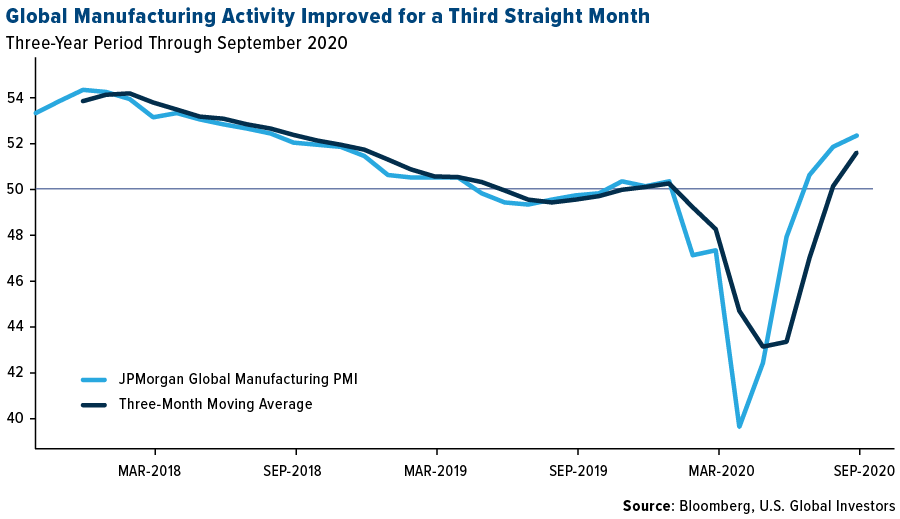

The good news in all of this is that global factories appear to have recovered to pre-pandemic levels. The JPMorgan Global Manufacturing PMI rose to a 25-month high of 52.3 in September, marking the third straight month of expansion.

The improvement was virtually across the board. According to JPMorgan, 21 out of 29 economies showed improvement, with Brazil, India and Germany improving the most. Mexico, Indonesia, Japan and Russia were among those that continued to contract in September.

As I’ve explained many times before, we use the PMI as a forward-looking economic indicator. Because the PMI measures new orders and hiring activity, among other things, we can reasonably expect prices of raw materials and energy to appreciate in the coming months as demand increases.

To get a better understanding of how the PMI affects commodities, watch my two-minute YouTube video by clicking here. Be sure to “thumbs up” the video and subscribe to our YouTube channel. Thank you!

Gold Market

This week spot gold closed at $1,899.84, up $38.26 per ounce, or 2.06 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher/lower by 1.39 percent. The S&P/TSX Venture Index came in up 1.92 percent. The U.S. Trade-Weighted Dollar retreated 0.88 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-29 | Germany CPI YoY | 0.0% | -0.2% | 0.0% |

| Sep-29 | Conf. Board Consumer Confidence | 90.0 | 101.8 | 86.3 |

| Sep-29 | Caixin China PMI Mfg | 53.1 | 53.0 | 53.1 |

| Sep-30 | ADP Employment Change | 649k | 749k | 481k |

| Sep-30 | GDP Annualized QoQ | -31.7% | -31.4% | -31.7% |

| Oct-1 | Initial Jobless Claims | 850k | 837k | 873k |

| Oct-1 | ISM Manufacturing | 56.5 | 55.4 | 56.0 |

| Oct-2 | Eurozone CPI Core YoY | 0.4% | 0.2% | 0.4% |

| Oct-2 | Change in Nonfarm Payrolls | 859k | 661k | 1489k |

| Oct-2 | Durable Goods Orders | 0.4% | 0.5% | 0.4% |

| Oct-8 | Initial Jobless Claims | 820k | — | 837k |

Strengths

- The best performing precious metal for the week was platinum, up 3.76 percent. Bank of America Research noted that platinum should benefit from the expansion of the fuel cell economy which uses the metal as a catalyst. Gold climbed back above $1,900 an ounce on Thursday as the dollar weakened, and investors weighed hopes for a new stimulus package from the U.S. government. The Bloomberg Dollar Spot Index fell as much as 0.5 percent – and gold typically moves in the opposite direction of the dollar.

- Silver had its best quarter since 2010, up a massive 27.62 percent for the three months ended September 30. Gold also had a strong quarter, up 5.89 percent despite a weak September. Holdings in gold-backed ETFs saw an eighth straight quarter of expansion. So far in 2020 they have added around 860 tons.

- Titan Co., India’s largest gold jeweler, rose 27 percent in the third quarter as investors bet on a demand recovery ahead of the key festive season. Gold prices in India had a second consecutive monthly loss but are still near record highs. The world’s second biggest consumer of gold often sees demand pick up ahead of its festival season where gold jewelry is a prominent part of gift-giving.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 2.06 percent. Gold had its biggest monthly loss in four years in September due to a stronger U.S. dollar. However, gold still had a quarterly gain supported by inflows into ETFs backed by the metal.

- The Perth Mint said gold coin and minted bar sales totaled 62,637 ounces in September, down from 67,462 in August. However, September sales were up 33 percent from the same period a year earlier.

- Ghana’s anti-graft agency is delaying the IPO of its gold royalty fund to complete a corruption risk assessment, reports Joy FM. The Ministry of Finance is being asked to provide documents and additional information on the fund that has been criticized for lacking transparency.

