This Mining Company Is Back to Creating Value for Investors

Date Posted: July 5, 2019

Read time: 52 min

The constant flying and wildly fluctuating temperatures were well worth it, though. I'm very pleased to say that a satisfactory agreement was reached between HIVE and its strategic partner, Genesis Mining.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

As many of you know, I serve as interim CEO and chairman of HIVE Blockchain Technologies, the first publicly traded company involved in the mining of cryptocurrencies. We maintain facilities in Iceland, Sweden and Norway, all of which have optimally cool climates and cheap renewable energy.

Last week, HIVE business took me to just within the frigid Arctic Circle. This was followed by stops in Zurich, Geneva and Milan, where temperatures soared in a record-setting heat wave. Keep in mind that many European hotels still do not have air conditioning.

The constant flying and wildly fluctuating temperatures were well worth it, though. I’m very pleased to say that a satisfactory agreement was reached between HIVE and its strategic partner, Genesis Mining. All claims arising from the master service agreements, as well as legal proceedings, have been withdrawn and discontinued. You can read the full press release here.

Above all else, I’m thrilled that HIVE can return to creating value for its shareholders, to whom I extend my gratitude.

Cryptocurrencies Challenging Traditional Monetary Policy

The agreement couldn’t have come at a better or more interesting time. Economic conditions have improved in the cryptocurrency ecosystem, with bitcoin surging as high as $13,764 late last month. Meanwhile, Facebook’s upcoming Libra coin is drawing fresh attention to digital currencies as a concept.

That includes attention from Congress. In a July 2 letter, lawmakers on the House Committee on Financial Services requested that Facebook and its partners halt development of Libra, as they fear the coin could lead “to an entirely new global financial system that is based out of Switzerland and intended to rival U.S. monetary policy and the dollar.”

Agustín Carstens, head of the Bank of International Settlements (BIS), also weighed in on Facebook’s announcement, telling the Financial Times that “many central banks” were working on developing their own cryptocurrencies.

“It might be that it is sooner than we think that there is a market, and we need to be able to provide central bank digital currencies,” commented Carstens, a harsh critic of cryptocurrencies.

This is quite an admission. But if you recall, it wasn’t so long ago that JPMorgan CEO Jamie Dimon was calling people who buy bitcoin “stupid.” Today, his bank is starting client trials of its very own digital currency, the JPM Coin.

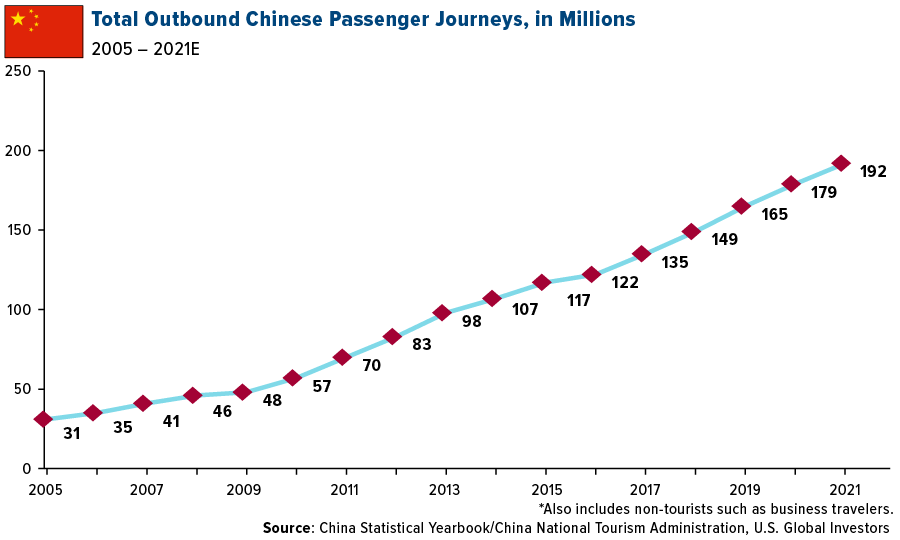

The times are definitely changing, and that includes international tourism. When I was in Europe, I saw busloads full of Chinese tourists, who are the biggest spenders of any other nationality. This is very constructive for airlines and the travel industry as a whole. Many of the tourists gobbled up all of the three and four-star hotels, leaving only the five-star hotels, which naturally raised their rates—often to outrageous levels.

On an unrelated note, I want to congratulate my good friend Frank Giustra for being awarded the Order of Canada for “his impactful contributions to business and to international humanitarian initiatives addressing global crises and development.” This is a huge honor, equivalent to knighthood in the U.K., and I can’t think of too many people who are as deserving of it as Frank is.

Finally, I don’t normally recommend movies, but I saw Pavarotti recently and can’t stop thinking about it. The Ron Howard-directed documentary of the great Italian tenor Luciano Pavarotti is a marvel, both inspirational and moving. You need not be an opera fan to enjoy the film or appreciate Pavarotti’s contribution to world music of the past half century. It’s for anyone who’s interested in the lives of high achievers, of which Pavarotti was decidedly one, having sold more than 100 million records.

Farewell to an American Legend

Lee Iacocca posing with the 2009 Ford Mustang

Photo by: The World of Mustang, Lee laccoca 2009 Mustang serial #001 | Attribution-ShareAlike 2.0 Generic (CC BY-SA 2.0)

“The Depression turned me into a materialist. Years later, when I graduated from college, my attitude was: ‘Don’t bother me with philosophy. I want to make ten thousand a year by the time I’m twenty-five, and then I want to be a millionaire.’ I wasn’t interested in a snob degree; I was after the bucks.”

