The Hunger for Muni Bonds (And Gold!) Is Real

Date Posted: April 18, 2019

Read time: 54 min

Another Tax Day has come and gone. Although it might be some time before we get the full picture of what Americans earned and paid in taxes last year, it's probably safe to assume that the top 1 percent of earners shouldered most of the U.S. tax burden.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Another Tax Day has come and gone. Although it might be some time before we get the full picture of what Americans earned and paid in taxes last year, it’s probably safe to assume that the top 1 percent of earners shouldered most of the U.S. tax burden.

In 2016, the most recent year of available data, the top 1 percent was responsible for over 37 percent of all income taxes. Compare that to the bottom 50 percent, which was responsible for about 3 percent of all taxes.

Of course, the highest earners also paid the highest average income tax rate of 26.9 percent, which is seven times more than the rate faced by the bottom 50 percent.

This was the first year that Americans paid taxes under President Donald Trump’s tax cuts. And yet many filers—especially those living in high income tax states such as New York, California and New Jersey—saw their payments rise significantly due to state and local tax (SALT) deductions being capped at $10,000.

This change has been a boon for municipal bonds, which are exempt from taxes not only at the federal level but also, in most cases, state and local levels.

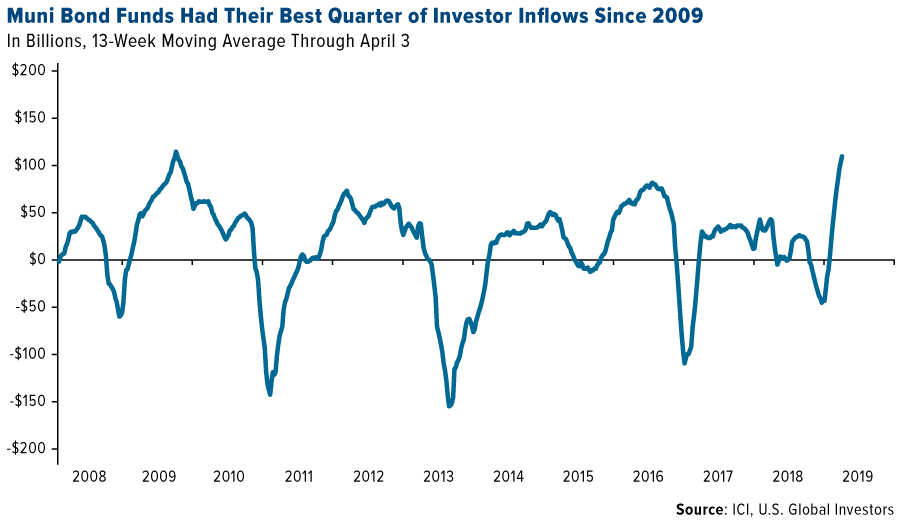

Muni bond funds, in fact, just had their best quarter of inflows since 2009, as you can see below.

According to Morningstar data, tax-free muni bonds saw more than $8.8 billion in net flows in the three months ended March 31, beating U.S. equity funds ($6.2 billion) and international equity funds ($1.3 billion). This tells me that investors were seeking stability as well as a strategy to counteract the changes to the tax code.

Investors Prefer Actively Managed Muni Bond Funds

Actively managed muni funds were more popular than passively managed funds, including ETFs. Active funds attracted $7.5 billion, more than five and a half times more than passive muni funds, which saw only $1.3 billion in net flows, according to Morningstar.

As I told you in a previous post, I think the reason investors prefer active muni funds is that they want a manager who knows how to conduct deep credit research, adjust for duration and monitor for risks and opportunities. You don’t get that with a passive fund.

Muni Supply Has Tightened

Trump’s tax law supports the outlook for muni demand in more ways than one. The supply of municipal debt has been restricted thanks to the elimination of a category known as “advanced refunding issues,” which in years past accounted for about a fifth of muni bond issuances annually.

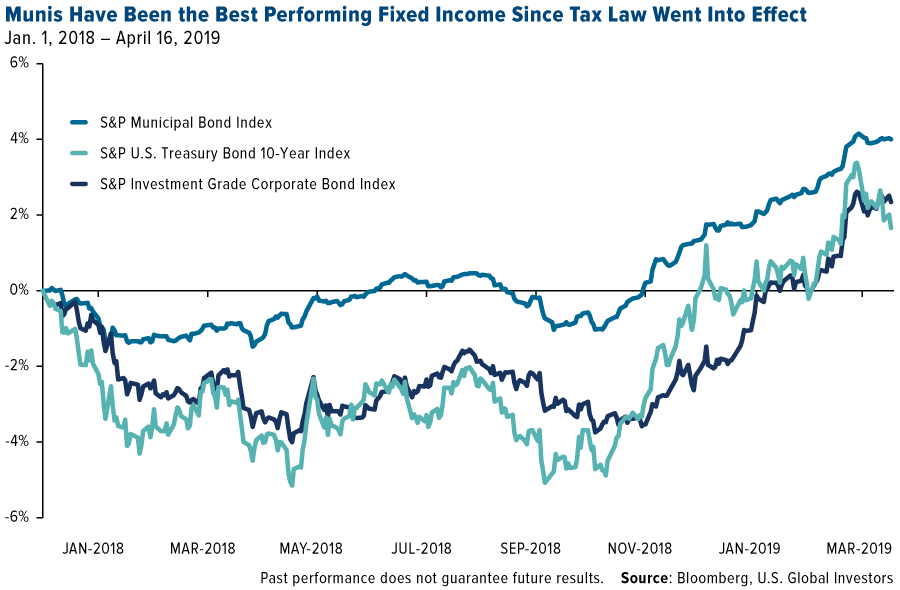

Any casual student of economics knows that tighter supply, combined with increased demand, creates investment opportunities. And since the tax law went into effect in January 2018, muni bonds have outperformed both 10-year Treasuries and investment-grade corporate debt.

On a final note, I should point out that munis have a history of doing well in late-cycle environments, which we seem to be in right now. This, along with flat issuance and stronger demand for tax-free income, should help the asset class remain resilient throughout the year and beyond.

Gold “Lives Up to the Hype”

Another asset whose supply is forecast to tighten in the coming years is gold, due mainly to shrinking exploration budgets and the lack of large discoveries. As I told Streetwise Reports this week, the gold mining industry hasn’t seen any technological breakthroughs as there have been in oil and gas with fracking.

Also like munis, demand for the yellow metal remains strong and should continue to strengthen as incomes grow in emerging markets such as China, India and Turkey.

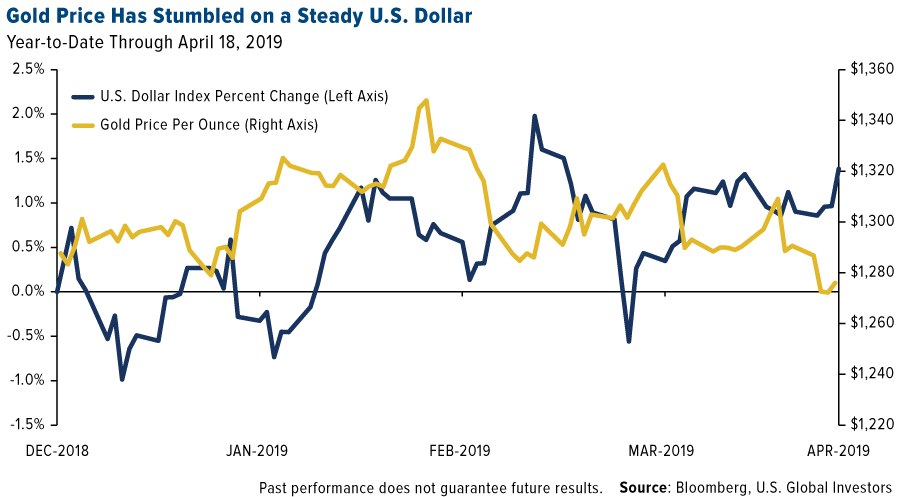

This week, the price of gold fell to a 2019 low of around $1,270 an ounce as the 10-year Treasury yield ticked up and U.S. dollar stayed at elevated levels.

Nevertheless, some analysts continue to see this as an “extremely attractive environment,” in the words of British banking firm Standard Chartered.

“We are very constructive on gold, both within our strategy teams and within our commodity research teams,” Standard Chartered’s Eric Robertson told Bloomberg. “Even with the recovery that we’ve seen in equity prices and nominal bond yields over the last few weeks, real or inflation-adjusted yields remain extremely low. And that’s a better indicator for gold.”

In a report this week titled “Gold lives up to the hype as a safe haven,” research firm Capital Economics said it sees gold rallying to $1,400 an ounce or more by mid-2019 on equity weakness.

“Given that we expect the S&P 500 to drop by roughly a fifth this year, we think gold’s safe-haven credentials will soon come to the fore again,” says commodities economist Ross Strachan, who goes on to explain that in seven out of eight times since 1990 in which the S&P declined more than 10 percent over a prolonged period, the price of gold rose 7.2 percent on average.

Venezuela’s $400 Million Sale Weighed on Gold

Gold traded down following the news on Monday that Venezuela sold as much as $400 million of the metal, the South American country’s only remaining liquid asset. This comes after Venezuela opposition leader Juan Guaido in February urged the U.K. not to send cash to President Nicolas Madura upon sale of the country’s gold reserves, held in the Bank of England’s (BoE) vaults.

The recent sale could mean that President Maduro has found a way to sidestep sanctions, according to Bloomberg.

The report also points out that Venezuela’s central bank “has been operating with what it calls an emergency team of only about 100 workers of about 2,000 since a power outage left its headquarters without running water.” What Maduro has done to this once prosperous country and its people is nothing short of tragic.

In any case, the gold market should stabilize once Venezuela is done selling this quarter.

Frank Talk at 12

I’m delighted to share with you that my CEO blog, Frank Talk, turned 12 this month. Its mission is the same today as it was then—to educate curious investors about not just the whats but the whys in today’s marketplace, and to relay interesting insights I pick up along my global travels.

Something else that hasn’t changed is the joy it brings me to be able to communicate directly with you. To those who’ve taken this journey with me over the years, in whole or in parts, I say thank you! To those who only recently discovered Frank Talk, I say welcome!

No matter which category you fall into, I hope that you stick around because there’s so much more to come.

On behalf of everyone at U.S. Global Investors, I wish you all a blessed Easter and/or Passover this weekend!

Gold Market

This week spot gold closed at $1,275.82, down $14.53 per ounce, or 1.13 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.09 percent. The S&P/TSX Venture Index came in off 2.63 percent. The U.S. Trade-Weighted Dollar rose 0.50 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-16 | Germany ZEW Survey Current Situation | 8.5% | 5.5% | 11.1% |

| Apr-16 | Germany ZEW Expectations | 0.5% | 3.1% | -3.6% |

| Apr-16 | China Retail Sales YoY | 8.4% | 8.7% | — |

| Apr-17 | Eurozone CPI Core YoY | 0.8% | 0.8% | 0.8% |

| Apr-18 | Initial Jobless Claims | 205k | 192k | 197k |

| Apr-19 | Housing Starts | 1230k | — | 1162k |

| Apr-23 | New Home Sales | 650k | — | 667k |

| Apr-25 | Durable Goods Orders | 0.9% | — | -1.6% |

| Apr-25 | Initial Jobless Claims | — | — | 192k |

Strengths

- The best performing metal this week was palladium, up 3.52 percent as CPM Group noted that the price could climb to $1,800 on supply constraints. Gold traders and analysts switched from bullish to mostly neutral or bearish on the yellow metal this week, according to the weekly Bloomberg survey.

- Turkey’s gold reserves reversed this week by rising $227 million from the previous week. The central bank’s holdings are now worth $20.9 billion as of April 12, according to official figures. Kazakhstan also increased its gold holdings to 11.63 million ounces in March, up from 11.46 million in February. Mexico, too, raised gold reserves by 3.86 million ounces last month.

- Bloomberg’s Cormac Mullen writes that currency traders should get ready for a big move in the dollar, if past periods of low volatility are a guide. Over the last 25 years, there have been three previous troughs in the JPMorgan Global FX Volatility Index, and each time the U.S. Dollar Index has moved around 10 percent over the subsequent six months, according to Bloomberg data. A weaker U.S. dollar has historically been positive for the gold price as the two trade inversely.

Weaknesses

- The worst performing metal this week was gold, down 1.13 percent. The yellow metal tumbled to its lowest since January on Tuesday morning just as the market opened after someone dumped 11,000 gold futures contracts, worth around $1.5 billion, into the market. Traders were said to be using the F-word—“fiduciary.” Who recklessly dumps so many contracts unless their motive is to drive the price down?

- Gold is headed for its fourth weekly drop – the longest run of weekly declines in eight months – amid speculation that the U.S. and China are nearing a trade deal. Bloomberg writes that better-than-expected first quarter growth and March industrial production for China weighed on gold prices. The data eased concerns about a slowdown in global growth that rattled investors.

- Holdings in the SPDR Gold Shares fund fell to its lowest since October on Tuesday, which also happens to be the same day that gold gave up all its 2019 gains. Unexpectedly strong data from emerging markets, and China in particular, helps explain gold’s slip as investors are turning away from safe haven assets. Japan’s largest bullion retailer, Tanaka Kikinzoku Kogyo K.K., said that first quarter sales of gold bars fell 33 percent year-over-year and platinum bars also fell 34 percent.

Opportunities

- Federal Reserve Chairman Jerome Powell has made an important shift in strategy for dealing with inflation, in a prelude to what could be a more radical change next year, writes Bloomberg’s Rich Miller and Craig Torres. “The Fed is evolving to a ‘white-of-the-eyes’ approach in terms of inflation” under which it won’t hike rates until price rises accelerate, said Stephen Stanley, chief economist at Amherst Pierpont Securities. Higher inflation is typically good for gold.

- Rio Tinto, the world’s second biggest miner, released a statement last week saying that it will only work with groups aligned with its own climate principals and pledged to become a “greener” miner. Mining.com writes that “Rio Tinto has effectively put mining industry lobby groups on notice that they need to adapt to a world in which the challenge of climate change is recognized and that mining should be a positive force for change.”

- According to a joint statement, ICBC and the World Gold Council are partnering to develop the Chinese gold market. The two groups will leverage online technology and ICBC’s platform advantages to design and develop new gold products and services for millennials in particular.

Threats

- Venezuela managed to sell as much as $400 million, or nearly 9 tons, in gold with sanctions in force, somehow skirting international sanctions. The sale not only means President Maduro has found a way to sidestep the economic blockage, but it also may have contributed to the drop in gold price this week, according to some analysts. “Of course [the sale] impacts the gold price,” RBC Wealth Management managing director George Gero told Kitco News. “Anytime you have a large supply overhanging the market, it impacts trading. It did not help attract buyers.”

- Gold demand has been supported lately by the idea that global output could begin to roll over on higher operating costs and the lack of large discoveries. However, it doesn’t look as if “peak gold” has arrived just yet. Output is expected to rise to 109.6 million ounces this year, an increase of 2.1 percent more than in 2018, according to S&P Global Market Intelligence. This will be “the strongest growth in the past three years, debunking commentary calling for peak gold,” analyst Christopher Galbraith told Bloomberg. Galbraith added that more than half of the increase “is projected to come from new mines that are expected to come on stream this year or have recently commissioned.”

- For the past two decades, U.S. corporate profits have widened on average, but this is unlikely to last much longer. According to a note by Bridgewater Associates’ Greg Jensen, “some of the forces that supported margins over the last 20 years are unlikely to provide a continued boost.” This could lead to a major valuation problem, Jensen says, adding that incentives for offshore production have been reduced “as global labor costs have moved closed to equilibrium, with domestic costs and rising trade conflict increasing the risk of offshoring, while the potential tax rate arbitrage from moving abroad is now much smaller.” As a result, it could be challenging for companies to maintain profitability levels over the next several years, let alone widen margins further.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 1.59 percent. The S&P 500 Stock Index rose 0.58 percent, while the Nasdaq Composite climbed 0.64 percent. The Russell 2000 small capitalization index lost 0.85 percent this week.

- The Hang Seng Composite rose 0.55 percent this week; while Taiwan was up 1.42 percent and the KOSPI fell 0.48 percent.

- The 10-year Treasury bond yield rose 6 basis points to 2.56 percent.

Domestic Equity Market

Strengths

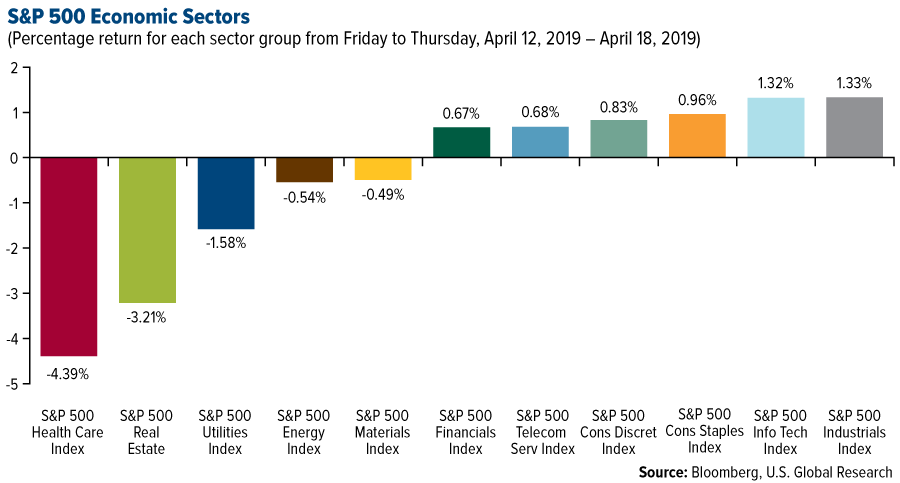

- Industrials was the best performing sector of the week, increasing by 1.33 percent versus an overall decrease of 0.10 percent for the S&P 500.

- Qualcomm was the best performing stock for the week, increasing 40.28 percent.

- Qualcomm’s stock spiked 23 percent on Tuesday after the company reached an agreement with Apple to dismiss all litigation related to their royalty dispute. The companies also agreed to a six-year licensing deal and a chipset supply agreement.

Weaknesses

- Health care was the worst performing sector for the week, decreasing by 4.39 percent versus an overall decrease of 0.10 percent for the S&P 500.

- Regeneron Pharmaceuticals was the worst performing stock for the week, falling 12.95 percent.

- JB Hunt missed on earnings. The trucking giant missed on both the top and bottom lines, pinning the disappointing results on bad weather and higher driver salaries.

Opportunities

- Apple is spending hundreds of millions of dollar on securing games for its upcoming game-streaming service called Arcade, the Financial Times reports. The tech giant unveiled its gaming plans last month along with new its TV-streaming and news services.

- The IPO market is ramping back up after seeing its quietest quarter in three years. Healthcare listings are dominating the slate of new companies coming to market this year, according to Renaissance Capital. This week’s big IPOs were social media giant Pinterest and video communication company Zoom. Both started trading on the New York Stock Exchange under the tickers PINS and ZOOM.

- The head of research at the world’s largest hedge fund says China opening up is a once-in-a-lifetime opportunity for investors. "The thing that makes this opportunity so compelling is that, for many investors, this a market that essentially didn’t exist," according to Karen Karniol-Tambour, the head of investment research at Bridgewater Associates. "If you believe in diversification, you’re not going to get a lot of opportunities where such a large market opens up."

Threats

- Facebook’s activist shareholders are making another dramatic bid to oust Mark Zuckerberg and abolish the firm’s share structure. Investors will vote on two proposals to overhaul Facebook’s governance at the social network’s annual shareholder meeting on May 30. Furthermore, Facebook went down for the third time this year, with both the Facebook and Instagram platforms going offline for several hours last Sunday.

- American Airlines has extended its cancellations of Boeing 737 Max flights. Flights using the aircraft will be suspended through August 19, Reuters says, citing a letter from American Airlines CEO Doug Parker and the airline’s president, Robert Isom.

- IBM missed on revenue. The computer-solution provider said revenue slumped 4.7 percent year-over-year to $18.2 billion in the first quarter, marking the third straight quarterly drop.

The Economy and Bond Market

Strengths

- The number of American jobless claims fell to more than a 49-and-a-half-year low last week, pointing to sustained strength in the economy, reports Reuters. For the week ended April 13, initial claims for state unemployment fell by 5,000 to a seasonally adjusted 192,000, according to the Labor Department. A Reuters’ poll of economists forecasted the claims rising to 205,000 in the latest week.

- Advance estimates of U.S. retail sales for March 2019 were up 1.6 percent from the previous month, and 3.6 percent above March 2018, reports Reuters. That was higher than the 1 percent month-over-month increase forecasted by economists.

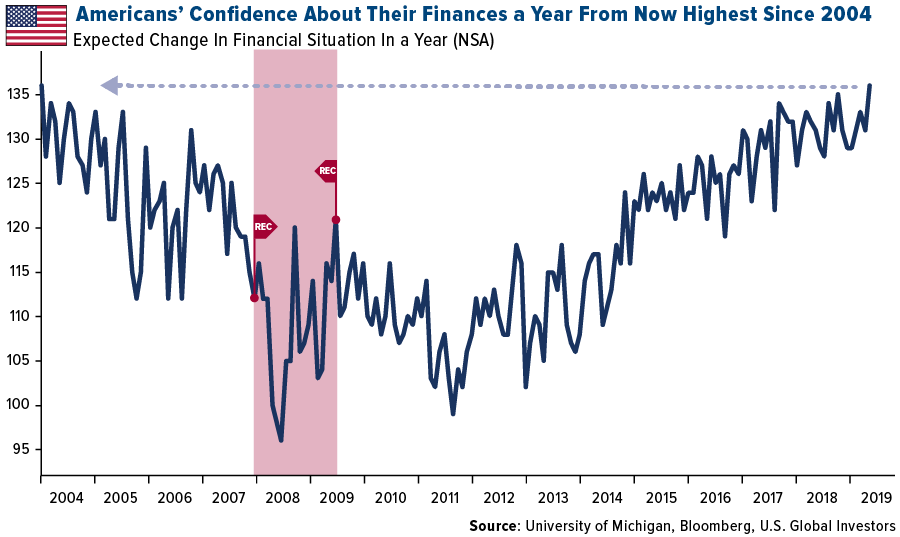

- It may be tax time, but Americans are the most upbeat in 15 years about their personal finances. The University of Michigan Index, measuring confidence a year from now, reached the highest since January 2004 in April.

Weaknesses

- U.S. industrial production declined 0.1 percent in March after rising 0.1 percent in February, according to the Federal Reserve. In the first quarter of the year, the industrial production index, which measures the output of the manufacturing, mining and electric & gas utilities industries, declined 0.3 percent at an annual rate.

- According to IHS Markit’s survey of business executives, American businesses expanded in April at the slowest pace in 31 months, writes MarketWatch. IHS Markit’s flash PMI for services slipped to 52.9 from 55.3, while the manufacturing index was flat at 52.4. "The U.S. economy started the second quarter with its weakest expansion since mid-2016 as businesses reported a marked slowing in output, new orders and hiring," said Chris Williamson, chief business economist at IHS Markit.

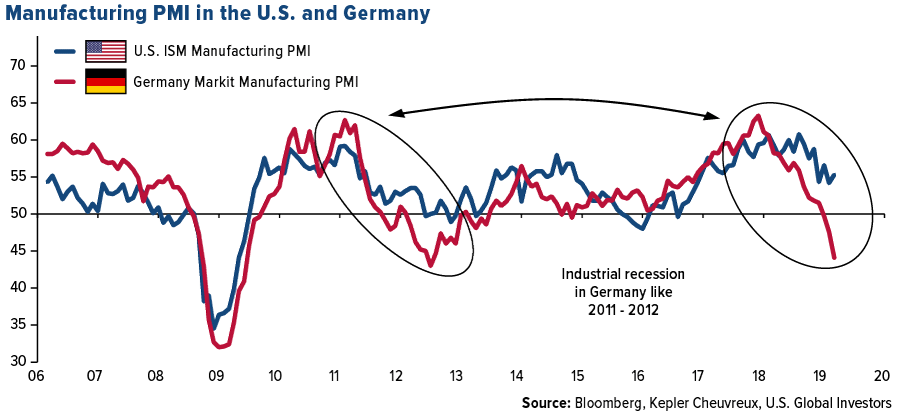

- Germany’s economy is looking weak, reports Business Insider. Manufacturing PMI inched up to 44.5 in April from 44.1 in March, marking the second-lowest reading since mid-2012 amid what the IHS Markit economist Phil Smith called "a declining car industry, strong competition across Europe, and generally subdued global demand."

Opportunities

- The Federal Reserve Bank of Atlanta’s GDPNow model rebounded sharply in recent weeks, which could mean the advance reading of first quarter GDP may not be quite so grim, writes Reuters. GDPNow estimated an annualized 0.2 percent growth a month ago, the article explains, which would have been the lowest since a one-off GDP contraction in the first 2014 quarter. However, the model now shows quarterly growth should come in at 2.4 percent. Not only would that top current estimates of 1.8 percent but it would mean that growth actually accelerated from the fourth quarter’s 2.2 percent.

- As reported by Morningstar, in the quarter ended March 31, tax-free muni bonds saw more than $8.8 billion in net flows. What’s more is that beat U.S. equity funds which saw $6.2 billion in inflows and international equity funds which saw $1.3 billion.

- Ahead of the holiday weekend, Bloomberg reports U.S. stocks edging higher as gains in industrial stocks slightly outweighed weakness in health care and energy shares.

Threats

- A majority of U.S. economic data through the first quarter fell short of forecasts. As a result, Citigroup’s U.S. economic surprise index is near the most negative in around two years.

- President Donald Trump’s tax law has increased after-tax home-ownership costs and reduced incentives to own homes, according to a report from the New York Fed economists Richard Peach and Casey McQuillan. According to this analysis, it appears the tax cuts may be contributing to the housing slowdown.

- The United States corporate sector is widely seen as heading into an earnings recession (defined as two straight quarters of negative year-on-year earnings growth), writes Reuters. Europe looks to be following suit with European firms expected to deliver their first quarter of negative earnings growth since 2016. The latest I/B/E/S Refinitiv analysis predicts first quarter earnings to fall 3.4 percent year-on-year, the article continues.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, up 3.58 percent on Indonesia’s announcement to expand the percentage it will blend into biofuels in the country. Copper reached its highest level in one month fueled by better-than-expected Chinese economic growth and speculation that new stimulus measures will bolster consumption of the metal. A weekly Bloomberg survey showed that copper traders and analysts were largely bullish on copper prices this week. Rio Tinto Group will invest a further $302 million in the Resolution copper project in Arizona, in an effort to boost its exposure to the red metal.

- Microsoft Corp. is joining a climate advocacy group backed by big energy corporations and high-profile Republicans. This is an effort by the company to find middle ground on environmental issues that have polarized U.S. politics for years, writes Bloomberg’s Dina Bass. The company said it will back the Climate Leadership Council to push for a carbon tax and pledged to use more green energy at its data centers.

- Bloomberg writes that more than a dozen governments and companies are planning to launch satellites that measure concentrations of heat-trapping greenhouse gases. This new wave of satellites will be able to pinpoint producers of greenhouse gases and get as specific as the location of an individual leak at an oil rig.

Weaknesses

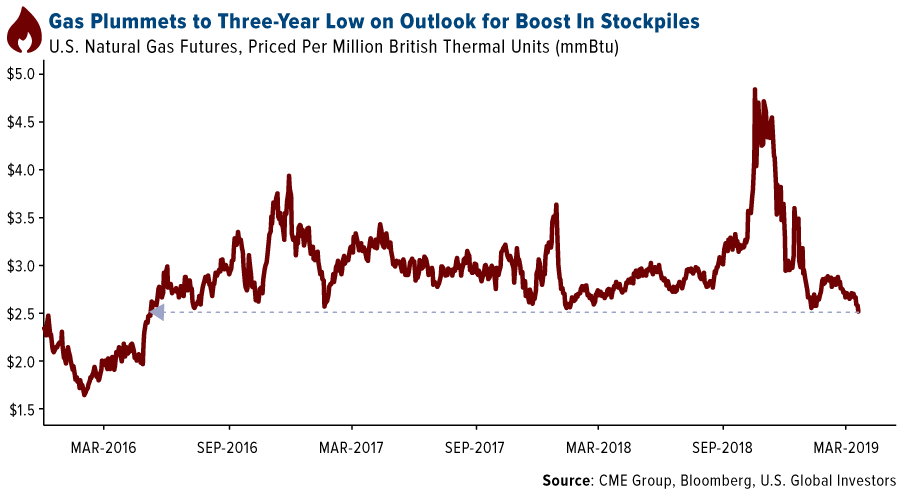

- The worst performing major commodity for the week was natural gas, which fell 6.68 percent. Natural gas futures plummeted to a three-year low as U.S. shale output continues to flood the market amid mild spring weather. Bloomberg writes that although inventories are more than 30 percent below average, they are expected to refill quickly. Iron ore also took a tumble this week on news that Vale SA will restart operations at a major mine in Brazil in the next few days, offsetting concerns about a shortage out of Australia.

- In another big hit to coal, Oversea-Chinese Banking Corp., which is Southeast Asia’s second-largest lender, said that two Vietnamese coal power plants will be the last ones it finances, writes Bloomberg. CEO Samuel Tsien said in an interview at its Singapore headquarters that the company “won’t do any new coal-fired power generation plants in any countries, except for the power projects that we are already in.”

- Shares of Petrobas, Brazil’s state-controlled oil company, fell late last week after a decision to reverse a previously announced diesel price increase raised concerns that the company will undo a policy of market-based prices, reports Bloomberg. The diesel price decision sparks memory of fuel subsidies that cost the company tens of billions of dollars earlier this decade.

Opportunities

- Concho Resources Inc. has agreed to form an equally split joint venture with Frontier Midstream Solutions IV LLC to build a crude pipeline system for the rapidly-growing Permian Basin, reports Bloomberg. This is very positive for the region, which has seen infrastructure lag behind output.

- According to data from the China National Renewable Energy Center, solar capacity additions slumped 46 percent in the first quarter of this year. However, total capacity is still expected to reach 460 gigawatts by 2025, up significantly from 174 gigawatts at the end of 2018. Research from WindEurope shows that European investment in wind energy could reach $111 billion over the next three years that would translate into an extra 53 gigawatts of wind power capacity by 2021.

- Oil bullishness is at a 2019 high as bets on Brent weakness plunged 18 percent, reports Bloomberg. Tyler Richey, co-editor at Sevens Reports, says “we could be near a market top, but it’s just too early to tell. Right now, the path of least resistance is higher for oil.” Bloomberg’s David Wethe writes that the world’s biggest oilfield servicer, Schlumberger Ltd., says that the global oil industry is set to improve in 2019, supported by a solid demand outlook as production cuts from OPEC and its partners take effect.

Threats

- While many are bullish on oil’s continued rise, some see roadblocks in the form of weaker demand out of Asia. Bloomberg’s Serene Cheong writes that global benchmark prices around $71 per barrel will put pressure on government finances in Asia’s import-dependent nations. Tushar Tarun Bansal, trading and downstream expert at McKinsey & Co., says that “demand for crude in Asia and other regions is directly dependent upon downstream fuel margins” and that in the near term they’re seeing “weak margins and higher-than-usual planned refinery maintenance in Asia.”

- Codelco, the world’s top copper producer, is struggling to stay ahead as its flagship open pit Chuquicamata mine in Chile is being shut and replaced by an underground mine that will take five years to reach its potential. Colin Hamilton, managing director for commodities at BMO Capital Markets, says that “it’s looking increasingly like Codelco might be a 1-million ton producer and not the two million tons that they’ve always promised.”

- Bloomberg News writes that the $18 billion electric vehicle (EV) bubble is at risk of bursting in China. According to BloombergNEF, annual sales of passenger EVs only surpassed 1 million units for the first time in 2018, largely spurred by government subsidies. There are now 486 EV manufacturers in China; however, a factory typically needs to produce tens of thousands of vehicles a year to be profitable. China wants annual sales to reach 7 million units by 2025, but that still would be barely enough to sustain a few dozen EV companies.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 1.7 percent. Greek 10-year bonds yields have declined significantly in recent months, and this reflects the impact of improved liquidity and financial market sentiment toward the country. MSCI announced that Eurobank will be added back to its Mid-Cap Index following the completion of its acquisition of Grivalia.

- The Russian ruble was the best performing currency this week, gaining 45 basis points against the U.S. dollar. The currency is supported by an uptrend in the price of Brent crude oil.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 30 basis points. OTP Bank had the biggest negative effect on the performance of the Budapest stock exchange this week. Shares of the bank have declined by 1.5 percent in the past four days.

- The Czech koruna was the worst performing currency this week, losing 90 basis points against the U.S. dollar. The koruna depreciated with the euro, which dropped against the dollar on unfavorable preliminary PMI data released on Thursday. The April Manufacturing PMI reading for the Eurozone slid to 47.8, white the Service PMI reading declined to 52.5.

- Communication service was the worst performing sector among eastern European markets this week.

Opportunities

- According to research from Kepler Cheuvreux, the German economy was one of the first to enter the current global economic slowdown due to its high exposure to global growth in general and to Asia in particular. The industrial recession in Germany is similar in profile to that of 2011-2012. Kepler believes that the phase of collapse of output is complete, but Kepler’s team does not expect a recovery of any significance before summer. They conclude that the fall of growth expectations in Europe is virtually complete. Europe is not moving into recession, and growth will rebound due to strong domestic demand.

- German investor confidence improved for the sixth consecutive month. For the Eurozone, the expectation for economic growth improved from a negative reading 2.5 in March to a positive 4.5 in April. The improved growth sentiment across Europe is most likely due to Brexit’s deadline extension.

- Turkish election officials Wednesday certified the victory of an opposition candidate in the race for mayor of Istanbul, despite a determined effort by President Recep Tayyip Erdogan’s governing party to appeal the results of the vote. The election board in Istanbul confirmed that Ekrem Imamoglu, a member of the Republican People’s Party, or CHP, was elected mayor in the contest more than two weeks ago. Turkey most likely will avoid another election and will concentrate of implementing reforms that should stimulate economic growth.

Threats

- Domestically-focused equity mutual and exchange-traded funds have booked back-to-back months of inflows, while international funds traded in the U.S. have suffered outflows, according to DataTrek Research co-founder Nicholas Colas. It is the first time since the trade war heated up in the middle of 2018 that withdrawals have hit non-U.S. oriented funds two months in a row. The U.S. stock market continues to perform well, and investors are rotating out of international laggards into domestic gainers.

- The Polish government plans to transfer all state-guaranteed private pension funds to individual retirement accounts, which are similar to 401K plan in the U.S. Back in 2014, the previous government transferred half of the state-guaranteed private pension funds (bonds) to the government. The government imposed a transfer fee in the amount of 15 percent of the assets and will be able to collect around $6.5 billion.

- Russia may offer passports to people living in breakaway regions of eastern Ukraine, a move that would create more political tension in the region. This Sunday, Ukraine will hold a second round of presidential elections, and according to polls, Volodymyr Zelensky will win. He has been criticized for s lack of political experience.

China Region

Strengths

- The Shanghai Composite Index was up 1.93 percent for the week heading into trading on Friday, while Indonesia’s Jakarta Composite jumped 1.58 percent; the island nation wrapped up elections this week and Joko Widodo looks set to cruise into another term. The Taiwan Stock Exchange was up 1.45 percent on the week heading into Friday.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index for the week was financials, which rose 1.88 percent.

- China’s first quarter gross domestic product (GDP) reading surpassed analysts’ expectations, clocking in at a 6.4 percent pace, ahead of the expected 6.3 percent print analysts were looking for.

Weaknesses

- Vietnam’s Ho Chi Minh Stock Index declined 2.10 percent this week through Thursday, while Korea’s KOSPI was down 88 basis points and Malaysia’s KLCI was down 60. The Philippines Stock Exchange dropped 58 basis points over the three days it was open this week before closing for holidays Thursday and Friday.

