With Everything Up Right Now, Where are the Value Buying Opportunities?

Date Posted: April 30, 2021

Read time: 51 min

If you've ever wondered what trillions of dollars in monetary and fiscal stimulus looks like, it appears you got your answer. Everything is up right now.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

If you’ve ever wondered what trillions of dollars in monetary and fiscal stimulus looks like, it appears you got your answer. Everything is up right now.

Stocks are up. Earnings are up. Consumer spending is up. Commodities are up. Food prices are up. Home prices are up. Car prices are up. Cryptos are up.

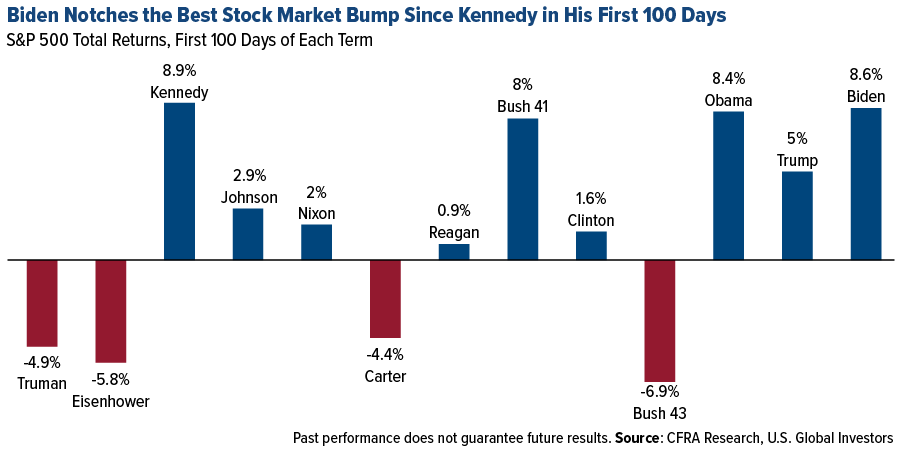

This week marked President Joe Biden’s 100th day in office. Since Inauguration Day, the S&P 500 has increased an impressive 8.6%. Those are the best returns for the start of a presidential term since Kennedy in 1961. All those stimmy checks have to go somewhere.

With the Federal Reserve signaling it will keep accommodative measures in place for some time longer, and Biden making the case for trillions more in government spending, is this what we can expect going forward?

And with everything up, where are the value buying opportunities?

Pain at the Car Lot and Grocery Store

Before I get into that, it’s important I point out that not every example of price appreciation is being driven strictly by stimulus checks and money-printing. Pandemic lockdowns are still having a massive effect on the global supply of everything from building materials to semiconductor chips, which is driving up production costs that are being passed on to consumers.

Take lumber. Because sawmills have had trouble ramping up production to meet demand, the price of framing lumber has skyrocketed 250% over the past 12 months to around $1,200 per thousand board feet. This has added close to $36,000 to the price of a new home, according to the National Association of Home Builders (NAHB).

Indeed, home prices surged 12% in February compared to the same month last year, S&P Dow Jones Indices reported this week. That’s the fastest annual pace since 2006, soon before the housing bubble burst.

Or take the ongoing chip shortage, which has been exacerbated in recent months by the winter freeze in Texas and a fire at Japan’s Renesas Semiconductor Manufacturing plant. According to Goldman Sachs, the shortage has impacted a whopping 169 industries, most notably carmakers. This week General Motors President Mark Reuss told Fox Business that the crisis “is probably the worst crisis I’ve seen in the auto industry, at least in my career, in terms of supply chain.”

As a result, the price of used vehicles, as measured by the Manheim Used Vehicle Value Index, has increased 52% over the past year. Preowned pickups have jumped an unbelievable 75%.

And then there’s food and consumer staples such as diapers and toilet paper. Recently I shared with you that corn prices have almost doubled over the past year, and this week Bloomberg reported that corn has gotten so pricey that some farmers are feeding their livestock wheat intended for human consumption. A host of consumer goods giants, from Procter & Gamble to Kimberly-Clark, have all announced they’ll be raising their prices in the coming months as commodity prices continue to soar.

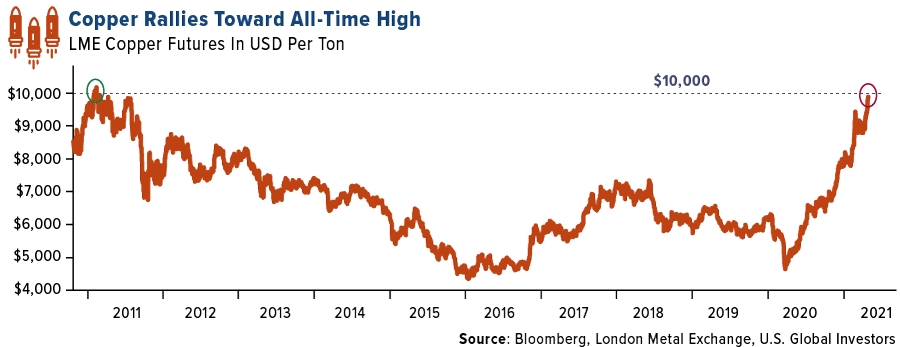

Copper Near Record Highs

Iron ore and copper are both near record highs on tight supply and strong demand from China. Copper traded above $10,000 per tonne this week, its highest level in 10 years, as investors anticipate further supply constraints on global efforts to decarbonize and electrify everything.

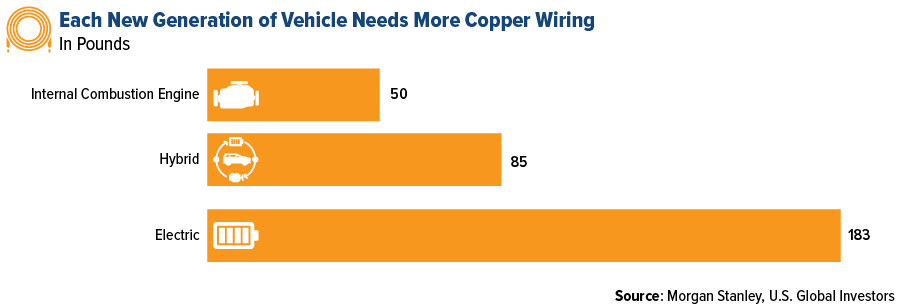

To give you some idea of what I’m talking about, the NAHB this week recommended to homebuilders that they should start pre-wiring new houses for electric vehicle (EV) charging. That calls for more copper wiring in the home as well as the vehicle.