That’s from the first chapter of Lee Iacocca’s best-selling autobiography, published in 1984. The larger-than-life auto executive, who gave the world the iconic Ford Mustang and later saved Chrysler from bankruptcy, died this week at the age of 94.

It’s appropriate that his passing should coincide with our celebration of America’s independence. Iacocca embodies the American spirit of innovation and “can-do-it-ness” as few people have in the 243 years since the birth of the country that helped make his infinite success possible.

Born to Italian immigrants, Iacocca worked his way up the ranks at Ford, eventually finding national renown in 1964 with the launch of the Mustang, which he conceived as “a sports car but more than a sports car.” Retailing for less than $2,400—or about $20,000 in today’s dollars—it was a runaway hit, generating $1.1 billion in profits over the next two years.

But Iacocca is perhaps best known for reviving the struggling Chrysler, which he led after being fired from Ford by Henry Ford II. In 1980, Chrysler was looking at a loss of $1.7 billion. This was turned into a $2.4 billion profit by 1984. Investors were handsomely rewarded. A New York Times article in January 1983 named Chrysler “the surprise stock” of the past year, beginning at just above $3 a share and ending at $18—an incredible increase of around 500 percent.

So great was Iacocca’s superstar celebrity that he was rumored to be a presidential contender in 1988. And yes, he became a millionaire, many times over. I have no doubts that his legacy will continue to strengthen in the years to come, as his remarkable story is uniquely American. Although he’s gone, we’ll see him again—or, at least, an actor’s portrayal of him—as soon as this November, when the 1960s period film Ford v Ferrari hits theaters.

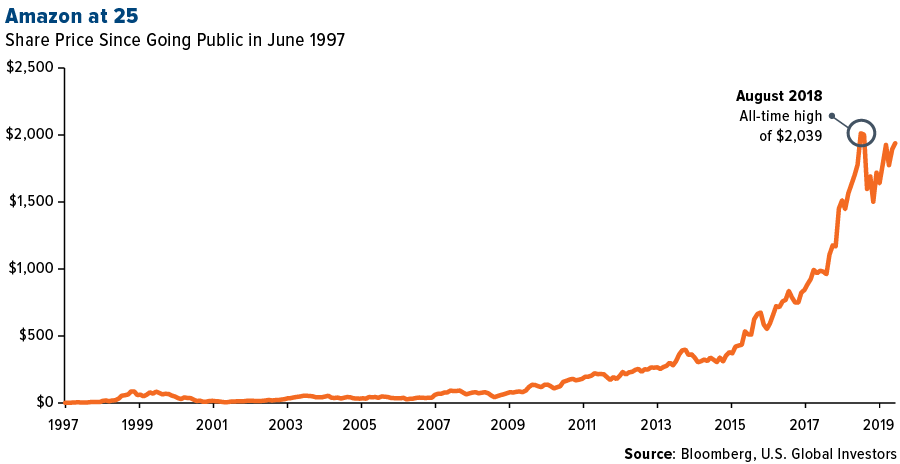

After 25 Years, Has Amazon Become Too Large?

Other notable milestones took place this week. For one, the current economic expansion reached a record 121 months. This is enough to beat the previous record-holder, the period between March 1991 and March 2001. As I’ve said before, business cycles die not of old age but by the Federal Reserve. We’ll see if the Fed chooses to lower rates later this month, though the better-than-expected June jobs report makes that look less likely.

Also of note is that, Amazon, another American success story, turned 25 years old. Jeff Bezos founded the book seller—now the world’s largest retailer, having surpassed Walmart—amazingly at a time when very few people even had access to the internet. Less than half a percent of the world’s population was online in 1994, according to the World Bank.

A lot has changed since then, as you well know. Bezos’ nearly $1 trillion empire has completely redefined how we shop and consume media. It’s given us the Kindle, Prime, Alexa and much more. Today it’s the eighth largest grocer in the U.S., having bought Whole Foods in August 2017. It’s even started selling tiny modular homes, some of which go for as little as $5,000.

For many investors, Amazon has been life-changing. A $100 investment in the company’s IPO in 1997 would have been worth a whopping $120,762 in August 2018, when its stock hit an all-time high of $2,039.

But can the momentum continue? Like its digital peers Google and Facebook, Amazon’s tremendous success may also be its greatest obstacle going forward. Calls to break up the online retailer are intensifying, with some antitrust authorities citing previous cases such as Standard Oil and AT&T. Last month, it was announced that the Federal Trade Commission (FTC) agreed to scrutinize Amazon and Facebook for antitrust violations, while the Department of Justice (DOJ) took on Google and Apple.

“I think it is inevitable that they’ll get broken up,” Stacy Mitchell, co-director of the advocacy group Institute for Local Self-Reliance (ILSR), told CNET. “You can’t mask the kind of structural power that these companies have and maintain that power in a democracy.”

The company’s antitrust troubles aren’t confined to the U.S. Just today, the United Kingdom’s Competition and Markets Authority ordered Amazon to halt its acquisition of food delivery service Deliveroo.

Looking to make sense of the markets? Subscribe to my award-winning Frank Talk CEO blog! Click here to sign up!

