Signal and Bitcoin: Twenty-First Century Tools of Personal and Economic Freedom

Date Posted: January 15, 2021

Read time: 50 min

Founding Father Benjamin Franklin said it best: "They who can give up essential liberty to obtain a little temporary safety deserve neither liberty nor safety." In this light, what are we to make of Trump's social media suspension?

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Key Points:

- Social media’s suspension of President Trump’s social media accounts should be troubling to everyone, whether you support him or not. Recall Ben Franklin: “They who can give up essential liberty to obtain a little temporary safety deserve neither liberty nor safety.”

- Privacy seekers are downloading Signal to replace WhatsApp.

- Biden’s proposed relief package, at $1.9 trillion, is expected to boost investor demand for real assets, including gold, Bitcoin and Ethereum.

In my final commentary of 2020, I wrote that the U.S. media has a major trust issue. According to recent polls, most Americans put little faith in what they see and read on TV and the internet.

These negative sentiments were probably not improved much by big tech firms’ decision to suspend President Donald Trump from their platforms.

Twitter was the first to announce a permanent ban last Friday, following Wednesday’s storming of the Capitol. In the blink of an eye, more than 88 million followers could no longer visit the U.S. president’s account.

Other platforms soon followed suit: Facebook, Instagram, Snapchat, TikTok, YouTube, Pinterest.

The decision to muzzle Trump may not technically be unconstitutional—it was made not by the government but private corporations—but it’s highly problematic.

Even Twitter CEO Jack Dorsey admits as much. Defending his company’s deletion of Trump’s account, Dorsey tweeted that such bans “fragment the public conversation” and “limit the potential for clarification, redemption and learning.” He added that it “sets a precedent that I feel is dangerous.”

Many of Trump’s overseas critics agree. German chancellor Angela Merkel, who’s often shared an icy relationship with her U.S. counterpart, called Twitter’s move a breach of Trump’s “fundamental right to free speech.” Clément Beaune, France’s minister of state for European affairs, told Bloomberg TV that silencing an elected official “should be decided by citizens, not by a CEO.”

The crackdown isn’t limited to Trump. Parler, a networking app favored by Trump’s supporters, hit roadblocks this week when Apple and Google removed the app from its online stores. The service, which is financed in large part by hedge fund manager Robert Mercer, finally went offline after Amazon dropped it as a web hosting client.

I acknowledge these actions were prompted by a need to root out extremism and violence. I join others in calling on social media companies to do a better job at preventing extremism from flourishing. At the same time, there has to be a more equitable solution than permanently shutting down entire channels of free speech.

Founding Father Benjamin Franklin said it best: “They who can give up essential liberty to obtain a little temporary safety deserve neither liberty nor safety.”

Coinbase learned this lesson the hard way. In late September, the digital currency exchange instated a companywide ban on talking politics of any kind at work. Within days of the announcement, as many as 60 Coinbase employees had resigned.

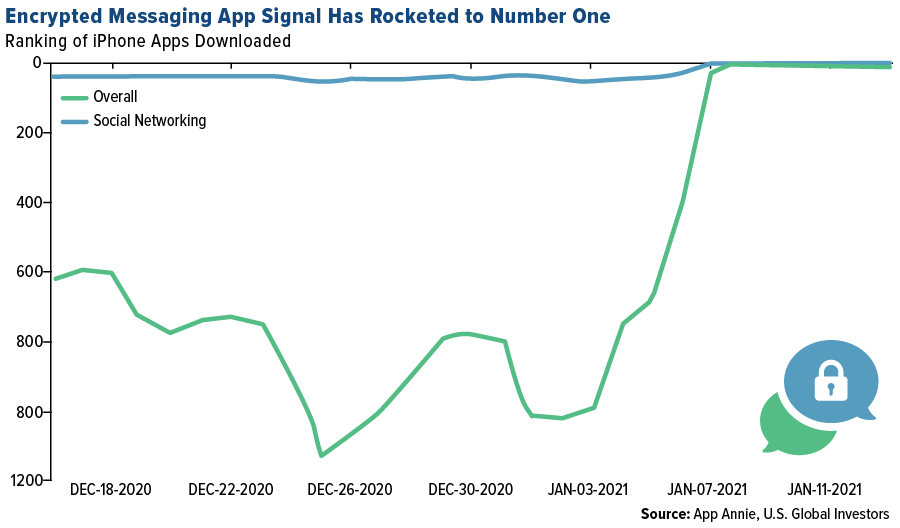

A Signal of Privacy and Free Speech

The social media crackdowns have helped fuel people’s search for alternative communications platforms. One of those alternatives is Signal, a little-known messaging service that first debuted in 2014.

Similar to WhatsApp, Signal encrypts users’ messages end-to-end. Unlike WhatsApp, though, Signal isn’t owned by Facebook—or any other big tech firm, for that matter. It’s run by a tax-exempt non-profit, meaning its operations rely on donations.

So far this month, the app has seen a massive spike in downloads following WhatsApp’s announcement to users that it was changing its privacy policy. Tesla chief Elon Musk also threw his weight behind the app, tweeting to his 42 million followers: “Use Signal.”

According to app analytics firm App Annie, Signal has ranked number one in iPhone app downloads every day since January 9.

As expected, Musk’s tweet triggered not only downloads but also investor interest. The problem is that Signal the messaging app isn’t listed, so investors were mistakenly buying shares of Signal Advance, a thinly-traded medical supplies company. As of January 11, Signal Advance stock had jumped more than 10,000% in 30 days, from $0.38 to $38.70. Daily trading volume surged from as little as a few thousand shares to over 2 million shares.

A similar phenomenon occurred last spring when investors began buying the wrong Zoom. Instead of investing in Zoom Video Communications—whose video conferencing services were suddenly in high demand thanks to lockdowns—investors piled into Zoom Technologies, a small Chinese firm.

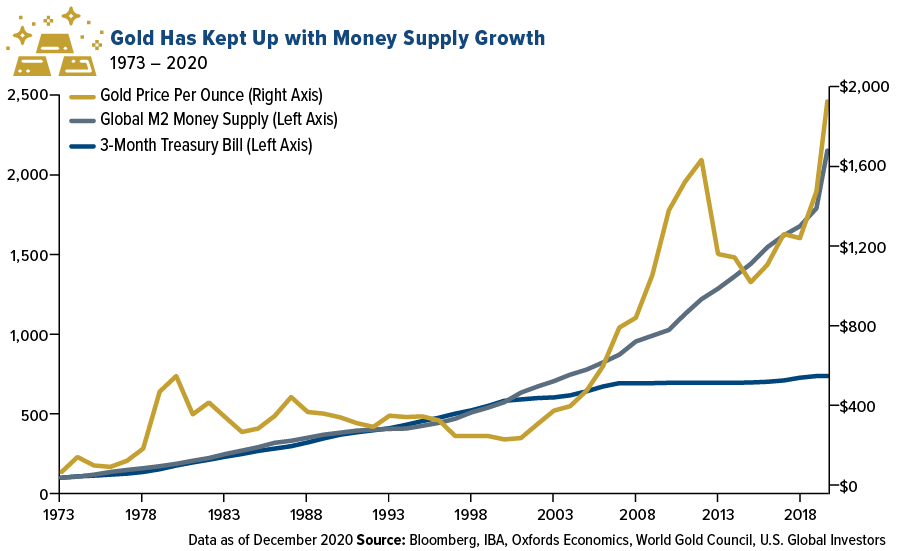

The Price of Gold Has Historically Kept Pace with Money Supply Growth

The World Gold Council (WGC) has released its 2021 outlook, which you can download here, and there’s one chart in particular that stood out to me.

As you can see below, since President Richard Nixon formally ended the gold standard in the early 1970s, the price of gold has done a much better job at keeping pace with global money supply growth than Treasury bills have. Over the years, this has helped investors and savers preserve capital.

I believe preserving your family’s wealth is reason enough to ensure you follow the 10% Golden Rule. As I shared with you recently, we’ve entered an era of record money-printing in an effort to curb the economic effects of the pandemic. U.S. money supply growth is up an unheard-of 66% from the last year.

The more fiat currency that’s in circulation, the more valuable I expect real assets like gold to become.

President-elect Joe Biden, who’s scheduled to take office next week, has called for a massive $1.9 trillion relief package that would include $1,400 checks for American adults. The bill, if passed, could lead to additional money-printing and, consequently, boost inflation.

In which case, you’d want to have some exposure to gold and other real assets like real estate and commodities.

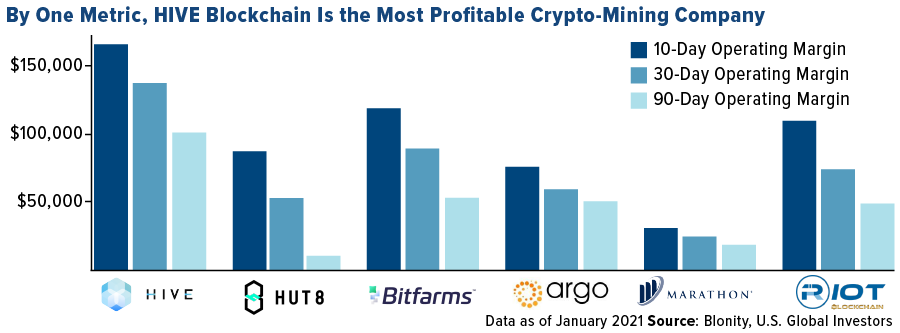

HIVE Is Delivering on Operating Margin

That includes Bitcoin and Ethereum, two payment systems that provide end-to-end encryption, much like Signal. The world’s number one and number two cryptocurrencies recorded a weekly loss after Bitcoin hit a record high of nearly $42,000. After such a move, a correction is to be expected. I see the dip as a buying opportunity.

Investors seeking other ways to gain exposure have a few options. CME Group already offers Bitcoin futures and options, and next month, the exchange will be launching Ether futures. This is expected to support demand for Ethereum.

Then there are the miners. At the moment, HIVE Blockchain Technologies is the only one that mines both Bitcoin and Ethereum. What’s more, by one metric, HIVE is also the most profitable, beating its peers on operating margin for the 10-day, 30-day and 90-day periods.

Curious about the difference between Bitcoin and Ethereum? Watch my latest video to get the full details. Click here!

January 11, 2021Silver Was the Top Performing Commodity in 2020. Will Copper Be Next? |

January 7, 2021Gold and Precious Metals in the Spotlight: 2020 Recap |

January 4, 2021Low Inflation? Asset Prices at Record Highs Suggests Otherwise |

|||

Gold Market

This week spot gold closed the week at $$1,828.45, down $20.56 per ounce, or 1.11%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.56%. The S&P/TSX Venture Index came in up 1.26%. The U.S. Trade-Weighted Dollar rose 0.76%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-13 | CPI YoY | 1.3% | 1.4% | 1.2% |

| Jan-14 | Initial Jobless Claims | 789k | 965k | 784k |

| Jan-15 | PPI Final Demand YoY | 0.8% | 0.8% | 0.8% |

| Jan-17 | China Retail Sales YoY | 5.5% | — | 5.0% |

| Jan-19 | Germany CPI YoY | -0.3% | — | -0.3% |

| Jan-19 | Germany ZEW Survey Expectation | 58.5 | — | 55.0 |

| Jan-19 | Germany ZEW Current Situation | -68.5 | — | -66.5 |

| Jan-20 | Eurozone CPI Core YoY | 0.2% | — | 0.2% |

| Jan-21 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Jan-21 | Initial Jobless Claims | 830k | — | 965k |

| Jan-21 | Housing Starts | 1562k | — | 1547k |

Strengths

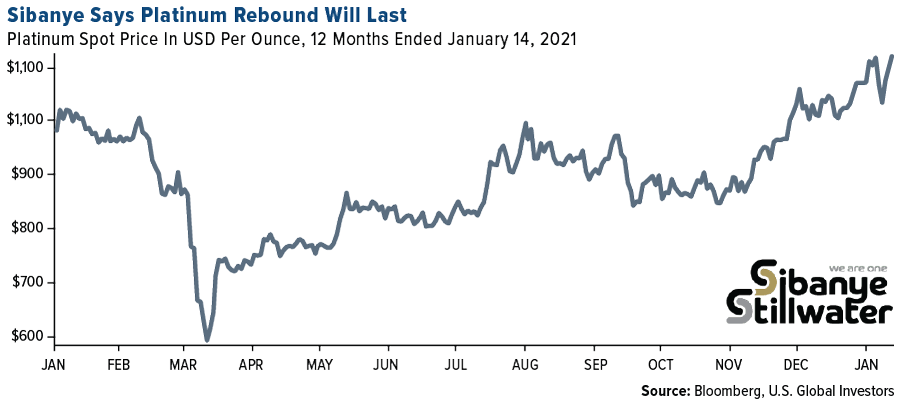

- The best performing precious metal for the week was platinum, up 0.56% on positive comments on price outlook by an industry leader. After dropping on Monday, gold climbed back on Tuesday as President-elect Joe Biden is set to unveil plans for a multi-trillion-dollar stimulus package. This could mean huge inflation, which is historically supportive for the yellow metal. Rhodium is on a tear already for the year. Prices now exceed $20,000 an ounce, according to Johnson Matthey Plc data. The precious metal used to clean toxic emissions is soaring on the bet that China will see a recovery in vehicle sales.

- Russia’s $583 billion reserves now consistent of more gold than U.S. dollars for the first time on record. Bloomberg notes gold made up 23% of Russia’s central bank holdings as of the end of June 2020 and the share of dollar assets fell to just 22%, which is down from over 40% in 2018. The move is part of the country’s goal to “de-dollarize” the economy amid U.S. sanctions and growing tensions. Gold is now the second-biggest component of reserves after the euro.

- The World Gold Council (WGC) predicts gold demand in India will rebound this year after more than halving to just 275.5 tons in 2020. The group estimates pent-up demand from delayed weddings and festivals will boost sales. Newmont, the world’s largest gold producer, announced a $1 billion share repurchase plan for a second year, reports Bloomberg. The miner raised its dividend by 60% to 40 cents a share less than three months ago on the heels of higher gold prices boosting returns.

Weaknesses

- The worst performing precious metal for the week was silver, down 2.57% on the fall in gold. Gold slid as much as 1.7% on Monday after suffering its worst three-day decline through Friday since August. “The metal is starting to look precarious,” said Rick Bensignor, president of Bensignor Investment Strategies in a Bloomberg interview, highlighting gold’s failure to move above $1,927 was a major technical miss. The rising U.S. dollar and higher Treasury yields threaten more trouble for the yellow metal.

- UBS Group sees gold weakening to $1,800 by year-end as the macroeconomic backdrop improves and the Federal Reserve signals it will taper its bond-buying program. Analysts including Giovanni Staunovo said low real rates and a weaker dollar should support gold’s recovery to around $1,950 in the first quarter. However, prices may come under pressure mid-year due to modest ETF inflows.

- Hecla Mining announced preliminary results for the fourth quarter and full-year 2020 that estimate gold production fell 23% year-over-year to 208,962 ounces. 2019 was Hecla’s highest gold production on record. The miner did say it expects an increase of 7% in silver ounces from the year prior.

Opportunities

- Peru’s new mining minister Jaime Galvez has vowed to streamline the consultation period prior to granting mining licenses as part of planned reforms to the country’s mining regulations. Peru currently has a $56 billion mining construction portfolio and could continue to grow amid new interest. Precious metals producers such as Rio Tinto, Barrick Gold, Fortuna Silver Mines and Gold Fields could be big beneficiaries. Oro X Mining, a gold explorer already developing projects in the country, now has an even more favorable environment.

- Gold production in Burkina Faso surged to a record 60.8 tons last year, according to the country’s Chamber of Mines, after recovering from a jihadist raid in 2019 that killed 39 employees of Semafo’s operation. Endeavour Mining bought Semafo in 2020 for $690 million in shares. Bloomberg reports Burkina Faso is now Africa’s fourth-biggest gold miner after Ghana, South Africa and Sudan.

- Sibanye Stillwater, the world’s top platinum miner, said it expects the price of the precious metal to climb more than 80% over the next four to five years as the globally economy improves and supply shrinks. “Platinum has only just started to re-rate and it will continue,” CEO Neal Froneman said. “There is no reason why platinum will not eventually trade at $2,000 an ounce and probably even higher.” Bloomberg reports the metal has nearly doubled since its 18-year low in March due to supply disruptions and growing demand from China for use in pollution-control devices.

Threats

- U.S. retail sales disappointed, falling 0.7% in December after a drop of 1.4% in November. Economists were expecting a decrease of just 0.2%, reports Kitco. Gold fell immediately after the data was released to $1,841 an ounce. The U.S dollar was also higher on Friday morning, sending both bullion and silver lower. A strengthening dollar is a threat for precious metal and commodity prices.

- Chile’s state-owned Codelco, the world’s top copper producer, said it will up precautionary measures against the coronavirus at its mines amid a recent increase in infections. This is a cautious sign that other miners might need to take similar measures. Rising virus cases worldwide remains a threat to miners of all types who might face another round of lockdowns.

- Members of Arizona’s San Carlos Apache tribe filed a property lien on Thursday in an attempt to regain control over land the U.S government is set to give to Rio Tinto for its copper mine, reports Reuters. The tribal members say the government has illegally occupied the land for more than 160 years and does not have the right to give it to anyone.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.91%. The S&P 500 Stock Index fell 1.48%, while the Nasdaq Composite fell 1.54%. The Russell 2000 small capitalization index gained 1.51% this week.

- The Hang Seng Composite gained 2.05% this week; while Taiwan was up 0.99% and the KOSPI fell 2.10%.

- The 10-year Treasury bond yield fell 2 basis points to 1.092%.

Domestic Economy and Equities

Strengths

- Industrial production rose 1.6% in December, the Federal Reserve reported Friday. That’s the largest gain since July. The gain was well above Wall Street expectations of 0.5%, according to a survey by the Wall Street Journal. For the fourth quarter, industrial production rose at an 8.4% annual rate. Manufacturing has been a bright spot in the economy and has rolled along even as the broader economy has slowed.

- Fed Chairman Jerome Powell said Thursday the U.S. economy could return to pre-coronavirus pandemic level "fairly soon" thanks to a torrent of monetary and fiscal aid over the past year. The nearly $4 trillion in direct fiscal stimulus approved by Congress and the Trump administration — including the $2.2 trillion March CARES Act and the $900 billion relief bill passed in December — played a vital role in staving off deeper economic damage, Powell said. While he stressed that the economy will not fully recover until the pandemic is under control, the central bank head said he was "optimistic" about the outlook over the "next couple of years."

- Etsy was the best performing S&P 500 stock for the week, increasing 16.38 percent. The stock’s price target was raised to a street-high view of $235 from $165 at Roth Capital Partners, which wrote that strong traffic data pointed to robust sales in the holiday season.

Weaknesses

- First-time claims for unemployment insurance jumped to 965,000 last week amid signs of a slowdown in hiring due to pandemic restrictions, the Labor Department reported Thursday. The total was worse than Wall Street estimates of 800,000 and above the previous week’s total of 784,000. The total was the highest since the week of Aug. 22, when just over 1 million claims were filed. Continuing claims also were higher, rising 199,000 to 5.27 million. That figure runs a week behind the weekly claims total and increased for the first time since late November.

- U.S. retail sales declined further in December as renewed measures to slow the spread of COVID-19 undercut spending at restaurants and reduced traffic to shopping malls, the latest sign the economy lost considerable speed at the end of 2020. Retail sales dropped 0.7% last month, the Commerce Department said on Friday. Data for November was revised down to show sales declining 1.4% instead of 1.1% as previously reported. Economists polled by Reuters had forecast retail sales unchanged in December.

- Twitter Inc was the worst performing S&P 500 stock for the week, decreasing 12.24%. The stock seemed to drop on backlash from the widespread banning of accounts that started with the permanent banning of Donald Trump’s account.

Opportunities

- President-elect Joe Biden on Thursday unveiled the details of a $1.9 trillion coronavirus rescue package designed to support households and businesses through the pandemic. The proposal, called the American Rescue Plan, includes several familiar stimulus measures in the hope the additional fiscal support will sustain U.S. families and firms until the Covid-19 vaccine is widely available. The plan is the first of two major spending initiatives Biden will seek in the first few months of his presidency, according to senior Biden officials. The second bill, expected in February, will tackle the president-elect’s longer-term goals of creating jobs, reforming infrastructure, combating climate change and advancing racial equity.

- Amazon-backed Deliveroo could go public at a $13.6 billion valuation. Sources said the food delivery startup may be aiming for an April IPO, in what’s expected to be a blockbuster year for European tech IPOs.

- $2 billion Kaseya is planning to IPO. The IT management firm caters to small and mid-size companies and has seen significant growth in the past year as business moves online amid the COVID-19 pandemic.

Threats

- The focus for traders next week will be on Wednesday’s inauguration proceedings for President-elect Joe Biden. The threat of violent protests looms ahead of what is normally a non-event for financial markets. But with President Trump’s supporters still refusing to accept that the election outcome was fair and after the historic storming of Capitol Hill by rioters on January 6, fresh unrest could unsettle markets, sparking some risk aversion, as it could be foretelling of more insurgence to come.

- Warren Buffett’s favorite market indicator has surged to a 13-year high, signaling global stocks are the most overvalued since the financial crisis and ripe for a correction. The global version of the "Buffett indicator" takes the combined market capitalizations of publicly traded stocks worldwide and divides it by global GDP. A reading north of 100% suggests the global stock market is overvalued relative to the world economy. The gauge climbed past 121% last weekend, Bloomberg data shows, marking its highest reading since October 2007.

- Biden will still examine Big Tech. Makan Delrahim, the Department of Justice’s (DOJ) antitrust boss, said Wednesday the Biden administration will continue the federal government’s antitrust investigations into US tech companies once it comes to power in January.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was corn, up 6.95% on worries that a drought in Argentina will reduce the harvest in addition to a USDA forecast of reduced domestic supplies. Rhodium is on a tear already for the year. Prices now exceed $20,000 an ounce, according to Johnson Matthey Plc data. The precious metal used to clean toxic emissions is soaring on the bet China will see a recovery in vehicle sales.

- Wall Street is the most bullish on commodities in a decade based on net-long positions. Bloomberg data shows investors held 2.3 million futures and options contracts on commodities in the week ended January 5, which is the most since January 2011. Corn and sugar supplies are tightening and sending prices soaring. Bets on rising gold prices rose to a 16-week high, and platinum net-longs are at the highest since February. Investors also boosted net-long positions bets on silver for the fifth week in six.

- Rock Tech Lithium plans to raise $400 million to build a lithium refinery in Germany and has already attracted support from billionaire investors such as Peter Thiel. The development is part of Europe’s push to create a local electric-vehicle battery industry, reports Bloomberg. “We believe there will be bottlenecks as access to sustainably sourced lithium and conversion capacities outside China is scarce,” said Rock Tech co-owner.

Weaknesses

- The worst performing commodity for the week was palm oil, down 10.63% on fears key buyers will have restrained demand with COVID-19 infections approaching a new peak. Nickel dropped from a six-year high on Friday and copper had a weekly decline amid doubts regarding the approval of a U.S. stimulus package. Nickel fell 1.1% in London, but still rose 2.4% for the week due to demand in electric vehicle batteries.

- Exxon Mobile is under investigation by the SEC after a whistleblower complaint alleges overvaluation of property in the Permian Basin. The Wall Street Journal reports several people involved in the valuation complained during a 2019 internal assessment that workers were being forced to use unrealistic assumptions about how quickly wells could be drilled to reach a higher valuation. Exxon shares fell 4.81 percent in on Friday,

- Widespread, extreme cold temperatures took energy markets by surprise and is straining global systems. Bloomberg reports the spikes in energy demand, coupled with weak wind generation, power plant closures and LNG tanker delays, highlight shortcomings in global systems in weather conditions that are only set to get more volatile. Record high demand in China, Japan and South Korea led to a scramble for natural gas to keep lights on. Heavy snow brought down grid sections in Sweden and French households were advised to delay laundry to save electricity.

Opportunities

- Deal making in the utility space could pick up this year as companies recover from 2020. “We believe 2021 will be a volatile and intense year, with incredible pace,” said George Bilicic, vice chairman of investment banking and the global head of Power, Energy & Infrastructure at Lazard Ltd. “It is completely possible to see a couple or more very large transactions, whether of a merger-of-equals type or otherwise.” Bloomberg predicts more utilities may look to sell off their natural gas assets on climate concerns.

- Employment at oilfield services companies rose by 4,592 in December, the fourth straight month of increases, which could be a sign that the industry is through the worst of the downturn. Oil futures in New York rose to a 10-month high on Tuesday to above $53 a barrel as the dollar declined and Saudi Arabia announced output cuts. Goldman Sachs says oil demand could get a boost of at least 1 million barrels day due to colder temperatures in Asia and Europe. OPEC appears on track with its objective to deplete the world’s bloated oil inventories through production cuts.

- Occidental Petroleum plans to build a facility in the Permian Basin, America’s biggest oilfield, that it believes could change the way the world thinks about fossil fuel emissions. The world’s first large-scale direct air capture plant will take CO2 from the atmosphere and pump it underground to remain for millions of years, reports Bloomberg. The facility is expected to cost millions of dollars and will need support from tax credits and outside investors to be economically viable. There may be other choices Occidental or the industry could make to address the total costs of using fossil fuels.

Threats

- A surge in LNG prices has put more than $50 billion worth of planned power projects and import infrastructure at risk of being economically unviable, reports Bloomberg. Countries such as Vietnam, Pakistan and Bangladesh have proposed LNG-fired energy plants that are now at high risk of cancellation due to rising input prices. The Institute for Energy Economics and Financial Analysis says unpredictable spot prices and increasingly volatile contracts could make electricity produced by these projects unaffordable.

- Cargill Inc. is in talks to sell its 50% stake in Alvean, the world’s largest sugar trader, as it seeks to focus on food processing and meat. Cargill is one of America’s biggest closely held businesses and has been changing its business focus as agricultural commodity traders have struggled to make money in recent years. This move could spark a larger movement away from the sugar trade and the liabilities the food industry could face over purposely adding sugar to a wide array of nutrients to make them sweet but unhealthy food products.

- Growing demand from China for corn is likely to strain global supplies. Chinese corn futures rose for a 10th straight day as the USDA made a big cut to its forecast for U.S. output. The agency also increased is estimate for Chinese imports by 1 million tons to 17.5 million tons due to the recovery of China’s domestic hog herd. Bloomberg reports icy conditions, hoarding and stockpiling ahead of the Lunar New Year are exacerbating the shortage.

Airline Sector

Strengths

- The best performing airline stock for the week was Azul, up 11.3%. The space travel industry got a boost of interest this week. Ark Investment Management announced its plans to launch a space-focused ETF. Shares of Virgin Galactic Holdings jumped as much as 18% on Thursday morning on the news.

- Low-cost leisure carrier Allegiant is adding three cities and 21 non-stop routes to its network. The airline is offering fares as low as $39 to stimulate traffic on these new routes. Low cost, retail-oriented carriers (point-to-point) continue to show the earliest improvements in the industry, far ahead of the business-oriented, hub and spoke carriers. Dubai’s Emirates plans to expand services to the U.S. by resuming nonstop services to Seattle from February 1 and to Dallas and San Francisco from March 2.

- The U.S. is requiring negative COVID tests for all inbound arrivals and could take effect as soon as January 26. These tests have already been required for travelers from the U.K., where a highly contagious virus strain is spreading. The move could allow for higher international traffic in the future and help revive air travel.

Weaknesses

- The worst performing airline stock for the week was Norwegian Air Shuttle, down 10.4%. Low-cost carrier Norwegian Air announced on Thursday its plans to cut long-haul flights between the U.S. and Europe. Its airline fleet will drop to just 50 aircraft from 140 and cut more than 1,000 jobs in the U.K. Norwegian was known for transatlantic flights for as low as $100. The carrier will focus its business on offering cheap flights for domestic routes in Norway, across Nordic countries and to key European destinations. Although a way to shore up finances, the move shows just how tough the pandemic has been for carriers.

- Airline schedules are still restrained. Future airline flights are expected to be down 47% in February, but down only 30% from March onward. U.S.-Europe and U.S.-Asia routes are both down about 60%. December international arrivals into the U.S. were down 76% in December, and non-citizen arrivals were down 83%. Air Canada, which has significant revenue between the U.S. and Canada, will operate only 20% of the flights in the first quarter of 2021 than it did in the first quarter of 2019. Air Canada announced significant layoffs this week, angering the Canadian government.

- Srivijaya Air Flight 182 crashed into the sea shortly after takeoff on January 9, killing all passengers and crew on board. Indonesia’s aviation industry has been plagued with safety issues for years. The flight between islands took place during heavy rains and was operating 27-year-old Boeing 737 aircraft. The cause of the crash is still under investigation as the black box is yet to be recovered.

Opportunities

- TSA checkpoint trends hit as high as 50% of previous years’ levels over the holidays, but more recently are at 40-45% of previous years’ levels. As countries get control over COVID-19, traffic growth has significant upside potential as schedules try to return to normal over the next one to two years.

- Boeing has added a new senior management position: the chief aerospace safety officer. The jet maker appointed long-time engineering executive Mike Delaney to the role, giving Delaney control of internal safety initiatives and a seat on Boeing’s executive council. This is a positive step forward in improving safety measures in the wake of two deadly crashes that left 737 MAX jets grounded.

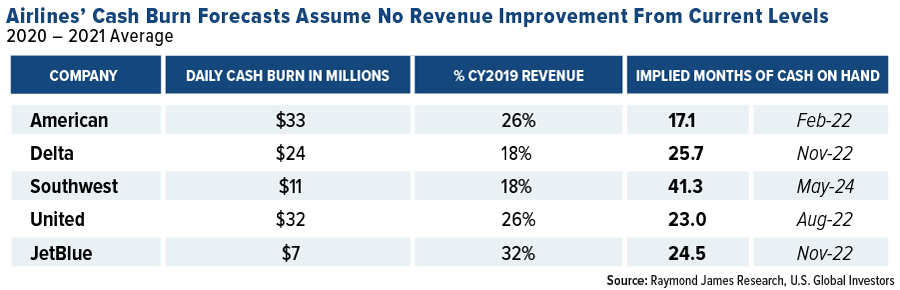

- The U.S. government is helping backstop the U.S. airline industry. Alaska Air and JetBlue have $1.8 billion remaining on their CARES Act allocation. Allegiant, Delta, Southwest and Spirit have yet to participate in the program. There appears to be plenty of liquidity available to the airline industry, if needed. Airlines have 18-24 months of cash burn, as seen in the table below. Airlines have done an excellent job of reducing monthly cash costs, by parking fleet, restructuring leases, and reducing staff. Delta has indicated that it may be profitable in the third quarter as vaccinations continue and pent-up travel demand turns into bookings. The carrier is expected to be cash flow break-even in the second quarter.

Threats

- SAS CEO, Rickard Gustafson, unexpectedly left to be the CEO at SKF AB. This leaves the company in a critical situation as it navigates through the pandemic. The company lost $1.1 billion in December alone, and does not have guidance for 2021. SAS traffic was down 80% in December.

- Technology, particularly video conferencing, remains a long-term threat for air travel. Delta feels that business travel will return to 80-90% of normal levels after the pandemic. Bill Gates predicts it will only be 50% of pre-pandemic levels. Business passengers are a major source of profits for carriers due to higher ticket prices, change fees and extra accommodations.

- High virus cases and deaths in the U.S. are placing a lid on demand. So far, 6.7 million doses of vaccines have been administered, which is far below expectations. In Europe, bookings are expected to be down from the fourth quarter of last year to the first quarter of this year due to a resurgent virus. As the U.K. lockdown continues, airlines there have cut back service significantly. Ryanair is not flying flights to and from the U.K. and Ireland, and EasyJet has said it is maintaining only essential flights.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 65 basis points. The best performing country in Asia this week was Vietnam, gaining 2.3%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 54 basis points. The Indonesia rupiah was the best performing currency in Asia this week, gaining 40 basis points.

- Imports and exports in China grew faster than expected at the end of last year and China ended 2020 with record trade surplus of $80 billion. Southeast Asian nations became China’s top trading partners, with the European Union in second place followed by the United States.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 3.3%. The worst performing country in Asia this week was South Korea losing 2.1%.

- The Polish zloty was the worst performing currency in emerging Europe this week, losing 1.6%. The South Korean won was the worst performing currency in Asia this week, losing 83 basis points.

- The U.S. Administration dropped its plan to add Alibaba, Tencent and Baidu to its Chinese blacklist which bans U.S. investors from owning company’s shares. However, nine other names were added to the blacklist, including mobile phone maker Xiaomi and China National Offshore Oil Company.

Opportunities

- MSCI China Index has broken out of its 2007-2020 consolidation pattern reinforcing a multi-year breakout. Moreover, the MSCI emerging market stocks versus MSCI developed markets stock ratio continues to work its way higher. Jeffery Gundlach, formerly the head of the $9.3 billion TCW Total Return Bond Fund, is short-term bearish on the dollar and positive on emerging markets, especially in Asia.

- Turkey has seen healthy money flows in recent months and the trend could continue with the absence of unexpected negative events. According to Wood & Company research, international net inflows to Turkish equites topped $1 billion in November, followed by $600 million in December and $300 million in the first week of January.

- Hungary plans to exempt anyone under 25 from paying income tax, as a new law may come into effect by the start of next year. The exemption may apply up to the average wage, but the government has yet to decide on the details. Critics of the government point out that this is clearly a move by Prime Minister Viktor Orban to win over the youth vote ahead of the parliamentary elections next year.

Threats

- The U.K. announced that it will fine companies if they cover up imports from the Xinjiang region of China, where international observers have accused China of overseeing forced labor by Uighur Muslims. Moreover, this week the United States banned entry of all cotton products and tomatoes from the Xinjiang region. The U.S. imported $9 billion of cotton products in the past year and $10 million of tomatoes from China.

- China is seeing a spike in new coronavirus cases and has been imposing local lockdowns in order to stop the spread of the infections. More than 20 million people have been quarantined just weeks ahead of the biggest holiday of the year. This week, the country reported its first COVID deaths in more than six months.

- Emerging market equities, as measured by MSCI Emerging Markets Index have gained 20 percent in the past three months, outperforming significantly developed markets in the year-to-date period. A short-term market correction is expected.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was HedgeTrade, rising 219.41%. The Agricultural Bank of China has enabled its customers to have access to ATMs around the city of Shenzhen to offer trial services for the digital yuan. AgBank is allowing its customers to deposit and withdraw digital yaun to or from their current savings accounts. Shenzhen is holding its second digital currency lottery which is giving away 20 million digital yuan, worth around $3 million.

- The U.S. Navy awarded a $1.5 million jet fighter contract to SIMBA Chain, a cloud-based smart contract platform, which has been tasked with revamping the U.S. military’s supply chain. The project will be responsible for generating a blockchain-based solution to create real-time demand sensing models for critical military equipment and components for the Boeing F/A-18, which will forecast supply chain logistics to accurately predict demand ahead of time. SIMBA Chain will work in tandem with the Naval Enterprise Sustainment Technology Team (NESTT) for this project.

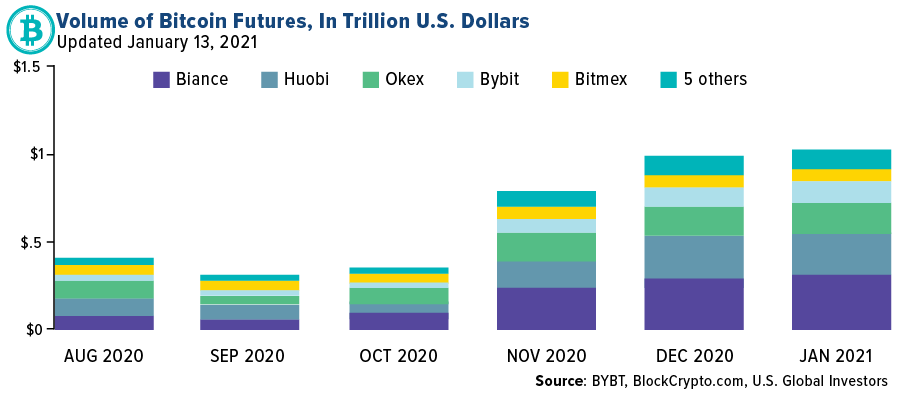

- Total value in Bitcoin futures has risen to new highs, surpassing $1 trillion for the month of January 2021. This value has increased by 210% since October 2020.

click to enlarge

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Verge, down 26.03%.

- Chainalysis, a cryptocurrency compliance startup, reported that extremist individuals received donations of more than $500,000 in Bitcoin a month before the attack on the U.S. Capitol. The report suggests that the payments were made by a French blogger, who is believed to be deceased now.

- Bitcoin’s price volatility was in full effect the past 8 days. During that time, Bitcoin has had four major trading cycles, rising in two of them and falling off in the other two. This presents a crucial talking point for its critics who believe Bitcoin’s volatility ensures that it cannot be used as a widely accepted medium for transactions.

Opportunities

- President-elect Joe Biden announced Gary Gensler as his pick for the Chairman of the SEC. Gensler has closely studied the cryptocurrency and blockchain fields and taught a course on those topics at MIT Sloan, calling the technology “a catalyst for change in the world of finance and the broader economy.” His appointment is likely to play a key role in the SEC’s consideration for a cryptocurrency ETF given the renewed efforts to launch one in the U.S. and rising institutional interest in such products.

- BitCluster, a Russian cryptocurrency mining company, is reportedly expanding its mining operations in Norlisk, Serbia, making it the first cryptocurrency mine in the Artic Circle. Given the cheap electricity rates and low average annual temperatures, BitCluster is planning on doubling its current capacity to 31 megawatts a year and mine up to six bitcoins a day on average.

- Crypto custodian Anchorage has received conditional approval by the U.S. Office of the Comptroller of the Currency (OCC) for a national trust charter, making it the first national “digital asset bank” in the country. This approval is set to pave a path for banks to act as custodians for cryptocurrencies, participate in blockchain networks and become payment providers using the technology. Another opportunity this week comes from Osprey Funds, which is launching the Osprey Bitcoin Trust in the over-the-counter markets with a management fee of 0.49%, directly competing with Grayscale Bitcoin Trust, which charges 2%.

Threats

- European Central Bank’s (ECB) President, Christine Lagarde, targeted Bitcoin on its role in facilitating criminal activity and the speculative nature that surrounds the general cryptocurrency market. Her statement comes after the German police took down the world’s largest “Darknet” marketplace, where users could partake in illegal activities and pay for the services using cryptocurrencies, including Bitcoin. She also mentioned that world leaders need to increase regulations on the use of cryptocurrencies, while the ECB itself is focused on developing their own digital currency.

- After a hack that affected Ledger’s 1 million customers in December 2020, the company’s new Chief Information Security Officer (CISO), Matt Johnson, also revealed that certain rogue actors at Ledger’s e-commerce partner Shopify exposed 20,000 customer records. The original estimate of customers affected was 9,500, significantly lower than the actual number. Matt and Ledger are working with law enforcement and Chainalysis to find the hacker(s) and have set a bounty of 10 Bitcoins for any information that might lead them to the perpetrators.

- UBS Wealth Management is warning its clients against investing in cryptocurrencies, as they believe that regulatory threats and central bank-issued competitors can potentially wipe-out the big-name digital currencies. The Chief Investment Officer for Global Emerging Markets, Michael Bolliger, said that he thinks that there is nothing stopping a cryptocurrency’s price from going to zero when a better designed version is launched. Although the firm agrees that near-term crypto prices could climb but do not have a positive outlook for the current offerings in the long run.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

Boeing

Azul SA

Allegiant Travel

Delta

Southwest

Spirit Airlines

United Airlines

American Airlines

JetBlue Airways

Alibaba

Tencent

Facebook Inc

Amazon.com Inc

Alphabet Inc

Apple Inc

Tesla Inc

Hecla Mining Co

Sibanye Stillwater Ltd

Barrick Gold Corp

Fortuna Silver Mines Inc

Gold Fields Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MSCI China Free Index is a capitalization weighted index that monitors the performance of stocks from the country of China. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. M2 is a calculation of the money supply that includes all elements of M1 as well as "near money." M1 includes cash and checking deposits, while near money refers to savings deposits, money market securities, mutual funds, and other time deposits. Operating margin measures how much profit a company makes on a dollar of sales after paying for variable costs of production, such as wages and raw materials, but before paying interest or tax. It is calculated by dividing a company’s operating income by its net sales. Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE.