What’s With All the Mass Protests? (Hint: It’s Not About Income Inequality)

Date Posted: November 15, 2019

Read time: 56 min

The answer I happen to be looking for is that these countries, among others, are seeing mass protests at the moment. Hong Kong's appears to be the longest-running at five straight months now. With so many of them happening around the world all at once, it raises the question: Are they related?

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Protests in Puerto Montt, Chile | October 2019

Protests in Puerto Montt, Chile | October 2019Photo by: Natalia Reyes Escobar | Attribution-Share Alike 4.0 International

Quick! What do Hong Kong, Chile, Ecuador and Lebanon all have in common with one another?

The answer I happen to be looking for is that these countries, among others, are seeing mass protests at the moment. Hong Kong’s appears to be the longest-running at five straight months now. With so many of them happening around the world all at once, it raises the question: Are they related?

That depends on who you ask.

If you get your news from the “mainstream” media, you’re probably being led to believe that the protests are all about income inequality and that protesters are laying their grievances solely at the feet of the wealthy.

Although this may be part of it, the inequality narrative completely ignores the fact that the demonstrations are, at the end of the day, in response to government incompetence and failed socialist policies. If you look across the spectrum of global unrest, you’ll find that the common denominator is not billionaires and other successful people but corrupt, power-hungry bureaucrats and politicians.

In Hong Kong, residents are demanding democratic reforms and greater autonomy. In Lebanon, it’s corruption, a lack of accountability and bank secrecy laws that allow officials to steal tens of billions of dollars in public funds. The protests in Chile were sparked by a hike in subway fare in Santiago, the nation’s capital.

Reinforcing Peoples’ Confirmation Bias

Sadly, all of this is downplayed in the media. Corruption and mismanagement don’t get the blame for the unrest. Instead, it’s the rich who are cast as the villains suppressing the masses.

Why? Because it reinforces some people’s confirmation bias against millionaires and billionaires.

Without the inequality narrative, far-left lawmakers in the U.S. have no other grounds to raise taxes and push for more government control and socialist policies—all in an effort to “solve” inequality.

But this is faulty thinking. What’s more, it adds fuel to the anti-business, anti-wealth sentiment that’s destroyed otherwise thriving economies such as Cuba, Venezuela and others.

In some cases, the bias only seems to be worsening. This week, progressive presidential candidate Elizabeth Warren’s website began selling $25 mugs that have “BILLIONAIRE TEARS” written in bold text on them. “Savor a warm, slightly salty beverage of your choice in this union-made mug as you contemplate all the good a wealth tax could do,” the website reads.

Such disdain for the most successful among us is a slippery slope that leads only to economic and financial stagnation, not to mention mediocrity.

Headwinds to Junior Miner Speculation

Socialist policies that punish entrepreneurialism and innovation have created additional uncertainty for explorers and producers of metals and other materials that all of us depend on.

Last week I was in Lima, Peru, attending the Mining & Investment Latin America Summit, where I heard from a number of industry leaders that mining in South America has become more challenging in recent years. One of the biggest reasons why is that the burden for taking care of local communities has, in many cases, fallen on the miners’ shoulders. Venezuela’s corrupt socialist president Nicolas Maduro continues to destabilize and finance radicalism throughout the continent using revenue from narcotics, and mining companies often end up having to pay the price.

Chilean lawmakers, for instance, are considering a new tax on mining and mineral extraction to address the country’s social unrest I described earlier.

As you can imagine, this could discourage speculation in the junior mining area. Think of it this way: What if your gambling or lottery winnings were taxed at 50 percent or higher? I suspect there would be fewer people headed to Las Vegas or buying lotto tickets.

But Latin America isn’t the only region causing uncertainty for miners. Late last month, British Columbia (BC) became the first Canadian province to pass legislation based on the United Nation’s Declaration on the Rights of Indigenous Peoples, or UNDRIP. Intended to end “discrimination and conflict” and ensure “more economic justice and fairness,” UNDRIP has some BC-based mining companies wondering if their rights to extract minerals on lands once inhabited by Native peoples could be undermined.

Bullish on Metals and Minerals

Be that as it may, I’m still extremely bullish on metals and minerals. Every year, some 140 million people are born, and each one of them will need a fresh supply of commodities for their homes, automobiles, appliances, smartphones and more. It’s been estimated that each American requires an average 38,449 pounds of various minerals every year.

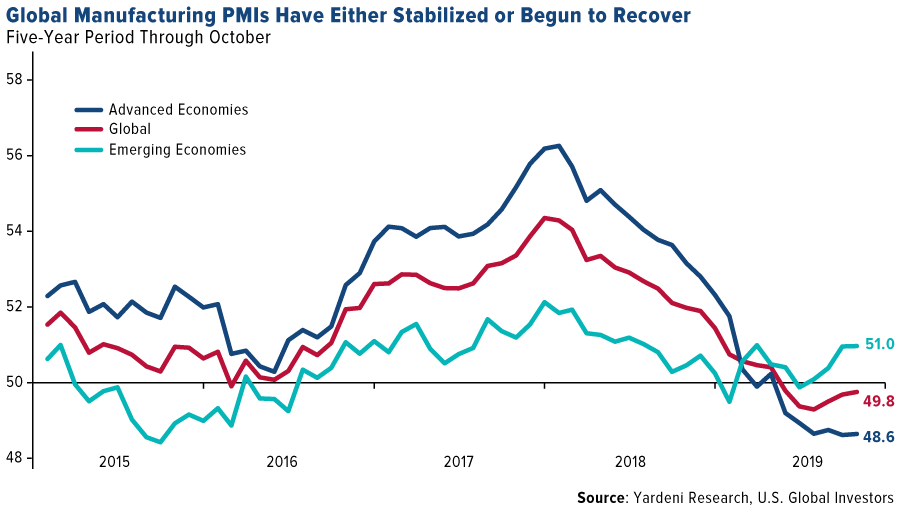

Also driving my bullishness right now is the likelihood that the global manufacturing purchasing manager’s index (PMI) looks to have either stabilized (in advanced economies) or begun to recover (in emerging economies). As I’ve explained many times before, the PMI is a leading indicator of commodities demand from factories and manufacturers.