Opportunities

- Ramelius Resources reported first quarter gold production of 71,344 ounces, exceeding guidance of 65,000 to 70,000 ounces. The miner also shared it has a positive net cash position of A$205.7 million. Shandong Gold Mining, a state-backed Chinese miner, agreed to buy rival Hengxing Gold Holding for $393 million. Bloomberg notes that China has been encouraging bigger companies to take over smaller, privately-owned firms.

- Citigroup forecasts that central bank gold-buying will pick back up in 2021 after a slowdown this year. The bank sees demand rising to 450 tons after a drop to 375 tons in 2020 – the lowest figure in a decade. HSBC Securities predicts an increase to 400 tons after an estimated 3090 tons this year. Bloomberg notes that central bank purchases are an important driver of gold’s price action.

- Bloomberg’s Jake Lloyd-Smith share his four reasons why gold could make a comeback in October: 1) the dollar appears to have run its course, 2) global holdings in gold-backed ETFs were up 50 tons in September, 3) the Fed remains accommodative amid the pandemic and 4) the presidential election could stir up volatility.

Threats

- Disney is cutting 28,000 workers and Shell is cutting 9,000 jobs – sounding an economic alarm. Bloomberg reports that tens of thousands of layoffs were announced by blue-chip companies on Wednesday. This is a grim sign that the economic recovery could take much longer than expected.

- U.S. stocks fell on Friday after President Donald Trump announced he and the first lady had tested positive for the coronavirus. This creates uncertainty and could increase volatility in the markets. The Labor Department said American employers added 661,000 jobs in September, lower than forecasts for 857,500 new jobs, also contributing to the rocky market performance.

- Speculation is growing of a possible Barrick Gold and Freeport-McMoRan merger. Combining the companies would create the world’s largest gold and copper miner. However, many gold fund managers think this would not be a smart deal and could eliminate Barrick’s gold premium.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.87 percent. The S&P 500 Stock Index rose 1.61 percent, while the Nasdaq Composite climbed 1.48 percent. The Russell 2000 small capitalization index gained 4.56 percent this week.

- The Hang Seng Composite gained 1.62 percent this week; while Taiwan was up 2.31 and the KOSPI rose 2.15 percent.

- The 10-year Treasury bond yield rose 3 basis points to 0.691 percent.

Domestic Equity Market

Strengths

- Real estate was the best performing sector of the week, increasing by 4.87 percent versus an overall increase of 1.83 percent for the S&P 500.

- Paycom Software was the best performing S&P 500 stock for the week, increasing 16.86 percent.

- Warren Buffett’s Berkshire Hathaway officially disclosed its stake in Snowflake on Monday, confirming an $800 million gain on its investment in the cloud-data platform.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 2.85 percent versus an overall increase of 1.83 percent for the S&P 500.

- Halliburton was the worst performing S&P 500 stock for the week, falling 8.57 percent.

- The Tokyo Stock Exchange froze trading for an entire day on Thursday after experiencing its worst outage in history. A hardware error caused a system collapse.

Opportunities

- Steven DeSanctis, Jefferies equity strategist, told CNBC on Tuesday that many large technology stocks are getting "pricey" and investors should look for alternatives. "At nine times revenue, 10 times revenue, it gets a little pricey, and with that any bad news will actually be a huge detriment to these stocks," he said. DeSanctis recommends investors buy stocks in industrials, consumer discretionary, and materials sectors as alternatives.

- Stock bullishness across Wall Street is back to pre-pandemic levels – and will likely spike even more after the U.S. election, BofA says. After months of virus fears, record-breaking rallies, and unprecedented stimulus, Wall Street’s outlook for stocks is back to its pre-pandemic norm.

- The S&P 500’s 11 percent peak-to-trough sell-off in September has tested bullish investors as a resurgence in daily COVID-19 cases and uncertainty about additional stimulus and the November election hang over the stock market. But according to Fundstrat’s Tom Lee, investors can rest easy if the S&P 500 manages to close above a "line in the sand" of 3,363.31. If the market is able to close above that level, investors would have "a greater sense the worst is indeed behind us," Lee said.

Threats

- Famed economist David Rosenberg warns that Snowflake-led IPO mania is inflating a market bubble that could soon pop, writes Business Insider. Rosenberg is concerned about a marketplace that "is starting to look like the frenzy that took place in the dot-com bubble."

- Uber’s push to expand its food delivery empire just hit another roadblock as the DOJ scrutinizes its plan to buy Postmates. The DOJ put in a "second request," which signals it’s "concerned about the deal" according to former DOJ antitrust lawyer Sam Weinstein.

- As reported by Business Insider, traditional hedges are failing, and it is too dangerous to be buying more stocks during this sell-off, warns Academy Securities’ Peter Tchir.

The Economy and Bond Market

Strengths

- The Conference Board Consumer Confidence Index came in at 101.8 for September, the highest in six months. The metric exceeded the consensus estimate of 89.6.

- The number of Americans who applied for jobless benefits fell slightly in mid-September to the lowest level since the start of the coronavirus pandemic. Initial jobless claims filed through state programs dropped to 837,000 in the week ended September 26 from a revised 873,000 in the prior week, the Labor Department said Thursday.

- New orders for durable goods posted a fourth consecutive month of rebound in August, rising 0.5 percent following a gain of 11.7 percent in July, 7.7 percent in June and 15.0 percent in May.

Weaknesses

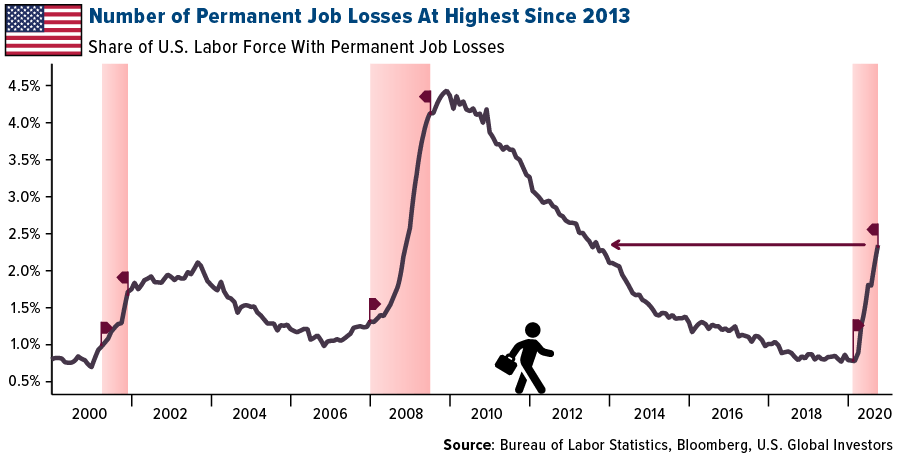

- The U.S. economy added fewer jobs than forecast in September, suggesting the recovery is slowing. The addition of 661,000 nonfarm payrolls missed the median estimate of 870,000 in a Bloomberg survey. A look at permanent job losses also paints a dismal picture. The share of total labor force with permanent employment loss continues to climb at a faster pace than during the Great Recession and is now the highest since 2013.

- The Commerce Department reported gross domestic product (GDP), the economy’s total output of goods and services, fell at a rate of 31.4 percent in the April to June quarter, only slightly changed from the 31.7 percent drop estimated one month ago.

- Personal income fell 2.7 percent in August, according to data from the Bureau of Economic Analysis. Personal income data over the past six months has been sharply distorted by lockdown policies which caused massive layoffs, and government stimulus programs that sent transfer payments skyrocketing. As those payments fade, measures of personal income and components are returning to trend. Disposable personal income fell 3.2 percent after a 0.3 percent increase in July.

Opportunities

- If the uncertainty surrounding America’s presidential election triggers a rout in the municipal-bond market, analysts at Citigroup said it will be a good time to buy. The advice echoes the bullish call the bank’s analysts made in March, when they suggested investors swoop in as a panic about the coronavirus sent the $3.9 trillion market into its biggest crash on record

- Next Wednesday’s minutes from the September Fed meeting might reveal policymakers’ views on what additional measures the Fed could take should America’s virus turnaround run into trouble. While officials have been keen to reassure markets that accommodative policy is here to stay, they’ve so far steered clear of discussing what other tools the Fed would consider using in its fight against the pandemic.

- Talks on another virus relief bill finally seem to be headed in the right direction and a deal could soon be within reach. If lawmakers are able to strike an agreement, it would add much needed support to the economy, which has been showing renewed signs of slowing down as the current fiscal support wanes.

Threats

- The White House said Friday that President Donald Trump was suffering “mild symptoms” of COVID-19, adding that he was in good spirits and working in the family quarters though the announcement of his illness threw the country deeper into uncertainty just a month before the presidential election. First lady Melania Trump also tested positive, the president said, and several others in the White House have, too, prompting concern that the White House or even Trump himself might have spread the virus further.

- State tax collections are expected to drop 11 percent by the end of fiscal year 2021 with the declines concentrated in the states that were hardest hit by the pandemic, according to Moody’s.

- The U.S. and China could be headed for a ‘new cold war’ lasting a generation that forces countries to pick sides, one analyst says. A split in ideology between the two superpowers could lead to a "new cold war" in the coming decades, Darren Tay of Fitch Solutions said at a virtual seminar, CNBC reported.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was wheat, up 5.33 percent after USDA data showed American wheat production was smaller than forecast. Zinc had its best quarter in nearly a decade – up 17.31 percent – driven by virus-related supply cuts and growing demand out of China.

- Silver had its best quarter since 2010, up a massive 27.62 percent for the three months ended September 30. Gold also had a strong quarter, up 5.89 percent despite a weak September. Holdings in gold-backed ETFs saw an eighth straight quarter of expansion. So far in 2020 they have added around 860 tons.

- Blue ammonia, a fuel that is produced through converting hydrocarbons into hydrogen and then ammonia, can be used in power stations to produce electricity without carbon emissions. The first shipment is on its way from Saudi Arabia to Japan. Aramco says blue ammonia “has the potential to make a significant contribution to an affordable and reliable low-carbon energy future.”