Several car manufacturers have already announced they’ll be phasing out internal combustion engine (ICE) vehicles in favor of EVs between 2025 and 2040. As I’ve mentioned before, EVs require three to four times as much copper wiring as a traditional vehicle. Morgan Stanley reports that ICE vehicles use around 50 pounds of copper on average, compared to 85 pounds for a hybrid and as much as 183 pounds for an EV.

Ivanhoe Mines remains our favorite way to play the copper rally. The company, which reported phenomenal production results in early April at its Kamoa-Kakula project, has yet to report first-quarter earnings. However, other copper companies have, and results so far have been amazing. Brazil’s Vale, for instance, reported incredible net income of $5.6 billion, well above Wall Street estimates.

Gold Miners Should HODL

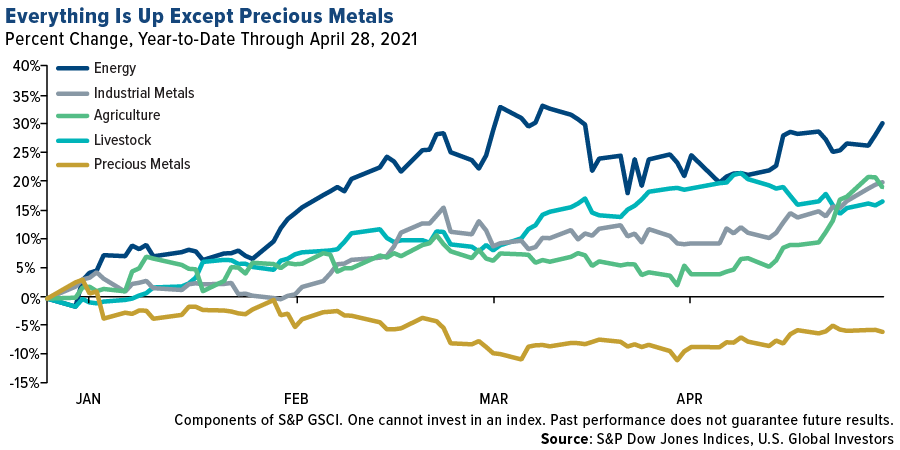

The chart below says it all. Every commodity subindustry of the S&P GSCI is up double digits for the year, with the one exception of precious metals.

That’s where I see the opportunity right now. Not only is gold on sale, but so are the gold and precious metal miners, particularly the royalty and streaming companies. Whereas the NYSE Arca Gold Miners Index is down close to 5% for the year, the big three royalty and streaming companies have performed relatively well, with Franco-Nevada up 12%, Royal Gold up 6% and Wheaton Precious Metals essentially flat.

As for the producers, I would like to see them “HODL” gold as we wait for higher metal prices on unprecedented money-printing and fiscal stimulus. (HODL, in case you’re not aware, is crypto-trading lingo to describe a buy and hold strategy.)

Between the U.S., Europe and China and others, we’ve spent a collective $17 trillion (and counting) to combat the coronavirus and the economic havoc it’s wreaked. Gold has historically tracked the growth in money supply, and in March, the amount of money circulating the global economy expanded more than 17% in March compared to last year, according to Haver Analytics.

Crypto Prices Are Up, but What About the Miners?

Speaking of cryptos… Ether, the number two cryptocurrency by market cap, hit an all-time high of nearly $2,800 this week, outperforming Bitcoin, which is still off its recent high of over $63,000. Ether’s price surge could be related to reports that DeFi, or decentralized financing, is now a $100 billion industry. In fact, according to calculations by CoinGecko, the market cap for DeFi coins, which includes Ether, now stands at more than $128 billion.

Ether, Bitcoin and other coins also continue to benefit from Metcalfe’s law, which says that a network’s value increases geometrically as the number of users within that network increases. Visa, Paypal and Venmo have recently announced they will allow their hundreds of millions of customers to use cryptos as a method of payment, while PayPal also permits trading of Bitcoin, Ethereum, Litecoin and Bitcoin Cash.

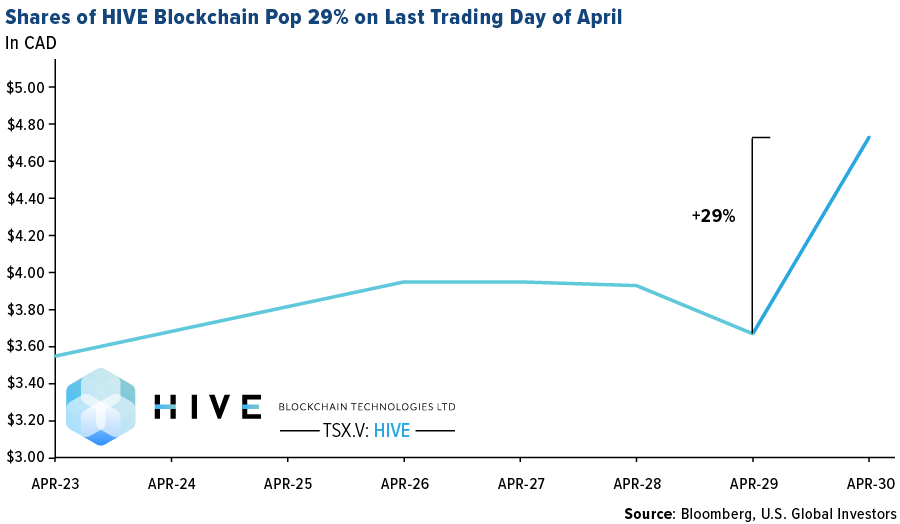

With cryptos up big right now, you may be wondering why the miners aren’t. HIVE Blockchain Technologies, the only miner that mines both Ether and Bitcoin using 100% green energy, is currently off about 44% from its 52-week high of C$7.25 in February. That’s after a nearly 30% gain on Friday alone, its best single-day jump since December. It goes without saying that the crypto-mining ecosystem remains highly volatile.

There may be a number of contributing factors to the discrepancy between cryptos and miners, but as I see it, one of the biggest involves Coinbase. As you know, the crypto exchange went public in mid-April in a direct listing. This had the effect of siphoning off billions in investor flows that may have instead gone toward shares in the crypto miners. On the first day of trading alone, Coinbase CEO Brian Armstrong sold nearly $292 million in shares. Other directors and executives sold even more, with one pocketing more than $1.8 billion.

It’s important to keep in mind that Coinbase hasn’t been listed for more than 30 days right now, so it still has that new car smell. I believe investors will rotate back into the miners such as HIVE once they see a jump in earnings.

For more on cryptos and Metcalfe’s law, watch my video here or by clicking below. Be sure to give it a thumbs up and subscribe to our YouTube channel!

Gold Market

This week spot gold closed the week at $1,769.13, down $8.07 per ounce, or 0.45%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.99%. The S&P/TSX Venture Index came in up 2.65%. The U.S. Trade-Weighted Dollar rose 0.49%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-26 | Durable Goods Orders | 2.3% | 0.5% | -1.2% |

| Apr-27 | Hong Kong Exports YoY | 15.8% | 26.4% | 30.4% |

| Apr-27 | Conf. Board Consumer Confidence | 113.0 | 121.7 | 109.0 |

| Apr-28 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Apr-29 | Germany CPI YoY | 1.9% | 2.0% | 1.7% |

| Apr-29 | Initial Jobless Claims | 540k | 553k | 566k |

| Apr-29 | GDP Annualized QoQ | 6.7% | 6.4% | 4.3% |

| Apr-29 | Caixin China PMI Mfg | 50.9 | 51.9 | 50.6 |

| Apr-30 | Eurozone CPI Core YoY | 0.8% | 0.8% | 0.9% |

| May-3 | ISM Manufacturing | 65.0 | — | 64.7 |

| May-4 | Durable Goods Orders | — | — | 0.5% |

| May-5 | ADP Employment Change | 888k | — | 517k |

| May-6 | Initial Jobless Claims | 540k | — | 553k |

| May-7 | Change in Nonfarm Payrolls | 970k | — | 916k |

Strengths

- The best performing precious metal for the week was palladium, up 2.85%. Palladium surged above $3,000 an ounce for the first time ever as the global shortage for the precious metal deepens on strong demand from automakers. Palladium is up over 20% so far this year, building on five straight annual gains, according to Bloomberg data. Gold production is forecast to grow 6% in 2021, according to S&P. Gold production had fallen to a six year low in 2020 due to pandemic lockdowns.

- The World Gold Council (WGC) says China’s demand for gold bars and coins will remain robust and investor interest is likely to be positive in 2021. China, the world’s top consumer of bullion, saw jewelry demand rise 212% year-over-year in the first quarter to 191.1 tons, the highest amount since 2015. Chinese gold ETFs saw inflows of 11.5 tons in the first quarter, contrasting with the global trend of outflows.

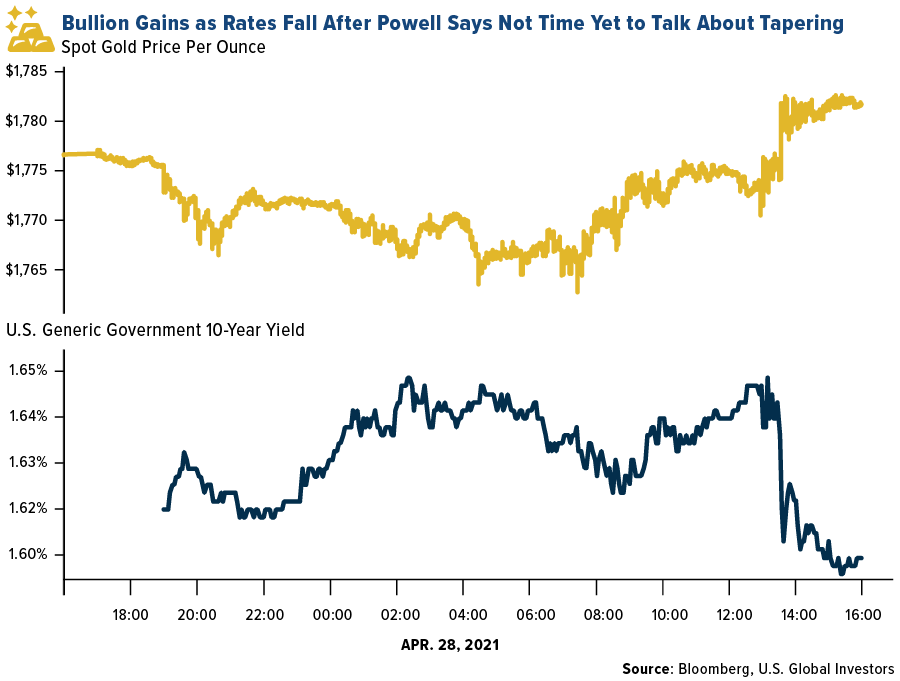

- Gold rose on Wednesday after Fed Chair Jerome Powell said it is “not time yet” to start conversations about slowing the pace of purchases by the central bank, reports Bloomberg. Bullion is up from a nine-month low hit in March as bond rates and the U.S. dollar weaken.

Weaknesses

- The worst performing precious metal for the week was platinum, down 2.31%, perhaps on investors jumping into sister metal palladium. Auto production cuts, some as much at 50%, on the worldwide computer chip supply chain shortage could weaken platinum demand near-term. After staging a comeback in April, gold saw a weekly loss for the first week in four as bond yields and the dollar firmed up.

- The worsening COVID-19 pandemic in India could hamper its gold demand recovery. WGC reported consumer demand rose 37% in the first quarter but could fall again as the total number of cases rises past 18 million. Many states have reimposed restrictions and shut non-essential businesses such as jewelry shops.

- Newmont, the world’s largest gold producer, reported first quarter production 6% below consensus, which resulted in earnings and cash flow being below expectations. Earnings per share were 74 cents, below the 80-cent estimate for the first quarter.

