The U.K. Just Said No to Socialism. Will U.S. Voters Do the Same in 2020?

Date Posted: December 20, 2019

Read time: 53 min

Imagine you wake up tomorrow from a three and a half-year coma. Everything that's happened in the meantime--the election of Donald Trump, impeachment, Brexit and more--is a complete mystery to you.

Press Release: U.S. Global Investors Funds to Pay Year-End Distributions

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Let’s begin with a thought experiment.

Imagine you wake up tomorrow from a three and a half-year coma. Everything that’s happened in the meantime—the election of Donald Trump, impeachment, Brexit and more—is a complete mystery to you.

Now imagine that I try to catch you up on what you’ve missed, but instead of handing you a stack of newspapers and magazines with manic headlines, or logging you on to Trump’s Twitter feed, I show you only the data: leading economic indicators, sentiment indices, stock averages. (The U.S. manufacturing purchasing manager’s index (PMI) is the one exception, which I’ll get to in a second.)

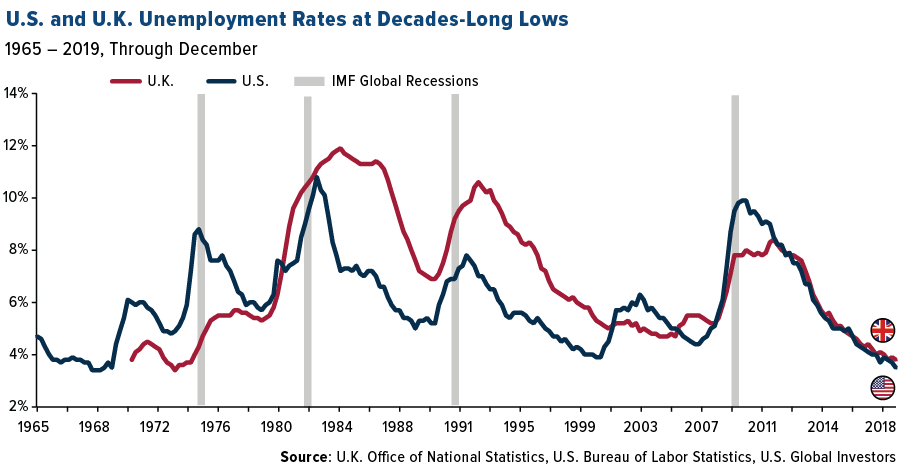

I show you the unemployment rate in the U.S. and U.K., both of which are at decades-long lows. And Britain’s employment rate, at 76.2 percent as of October, is the highest ever.

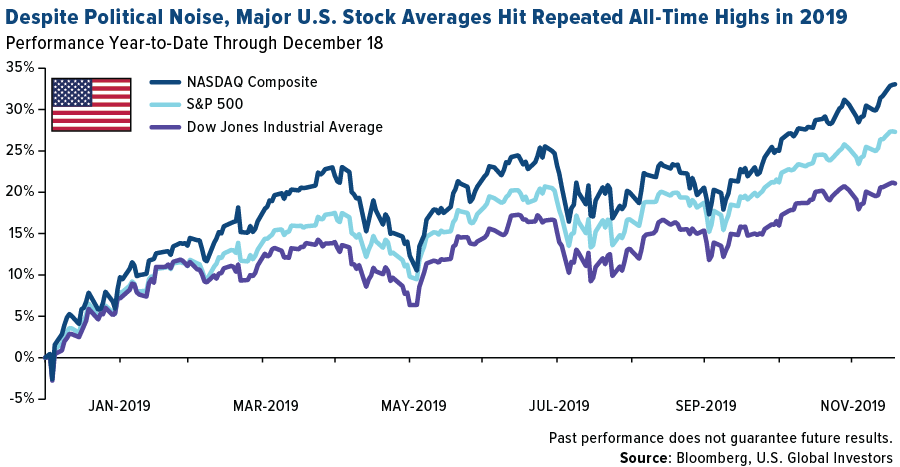

I show you the phenomenal returns for each of the three U.S. stock indices. The historic bull market is alive and kicking, you learn. And with a handful of trading days left in 2019, there’s plenty of room for this year to be the best of the more than 10-year bull run, beating even 2013, when the S&P 500 surged 32 percent.

Even if 2019 ended today, it would still end up as the 10th or 11th best year for the stock market going back to 1970.

After taking all of this in, you may very well believe, at the worst, that things are just “fine” right now.

At the best, you may think they couldn’t get any better. In some respects, you would be right.

And yet there’s an alarming number of people right now—having been exposed to the breathless, apoplectic headlines over the past few years, and wrung their hands at every crass thing the president has said—who are absolutely convinced that the sky is falling.

To illustrate, a recent Financial Times survey of approximately 1,000 Americans found that a shocking 42 percent believe the stock market is at “about the same” levels as at the beginning of the year. An incredible 18 percent think it’s actually decreased. About two-thirds of respondents say their personal finances have not improved since Trump’s election, even though the market is up roughly 55 percent since then, and average hourly wages have increased more than 9 percent.

Today, in fact, the government released data showing that third-quarter personal spending rose 3.2 percent, after rising 4.6 percent in the April-to-June period—the best back-to-back quarters in five years. This alone undermines some people’s negative outlook.

Follow the Trend Lines, Not the Headlines

Obviously I would never wish a coma on anyone, but you can see why it’s important to follow the trend lines, not the headlines. Spared the pervasively negative bias, a person newly awoken from a three-year sleep would be in a far better position, I believe, to make financial and investment decisions than someone whose outlook has been shaped by the evening news.

As I shared with you last week, investors this year yanked a whopping $135.5 billion from U.S. equity-focused mutual funds and ETFs. That’s the biggest 12-month withdrawal on record going back to 1992, and there appears to be little basis for it other than geopolitical noise.

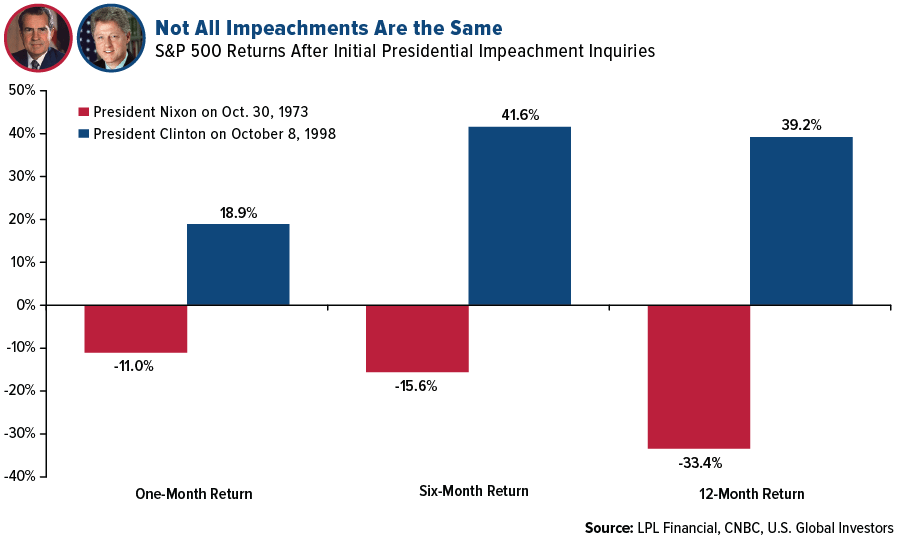

Threats to this bull market exist, but I don’t see Trump’s impeachment as one of them. The Republican-led Senate is unlikely to convict, and so I expect him to survive, politically, to end up on the 2020 ballot. Fortunately for Trump, many Americans vote with their wallets. As long as the economy continues to grow and stocks continue to hit all-time highs, voters may be willing to overlook the president’s shortcomings and give him another four years in the White House.

The biggest risk to Trump’s reelection is the sagging U.S. manufacturing PMI. The leading indicator was below the key 50.0 threshold for the fourth straight month in November, making this one of the longest-running periods of month-over-month contraction of the past 40 years. Keep in mind, though, that the weakness is a reflection of the U.S.-China trade war, and if Trump can broach a deal to end the dispute, the PMI should quickly recover, increasing his chances of winning a second term.

The 2010s saw the longest economic expansion in U.S. history, with the S&P 500 soaring to record highs. Test your knowledge of the stock market this past decade by clicking here!

A Bellwether From Across the Atlantic

What also bodes well for Trump is Boris Johnson’s earth-shattering victory in the U.K. last week. Johnson’s Conservative party toppled the so-called “red wall,” winning seats across rural, working-class North and Midlands counties that had for decades been considered safe Labour territory.

Trump pulled off a similar feat in 2016, if you recall, when he attracted scores of disaffected voters in heavily unionized, Democratic stronghold “Rust Belt” states.

In the U.K., Johnson’s sweeping win can only be seen as a renunciation not just of Labour leader Jeremy Corbyn’s 1970s-style socialism, but of capital-S Socialism in general.

The Brexit referendum more than three years ago was itself a referendum on what I called “a classic case of failed socialism”:

“Defying sentiment polls leading up to last week’s historic Brexit referendum, British voters said ‘thanks, but no thanks’ to excessive EU taxation and regulation, choosing to take back Britain’s sovereignty in financing, budgeting, immigration policy and other areas essential to a nation’s self-identity.”

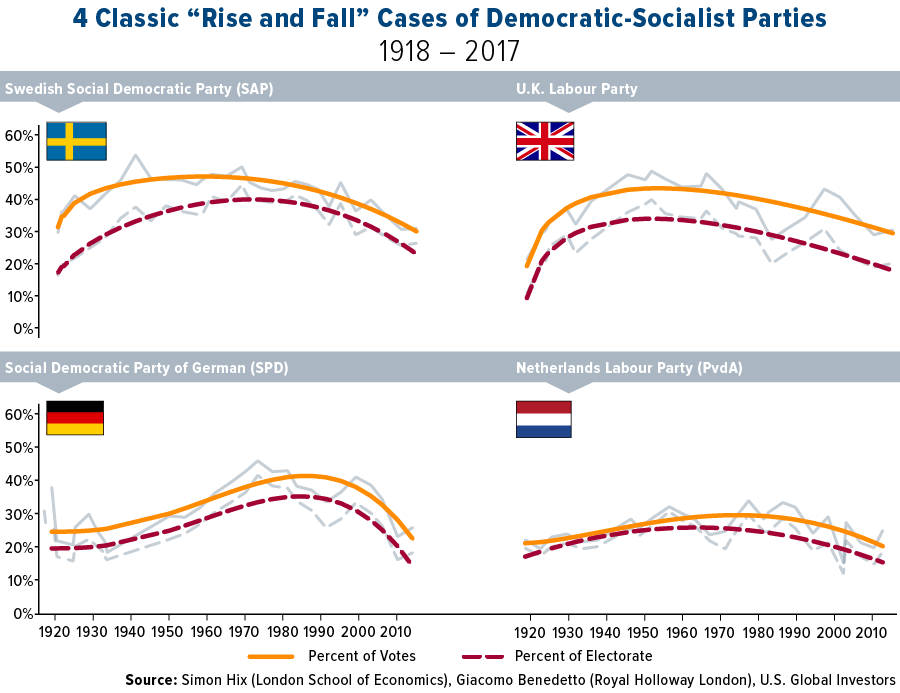

Brexit and now Johnson’s victory are also part of a macro trend we’re seeing in Europe right now, as hard as it might be to believe sometimes. According to political analysts Giacomo Benedetto, Simon Hix and Nicola Mastrorocco, we’re well past the peak in popularity of democratic-socialist parties in Western European countries such as Sweden, the U.K., Germany and the Netherlands. With a January 31 Brexit looking more likely than ever before, Europe’s slide away from socialism should only pick up further steam.

If I were the Democratic National Committee (DNC), I might be rethinking the possibility of putting up a socialist leaning candidate against Trump.

To all of my readers, new and old, I wish you a Merry Christmas, Happy Hanukkah and Happy New Year! May 2020 bring you good health, happiness and great fortune!

Gold Market

This week spot gold closed at $1,481.64, up $5.31 per ounce, or 0.36 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.94 percent. The S&P/TSX Venture Index came in up 1.54 percent. The U.S. Trade-Weighted Dollar rose 0.55 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-15 | China Retail Sales YoY | 7.6% | 8.0% | 7.2% |

| Dec-17 | Housing Starts | 1345k | 1365k | 1323k |

| Dec-18 | Eurozone CPI Core YoY | 1.3% | 1.3% | 1.3% |

| Dec-19 | Initial Jobless Claims | 225k | 234k | 252k |

| Dec-20 | GDP Annualized QoQ | 2.1% | 2.1% | 2.1% |

| Dec-23 | Durable Goods Orders | 1.5% | — | 0.5% |

| Dec-23 | New Homes Sales | 730k | — | 733k |

| Dec-26 | Initial Jobless Claims | 220k | — | 234k |

Strengths

- The best performing metal this week was silver, up 1.57 percent with money managers raising their net long position by about 20 percent. The number of gold bulls outnumbered the bears for a third straight week, according to the Bloomberg survey of gold traders and analysts. Turkey increased its gold reserves overall in the month of November to 18.16 million ounces, up from 17.79 million in October. Kazakhstan also boosted its gold reserves last month to 12.28 million ounces, up from 12.13 million in October.

- Russia has taken steps to potentially limit gold exploration, which could be positive for the gold price with tighter supply. The Natural Resources Ministry will not raise the threshold for deeming a gold field strategic, leaving the number at 50 tons. Bloomberg reports that the Russian government can seize a gold mining license for a deposit from a company if exploration shows reserve exceed 50 tons – this should limit exploration by non-Russian companies. Australia hopes to dethrone China as the world’s top gold producer in 2019. Currently in the number two spot, Australia has seen gold production increase from 302 tons in 2017 to 322 tons in 2018, and expects to mine 337 tons by year end.

- Bloomberg reports that Alamos Gold intends to buy back 10 percent of the public float of its common shares, or 28.8 million class A shares, over the next 12-month period. QMX Gold Corp announced that Eldorado Gold Corp will make over a $4 million investment in the company in a private placement. Eldorado’s holding in QMX will be nearly 20 percent.

Weaknesses

- The worst performing metal this week was palladium, down 3.93 percent on what appears to be profit taking from a more than 50 percent gain in price this year. Although Turkey’s gold reserves were up for the month of November, they fell in the week ended December 13 by $840 million from the previous week. GDP in Ghana grew by 5.6 percent from a year earlier, slower than the 5.7 percent in the previous quarter. Bloomberg reports that the slowdown is mainly due to a 19 percent contraction in annual gold output and processing for value addition. The West African nation overtook South Africa earlier this year to be the continent’s biggest producer of the metal.

- De Beers announced that its diamond sales this year fell by almost $1.4 billion – capping a very bad 12 months. Bloomberg writes that there has been little good news this year for the diamond industry as an oversupply of rough diamonds hurt prices. In November the company cut prices across the board by 5 percent.

- A security contractor was killed in an armed attack at a Harmony Gold Mine in South Africa. The company reported that no gold was stolen during the attack. Bloomberg reports this was the second incident in just a few months with a security officer killed and 17 kilograms of gold stolen from DRDGold’s Ergo plant in the country in October.

Opportunities

- On Wednesday, Comex gold open interest rose close to a record high seen in November. ABN Amro Bank NV strategist Georgette Boele said investors “are opening positions because they hope or think that we have seen the low” for gold prices. Bloomberg reports that even though global stocks are close to all-time highs, several risks remain such as the yet to be finalized U.S.-China trade deal, President Trump’s impeachment and Brexit. Investors have flooded into gold in 2019. Long-only ETFs focused on gold have gained almost $18 billion so far this year, the most since 2016. Nitesh Shah, director of research at WisdomTree, says political turmoil in Washington may spur more interest in gold as safe haven demand.

- Conor Sen, portfolio manager for New River Investments, wrote in a Bloomberg opinion piece this week that the U.S. dollar might finally be poised to weaken. Sen writes that if the dollar’s rally does come to an end, it could push the global economy into higher gear in 2020. “A rebound in commodity prices could contribute to a new cycle of global investment. Higher import prices should put upward pressure on domestic prices, helping the Fed hit its 2 percent inflation target.”

- Equinox Gold Corp is acquiring Leagold Mining Corp for $586 million. Bloomberg reports the deal would expand Equinox’s production to 700,000 ounces in 2020, with the new company operating six mines in the U.S., Mexico and Brazil. This is another example of a major producer picking up a junior with one large deposit. With a need to replenish reserves, we could see more juniors being acquired by the majors. Sean Boyd, CEO of Agnico Eagle Mines, told Bloomberg in its 2020 outlook that “the greatest challenge for the industry is replenishing reserves.” CEO of Barrick Gold Mark Bristow said that “more mining consolidation is still needed, especially in the gold sector.”

Threats

- Fedex Corp. saw its shares plunge this week after cutting its profit forecast for the second straight quarter. Bloomberg reports that the retail giant Amazon.com Inc. ended most of its business ties this year as the online retailer is building out its own delivery network. This is yet another sign of consolidation hurting a longtime industry player, similar to what happened to Dean Foods after Walmart created its own milk production, resulting in Dean’s bankruptcy.

- In a bad sign for the economy, Bloomberg reports that personal income has been falling since March and real earnings have been falling since February. Disposable income was taken up largely by housing and medical costs. Additionally, November headline retail sales were less than half of what the consensus projected, rising just 0.2 percent, compared with an estimate of 0.5 percent.

- The Endeavour Mining Corp and Centamin Plc deal is looking unlikely to make the December 31 regulatory deadline. Endeavour suggested that Centamin seems unwilling to explore the benefits of combining the two Africa-focused gold producers, reports Bloomberg. Under the U.K. takeover code, if the end of year deadline passes then Endeavour won’t be able to bid again for six months. This is called a “put up or shut up” takeover timetable.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.14 percent. The S&P 500 Stock Index rose 1.65 percent, while the Nasdaq Composite climbed 2.18 percent. The Russell 2000 small capitalization index gained 2.07 percent this week.

- The Hang Seng Composite gained 0.87 percent this week; while Taiwan was up 0.26 percent and the KOSPI rose 1.56 percent.

- The 10-year Treasury bond yield rose 9 basis points to 1.918 percent.

Domestic Equity Market

Strengths

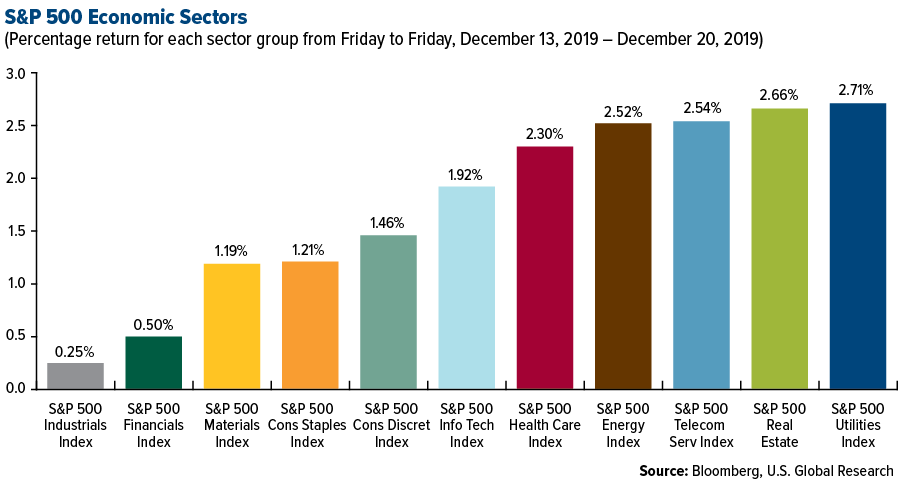

- Utilities was the best performing sector of the week, increasing by 2.71 percent versus an overall increase of 1.64 percent for the S&P 500.

- Conagra Brands was the best performing S&P 500 stock for the week, increasing 23.57 percent.

- Carnival Corp. jumped the most in a decade after earnings and its 2020 outlook topped expectations as the company made adjustments to mitigate effects from the weak European market. Carnival, which is the largest cruise operator and has significant exposure to continental Europe, was able to meet the challenges in part through adjusting itineraries and effective marketing, Chief Executive Office Arnold Donald said on a conference call Friday. Fiscal fourth quarter adjusted earnings per share were 62 cents, topping the 50-cent average analyst estimate. The company projected 2020 net cruise revenue will increase 5 percent. The stock soared as much as 9.8 percent in New York, its biggest intraday jump since June 2009.

Weaknesses

- Industrials was the worst performing sector for the week, increasing by 0.25 percent versus an overall increase of 1.64 percent for the S&P 500.

- Fedex was the worst performing S&P 500 stock for the week, falling 10.59 percent.

- Movie-goers will watch James Bond test drive Aston Martin Lagonda Global Holdings Plc’s luxury sports cars in “No Time to Die” in April, during what could be a critical year for the company. The firm, whose stock has tumbled since its 2018 initial public offer, is taking orders for its new $189,000 sports utility vehicle, the DBX, but will need to raise cash regardless of how many it sells in order to deleverage, says Jefferies’ Philippe Houchois. “There’s no way around the company needing some equity, it’s a question of how and when,” he said, estimating a requirement of about $262 million.

Opportunities

- Value stocks have gained traction among investors in 2019. Banks, while still the cheapest sector after autos, no longer appear to be pariahs. They could be positioned to do well in the short-term, given the current positioning and extremely cheap valuations along with positive loan growth and declining non-performing loans.

- Energy is one of the “value” sectors forgotten in the recent rally, as the market is not convinced of the positive impact of so-called IMO2020 new regulations. Consequently, oil and gas stocks are a potential opportunity after an underwhelming year for the sector.

- Investors are overlooking an “oasis” of growth potential in small and mid-cap stocks worldwide. So called SMID-caps offer an attractive growth alternative to volatile emerging market shares and price, high-growth large-cap stocks, said Ned Bell, chief investment officer at Bell Asset Management.

Threats

- FedEx’s dismal earnings have investors scrambling to find the bottom as Amazon’s logistics network looms. The company’s shares plunged Wednesday after it released disappointing earnings a day earlier and cut its profit outlook for at least the third time in 2019. The delivery company is struggling to adapt to the rise in e-commerce and additional costs to build out its ground network, which is more expensive to run and less profitable than its niche business-to-business delivery model.

- The Federal Trade Commission filed a suit against FleetCor, a company that sells fuel card services to businesses, alleging that it has charged customers at least hundreds of millions of dollars in hidden fees after making false promises about helping customers save on fuel costs.

- CarMax fell the most in five months after earnings missed expectations due to higher advertising spending and share-based compensation costs, analysts said. KMX shares slid as much as 6.1 percent, the biggest intraday drop since July.

The Economy and Bond Market

Strengths

- U.S. economic growth nudged up in the third quarter, the government confirmed on Friday. Gross domestic product increased at a 2.1 percent annualized rate, the Commerce Department said in its third estimate of third-quarter GDP. The economy grew at a 2.0 percent pace in the prior quarter.

- The University of Michigan said the final reading of its consumer sentiment index in December was 99.3, up from 96.2 in the prior month. Consumers’ assessment of current conditions rose to 115.5 in the final December reading from 111.6 in the prior month, and the index of consumer expectations rose to 88.9 from 87.3. Most of the December gain was among upper-income households as a healthy job market and the rising stock market are bolstering consumer confidence.

- After reporting a slight uptick in U.S. personal income in the previous month, the Commerce Department released a report on Friday showing a notable acceleration in the pace of income growth in the month of November. The report said personal income climbed by 0.5 percent in November after inching up by a revised 0.1 percent in October.

Weaknesses

- According to the National Association of Realtors (NAR), existing home sales were down again in November, dropping 1.7 percent over the month and 2.7 percent from one year prior. NAR is calling it “a small step back.” Regionally, November’s existing home sales rose in the Midwest (2.3 percent) and Northeast (1.4 percent), but fell in the South (-3.9 percent) and West (-3.5 percent).

- The December Manufacturing PMI reading fell short of market expectation. The Manufacturing PMI ticked down to 52.5 in December’s preliminary reading from 52.6 in November and below the market expectation of 52.5.

- The Philadelphia Fed Manufacturing Business Outlook Survey fell more than expected in December, hanging just above expansion territory at 0.3. The consensus forecast for the regional factory activity survey was 8.5.

Opportunities

- In the U.S., the most important data release next week will be durable goods orders for November, due on Tuesday. This data set is seen as a proxy for business investment. Forecasts suggest that the headline rate picked up to 1.9 percent on a monthly basis, from 0.5 percent in October.

- MNI’s regional Chicago Purchasing Managers’ Index will be released next week, with the report of increasing interest going forwards in the wake of Boeing’s recent troubles.

- A closely watched section of the Treasury yield curve — the spread between the three-month bill and 10-year note — may be on track to close out 2019 above where it began. After the Federal Reserve’s series of quarter-point rate cuts, followed by a hold in its final meeting of the year, Chairman Jerome Powell told reporters that “both the economy and monetary policy right now are in a good place.”

Threats

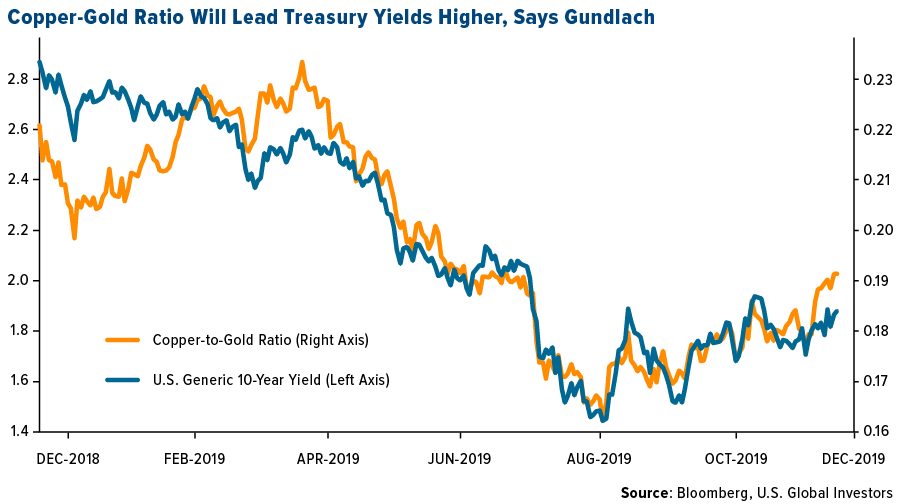

- Copper is clawing back ground lost to gold, paving the way for Treasury yields to follow. The copper-to-gold relationship, known as the Gundlach Ratio, has bottomed out with the U.S.-China phase-one trade deal set to be signed.

- European growth may be bottoming, as ECB President Lagarde hinted recently, but it’s stabilizing at a very low level. Unless euro area governments launch a substantial fiscal spending package to boost growth, there’s little prospect for a real rebound in the Eurozone.

- Investors will be monitoring events on the Korean peninsula ahead of Pyongyang’s self-chosen year-end deadline for the international community to unilaterally relax its economic sanctions against it.

Energy and Natural Resources Market

Strengths

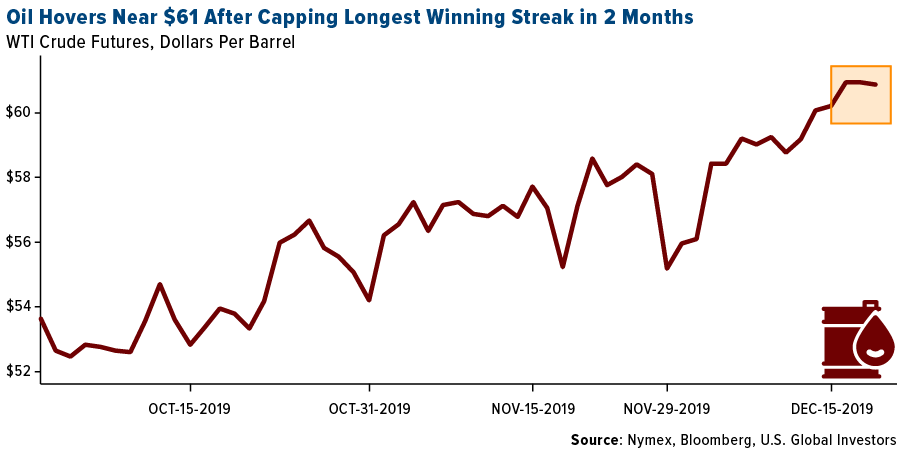

- The best performing major commodity for the week was zinc, which gained 3.35 percent as base metals experienced gains. Copper saw a fifth weekly gain on strengthening global trade sentiment. Even as Chinese President Xi Jinping was reported to be skipping next month’s Davos summit, it wasn’t enough to diminish positive sentiment and falling stockpiles of the metal. Oil also saw a third weekly gain on U.S.-China trade optimism. Bloomberg reports that oil steadied near $61 per barrel after hitting its highest in more than three months on Thursday.

- WPX Energy Inc. is buying rival oil producer Felix Energy for $2.5 billion in cash and stock to expand in the Permian Basin, reports Bloomberg News. WPX said in a statement that Felix has 1,500 undeveloped locations in the eastern portion of the Delaware Basin.

- BP has formed a consortium with users and makers of packaging to speed up the commercialization of methods to turn difficult-to-recycle plastic waste into components that are easy to reuse. Bloomberg reports that BP is just the latest oil giant to announce efforts to improve recycling technology, following Total SA who announced last week it would develop a nascent chemical recycling industry in France. BP says that only 12 percent of plastic bottles collected globally become new bottles again, even though more than 75 percent are recycled.

Weaknesses

- The worst performing major commodity for the week was iron ore, which fell 1.84 percent. Iron ore futures fell 2.4 percent on Friday morning in Singapore, back to the $80s per ton. The Australian government warned that iron prices will average $63 per ton next year as global mine output will rebound following disruptions in Brazil early this year. Bloomberg reports that the decline won’t be immediate, but there will be a significant retreat over the full course of 2020 due to a slowdown in Chinese steel production.

- U.S. coal companies are trimming dividends and share buybacks as cash flow dries up, after paying outsized returns for investors for the past two years. Bloomberg reports prices for coal used to make steel are down 30 percent since May and that coal producers’ share prices have taken a hit. Peabody, the largest domestic coal producer, is down 68 percent this year, but still paid out its biggest dividend ever in March. Daniel Scott, analyst at Clarksons Platou Securities, said “the reality is, met coal down 30 percent this year has hamstrung all companies’ ability to return cash to shareholders.”

- Using data from satellites, a team of American and Dutch scientists found that an Exxon Mobile Corp. natural gas well in Ohio emitted more methane into the air during a blowout in 2018 than most countries do in an entire year, reports Bloomberg News. Methane was leaked into the atmosphere at a rate of 80 tons per hour and lasted for almost 20 days.

Opportunities

- Mining companies in the Democratic Republic of Congo rely on diesel generators to offset a shortage of electricity. Bloomberg reports that a joint venture between two Italian-owned firms and the government plans to spend as much as $420 million to overhaul the nation’s fuel-distribution network to reduce gasoline prices, which are among the highest in Africa. The new investments would modernize the infrastructure used to import, store and distribute refined petroleum products, including building a pipeline from the Congo-Zambia border to the mining hub of Lubumbashi.

- BloombergNEF reports that around 75 percent of the 5.9 gigawatts of clean energy purchased by mining companies since 2008 have come online in the last two years. The exponential growth is largely driven by massive power purchase agreements signed by mines in Chile. Top global buyers include BHP Group, Anglo American Plc and Antofagasta. Further research by BloombergNEF found that mining companies can save up to 25 percent of their total electricity costs and can remove up to 50 percent of electricity-related emissions by installing solar, wind and batteries at their mine sites.

- Wind and solar farms are putting European nuclear plants out of work. Bloomberg reports that Vattenfall AB, the Nordic region’s biggest utility, made the decision not to invest to keep the 44-year old Ringhals-2 reactor going because it has struggled to break even. The reactor will close at the end of December, which has long served Sweden and Germany. Germany is also closing a major reactor, which had helped power the car industry’s mega-automobile plants since the mid-1980’s, due to the country’s push for renewables.

Threats

- Bloomberg reports that U.S. Steel Corp. has announced a slate of bad news: a warning of a fourth-quarter loss, the shuttering of its Great Lakes Works near Detroit, laying off more than 1,500 workers and cutting its dividend. The company’s shares fell as much as 9.5 percent in pre-market trading Friday morning. Analysts including Martin Englert wrote in a note that the loss “likely surprises most investors” but the “proactive move to permanently idle Great Lakes Works is laudable.”

- The International Energy Agency (IEA) wrote in its annual coal report that although coal use dipped in 2019, it expects to see a rise in use in the next five years due to electricity demand in developing countries. IEA wrote “there are few signs of change.” Demand for coal is driven by India, China and Southeast Asia. Bloomberg reports that China’s coal output hit a record of 334.06 million tons in November, which is up 4.5 percent from a year ago.

- A severe drought continues to leave several African countries in the dark. Bloomberg reports that turbines at Kariba, the world’s biggest man-made reservoir, could be forced to shut completely due to low water levels. The dam powers most of Zambia and Zimbabwe and has forced rolling electricity blackouts lasting 18 hours a day. Both countries are facing debt crises that could make it difficult to borrow money to pay for new plants and production capacity.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 1.4 percent. The central bank left its main rate unchanged at 2 percent despite inflation spiking above the bank’s tolerance band. Shares of Erste Group Bank, an Austrian bank trading on the Prague exchange, gained 4.9 percent in the past five days. Erste Bank, among four other banks, may be bidding for Poland’s mBank. The acquisition would potentially raise Erste Group’s number of customers by 30 percent, increase the loan book size by almost 16 percent and secure more than 9 percent market share of the Polish market, according to PKO BP Securities research.

- The Russian ruble was the best performing currency this week, gaining 80 basis points. The ruble moved higher with the price of crude oil, which gained 1.2 percent, closing at $66.03 per barrel on Friday. As expected, Russia’s central bank cut its main rate by 25 basis points to 6.25 percent.

- Healthcare was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 30 basis points. December economic and business confidence both dropped and the current account deficit balance widened by more than expected due to a rise in imports related to investments. Shares of OTP Bank, Hungary’s biggest lender, fell 2.6 percent in the past five days. OTP Bank is planning to exit the Slovak market, but it is still willing to expand across Eastern Europe when the right opportunity comes.

- The Turkish lira was the worst performing currency in the region this week, losing 2.2 percent. The U.S. Senate passed a highly expected defense bill, which includes measures against Turkey for buying S-400 missiles from Russia and military action in northern Syria.

- Industrial was the worst performing sector among eastern European markets this week.

Opportunities

- OPEC expects Russia’s oil output to grow next year despite the country’s pledge to make deeper cuts. They forecast an increase of 0.61 percent next year to 11.5 million barrels a day, compared to 2019 when output is expected to grow 0.73 percent from last year. Stronger oil production will benefit Russia’s revenue, which mostly comes from the sale of oil and gas.

- The Eurozone Composite PMI, which combines service and manufacturing activity, stayed above the 50 level that separates growth from contraction. The manufacturing PMIs in Germany, France and Great Britain corrected, however, the service sector once again saved the composite PMI from falling below the 50 level. Many economists believe that PMIs are bottoming in Europe and they will rebound next year. Investors are becoming more positive as the threat of UK leaving without a deal declined significantly and ECB President Christine Lagarde committed to stick with a dovish bias for now.

- Reuters interviewed Greek Finance Minister Staikouras, who said Greece is considering repaying more IMF loans ahead of time next year to offload expensive debt and wants to convince its official lenders to lower its post-bailout fiscal targets. Staikouras wants Greece to pay up to a certain amount that would allow the IMF to keep its presence until the end of the post-program surveillance period.

Threats

- Poland’s Supreme Court is pushing forward with judicial reforms and working on a disciplinary proposal for judges. In the new legislation, Law & Justice, the ruling party, wants to introduce disciplinary penalties for judges, including dismissals for questioning the legality of judicial appointments. The Court of Justice of the European Union (ECJ) found that the National Council of the Judiciary (NCJ) – the body that recommends the judges for a presidential appointment is not independent. This bill sparked protests throughout Poland.

- The threat of a no-deal Brexit was revived this week. Prime Minister Boris Johnson wants to fix a hard deadline of December 2020 to reach a trade deal with the European Union. It may be impossible to complete a trade deal in a year. It took more than 3 years for the U.K. and EU to agree that the withdrawal will happen, but the hard Brexit outcome is not completely out of the picture yet.

- U.S. lawmakers advanced new sanctions against Russia this week. If both Congress and the Senate approve the bill, President Trump will be forced to introduce at least part of the measures, from sanctions against Russian government debt and energy projects to a freezing of correspondent accounts of state banks.

China Region

Strengths

- The best performing country in the region for the week was Malaysia, where the FTSE Bursa Malaysia Kuala Lumpur Composite Index rose 2.48 percent over the last five trading days.

- Energy was the top performing sector in Hong Kong’s Hang Seng Composite Index for the week, climbing 3.20 percent.

- China’s industrial production and retail sales numbers both beat for the November measurement period. Production clocked in at 6.2 percent year-over-year growth, well ahead of expectations for a 5.0 percent print, while retail sales showed up at an 8.0 percent year-over-year growth rate, ahead of analyst consensus for a 7.6 percent pace. Retail sales were likely helped out by Alibaba’s record Singles Day sales.

Weaknesses

- The worst performing countries in the region were the Philippines and Vietnam, which fell by 1.27 and 0.96 percent, respectively.

- Materials constituted the poorest-performing sector in the HSCI on the week, falling 1.14 percent.

- Indonesia’s exports number missed expectations for November, declining at a year-over-year pace of 5.67 percent, worse than analyst consensus for an only 2.80 percent decline. Imports also declined year over year, but did come in slightly better than expected.

Weaknesses

- The Phase One market honeymoon continued this week, with a yet-to-be-specified date for bilateral signing of the 86-page agreement reportedly sometime in January. President Trump tweeted on Friday that he “[h]ad a very good talk with President Xi of China concerning our giant Trade Deal. China has already started large scale purcha[s]es of agricultural product & more. Formal signing being arranged.” U.S. trade representative Robert Lighthizer said that he expects the trade deal will go into effect 30 days after signing.

- Bloomberg News reported that JPMorgan Chase & Co. was approved for a securities business license by Chinese regulators, which clears another hurdle for the U.S. bank to expand in the world’s second-biggest economy as it opens its $40 trillion financial market.

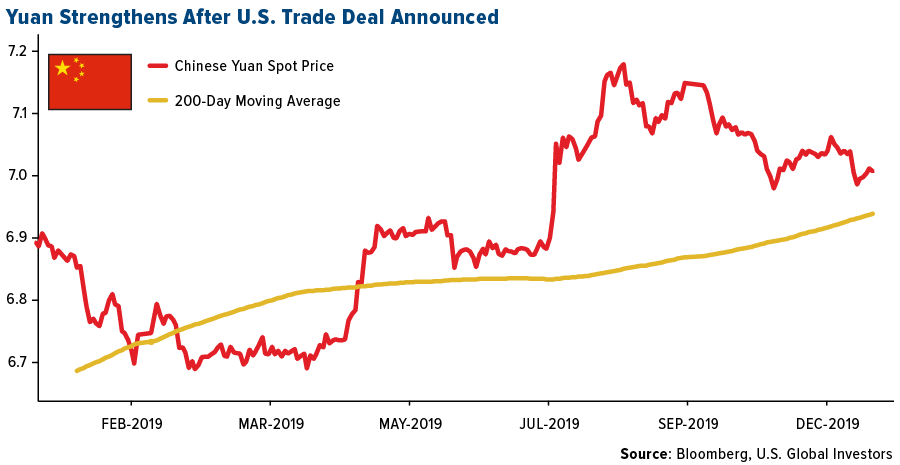

- The Chinese yuan, which strengthened post-trade deal announcement even as the U.S. dollar weakened (demonstrating some tangible gains for the U.S., which seeks to export more, and perhaps vice versa for China), has stayed at or near the round big figure of 7, indicative of some substance and reality to the new trade deal. U.S. officials will surely be watching the yuan…

Threats

- The upside of a trade deal is obvious. But here’s a possible complicating effect of Hong Kong’s continued protests amid a trade deal: media reported this week that authorities in Beijing may also consider rerouting trade now sent via Hong Kong—which is of course a separate customs territory from the mainland—to mainland ports as part of a step-up in U.S. purchases. Beijing is reportedly concerned about the effects to Hong Kong’s already-suffering economy.

- Bloomberg noted this week that China threatened to retaliate if Germany moved to ban Huawei as a 5G supplier. Beijing "will not stand idly by," Handelsblatt quoted Ambassador Wu Ken as saying, and noting the millions of German cars sold in China. 5G supplier issues remains a point of contention around the world, with the U.S. continuing to press its case among allies for banning the Chinese technology infrastructure on security concerns.

- And speaking of security concerns, here’s something to think about: The New York Times had a concerning piece this week on the unchecked scope and pace of Chinese domestic spying. A sample: “China is ramping up its ability to spy on its nearly 1.4 billion people to new and disturbing levels, giving the world a blueprint for how to build a digital totalitarian state. Chinese authorities are knitting together old and state-of-the-art technologies — phone scanners, facial-recognition cameras, face and fingerprint databases and many others — into sweeping tools for authoritarian control, according to police and private databases examined by The New York Times.” The basic idea is a massive cross-referencing system combining all available data and building a large-scale, big-data, real-time spying network for keeping tabs on all the citizens of (as the authors observe) China’s “digital totalitarian state.” RIP, privacy…

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended December 20 was HTMLCOIN, up 250.94 percent.

- According to CoinDesk’s Bitcoin Price Index, the largest cryptocurrency by market value is currently reporting triple-digit gains since the 2018 bear market bottomed out exactly a year ago. It is currently priced around $7,050, which is a 127 percent rise from the low of $3,122 on December 15, 2018, the article explains.

- Coinbase CEO Brian Armstrong was granted a U.S. patent this week for an invention that makes sending and receiving bitcoin as easy as email, according to CoinDesk. The patent “details a system for users to make cryptocurrency payments with email addresses linked to corresponding wallet addresses,” CoinDesk’s Paddy Baker writes. “The sender makes a request to send cryptocurrency to an email address, and the system automatically transmits the agreed amount—so long as they have the required balance—from the sender’s wallet to the wallet corresponding to the receiver’s email address.” What’s more, the proposed email system will not charge users fees of any kind.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended December 20 was Tratok, down 33.23 percent.

- Yang Zuoxing, a Chinese chip designer who helped Bitmain Technologies become the world’s largest maker of bitcoin mining rigs, has been arrested according to people familiar with the matter. A December 12 statement notes that he was arrested on suspicion of embezzlement. As Bloomberg explains, Yang started his own crypto mining company called MicroBTa month after quitting Bitmain. It has grown into a “serious contender” to Bitmain, clawing market share away with its Whatsminer equipment.

- The U.K.’s longest-running crypto exchange, Coinfloor, will be delisting Ethereum next month, along with bitcoin cash, writes CoinDesk. The company cites an unclear future of hard forks along with the need for onerous technical support for the second-biggest coin by market capitalization.

Opportunities

- The accountancy giant Ernst and Young (EY) has made its token and smart contract review service available for public testing, writes CoinDesk. The public beta version, launched on Wednesday, lets users paste code for analysis, during which it identifies security risks “by testing the functionality and efficiency of a smart contract, as well as evaluating the quality of the coding,” the article continues.

- Hong-Kong based venture capital firm CMCC Global has hired a new partner from one of the largest blockchain companies in China. As reported by CoinDesk, Zhao Chen from Neo Global Development will open an office in Shanghai to lead on equity investments in mainland China blockchain firms. “The creation of a presence in Shanghai demonstrates our commitment towards discovering and supporting the leading blockchain teams globally,” CMCC’s CEO Martin Baumann said in a statement.

- On Wednesday, the U.S. Securities and Exchange Commission issued a press release with intentions to add a list of new qualifications to become an accredited investor. Under the amendment, the term “accredited investor” would expand to include new categories of “natural persons,” individuals who qualify as “knowledgeable employees” of certain private funds, companies which meet certain restrictions, entities who “own ‘investments’” defined under the Investment Company Act, family offices with a minimum of $5 million in assets, and spousal equivalents who can pool finances to qulify, explains CoinDesk.

Threats

- According to researcher Chainalysis Inc., bitcoin might have a tough time getting out from under the fallout from one of the biggest crypto scams ever. As perpetrators of the estimated more than $2 billion PlusToken scandal dump coins to cash out, Bloomberg writes that the popular digital currency is likely to remain under pressure. In fact, bitcoin is down 50 percent from its 2019 peak after Chinese authorities arrested multiple suspects in the pyramid scheme that promised investors returns as high as 600 percent.

- In a ruling issued September 27, but published just last week, a district court in Shenzhen, China, ordered the freezing of almost $680,000 in assets belonging to a fully-owned subsidiary of bitcoin mining giant Bitmain. As reported by CoinDesk, the Shenzhen Bao’An District Court sided with a firm called Dongguan Yongjiang Electronics, granting an application for asset protection in a contract dispute with the defendant, Shenzhen Century Cloud Core.

- After the CEO of Quadriga CX, Gerald Cotton, died last year, with no access to crucial passwords, many users could not recover millions in their accounts. Now, according to Morning Consultant, they want proof that Mr. Cotton is even dead. According to the article, lawyers appointed by the Supreme Court of Nova Scotia to represent users, asked Canadian law enforcement to exhume his body and coduct an autopsy. The official letter cited “the questionable circumstances surrounding Mr. Cotton’s death and significant losses” suffered by his company’s investors.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.92 | +0.10 | +5.21% |

| Oil Futures | 60.33 | +0.26 | +0.43% |

| Hang Seng Composite Index | 3,783.22 | +32.53 | +0.87% |

| S&P Basic Materials | 382.07 | +4.51 | +1.19% |

| Korean KOSPI Index | 2,204.18 | +33.93 | +1.56% |

| S&P Energy | 452.48 | +11.13 | +2.52% |

| Nasdaq | 8,924.96 | +190.08 | +2.18% |

| DJIA | 28,455.09 | +319.71 | +1.14% |

| Russell 2000 | 1,671.89 | +33.92 | +2.07% |

| S&P 500 | 3,221.23 | +52.43 | +1.65% |

| Gold Futures | 1,481.70 | +0.50 | +0.03% |

| XAU | 97.56 | -2.72 | -2.71% |

| S&P/TSX VENTURE COMP IDX | 548.84 | +8.31 | +1.54% |

| S&P/TSX Global Gold Index | 244.45 | -6.95 | -2.76% |

| Natural Gas Futures | 2.33 | +0.04 | +1.57% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,204.18 | +78.86 | +3.71% |

| 10-Yr Treasury Bond | 1.92 | +0.17 | +9.79% |

| Gold Futures | 1,481.70 | +0.70 | +0.05% |

| S&P Basic Materials | 382.07 | +10.26 | +2.76% |

| S&P 500 | 3,221.23 | +112.77 | +3.63% |

| DJIA | 28,455.09 | +634.00 | +2.28% |

| Nasdaq | 8,924.96 | +398.22 | +4.67% |

| Oil Futures | 60.33 | +3.22 | +5.64% |

| Hang Seng Composite Index | 3,783.22 | +135.67 | +3.72% |

| S&P/TSX Global Gold Index | 244.45 | -2.38 | -0.96% |

| XAU | 97.56 | +1.89 | +1.98% |

| Russell 2000 | 1,671.89 | +80.28 | +5.04% |

| S&P Energy | 452.48 | +19.87 | +4.59% |

| S&P/TSX VENTURE COMP IDX | 548.84 | +24.70 | +4.71% |

| Natural Gas Futures | 2.33 | -0.23 | -8.87% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 97.56 | +4.57 | +4.91% |

| S&P/TSX Global Gold Index | 244.45 | -2.03 | -0.82% |

| Gold Futures | 1,481.70 | -30.80 | -2.04% |

| DJIA | 28,455.09 | +1,360.30 | +5.02% |

| S&P 500 | 3,221.23 | +214.44 | +7.13% |

| Nasdaq | 8,924.96 | +742.08 | +9.07% |

| Korean KOSPI Index | 2,204.18 | +123.83 | +5.95% |

| Natural Gas Futures | 2.33 | -0.21 | -8.12% |

| S&P Basic Materials | 382.07 | +15.35 | +4.19% |

| Russell 2000 | 1,671.89 | +110.42 | +7.07% |

| Oil Futures | 60.33 | +2.20 | +3.78% |

| Hang Seng Composite Index | 3,783.22 | +211.04 | +5.91% |

| S&P/TSX VENTURE COMP IDX | 548.84 | -35.38 | -6.06% |

| S&P Energy | 452.48 | +0.59 | +0.13% |

| 10-Yr Treasury Bond | 1.92 | +0.13 | +7.39% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Alamos Gold Inc

Anglo American Plc

Harmony Gold Mining Co Ltd

Leagold Mining Corp

Agnico Eagle Mines Ltd

Barrick Gold Corp

Centamin Plc

BHP Group Ltd

OTP Bank

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The Philadelphia Federal Index is a regional federal-reserve-bank index measuring changes in business growth. The index is constructed from a survey of participants who voluntarily answer questions regarding the direction of change in their overall business activities. The survey is a measure of regional manufacturing growth. When the index is above 0 it indicates factory-sector growth, and when below 0 indicates contraction. Also known as the "Business Outlook Survey". The FTSE Bursa Malaysia KLCI Index comprises of the largest 30 companies by full market capitalization on Bursa Malaysia’s Main Board.