Should You Buy the Saudi Aramco IPO?

Date Posted: November 8, 2019

Read time: 61 min

Saudi Aramco is the world's most profitable company. With a valuation of between $1 trillion and $2 trillion, it's worth more than the entire Saudi Arabian stock market.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Imagine waking up in your posh high-rise penthouse facing the Red Sea. Above the bustling city hangs a giant artificial moon that livestreams images from outer space. You call for an automated flying taxi, and it carries you to your job genetically modifying humans to make them stronger. When you return home in the evening, you find that robot maids have made a thorough cleaning of the place. Later, you decide to step out for the night at one of the city’s many five Michelin star restaurants, followed by a visit to the robot dinosaur park.

Sound like science fiction? Maybe. But believe it or not, this is the future envisioned by Saudi Arabia’s crown prince, Mohammad bin Salman Al-Saud. Everything I described above is lifted directly from his plans for a brand new city.

|

This “land of the future,” called Neom, is to be built on a Massachusetts-size area of barren desert along the Saudi kingdom’s northwest coastline. Its goal is not only to attract “the world’s greatest minds and best talents,” but also to lure international tourists and luxury travelers.

As ambitious (crazy?) as bin Salman’s plan sounds, it’s already moving forward. Bloomberg reports that the kingdom has awarded two Saudi construction firms with contracts to begin building housing for workers.

Altogether, the cost to bring Neom to fruition will run an estimated $500 billion—which has some investors sweating. This year the oil-rich kingdom’s budget deficit has widened further to around 7 percent of its gross domestic product (GDP), according to the International Monetary Fund (IMF).

So where does bin Salman, also known as MBS, expect to come up with this cash?

Do I even need to say it?

Saudi Aramco, World’s Most Profitable Company, Going Public at Long Last

It may be no coincidence that at the same time that construction starts on Neom, Saudi Arabia is finally set to sell shares of its national oil company, Saudi Aramco. Coincidence or not, the timing is interesting.

Early this week, the kingdom’s Capital Market Authority announced that, after years of speculation, Aramco will at long last begin trading on the Saudi Stock Exchange, or Tadawul, sometime next month. The energy giant is the world’s most profitable company—in 2018 it generated a mind-boggling $111 billion in net income and some $86 billion in free cash flow. And with a valuation of between $1 trillion and $2 trillion, it’s worth more than the entire $550 billion Saudi equity market.

In fact, at the low end of that valuation, Aramco “will still be worth more than all Brazilian stocks, and the top valuation would make it worth more than Korean, Australian, Swiss or German stocks,” writes the Wall Street Journal’s James Mackintosh.

He adds: “This is an asset class all on its own.”

Indeed, there’s a lot that, on the surface, is enticing about Aramco as an investment. Consider the dividends alone. According to the summary prospectus, Aramco intends to pay out an incredible $75 billion in cash dividends next year. Not only does that amount to a potential 5 percent yield per share, but it’s almost 30 times more than the $2.6 billion Apple distributed to investors in 2018.

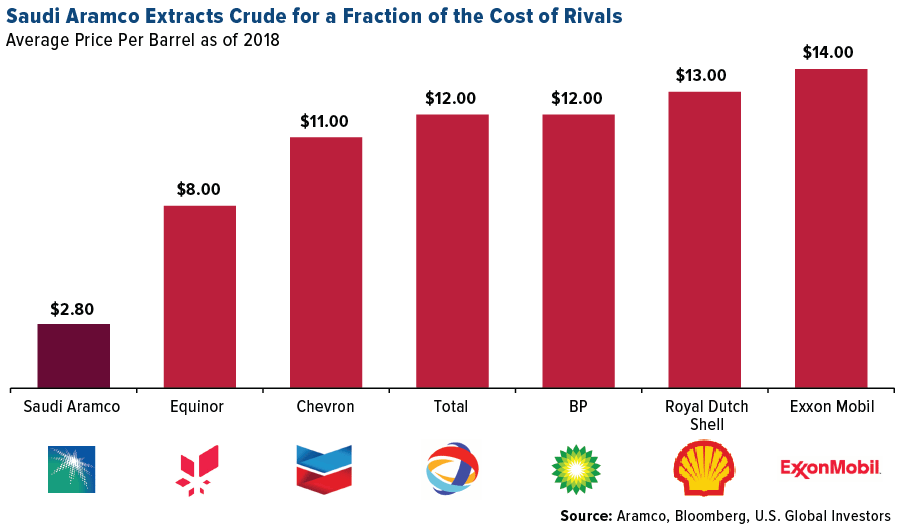

As for production, it has the world’s largest oil reserves for any one company, and its cost for extracting the stuff is a low, low $2.80 per barrel, far less than any of its rivals.

The IPO also comes just a few months after Saudi Arabian stocks were finally included on the MSCI Emerging Markets Index, giving a greater number of global investors exposure to the oil-rich kingdom.

But Should You Invest?

Despite all this, Aramco may have a hard time convincing foreign investors to look past some of the significant drawbacks.

For one, shares will only be available to buy on the Tadawul in Riyadh—for now, anyway. Second, the public float will be in the neighborhood of 2 percent of shares, making this a relatively small public debut for such a massive company. Depending on the company’s final valuation, and depending on the percent of shares it ends up listing, Aramco could end up making between $30 billion and $51 billion in this round of fundraising. That’s according to estimates by Ellen R. Wald, author of the 2018 bestseller Saudi, Inc.: The Arabian Kingdom’s Pursuit of Profit and Power.

The rest of the shares will be owned, of course, by the crown prince and the House of Saud. This is an absolute monarchy we’re talking about, after all, and so global investors should not expect to have any shareholder rights. Aramco’s board of directors will have a fiduciary duty to MBS and any future monarch, not to investors. This has some serious implications.

In the past, the monarchy has used Aramco as a piggy bank, dipping into its vast coffers to finance any number of pursuits and projects. As Ellen Wald puts it in a recent New York Times op-ed:

“The money raised from the Aramco IPO, and any subsequent offerings, will not go to the company. It will go to Saudi Arabia—to the king and his government. And every subsequent purchase of Aramco shares will raise the value of the company just a little, further enriching the king.”

And getting him closer to realizing the futuristic city of Neom.

OPEC Cuts on Deck While U.S. Shale Could Be Headed for a “Major Slowdown”

According to reports, Aramco’s growth assumptions and basis for such a generous dividend package are predicated on Brent crude prices at or above $65 a barrel, a level last seen in September. The average price for a barrel of oil for the three-year period through November 8 is just shy of $63.

In an attempt to prop up prices before its IPO, Aramco has been making production cuts for the better part of a year, and at next month’s OPEC meeting, Saudi Arabia is expected to push for additional cuts from fellow oil-exporting members. Output could collectively be lowered by some 1.2 million barrels a day.

Meanwhile, U.S. shale production has only continued to rise thanks to advances in fracking technology, helping to keep global crude prices in check. In August, the most recent month of data, American producers pumped out a record 12.4 million barrels a day, an amazing 128 percent increase from a decade earlier. Last year, the industry was producing an extra 2 million barrels a day compared to 2017.

That explosive growth, however, could be headed for a “major slowdown,” according to a new report by IHS Markit, the same people who put out the monthly purchasing manager’s index (PMI). Shale production growth next year will be only 440,000 barrels a day, the group says, down significantly from 2 million barrels a day. Output will slow even more before “essentially flattening out in 2021.”

Says IHS Markit’s Raoul LeBlanc, this slowdown could be coming due to lower oil prices and more challenging access to capital markets. (Important here to recall Norway’s complete divestiture from fossil fuel equities, not to mention the general rise of ESG investing—or “environmental, social and corporate governance”—which rules out fossil fuel companies.)

“The combination of closed capital markets and weak prices are pulling cash out of the system,” LeBlanc comments. “Investors are imposing capital discipline on exploration and production (E&P) companies by pushing down equity prices and pushing up the cost of capital on debt markets.”

This is both good and bad news for Aramco. Oil prices could surge above $65 with even more product coming offline, but at the same time, the company could run into challenges attracting investors.

Are You Underinvested in Gold?

A couple of weeks ago, I wrote an article called “You’re Probably Underinvested in Gold.” The response from readers was very positive, and yesterday, the article was retweeted by none other than the World Gold Council (WGC). I’d like to extend a sincere thank you for the recognition!

If you missed the article the first time, you can check it out by clicking here.

New Monthly SWOT Section

On a final note, I’d like to draw your attention to an exciting new SWOT section in today’s Investor Alert. Besides gold, emerging markets, cryptocurrencies and others, we’ll also now be covering the global airlines sector on a monthly basis.

To jump directly to the airlines section, click here!

Gold Market

This week spot gold closed at $1,458.52, down $55.88 per ounce, or 3.69 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 6.07 percent. The S&P/TSX Venture Index came in off just 0.83 percent. The U.S. Trade-Weighted Dollar rose 1.16 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-4 | Durable Goods Orders | -1.1% | -1.2% | -1.2% |

| Nov-7 | Initial Jobless Claims | 215k | 211k | 219k |

| Nov-12 | Germany ZEW Survey Current Situation | -22 | — | -25.3 |

| Nov-12 | Germany ZEW Survey Expectations | -13 | — | -22.8 |

| Nov-13 | Germany CPI YoY | 1.1% | — | 1.1% |

| Nov-13 | CPI YoY | 1.7% | — | 1.7% |

| Nov-13 | China Retail Sales YoY | 7.8% | — | 7.8% |

| Nov-14 | PPI Final Demand YoY | 0.9% | — | 1.4% |

| Nov-14 | Initial Jobless Claims | — | — | 211k |

| Nov-15 | Eurozone CPI Core YoY | 1.1% | — | 1.1% |

Strengths

- The best performing metal this week was palladium, down 3.39 percent. Although gold, and all the precious metals, suffered a bad week due to optimism surrounding a U.S.-China trade deal, it did recover slightly on Friday after President Trump said there would not be a full rollback of tariffs. Platinum prices hit a five-week high on Monday after its longest run of gains since April. Palladium has attracted more attention this year as it is up around 44 percent; however, investors are now paying increased attention to platinum.

- Turkey’s official gold reserves rose $522 million from the previous week to now total $27 billion as of November 1. According to central bank data, Turkish gold reserves are up 42 percent year-over-year.

- South African gold miner Heaven-Sent Gold Group Co. is set to begin trading in Hong Kong on November 25. The company owns two mines in South Africa and will be the first gold miner initial public offering (IPO) in Hong Kong in more than a year.

Weaknesses

- The worst performing metal this week was silver, down 7.18 percent. Gold had its biggest weekly loss in three years as progress in the U.S.-China trade war hurt demand for safe haven asses. The yellow metal fell nearly 4 percent for the week and silver lost over 7 percent. JPMorgan and Citigroup both closed out long bets on gold citing easing geopolitical tensions and synchronized monetary easing.

- China has halted its 10-month gold buying spree. The People’s Bank of China, which purchased over 100 tons of gold from December to September, kept holdings at 62.64 million ounces from September to October. Gold imports by India fell for a fourth month to 20.8 metric tons in October, down 46 percent year-over-year. Bloomberg reports that the figure is a small improvement from 13.5 tons in September. Higher gold prices and a weak Indian economy are hurting demand in the world’s second largest consuming nation.

- De Beers, the world’s biggest diamond producer, cut diamond prices by 5 percent at its November sale, reports Bloomberg. The diamond industry is suffering from an oversupply of polished gems, which has hurt prices.

Opportunities

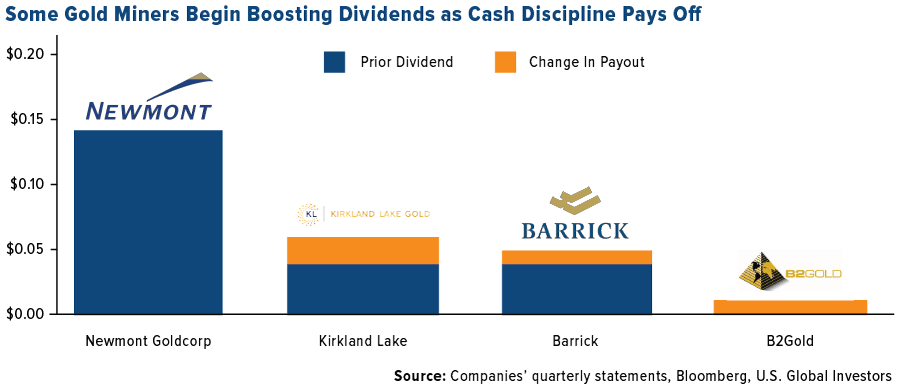

- Several major gold miners have boosted dividends as they work to cut costs and consolidate operations in the midst of higher bullion prices. Barrick Gold raised its dividend by 25 percent, Kirkland Lake Gold raised its quarterly payout by 50 percent and B2Gold Corp announced its first ever dividend, reports Bloomberg. Stephen Walker, RBC Capital Markets’ head of global mining research, said in a phone interview that “the ability to return a portion of excess capital to shareholders” is evidence of their improved cost performance.

- Liberty Gold Corp. announced strong drill results this week at its Black Pine Project in Idaho. The company reported 3.4 grams per ton oxide gold over 62.5 meters and 6.21 grams per ton of gold over 21.3 meters. President and CEO Cal Everett said “the results to date, combined with modeling of historic results, continue to support our premise that Black Pine hosts a multi-million ounce gold system.”

- Macquarie, an Australian bank, wrote in its latest report that gold is likely to stabilize around $1,400 an ounce in 2020 before rallying to $1,600 an ounce in 2021. Although gold faces potential headwinds of global growth improving or stabilization of geopolitical turmoil, the bank says prices should be supported by ongoing central bank buying and increased long-term investor allocations. Strategists wrote that “investors worldwide have already substantially boosted their exposure to the metal, net-length in CME futures and ETF holdings are oscillating around all-time highs.”

Threats

- Barrick Gold Corp is fighting a $1 billion tax bill tied to the 2015 sale of its 50 percent interest in the Zaldivar copper mine in Chile to Antofagasta. Bloomberg reports that Barrick said it is appealing a determination by the Chilean tax authority that a subsidiary wrongly deducted a loss from an inter-company transaction in an effort to offset capital gains tax on the sale of that mine.

- A convoy transporting workers of Canadian gold producer Semafo Inc. in Burkina Faso was attacked on Wednesday and killed at least 38 people. An ongoing conflict in the West African nation has displaced more than half a million people and has led to an increase in violence. This attack was the third in the past 15 months for Semafo and occurred just 25 miles away from a mine site.

- The total amount of negative-yielding bonds globally dropped to $12.5 trillion, the lowest since July, after rates on French and Belgian securities rose above zero percent, reports Bloomberg. The improving relationship between China and the U.S. could be a factor driving bond yields up. A lower amount of negative-yielding debt is bad news for the price of gold, since it raises the appeal of bonds as an asset class.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.22 percent. The S&P 500 Stock Index rose 0.85 percent, while the Nasdaq Composite climbed 1.06 percent. The Russell 2000 small capitalization index gained 0.60 percent this week.

- The Hang Seng Composite gained 2.03 percent this week; while Taiwan was up 1.58 percent and the KOSPI rose 1.76 percent.

- The 10-year Treasury bond yield rose 22 basis points to 1.94 percent.

Domestic Equity Market

Strengths

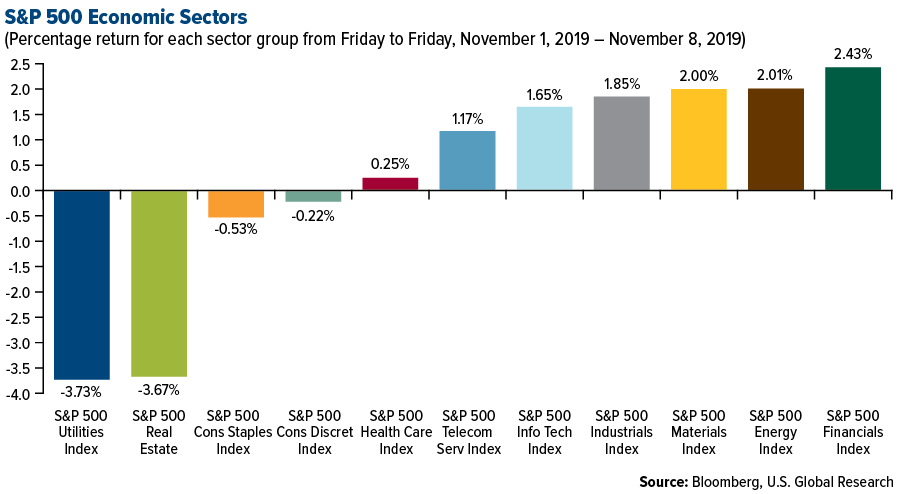

- Financials was the best performing sector of the week, increasing by 2.43 percent versus an overall increase of 0.76 percent for the S&P 500.

- Davita Inc. was the best performing stock for the week, increasing 17.32 percent.

- Toyota Motor Corp. unveiled a $1.8 billion share buyback after strong second-quarter profits, the company reported Thursday. Japan’s biggest automaker posted a 14 percent rise in operating profit to 6 billion for the three months ended September.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 3.73 percent versus an overall increase of 0.76 percent for the S&P 500.

- Expedia Group Inc. was the worst performing stock for the week, falling 26.47 percent.

- “SoftBank reported an eye-watering $6.5 billion loss in the wake of WeWork’s catastrophic failed IPO,” writes one Business Insider headline this week. The company reported its first quarterly operating loss in 14 years, posting a 6.46 billion decline in the July-September period.

Opportunities

- BlackRock CEO Larry Fink says the world will see higher equity markets in 2020, adding that there have been positive changes in emerging economies including Saudi Arabia, speaking at the Saudi Future Investment Initiative conference.

- Citigroup is looking to expand its consumer-banking presence, targeting big markets like Seattle and Dallas as battlegrounds to snatch deposits from rivals like JPMorgan Chase and Bank of America. The bank for years has lagged behind competitors in attracting deposits, thanks in part to a vastly smaller bank-branch footprint, reports Business Insider.

- Xerox is considering a takeover offer for personal computer and printer maker HP, reports the Wall Street Journal, in what could be a $27 billion deal.

Threats

- California’s attorney general revealed he’s investigating Facebook, and says the company is not complying with subpoenas. California has been quietly investigating Facebook over privacy issues and its business model for more than a year. Furthermore, Facebook admitted to another data leak, saying that up to 100 developers accessed people’s data from Groups. In April 2018 Facebook implemented new rules restricting the amount of personal data third parties could access following the Cambridge Analytica scandal, but some apps seem to have been unaffected by the new rules.

- Uber reported its third-quarter earnings on Monday, reports Business Insider, which topped Wall Street’s revenue estimates. Unfortunately the company lost more money on a per-share basis than analysts expected, and shares sank by as much as 6 percent in after-hours trading following the report.

- Under Armour cuts its annual revenue forecast, reports Yahoo! Finance. The forecast comes a day after the company said it was being probed by the federal investigators on its accounting practices and was cooperating with them.

The Economy and Bond Market

Strengths

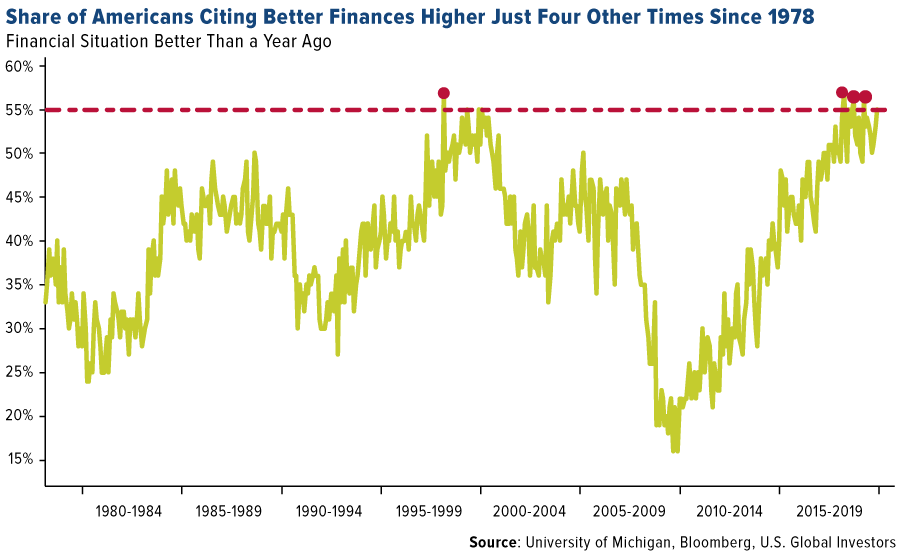

- The stock market rally, steady job and wage growth and keeping debt levels manageable are improving the financial situations of more Americans. Some 55 percent of respondents in the latest University of Michigan survey of consumers said their finances were in ‘better’ shape than last year, helping boost confidence for a third month in November. The share, which has been higher only four separate instances since 1978, indicates households are well positioned to continue spending and provide more fuel for the economy.

- The U.S. services sector rebounded in October after hitting a three-year low in September. The ISM non-manufacturing index rose 2.1 percentage points to 54.7 as respondents remained “concerned about tariffs, labor resources and the geopolitical climate,” according to the Institute for Supply Management. A reading above 50 signals the sector is growing. Business activity, new orders and employment all showed improvement while prices fell. The services sector makes up about two-thirds of the economy.

- The number of people who applied for unemployment benefits in early November fell to the lowest level in a month and clung near a half-century low, reflecting the resilience of the strongest labor market in decades. Initial jobless claims declined by 8,000 to 211,000 in the seven days ended November 2.

Weaknesses

- Orders for U.S. manufactured goods decreased 0.6 percent to a seasonally adjusted $496.7 billion in September, the Commerce Department said Monday. Economists surveyed by The Wall Street Journal expected a 0.5 percent decrease.

- U.S. wholesalers reduced inventories in September at the fastest pace in nearly two years. Wholesale inventories fell a seasonally adjusted 0.4 percent in September from the prior month, the largest decline since October 2017. Economists surveyed by The Wall Street Journal expected a 0.3 percent drop.

- American workers were unexpectedly less productive during the third quarter, with growth in their output failing to keep up with hours worked. The Labor Department said on Wednesday nonfarm productivity, which measures hourly output per worker, fell at a 0.3 percent annualized rate between July and September, the biggest decline in almost four years. The decline might set back the prospects of a pick-up expected by some economists in the trend growth rate for productivity following 2017 tax law changes partially aimed at fostering investment. Analysts had expected productivity growth of 0.9 percent during the quarter.

Opportunities

- China is considering the removal of restrictions on poultry imports from the U.S., state-owned Xinhua News Agency reported on Thursday. The report came after the commerce ministry said the two countries have agreed to cancel in phases the tariffs imposed during the months-long trade war.

- Germany posted a surprise rebound in manufacturing, a sign the ‘deep recession in German industry may be bottoming out’. Data from Germany’s federal statistics office showed that new orders rose 1.3 percent in September, reversing a decline since June.

- U.S. retail sales next Friday will grab investor attention. Consumption has been the main pillar holding up the American economy lately, so a confirmation that it remains healthy will be applauded by markets.

Threats

- Europe’s biggest economy will be under the microscope next Thursday, when preliminary GDP data for the third quarter hits the markets. Having contracted in the second quarter, another negative number now would constitute a technical recession, reigniting worries about the euro area’s future.

- U.S. CPI inflation data next Wednesday will be an item investors will be watching. With readings failing to keep up with the Fed’s target, another miss will add to the unease about the strength of the economy.

- Fed Chairman Jay Powell testifies before the Joint Economic Committee of Congress next Wednesday. Investors will tune in for any signals on monetary policy, as Powell is likely to be questioned on the recent rate cuts and the subsequent ‘pause’ announced by the central bank.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, which gained 4.29 percent. The Stoxx Europe 600 Basic Resources Index is on its way to a bull market after a 20 percent rise from a low in August, reports Bloomberg. The heaviest weight in the index is miners and steelmakers, which have risen due to optimism about a U.S.-China trade deal.

- Although optimism surrounding a possible trade deal fell slightly on Friday morning, positive developments early in the week helped commodities. The Bloomberg Commodity Spot Index closed at the highest since mid-April on Tuesday and has risen 9.4 percent so far this year. “In the past two weeks, top negotiators had serious, constructive discussions and agreed to remove the additional tariffs in phases as progress is made on the agreement,” said China’s Ministry of Commerce spokesperson. The majority of copper traders and analysts turned bullish on the metal for the first time since September in the weekly Bloomberg survey, as China is a big consumer of copper and a trade deal could spur demand.

- French oil giant Total SA is not renewing its membership with a key industry lobby group, American Fuel & Petrochemical Manufacturers, due to differing stances on climate change. Total joins Royal Dutch Shell Plc who left earlier this year and demonstrates the growing pressure that oil majors are feeling from investors over demands that business models align with the Paris climate accord.

Weaknesses

- The worst performing major commodity for the week was silver, which fell 7.18 percent. Exports of copper from Chile, the world’s top producer, fell to the lowest level since 2017 in October due to unrest and protests. The nation’s central bank reported that exports fell to $2.5 billion, down from $3.2 billion in the same period last year. Bloomberg reports that Chile’s largest copper mines and ports were disrupted as miners participated in anti-government protests. Tighter supply of the metal could push prices higher.

- Chesapeake Energy Corp., a U.S. natural gas producer, fell as much as 17 percent this week after reporting a wider-than-expected loss for the third quarter and warning that depressed oil and gas prices are a growing concern. The steel industry downturn is spreading to Europe now due to the ongoing U.S.-China trade war, according to Austrian steelmaker Voestalpine. The company has fallen 7.6 percent so far this year and said this week that “the weakening of the export industry due to increasing global barriers to trade, decreasing demand from the automotive industry as well as fewer investments affected all of the group’s divisions.”

- Although natural gas rallied on Monday due to colder temperatures across the U.S., the fuel is trading lower in Asia due to warmer winter outlooks. Bloomberg reports that China, Japan and South Korea – the region’s top three buyers – all see a low chance of colder weather, hurting demand outlooks. Asia LNG and coal prices have sunk around 40 percent in the past year.

Opportunities

- Germany is increasing incentives for citizens to move away from combustion engines and jump on the electric car movement. The country will double an environment bonus to as much as 6,000 euros per electric vehicle and the auto industry will continue to cover half of that cost, according to Chancellor Angela Merkel’s chief spokesperson. “It will therefore be possible to provide support for another 650,000 to 700,000 electric vehicles.”

- One of renewable energy’s biggest challenges is how to keep power reliable even when the sun isn’t shining and winds aren’t blowing. Bloomberg reports that the answer to this is emerging from the Australian outback. In northern Queensland state a project that combines solar and wind generation with battery storage will open in early 2020. This project could serve as a model for future projects around the globe as costs plummet for renewable energy.

- According to data released on Tuesday by the Commerce Department, the U.S. registered its first petroleum trade surplus in over four decades due to record production. The U.S. took in $252 million more from petroleum sales than it spent on imports in September, compared with a $268 million deficit in August, writes Bloomberg. The American shale boom is partly why OPEC sees its market share shrinking. OPEC said that it expects demand for its oil to slide by 7 percent over the next four years, according to its annual report.

Threats

- Ecuador could face delays in attracting foreign oil investment after an 11-day uprising last month. After the government announced plans to increase fuel prices in order to meet demand tied to an IMF loan, protests erupted around the county. Bloomberg writes that the protests damaged 101 wells across 20 fields and forced 24 rigs to halt production. Fernando Santos, a former oil minister and now industry analyst, says the level of devastation might keep investors on the sidelines until the end of the current administration.

- Brazil’s largest-ever auction of oil deposits flopped this week, sending the Brazilian real tumbling after state-controlled Petrobras did most of the bidding, reports Bloomberg. The auction was expected to help the country shift away from nationalistic oil policies, however, no oil majors participated. The reserves up for auction contain 20 billion barrels of oil and were expected to raise $25 billion in government fees. Many considered the oil fields to be expensive due to the fact that it already produces over 400,000 barrels a day of crude and the buyer would have to compensate Petrobras, which operates it.

- A convoy transporting workers of Canadian gold producer Semafo Inc. in Burkina Faso was attacked on Wednesday and killed at least 38 people. An ongoing conflict in the West African nation has displaced more than half a million people and has led to an increase in attacks. This attack was the third in the past 15 months for Semafo and occurred just 25 miles away from a mine site.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 4.8 percent. Recently, Fitch revised Turkey’s outlook from negative to stable, saying that Turkey made progress in rebalancing and stabilizing its economy. On the geopolitical front, the situation is improving too. Erdogan, the President of Turkey, is scheduled to meet President Trump in the White House next week, despite increased tensions between both nations this year.

- The Russian ruble was the best relative performing currency this week, losing 40 basis points. All Emerging European currencies recorded losses against the U.S. dollar in the past five days. However, the ruble was the best relative performing currency despite Brent crude oil weakening by 1.3 percent as stronger economic data supported the country’s currency. The composite PMI reading moved higher to 53.3 from 51.4 and inflation remained below the central bank’s target as of October at 3.8 percent.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.8 percent. Banks corrected, coming down a bit lower from a new one-year high reached last week. Stocks trading on the Athens exchange are the best performers, gaining 36 percent year-to-date. The Greek economy should accelerate its growth to 2.8 percent next year, and the new project Hercules, a government guarantee scheme for securitization, will further reduce banks’ non-performing loan portfolios.

- The Hungarian forint was the worst performing currency in the region this week, losing 3 percent. Inflation in October was reported at 2.9 percent, above the expected 2.8 percent, but still below the central bank’s target. Current account is worsening, and the dovish tone of the central bank puts pressure on the country’s currency.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

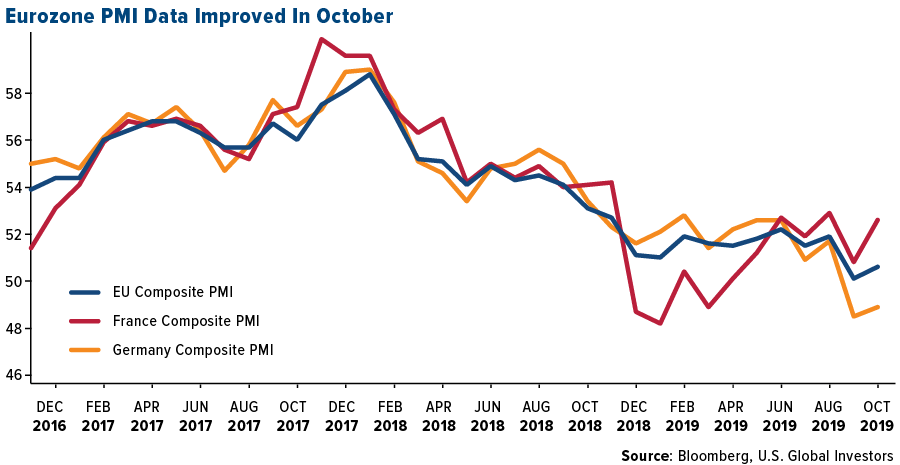

- Eurozone composite PMI, which is comprised of service and manufacturing PMI, improved in the month of October, moving higher above the 50 level that separates growth from contraction. Service firms recorded continued growth in the euro area, and the manufacturing sector improved slightly. France once again recorded the strongest composite PMI data while Germany was still very weak, mostly due to declining industrial production.

- Russia inflation eased to the lowest level in a year even after four consecutive interest rate cuts, paving way for the Russian central bank to cut rates further. Economy Minister forecasts inflation to drop to 3 – 3.3 percent from the current 3.8 percent, and the central bank target CPI is set at 4 percent.

- Bloomberg reported that some analysts think that the euro is becoming an attractive buying option for some after lagging most of its major peers this year. It highlighted that the euro has been undermined by global trade tensions and Brexit uncertainty, but some investors see an improvement in growth and progress in U.S.-China trade talks. It said this could fan risk sentiment and drive the euro higher.

Threats

- The European Commission published its latest economic update and cut its outlook for eurozone growth to 1.1 percent in 2019 from prior 1.2 percent, and revised down next year’s GDP forecast from 1.4 percent to 1.2 percent. It highlighted that the external environment has been much less supportive and uncertainty is running high. In particular, it noted weakness in manufacturing activity.

- The President of Turkey once again asked the central bank to lower rates further, after the new Governor Murat Uysal delivered bigger-than-expected cuts all three times since his appointment. The main rate was cut by 10 percent since July and further cuts may put new pressure on the Turkish currency.

- Global markets seem to be following optimism around trade negotiations, and European equities are moving higher as the U.K. avoided exiting the EU without a deal on October 31. Emerging Europe, as measured by MSCI Emerging Europe Index (MXMU), year-to-date gained 29 percent, and unexpected negative news around trade talks might spark some profit taking.

China Region

Strengths

- The best performing index in the region was Thailand’s SET Index, which jumped 2.85 percent for the week as the Thai central bank cut rates. Hong Kong’s Hang Seng Composite also put in a strong showing, with a 2.11 percent return for the last five trading days.

- Materials and energy bounced back this week, constituting the two top-performing sectors in the Hang Seng Composite, rising 4.69 and 4.31 percent, respectively.

- The Philippines’ Markit Manufacturing PMI rose to 52.1 for the October period from a September reading of 51.8. Inflation also remained low versus a year ago, with CPI in the Philippines now having dropped to 0.8 percent, well down from the scorching levels of latter 2018.

Weaknesses

- The poorest performing index in the region was the Jakarta Composite in Indonesia, which finished down 49 basis points for the week.

- Haven-ish sector telecommunications was the worst performing one in the Hang Seng Composite for the week, falling 67 basis points amid a relatively more risk-on set of sessions.

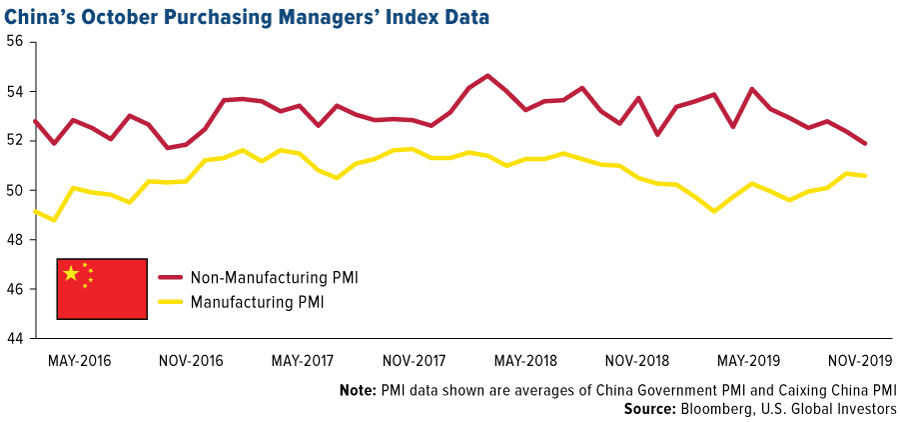

- We got the Caixin China Services PMI this week, which clocked in right on consensus at a 51.1, but recall that last week we did have both the official Manufacturing PMI as well as Non-manufacturing PMI miss in China, with a contractionary 49.3 and a 52.8 reading, respectively. The Caixin China Manufacturing PMI was the lone bright spot, with a 51.7 reading coming in better than expectations. On that note, while both imports and exports for China came in slightly better than admittedly soured analyst expectations for their respective readings, they nonetheless remain year-over-year declines from October 2018.

Opportunities

- U.S.-China trade talks continue across various channels, and the tone this week continued much of the optimism of recent days, with U.S. markets hitting all-time highs amid earnings season and a degree of expectation of halts to tariff implementation as well as “concessions” of some form, per Larry Kudlow, considered by many to be possible tariff roll-backs under certain conditions. Details remain scanty but optimism is moving higher along with expectations of some sort of skinny deal in the near future. “Phase One” does appear closer, although media reports suggest that a Trump-Xi Phase One signing event could be delayed until December sometime given the Chilean cancellation.

- Taiwan’s TWSE put in new 52-week highs this week. Vietnam’s Ho Chi Minh put in new 52-week highs this week. India’s Sensex put in new 52-highs this week. Watch the price action…

- As highlighted last week, the Hong Kong Exchange may well be keeping busy in the near future, with Alibaba reportedly nearer to filing for a HK IPO (even as its massive “Singles Day” sale next week approaches, coincidentally…). A listing closer to home for other Chinese ADRs in Hong Kong could, of course, follow an Alibaba success and draw southbound money flows from the Chinese mainland down to HK (or west or east, as it were, from elsewhere, too…). The latest reports from Bloomberg News as of Friday afternoon suggest Alibaba may seek up to $15 billion in an HK listing and the company is still currently expected to proceed with its listing hearing in Hong Kong next week.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. Even as the two dueling sides in the U.S.-China trade war make nice and talk about tariff delays and a Phase One deal appears to remain on approach—possibly by December now, as of latest reports—it also remains possible that trade talks go sideways or that “concessions” are not viewed as enough to satisfy one side or the other and a negative cycle once again ensues. That scenario is seeming less likely at this point than some sort of delay or cancellation to the December tariffs amid an as-yet-undetailed “Phase One” agreement that sees both sides giving up a little but promising “bigly” (if vaguely) and perhaps hammering out a few preliminaries that set up larger negotiations post-U.S.-elections. Then again, who knows? Any shocks to what is clearly perceived as trade progress by markets might weigh on markets, obviously. The U.S. side ensured late this week that tariff rollbacks were by no means a certain thing.

- Hong Kong protests continue to weigh on HK retail sales and tourism (even Disney’s CEO Bob Iger remarked this week that HK protests could hit earnings via Hong Kong Disneyland, for example). A protester died—student Chow Tsz-lok—after suffering brain damage in a fall amid the tear-gassing of protestors.

- Moody’s cut India’s outlook, Bloomberg reported today, noting that India’s rupee declined the most in Asia after Moody’s Investors Services lowered the nation’s rating outlook and cited negative growth concerns. A change in the rating outlook remains only the first step toward a downgrade, and as Moody’s rates India a step higher than both Fitch and S&P, the move may not have come as entirely surprising, the article continued.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 8 was DUO Network Token, up 471 percent.

- Coke One North America, the IT firm behind Coca-Cola’s bottle manufacturing supply chain processes, is expanding its blockchain efforts to 70 partners, reports CoinDesk. The blockchain project promises to improve distribution for the participants, the article explains, as all manufacturers can access a permissioned blockchain containing each other’s’ orders, capabilities and requirements.

- Cryptocurrency commerce has started growing again, reports Bloomberg, with the amount of digital money sent to 16 merchant service providers such as BitPay rising 65 percent between January and July, according to Chainalysis data. “It suggests there’s more overall trust in crypto,” senior economist at Chainalysis Kim Grauer said in a phone interview. Looking year-to-date as well, bitcoin has more than doubled, as seen in the chart below.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 8 was carVertical, down 86.07 percent.

- Another flash crash is sparking concerns that traders are manipulating the bitcoin market, reports CoinTelegraph. Last week we saw sudden, erratic behavior between two exchanges that seemed to influence BTC/USD, and on Tuesday, the CME Group’s bitcoin futures continued the trend. In early trading, BTC/USD futures suddenly tanked below $8,500 before rebounding to $9,300.

- According to Bitcoin’s global strength indicator, the currency’s price is likely to decline soon after becoming overheated, according to Bloomberg. The indicator is a measure of upward and downward movement of successive closing prices and is nearing the 70 level, which indicates overbought territory.

Opportunities

- The “Bitcoin Rich List,” or the number of addresses holding more than 1,000 BTC has grown over the past 12 months, reports CoinDesk. Since September 2018, the metric has registered growth of 30 percent, possibly reflecting an influx of high-net-worth investors, the article explains.

- A blockchain-powered gold trading platform known as Tradewind Markets has developed and launched a system for stablecoin issuers on its platform to track the provenance of their precious metals, reports CoinDesk. Designed with the Royal Mint of Canada, Tradewind Origins is “taking its shot at stopping counterfeit gold seals and helping precious metals investors find metals that are produced responsibly.”

- In more precious metal-crypto news, CoinShares Group is launching a gold-backed cryptocurrency that “could functionally act as a stable coin, but be backed by something physical” such as gold. The token, called DGLD, is set to begin trading on Blockchain Luxembourg SA’s and MKS SA’s platforms in the next few week following final regulatory approvals, reports Bloomberg News.

Threats

- According to one Bloomberg article, states dabbling in blockchain technology, or planning to issue their own digital currencies, isn’t flattery – it could be competition instead. The future of digital currency is being shaped more and more by national governments, which is ironic since bitcoin’s origins almost seem anarchic. A survey from the Bank for International Settlements show that some 70 percent of central banks are examining their options in the area of issuance.

- A news release from the Commodity Futures Trading Commission (CFTC) states that the district court for the Eastern District of New York ordered a fine of $4.25 million for another cryptocurrency investment scheme – for fraud and misappropriating client funds, reports CoinDesk. The fine was set against Blake Harrison Kantor and Nathan Mullins, plus four firms. Kantor and Mullins were further ordered to hand over “ill-gotten gains” of $515,759 and $89,574, respectively.

- Five men have been apprehended by Malaysian authorities and charged with stealing 85 bitcoin machines, reports CoinDesk. Four men and one woman rented a building in Seremban, Malaysia, adjacent to a warehouse storing the bitcoin machines, according to the Sun Daily. They drilled through the concrete wall connecting the two buildings.

Airline Sector

Strengths

- Delta Air Lines reported stellar earnings for the third quarter. Net income rose 13.1 percent year-on-year to $1.5 billion, or $2.31 per share. Operating cash flow was $2.2 billion, up an incredible 50 percent from the same three-month period a year earlier. Delta returned $470 million to shareholders through dividends and share buybacks during the quarter.

- Spirit Airlines announced that it has signed a deal with Airbus for the purchase of 100 new Airbus A320neo Family aircraft, with the option to buy up to 50 additional aircraft. The jets are planned for delivery through 2027. Spirit President and CEO Ted Christie called the order “another milestone” for the low-cost carrier, which is the fastest growing airline in the U.S. What’s more, the carrier will unveil its new cabin redesign in December 2019, complete with new, more comfortable seats and extra legroom.

- Global flight demand, as measured by revenue passenger kilometers (RPKs), edged up a modest 3.8 percent year-on-year in August, according to the International Air Transport Association (IATA). China saw the fastest demand growth of any region, at 10.1 percent, though this number was down from 11.7 percent annual growth in the previous month. The most impressive stat from IATA’s monthly report was that the industry-wide load factor reached a new all-time record for August. The passenger load factor, which measures how efficiently a carrier fills seats and generates revenue, registered 85.9 percent, up a tick from the same month last year.

Weaknesses

- Investigators from the Indonesian National Transportation Safety Committee officially put the blame on the Boeing 737 MAX for the downing of the country’s Lion Air flight last year. After months of investigation, officials said Boeing was at fault for “introducing an automated system in the MAX without adequately briefing airlines and their crews about its existence or instructing them how to override the software should it malfunction,” writes the New York Times. The report undercuts Boeing’s insistence that pilots should have been able to deal with the software malfunction using standard emergency procedures.

- Boeing’s earnings took a major hit in the third quarter and the first nine months of the year. The manufacturer reported net earnings of $1.2 billion in the three months through September 30, more than half of what they were a year earlier. As for the nine-month period through September, net earnings were $374 million, down a whopping 95 percent from the $7.0 billion the company made in the same period in 2018. Operating cash flow for the quarter was negative $2.4 billion, reflecting lower deliveries of its 737 jet as well as advance payments.

- Alaska Airlines and American Airlines scaled back their shared rewards program for the second time in the third quarter, a move that will likely raise the ire of some frequent fliers who have taken advantage of the partnership over the years. What this means is that passengers may no longer redeem their Alaska rewards points on American flights, and vice versa. When asked for an explanation, an American spokesperson said the cuts were put in place after a “review of its airline partners and programs.”

Opportunities

- United Continental raised its earnings forecast for the remainder of the year as travel demand continues to climb. Thanks to another quarter of expanding pre-tax margin, the carrier has “further confidence to raise our full year 2019 adjusted diluted EPS guidance, putting us ahead of pace to achieve our goal of $11 to $13 in adjusted diluted EPS by the end of 2020,” United CEO Oscar Munoz stated.

- American Airlines announced it will be spending $100 million on a new parts distribution facility at its main hub, DFW International Airport. The project, construction for which will begin this fall and take between 12 and 18 months, will help speed up the delivery of parts across the carrier’s supply chain. “This new facility will provide ample space to store parts, which enables us to select parts up to 75 percent faster than we currently can, minimizing any potential maintenance delays,” an American spokeswoman told the Dallas Morning News.

- Australia’s Qantas Airways successfully completed its test run of a 19-hour nonstop flight from New York City to Sydney, a route that some analysts believe will revolutionize air travel. For one, regulators will need raise the cap on pilot duty time from its present 18.5 hours for the Qantas route to be regularly scheduled. “This is the last frontier in commercial aviation,” commented Qantas CEO Alan Joyce.

Threats

- Congress is set to ratchet up its scrutiny of Boeing leadership as new details emerge suggesting management put pressure on company engineers to certify their own systems. The House Transportation and Infrastructure Committee will be investigating such conflicts of interest that are believed to have contributed to the crash of Indonesia’s Lion Air flight in October 2018. In related news, a Southwest Airlines pilots union have filed a lawsuit against Boeing, saying the manufacturer misled pilots. The group is seeking some $100 million in lost income from Boeing since the group believes it was the company’s negligence that led to the grounding of its 737 MAX aircraft. Boeing maintains that the MAX will return to service by the end of the year.

- Operating margins for U.S.-based carriers will contract for the third straight year in 2019 due to oversupply, according to Oliver Wyman’s most recent economic analysis. With flight demand rising worldwide, airlines have added capacity and new routes at a rapid pace, making pricing more competitive and putting pressure on yields. As such, margins are expected to narrow to between 5 and 6 percent by the end of the year, down from 9.2 percent in 2018 and 12.7 percent a year earlier.

- The International Monetary Fund (IMF) revised down its growth forecast for the world economy to just 3 percent, its lowest level since the financial crisis. In addition, odds of a full-blown recession are the highest they’ve been in more than a decade. Slower economic growth could dampen air travel demand.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.94 | +0.23 | +13.33% |

| Oil Futures | 57.43 | +1.23 | +2.19% |

| Hang Seng Composite Index | 3,734.97 | +77.12 | +2.11% |

| S&P Basic Materials | 377.42 | +7.39 | +2.00% |

| Korean KOSPI Index | 2,137.23 | +37.03 | +1.76% |

| S&P Energy | 446.13 | +8.77 | +2.01% |

| Nasdaq | 8,475.31 | +88.92 | +1.06% |

| DJIA | 27,681.24 | +333.88 | +1.22% |

| Russell 2000 | 1,598.86 | +9.53 | +0.60% |

| S&P 500 | 3,093.08 | +26.17 | +0.85% |

| Gold Futures | 1,459.20 | -52.20 | -3.45% |

| XAU | 91.69 | -4.25 | -4.43% |

| S&P/TSX VENTURE COMP IDX | 536.97 | -4.52 | -0.83% |

| S&P/TSX Global Gold Index | 234.00 | -13.01 | -5.27% |

| Natural Gas Futures | 2.79 | +0.08 | +2.80% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,137.23 | +90.98 | +4.45% |

| 10-Yr Treasury Bond | 1.94 | +0.35 | +22.33% |

| Gold Futures | 1,459.20 | -53.60 | -3.54% |

| S&P Basic Materials | 377.42 | +28.13 | +8.05% |

| S&P 500 | 3,093.08 | +173.68 | +5.95% |

| DJIA | 27,681.24 | +1,335.23 | +5.07% |

| Nasdaq | 8,475.31 | +571.57 | +7.23% |

| Oil Futures | 57.43 | +4.84 | +9.20% |

| Hang Seng Composite Index | 3,734.97 | +260.28 | +7.49% |

| S&P/TSX Global Gold Index | 234.00 | -14.60 | -5.87% |

| XAU | 91.69 | +0.23 | +0.25% |

| Russell 2000 | 1,598.86 | +119.40 | +8.07% |

| S&P Energy | 446.13 | +29.36 | +7.04% |

| S&P/TSX VENTURE COMP IDX | 536.97 | -13.63 | -2.48% |

| Natural Gas Futures | 2.79 | +0.56 | +24.89% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 91.69 | -5.23 | -5.40% |

| S&P/TSX Global Gold Index | 234.00 | -20.92 | -8.21% |

| Gold Futures | 1,459.20 | -50.30 | -3.33% |

| DJIA | 27,681.24 | +1,303.05 | +4.94% |

| S&P 500 | 3,093.08 | +154.99 | +5.28% |

| Nasdaq | 8,475.31 | +436.16 | +5.43% |

| Korean KOSPI Index | 2,137.23 | +216.62 | +11.28% |

| Natural Gas Futures | 2.79 | +0.66 | +31.11% |

| S&P Basic Materials | 377.42 | +13.21 | +3.63% |

| Russell 2000 | 1,598.86 | +66.73 | +4.36% |

| Oil Futures | 57.43 | +4.89 | +9.31% |

| Hang Seng Composite Index | 3,734.97 | +238.89 | +6.83% |

| S&P/TSX VENTURE COMP IDX | 536.97 | -59.36 | -9.95% |

| S&P Energy | 446.13 | +4.64 | +1.05% |

| 10-Yr Treasury Bond | 1.94 | +0.22 | +12.86% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Semafo Inc

Petroleo Brasileiro SA

Barrick Gold Corp

Kirkland Lake Gold Ltd

Liberty Gold Corp

Newmont Goldcorp Corp

Chevron Corp

Equinor ASA

Royal Dutch Shell PLC

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. Formerly known as Dow Jones-UBS Commodity Spot Index (DJUBSSP), the Bloomberg Commodity Spot Index measures the price movements of commodities included in the Bloomberg CI and select subindexes. It does not account for the effects of rolling futures contracts or the costs associated with holding physical commodities and is quoted in USD. The MSCI Emerging Markets Europe 10/40 Index (Net Total Return) is a free float-adjusted market capitalization index that is designed to measure equity performance in the emerging market countries of Europe (Czech Republic, Greece, Hungary, Poland, Russia, and Turkey). The index is calculated on a net return basis (i.e., reflects the minimum possible dividend reinvestment after deduction of the maximum rate withholding tax). The index is periodically rebalanced relative to the constituents’ weights in the parent index. There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. The Bangkok SET Index is a capitalization-weighted index of all the stocks traded on the Stock Exchange of Thailand. The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange. The TWSE, or TAIEX, Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The index was based in 1966. The index is also known as the TSEC Index. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The index was created with a base index value of 100 as of July 28, 2000 The Bombay Stock Exchange Sensitive Index (Sensex) is a cap-weighted index. The selection of the index members has been made on the basis of liquidity, depth, and floating-stock-adjustment depth and industry representation. Sensex has a base date and value of 100 on 1978-1979. The index uses free float. The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries. With 1,202 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. Free cash flow (FCF) is a measure of how much cash a business generates after accounting for capital expenditures such as buildings or equipment. This cash can be used for expansion, dividends, reducing debt, or other purposes.