Opportunities

- Gold Fields plans to set carbon emission reduction and workforce diversity targets by the end of 2021 and aims to become net zero carbon by 2050. Russian producer Polymetal seeks to cut greenhouse emission intensity per ounce of gold equivalent by 30% by 2023. The company announced on Thursday that it will run 100% on renewable power and has already agreed to get 90% of its needs from hydropower. Miners that cater toward more ESG-conscious investors could attract more capital.

- Fortuna Silver Mines is acquiring Roxgold. Fortuna shareholders will own 64% of the combined company. The price offered is a 42% premium to the pre-announcement price but is at 0.88x of NAV. The company aims to have a low-cost platform for gold and silver in the world’s fastest growing metals producing regions. Again, we see another acquisition proposed in the gold space because the target’s share price is too low for the value that can be identified within its holdings. The current synergy is just the surface of the value within Roxgold in the future. Other mining companies in West Africa should consider what their logistical synergies could bring to the table.

- Gold companies with exposure to copper are set to benefit from surging prices for the red metal, especially during periods of weak bullion prices. Newmont, the world’s largest gold producer, is boosting its exposure to copper through “mega projects.” CEO Tom Palmer said copper will account for 15 to 20% of the miner’s total output by the end of the decade. Despite the negativity surrounding bullion, Palmer said in a Bloomberg TV interview that gold prices are at “healthy levels.”

Threats

- ETFs sold 755,476 troy ounces of gold on Wednesday, the biggest one-day decrease since 2016, to bring net sales for 2021 to 8.43 million ounces, according to Bloomberg data. Total gold held by ETFs is down 7.6% so far this year, a continued trend that shows investors are moving on from the yellow metal.

- Diamond Foundry received a $200 million investment by Fidelity to fund a lab-grown diamond startup. The goal is to compete with gemstone miners like DeBeers. The immediate goal is to quadruple production at its Washington state factory to 5 million carats per year by 2022.

- Russian miners may face U.S. sanctions, according to former U.S. Government officials and S&P. Sanctions have already been placed on Russia for meddling in the 2020 election, gathering troops on the Ukraine border, sending warships to the Black Sea and having a global cyber espionage campaign. Russia represents 45% of global palladium production and 14% of global platinum production.

Index Summary

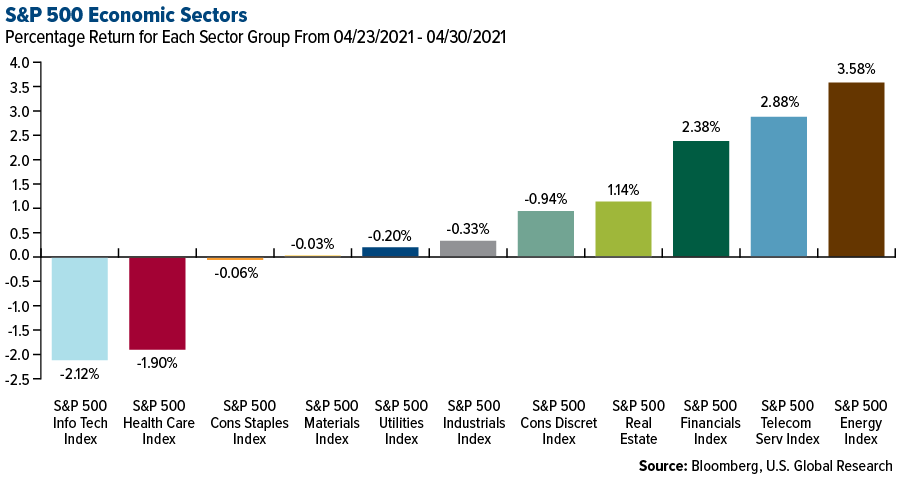

- The major market indices finished mostly down this week. The Dow Jones Industrial Average lost 0.50%. The S&P 500 Stock Index rose 0.01%, while the Nasdaq Composite fell 0.39%. The Russell 2000 small capitalization index lost 0.23% this week.

- The Hang Seng Composite lost 1.10% this week; while Taiwan was up 1.54% and the KOSPI fell 1.20%.

- The 10-year Treasury bond yield rose 7 basis points to 1.628%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Polygon, rising 150.67%.

- Ether, the native token on the Ethereum blockchain, skyrocketed to new all-time highs of almost $2,800 this week on the back of positive news from the European Investment Bank (EIB). The EIB is set to issue a two-year 100-million-euro digital bond on the Ethereum network, with the sale being led by Goldman Sachs, Banco Santander and Societe Generale. Moody’s and Fitch have awarded the bond with the top triple-A rating. Ethereum’s total market capitalization exceeded $315 billion, topping that of mined platinum which is currently estimated at around $303 billion. Ethereum’s returns are more than twice that of Bitcoin over the past one year.

- Paxos, a major cryptocurrency firm, closed its $300 million Series D funding round that included Oak HC/FT, Declaration Partners, PayPal Ventures and others, that values the company at $2.4 billion. The deal comes on the back of Paxos securing a conditional charter from the U.S. Office of the Comptroller of the Currency (OCC) to spin up the Paxos National Trust Bank, making it the first crypto-native company to win this approval for a national trust bank. CEO Charles Cascarilla said in an interview that the company is planning on using this capital injection to scale their business and make strategic acquisitions.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Celsius, down 1.34%.

- Bitcoin is on track to post its worst month since January, with the cryptocurrency down 10% month-to-date even after retracing roughly 50% of the selloff it experienced in these past two weeks, which ended at a low of around $47,000. On the technical side, Bitcoin remains below its 50-day moving average, a sign of slowing momentum, and is facing resistance around $56,000.

- Hotbit, a Chinese cryptocurrency exchange, reported that it had to shut down all services after an attempted cyberattack. The said the hackers were unable to gain access to Hotbit wallets, but they compromised the platform’s user database. The maintenance could take at least seven days and the investigation and system upgrade could take as long as two weeks.