Weaknesses

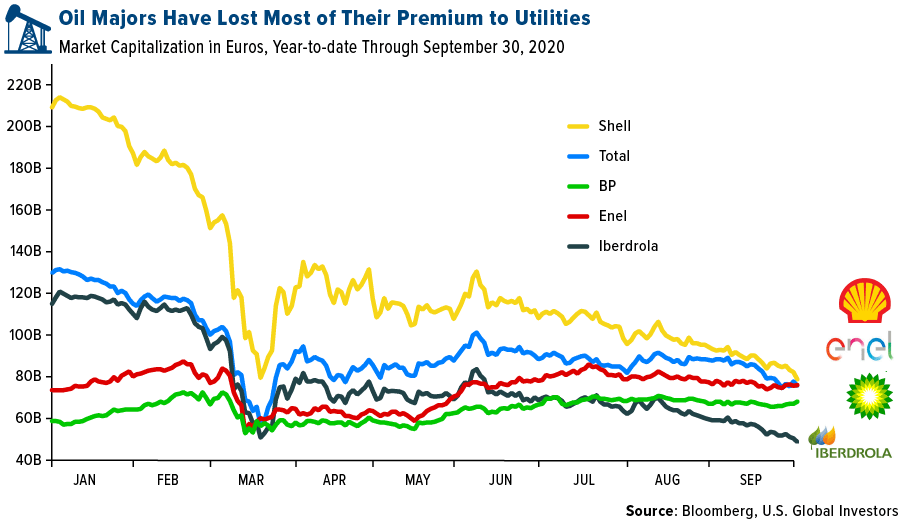

- The worst performing commodity for the week was natural gas, down 12.18 percent with the broader weakness in the oil markets. Crude oil fell to a two-week low due to conflicting signals of U.S. fiscal relief and rising supply from major producers, reports Bloomberg. Futures in New York fell as much as 6.5 percent on Thursday. Shell announced as many as 9,000 job cuts by the end of 2022, or around 11 percent of the workforce. The stock fell to the lowest in 25 years on Thursday, the day after announcing the news. Shell had the largest market cap among producers at the start of this year, and has seen its value tumble, along with most other oil majors to the extent they are trading like utility company valuations with no growth.

- President Trump has ruled out new oil and gas leasing along Florida, Georgia, and North and South Carolina from 2022 to 2032. This ban also halts the production of new offshore wind farms. Bloomberg reports that both oil drilling and wind energy advocates are condemning the approach.

- Exelon Corp, Illinois’s largest electric utility, is closing a pair of nuclear stations in 2021, which will eliminate thousands of jobs and severely cut local budgets. This shows how deep the financial risk is to small communities with economies tethered to single employers or industries. The Bryon Community Unit School District 22, west of Chicago, relies on the local Exelon plant for three fourths of its property taxes, reports Bloomberg.

Opportunities

- Devon Energy is acquiring WPX Energy in a $2.56 billion all-stock deal, creating one of the largest independent U.S. shale producers, reports Bloomberg. This is a positive signal for investors who have called for industry consolidation during a time of crisis for shale.

- Total SE announced plans for a bioplastics and chemical recycling plant at its Grandpuits refinery in France in efforts to make it a zero-crude platform by 2024, reports Bloomberg. The plant will produce 100,000 metric tons of PLA, a sugar-based and biodegradable plastic, a year.

- President Trump signed an executive order aimed at expanding domestic production of rare earth minerals to reduce dependence on China, which produces nearly 80 percent of the world’s supply of minerals critical to manufacturing sectors. The order declares a national emergency in the mining industry and directs the Interior Department to consider using the Defense Production Act to speed up the development of American mines.

Threats

- Vitol Group’s Chris Bake says crude prices have little room to rise in the fourth quarter as the recovery in global demand is slowing due to new coronavirus cases and restrictions. “The conventional wisdom going into the fourth quarter was that things were going to improve…it doesn’t feel like we have a huge catalyst.” Oil prices are holding just above $40 a barrel as renewed curbs on travel and social gatherings move through Europe.

- California Governor Gavin Newsom signed an executive order last week to phase out sales of new gasoline-powered cars by 2035, which could drive up power demand as much as 9.5 percent in the next 10 years. Bloomberg notes this could potentially crush the grid in the state where power supplies can be so tight that rolling blackouts are ordered.

- Copper miners in Zambia have halted $2 billion of planned investments, reports Bloomberg. The country introduced a new royalty tax last year and has made projects unviable, according to an industry lobby group. First Quantum Minerals said its $1 billion investment to extend the life of its local operation won’t move forward until the royalty is deductible from other corporate taxes. Zambia’s relationship with mining companies has deteriorated over the past 12 months as the country faces economic challenges.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 4.8 percent. The country’s’ economic data released this week was soft. Manufacturing PMI dropped below the 50 level in September. Economic sentiment, unemployment rate and gross wages were all reported lower as well. However, the Budapest Stock Exchange outperformed its peers, supported by strong gains in OTP Bank (the largest member of the Budapest Stock Exchange). Equities gained 9.5 percent over the past five days on the news that the bank’s Chairman Sandor Csanyi has been buying shares.

- The Hungarian forint was the best relative performing currency this week, gaining 2 percent. The currency recovered some of its loses from last week’s sell off. The central bank left its one-week deposit rate unchanged after a surprise hike of 15 basis points last week.

- Consumer discretionary was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.5 percent. The Russian government approved changes to the proposed tax hike putting pressure on commodity producers. With news of Donald Trump testing positive for COVID-19, the probability for Biden victory increased. Russia is an obvious loser from a potential Biden victory. Lukoil was the worst performing equity trading in the VanEck Russia ETF (RSX), losing 4.8 percent over the past five day. Lukoil shares declined with weakness in the oil price.

- The Turkish lira was the worst performing currency in the region this week, losing 1.5 percent. The currency continued to weaken against the U.S. dollar. This is due to softer economic data and a renewed threat of sanctions from EU for Turkey’s oil and gas exploration projects in the disputed water of the Mediterranean Sea near Greece.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- The final eurozone manufacturing PMI was unchanged from the flash reading of 53.7 in September. It is the highest reading in two years, supported by gains in output and new orders. In central emerging Europe, Poland, Turkey, Greece and Czech Republic reported their PMIs in the expandatory territory above the 50 level. Unexpectedly, Russia and Hungary’s PMIs dropped below the 50 level, indicating weakening manufacturing activity.

- E-commerce platform Allegro raised about 9.2 billion zloty ($2.3 billion) in Warsaw’s largest-ever listing after selling more shares than planned thanks to strong demand for technology-related stocks in Europe. The Warsaw stock exchange will have its big technology name, diversifying its holdings away from banks and utilities. The entrance of this high-tech company could attract new investors to the Polish stock market.

- The European Union agreed to sanction Belarus in order to pressure President Alexander Lukashenko to hold a fresh election. The deal was reached after Cyprus lifted its veto on the measures. Lukashenko was sworn in for a sixth term at a surprise ceremony on September 23, despite nation-wide protests and claims that the last held elections were not valid. While in exile, opposition leader Sviatlana Tsikhanouskaya said that she is the legitimate winner of the election.

Threats

- The European Commission released a critical report about the state of democracy in Hungary and Poland. This might limit these countries’ access to EU funds, including the new 750-billion-euro coronavirus recovery fund. Poland and Hungary have been criticized by the EU for putting courts, media, NGOs and academics under more state control.

- Turkey announced the country’s new economic program for years 2021-2023. The program will concentrate on rebalancing and sustainable growth with a focus on increasing exports and job creation. The GDP growth for 2020 is expected to be in positive territory at 0.3 percent; increasing by more than 5 percent in 2021.

- Eurozone’s economic sentiment rose to 91.1 in September versus consensus 89.0 and a prior month reading of 87.7. This is the fifth-consecutive month of improvement. However, the pace is slowing down with the number of coronavirus infections on the rise again. The confidence remains more than 30 percent below its pre-crisis level and evidence is building that the steep rebound following the end of lockdowns has started to level off.

China Region

Strengths

- India was the best performing country this week, gaining 3.5 percent. India’s manufacturing PMI for September rose for the second straight month to an eight-year high led by an increase in new orders after COVID-19 restrictions were loosened and production increased. Shriram Transport Finance was the best performing equity among the stocks trading in the iShares India ETF (INDA), gaining 11.6 percent over the past five days.

- The South Korea won was the best performing currency this week, gaining 71 basis points. The currency advanced supported by gains in equites and strong inflows into the nation’s bond market.

- Consumer durable stocks were the best performing among those trading on the Hong Kong Stock Exchange.

Weaknesses

- Pakistan was the worst performing market this week, losing 3.9 percent. With a sudden increase of COVID-19 infections, the country imposed new restrictions to prevent the spread. Moreover, the Indian and Pakistan deadly border fights continue souring investors’ confidence. Honda Atlas, a car producer, was the worst performing equity among stocks trading in the GlobalX MSCI Pakistan ETF (PAK), losing 13 percent over the past five days. The company announced a shares sale plan at a discount.

- The Philippine peso was the worst performing currency this week, losing 3 basis points. The central bank kept its overnight borrowing rate unchanged at 2.25 percent and trimmed its inflation forecast from 2.6 percent for 2020 to 2.3 percent. Second quarter GDP contracted by 16.5 percent and 8.8 percent contraction is expected in the third quarter.

- Health service stocks were the worst performing among those trading on the Hong Kong Stock Exchange.

Opportunites

- September’s purchasing manager’s index (PMI) data was released, and as expected China saw strong figures. Manufacturing PMI came in at 51.5, up from 51.0 in August and higher than expectations for a 51.3 number.

- The People’s Bank of China (PBOC) has pledged to increase support for the real economy and will ensure that new financing will focus on the manufacturing sector and small and medium-sized businesses. The bank stressed that monetary policy should be more flexible and targeted and called for a higher level of opening-up the financial sector.

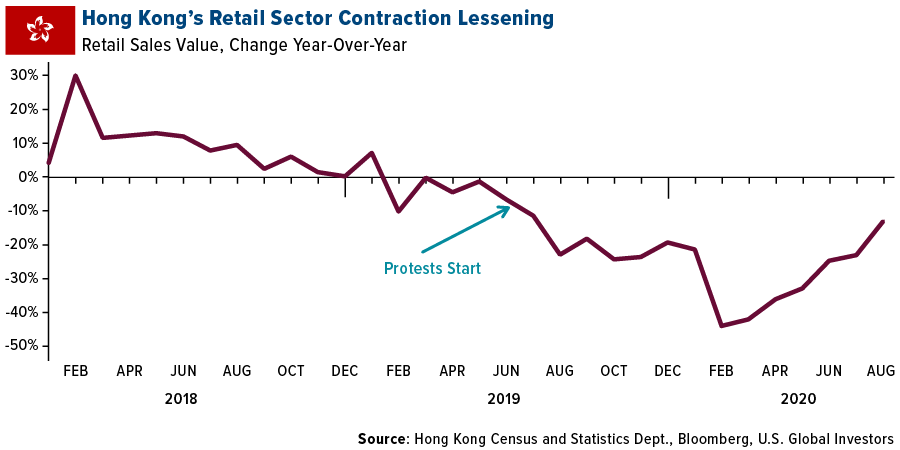

- Hong Kong retail sales are improving despite extended social distancing measures. Retail sales by value contracted 13.1 percent from a year earlier in August, which is better than the median forecast for a 17.5 percent decline. The figure is also far better than the 23.8 percent decline in July.

Threats

- The Trump administration issued new restrictions on technology exports to Semiconductor Manufacturing International Corp (SMIC), which is China’s largest semiconductor manufacturer. The Commerce Department warned that the exports could benefit the Chinese military, reports the Washington Post.

- A letter signed by 50 U.S. senators is urging trade representative Robert Lighthizer to start negotiating a comprehensive trade deal with Taipei to reduce American reliance on China. The senators wrote that a deal would “serve as a signal to other nations that Taiwan is a viable partner that is open for business.” A U.S. deal with Taiwan would likely greatly increase tensions with China.

- Hundreds of Hong Kong residents held an unauthorized protest on China’s National Day, which is an annual day of action to air grievances against China’s rule over Hong Kong. Police said 69 people have been detained and could face up to five years in prison for unauthorized assembly.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 2 was YFMoonshot, up 7,840 percent.

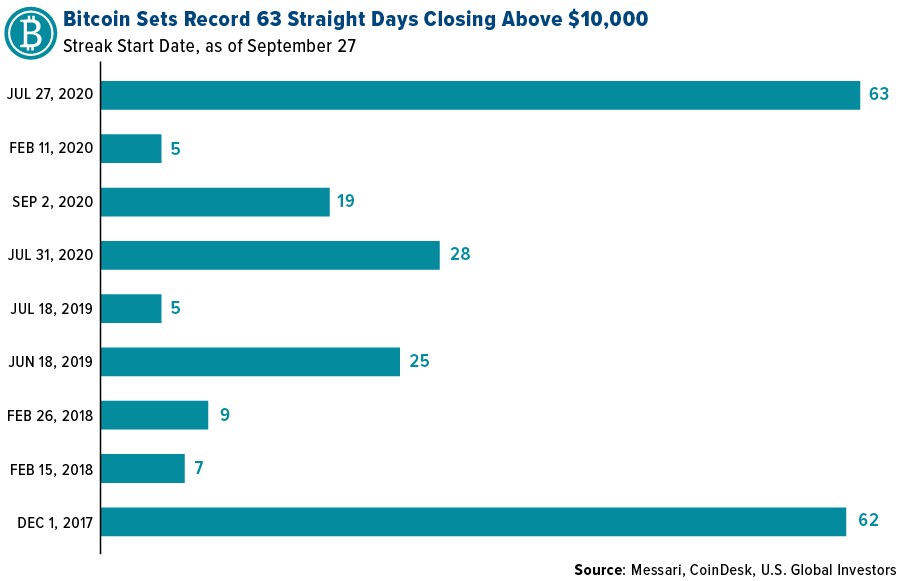

- The price of bitcoin closed above $10,000 for 63 straight days on September 28, setting a new record streak. The digital currency formerly went 62 days above that level between December 1, 2017, and January 31, 2018.

- Venezuela has announced a 90-day trial for a decentralized stock exchange supporting “alternative digital assets” and fiat currencies, writes CoinTelegraph. Despite the international sanctions, the country aims to have a global reach. The exchange is known as BDVE and its website claims that the platform comprises “the first decentralized stock exchange in the world.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended October 2 was BTC3L, down 96.29 percent.

- District police have arrested a 36-year-old man from the Malappuram district of the south Indian state of Kerala on charges of operating a cryptocurrency scam, writes CoinTelegraph. Nishad, who is also the managing director of startup Long Rich Technologies, has been charged under the Prize Chits and Money Circulation Schemes Act. Several documents were seized from Nishad’s house showing he allegedly duped thousands of people from across India of hundreds of thousands of dollars.

- The U.S. Commodity Futures Trading Commission, or CFTC, has charged the BitMEX derivatives exchange with operating an unregistered trading platform and violating anti-money laundering regulations, writes CoinTelegraph. A statement released Thursday shows the CFTC filed a civil enforcement action against five entities and three individuals who allegedly own and operate the exchange.

Opportunities

- Diginex’s stock, a digital finance company, has listed on the Nasdaq exchange under the ticker symbol EQOS, writes CoinTelegraph. Diginex is the “first Nasdaq-listed company that covers the full virtual currency ecosystem,” CEO Richard Byworth told CoinTelegraph in an interview. “This is hugely important for the development of the industry. Prior to this, you’ve pretty much only had exposure to direct crypto assets via ETF-like structures.”

- A tech talent marketplace known as Braintrust has raised an $18 million strategic growth round, bringing its total funding to date to $24 million. Employing a system of blockchain-based tokens to align the incentives of users and keep fees low, Braintrust boasts a nice mix of seasoned Silicon Valley VCs and crypto heavyweights, the article explains, including Pantera, Multicoin and Galaxy Digital.

- Demand for bitcoin is surging in India, particularly in urban tech hubs, reports Coindesk, meaning that smart-contract platforms like Ethereum and others are also gaining momentum. Promoted by Switzerland-based Interchain Financial, Cosmos is especially finding traction with students like Aditya Nalini at the Vellore Institute of Technology.

Threats

- An unreleased project being built by Yearn’s Andre Cronje known as Eminence, has been drained of $15 million, reports CoinTelegraph. Excitement for the upcoming project quickly reached fever pitch, “with the community FOMOing roughly $15 million into the EMN protocol,” the article explains. Unfortunately, the protocol was quickly exploited and drained.

- Foreigners granted remote access to Estonia’s digital infrastructure through its e-residency program are being linked to cryptocurrency frauds abroad, writes Bloomberg. This threatens efforts to repair the nation’s image after one of Europe’s largest money laundering scandals. A report by the police’s Financial Intelligence Unit outlines how Estonian firms and e-residents have also been linked to organizing “suspicious initial coin offerings and the misappropriation of large sums within them.”

- Coinbase Inc.’s newly announced policy of not debating politics at work has garnered criticism from Twitter’s CEO Jack Dorsey, with Dorsey saying it runs counter to the core principles of cryptocurrency. Dorsey argues that the entire purpose of cryptocurrencies like bitcoin, which is traded on Coinbase, is social activism.

Airline Sector

Strengths

- Airlines are touting coronavirus tests to lure travelers. Hawaiian Airlines is offering customers drive-through COVID testing in California to help Hawaii-bound travelers avoid a 14-day quarantine rule. United is offering on-the-spot testing to customers flying to Hawaii for $250 to avoid the two-week quarantine. Airports are also offering rapid tests to bring back travel. The Rome airport introduced rapid screening on September 16, reports Bloomberg.

- Airbus is preparing to deliver its first American-made A220 jetliner to Delta later this month, doubling down on its Alabama site with a new assembly line building this model after making more than 180 A320s, reports Bloomberg. Despite a long-running dispute with the World Trade Organization, Airbus’ U.S. facility has expanded its global reach.

- JetBlue Airways President Joanna Geraghty, citing Harvard’s School of Public Health data, says that wearing a mask and HEPA air filtration systems yield a “less than 1 percent risk of transmitting COVID in an aircraft.” This positive data could help spur an increase in air travel if passengers are confident that they have a low chance of contracting the virus from another passenger.

Weaknesses

- The airline industry continues to cut jobs around the world. British Airways says it could cut as many as 10,000 jobs. Lufthansa said it plans to cut its fleet by 100 jets and shed 22,000 full-time positions. Singapore Airlines will eliminate 20 percent of its workforce – about 4,300 jobs.

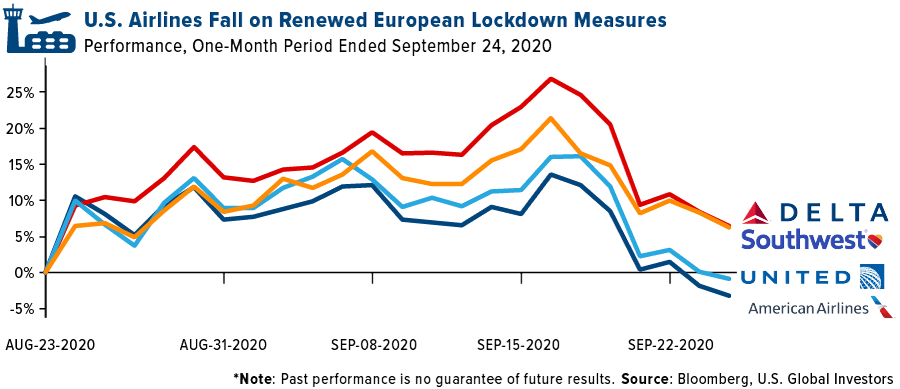

- Coronavirus cases are spiking back up – especially in Europe. U.S. carrier stocks, in addition to global carriers, fell after rising early in the month on the news that new lockdown measures are in place. Some fear this is the “second wave” of cases moving through Europe and could expand to the U.S. A grim milestone was reached in the pandemic – 1 million deaths from the virus globally.

- Tourism is also suffering from the lack of air travel. U.K. hotel operator Whitbread said it plans to eliminate nearly one in five jobs, or about 6,000 workers. The U.K. announced bars will start closing and companies should again have people work from home if possible. Daily COVID cases rose above 4,000 – a number not seen since May.

Opportunities

- Airlines continue to get creative on new sources of income. Thai Airways is opening up its Airbus and Boeing flight simulators to the public, reports Bloomberg. Starting in October, customers can get into a mock cockpit for 30-minutes for around $380. The carrier also transformed its cafeteria into an airplane-themed restaurant complete with plane seats and furniture made from spare jet parts. Australia’s Qantas Airways is selling fully stocked bar carts from its retired Boeing 747 fleet for $1,000 – complete with mini wine bottles. Singapore Airlines has turned its A380 superjumbo jet into a pop-up restaurant.

