Transitory or Not, Inflation Is Here. It Could Be Much Higher Than You Realize

Date Posted: June 11, 2021

Read time: 48 min

I've been writing about the possibility of higher inflation for months, and now it looks to have finally made landfall. The headline consumer price index (CPI) came in at 5% year-over-year, the highest in over a decade.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

I’ve been writing about the possibility of higher inflation for months, and now it looks to have finally made landfall. The headline consumer price index (CPI) came in at 5% year-over-year, the highest in over a decade.

The real rate is likely even higher.

Energy commodities, and gasoline in particular, jumped the most of any other measured item. Energy increased 54.5% year-over-year, gasoline 56.2%, as oil prices hit multiyear highs this week on strong travel demand. A barrel of West Texas Intermediate (WTI) touched $71 today, a level we haven’t seen since October 2018.

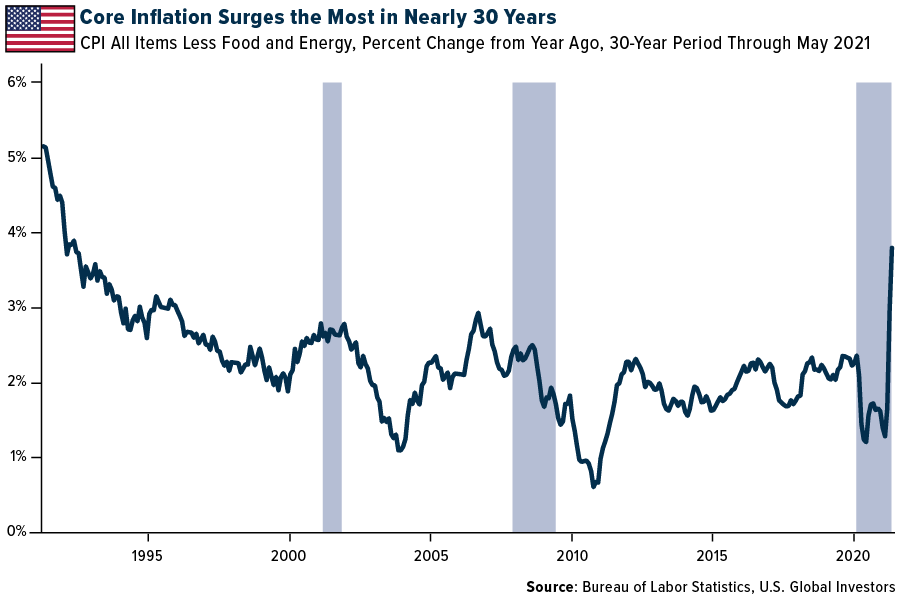

Take a look at what happens when you strip out volatile energy and food prices. Core inflation, as it’s called, surged 3.8% compared to last year—which doesn’t sound impressive until you realize that’s the fastest rate in nearly 30 years. The last time we saw core inflation this high, the top films in America were White Men Can’t Jump and Basic Instinct, and General Motors topped the list of Fortune 500 companies.

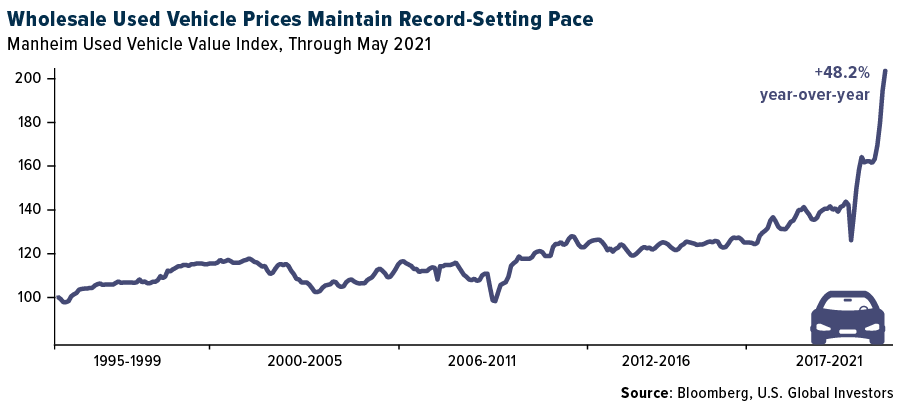

I hope no one reading this is in the market for a new car right now. Thanks to the ongoing semiconductor chip shortage, the supply of new vehicles has all but evaporated, pushing up the price of previously owned cars and trucks. The Manheim Used Vehicle Value Index hit a fresh all-time high in May, suggesting a 48% increase in prices compared to last year. Pickup trucks were up a staggering 70%.

Expectations are mixed for how much longer the chip shortage will last. Goldman Sachs chief Asia economist Andrew Tilton told CNBC this week that he believes we’re in “the worst period” right now, insinuating we’ll see some improvement in the second half of the year. Patrick Gelsinger, CEO of chipmaker Intel, isn’t so sure. He says the shortage could last another two years.

Hope for the Best, Prepare for the Worst

I think policymakers and analysts are just as torn about the potential longevity of this current rash of inflation. The Federal Reserve insists on describing it as “transitory,” mostly in an effort to allay investors’ fears and calm markets.

Only time will tell if this assessment was accurate, but for the time being, the gesture seems to be working: The S&P 500 closed at a new record high yesterday. Meanwhile, gold, historically used as an inflation hedge, barely budged, and bitcoin, a digital version of gold, retreated by as much as 1.8%.

It’s possible that May’s inflation rate was already priced in. That being said, I would still strongly consider adding to my gold exposure, including gold mining stocks. Bitcoin should also be a consideration.

As I’ve pointed out before, I believe the CPI significantly understates the impact inflation has on household wealth. The real rate is likely much higher. An alternate measure, John Williams’ Shadow Government Statistics, shows that inflation could actually be closer to 13% year-over-year. Invest accordingly.

On the Road Again

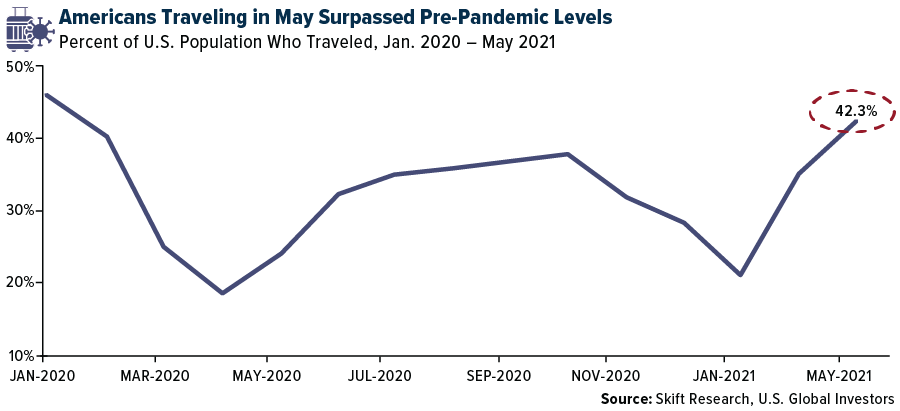

At the same time that new vehicles are in short supply, Americans have begun to travel as much as they ever have, a key driver behind rising fuel prices. According to the travel industry news website Skift, the number of Americans who traveled in May surpassed those who traveled in February 2020, before the pandemic. More than 42% of Americans said they traveled within the U.S., compared to 40.5% 16 months ago.

And it’s not just vehicular travel we’re talking about here. U.S. airports have gotten so unexpectedly busy that the Transportation Security Administration (TSA) is seeking internal office volunteers to handle non-screening tasks such as management of security lines

This is hugely supportive of travel industry equities, airlines in particular, as we progress deeper into the busy summer travel season.

Although only 2% of Americans traveled outside of the U.S. in May, compared to 7% in February 2020, I expect this to change soon as vaccination rates improve. This week, France became the latest European Union (EU) member to start accepting vaccinated visitors from the U.S. and elsewhere, and a new travel pass that allows people to move more freely between European countries was finally endorsed by EU lawmakers.

“Travel companies need to be prepared” for the summer surge, commented Haixia Wang, VP of research at Skift.

That’s precisely what domestic and international airlines continue to do. Air France is set to bring 22 aircraft out of storage in order to significantly increase flights to the U.S. Air Canada will reportedly resume a number of international flights this month, from Canada to India, Mexico, the Caribbean and more.

Watch my six reasons to invest in airlines before the make a full recovery from pandemic lows. Click here!

Index Summary

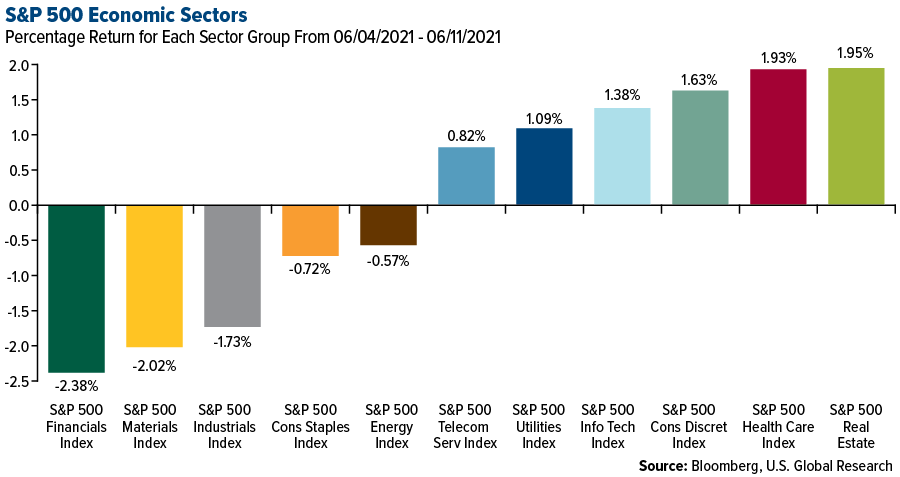

- The major market indices were mixed this week. The Dow Jones Industrial Average lost 0.80%. The S&P 500 Stock Index rose 0.33%, while the Nasdaq Composite climbed 1.85%. The Russell 2000 small capitalization index gained 2.05% this week.

- The Hang Seng Composite lost 0.26% this week; while Taiwan was up 0.39% and the KOSPI rose 0.29%.

- The 10-year Treasury bond yield fell 10 basis points to 1.45%.

Airline Sector

Strengths

- The best performing airline stock for the week was Avianca, up 62.9%. Volaris, a leading airline in Mexico, continues to do well, with traffic up 17% from pre-pandemic levels, reports Seeking Alpha. The company’s second-quarter unit revenue could be up between 8-10% with capacity at 110-113% of 2019 levels. Volaris has seen structural improvements in its competitive position in Mexico during the pandemic.

- Revenue growth continues to trend favorably across the airline industry. JetBlue, for example, has seen success at selling ancillary services as people are back to flying. The company is on track to make its goal of $100 million of EBIT (earnings before interest and taxes) from ancillary sources by next year. Bookings are now twice that seen in 2019. Southwest Airlines published an investor update guiding to the better end of both May and June’s prior revenue guides and introduced a July revenue outlook that is sequentially better than June. Southwest is now guiding current quarter revenue to be down 32% versus 2019, which compares favorably to the consensus of down 35%.

- The positive trend in European airline bookings continued in the past week with a significant improvement in both intra-European and international bookings. Intra-European net sales increased by 9% to -59% of 2019 levels versus -68% in the prior week, the highest growth since June 2020. Seven EU countries have begun using the new digital COVID certificate which allows frictionless travel within the block, with the remainder set to follow suit by July 1.

Weaknesses

- The worst performing airline stock for the week was Great Lakes Aviation, down 30.0%. The cost of jet fuel is rising, a major input cost for airlines and potential headaches for those still struggling from depressed demand during the height of COVID. The current price of $1.76 per gallon is approaching pre-pandemic levels.

- The summer capacity ramp up in Europe is slightly below expectations. It is 38% below 2019 levels on long haul flights and 17% below on short haul flights compared to 2019. Additionally, airlines are deploying smaller capacity at shorter ranges to the detriment of widebodies.

- Airline bookings are slowing after the Memorial Day holiday. The number of domestic and international tickets sold both decelerated and fell 32.2% versus falling 28.2% the week before and -50.8% versus -34.8% last week, respectively, versus 2019. Similarly, the number of domestic leisure tickets sold reverted back down alongside a step down of corporate tickets sold.

Opportunities

- Airlines continue to ramp up capacity. Domestic industry capacity is expected to decline only 1.6% in the third quarter of 2021. Current published schedules indicate June, July and August capacity at 88%, 92% and 96% of 2019 levels, respectively.

- U.S. airline industry web traffic increased 6% week-over-week, according to research from Evercore ISI, which is the sixth consecutive weekly increase. In Latin America, web traffic increased 6% week-over-week, which is the fourth consecutive week of growth and is down 28% versus 2019. Ultimately, a portion of this increased web traffic will be converted to bookings, the research group notes.

- United Airlines placed an order for 15 “Overture” aircraft from Boom Supersonic (a Denver-based aerospace company), which claims the aircraft will take flight in 2029. The Overture airliners are expected to be the first large commercial aircraft to be net-zero carbon, according to United. “United continues on its trajectory to build a more innovative, sustainable airline and today’s advancements in technology are making it more viable for that to include supersonic planes,” said United CEO Scott Kirby.

Threats

- The U.K. government is probing whether British Airways and Ryanair have broken consumer laws regarding customer refunds. The companies are being accused of refusing to allow refunds when consumers were not able to fly, offering vouchers instead.

- Delta Air Lines retired 200 aircraft during the pandemic and anticipates retiring a further 200 aircraft over the coming years. The company highlighted that because so many widebodies have been retired, particularly high capacity widebodies such as A380s and 747s, the industry will experience a shortage of widebody capacity when international traffic ultimately recovers.

- Delta Air Lines has indicated that the time it takes to bring an aircraft back into service can be lengthy. In fact, according to management, it can take as long as one to five months to bring an aircraft back into service. This includes the time required time to conduct airframe checks and engine overhauls.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 2.0%. The best performing country in Asia this week was Thailand, gaining 1.7%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 3.7%. The Malaysian ringgit was the best performing currency in Asia this week, gaining 0.46%.

- Taiwan exports increased 38.6% last month from a year earlier to a record $37.4 billion. The country’s exports were supported by global demand for Taiwan’s computer chips and other technology goods, with exports to Europe, South Korea and Southeast Asia all up more than 50% compared to a year earlier.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 1%. The worst performing country in Asia this week was Hong Kong, losing 0.26%.

- The Polish zloty was the worst performing currency in emerging Europe this week, losing 1.1%. The Pakistani rupee was the worst performing currencies in Asia, losing 0.83%.

- Inflation is on the rise globally. The central bank of Russia hiked its repo rate this week, making a third consecutive increase in the past three months. Other central banks may start to switch to tightening monetary policies as well.

Opportunities

- Joe Biden left the U.S. on Wednesday and headed to Europe for his first foreign trip. He plans to remain in Europe for eight day and meet EU officials and leaders. Before he began his journey, he expressed that this trip is about realizing America’s renewed commitment to allies and partners and demonstrating the capacity of democracies to both meet the challenges and deter the threats of this new age. This trip presents an opportunity to smooth trade deals between both continents and quiet down some geopolitical tensions. The presidents of Turkey and Russia are scheduled to have personal discussions with Biden.

- The European Central Bank (ECB) met this week and left all rates unchanged and decided not to change its bond buying program for now. The ECB will continue its bond buying program in the coming weeks despite some policymakers calling for tapering due to the eurozone economic recovery. The ECB has just over 700 billion euros of the overall 1.85 trillion euros left to spend under the current crisis-fighting policy, which is due to last until at least March 2022.

- Summer travel looks much better this year in Europe. The European Parliament approved the introduction of mutually recognized certificates that will allow quarantine-free travel within the bloc. It should operate across all 27 EU member states by July 1. Airlines may continue to recover from last year’s travel restrictions.

Threats

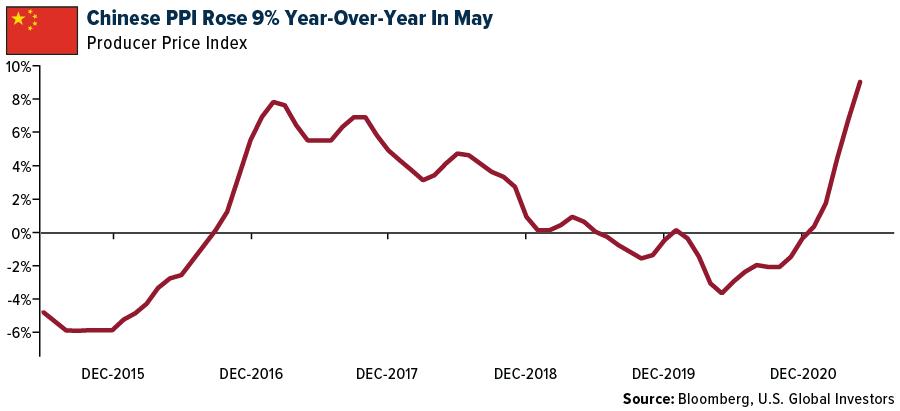

- China’s inflation pressure continues to mount. The producer price index (PPI), which measures the change in the price of goods as they leave production facility, rose 9% year-over-year in May, making the highest year-over-year growth since 2008, and compared to 6.8% in April. The high cost of production for companies may lead to earnings losses. Inflation in May increased moderately at 1.3% versus consensus at 1.6% and 0.9% in April. The gap between China’s PPI and CPI is the highest on record, surpassing the previous peak of 7% in 2017.

- On Tuesday, the U.S. approved the Innovation and Competition Act, a $250 billion package aimed at challenging China’s technological ambitions. About $190 billion would be directed at U.S. technology and research to better compete globally. Another $45 billion would increase U.S. production and research into semiconductor and telecom equipment, as well as design and manufacturing initiatives.

- China reported a Covid-19 outbreak in the major trading hub in Guangdong province. More than 100 new cases have been reported since late May in the region, leading to strict countermeasures from the government. Yanitan container terminal in Shenzhen suspended exports for almost a week recently after workers tested positive.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was natural gas, up 6.01%. U.S. natural gas futures gained amid forecast of warmer weather and an increase in natural gas exports.

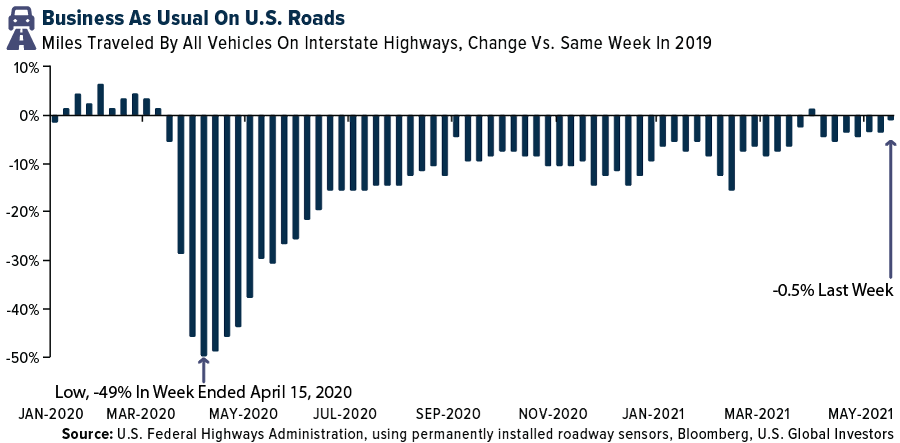

- Oil rallied to its third straight weekly gain as demand for the commodity improved and the International Energy Agency (IEA) warned that the market will need extra supply next year. With road traffic in the U.S. and most of Europe inching towards pre-pandemic levels, the IEA expects that the Organization of Petroleum Exporting Countries and its allies (OPEC+) will have to increase output to keep the market adequately supplied. Further, the IEA expects demand for oil to hit pre-pandemic levels by the end of 2022, mainly due to a lag in recovery for jet fuels. West Texas Intermediate (WTI) crude rose 1.67% during the week to settle at $70.78, while Brent Crude traded at $72.60, up 1.00% this week. The chart below shows the weekly change in miles traveled by U.S. vehicles compared to 2019 levels.

- The U.S. Interior Department is planning on auctioning off eight lease areas for the development of offshore wind power in the Atlantic Ocean, between New York’s Long Island and New Jersey. The department noted that the proposed sites have the potential to generate up to 7 gigawatts of electricity, enough to power more than 2.6 million homes. This offshore wind lease is the first sale under the Biden administration’s plan to deploy 30 gigawatts of offshore wind power by 2030. Head of the National Ocean Industries Association commented on the auction, saying that the coastal states of New York and New Jersey, with their massive populations, are integral to the development of offshore wind farms in the U.S., and will support jobs and businesses throughout the nation.

Weaknesses

- The worst performing commodity for the week was lumber, down 17.52%. Lumber prices fell for the eighth straight day due to rising supply and homebuilders seeking alternative materials.

- President Joe Biden’s administration’s decision to provide relief to U.S. refiners on biofuel blending mandates led to a drop in prices of corn, soybean oil and the crackspread, which is a rough measure of profit for processing a barrel of oil. The crackspread for gasoline and diesel futures against the West Texas Intermediate (WTI) crude dropped to the lowest since March, after plunging as much as 10%. The U.S. government’s existing mandate requires the nation’s oil refiners to blend biofuels, like ethanol, into their fuel supply. Refiners use corn and soybean oil in the production of biofuels. Corn and soybean oil had been surging recently in part as more oil refiners ramped up plans to make renewable fuels, putting the refiners in direct competition with food processors and the meat industry, which uses these grains as fodder for its livestock.

- Companies in the lithium mining sector believe that global electric vehicle and battery producers are not taking the challenges of the long-term lithium supply seriously. CEO of Pilbara Minerals Ltd., an Australia-based lithium miner, said at an energy conference that engagement from electric vehicles and battery manufacturers has been poor regarding supply-side issues that might spring up in the future. Credit Suisse analysts forecast that the lithium supply could see a shortfall by 250,000 tons by 2025, while other forecasts project the shortage to blow out to 1 million tons by 2030. This is the result of decreased investment in exploration of new lithium deposits at a time when countries across the world are committing to increasing the proportion of electric cars on the roads.

Opportunities

- BP PLC, one of the largest oil and gas companies in the world, is devising a strategy to spin off its operations in Iraq’s giant Rumaila oil fields, one of the largest in the world, into a stand-alone company which will be jointly owned by China National Petroleum Corp. The new company will hold its own debt, separate from BP, and is expected to distribute profits via dividends. This spin-off is a part of the oil giant’s strategy to shuffle its assets and investment plans as it pivots towards a low-carbon future, giving BP more flexibility to invest in alternate energies by reducing its spending on oil and gas.

- Royal Vopak NV, the world’s largest independent oil storage company based in Netherlands, announced its partnership with Elestor BV, a Dutch battery startup, to develop cheaper batteries that can store electricity in large quantities. Elestor’s battery, which stores electricity in molecules, uses two tanks of hydrogen and dissolved bromine, both of which are cheap and abundantly available. The capacity of the batteries can be boosted by simply increasing the size of the vessel. This strategic partnership is a sign of how companies in the oil and energy industry are planning of positioning themselves to compete in a greener future.

- In its latest bid to tame the surge in commodity prices, China is planning to use its massive state reserves after targeting the country’s futures market last month, when it singled out hoarders and speculators and pressured firms to pare back on their bullish bets. China is set to expand its pork inventories to extend its control over the market, increase its capacity to store coal reserves and offer metals like copper, aluminum, and zinc directly to end-users to curb the price rally. Chief Economist for Greater China at ING Bank, Iris Pang, noted that the use of state reserves might create a self-fulfilling psychological downward price spiral and could deter speculators of long positions on commodity prices, stabilizing the market.

Threats

- The United Nations’ Food & Agriculture Organization (FAO) noted in a report this week that the cost of importing food is expected to rise by 12%, to an all-time high of $1.72 trillion, led by an increase in prices of grains, vegetable oils and oilseeds. It added that the soaring cost of staples will hit poor nations particularly hard, with developing nations facing 21% increase in their total bill, compared to a 6% increase for the richest nations. Furthermore, the rise in freight costs and a sharp fall in local currencies of less-developed nations is leaving countries vulnerable to widespread hunger.

- Restaurant Brands International Inc., which owns Burger King, Popeyes and Tim Hortons amongst other brands, noted in a company report that it is experiencing significant inflation across meats and oils compared to historical five-year averages, and that price increases for meats have exceeded their most bullish forecasts. One of the drivers of this price inflation, according to the report, is that dining out is inching towards pre-Covid levels while grocery sales remain high, putting pressure on supply chains amidst an extremely tight labor market. The company is projecting an 8% increase in prices of finished beef products for the second half of 2021, compared to the first half, for its store owners.

- Citigroup Inc. reported that the rising cost of steel, cement and other supplies and services is leading to higher costs for oil explorers in the shale industry. The New York-based bank expects inflation for the sector to reach 12% by the end of 2021 in North America, with the steel prices for the drill pipe used in new wells to rise by 50%. Although oil production has remained subdued in the U.S. since the pandemic began last year, the number of rigs drilling for crude oil and natural gas has almost doubled since bottoming out in August 2020. With an increased competition in North America, services providers have been unsuccessful in hiking prices and are strategizing plans to pivot away from the continent in search of growth overseas.

Domestic Economy and Equities

Strengths

- Initial jobless claims declined to another post-pandemic low of 376,000, though missed consensus of 368,000. Continuing claims were reported lower by 298,000 week-over-week to 3.499 million, beating 3.62 million consensus.

- U.S. job openings jumped to 9.3 million from 8.3 million in April, setting a new record high. The reading comes in above the median estimate of 8.2 million and marks a fourth straight gain.

- Biogen Inc, an oil and gas exploration and production company, was the best performing S&P 500 stock for the week, increasing 38.62%. Shares gained after U.S. regulators approved its Alzheimer’s therapy. Biogen plans to sell the therapy under the brand name of Aduhelm. It will cost $56,000 a year.

Weaknesses

- Much of the focus this week has been on rising inflation. Month-over-month inflation increased by 0.6% versus expected 0.5% and prices rose by 5% year-over-year versus expected 4.7%.

- The U.S. saw an up-tick in large corporate bankruptcy fillings last week, led by two health care companies that sought Chapter 11 protection from creditors. As of June 7, 64 large companies have sought Chapter 11 protection this year, higher than the 10-year average of about 59, but lower than the 103 filings seen in the same period in 2020.

- Organon & Co., a pharmaceutical company, was the worst performing S&P 500 stock for the week, losing 13.2%. Shares sold off after the company spin-off from Merck recently.

Opportunities

- So far this year, the muni market has outperformed all other highly rated fixed income categories. Going forward, muni returns will be supported for the rest of 2021, Copper Howard says from Bond Insights. Prospects for higher taxes in U.S. should keep demand for municipal bonds high, which are generally exempt from federal and potentially state income tax.

- Bond yields are declining again, which is stimulative for the economy. The 10-year government yield declined to 1.5% from a recent high of 1.7% at the end of March. The Cornerstone research team believes that yields will continue to decline, which should support equity prices and economic activity.

- President Joe Biden began his first overseas trip of his presidency in the UK. He will be attending meetings with G7 leaders through Sunday. The agenda for that meeting is broad, with the group expected to discuss the coronavirus recovery, fair trade and climate issues. Biden’s European trip will conclude on June 16 in Geneva with what is seen as a more momentous meeting with Russian President Putin. Among other topics, the two are expected to discuss Russia’s degree of involvement in the recent cyberattacks on corporate targets, FactSet reports.

Threats

- President Biden has ended infrastructure talks with a group of Republican senators after the two sides failed to reach an agreement. The administration is now shifting its efforts to a coming proposal from a bipartisan group on senators led by Democratic senators Joe Manchin and Krysten Sinema.

- The Federal Reserve is likely to announce in August or September a strategy for reducing its massive bond buying program but won’t start cutting monthly purchases until early next year, a Reuters poll of economists found. Nearly 60% of economists, or 29 of 50, who responded to an additional question said a much-anticipated taper announcement from the central bank will come next quarter, despite a patchy recovery in the job market in recent months.

- A number of companies has warned in recent days that higher input costs could weigh on margins in quarters ahead. Procter & Gamble and Lowe’s have announced higher prices in recent weeks to offset soaring input and transportation costs in an effort to protect their profit margins, while Chipotle said this week it would increase prices by 3-4% to cover higher labor costs.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Amp, rising 95.31%.

- El Salvador’s legislature voted in favor of recognizing Bitcoin as an official legal tender. The nation’s president, Nayib Bukele, signed the bill into a law, making it the first country to adopt the largest cryptocurrency as a legal tender. In a Twitter space conversation, President Bukele pitched his vision as an effort to increase financial inclusion in the nation where only 30% of citizens have access to financial services. He added that the government will act as a backdrop for businesses that do not want to take on the risk of a volatile cryptocurrency by setting up a $150 million trust at the Development Bank of El Salvador to instantly convert Bitcoin to U.S. dollars.

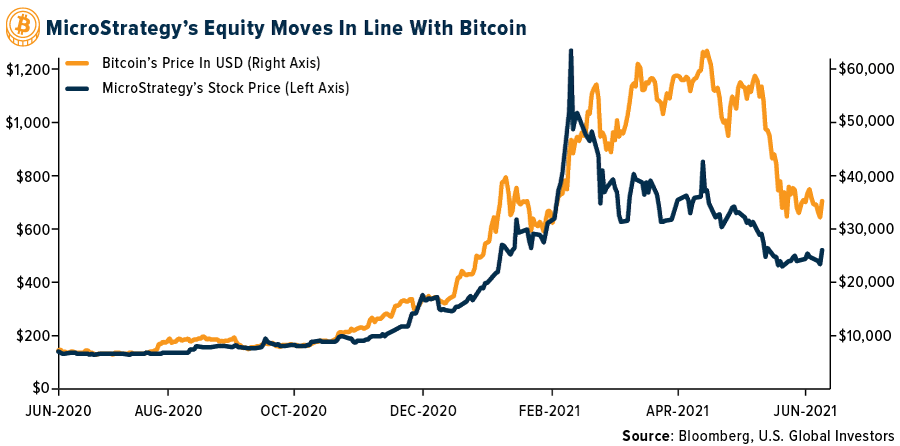

- MicroStrategy Inc., led by CEO and crypto bull Michael Saylor, raised $500 million through a junk bond sale to buy more Bitcoin. After announcing the sale of junk bonds to raise $400 million, the debt offering was raised as the company got orders for more than $1.6 billion. The technology company that provides business intelligence, analytics and cloud-based services has been touted as a proxy to Bitcoin, as the company currently holds more than 90,000 coins which it plans to store under a subsidiary named MacroStrategy LLC. The chart below shows that Bitcoin and MicroStrategy’s stock price have moved in tandem.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Internet Computer, down 44.36%.

- Government of the Qinghai Province in China issued an order instructing all cryptocurrency miners to shut down their operations, following similar orders in Xinjiang and Inner Mongolia. The mandate, issued by the Qinghai Industry and Information Technology Department, stated that cryptocurrency miners will not be approved to operate in the province and that the provincial government may also randomly inspect businesses to ensure compliance with new guidelines. China’s crackdown on crypto mining is seen as part of a broader move to curtail the country’s carbon emissions as the Chinese electricity grid remains heavily reliant on coal.

- Chainalysis, the blockchain analytics firm, reported that Ryuk, a cybercriminal group, has collected more than $100 million in cryptocurrency ransoms in the last year alone. The Wall Street Journal estimated that Ryuk had struck 235 U.S. hospital facilities with its ransomware attacks, disrupting medical care and endangering patients. Although cryptocurrencies are not the main reason for the growing popularity of ransomware attacks, it does a play a major role in allowing such groups to carry out attacks and receive the ransom.

Opportunities

- ForUsAll, a 401(k)-provider based in San Francisco, is partnering with Coinbase to allow its clients to invest part of their retirement plans in cryptocurrencies. According to the details of the partnership, employees enrolled in plans administered by ForUsAll will be able to invest up to 5% of their contributions into cryptocurrencies using Coinbase’s institutional crypto platform, with the option to invest in over 50 cryptocurrencies. Currently, ForUsAll has around 400 employer clients and manages $1.7 billion in assets.

- Atlanta-based Invesco, the investment management giant with $1.5 trillion in assets, is planning on launching two cryptocurrency-focused exchange-traded funds (ETFs). According to a filing with the U.S. Securities and Exchange Commission (SEC), around 85% of the proposed Invesco Galaxy Blockchain Economy ETF and Invesco Galaxy Crypto Economy ETF will invest in crypto-linked equities and the rest will be in trusts or funds that hold cryptocurrencies.

- The Texas Department of Banking announced that it will allow state-chartered banks to custody crypto assets on behalf of their customers. The state regulator also noted that the banks can only provide crypto custody services if there are adequate protocols, compliant with existing legal frameworks. Individual banks will have the opportunity to decide what type of custody services they can based on their expertise, risk appetite and business model, and could range from storing copies of customer’s private keys to controlling their crypto assets.

Threats

- Banks in Kenya have been issuing alerts to customers who have used debit and credit cards to buy cryptocurrencies on various exchanges, citing that virtual currencies like Bitcoin are not legal tender in the country. BitcoinKE, a community and media advocacy company in the blockchain and cryptocurrency space in Kenya and East Africa, reported that some banks are also advising customers to not buy, hold or trade cryptocurrencies. Furthermore, BitcoinKE added that the NCBA Bank Kenya sent an email to its customers stating that no protection exists for any customer if a platform that holds cryptocurrency or facilitates cryptocurrency trading fails or goes out of business.

- The U.S. Securities and Exchange Commission (SEC) issued its second warning regarding risks of investing in Bitcoin futures-focused funds, reiterating that the largest cryptocurrency remains a highly speculative investment. It also highlighted that due to Bitcoin’s volatility, it may not be safe yet to approve an exchange-traded fund (ETF) under the Investment Advisers Act of 1940.

- WazirX, an Indian cryptocurrency exchange that was acquired by Binance in 2019, came under scrutiny by India’s Enforcement Directorate (ED) for alleged violations of the nation’s Foreign Exchange Act (FEMA). The ED tweeted that cryptocurrency transactions worth more than $389 million are under investigation, which the ED came across during a money-laundering investigation into illegal online betting applications, which involved Chinese nationals. The ED is also alleging that WazirX failed to gather the required information to vet its clients and transactions, failing to meet the country’s Anti-Money Laundering and Combating Financing of Terrorism Laws.

Gold Market

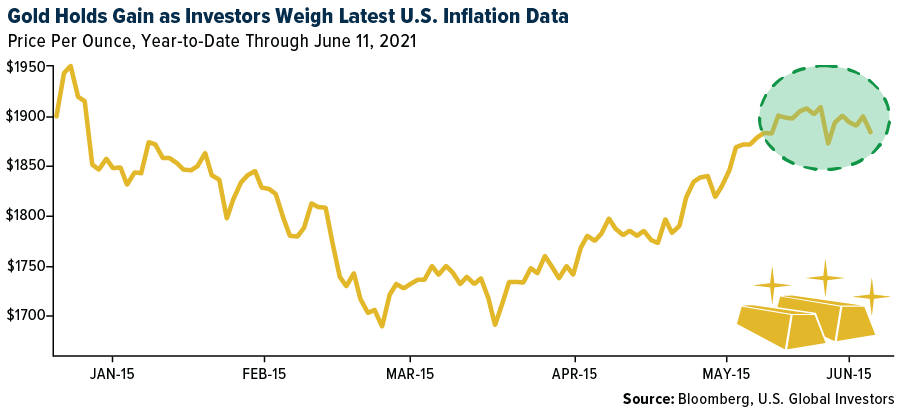

This week spot gold closed the week at $1,877.53, down $14.06 per ounce, or 0.74%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.53%. The S&P/TSX Venture Index came in up just 0.17%. The U.S. Trade-Weighted Dollar rose 0.43%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-8 | Germany ZEW Survey Expectations | 86.0 | 2.5% | 2.0% |

| Jun-8 | Germany ZEW Current Situation | -28.0 | -9.1 | -40.1 |

| Jun-10 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jun-10 | CPI YoY | 4.7% | 5.0% | 4.2% |

| Jun-10 | Initial Jobless Claims | 370k | 376k | 385k |

| Jun-15 | Germany CPI YoY | 2.5% | — | 2.5% |

| Jun-15 | PPI Final Demand YoY | 6.2% | — | 6.2% |

| Jun-16 | China Retail Sales YoY | 14.0% | — | 17.7% |

| Jun-16 | Housing Starts | 1640k | — | 1569k |

| Jun-16 | FOMC Rate Decision (Upper Bound) | 0.25% | — | 0.25% |

| Jun-17 | Eurozone CPI Core YoY | 0.9% | — | 0.9% |

| Jun-17 | Initial Jobless Claims | 360k | — | 376k |

Strengths

- The best performing precious metal for the week was silver, up 0.45%, but still finding resistance trying find a level above $28 to hold for the last month. De Beers has raised some rough-diamond prices by about 10%, as the world’s top producer cashes in on rampant demand from cutters and polishers. The global palladium market is expected to be in deficit on a rebound in the auto industry, tougher pollution controls and an unexpected tightening of supply after the world’s largest producer said flooding at its Arctic mines will curb output. Gold prices are increasing as comments by Treasury Secretary Janet Yellen on inflation raised expectations for inflation, which is positive for gold. Recently reported CPI data indicated a surge in inflation in May. Demand should also be strong, as one in five central banks intend to increase reserves over the next year, according to the World Gold Council (WGC). One in three central banks in emerging markets are likely to increase gold holdings in the next year.

- SSR Mining Inc. announced that it has amended its existing undrawn revolving credit facility on favorable terms, increasing the Facility size from $75 million to $200 million. The term of the Facility has been extended by four years to June 8, 2025.

- A junior Australian miner is confident that its gold discovery in the nation’s Pilbara region – more commonly known as the world’s premier iron ore province – will propel the company into the ranks of the nation’s top bullion producers. De Grey Mining Ltd. has seen its market value surge to A$1.9 billion ($1.5 billion) from just over A$45 million in about 18 months because of optimism surrounding its Mallina project. The company has set itself the goal of becoming a top 10 producer in Australia with output seen at over 300,000 ounces a year for at least a decade.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.41%, perhaps on news that a project in Russia has received funding that is projected to produce 4.2 million palladium ounces per year. Fed up with years of political dysfunction and wracked by the world’s worst per capita COVID death toll, Peruvians have made a radical new choice for president. The results of Sunday’s runoff appear to show that Pedro Castillo, a Marxist-leaning former schoolteacher, has edged out Keiko Fujimori, the authoritarian-minded daughter of the country’s former dictator. Castillo has ambitious policy proposals, which his supporters say most Peruvians want: rewrite the constitution, spend 10% of GDP on education and health, and redistribute mining profits to fund social programs.

- Centerra Gold’s Kumtor Gold Company Chapter 11 hearings have started. The company’s strategy is to pursue Ontario Superior Court proceedings against former CG Director Tengiz Bolturuk by seeking to prevent him from having any direct or indirect contact with Kumtor Mine management. They want to start international arbitration in Stockholm as provided for in the 2009 Investment Agreement. Additionally, the Chapter 11 bankruptcy proceedings are seeking a Worldwide Automatic Stay in the Southern District of New York.

- A drive by mining companies to hire more women has lost momentum, leaving the industry as one of the world’s most male-dominated professions. In the U.S., 14.3% of people employed in mining in 2020 were women, only 0.3 percentage point higher than in 2015. In other news, gold imports by India plummeted in May. This is due to the recent surge of COVID in India and restricted mobility. Only 11.3 tons of gold were imported, compared to 70.3 tons in April.

Opportunities

- Endeavor Mining recently had an analyst meeting with several positive developments. The company highlighted balancing near-term growth projects Sabodala-Massawa Phase 2 and Fetekro, as well as exploration, and returning more capital to shareholders via dividends and opportunistic buybacks. Endeavour expects to achieve its targeted $250M net cash position in the near-term. The company expects annual production to average 1.4-1.5 million ounces thorough 2023, before increasing to 1.5 million ounces in 2024 and 1.6 million ounces in 2025. Endeavour is targeting 30% lower emissions by 2030, and net zero by 2050. To achieve this, a focus area is implementing solar power at the mines. The company has identified potential to add up to 150MW solar power across its portfolio.

- Aya Gold & Silver reported very positive drilling results. The results were 6,437 grams/ton Ag over 6.5m incl 24,613 grams/ton over 0.5m, 12,775 grams/ton over 0.5m and 11,483 grams/ton over 0.5m. This newly discovered high grade zone is only 35m from surface and 75m east of the current resource.

- Newcore Gold announced the positive results of an updated independent Preliminary Economic Assessment completed for the Company’s 100%-owned Enchi Gold Project in Ghana. Average annual gold production in years two through five may be 104,171 ounces gold, with 983,296 ounces gold recovered over an 11-year life of the mine. Operating costs are estimated at $923 per ounce of gold, with cash costs estimated at $1,043 per ounce of gold.

Threats

- Gold will surge to fresh highs next year, but investors seeking currency alternatives as global debt balloons should look to Bitcoin, according to a $7.5 billion hedge fund, SkyBridge Capital. Former Treasury Secretary Lawrence Summers says cryptocurrencies could stay a feature of global markets as a form of digital gold.

- Royalty company streaming business models in part rely upon incorporation in U.S. and Canada, while receiving production and profits in a low-taxation jurisdiction. The risk of increased minimum corporate taxation applied to G7 countries could affect the streaming business’s offshore taxation structure, which has the potential to affect existing streaming transactions in place and the pricing of future transactions. The nature of implementation and timing of potential changes are not yet clear, and various key questions are outstanding, including how deductions for stream deposits will be implemented and whether a corporate tax rate >15% will be sufficient to avoid this taxation being applicable.

- Sarah House and Shannon Seery of Wells Fargo & Co. note that inflationary pressures may not be as short-lived as the Fed contemplates. Core inflation over the last three months has increased to 5.2%, the largest jump since 1991. If the Fed starts raising interest rates too early in this recovery, that could hurt gold’s chances to make further gains.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2021):

JetBlue Airways Corp.

Southwest Airlines

United Airlines

Delta Air Lines

SSR Mining Inc.

De Grey Mining Ltd

Centerra Gold Inc.

Aya Gold & Silver Inc.

Newcore Gold Ltd.

Air Canada

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Fortune 500 is an annual list compiled and published by Fortune magazine that ranks 500 of the largest United States corporations by total revenue for their respective fiscal years. The Manheim Used Vehicle Value Index is a time-series measurement of wholesale used vehicle prices.