Pierre Lassonde Says Gold Could Hit $25,000 in 30 Years

Date Posted: September 20, 2019

Read time: 55 min

This year marked the 30th anniversary of the Denver Gold Forum (DGF), the world's most prestigious precious metal equities investment conference.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

This year marked the 30th anniversary of the Denver Gold Forum (DGF), the world’s most prestigious precious metal equities investment conference. The invitation-only event, held earlier this week, was attended by an incredible seven-eighths of the world’s publicly traded gold and silver companies by production, as well as leading metals and mining executives, money managers, analysts and investors.

We were one of the founding members of the DGF back in 1989, when I first bought a controlling interest in U.S. Global Investors. During this year’s forum, I was honored and moved to be recognized for our company’s contribution to the group’s creation and ongoing legacy.

U.S. Global gold and precious metal expert Ralph Aldis and I had the opportunity to meet with a number of companies and analysts while at the DGF. We were surprised to learn that some were still unaware that quantamental factors were being applied more and more to gold equities investing. Here at U.S. Global, for example, we like to combine old-fashioned, bottom-up stock selection with cutting-edge quant strategies such as data mining and machine learning.

30 Years of (Denver) Gold

|

Indeed, much has changed in the precious metals and mining industry in the past 30 years, as we were all reminded by my longtime friend and mentor Pierre Lassonde. Pierre, as many of you know, is the legendary co-founder, along with Seymour Schulich, of Franco-Nevada, the first publicly-traded gold royalty company. What you may not know is that Pierre is also one of Canada’s most gracious philanthropists and currently serves as the chairman of the Canada Council for the Arts Board of Directors.

According to Pierre, annual global gold demand has exploded in the years since the first DGF was held. Demand grew more than fivefold, from a value of $32 billion in 1989 to $177 billion in 2018.

Loyal readers know that today’s central banks are net buyers of gold as they seek to diversify away from the U.S. dollar. But 30 years ago, they were net sellers. In 1989, banks collectively unwound as much as 432 tonnes from their reserves. Compare that to last year, when they ended up buying some 651.5 tonnes, the largest such purchase since the Nixon administration, with Russia and China leading the way.

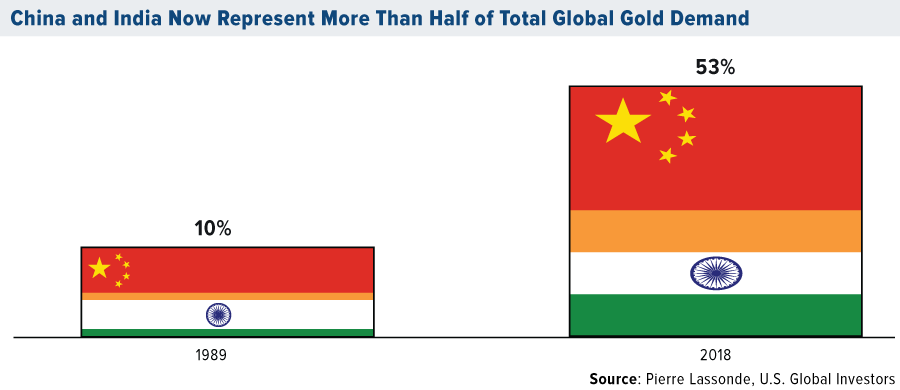

Speaking of China… Pierre pointed out to us that we’ve seen a significant shift in gold demand over the past 30 years, from west to east, as incomes in China and India—or “Chindia”—have risen. In 1989, Chindia’s combined share of global demand for the precious metal was only about 10 percent. Fast forward to today, and it’s 53 percent!

“Don’t forget the Golden Rule,” Pierre said. “He who has the gold makes the rules!”

The Gold Price in 2049 Will Be…

One of the highlights of Pierre’s presentation was his forecast for the price of gold in the next 30 years. After analyzing gold’s historical compound annual growth rate (CAGR) over the past 50 years, ever since President Nixon formally took the U.S. off the gold standard, Pierre says he sees an average price target of $12,500 an ounce by 2049. And under the “right” conditions, it could go as high as $25,000!

“I think gold is in a good place,” Pierre told Kitco News’ Daniela Cambone on the sidelines of the DGF. “The financial demand is being driven by negative interest rates. Should the U.S. Treasury 30-year bond yield ever, ever go negative, like in Germany and France, God bless, we’re looking at $5,000 gold.”

I’m sure Pierre will have more to add when he joins me on our upcoming gold opportunities webcast, to be held October 31. Save the date, and stay tuned for more details!

ESG Investing Goes Mainstream

One of my own observations of how the DGF has changed over the last 30 years is the way in which mining companies pitch their stock to investors. Before, they would jump right into financials, production costs, mining feasibility and the like. Today, however, they begin by discussing topics such as sustainability and environmental impact.

You may have heard of ESG investing—which stands for environmental, social and governance. This set of criteria has grown in importance among “socially conscious” investors over the past decade, as you can see in the chart below. In the U.S. alone, assets under management (AUM) in ESG-oriented funds and ETFs have more than doubled from approximately $40 billion in 2013 to $90 billion in 2019, according to Morningstar data. In Europe, where institutional investors and money managers must now comply with certain ESG standards, the figure’s likely even higher.

Please don’t get the wrong idea. If these issues are important to investors, they should be free to allocate their money toward companies whose beliefs are aligned with their own.

My concern is that companies, money managers and institutional investors are increasingly pressured—especially by European governments—to comply with an ever-shifting set of standards, or else face divestment or, in extreme cases, being delisted from a stock exchange.

Take Norway’s government pension fund. Valued at more than $1 trillion, it’s the largest such fund in the world. It got this big largely thanks to the country’s highly profitable North Sea oilfields. But based on a recent recommendation from the Norwegian parliament, the fund is actively dumping all of its fossil fuel stocks.

Then there’s just the general confusion and inconsistency over what constitutes an ESG-compliant company, and who can invest if the company is deemed out of compliance. Every government in Europe, it seems, has its own definitions, disclosures and regulations. To operate in France, for instance, asset managers are now required to disclose how climate change considerations are incorporated in their investment decisions. The same is true for pension funds in the Netherlands.

All of these extra rules and procedures come at a cost for everyone involved, from the companies themselves to asset managers. At the DGF, I heard that one mining company in particular had to pay as much as $40 million just to remain ESG-compliant. I worry too about directors and board members joining companies who care only about sustainability and have little regard for creating value for shareholders.

Gold’s “Green Credentials” May Be Understated: RBC

The good news is that gold and gold mining look very attractive from an ESG perspective. Gold’s “green credentials,” in fact, may be understated, according to a recent report by the Royal Bank of Canada (RBC). For one, owning physical gold—in coins, bars or jewelry—has absolutely no environmental impact and actually increases a portfolio’s ESG rating.

As for gold mining, the process gives off significantly less greenhouse gasses (GHG) on a per dollar basis relative to some other mined products, including aluminum, steel, coal and zinc. What this means is that gold has a much smaller “carbon footprint” than what some people might think.

Many mining companies are also working to meet some investors’ changing attitudes. IAMGOLD, for instance, is investing heavily in solar infrastructure, and its mine in Burkina Faso is the world’s largest hybrid solar/thermal plant, according to RBC. Newmont Goldcorp is moving forward with its “Smart Mine Initiative,” which uses optimizer software to maximize ore recovery and minimize waste. And Torex Gold has developed what it calls the “Muckahi Mining System,” which alleges to limit surface disruption and reduce the use of fossil fuels underground.

In the same report, RBC says it remains “positive on gold,” writing that the metal’s “deep liquidity, near global acceptance and role as a ‘perceived safe haven’ and ‘store of value’ make it very difficult to displace” as an investment.

Want more on the Denver Gold Forum? Find out why investors are cautiously bullish on the yellow metal by watching my latest video!

Gold Market

This week spot gold closed at $1,516.90, up $28.25 per ounce, or 1.90 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.19 percent. The S&P/TSX Venture Index came in up just 0.22 percent. The U.S. Trade-Weighted Dollar rose 0.22 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-17 | Germany ZEW Survey Current Situation | -15.0 | -19.9 | -13.5 |

| Sep-17 | Germany Zew Survey Expectations | -38.0 | -22.5 | -44.14 |

| Sep-18 | Eurozone CPI Core YoY | 0.9% | 0.9% | 0.9% |

| Sep-18 | Housing Starts | 1250k | 1364k | 1215k |

| Sep-18 | FOMC Rate Decision (Upper Bound) | 2.00% | 2.00% | 2.00% |

| Sep-19 | Initial Jobless Claims | 213k | 208k | 206k |

| Sep-24 | Conf. Board Consumer Confidence | 133.0 | — | 135.1 |

| Sep-25 | New Home Sales | 656k | — | 635k |

| Sep-26 | Hong Kong Exports YoY | -7.3% | — | -5.7% |

| Sep-26 | GDP Annualized QoQ | 2.0% | — | 2.0% |

| Sep-26 | Initial Jobless Claims | 211k | — | 208k |

| Sep-27 | Durable Goods Orders | -1.2% | — | -2.0% |

Strengths

- The best performing metal this week was silver, up 3.16 percent, as gold rebounded this week. As gold was set for a small weekly gain for the first week in four, traders were mostly bullish or neutral on bullion’s trajectory in the weekly Bloomberg survey. Palladium, however, rallied as much as 1.8 percent to a record $1,648.65 an ounce for its best run since 2012 with seven weeks of gains. The precious metal is gaining from tighter supplies. Although car sales are down slightly, stricter environmental standards are creating a need for more palladium loading in auto catalysts, which are used to reduce pollution from vehicles.

- The yellow metal bounced back above $1,500 per ounce, recovering from a fall Wednesday, after the Federal Reserve announced a 25 basis point rate cut. Carsten Menke, head of research at Julius Baer, says he expects gold to move higher to $1,575 an ounce in the next three months due to further rate cuts. Swiss gold exports rose to the highest level since 2016 in August due to increased demand from the U.K. offsetting lower demand in Asia, according to customs data.

- Investors now appear to be shifting money down market to smaller capitalization names as confidence grows in duration of the coming gold cycle. On Tuesday, investors poured $193 million into the VanEck Junior Gold Miners ETF (GDXJ), the largest ETF that invests in junior gold miners. The fund attracted the most money in more than two years on growing optimism that companies will perform strongly alongside higher gold prices, reports Bloomberg.

Weaknesses

- The worst performing metal this week was platinum, down 0.27 percent, as hedge funds cut net bullish platinum positions. As mentioned above, gold took a tumble on Wednesday after Fed policymakers were spilt over the need for additional rate cuts after the one announced this week. Bob Haberkorn, senior market strategist at RJ O’Brien & Associates LLC, said in a phone interview with Bloomberg that “if you’re a gold trader right now, you’re a little confused.” Turkey’s central bank gold holdings fell $615 million from the previous week, but reserves are still up 34 percent year-over-year.

- It’s rare for the Department of Justice to bring criminal Racketeer Influenced and Corrupt Organizations Act (RICO) charges, but it just did. Bloomberg reports that two current and one former JPMorgan Chase & Co. metals traders were charged with RICO criminal violations for rigging precious metal futures markets over the course of a decade. The three individuals are accused of engaging in “a massive, multiyear scheme to manipulate the market for precious metals futures contracts and defraud market participants.”

- Negative rates just got more negative for a record group of bank clients in Denmark. Jyske Bank A/S is offering the first 10-year mortgage at negative coupons and said that it has no choice but to drag more retail depositors into its negative-rates after the country’s central bank lowered its policy rate to minus 0.75 percent, writes Bloomberg. CEO Anders Dam said in a statement: “Due to the rate reduction last week, we are losing even more money. And we need to share that bill with some of our clients.”

Opportunities

- At the Denver Gold Forum earlier in the week, China Gold International Resources Corp. said it is on the hunt for M&A deals worth as much as $2 billion. Executive Vice President Jerry Xie said in an interview that they need more pipeline in gold production and are looking for acquisition opportunities “quite aggressively.” And there could be big opportunity for deals as many mining companies could use some lowering of general and administrative (G&A) costs, according to Shareholders’ Gold Council. In a recent report, the group writes that $2.5 billion of profits generated by 47 gold companies goes to pay the salaries and costs of head office management and boards, while financial markets discount the value of these companies by approximately $21 billion. M&A generally helps lower G&A costs for the company that got taken out.