- American Airlines announced it will begin updated computer-based training for pilots on the grounded Boeing 737 Max in late October. Bloomberg reports the carrier expects all pilots to be re-trained by January and is laying out plans for the Max’s returns “in the near future.” This is a big win for Boeing that a major carrier is showing confidence in the troubled jet’s return to the skies.

- United Airlines boosted its flight schedule in October. The major domestic carrier will fly 40 percent of its schedule from the same month last year, up from 34 percent of its year-earlier schedule in September.

Threats

- Tens of thousands of U.S. airline workers are set to lose their jobs on October 1. The government aid package in March gave carriers support for payroll in return for not cutting jobs until the end of September. However, it seems unlikely that another relief package will pass before then, forcing carriers to make massive staff reductions due to the continued decimation in air travel with a recovery not seen in the near future.

- The impending Brexit could threaten British pilots. A no-deal exit of Britain from the European Union at year-end could deprive British pilots of the right to fly EU-registered planes. Bloomberg notes that The Department of Transport is hoping for a bilateral agreement on aviation safety that would include mutual recognition of pilot licenses.

- According to Air New Zealand’s CEO, quarantine-free travel between Australia and New Zealand is unlikely to resume for at least another six months. Plans for a safe-travel corridor to stimulate tourism was put on hold after renewed coronavirus outbreaks in both countries, reports Bloomberg.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.69 | +0.03 | +5.34% |

| Oil Futures | 36.99 | -3.26 | -8.10% |

| Hang Seng Composite Index | 3,694.05 | +58.88 | +1.62% |

| S&P Basic Materials | 397.67 | +4.75 | +1.21% |

| Korean KOSPI Index | 2,327.89 | +49.10 | +2.15% |

| S&P Energy | 222.55 | -6.54 | -2.85% |

| Nasdaq | 11,075.02 | +161.46 | +1.48% |

| DJIA | 27,682.81 | +508.85 | +1.87% |

| Russell 2000 | 1,542.15 | +67.24 | +4.56% |

| S&P 500 | 3,351.69 | +53.23 | +1.61% |

| Gold Futures | 1,907.00 | +40.70 | +2.18% |

| XAU | 142.84 | +2.88 | +2.06% |

| S&P/TSX VENTURE COMP IDX | 708.69 | +13.43 | +1.93% |

| S&P/TSX Global Gold Index | 362.25 | +3.47 | +0.97% |

| Natural Gas Futures | 2.47 | +0.33 | +15.29% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,327.89 | -36.48 | -1.54% |

| 10-Yr Treasury Bond | 0.69 | +0.04 | +6.47% |

| Gold Futures | 1,907.00 | -37.70 | -1.94% |

| S&P Basic Materials | 397.67 | -18.19 | -4.37% |

| S&P 500 | 3,351.69 | -229.15 | -6.40% |

| DJIA | 27,682.81 | -1,417.69 | -4.87% |

| Nasdaq | 11,075.02 | -981.42 | -8.14% |

| Oil Futures | 36.99 | -4.52 | -10.89% |

| Hang Seng Composite Index | 3,694.05 | -244.56 | -6.21% |

| S&P/TSX Global Gold Index | 362.25 | -18.35 | -4.82% |

| XAU | 142.84 | -9.55 | -6.27% |

| Russell 2000 | 1,542.15 | -50.14 | -3.15% |

| S&P Energy | 222.55 | -40.40 | -15.36% |

| S&P/TSX VENTURE COMP IDX | 708.69 | -40.95 | -5.46% |

| Natural Gas Futures | 2.47 | -0.02 | -0.80% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 142.84 | +15.78 | +12.42% |

| S&P/TSX Global Gold Index | 362.25 | +21.63 | +6.35% |

| Gold Futures | 1,907.00 | +95.00 | +5.24% |

| DJIA | 27,682.81 | +1,855.45 | +7.18% |

| S&P 500 | 3,351.69 | +221.68 | +7.08% |

| Nasdaq | 11,075.02 | +867.39 | +8.50% |

| Korean KOSPI Index | 2,327.89 | +192.52 | +9.02% |

| Natural Gas Futures | 2.47 | +0.73 | +42.21% |

| S&P Basic Materials | 397.67 | +35.56 | +9.82% |

| Russell 2000 | 1,542.15 | +110.29 | +7.70% |

| Oil Futures | 36.99 | -3.66 | -9.00% |

| Hang Seng Composite Index | 3,694.05 | +16.58 | +0.45% |

| S&P/TSX VENTURE COMP IDX | 708.69 | +81.18 | +12.94% |

| S&P Energy | 222.55 | -60.91 | -21.49% |

| 10-Yr Treasury Bond | 0.69 | +0.02 | +3.13% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2020):

Qantas Airways Ltd

American Airlines Group Inc

United Airlines Holdings Inc

Delta Air Lines Inc

Southwest Airlines Co

Deutsche Lufthansa AG

Singapore Airlines Ltd

JetBlue Airways Corp

Hawaiian Holdings Inc

OTP Bank

Lukoil

Ramelius Resources Ltd

Barrick Gold Corp

Total SA

Microsoft Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

–>