Investor Alert

When Will Social Security Run Dry? Sooner Than You Might Think

Date Posted: September 3, 2021

Read time: 44 min

I’ve been in Sweden all week, representing HIVE Blockchain Technologies and searching for new expansion opportunities. I can’t wait to share the details with you, so make sure you’re subscribed to Frank Talk by clicking here.

In the meantime, I have some sobering news: Social Security is in worse shape than we thought. The program’s Old-Age and Survivors Insurance (OASI) Trust Fund is now expected to be insolvent by 2033, a year earlier than anticipated.

According to the annual report, its finances have been “significantly affected” by the pandemic and 2020 recession, not to mention “rapid population aging.”

Indeed, the ratio between contributors and beneficiaries has been shrinking for decades. In 1941, there were about 42 workers for every Social Security recipient. Today, that figure is around 2.5 workers per beneficiary.

A tipping point will occur in 2034: Americans age 65 and over will, for the first time ever, outnumber those 18 and under, according to Census Bureau estimates.

It’s believed that around 40% of older Americans only receive income from Social Security, and there have been calls to expand the program. I’ll leave that to lawmakers to decide.

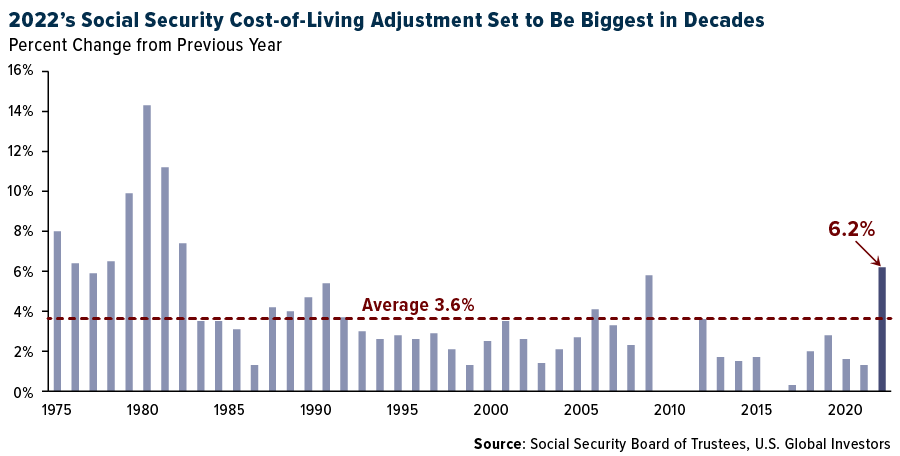

For my part, I’ll say that it might make sense just to assume Social Security won’t be there when you’re ready to retire. Either that, or the income will be even less sufficient than it is now—especially if inflation proves not as “transitory” as Jerome Powell insists it is. I think it’s very telling that next year’s Social Security cost-of-living adjustment is expected to be above 6%. That would be the biggest bump since the early 1980s, when consumer price increases were sky high.

I don’t want to insult anybody’s intelligence or preparedness, but if you’re reading this and haven’t been participating in a defined-contribution (DC) plan such as a 401(k), or if you haven’t been contributing to an individual retirement account (IRA), I urge you to get started today.

If you have been doing those things, you might want to consider increasing your contributions. A 2021 survey found that just over half of older U.S. workers have less than $50,000 saved for retirement.

It doesn’t have to cost a lot. Our own ABC Investment Plan is only $1,000 to get started, then $100 per month in a fund of your choice. Want to invest in Amazon but can’t afford the $3,460 share price? With Robinhood, you can buy a fraction of a share if you wish. Plus, it’s commission-free.

Retirement Balances Hit Record High, Retail Trading Volumes Up

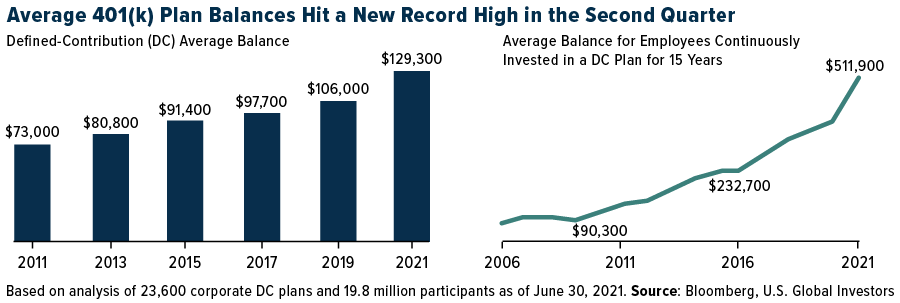

Now for the good news. Americans who’ve already been saving and investing for retirement saw their account balances hit record average highs in the second quarter of 2021. That’s according to Fidelity Investment’s analysis of more than 30 million IRA, 401(k) and 403(b) retirement accounts.

Looking just at 401(k) plans, Fidelity found that the average balance was just under $130,000, a new record high. That may not sound like a lot, but this includes everyone with a 401(k), including young people who may have just got started. The overall average balance for employees who have been contributing continuously for the past 10 years crossed above $400,000 for the first time ever, while that of people who have been investing for 15 years exceeded half a million dollars.

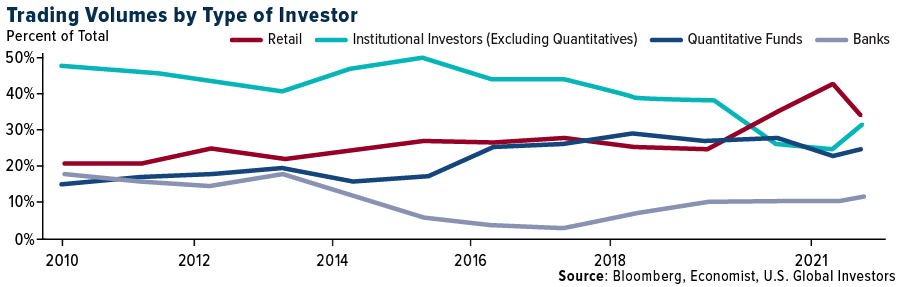

Individual investors and traders have also gotten more involved in the market, at least since the start of the pandemic. A recent article in the Economist shows that the number of trading accounts at brokerage firms, including Robinhood, has exploded from 59 million at the end of 2019 to 95 million today. Retail trading has likewise expanded. As a share of total trading volume, retail activity spiked to over 40% in the first quarter of this year, twice the volume from a decade ago. To meet the surging demand for stock and ETF trading, Fidelity is planning to hire as many as 9,000 new employees by year end.

Granted, trading is not the same thing as investing—and certainly not the same as planning for retirement—but I’m encouraged to see interest in personal finance improve among young people.

Only 12% of Americans Own Gold, 15% Own Silver

I believe gold and silver should also be part of a diversified retirement portfolio, but too few Americans are invested. One survey in 2019 found that only 15% of respondents held silver, and a little over one in 10 held gold.

Hopefully people will change their minds about hard assets, especially as we face the after effects of unprecedented monetary and fiscal stimulus measures. I agree with emerging markets investor Mark Mobius, who earlier this week recommended people buy gold in anticipation of “significant” currency devaluation as a result of runaway money-printing.

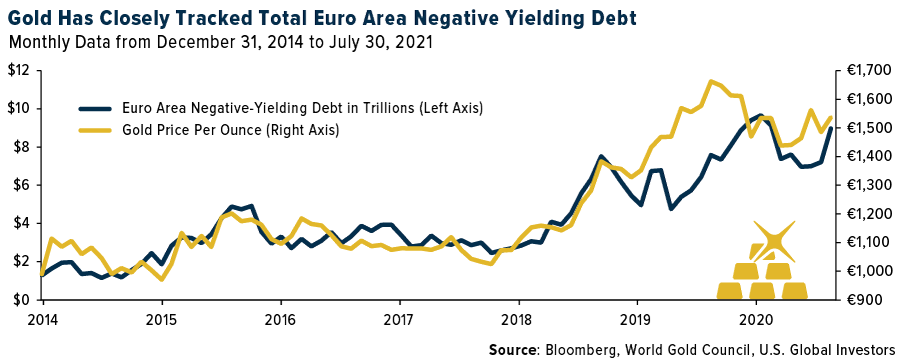

It appears more and more Europeans are getting the message. I’ve shared with you already that German investors’ gold purchases were highest in the first half of 2021 than in any period since at least 2009. The World Gold Council (WGC) attributes this activity to negative real rates and asset purchases made by the European Central Bank (ECB). As you can see below, euro-priced gold has closely tracked negative-yielding debt.

As always, I recommend a 10% weighting in gold, with 5% in physical bullion and 5% in high-quality gold stocks and ETFs. I also recommend no more than 2% in cryptos, particularly Bitcoin and Ether. Remember to rebalance on a quarterly basis.

I will be speaking on gold and cryptocurrencies at Gold Forum Americas 2021 in Colorado Springs, September 13. For those not attending in person, you can register to tune in virtually by clicking here!

Index Summary

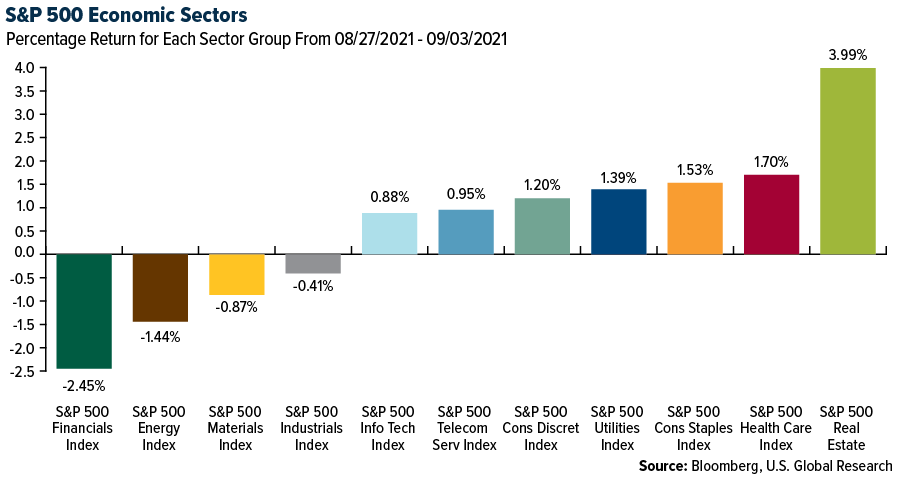

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.24%. The S&P 500 Stock Index rose 0.62%, while the Nasdaq Composite climbed 1.55%. The Russell 2000 small capitalization index gained 0.69% this week.

- The Hang Seng Composite gained 2.83% this week; while Taiwan was up 1.78% and the KOSPI rose 2.14%.

- The 10-year Treasury bond yield rose 1 basis point to 1.323%.

Airline Sector

Strengths

- The best performing airline stock for the week was Hainan Air, up 14.4%. According to Credit Suisse, the situation for U.K. airlines is fluid and equity raises cannot be ruled out. EasyJet has almost two years of cash burn coverage, while IAG has around four years. In Credit Suisse’s view, if either company were to deem an equity raise necessary, liquidity levels would allow them to time such an event to take advantage of potentially higher share prices.

- European leisure carriers are doing well. Wizz Air had a load factor of 83.6% in August, which is only 11% off pre-pandemic activity levels. This is the highest load factor since the pandemic began with passenger volumes at 89% of August 2019 levels. Ryanair had a load factor of 82% in August, the highest load factor since the pandemic began.

- In China, domestic traffic continues to recover as domestic outbreaks of COVID-19 seem more under control. Travelsky Technology’s measurement of domestic volume was -55% versus 2019 levels (-68% last week) and up 32% week-to-week.

Weaknesses

- The worst performing airline stock for the week was Avianca Holdings, down 45.9%. System net sales decelerated for the fifth straight week with another step back to -61.5% versus 2019 for the week, versus -58.9% last week. The deceleration in net sales came from softer pricing, which weakened by 3-4% in all channels.

- At a recent Raymond James conference, major airline companies indicated that the delta variant of the coronavirus has caused August numbers to underperform expectations and the anticipated improvement in business travel is likely to be delayed. Based on flight schedules, the U.S. is seeing material September and October cuts, likely reacting to both weaker demand and strained operations.

- Airlines continue to see yields weaken with the latest week of data pointing to domestic yields down 20-30% with August now trending to -13%, September at -8% and October at -4%. International airlines have similar yield trends, with August and September now down 20% in the most recent week while October went to -16%.

Opportunities

- During the European Union (EU) delta variant outbreak, short-haul bookings went from -29% at the end of June to -48% by mid-July, before flattening out in the -30% range. Thus far, the U.S. has also seen a four-week decline after the start of flight weakness in the country mid-July, when domestic bookings went from -18% to -29%. Using the EU timeframe as a comp, the delta variant impact in the U.S. could be peaking. The main difference is the timing of the variant, and analysts believe with many large U.S. companies delaying a return to office, the corporate travel recovery may be pushed out by about a quarter.

- According to Credit Suisse, there are some opportunities within Latin American airlines, noting they should benefit from demographics and air travel penetration relative to other global economies. Moreover, most Latin American economies look ready to benefit from higher oil prices since they are considered net producers, leading to higher available income and potentially higher flights per capita. Lastly, higher fuel prices usually bring capacity discipline, allowing airlines to achieve a healthier yield environment.

- Jet2.com is indicating some positive trends for the summer of 2022. Looking ahead into next year, the company says load factors are in line with this time pre-pandemic, suggesting consumers may be more comfortable booking further out.

Threats

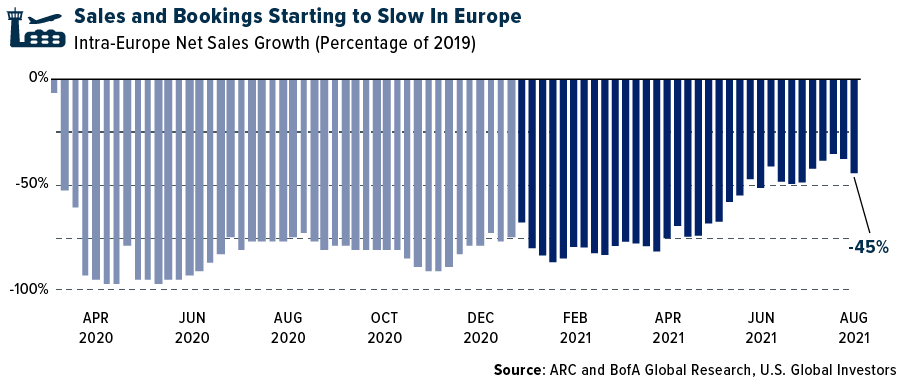

- European airline bookings stepped down this week, with both intra-Europe and international numbers showing a week-on-week decline. Intra-Europe net sales fell by 7 points to -45% versus 2019 (and versus -38% in the prior week) and declined by 8% week-to-week. International net sales were down by 5 points to -70% versus 2019 (and versus -65% in the prior week), with a similar 7% week-to-week decline. As the booking curve remains short, the decline is likely to reflect the summer season coming to an end.

- American Airlines Chief Revenue Officer, Vasu Raja, stated that while both July passenger demand and revenue were better than initially expected, the recent uptick in COVID-19 cases is starting to create softness in close-in bookings, with a corresponding increase in close-in cancellations. Given the fluidity of the current demand environment, management also said that August revenues are trending below their previous internal forecasts.

- Earlier this week, the EU recommended that unvaccinated Americans should be banned from nonessential travel to its member states, following a rise in COVID-19 infections throughout the U.S. Under the new guidance, Israel, Kosovo, Lebanon, Montenegro, and the Republic of North Macedonia were also removed from the EU’s “safe list.”

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Russia, gaining 2.4%. The best performing country in Asia this week was India, gaining 4.4%.

- The Polish zloty was the best performing currency in emerging Europe this week, gaining 2.4%. The Malaysian ringgit was the best performing currency in Asia this week, gaining 1.1%.

- Eurozone PMIs remain strong despite worries over the spread of the coronavirus along with supply constraints. The final Eurozone Manufacturing PMI reading for August was released at 61.4, the Service PMI at 59.0, and the Composite PMI at 59.0.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 0.50%. The worst relative performing country in Asia this week was Malaysia, gaining 1%.

- The Turkish lira was the worst relative performing currency in emerging Europe this week, gaining 0.48%. The Pakistani rupee was the worst performing currency in Asia, losing 0.70%.

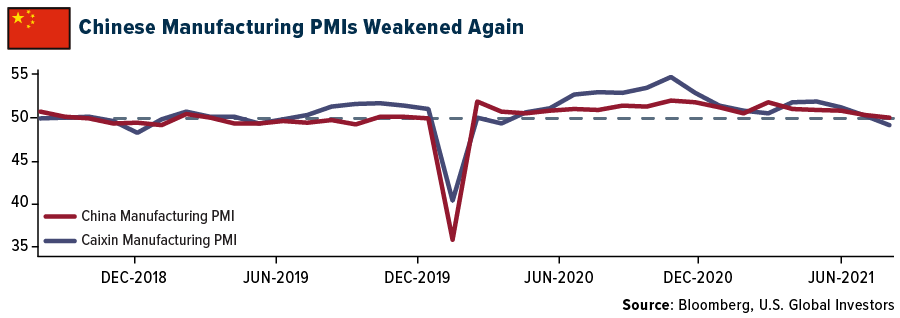

- China PMIs weakened further in August. Manufacturing PMI dropped to 50.1 from 50.4 in July and below the expected 50.2. The Caixin Manufacturing PMI, which measures production in small private companies, fell to 49.2. The biggest decline was noted in the China Service PMI, which fell to 47.5 from 53.3, and well below the 50 level that separates growth from contraction. The Caixin Service PMI fell below the 50 level as well to 46.7, bringing the Caixin China Composite PMI to 47.2.

Opportunities

- Weaker economic data coming out of China has prompted the government to provide additional stimulus. The PBOC has been injecting additional money into the banking system to provide liquidity in the financial markets. In addition, Beijing announced more help for small firms by supporting local banks in issuance loans to micro and small businesses, as well as self-employed individuals.

- China will set up its third mainland stock exchange to serve private companies in its capital of Beijing, President Xi Jinping said Thursday, expanding official support for entrepreneurs in the state-dominated economy. The first mainland stock exchange since the 1949 communist revolution opened in Shanghai in 1990 to raise money for state-owned companies. A second exchange opened in the southern city of Shenzhen, adjacent to Hong Kong, in 1991.

- According to the COVID-19 vaccination tracker, as of September 1, more than half on the Chinese population has been vaccinated (55.8%), coming in close to the United States’ vaccination rate (53.4%). Countries with the highest rates of vaccinations are Canada (68.8%), the United Kingdom (64.5%), Italy (61%) and Germany (60.8%). This week, the EU reported that it has reached 70% fully vaccinated.

Threats

- Ten Eurozone countries are already getting recovery money from the EU, excluding Poland and Hungary. Poland and Hungary could lose large grants and cheap loans from the EU as the European Commission did not approve the distribution of funds due to concerns that the two countries undermine the independence of courts and media freedom. If they are not approved to receive the recovery funds, Poland could lose 23 billion euros in EU grants and 34 billion euros in cheap loans, while Hungary could miss out on 7.2 billion euros in grants.

- Latest Eurozone PPI data came in ahead of expectations, with the July reading up 2.3% month-over-month versus consensus of 1.1%. On a year-over-year basis, prices accelerated 12.1% versus consensus of 11%. Poland reported its highest inflation in the past two decades.

- China will release trade balance data next week and Bloomberg economists predict another weaker data point for the country. Trade balance is August may further decline to $54.4 billion from $56.58 billion in July. Coronavirus restrictions and Chinese port closures in August will likely have a negative effect on trading activity.

Energy and Natural Resources Market

Strengths

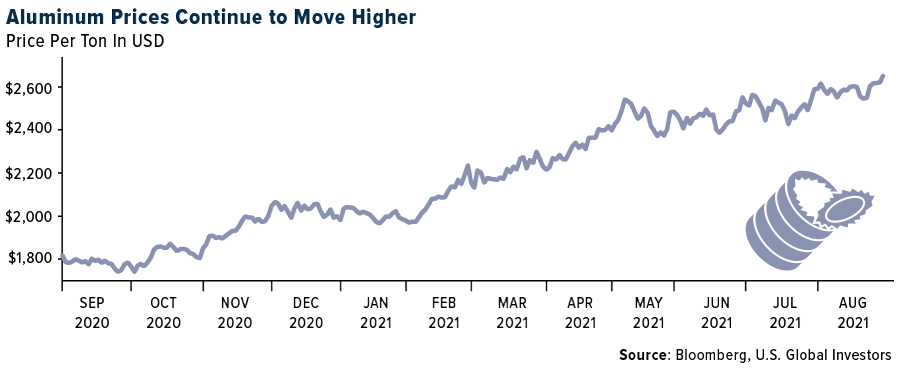

- Lumber was the best performing commodity this week, up 22.10%, on concerns that damage from Hurricane Ida will disrupt supply chains, along with recent announcements of curtailing production at sawmills. Aluminum continues to rise, to nearly the highest in a decade, as deepening Chinese output cuts raise fears of a supply shortfall. The southwestern Chinese province of Guangxi, a major metals producer, will cut output of energy-intensive materials including aluminum. This comes after the Xinjiang autonomous region started similar curbs in August.

- Longi Green Energy Technology Co., the world’s largest solar manufacturer, reported higher first-half profits supported by stronger production and a growing market outside its domestic base in China. Overseas operations accounted for almost half of Longi’s revenue, up from 38% in the same period a year earlier, with new markets emerging in India, Brazil, and Chile to add to continued strong demand from regions including Europe, the U.S., and Australia. Net income rose 21% to 4.99 billion yuan ($771 million) in the first six months.

- Workers at Codelco’s Andina copper mine in Chile accepted the state-owned company’s latest wage offer, signaling the end of a strike that began almost three weeks ago. About 52% of union members voted in favor of the proposal, according to a union statement.

Weaknesses

- The worst performing commodity for the past week was DCE iron ore futures, off 6.63%, on global headline weakness in steel demand. Iron ore futures in Singapore declined as the world’s top steel producer delivered a cautious outlook on price prospects. Iron ore prices have “entered a downward channel” with the implementation of China’s curbs on steel output, Zou Jixin, Chairman of Baosteel, said at an online briefing. The company is sticking to its strategy of keeping stockpiles of raw materials at low levels.

- Credit Suisse has compiled a list of refineries that were safely shut down before Hurricane Ida made landfall. These include PBF’s Chalmette, Shell’s Norco, PSX’s Alliance, PSX’s Lake Charles, VLO’s Meraux, VLO’s Saint Charles and MPC’s Garyville. XOM’s Baton Rouge and CITGO’s Lake Charles were operating at reduced rates. The company estimates over 2 million barrels per day of capacity is currently non-operating due the hurricane. Even if there is no actual damage to any of these refineries, given the excessive flooding and loss of electricity, it could be a few weeks before the refineries are back at full rates.

- Gulf Coast-based producers commenced preliminary assessments of damages following Hurricane Ida’s landfall. ICIS (chemical industry consultants) notes that 95% of the current oil production and nearly 94% of gas production have been shut down. For chemical plants, WLK shut down its Geismar and Plaquemine plants on Saturday, along with Shintech in Addis and Plaquemine. Dow also shut down its plants in St. Charles and Plaquemine, along with BASF idling its Geismar plants.

Opportunities

- Rio Tinto is prepared to make concessions to the government of Mongolia as it aims to finish the development of a copper mine in the Gobi Desert, the Financial Times reports, citing a letter sent to Mongolia’s Prime Minister L Oyun-Erdene last week by copper division head Bold Baatar and Steve Thibeault, head of Canadian subsidiary Turquoise Hill Resources. Baatar and Thibeault offer to collaborate with the government to generate $350 million of additional revenue for Mongolia over the next three years.

- The U.S. installed a record amount of wind-generating capacity last year, adding nearly 17,000 megawatts of power on land, according to an Energy Department. Wind energy’s share of total utility-scale generating capacity in the U.S. was only 11% in 2020, behind natural gas at 43% and nuclear and coal which both represented about 20%. However, wind id gaining. It accounted for 42% of all new capacity in 2020. Solar was second, accounting for 38% of new capacity, followed by natural gas at about 20%. Overall, renewable energy comprised 80% of new capacity added last year.

- Six crackers that make up approximately 16% of ethylene capacity were in the path of Hurricane Ida. It should be noted that 5% of U.S. ethylene capacity was offline before the hurricane, amid planned and unplanned downtime. Supply disruptions of this magnitude (even if temporary) do provide support to ethylene margins, especially given the strength of end markets.

Threats

- New South Wales’ planning regulator rejected a plan by a unit of South Korea’s POSCO to develop a coking coal mine and rail line in the Australian state, saying that the environmental and social impacts would be too great. The Independent Planning Commission (IPC) declined to grant planning permission to Hume Coal for the project, citing the potential impact to groundwater stores and Sydney’s drinking water catchment.

- With Brent crude oil back above $70 per barrel, Citigroup Inc. analysts reiterated their bearish view in a September 1 note. Demand could be threatened by the emergence of new coronavirus strains, while the U.S. and Iran could still reach a deal, allowing for a gradual increase of Iranian exports, although the timeline is likely to be slower than expected.

- A bill that would create the heaviest tax burden among major copper-producing nations was approved by a Chilean senate mining committee on Tuesday. The royalty proposal passed by three votes to two in the committee and will now go to the senate floor for debate, with modifications likely to be presented to soften the blow of a version passed in the lower house in May.

Domestic Economy and Equities

Strengths

- Manufacturing purchasing managers’ index (PMI) data remains strong in the United States. The final August reading was reported at 61.1, slightly lower than the preliminary reading of 61.2.

- Initial jobless claims continue to decline. The weekly number came in at 340,000, which is a new pandemic low. The number, however, is better than consensus for 350,000 and last week’s upwardly revised 354,000.

- Cabot Oil & Gas Corporation was the best performing S&P 500 stock for the week, increasing 13.95%. Oil and gas companies appreciated this week with higher gas and oil prices. U.S. natural gas weekly storage estimates were lower than expected and oil futures topped $70 a barrel for the first time in nearly a month.

Weaknesses

- General Motors is once again significantly cutting production at its North American plants due to the semiconductor chip shortage, signaling that the global parts problem remains a serious issue for the automotive industry. The semiconductor chip shortage is expected to cost the global auto industry $110 billion in revenue in 2021, according to a May forecast from consulting firm AlixPartners.

- August payroll growth was well below economists’ estimates. It also was down from monthly payroll gains of 1.1 million in July and 962,000 in June, the Labor Department said Friday. U.S. payrolls grew by 235,000 in August, well below the expected 733,000.

- Wells Fargo was the worst performing S&P 500 stock for the week, losing 11.32%. Shares declined after U.S. regulators warned that it may impose new sanctions on the bank tied to its years-old sales practice scandals.

Opportunities

- Equities moved higher this week supported by last week’s dovish comments from the Federal Reserve. The S&P 500 hit a new high intra-week and may continue to climb even higher. Investors are closely watching the jobs market; any weaker data will suggest further extension of monetary policy accommodation.

- Nominal wages and salaries have been raising in the U.S. putting more buying power in consumers’ hands and driving consumer spending. Ed Hyman from Evercore ISI said that nominal wages and salaries increased more than 1% month-over-month in July and increasing at an 8% annual rate in the second quarter. At the same time, the surge in corporate profits is providing firepower for business spending.

- Next week is a short trading week in the U.S. due to the Labor Day holiday on Monday. Nevertheless, important economic data will be released. The JOLTS job openings, initial jobless claims, continuing claims, and producer price index (PPI) data will be reported after the long weekend.

Threats

- Businesses are still struggling with finding workers. Walmart, the nation’s largest private employer, said Thursday that it is raising the hourly wages for more than 565,000 store workers by at least one dollar. The retail industry must find ways to attract the labor force, particularly before the busy holiday shopping season ramps up.

- Economists at Morgan Stanley cut their third-quarter gross domestic product (GDP) forecast from 6.5% to 2.9%. The markdown includes consumption cut from 2.9% to 0.3%. Another concern is the ongoing supply constraints holding back high-value-add industries like automobiles, reflected by four straight months of declining auto sales. However, the economists left the fourth quarter GDP forecast at 6.7%

- Nearly 94% of crude oil production in the Gulf of Mexico remined shut on Thursday after Hurricane Ida left the area. OPEC members agreed to lift production. Crude oil has rallied about 40% this year and could continue to climb higher.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Presearch, rising 579.27%.

- Asset manager Franklin Templeton is increasing staff to execute trades for Bitcoin and Ether, writes CoinDesk, according to a series of job postings. According to the listings, at least two crypto-focused jobs were posted this week – one trader, one researcher – to join the growing investments team within the company’s Digital Assets Management division.

- Japanese financial conglomerate SBI Holdings is aiming to launch the country’s first cryptocurrency fund by the end of November, writes Bloomberg, aiming to give individual investors a way to diversify their broader portfolio. According to the article, investors may need to put in a minimum of roughly 1 million yen ($9,100 USD) to 3 million yen ($27,360 USD) and it will primarily be aimed at people who understand risks associated with cryptocurrencies, such as big price swings.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Liquidity Dividends Protocol, down 99.63%.

- Ever since John Paulson bet against the U.S. housing market more than a decade ago, people keep asking him about his next big trade, writes Bloomberg. His harshest words, the article continues, are for the hottest investments of this era. SPACs, on average will be a losing proposition, while cryptocurrencies are a bubble that will “eventually prove to be worthless,” according to Paulson.

- Federal regulators sued the founder of crypto exchange platform BitConnect, reports Bloomberg, for fraudulently raising more than $2 billion from investors in an offering that wasn’t registered with the U.S. SEC. A complaint filed this week in federal court in New York shows that the SEC sued founder Satish Kumbhani and a promoter for improperly selling securities tied to the company’s purported “lending program” for about a year starting in January of 2017.

Opportunities

- As reported by Bloomberg, FTX.US has agreed to acquire LedgerX for an undisclosed sum, a move that will expand the crypto exchange’s product offerings to futures and options trading in the U.S. “Our longer-term expansion strategy is for FTX.US to offer a wide array of asset classes in regulated markets, and this is our first major step in that direction,” said Brett Harrison, president of FTX.US.

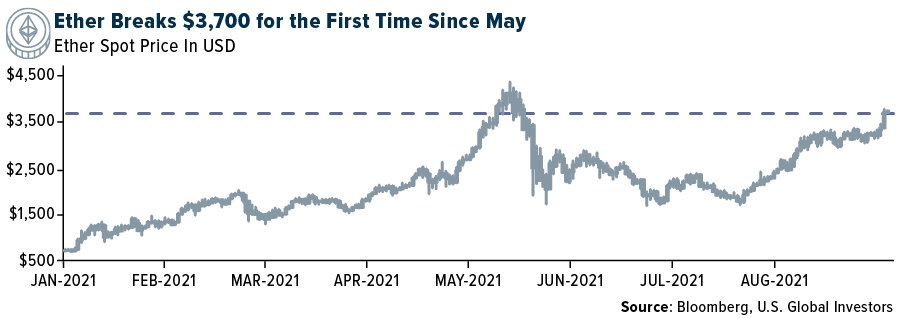

- Ether is off to a blazing start in September, writes Bloomberg, breaking $3,700 intraday on the first of the month and after logging a 36% return last month. The popular digital currency may be running a bit hot, however, as it continues to outperform Bitcoin in a big way this year. The crypto crossed into overbought territory on Monday, the article continues, indicating that investors should be aware of a potential pullback.

- Solana (SOL) started Friday at a new record high, reports CoinTelegraph, as investors continued to bet positively on its success in the DeFi and nonfungible tokens (NFT) sector. “The growth of Solana to $146.28 is steered positively by the increasing demand for the tokens for use in minting thousands of NFTs being launched on the Solana blockchain,” Yuriy Mazur, head of data analytics at crypto exchange CEX.IO told CoinTelegraph via email this week.

Threats

- Retirees and veterans living in El Salvador are worried that the government will start paying their pensions in Bitcoin instead of the U.S. dollar, writes CoinTelegraph. The country’s anti-Bitcoiners have expressed discontent regarding the government’s plans to adopt the popular digital currency as legal tender, (retirees in particular) voicing their concerns over its unstable price. “We know this coin fluctuates drastically. Its value changes from one second to another, and we will have no control over it,” Stanley Quinteros, a member of the Supreme Court of Justice’s workers’ union said.

- Former chief U.S. commodities regulator Cristopher Giancarlo (“Crypto Dad”) has resigned from BlockFi’s board of directors after four months, reports CoinDesk. His unexpected departure comes at a critical juncture for BlockFi, as the company faces mounting legal pressure over its flagship interest-bearing crypto accounts. According to the article, multiple U.S. states alleged in July that the company’s flagship BlockFi Interest Accounts (BIA) were unregistered securities, including regulators in BlockFi’s home state of New Jersey.

- Russian cybersecurity firm Kaspersky has detected more than 1,500 fraudulent entities targeting potential crypto investors and miners just in the first half of 2021, writes CoinTelegraph. The firm’s research shows that 0.60% of users from South African countries have already been targeted by malicious crypto miners. The most common methods of duping users, the article continues, involves false advertisements claiming to sell mining equipment and fake websites posing as crypto exchanges.

Gold Market

This week spot gold closed the week at $1,827.73, up $10.16 per ounce, or 0.56%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.05%. The S&P/TSX Venture Index came in up 3.56%. The U.S. Trade-Weighted Dollar fell 0.61%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-30 | Germany CPI YoY | 3.9% | 3.9% | 3.8% |

| Aug-31 | Eurozone CPI Core YoY | 1.5% | 1.6% | 0.7% |

| Aug-31 | Conf. Board Consumer Confidence | 123.0 | 113.8 | 125.1 |

| Aug-31 | Caixin China PMI Mfg | 50.1 | 49.2 | 50.3 |

| Sep-1 | ADP Employment Change | 625k | 374k | 326k |

| Sep-1 | ISM Manufacturing | 58.5 | 59.9 | 59.5 |

| Sep-2 | Initial jobless Claims | 345k | 340k | 354k |

| Sep-2 | Durable Goods Orders | -0.1% | -0.01% | -0.1% |

| Sep-3 | Change in Nonfarm Payrolls | 733k | 235k | 1053k |

| Sep-7 | ZEW Survey Expectations | 30.5 | — | 40.4 |

| Sep-7 | ZEW Survey Current Situations | 34.0 | — | 29.3 |

| Sep-9 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Sep-9 | Initial Jobless Claims | 345k | — | 340k |

| Sep-10 | Germany CPI YoY | 3.9% | — | 3.9% |

| Sep-10 | PPI Final Demand YoY | 8.2% | — | 7.8% |

Strengths

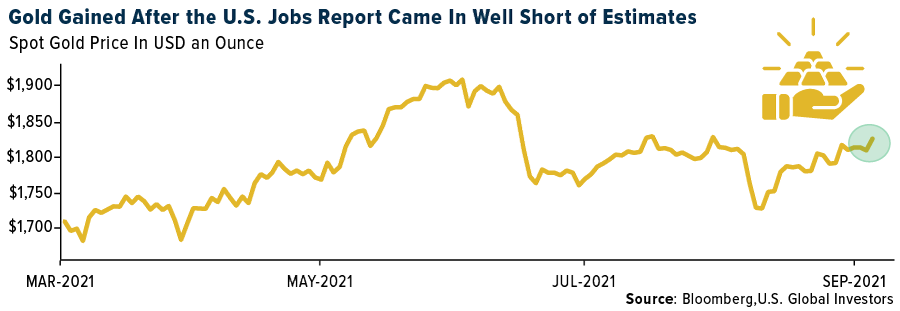

- The best performing precious metal for the week was silver, up 2.87%, outpacing gold on the sensitive jobs report update. Gold jumped after a key labor-market report showed the U.S. economy added fewer jobs than forecast, diminishing the possibility that the Federal Reserve will taper stimulus soon. Nonfarm payrolls data showed the U.S. added 235,000 jobs in August, well below economists’ forecasts and far less than the gains seen last month, reports Bloomberg. The dollar sank after the report, boosting gold. Bullion has struggled this year amid a global economic rebound from the pandemic, which has raised the prospect of central banks reining in their monetary stimulus.

- Sales of gold bracelets, pendants, earrings, and necklaces that draw on dragons, phoenixes, peonies and other traditional Chinese patterns and symbols, are flying among consumers, especially those in their 20s and 30s, reports Reuters. The popularity among millennials is helping drive a rebound in gold demand in the country after a pandemic-induced slump. An e-commerce boom and national pride are fueling the rise in demand for what is known as heritage gold jewelry, which requires intricate craftsmanship and can command premiums of 20% or more over conventional gold jewelry, industry executives say.

- Impala Platinum Holdings Ltd. announced a four-fold increase in its dividend after surging platinum prices yielded a record profit. The final dividend of 9.8 billion rand ($680 million) brings the total payout for the year to the equivalent of about 50% of free cash flow.

Weaknesses

- The worst performing precious metal was palladium, which finished the week essentially unchanged in price. Australia’s gold production was 157 tons in the first half of 2021, four tons more than China’s output in the same period, according to Surbiton Associates. China’s gold output was adversely affected by accidents and resulting shutdowns, director Sandra Close said in a statement.

- Centerra Gold Inc. is claiming that a Kyrgyz open-pit mine it once ran has flooded and poses safety and environmental risks, reports Bloomberg, although the government-appointed administrator says the water has always been there. There could be at least 40 meters of water at the bottom of the Kumtor central pit, the Canadian mining company said in a statement, citing photos on Kumtor Gold Co.’s website and a company video posted mid-August on Facebook.

- Gunmen attacked a convoy of Iamgold Corp vehicles traveling to the Essakane gold mine in Burkina Faso on Tuesday, reports Reuters, wounding one police officer before being repelled by the convoy’s security detail, the Canadian mining company said. Following the attack, Iamgold has suspended convoys to and from Essakane, which is the company’s biggest operating mine and is near the border with Niger.

Opportunities

- K92 Mining reported its latest batch of assay results from its ongoing drilling program on the Judd vein system at the Kainantu Mine. These 17 holes, part of the initial drill program at Judd, showcase high-grade intercepts over a strike length of 650 meters, thus defining an area of notably high-grade mineralization with solid thickness. Silver X Mining reported channel samples from its Tangana 1 vein of up 70.88 grams per ton gold over 0.95 meters, 1,675 grams per ton silver over 0.95 meters, 7.37% lead over 0.60 meters, and 6.75% zinc over 0.80 meters. The sampling program now extends the mineralized horizon by 120 meters and vertically another 200 meters in depth.

- Veteran investor Mark Mobius says investors should have 10% of a portfolio in gold as currencies will be devalued following the unprecedented stimulus rolled out to fight the coronavirus pandemic. At this stage, “10% should be put into physical gold,” said Mobius, who set up Mobius Capital Partners after more than three decades at Franklin Templeton Investments.

- After 14 years of trailing China, Australia is poised to be the world’s largest gold producer this year. In the first half of 2021, Australia produced 157 tons of gold versus 153 tons in China. Exploration successes like De Grey Mining’s Hemi gold project and Chalice Mining’s Julimar Nickel Copper-PGE project are world class mineral discoveries formed in Australia in recent years.

Threats

- Sibanye Stillwater CEO Neal Froneman said palladium could decline to about $1,000 an ounce after 2025, as automakers switch to using more platinum in auto catalysts used to curb pollution from vehicles. “Palladium is somewhat at risk post-2025 and in addition, as the demand drops off, there are a number of new palladium-rich projects coming into production,” he said. “If demand falls and supply increases, the prices will drop, they will probably drop down to levels of around $1,000 an ounce”

- Around 28% of Brazilian gold exports in 2019 and 2020 likely came from illegal mines, a report by public prosecutors and the Federal University of Minas Gerais found, pointing to widespread forging of documents and lack of effective law enforcement. This gold production is unregulated, and mercury is typically used to extract the gold, creating an environmental risk.

- Nevada lawmakers on the final day of the 81st Legislative Session set in motion a significant shift in tax policy toward an industry that has long been scrutinized for having a unique constitutional carve-out protecting it from tax hikes. Assembly Bill 495 was a bipartisan compromise forced by multiple proposed ballot questions aimed at some of the most politically powerful industries within the state. The bill would create a new excise tax on gold and silver mining companies with more than $20 million in gross revenue annually. Gross revenue between $20 million and $150 million would be taxed at 0.75% and gross revenue above $150 million would be taxed at a rate of 1.1%.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

EasyJet PLC American Airlines

Ryanair Holdings

WizzAir Holdings Plc

Impala Platinum Holdings

Centerra Gold Inc.

Iamgold Corp

K92 Mining

Silver X Mining Corp.

De Grey Mining Ltd.

Chalice Mining Ltd.

Sibanye Stillwater Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

JOLTS Job Openings is a survey done by the US Bureau of Labor Statistics to help measure job vacancies.

The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

Free Cash Flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base.