- RBC writes that by 2025 it sees the gold sector in better shape. It forecasts that margins will improve and that output will be broadly flat due to the inability to stop the decline of reserves. “To deliver improved margins and sustain mine life, companies will need to stay active in both M&A deal and exploration, making strategic direction on these fronts critical, in our view.” Output will also continue to fall due to a lack of new technological developments on how to extract the metal from the ground.

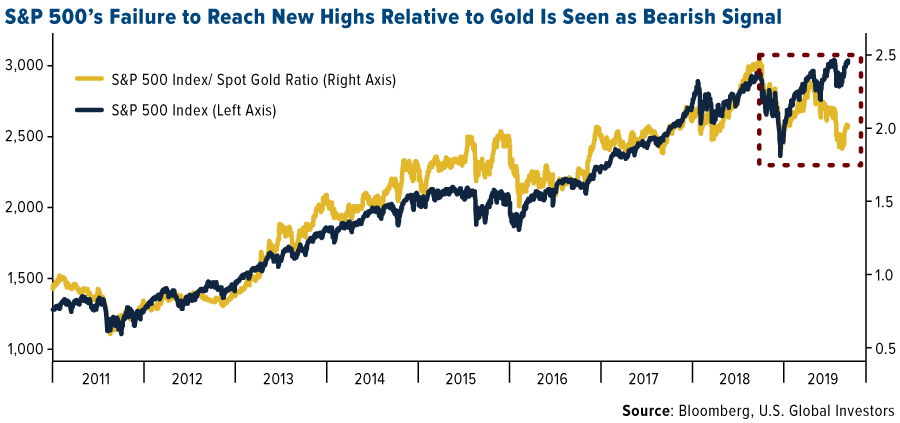

- HSBC wrote in a note this week that global mining capex is now two years into a more sustainable and product-driven cycle and is unlikely to return to levels last seen in 2012 during the China commodity boom due to better capital discipline. According to Mike Wilson, chief U.S. equity strategist at Morgan Stanley, the S&P 500’s instability to reach new highs relative to gold “raises questions about the quality of this month’s rally” in stocks, reports Bloomberg. As seen in the chart below, the S&P 500 divided by the price of gold has fallen in 2019, indicating gold is beginning to outpace the broader markets.

Threats

- Bloomberg’s Liz Capo McCormick writes that there is not enough cash on hand at major Wall Street firms to meet the funding demands of a market trying to absorb record Treasury bond sales needed to cover U.S. budget deficits. She adds that there isn’t enough liquidity and that there are deep structural problems in the money markets. The big catalyst causing the squeeze in repo liquidity is the big swath of new Treasury debt that settled into the marketplace just as cash left due to quarterly tax payments to the government.

- The liquidity issue as discussed above could get worse. Bloomberg’s Stephen Spratt reports that the dollar-funding squeeze, which rocked short-term interest rate markets this week, may deepen further due to the upcoming quarter end when banks usually start their pattern of cutting back on providing liquidity. Another round of Treasury auctions next week could leave markets short of another $45 billion in cash. Spratt writes that those two factors could explain why stress is showing up in bill sales and currency markets even after the Fed took measures to ease a liquidity shortage.

- The Organization for Economic Cooperation and Development (OECD) cut almost all economic forecasts it made just four months ago as intensifying trade conflicts have sent global growth momentum tumbling. The organization forecasts world growth at 2.9 percent this year, a level not seen since the last financial crisis.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.05 percent. The S&P 500 Stock Index fell 0.52 percent, while the Nasdaq Composite fell 0.72 percent. The Russell 2000 small capitalization index lost 1.17 percent this week.

- The Hang Seng Composite lost 2.76 percent this week; while Taiwan was up 0.94 percent and the KOSPI rose 2.07 percent.

- The 10-year Treasury bond yield fell 18 basis points to 1.719 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing by 2.20 percent versus an overall decrease of 0.51 percent for the S&P 500.

- Incyte Corp was the best performing stock for the week, increasing 6.25 percent.

- Datadog Inc.’s IPO was a huge success with a market debut that stood out as one of the best so far this year. The shares opened more than 49 percent above the $27 offering price, the seventh largest first day pop among technology IPOs in 2019.

Weaknesses

- Consumer discretionary was the worst performing sector for the week, decreasing by 2.16 percent versus an overall decrease of 0.51 percent for the S&P 500

- Fedex Corp was the worst performing stock for the week, falling 14.54 percent.

- OxyContin maker Purdue Pharma filed for bankruptcy protection. Purdue reached a tentative deal to resolve lawsuits with 24 states and five U.S. territories, as well as the lead lawyers for more than 2,000 cities, counties and other plaintiffs, the company said.

Opportunities

- Risk appetite may be set to improve, at least according to one indicator. The Citi U.S. Economic Surprise Index, which measures data surprises relative to market expectations, climbed above zero last week for the first time since February. If that move is sustained, a reversal in the downtrend for 10-year Treasury yields may be on the way, and that could in turn be a positive for risk assets, particularly stocks.

- Toyota is working on an innovative solar-powered electric car that can run forever and never needs charging. The Japanese car giant has partnered with Sharp and NEDO (New Energy and Industrial Technology Development Organization of Japan) to create the vehicle.

- Fitbit is in talks with investment bank Qatalyst Partners about exploring a potential sale, according to Reuters. The company’s stock surged 7 percent on the news of the possible deal.

Threats

- Video game retailer GameStop is closing 180 to 200 of stores as it attempts to stay afloat. GameStop CFO Jim Bell said he expects a "much larger" group of stores will be closed in the next one to two years.

- FedEx disappointed shareholders again by slashing its profit outlook. At least four analysts downgraded the company, sending shares tumbling Wednesday by the most in four years. While FedEx said trade tensions were weakening the global economy and sapping demand for parcel deliveries, the company’s critics emphasized “elusive’’ business execution, an insufficient grip on costs and “acquisition debacles.”

- Uber and Lyft just took a major blow in California, and now they’re gearing up for war. California lawmakers approved a landmark bill that would force gig-economy companies like Uber, Lyft and others to treat many workers as employees instead of independent contractors, throwing their business models into question.

The Economy and Bond Market

Strengths

- The U.S. economy is outperforming expectations by the most this year, offering a fresh rebuttal to last month’s resurgent recession fears fueled by the trade war and a manufacturing slump. The Bloomberg Economic Surprise Index reached an 11-month high after four indicators released Thursday, including existing home sales and jobless claims, each surpassed expectations. The gauge continued to advance after swinging to positive from negative on Tuesday for the first time this year.

- U.S. factory output increased in August by more than forecast in a broad advance that signals manufacturing may be starting to stabilize. Production at manufacturers rose 0.5 percent, Federal Reserve data showed Tuesday, exceeding the median estimate in a Bloomberg survey of economists, after falling the prior month. Total industrial production, which also includes output at mines and utilities, increased 0.6 percent, the most in a year as crude oil extraction bounced back after Hurricane Barry depressed drilling in the Gulf of Mexico a month earlier.

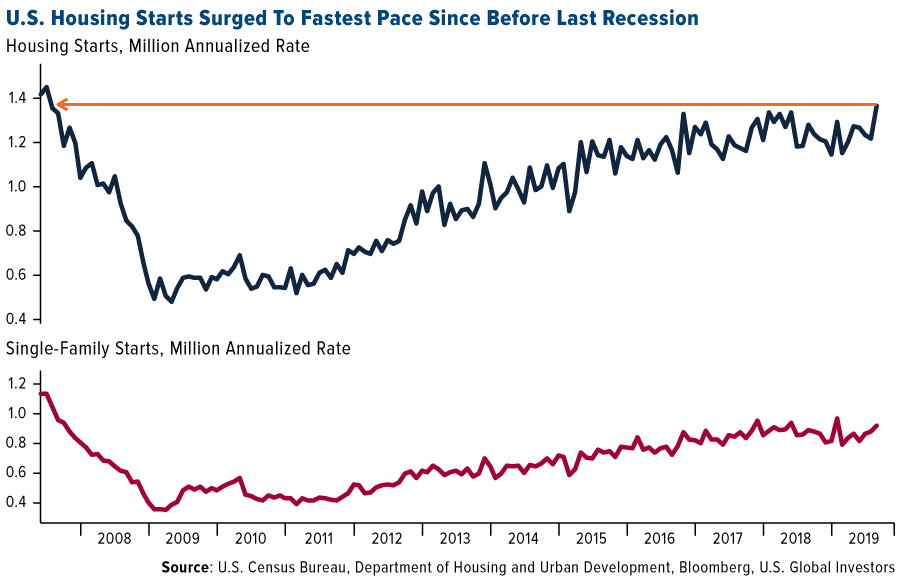

- U.S. home construction surged in August to the fastest pace since mid-2007 on more apartment projects and single-family houses, a welcome sign for the housing sector that has struggled to gain momentum. Residential starts climbed 12.3 percent to a 1.36 million annualized rate after an upwardly revised 1.22 million pace in the prior month, according to government figures released Wednesday.

Weaknesses

- China’s slowdown deepened in August: industrial output growth fell to a 17 and a half year low. Despite a slew of growth-boosting measures since last year, the world’s second largest economy has yet to stabilize, and analysts say Beijing needs to roll out more stimulus to ward off a sharper slowdown.

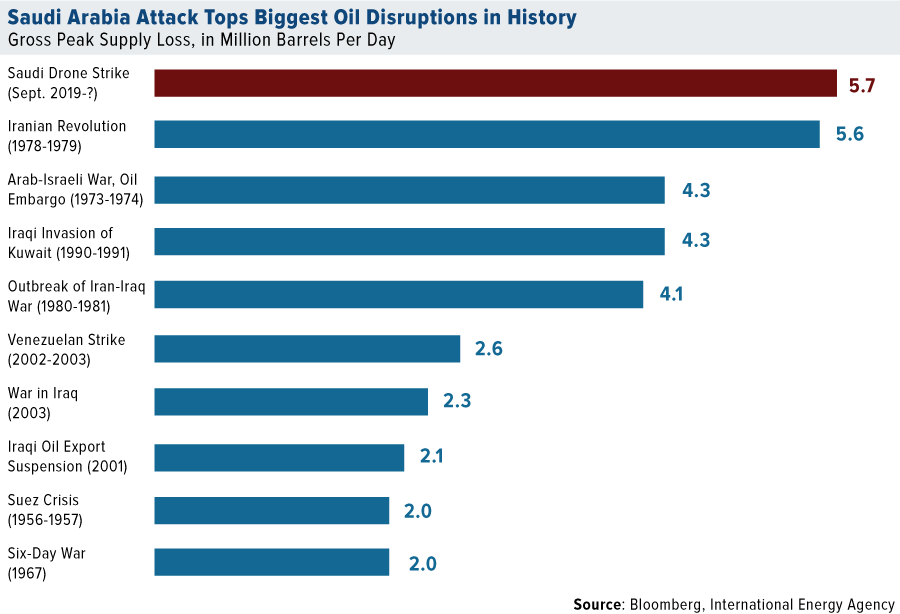

- Oil spiked as much as 20 percent after a sudden attack on Saudi oil supplies over the weekend. The attack affected almost 6 million barrels of daily production or about 5 percent of global output.

- The liquidity issue as discussed above could get worse. Bloomberg’s Stephen Spratt reports that the dollar-funding squeeze, which rocked short-term interest rate markets this week, may deepen further due to the upcoming quarter end when banks usually start their pattern of cutting back on providing liquidity. Another round of Treasury auctions next week could leave markets short of another $45 billion in cash. Spratt writes that those two factors could explain why stress is showing up in bill sales and currency markets even after the Fed took measures to ease a liquidity shortage.

Opportunities

- President Donald Trump said on Monday the United States has reached an initial trade agreement with Japan. In a letter to Congress released by the White House, Trump said he intends to enter into the deal on tariff barriers in the coming weeks.

- Next week, all eyes will be on economic releases, kicking off with the preliminary Markit PMIs for September on Monday.

- The data barrage intensifies on Friday, with personal income and spending numbers, the core PCE price index and durable goods orders.

Threats

- The Organization for Economic Cooperation and Development (OECD) cut almost all economic forecasts it made just four months ago as intensifying trade conflicts have sent global growth momentum tumbling. The organization forecasts world growth at 2.9 percent this year, a level not seen since the last financial crisis.

- “While risks clearly exist related to trade and geopolitical concerns, lowering rates to address uncertainty is not costless,” says Federal Reserve Bank of Boston President Eric Rosengren. “Additional monetary stimulus is not needed for an economy where labor markets are already tight, and risks further inflating the prices of risky assets and encouraging households and firms to take on too much leverage.”

- The CEO of Pimco, which manages $1.8 trillion, says the U.S. economy will slow to just 1 percent growth in 2020.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was crude oil, which gained 5.91 percent. Oil had its best weekly gain since January after Brent crude oil had its biggest-ever one day jump, according to Bloomberg data. Crude prices spiked early in the week after attacks on Saudi Arabia’s processing facilities over the weekend disabled 5 percent of global supply. The nation vowed to restore production within the next few weeks.

- According to a report from EnergySage Inc., the average cost for U.S. homeowners to install rooftop solar systems fell below $3 per watt for the first time ever, which is 23 percent lower than the cost five years ago. Overall, solar energy is becoming more affordable and is being installed globally even without subsidies. BloombergNEF reports that several European nations continue to build solar farms as developers become increasingly efficient and drive down costs. Spain is building 2,484 megawatts worth of subsidy-free solar projects while Italy has 569 megawatts in the works.

- Russia and Ukraine signaled progress toward an agreement to transport natural gas into Europe. Bloomberg reports that energy ministers from the two nations met with European Union (EU) officials and all voiced optimism that they could overcome tensions that have threatened to halt contracts needed to ensure gas keeps flowing into Europe from Russia. At least 14 countries get half of their gas from Russia, which is transported through Ukraine.

Weaknesses

- The worst performing major commodity for the week was iron ore, which fell 6.94 percent. Steelmakers globally are feeling the pain of slowing growth, a dragged out trade war and higher iron ore prices from the first half of the year. Bloomberg reports that U.S. Steel joined Nucor and Steel Dynamics in reducing its outlook for the quarter. The company has fallen almost 40 percent so far this year. Bloomberg reports that Japan’s top steelmakers, Nippon Steel Corp. and JFE, warned last month that full-year profit will drop. Europe’s ArcelorMittal also cuts its estimate for global demand growth.

- Zambia, the world’s second-largest copper producer, could double power tariffs to offset a shortfall from its drought-stricken hydropower dams, reports Bloomberg. The nation has an electricity deficit of more than 700 megawatts and wants to import electricity from South Africa. However, it would cost significantly more. Mining companies account for about half of Zambia’s power demand and have yet to be impacted by power cuts. The increase in prices would negatively affect the companies by increasing their costs for operating in the country.

- Although the world’s biggest manufacturer of fuel from coal is making changes to improve profitability, it is still struggling with the global move away from the fossil fuel. Sasol Ltd. announced this week that it plans to sell its South African coal-mining business, reports Bloomberg. The company produces about 40 million tons of coal a year from its mines. The company is facing cost overruns and delays at its giant Louisiana chemicals project that the company hopes will transform its production mix to focus on chemicals. Sasol shares have fallen 48 percent in the past year.

Opportunities

- There was a range of good news in the wind energy space this week. According to a statement on Thursday, Denmark-based Orsted A/S plans to use 12-megawatt turbines made by GE for projects off the coast of Maryland and New Jersey. Bloomberg reports that the turbines are 853 feet long—almost as tall as New York’s Chrysler building. The cost of offshore wind continues to fall, especially in England. The world’s biggest offshore wind park planned off the coast of England will likely generate power cheaper than coal in the next decade, writes William Mathis. Lastly, wind power in Texas is about to surpass coal. According to a report from Rystad Energy, wind power is forecast to generate 87 terawatt-hours of electricity in 2020, which is greater than the expected 84 terawatt-hours from coal.

- Investors, and teenagers, are demanding government action on climate change. Greta Thunberg, a 16-year-old environmental activist, backed a global movement that went underway on Friday where students in Europe, Australia and elsewhere are skipping school and workers are walking off jobs to demand action on climate change. Investors are also calling for change. On Wednesday a group of investment managers who oversee $16 trillion in assets called on companies to implement anti-deforestation policies for their supply chains, reports Bloomberg. Stephanie Pfeifer, CEO of the Institutional Investors Group on Climate Change, said “climate change is such a critical issue for investors’ portfolios and there are so many risks associated with it and also huge opportunities.”

- With the rise of cheaper renewable energy, nuclear power plants are looking to make more than just power, reports Bloomberg’s Will Wade. FirstEnergy Corp, Xcel Energy Inc. and Pinnacle West Capital Corp. are planning to use reactors to produce hydrogen as a part of a U.S. Energy Department program aimed at helping the industry develop new sources of revenue.

Threats

- Over the weekend, Saudi Arabia suffered strikes on its oil processing plants that forced the kingdom to shut down half of its production, which led to 5 percent of the world’s supply being cut off. Although the nation claims that production will be back up and running in just a few weeks, there could be further geopolitical trouble. There are disagreements over who initiated the attack as Saudi Arabia suggested Iran is behind it while Yemen’s Houthi movement claimed responsibility. U.S. Secretary of State Mike Pompeo accused Iran of carrying out an “act of war.”

- European Trade Commissioner Cecilia Malmstrom told a conference in Brussels on Friday that relations are tense between the U.S. and the EU regarding auto tariffs, reports Bloomberg. Malmstrom said, “We firmly reject that we are a security threat. That is absurd. If there will be tariffs there, we would take countermeasures.” Last year, tensions rose between the powers after President Trump imposed tariffs on steel and aluminum, among other goods, after citing security threats. The EU then retaliated with tariffs on American goods. According to the European Commission, a 25 percent tax on foreign cars by the U.S. would add 10,000 euros to the price of EU vehicles imported.

- Indonesia is experiencing a particularly bad year for forest fires, reports Bloomberg News. The fires are largely caused by illegal slash-and-burn methods to clear farmland for palm oil, pulpwood and rubber trees. Almost 3,000 hotspots were detected in mid-September and over 320,000 hectares of land have burned in the first eight months of this year. The fires could have a big impact on Indonesia’s economy, the world’s largest producer of palm oil, as the fires disrupt operations at plantation and mills.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 2.3 percent. The country is preparing for presidential elections in November. Despite recent political noise, economic growth has been robust. Second quarter GDP surprised to the upside with Romania recording strong growth of 4.4 percent. Year-to-date Romanian equites are up 21 percent.

- The Russian ruble was the best performing currency this week, gaining 80 basis points against the U.S. dollar. The ruble appreciated alongside the price of crude oil, which increased sharply this week after Saudi Arabia’s oil production facilities were attacked by drones, removing more than 5 percent of global oil supply from the market.

- Energy was the best performing sector among eastern European markets this week. Motor Oil, a Greek refinery, was the best preforming equity gaining more than 6 percent.

Weaknesses

- Turkey was the worst performing country this week, losing 2.8 percent. The attacks on Saudi Arabia’s oil production could delay Turkey’s efforts to bring down inflation and stimulate growth as oil prices may stay elevated. Turkey imports almost all of its energy needs. Moreover, further escalation of tensions in the Middle East could push the lira lower against the U.S. dollar.

- The Polish zloty was the worst performing currency in the region this week, losing 65 basis points. On Friday, the zloty dropped sharply after the EU Court of Justice set October 3 as a date for its final ruling regarding swiss franc loans. The courts’ final decision may negatively impact the market value of the Polish banking industry’s $33 billion portfolio of non-zloty denominated mortgages.

- Industrial was the worst performing sector among eastern European markets this week. Tekfen, a Turkish construction Company, was the worst preforming equity losing more than 9 percent.

Opportunities

- The aforementioned drone attack on Saudi Arabia’s oil production facilities could push oil prices higher, and higher oil prices will be beneficial to oil producing countries, such as Russia. The currencies of the oil producing nations are likely to outperform near-term as well. In Emerging Markets, the Colombian peso and Russian ruble have the strongest correlation with Brent crude oil.

- The German economic outlook improved in September. The ZEW Survey Expectation Index was reported at negative 22.5, up from the eight-year low of minus 44.1 it reported in August. The stronger data could indicate concerns eased about the impact of the U.S. – China trade war and Brexit. However, the results of the survey were still gloomier than the long-term average.

- JPMorgan initiated a research report on Greek banks, recommending an overweight position in Eurobank and National Bank of Greece. Their call is based on the macro recovery, which is still in an early state and fragile, but they like the banks’ progress on reduction of bad loans. They added that the market likely underestimates the magnitude of bad debt reduction and how soon it will feed through.

Threats

- The ECB’s chief economist said in a prepared speech in London on Monday that incoming information is signaling a more extended slowdown in Euro area growth dynamics than previously expected. The ECB once again reiterated that it would do whatever it takes to stimulate the economy and raise inflation. If needed, the bank will further lower the deposit facility rate and the money market rate.

- Financial Times reported that European lenders are facing deeper cost cuts and consolidation after the ECB announced a prolonged stretch of negative interest rates last week. The newly announced tiering system designed to shield a portion of lenders’ deposits at the ECB from negative rates will barely offset the lost earnings from lower base rates.

- Eastern Europe has a highly skilled work force, but people still leave their home countries to look for better work opportunities elsewhere, mostly due to corruption and lower pay compared to other nations. Brain drain is a common problem for Romania, Ukraine and Serbia. It contributed to 600,000 people from these three countries combined leaving in 2016 for better jobs and life prospects around the world. That is three times more than the outflow in 2000, according to the Organization for Economic Cooperation and Development.

China Region

Strengths

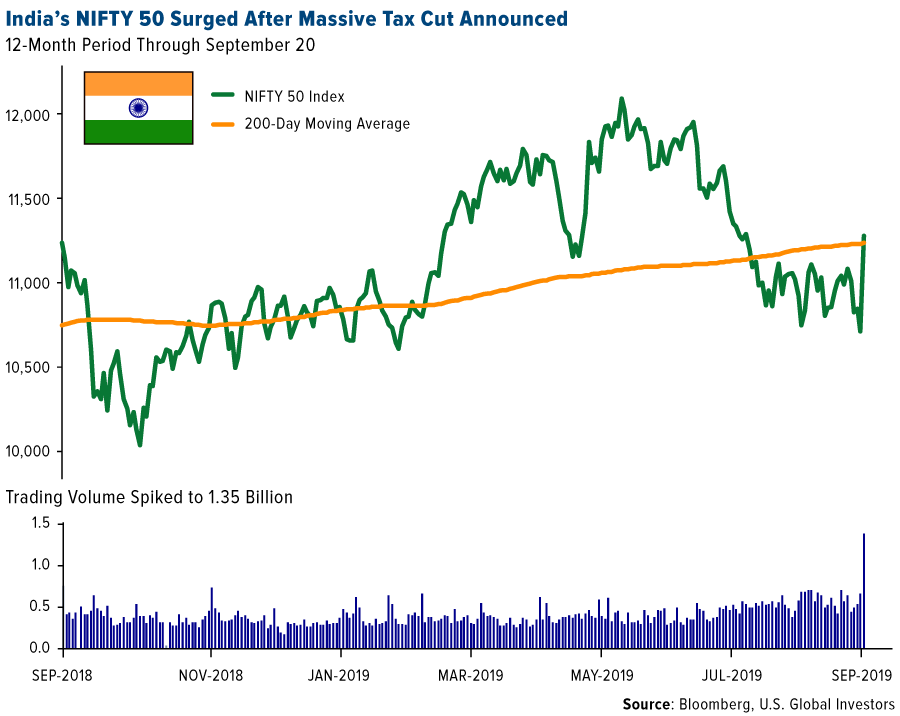

- The best performing indices in the region for the week were Korea’s KOSPI, up 2.07 (although the index was closed the 12th and 13th last week) and Taiwan’s Capitalization Weighted Stock Index, which was up 1.13 percent since its return from holiday. Vietnam’s Ho Chi Minh was up 43 basis points; Malaysia’s KLCI rose 13 basis points. Of special note are India’s NIFTY and SENSEX Indices, which jumped by 1.91 and 1.68 percent on the week, respectively, in a massive surge on Friday following the government’s announcement of a major stimulative corporate tax cut.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index was consumer services, which climbed 4.04 percent on the week.

- Singapore’s non-oil domestic exports jumped 6.7 percent for the August measurement period, outperforming expectations for a gain of only 1.6 percent and rising the prior period’s revised growth of 3.5 percent.

Weaknesses

- The worst-performing index in the region was Hong Kong’s Hang Seng Composite, which declined by 2.76 percent on the week.

- The laggard sector in Hong Kong’s Hang Seng Composite Index this week was financials, which fell 3.73 percent.

- We continued to see a degree of weakening in Chinese data. Retail sales clocked in at only a 7.5 percent year-over-year growth rate, shy of expectations for a 7.9 percent print. Industrial output for the same period was up only 4.4 percent, below consensus for a 5.2 percent showing, and FAI came in at only 5.5 percent through the first eight months of the year.

Opportunities

- In what has of late developed into a regularly weekly comment, there remains opportunity for a degree of resolution to the U.S.-China trade war, which could potentially have immediate positive effects upon investor sentiment and add more corporate certainty. While it seems unlikely things will change overnight, the relative centrality of the U.S.-China trade issues and the size of the two juggernaut economies mean collectively that any positive developments, resolution, interim deal, etc. could well provide markets a boost.

- Taiwan’s TWSE now lies only about 1.5 percent off its 52-week highs, bouncing back strongly and sharply from its August trading range lows.

- North Korean leader Kim Jong Un sent President Donald Trump a letter, various media sources are reporting this week, in which Kim offered for President Trump to visit Pyongyang and announced hopes for a third summit between the two leaders.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. Latest developments in the week as of time of writing involved the Chinese cancellation of a planned tour through U.S. farmland as well as an announcement by President Trump that he has no interest in a partial deal. The two sides, which began talks again this week, are—so far as we know right now—still planning on high-level talks in mid-October, shortly after Chinese holidays and shortly before the (as-of-now-delayed) implementation of the October 1 tariff hike that was pushed back to October 15.

- As unrest has continued in Hong Kong, Bloomberg News reported that air traffic in the city declined by 12 percent for the August measurement period as the violence and protests continue to take a clear toll on the SAR. Moody’s Investors Service lowered its outlook to negative from stable for Hong Kong, though it did affirm the Aa2 rating. More protests are scheduled for this upcoming weekend.

- The U.S. dollar remains relatively strong, which could create headwinds for emerging markets already caught, to some degree, amid a degree of slowing global growth and trade uncertainty.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 20 was Silverway, up 279.48 percent.

- In a Tuesday press release, Wells Fargo announced the development of a U.S. dollar-linked stablecoin that will run on the firm’s first blockchain platform. The tokenized dollar, Wells Fargo Digital Cash, will be used in a pilot initially for internal settlement across the company’s business, CoinDesk reports. Even the company’s international locations will be able to move funds using the token.

- Argo Blockchain, which trades publicly on the London stock exchange, announced the installation of 1,000 more mining machines, according to a report on September 19. The new machine count would take the company’s total number of miners to 6,000, reports Coindesk, and Argo plans to acquire another 6,000 of them in the next two quarters.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 20 was Opennity, down 37.74 percent.

- In an announcement on September 13, the U.S. Department of the Treasury sanctioned three North Korean entities for cyber crimes, reports CoinDesk, mentioning cryptocurrency thefts as one of the reasons for the action. The entities are believed to be responsible for the theft of $571 million worth of cryptos from five exchanges in Asia in 2017 and 2018.

- As reported by Tech.co, Facebook’s Libra cryptocurrency has “hit another snag.” Both France and Germany have decided to block its launch in their respective countries over concerns that the social media giant is overstepping its authority, the article explains.

Opportunities

- OpenSC, a joint venture and blockchain startup, announced Monday $4 million in seed funding for ethical supply chain management to track goods for ethical malpractice, reports CoinDesk. According to incoming OpenSC CEO Markus Mutz, the capital will be used to further develop blockchain-based suppky chains such as overfishing and human rights violations.

- After receiving final regulatory approval, messaging app LINE has officially launched a cryptocurrency exchange, dubbed Bitmax, which will service its 80 million users based in Japan, reports CoinDesk. In a statement on Tuesday, the Shinjuku-based messaging provider said the service is now live with trading of five crypto assets including bitcoin, ethereum, ripple, bitcoin caseh and litecoin.

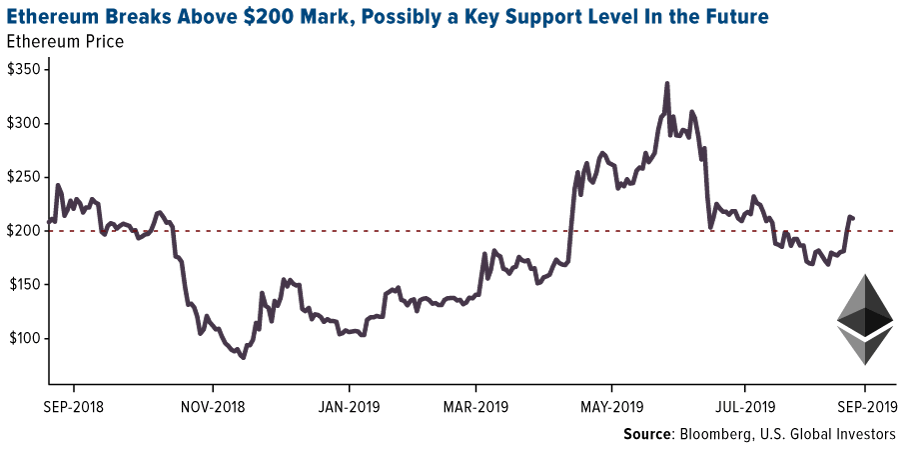

- Despite bitcoin erasing gains, Ethereum has been able to extend its momentum. The cryptocurrency has been able to break above the $200 mark, which will likely prove to be a key support level in the near term.

Threats

- At this week’s Gartner IT Symposium/Xpo, analysts at Gartner have been discussing how businesses and IT leaders can create value from blockchain technology. According to a press release from the group, however, lack of interoperability standards could prevent deployment of this technology across financial services ecosystems for at least three years. “Blockchain standards for financial services companies are currently fragmented and immature,” senior research director at Gartner Fabio Chesini said. “We are three to five years until standards mature and settle.”

- According to a September 17 filing, the Cboe BZX Exchange withdrew its VanEck/SolidX bitcoin ETF proposal, just weeks after VanEck and SolidX began offering shares of the Trust to qualified institutional buyers. As reported by CoinDesk, a decision on the proposal had already been delayed numerous times, and a final deadline of approval or rejection by the SEC was set for October 18 – which could have made this one of the very first bitcoin ETFs in the country.

- The world’s seventh-largest blockchain by market cap, EOS, has a value topping $3 billion since February 2019. As CoinDesk explains, however, the project “has long been plagued by fears that its structure was too centralized, and now the lion’s share of entities that govern the chain are in China, prompting fears of state intervention.”

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 251.09 | +15.62 | +6.63% |

| Gold Futures | 1,523.40 | +23.90 | +1.59% |

| Natural Gas Futures | 2.54 | -0.07 | -2.87% |

| S&P/TSX VENTURE COMP IDX | 589.52 | +0.36 | +0.06% |

| 10-Yr Treasury Bond | 1.72 | -0.18 | -9.43% |

| Nasdaq | 8,117.67 | -59.04 | -0.72% |

| Oil Futures | 58.09 | +3.24 | +5.91% |

| Hang Seng Composite Index | 3,571.07 | -101.54 | -2.76% |

| S&P 500 | 2,991.73 | -15.66 | -0.52% |

| DJIA | 26,935.07 | -284.45 | -1.05% |

| Korean KOSPI Index | 2,091.52 | +42.32 | +2.07% |

| Russell 2000 | 1,559.69 | -18.45 | -1.17% |

| S&P Energy | 452.25 | +4.44 | +0.99% |

| S&P Basic Materials | 366.12 | -3.19 | -0.86% |

| XAU | 94.60 | +5.11 | +5.71% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.54 | +0.37 | +17.00% |

| S&P/TSX Global Gold Index | 251.09 | -1.64 | -0.65% |

| 10-Yr Treasury Bond | 1.72 | +0.13 | +8.11% |

| Oil Futures | 58.09 | +2.41 | +4.33% |

| Gold Futures | 1,523.40 | +7.70 | +0.51% |

| S&P 500 | 2,991.73 | +67.30 | +2.30% |

| S&P Energy | 452.25 | +25.17 | +5.89% |

| Hang Seng Composite Index | 3,571.07 | +50.74 | +1.44% |

| DJIA | 26,935.07 | +732.34 | +2.79% |

| Korean KOSPI Index | 2,091.52 | +126.87 | +6.46% |

| Nasdaq | 8,117.67 | +97.47 | +1.22% |

| S&P Basic Materials | 366.12 | +11.52 | +3.25% |

| Russell 2000 | 1,559.69 | +49.84 | +3.30% |

| S&P/TSX VENTURE COMP IDX | 589.52 | +13.62 | +2.36% |

| XAU | 94.60 | +0.07 | +0.07% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.54 | +0.35 | +16.20% |

| 10-Yr Treasury Bond | 1.72 | -0.31 | -15.28% |

| DJIA | 26,935.07 | +181.90 | +0.68% |

| Oil Futures | 58.09 | +1.44 | +2.54% |

| S&P 500 | 2,991.73 | +37.55 | +1.27% |

| Gold Futures | 1,523.40 | +115.10 | +8.17% |

| S&P Energy | 452.25 | -14.49 | -3.10% |

| Nasdaq | 8,117.67 | +66.33 | +0.82% |

| Korean KOSPI Index | 2,091.52 | -39.77 | -1.87% |

| S&P Basic Materials | 366.12 | +3.14 | +0.87% |

| Russell 2000 | 1,559.69 | -3.80 | -0.24% |

| Hang Seng Composite Index | 3,571.07 | -218.74 | -5.77% |

| S&P/TSX Global Gold Index | 251.09 | +34.61 | +15.99% |

| S&P/TSX VENTURE COMP IDX | 589.52 | -3.74 | -0.63% |

| XAU | 94.60 | +12.81 | +15.66% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2019):

Tekfen Holding AS

Eurobank Ergasias SA

National Bank of Greece SA

Motor Oil Hellas Corinth Refin

IAMGOLD Corp

Newmont Goldcorp Corp

Torex Gold Resources Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001). The Korea Composite Stock Price Index or KOSPI is the index of all common stocks traded on the Stock Market Division—previously, Korea Stock Exchange—of the Korea Exchange. The Taiwan Capitalization Weighted Stock Index is a stock market index for companies traded on the Taiwan Stock Exchange (TWSE). The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The FTSE Bursa Malaysia KLCI, also known as the FBM KLCI, is a capitalization-weighted stock market index, composed of the 30 largest companies on the Bursa Malaysia by market capitalization that meet the eligibility requirements of the FTSE Bursa Malaysia Index Ground Rules. The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market. Sensex, otherwise known as the S&P BSE Sensex index, is the benchmark index of the Bombay Stock Exchange (BSE) in India. The Citigroup U.S. Economic Surprise Index is a quantitative measure of economic news. It is defined as a weighted historical standard deviation of data surprises (actual releases versus the Bloomberg survey median). A positive reading of the Economic Surprise Index suggests that economic releases have on balance [been] beating consensus. It is calculated daily in a rolling three-month window.