In a research note dated November 10, Cornerstone Macro founder and economic analyst Nancy Lazar writes that the firm’s model suggests a PMI “upturn is underway, supported by lower global interest rates… and the modest improvement in China.”

A sign that reports of China’s slowdown have been overdone includes the news that sales of excavators by Chinese manufacturers hit a record high this year as hopes escalate that the government will stimulate the economy by boosting infrastructure spending.

According to Caixin Global, Chinese manufacturers sold 196,222 of the earth-moving machines, essential for large construction projects. Almost 90 percent of these excavators were purchased by domestic firms.

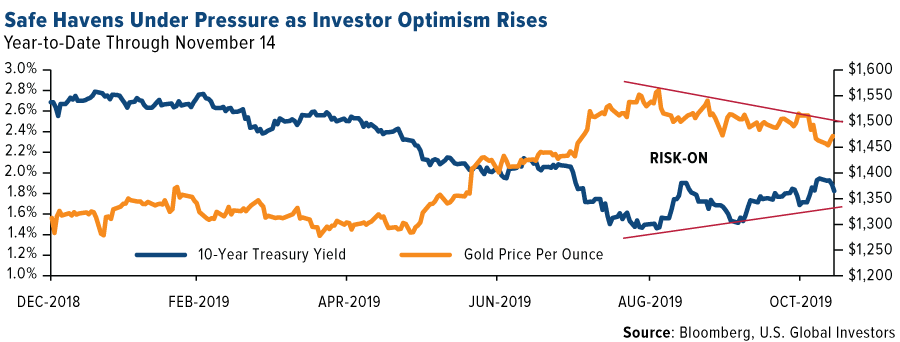

Investors Have a Serious Case of FOMO

To Nancy’s point, I might also add that progress in the U.S.-China trade dispute has been constructive for commodities demand expectations, not to mention trade. This has helped spark a year-end stock rally as investors catch a case of “fear of missing out,” or FOMO.

Fund managers’ cash levels have dropped in November to their lowest since June 2013 on improved optimism. According to Bank of America Merrill Lynch’s most recent survey of managers overseeing more than $500 billion in assets, cash levels fell from 5 percent in October to only 4.2 percent this month. That’s the biggest one-month drop since Donald Trump was elected president.

Safe haven assets, including gold, U.S. Treasury bonds and the Japanese yen, have normally receded in “risk-on” environments, and this cycle has been no exception. Gold prices have fallen around 6.3 percent from their six-year highs of more than $1,565 an ounce in early September.

Consequentially, investors have been taking money out of gold-backed ETFs at a rapid pace. Last Friday, as much as $620.7 million was withdrawn from SPDR Gold Shares (GLD), the world’s largest ETF backed by physical gold. That amount was the most for a single week since October 2016.

I still this decline as a healthy correction, and I urge investors to consider taking advantage of the discount. After all, we wait to buy certain items until Black Friday or Cyber Monday, when they go on sale and are more affordable. We should have the same buying habits with regard to gold and other assets.

Thinking about buying the dip in gold? Watch my interview with Kitco’s Daniela Cambone by clicking here!

Gold Market

This week spot gold closed at $1,468.30, up $9.38 per ounce, or 0.64 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.18 percent. The S&P/TSX Venture Index came in off 1.56 percent. The U.S. Trade-Weighted Dollar fell 0.36 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-12 | Germany ZEW Survey Current Situation | -22.3 | -24.7 | -25.3 |

| Nov-12 | Germany ZEW Survey Expectations | -13.0 | -2.1 | -22.8 |

| Nov-13 | Germany CPI YoY | 1.1% | 1.1% | 1.1% |

| Nov-13 | CPI YoY | 1.7% | 1.8% | 1.7% |

| Nov-13 | China Retail Sales YoY | 7.8% | 7.2% | 7.8% |

| Nov-14 | PPI Final Demand YoY | 0.9% | 1.1% | 1.4% |

| Nov-14 | Initial Jobless Claims | 215k | 225k | 211k |

| Nov-15 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.1% |

| Nov-19 | Housing Starts | 1320k | — | 1256k |

| Nov-21 | Initial Jobless Claims | 215k | — | 225k |

Strengths

- The best performing metal this week was silver, up 1.02 percent on little news. Gold traders and analysts were mostly bullish on their outlooks for gold next week despite lower prices. Fifty-three percent of respondents were bullish in the weekly Bloomberg survey. Serbia bought nine tonnes of gold in October and the metal now accounts for 10 percent of the nation’s foreign reserves. Serbian central bank governor told reporters that “Serbia is safer today” now that it bought more gold. Bloomberg reports that the purchase is one of many moves by the country to shore up its financial stability by changing the structure of its foreign debt.

- Gold prices are down from recent highs, but that doesn’t mean investors are giving up. Open interest is still rising, showing that lower prices are driven by new short-sellers rather than by long investors liquidating. Another potential catalyst for the yellow metal is President Donald Trump pushing the Federal Reserve to deploy negative interest rates, which are positive for gold.

- Although not the greatest news for miners, South Africa’s gold production fell for a 24th straight month in September for the longest streak of decreases since 2008, according to Statistics South Africa. Tighter supply of the metal could push prices higher. Output of platinum-group metals also fell for the month by 2 percent.

Weaknesses

- The worst performing metal this week was palladium, down 1.75 percent following strong gains in September and October. On Monday, contracts equal to 3 million ounces of gold changed hands in just 30 minutes fueling a selloff. Bloomberg reports that this was triple the 100-day average of contracts traded during the time of day. As a result, gold fell as low as $1,448.90 an ounce. Selling continued throughout the week with the largest gold-backed ETF, SPDR Gold Shares, seeing its biggest outflow in three years.

- Semafo’s Boungou gold mine in Burkina Faso remains closed as the area continues to be secured after an attack last week. The company’s CEO said that the death toll has risen to 39 after a convoy of workers was attacked. According to the International Crisis Group, artisanal gold miners in West Africa’s Sahel zone have become a source of financing and recruits for Islamist militants. The group said in a report that “the main jihadist groups in the Sahel benefit financially from gold extraction – an activity that they consider lawful.”

- Turkey’s central bank gold reserves fell $397 million from the previous week to now total $26.6 billion. According to central bank data, reserves are still up 41 percent year-over-year. U.S. core inflation unexpectedly slowed down in October despite a new round of tariffs on Chinese goods. The core consumer price index (CPI) rose 2.3 percent from a year earlier. Slowing inflation can be negative for gold prices.

Opportunities

- Growing electric vehicle demand could fuel the palladium deficit and push prices higher as the precious metal is a key component in building cars. Daimler said that electric vehicles are expected to constitute 15 percent of its car portfolio by 2021 from just 2 percent in 2019. Bloomberg’s Elena Mazneva writes that palladium has risen by more than any other major commodity over the past year and its recent pullback doesn’t spell an end to the rally since it is driven by demand for autos. South Africa’s platinum union agreed to a wage deal with miners and broke a deadlock that threatened to disrupt the industry. Reaching an agreement quickly demonstrates that South Africa is striving to be the most reliable supplier of choice of platinum group metals.

- According to a statement from Lundin Gold, the company has received a key permit for its Fruta del Norte gold project in Ecuador. Lundin says the project can now move forward toward production this quarter. The mine will provide $1.96 billion to the Ecuadorian state through taxes and royalties through 2034 and will have a mine lifetime of 15 years.

- UBS published a survey of over 3,000 family offices showing that they are now holding 25 percent of assets in cash. The survey says that almost 80 percent of the offices are expecting volatility to increase and more than half are expecting a significant selloff in equities in the months ahead. Since the yield on bonds are so low, other assets such as gold may benefit if cash is shifted to gold to diversify away from the stock market.

Threats

- Billionaire investor Ray Dalio warned investors of a capital war between the U .S. and China as some lawmakers work to pressure a slowdown in the flow of money from U.S. pension and investment funds into Chinese companies. “There is a trade war, there is a technology war, there is a geopolitical war, and there could be a capital war. How that is approached is going to determine our futures,” said Dalio on Thursday. However, sentiment was largely positive this week on a possible trade deal between the two superpowers.

- We are now entering tax loss selling season and it could spell big volatility for Canadian equities. Bloomberg reports that energy and pot stocks are among the biggest losers in Canada’s stock market this year and are prone to further weakness as investors sell low to reduce their tax bills. Perhaps some of that money could flow into junior miners.

- A World Gold Council (WGC) survey shows that just 12 percent of China’s generation Z intend to buy gold jewelry in the coming year, which is lower than the millennial generation and people over 39 years old. China is the world’s top buyer of the metal, and changing tastes between generations could hurt overall demand.

Index Summary

- The major market indices finished mostly up this week. The Dow Jones Industrial Average gained 1.17 percent. The S&P 500 Stock Index rose 0.82 percent, while the Nasdaq Composite climbed 0.77 percent. The Russell 2000 small capitalization index lost 0.16 percent this week.

- The Hang Seng Composite lost 4.31 percent this week; while Taiwan was down 0.47 percent and the KOSPI rose 1.17 percent.

- The 10-year Treasury bond yield fell 11 basis points to 1.833 percent.

Domestic Equity Market

Strengths

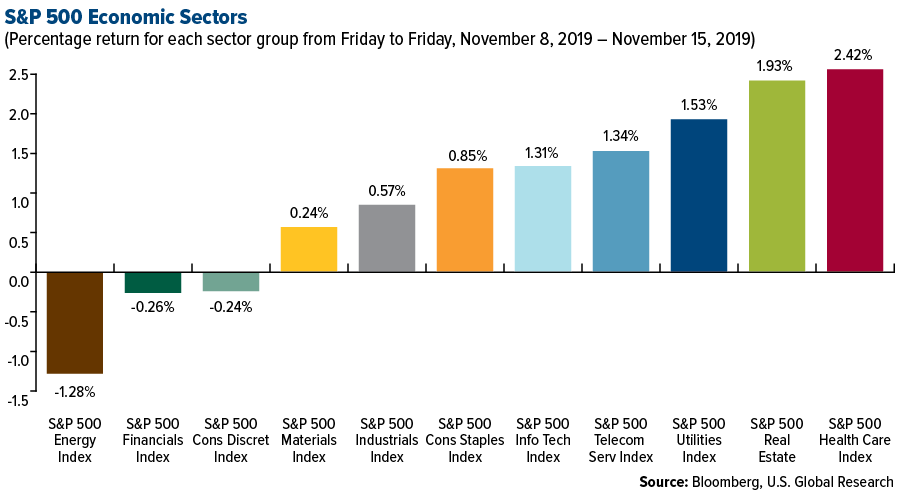

- Health care was the best performing sector of the week, increasing 2.42 percent compared to an overall increase of 0.88 percent for the S&P 500 Index.

- DXC Technology was the best performing stock for the week, increasing 23.77 percent.

- Disney announced on Wednesday that its new content streaming service, Disney+, had 10 million sign-ups since launching on Tuesday. Disney+ had 1.9 million preorders in the U.S. by Sunday, a few days before launch, according to data provided to Business Insider by analytics company Jumpshot.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 1.28 percent compared to an overall increase of 0.88 percent for the S&P 500.

- Expedia Group was the worst performing stock for the week, falling 11.47 percent.

- Cisco’s sharp cut to the second fiscal quarter, as well as its 2020 sales estimates, reflect broadening demand weakness due to macroeconomic concerns. However, the weakness may linger a few quarters, according to Bloomberg Intelligence.

Opportunities

- Investor appetite for risk, which has sent equity markets to record highs, has the potential to extend into next year, according to Credit Suisse. Although 2019’s rally in bonds and stocks will be hard to match, riskier assets can still post further gains as sentiment improves, said Walter Edelmann, chief global strategist at the Swiss lender. “In the shorter term, the sentiment has improved a lot but if we think more about the next six months, there’s still room for improvement,” said Edelmann in a phone interview. “The returns in equities from here, of course, are more limited, but so far what we’ve seen this year has been an extraordinary rally, and on top of that, we can see further gains.”

- A headwind for the global equity rally is showing signs of reversing, and that could give a further boost to stocks, according to Citigroup. Investors have sold a net $230 billion in shares this year amid a 20 percent rise in a gauge of global stocks, strategists including Robert Buckland wrote in a note Wednesday. That has only happened twice before and when the trend reversed, inflows helped spur another 20 percent gain over the next year, they said. “November is on track to be the first month of inflows into emerging and developed market equities funds in two years,” the Citi team wrote. “If they continue, this could add further momentum to the rally.”

- The existence of a big contingent of bears is often a good sign to contrarians. It means there are more people to change their minds and buy, should a rally get going. Data on a particularly stubborn group of market skeptics suggest that’s happening in U.S. stocks at a furious clip. Hedge funds that make both bullish and bearish equity bets have boosted their long positions relative to shorts at the fastest pace in a year over the past few weeks, primary brokerage data compiled by Morgan Stanley showed. From a two-year trough that indicated extreme levels of pessimism last month, the ratio is rebounding sharply.

Threats

- The world’s biggest shipping company warns that the global trade slump is probably here to stay in 2020. Maersk is seen as a bellwether for global trade, given that it handles about 20 percent of all consumer goods shipped.

- America’s biggest banks will soon have to add billions to their reserves, and they say they could cut lending in response. Starting in January 2020, big banks will have to record all expected future losses on their loans once they’re issued, thanks to a new accounting rule.

- A multistate investigation into potential anticompetitive behavior by Google has expanded to its search and Android businesses. Previously, attorneys general from 48 states, Washington, D.C. and Puerto Rico were only looking into Google’s digital ads business, but the broadened investigation adds to Google’s regulatory headaches.

The Economy and Bond Market

Strengths

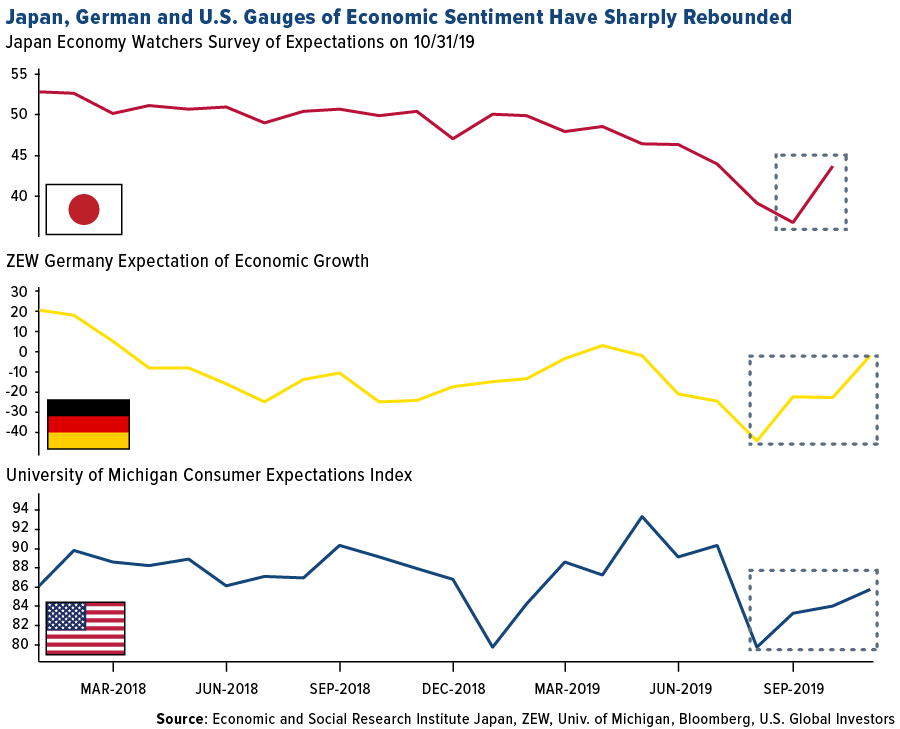

- The latest expectations surveys are rebounding sharply, reports Bloomberg. The positive news from Japan and Germany this week, coupled with a consumer report last week in the U.S., all highlight a turning point in sentiment as 2019 draws to a close.

- Small-business owners’ confidence in the U.S. economy rose in October, according to a survey by the National Federation of Independent Business. The NFIB Small Business Optimism Index was up 0.6 point from the prior month. The NFIB said optimism rose because business owners are still creating jobs, writes Bloomberg, raising wages and expanding their businesses.

- Americans spent more on shopping in October while pulling back on nonessential items, reports the Wall St. Journal, which suggests their willingness to buy, but in a cautious way. The Commerce Department reported that retail sales rose a seasonally adjusted 0.3 percent in October from the month prior.

Weaknesses

- U.S. industrial production dropped 0.8 percent in October, the Federal Reserve reported Friday. The drop was steeper than Wall Street expectations of a 0.5 percent fall, MarketWatch reports, and was the third decline in output in the past four months.

- U.S. weekly jobless claims rose to a five-month high last week, reports Reuters. Initial claims for state unemployment benefits increased 14,000 to a seasonally adjusted 225,000 for the week ended November 9, the highest reading since June 22, the Labor Department said on Thursday.

- As reported by Business Insider, the U.S. budget deficit continued to swell at the start of the fiscal year. Government spending outpaced revenue, despite solid economic growth. “Even with lower rates and even with decent growth, there is still going to be a need to reduce these deficits,” Fed Chair Jerome Powell told the Joint Economic Committee.

Opportunities

- In the U.S., the spotlight could fall on the minutes of the most recent Fed meeting that will hit markets on Wednesday, reports FXStreet. The upcoming minutes could shed some light on something Jerome Powell alluded to during his press conference – namely, that it would take a “really significant move up in inflation” before the Fed considers raising rates again. This triggered a notable market reaction back then, as investors saw it as a signal that the Fed is willing to let the economy ‘run hot’, meaning it would tolerate a period of above-target inflation without raising rates.

- Investors continue to pay close attention to the U.S.-China trade talks. The latest commentary from the Chinese side put hardly any emphasis on how close they are to a signing ceremony date, writes Bloomberg. The two are talking and “China is willing to work with the U.S. to address each other’s core concerns and to create conditions for reaching a phase-one agreement,” Ministry of Commerce spokesman Gao Feng said yesterday.

- Federal Reserve Bank of San Francisco President Mary Daly said the monetary situation is in a good place given healthy momentum in the economy and consumer spending, despite headwinds from weaker business investment and manufacturing.

Threats

- The conflict between China and the U.S. could expand beyond trade and technology, Bridgewater Associates founder Ray Dalio said at the annual gala of the National Committee on U.S.-China Relations in New York on Thursday. “There is a trade war, there is a technology war, there is a geopolitical war, and there could be a capital war. How that is approached is going to determine our futures,” said Dalio. “I hope that it is done with mutual understanding instead of wars, a win-win relationship rather than a lose-lose relationship.”

- The main event next week will be the preliminary eurozone PMIs for November, due on Friday. Forecasts point to an uptick in both the manufacturing and services indices, but even if those expectations are met, such numbers would still point to stagnation in the euro area.

- Continuing low interest rates could dent U.S. bank profits and push bankers into riskier behavior that might threaten the nation’s financial stability, the Federal Reserve said in a report released Friday. The latest version of the twice-yearly report highlighted the rate squeeze facing banks and insurers, writes Bloomberg, noting that it could erode lending standards.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was iron ore, which gained 3.47 percent. Copper rose with most base metals on Friday on renewed hopes for a trade agreement between the U.S. and China, reports Bloomberg. White House economic advisor Larry Kudlow said that an agreement is “coming down to the short strokes.” China also injected $29 billion into its banking system to aid the economy, which could help demand for commodities.

- In recent years several multinational energy companies have left or reduced their presence in Canada. Royal Dutch Shell Plc reassured investors this week that it would not be one of the companies leaving the nation and says it is focused on a $30 billion LNG project. Shell has been in Canada for over 100 years, says the company’s president and country chair Michael Crothers, and they see “enormous opportunity here [in Canada] because of the resource base.” The energy giant is also exploring ways to expand its carbon capture project in Alberta to trap more emissions.

- Russia’s oldest steelmaker, Magnitogorsk Iron & Steel PJSC, is spending $600 million on environmental projects by 2025 in a move to appeal to investors who are concerned about ESG. The company is a top polluter and has already made big moves to clean up some of its surrounding areas. It cleaned up mountains starting in the 2000s and has a program to clean the air from sulfurous fumes and recycle water at its plants. According to a report by the Russian Ministry of Natural Resources and Environment, Magnitogorsk was removed from the list of cities with the most polluted air due to MMK slashing emissions.

Weaknesses

- The worst performing major commodity for the week was nickel, which fell 6.39 percent. Several commodities suffered from lower demand outlooks this week. Nickel had at least seven straight days of losses due to weaker Chinese stainless steel prices hurting demand outlooks. Right now aluminum is this year’s second worst performing base metal after analysts predict that China’s demand will fall 1.2 percent – the first drop in three decades. RBC sees a near-term supply and demand imbalance for lithium due to weak prices and weakness in autos. Lastly, 57 percent of steel buyers in the U.S., as surveyed by UBS Group, expect demand to fall in the next three months. Steel prices in the U.S. have fallen 32 percent so far this year, hurting producers’ profits and growth outlooks, reports Bloomberg.

- Dean Foods Co., a top U.S. milk processor, filed for Chapter 11 bankruptcy and is in talks with Dairy Farmers of American Inc. regarding a possible sale. The company has seen big losses after its top consumer, Walmart Inc., built its own plant, reports Bloomberg. The price of milk has been rising due to tighter supplies; however, production costs have increased and demand has fallen due to Americans drinking less cow milk. Dean shares have fallen 79 percent so far this year. Consumers switching to almond, soy, or oatmeal milk, in recent years has also had an impact on milk demand.

- In November 2018, Contura Energy bought its rival Alpha Natural Resources and became America’s largest metallurgical coal supplier at a time when prices were rising along with demand from China. Since then, met coal prices have dropped sharply and Contura’s shares are down a whopping 86 percent so far this year. Bloomberg reports that the fall of Contura reflects the broader struggles in America’s coal industry. Despite coal prices being down 30 percent in the last 12 months, two domestic producers are moving ahead with new mines. Arch Coal Inc. and Consol Energy Inc. are both on track to open new mines in West Virginia. Consol CEO Jimmy Brock said “we expect to hold our ground” despite a lot of pain in the marketplace.

Opportunities

- Suncor Energy Inc. will pay Microsoft to use its cloud technology to improve performance from oil production to final sales at retail stations, reports Bloomberg. The use of machine learning, automation and visualization technologies in the cloud could increase safety, performance and reduce costs. Several other majors are in partnerships with Microsoft including Equinor ASA, Chevron Corp and ExxonMobil Corp.

- Billionaire investors such as Sam Zell are circling the distressed oil and gas patch and are looking to pick up assets for cheap when the U.S. industry is scaring off other investors, reports Bloomberg. Zell is looking at buying assets in California, Colorado and Texas at low prices as companies are trying to get ahead of a credit crunch. The billionaire said that “the amount of capital available in the oil patch is disappearing.” Jerry Jones said he is in talks to acquire natural gas assets in Louisiana from struggling Chesapeake Energy Corp. Producers are in need of cash and lenders are becoming more discerning due to drillers being down more than 40 percent since 2014.

- According to BNP Paribas, money flowing into ESG funds has outpaced growth in both U.S. and European equity funds over the last 12 months. ESG equity funds were the second most popular asset class with 28 percent of inflows. The European Investment Bank approved a new energy policy that includes increased support for clean energy projects and will not considering new financing of unabated fossil fuels from the end of 2021. This is a massive leap toward ending fossil fuel financing and helping Europe to become the first climate-neutral continent.

Threats

- The International Energy Agency (IEA) predicts that global oil demand will plateau in 2030 as the use of more efficient cars and electric vehicles will end an expansion of oil use. The current growth rate of 1 million barrels a day will hold for the next five years then fall to just 100,000 a day in the 2030s. In the nearer term, OPEC said that oil markets will be in surplus in 2020 and that global supplies will exceed demand by around 645,000 barrels per day. The prospectus for Saudi Aramco’s initial public offering was released this week and includes an assessment from IHS Markit that oil demand will peak around 2035.

- Thousands of acres of former coal mining land and groundwater in Texas could be contaminated due to a lack of enforcement of industry standards by the Railroad Commission, according to an investigation by Grist and the Texas Tribune. Coal companies are required to restore land once they are done mining, but the state has allowed companies to do the bare minimum restoration work and save millions of dollars. Additionally, the investigation found that for decades power companies have discarded coal ash in pits located near waterways, which increases the likelihood of the toxins leaking into underground water supplies.

- Australia is suffering from deadly bushfires and the worst drought in decades. Bloomberg writes that the nation is the world’s driest inhabited continent and is considered one of the most vulnerable developed countries to climate change. Australia gets the majority of its energy from burning coal and is a top miner of several metals and minerals.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 2.38 percent. The Greek financial sector outperformed. The National Bank of Greece and Eurobank were the best performing lenders, gaining nearly 10 percent each over the past five days.

- The Turkish lira was the best performing currency this week, gaining 41 basis points. The lira was supported by an improving geopolitical situation. President Erdogan visited the White House and discussions will continue between both countries to find a common ground on outstanding political issues. Trump proposed that both countries could increase trade up to $100 billion quickly from the $24 billion in 2017.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 1.29 percent. Russian equites have been on the run since mid-October, and this week a small correction occurred. Gazprom, a gas producer and distributor, was the weakest performer over the past five days, losing almost 7 percent.

- The Polish zloty was the worst performing currency in the region this week, losing 4 basis points. Slower economic growth and continuous noise around Swiss-franc loans put pressure on the currency. Third-quarter GDP came in at 3.9 percent on a year-over-year basis, versus 4.5 percent in the prior quarter. Polish banks might have to increase provisions in the next quarter, as more customers will sue lenders.

- Materials was the worst performing sector among eastern European markets this week.

Opportunities

- According to the latest reading of the ZEW Expectation of Economic Growth, economic sentiment has risen substantially in Europe led by a strong increase in Germany. Germany’s ZEW Indicator of Economic Sentiment climbed 20.7 points from the previous month to negative 2.1 points in November. The indicator has been in a negative territory since May 2019. The European Central Bank’s (ECB’s) new stimulus hopes for an agreement between Great Britain and the EU, while growing optimism around trade talks have a positive impact on growth expectations in Europe.

- Spending by the Russian government in 2019 is running at the slowest pace in five years. Banks were holding $3.4 trillion ($53 billion) worth of federal budget money in deposits and repo operations as of the middle of October, according to the Finance Ministry, triple the amount held three years ago. Russia’s budget surplus reached 3.8 percent of GDP by the end of September. The country has plenty of money available to put to work to revive its economy.

- The high current account deficit in Turkey was a main concern for investors, as a large deficit made the country dependent on foreign flows to finance the shortfall. However, the current account has improved drastically and the country recorded an annual surplus of $5.9 billion in September. Ankara forecast the annual current account at $1 billion in 2019, compared to a deficit of $27.6 billion in the previous year. The current account balance as a percent of GDP is at 16 basis points and in positive territory for the first time since 2002. In addition, an improving geopolitical situation with Erdogan’s visit to the White House could be warming investors’ sentiment toward one of the most oversold countries.

Threats

- The Polish parliament resumed work after last month’s general elections. The ruling party, Law & Justice, retained its absolute majority in the lower house but lost absolute majority in the upper house, winning only 48 seats out of 100. New legislations will not be quickly passed through the lower and upper house as the government no longer will have majority in both houses. The Polish economy has been growing at 4-5 percent since 2016, supported by increased government spending since the new government came to power back in 2015. According to analysts surveyed by Bloomberg, GDP will slow to 3.4 percent in 2020 and 2.8 percent in 2021.

- Economic growth eased more than forecast in Poland, Romania, the Czech Republic and Slovakia, while Hungary and Bulgaria recorded stronger growth in the third quarter. The largest economy in Eastern Europe, Poland, posted preliminary GDP growth of 3.9 percent year-over-year, versus an expected 4 percent. The Czech Republic recorded a preliminary growth in the third quarter of just 30 basis points versus an expected 40 basis points. Strongest growth data was reported in Hungary, where GDP was posted at 5 percent versus expected 4.4 percent.

- Germany avoided recession, posting 10 basis points growth in the third quarter, versus expected contraction of 10 basis points. However, the German Economy Minister commented that the growth was weak in the past three months and there are no signs of recovery. German companies are not expecting pickup in exports in the coming months.

China Region

Strengths

- The best performing index in the region was Korea’s KOSPI, which defied the sea of primarily red in the region and rose 1.17 percent. India’s SENSEX also climbed, albeit mildly, finishing up 8 basis points.

- Information Technology finished out as the “best” Hang Seng Composite Index on the week, closing down only 1.57 percent.

- Alibaba’s “Singles’ Day” sale generated more than $38 billion in purchases, surpassing its previous records for the 24-hour shopping marathon that has become the world’s largest shopping event.

Weaknesses

- The poorest performing index in the region was Hong Kong’s Hang Seng Composite, which declined by 4.31 percent. Thailand’s SET and China’s Shanghai Composite also declined by more than 2 percent this week.

- Properties & Construction finished out as the worst performing Hang Seng Composite Index on the week in Hong Kong, closing down some 5.94 percent in a rough week overall.

- China’s retail sales for the October measurement period rose only 7.2 percent year over year, shy of estimates for a 7.8 percent growth rate.

Opportunities

- As top White House economic advisor Larry Kudlow puts it, the U.S.-China “Phase One” deal is getting closer, and now down to “the short strokes.” That sure sounds promising. And yet at the same time, reports of snags over the timing and scope of agricultural purchases also sprang up mid-week before being smoothed out somewhat by administration officials. With U.S. markets pushing up to and closing at all-time highs, it sure seems like markets are reading recent developments as, on the whole, meaningfully constructive and likely to produce some kind of fruit.

- And on that note, look what else has been especially perky of late: Korea’s KOSPI Index put in new multi-month highs this week…

- Interestingly, while Hong Kong itself is caught up amid protests and headline-grabbing current events, and even as Chinese ecommerce and tech juggernaut Alibaba continues to seek a Hong Kong listing, China-based cloud fintech platform OneConnect Financial Technology Co.—a Ping An Insurance affiliate backed by SoftBank’s Vision Fund—filed for a U.S. IPO this week, Bloomberg News reported.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. As in recent weeks, one can only say, “Stay tuned.” The December 15 tariffs yet loom—now exactly one month out—with markets seemingly baking in more and more of a truce on tariffs and a Phase One deal. And of course, there is positive seasonality here in the United States as late November-December-January holidays approach…but should the markets be caught wrong-footed on trade, the response will likely be swift to the downside.

- The situation in Hong Kong continues unabated, with Chinese President Xi Jinping sounding threats by Hong Kong “radicals” to the SAR’s rule of law as he seemed to indicate support for embattled CEO Carrie Lam. Protests go on anyway, and seem likely to continue, at least in the short run. The question increasingly is, “What makes them stop?”

- In addition to the obvious and interrelated political concerns about Hong Kong, there are increasing economic woes brought on by major interruptions to tourism and retail sales. The city of Hong Kong revised down its estimate for economic growth this year and the government now projects, per recent Bloomberg reporting, the first annual contraction since the global financial crisis a decade ago. GDP will contract 1.3 percent in 2019 versus the year prior, government officials are expecting, and final third quarter GDP contracted 3.2 percent from the prior.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 15 was BLOCKv, up 7,117.83 percent.

- China-based bitcoin miner maker Canaan intends to raise around $100 million in its initial public offering (IPO) in the U.S., reports CoinDesk. Canaan is aiming to offer 10 million American depository shares (ADS) with each at a price of between $9 and $11. “With that offering size, it would mean Canaan commands a diluted market value of about $1.5 billion with about 2.3 billion outstanding ordinary shares after the offering,” the article explains.

- U.S.-based cryptocurrency exchange Coinbase announced Thursday that it has expanded its availability to 10 more European nations and also added support for five new crypto options to its Visa debit card, reports CoinDesk. “By more than doubling the number of assets our customers can spend on Coinbase Card, as well as introducing the card to 10 new countries, Coinbase continues to help drive crypto’s role as a utility, and not just an investment,” CEO at Coinbase U.K. Zeeshan Feroz said in a statement.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 15 was Akropolis, down 67.07 percent.

- Is the enthusiasm for blockchain technology fading? According to one Bloomberg article, it’s getting its last rites read at the Consensus Invest conference in New York this week. “Blockchain is dead,” said Meltem Demirors, chief investment officer of CoinShares Group. Demirors points to early adapters which she says are pivoting into new business models. “Most of the companies that raised massive amounts of capital in 2016, 2017 to build blockchain, they don’t exist anymore or they’ve pivoted into cryptocurrency and tokenization.”

- The trading range between bitcoin’s 50- and 200-day moving averages has diminished to its narrowest since June, reports Bloomberg, indicating a potential inflection point on the horizon. “The best way to describe the market is it’s retracing last year’s bear market,” Bloomberg Intelligence analyst Mike McGlone said. “It’s in no hurry to take out the old highs – there’s a hangover of residual selling from the parabolic rally in 2017.”

Opportunities

- The CME Group has announced that it will launch options on its bitcoin futures contracts in January, writes CoinDesk. On Tuesday, the derivatives exchange posted on its website stating that as long as it gets the green light from regulators, the options will go live on January 13, 2020.

- At CoinDesk’s Invest: NYC conference this week, BitGo announced that it is processing more than 20 percent of bitcoin transactions. This raises the question about market collapse and whether or not those assets would be at risk should BitGo go down. In a statement, however, BitGo CEO Mike Belshe reassured conference attendees there is nothing to fear. “It is a great assurance to our clients that they are always in control of their own assets no matter the circumstances,” he explained. “BitGo is their trusted partner that is focused on making the market for digital assets bigger, stronger and more secure every day.”

- HSBC Singapore, in partnership with Singapore Exchange and investment firm Temasek, are looking into whether or not digitizing bonds with distributed ledger technology (DLT) can bring benefits to market participants. As reported by CoinDesk, the trial will examine the potential of DLT to streamline the issuance and servicing of fixed income securities, debt instruments that pay fixed interest to investors, with a specific focus on the Asian bond markets.

Threats

- According to Bloomberg, bitcoin could retest the lows seen prior to its rampant run-up following positive comments by China’s President in October. The GTI Vera Convergence Divergence Indicator shows a narrowing gap between the signal and vera lines, the article explains, which suggests a trend change may be on the horizon. The popular digital currency continues to face resistance at the $10,000 level.

- In his speech to the U.S. Congress, Facebook CEO Mark Zuckerberg was “at least half right” when he told the group that there isn’t a U.S. monopoly on regulation of next-generation payments technology. As one Bloomberg opinion reporter points out, Zuckerberg implied that why you may not like Facebook’s proposed Libra cryptocurrency, you would like a state-run Chinese digital currency with global ambitions even less. The government-backed digital currency planned by China is perhaps only a few months away, too.

- According to records released publicly this week, the Department of Justice reached a plea deal with Konstanin Ignatov, the brother of the founder of OneCoin Ltd., for his involvement in the cryptocurrency project based out of Bulgaria. As reported by CoinDesk and BBC, Ignatov pleaded guilty to multiple counts including money laundering.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 239.80 | +5.86 | +2.50% |

| XAU | 93.61 | +1.92 | +2.09% |

| DJIA | 28,004.89 | +323.65 | +1.17% |

| Korean KOSPI Index | 2,162.18 | +24.95 | +1.17% |

| Oil Futures | 57.79 | +0.55 | +0.96% |

| S&P 500 | 3,118.54 | +25.46 | +0.82% |

| Nasdaq | 8,540.83 | +65.52 | +0.77% |

| Gold Futures | 1,467.30 | +4.40 | +0.30% |

| S&P Basic Materials | 378.32 | +0.90 | +0.24% |

| Russell 2000 | 1,596.33 | -2.53 | -0.16% |

| S&P Energy | 440.43 | -5.70 | -1.28% |

| S&P/TSX VENTURE COMP IDX | 528.43 | -8.54 | -1.59% |

| Natural Gas Futures | 2.68 | -0.11 | -4.02% |

| Hang Seng Composite Index | 3,574.15 | -160.82 | -4.31% |

| 10-Yr Treasury Bond | 1.83 | -0.11 | -5.66% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.68 | +0.37 | +16.24% |

| Oil Futures | 57.79 | +4.43 | +8.30% |

| XAU | 93.61 | +5.35 | +6.06% |

| 10-Yr Treasury Bond | 1.83 | +0.09 | +5.34% |

| Nasdaq | 8,540.83 | +416.65 | +5.13% |

| S&P Basic Materials | 378.32 | +18.05 | +5.01% |

| Russell 2000 | 1,596.33 | +71.28 | +4.67% |

| S&P 500 | 3,118.54 | +128.85 | +4.31% |

| S&P Energy | 440.43 | +17.62 | +4.17% |

| Korean KOSPI Index | 2,162.18 | +79.35 | +3.81% |

| DJIA | 28,004.89 | +1,002.91 | +3.71% |

| S&P/TSX Global Gold Index | 239.80 | +5.15 | +2.19% |

| Hang Seng Composite Index | 3,574.15 | -28.54 | -0.79% |

| Gold Futures | 1,467.30 | -26.70 | -1.79% |

| S&P/TSX VENTURE COMP IDX | 528.43 | -10.62 | -1.97% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 2.68 | +0.45 | +19.94% |

| 10-Yr Treasury Bond | 1.83 | +0.30 | +19.88% |

| Korean KOSPI Index | 2,162.18 | +223.81 | +11.55% |

| Nasdaq | 8,540.83 | +774.21 | +9.97% |

| S&P 500 | 3,118.54 | +270.94 | +9.51% |

| DJIA | 28,004.89 | +2,425.50 | +9.48% |

| Russell 2000 | 1,596.33 | +134.68 | +9.21% |

| S&P Basic Materials | 378.32 | +30.10 | +8.64% |

| S&P Energy | 440.43 | +26.31 | +6.35% |

| Oil Futures | 57.79 | +3.32 | +6.10% |

| Hang Seng Composite Index | 3,574.15 | +165.91 | +4.87% |

| XAU | 93.61 | -0.21 | -0.22% |

| Gold Futures | 1,467.30 | -63.90 | -4.17% |

| S&P/TSX Global Gold Index | 239.80 | -11.23 | -4.47% |

| S&P/TSX VENTURE COMP IDX | 528.43 | -40.35 | -7.09% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2019):

Eurobank Ergasias SA

National Bank of Greece SA

Gazprom PJSC

Royal Dutch Shell Plc

Magnitogorsk Iron & Steel Work

Suncor Energy Inc

Equinor ASA

Semafo Inc

SPDR Gold Shares

Lundin Gold Inc

PING AN

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

ZEW Germany Expectation of Economic Growth is a survey on the question of economic growth in six months.

The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1221 member firms.

The Bangkok SET Index is a capitalization-weighted index of stocks traded on the Stock Exchange of Thailand.

The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange.

The BSE SENSEX is a free-float market-weighted stock market index of 30 well-established and financially sound companies listed on Bombay Stock Exchange. The 30 component companies which are some of the largest and most actively traded stocks, are representative of various industrial sectors of the Indian economy.