Retire Happy With Dollar Cost Averaging

Date Posted: March 29, 2019

Read time: 57 min

This week I had the pleasure of attending and presenting at the Oxford Club's 21st Annual Investment U Conference in St. Petersburg, Florida. As many as 400 accredited investors were in attendance from all over the U.S.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

This week I had the pleasure of attending and presenting at the Oxford Club’s 21st Annual Investment U Conference in St. Petersburg, Florida. As many as 400 accredited investors were in attendance from all over the U.S.

The main topic was the current retirement crisis, which I wrote about earlier this month. Baby boomers are reaching retirement in worse financial shape than the previous generation—a phenomenon we haven’t seen in at least six decades.

So how can we reverse course and assure future generations are financially prepared to leave the workforce?

A common theme running through many of the Oxford presentations was to start investing early and to take advantage of compound interest.

This is so important. Albert Einstein once described compounding as “the eighth wonder of the world.”

If you’re reading this and have kids or grandkids, I urge you to help them on the path to participating in the market now. It doesn’t require as much capital as you might think—especially if you’re investing with dollar cost averaging.

What is does require, though, is discipline. Put a long-term plan in place and let compound interest work its magic.

I’ve shared this chart with you before, but I think it’s worth sharing again. It shows a hypothetical initial investment of $1,000 in an S&P 500 Index fund in March 2009. Ten years later, after regular monthly contributions of only $100, the value of that initial investment grew at an annualized 12.96 percent to more than $26,385. Investors who had the discipline to stick with this plan and reinvest the dividends were rewarded handsomely.

Remember, the illustration above includes only the period during the 10-year bull market, and there’s no guarantee that the good times will continue.

But with dollar cost averaging, some of the guesswork involved in market timing is eliminated. Our own plan, which we call the ABC Investment Plan, automatically lets you purchase more shares when prices are low and fewer shares when they’re high.

The ABC Plan doesn’t assure a profit, of course, or fully protect against losses. No investment plan can guarantee those things.

Nevertheless, because it requires only a small initial investment, I think it’s a great way to get a young person started in today’s market. The Plan is also helpful for people who might be worried about their retirement goals but unsure how to build their wealth.

It’s never too late to start participating. Download an application today by clicking here.

The 10 Percent Golden Rule

I’d like to address a question I received over email this week from an investor. He asked for clarification on my 10 Percent Golden Rule. As you know, I often recommend a 10 percent weighting in gold, with 5 percent in physical gold and 5 percent in gold mining stocks.

“What does ‘weighting in gold’ actually mean?” he wrote. After explaining that he already owns a number of gold and silver coins, he asked how he knows if he has enough.

First of all, I think these are excellent questions.

The best way to show what I mean is with a visual. Below is a hypothetical portfolio of stocks, bonds, real estate, options, hard assets and more. To keep things simple, let’s say the total portfolio value is $1 million.

Using the 10 Percent Gold Rule, your total gold allocation would be valued at approximately $100,000, with $50,000 in physical gold (coins, bars and 24-karat jewelry) and the remaining $50,000 in gold mining equities, including mutual funds and ETFs.

Of course, asset prices are always fluctuating, which is why I also remind investors to rebalance their portfolios at least once a year. If gold shoots up in price, it might make sense to take some profits. If it plunges in price, consider it a buying opportunity.

The Fear Trade Is Heating Up Gold Mining Stocks

|

As a reminder, there are a number of important reasons why the 10 percent rule might make sense.

For one, a certain amount of gold has been shown to improve a portfolio’s Sharpe ratio, or its risk-adjusted returns relative to its peers, based on standard deviation. The higher the ratio is over its peers, the better the risk-adjusted returns. One recent study found that an institutional portfolio with a 6 percent weighting in gold had a higher Sharpe ratio than one without any gold exposure.

This means that volatility was reduced without hurting returns.

This week I gave you another reason.

Yields are sliding all over the world right now on concerns that the global economy is slowing. Here in the U.S., the 10-year Treasury yield ended the week at 2.41 percent, after President Donald Trump’s nominee for the Federal Reserve Board, Stephen Moore, said he was in favor of cutting interest rates half a percentage point.

With regard to our discussion here, gold has historically traded inversely to bond yields. When yields have fallen, the yellow metal has shined.

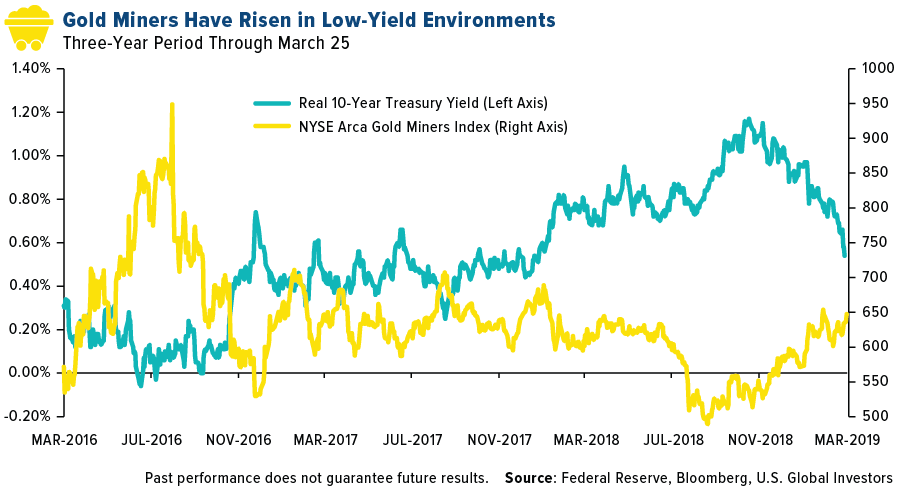

Gold mining stocks have behaved similarly. Take a look below. What the chart shows is the inverse relationship between gold mining stocks and the real 10-year Treasury yield—“real” meaning inflation-adjusted. As you can see, gold stocks soared in the summer of 2016 as yields deteriorated and finally dipped below zero.

Today, yields are similarly on a downward path, boosting gold stocks. From its 2019 low on January 22, the NYSE Arca Gold Miners Index is up more than 14 percent.

For more on gold stocks, watch my recent interview with Kitco News’ Daniela Cambone, live from the New York studio, by clicking here!

Gold Market

This week spot gold closed at $1,292.2, down $21.50 per ounce, or 1.64 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.46 percent. The S&P/TSX Venture Index came in off 1.71 percent. The U.S. Trade-Weighted Dollar rose 0.62 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-26 | Hong Kong Exports YoY | -2.4% | -6.9% | -0.4% |

| Mar-26 | Housing Starts | 1210k | 1162k | 1273k |

| Mar-26 | Conf. Board Consumer Confidence | 132.5 | 124.1 | 131.4 |

| Mar-28 | GDP Initial Jobless Claims | 2.3% | 2.2% | 2.6% |

| Mar-28 | Initial Jobless Claims | 220k | 211k | 216k |

| Mar-28 | Germany CPI YoY | 1.5% | 1.3% | 1.5% |

| Mar-29 | New Home Sales | 620k | 667k | 636k |

| Mar-31 | Caixin China PMI Mfg | 50.0 | — | 49.9 |

| Apr-1 | Eurozone CPI Core YoY | 0.9% | — | 1.0% |

| Apr-1 | ISM Manufacturing | 54.5 | — | 54.2 |

| Apr-2 | Durable Goods Orders | -1.6% | — | 0.3% |

| Apr-3 | ADP Employment Change | 180k | — | 183k |

| Apr-4 | Initial Jobless Claims | 216k | — | 211k |

| Apr-5 | Change in Nonfarm Payrolls | 178k | — | 20k |

Strengths

- The best performing metal this week was platinum, up 0.26 percent as money managers boosted their positions on expectations for higher prices. Gold traders remained bullish this week even though the yellow metal tumbled below $1,300 an ounce, according to the weekly Bloomberg survey. Turkey saw its gold reserves rise again, up $331 million from the prior week, according to central bank data. The nation’s reserves are now worth $21 billion as of March 22.

- Globally, central banks have purchased a whopping 126 tons of gold so far this quarter, the fastest rate since 1971, according to Morgan Stanley. Most of this purchasing has come from China, Russia and Turkey. Russia has been adding to its gold reserves rapidly in an effort to “de-dollarize” and break reliance on the U.S. dollar. Renaissance Capital says that gold buying in Russia has now exceeded its mine supply and the country could soon start to import the metal.

- Bloomberg reports that the mine that found the world’s largest-ever diamond, a 3,106-carat gem in 1905, has delivered yet another massive treasure. Petra Diamonds’ Cullinan mine in South Africa turned up a 425-carat white color Type II stone. Shares of Petra rose over 7 percent on the news, rebounding from a 16-year low. Zimbabwe’s Finance Minister announced that the country plans to ditch rules within two years that requires all businesses to be controlled by black citizens. This is in hopes of attracting foreign investment into the nation, which has the world’s second-largest platinum reserves, plus many other significant mineral deposits.

Weaknesses

- The worst performing metal this week was palladium, down 10.82 percent as hedge funds cut their positions to a 21-week low. Gold prices saw the largest single-session percentage decline since August on Thursday and landed below the $1,300 per ounce mark for the first time in two weeks, according to MarketWatch. This is partly due to a stronger U.S. dollar, which has rallied in recent days, and due to lower GDP and economic growth forecasts. Lower economic growth can indicate inflation might be lower.

- Palladium also took a tumble this week. The metal fell over 5 percent on Wednesday, the most since August, as signs of slowing economic growth created demand worries. This could be a sign that its multi-month rally is over, as it shot up in the last year with the rise in demand for auto catalysts. Or maybe palladium’s fall is due to Russia’s richest man announcing this week that he plans to issue cryptocurrency tokens backed by the metal?

- Mongolia passed an amendment doubling its gold royalty rate to 5 percent, which will apply to both mining companies and individual artisanal miners. The amendment is to the Minerals Law that previously set the rate at 2.5 percent. South African mining companies are challenging parts of a government charter saying that it will hinder foreign investment and breaches a court order. The charter is aimed at redistributing South Africa’s mineral wealth. The Gold Field’s board has asked its CEO for other options to get its flagship South Deep mine profitable again, should the fifth restructure in 13 years fail to do the job. The company recently invested $800 million in the South African mine.

Opportunities

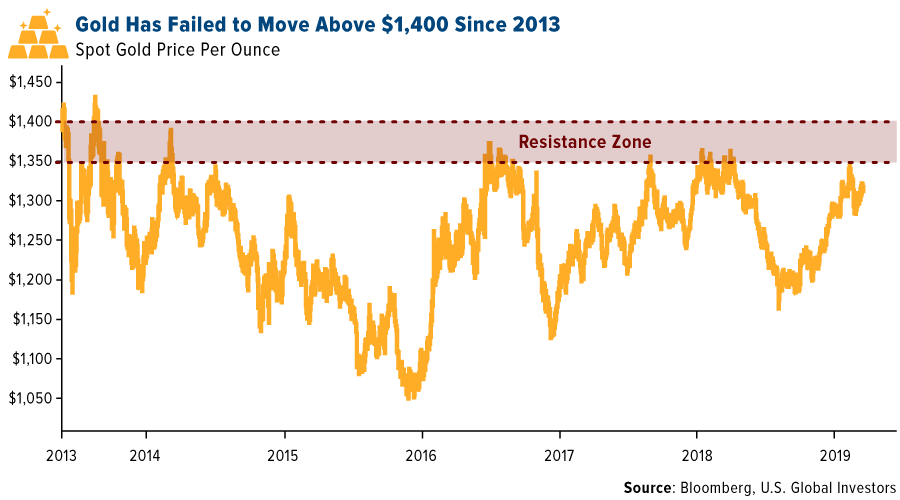

- Although gold has failed to break above $1,400 an ounce since 2013, United Overseas Bank is bullish and thinks the metal can crack that level this year. The bank said in a note that gold needs to overcome a “stack of strong resistances” that have stymied rallies in recent years and that “the underlying tone has clearly improved,” reports Bloomberg. Another reason to be bullish on the metal is that the Basel III rules will be enforced in full in 2019. These rules say that gold held in an institution’s vaults or in trust now qualifies as “a 0 percent risk weighting for risk-based capital purposes.” This means that gold will now be treated as safer and more like actual money. Nick Barisheff, CEO of BMG Group, writes that “Canadian banks are now free to add monetary gold to their increased reserve positions, and to treat it in the same as they would cash of AAA-rated government bonds.”