- The worst-performing sector in Hong Kong’s Hang Seng Composite was the properties and construction sector, which declined 1.71 percent.

- Overseas remittances to the Philippines missed this month, falling down to a 1.5 percent gain in February from last year, coming up shy of an anticipated 3.9 percent pace.

Opportunities

- Indonesia went to the polls this week, and it looks as if Joko Widodo is set for a second term. “Jokowi,” as he’s popularly known, is now officially claiming victory, although we won’t get final tallies until May. Unofficial independent pollsters—which have been quite historically reliable—are showing the incumbent and his running mate Ma’ruf Amin bringing in some 54.5 percent on average. Indonesia’s markets and currency responded positively on Thursday to the results. While we’ll hear more on Indonesia and from Jokowi on specifics and initiatives over coming weeks and months, one important thing to highlight is the administration’s new plan for aiding in further land reform. Some recent CLSA reports have covered the topic quite well. The land reform campaign aims not only to continue to boost certificates for non-forestry land but to allow rural citizens to use more easily their land holdings as collateral for bank loans (and presumably, growth). This in turn can boost the financial system’s role in the economy while cutting the income gap between rich and poor.

- A resolution perceived as positive by markets to the U.S.-China trade spat may provide more impetus to global and regional markets. Talk of a signing ceremony possible by the end of May did not elicit much reaction from markets. But no news seems to be considered relatively good news on the whole, because it is not being perceived as bad news, and the two sides appear to making some concessions. The U.S. indicated it is also open to penalties and enforcement mechanisms if it fails to live up to its side of any bargain, while the U.S. is apparently requesting the Chinese to redirect tariffs away from agriculture and toward other non-agricultural items.

- Beijing will host the second Belt and Road Initiative (BRI) Forum next week, as China continues to push on with its so-called modern-day Silk Road that aims to revive and extend ancient routes (and of course, project some soft power while exporting overcapacity). As noted in a recent Investor Alert, China has called publicly for more assistance in its global projects, encouraging the U.S. and European Union (EU) countries to partner with the Asian nation on this ambitious BRI. Note also that in the same week China’s GDP print beat expectations, China’s Premier Li Keqiang voiced confidence in the Asian nation’s capability in delivering on growth targets for the year and the People’s Bank of China (PBOC) Deputy Governor Chen Yulu expressed to the International Monetary Fund (IMF) that the Chinese economy has been generally stable.

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter remain a collective threat until resolution one way or the other amid the dispute. This week rumors of hopes for a signing ceremony by the end of May were the latest development, which seems positive, but the market did not much care. Somewhat ironically, some market analysts took as a negative the buoyant sense of overall optimism toward the Chinese economy following a better-than-expected GDP print and the positive remarks mentioned immediately above by Li Keqiang. Why, you ask? Because, the reasoning goes, it might weaken the Trump administration’s hand in negotiations, thus strengthening China’s, and possibly undo the sense of urgency for a deal or call for revisions. It is hard, though, given the stimulus announcements that have played out over recent months, to imagine this scenario was not considered a real possibility, and one can thus further imagine the United States was at least prepared for this possibility (as indeed was China), and so there may be less surprise in the mix than naysayers would like to admit.

- We may be subject to a bit of wait-and-see mode on China and additional stimulus measures now with the (literally) new and improved data. It’s a good problem to have, but could lead to some sectors or analyses being subjected to some disappointment on easing measures.

- The U.S. dollar remains strong, which could possibly weigh on or spook emerging markets (EM) at some point. The dollar has not yet broken out to new 52-week highs, and the Federal Reserve remains in “pause” mode, but the U.S. has not yet ruled out further hikes, and the dollar remains strong in the meantime.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 18 was Open Platform, up 764.23 percent.

- Both Accenture and Generali Employee Benefits announced this week the debut of a first-of-its-kind blockchain solution for the employee benefits industry, according to a press release. The aim of implementing this technology is to allow participants in the reinsurance process for captive or pooling services to access the same data and reduce processing errors through smart contracts and automated reconciliation, the announcement goes on to explain.

- The launch of the Coinbase Card was announced this week, a Visa debit card that lets customers in the U.K. spend cryptocurrency “as effortlessly as the money in their bank,” according to the Coinbase blog. The card is powered by customers’ own Coinbase account balances and gives them the ability to pay in-store and online using bitcoin, Ethereum, litecoin and more.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 18 was SuperEdge, down 77.95 percent.

- SBI Virtual Currencies, a Japanese cryptocurrency exchange, has decided to drop Bitcoin Cash (BCH) from its list of supported coins by month end due to dwindling market cap, the company announced in a press release this week. According to the exchange, as the BCH market cap continues to fall, this would ultimately make the blockchain susceptible to a 51 percent attack.

- Amid an ongoing feud between bitcoin SV (BSV) creator Craig Wright and outspoken members of the bitcoin community, another major crypto exchange will be delisting BSV, reports Coindesk. Kraken announced on Tuesday that it will disable BSV deposits starting April 22 and that trading will cease on all trading pairs on April 29, with withdrawals stopping May 31.

Opportunities

- The International Monetary Fund (IMF) and the World Bank have launched a cryptocurrency token called “Learning Coin” in order to better understand how blockchain technology works, reports CoinDesk. As reported by the Financial Times on Saturday, the two institutions clarified that the coin would have no monetary value and would not be made openly available, but is aimed at building a “strong knowledge base” around blockchain among the staff at both organizations.

- John McAfee, a closely followed British-American cybersecurity expert, has shared his detailed prediction for the price of bitcoin based on mathematics, reports FXStreet. McAfee claims that it is “mathematically impossible” for bitcoin to be less than $1 million by the end of 2020, explaining that the digital currency is not a stock and that people should not apply stock paradigms or formulas to it and expect answers.

- France’s Minister of Economy and Finance, Bruno Le Maire, has stated in an interview with French economics and business magazine “Capital” that blockchain technology is a priority for his country’s government. In fact, Le Maire revealed that the state plans to invest 4.5 billion euros ($5 million) in breakthrough innovations – including blockchain – in a bid to fight Chinese and American technological dominance, writes CoinTelegraph.

Threats

- Unocoin, a cryptocurrency trading platform based in Bengaluru, has given pink slips to half of its remaining employees, writes the Economic Times of India, in a bid to conserve cash after talks to raise another round of funding failed to take off. The startup was founded in 2013, and with a team scaled back now to 14 employees (from over 100 last February), and is currently fighting for survival in an uncertain regulatory environment.

- Intercontinental Exchange Inc. continues to face resistance from federal regulators over its plan to bring bitcoin to the masses via a project known as Bakkt, reports Bloomberg. Bakkt has been delayed for months as the Commodity Futures Trading Commission (CFTC) has issues with how clients’ tokens will be stored, thus safeguarded from possible theft. The light at the end of the tunnel comes from the possibility of seeking a license from the New York financial regulators that would permit Bakkt itself to hold custody of customers’ tokens, the article explains.

- According to a report from Coveware, the average payment requested in a ransomware attack in bitcoin is $12,762 for the first quarter of 2019. This is significantly higher than $6,733 in the fourth quarter of 2018. Ransomware attacks on crypto exchanges are becoming increasingly common and more sophisticated.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 186.44 | -7.90 | -4.07% |

| Gold Futures | 1,277.30 | -16.00 | -1.24% |

| Natural Gas Futures | 2.49 | -0.18 | -6.68% |

| S&P/TSX VENTURE COMP IDX | 609.20 | -15.21 | -2.44% |

| 10-Yr Treasury Bond | 2.56 | +0.06 | +2.52% |

| Nasdaq | 7,998.06 | +50.70 | +0.64% |

| Oil Futures | 64.03 | +0.45 | +0.71% |

| Hang Seng Composite Index | 4,031.39 | +22.24 | +0.55% |

| S&P 500 | 2,905.05 | +16.73 | +0.58% |

| DJIA | 26,559.54 | +416.49 | +1.59% |

| Korean KOSPI Index | 2,213.77 | -10.67 | -0.48% |

| Russell 2000 | 1,565.75 | -13.39 | -0.85% |

| S&P Energy | 496.88 | -1.80 | -0.36% |

| S&P Basic Materials | 362.00 | +2.94 | +0.82% |

| XAU | 72.89 | -3.09 | -4.07% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.49 | -0.39 | -13.50% |

| S&P/TSX Global Gold Index | 186.44 | -4.63 | -2.42% |

| 10-Yr Treasury Bond | 2.56 | -0.05 | -1.99% |

| Oil Futures | 64.03 | +5.00 | +8.47% |

| Gold Futures | 1,277.30 | -35.40 | -2.70% |

| S&P 500 | 2,905.05 | +72.48 | +2.56% |

| S&P Energy | 496.88 | +6.73 | +1.37% |

| Hang Seng Composite Index | 4,031.39 | +92.71 | +2.35% |

| DJIA | 26,559.54 | +672.16 | +2.60% |

| Korean KOSPI Index | 2,213.77 | +36.15 | +1.66% |

| Nasdaq | 7,998.06 | +274.12 | +3.55% |

| S&P Basic Materials | 362.00 | +14.62 | +4.21% |

| Russell 2000 | 1,565.75 | +10.77 | +0.69% |

| S&P/TSX VENTURE COMP IDX | 609.20 | -26.87 | -4.22% |

| XAU | 72.89 | -2.51 | -3.33% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.49 | -0.90 | -26.54% |

| 10-Yr Treasury Bond | 2.56 | -0.16 | -5.95% |

| DJIA | 26,559.54 | +2,352.38 | +9.72% |

| Oil Futures | 64.03 | +11.72 | +22.40% |

| S&P 500 | 2,905.05 | +288.95 | +11.05% |

| Gold Futures | 1,277.30 | -29.30 | -2.24% |

| S&P Energy | 496.88 | +38.78 | +8.47% |

| Nasdaq | 7,998.06 | +963.37 | +13.69% |

| Korean KOSPI Index | 2,213.77 | +107.67 | +5.11% |

| S&P Basic Materials | 362.00 | +37.86 | +11.68% |

| Russell 2000 | 1,565.75 | +111.06 | +7.63% |

| Hang Seng Composite Index | 4,031.39 | +458.72 | +12.84% |

| S&P/TSX Global Gold Index | 186.44 | +12.28 | +7.05% |

| S&P/TSX VENTURE COMP IDX | 609.20 | +11.16 | +1.87% |

| XAU | 72.89 | +3.35 | +4.82% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

American Airlines Group Inc

Boeing Co/The

OTP Bank Nyrt

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Citi Economic Surprise Index measures actual data against Wall Street estimates to gauge the optimism about the economy.

The S&P Municipal Bond Index is a broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market.

The S&P U.S. Treasury Bond Current 10-Year Index is a one-security index comprising the most recently issued 10-year U.S. Treasury note or bond.

The S&P 500 Investment Grade Corporate Bond Index, a sub-index of the S&P 500 Bond Index, seeks to measure the performance of U.S. corporate debt issued by constituents in the S&P 500 with an investment-grade rating.

The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies.

The industrial production index (IPI) is an economic indicator that is released monthly by the Federal Reserve Board. The indicator measures the amount of output from the manufacturing, mining, electric and gas industries.

The J.P. Morgan Global FX Volatility Index is a benchmark for implied volatility across the global FX market. The VXYs are liquidity-weighted baskets of 3-month at-the-money implied volatilities based on FX options turnover reported in the BIS Triennial Central Bank Survey. The minimum daily turnover threshold is USD 300mm. The VXY Global covers 23 USD-based currency pairs.

The MSCI Europe Mid Cap Index captures mid cap representation across the 15 Developed Markets (DM) countries in Europe. With 247 constituents, the index covers approximately 15% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange.

The TWSE, or TAIEX, Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The index was based in 1966. The index is also known as the TSEC Index.

The Kuala Lumpur Stock Exchange Composite Index (KLCI) is a broad-based capitalization-weighted index of 100 stocks designed to measure the performance of the Kuala Lumpur Stock Exchange.

The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange.