The Urban-to-Suburban Exodus May Be the Biggest in 50 Years

Date Posted: September 18, 2020

Read time: 47 min

In the past three or four months, you may have noticed a plethora of headlines proclaiming the "death" of big U.S. cities such as New York, Chicago and Seattle. To paraphrase Mark Twain, these reports may be greatly exaggerated. However, there's no denying that many urban city-dwellers--a great number of them high-income--are either relocating into the suburbs or strongly considering it, due to the double-whammy of the coronavirus and historic social unrest.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

In the past three or four months, you may have noticed a plethora of headlines proclaiming the “death” of big U.S. cities such as New York, Chicago and Seattle. To paraphrase Mark Twain, these reports may be greatly exaggerated. However, there’s no denying that many urban city-dwellers—a great number of them high-income—are either relocating into the suburbs or strongly considering it, due to the double-whammy of the coronavirus and historic social unrest.

This latent “exodus,” as some are already calling it, may end up being among the biggest in U.S. history, or at least the biggest since the “white flight” of the 1950s and 60s. According to real estate brokerage firm Redfin, a record 27.4 percent of homebuyers sought to move out of their metro areas in the second quarter, with New York City, San Francisco, Los Angeles and Washington, D.C., seeing the highest net outflows.

The implications of this exodus will be felt not just by apartment tenants and city managers but also, potentially, municipal bond investors. The COVID-19 pandemic has led to an enormous loss of tax revenue for cities and states, and combined with the monumental cost of repairing damages sustained during summer-month riots, municipalities could be facing a $1 trillion budget shortfall. (I’ll have more to say on muni bonds later.)

Costliest Demonstrations in U.S. History

It’s now being estimated that the nationwide protests and riots that were sparked by the May 25 death of George Floyd in Minneapolis, Minnesota, may collectively be the costliest in U.S. history. According to Axios’ reporting of data compiled by Property Claim Services (PCS), the demonstrations across 20 states will cost the insurance industry between $1 billion and $2 billion. Adjusted for inflation, that may be an even greater cost than the demonstrations that took place in Los Angeles following the 1992 acquittal of police officers involved in the Rodney King case.

| Dates | Location | Dollars | 2020 Dollars | ||

|---|---|---|---|---|---|

| May 26 – June 8, 2020 | 20 States Across U.S. | $1-2B | $1-2B | ||

| Apr. 29 – May 4, 1992 | Los Angeles, CA | $775m | $1.42B | ||

| Aug. 11-17, 1965 | Los Angeles, CA | $44M | $357M | ||

| Jul. 23, 1967 | Detroit, MI | $42M | $322M | ||

| May 17-19, 1980 | Miami, Fl | $65M | $204M | ||

| Apr. 4-9, 1968 | Washington, DC | $24M | $179M | ||

| Jul. 13-14, 1977 | New York, NY | $28M | $118M | ||

| Jul. 12. 1967 | Newark, NJ | $15M | $115M | ||

| Apr. 6-9, 1968 | Baltimore, MD | $14M | $104M | ||

| Apr. 4-11, 1968 | Chicago, IL | $13M | $97M | ||

| Source: Axios, Property Claim Services (PCS), U.S. Global Investors | |||||

In Minneapolis and St. Paul, where this year’s riots began, as many as 1,500 businesses were heavily damaged, and demolition costs have skyrocketed so incredibly high that large sections of the Twin Cities are left with “scorched buildings and piles of rubble that will linger for months,” according to Minnesota’s Star Tribune.

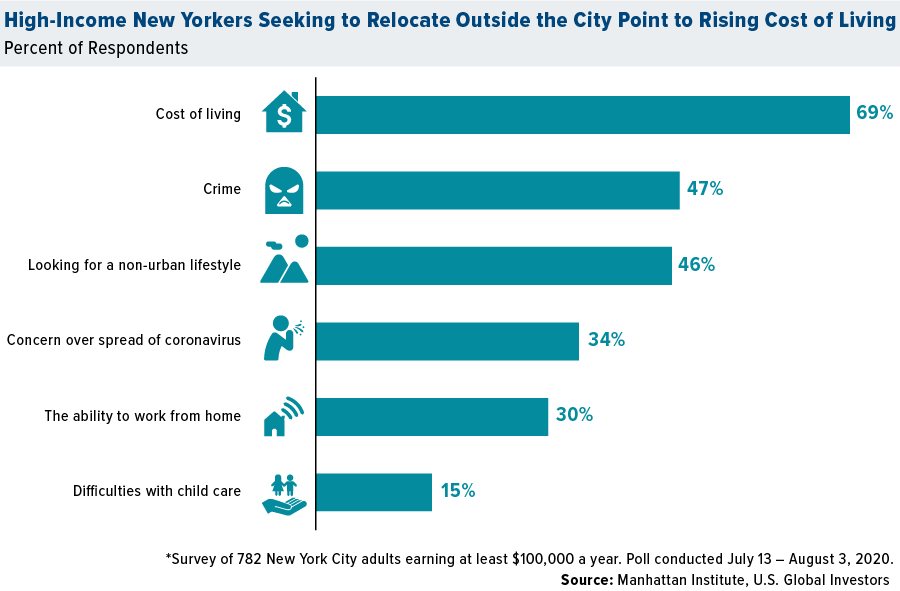

Violence and crime are top of mind among many people looking to move out of cities. The free-market think tank Manhattan Institute found that nearly half of high-income New Yorkers who were seeking to relocate cited crime as a contributing factor. At 47 percent, that was the number two reason for moving, number one being cost of living (69 percent).

The number of empty Manhattan apartments rose to a record 15,025 in August, up more than 166 percent from the same month in 2019, according to the Elliman Report. This brought the borough’s vacancy rate up to 5.1 percent, the highest in the report’s 14-year history. Movers in New York City are reportedly so busy right now, they’re having to turn people away.

Respondents to the Manhattan Institute’s survey aren’t overreacting over crime. Gun-related homicides across the U.S. are on track to be the worst since 1999. This past July was Chicago’s deadliest month in 28 years.

Money Flows Where It’s Respected Most

They aren’t overreacting over the rising cost of living either. Legislatures in certain cities and states have lately approved tax policies that are near guaranteed to drive many of the highest earners and businesses away.

This week, New Jersey lawmakers agreed on a budget deal that will raise incomes taxes from 8.97 percent to 10.75 percent for tens of thousands of residents earning over $1 million.

Meanwhile, Seattle businesses, including Amazon, continue to urge the city council to repeal a payroll tax that is set to levy payrolls of those making at least $150,000 a year. The “Amazon tax,” as it’s called, is just one of many reasons why the retail giant is rumored to be considering moving operations elsewhere.

As I’ve often said, money flows where it’s respected most, and the survey above is proof positive of that.

Housing Market White Hot After Labor Day

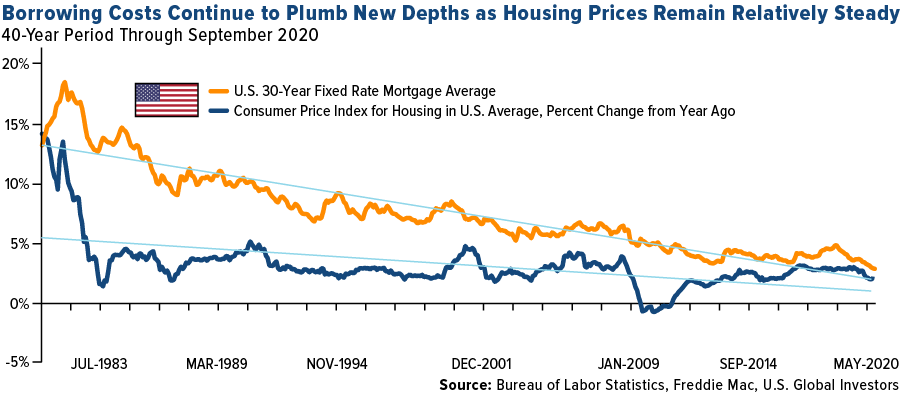

So where is the money flowing instead? Again, homes in the nation’s suburbs are seeing incredible demand right now, which is leading to an inventory shortage and pushing up home values. It doesn’t hurt that 30-year mortgage rates remain near record lows and, the past few months notwithstanding, prices have been rising relatively in line with consumer prices.

Median home sale prices climbed to $319,261 in the four weeks ended September 13, a 13 percent increase from the same period a year earlier. That’s the biggest such increase since October 2013, according to Redfin. Nearly half of all homes that went on the market had an accepted offer within the first two weeks, the highest level since 2012.

In the Hamptons, traditionally a weekend or summer destination for New Yorkers, new signed contracts for single-family homes more than doubled in August from a year ago.

We Practice Caution as Muni Investors

Back to municipal bonds. August was a challenging month for fixed-income markets, including the $3.9 trillion muni market. Although the Municipal Bond Index fell 0.47 percent in August, munis still outpaced both corporate bonds and Treasuries for the month.

It’s key that muni investors practice caution at this time. According to RBC Wealth Management, the pandemic “is beginning to pressure the ratings of many municipal issuers, and we expect this trend to continue through the remainder of” September.

So far, none of the major cities that have seen the most negative news coverage at this time—Seattle, Portland, Chicago, New York City—have seen their credit downgraded, but that could change.

For what it’s worth, we have no exposure to Seattle’s or Portland, Oregon’s debt, and given the current risks, I don’t see that changing in the near future.

Our YouTube channel is growing! We’ve been working hard to bring you timely and insightful videos on financial markets, including gold and precious metals, commodities, energy and more. If you haven’t already done so, follow the link below to subscribe to our YouTube Channel today!

SUBSCRIBE TO U.S. GLOBAL INVESTORS

Gold Market

This week spot gold closed at $1,950.86, up $10.31 per ounce, or 0.53 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.76 percent. The S&P/TSX Venture Index came in up 1.64 percent. The U.S. Trade-Weighted Dollar fell 0.37 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-14 | China Retail Sales YoY | 0.0% | 0.5% | -1.1% |

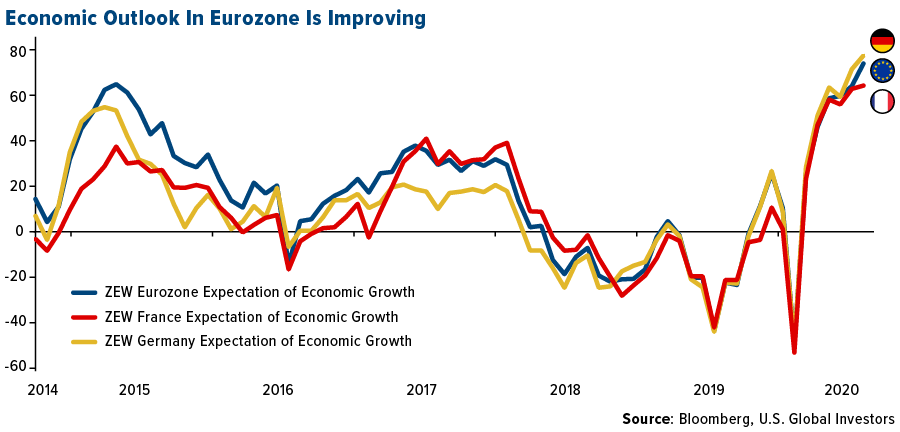

| Sep-15 | Germany ZEW Survey Expectations | 69.5 | 77.4 | 71.5 |

| Sep-15 | Germany ZEW Survey Current Situation | -72.0 | -66.2 | -81.3 |

| Sep-16 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Sep-17 | Eurozone CPI Core YoY | 0.4% | 0.4% | 0.4% |

| Sep-17 | Initial Jobless Claims | 850k | 860k | 893k |

| Sep-17 | Housing Starts | 1488k | 1416k | 1492k |

| Sep-24 | Hong Kong Exports YoY | -3.0% | — | -3.0% |

| Sep-24 | Initial Jobless Claims | 845k | — | 860k |

| Sep-24 | New Home Sales | 891k | — | 901k |

| Sep-25 | Durable Goods Orders | 1.4% | — | 11.4% |

Strengths

- The best performing precious metal for the week was palladium, up 1.57 percent as hedge funds boosted their net-long position to the highest in six-months. Gold had a second weekly gain after the U.S. dollar steadied and investors weighed a growing number of coronavirus cases.

- Platinum exports from Switzerland remained at elevated levels in August. According to data from the Swiss Federal Customs Administration, supplies of platinum hit 6.7 tons last month, up 40 percent from the previous month. Gold shipments from Switzerland resumed last month to China after a five-month break. China’s gold demand is showing signs of recovery after importing 10 tons in August.

- As the Turkish lira remains weak, Turks are piling into gold despite record high local prices. The average daily volume of gold sold at the Grand Bazaar was 4,500 pounds, up from 450 pounds. Ozgur Anik, general manager of Ozak Precious Metals AS, says “when gold prices are at record high, people normally sell their gold. This time, they kept buying more.”

Weaknesses

- The worst performing precious metal for the week was platinum, still up by just 0.04 percent, but posted its biggest drop this month on Thursday with weaker auto sales in Europe where diesel is a bigger percentage of the market. Gold slipped after investors weighed the Fed’s outlook for a shallower contraction of 3.7 percent, up from June estimates of a 6.5 contraction. The FOMC expects to maintain an accommodative stance of money policy until it achieves inflation averaging 2 percent.

- The world’s biggest gold ETF, the $79 billion SPDR Gold Shares, saw a third straight week of outflows after eight consecutive months of inflows. This is a sign of profit-taking. On the other hand, the iShares Gold Trust continued its inflow streak of 25 weeks.

- Former Deutsche Bank AG analyst David Liew told a Chicago jury that he learned how to manipulate precious metal prices, of the practice of spoofing, from two senior traders, writes Bloomberg News. Spoofing is when traders place buy and sell orders they never intended to execute in a strategy to influence prices for illegal profits. Liew, who is pleading guilty and aiding the prosecution, said he knew manipulation was wrong, but the spoofing trades were “so commonplace” among co-workers that he thought it was okay to do.

Opportunities

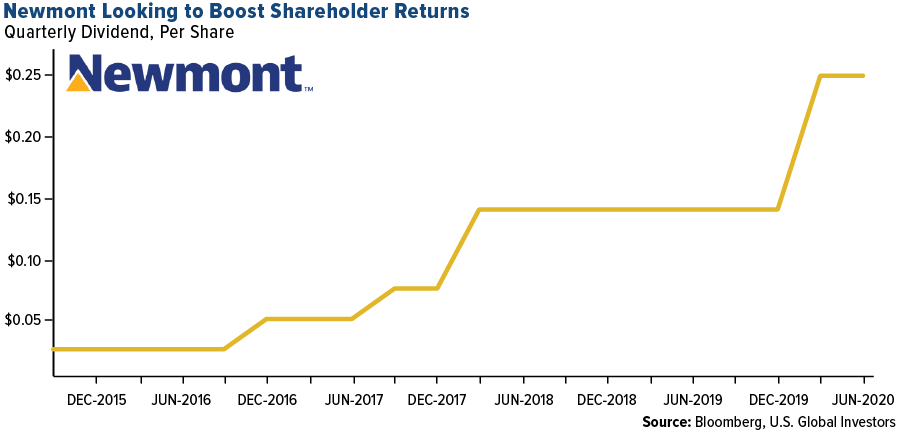

- Kinross Gold, a Canadian miner, is paying its first dividend in seven years after boosting output and seeing record high gold prices. Shareholders will receive 3 cents a common share and resume quarterly dividends of the same amount. The company said production is expected to increase 20 percent by 2023. Newmont CEO Tom Palmer said he expects gold prices to remain elevated and boasted the company’s high dividend. “As we now look at the strength of our balance sheet, the discipline we have in running our business and our sustainable portfolio, we are actively debating and assessing opportunities for further shareholder returns.” Newmont increased its dividend by 79 percent earlier this year to $1 per share.

- Petra Diamonds found five blue diamonds, considered the most valuable in the world, at its flagship Cullinan mine in South Africa. The gems range in size from 9.6 carats to 25.8 carats. Bloomberg notes Petra sold a 20-carat blue diamond for almost $15 million last year. This is rare positive news for the struggling producer.

- Lundin Gold received an exploration permit for its Barbasco project in Ecuador. Kore Mining announcement a positive preliminary economic assessment for its Long Valle Gold Deposit in California. SSR Mining said it expects to see at least a 60 percent increase in gold production this year after its acquisition of Alacer Gold Corp.

Threats

- Russia is considering raising mineral-extraction taxes on mining companies to narrow a budget deficit of 4 percent of GDP, reports Bloomberg. The Finance Ministry proposed more than tripling taxes for extracting most metal and fertilizers for next year. This is a threat to Russian mining companies and would increase costs.

- B2Gold Corp is expanding its gold mining operations in Mali, even as the West African nation ousted its president last month – the second coup in less than 10 years. Mali’s gold mines have not been affected by the political turmoil, but it is still a threat to operation in the region. CEO Clive Johnson said in a phone interview with Bloomberg that “the current situation doesn’t deter us.”

- Equities and gold have benefitted from the trillions of dollars in fiscal spending and money printing, but those efforts are debasing the dollar and raising the possibility that the U.S. will go too far in testing the limits of government stimulus, says Ray Dalio in a Bloomberg TV interview. “There is so much debt production and debt monetization.” Again, this is positive for gold and Dalio recommends the metal, but it is a threat in the dollar losing its status as the world’s reserve currency.

September 17, 2020Got Gold? Bottom-Barrel Rates to Last for Years to Come |

September 14, 2020Ivanhoe Set to Begin Production at World’s Second-Largest Copper Project |

September 8, 2020Helium Is Soaring on Red-Hot Demand, Shrinking Supply |

|||

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.45 percent. The S&P 500 Stock Index fell 0.59 percent, while the Nasdaq Composite fell 1.16 percent. The Russell 2000 small capitalization index gained 1.93 percent this week.

- The Hang Seng Composite gained 2.25 percent this week; while Taiwan was up 1.45 and the KOSPI rose 0.66 percent.

- The 10-year Treasury bond yield rose 1 basis point to 0.695 percent.

Domestic Equity Market

Strengths

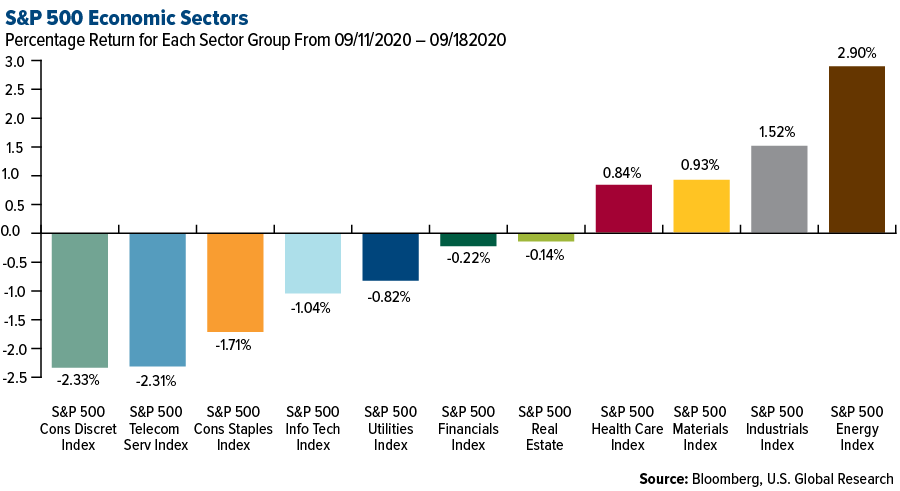

- Energy was the best performing sector of the week, increasing by 2.90 percent versus an overall decrease of 0.64 percent for the S&P 500.

- General Electric was the best performing S&P 500 stock for the week, increasing 15.63 percent.

- Buffett-backed cloud startup Snowflake raised a record-breaking $3.4 billion on Wednesday in the largest ever initial public offering (IPO) for a software company.

Weaknesses

- Consumer discretionary was the worst performing sector for the week, decreasing by 2.33 percent versus an overall decrease of 0.64 percent for the S&P 500.

- Illumina was the worst performing S&P 500 stock for the week, falling 15.55 percent.

- Technology shares pushed stocks to a six-week low as investors search for new catalysts to give direction to global markets. The S&P 500 fell for a third day on Friday, with losses accelerating after the benchmark fell below its 50-day moving average.

Opportunities

- Billionaire Richard Branson is set to raise $400 million for new SPAC as he looks to expand his Virgin empire.

- Tech tools developer JFrog leaped 62 percent after raising about half a billion in an upsized IPO.

- The pullback in the energy sector offers investors an opportunity to enter into oil services stocks they might have missed early in the year, Goldman Sachs analyst, Angie Sedita, said in a note on Wednesday.

Threats

- The Federal Trade Commission is reportedly working on an antitrust lawsuit against Facebook. The agency hasn’t decided yet whether to sue Facebook but is building its case as part of its year-long investigation into the company, according to the report.

- Goldman Sachs says stock volatility will likely increase in the next month driven by a seasonal pickup in investor uncertainty and recommends option buyers focus on stocks orsectors with “significant fundamental catalysts” instead of index option buying strategies for alpha.

- Barclays on Friday downgraded Apple, Microsoft and the FANG stocks to market weight, or neutral. In a note to clients, Barclays analysts said stock valuations are approaching extreme levels last seen during the dot-com bubble 20 years ago.

The Economy and Bond Market

Strengths

- The University of Michigan said the preliminary reading of its U.S. consumer sentiment index in September was 78.9, up from 74.1 in the prior month and the highest reading since March.

- The New York Fed’s Empire State business conditions index rose 13.3 points to 17 in September. The gain reverses a 14 point decline in August and is the third consecutive month of a positive reading.

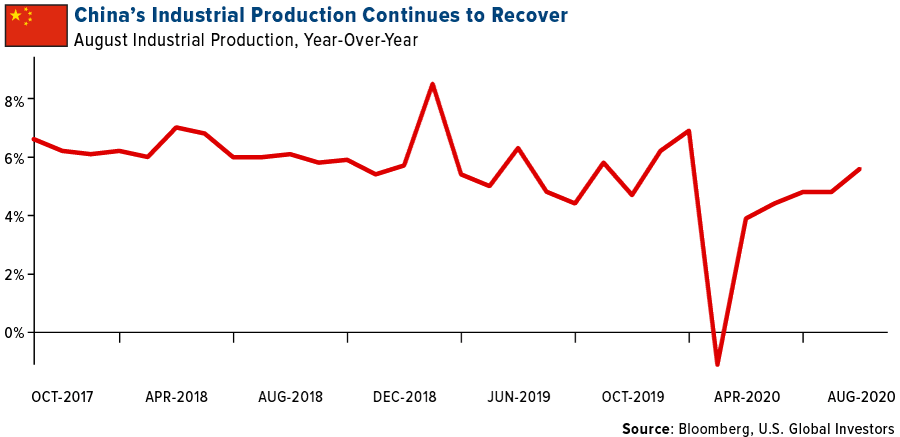

- Chinese retail sales rose for the first time this year in August, while industrial production increased for a fifth straight month, showing both consumers and producers in the world’s second largest economy are recovering from the pandemic.

Weaknesses

- The OECD warns the world economy will collapse by 4.5 percent this year – the worst slowdown since WWII.

- Consumer spending appeared to slow in August as extended unemployment benefits were cut for millions of Americans, offering more evidence that the economic recovery from the Covid-19 recession was faltering. Core retail sales, which correspond most closely with the consumer spending component of gross domestic product, fell 0.1 percent last month.

- The ranks of jobless Americans grew yet again last week, with 860,000 first-time unemployment benefits filed last week, rising slightly from the prior week’s level and reaffirming that a relatively robust recovery is losing momentum.

Opportunities

- The Federal Reserve’s so-called dot plot, which the central bank uses to signal its outlook for the path of interest rates, shows that officials expect no change in policy this year and borrowing costs near zero through 2023, based on median estimates. The Fed on Wednesday kept its benchmark rate on hold for a fourth straight meeting.

- The U.S. PMIs are released a few hours after the European figures next week and should they again show that the American economy outperformed the Eurozone’s, the dollar could see a boost.

- St. Louis Fed President James Bullard said the economy could grow 30 percent in the third quarter from its second-quarter depths, and inflation could soon pick up as the recovery gains ground.

Threats

- World Bank chief economist says full global recovery from the coronavirus crisis may take five years. "Everything depends" on when a vaccine gets approved and how long it would take for global access.

- Housing data will be watched next week as the boom in the interest-rate sensitive property sector has been one of the few bright spots in the economy during the pandemic. The latest dip in housing data this week has given investors some pause. Existing home sales are due on Tuesday, followed by new home sales on Thursday.

- Next Friday’s durable goods orders for August will be important as a gauge of the recovery’s momentum. The reading is expected to come in at growth of 1.2 percent, a slowdown from the prior 11.4 percent.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was crude palm oil, up 10.87 percent, on concern over lower supplies from Malaysia and steady demand from India and China. Copper hit a two-year high as the U.S. dollar remained lower – making commodities cheaper for other currency holders.

- BHP Group says it will benefit from a shift toward faster and more dramatic measures to address climate change. BHP plans to reduce greenhouse gas emissions by almost a third by 2030 and to zero by 2050. The miner will spend between $2 billion and $4 billion over the next decade on projects such as replacing diesel-fueled trucks and accelerating the development of carbon capture plants.

- RBC Capital Markets is bullish on Glencore’s turnaround. A management buyout at the commodity trader could deliver $15 billion in returns. Analysts including Tyler Broda write that Glencore has $38 billion of potential unrealized value after its underperformance. The company could generate 91 percent of its market cap in free cash flow over the next five years.

Weaknesses

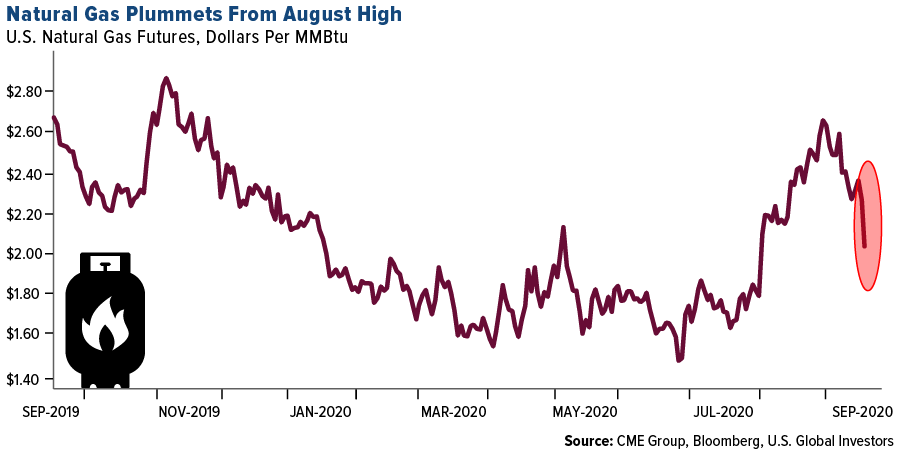

- The worst performing commodity for the week was coffee, down 13.43 percent on optimal weather conditions in Brazil that foreshadows ample supplies. Natural gas plummeted on Thursday after a massive stockpile gain was announced. Bloomberg reports that U.S. inventories of the fuel grew by 89 billion cubic feet last week, well above analyst expectations. Despite heat waves and hurricanes, stockpiles are still growing of the fuel.

- Crude stockpiles in the U.S. are at the lowest since April, but supplies of distillates, which include diesel, heating oil and jet fuel, are continuing to swell and hit the highest level for this time of year, reports Bloomberg. The diesel glut makes it difficult for companies to make money turning crude into gasoline and diesel. The diesel crack spread fell to $6.56 a barrel this week – the lowest since June 2010.

- Former Deutsche Bank AG analyst David Liew told a Chicago jury that he learned how to manipulate precious metal prices, or the practice of spoofing, from two senior traders, writes Bloomberg News. Spoofing is when traders place buy and sell orders they never intended to execute in a strategy to influence prices for illegal profits. Liew, who is pleading guilty and aiding the prosecution, said he knew manipulation was wrong, but the spoofing trades were “so commonplace” among co-workers that he thought it was okay to do.

Opportunities

- Former Goldman Sachs CEO Llyod Blankfein says now is a good time to invest in commodities. “From an inflation point of view, as an investor, I think investing in material sectors while they’re under-appreciated is not a bad thing now,” Blankfein said at the CME Group virtual metals briefing. Bloomberg notes that its commodity index is down almost 11 percent this year, compared with a 2.1 percent return for the MSCI World Index and 8.8 percent for iShares TIPS bond ETF.

- Amazon made the first five investments for its $2 billion climate fund: Rivian, Redwood Materials, CarbonCure Technologies, Pachama and Turntide Technologies. Matt Peterson, Amazon’s director of corporate development, said “each of these companies, from Amazon’s perspective, is a key piece of the puzzle that will help us decarbonize by the year 2040.”

- Petra Diamonds found five blue diamonds, considered the most valuable in the world, at its flagship Cullinan mine in South Africa. The gems range in size from 9.6 carats to 25.8 carats. Bloomberg notes Petra sold a 20-carat blue diamond for almost $15 million last year. This is rare positive news for the struggling producer.

Threats

- OPEC reduced its forecast for global oil demand for each quarter to the end of 2021 by an average of 768,000 barrels a day, as consumption is on track to fall by 9.46 million barrels a day this year. The group decided to ease production cuts in August, even as demand remains at historic lows. OPEC produced 760,000 barrels a day to global markets last month at the same time analysts were revising down demand for its crude by more than 1 million barrels a day.

- BP became the first oil supermajor to call for the end of oil’s growth era. According to a report released on Monday, BP said oil consumption may never return to levels seen before the coronavirus pandemic. Bloomberg notes BP has taken the boldest steps so far among peers to align its business with the goals of the Paris climate accord.

- Hitachi exited a long-planned Wylfa nuclear power project in Wales due to a worsening investment environment amid the coronavirus pandemic, despite a generous support package for an atomic station in Britain. The decision is a setback for the nuclear revival, which supporters promote as a carbon-free salutation for reliable power.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 1.4 percent. Despite the government announcement of the possible removal of tax breaks for Russian producers, stocks moved higher supported by stronger economic data. The central bank left its main rate unchanged at 4.25 percent. X5 Retail Group was the best equity trading among stocks in the VanEck Russia ETF (RSX), gaining 9.2 percent over the past five days. X5 was raised to “overweight” rating at JPMorgan.

- The Romanian leu was the best performing currency this week, gaining 5 basis points. The Bucharest Stock Exchange has been reclassified from Frontier to Secondary Emerging Market by FTSE Russell, three years after being added to the watch list. This is a historic moment for Romania and its capital market, as more investors will be able to enter.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 3.58 percent. The government will decide on the future of a loan moratorium on Saturday after allowing borrowers to suspend repayments until the end of this year. Shares of Hungary’s largest bank, OTP Bank, continued to sell off. Budapest Real Estate Company, a developer that is not very liquid, was the worst performing equity trading on the Budapest Stock Exchange, losing 19.7 percent over the past five days. Shares fell sharply on news of exclusion from Budapest’s main benchmark and the addition to Austria’s CECE Composite Index.

- The Turkish lira was the worst performing currency in the region this week, losing 1.35 percent. The lira fell to another record low despite local state banks selling dollars to support the domestic currency. The central bank will meet next week and most Bloomberg economists predict the main rate to be unchanged at 8.25 percent.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- The September reading of the eurozone’s ZEW survey of economic growth expectations rose 10 points from August to 73.9, the highest level in 16 years, supported by a strong reading in Germany and France. Once again re-emerging noise about Brexit talks and a spike in coronavirus cases across Europe cannot dampen the positive mood in the EU supported by stimulus and optimism on a vaccination being announced soon.

- Europe is on high alert as coronavirus cades continue to increase. The European Centre for Disease Prevention and Control (ECDC) said that over half of all EU countries currently are experiencing an increase in cases. Hospitals in Europe’s COVID-19 hot spots are close to a saturation point. Madrid cases account for a third of all new cases in Spain. Czech Republic reported this week more than 2,000 daily cases for the first time; governments are debating tighter distancing measures.

- Next week eurozone’s preliminary PMIs will be released for the month of September. Bloomberg economists predict all PMIs to remain above the 50 level, that separates growth from contraction. Manufacturing PMI should be at 51.5, service PMI at 51 and composite at 52.4.

Threats

- With budget deficit growing in Russia due to increased government spending to minimize the negative effects of the coronavirus on the economy, the Finance Minister proposed to fully scrap tax benefits for highly viscous oil producers. According to Wood & Company, Tatneft looks the most exposed as the tax breaks on highly viscous oil accounted for 25 percent of its free cash flow last year. In addition, Russia seeks higher taxes on metals and fertilizer companies. If this measure would be implemented, potential revenue for the budget would be around RUB 90bn.

- Tensions in Belarus continue with thousands of protestors on the streets demanding another election and transition of power to the opposition. President of Belarus Lukashenko met with Vladimir Putin in Sochi on Monday, and it looks like Putin supports Lukashenko to remain in power for now. Russia offered Belarus a $1.5 billion loan to help with the economic crisis in the short term.

- Turkey was cut deeper into junk by Moody’s this week, which warned of a possible balance-of-payments crisis. The B2 rating puts it on a par with Egypt, Jamaica and Rwanda. Moody’s kept a negative outlook. The lira may continue its downtrend unless the central bank will act with a bigger hike.

China Region

Strengths

- China was the best performing country this week, gaining 2.4 percent. Strong economic data pushed equites higher. Industrial production bounced more than expected in August, retail sales are improving, and property investments continue to grow. Longfor Group Holdings, a real estate company, was the best performing equity among stocks trading in the iShares China Large-Cap ETF (FXI), gaining 7.4 percent over the past five days.

- The Indonesia rupiah was the best performing currency this week, gaining 2.24 percent. The currency gained after the central bank kept its policy rate unchanged for a second straight month.

- Consumer durable stocks were the best performers among those trading on the Hong Kong Stock Exchange.

Weaknesses

- The Philippines was the worst performing market this week, losing 1 percent. The EU Parliament on Thursday adopted a resolution pushing for immediate trade sanctions against the Philippines. The resolution called on the European Commission to initiate the procedure for the temporary withdrawal of the Generalized Scheme of Preferences Plus (GSP+) program granted by the 27-nation bloc to the Philippines over rapidly deteriorating human rights under President Rodrigo Duterte’s administration. Universal Robina Corp., a food producer and distributor, was the worst performing equity among stocks trading in the iShares MSCI Philippines ETF (EPHE), losing 7.5 percent over the past five days.

- The Indian rupee was the worst performing currency this week, losing 15 basis points. India’s economic recovery does not look good after the nation emerged as a new global hotspot for the coronavirus pandemic with more than 5 million infections. Goldman Sachs now predicts a 14.8 percent GDP contraction for the year ending March 2021.

- Communication stocks were the worst performing among those trading on the Hong Kong Stock Exchange.

Opportunites

- Industrial output in China accelerated the most in eight months in August and retail sales grew for the first time in 2020. This suggests an economic recovery is gathering pace as demand returns from the coronavirus slump.

- The Organization for Economic Cooperation and Development (OECD) released its forecast that the global economy will contract by 4.5 percent this year – up from a previous estimate of a 6 percent contraction. The OECD estimates that China will grow 1.8 percent in 2020 – the only country expected to experience growth.

- Relatively cheap equities, predictable monetary policy, positive bond yields and a robust response to the coronavirus are all reasons to be bullish on China, writes the Financial Times. With many institutional investment funds staying out of the market “for fear of more anti-China moves from Washington in the run-up to the November election,” now is arguably a good time to increase allocations to that market.

Threats

- Terry Branstad, the U.S. ambassador to China, is stepping down from the role in October citing his role in the trade war truce and a pledge by China to crack down on the illicit trade in fentanyl. The New York Times notes that U.S.-China relations have deteriorated since Mr. Branstad began his tenure in summer 2017, although it is not uncommon for political appointees to serve only a single term. This departure could cause a further downward spiral in the relationship between the two superpowers.

- The number of coronavirus cases in India hit 5 million this week with the addition of 98,000 new infections. The country saw the virus spread at one of the fastest paces and has the world’s third highest death toll. The strict lockdown implemented in March led to a 23.9 percent contraction in GDP in the second quarter compared to the year prior.

- Reuters reports that the U.S. plans to sell as many as seven major weapons systems to Taiwan. Pursuing several sales at once is a departure from years of precedent in which the American military sales to Taiwan were spaced out to minimize tensions with China.

Blockchain and Digital Currencies

Strengths

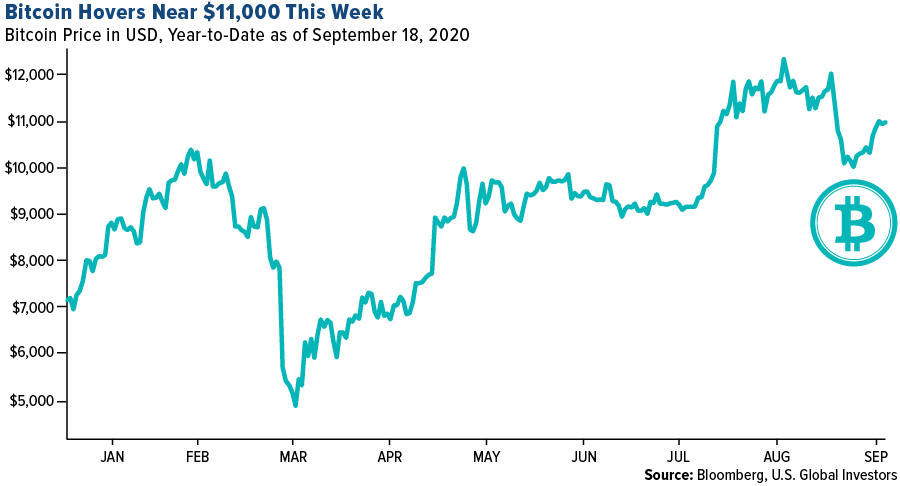

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 18 was UNICORN Token, up over 9,000 percent. The price of bitcoin ended the week hovering very close to the $11,000 mark. Investors are keeping a close eye on if it could climb back up next week.

- The Libra Association has appointed HSBC veteran James Emmett as managing director of its subsidiary firm, Libra Networks LLC, writes CoinTelegraph. Levey is also the former Under Secretary for Terrorism under the administrations of George W. Bush and Barack Obama.

- Patrick Stanley, Blockstack’s former head of growth, is launching a complementary crypto company of his own, Freehold. As reported by CoinDesk, Stanley now runs Freehold as an independent company within the token ecosystem related to Blockstack’s namesake cryptocurrency, STX.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 18 was Dragon Ball, down 97.66 percent.

- India plans to introduce a new law banning trade in cryptocurrencies, writes Bloomberg, placing it out of step with other Asian economies which have chosen to regulate the fledgling market. According to two people familiar with the matter, the federal government will encourage blockchain, the technology underlying cryptocurrencies, but is not keen on crypto trading.

- Unikrn, an initial coin offering from 2017, is facing action from the U.S. Securities and Exchange Commission, writes CoinTelegraph. Based on the September 15 statement from the regulating body, the SEC has accused the startup of running its ICO without going through the proper legal channels.

Opportunities

- Kraken is the first cryptocurrency firm in the U.S. to become a bank, reports CoinDesk. On Wednesday, the Wyoming Banking Board voted to approve the San Francisco-based crypto exchange’s application for a special purpose depository institution (SPDI) charter, the article continues. This makes Kraken the very first SPDI bank in Wyoming.

- Wirex’s new Mastercard-supported card will be linked to 19 crypto and fiat currency accounts in the Wirex app, reports CoinTelegraph. The company wants to encourage the use of cryptocurrency for everyday payments, so is also upgrading its existing “Cryptoback” rewards program. Wirex is based in London and has a license to issue crypto cards in Europe.

- Miners on crypto’s second-biggest blockchain had a bumper day Thursday, writes CoinDesk, earning a record $16 million for confirming a growing number of DeFi-related transactions. According to data from Etherscan, miners collected a total 42,763 ether in transaction fees on Thursday – a new all-time high.

Threats

- As reported by CoinTelegraph, the two Russians who were sanctioned earlier this week by the U.S. Treasury Department (on accusations of being crypto thieves) allegedly got their millions through market manipulation and phishing. A 30-page forfeiture complaint details how the two allegedly “deployed” a series of bogus, lookalike sites that duped users into sharing their login credentials, giving the hackers

- The drama continues over alleged fraud involving Bithumb’s senior executives, writes CoinTelegraph, as the company’s chairman has reportedly been summoned for interrogation. Lee Jung-hoon, chairman of the board of Bithumb Korea and Bithumb Holdings, is allegedly accused of multiple fraud and embezzlement offenses regarding the failed listingof the BXA token.

- On Thursday, bitcoin lost some of its momentum, writes CoinDesk, while DeFi delirium pushes fees on Ethereum back up. The popular digital currency went as low as $10,735 on spot exchanges such as Coinbase. Katie Stockton, an analyst for Fairlead Strategies, blamed a lack of momentum in the bitcoin market on Thursday.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.70 | +0.02 | +2.51% |

| Oil Futures | 40.88 | +3.58 | +9.60% |

| Hang Seng Composite Index | 3,837.87 | +84.63 | +2.25% |

| S&P Basic Materials | 411.95 | +9.07 | +2.25% |

| Korean KOSPI Index | 2,412.40 | +15.92 | +0.66% |

| S&P Energy | 250.65 | +7.69 | +3.17% |

| Nasdaq | 10,793.28 | -126.31 | -1.16% |

| DJIA | 27,657.42 | +122.84 | +0.45% |

| Russell 2000 | 1,536.78 | +29.03 | +1.93% |

| S&P 500 | 3,319.41 | -19.78 | -0.59% |

| Gold Futures | 1,957.80 | -6.50 | -0.33% |

| XAU | 151.51 | -0.83 | -0.54% |

| S&P/TSX VENTURE COMP IDX | 746.38 | +4.33 | +0.58% |

| S&P/TSX Global Gold Index | 377.08 | -7.45 | -1.94% |

| Natural Gas Futures | 2.07 | -0.25 | -10.93% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,412.40 | +51.86 | +2.20% |

| 10-Yr Treasury Bond | 0.70 | +0.01 | +1.91% |

| Gold Futures | 1,957.80 | -12.50 | -0.63% |

| S&P Basic Materials | 411.95 | +19.23 | +4.90% |

| S&P 500 | 3,319.41 | -55.44 | -1.64% |

| DJIA | 27,657.42 | -35.46 | -0.13% |

| Nasdaq | 10,793.28 | -353.18 | -3.17% |

| Oil Futures | 40.88 | -2.05 | -4.78% |

| Hang Seng Composite Index | 3,837.87 | -9.81 | -0.25% |

| S&P/TSX Global Gold Index | 377.08 | +0.02 | +0.01% |

| XAU | 151.51 | +3.02 | +2.03% |

| Russell 2000 | 1,536.78 | -35.29 | -2.24% |

| S&P Energy | 250.65 | -26.40 | -9.53% |

| S&P/TSX VENTURE COMP IDX | 746.38 | +6.43 | +0.87% |

| Natural Gas Futures | 2.07 | -0.36 | -14.72% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 151.51 | +38.94 | +34.59% |

| S&P/TSX Global Gold Index | 377.08 | +70.28 | +22.91% |

| Gold Futures | 1,957.80 | +209.90 | +12.01% |

| DJIA | 27,657.42 | +1,577.32 | +6.05% |

| S&P 500 | 3,319.41 | +204.07 | +6.55% |

| Nasdaq | 10,793.28 | +850.23 | +8.55% |

| Korean KOSPI Index | 2,412.40 | +278.92 | +13.07% |

| Natural Gas Futures | 2.07 | +0.43 | +26.31% |

| S&P Basic Materials | 411.95 | +58.91 | +16.69% |

| Russell 2000 | 1,536.78 | +109.70 | +7.69% |

| Oil Futures | 40.88 | +2.04 | +5.25% |

| Hang Seng Composite Index | 3,837.87 | +268.34 | +7.52% |

| S&P/TSX VENTURE COMP IDX | 746.38 | +188.11 | +33.70% |

| S&P Energy | 250.65 | -50.80 | -16.85% |

| 10-Yr Treasury Bond | 0.70 | -0.01 | -1.97% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2020):

Amazon.com Inc.

BHP Group Ltd.

SPDR Gold Shares

Kinross Gold Corp

Newmont Corp

Lundin Gold Inc

Kore Mining Ltd

SSR Mining Inc

Alacer Gold Corp

B2Gold Corp

OTP Bank Nyrt

Tatneft PJSC

Facebook Inc.

Microsoft Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Municipal Bond Index is a broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market. Bloomberg Commodity Index (BCOM) is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification. The MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. With 1,601 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The University of Michigan Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in December 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample. The NY Empire State Index is the result of a monthly survey of manufacturers in New York state. Known as the Empire State Manufacturing Survey, it is conducted by the Federal Reserve Bank of New York. The headline number for the NY Empire State Index refers to the main index of the survey, which summarizes general business conditions in New York state. ZEW Germany Expectation of Economic Growth is a survey on the question of economic growth in six months. CECE Composite Index (CECE) is a free float weighted price index made up of the most liquid stocks traded on Budapest, Prague and Warsaw Stock Exchange.