- UBS raised its six- and 12-month silver price forecasts to $16.30 per ounce on the news that the U.S. Federal Reserve will likely not hike rates this year or next and that its balance sheet reduction may end soon. UBS analysts in a report say that the price of gold would likely pull the white metal as well, as it did late last year, reports Bloomberg. In a pleasant reversal, the Mexican senate halted the advance of a mining initiative that would have allowed the government to cancel concessions. The announcement of that initiative back in November sent shares of the country’s top mining companies plunging.

- Johnson Matthey Plc is moving toward the battery-materials space. The company secured a site for a new battery-materials plant in Eastern Europe in a shift toward electric car supply to counter falling demand for its diesel auto-exhaust catalysts, writes Bloomberg. Johnson Matthey said in a statement this week that it has also partnered with Canada’s Nemaska Lithium Inc. to provide the metal for processing in the facility.

Threats

- In another big hit to South Africa’s mining industry, Sibanye Gold Ltd. announced that it will not extend the life of its Driefontein mine, which was once the biggest mines on the continent. Bloomberg reports that the company plans to shut down operations within 10 years and will cut thousands of jobs as it closes unprofitable shafts. South Africa has some of the deepest and most dangerous gold mines in the world. Rene Hochreiter, an analyst at Noah Capital Markets, said that “below 3,000 meters you are not going to make money and you probably end up killing a lot of people.” Sibanye CEO Neal Froneman said that “it’s difficult to convince shareholders that South African mining is an investment case.”

- Bloomberg reports that two separate reports were released this week saying that the diamond market will flip into deficit in 2021.The diamond industry has been hit hard over the years due to oversupply and weak demand, and will have to wait another two years for prices to potentially increase 1 percent.

- The government of Ecuador had big plans to boost mining in the nation, but newly elected anti-mine candidates could be a threat to those plans. Ecuador’s deputy mining minister said in a statement this week that “the results of the vote endanger projects of national interest and will probably have legal and investment consequences.” Are you tracking Venezuela’s gold movements? Some of it might have been found in Uganda. AP reports that a gold refinery primarily owned by a Belgian is facing Ugandan sanctions over the questionable importation of 7.4 tons of gold earlier in March that may have originated from South America.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.67 percent. The S&P 500 Stock Index rose 1.20 percent, while the Nasdaq Composite climbed 1.13 percent. The Russell 2000 small capitalization index gained 2.25 percent this week.

- The Hang Seng Composite gained 0.01 percent this week; while Taiwan was up 0.02 percent and the KOSPI fell 2.12 percent.

- The 10-year Treasury bond fell 3 basis points to 2.41 percent.

Domestic Equity Market

Strengths

- Industrials was the best performing sector of the week, increasing by 2.85 percent versus an overall increase of 1.08 percent for the S&P 500.

- PVH Corp. was the best performing stock for the week, increasing 13.63 percent.

- Lululemon soared on earnings this week. The athletic-apparel maker beat on earnings, revenue and guidance, which sent shares up more than 10 percent after Wednesday’s closing bell.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing 0.51 percent versus an overall increase of 1.08 percent for the S&P 500.

- Nielsen Holdings Plc was the worst performing stock for the week, falling 11.84 percent.

- Wow Airlines suddenly closed up shop this week, leaving thousands of passengers stranded around the world. The 7-year-old Icelandic budget carrier ceased operations on Thursday due to an unbearable debt burden.

Opportunities

- Apple had a big week. It announced a video streaming service, news subscriptions and its own credit card. The company says its video game service will launch this fall with over 150 games. It also announced major updates to its AppleTV. These are all part of its push to drive revenue as iPhone sales have been slipping globally.

- UPS just beat out Amazon, FedEx and Uber to make America’s first revenue-generating drone delivery operations. UPS, in partnership with drone technology company Matternet, began its daily drone delivery of medical supplies within the WakeMed Raleigh campus on Tuesday.

- Sony announced what’s next for PlayStation with a Nintendo-style presentation called "State of Play". The upcoming games are split evenly between the PlayStation 4 and PlayStation VR, showing that Sony is committed to virtual reality.

Threats

- The month-long rout in health insurers driven by competing policy proposals in Washington that threaten a long period of uncertainty has wiped out about $40 billion of market value. The 10 percent sell-off in the S&P 500 Managed Care Index began in late February as progressive Democrats in Congress started to get behind a plan to replace private medical benefits with a government-run single payer system. It worsened this week as the Trump administration renewed its effort to scrap the Affordable Care Act.

- As a key pocket of the U.S. yield curve inverted, German bonds are now in negative territory and a measure of interest rate volatility staged its biggest two-day surge since 2016 this week. Wall Street strategists including Bank of America warn growth fears coursing through government debt around the globe could awaken U.S. equity volatility from their slumber.

- MoviePass’ parent company has sold more shares to raise cash. Helios & Matheson sold 60,000 new shares of "Helios’ Series B Preferred Stock," which are convertible to 1,000,020,000 shares of its common stock, and issued accompanying warrants, sending shares down more than 50 percent.

The Economy and Bond Market

Strengths

- Special counsel Robert Mueller’s investigation of Russian interference in the 2016 U.S. election "did not find that the Trump campaign or anyone associated with it conspired or coordinated with Russia," Attorney General William Barr announced on Sunday.

- The number of Americans filing applications for unemployment benefits unexpectedly fell last week, reports Reuters, suggesting labor market conditions remained solid, despite slowing job growth. According to the Labor Department on Thursday, initial claims for state unemployment benefits fell 5,000 to a seasonally adjusted 211,000, for the week ended March 23.

- The University of Michigan’s final sentiment index climbed to 98.4 from the prior month’s 93.8, according to a report Friday. Plentiful jobs, rising wages and the Federal Reserve’s reticence toward raising interest rates are proving beneficial to consumer attitudes. The gain in consumer sentiment was concentrated in the bottom two-thirds of the income distribution, with the share citing improved finances at a record for this group.

Weaknesses

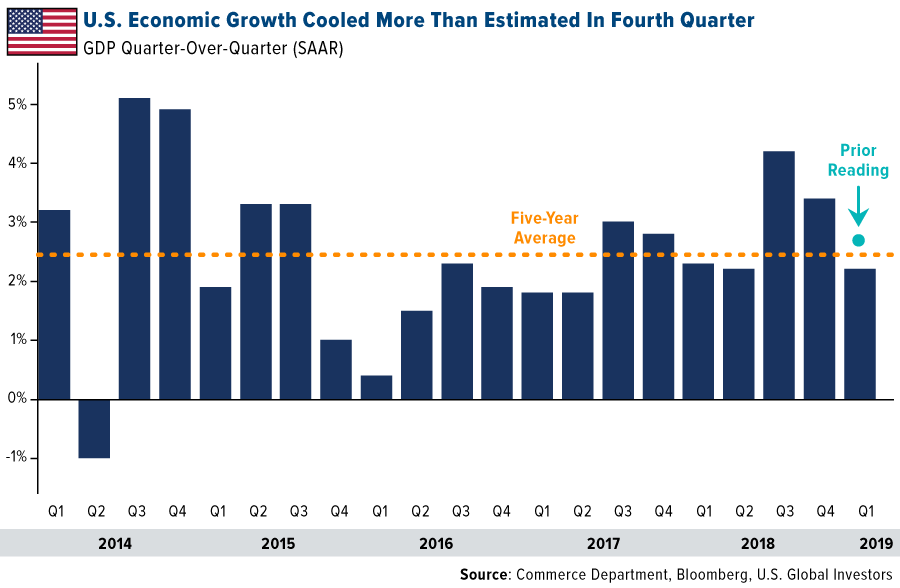

- The U.S. economy cooled more than was reported initially in the fourth quarter of 2018, reports Bloomberg, on revisions to both consumer and government spending. This signals “mounting challenges to the expansion as it nears a record duration,” the article continues. Commerce Department data on Thursday showed GDP growing at a 2.2 percent annualized rate, less than the initial 2.6 percent figure and projections for a revision of 2.3 percent.

- Weak first-quarter growth and slower job gains in the month of February are weighing on attitudes and potentially spending, reports Bloomberg. This is reflected in U.S. consumer confidence, which declined for the fourth time in five months. On Thursday, the Conference Board’s index was reported as falling to 124.1 from 131.4, missing economist estimates in a Bloomberg survey calling for the number to rise to 132.5.

- U.S. housing starts in February fell more than expected, reports Reuters, decreasing 8.7 percent to a seasonally adjusted annual rate of 1.162 million units, the Commerce Department said Tuesday. The percent decline was the largest in eight months, however bad weather could have contributed to the sharp drop in homebuilding last month.

Opportunities

- Trade talks are starting up again as senior U.S. officials head to Beijing on Thursday and Friday. Officials will work on a deal meant to halt the trade war that has seen the world’s largest economies impose tariffs on $360 billion worth of each other’s’ goods, Bloomberg reports. In addition, China’s top trade negotiator, Vice Premier Liu He, will be in the U.S. next week.

- The municipal bond market is likely headed for a "bullish acceleration" in the next few weeks after the Federal Reserve signaled it will not raise rates in 2019, Bank of America strategists said in a note this week. The strategists said they’re not seeing signs of "rally exhaustion," and forecast that 10-year, AAA yields will reach 1.8 percent or lower in 2019.

- The jump in existing home sales in February stemmed from the year-end drop in mortgage rates, writes Bloomberg Economics. Since then, the Fed’s dovish tone has pushed down mortgage rates even further. Along with the deceleration in home prices and rising wages, declining rates are a perfectly timed opportunity to potential homeowners at the start of the spring buying season, the article continues.

Threats

- Whether or not the U.S. will fall into recession in the coming year is a main point of disagreement among economists lately – and that in itself may be an ominous sign, writes Bloomberg’s Mark Whitehouse. As of Friday, Bloomberg’s survey of dozens of economists, on the outlook for the U.S., show that they expected the economy to grow 2.25 percent in the next 12 months. However, there was a lot of variation as well, particularly on the downside – ranging from 3.2 percent growth to 0.8 percent contraction. According to Whitehouse, variation matters. Back in 2007, although economists weren’t very good at predicting recessions, they did tend to disagree more when one was imminent. That’s what happened before the downturns of 1990 and 2001, and what ultimately happened before 2008.

- The Treasury market appears to be in risk-management mode and is priced for economic growth to be weaker than will likely occur, writes Bloomberg Intelligence (BI). Ten-year Treasury yields have scope to stabilize and potentially rise in the near term to 2.91 percent at year-end, BI forecasts.

- Next week’s jobs report will be highly anticipated by investors given the disastrous February report of only 20,000 new jobs. Forecasts call for 175,000 this month, and any major disappointment will be taken as an ominous sign of economic slowdown.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was copper, which gained 3.31 percent. Codelco, the world’s largest copper producer, experienced a 3.3 percent fall in copper production in 2018 due to the processing of lower grade ores. Funding totaling $21 billion is needed by Codelco to modernize its operations but the Chilean government seems reluctant to provide the capital. Oil is set for its best quarter since 2009 due to OPEC supply cuts and the loss of barrels due to U.S. sanctions on Iran and Venezuela. This is also despite a price slide this week on the news of an unexpectedly big jump in crude supplies. Bloomberg reports that WTI crude futures have risen 32 percent so far this year. Hedge funds in Saudi Arabia are bullish on U.S. oil prices as they boosted bets on a rally by 35 percent in the week ended March 19 – the most in two years. Oil product demand in Germany gained 10 percent year-over-year in January, according to federal data, and diesel car sales also gained for the first time since last April.

- Italy’s gas network operator, Snam SpA, is conducting Europe’s first commercial test of a hydrogen-methane blend in a high-pressure network. The company is pumping a hydrogen blend into a pipeline that fuels a pasta maker and a mineral water bottle at a facility that previously ran entirely on natural gas. Bloomberg writes that Snam’s move into clean energy for food production is a step first in a nearly $1 billion plan to invest in green energy projects throughout Europe.

- BloombergNEF estimates that the U.S. was the busiest market globally for solar acquisitions in 2018, with 4.2 gigawatts changing hands, and 3.7 of those gigawatts via 10 big portfolio buyouts. 75 percent of total global solar transactions were concentrated in the U.S., China, Mexico, Spain and the U.K., with these markets attracting $13.1 billion of the global $20.2 billion spent on solar buyouts last year. EnBW is in talks to buy French clean power developer Valeco from France’s Caisse des Depots, according to a statement from the company. Bloomberg reports that Valeco has an installed output of 276 megawatts of onshore wind power and 56 megawatts of solar power.

Weaknesses

- The worst performing major commodity for the week was corn, which fell 5.75 percent on news that farmers plan to plant a larger percentage of corn next year according to a survey released by the U.S. Department of Agriculture. China is reducing subsidies on electric vehicles in order to encourage manufacturers to rely on innovation rather than government assistance as the industry is maturing. The total reduction is around 67 percent, which is more drastic than the expected 40 or 50 percent cut, according to Jefferies analyst Patrick Yuan. Bloomberg reports that the subsidy for pure battery electric cars with driving ranges of 400 kilometers or more will be cut by half, which amounts to around $3,700 per vehicle. This news sent shares of the country’s top electric vehicles makers down.

- China, the world’s biggest crude importer, boosted its imports from Venezuela and Iran last month from January. Oil from these countries is cheaper right now, as other buyers are avoiding it in the face of U.S. sanctions. Customs data shows that China bought 2.03 million metric tons of crude from Venezuela in February, up 17 percent from January. Li Li, analyst at ICIS-China, says that “increased purchases from Venezuela may very likely be due to cost concerns” and that if the import price is low enough, PetroChina Co. could easily make a profit by selling to independent refiners at a higher premium. A report from the International Energy Agency (IEA) shows that carbon emissions from fossil-fuel use hit a record last year due to higher oil consumption in the U.S. and more coal burning in China and India. The IEA also found that energy demand grew 2.3 percent in 2018, the most in a decade.

- Bloomberg reports that the rally in metals at the beginning of this year has halted as trade talks drag on between the U.S. and China and economic indicators show that global growth could be slowing. Copper has remained in the narrow trading range of $6,300 and $6,550 a ton as there haven’t been any new catalysts. According to a report by Australia’s Department of Industry, Innovation and Science, the January dam disaster at Vale SA operations in Brazil could have a massive impact for years to come. The report shows that the dam closures following the accident could cut global iron supply by 46 million tons this year and by 25 million tons annually through 2024. Cargill, an American company that trades in metals and is engaged in ocean transport, said its quarterly earnings were hurt by the industry-wide impact of the Vale SA mine closures and subsequent reduced shipping volumes.

Opportunities

- BloombergNEF analyst Yayoi Sekine said in an interview this week that “there’s a lot more solar and storage happening now than we’ve seen before” and that “natural gas is still king, but it’s starting to get displaced.” The chart below shows that it was only three years ago that natural gas overtook coal to become the top source of energy in the U.S. Now batteries are beginning to challenge natural gas as some solar farms with batteries are able to compete with gas plants. Increasing storage systems allows solar plants to store cheap electricity, plus solar-storage projects are already cheaper than gas plants to build in the U.S. Southwest, writes Bloomberg. Additionally, onshore wind technologies are cheaper to build than coal or natural gas projects in most nations now.

- Record alumina prices have drawn new investments in mining in Jamaica, fueling resurgence in an industry that was going strong in the late 1960’s. Jack Farchy of Bloomberg writes that a 50-year old facility in the island nation is benefitting from a realization across the aluminum industry that the supply chain is fragile. Jiangxi Copper Co. says that government stimulus and growth of home appliances and the auto market in China will boost demand for copper and support a moderately positive price trend this year. Lastly, Credit Suisse raised its rating on miners to overweight due to its research that mining usually outperforms a few months down the road after China PMIs turn and global industry production troughs, writes Bloomberg.

- Tellurian CEO Meg Gentle said in an interview on Bloomberg TV this week that the U.S. needs to quadruple its LNG export capacity, or add 100 million metrics tons per year, in order to capture the full potential of its gas reserves. “We have not even begun to understand how much stranded gas we have in the U.S.,” said Gentle. BloombergNEF data shows that the U.S. currently has 32.3 million tons of export capacity and that global capacity is 382 tons. Gentle pointed out that there are 400 million cubic feet of gas being flared in the Permian Basin, which she says is “telling you that there’s not enough infrastructure” to take away the supply.

Threats

- Bloomberg reports that some of the biggest independent oil and metals trading houses are facing bribery and corruption investigations in jurisdictions all over the world, including in the U.S. William Garrett, who manages a legal database tracking cases related to the Foreign Corrupt Practices Act at Stanford University, told Bloomberg that “oil and gas is the number one industry being openly investigated.” He added that in the past few years there has been “global cooperation between enforcement agencies, and other countries taking foreign corruption more seriously.”

- Macquarie cut its cobalt price forecast for 2019 by 29 percent as supplies swamp the market. Analysts said in a report that they’ve “cut more from our bearish cobalt view, as prices have failed to find a floor yet.” Bloomberg writes that cobalt surged in 2017 on the optimism of growing electric vehicle demand. However, there was a boom in supply from the DRC and prices have plunged almost 70 percent from a peak in April 2018.

- Although production from the Permian Basin is growing and a huge opportunity, there are concerns over supply flooding the market and sending prices plunging for natural gas. As covered in CEO Meg Gentle’s comments in the opportunities section, Permian drillers are already burning off significant amounts of natural gas as there isn’t enough installed infrastructure to store and export it. Bloomberg writes that Magellan Midstream Partners LP cut its spending expectations for this year because it doesn’t view the Permian Gulf Coast pipeline moving forward as initially planned. However, one of the partners on the project, Energy Transfer LP said it still sees the proposed pipeline being “very accretive.”

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 2 percent. Banks moved higher, supported by the new household insolvency framework. Banking stocks gained 3 percent in the past four days. On Monday, the Athens stock market closed in observation of the country’s Independence Day.

- The Turkish lira was the best performing currency this week, gaining 3.3 percent against the U.S. dollar. Just days before local elections, many hedge funds were trapped in trades they wanted to exit because Turkish banks were under pressure not to provide liquidity. In addition, the central bank has used up around one-third of its foreign reserve in the first three weeks of the month to support its currency.

- Communication services was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 6 percent. Equites trading on the Istanbul exchange sold off sharply ahead of Sunday’s municipal elections. Investors unable to sell the Turkish lira due to lack of liquidity were selling equities instead.

- The Hungarian forint was the worst performing currency this week, losing 2.1 percent against the U.S. dollar. The central bank of Hungary announced a symbolic rate hike, raising the overnight rate from negative 15 basis points to negative 5 basis points. Governor Gyorgy Matolcsy said the move was a “one-off,” and is not the start of new tightening policy.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

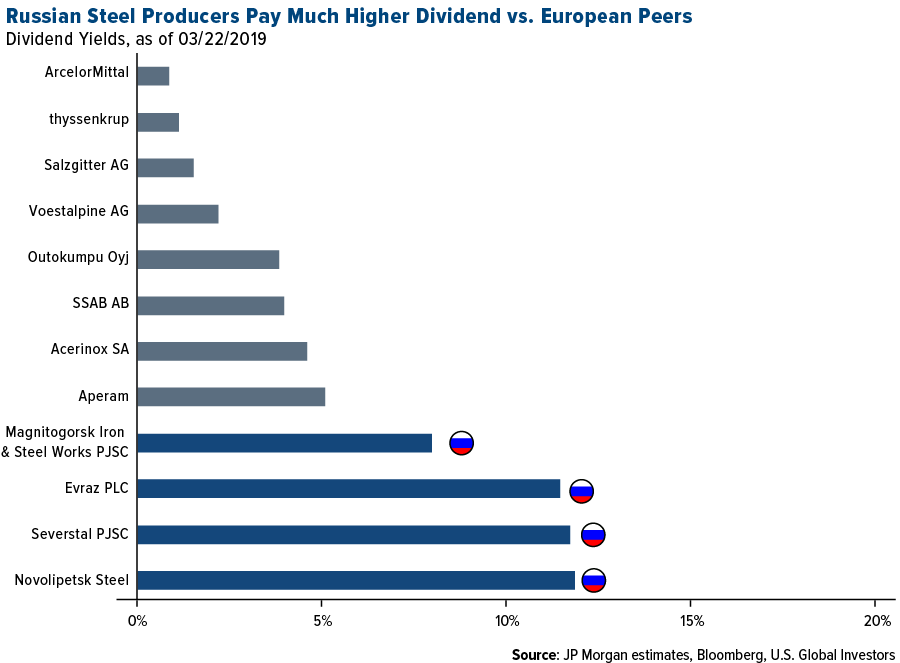

- JPMorgan initiated coverage on four Russian steel makers, with two “overweight” rankings, one “neutral” and one “underweight.” The bank likes steel makers for strong cash generation, high dividends and cheap valuations, trading at 25-30 percent discount versus their European peers. The “Russian Steel Sector Initiation” report was published on March 25.

- The Ministry of Finance in Romania published a draft emergency ordinance, which significantly changes the provisions of the banking tax. The tax rate would be set at 0.4 percent of the tax basis for banks with a market share of more than 1 percent. The tax rate would be set at 0.2 percent for banks with a market share below 1 percent. The tax basis was also lowered versus the initial version to financial assets. This level of taxation is in line with market expectations and can easily be absorbed by the banks.

- According to a survey conducted by the Czech-German Chamber of Industry and Trade, the Czech Republic is no longer the most attractive country for German investors in central and Eastern Europe, as it has been overcome by Estonia. Czech has a very tight labor market and investors worry about weakening demand abroad especially in the automotive industry. The Czech Republic now ranks second ahead of Poland.

Threats

- Turkey has entered a recession, recently recording two consecutive quarters of falling economic growth. Mr. Erdogan has led Turkey through 18 years of continuous growth, but much of this was achieved by unrestrained borrowing. Municipal elections will take place this Sunday. If Erdogan’s AKP Party can hold the majority, he will have to proceed with reforms that stimulate growth and stabilize the financial situation of individuals and businesses.

- Another week has passed and the United Kingdom has no agreement on the Brexit deal, with the new deadline for the country’s exit from the eurozone approaching fast, set for April 12. Theresa May lost control of the parliament and MPs are unsuccessfully trying to come up with another exit plan.

- According to a Wall Street Journal article titled “Mueller report clears Trump – but not Putin” by Gerald F. Seib, Trump is off the hook, but the same is not true for Vladimir Putin after the Muller report was released. Attorney General William Barr concluded that Trump did not work with Russia to secure his presidential victory in 2016. However, Muller’s report concluded that Russia engaged in disinformation and social media campaigns in order to interfere with the elections. In addiiton, Russia hacked into computers of Democratic organizations and Democratic presidential nominee Hilary Clinton and disseminated the stolen emails. Democrats are pushing for more sanctions on specific Russian assets and want to block Russia’s access to dollar financing.

China Region

Strengths

- Singapore, Taiwan and Hong Kong did eke out mildly green weeks, but India’s NIFTY and SENSEX indices closed up 1.47 percent and 1.34 percent, respectively. In addition, China’s off to its best first quarter start since 2014.

- Properties and construction was the top performing sector in Hong Kong’s Hang Seng Composite Index for the week, closing 2.91 percent higher.

- Bloomberg News reported this week that Vietnam’s economic growth clocked in at 6.79 percent in the first quarter from a year earlier, beating analysts’ estimates for a 6.5 percent pace. Inflation picked up slightly to 2.7 percent for the March measurement period from the prior reading of 2.6 percent.

Weaknesses

- South Korea’s KOSPI Index closed down 2.12 percent for the week, while Malaysia and the Philippines both closed down more than 1 percent in the same time frame.

- The weakest performing sector of the Hang Seng Composite Index on the week was materials, which dropped by 2.91 percent.

- China’s year-to-date industrial profits dropped 14.0 percent versus last year.

Opportunities

- The U.S.-China trade talks continue, with U.S. negotiators including Secretary Steven Mnuchin and USTR Robert Lighthizer returning to Beijing, even as media confirmed China’s Vice Premier Liu He will, in turn, come back to the United States next week when talks return to Washington. Trump administration officials reiterated a need for patience on the deal-making and indicated that the question is not one of precise dates but rather one of precise language and enforceability of any ultimate agreements, and therefore worth waiting on and continuing to work toward.

- Overseas investors have sent more than $6.5 billion into Indian equities year to date—among the best flows in Asia outside of China. Indian elections are coming over the next several weeks, with all votes to be tallied by May 23.

- The Federal Reserve may put hikes on hold or even cut rates if economic forecasts disappoint, Chicago Fed chief Charles Evans said in Hong Kong early this week. “The risks from the downside scenarios loom larger than those from the upside ones," Bloomberg reported Evans as saying. More dovish comments from Fed speakers—and a prominent nominee who claimed the December hike was a mistake and rates should be cut—later in the week may help bolster EM if the tone is not pessimistic. A weaker outlook for the dollar with stable or moderate growth may be a sweet spot for EM amid trade talks with China, while of course resolution of the talks in a positive direction may make for an even “sweeter” spot, if it helps resolve uncertainty and firm up the outlook on the trade situation. The dollar is not helped at present by an arduous Brexit process that complicates the pound sterling’s and euro’s outlooks.

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter remain a collective threat until resolution one way or the other.

- The New York Times reported earlier in the week that Indian officials announced that the country shot down a satellite. This would place India “in the exclusive club of nations, along with the United States, Russia and China, that have proved their ability to destroy targets in space,” and some analysts suspect it may have been a demonstration against China’s ability to do the same. No other country has yet confirmed the destruction of the satellite, but PM Narenda Modi tweeted after the announcement, “India stands tall as a space power!”

- While there is indeed much talk of the Fed pause and (possible sometime) rate cuts, and while every talking head pronounces preference for what the Fed should or should not do, the U.S. dollar all the while remains only about half a percent off its 52-week highs, and a stronger dollar could weigh on EM.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 29 was CustomContractNetwork, up 948.75 percent.

- Owner of the iconic Louis Vuitton label, luxury brand conglomerate LVMH will be launching a blockchain for providing the authenticity of high-priced goods, reports CoinDesk. The platform, code-named AURA, is expected to go live in May or June. “To begin with, AURA will provide proof of authenticity of luxury items and trace their origins from raw materials to point of sale and beyond to used-goods markets,” one source involved with the build told CoinDesk.

- In early trading on Friday, bitcoin prices rose and were holding above the psychologically significant $4,000 mark, reports MarketWatch.In addition, a look at the coin’s 30-day volatility measure shows a downward trend. While volatility is in itself a neutral signal, explains Bloomberg, low volatility periods in bitcoin have historically preceded prolonged bull runs. This signal might also attract new investors to bitcoin who before now have been hesitant to participate.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 29 was Ormeus Coin, down 52.40 percent.

- Bitmain’s application for an initial public offering (IPO) on the Hong Kong Stock Exchange has officially lapsed, reports CoinDesk, meaning no such transaction is happening anytime soon. In an announcement published Tuesday, the company said “We will restart the listing application work at an appropriate time in the future.” In the same announcement it was confirmed that co-founders Jihan Wu and Micree Zhan have stepped down as co-CEOs.

- According to one Bloomberg headline this week, Ethereum is losing its luster and its market share. One reason the cryptocurrency was hailed as a savvier successor to bitcoin was its offering of tools that allowed programmers to create apps which would perform automatic transactions, not solely serving as a means of exchange. Four years later, the article continues, the Ether digital currency is losing market share to rival platforms able to deliver the same long-promised projects that touted better features.

Opportunities

- Blockchain-based trading platform CEDEX has overcome several hurdles that previously prevented diamonds from becoming a tradable asset class like gold, using blockchain technology as well as a proprietary algorithm, CoinDesk reports. The hurdles included lack of transparency, liquidity and fungibility. However, CEDEX announced on Wednesday that it has secured a supply of more than 6,000 diamonds ahead of its launch of a diamond exchange-traded fund (ETF). The diamonds will provide traders with a variety of investment options prior to the launch of the ETF.

- During the U.S. Commodity Futures Trading Commission’s (CFTC) Technology Advisory Committee meeting this week, HSBC senior vice president Jesse Drennan provided a specific recommendation to the regulatory body, reports CoinDesk. Drennan shared his belief that “it would also be beneficial if the CFTC would give some positive words around distributed ledger technology (DLT) and DLT adoption,” in order to encourage adoption of blockchain use by hesitant businesses.

- In an effort to attract institutional clients, blockchain services firm AlphaPoint has upgraded its tech solution for security token offerings (STOs), reports CoinDesk. AlphaPoint explains that with its upgraded technology stack, “financial institutions such as private equity, real estate firms and funds can issue asset-backed security tokens,” the article reads, thereby increasing liquidity in the market.

Threats

- Last week, Bitwise Asset Management said in a report that the cryptocurrency market data reported on CoinMarketCap.com, one of the biggest aggregators of such data, “was wrong.” In response to the comments, CoinMarketCap has come out saying concerns over inaccuracies “are valid” and that it is adding data on liquidity, exchange volume and industry rankings to enable users to make better decision, Bloomberg reports.

- Bitcoin prices moved higher earlier in the week, recovering part of the prior session’s losses, reports MarketWatch. Despite the overnight recovery, Jani Ziedins of the CrackedMarket blog says bitcoin is far from out of the woods. “Bitcoin cannot escape $4K resistance even after poking its head above it the last week,” Ziedens explains. “An investment that refuses to go up will eventually go down. Bitcoin owners need to be prepared for more near-term weakness.”

- On Wednesday, Switzerland’s finance watchdog announced that cryptocurrency mining firm Envion AG, which raised millions through an initial coin offering (ICO), held the sale illegally and “seriously violated” laws, reports CoinDesk. The country’s Financial Market Supervisory Authority (FINMA) said that Envion unlawfully received public deposits worth over 90 million francs from at least 37,000 investors through its token offering early in 2018, the article continues.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 195.36 | -3.64 | -1.83% |

| Gold Futures | 1,297.00 | -21.70 | -1.65% |

| Natural Gas Futures | 2.67 | -0.08 | -2.94% |

| S&P/TSX VENTURE COMP IDX | 626.89 | -10.93 | -1.71% |

| 10-Yr Treasury Bond | 2.41 | -0.03 | -1.43% |

| Nasdaq | 7,729.32 | +86.65 | +1.13% |

| Oil Futures | 60.14 | +1.10 | +1.86% |

| Hang Seng Composite Index | 3,897.86 | +0.47 | +0.01% |

| S&P 500 | 2,834.40 | +33.69 | +1.20% |

| DJIA | 25,928.68 | +426.36 | +1.67% |

| Korean KOSPI Index | 2,140.67 | -46.28 | -2.12% |

| Russell 2000 | 1,539.74 | +33.82 | +2.25% |

| S&P Energy | 489.45 | +4.59 | +0.95% |

| S&P Basic Materials | 347.27 | +6.94 | +2.04% |

| XAU | 76.36 | -1.02 | -1.32% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.67 | -0.13 | -4.54% |

| S&P/TSX Global Gold Index | 195.36 | +5.09 | +2.68% |

| 10-Yr Treasury Bond | 2.41 | -0.28 | -10.32% |

| Oil Futures | 60.14 | +3.20 | +5.62% |

| Gold Futures | 1,297.00 | -30.90 | -2.33% |

| S&P 500 | 2,834.40 | +42.02 | +1.50% |

| S&P Energy | 489.45 | +4.80 | +0.99% |

| Hang Seng Composite Index | 3,897.86 | +32.39 | +0.84% |

| DJIA | 25,928.68 | -56.48 | -0.22% |

| Korean KOSPI Index | 2,140.67 | -94.12 | -4.21% |

| Nasdaq | 7,729.32 | +174.81 | +2.31% |

| S&P Basic Materials | 347.27 | -1.19 | -0.34% |

| Russell 2000 | 1,539.74 | -41.31 | -2.61% |

| S&P/TSX VENTURE COMP IDX | 626.89 | +6.54 | +1.05% |

| XAU | 76.36 | +0.10 | +0.13% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.67 | -0.97 | -26.63% |

| 10-Yr Treasury Bond | 2.41 | -0.36 | -13.08% |

| DJIA | 25,928.68 | +2,789.86 | +12.06% |

| Oil Futures | 60.14 | +15.53 | +34.81% |

| S&P 500 | 2,834.40 | +345.57 | +13.88% |

| Gold Futures | 1,297.00 | +3.20 | +0.25% |

| S&P Energy | 489.45 | +63.48 | +14.90% |

| Nasdaq | 7,729.32 | +1,149.83 | +17.48% |

| Korean KOSPI Index | 2,140.67 | +112.23 | +5.53% |

| S&P Basic Materials | 347.27 | +31.26 | +9.89% |

| Russell 2000 | 1,539.74 | +207.92 | +15.61% |

| Hang Seng Composite Index | 3,897.86 | +503.55 | +14.84% |

| S&P/TSX Global Gold Index | 195.36 | +8.63 | +4.62% |

| S&P/TSX VENTURE COMP IDX | 626.89 | +89.61 | +16.68% |

| XAU | 76.36 | +5.58 | +7.88% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Severstal PJSC

Evraz PLC

Novolipetsk Steel PJSC

Magnitogorsk Iron & Steel Work

PetroChina Co Ltd

Gold Fields Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

A program of regular investing doesn’t assure a profit or protect against loss in a declining market. You should evaluate your ability to continue in such a program in view of the possibility that you may have to redeem fund shares in periods of declining share prices as well as in periods of rising prices.

Sharpe ratio is a measure of risk-adjusted performance calculated by subtracting the risk-free rate from the rate of return for a portfolio and dividing the result by the standard deviation of the portfolio returns.

The Conference Board index of leading economic indicators is an index published monthly by the Conference Board used to predict the direction of the economy’s movements in the months to come. The index is made up of 10 economic components, whose changes tend to precede changes in the overall economy.

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The S&P 500 Managed Care Index is comprised of companies that are included in the S&P 500 and classified as members of the health care sector.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. The NIFTY 50 index is National Stock Exchange of India’s benchmark broad based stock market index for the Indian equity market.

The BSE SENSEX is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange.