Texas Freezes, but a New Commodities Supercycle Could Be Heating Up

Date Posted: February 19, 2021

Read time: 45 min

But then, roads in the north are plowed, sanded and salted when there's snowfall. With rare exception, the roads here in sunny San Antonio, Texas, do not see that kind of maintenance. There are no snow plows or salt trucks. Driving, then, can be several times more precarious when we get the kind of extreme weather that hit us this week.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

As many of you know, I grew up in Toronto, where winters can be brutally cold. Like most people who live in northern U.S. states, I’m accustomed to driving on snowy, icy roads.

But then, roads in the north are plowed, sanded and salted when there’s snowfall. With rare exception, the roads here in sunny San Antonio, Texas, do not see that kind of maintenance. There are no snow plows or salt trucks. Driving, then, can be several times more precarious when we get the kind of extreme weather that hit us this week.

Similarly, our electrical power infrastructure was designed to withstand heatwaves, not blizzards. I think a lot of Texans this week learned for the first time that a large share of the Lone Star State’s power grid operates separately from the rest of the U.S. Because of this, much of the infrastructure, including plants and pipelines, has not been winterized, which contributed to the widespread outages that left millions without power and water for days.

That fact alone, I believe, presents a good investment case for commodities and natural resources.

A joint state and federal investigation into the outages has already been announced. Improvements to (and winterization of) aging infrastructure will likely be recommended, if not required, to prevent this from happening again. Such a massive overhaul would require an incredible amount of metals and other basic materials, which would be positive for miners and producers.

We’re particularly bullish on copper, used extensively in electrical wiring and circuitry. Our favorite explorer-producer is Ivanhoe Mines, which recently announced positive mining results at its Kamoa-Kakula project in the Democratic Republic of Congo (DRC). Ivanhoe is up about 116% over the past 12 months. Our favorite speculation play is CopperBank Resources, which offers investors optionality to higher copper prices. Shares of the company are up more than 200% for the 12-month period, and today they hit a new all-time high of C$0.61.

Texas is the ninth largest economy in the world, ahead of Canada, South Korea and now Brazil. It consumes the most energy of any other U.S. state. Its residents and businesses deserve a world-class power grid that operates reliably in all weather conditions, even those that strike only once every 100 years.

No Energy Source Alone Is to Blame for the Outages

I want to briefly address something that I’ve been hearing and reading this past week. Some have used the outages as an opportunity to point fingers and criticize the reliability of different forms of energy, from fossil fuels to renewables.

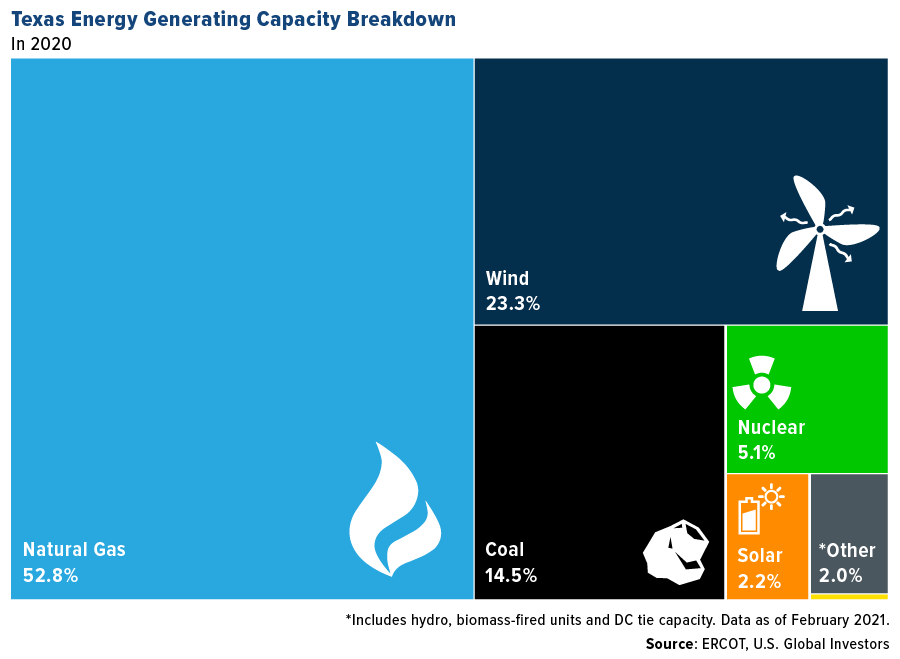

Not only is this kind of talk counterproductive, but it’s also simply not rooted in fact. No single energy source was responsible for bringing the whole system down. Texas is well diversified when it comes to electricity generation, as you can see below.

A little over half of Texas’s power comes from natural gas, which largely went down due to frozen wells and pipelines.

The state’s next biggest source, wind, also had issues, but these issues represented only around 13% of the blackouts. That’s according to Dan Woodfin, senior director for the Electric Reliability Council of Texas (ERCOT), which manages the Texas grid.

As I’ve pointed out before, Texas is the U.S. leader in wind energy, with close to 31,000 megawatts (MW) of installed capacity and 7,620 MW currently under construction.

However, another state’s wind capacity ranks higher in terms of percentage of its total energy. In 2019, wind accounted for 42% of Iowa’s net generation, the largest share of any other state.

We invest heavily in renewable energy, and we will continue to do so because that’s where the trend is headed. Among our largest holdings are Vestas Wind Systems, Canadian Solar and Plug Power. These positions have helped us crush the S&P Global Natural Resources Index over a number of time periods.

JPMorgan: A New Commodities Supercycle Has Begun

It’s not just renewables, though. We believe commodities as a whole look very attractive right now due to a number of factors.

I believe we’ll see demand from China surge in the coming months and years as the country comes out of the pandemic as the only major economy to expand in 2020. Yesterday, February 18, Chinese stocks, as measured by the CSI 300 Index, hit a new all-time high, exceeding the previous record set in October 2007.

That was near the end of the last commodities supercycle. One highly regarded quant analyst believes we may be on the verge of the next one.

In a note to clients this week, JPMorgan’s Marko Kolanovic wrote that he thinks commodities have finally turned after a 12-year down cycle. The potential drivers of a secular bull market, says Kolanovic, include the end of the pandemic and reopening of economies, fiscal stimulus, end of the U.S.-China trade war, ultraloose monetary policies and increased and “tolerated” inflation.

He also notes ESG investors, or those who put special emphasis on environmental, social and corporate governance concerns. President Joe Biden seeks to go big on an infrastructure package that’s expected to favor renewables, which is supportive of metals, electric vehicles (EVs) and batteries.

Kolanovic’s outlook is shared by many other analysts and investors, including Goldman Sach’s Jeff Currie, head of commodity research. In a recent interview with S&P Global Platts, Currie (who called the previous supercycle) said he’s bullish on oil and believes copper is likely already in a secular up cycle. “I want to be long oil and hang on for the ride,” he said in the February 5 interview.

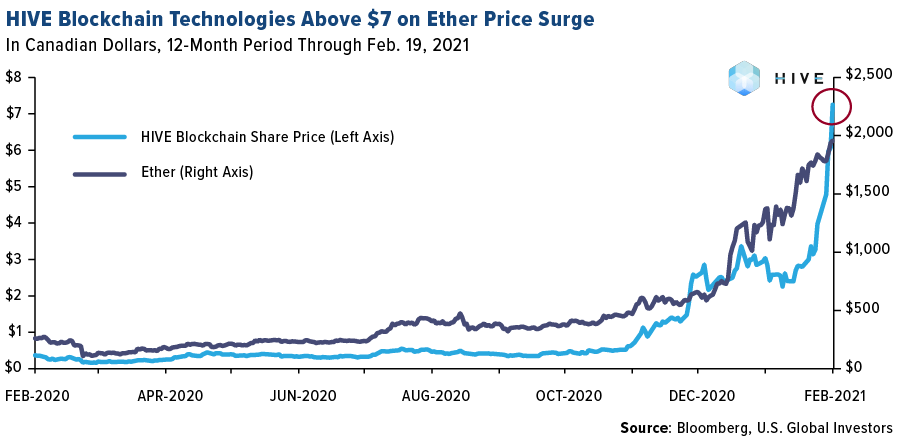

HIVE Blockchain Valued Over $2 Billion

One year ago around this time, HIVE Blockchain Technologies had a market cap of about C$120 million. This week it soared past $2 billion. Today it sits at $2.4 billion.

I want to thank all of the investors who believe in HIVE’s potential and who have come along on this incredible journey. We took the company public in 2017 to give investors like you access to the emerging industry of cryptocurrency mining. We were the first to come to market, and today we’re the only one that mines both Bitcoin and Ether using all-green energy sourced in Sweden and Iceland. Today, February 19, shares of HIVE smashed above C$7.00 for the first time ever. With a high of $7.25, the stock is up more than 1,500% over the past 12 months.

HIVE trades in Canada on the TSX Venture Exchange, over the counter in the U.S. and in Germany.

Many investors have reached out to me to ask when HIVE stock might become available on a bigger exchange, such as the Nasdaq. Such a move would naturally help it get more eyeballs.

I can’t say anything specific right now, but I will say that I hear you loud and clear. Getting listed is a process, and as soon as there’s something specific to share, I’ll let you know.

Speaking of cryptos, we have a webcast coming up on March 10 that I hope you’ll join us for. The topic will be gold and cryptocurrencies and how there’s room in your portfolio for both. Register for this free event by clicking here!

Gold Market

Strengths

- The best performing precious metal for the week was platinum, up 1.53%.

- Platinum rose above $1,300 an ounce for the first time in six years on bets that a recovery in industrial demand and stricter emissions rules will tighten supply. The precious metal is up 21% so far in 2021. After years of surpluses of platinum, COVID-19 shutdowns in South Africa saw the deficit widen to 400,000 ounces last year.

- Barrick Gold, the most profitable major gold miner, reported a sixth straight quarter of earnings outperformance after boosting production and reducing costs in the fourth quarter. Barrick met its full-year guidance and achieved a 3.8% drop in costs, with all-in-sustaining costs of $929 an ounce. Newmont, the world’s largest gold producer, also posted strong fourth quarter earnings with revenue up 14% to 3.38 billion. Bullion averaged $1,876 an ounce in the last quarter, reports Bloomberg, helping miners stay profitable.

Weaknesses

- The worst performing precious metal for the week was gold, down 2.39%. Gold fell to the lowest in more than two months on Tuesday due to a stronger dollar and better-than-expected economic data and fell to a 7-month low later in the week. Bullion has had its worst start to a year in 30 years, down already 6% year-to-date. Gold is also suffering from a rally in Treasury yields.

- BlackRock Inc.’s $17 billion iShares Silver Trust, which garnered the attention of Reddit investors, saw a near-record outflow of $712 million in the past week, after absorbing $1.5 billion the prior week in its biggest-ever inflow. The prospectus for the physically-backed-by-silver fund has been updated to warn that the fund’s authorized participants may be unable to acquire enough of the metal. As a result, the trust “may suspend or restrict the issuance” of baskets of shares, according to Bloomberg.

- Six people were killed in a fire at a gold mine in China’s eastern province of Shandong. The province will conduct safety checks of all underground non-coal mines and stop production at facilities until they are inspected reports Bloomberg.

Opportunities

- The platinum-group metals market could remain “balanced to tight” through 2026, even as battery-powered electric vehicles penetration rates grow at 13% by 2025, Morgan Stanley analysts including Christopher Nicholson say in note. Platinum, palladium and rhodium may swing to a surplus from 2027 to mid-2040s on strong demand for green energy technology. There’s also potential for fuel-cell electric vehicles to obtain “technological dominance” in heavy-duty vehicles and a portion of light commercial vehicles may push platinum demand to 4.5 million to 11.5 million ounces by 2050.

- AKH Gold, backed by one of Egypt’s richest men Naguib Sawiris, signed four contracts to explore in nine blocks of Egypt’s gold-rich eastern desert. Bloomberg reports the deals were among 10 contracts signed by the oil ministry this week. Last year the country introduced new regulations that boosted investor interest by limiting levies and removing the requirement that miners form joint ventures with the government.

- Exploration company Midas Gold Corp has been renamed Perpetua Resources Corp and debuted on the Nasdaq Thursday. The Idaho-based company aims to restore an abandoned mine in the state to produce both gold and the only mined source of antimony in the U.S.

Threats

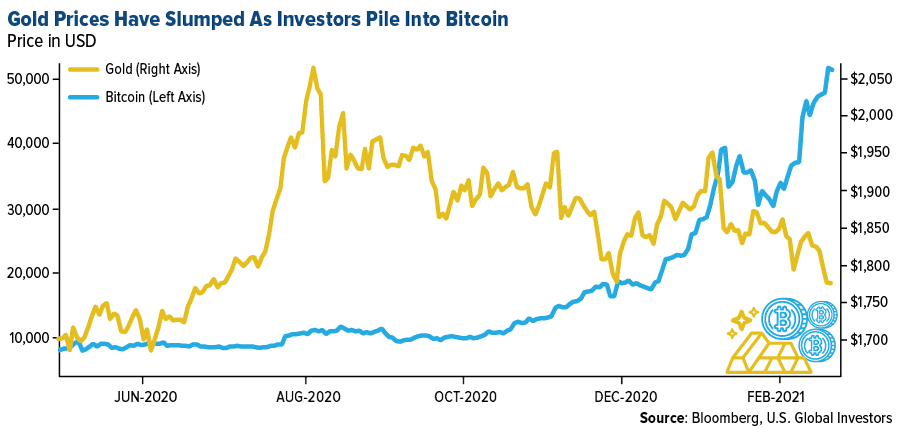

- DoubleLine Capital chief Jeffrey Gundlach has changed his mind on gold and considers Bitcoin a better trade after the crypto crossed above $52,000 this week. Gundlach tweeted he’d been a long-term gold bull and U.S. dollar bear but has turned neutral on both. Bitcoin may well be “the stimulus asset,” he said, a reference to the cryptocurrency’s rally amid pandemic-induced stimulus. As seen in the chart below, Bitcoin continues to rise while gold loses steam.

- Gold’s recent decline could post challenges for miners to keep investor interest. Despite just reporting strong earnings, Newmont is down 5.5% this year while Barrick is down 10%. Lower gold prices create pressure for miners to keep up profits and dividend payments.

- Warren Buffett’s Berkshire Hathaway has exited gold entirely, less than a year after moving into the space. According to the latest filings, Berkshire sold its Barrick Gold shares entirely in the fourth quarter after purchasing 21 million shares in the second quarter of 2020.

Index Summary

- The major market indices finished mostly down this week. The Dow Jones Industrial Average gained just 0.11%. The S&P 500 Stock Index fell 0.64%, while the Nasdaq Composite fell 1.57%. The Russell 2000 small capitalization index lost 1.15% this week.

- The Hang Seng Composite gained 1.23% this week; while Taiwan was up 3.41% and the KOSPI fell 0.42%.

- The 10-year Treasury bond yield rose 13 basis points to 1.34%.

Blockchain and Digital Currencies

Strengths

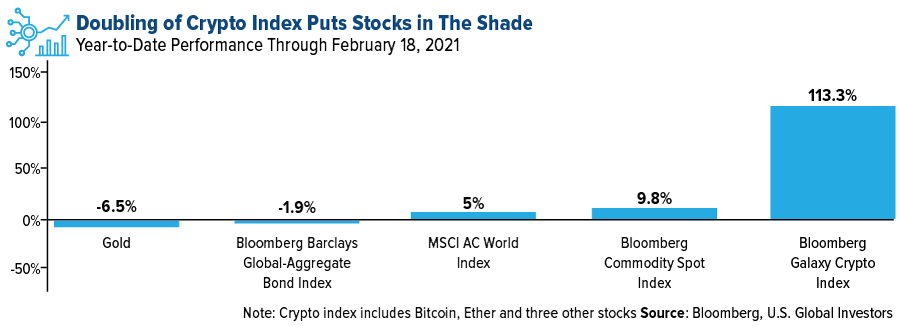

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Yield Panda, rising 865%. The Bloomberg Galaxy Crypto Index is putting other stocks and commodities in the shade, writes Bloomberg. Bitcoin’s market value reached $1 trillion for the first time, a surge that’s helping cryptocurrency returns far outstrip the performance of more traditional assets like stocks and gold, the article continues.

click to enlarge

- Tesla indicated recently that it is investing $1.5 billion into Bitcoin and says that it will also accept this as a form of payment in the future. Elon Musk defended this decision on Twitter this week: "Having some Bitcoin, which is simply a less dumb form of liquidity than cash, is adventurous enough for an S&P500 company.”

- Bitcoin has hit a $1 trillion value. The value of the digital token surged to almost $56,000 and has increased over 100 percent in 2021. Some buyers are seeing this an alternative to protect against inflation, while others see it as a vehicle for liquidity induced speculation.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was 3X Short BNB Token, down 96%.

- Riot Blockchain stock plunged 20% this week following a parabolic rally. The stock is still up over 200% for the month, however, based on several announcements about higher capacity rates.

- Hackers continue to be active with blockchain technology. There may have been an attack on the cryptocurrency that wiped 5,600 blocks on the trade list. This was due to a double-spend where two tokens are used simultaneously for separate transactions.

Opportunities

- Mark Cuban indicated that he thinks that Bitcoin may be the currency of the future and compared its development like the early days of the internet. He prefers Ethereum currently, however, and said “ETH has an advantage over BTC as a store of value,” writes Yahoo! Finance.

- Companies are being more involved in the bitcoin market. Geeley announced that it is starting a blockchain venture in China while MicroStrategy increased the size of its corporate bond offering to $900 million so it could invest in bitcoin. They want to buy $690 million more in Bitcoin, to add to the $3.5 billion holding it has currently.

- ETFs and passive investments are entering the bitcoin market one after another. Purpose Investments has introduced the first regulated crypto ETF. NYDIG has filed an application with the SEC for a Bitcoin ETF.

Threats

- The value of cryptocurrency is driven by the faith in the network, as the currency is not a company, nor does it have assets. In fact, speculation may be driving the price of Bitcoin higher. There is the risk of a plunge should investors move to the next new idea.

- Volatility is very high in the current crypto market. The options market is pricing in the downside near $40,000, which is far below the $50,000 price. There is significant downside risk.

- Hong Kong has proposed limiting trading in Bitcoin to professional investors only, which might move retail trading to the underground in unregulated peer to peer markets.

Domestic Economy and Equities

Strengths

- U.S. retail sales surged in January by the most in seven months, beating all estimates and suggesting fresh stimulus checks helped spur a rebound in household demand following a weak fourth quarter. The value of overall sales increased 5.3% from the prior month after a 1% decline in December, Commerce Department figures showed Wednesday. It was the first monthly gain since September and all major categories showed sharp advances.

- U.S. industrial production rose 0.9% in January, the Federal Reserve reported Wednesday, for the fourth straight monthly gain. The gain was above Wall Street expectations of a 0.5% gain, according to a survey by the Wall Street Journal. Economists remain optimistic about the prospects for manufacturing production in coming months. Total production has not returned to pre-pandemic levels though, held down by weakness in the energy and aircraft sectors. But with crude oil prices rising to near $60 a barrel, active rig activity should boost production in the second quarter.

- Freeport-McMoran Inc was the best performing S&P 500 stock for the week, increasing 20.97%. The stock rallied after the price of copper extended its surge to a nine-year high amid warnings of a historical shortage.

Weaknesses

- Applications for U.S. state unemployment insurance jumped to a four-week high, indicating the labor market is suffering fresh setbacks even as the coronavirus pandemic shows signs of ebbing. Initial jobless claims in regular state programs totaled 861,000 in the week ended February 13, up 13,000 from the prior week, Labor Department data showed Thursday. Last week’s report had originally shown a decrease but was revised up to show a 36,000 increase.

- U.S. home construction starts fell in January for the first time in five months, signaling that rising residential real estate prices may be constraining buyer demand. Residential starts dropped by 6% from the prior month to a 1.58 million annualized rate, according to government data released Thursday. The median in a Bloomberg survey of economists had called for a decline to a 1.66 million annualized rate. The figures suggest that record-high prices may be weighing on affordability and subduing further growth in the housing market. Still, housing starts remain above pre-pandemic levels thanks to the Federal Reserve’s ultra-easy monetary policy pushing mortgage rates to record lows and driving demand upward. Single-family housing starts, which were at the highest since 2006 by the end of last year, decreased by 12.2% to a 1.16 million pace.

- Davita was the worst performing S&P 500 stock for the week, decreasing 9.94%. Shares have been pressured after analysts’ views that the uncertainly of the true effect of continued treatment losses due to the pandemic-caused mortality among DaVita’s patients makes forecasting revenue growth difficult.

Opportunities

- The U.S. vaccine supply is poised to double, according to Bloomberg reports. Currently, the U.S. is administering 1.6 million doses a day, constrained by the recent supply of about 10 million to 15 million doses a week. But Covid-19 vaccine manufacturers and U.S. officials have accelerated their production timelines and signaled that the spigots are about to open, providing hundreds of millions of doses to match the growing capacity to immunize people at pharmacies and mass-vaccination sites. A review of drugmakers’ public statements and their supply deals suggests that the number of vaccines delivered should rise to almost 20 million a week in March, more than 25 million a week in April and May, and over 30 million a week June. By summer, it would be enough to give 4.5 million shots a day.

- Berkshire Hathaway revealed billion-dollar stakes in Chevron and Verizon. It disclosed a $4.1 billion stake in the energy titan and a $8.6 billion position in the telecoms giant.

- YouTube’s TikTok rival is headed to the U.S. YouTube says a test version of Shorts will launch in the U.S. in March after an extensive test in India, but hasn’t said when a full rollout might follow. YouTube is a subsidiary of Alphabet.

Threats

- Credit Suisse’s annual net profit dropped 22%. The Swiss lender’s earnings cap a tumultuous year for the bank, which began with the ousting of Tidjane Thiam as CEO.

- eHealth shares fell 4.8% after reporting a sharp decline in revenue and profitability in the fourth quarter, driven by weak Medicare enrollments and a difficult year-over-year comparison, drawing analysts from Deutsche Bank to downgrade shares.

- JPMorgan analyst Sean Meakim downgraded NOW Inc. to Underweight from Neutral with a $5 price target. The analyst believes the rally in the energy distribution space is "looking tired."

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was sugar, up 7.99%. Tin was the second best for the week up 7.17%. Tin had a 16th straight weekly gain amid a major supply squeeze of the base metal. Tin is up a massive 25% so far this year, reaching as high as $25,455 a ton.

- Copper hit a new nine-year high in London trading, powering past $8,000 a ton, and is up over 24% so far this year. The metal was up more than 2% on Friday alone. Bloomberg notes markets are bullish over prospects for growing demand and the economic recovery from the coronavirus. Copper is often viewed as a bellwether for the wider economy.

- Iron ore futures in China surged to the highest in almost two months as markets re-opened after Lunar New Year and miners pointed to strong demand in the world’s top consumer, reports Bloomberg. Fortescue Metals Group Ltd., the world’s fourth largest iron exporter, reported a surge in first half profit and expects the market to stay very robust for some time.

Weaknesses

- The worst performing commodity for the week was oil, down 0.87%. Oil fell the most in a month with the ongoing energy crisis in the U.S. keep refineries closed for another week, reports Bloomberg. Crude fell 1% in Thursday trading. The 14-day Relative Strength Indexes (RSI) for both the U.S. and global crude benchmarks remain above 70, which is a sign the commodity is overbought and due for a pullback.

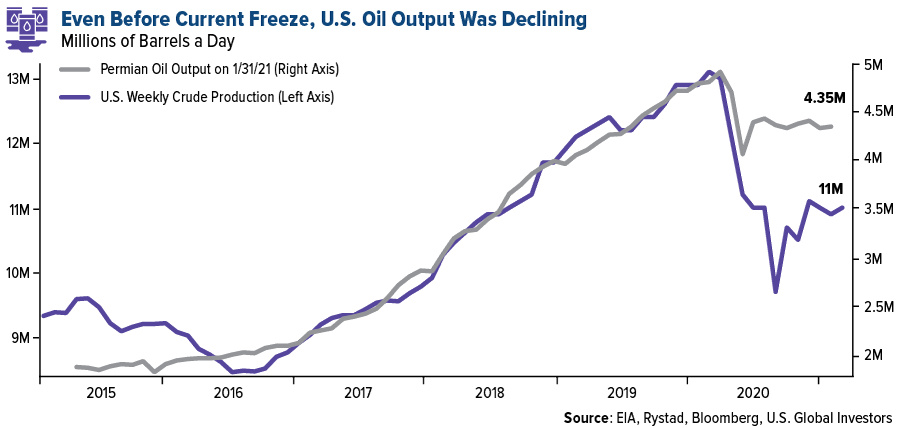

- Total U.S. oil production has plunged by close to 40% — the most ever — as an unprecedented cold blast freezes well operations across the central U.S. Oil output from just the Texas portion of the Permian patch was estimated at only 600,000-700,000 barrels a day on Tuesday, down from its typical volume of 3.5 million barrels a day, said Bert Gilbert, head of North American Business Development at OilX. Even before the freeze hit Texas, and much of the U.S., oil output was already declining, as seen in the chart below.

- As millions of Texans remain without power, Governor Greg Abbott has banned natural gas from leaving the state through Sunday, sending shockwaves through the market. Texas is the top gas producing state, with 23 billion cubic feet a day before the winter freeze nearly halted production. Some are calling the export ban unconstitutional and many traders were caught off guard losing millions in minutes.

Opportunities

- Ford Motor Co. will drastically overhaul its business in Europe, where it did not sell a single fully electric vehicle in 2020, pledging to go nearly entirely electric by the end of the decade, reports Bloomberg. The carmaker announced on Wednesday it will invest $1 billion into a German assembly plant that will make all-electric models in two years. By mid-2026, Ford will offer hybrid or fully electric car models across its entire product line. Ford Europe President Stuart Rowley said in an interview, “Our customers are very focused on sustainability and they want the brands and companies they work with to go on this journey with them.”

- The alternative meat movement is heading beyond burgers and into steak. Israel’s Redefine Meat Ld. Is targeting steakhouses with its 3D-printed beef cuts and has already raised $29 million in funding. This is yet another sign of the pickup in the anti-meat movement that has spurred major food companies to explore their own non-meat alternatives.

- The platinum-group metals market could remain “balanced to tight” through 2026, even as battery-powered electric vehicles penetration rates grow at 13% by 2025, Morgan Stanley analysts including Christopher Nicholson say in note. Platinum, palladium and rhodium may swing to a surplus from 2027 to mid-2040s on strong demand for green energy technology. There’s also potential for fuel-cell electric vehicles to obtain “technological dominance” in heavy-duty vehicles and a portion of light commercial vehicles may push platinum demand to 4.5 million to 11.5 million ounces by 2050.

Threats

- China is exploring whether it can hurt U.S. defense contractors by limiting supplies of rare-earth minerals that are critical to the industry, the Financial Times reported. Industry executives said government officials had asked them how badly companies in the U.S. and Europe would be affected if China restricted rare-earth exports during a bilateral dispute. China remains the dominant supplier of these minerals used widely in electronic devices.

- Federal regulators warned Texas a decade ago that its power plants were unreliable in bitter cold conditions and recommended utilities use more insulation, heat pipes and to take steps to winterize plants. Texas’ power grid operates entirely separate from all other states and is free of federal regulation. At least 10 people have died and up to 4 million residents were out of power for multiple days as a winter storm pummeled the entire state. An investigation into the failures could question why no steps were taken after the finding of the 2011 analysis by the Federal Energy Regulatory Commission.

- The cost of shipping dry bulk goods has hit the highest level in a decade and is threatening the profits of grain traders. Crude oil has rebounded to the strongest levels in a year. Meanwhile, freezing temperatures and quarantine restrictions have led to longer delays and vessels shortages.

Airline Sector

Strengths

- The best performing airline stock for the week was TUI AG, up 13.1%, due to an earnings surprise. Passenger traffic is continuing to improve, with traffic up 26% versus last week but still down 59% versus a year ago. Traffic is expected to slowly improve as more and more individuals are vaccinated and feel safe flying again.

- United Airlines won a lawsuit to dismiss some of its class action lawsuits related to flight cancellations. Plaintiffs are demanding refunds, but the carrier, to save cash, is calling this a force majeure event. The airline can offer vouchers instead. Perhaps we may see more developments related to this with respect to other carriers in the coming months.

- Southwest continues to manage its cash burn, which stands at $15 million per day, down from $17million per day in recent months. The carrier lowered its costs 15-20% year-over-year, with capacity down 35%. The company has been among the best U.S. airlines in managing its operations through the pandemic.

Weaknesses

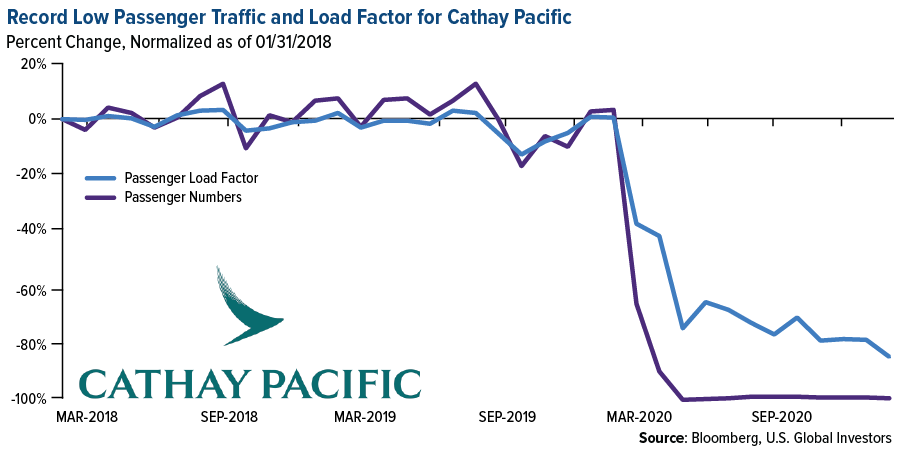

- The worst performing airline stock for the week was Qantas Air, down 1.5% due to poor earnings. Turkish Air reported a drop in traffic by 65% in January, with a corresponding 57% drop in capacity. Load factors fell to 60.3%. Allegiant Air also announced that its traffic fell 47% in January, while Thai Air said its traffic fell 40%. Cathay Pacific’s load factor was only 13% in January. Lufthansa indicated that it flew only 9% of normal passenger volume.

- Air Canada reported fourth quarter revenues down 81% with a reported operating loss of C$1.0 billion. Capacity was down 85% and the workforce has been reduced 50%. The carrier is expecting some form of government aid soon.

- EasyJet said that 2021 revenues would be at least 50-70% below the prior year, and the carrier would fly only 10% of its capacity in the second quarter. Revenues fell 88% in the first quarter. A slow recovery is expected in the second half of the year.

Opportunities

- Air Arabia feels that higher oil prices are good for the airline since this will help the economies it serves in the Middle East. Abu Dhabi is the carrier’s base. The carrier is locked in at $50-55 Brent for the next two years, which should be keep fuel prices stable.

- Austrian Airlines outlined its summer flight schedule, announcing it will add 150 flights per week to 20 cities during the summer. This is a big increase, as the carrier had reduced its active fleet to 60 aircraft during the pandemic.

- Lufthansa is in talks with Boeing and Airbus on shifting its fleet to smaller jets. Traffic is expected to recover to 50% of 2019 levels. The cabins will have more leisure class seats and less business class seats. The carrier is also seeking to exchange some orders of 777s and A330/350s for 787s and Airbus 321 Neos. This is a switch from dual aisle to single aisle aircraft.

Threats

- Singapore Airlines wage subsidy will decrease as Singapore tapers its jobs support scheme to zero by September. The company is already burdened with having 73% of its fuel needs locked in via hedges at $58-62 per barrel, which is slightly above market prices and above other levels that airlines have hedged at. These issues are keeping the airline’s monthly cash burn high. The carrier’s load factor was 11.5% in January, compared to 84.5% in the past year.

- Air Transat’s proposed takeover by Air Canada was not approved by the European authorities by the February 15 deadline. Air Canada is not agreeing to an extension of the deadline, meaning that the carrier has a legal right to walk away from the deal. The deal was initially struck In June 2019 and was renegotiated downward after the pandemic started.

- The courts have ruled that EU rules were not broken when some EU airlines received bailouts. This is a negative for Ryanair, who sees these bailouts and state assistance as an unfair competitive advantage. Ryanair has said it will appeal the ruling. Air France has said following disappointing results that it expects a bailout from the French Government in the coming weeks.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Poland, gaining 2.2%. The best performing country in Asia this week was Vietnam, gaining 5.3%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 11%. The Taiwanese dollar was the best performing currency in Asia this week, gaining 20 basis points.

- FactSet reported this week that China’s domestic ETF market rose almost 60% in value in 2020. A report from the Shenzhen stock exchange that calculates the domestic ETF market saw the value of its funds rose 57.69% in 2020 to CNY1.1 trillion ($170.9 billion). 366 ETFs were listed and most of the new ETFs mainly focused on chip, new energy, artificial energy and 5G. Individual investors accounted for 30.7% of investors, with institutional investors holding the remainder.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 1.4%. The worst performing country in Asia this week was India losing 1.3%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 42 basis points. The Indonesian rupiah was the worst performing currency in Asia, losing 90 basis points.

- The Eurozone preliminary Service PMI for February was released at 44.7, below the expected reading of 45.9 and January’s reading of 45.4. The service sector continues to lag in the euro area, but manufacturing is improving despite the lockdown measures. The January preliminary Manufacturing PMI jumped to 57.7 above expected 54.3, and the prior reading of 54.8.

Opportunities

- Brent crude oil continues to move higher. Stronger oil will benefit Russia as most of the country’s revenue comes from the production and sale of oil and gas. OPEC production cuts and cold weather in the United States, which shot down refiners in Texas and left many parts of the state without power, may further push oil higher. More than 4 million barrels a day in output, almost 40% of United States crude production has been interrupted according to traders and executives.

- China’s holiday spending during the Lunar New Year celebration surged. Combined sales of retail and catering services rose 28.7% year-over-year. Transportation services and companies relying on travel will suffer due to the restrictive measures, however the e-commerce businesses benefited from less travel and increased spending.

- China tested usage of cryptocurrency during the Lunar New Year. As many as 50,000 residents of Beijing received CNY200 ($31) each in digital red envelopes as a test for something much larger. However, it warned that an earlier test in Cambodia had shown a slow pick up. China plans more tests in coming years including during Beijing winter Olympics next year, FactSet reported.

Threats

- The Eurozone Court of Human Rights asked Russia to release Alexei Novalny from prison; failure to release him could breach the Eurozone’s Convention of Human Rights. Further action from the EU most likely will follow. Sanctions of individuals may follow but most likely they will not apply to financial markets.

- Reuters reported remarks from President Biden who said China will pay a price for its human rights abuses. The President was responding to questions about China’s handling of Muslim minorities in Xinjiang and he added that President Xi of China knows there will be repercussions. He said that China wants to become a world leader, but it will be hard to do that so long as it is engaged in activity that is contrary to basic human rights.

- BBH Currency Research Team believes that U.S. dollar will continue to recover on the back of rising U.S. yields and improving economic data. A stronger dollar will negatively affect emerging markets.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.34 | +0.13 | +10.73% |

| Oil Futures | 58.97 | -0.50 | -0.84% |

| Hang Seng Composite Index | 4,950.02 | +60.23 | +1.23% |

| S&P Basic Materials | 471.21 | +4.15 | +0.89% |

| Korean KOSPI Index | 3,107.62 | -13.01 | -0.42% |

| S&P Energy | 345.23 | +10.24 | +3.06% |

| Nasdaq | 13,874.46 | -221.01 | -1.57% |

| DJIA | 31,494.32 | +35.92 | +0.11% |

| Russell 2000 | 2,263.05 | -26.31 | -1.15% |

| S&P 500 | 3,909.72 | -25.11 | -0.64% |

| Gold Futures | 1,781.40 | -41.80 | -2.29% |

| XAU | 136.78 | -4.94 | -3.49% |

| S&P/TSX VENTURE COMP IDX | 1,094.37 | +26.93 | +2.52% |

| S&P/TSX Global Gold Index | 281.16 | -22.74 | -7.48% |

| Natural Gas Futures | 3.07 | +0.16 | +5.49% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,107.62 | -6.93 | -0.22% |

| 10-Yr Treasury Bond | 1.34 | +0.26 | +24.05% |

| Gold Futures | 1,781.40 | -88.80 | -4.75% |

| S&P Basic Materials | 471.21 | -6.40 | -1.34% |

| S&P 500 | 3,909.72 | +57.87 | +1.50% |

| DJIA | 31,494.32 | +305.94 | +0.98% |

| Nasdaq | 13,874.46 | +417.21 | +3.10% |

| Oil Futures | 58.97 | +5.73 | +10.76% |

| Hang Seng Composite Index | 4,950.02 | +162.02 | +3.38% |

| S&P/TSX Global Gold Index | 281.16 | -34.25 | -10.86% |

| XAU | 136.78 | -6.46 | -4.51% |

| Russell 2000 | 2,263.05 | +102.43 | +4.74% |

| S&P Energy | 345.23 | +14.76 | +4.47% |

| S&P/TSX VENTURE COMP IDX | 1,094.37 | +148.22 | +15.67% |

| Natural Gas Futures | 3.07 | +0.53 | +20.99% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 136.78 | +0.89 | +0.65% |

| S&P/TSX Global Gold Index | 281.16 | -39.66 | -12.36% |

| Gold Futures | 1,781.40 | -89.70 | -4.79% |

| DJIA | 31,494.32 | +2,011.09 | +6.82% |

| S&P 500 | 3,909.72 | +327.85 | +9.15% |

| Nasdaq | 13,874.46 | +1,969.75 | +16.55% |

| Korean KOSPI Index | 3,107.62 | +560.20 | +21.99% |

| Natural Gas Futures | 3.07 | +0.48 | +18.52% |

| S&P Basic Materials | 471.21 | +32.79 | +7.48% |

| Russell 2000 | 2,263.05 | +478.91 | +26.84% |

| Oil Futures | 58.97 | +17.23 | +41.28% |

| Hang Seng Composite Index | 4,950.02 | +803.29 | +19.37% |

| S&P/TSX VENTURE COMP IDX | 1,094.37 | +364.93 | +50.03% |

| S&P Energy | 345.23 | +76.58 | +28.51% |

| 10-Yr Treasury Bond | 1.34 | +0.51 | +61.57% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

United Airlines

Air Canada

Singapore Airlines Ltd.

Ivanhoe Mines Ltd.

Vestas Wind Systems A/S

Canadian Solar Inc.

Plug Power Inc.

CopperBank Resources Corp.

Barrick Gold Corp

Newmont Corp

Tesla Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

CSI 300 Index consists of the 300 largest and most liquid A-share stocks. The Index aims to reflect the overall performance of China A-share market. The S&P Global Natural Resources Index is comprised of 90 of the largest U.S. and foreign publicly traded companies, based on market capitalization, in natural resources and commodities businesses that meet certain investability requirements. The S&P Goldman Sachs Commodity Index GSCI serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. The MSCI All Country World Index (ACWI) is a market-cap-weighted global equity index that tracks emerging and developed markets. It currently monitors nearly 3,000 large- and mid-cap stocks in 49 countries. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. The Bloomberg Galaxy Crypto Index (BGCI) is a capped market capitalization-weighted index designed to measure the performance of the largest digital assets traded in USD. Eligible index constituents are diversified across different categories, including stores of value, mediums of exchange, smart contract protocols and privacy assets.