Gold Market

This week spot gold closed at $1,398.75, down $10.70 per ounce, or 0.76 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.59 percent. The S&P/TSX Venture Index came in slightly higher by 0.23 percent. The U.S. Trade-Weighted Dollar gained 1.16 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-30 | Caixin China PMI Mfg | 50.1 | 49.4 | 50.2 |

| Jul-1 | ISM Manufacturing | 51.0 | 51.7 | 52.1 |

| Jul-3 | ADP Employment Change | 140k | 102k | 41k |

| Jul-3 | Initial Jobless Claims | 223k | 221k | 229k |

| Jul-3 | Durable Goods Orders | -1.3% | -1.3% | -1.3% |

| Jul-5 | Change in Nonfarm Payrolls | 160k | 224k | 72k |

| Jul-11 | Germany CPI YoY | 1.6% | — | 1.6% |

| Jul-11 | CPI YoY | 1.6% | — | 1.8% |

| Jul-11 | Initial Jobless Claims | — | — | 221k |

| Jul-12 | PPI Final Demand YoY | 1.7% | — | 1.8% |

Strengths

- The best performing metal for the week was palladium, which gained 2.11 percent as the market remains undersupplied with implementation of tougher emission standards in China. A Bloomberg survey of traders and analysts turned bullish for next week’s price expectations. Gold recorded its best monthly advance since June 2016, reports Bloomberg, although admittedly the U.S.-China trade tensions could test demand. In addition, American Eagle gold coin sales rose 25 percent to 5,000 ounces in June from a month earlier, according to U.S. Mint data. The Perth Mint also released figures this week showing gold coin and minted bar sales were 19,449 ounces in June, up from 10,790 ounces in May.

- Despite gold prices falling back on Monday, sinking by the most in two years, that didn’t stop investors’ commitment to the yellow metal. Inflows into bullion-backed exchange-traded funds (ETFs) kept coming, writes Bloomberg, with holdings expanding for 16 of the last 17 days. This brought net purchases to over 3.22 million ounces. Commodity ETFs also saw inflows, with around $5.6 billion going into raw material funds this month, “the biggest influx in almost three years,” Bloomberg explains, while gold rallied to a six-year high.

- Poland’s central bank boosted its gold reserves, the bank said in a statement, bringing its holdings up by 100 tons to 228.6 tons. Joni Teves of UBS wrote in this week’s Global Precious Metals Comment that central banks look to remain gold buyers, but the pace could vary. Preliminary data shows that at least 29 tonnes of purchases came from the more active central banks—Russia, China, Kazakhstan, Turkey and Kyrgyz.

Weaknesses

- The worst performing metal the week was platinum, which fell 2.83 percent, but nearly all the losses for the week came on Friday with the stronger-than-expected jobs report. Gold futures also fell on Friday as payroll gains in the U.S. “called into question expectations for the Federal Reserve to cut interest rates.” Government data showed payrolls climbing 224,000 in June.

- President Donald Trump said he would hold off imposing an additional $300 billion in tariffs, reports Bloomberg, and the world’s two largest economies agreed to resume negotiations. This truce hurt demand for haven assets, the article continues, sending gold lower by 1.8 percent to $1,384.06 per ounce—the biggest drop in a year.

- Factory activity across Asia and Europe shrank in the month of June, while the U.S. showed only minimal growth, reports Bloomberg. Due to fresh strains on the economy (in the form of purchasing managers’ index data), however, gold rebounded from its biggest decline in more than two years. A global measure of activity showed a second straight contraction, which is the first time this has happened since 2012.

Opportunities

- Some big names are backing gold this week—veteran investor Mark Mobius is one of them. As reported by Bloomberg, Mobius says that gold is set to push higher, potentially topping $1,500 an ounce, as interest rates head lower, central banks extend purchases and uncertainty surrounding geopolitics and cryptocurrencies fans demand. Strategists from Societe Generale are also looking at the yellow metal, particularly in the form of gold miners. In a note to investors, the strategists explain that gold equities tend to outperform physical gold through every cycle and have further to run. In addition, UBS raised its gold forecast to $1,450 on both trade and geopolitical risks.

- President Trump’s latest “dove” picks to the Fed’s board could be positive for gold, reports Bloomberg. The two economists are both seen as likely to support the president’s call for lower interest rates, the article explains. In addition, weaker-than-expected U.S. payrolls and service industry data overshadowed a decline in jobless claims. Robin Tsui, Asia Pacific gold strategist with SPDR ETFs, says there are several bullish factors for gold right now. “There’s a lot of momentum trading right now into gold,” Tsui explains. “It’s definitely good as a hedge against all this uncertainty, as portfolio insurance, and as the ultimate safe haven.” UBS is raising its palladium forecast, analyst Giovanni Staunovo said in a note this week. Both six- and 12-month palladium forecasts raised to $1,600 an ounce from $1,500 an ounce previously, as prices move back toward records and the market remains undersupplied, Bloomberg reports.

- According to an official filing, and as reported by Bloomberg, B2Gold and Calibre Mining announced that Calibre will acquire El Limon and La Libertad gold mines. Calibre will also acquire the Pavon Gold Project and additional mineral concessions in Nicaragua for an aggregate consideration of $100 million. B2Gold will own an approximate 31 percent direct equity interest in Calibre following the completion of the deal. In addition, Calibre announced a concurrent C$100 million equity financing. The management team at Calibre has a history of surfacing value from deals they have structured.

Threats

- In an interview with Reuters this week, Governor Elvira Nabiullina said that the Bank of Russia has introduced discounts for purchasing gold to spur miners to export more of the precious metal. Previously, sellers were seeking to sell all gold to the central bank, reports Bloomberg. The discount should balance Russia’s domestic and export sales, with more now being offered to international buyers.

- India’s Finance Minister Nirmala Sitharaman says that the finance ministry has received representations for reduction in basic customs duty on gold, Bloomberg reports, including from the trade ministry in the past. Such recommendations are examined as a part of the budget exercise. UBS’ Joni Teves reports that India raised its duties on gold to 12.5 percent from 10 percent during the Union Budget on Friday. Similarly, the tariff for silver dore was raised to 11 percent from 8.5 percent. The increase comes as a surprise “considering that expectations heading into today’s announcement were for a potential cut in import taxes.”

- Recent issues with OceanaGold’s Didipio mine in the Philippines have intensified, reports CIBC Capital Markets. The governor of the Nueva Vizcaya province has ordered local authorities to restrain any of OGC’s activities at the operation. “As a result, a local government unit blocked a supply truck from reaching Didipio, and OceanaGold has now suspended all heavy truck movements to prevent any further escalation,” the CIBC report continues.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.21 percent. The S&P 500 Stock Index rose 1.65 percent, while the Nasdaq Composite climbed 1.94 percent. The Russell 2000 small capitalization index gained 0.58 percent this week.

- The Hang Seng Composite gained 1.05 percent this week; while Taiwan was up 0.51 percent and the KOSPI fell 0.94 percent.

- The 10-year Treasury bond yield rose 3 basis points to 2.04 percent.

Domestic Equity Market

Strengths

- Communication services was the best performing sector of the week, increasing 2.74 percent compared to an overall increase of 1.65 percent for the S&P 500.

- Symantec was the best performing stock for the week, increasing 14.89 percent.

- U.S. stocks closed on an all-time high on Wednesday, led by the technology and consumer sectors. For the S&P 500, it was the third straight record intraday high and second straight record close this week.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 0.94 percent compared to an overall increase of 1.65 percent for the S&P 500.

- Coty was the worst performing stock for the week, falling 13.81 percent.

- The world’s biggest gaming retailer, GameStop, has been in steady decline. This year its stock bottomed from $16 a share in January to just $5 by July.

Opportunities

- Anheuser-Busch InBev, the world’s biggest beer company, is seeking to raise as much as $9.8 billion from public listings of a minority stake of its Asia Business.

- Intel is putting about 8,500 of its 90,000 patents on the auction block as it exits the 5G smartphone modem market. The Santa Clara, California-based company told Business Insider it is looking to sell intellectual property assets related to 3G, 4G and 5G cellular and wireless technologies.

- Tesla’s stock jumped after setting a new quarterly deliveries record. CEO Elon Musk and his team delivered 95,200 vehicles, 4,000 more than expected.

Threats

- An association of U.S. retail giants, including Walmart, Target and Best Buy, has backed calls for an antitrust investigation into Amazon and Google. The Retail Industry Leaders Association (RILA) wrote to the Federal Trade Commission (FTC) with the demand, emphasizing the dominance they have over consumer data.

- Advanced Micro Devices denied that it broke U.S. laws after a news report said an AMD joint venture gave China access to state-of-the-art processors. The AMD partnership with a military contractor is helping China compete with the U.S. in building the next generation supercomputer with AMD’s chip technology, according to a Thursday report in the Wall Street Journal.

- Australia’s prime minister Scott Morrison secured a deal with the leaders of other G20 nations to take on social media firms that don’t tackle terrorist content. Social media platforms are expected to develop technology which will allows them to quickly identify extreme content, prevent its proliferation and record who uploaded it so as to persecute offenders.

The Economy and Bond Market

Strengths

- U.S. hiring rebounded in June and topped all estimates of economists, reports Bloomberg, a sign of labor market strength that may ease calls for a Federal Reserve interest rate cut. Nonfarm payrolls climbed 224,000 after an advance of 72,000 in May, according to a Labor Department report.

- Home prices increased nationally by 3.6 percent from May 2018, according to data from CoreLogic. “Interest rates on fixed-rate mortgages fell by nearly one percentage point between November 2018 and this May,” said Dr. Frank Nothaft, chief economist at CoreLogic. “This has been a shot-in-the-arm for home sales. Sales gained momentum in May and annual home-price growth accelerated for the first time since March 2018.”

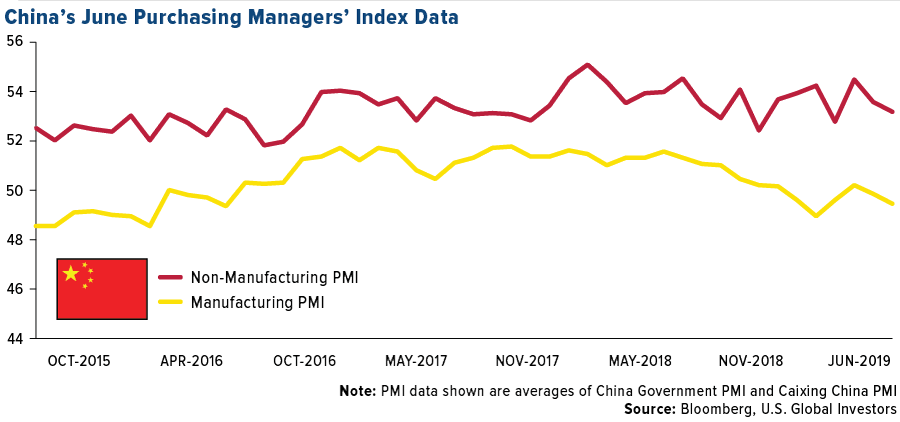

- The U.S. manufacturing purchasing managers’ index (PMI) improved by half-a-point to 50.6 in June from the preliminary reading of 50.1 released last week, according to IHS Markit. However, the June index remains near the lowest level in a decade. Both domestic and new orders from abroad improved in June after seeing declines in the prior month. The report cited anecdotal evidence suggesting new orders increased from the acquisition of new clients. New business from abroad rose at the fastest pace since 2018 signaling that businesses are finding ways to navigate President Trump’s trade policies.

Weaknesses

- New orders for manufactured durable goods decreased 1.3 percent in May to $243.4 billion, following a 2.8 percent May decrease, according to the U.S. Census Bureau. Declining three of the last four months, transportation equipment drove the decrease, declining 4.6 percent to $80.0 billion over the month.

- American farmers are hoping that Trump’s renewed trade deal talks with China will bring a reprieve after U.S. pig farmers lost hundreds of millions of dollars in export sales to China and Mexico due to the dispute.

- The latest eurozone PMI manufacturing survey shows the sector contracted for a fifth consecutive month in June. U.S. manufacturing activity also slowed to its lowest level in close to three years, according to ISM data.

Opportunities

- The rebound in U.S. nonfarm payrolls growth after disappointing data for May led traders to trim their more aggressive rate-cut bets for the Federal Reserve when policy makers meet at the end of the month. While markets before the report were leaning toward a cut of as much as a half-point, based on Fed fund futures, that edged briefly below a quarter point following the Labor Department release.

- The U.S. and China have struck an interim trade-war truce. Donald Trump and Xi Jinping reached a deal on Saturday that avoids further tariff hikes and eases trade restrictions on Chinese tech giant Huawei.

- Next week, attention from investors will move onto the latest consumer and producer prices, as well as the minutes of the Fed’s June policy meeting.

Threats

- Morgan Stanley downgraded its forecast for world growth, saying the recent truce wasn’t enough to remove the uncertainty around trade, which will weigh on the outlook.

- Mark Carney warned of damage to the global economy from rising protectionism, describing a “widespread slowdown” that may require a major policy response. The Bank of England governor said the “intensification of trade tensions has increased the downside risks to global and U.K. growth,” citing falling business confidence and pessimism among households. He also said the U.K. faces the additional threat of a no-deal Brexit on business investment. Given that it was only the Bank of England that had kept a neutral monetary stance, Carney’s comments mean most of the developed economies have now turned dovish.

- Trump’s trade war is threatening the European Union (EU) by slapping $4 billion worth of tariffs on meat, cheese and other EU goods in retaliation for the union’s subsidies to aircraft-manufacturer Airbus.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was natural gas, which gained 4.07 percent on forecasts of hotter-than-normal weather expected across the lower 48 states, July 15-19. According to data from BloombergNEF, it’s time to get ready for a low-carbon Britain. Power from offshore wind will overtake coal for the first time as early as this year. While the construction of offshore wind stations powers ahead, the article continues, government policy is for coal to disappear completely by 2025.

- Copper’s rally continues this week, reports Bloomberg, as a trade war truce between the U.S. and China fuels a relief rally across risky assets. The agreement brightened the demand outlook for China, the top metal user. Iron ore also rose this week, holding above $120 a ton and notching a fresh five-year high. Bloomberg reports the price move amid signs that demand from mills in China is being sustained after steel prices gained.

- Nearly half of all cars sold in Norway during the first half of the year were electric, reports Bloomberg. Booming sales of Tesla Inc.’s Model 3 meant that 45 percent of all cars were electric, which is up from 31 percent share in 2018. Compared to the same period last year, the sale of petrol-fueled cars declined about 29 percent, the article continues.

Weaknesses

- The worst performing major commodity for the week was zinc, which lost 5.09 percent as tariff worries have kept base metals in the doldrums. For the oilfield services industry, few signs of recovery are present just five years after oil’s collapse to less than $30 a barrel from over $100, reports Bloomberg. The service companies that handed out discounts during the downturn are barely hanging on, with Schlumberger and Halliburton (the two biggest) having each fallen by over 65 percent since crude started tumbling. On a related note, an oil tanker that took a cargo of crude from the Middle East to Italy (a 10,700 mile trip), is returning the unsold shipment back to the Persian Gulf – this, after the Italian oil company subsequently rejected it.

- Nickel extended its losses this week, reports Bloomberg, after recording the biggest daily decline in nearly five months. The drop in prices have coincided with a drop in aggregate open-interest in Shanghai contracts, the article continues, signaling that investors have been closing out long positions during the selloff. Copper is also set for a weekly loss, as concerns over the health of Chinese demand held back the price, reports Bloomberg. Top copper producer Codelco is “again delaying the return to normal operations at its Chuquicamata smelter, and the facility is unlikely to return to full capacity until mid-August.”

- At a meeting in Vienna, all members of the Organization of Petroleum Exporting Countries (OPEC), and its allies in the OPEC+ coalition, have now settled on maintaining quotas for another nine months, reports Bloomberg. “The rollover of curbs into a fourth year shows oil producers are ever more bogged down in a struggle to wrest control of the market from the booming U.S. shale industry,” the article reads. OPEC’s dominant producer, Saudi Arabia, will likely continue to do the heavy lifting.

Opportunities

- Following bad weather and output setbacks, iron ore exports in Australia are set to post the first annual drop in nearly two decades, reports Bloomberg. This worsens the global shortage but boosts prices that have already surged to a five-year high. According to the article, iron ore has soared past $100 a ton, driven by 1) twin forces of supply disruptions in Brazil and Australia, and 2) strong demand from steel mills in China.

- At Origin Energy Ltd.’s Quarantine power station in South Australia, when an old gas turbine comes up for major maintenance, rather than doing it they replace the turbine with a new lightweight version that can deliver power to the grid within five minutes of starting. As Bloomberg writes, this rapid-response technology can help the company manage the transition to cleaner energy because it can quickly offset intermittent power from wind- and sun-powered generation. Then there are battery-powered cars in Europe, which the government is working closely with industry and banks to spur technology for. “In the past few months, government officials led by European Commission VP Maros Sefcovic have joined with manufacturers, development banks and commercial lenders on measures that will channel more than 100 billion euros into a supply chain for the lithium-ion packs that will power electric cars,” Bloomberg explains.

- One Bloomberg article this week says there is a whisper on Wall Street that Democratic senator Elizabeth Warren isn’t so bad. Apparently Warren is winning respect from a small but growing circle of senior bankers and hedge fund managers. “If she ends up being the nominee, I’d have no trouble supporting her at all,” said David Schamis, chief investment officer at Atlas Merchant Capital. And although she is not Schamis’ top choice, he added: “I think she is smart, hardworking, responsible and thoughtful. I think she thinks markets are important.”

Threats

- India’s Central Electricity Authority released an analysis of the country’s power generation, and according to the assessment, coal could account for half in 2030 despite a boom in solar and wind energy projects, reports Bloomberg. India has a large existing fleet of coal plants and there seems to be a mismatch between peak periods of demand and output from renewables – leaving a big role for “the most-polluting fuel in the nation’s future electricity mix.”

- Head of Roubini Macro Associates, Nouriel Roubini, and otherwise known as “Dr. Doom,” believes that a U.S.-China trade war and a spike in oil prices from geopolitical tensions have the potential to push the world into recession next year, reports Bloomberg. In an interview with Bloomberg TV, Roubini said “It’s a scary time for the global economy,” and a recessionary shock could materialize next year.

- American oil explorers cut back on the number of drilling rigs this week, reports Bloomberg, matching a one-year low reached last month. Crude’s rally is faltering amid growing concerns over demand. According to data released Wednesday by oilfield-services provider Baker Hughes, working oil rigs in the U.S. fell by five to 788.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 3.2 percent. Investors are becoming more optimistic that the U.S. will not impose sanctions on Turkey for buying the S-400 defense system from Russia. During the G20 meeting last weekend, Trump said that Turkey has been treated unfairly over the contract.

- The Turkish lira was the best performing currency this week, gaining 2.9 percent against the U.S. dollar. Turkey’s government successfully sold $2.25 billion of dollar-denominated bonds due in 2024 with a yield of 6.45 percent.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst relative performing country this week, gaining 73 basis points. Retailers underperformed in Poland as the government wants to re-impose a retailer tax from September, not at the beginning of 2020 as previously announced.

- The Hungarian forint was the worst performing currency this week, losing 1.6 percent against the U.S. dollar. Moody’s lowered its outlook on the Hungarian banking system, citing limited loan quality improvements.

- Communication services was the worst performing sector among eastern European markets this week.

Opportunities

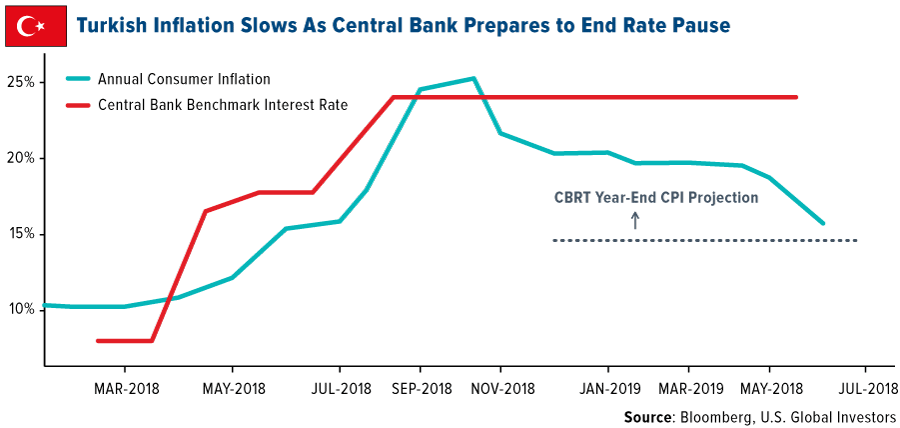

- Turkey’s June inflation came in at 15.7 percent versus 18.71 percent the prior month. Lower inflation may finally allow central bank to cut rates. The current one-week repo rate is set at 24 percent; the central bank’s next decision is scheduled for July 25.

- Greece will hold elections on Sunday. The expectation is that the current opposition party will form a new government with a majority in the parliament. This should be positive news for the market, as the New Democracy party is market-friendly, with a focus on reducing taxation, increasing foreign investment and completing the privatization programme.

- Christie Lagarde, the current IMF chief, was nominated to succeed Mario Draghi as president of the European Central Bank (ECB). Lagarde was very vocal against the Federal Reserve raising rates in 2015, and her dovish tone should be good for equities. This change of leadership will take place on November 1.

Threats

- Final June manufacturing PMI data for the eurozone area was reported at 47.6 versus 47.8, a weaker reading and below the 50 level that separates growth from contraction. However, the services PMI remains very strong in the euro area, supporting the composite PMI and above the 50 level.

- European shares declined on Friday after better-than-expected U.S. jobs data curbed expectation for monetary easing. In the past month, European equites were lifted on expectations of sharp rates cuts in the U.S. and a trade truce between America and China.

- The possibility of snap elections in the Czech Republic is rising. On Thursday, Prime Minister Andrej Babis’ ruling party and its junior center-left coalition partner, the Social Democrats, demanded dismissal of the Culture Minister saying he has failed to fulfil his duties. However, president Zeman refused to do so. Under the Czech constitution, the president is obligated to fire ministers if requested by the prime minister, but Zeman is known for acting independently of the government.

China Region

Strengths

- The best performing index in the region for the week was Vietnam’s Ho Chi Minh Stock Index, which climbed 2.68 percent, although Singapore, the Philippines, China, Hong Kong and Taiwan all finished up more than 1 percent on the week as well.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index since last Friday was consumer services, which jumped 3.71 percent.

- Singapore’s Purchasing Managers Index (PMI) dropped to 49.6, shy of estimates and remaining down in contractionary territory.

Weaknesses

- The worst-performing index in the region for the week was South Korea’s KOSPI Index, which declined by 94 basis points.

- The poorest-performing sector in Hong Kong’s Hang Seng Composite Index this week was energy, which fell 1.41 percent.

- The Caixin China Services PMI fell to 52.0 for the June reading, down from May’s 52.7 and short of consensus for a 52.6 reading.

Opportunities

- U.S.-China trade talks are back post-G20, with negotiations picking back up following the agreement between Presidents Trump and Xi to suspend new tariffs and try talks again. While there is no set time frame on Truce 2.0 and major face-to-face meetings haven’t been set yet, Larry Kudlow, director of the National Economic Council, advised that United States Trade Representative Robert Lighthizer and Secretary Steve Mnuchin have been speaking with China’s chief negotiator and Vice Premier Liu He by telephone.

- Trump has rekindled the possibility of talks again with North Korea. He not only visited the Demilitarized Zone (DMZ) on the Korean borders but invited North Korea’s Kim Jong Un to meet him there to shake hands. The president walked across the border into North Korea, and there are as-yet unconfirmed rumors (as though there’s any other kind) of a third Trump-Kim summit to come.

- Over the weekend, Vietnam’s official free trade agreement with the European Union kicked in, bringing the rising manufacturing powerhouse more access to Europe, potentially enticing more Chinese manufacturers to relocate, and ushering in the consummation of a seven year negotiation with the EU in what that economic bloc’s press releases have said is “the most ambitious free trade deal ever concluded with a developing country.” Some 99 percent of customs duties between the trading partners will be eliminated over time as part of the deal, the South China Morning Post reported.

Threats

- The threat of U.S.-China trade war escalation must remain a threat until resolved with more certainty.

- Bloomberg News reported this week that “the U.S. is now targeting Vietnam for tariffs in an expansion of its trade war. The Commerce Department imposed duties of more than 400 percent on the nation’s steel imports, saying some products produced in South Korea and Taiwan were being shipped to Vietnam before being exported to America to evade levies.” Vietnam’s prime minister ordered a crackdown on the export issue within his country, reports later in the week observed.

- On the Monday holiday in Hong Kong celebrating HKSAR Establishment Day, or the anniversary of the British colonial handover of the Asian city to China, protests continued in Hong Kong against its CEO Carrie Lam and the controversial extradition bill, with protesters storming the HK legislature building, breaking windows, and vandalizing the building even as more peaceful protesters marched in demonstration.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 5 was IZIChain, up 312.28 percent.

- BAM Trading Services, which is the operator of Binance’s upcoming U.S. crypto exchange, has hired a former Ripple executive as its CEO, reports CoinDesk. On Tuesday, Catherine Coley was appointed as CEO, with the responsibility of rolling out Binance U.S. as well as expanding the exchange’s marketplace in North America.

- The largest food company by revenue, Nestle, announced a pilot program to track its supply chains using blockchain, the company noted in a statement. The pilot system will last six months and will be separate and distinct from Nestle’s ongoing participation with IBM Food Trust blockchain.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 5 was Fox Trading, down 70.37percent.

- An outage on Tuesday morning took down a number of cryptocurrency information and trading websites, reports CoinDesk, including Coinbase and CoinMarketCap. Automatic pricing engines were impacted and at one point CoinDesk’s widget displayed a price of $26 per bitcoin.

- According to Bloomberg, U.K. regulators have approved the first cryptocurrency hedge fund. Prime Factor Capital is the first crypto hedge fund approved as a full-scope alternative investment fund manager. The firm will abide by European regulations, reports CoinDesk, and under these guidelines it will be allowed to hold more than 100 million euros in assets under management.

Opportunities

|

|

- Despite his highly critical comments of the cryptocurrency space over the last several years, Agustin Carstens, chief of the Bank for International Settlements (BIS), now acknowledges that central banks will likely soon need to issue their own digital currencies, reports CoinDesk. Carstens told the Financial Times on Sunday that the BIS is supporting global central banks’ efforts to research and develop digital currencies based on national fiat currencies.

- As CoinDesk reports, Russia has no plans to ban Facebook’s Libra currency, says Russia’s deputy minister Alexei Moisseev. The Russian Ministry of Finance will treat the Libra like any other digital asset, regulations for which are coming, according to news agency Interfax.

- Casa’s new mobile app, the Sats App, launched on Wednesday, will make it easier to manage your lightning node on the go, reports CoinDesk. It works like a noncustodial wallet with some unique features; the goal of the app is the help crypto newbies graduate from earning their first bitcoin all the way to managing a lightning node with just one mobile app.

Threats

- After its impressive rally in recent week’s, bitcoin could fall below $10,000 this week as a strong sign of buyer exhaustion has emerged on the weekly chart in the form of a “gravestone doji” candle, writes CoinDesk. The narrative behind this candle is that buyers had pushed process up to unsustainable levels during a specific period, then sellers ended up pushing prices back to the starting point, the article continues.

- A U.K. financial regulator, the Financial Conduct Authority (FCA), said in a press release on Wednesday that it is consulting over an outright ban on the “sale, marketing and distribution to all retail consumers,” of derivatives, reports CoinDesk. This includes CFDs, options and futures, as well as exchange-traded notes (ETNs) linked to “unregulated transferable cryptoassets” by firms operating or based in the U.K.

- On Tuesday, Democrats from the U.S. House of Representatives wrote an open letter to Facebook, reports CoinDesk, calling on a moratorium to all libra development. The lawmakers from the Financial Services Committee and affiliated subcommittees want to first hold hearings to determine how the new cryptocurrency would operate and what protections would be implemented to protect user privacy.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 205.10 | +5.69 | +2.85% |

| Gold Futures | 1,344.60 | -1.50 | -0.11% |

| Natural Gas Futures | 2.39 | +0.05 | +2.27% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -9.57 | -1.60% |

| 10-Yr Treasury Bond | 2.09 | +0.00 | +0.10% |

| Nasdaq | 7,796.66 | +54.56 | +0.70% |

| Oil Futures | 52.53 | -1.46 | -2.70% |

| Hang Seng Composite Index | 3,620.02 | +26.25 | +0.73% |

| S&P 500 | 2,887.01 | +13.67 | +0.48% |

| DJIA | 26,089.61 | +105.67 | +0.41% |

| Korean KOSPI Index | 2,095.41 | +23.08 | +1.11% |

| Russell 2000 | 1,522.44 | +8.05 | +0.53% |

| S&P Energy | 447.48 | -2.21 | -0.49% |

| S&P Basic Materials | 360.98 | +1.78 | +0.50% |

| XAU | 75.81 | +1.48 | +1.99% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.21 | -8.11% |

| S&P/TSX Global Gold Index | 205.10 | +22.96 | +12.61% |

| 10-Yr Treasury Bond | 2.09 | -0.29 | -12.17% |

| Oil Futures | 52.53 | -9.49 | -15.30% |

| Gold Futures | 1,344.60 | +40.90 | +3.14% |

| S&P 500 | 2,887.01 | +36.05 | +1.26% |

| S&P Energy | 447.48 | -23.94 | -5.08% |

| Hang Seng Composite Index | 3,620.02 | -150.49 | -3.99% |

| DJIA | 26,089.61 | +441.59 | +1.72% |

| Korean KOSPI Index | 2,095.41 | +2.63 | +0.13% |

| Nasdaq | 7,796.66 | -25.49 | -0.33% |

| S&P Basic Materials | 360.98 | +21.80 | +6.43% |

| Russell 2000 | 1,522.44 | -25.83 | -1.67% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -20.57 | -3.39% |

| XAU | 75.81 | +7.51 | +11.00% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.39 | -0.47 | -16.29% |

| 10-Yr Treasury Bond | 2.09 | -0.55 | -20.75% |

| DJIA | 26,089.61 | +379.67 | +1.48% |

| Oil Futures | 52.53 | -6.08 | -10.37% |

| S&P 500 | 2,887.01 | +78.53 | +2.80% |

| Gold Futures | 1,344.60 | +37.00 | +2.83% |

| S&P Energy | 447.48 | -37.76 | -7.78% |

| Nasdaq | 7,796.66 | +165.75 | +2.17% |

| Korean KOSPI Index | 2,095.41 | -60.27 | -2.80% |

| S&P Basic Materials | 360.98 | +14.33 | +4.13% |

| Russell 2000 | 1,522.44 | -27.19 | -1.75% |

| Hang Seng Composite Index | 3,620.02 | -238.07 | -6.17% |

| S&P/TSX Global Gold Index | 205.10 | +12.28 | +6.37% |

| S&P/TSX VENTURE COMP IDX | 586.97 | -36.10 | -5.79% |

| XAU | 75.81 | +0.48 | +0.64% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2019):

B2Gold Corp.

Calibre Mining Corp.

OceanaGold Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The KOSPI Index is comprised of 200 of the largest and most liquid issues traded on the Korean Stock Exchange. The Caixin China General Services PMI (Purchasing Managers’ Index) is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private service sector companies. The index tracks variables such as sales, employment, inventories and prices. The Caixin China Manufacturing PMI (Purchasing Managers’ Index) is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private manufacturing sector companies.