Opportunities

- WisdomTree Investments reported that it has listed its Ethereum exchange-traded product (ETP) on the Deutsche Boerse’s Xetra market in Frankfurt and the Swiss Stock Exchange (SIX) in Zurich. Trading under the ticker ETHW, the physically backed ETP will track the spot price of Ethereum and has an expense ratio of 0.95%. This listing follows WisdomTree’s Bitcoin ETP, trading under the ticker WBIT, being listed on the Xetra market on April 14. WisdomTree also submitted a filing in March with U.S. Securities and Exchange Commission (SEC) for a Bitcoin ETF that would trade on the Chicago Board Options Exchange’s bZx platform, which is currently under review.

- Mastercard CEO Michael Miebach announced during the company’s first quarter earnings call that the company is planning to help the government evaluate the utility of central bank digital currencies (CBDCs) outside of just payments. Miebach added that Mastercard is exploring applications that can exist on top of CBDCs and is heavily investing in smart contract technology.

- Osprey Funds announced it is launching the Osprey Polkadot Trust, which will be available to accredited investors with a $25,000 minimum and will be listed on the OTCQX market. CEO Greg King said that appetite for next generation crypto investment vehicles is increasing and that their decision to launch a Polkadot trust is both a vote of confidence and addresses consumer demand for access vehicles.

Threats

- BaFin, Germany’s Financial Supervisory Authority, has issued a warning to investors that Binance might have violated European securities rules with its stock tokens that track the movement of shares in Tesla, Coinbase, MicroStrategy and Apple and are settled using Binance USD (BUSD). BaFin said that the Binance stock tokens require a prospectus, which was not issued prior to trading, and that the violation constitutes an administrative offense. The company could be fined up to $6 million or 3% of its annual revenue.

- Reuters reported that the Beijing Municipal Bureau of Economy and Information Technology issued an emergency notice to the city’s data centers asking them to report any involvement in crypto mining operations. These operations have come under scrutiny lately due to its consumption of large amounts of energy and subsequent environmental impact. Inner Mongolia, an autonomous region in China, is set to force crypto mining businesses to close shop by the end of April.

- The Ransomware Task Force, led by the Institute for Security and Technology with support from Microsoft, McAfee and various government agencies, reported that better enforcement of cryptocurrency regulations can help address an increasing number of ransomware attacks. In 2020, ransomware victims paid close to $350 million in cryptocurrencies to attackers last year. The task force recommended that existing know-your-customer (KYC) and anti-money laundering (AML) laws should be enforced internationally to help tam down payments made in crypto. The task force also mentioned that attackers prefer being paid in Bitcoin and warns that attackers might use mixing services to obfuscate how the transactions occur.

Domestic Economy and Equities

Strengths

- Gross domestic product (GDP), the sum of all goods and services produced in the economy, jumped 6.4% for the first three months of the year on an annualized basis. Outside of the reopening-fueled third-quarter surge last year, it was the best period for GDP since the third quarter of 2003.

- U.S. consumer confidence jumped to a 14-month high in April as increased vaccinations against COVID-19 and additional fiscal stimulus allowed for more services businesses to reopen, boosting demand and hiring. The Conference Board’s consumer confidence index raced to a reading of 121.7 this month. That was the highest level since February 2020, just before the onset of the COVID-19 pandemic. It was the fourth straight monthly increase in the index.

- United Parcel Service was the best performing S&P 500 stock for the week, increasing 13.87%. UPS delivered a blowout quarter as the package delivery company posted a 27% year-on-year growth in first quarter revenues to $22.9 billion. Adjusted diluted EPS of $2.77 per share jumped 141% year-on-year and beat consensus estimates of $1.73 per share.

Weaknesses

- Dallas Federal Reserve Bank President Robert Kaplan said on Friday that he is concerned about potential leverage, excess risk-taking in the nonbank financial system and added that they need more visibility, as reported by Reuters. "If the world grows more slowly, the US economy will grow more slowly than it would otherwise," Kaplan added. "Vaccinations are the primary economic development tool worldwide."

- Pending home sales, a measure of signed contracts on existing homes, rose 1.9% in March compared with April, according to the National Association of Realtors. Home prices, already sky high, are continuing to rise at a pace not seen in more than 15 years. Strong demand and record-low supply are fueling bidding wars across the nation. The average contract rate on the 30-year fixed mortgage started the month at 3.22% and ended around 3.45%, according to Mortgage News Daily. It started the year at 2.76%.

- Twitter Inc was the worst performing S&P 500 stock for the week, decreasing 17.80%. The social media company posted a sluggish start to the year in its advertising business and gave a disappointing revenue forecast, a sign the platform hasn’t fully capitalized on the digital advertising boom amid the pandemic like companies such as Facebook Inc. and Google.

Opportunities

- Goldman Sachs recommends taking advantage of the recent pullback in Boeing’s shares as its end-market is recovering. Analyst Noah Poponak said that recent data points on air travel were positive and showed clear stabilization in the aircraft order book and production rates. He also noted that BA has largely resolved its individual aircraft challenges with the 787 and the MAX.

- Cimarex Energy and Devon Energy were upgraded at Evercore ISI, which sees a “new paradigm” across the E&P sector with a reset of reinvestment targets and in turn growth expectations. Analyst Stephen Richardson says the E&P space should become more insulated against commodity volatility and sees Cimarex and Devon as “logical extensions of a more bullish view.

- Floral and foods gift retailer 1-800-Flowers.com posted record earnings and received a buy rating from D.A. Davidson & Co, which said the company has evolved into a best-in-class e-commerce company. Analyst Linda Bolton Weiser raised her recommendation from neutral and almost doubled her price target to $57.

Threats

- Ebay shares tumbled as much as 10% Thursday, the most since October 2019, after the online marketplace issued a revenue forecast for the current quarter suggesting spending on the site could recede as more people get vaccinated. Wedbush and Susquehanna downgraded the stock, while several firms trimmed their price targets.

- Verizon Communications was downgraded to neutral from buy at MoffettNathanson, which wrote that results from AT&T suggested “a period of greater competitive intensity” ahead that could pressure the stock. AT&T’s results showed its ability to sustain its promotional stance, and if this continues, “Verizon and T-Mobile will feel more and more pressure to respond” by cutting wireless prices.

- Cree reported an adjusted third-quarter gross margin that was below expectations, prompting a round of cautious commentary. JPMorgan downgraded the semiconductor device company, also citing the stock’s valuation.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 11.13%. Lumber futures continued the record rally as sawmills struggle to meet increasing demand, with the biggest U.S. producer reporting that it is sold out of certain key homebuilding materials for the next several weeks. In the past year, lumber prices have quadrupled, fueled by an unexpected surge in home building and renovations.

- Copper topped $10,000 a ton this week for the first time in a decade. The metal’s recent rally has made it one of the best performers this year, fueled by stimulus measures, near-zero interest rates and the global economic recovery from the pandemic. In the last month, trading groups and banks have increased their price target for copper to more than $10,000, citing increased future demand for the metal due to countries pledging to decarbonize their economies.

- The rally in crude oil prices helped Exxon Mobil Corp. and Chevron Corp. to generate the most free cash flow in more than a year. A boost in energy demand around the world and demand for chemicals used in plastics offset losses from refining units of the largest North American explorers. Exxon posted its first positive free cash flow figure since late 2018, at roughly $6 billion, while Chevron’s free cash flow stood at $3.4 billion. Both oil giants mentioned that a key driver of cash-flow increases was steep cuts in spending as less risky endeavors such as shale drilling was favored over costlier mega-projects. Exxon earnings per share (EPS) stood at $0.64 a share for the first quarter, beating the $0.61 cents a share estimate from analysts.

Weaknesses

- The worst performing commodity for the week was palm oil, down 1.50%. The crude palm oil futures contracts closed marginally lower this week due to profit-taking activities ahead of the release of the May supply and demand estimates.

- Fort Worth, Texas-based Basic Energy Services Inc. might file for bankruptcy for the second time in five years. The oil and gas services company is negotiating with creditors to restructure its debt load of more than $300 million, and is weighing in-court and out-of-court options to address it.

- The winter freeze that left millions of Texans without power for days revealed the state’s two biggest polluters that have been hiding in plain sight. The Wildcat and Sand Hills plants, run by Houston-based Targa Resources Corp., accounted for 20% of the state’s total pollution during the freeze. These facilities burned off or released huge quantities of hazardous gases as they were stricken by power outages and mechanical failures, emitting nearly four times the amount emitted by the country’s largest refinery. According to filings with the Texas Commission on Environmental Quality (TCEQ), both Wildcat and Sand Hills plants have released hazardous compounds like benzene, hydrogen sulfide and sulfur dioxide above permitted levels more than 400 times since beginning of 2019.

Opportunities

- OPEC+ decided this week that it will proceed with plans to gently increase oil production as global demand recovers from the pandemic. The coalition is pressing on with its roadmap to increase supply by 2 million barrels a day over the next three months. OPEC+ estimates that world oil consumption will recover by more than 6 million barrels a day, and that oil stockpiles that amassed when demand collapsed last year will be gone by the end of this quarter. Secretary General of OPEC said that the alliance needs to remain cautious and not stray from its steadfast approach as Covid-19 is still raging in places like India and Latin America.

- Pacific Investment Management Co. (PIMCO) believes that the current rally in commodities is being driven by real shortages of raw materials as much as it is driven by anticipation of future demand. Premiums on near-term deliveries of commodities over future deliveries – known as backwardation—have jumped to the highest in over 15 years, signaling immediate physical shortages across economies. About half of the major commodities including oil, natural gas, copper, soybeans and corn are in backwardation.

- The China Nonferrous Metals Industry Association (CNIA) announced that the world’s largest base metals industry aims to have its emissions peak before 2025 and fall by 40% before 2040. The CNIA’s secretary said that the industry, led by aluminum and copper, will limit production capacity, shift production into capacity fueled by renewable energy and develop technologies like carbon capture.

Threats

- Chile’s congressional mining committee approved a new version of a bill to ratify the country’s mining royalty system that could stifle investment in the world’s biggest copper-producing nation. The original text stated a flat 3% tax on sales, and the new version proposes marginal rate starting at 15% and could go up as much as 75%. At current copper prices, the effective rate would be 21.5%. The bill is expected to be challenged by some government officials and might even attract lawsuits from foreign mining companies in the International Chamber of Commerce, according to an analyst at BTG Pactual, a Brazilian financial services company.

- Grain prices have reached eight-year highs, making it extremely expensive to feed the world’s chickens, pigs and cows. The latest rally in grain prices shows that the market is tightening, and it has seen some unusual trades. Perdue Farms Inc., an American chicken giant, took the rare step of buying soybean, an American staple, from rival Brazil. Further, Brazil’s top poultry producer BRF SA ordered corn from its neighbor Argentina. Such high prices are starting to cut into margins of poultry and pig producers throughout the world, but rising demand could help increase overall sales as the cost is shifted to consumers. Corn futures have climbed to $6.84 a bushel in April, the highest since 2013.

- Middle Eastern petrostates are actively looking at ways to diversify their economies and invest in their green energy transition. The Saudi crown prince announced this week that the kingdom is already in talks with a global energy company to sell a stake worth $20 billion in state oil firm Saudi Aramco. The pandemic upended global demand for oil, ballooning budget deficits of Middle Eastern oil exporters to 10.8% of their gross domestic product (GDP). Moreover, Adnoc, which pumps almost all of United Arab Emirates’ oil and gas, is planning IPOs of its drilling and fertilizer units. The recent trend of divesting from oil is expected to increase in the coming years in the Middle East as countries around the world push to decarbonize their economies, making such divestures a necessity.

Airline Sector

Strengths

- The best performing airline stock for the week was Jet2 PLC, up 9.1%. Flights for the initial phase of the Hong Kong-Singapore travel bubble opening on May 26 have all but sold out, according to the websites of Cathay Pacific and Singapore Airlines. This is a strong positive signal that travelers are ready to return to the skies.

- ANA Holdings, Japan’s top carrier, issued a surprise profit outlook for its fiscal year of 28 billion yen, which is far higher than analyst projections of a 93.6 billion yen loss. CEO Shinya Katanozaka said the company will be cash flow positive by July and that current spending is sustainable for another three years, reports Bloomberg.

- The world’s largest aircraft measured by wingspan completed its second flight ever this week after being grounded for two years. The Stratolaunch performed a test flight at the Mojave Air and Space Port in California. The twin-hulled plane, which is 385 feet over the wings, is powered by six Boeing 747 engines. The aircraft serves as a launch vehicle for reusable hypersonic flight research vehicles.

Weaknesses

- The worst performing airline stock for the week was Avianca, down 9.2%. Global capacity was down 53% in April, which is unchanged from March, and is expected to be down 49% in May. China and the U.S. are the only countries seeing improved as the pandemic ranges on in other regions.

- The Federal Aviation Administration (FAA) will require airlines to fix a manufacturing flaw on electrical components on Boeing 737 MAX jets. Repairs will cost $155,000 to fix the 71 plans in operation in the U.S. Bloomberg notes airlines have voluntarily grounded more than 100 of the aircraft while waiting for guidance. The repairs will also be needed on several hundred jets built since 2019 that are currently in storage.

- The Royal Bank of Canada lowered estimates for Air Canada citing lower-than-expected yields and higher jet fuel costs. Analysts are also lowered Allegiant due to business weakness in the first quarter.

Opportunities

- Breeze Airways, a new U.S. carrier founded by JetBlue founder David Neeleman, has boosted its growth plans with an additional order for 20 Airbus A220-300 jets, reports Reuters. The startup’s total order for the aircraft is 80 and would make Breeze the second-biggest customer. Neeleman said the carrier is on course to start flying by summer.

- The Indian Ocean nation Seychelles repurchased Etihad Airways’ 40% stake in its flag carrier, Air Seychelles, for just $1 then ousted its board and began restructuring debt. Bloomberg reports Etihad took a 79% cut on $72.3 million of debt owned by Air Seychelles and the government has offered to pay $20 million to bondholders. The revamp of the Seychelles’ flag carrier is an opportunity to focus on profitable routes as travel slowly recovers to the pristine beach destination.

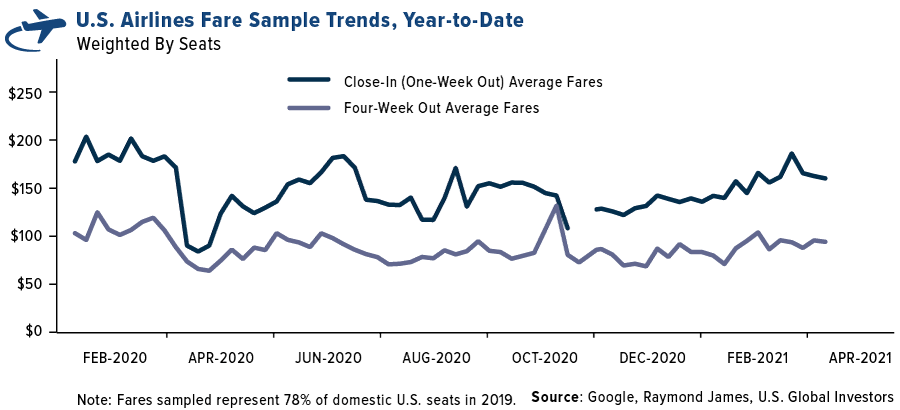

- According to the European Commission, unrestricted travel between the U.S. and E.U. may soon be possible for fully vaccinated passengers. Ursula von Leyen, president of the European Commission, said that America’s strong vaccination progress and use of European Medicines Agency-approved vaccines “will enable free movement and the travel to the EU.” UBS’ airline fare tracker shows a recovery in U.S. ticket prices, which are up 13% year-over-year. Raymond James did a similar survey and found that airline fares are up 9% versus first quarter 2021 levels.

Threats

- The COVID-19 pandemic continues to worsen in India. The country has over 18.8 million confirmed cases and hit a new record today with 386,452 cases. Deaths form the virus now total 208,330. International carriers are boosting flights out of India to bring home residents. A Bloomberg analysis of data from flight tracker OAG shows that carriers in India had reached 87% of their pre-pandemic capacity through early April, but much of that progress has been lost.

- Pakistan International Airlines Corp. (PIA) announced it will layoff half of its 14,000 employees, replace some of its fleet and permanently end loss-making routes, reports Bloomberg. The struggling carrier only has 30 planes and the government is struggling to streamline operations. Even prior to the pandemic, PIA was banned from the U.S. and Europe after Pakistan’s aviation minister said that almost a third of the nation’s pilots had fake licenses. The carrier reported a net loss of $226 million for 2020.

- The recovery of business travel appears further and further away as several major banks have commented on reducing work trips. Nordea Bank Apb said there “will definitely be much less traveling” and Standard Chartered said “we see a step change down in the level of travel once we normalize.” Additionally, HSBC said its was budgeting for travel costs to fall by half due to greater reliance on video conferencing. Bloomberg notes that business travel is the most lucrative market for airlines.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey gaining 3.9%, while the best performing country in Asia was Thailand, up 2.1%.

- The Turkish lira was the best performing currency in emerging Europe, gaining 1.4%.The Indian rupee was the best performing currency in Asia, rising 1.6%.

- Germany’s government raised its growth forecast to 3.5% from the previous forecast of 3% as it expects household spending to support the recovery once COVID-19 restrictions are lifted. Cornerstone Macro said that Germany once again will become the locomotive of Europe, and they expect the country to grow 5% in 2021. Germany accounts for 30% of the Eurozone gross domestic product (GDP).

Weaknesses

- The worst performing country in emerging Europe for the week was Russia, losing 1.5%, while the worst performing country in Asia was South Korea, losing 1.2%.

- The Czech koruna was the worst performing currency in emerging Europe, losing 70 basis points. The Pakistani rupee was the worst performing currency in Asia, losing 28 basis points.

- China reported weaker PMIs for April. Non-manufacturing PMI declined to 54.9 from 56.3 in March. Manufacturing PMI dropped to 51.1 from 51.9, bringing the Composite PMI to 53.8 (versus the prior reading of 55.3). However, the Manufacturing Caixin PMI, which measures activity for smaller private companies, increased to 51.9 in April from 50.6 in March. All PMIs remain in above the 50 level that separates growth from contraction.

Opportunities

- Greece’s debt reached 205.6% of GDP, the highest in Europe, but at the same time the S&P upgraded Greece and gave it a positive outlook. It is the only MSCI Europe, Middle East and Africa country to have been upgraded for this year. MSCI said that it is not the debt level that matters, but the interest rates. As seen in the chart below, Greece has the highest 5-year real interest rates.

- Polish banking shares surged this week on news that Eurozone judges refrained from blocking Polish lenders from counter-suing their clients in FX-loan cases, which has been seen earlier as a major risk. Poland still has $31 billion in foreign exchange loans and it will be up to local courts to decide on the solution for this multi-year conversion process. The court decision is expected on May 11.

- China travel levels this weekend will likely break all records. It is estimated more than 200 million trips will be made. Bookings for air travel are up 23%, hotels up 43% and car rentals up 126% compared to the same period in 2019. China’s controlled COVID-19 situation allows people to be more active and support the domestic economy through travel.

Threats

- China’s government has expanded its antitrust crackdown beyond Jack Ma’s technology giant Alibaba, launching investigations into suspected monopolistic practices by food-delivery company Meituan. The Chinse State Administration of Market Regulation is preparing to fine Tencent around $1.5 billion for anti-trust breaches, less than the $2.75 billion penalty given to Alibaba earlier this month.

- The COVID-19 pandemic continues to worsen in India. On Thursday, the country reported 379,257 new cases in a single day, pushing the total to 18.38 million. Fatalities rose by a record 3,645 to 204,832. Asian countries are closing borders to incoming visitors from India.

- Due to the increased number of cases, Thailand reintroduced the longer quarantine period for incoming foreign visitors after cutting it to just 7 days. Thailands’s Finance Minister cut GDP growth forecasts to 2.3% this year from 2.8%. In January, GDP was already revised down from 4.5% to 2.8%.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.63 | +0.07 | +4.36% |

| Oil Futures | 63.48 | +1.34 | +2.16% |

| Hang Seng Composite Index | 4,524.63 | -50.37 | -1.10% |

| S&P Basic Materials | 521.05 | +0.18 | +0.03% |

| Korean KOSPI Index | 3,147.86 | -38.24 | -1.20% |

| S&P Energy | 371.60 | +12.86 | +3.58% |

| Nasdaq | 13,962.68 | -54.13 | -0.39% |

| DJIA | 33,874.85 | -168.64 | -0.50% |

| Russell 2000 | 2,266.60 | -5.26 | -0.23% |

| S&P 500 | 4,180.63 | +0.46 | +0.01% |

| Gold Futures | 1,767.30 | -10.50 | -0.59% |

| XAU | 142.13 | -6.40 | -4.31% |

| S&P/TSX VENTURE COMP IDX | 955.26 | +24.63 | +2.65% |

| S&P/TSX Global Gold Index | 294.54 | -18.57 | -5.93% |

| Natural Gas Futures | 2.94 | +0.21 | +7.58% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,147.86 | +86.44 | +2.82% |

| 10-Yr Treasury Bond | 1.63 | -0.11 | -6.54% |

| Gold Futures | 1,767.30 | +51.70 | +3.01% |

| S&P Basic Materials | 521.05 | +26.34 | +5.32% |

| S&P 500 | 4,180.63 | +207.74 | +5.23% |

| DJIA | 33,874.85 | +893.30 | +2.71% |

| Nasdaq | 13,962.68 | +715.81 | +5.40% |

| Oil Futures | 63.48 | +4.32 | +7.30% |

| Hang Seng Composite Index | 4,524.63 | +76.64 | +1.72% |

| S&P/TSX Global Gold Index | 294.54 | +9.84 | +3.46% |

| XAU | 142.13 | +7.74 | +5.76% |

| Russell 2000 | 2,266.60 | +46.08 | +2.08% |

| S&P Energy | 371.60 | +1.71 | +0.46% |

| S&P/TSX VENTURE COMP IDX | 955.26 | +2.71 | +0.28% |

| Natural Gas Futures | 2.94 | +0.33 | +12.62% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 142.13 | +3.45 | +2.49% |

| S&P/TSX Global Gold Index | 294.54 | -11.34 | -3.71% |

| Gold Futures | 1,767.30 | -76.40 | -4.14% |

| DJIA | 33,874.85 | +3,271.49 | +10.69% |

| S&P 500 | 4,180.63 | +393.25 | +10.38% |

| Nasdaq | 13,962.68 | +625.52 | +4.69% |

| Korean KOSPI Index | 3,147.86 | +78.81 | +2.57% |

| Natural Gas Futures | 2.94 | +0.27 | +10.25% |

| S&P Basic Materials | 521.05 | +67.34 | +14.84% |

| Russell 2000 | 2,266.60 | +159.99 | +7.59% |

| Oil Futures | 63.48 | +11.14 | +21.28% |

| Hang Seng Composite Index | 4,524.63 | -30.55 | -0.67% |

| S&P/TSX VENTURE COMP IDX | 955.26 | +31.33 | +3.39% |

| S&P Energy | 371.60 | +64.68 | +21.07% |

| 10-Yr Treasury Bond | 1.63 | +0.58 | +55.49% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2021):

Alibaba Group Holdings

Meituan

Tencent Holdings Ltd

Singapore Airlines Ltd

ANA Holdings Inc

Air Canada

Allegiant Travel Co

JetBlue Airways Corp

Newmont Corp

Gold Fields Ltd

Polymetal International Plc

Fortuna Silver Mines Inc

Roxgold Inc

Ivanhoe Mines Ltd

Franco Nevada Corp

Wheaton Precious Metals Corp

Royal Gold Inc

Visa Inc

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation. The S&P CoreLogic Case-Shiller U.S. National Home Price Index (“the U.S. national index”) measures the value of single-family housing within the United States. The index is a composite of single-family home price indices for the nine U.S. Census divisions and is calculated monthly. The Manheim Used Vehicle Value Index is a measurement of used vehicle prices that is independent of underlying shifts in the characteristics of vehicles being sold. Statistical analysis is applied to its database of more than 5 million used vehicle transactions annually. The S&P GSCI serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. It is a tradable index that is readily available to market participants of the Chicago Mercantile Exchange. Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Blockchain Technologies. Mr. Holmes owns shares of HIVE while U.S. Global Investors owns convertible securities. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE.